The Effect of Market Isolation on Competitive Behavior in Retail Petrol Markets

Abstract

1. Introduction

2. Background and Literature

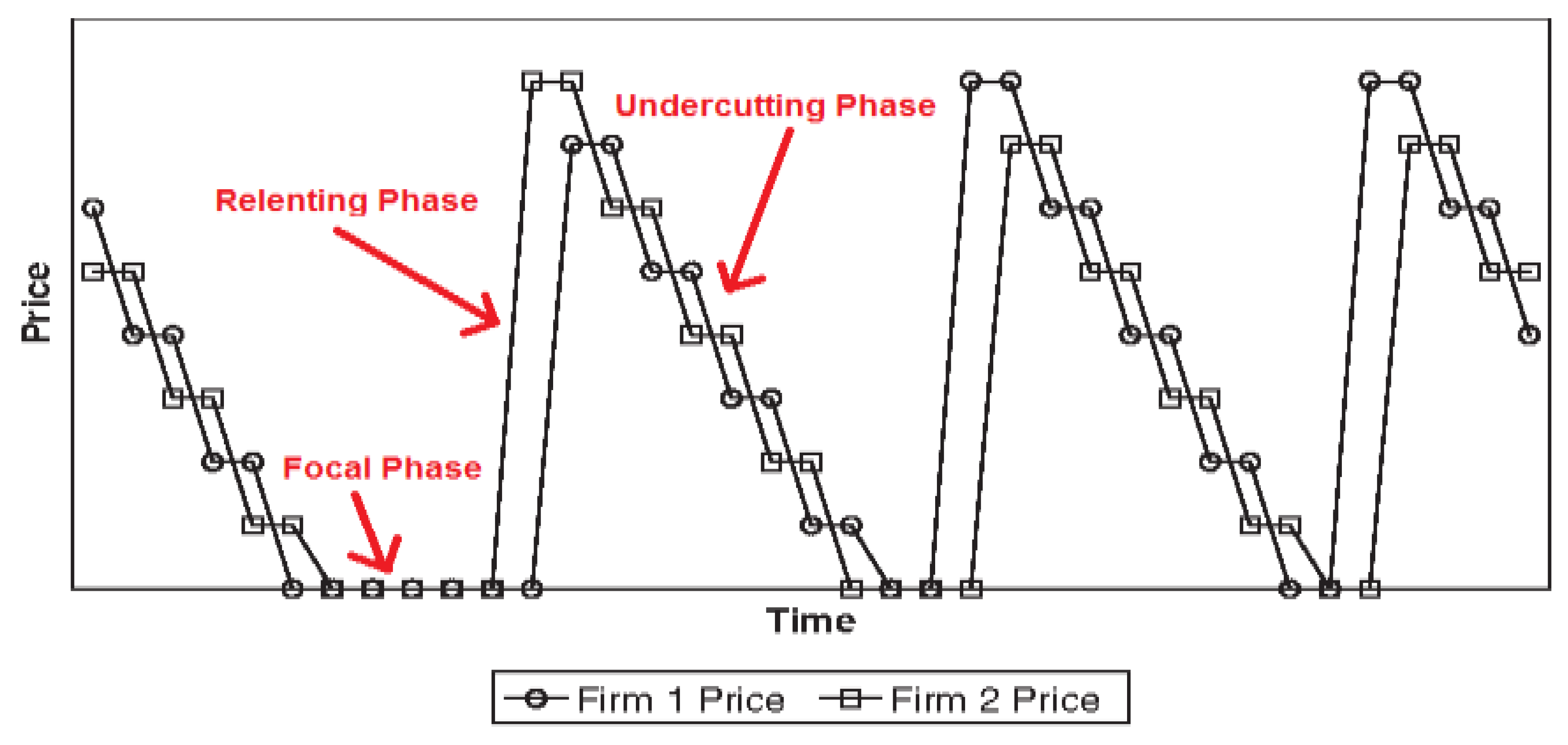

2.1. Edgeworth Price Cycle Theory

2.2. Markov Regime-Switching Model

2.3. Related Literature

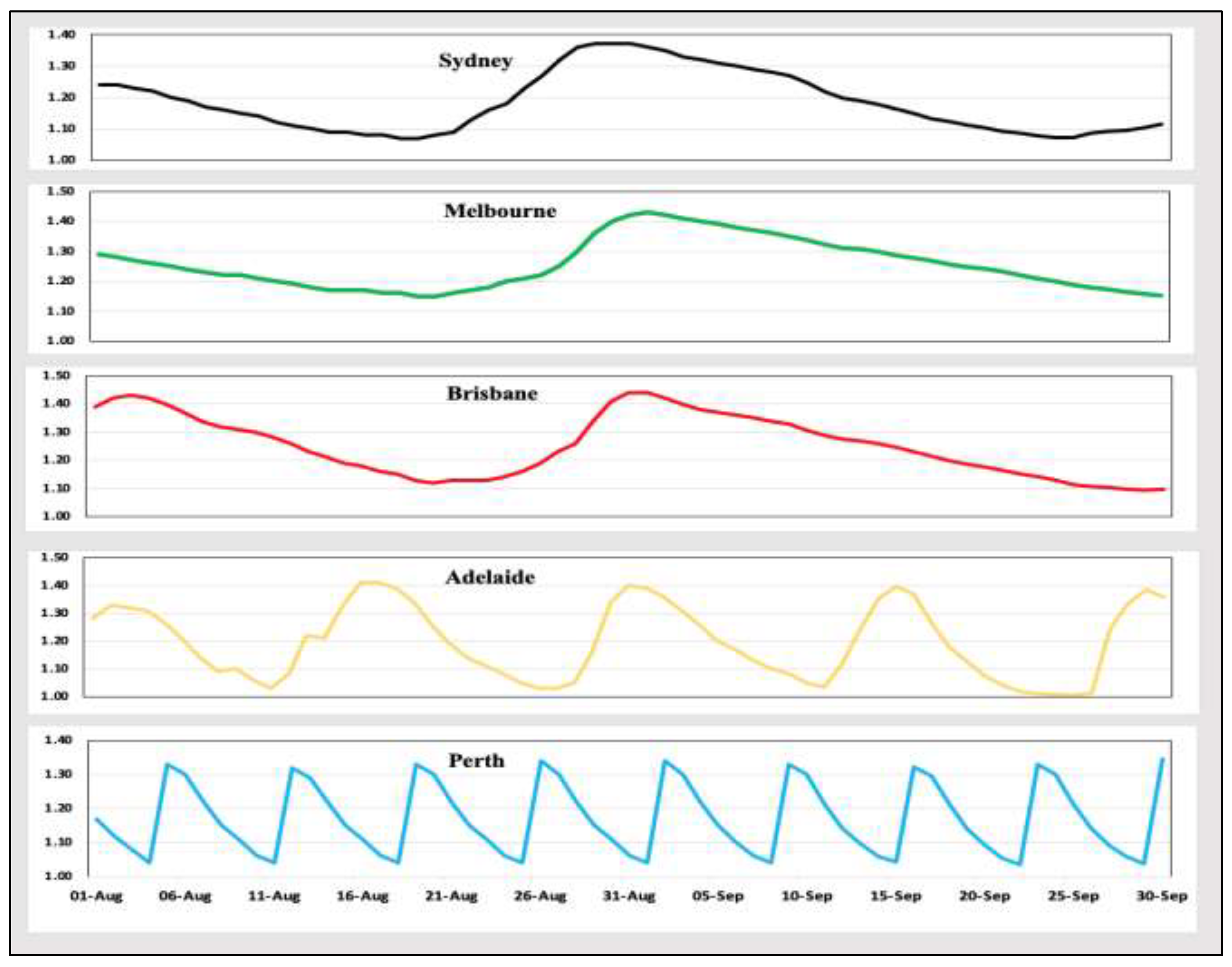

3. The Retail Petrol Market in Perth

4. Empirical Framework

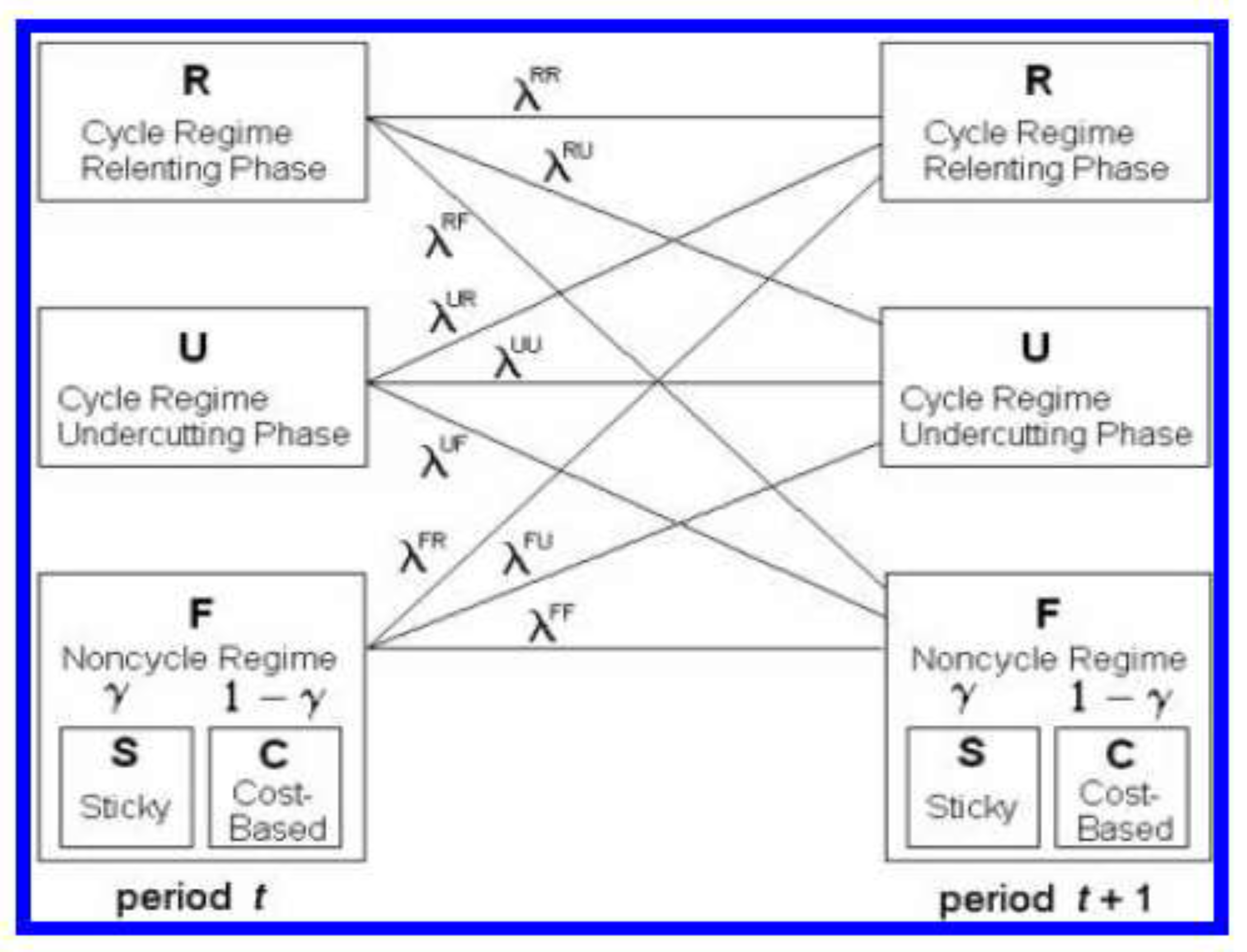

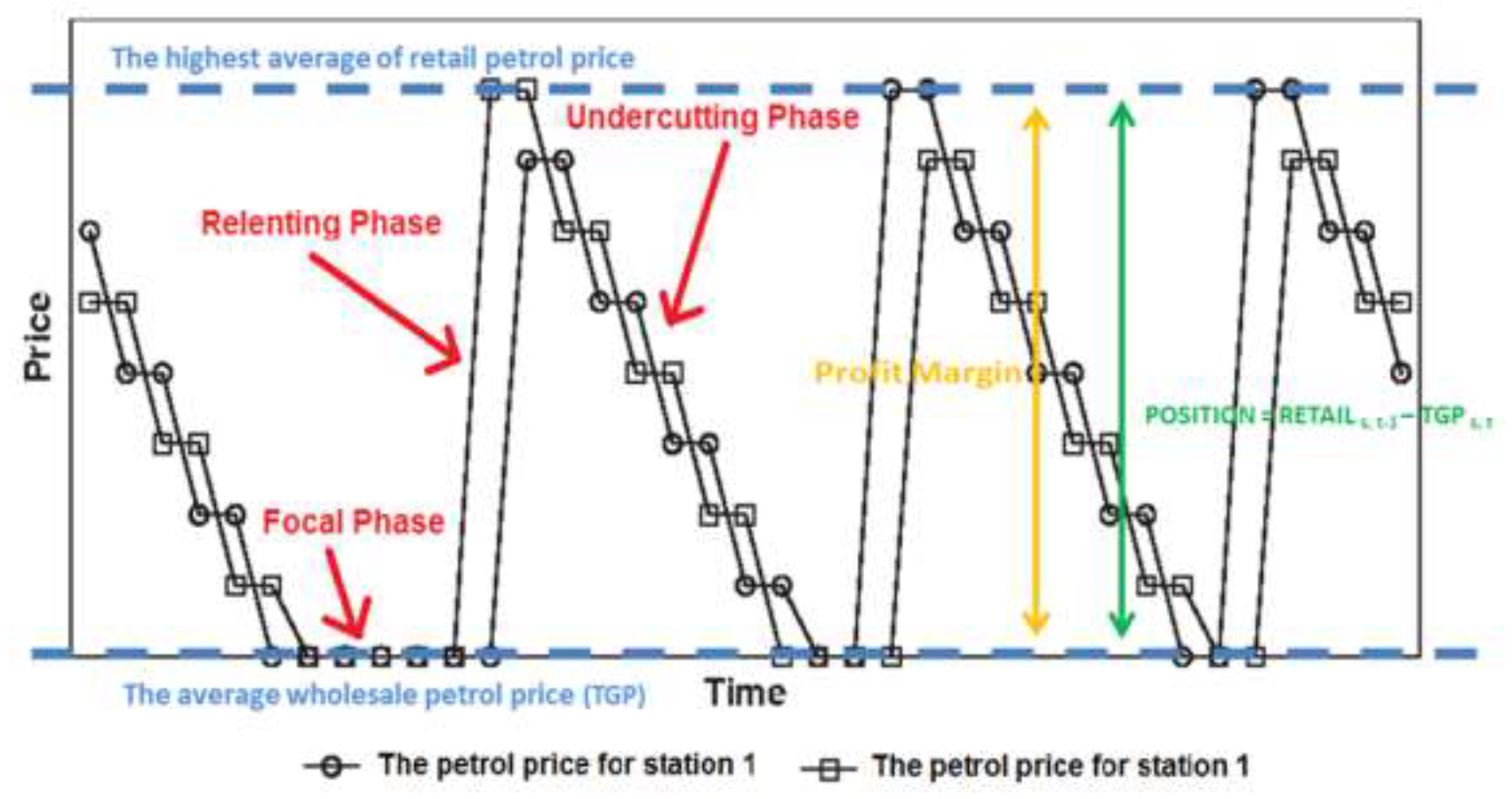

- The undercutting phase (U) illustrates the decrease in petrol prices.

- The relenting phase (R) corresponds to a sharp rise in price.

- A non-cycling or focal regime (F), that is, the period when the price is stable. There are two sub-regimes in the focal regime:

- ◦

- Cost-based pricing (sub-regime “C”); when there are no specific regimes, retail prices follow the wholesale prices.

- ◦

- Price stickiness (sub-regime “S”); when the prices are stable outside cycles.

4.1. Model for Undercutting and Relenting Regimes

4.2. Model for the Focal Regime

4.3. The Switching Probability

4.4. Cycle Characteristics

4.5. Description of the Empirical Model

4.5.1. Within-Regime Estimation

4.5.2. The Effect of Position of Stations on the Petrol Price Cycle

- (1)

- The reactions of firms are fast but not simultaneous.

- (2)

- Small-size companies tend to be the leaders in decreasing prices.

- (3)

- Large-size companies tend to be the leaders in increasing prices [50].

4.5.3. The Role of Stations in the Price Cycle

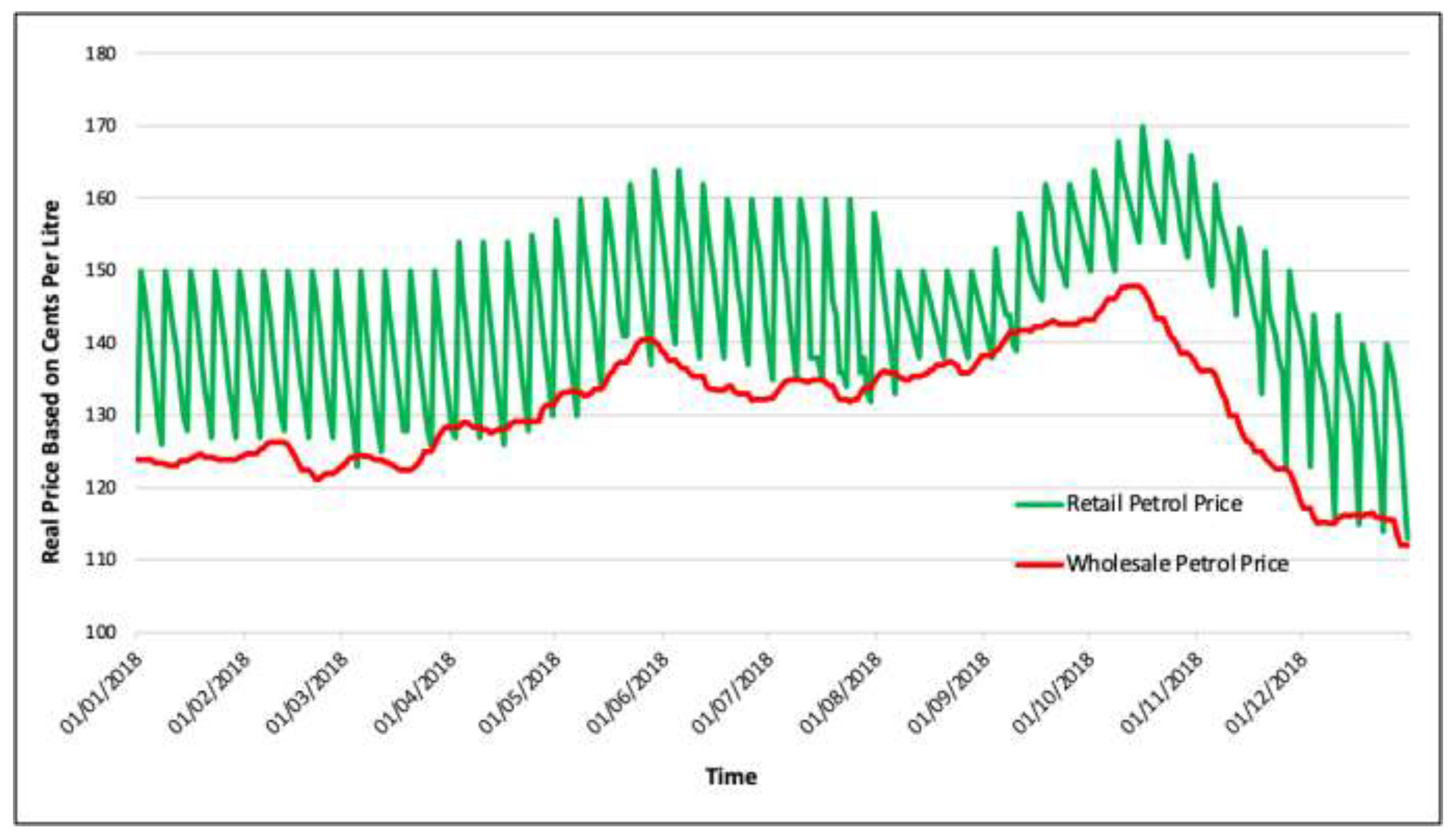

5. Data

6. Empirical Results

6.1. Basic Characteristics of the Petrol Price Cycle

6.2. Effect of the Stations’ Positions on the Price Cycle

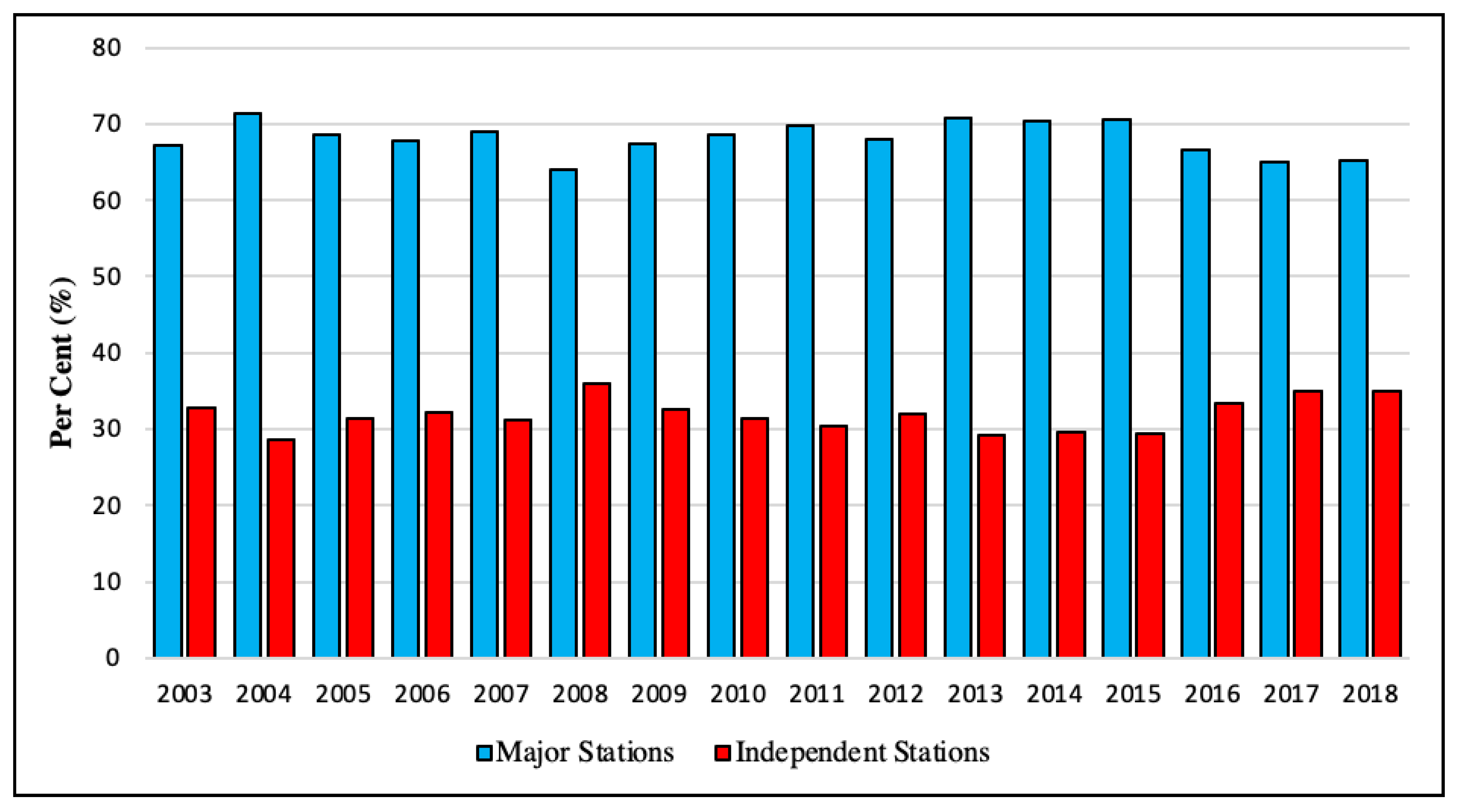

6.3. The Role of Stations in the Petrol Price Cycle

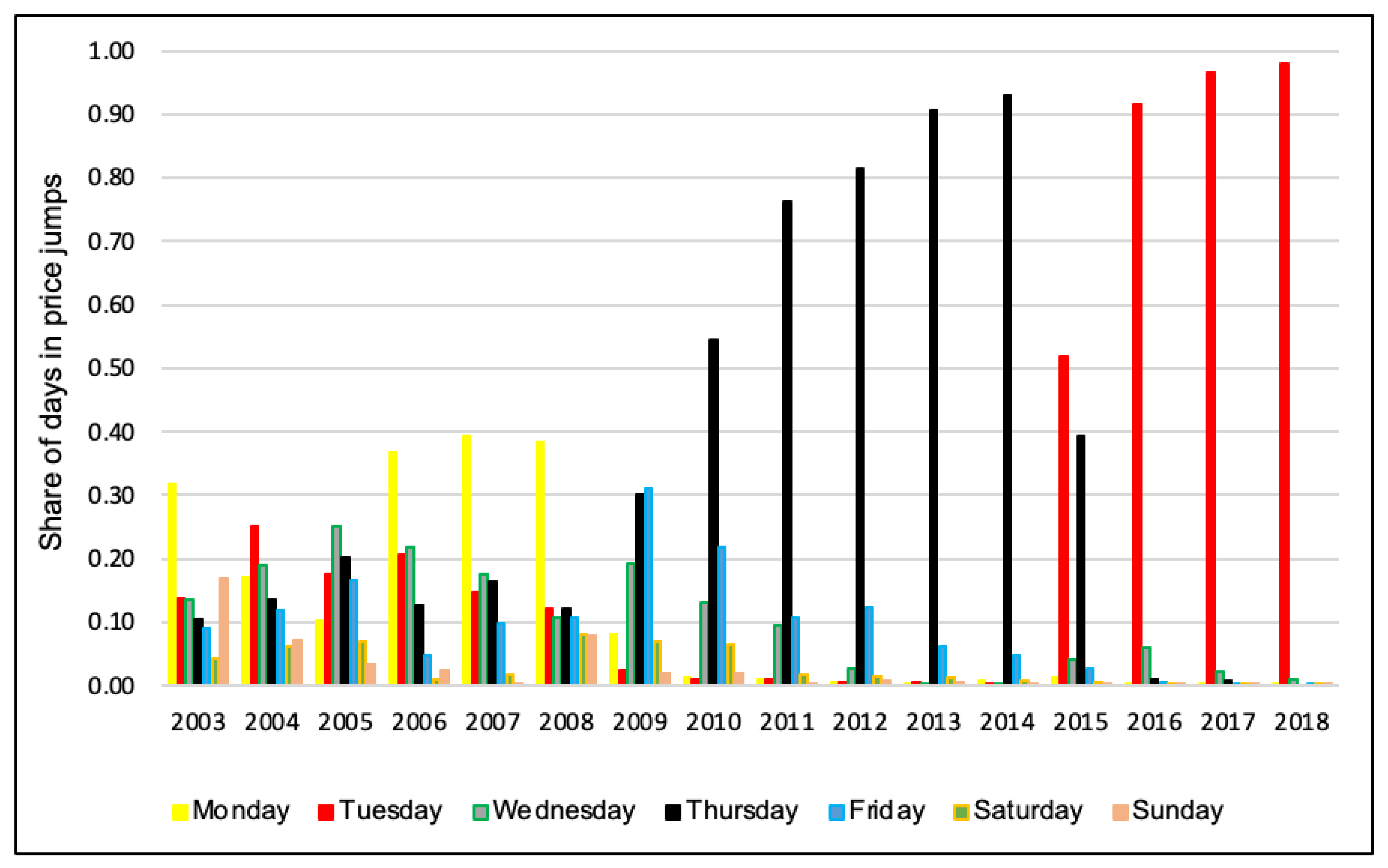

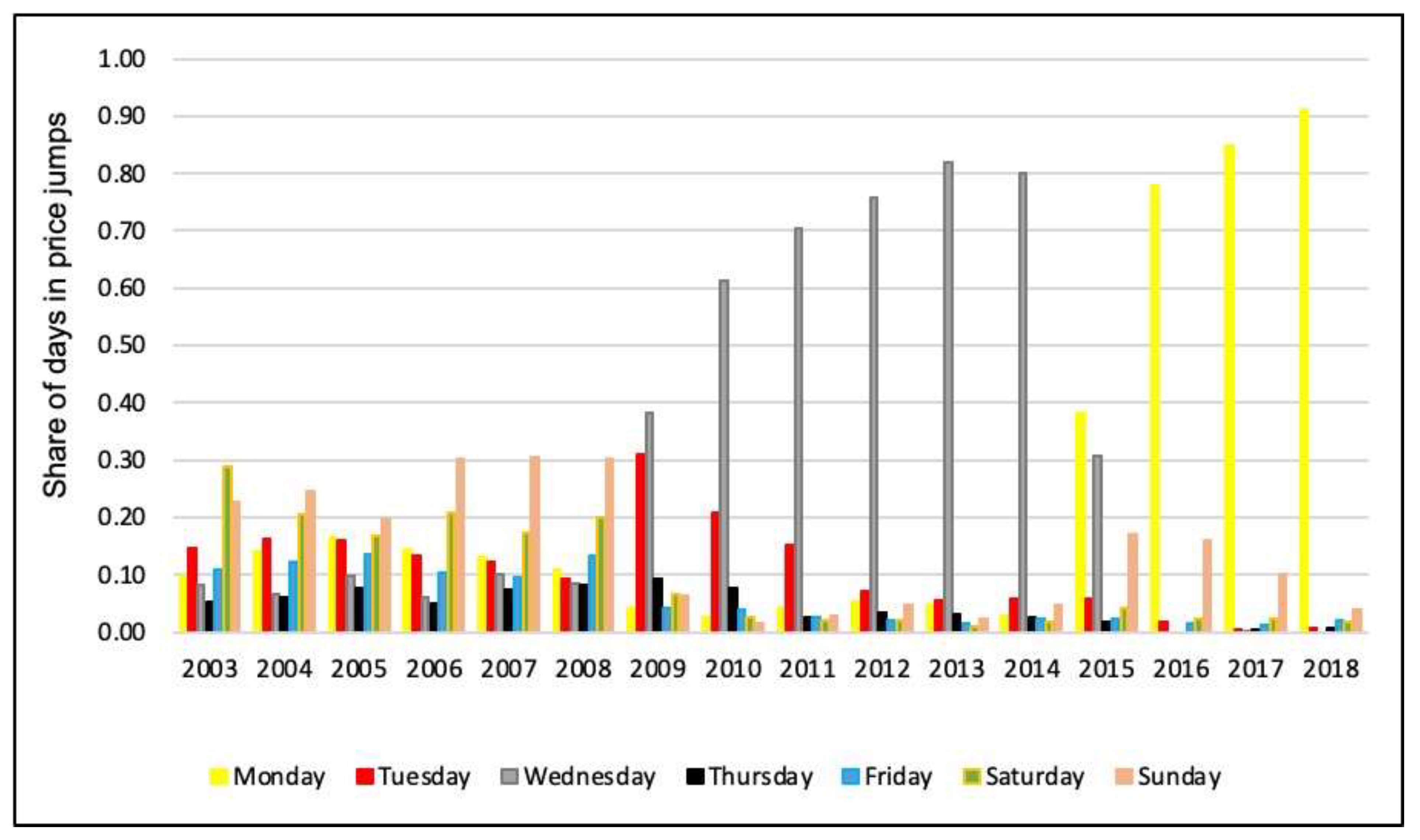

6.4. Peak and Trough Days

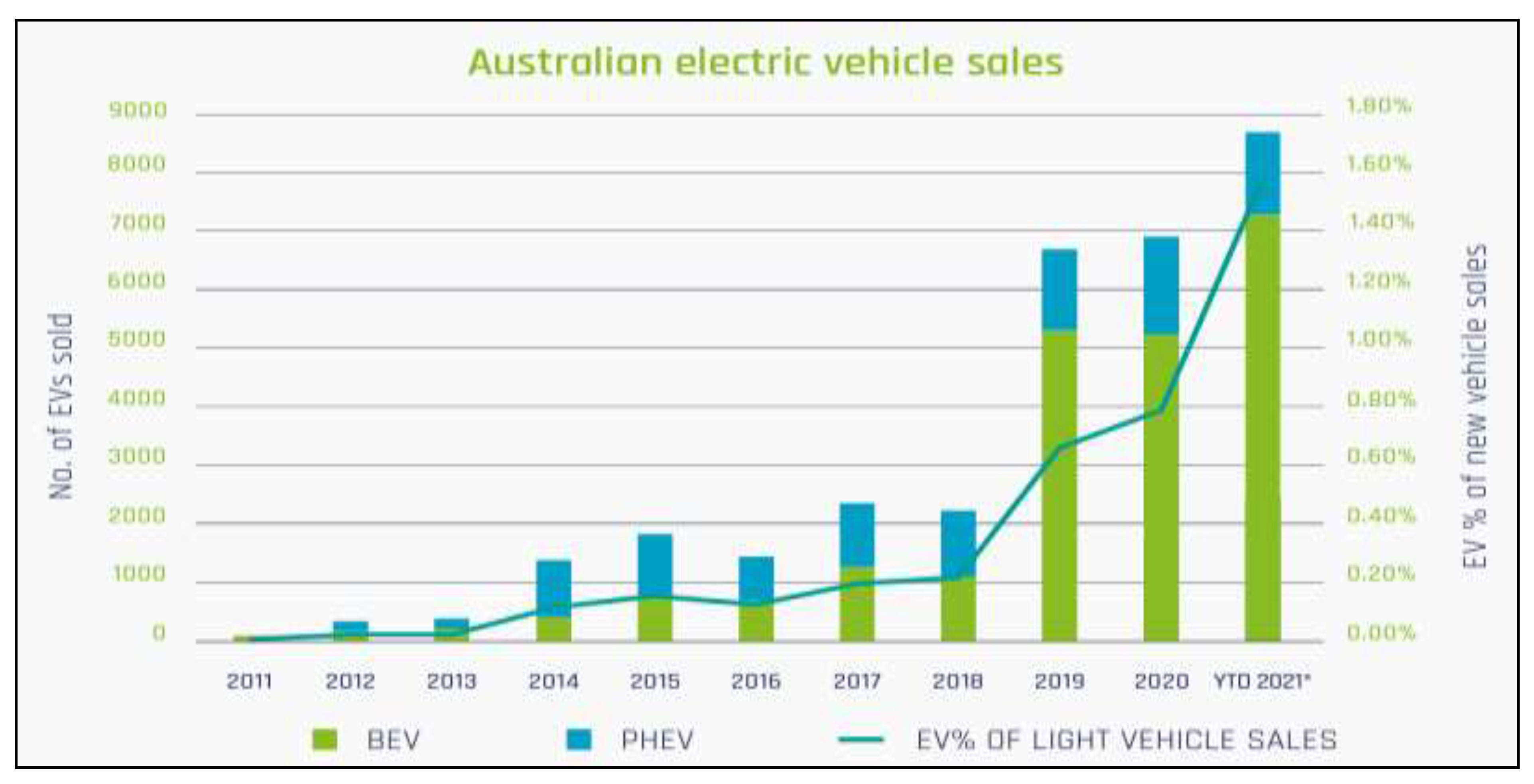

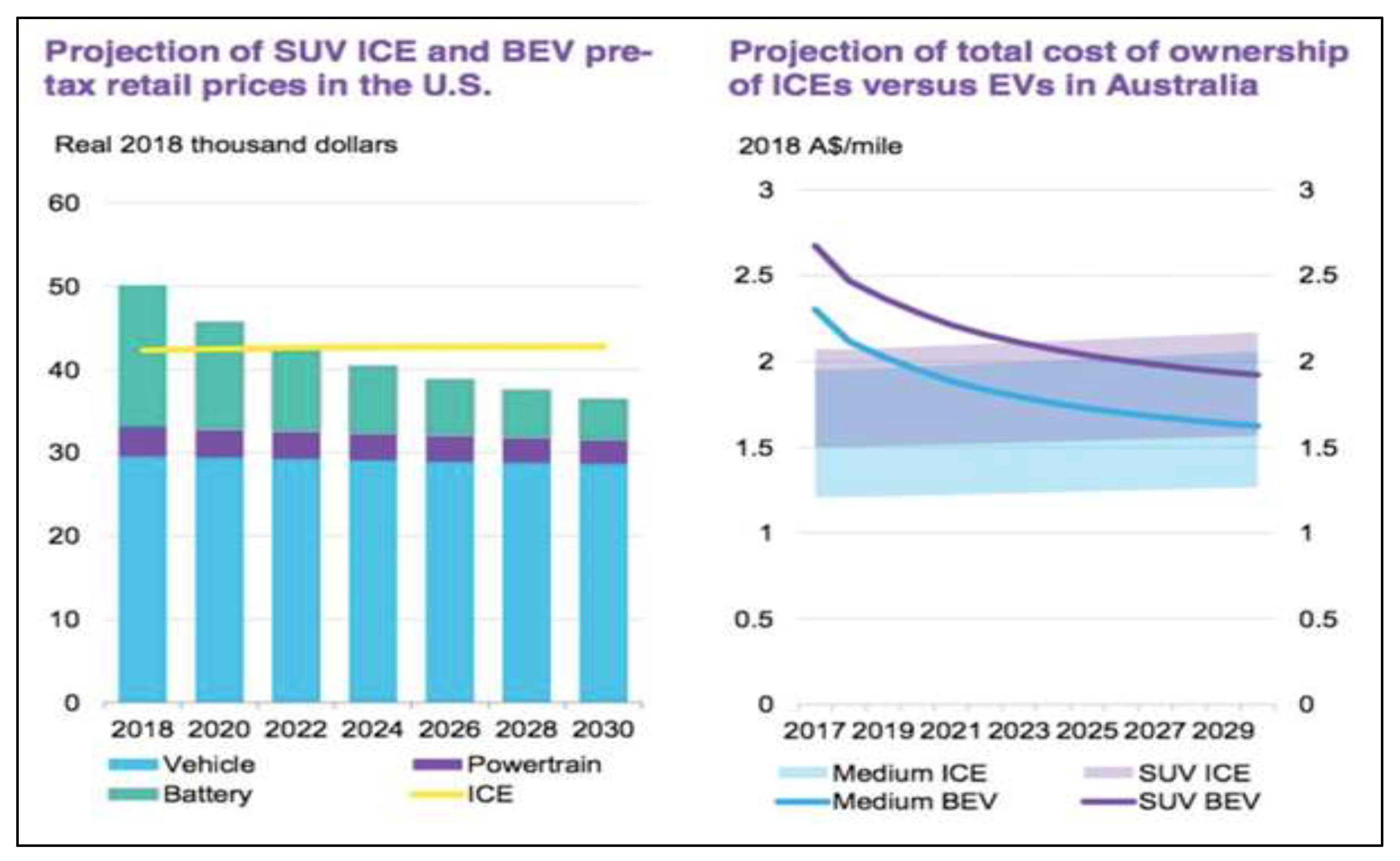

6.5. Investigation of Energy Markets Regarding Substitute Petrol by Clean Energy Source in the Future in Australia

7. Conclusions and Policy Implications

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- FuelWatch. How FuelWatch Works; The Department of Mines, Industry Regulation and Safety: Perth, Australia, 2021. [Google Scholar]

- Byrne, D.P. Petrol price cycles. Aust. Econ. Rev. 2012, 45, 497–506. [Google Scholar] [CrossRef]

- Australian Competition and Consumer Commission. About Fuel Prices. 2021. Available online: https://www.accc.gov.au/consumers/petrol-diesel-lpg/about-fuel-prices (accessed on 3 May 2022).

- Fuel Price, Monitoring of Petrol Price. Available online: www.fuelprice.io (accessed on 3 May 2022).

- MotorMouth, Reports of the Average Petrol Prices. Available online: www.motormouth.com.au (accessed on 3 May 2022).

- Australian Competition and Consumer Commission. Petrol Price Cycles in Australia; ACCC: Canberra, Australia, 2021. [Google Scholar]

- Maskin, E.; Tirole, J. A Theory of Dynamic Oligopoly, II: Price Competition, Kinked Demand Curves, and Edgeworth Cycles. Econometrica 1988, 56, 571. [Google Scholar] [CrossRef]

- Cannan, E.; Edgeworth, F.Y. Papers Relating to Political Economy. Economica 1925, 332, 111–142. [Google Scholar] [CrossRef]

- Bertrand, J. Review of theorie mathematique de la richesse sociale et recherches sur les principes mathematiques de la Richesse. J. Des. Savants 1883, 67, 499–508. [Google Scholar] [CrossRef]

- Noel, M.D. Edgeworth Price Cycles. New Palgrave Dictionary of Economics; Palgrave Macmillan: London, UK, 2011. [Google Scholar] [CrossRef]

- Eckert, A. Retail price cycles and the presence of small firms. Int. J. Ind. Organ. 2003, 21, 151–170. [Google Scholar] [CrossRef]

- Noel, M.D. Edgeworth Price Cycles and Focal Prices: Computational Dynamic Markov Equilibria. J. Econ. Manag. Strat. 2008, 17, 345–377. [Google Scholar] [CrossRef]

- Noel, M.D. Edgeworth price cycles: Evidence from the Toronto retail gasoline market. J. Ind. Econ. 2007, 55, 69–92. [Google Scholar] [CrossRef]

- Noel, M.D. Edgeworth Price Cycles in Retail Gasoline Markets; Massachusetts Institute of Technology: Cambridge, MA, USA, 2002. [Google Scholar] [CrossRef]

- Noel, M.D. Edgeworth Price Cycles, Cost-Based Pricing, and Sticky Pricing in Retail Gasoline Markets. Rev. Econ. Stat. 2007, 89, 324–334. [Google Scholar] [CrossRef]

- Australian Institute of Petroleum (AIP). Available online: https://www.aip.com.au (accessed on 3 May 2022).

- Hou, C.; Nguyen, B.H. Understanding the US natural gas market: A Markov switching VAR approach. Energy Econ. 2018, 75, 42–53. [Google Scholar] [CrossRef]

- Boroumand, R.H.; Goutte, S.; Porcher, S.; Porcher, T. Asymmetric evidence of gasoline price responses in France: A Markov-switching approach. Econ. Model. 2016, 52, 467–476. [Google Scholar] [CrossRef]

- Balcilar, M.; Gupta, R.; Miller, S.M. Regime switching model of US crude oil and stock market prices: 1859 to 2013. Energy Econ. 2015, 49, 317–327. [Google Scholar] [CrossRef]

- Kim, C.-J.; Piger, J.; Startz, R. Estimation of Markov regime-switching regression models with endogenous switching. J. Econ. 2008, 143, 263–273. [Google Scholar] [CrossRef]

- Chen, S.-W. Measuring business cycle turning points in Japan with the Markov Switching Panel model. Math. Comput. Simul. 2007, 76, 263–270. [Google Scholar] [CrossRef]

- Cosslett, S.R.; Lee, L.-F. Serial correlation in latent discrete variable models. J. Econ. 1985, 27, 79–97. [Google Scholar] [CrossRef]

- Ellison, G. Theories of Cartel Stability and the Joint Executive Committee. RAND J. Econ. 1994, 25, 37. [Google Scholar] [CrossRef]

- Hamilton, J.D. Regime Switching Models. Macro Econometrics and Time Series Analysis; Springer: Berlin/Heidelberg, Germany, 2005; pp. 202–209. [Google Scholar] [CrossRef]

- De Roos, N.; Katayama, H. Gasoline Price Cycles Under Discrete Time Pricing. Econ. Rec. 2013, 89, 175–193. [Google Scholar] [CrossRef]

- Wlazlowski, S.; Giulietti, M.; Binner, J.; Milas, C. Price dynamics in European petroleum markets. Energy Econ. 2009, 31, 99–108. [Google Scholar] [CrossRef]

- Eckert, A. A Study of Canadian Gasoline Retail Prices; University of British Columbia: Vancouver, BC, Canada, 1999. [Google Scholar]

- Eckert, A. Retail price cycles and response asymmetry. Can. J. Econ. Rev. Can. D’économique 2002, 35, 52–77. [Google Scholar] [CrossRef]

- Eckert, A.; West, D. Retail Gasoline Price Cycles across Spatially Dispersed Gasoline Stations. J. Law Econ. 2004, 47, 245–273. [Google Scholar] [CrossRef]

- Eckert, A.; West, D.S. A tale of two cities: Price uniformity and price volatility in gasoline retailing. Ann. Reg. Sci. 2004, 38, 25–46. [Google Scholar] [CrossRef]

- Roarty, M.J.; Barber, S. Petrol Pricing in Australia: Issues and Trends; Department of the Parliamentary Library: Melbourne, Australia, 2004. [Google Scholar]

- Al-Gudhea, S.; Kenc, T.; Dibooglu, S. Do retail gasoline prices rise more readily than they fall? A threshold cointegration approach. J. Econ. Bus. 2007, 59, 560–574. [Google Scholar] [CrossRef]

- Li, Z. Modelling and forecasting the demand for automobile petrol in Australia, and its policy implications. In Proceedings of the 29th Conference of Australian Institutes of Transport Research (CAITR), Adelaide, Australia, 5–7 December 2007. [Google Scholar]

- Lewis, M. Price dispersion and competition with differentiated sellers. J. Ind. Econ. 2008, 56, 654–678. [Google Scholar] [CrossRef]

- Lewis, M.S. Temporary Wholesale Gasoline Price Spikes Have Long-Lasting Retail Effects: The Aftermath of Hurricane Rita. J. Law Econ. 2009, 52, 581–605. [Google Scholar] [CrossRef]

- Wang, Z. Station level gasoline demand in an Australian market with regular price cycles. Aust. J. Agric. Resour. Econ. 2009, 53, 467–483. [Google Scholar] [CrossRef]

- Wang, Z. (Mixed) Strategy in Oligopoly Pricing: Evidence from Gasoline Price Cycles Before and Under a Timing Regulation. J. Political Econ. 2009, 117, 987–1030. [Google Scholar] [CrossRef]

- Doyle, J.; Muehlegger, E.; Samphantharak, K. Edgeworth cycles revisited. Energy Econ. 2010, 32, 651–660. [Google Scholar] [CrossRef]

- Wills-Johnson, N.; Bloch, H. A simple spatial model for Edgeworth Cycles. Econ. Lett. 2010, 108, 334–336. [Google Scholar] [CrossRef]

- Bloch, H.; Wills-Johnson, N. The Shape and Frequency of Edgeworth Price Cycles in an Australian Retail Gasoline Market. SSRN 1558747. 2010. Available online: https://doi.org/10.2139/ssrn.1558747 (accessed on 3 May 2022). [CrossRef]

- De Roos, N. Do Firms Play Markov Strategies? SSRN 1597064. 2010. Available online: https://doi.org/10.2139/ssrn.1597064 (accessed on 3 May 2022). [CrossRef]

- Anderson, E. A new model for cycles in retail petrol prices. Eur. J. Oper. Res. 2011, 210, 436–447. [Google Scholar] [CrossRef]

- Lewis, M. Price leadership and coordination in retail gasoline markets with price cycles. Int. J. Ind. Organ. 2012, 30, 342–351. [Google Scholar] [CrossRef]

- Zimmerman, P.R.; Yun, J.M.; Taylor, C.T. Edgeworth Price Cycles in Gasoline: Evidence from the United States. Rev. Ind. Organ. 2013, 42, 297–320. [Google Scholar] [CrossRef]

- Valadkhani, A. Do petrol prices rise faster than they fall when the market shows significant disequilibria? Energy Econ. 2013, 39, 66–80. [Google Scholar] [CrossRef]

- Valadkhani, A. Seasonal patterns in daily prices of unleaded petrol across Australia. Energy Policy 2013, 56, 720–731. [Google Scholar] [CrossRef]

- Valadkhani, A.; Babacan, A. Modelling how much extra motorists pay on the road? A cross-sectional study of profit margins of unleaded petrol in Australia. Energy Policy 2014, 69, 179–188. [Google Scholar] [CrossRef]

- Atkinson, B.; Eckert, A.; West, D.S. Daily Price Cycles and Constant Margins: Recent Events in Canadian Gasoline Retailing. Energy J. 2014, 35. [Google Scholar] [CrossRef]

- Noel, M.D.; Chu, L. Forecasting gasoline prices in the presence of Edgeworth Price Cycles. Energy Econ. 2015, 51, 204–214. [Google Scholar] [CrossRef]

- Noel, M.D. Retail gasoline markets. In Handbook on the Economics of Retailing and Distribution; Edward Elgar Publishing: Northampton, MA, USA, 2016; p. 392. [Google Scholar] [CrossRef]

- Hashimi, H.; Jeffreys, I. The impact of lengthening petrol price cycles on consumer purchasing behaviour. Econ. Anal. Policy 2016, 51, 130–137. [Google Scholar] [CrossRef]

- Dewenter, R.; Heimeshoff, U.; Lüth, H. Less Pain at the Pump? The Effects of Regulatory Interventions in Retail Gasoline Markets. Appl. Econ. Q. 2017, 63, 259–274. [Google Scholar] [CrossRef]

- Byrne, D.P.; de Roos, N. Consumer Search in Retail Gasoline Markets. J. Ind. Econ. 2017, 65, 183–193. [Google Scholar] [CrossRef]

- Valadkhani, A.; Smyth, R. Asymmetric responses in the timing, and magnitude, of changes in Australian monthly petrol prices to daily oil price changes. Energy Econ. 2018, 69, 89–100. [Google Scholar] [CrossRef]

- Byrne, D.P.; Nah, J.S.; Xue, P. Australia Has the World’s Best Petrol Price Data: FuelWatch and FuelCheck. Aust. Econ. Rev. 2018, 51, 564–577. [Google Scholar] [CrossRef]

- Byrne, D.P.; de Roos, N. Learning to Coordinate: A Study in Retail Gasoline. Am. Econ. Rev. 2019, 109, 591–619. [Google Scholar] [CrossRef]

- Wilhelm, S. Price Matching and Edgeworth Cycles. SSRN 2708630. 2019. Available online: https://doi.org/10.2139/ssrn.2653089 (accessed on 3 May 2022). [CrossRef]

- De Haas, S. Do Pump Prices Really Follow Edgeworth Cycles? Evidence from the German Retail Fuel Market; MAGKS Joint Discussion Paper Series in Economics No. 13-2019; Philipps-University Marburg, School of Business and Economics: Marburg, Germany, 2019. [Google Scholar]

- Benoit, S.; Lucotte, Y.; Ringuedé, S. Competition and Price Stickiness: Evidence from the French Retail Gasoline Market. 2019. Available online: https://hal.archives-ouvertes.fr/hal-02292332 (accessed on 3 May 2022).

- Ghazanfari, A. Regional patterns for the retail petrol prices. Int. J. Energy Econ. Policy 2021, 11, 383–397. [Google Scholar] [CrossRef]

- Valadkhani, A.; Anwar, S.; Ghazanfari, A.; Nguyen, J. Are petrol retailers less responsive to changes in wholesale or crude oil prices when they face lower competition? The case of Greater Sydney. Energy Policy 2021, 153, 112278. [Google Scholar] [CrossRef]

- Kennewell, C.; Shaw, B.J. Perth, Western Australia. Cities 2008, 25, 243–255. [Google Scholar] [CrossRef]

- Australian Competition and Consumer Commission. Quarterly Report on the Australian Petroleum Market; ACCC: Canberra, Australia, 2018. [Google Scholar]

- Armin Razmjoo, Development of smart energy systems for communities: Technologies, policies and applications. Energy 2022, 248, 123540. [CrossRef]

- Gong, S.; Ardeshiri, A.; Rashidi, T.H. Impact of government incentives on the market penetration of electric vehicles in Australia. Transp. Res. D Transp. Environ. 2020, 83, 102353. [Google Scholar] [CrossRef]

- Sheng, M.S.; Sreenivasan, A.V.; Sharp, B.; Du, B. Well-to-wheel analysis of greenhouse gas emissions and energy consumption for electric vehicles: A comparative study in Oceania. Energy Policy 2021, 158, 112552. [Google Scholar] [CrossRef]

- Available online: https://www.comparethemarket.com.au/wp-content/uploads/2021/08/EVC1.png (accessed on 3 May 2022).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Author | Year | Title | Research Scope | Sample Frequency | Aim | Finding |

|---|---|---|---|---|---|---|

| Andrew Eckert [28] | 2002 | Retail Price Cycles and Response Asymmetry | Ontario | 1989–1994 | To determine the effect of wholesale petrol prices on the retail petrol markets. | Petrol prices respond faster to wholesale price increases than decreases but show a cyclic pattern inconsistent with a common explanation for response asymmetry. |

| Eckert and West [29] | 2004 | Retail gasoline price cycles across spatially dispersed gasoline stations. | Vancouver | 1999 | To study petrol price behavior. | This study found characteristics of the retail petrol price cycle. |

| Eckert and West [30] | 2004 | A tale of two cities: Price uniformity and price volatility in gasoline retailing. | Vancouverand Ottawa | 2000 | To analyze volatility, dispersion, rigidity, and uniformity in the retail petrol markets in metropolitan areas. | They came up with a theory to explain petrol pricing behavior. |

| Roarty and Barber [31] | 2004 | Petrol pricing in Australia: issues and trends | Australia | To provide an overview of petrol prices and issues facing consumers in Australia. | Some of these factors are crude oil prices; exchange rates; retail competition and price cycles; government policies; and taxation. | |

| Al-Gudhea et al. [32] | 2007 | Do retail gasoline prices rise more readily than they fall?; A threshold cointegration approach | U.S. | 1998–2004 | To determine how retail petrol prices respond to changes in upstream prices. | Petrol prices respond more rapidly to increases in upstream prices than falls. Additionally, the asymmetry is more pronounced for small shocks, possibly due to consumer search costs. |

| Michael D. Noel [15] | 2007 | Edgeworth price cycles, cost-based pricing, and sticky pricing in retail gasoline markets | Canada | 2007 | To examine the dynamic pricing behavior in Canadianretail petrol markets | Cycles are more prevalent when there are more small firms and are accelerated and heightened when there are many small firms. |

| Zheng Li [33] | 2007 | Modeling and forecasting the demand for petrol, and its policy implications | Australia | 1977–2006 | To analyze the petrol demand in the Australian road transport sector. | They could forecast demand for automobile petrol in Australia from 2007 through to 2020. |

| Lewis [34] | 2008 | Price dispersion and competition with differentiated sellers | San Diego, California | 2000–2001 | To determine price dispersion among sellers and analyze the relationship between dispersion and competition. | Price dispersion is correlated with local competition density, but this relationship varies significantly by seller type and its competitors. |

| Lewis [35] | 2009 | Temporary wholesale gasoline price spikeshave long-lasting retail effects | 85 Cities in the U.S. | 2009 | To find out why prices dropped faster in cities with retail price cycles. | It was found that cycling cities tend to be denser and more concentrated in large retailers than non-cycling cities. |

| Zhongmin Wang [36] | 2009 | Station level gasoline demand in an Australian market with regular price cycles | Perth | 2003–2006 | To determine the petrol demand at the station level in Perth’s cycling market. | The petrol demand depends critically on the level of local competition. |

| Wang, Z [37] | 2009 | (Mixed) strategies in oligopoly pricing | Perth | 2000–2003 | To examine price behavior in Perth before and after the 24-h price legislation. | He found that the Edgeworth price cycle can explain the cyclical behavior of petrol prices in Perth. |

| Doyle et al. [38] | 2010 | Edgeworth cycles revisited | 115 U.S. cities | 2000–2001 | To extend the Edgeworth cycle and test its predictions with a new dataset of daily station-level prices in 115 | According to their research, markets with the least and most concentration are less likely to exhibit cycling. |

| Wills and Bloch [39] | 2010 | A simple spatial model for Edgeworth cycles | Australia | To present a model to show how the Edgeworth cycle might arise in a petrol market where spatial competition is vital. | ||

| Wills and Bloch [40] | 2010 | The shape and frequency of Edgeworth price cycles | Perth | 2003–2004 | To investigate the factors that influence the pattern of retail petrol price. | They found that the market structure influences both the shape and the length of price cycles. |

| de Roos [41] | 2010 | Do firms play Markov strategies? | Perth | 2001–2007 | To examine whether firms play Markov strategies in Australia. | The retail petrol market in Perth satisfies most assumptions related to the MT model. |

| Anderson [42] | 2011 | A new model for cycles in retail petrol prices | Adelaide, Melbourne, Sydney | 2005 | To provide an explanation for price cycles that do not follow Edgeworth, but instead arises from the interaction of customer expectations of future prices and profit maximization. | They found that the period of the cycle is endogenous, price changes at the beginning of each day and the length of the cycle depends on the rate at which motorists use fuel. |

| Lewis [43] | 2012 | Price leadership and coordination in retail gasoline markets with price cycles | 280 cities in the U.S. | 2004–2010 | To study how stations manage their prices where there are highly cyclical patterns known as Edgeworth cycles. | Each city has a retail chain that leads the price restoration process. |

| Zimmerman et al. [44] | 2013 | Edgeworth Price Cycles in Gasoline: Evidencefrom the United States | U.S. | 1996–2010 | To examine the retail petrol price patterns. | Analyzed the petrol price cycles in the U.S. |

| Valadkhani [45] | 2013 | Do petrol prices rise faster than they fall when the market shows significant disequilibria? | 111 Australian cities | 2007–2012 | To study the long-run relationship between the retail and wholesale petrol prices in Australia. | He found asymmetric behavior in the petrol price in 28 cities, which were mostly in Queensland, Tasmania, and New South Wales. |

| Valadkhani [46] | 2013 | Seasonal patterns in daily prices of unleaded petrol across Australia | 114 Australian locations | 2005–2012 | To provide an analysis of the day of the week effect in the retail ULP prices in 114 locations in Australia. | Thursdays or Fridays were the most expensive days and Sundays or Tuesdays were the cheapest days to purchase petrol in most Australian areas. |

| de Roos and Katayama [25] | 2013 | Gasoline price cycles under discrete time pricing | Perth | 2003 | To provide a quantitative analysis of the petrol price cycle in Perth. | They found that petrol price cycles are frequent and asymmetric and like the Edgeworth cycle. |

| Valadkhani and Babacan [47] | 2014 | Modeling how much extra motorists pay on the road? | 108 Australian cities | 2007–2012 | To identify the determinants of profit margins in the retail petrol markets in Australia. | It showed that 13 locations had high abnormal margins. |

| Atkinson et al. [48] | 2014 | Daily price cycles and constant margins: recent events in Canadian gasoline retailing | Toronto | 2004–2007 | To analyze changes in pricing patterns that result in new equilibrium behavior, and to discuss possible explanations for these changes. | The study revealed that the volatility changes are related to an increased frequency of the price cycle and the replacement of the cycle with fixed retail margins. |

| Noel and Chu [49] | 2015 | Forecasting gasoline prices in the presence of Edgeworth price cycles | U.S. | 2007–2013 | To forecast petrol prices in the retail petrol markets. | They examined a number of purchase timing decision methods and feasible forecasting algorithms to predict petrol prices. |

| Michael D. Noel [50] | 2016 | Retail gasoline markets | U.S. | Provide a review of the previous literature about the retail petrol markets. | They presented a survey of the recent literature on retail petrol markets | |

| Hashimi and Jeffreys [51] | 2016 | The impact of lengthening petrol price cycles on consumer purchasing behavior | Brisbane | 2011–2013 | To find the effect of petrol price cycles and other factors on the purchasing behavior of consumers. | It found that high prices result in a relatively high financial burden for motorists and the recent changes in the petrol price cycles have negatively influenced both females and males. |

| Dewenter and Heimeshoff [52] | 2017 | Less pain at the pump? The effects of regulatory interventions in retail gasoline markets | Austria and Western Australia | 1998–2012 | To find the effect of price regulation on the petrol price. | Their findings showed that the level of prices decreased in Austria after implementing the pricing regulation. However, they did not find considerable effects of such pricing rules on price levels in Western Australia. |

| Byrne and de Roos [53] | 2017 | Consumer search in retail gasoline markets | Perth | 2012–2013 | Their results provided strong evidence of both cross-sectional and intertemporal price search. | |

| Valadkhani and Smyth [54] | 2018 | Asymmetric responses in the timing, and magnitude of changes in Australian monthly petrol prices to daily oil price changes | Australia | 1998–2017 | To find how petrol prices respond to the changes in crude oil price. | They found the existence of asymmetry in the response of retail petrol prices to changes in oil price. |

| Byrne et al. [55] | 2018 | Australia has the world’s best petrol price data: FuelWatch and FuelCheck | Australia | 2001–2017 | To introduce two databases in Australia that provide station-level data of petrol price for public access. | They explained the FuelWatch and FuelCheck websites. |

| Byrne and de Roos [56] | 2019 | Learning to coordinate: A study in retail gasoline. | Perth | 2001–2015 | To provide a unique empirical analysis of equilibrium selection in the retail petrol market. | Their results showed the theory of collusion and highlight novel insights into merger policy and collusion detection strategies. |

| Sascha Wilhelm [57] | 2019 | Price Modeling and Edgeworth Cycle | Germany | 2014–2015 | To find how price matching affects pricing decisions in dynamic markets with cycling prices. | The study predicts that price-matching retailers will post higher prices and will be at the forefront of price restorations. |

| De Hass [58] | 2019 | Do pump prices really follow Edgeworth cycles? Evidence from the German retail fuel market | Germany | To analyze the petrol price patterns. | His findings showed that petrol prices do not fall to marginal costs. | |

| Benoit et al. [59] | 2019 | Competition and price stickiness: Evidence from the French retail gasoline market | France | 2012–2013 | To examine how competition affects price stickiness on the retail petrol market. | The study found that local competition is an essential factor of the pricing behavior of stations. |

| Arezoo Ghazanfari [60] | 2021 | Regional patterns for the retail petrol prices | Western Australia | 2017–2018 | To develop a clearer understanding of petrol price patterns in urban and rural areas in Western Australia. | There was a mismatch between pricing patterns across regions and cities. There are two types of patterns, cities with cycles and cities without. |

| Valadkhani, et al. [61] | 2021 | Are petrol retailers less responsive to changes in wholesale or crude oil prices when they face lower competition? | Greater Sydney | 2018 | To examine the effects of upstream shocks (oil or wholesale prices) on the retail petrol prices by specifically focusing on the effect of competition. | Their findings showed that the pass-through parameters are significantly lower for stations with fewer competitors in their immediate proximity. |

| Brands | Stations (Number) | Mean (CPL) | Mean Rank | Max | Min | Std. Dev. | Q1 | Q3 |

|---|---|---|---|---|---|---|---|---|

| Shell | 1 | 133.79 | 1 | 169.9 | 93.9 | 16.97 | 123.9 | 146.9 |

| Wesco | 1 | 131.88 | 2 | 169 | 88 | 19.04 | 120 | 147.9 |

| Independent | 7 | 129.76 | 3 | 172 | 80.5 | 18.48 | 118.7 | 143.7 |

| Coles | 27 | 129.29 | 4 | 167.9 | 85.9 | 16.85 | 117.9 | 142.7 |

| United | 1 | 128.82 | 5 | 166.9 | 79.9 | 18.37 | 118.9 | 142.9 |

| BP | 30 | 127.49 | 6 | 169.9 | 79.2 | 18.47 | 115.9 | 141.9 |

| Liberty | 1 | 126.43 | 7 | 164.9 | 81.9 | 17.92 | 115.9 | 139.9 |

| Caltex | 20 | 126.38 | 8 | 169.9 | 78.9 | 18.86 | 113.9 | 141.9 |

| Puma | 19 | 125.98 | 9 | 167.9 | 79.4 | 18.58 | 113.9 | 140.5 |

| Woolworths | 8 | 125.74 | 10 | 167.9 | 78.8 | 18.32 | 113.5 | 139.9 |

| Kwikfuel | 1 | 125.73 | 11 | 161.9 | 83.5 | 17.14 | 115.9 | 138.9 |

| Vibe | 2 | 125.45 | 12 | 161.9 | 79.5 | 17.48 | 114.9 | 138.9 |

| Gull | 2 | 125.14 | 13 | 169.9 | 79.4 | 18.34 | 113.9 | 139.9 |

| Better choice | 3 | 124.67 | 14 | 159.7 | 78.9 | 17.41 | 114.7 | 138.9 |

| Peak | 2 | 124.44 | 15 | 161.9 | 79.9 | 18.20 | 113.9 | 138.9 |

| Total Number of Stations: 125 (Observations = 707,083) | ||||||||

| Major | Independent | |

|---|---|---|

| Relenting Regime (R) | ||

| αR (the daily average price increase) | 14.10 (0.025) | 13.14 (0.046) |

| σR | 5.42 (0.004) | 5.95 (0.013) |

| Undercutting regime (U) | ||

| αU (the daily average price decrease) | −2.25 (0.003) | −1.92 (0.008) |

| σU | 2.37 (0.00) | 2.62 (0.003) |

| Pr (ΔP = 0|U) | 0.00 (0.001) | 0.002 (0.031) |

| Focal Regime (F) | ||

| Constant | 1.18 (0.138) | 9.69 (0.222) |

| TGP | 1.05 (0.001) | 0.98 (0.002) |

| σF | 7.03 (0.054) | 9.51 (0.034) |

| Pr (ΔP = 0|F) | 0.70 (0.00) | 0.87 (0.038) |

| Switching Probabilities | ||

| λRR (switching probability from R to R) | 0.00 (0.000) | 0.00 (0.003) |

| λRU (switching probability from R to U) | 0.97 (0.005) | 0.92 (0.043) |

| λRF (switching probability from R to F) | 0.03 (0.002) | 0.08 (0.005) |

| λUR (switching probability from U to R) | 0.12 (0.06) | 0.09 (0.011) |

| λUU (switching probability from U to U) | 0.84 (0.005) | 0.82 (0.046) |

| λUF (switching probability from U to F) | 0.04 (0.011) | 0.09 (0.009) |

| λFR (switching probability from F to R) | 0.02 (0.003) | 0.07 (0.001) |

| λFU (switching probability from F to U) | 0.03 (0.001) | 0.02 (0.022) |

| λFF (switching probability from F to F) | 0.95 (0.000) | 0.91 (0.006) |

| Stations | 86 | 39 |

| Observations | 482,599 | 224,484 |

| Major | Independent | |

|---|---|---|

| Relenting Regime | ||

| αR (the daily average price increase) | 14.36 (0.025) | 13.57 (0.045) |

| ∂αR / ∂POSITION | −0.165 (0.005) | −1.14 (0.03) |

| σR | 5.367 (0.004) | 5.72 (0.001) |

| Undercutting Regime | ||

| αU (the daily average price decrease) | −1.046 (0.006) | −0.72 (0.058) |

| ∂αU / ∂POSITION | −0.133 (0.000) | −0.01 (0.003) |

| σU | 2.160 (0.007) | 2.62 (0.031) |

| γU = Pr (ΔP = 0|U) | 0.097 (0.001) | 0.01 (0.001) |

| Focal Regime | ||

| Constant | 1.328 (0.136) | 9.69 (0.222) |

| Terminal Gate Price | 1.051 (0.001) | 0.98 (0.002) |

| σF | 6.939 (0.062) | 9.51 (0.013) |

| Pr (ΔP = 0|F) | 0.87 (0.002) | 0.75 (0.062) |

| Switching Probability | ||

| λRR | 0.01 (0.000) | 0.00 (0.061) |

| λRU | 0.91 (0.003) | 0.93 (0.001) |

| λRF | 0.09 (0.001) | 0.07 (0.003) |

| λUR | 0.12 (0.001) | 0.15 (0.011) |

| λUU | 0.87 (0.002) | 0.74 (0.024) |

| λUF | 0.01 (0.021) | 0.11 (0.001) |

| λFR | 0.005 (0.003) | 0.04 (0.014) |

| λFU | 0.005 (0.014) | 0.01 (0.002) |

| λFF | 0.99 (0.006) | 0.96 (0.007) |

| ∂ γU/∂POSITION | 0.02 (0.001) | −0.01 (0.001) |

| ∂ λUR/∂POSITION | −0.01 (0.034) | −0.03 (0.017) |

| ∂ λUU/∂POSITION | 0.01 (0.0542) | 0.04 (0.023) |

| ∂ λUF/∂POSITION | 0.00 (0.001) | 0.00 (0.004) |

| Stations | 86 | 39 |

| Observations | 482,599 | 224,484 |

| Major | Independent | |

|---|---|---|

| Relenting Regime | ||

| αR | 14.52 (0.007) | 13.42 (0.071) |

| ∂αR/∂FOLLOW | −0.73 (0.041) | 1.9 (0.052) |

| σR | 5.2 (0.003) | 6.01 (0.004) |

| Undercutting Regime | ||

| αU | −2.3 (0.016) | −1.96 (0.027) |

| σU | 2.41 (0.032) | 3.2 (0.009) |

| γU = Pr (ΔP = 0|U) | 0.00 (0.00) | 0.012 (0.041) |

| Focal Regime | ||

| Constant | 1.98 (0.071) | 5.2 (0.34) |

| Terminal Gate Price | 1.74 (0.032) | 0.95 (0.004) |

| σF | 6.3 (0.0509) | 7.01 (0.024) |

| Pr (ΔP = 0|F) | 0.73 (0.003) | 0.77 (0.004) |

| Switching Probability | ||

| λRR | 0.02 (0.011) | 0.03 (0.001) |

| λRU | 0.95 (0.032) | 0.91 (0.004) |

| λRF | 0.03 (0.058) | 0.06 (0.011) |

| λUR | 0.14 (0.022) | 0.14 (0.007) |

| λUU | 0.83 (0.003) | 0.79 (0.006) |

| λUF | 0.03 (0.004) | 0.07 (0.014) |

| λFR | 0.03 (0.014) | 0.01 (0.033) |

| λFU | 0.05 (0.032) | 0.03 (0.062) |

| λFF | 0.92 (0.022) | 0.96 (0.024) |

| ∂ λUR/∂FOLLOW | 0.7 (0.019) | 0.36 (0.008) |

| ∂ λUU/∂FOLLOW | −0.34 (0.076) | −0.47 (0.019) |

| ∂ λUF/∂FOLLOW | 0.001 (0.019) | 0.001 (0.001) |

| Stations | 86 | 39 |

| Observations | 482,599 | 224,484 |

| Major | Independent | |

|---|---|---|

| Relenting Regime | ||

| αR | 14.63 (0.016) | 13.73 (0.051) |

| ∂αR/∂POSITION | −0.18 (0.031) | −1.01 (0.001) |

| ∂αR/∂FOLLOW | −0.81 (0.005) | −0.62 (0.002) |

| σR | 5.2 (0.002) | 6.4 (0.007) |

| Undercutting Regime | ||

| αU | −1.05 (0.004) | −0.7 (0.006) |

| ∂αU/∂POSITION | −0.129 (0.009) | −0.03 (0.004) |

| σU | 2.31 (0.022) | 2.88 (0.028) |

| γU = Pr (ΔP = 0|U) | 0.096 (0.005) | 0.093 (0.001) |

| Focal Regime | ||

| Constant | 1.412 (0.007) | 8.79 (0.09) |

| Terminal Gate Price | 1.13(0.019) | 1.04 (0.005) |

| σF | 6.05 (0.041) | 8.6 (0.009) |

| Pr (ΔP = 0|F) | 0.88 (0.008) | 0.79 (0.007) |

| Switching Probability | ||

| λRR | 0.01 (0.001) | 0.01 (0.044) |

| λRU | 0.92 (0.005) | 0.94 (0.008) |

| λRF | 0.07 (0.016) | 0.05 (0.001) |

| λUR | 0.09 (0.009) | 0.11 (0.006) |

| λUU | 0.88 (0.033) | 0.79 (0.004) |

| λUF | 0.03 (0.005) | 0.1 (0.002) |

| λFR | 0.002 (0.001) | 0.02 (0.019) |

| λFU | 0.008 (0.041) | 0.01 (0.005) |

| λFF | 0.99 (0.008) | 0.97 (0.004) |

| ∂ λUR/∂FOLLOW | 0.82 (0.0012) | 0.29 (0.007) |

| ∂ λUU/∂FOLLOW | −0.05 (0.002) | −0.37 (0.015) |

| ∂ λUF/∂FOLLOW | 0.032 (0.0041) | 0.002 (0.004) |

| ∂ γU/∂POSITION | 0.012 (0.0032) | 0.02 (0.004) |

| ∂ λUR/∂POSITION | −0.0199 (0.024) | −0.04 (0.012) |

| ∂ λUU/∂POSITION | 0.0195 (0.014) | 0.03 (0.023) |

| ∂ λUF/∂POSITION | 0.0003 (0.003) | 0.00 (0.005) |

| Stations | 86 | 39 |

| Observations | 482,599 | 224,484 |

| Cycle Characteristics | ||

|---|---|---|

| Majors | Independents | |

| Average Price Jump in Relenting Phase | 14.10 | 13.14 |

| Average Price Drops in Undercutting Phase | −2.25 | −1.92 |

| Duration of Relenting Phase | 1.0001 (0.00) | 1.0001 (0.00) |

| Duration of Undercutting Phase | 6.09 (0.006) | 6.08 (0.014) |

| Cycle Duration | 7.09 (0.004) | 7.08 (0.003) |

| The number of Stations | 86 | 39 |

| Observations | 482,599 | 224,484 |

| Day/Year | Monday | Tuesday | Wednesday | Thursday | Friday | Saturday | Sunday |

|---|---|---|---|---|---|---|---|

| 2003 | 0.32 | 0.14 | 0.13 | 0.10 | 0.09 | 0.04 | 0.17 |

| 2004 | 0.17 | 0.25 | 0.19 | 0.13 | 0.12 | 0.06 | 0.07 |

| 2005 | 0.10 | 0.18 | 0.25 | 0.20 | 0.17 | 0.07 | 0.03 |

| 2006 | 0.37 | 0.21 | 0.22 | 0.13 | 0.05 | 0.01 | 0.02 |

| 2007 | 0.39 | 0.15 | 0.18 | 0.17 | 0.10 | 0.02 | 0.00 |

| 2008 | 0.38 | 0.12 | 0.11 | 0.12 | 0.11 | 0.08 | 0.08 |

| 2009 | 0.08 | 0.02 | 0.19 | 0.30 | 0.31 | 0.07 | 0.02 |

| 2010 | 0.01 | 0.01 | 0.13 | 0.55 | 0.22 | 0.06 | 0.02 |

| 2011 | 0.01 | 0.01 | 0.09 | 0.76 | 0.11 | 0.02 | 0.00 |

| 2012 | 0.01 | 0.01 | 0.03 | 0.81 | 0.12 | 0.02 | 0.01 |

| 2013 | 0.00 | 0.01 | 0.00 | 0.91 | 0.06 | 0.01 | 0.01 |

| 2014 | 0.01 | 0.00 | 0.00 | 0.93 | 0.05 | 0.01 | 0.00 |

| 2015 | 0.01 | 0.52 | 0.04 | 0.39 | 0.03 | 0.01 | 0.00 |

| 2016 | 0.00 | 0.92 | 0.06 | 0.01 | 0.01 | 0.00 | 0.00 |

| 2017 | 0.00 | 0.97 | 0.02 | 0.01 | 0.00 | 0.00 | 0.00 |

| 2018 | 0.00 | 0.98 | 0.01 | 0.00 | 0.00 | 0.00 | 0.00 |

| Day/Year | Monday | Tuesday | Wednesday | Thursday | Friday | Saturday | Sunday |

|---|---|---|---|---|---|---|---|

| 2003 | 0.10 | 0.15 | 0.08 | 0.05 | 0.11 | 0.29 | 0.23 |

| 2004 | 0.14 | 0.16 | 0.07 | 0.06 | 0.12 | 0.20 | 0.24 |

| 2005 | 0.16 | 0.16 | 0.10 | 0.08 | 0.14 | 0.17 | 0.20 |

| 2006 | 0.14 | 0.13 | 0.06 | 0.05 | 0.10 | 0.21 | 0.30 |

| 2007 | 0.13 | 0.12 | 0.10 | 0.07 | 0.10 | 0.17 | 0.31 |

| 2008 | 0.11 | 0.09 | 0.09 | 0.08 | 0.13 | 0.20 | 0.30 |

| 2009 | 0.04 | 0.31 | 0.38 | 0.09 | 0.04 | 0.07 | 0.06 |

| 2010 | 0.02 | 0.21 | 0.61 | 0.08 | 0.04 | 0.02 | 0.01 |

| 2011 | 0.04 | 0.15 | 0.70 | 0.03 | 0.03 | 0.02 | 0.03 |

| 2012 | 0.05 | 0.07 | 0.76 | 0.03 | 0.02 | 0.02 | 0.05 |

| 2013 | 0.05 | 0.05 | 0.82 | 0.03 | 0.01 | 0.01 | 0.02 |

| 2014 | 0.03 | 0.06 | 0.80 | 0.03 | 0.02 | 0.02 | 0.05 |

| 2015 | 0.38 | 0.06 | 0.31 | 0.02 | 0.02 | 0.04 | 0.17 |

| 2016 | 0.78 | 0.02 | 0.00 | 0.00 | 0.02 | 0.02 | 0.16 |

| 2017 | 0.85 | 0.00 | 0.00 | 0.00 | 0.01 | 0.02 | 0.10 |

| 2018 | 0.91 | 0.01 | 0.00 | 0.01 | 0.02 | 0.02 | 0.04 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ghazanfari, A.; Razmjoo, A. The Effect of Market Isolation on Competitive Behavior in Retail Petrol Markets. Sustainability 2022, 14, 8102. https://doi.org/10.3390/su14138102

Ghazanfari A, Razmjoo A. The Effect of Market Isolation on Competitive Behavior in Retail Petrol Markets. Sustainability. 2022; 14(13):8102. https://doi.org/10.3390/su14138102

Chicago/Turabian StyleGhazanfari, Arezoo, and Armin Razmjoo. 2022. "The Effect of Market Isolation on Competitive Behavior in Retail Petrol Markets" Sustainability 14, no. 13: 8102. https://doi.org/10.3390/su14138102

APA StyleGhazanfari, A., & Razmjoo, A. (2022). The Effect of Market Isolation on Competitive Behavior in Retail Petrol Markets. Sustainability, 14(13), 8102. https://doi.org/10.3390/su14138102