The Impact of B Corp Certification on Growth

Abstract

:1. Introduction

2. Literature and Hypotheses

3. Research Design

3.1. Methodology

3.1.1. Motivation

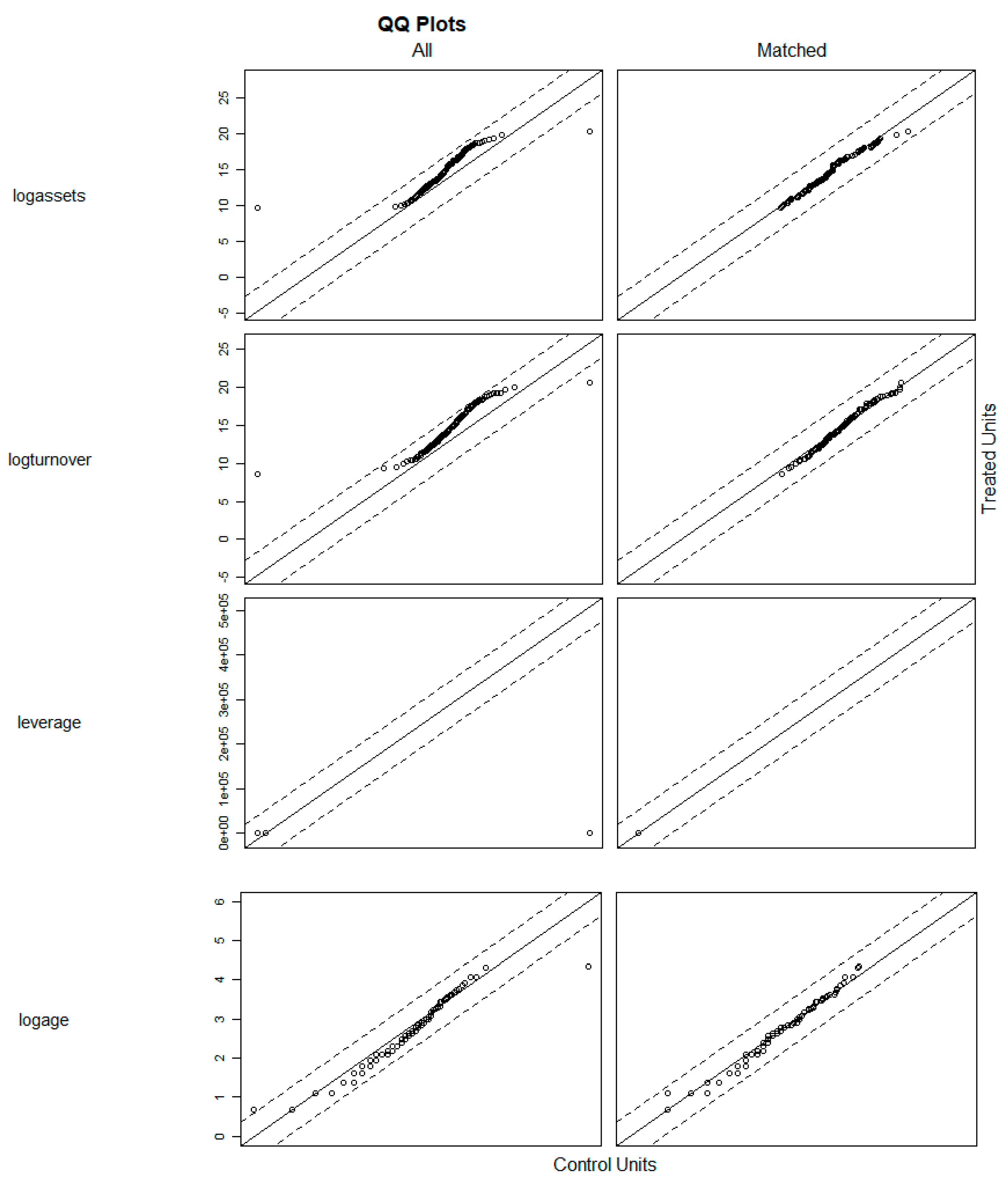

3.1.2. Propensity Score Matching

3.1.3. Difference-in-Differences Analysis

3.2. Sample Selection and Data Collection

4. Results

4.1. Propensity Score Matching

4.2. Difference-in-Differences Analysis

4.2.1. Descriptive Statistics

4.2.2. Correlations

4.2.3. Regression Analysis

4.2.4. Parallel Trend Assumption

5. Discussion

5.1. Contributions to the Literature

5.2. Implications for Practice

6. Concluding Remarks

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Saebi, T.; Foss, N.J.; Linder, S. Social Entrepreneurship Research: Past Achievements and Future Promises. J. Manag. 2018, 45, 70–95. [Google Scholar] [CrossRef]

- Haigh, N.; Walker, J.; Bacq, S.; Kickul, J. Hybrid Organizations: Origins, Strategies, Impacts, and Implications. Calif. Manag. Rev. 2015, 57, 5–12. [Google Scholar] [CrossRef] [Green Version]

- Muñoz, P.; Kimmitt, J. Social mission as competitive advantage: A configurational analysis of the strategic conditions of social entrepreneurship. J. Bus. Res. 2019, 101, 854–861. [Google Scholar] [CrossRef]

- Chauhan, Y.; O’Neill, H.M. Strategic Advantages through Social Responsiveness: The Case of Certified B-Corps; SSRN: Rochester, NY, USA, 2020. [Google Scholar] [CrossRef]

- Hynes, B. Growing the social enterprise—Issues and challenges. Soc. Enterp. J. 2009, 5, 114–125. [Google Scholar] [CrossRef]

- Moratis, L. Signalling Responsibility? Applying Signalling Theory to the ISO 26000 Standard for Social Responsibility. Sustainability 2018, 10, 4172. [Google Scholar] [CrossRef] [Green Version]

- B Lab. A Global Community of Leaders. Available online: https://bcorporation.net (accessed on 26 May 2021).

- B Lab. About B Corps. Available online: https://bcorporation.net/about-b-corps (accessed on 24 November 2020).

- Parker, S.C.; Gamble, E.N.; Moroz, P.W.; Branzei, O. The Impact of B Lab Certification on Firm Growth. Acad. Manag. Discov. 2019, 5, 57–77. [Google Scholar] [CrossRef]

- Conger, M.; McMullen, J.S.; Bergman, B.J.; York, J.G. Category membership, identity control, and the reevaluation of prosocial opportunities. J. Bus. Ventur. 2018, 33, 179–206. [Google Scholar] [CrossRef]

- Gamble, E.N.; Parker, S.C.; Moroz, P.W. Measuring the Integration of Social and Environmental Missions in Hybrid Organizations. J. Bus. Ethics 2020, 167, 271–284. [Google Scholar] [CrossRef] [Green Version]

- Moroz, P.W.; Gamble, E.N. Business model innovation as a window into adaptive tensions: Five paths on the B Corp journey. J. Bus. Res. 2021, 125, 672–683. [Google Scholar] [CrossRef]

- Muñoz, P.; Cacciotti, G.; Cohen, B. The double-edged sword of purpose-driven behavior in sustainable venturing. J. Bus. Ventur. 2018, 33, 149–178. [Google Scholar] [CrossRef] [Green Version]

- Sharma, G.; Beveridge, A.J.; Haigh, N. A configural framework of practice change for B corporations. J. Bus. Ventur. 2018, 33, 207–224. [Google Scholar] [CrossRef]

- Villela, M.; Bulgacov, S.; Morgan, G. B Corp Certification and Its Impact on Organizations Over Time. J. Bus. Ethics 2021, 170, 343–357. [Google Scholar] [CrossRef]

- Chen, X.; Kelly, T.F. B-Corps—A Growing Form of Social Enterprise. J. Leadersh. Organ. Stud. 2015, 22, 102–114. [Google Scholar] [CrossRef]

- Romi, A.; Cook, K.A.; Dixon-Fowler, H.R. The influence of social responsibility on employee productivity and sales growth. Sustain. Account. Manag. Policy J. 2018, 9, 392–421. [Google Scholar] [CrossRef]

- Paelman, V.; Van Cauwenberge, P.; Bauwhede, H.V. Effect of B Corp Certification on Short-Term Growth: European Evidence. Sustainability 2020, 12, 8459. [Google Scholar] [CrossRef]

- Toffel, M.W. Voluntary Environmental Management Initiatives: Smoke Signals or Smoke Screens? Ph.D. Thesis, University of California, Berkeley, CA, USA, 2005. [Google Scholar]

- Ye, Y.; Yeung, A.C.; Huo, B. Maintaining stability while boosting growth? The long-term impact of environmental accreditations on firms’ financial risk and sales growth. Int. J. Oper. Prod. Manag. 2020, 40, 1829–1856. [Google Scholar] [CrossRef]

- Doherty, B.; Haugh, H.; Lyon, F. Social Enterprises as Hybrid Organizations: A Review and Research Agenda. Int. J. Manag. Rev. 2014, 16, 417–436. [Google Scholar] [CrossRef] [Green Version]

- Dufays, F. Exploring the drivers of tensions in social innovation management in the context of social entrepreneurial teams. Manag. Decis. 2019, 57, 1344–1361. [Google Scholar] [CrossRef]

- Yin, J.; Chen, H. Dual-goal management in social enterprises: Evidence from China. Manag. Decis. 2019, 57, 1362–1381. [Google Scholar] [CrossRef]

- Austin, J.; Stevenson, H.; Wei–Skillern, J. Social and Commercial Entrepreneurship: Same, Different, or Both? Entrep. Theory Pract. 2006, 30, 1–22. [Google Scholar] [CrossRef] [Green Version]

- Park, K. B the Change: Social Companies, B Corps, and Benefit Corporations. Ph.D. Thesis, Princeton University, Princeton, NJ, USA, 2018. [Google Scholar]

- Lee, M.; Jay, J. Strategic Responses to Hybrid Social Ventures. Calif. Manag. Rev. 2015, 57, 126–147. [Google Scholar] [CrossRef]

- Bianchi, C.; Reyes, V.; Devenin, V. Consumer motivations to purchase from benefit corporations (B Corps). Corp. Soc. Responsib. Environ. Manag. 2020, 27, 1445–1453. [Google Scholar] [CrossRef]

- Fosfuri, A.; Giarratana, M.; Roca, E. Social Business Hybrids: Demand Externalities, Competitive Advantage, and Growth Through Diversification. Organ. Sci. 2016, 27, 1275–1289. [Google Scholar] [CrossRef]

- Rowley, T.; Berman, S. A Brand New Brand of Corporate Social Performance. Bus. Soc. 2000, 39, 397–418. [Google Scholar] [CrossRef]

- Kim, M.; Kim, J. Corporate social responsibility, employee engagement, well-being and the task performance of frontline employees. Manag. Decis. 2020. ahead of print. [Google Scholar] [CrossRef]

- Connelly, B.L.; Certo, S.T.; Ireland, R.D.; Reutzel, C.R. Signaling Theory: A Review and Assessment. J. Manag. 2010, 37, 39–67. [Google Scholar] [CrossRef]

- Bergh, D.D.; Connelly, B.L.; Ketchen, D.J.; Shannon, L.M. Signalling Theory and Equilibrium in Strategic Management Research: An Assessment and a Research Agenda. J. Manag. Stud. 2014, 51, 1334–1360. [Google Scholar] [CrossRef]

- Cao, K.; Gehman, J.; Grimes, M.G. Standing out and fitting in: Charting the emergence of Certified B Corporations by industry and region. In Hybrid Ventures; Emerald Publishing Limited: Bingley, UK, 2017; pp. 1–38. [Google Scholar]

- Nigri, G.; Del Baldo, M. Sustainability Reporting and Performance Measurement Systems: How do Small- and Medium-Sized Benefit Corporations Manage Integration? Sustainability 2018, 10, 4499. [Google Scholar] [CrossRef] [Green Version]

- B Lab. B Impact Report. Available online: https://bcorporation.net/directory/sep-jordan (accessed on 26 November 2020).

- B Lab. Certification. Available online: https://bcorporation.net/certification (accessed on 5 June 2020).

- Havnes, P.-A.; Senneseth, K. A Panel Study of Firm Growth among SMEs in Networks. Small Bus. Econ. 2001, 16, 293–302. [Google Scholar] [CrossRef]

- Mauboussein, M.J. The True Measures of Success; Harvard Business Review: Cambridge, MA, USA, 2012. [Google Scholar]

- Pischke, J.S. Empirical Methods in Applied Economics: Lecture Notes; MIT: Cambridge, MA, USA, 2005. [Google Scholar]

- Heckman, J.J.; Ichimura, H.; Todd, P.E. Matching as an Econometric Evaluation Estimator: Evidence from Evaluating a Job Training Programme. Rev. Econ. Stud. 1997, 64, 605–654. [Google Scholar] [CrossRef]

- Rosenbaum, P.R.; Rubin, D.B. The central role of the propensity score in observational studies for causal effects. Biometrika 1983, 70, 41–55. [Google Scholar] [CrossRef]

- Harjoto, M.; Laksmana, I.; Yang, Y.-W. Why do companies obtain the B corporation certification? Soc. Responsib. J. 2019, 15, 621–639. [Google Scholar] [CrossRef]

- Wilburn, K.; Wilburn, R. The double bottom line: Profit and social benefit. Bus. Horiz. 2014, 57, 11–20. [Google Scholar] [CrossRef]

- Almus, M.; Nerlinger, E.A. Growth of New Technology-Based Firms: Which Factors Matter? Small Bus. Econ. 1999, 13, 141–154. [Google Scholar] [CrossRef]

- Becchetti, L.; Trovato, G. The Determinants of Growth for Small and Medium Sized Firms. The Role of the Availability of External Finance. Small Bus. Econ. 2002, 19, 291–306. [Google Scholar] [CrossRef]

- Evans, D.S. Tests of Alternative Theories of Firm Growth. J. Political Econ. 1987, 95, 657–674. [Google Scholar] [CrossRef]

- B Lab. B Corp Index Report 2012; B Lab: Berwyn, PA, USA, 2012. [Google Scholar]

- Das, S. Size, age and firm growth in an infant industry: The computer hardware industry in India. Int. J. Ind. Organ. 1995, 13, 111–126. [Google Scholar] [CrossRef]

- Heshmati, A. On the Growth of Micro and Small Firms: Evidence from Sweden. Small Bus. Econ. 2001, 17, 213–228. [Google Scholar] [CrossRef]

- Siqueira, A.C.O.; Guenster, N.; Vanacker, T.; Crucke, S. A longitudinal comparison of capital structure between young for-profit social and commercial enterprises. J. Bus. Ventur. 2018, 33, 225–240. [Google Scholar] [CrossRef] [Green Version]

- Huynh, K.P.; Petrunia, R.J. Age effects, leverage and firm growth. J. Econ. Dyn. Control 2010, 34, 1003–1013. [Google Scholar] [CrossRef]

- Lang, L.; Ofek, E.; Stulz, R. Leverage, investment, and firm growth. J. Financ. Econ. 1996, 40, 3–29. [Google Scholar] [CrossRef] [Green Version]

- Hickman, L.; Byrd, J.; Hickman, K. Explaining the Location of Mission-Driven Businesses: An Examination of B-Corps. J. Corp. Citizsh. 2014, 2014, 13–25. [Google Scholar] [CrossRef]

- Lacmanovic, S.; Milec, D. The relevance and distribution of certified B Corporations in the European Union economy. In Proceedings of the Economic and Social Development: 36th International Scientific Conference on Economic and Social Development—“Building Resilient Society”: Book of Proceedings, Zagreb, Croatia, 14 December 2016; pp. 337–346. [Google Scholar]

- Jovanovic, B. Selection and the Evolution of Industry. Econometrica 1982, 50, 649. [Google Scholar] [CrossRef]

- Stuart, E.A. Matching Methods for Causal Inference: A Review and a Look Forward. Stat. Sci. 2010, 25, 1–21. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Ho, D.E.; Imai, K.; King, G.; Stuart, E.A. MatchIt: Nonparametric Preprocessing for Parametric Causal Inference. J. Stat. Softw. 2011, 42, 1–28. [Google Scholar] [CrossRef] [Green Version]

- StataCorp LLC. Stata Statistical Software: Release 15; StataCorp LLC: College Station, TX, USA, 2017. [Google Scholar]

- Autor, D.H. Outsourcing at Will: The Contribution of Unjust Dismissal Doctrine to the Growth of Employment Outsourcing. J. Labor Econ. 2003, 21, 1–42. [Google Scholar] [CrossRef] [Green Version]

- Vickers, I.; Lyon, F. Beyond green niches? Growth strategies of environmentally-motivated social enterprises. Int. Small Bus. J. Res. Entrep. 2012, 32, 449–470. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Before Matching | After Matching | |||||

|---|---|---|---|---|---|---|

| Means Treated | Means Control | SMD | Means Treated | Means Control | SMD | |

| Ln(Assets) | 14.4523 | 13.2035 | 0.5220 | 14.4523 | 14.5553 | −0.0431 |

| Ln(Turnover) | 14.5122 | 12.9055 | 0.6401 | 14.5122 | 14.5689 | −0.0226 |

| Leverage | 0.7224 | 2.2844 | −2.5951 | 0.7224 | 0.6542 | 0.1134 |

| Ln(Age) | 2.3335 | 2.4810 | −0.1736 | 2.3335 | 2.3940 | −0.0712 |

| Observations | 147 | 2,995,223 | 147 | 147 | ||

| Mean | S.D. | Min | Q25 | Median | Q75 | Max | |

|---|---|---|---|---|---|---|---|

| Growth | 0.1147 | 0.3741 | −0.7846 | −0.426 | 0.0658 | 0.2270 | 1.3862 |

| Treatment | 0.5 | 0.5002 | 0 | 0 | 0.5 | 1 | 1 |

| Post | 0.4464 | 0.4973 | 0 | 0 | 0 | 1 | 1 |

| Certified | 0.2232 | 0.4165 | 0 | 0 | 0 | 0 | 1 |

| Ln(Turnover) | 14.5344 | 2.3950 | 9.9002 | 12.8381 | 14.3637 | 16.0561 | 19.4936 |

| Ln(Age) | 2.4338 | 0.7342 | 1.0986 | 1.9459 | 2.3979 | 2.9444 | 3.8501 |

| Leverage | 0.6517 | 0.2646 | 0.0968 | 0.4651 | 0.6937 | 0.8438 | 1.1950 |

| n = 1362 | 1. | 2. | 3. | 4. | 5. |

|---|---|---|---|---|---|

| 1. Growth | 1 | ||||

| 2. Certified | 0.0248 | 1 | |||

| 3. Ln(Turnover) | −0.2168 *** | 0.0283 | 1 | ||

| 4. Ln(Age) | −0.2900 *** | 0.0581 ** | 0.5756 *** | 1 | |

| 5. Leverage | 0.0088 | 0.0168 | 0.0635 ** | −0.0464 * | 1 |

| (a) Hypothesis 1 | (b) Hypothesis 2 | ||

|---|---|---|---|

| Expected Sign | Dependent Variable Turnover Growth | Dependent Variable Turnover Growth | |

| Test variables | |||

| Certifiedi,t | + | 0.1430 *** (0.0381) | 0.0675 * (0.0518) |

| Certifiedi,t × YearsToTreatmenti,t | + | 0.0617 ** (0.0323) | |

| Control variables | |||

| Treatmenti,t × YearsToTreatmenti,t | ? | 0.0091 (0.0174) | |

| Ln(Turnover)i,t−1 | - | −0.3416 * (0.2044) | −0.3429 * (0.2006) |

| (Ln(Turnover)i,t−1)2 | ? | −0.0020 (0.0090) | −0.0020 (0.088) |

| Ln(Age)i,t−1 | ? | −0.9384 ** (0.4768) | −0.8674 * (0.4705) |

| (Ln(Age)i,t−1)2 | ? | 0.2423 * (0.1289) | 0.2359 * (0.1285) |

| Ln(Turnover)i,t−1 × Ln(Age)i,t−1 | ? | 0.0382 (0.0350) | 0.0348 (0.0346) |

| Leveragei,t−1 | ? | −0.0724 (0.1035) | −0.0851 (0.1021) |

| Firm Fixed Effects | Yes | Yes | |

| Year Fixed Effects | Yes | Yes | |

| Time Fixed Effects | Yes | Yes | |

| R-squared | 0.3261 *** | 0.3317 *** | |

| Observations | 1362 | 1362 | |

| Number of firms | 258 | 258 |

| Expected Sign | Dependent Variable Turnover Growth | ||

|---|---|---|---|

| Test variables | Coef. | ||

| T − 6 × Treatmenti | ? | −0.1713 | (0.1466) |

| T − 5 × Treatmenti | ? | 0.0154 | (0.0901) |

| T − 4 × Treatmenti | ? | −0.0101 | (0.0811) |

| T − 3 × Treatmenti | ? | 0.0100 | (0.0550) |

| T − 2 × Treatmenti | ? | 0.0275 | (0.0519) |

| T − 1 × Treatmenti = Base year | |||

| T0 × Treatmenti | + | 0.1003 * | (0.0525) |

| T + 1 × Treatmenti | + | 0.1744 *** | (0.0530) |

| T + 2 × Treatmenti | + | 0.1695 ** | (0.0777) |

| T + 3 × Treatmenti | + | 0.3348 *** | (0.1177) |

| T + 4 × Treatmenti | + | 0.6016 *** | (0.1724) |

| T + 5 × Treatmenti | + | 0.3923 *** | (0.1188) |

| Control variables | |||

| Ln(Turnover)i,t−1 | - | −0.3405 * | (0.1992) |

| (Ln(Turnover)i,t−1)2 | ? | −0.0021 | (0.0088) |

| Ln(Age)i,t−1 | ? | −0.8718 * | (0.4727) |

| (Ln(Age)i,t−1)2 | ? | 0.2414 * | (0.1302) |

| Ln(Turnover)i,t−1 × Ln(Age)i,t−1 | ? | 0.0342 | (0.0343) |

| Leveragei,t−1 | ? | −0.0892 | (0.1014) |

| Firm Fixed Effects | Yes | ||

| Year Fixed Effects | Yes | ||

| Time Fixed Effects | Yes | ||

| R-squared | 0.3353 *** | ||

| Observations | 1362 | ||

| Number of firms | 258 | ||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Paelman, V.; Van Cauwenberge, P.; Vander Bauwhede, H. The Impact of B Corp Certification on Growth. Sustainability 2021, 13, 7191. https://doi.org/10.3390/su13137191

Paelman V, Van Cauwenberge P, Vander Bauwhede H. The Impact of B Corp Certification on Growth. Sustainability. 2021; 13(13):7191. https://doi.org/10.3390/su13137191

Chicago/Turabian StylePaelman, Valerie, Philippe Van Cauwenberge, and Heidi Vander Bauwhede. 2021. "The Impact of B Corp Certification on Growth" Sustainability 13, no. 13: 7191. https://doi.org/10.3390/su13137191

APA StylePaelman, V., Van Cauwenberge, P., & Vander Bauwhede, H. (2021). The Impact of B Corp Certification on Growth. Sustainability, 13(13), 7191. https://doi.org/10.3390/su13137191