Decision Tree and AHP Methods Application for Projects Assessment: A Case Study

Abstract

1. Introduction

- The changes of the priorities leading to improved value of the object, e.g., the other burnt house might stimulate the investor to build the current project for himself, or some various reasons might drop the interest of having some property for the investor—he might tend to want to sell it, meaning the values in AHP assessment will shift.

- The investor might face the financial problems leading to drops in the costs to ratings mapping.

- The investor might financially succeed with some other projects, extending his abilities to invest, which would increase the costs to ratings mapping.

- The investor might react to some external factors, changing his priorities, such as financial crisis, any other reasons for the changes of the market prices.

- We provide the approach to assess the decision model in terms of sensitivity to the changes of conditions, more specifically—the mappings of the rating scale to the monetary values, which describe the investor-specific information.

- The application of the proposed techniques to the case study leads to a deeper understanding of how to apply it in a similar way to other types of applications that are required in other researches.

- The proposed methodology contributes to the general analysis of the robustness of decisions, i.e., how sensitive the possible decisions are, depending on the changes of the decision-maker.

2. The Background of the Research

3. The Methodology of the Research

- Identification of the major stakeholders involved in the project execution process.

- Development of a decision tree scheme to select the best project from the planned set of alternatives.

- Creation of the algorithms for the decision tree solution.

- Adaptation of AHP method to assess the investor’s subjective opinion about the various projects, predicting whether the investor would like to sell the completed project or not.

- The parametrisation of the investor’s behaviour with a special mapping of the ratings scale to the monetary values and the sensitivity analysis.

- Analysis of how the different mappings of the rating scale to the monetary values affect the assessment of the projects in the decision tree and visualisation of the obtained results.

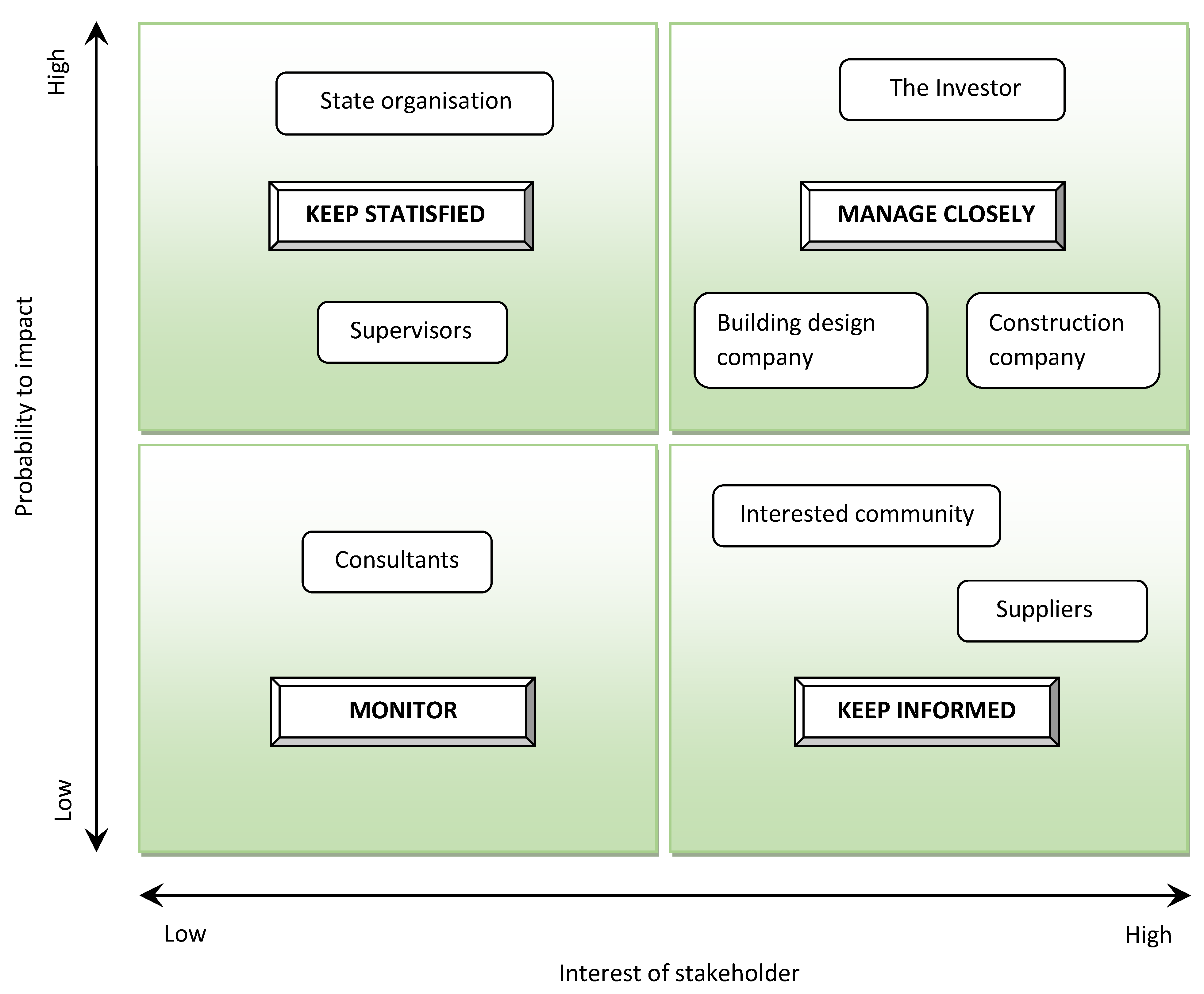

3.1. Identification of Major Stakeholders

- Investor in a roof installation project.

- State organisations.

- Building design company.

- Interested community.

- Construction company.

- Suppliers.

- Consultants.

- Supervisors.

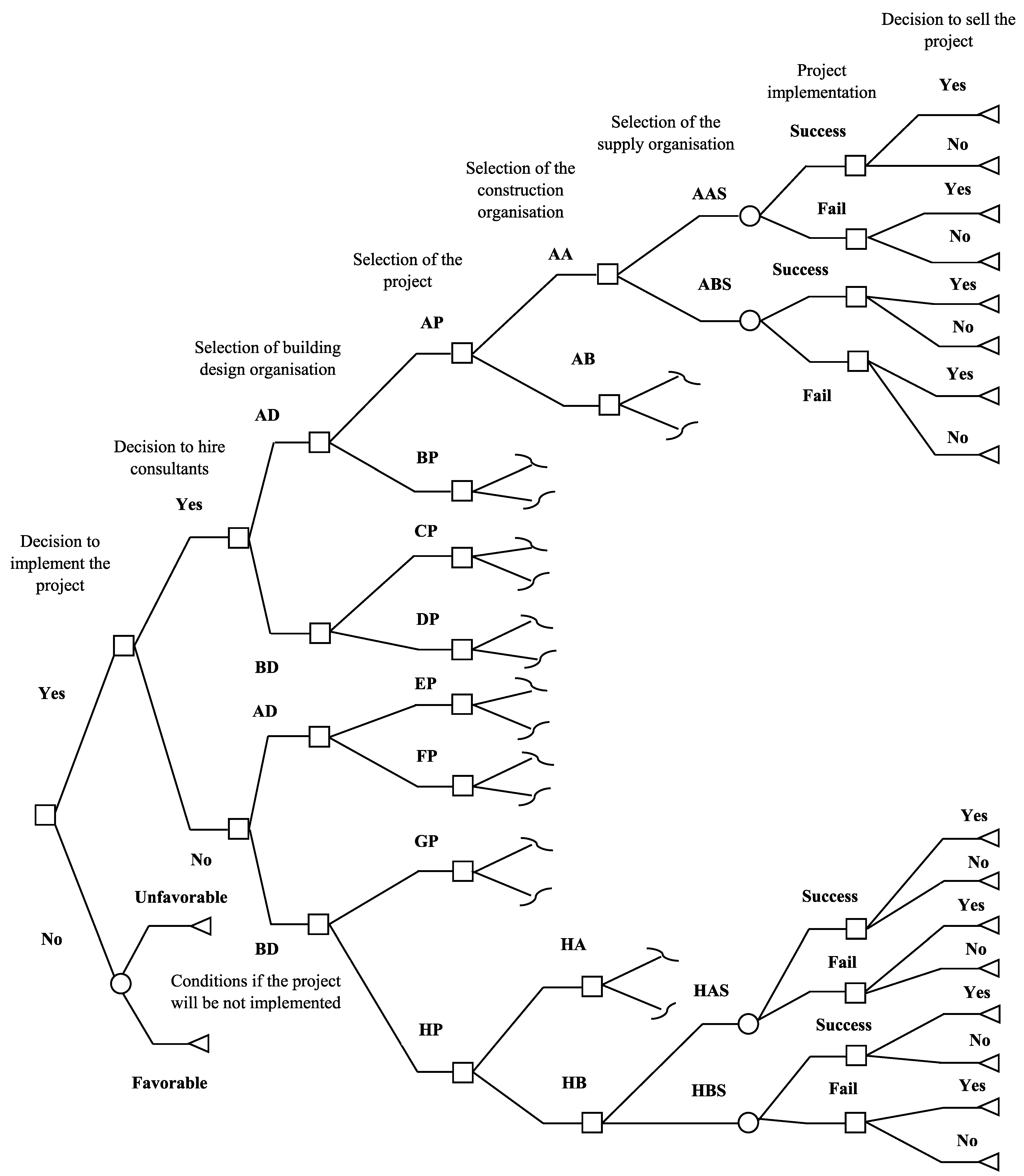

3.2. The Decision Tree

3.3. The Main Steps for the Sensitivity Analysis

- The investor’s behavior was parameterized based on a subjective opinion regarding the monetary value of the project (more details will be provided later, see Section 4.4).

- Subsequently, by changing the introduced monetary value for the economic criterion, a series of mappings with the rating scale were formed.

- It was calculated how the parameters of the economic criterion would change if we apply different scale mapping multipliers.

- It was analysed how the results (of the decision tree and AHP method application) were changed, depending on the changes in the scale.

- It was analysed how the investor’s behavior would change if we offer him various projects based on the market price.

- The consequences of decisions regarding whether to sell project results or not were investigated. It was taken into account that not only the investor was interested in the results of the project, but there were also other stakeholders affected by the investor’s changing opinion. It is well known that stakeholders were interested in how the starting market price was formed.

- The visualisation of the results of the decision tree for various projects was performed.

- It was described how the possible final result that was obtained in the decision tree might be changed, depending on possible changes in the investor’s opinion.

3.4. The AHP-Based Project Assessment

- Opinion data is written to Formula (3).

- The consistency ratio (11) is checked to fulfill the AHP method requirements (otherwise the opinion data must be re-evaluated).

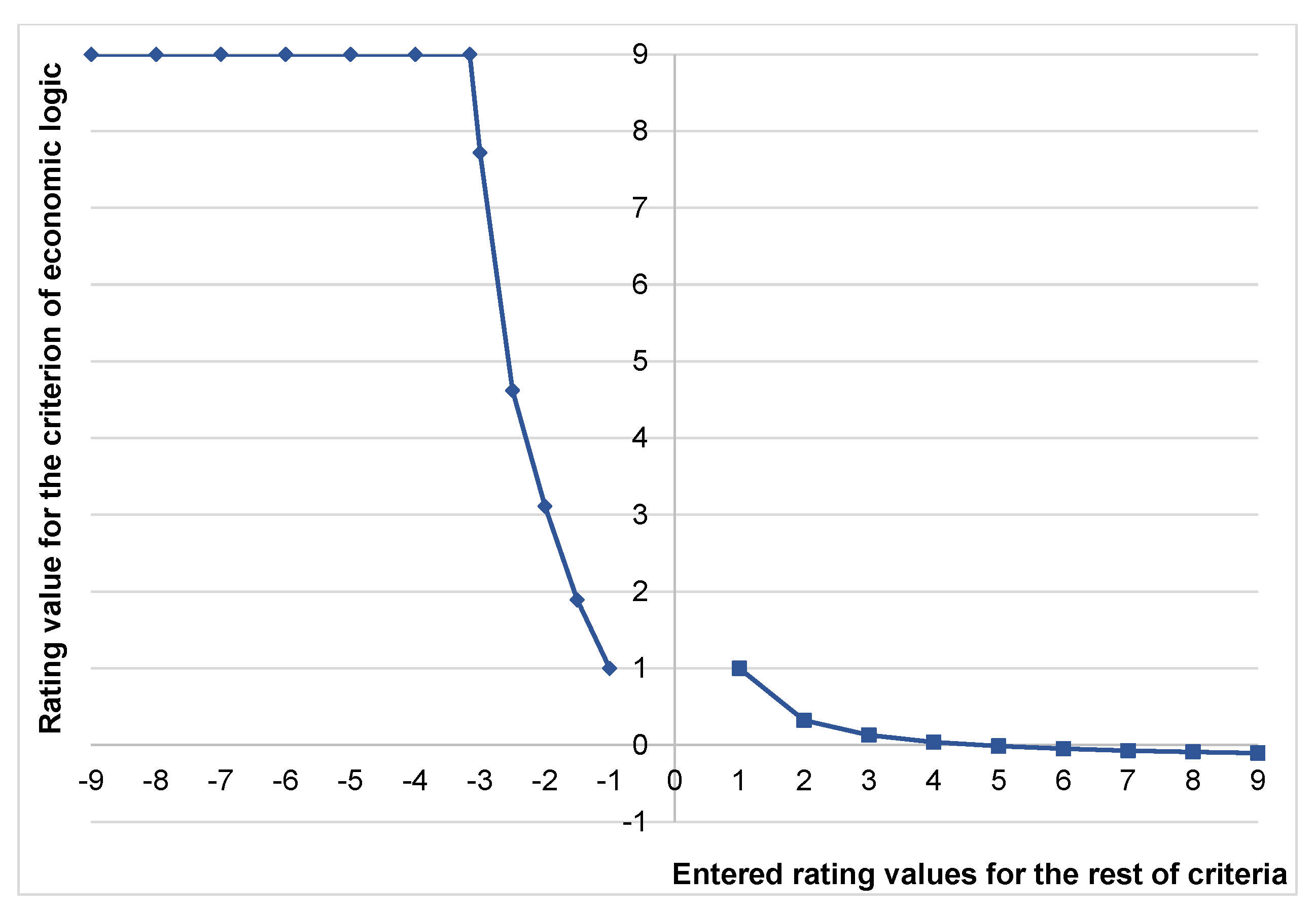

- The value representing the economic logic is calculated using Formula (14). Note that according to formula, this criterion expresses the remaining criteria.

- Depending on the case, the value is converted to a monetary value, e.g., using the scale and interpolation between scale values. See Section 4.4 for more details about the case which was studied in this research.

3.5. The Algorithms for a Solution

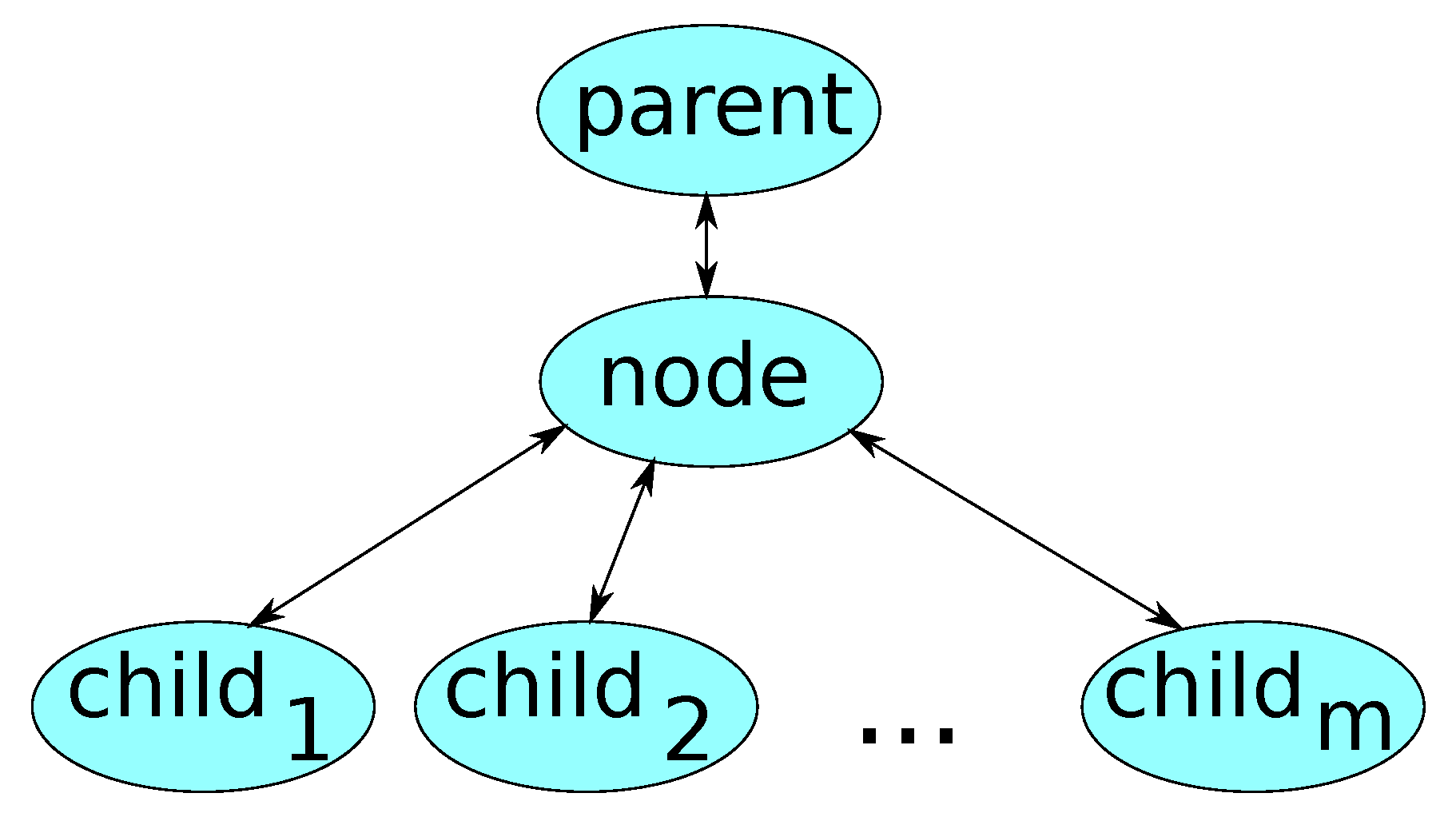

| Algorithm 1: Data structure |

| struct { int type; //type of the node float p; //probability for this node to be selected by a parentfloat price; //price of the event float time; //time before the event starts float ap; //probability of the additional cost and duration float aprice; //additional price float atime; //additional time float tariff; //additional price per day node* parent; //the pointer to parent node vector< node* > children; //list of children float priceTotal; //accumulated price float timeTotal; //accumulated time float value; //value of the expected profit of the node float extime; //expected time of the node string project; //reference to the project data } node; |

| Algorithm 2: The general calculation procedure |

| input: data output: Array of functions F tree = ReadTree(data); mappings = GenerateScales(data); for each scale p in mappings do ApplyAHP(tree, data, p); CalcPars(tree); CalcValues(tree); ; CollectProjectValues(tree, P); F.add(P); end |

| Algorithm 3: Sensitivity analysis procedure |

| Function ifthen P[] = ; end if then for each node t in do CollectProjectValues(t); end end end |

| Algorithm 4: The algorithm for the application of AHP to the tree |

| FunctionApplyAHP(,,p) ifthen evaluate v from AHP parameters from according to formula (14); evaluate by interpolating at the point v using mapping p; end if then for each node t in do ApplyAHP(t); end end end |

4. Case Study: The Modelling of Investor’s Behaviour

4.1. The Description of the Case

- The pool of possible construction solutions must be well-defined in order to define the leaves of the decision tree.

- The investor must have the leading developers role, i.e., he must initialise the project and lead the process of the project implementation. The involvement of additional stakeholders might change the role of the investor making some possible decisions in the tree obsolete, the decision strategy might become trivial from the investor’s point of view, and such modelling might become not useful.

4.2. The Application of the Proposed Approach to the Case Study

- Decision nodes which are represented by rectangle shapes.

- Chance nodes represented by circles.

- End nodes represented by triangles.

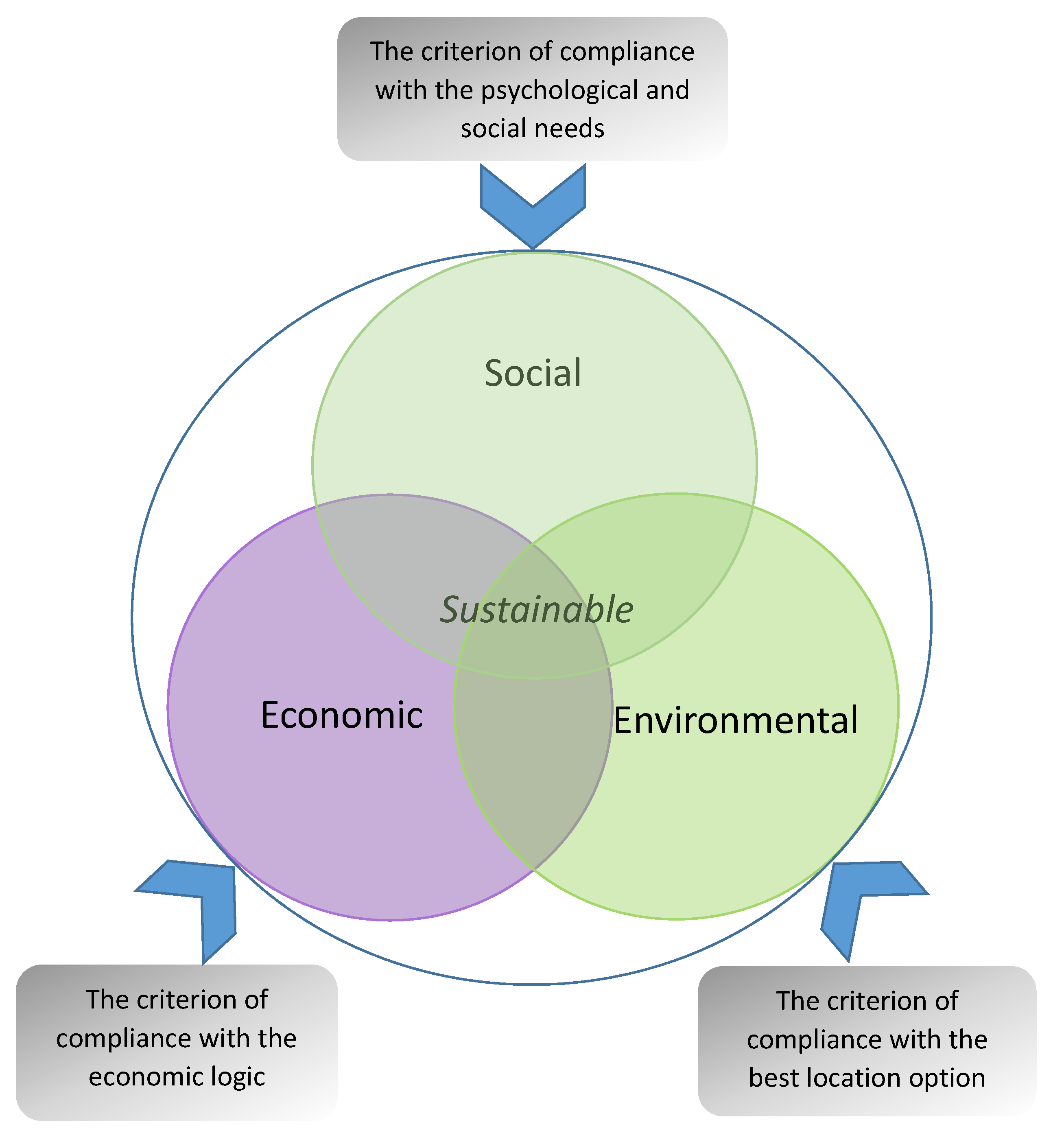

4.3. Criteria

- The criterion of compliance with the psychological and social needs (situation of neighborhood, habitual place, status, lifestyle, appearance, romanticism, and history).

- The criterion of compliance with the economic logic including an assessment of the object price.

- The criterion of compliance with the strategic (political) objectives including an assessment of the investor’s plans—whether the object will be rented, sold, or used for living.

- The criterion of compliance with the best location option—best location option including an assessment of the site quality, accessibility, and amenities of public and private service.

4.4. The Sensitivity Analysis

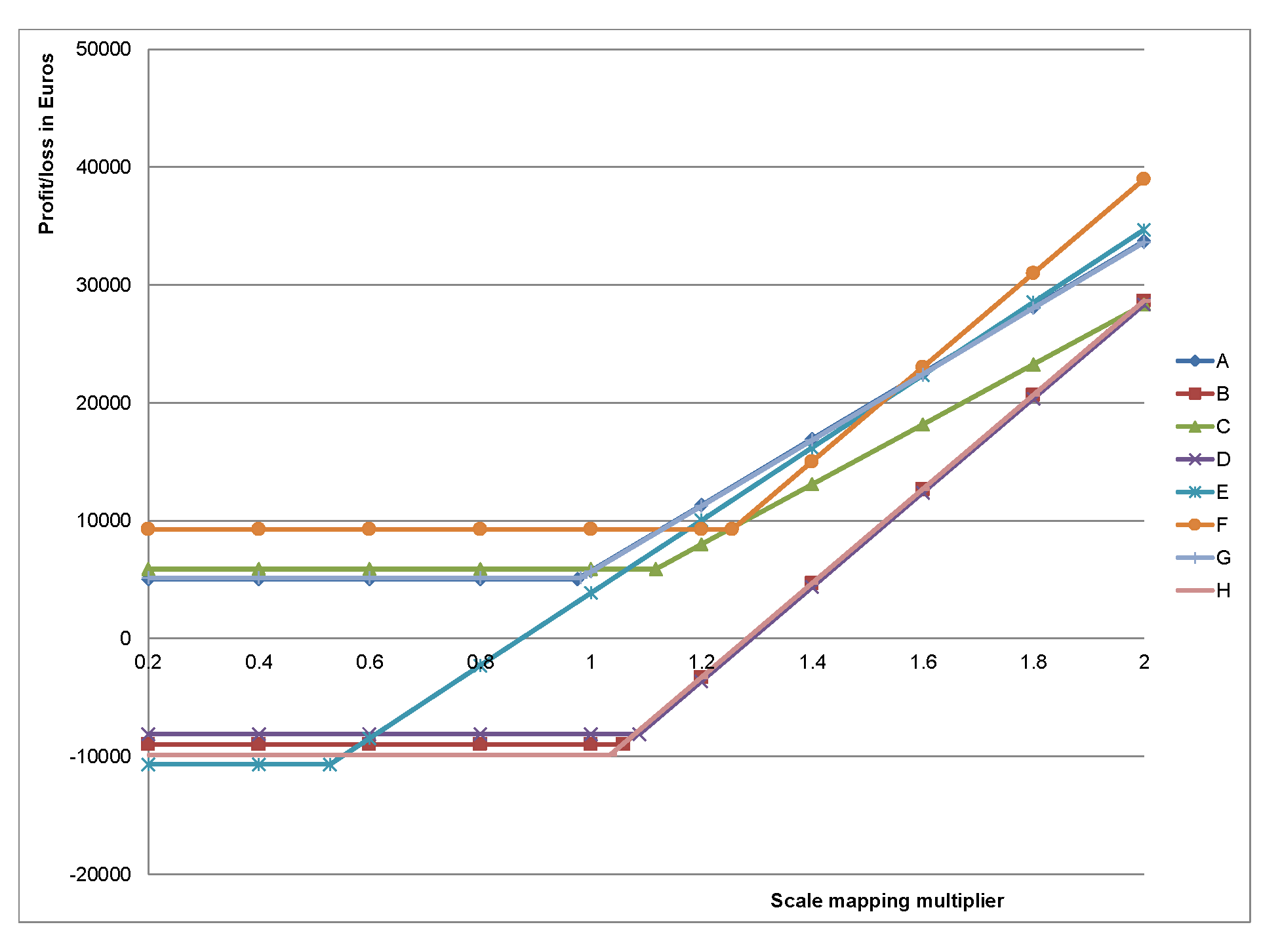

- Lower values of scale mapping mean a greater tendency to sell the project rather than not to.

- When choosing the project with lower values for sale, the project F is the best option.

- Higher mapping values mean the investor’s bigger tolerance to the higher costs, thus he tends not to sell the project.

- With values 1.2 and 1.4 the investor selects the medium-cost project, but does not sell it.

- As the scale multiplier raise, the investor chooses to invest in expensive project and not to sell it.

4.5. An Example of Case Assessment Made by Independent Expert

- The independent expert compares the criteria for weights determination (analogically to Table 4). All of the criteria are rated as equally important, i.e., by 1 point.

- Using AHP, the weights (Table 5) for criteria are calculated. The weights of the criteria in this case are the same and equal to 0.25.

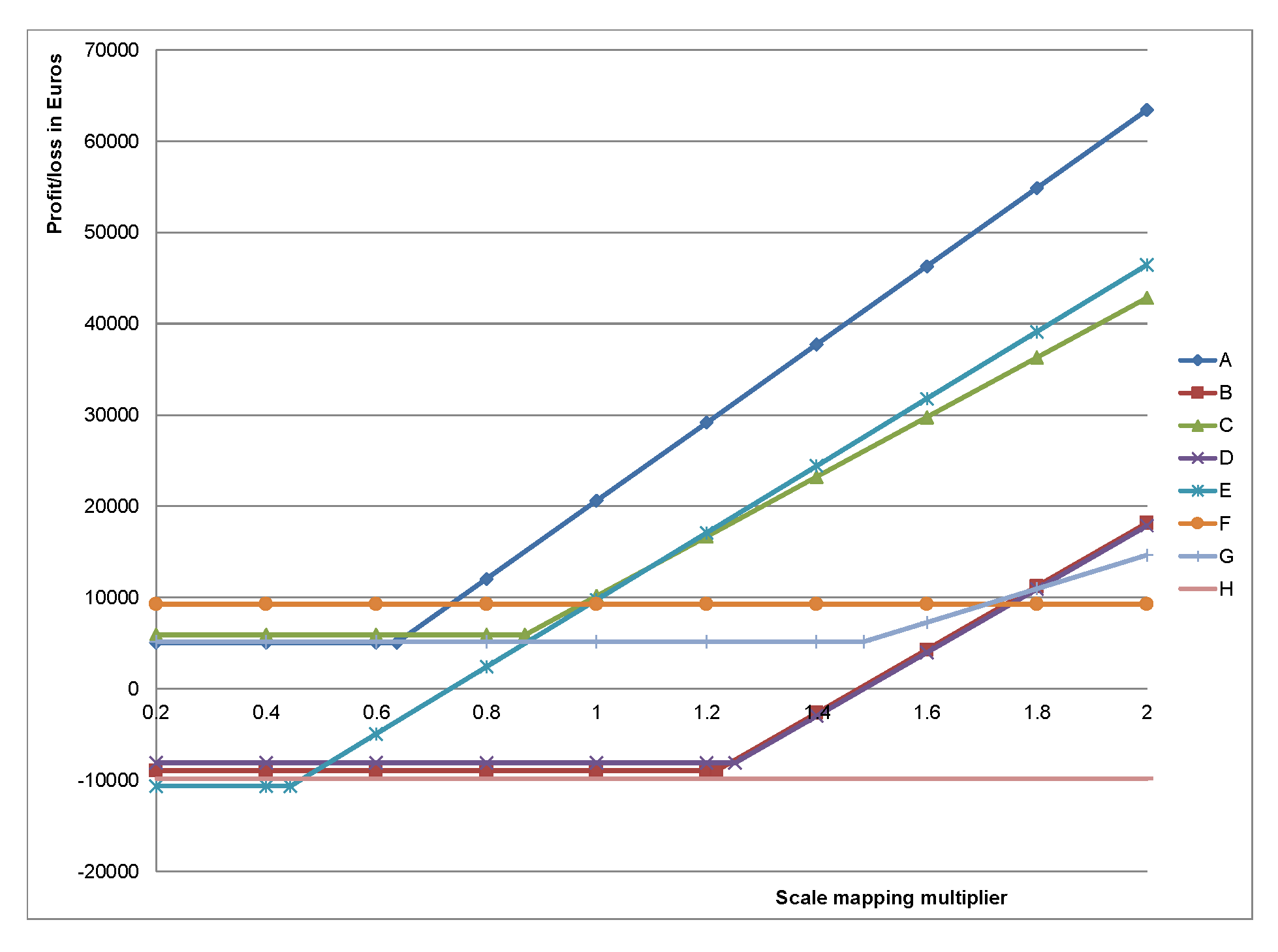

- The table, analogous to Table 7, is filled according to the new opinion. It is important to note, that every field in it can be evaluated individually, however, it can be simplified as it was done already—the interpolation can be applied to form the base mapping, and the multiplier can produce the rest of mappings. We interpolated between two values to create the base mapping; the results are provided in Table 10.

- Based on the achieved results, the new set of curves describing the dependency of profit/loss on the scale mappings are produced; the results are provided in Figure 7.

4.6. The Application of the Model to Other Cases

- The process being modelled must be described as a Markov process.

- All possible scenarios in different process states must be evaluated by the probabilities of their occurrence.

- The dependencies between states must form a tree, so, in some cases, some redundant information must be included (i.e., the structure of the tree branch is identical in both cases: either the consultant will be selected or not). However, there is an important feature—the model supports some process costs that occur as additional costs with some probabilities, it can be added directly without the duplication of some branches of a tree.

- The pool of projects must be formed with an appropriate assessment of each of them via AHP method.

- If one would like to an add additional parametrisation of the project, he should consider every set of parameters (e.g., some quality parameters) as a separate project entity and then add it as a leaf to the tree together with the needed branch.

- As was mentioned above, s wide variety of decisions can be added and the proposed algorithms are absolutely compatible with as many decision choices from the single state as needed, i.e., there is no requirement for the tree to be binary.

- The mappings of the scale to the monetary values are decisive for the outcome of the modelling. Thus, these mappings must be carefully thought of before the final sensitivity analysis.

5. Discussion

- including the possible changes of priorities, financial abilities, etc., into risk assessment routines; and,

- getting recommendations for selection of the consultants and supervisors, companies of building design, construction, and supply, also different roof installation projects.

- By investors to include the information into their risk assessment and obtain some recommendations.

- By building design or construction companies to improve their pool of potential projects.

- By government to model how possible restrictions might affect the priorities of investors.

- The representatives of interested community might be interested in predictable successful project implementation as a part of sustainable city development, so the lack of decision robustness might indicate an important information for these stakeholders.

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Issa, U.H.; Mosaad, S.A.; Hassan, M.S. Evaluation and selection of construction projects based on risk analysis. In Structures; Elsevier: Amsterdam, The Netherlands, 2020; Volume 27, pp. 361–370. [Google Scholar]

- Edjossan-Sossou, A.M.; Galvez, D.; Deck, O.; Al Heib, M.; Verdel, T.; Dupont, L.; Chery, O.; Camargo, M.; Morel, L. Sustainable risk management strategy selection using a fuzzy multi-criteria decision approach. Int. J. Disaster Risk Reduct. 2020, 45, 101474. [Google Scholar] [CrossRef]

- Kalra, N.; Hallegatte, S.; Lempert, R.; Brown, C.; Fozzard, A.; Gill, S.; Shah, A. Agreeing on Robust Decisions: New Processes for Decision Making under Deep Uncertainty; The World Bank: Washington, DC, USA, 2014. [Google Scholar]

- Bugajev, A.; Šostak, O. An algorithm for modelling the impact of the judicial conflict-resolution process on construction investment. Sustainability 2018, 10, 182. [Google Scholar] [CrossRef]

- Khan, A.S.; Pruncu, C.I.; Khan, R.; Naeem, K.; Ghaffar, A.; Ashraf, P.; Room, S. A Trade-Off Analysis of Economic and Environmental Aspects of a Disruption Based Closed-Loop Supply Chain Network. Sustainability 2020, 12, 7056. [Google Scholar] [CrossRef]

- Pedersen, S.; Gangås, K.E.; Chetri, M.; Andreassen, H.P. Economic Gain vs. Ecological Pain—Environmental Sustainability in Economies Based on Renewable Biological Resources. Sustainability 2020, 12, 3557. [Google Scholar] [CrossRef]

- Kamali, F.P.; Borges, J.A.; Meuwissen, M.P.; de Boer, I.J.; Lansink, A.G.O. Sustainability assessment of agricultural systems: The validity of expert opinion and robustness of a multi-criteria analysis. Agric. Syst. 2017, 157, 118–128. [Google Scholar] [CrossRef]

- Muñoz, B.; Romana, M.G.; Ordóñez, J. Sensitivity Analysis of Multicriteria Decision Making Methodology Developed for Selection of Typologies of Earth-retaining Walls in an Urban Highway. Transp. Res. Procedia 2016, 18, 135–139. [Google Scholar] [CrossRef]

- Hughes, W.; Murdoch, J.R. Roles in Construction Projects: Analysis and Terminology; Construction Industry Publications: Birmingham, UK, 2001. [Google Scholar]

- Chitkara, K. Construction Project Management; Tata McGraw-Hill Education: New York, NT, USA, 1998. [Google Scholar]

- Banaitiene, N.; Banaitis, A. Risk management in construction projects. Risk Management–Current Issues and Challenges. In Risk Management–Current Issues and Challenges; Banaitiene, N., Ed.; InTech: Rijeka, Croatia, 2012; pp. 429–448. [Google Scholar]

- Clough, R.H.; Sears, G.A.; Sears, S.K. Construction Project Management; John Wiley & Sons: Hoboken, NJ, USA, 2000. [Google Scholar]

- Phoya, S.; Pietrzyk, K. Holistic view on multi-stakeholders’ influence on health and safety risk management in construction projects in Tanzania. In Risk Management in Construction Projects; IntechOpen: London, UK, 2019. [Google Scholar]

- Alothaimeen, I.; Arditi, D. Overview of multi-objective optimization approaches in construction project management. In Multicriteria Optimization-Pareto-Optimality and Threshold-Optimality; IntechOpen: London, UK, 2019. [Google Scholar]

- Roberts, A. Code of Practice for Project Management for Construction and Development; John Wiley & Sons: Hoboken, NJ, USA, 2014. [Google Scholar]

- Al-Saggaf, A.; Nasir, H.; Hegazy, T. An Analytical Hierarchy Process-based system to evaluate the life-cycle performance of buildings at early design stage. J. Build. Eng. 2020, 31, 101364. [Google Scholar] [CrossRef]

- Maceika, A.; Bugajev, A.; Šostak, O.R. The Modelling of Roof Installation Projects Using Decision Trees and the AHP Method. Sustainability 2020, 12, 59. [Google Scholar] [CrossRef]

- Che, L. Investor types and stock return volatility. J. Empir. Financ. 2018, 47, 139–161. [Google Scholar] [CrossRef]

- da Silva, R.F.; Razzolini Filho, E. Sustainability in the Decision Making Process: A Systematic Review of Literature; Universities and Sustainable Communities: Meeting the Goals of the Agenda 2030; Springer: Berlin, Germany, 2020; pp. 291–305. [Google Scholar]

- Cabot, J.; Easterbrook, S.; Horkoff, J.; Lessard, L.; Liaskos, S.; Mazón, J.N. Integrating sustainability in decision-making processes: A modelling strategy. In Proceedings of the 2009 31st International Conference on Software Engineering-Companion Volume, Vancouver, BC, Canada, 16–24 May 2009; pp. 207–210. [Google Scholar]

- Cuadrado, J.; Zubizarreta, M.; Rojí, E.; García, H.; Larrauri, M. Sustainability-related decision making in industrial buildings: An AHP analysis. Math. Probl. Eng. 2015, 2015. [Google Scholar] [CrossRef]

- MacDonald, A.; Clarke, A.; Huang, L. Multi-stakeholder partnerships for sustainability: Designing decision-making processes for partnership capacity. J. Bus. Ethics 2019, 160, 409–426. [Google Scholar] [CrossRef]

- Beiragh, R.G.; Alizadeh, R.; Kaleibari, S.S.; Cavallaro, F.; Zolfani, S.H.; Bausys, R.; Mardani, A. An integrated multi-criteria decision making model for sustainability performance assessment for insurance companies. Sustainability 2020, 12, 789. [Google Scholar] [CrossRef]

- European Commission.The European Green Deal. Communication from the Commission to the European Parliament, the European Council, the Council, the European Economic and Social Committee, the Committee of the Regions and the European Investment Bank. 2019. Available online: https://ec.europa.eu/info/sites/info/files/european-green-deal-communication_en.pdf (accessed on 13 May 2021).

- Taha, F.F.; Hatem, W.A.; Jasim, N.A. Effectivity of BIM technology in using green energy strategies for construction projects. Asian J. Civ. Eng. 2020, 21, 995–1003. [Google Scholar] [CrossRef]

- European Commission. The 11th Sustainable Development Goal. 2015. Available online: https://ec.europa.eu/international-partnerships/sdg/sustainable-cities-and-communities_en (accessed on 13 May 2021).

- European Commission. Roadmap to a Resource Efficient Europe; European Commission: Brussels, Belgium, 2011. [Google Scholar]

- GPM, G. Insights into Sustainable Project Management. 2019. Available online: https://greenprojectmanagement.org/2019-insights-into-sustainable-project-management (accessed on 1 December 2020).

- Morioka, S.N.; Bolis, I.; Evans, S.; Carvalho, M.M. Transforming sustainability challenges into competitive advantage: Multiple case studies kaleidoscope converging into sustainable business models. J. Clean. Prod. 2017, 167, 723–738. [Google Scholar] [CrossRef]

- Rosa, P.; Sassanelli, C.; Terzi, S. Towards Circular Business Models: A systematic literature review on classification frameworks and archetypes. J. Clean. Prod. 2019, 236, 117696. [Google Scholar] [CrossRef]

- Bocken, N.M.; Short, S.W.; Rana, P.; Evans, S. A literature and practice review to develop sustainable business model archetypes. J. Clean. Prod. 2014, 65, 42–56. [Google Scholar] [CrossRef]

- Kudratova, S.; Huang, X.; Kudratov, K.; Qudratov, S. Corporate sustainability and stakeholder value trade-offs in project selection through optimization modeling: Application of investment banking. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 815–824. [Google Scholar] [CrossRef]

- Martens, M.L.; Carvalho, M.M. Key factors of sustainability in project management context: A survey exploring the project managers’ perspective. Int. J. Proj. Manag. 2017, 35, 1084–1102. [Google Scholar] [CrossRef]

- Aarseth, W.; Ahola, T.; Aaltonen, K.; ∅kland, A.; Andersen, B. Project sustainability strategies: A systematic literature review. Int. J. Proj. Manag. 2017, 35, 1071–1083. [Google Scholar] [CrossRef]

- Hatefi, S.M.; Tamošaitienė, J. Construction projects assessment based on the sustainable development criteria by an integrated fuzzy AHP and improved GRA model. Sustainability 2018, 10, 991. [Google Scholar] [CrossRef]

- French, N. Decision theory and real estate investment: An analysis of the decision-making processes of real estate investment fund managers. Manag. Decis. Econ. 2001, 22, 399–410. [Google Scholar] [CrossRef]

- Carbonara, S.; Stefano, D. An Operational Protocol for the Valorisation of Public Real Estate Assets in Italy. Sustainability 2020, 12, 732. [Google Scholar] [CrossRef]

- Dobrovolskienė, N.; Tamošiūnienė, R.; Banaitis, A.; Ferreira, F.A.; Banaitienė, N.; Taujanskaitė, K.; Meidutė-Kavaliauskienė, I. Developing a composite sustainability index for real estate projects using multiple criteria decision making. Oper. Res. 2019, 19, 617–635. [Google Scholar] [CrossRef]

- Mangialardo, A.; Micelli, E.; Saccani, F. Does Sustainability Affect Real Estate Market Values? Empirical Evidence from the Office Buildings Market in Milan (Italy). Sustainability 2019, 11, 12. [Google Scholar] [CrossRef]

- Shojaei, P.; Haeri, S.A.S. Development of supply chain risk management approaches for construction projects: A grounded theory approach. Comput. Ind. Eng. 2019, 128, 837–850. [Google Scholar] [CrossRef]

- Zavadskas, E.K.; Vilutienė, T.; Turskis, Z.; Šaparauskas, J. Multi-criteria analysis of Projects’ performance in construction. Arch. Civ. Mech. Eng. 2014, 14, 114–121. [Google Scholar] [CrossRef]

- Hatefi, S.M.; Tamošaitienė, J. An integrated fuzzy DEMATEL-fuzzy ANP model for evaluating construction projects by considering interrelationships among risk factors. J. Civ. Eng. Manag. 2019, 25, 114–131. [Google Scholar] [CrossRef]

- Singh, A.; Beg, I.; Kumar, S. Analytic Hierarchy Process for Hesitant Probabilistic Fuzzy Linguistic Set with Applications to Multi-criteria Group Decision-Making Method. Int. J. Fuzzy Syst. 2020, 22, 1596–1606. [Google Scholar] [CrossRef]

- Hatefi, S.M.; Basiri, M.E.; Tamošaitienė, J. An evidential model for environmental risk assessment in projects using dempster–shafer theory of evidence. Sustainability 2019, 11, 6329. [Google Scholar] [CrossRef]

- Ghasemi, F.; Sari, M.H.M.; Yousefi, V.; Falsafi, R.; Tamošaitienė, J. Project portfolio risk identification and analysis, considering project risk interactions and using Bayesian networks. Sustainability 2018, 10, 1609. [Google Scholar] [CrossRef]

- Asadi, P.; Zeidi, J.R.; Mojibi, T.; Yazdani-Chamzini, A.; Tamošaitienė, J. Project risk evaluation by using a new fuzzy model based on Elena guideline. J. Civ. Eng. Manag. 2018, 24, 284–300. [Google Scholar] [CrossRef]

- Chatterjee, K.; Zavadskas, E.K.; Tamošaitienė, J.; Adhikary, K.; Kar, S. A hybrid MCDM technique for risk management in construction projects. Symmetry 2018, 10, 46. [Google Scholar] [CrossRef]

- Benítez, J.; Carpitella, S.; Certa, A.; Izquierdo, J. Constrained consistency enforcement in AHP. Appl. Math. Comput. 2020, 380, 125273. [Google Scholar] [CrossRef]

- Mavi, R.K.; Standing, C. Critical success factors of sustainable project management in construction: A fuzzy DEMATEL-ANP approach. J. Clean. Prod. 2018, 194, 751–765. [Google Scholar] [CrossRef]

- Yunus, N. Dynamic Linkages Among US Real Estate Sectors Before and After the Housing Crisis. J. Real Estate Financ. Econ. 2019, 58, 264–289. [Google Scholar] [CrossRef]

- D’alpaos, C.; Canesi, R. Risks assessment in real estate investments in times of global crisis. WSEAS Trans. Bus. Econ. 2014, 11, 369–379. [Google Scholar]

- Agarwal, S.; He, J.; Sing, T.F.; Song, C. Do real estate agents have information advantages in housing markets? J. Financ. Econ. 2019, 134, 715–735. [Google Scholar] [CrossRef]

- Wang, C.; Wang, A.; Xu, J.; Wang, Q.; Zhou, F. Outsourced privacy-preserving decision tree classification service over encrypted data. J. Inf. Secur. Appl. 2020, 53, 102517. [Google Scholar]

- Mu, Y.; Liu, X.; Wang, L.; Zhou, J. A parallel fuzzy rule-base based decision tree in the framework of Map-Reduce. Pattern Recognit. 2020, 103, 107326. [Google Scholar] [CrossRef]

- Tian, Z.; Xiao, J.; Feng, H.; Wei, Y. Credit Risk Assessment based on Gradient Boosting Decision Tree. Procedia Comput. Sci. 2020, 174, 150–160. [Google Scholar] [CrossRef]

- Yan, J.; Zhang, Z.; Lin, K.; Yang, F.; Luo, X. A hybrid scheme-based one-vs-all decision trees for multi-class classification tasks. Knowl.-Based Syst. 2020, 198, 105922. [Google Scholar] [CrossRef]

- Barsacchi, M.; Bechini, A.; Marcelloni, F. An analysis of boosted ensembles of binary fuzzy decision trees. Expert Syst. Appl. 2020, 154, 113436. [Google Scholar] [CrossRef]

- Saaty, T.L. Fundamentals of Decision Making and Priority Theory with the Analytic Hierarchy Process; RWS Publications: Pittsburgh, PA, USA, 2000; Volume 6. [Google Scholar]

- Liu, Y.; Eckert, C.M.; Earl, C. A review of fuzzy AHP methods for decision-making with subjective judgements. Expert Syst. Appl. 2020, 113738. [Google Scholar] [CrossRef]

- Sangiorgio, V.; Uva, G.; Fatiguso, F. Optimized AHP to overcome limits in weight calculation: Building performance application. J. Constr. Eng. Manag. 2018, 144, 04017101. [Google Scholar] [CrossRef]

- Plebankiewicz, E.; Kubek, D. Multicriteria selection of the building material supplier using AHP and fuzzy AHP. J. Constr. Eng. Manag. 2016, 142, 04015057. [Google Scholar] [CrossRef]

- European Commission. Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions. EU Taxonomy, Corporate Sustainability Reporting, Sustainability Preferences and Fiduciary Duties: Directing Finance towards the European Green Deal. Brussels, 21.4.2021. COM(2021) 188 Final. 2021. Available online: https://ec.europa.eu/finance/docs/law/210421-sustainable-finance-communication_en.pdf (accessed on 1 April 2021).

- Migliorelli, M. What Do We Mean by Sustainable Finance? Assessing Existing Frameworks and Policy Risks. Sustainability 2021, 13, 975. [Google Scholar] [CrossRef]

- Huang, X. Optimal project selection with random fuzzy parameters. Int. J. Prod. Econ. 2007, 106, 513–522. [Google Scholar] [CrossRef]

- Puška, A.; Beganović, A.; Šadić, S. Model for investment decision making by applying the multi-criteria analysis method. Serb. J. Manag. 2018, 13, 7–28. [Google Scholar] [CrossRef]

- Lee, S.; Ahn, S.; Park, C.; Park, Y.J. Development of a resource allocation model using competitive advantage. Sustainability 2016, 8, 217. [Google Scholar] [CrossRef]

- Stojcetovic, B.; Nikolic, D.; Velinov, V.; Bogdanovic, D. Application of integrated strengths, weaknesses, opportunities, and threats and analytic hierarchy process methodology to renewable energy project selection in Serbia. J. Renew. Sustain. Energy 2016, 8, 035906. [Google Scholar] [CrossRef]

- Wang, W. The concept of sustainable construction project management in international practice. Environ. Dev. Sustain. 2021, 1–23. [Google Scholar] [CrossRef]

- European Commission. Proposal for a Directive Amending Directive 2013/34/EU, Directive 2004/109/EC, Directive 2006/43/EC and Regulation (EU) No 537/2014, as Regards Sustainable Corporate Reporting by Certain Undertakings, COM (2021) 189. 2021. Available online: https://ec.europa.eu/finance/docs/law/210421-proposal-corporate-sustainability-reporting_en.pdf (accessed on 1 April 2021).

- Duong, L.N.K.; Wang, J.X.; Wood, L.C.; Reiners, T.; Koushan, M. The value of incremental environmental sustainability innovation in the construction industry: An event study. Constr. Manag. Econ. 2021, 1–21. [Google Scholar] [CrossRef]

- Wojewnik-Filipkowska, A.; Węgrzyn, J. Understanding of Public–Private Partnership Stakeholders as a Condition of Sustainable Development. Sustainability 2019, 11, 1194. [Google Scholar] [CrossRef]

- Srinivasan, N.; Dhivya, S. An empirical study on stakeholder management in construction projects. Mater. Today Proc. 2020, 21, 60–62. [Google Scholar] [CrossRef]

- Demirkesen, S.; Ozorhon, B. Impact of integration management on construction project management performance. Int. J. Proj. Manag. 2017, 35, 1639–1654. [Google Scholar] [CrossRef]

- Li, H.X.; Patel, D.; Al-Hussein, M.; Yu, H.; Gül, M. Stakeholder studies and the social networks of NetZero energy homes (NZEHs). Sustain. Cities Soc. 2018, 38, 9–17. [Google Scholar] [CrossRef]

- Zhao, Z.Y.; Zhao, X.J.; Davidson, K.; Zuo, J. A corporate social responsibility indicator system for construction enterprises. J. Clean. Prod. 2012, 29, 277–289. [Google Scholar] [CrossRef]

- Freudenreich, B.; Lüdeke-Freund, F.; Schaltegger, S. A stakeholder theory perspective on business models: Value creation for sustainability. J. Bus. Ethics 2020, 166, 3–18. [Google Scholar] [CrossRef]

- Chu, X.; Shi, Z.; Yang, L.; Guo, S. Evolutionary Game Analysis on Improving Collaboration in Sustainable Urban Regeneration: A Multiple-Stakeholder Perspective. J. Urban Plan. Dev. 2020, 146, 04020046. [Google Scholar] [CrossRef]

- Vilutiene, T.; Ignatavičius, Č. Towards sustainable renovation: Key performance indicators for quality monitoring. Sustainability 2018, 10, 1840. [Google Scholar] [CrossRef]

- Zheng, X.; Lu, Y.; Li, Y.; Le, Y.; Xiao, J. Quantifying and visualizing value exchanges in building information modeling (BIM) projects. Autom. Constr. 2019, 99, 91–108. [Google Scholar] [CrossRef]

- Lin, X.; McKenna, B.; Ho, C.M.; Shen, G.Q. Stakeholders’ influence strategies on social responsibility implementation in construction projects. J. Clean. Prod. 2019, 235, 348–358. [Google Scholar] [CrossRef]

- Stackpole, C.S. A User’s Manual to the PMBOK Guide; John Wiley & Sons: Hoboken, NJ, USA, 2013. [Google Scholar]

- Zhang, Z.; Liao, H.; Al-Barakati, A.; Zavadskas, E.K.; Antuchevičienė, J. Supplier selection for housing development by an integrated method with interval rough boundaries. Int. J. Strateg. Prop. Manag. 2020, 24, 269–284. [Google Scholar] [CrossRef]

- Khalil, N.; Kamaruzzaman, S.N.; Baharum, M.R. Ranking the indicators of building performance and the users’ risk via Analytical Hierarchy Process (AHP): Case of Malaysia. Ecol. Indic. 2016, 71, 567–576. [Google Scholar] [CrossRef]

- Kamaruzzaman, S.N.; Lou, E.C.W.; Wong, P.F.; Wood, R.; Che-Ani, A.I. Developing weighting system for refurbishment building assessment scheme in Malaysia through analytic hierarchy process (AHP) approach. Energy Policy 2018, 112, 280–290. [Google Scholar] [CrossRef]

- Portal, O.S. Building Construction. 2019. Available online: https://osp.stat.gov.lt/informaciniai-pranesimai?articleId=6908417 (accessed on 13 May 2021).

- Antunes, R.; Gonzalez, V. A production model for construction: A theoretical framework. Buildings 2015, 5, 209–228. [Google Scholar] [CrossRef]

- Farokhad, M.R.; Otegi-Olaso, J.R.; Pinilla, L.S.; Gandarias, N.T.; de Lacalle, L.N.L. Assessing the success of R&D projects and innovation projects through project management life cycle. In Proceedings of the 2019 10th IEEE International Conference on Intelligent Data Acquisition and Advanced Computing Systems: Technology and Applications (IDAACS), Metz, France, 18–21 September 2019; Volume 2, pp. 1104–1110. [Google Scholar]

- Vilutiene, T.; Kumetaitis, G.; Kiaulakis, A.; Kalibatas, D. Assessing the Sustainability of Alternative Structural Solutions of a Building: A Case Study. Buildings 2020, 10, 36. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Sources | Researched Groups of Stakeholders | Content of the Research |

|---|---|---|

| Li et al. (2018) [74] | Buyers, sales personnel, financial institutions, developers, designers and drafting personnel, estimators, project managers/coordinators, regulators, superintendents, inspectors, trades/suppliers, home occupants and warranty staff | Stakeholder’s studies and the social networks of NetZero energy homes |

| Zhao et al. (2012) [75] | Employees, customers, shareholders, creditors, suppliers and partners, environment and resources agencies, local communities, government, competitors and non-governmental organisations | A corporate social responsibility indicator system for construction enterprises |

| Freudenreich et al. (2020) [76] | Social stakeholders, financial stakeholders, customers, business partners and employees | Value creation for sustainability |

| Chu et al. (2020) [77] | Government, developers and residents | Evolutionary game analysis on improving collaboration in sustainable urban regeneration |

| Vilutiene and Ignatavičius (2018) [78] | Finance institutions, local authorities, building owners, tenants, contractors, technology providers, material suppliers, consultants and facility managers | Key performance indicators for quality monitoring during sustainable renovation |

| Zheng et al. (2019) [79] | Governments, cost consultants, owners, building information modelling consultants, designers, general contractors and subcontractors | Quantifying and visualising value exchanges in building information modelling projects |

| Lin et al. (2019) [80] | Internal stakeholders (end users, developers and investors, main contractors, subcontractors, suppliers and employees) and external stakeholders (governments, non-governmental organizations, communities and the public) | Stakeholders’ influence strategies on social responsibility implementation in construction projects |

| Maceika et al. (2020) [17] | Project owner, state organisations, building design company, interested community, construction company, suppliers, construction business partners, consultants and supervisors | The modelling of roof installation projects using decision trees and the AHP method |

| Rating | Definition | Explanation |

|---|---|---|

| 9 | Extreme importance of the first element | The evidence favouring the first element over the second is of highest possible order of affirmation |

| 8 | Very, very strong importance of the first element | Intermediate value between two adjacent judgments when a compromise exists |

| 7 | Very strong or demonstrated importance of the first element | The first element is strongly favoured and its dominance is demonstrated in practice |

| 6 | Strong plus importance of the first element | Intermediate value between two adjacent judgments when a compromise exists |

| 5 | Strong importance of the first element | Experience and judgement strongly favour the first element over the second |

| 4 | Moderate plus importance of the first element | Intermediate value between two adjacent judgments when a compromise exists |

| 3 | Moderate importance of the first element | Experience and judgement favour a little more the first element over the second |

| 2 | Weak importance of the first element | Intermediate value between two adjacent judgments when a compromise exists |

| 1 and −1 | Equal importance of the elements | Both elements contribute equally to the objective |

| −2 | Weak importance of the second element | Intermediate value between two adjacent judgments when a compromise exists |

| −3 | Moderate importance of the second element | Experience and judgement favour a little more the second element over the first |

| −4 | Moderate plus importance of the second element | Intermediate value between two adjacent judgments when a compromise exists |

| −5 | Strong importance of the second element | Experience and judgement strongly favour the second element over the first |

| −6 | Strong plus importance of the second element | Intermediate value between two adjacent judgments when a compromise exists |

| −7 | Very strong or demonstrated importance of the second element | The second element is strongly favoured and its dominance is demonstrated in practice |

| −8 | Very, very strong importance of the second element | Intermediate value between two adjacent judgments when a compromise exists |

| −9 | Extreme importance of the second element | The evidence for favouring the second element over the first is of the highest possible order of affirmation |

| The Order | Description of the Investor’s Decisions |

|---|---|

| 1 | Decision whether to implement the project |

| 2 | Decision whether to hire the consultants and supervisor |

| 3 | Decisions whether to select the building design company “A” or “B” |

| for the branches of the decision tree with or without consulting | |

| 4 | Decisions whether to select the medium-cost project from a set of projects |

| “A”, “C”, “E”, “G” or expensive project from a set of projects “B”, “D”, “F”, “H” | |

| 5 | Decisions whether to select the construction company “AA” or “AB” for the project “A”; |

| “BA” or “BB” for the project “B”; “CA” or “CB” for the project “C”; | |

| “DA” or “DB” for the project “D”; “EA” or “EB” for the project “E”; | |

| “FA” or “FB” for the project “F”; “GA” or “GB” for the project “G”; | |

| “HA” or “HB” for the project “H” | |

| 6 | Decisions whether to select the supply company “AAS” or “ABS” for construction company “AA”; |

| “AAS” or “ABS” for construction company “AB”; “BAS” or “BBS” for construction company “BA”; | |

| “BAS” or “BBS” for construction company “BB”; “CAS” or “CBS” for construction company “CA”; | |

| “CAS” or “CBS” for construction company “CB”; “DAS” or “DBS” for construction company “DA”; | |

| “DAS” or “DBS” for construction company “DB”; “EAS” or “EBS” for construction company “EA”; | |

| “EAS” or “EBS” for construction company “EB”; “FAS” or “FBS” for construction company “FA”; | |

| “FAS” or “FBS” for construction company “FB”; “GAS” or “GBS” for construction company “GA”; | |

| “GAS” or “GBS” for construction company “GB”; “HAS” or “HBS” for construction company “HA”; | |

| “HAS” or “HBS” for construction company “HB” | |

| 7 | Decisions whether to sell the object of the project, |

| based on the results of applying the AHP method |

| Criteria for Comparison | Importance and Intensity |

|---|---|

| Compliance with the psychological and social needs | −3 |

| vs. Compliance with economic logic | |

| Compliance with the psychological and social needs | −3 |

| vs. Compliance with strategic objectives | |

| Compliance with the psychological and social needs | 2 |

| vs. Compliance with best location option | |

| Compliance with economic logic | −1 |

| vs. Compliance with strategic objectives | |

| Compliance with economic logic | 5 |

| vs. Compliance with best location option | |

| Compliance with strategic objectives | 5 |

| vs. Compliance with best location option |

| Criteria | Compliance with the Psychological and Social Needs | Compliance with Economic Logic | Compliance with Strategic Objectives | Compliance with Best Location Option |

|---|---|---|---|---|

| Weights | 0.1376 | 0.3935 | 0.3935 | 0.0754 |

| Criteria | Values of Projects Criteria | |||||||

|---|---|---|---|---|---|---|---|---|

| A | B | C | D | E | F | G | H | |

| Compliance with the psychological and social needs | −3 | −9 | −3 | −9 | −3 | −9 | −3 | −9 |

| Compliance with strategic objectives | −2 | −5 | −1 | −4 | −3 | −6 | −2 | -5 |

| Compliance with best location option | 2 | 2 | 2 | 2 | 2 | 2 | 2 | 2 |

| Compliance with economic logic, points from AHP when both alternatives are equal | 2.6 | 9 | 1.25 | 9 | 4.14 | 9 | 2.6 | 9 |

| Scale | Multiplier of the Scale Mapping and the Corresponding Monetary Values in Euros | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 0.2 | 0.4 | 0.6 | 0.8 | 1 | 1.2 | 1.4 | 1.6 | 1.8 | 2 | |

| 9 | 8000 | 16,000 | 24,000 | 32,000 | 40,000 | 48,000 | 56,000 | 64,000 | 72,000 | 80,000 |

| 8 | 7625 | 15,250 | 22,875 | 30,500 | 38,125 | 45,750 | 53,375 | 61,000 | 68,625 | 76,250 |

| 7 | 7250 | 14,500 | 21,750 | 29,000 | 36,250 | 43,500 | 50,750 | 58,000 | 65,250 | 72,500 |

| 6 | 6875 | 13,750 | 20,625 | 27,500 | 34,375 | 41,250 | 48,125 | 55,000 | 61,875 | 68,750 |

| 5 | 6500 | 13,000 | 19,500 | 26,000 | 32,500 | 39,000 | 45,500 | 52,000 | 58,500 | 65,000 |

| 4 | 6125 | 12,250 | 18,375 | 24,500 | 30,625 | 36,750 | 42,875 | 49,000 | 55,125 | 61,250 |

| 3 | 5750 | 11,500 | 17,250 | 23,000 | 28,750 | 34,500 | 40,250 | 46,000 | 51,750 | 57,500 |

| 2 | 5375 | 10,750 | 16,125 | 21,500 | 26,875 | 32,250 | 37,625 | 43,000 | 48,375 | 53,750 |

| 1 | 5000 | 10,000 | 15,000 | 20,000 | 25,000 | 30,000 | 35,000 | 40,000 | 45,000 | 50,000 |

| −1 | 5000 | 10,000 | 15,000 | 20,000 | 25,000 | 30,000 | 35,000 | 40,000 | 45,000 | 50,000 |

| −2 | 4625 | 9250 | 13,875 | 18,500 | 23,125 | 27,750 | 32,375 | 37,000 | 41,625 | 46,250 |

| −3 | 4250 | 8500 | 12,750 | 17,000 | 21,250 | 25,500 | 29,750 | 34,000 | 38,250 | 42,500 |

| −4 | 3875 | 7750 | 11,625 | 15,500 | 19,375 | 23,250 | 27,125 | 31,000 | 34,875 | 38,750 |

| −5 | 3500 | 7000 | 10,500 | 14,000 | 17,500 | 21,000 | 24,500 | 28,000 | 31,500 | 35,000 |

| −6 | 3125 | 6250 | 9375 | 12,500 | 15,625 | 18,750 | 21,875 | 25,000 | 28,125 | 31,250 |

| −7 | 2750 | 5500 | 8250 | 11,000 | 13,750 | 16,500 | 19,250 | 22,000 | 24,750 | 27,500 |

| −8 | 2375 | 4750 | 7125 | 9500 | 11,875 | 14,250 | 16,625 | 19,000 | 21,375 | 23,750 |

| −9 | 2000 | 4000 | 6000 | 8000 | 10,000 | 12,000 | 14,000 | 16,000 | 18,000 | 20,000 |

| Criteria | Projects | |||||||

|---|---|---|---|---|---|---|---|---|

| A | B | C | D | E | F | G | H | |

| Market price for sale (b) | 27,313 | 42,341 | 28,468 | 43,501 | 16,326 | 80,231 | 27,486 | 41,401 |

| Criteria | Values of the Projects Criteria | |||||||

|---|---|---|---|---|---|---|---|---|

| A | B | C | D | E | F | G | H | |

| Compliance with psychological and social needs | −2 | 1 | 1 | 1 | 2 | 5 | 3 | 7 |

| Compliance with strategic objectives | 1 | 2 | 2 | 2 | −2 | 5 | 2 | 3 |

| Compliance with best location option | −2 | −2 | 1 | −2 | −2 | 5 | 1 | 3 |

| Compliance with economic logic, points from AHP when both alternatives are equal | 5 | 1 | −2 | 1 | 2 | −9 | −9 | −9 |

| Scale | Multiplier of the Scale Mapping and the Corresponding Monetary Values in Euros | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 0.2 | 0.4 | 0.6 | 0.8 | 1 | 1.2 | 1.4 | 1.6 | 1.8 | 2 | |

| 9 | 10,200 | 20,400 | 30,600 | 40,800 | 51,000 | 61,200 | 71,400 | 81,600 | 91,800 | 102,000 |

| 8 | 9793.75 | 19,587.5 | 29,381.25 | 39,175 | 48,968.75 | 58,762.5 | 68,556.25 | 78,350 | 88,143.75 | 97,937.5 |

| 7 | 9387.5 | 18,775 | 28,162.5 | 37,550 | 46,937.5 | 56,325 | 65,712.5 | 75,100 | 84,487.5 | 93,875 |

| 6 | 8981.25 | 17,962.5 | 26,943.75 | 35,925 | 44,906.25 | 53,887.5 | 62,868.75 | 71,850 | 80,831.25 | 89,812.5 |

| 5 | 8575 | 17,150 | 25,725 | 34,300 | 42,875 | 51,450 | 60,025 | 68,600 | 77,175 | 85,750 |

| 4 | 8168.75 | 16,337.5 | 24,506.25 | 32,675 | 40,843.75 | 49,12.5 | 57,181.25 | 65,350 | 73,518.75 | 81,687.5 |

| 3 | 7762.5 | 15,525 | 23,287.5 | 31,050 | 38,812.5 | 46,575 | 54,337.5 | 62,100 | 69,862.5 | 77,625 |

| 2 | 7356.25 | 14,712.5 | 22,068.75 | 29,425 | 36,781.25 | 44,137.5 | 51,493.75 | 58,850 | 66,206.25 | 73,562.5 |

| 1 | 6950 | 13,900 | 20,850 | 27,800 | 34,750 | 41,700 | 48,650 | 55,600 | 62,550 | 69,500 |

| −1 | 6950 | 13,900 | 20,850 | 27,800 | 34,750 | 41,700 | 48,650 | 55,600 | 62,550 | 69,500 |

| −2 | 6543.75 | 13,087.5 | 19,631.25 | 26,175 | 32,718.75 | 39,262.5 | 45,806.25 | 52,350 | 58,893.75 | 65,437.5 |

| −3 | 6137.5 | 12,275 | 18,412.5 | 24,550 | 30,687.5 | 36,825 | 42,962.5 | 49,100 | 55,237.5 | 61,375 |

| −4 | 5731.25 | 11,462.5 | 17,193.75 | 22,925 | 28,656.25 | 34,387.5 | 40,118.75 | 45,850 | 51,581.25 | 57,312.5 |

| −5 | 5325 | 10,650 | 15,975 | 21,300 | 26,625 | 31,950 | 37,275 | 42,600 | 47,925 | 53,250 |

| −6 | 4918.75 | 9837.5 | 14,756.25 | 19,675 | 24,593.75 | 29,512.5 | 34,431.25 | 39,350 | 44,268.75 | 49,187.5 |

| −7 | 4512.5 | 9025 | 13,537.5 | 18,050 | 22,562.5 | 27,075 | 31,587.5 | 36,100 | 40,612.5 | 45,125 |

| −8 | 4106.25 | 8212.5 | 12,318.75 | 16,425 | 20,531.25 | 24,637.5 | 28,743.75 | 32,850 | 36,956.25 | 41,062.5 |

| −9 | 3700 | 7400 | 11,100 | 14,800 | 18,500 | 22,200 | 25,900 | 29,600 | 33,300 | 37,000 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Maceika, A.; Bugajev, A.; Šostak, O.R.; Vilutienė, T. Decision Tree and AHP Methods Application for Projects Assessment: A Case Study. Sustainability 2021, 13, 5502. https://doi.org/10.3390/su13105502

Maceika A, Bugajev A, Šostak OR, Vilutienė T. Decision Tree and AHP Methods Application for Projects Assessment: A Case Study. Sustainability. 2021; 13(10):5502. https://doi.org/10.3390/su13105502

Chicago/Turabian StyleMaceika, Augustinas, Andrej Bugajev, Olga Regina Šostak, and Tatjana Vilutienė. 2021. "Decision Tree and AHP Methods Application for Projects Assessment: A Case Study" Sustainability 13, no. 10: 5502. https://doi.org/10.3390/su13105502

APA StyleMaceika, A., Bugajev, A., Šostak, O. R., & Vilutienė, T. (2021). Decision Tree and AHP Methods Application for Projects Assessment: A Case Study. Sustainability, 13(10), 5502. https://doi.org/10.3390/su13105502