A Relationship between Supply Chain Practices, Environmental Sustainability and Financial Performance: Evidence from Manufacturing Companies in Jordan

Abstract

1. Introduction

2. Literature Review

2.1. Nexus Between Supply Chain Practices and Sustainable Performance

2.2. Environmental Sustainability

2.3. Financial Performance

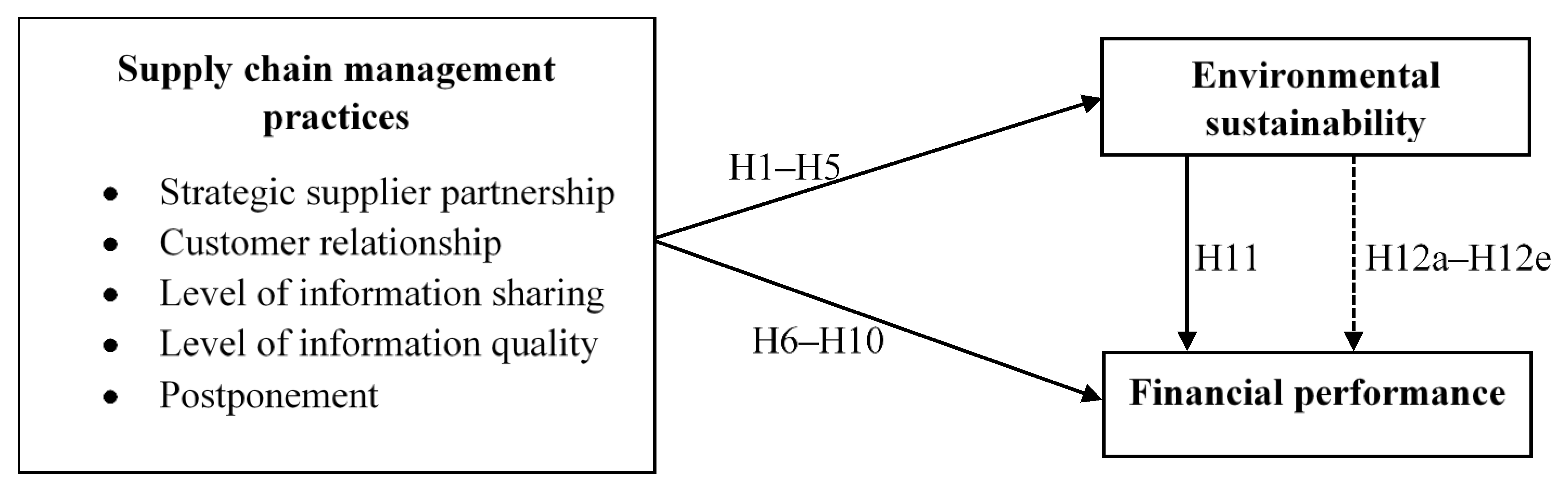

2.4. Hypotheses Development and Conceptual Framework

2.4.1. Supply Chain Practices towards Environmental Sustainability

2.4.2. Effect of SCM Practices on Firm’s Financial Performance

2.4.3. Nexus among Firm’s Financial Performance and Environmental Sustainability

2.4.4. Mediating Effect of Environmental Sustainability on the SCM Practices and Firm’s Financial Performance

2.4.5. Conceptual Framework

3. Research Methodology

3.1. Sampling and Data Collection

3.2. Study Measures

3.3. Respondents’ Profiles

4. Results

4.1. Descriptive Statistics

4.2. Multicollinearity Diagnosis

4.3. Measurement Model Analysis

4.3.1. Convergent Validity and Reliability

4.3.2. Discriminant Validity

4.4. Structural Equation Modeling (SEM)

4.5. Determination of Model Explanatory Power

4.5.1. Coefficient of Determination (R2)

4.5.2. F Square

4.5.3. Predictive Relevance

5. Discussion

6. Conclusions, Implications, and Further Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Alzaman, C. Green supply chain modelling: Literature review. Int. J. Bus. Perform. Supply Chain Model. 2014, 6, 16–39. [Google Scholar] [CrossRef]

- Amin, S.H.; Zhang, G. Closed-loop supply chain network configuration by a multi-objective mathematical model. Int. J. Bus. Perform. Supply Chain Model. 2014, 6, 1–15. [Google Scholar] [CrossRef]

- Ikram, M.; Sroufe, R.; Mohsin, M.; Solangi, Y.A.; Shah SZ, A.; Shahzad, F. Does CSR influence firm performance? A longitudinal study of SME sectors of Pakistan. J. Glob. Responsib. 2019, 11, 27–53. [Google Scholar] [CrossRef]

- Fonseca, L.M.; Domingues, J.P.; Pereira, M.T.; Martins, F.F.; Zimon, D. Assessment of Circular Economy within Portuguese Organizations. Sustainability 2018, 10, 2521. [Google Scholar] [CrossRef]

- Lysenko-Ryba, K.; Zimon, D. Customer Behavioral Reactions to Negative Experiences during the Product Return. Sustainability 2021, 13, 448. [Google Scholar] [CrossRef]

- Li, S.; Ragu-Nathan, B.; Ragu-Nathan, T.S.; Subba Rao, S. The impact of supply chain management practices on competitive advantage and organizational performance. Omega 2006, 34, 107–124. [Google Scholar] [CrossRef]

- Cook, L.S.; Heiser, D.R.; Sengupta, K. The moderating effect of supply chain role on the relationship between supply chain practices and performance. Int. J. Phys. Distrib. Logist. Manag. 2011, 41, 104–134. [Google Scholar] [CrossRef]

- Le, T.T. The effect of green supply chain management practices on sustainability performance in Vietnamese construction materials manufacturing enterprises. Uncertain Supply Chain Manag. 2020, 8, 43–54. [Google Scholar] [CrossRef]

- De, D.; Chowdhury, S.; Dey, P.K.; Ghosh, S.K. Impact of Lean and Sustainability Oriented Innovation on Sustainability Performance of Small and Medium Sized Enterprises: A Data Envelopment Analysis-based framework. Int. J. Prod. Econ. 2020, 219, 416–430. [Google Scholar] [CrossRef]

- Yildiz Çankaya, S.; Sezen, B. Effects of green supply chain management practices on sustainability performance. J. Manuf. Technol. Manag. 2019, 30, 98–121. [Google Scholar] [CrossRef]

- Näyhä, A.; Horn, S. Environmental sustainability—aspects and criteria in forest biorefineries. Sustain. Account. Manag. Policy J. 2012, 3, 161–185. [Google Scholar] [CrossRef]

- Goyal, S.; Routroy, S.; Shah, H. Measuring the environmental sustainability of supply chain for Indian steel industry. Bus. Process Manag. J. 2018, 24, 517–536. [Google Scholar] [CrossRef]

- Martínez-Jurado, P.J.; Moyano-Fuentes, J. Lean Management, Supply Chain Management and Sustainability: A Literature Review. J. Clean. Prod. 2014, 85, 134–150. [Google Scholar] [CrossRef]

- Yang, M.G.M.; Hong, P.; Modi, S.B. Impact of lean manufacturing and environmental management on business performance: An empirical study of manufacturing firms. Int. J. Prod. Econ. 2011, 129, 251–261. [Google Scholar] [CrossRef]

- Hofer, C.; Eroglu, C.; Rossiter Hofer, A. The effect of lean production on financial performance: The mediating role of inventory leanness. Int. J. Prod. Econ. 2012, 138, 242–253. [Google Scholar] [CrossRef]

- Iranmanesh, M.; Zailani, S.; Hyun, S.; Ali, M.; Kim, K. Impact of Lean Manufacturing Practices on Firms’ Sustainable Performance: Lean Culture as a Moderator. Sustainability 2019, 11, 1112. [Google Scholar] [CrossRef]

- Govindan, K.; Azevedo, S.G.; Carvalho, H.; Cruz-Machado, V. Impact of supply chain management practices on sustainability. J. Clean. Prod. 2014, 85, 212–225. [Google Scholar] [CrossRef]

- Bandehnezhad, M.; Zailani, S.; Fernando, Y. An empirical study on the contribution of lean practices to environmental performance of the manufacturing firms in northern region of Malaysia. Int. J. Value Chain Manag. 2012, 6, 144–168. [Google Scholar] [CrossRef]

- Green, K.W.; Inman, R.A.; Sower, V.E.; Zelbst, P.J. Impact of JIT, TQM and green supply chain practices on environmental sustainability. J. Manuf. Technol. Manag. 2019, 30, 26–47. [Google Scholar] [CrossRef]

- Jum′a, L. The effect of value-added activities of key suppliers on the performance of manufacturing firms. Pol. J. Manag. Stud. 2020, 22, 231–246. [Google Scholar] [CrossRef]

- Zimon, D. ISO 14001 and the creation of SSCM in the textile industry. Int. J. Qual. Res. 2020, 14, 739–748. [Google Scholar] [CrossRef]

- Ikram, M.; Sroufe, R.; Rehman, E.; Shah SZ, A.; Mahmoudi, A. Do quality, environmental, and social (QES) certifications improve international trade? A comparative grey relation analysis of developing vs. developed countries. Phys. A Stat. Mech. Its Appl. 2020, 545, 123486. [Google Scholar] [CrossRef]

- Imperatives, S. Report of the World Commission on Environment and Development: Our Common Future; United Nations: New York, NY, USA, 1987. [Google Scholar]

- Marshall, D.; McCarthy, L.; Heavey, C.; McGrath, P. Environmental and social supply chain management sustainability practices: Construct development and measurement. Prod. Plan. Control 2015, 26, 673–690. [Google Scholar] [CrossRef]

- Baliga, R.; Raut, R.D.; Kamble, S.S. Sustainable supply chain management practices and performance. Manag. Environ. Qual. Int. J. 2019, 31, 1147–1182. [Google Scholar] [CrossRef]

- Panigrahi, S.S.; Bahinipati, B.; Jain, V. Sustainable supply chain management. Manag. Environ. Qual. Int. J. 2019, 30, 1001–1049. [Google Scholar] [CrossRef]

- Chardine-Baumann, E.; Botta-Genoulaz, V. A framework for sustainable performance assessment of supply chain management practices. Comput. Ind. Eng. 2014, 76, 138–147. [Google Scholar] [CrossRef]

- Wisner, P.S.; Epstein, M.J.; Bagozzi, R.P. Environmental proactivity and performance. Adv. Environ. Account. Manag. 2009, 4, 105–127. [Google Scholar] [CrossRef]

- Sendawula, K.; Bagire, V.; Mbidde, C.I.; Turyakira, P. Environmental commitment and environmental sustainability practices of manufacturing small and medium enterprises in Uganda. J. Enterp. Communities People Places Glob. Econ. 2020. [Google Scholar] [CrossRef]

- Vu, T.T.; Dang, V.T.W. Environmental Commitment and Firm Financial Performance: A Moderated Mediation Study of Environmental Collaboration with Suppliers and CEO Gender. Int. J. Ethics Syst. 2020. [Google Scholar] [CrossRef]

- Singh, R.K.; Modgil, S.; Tiwari, A.A. Identification and evaluation of determinants of sustainable manufacturing: A case of Indian cement manufacturing. Meas. Bus. Excell. 2019, 23, 24–40. [Google Scholar] [CrossRef]

- Ikram, M.; Zhou, P.; Shah, S.A.A.; Liu, G.Q. Do environmental management systems help improve corporate sustainable development? Evidence from manufacturing companies in Pakistan. J. Clean. Prod. 2019, 226, 628–641. [Google Scholar] [CrossRef]

- Shamout, S.; Boarin, P.; Wilkinson, S. The shift from sustainability to resilience as a driver for policy change: A policy analysis for more resilient and sustainable cities in Jordan. Sustain. Prod. Consum. 2021, 25, 285–298. [Google Scholar] [CrossRef]

- Abu Hajar, H.A.; Tweissi, A.; Abu Hajar, Y.A.; Al-Weshah, R.; Shatanawi, K.M.; Imam, R.; Murad, Y.Z.; Abu Hajer, M.A. Assessment of the municipal solid waste management sector development in Jordan towards green growth by sustainability window analysis. J. Clean. Prod. 2020, 258, 120539. [Google Scholar] [CrossRef]

- Al-Ghwayeen, W.S.; Abdallah, A.B. Green supply chain management and export performance: The mediating role of environmental performance. J. Manuf. Technol. Manag. 2018, 29, 1233–1252. [Google Scholar] [CrossRef]

- Abdallah, A.B.; Al-Ghwayeen, W.S. Green supply chain management and business performance: The mediating roles of environmental and operational performances. Bus. Process. Manag. J. 2019, 26, 489–512. [Google Scholar] [CrossRef]

- Menor, L.J.; Kristal, M.M.; Rosenzweig, E.D. Examining the Influence of Operational Intellectual Capital on Capabilities and Performance. Manuf. Serv. Oper. Manag. 2007, 9, 559–578. [Google Scholar] [CrossRef]

- Boon-itt, S.; Yew Wong, C. The moderating effects of technological and demand uncertainties on the relationship between supply chain integration and customer delivery performance. Int. J. Phys. Distrib. Logist. Manag. 2011, 41, 253–276. [Google Scholar] [CrossRef]

- Zimon, G. Financial Liquidity Management Strategies in Polish Energy Companies. Int. J. Energy Econ. Policy 2020, 10, 365–370. [Google Scholar] [CrossRef]

- Feng, M.; Yu, W.; Wang, X.; Wong, C.Y.; Xu, M.; Xiao, Z. Green supply chain management and financial performance: The mediating roles of operational and environmental performance. Bus. Strategy Environ. 2018, 27, 811–824. [Google Scholar] [CrossRef]

- King, A.; Lenox, M. Exploring the Locus of Profitable Pollution Reduction. Manag. Sci. 2002, 48, 289–299. [Google Scholar] [CrossRef]

- Eng Ann, G.; Zailani, S.; Abd Wahid, N. A study on the impact of environmental management system (EMS) certification towards firms’ performance in Malaysia. Manag. Environ. Qual. Int. J. 2006, 17, 73–93. [Google Scholar] [CrossRef]

- Renukappa, S.; Akintoye, A.; Egbu, C.; Goulding, J. Carbon emission reduction strategies in the UK industrial sectors: An empirical study. Int. J. Clim. Chang. Strateg. Manag. 2013, 5, 304–323. [Google Scholar] [CrossRef]

- Russo, M.V.; Fouts, P.A. A Resource-Based Perspective on Corporate Environmental Performance and Profitability. Acad. Manag. J. 1997, 40, 534–559. [Google Scholar] [CrossRef]

- Luo, X.; Bhattacharya, C.B. The Debate over Doing Good: Corporate Social Performance, Strategic Marketing Levers, and Firm-Idiosyncratic Risk. J. Mark. 2009, 73, 198–213. [Google Scholar] [CrossRef]

- Malhotra, N.K. Marketing Research: An Applied Orientation, 6th ed.; Prentice Hall: Upper Saddle River, NJ, USA, 2010. [Google Scholar]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis: A Global Perspective, 8th ed.; Cengage Learning (EMEA): Andover, UK, 2019. [Google Scholar]

- Creswell, J.W. Research Design: Qualitative, Quantitative, and Mixed Methods Approaches, 3rd ed.; Sage Publications: Thousand Oaks, CA, USA, 2009. [Google Scholar]

- Sekaran, U.; Bougie, R. Research Methods for Business a Skill-Building Approach; John Wiley & Sons: Chichester, UK, 2016. [Google Scholar]

- Ringle, C.M.; Wende, S.; Becker, J.-M. 2015 “SmartPLS 3.” Boenningstedt: SmartPLS GmbH. Available online: http://www.smartpls.com (accessed on 5 January 2021).

- Cox, T.F. An Introduction to Multivariate Data Analysis (Neuausg); Wiley: Hoboken, NJ, USA, 2005. [Google Scholar]

- Claes, F.; Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar]

- Byrne, B.M. Structural Equation Modeling with AMOS: Basic Concepts, Applications, and Programming; Routledge: New York, NY, USA, 2013. [Google Scholar]

- Schumacker, R.E.; Lomax, R.G. A Beginner′s Guide to Structural Equation Modeling; Psychology Press: New York, NY, USA, 2004. [Google Scholar]

- Lin, C.; Chow, W.S.; Madu, C.N.; Kuei, C.-H.; Pei, Y.P. A structural equation model of supply chain quality management and organizational performance. Int. J. Prod. Econ. 2005, 96, 355–365. [Google Scholar] [CrossRef]

- Madzík, P. Capture and evaluation of innovative ideas in early stages of product development. TQM J. 2019, 31, 908–927. [Google Scholar] [CrossRef]

- Hristov, I.; Appolloni, A.; Chirico, A.; Cheng, W. The role of the environmental dimension in the Performance Management System: A systematic review and conceptual framework. J. Clean. Prod. 2021, 126075. [Google Scholar] [CrossRef]

- Zimon, G.; Dankiewicz, R. Trade Credit Management Strategies in SMEs and the COVID-19 Pandemic—A Case of Poland. Sustainability 2020, 12, 6114. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Dimensions | Description |

|---|---|

| Strategic supplier partnership | The partnership among the company and its stakeholders over the long term. It is intended to harness strategic capabilities and operational capabilities of the participating suppliers to help them gain substantial continuing benefits. |

| Customer relationship | The SC practices used for the managing the customer grievances, strongly building the customer long term relationship, and enhancing client satisfaction. |

| Level of information sharing | The degree to which sensitive and confidential information is shared with one’s partner of the supply chain. |

| Level of information quality | Refers to information which has timeliness, accurate, adequate and reputable. |

| Postponement | The method of transferring one or more tasks or activities forward (making, procurement and delivery) in the supply chain to a far later stage. |

| Author | SCM Systems | Performance | Moderating/ Mediating Effect | Country/ Region |

|---|---|---|---|---|

| Li et al. (2006) | SC activities, competitive advantage | Organizational performance | N/A | USA |

| Cook et al. (2011) | SC Practices | Organizational performance | Supply chain roles | North American |

| Yang et al. (2011) | Lean SC practices | Market performance & financial performance | Environmental Practices | International |

| Bandehnezhad et al. (2012) | Lean SC practices | Environmental outcome | N/A | Malaysia |

| Hofer et al. (2012) | Lean SC practices | Financial performance | Inventory leanness | USA |

| Govindan et al. (2014) | Lean and green SCM practices | Supply chain sustainability | N/A | Portugal |

| Al-Ghwayeen & Abdallah (2018) | GSCM | Export performance | Environmental performance | Jordan |

| Feng et al. (2018) | Green SC practices | Financial performance | Environmental and operational performance | China |

| Goyal et al. (2018) | Environmental sustainability enablers | Categories of SC | N/A | India |

| Abdallah & Al-Ghwayeen (2019) | GSCM | Business performance | Environmental and operational performance | Jordan |

| Green et al. (2019) | JIT, TQM and green SC practices | Environmental performance | N/A | USA |

| Iranmanesh et al. (2019) | SCM practices | Sustainable performance | Lean culture | Malaysia |

| Yildiz Çankaya and Sezen (2019) | Green SC practices | Economic, environmental and social performance | N/A | Turkey |

| De et al. (2020) | Lean SC practices and sustainability-oriented innovation (SOI) | Supply chain sustainabilit | N/A | India |

| Le (2020) | Green SC practices | Sustainable performance | N/A | Vietnam |

| Constructs | Code | Items |

|---|---|---|

| Strategic supplier partnership (SSP) | SSP1 | When we select suppliers, quality considered based on criterion |

| SSP2 | We have a centralized supplier complaint management system and operationalized at daily basis. | |

| SSP3 | We give feedback to our suppliers in order to improve the quality of product. | |

| SSP4 | We have incorporated the quality continuous management system and integrated with our key suppliers. | |

| SSP5 | We have a standard operating procedure in which our suppliers are performing the key roles in planning process. | |

| SSP6 | We fully involved our active suppliers in process of product development. | |

| Customer relationship (CR) | CR1 | We have a strong communication network with our customers which assist us to set reliability, responsiveness and to communicate with customers frequently |

| CR2 | We have a transparent customer satisfaction mechanism which measure the level of customer satisfaction on regular basis. | |

| CR3 | We always focus on customer needs and expectation on regular basis. | |

| CR4 | We have online customer care facility to assist customers. | |

| CR5 | We assess the relationship with our customers periodically. | |

| Level of information sharing (IS) | IS1 | We timely share the changing needs in advance with our supply chain member. |

| IS2 | We have strong share propriety information system with or supply chain members. | |

| IS3 | Our supply chain members keeping us fully up to date about business improvement opportunities. | |

| IS4 | Our supply chain members interact and share knowledge with us about our core business processes. | |

| IS5 | We have information sharing system with our supply chain members helps us in business planning. | |

| IS6 | We have an effective business partnership with our supply chain members to keep informed about future events. | |

| Level of information quality (IQ) | IQ1 | We have timely exchange of information system between with supply chain members. |

| IQ2 | We have an transparent exchange of information between our supply chain members. | |

| IQ3 | Information exchange between our supply chain members and us is complete. | |

| IQ4 | Information exchange between our supply chain members and us is adequate. | |

| IQ5 | We have reliable and accountable Information exchange mechanism with our supply chain members. | |

| Postponement (PP) | PP1 | Our products are designed for sub-assembly activities that leads to assembly modulation. |

| PP2 | Our manufacturing and supply chain designed on Just in time process and we postpone final product until customer orders received. | |

| PP3 | We delay product assembly activities at final stage until the last possible location (or nearest to customers) in the supply chain. | |

| Environmental sustainability (ES) | ES1 | Improvement of a firm’ environmental situation. |

| ES2 | Reduction in water waste and/or solid waste. | |

| ES3 | Reduction in air emission. | |

| ES4 | Decrease the usage of hazardous/harmful/toxic materials. | |

| ES5 | Decrease environmental accidents frequency. | |

| Financial performance (FP) | FP1 | Compared to last 3 years ago: Return on Sales (ROS). |

| FP2 | Compared to last 3 years ago: Return on Investment (ROI). | |

| FP3 | Relative to our main competitor(s): Return on Sales (ROS). | |

| FP4 | Relative to our main competitor(s): Return on Investment (ROI). |

| Category | Subcategory | Frequency (n) | Percent (%) |

|---|---|---|---|

| Gender | Male | 335 | 89.1 |

| Female | 41 | 10.9 | |

| Work experience | Less than 5 Years | 105 | 27.9 |

| 5–10 Years | 153 | 40.7 | |

| More than 10 Years | 118 | 31.4 | |

| Education level | Diploma degree | 15 | 4.0 |

| Bachelor’s degree | 308 | 81.9 | |

| Master’s degree and above | 53 | 14.1 | |

| Position | First-line managers | 270 | 71.8 |

| Middle managers | 65 | 17.3 | |

| Top managers | 41 | 10.9 | |

| Number of employees | Less than 20 | 137 | 36.4 |

| 20–99 | 192 | 51.1 | |

| 100 and more | 47 | 12.5 |

| Construct | Mean | Std. Deviation | Skewness | Std. Error | Kurtosis | Std. Error |

|---|---|---|---|---|---|---|

| Strategic supplier partnership | 3.97 | 0.93 | −1.997 | 0.126 | 3.486 | 0.251 |

| Customer relationship | 4.18 | 1.07 | −1.796 | 0.126 | 1.951 | 0.251 |

| Level of information sharing | 4.02 | 0.89 | −2.132 | 0.126 | 3.491 | 0.251 |

| Level of information quality | 3.88 | 0.89 | −1.726 | 0.126 | 2.920 | 0.251 |

| Postponement | 3.96 | 0.91 | −1.680 | 0.126 | 3.030 | 0.251 |

| Environmental sustainability | 3.87 | 0.99 | −1.486 | 0.126 | 2.078 | 0.251 |

| Financial performance | 3.35 | 0.74 | −1.265 | 0.126 | 1.778 | 0.251 |

| Latent Variables | Environmental Sustainability | Financial Performance | ||

|---|---|---|---|---|

| Tolerance | VIF | Tolerance | VIF | |

| Strategic supplier partnership | 0.574 | 1.743 | 0.574 | 1.743 |

| Customer relationship | 0.583 | 1.715 | 0.583 | 1.715 |

| Level of information sharing | 0.511 | 1.957 | 0.511 | 1.957 |

| Level of information quality | 0.550 | 1.818 | 0.550 | 1.818 |

| Postponement | 0.905 | 1.105 | 0.905 | 1.105 |

| Latent Variables | Items | Factor Loadings | Cronbach’s Alpha | Composite Reliability | Average Variance Extracted (AVE) |

|---|---|---|---|---|---|

| Strategic supplier partnership | SSP1 | 0.941 | 0.965 | 0.971 | 0.850 |

| SSP2 | 0.921 | ||||

| SSP3 | 0.904 | ||||

| SSP4 | 0.938 | ||||

| SSP5 | 0.928 | ||||

| SSP6 | 0.898 | ||||

| Customer relationship | CR1 | 0.953 | 0.972 | 0.978 | 0.898 |

| CR2 | 0.949 | ||||

| CR3 | 0.931 | ||||

| CR4 | 0.950 | ||||

| CR5 | 0.955 | ||||

| Level of information sharing | IS1 | 0.907 | 0.945 | 0.956 | 0.785 |

| IS2 | 0.857 | ||||

| IS3 | 0.858 | ||||

| IS4 | 0.912 | ||||

| IS5 | 0.885 | ||||

| IS6 | 0.894 | ||||

| Level of information quality | IQ1 | 0.937 | 0.963 | 0.971 | 0.871 |

| IQ2 | 0.944 | ||||

| IQ3 | 0.927 | ||||

| IQ4 | 0.944 | ||||

| IQ5 | 0.913 | ||||

| Postponement | PP1 | 0.958 | 0.955 | 0.971 | 0.917 |

| PP2 | 0.966 | ||||

| PP3 | 0.949 | ||||

| Environmental sustainability | ES1 | 0.958 | 0.978 | 0.983 | 0.919 |

| ES2 | 0.960 | ||||

| ES3 | 0.967 | ||||

| ES4 | 0.954 | ||||

| ES5 | 0.955 | ||||

| Financial performance | FP1 | 0.786 | 0.822 | 0.882 | 0.652 |

| FP2 | 0.783 | ||||

| FP3 | 0.832 | ||||

| FP4 | 0.827 |

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | |

|---|---|---|---|---|---|---|---|

| 1. Customer relationship | 0.948 | ||||||

| 2. Environmental sustainability | 0.495 | 0.959 | |||||

| 3. Financial performance | 0.470 | 0.699 | 0.807 | ||||

| 4. Level of information quality | 0.547 | 0.542 | 0.464 | 0.933 | |||

| 5. Level of information sharing | 0.580 | 0.576 | 0.511 | 0.582 | 0.886 | ||

| 6. Postponement | 0.236 | 0.533 | 0.494 | 0.229 | 0.230 | 0.958 | |

| 7. Strategic supplier partnership | 0.487 | 0.444 | 0.476 | 0.554 | 0.576 | 0.281 | 0.922 |

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | |

|---|---|---|---|---|---|---|---|

| 1.Customer relationship | |||||||

| 2.Environmental sustainability | 0.507 | ||||||

| 3. Financial performance | 0.524 | 0.779 | |||||

| 4. Level of information quality | 0.564 | 0.557 | 0.519 | ||||

| 5. Level of information sharing | 0.606 | 0.599 | 0.580 | 0.610 | |||

| 6. Postponement | 0.244 | 0.551 | 0.556 | 0.239 | 0.242 | ||

| 7. Strategic supplier partnership | 0.501 | 0.456 | 0.533 | 0.574 | 0.602 | 0.293 |

| Direct Paths | Path Coefficients (β) | T Statistics | p-Values | Results |

|---|---|---|---|---|

| H1: Strategic supplier partnership → Environmental sustainability | −0.020 | 0.381 | 0.703 | Rejected |

| H2: Customer relationship → Environmental sustainability | 0.115 | 2.167 | 0.030 * | Accepted |

| H3: Level of information sharing → Environmental sustainability | 0.300 | 6.214 | 0.000 * | Accepted |

| H4: Level of information quality → Environmental sustainability | 0.226 | 4.994 | 0.000 * | Accepted |

| H5: Postponement → Environmental sustainability | 0.391 | 7.116 | 0.000 * | Accepted |

| H6: Strategic supplier partnership → Financial performance | 0.133 | 3.224 | 0.001 * | Accepted |

| H7: Customer relationship → Financial performance | 0.090 | 1.866 | 0.062 | Rejected |

| H8: Level of information sharing → Financial performance | 0.074 | 1.409 | 0.159 | Rejected |

| H9: Level of information quality → Financial performance | 0.012 | 0.236 | 0.813 | Rejected |

| H10: Postponement → Financial performance | 0.173 | 3.813 | 0.000 * | Accepted |

| H11: Environmental sustainability → Financial performance | 0.454 | 7.624 | 0.000 * | Accepted |

| Indirect Effect | Path Coefficients (β) | T Statistics | p Values | Results |

|---|---|---|---|---|

| H12a: Strategic supplier partnership → Environmental sustainability → Financial performance | −0.009 | 0.380 | 0.704 | Rejected |

| H12b: Customer relationship → Environmental sustainability → Financial performance | 0.052 | 2.149 | 0.032 | Accepted |

| H12c: Level of information sharing → Environmental sustainability → Financial performance | 0.136 | 4.744 | 0.000 | Accepted |

| H12d: Level of information quality → Environmental sustainability → Financial performance | 0.103 | 4.421 | 0.000 | Accepted |

| H12e: Postponement → Environmental sustainability → Financial performance | 0.177 | 4.600 | 0.000 | Accepted |

| Latent Variables | R Square | R Square Adjusted | Comment |

|---|---|---|---|

| Environmental sustainability | 0.551 | 0.545 | Moderate |

| Financial performance | 0.552 | 0.545 | Moderate |

| Latent Variables | Environmental Sustainability | Financial Performance |

|---|---|---|

| Customer relationship | 0.017 | 0.010 |

| Environmental sustainability | 0.207 | |

| Level of information quality | 0.063 | 0.000 |

| Level of information sharing | 0.102 | 0.006 |

| Postponement | 0.308 | 0.046 |

| Strategic supplier partnership | 0.001 | 0.022 |

| Latent Variables | SSO | SSE | Q2 (=1-SSE/SSO) |

|---|---|---|---|

| Customer relationship | 1880.000 | 1880.000 | |

| Environmental sustainability | 1880.000 | 937.785 | 0.501 |

| Financial performance | 1504.000 | 981.287 | 0.348 |

| Level of information quality | 1880.000 | 1880.000 | |

| Level of information sharing | 2256.000 | 2256.000 | |

| Postponement | 1128.000 | 1128.000 | |

| Strategic supplier partnership | 2256.000 | 2256.000 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Jum’a, L.; Zimon, D.; Ikram, M. A Relationship between Supply Chain Practices, Environmental Sustainability and Financial Performance: Evidence from Manufacturing Companies in Jordan. Sustainability 2021, 13, 2152. https://doi.org/10.3390/su13042152

Jum’a L, Zimon D, Ikram M. A Relationship between Supply Chain Practices, Environmental Sustainability and Financial Performance: Evidence from Manufacturing Companies in Jordan. Sustainability. 2021; 13(4):2152. https://doi.org/10.3390/su13042152

Chicago/Turabian StyleJum’a, Luay, Dominik Zimon, and Muhammad Ikram. 2021. "A Relationship between Supply Chain Practices, Environmental Sustainability and Financial Performance: Evidence from Manufacturing Companies in Jordan" Sustainability 13, no. 4: 2152. https://doi.org/10.3390/su13042152

APA StyleJum’a, L., Zimon, D., & Ikram, M. (2021). A Relationship between Supply Chain Practices, Environmental Sustainability and Financial Performance: Evidence from Manufacturing Companies in Jordan. Sustainability, 13(4), 2152. https://doi.org/10.3390/su13042152