Empirical Evaluation of the Impact of Resilience and Sustainability on Firms’ Performance

Abstract

1. Introduction

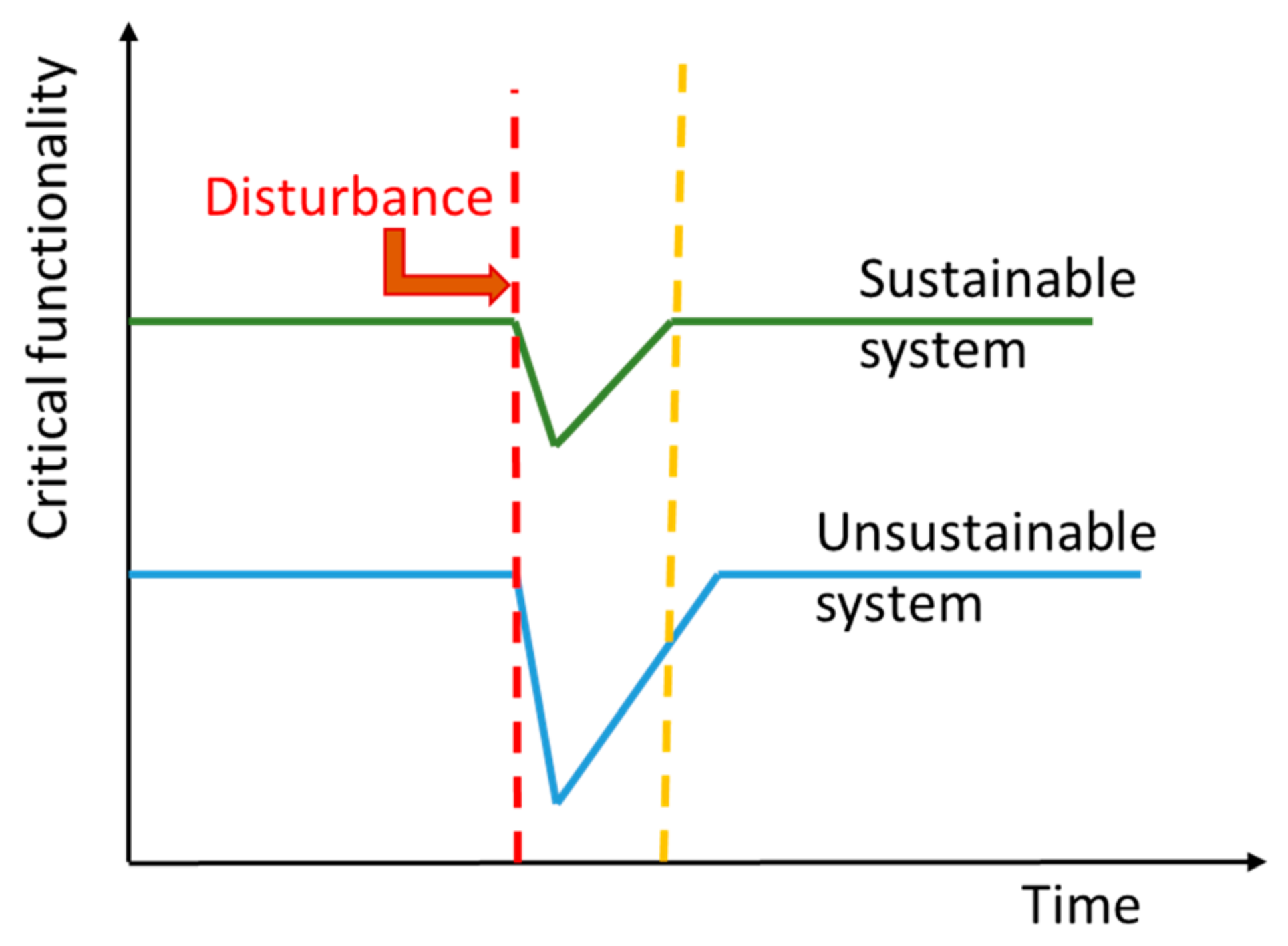

2. Resilience, Sustainability, and Firms’ Performance Relationship: An Overview

3. Methodology

3.1. Operations Sustainability Maturity Model and SMI Definition

- Corporate sustainability (CS). Reflecting the extent of the economic, social and environmental value being created from the optimal use of resources, the responsibility upheld towards the community’s well-being and the conservation efforts from responsible decision-making.

- Economic capital (EC). An illustration of the organization’s efforts in instigating value-creating strategies, resource optimization and creating value-adding activities.

- Societal capital (SC). An accumulation of the corporation’s public networks and social relations in the community in which it operates. It can be acquired through the corporation’s efforts to address societal concerns and the maximizing of social benefits to the community.

- Human capital (HC). An accumulation of knowledgeable, skillful, and competent individuals in the corporation. Human capital can be acquired through the corporation’s efforts to encourage internal and external learning, and the building of internal loyalty.

- Natural capital (NC). An illustration of its conservation efforts aimed to reduce environmental impacts and initiation of responsible decision-making to promote or maintain the well-being of the planet.

3.2. Questionnaire Design

3.3. Interview Structure

3.4. OSMM as a Resilience Driver

3.5. Statistical Analysis

- Principal component analysis (PCA).

- Simple linear regression.

- Simple robust linear regression.

- Simple linear regression’s Cook’s distance.

- Simple linear regression’s t-test.

- Simple robust linear regression’s t-test.

4. Results

4.1. Data Structure

- SIC classification.

- Country.

- Employees.

- Operating income.

- Net margin.

- EBT.

- Return on assets.

- Return on equity.

4.2. Sustainability Indices PCA

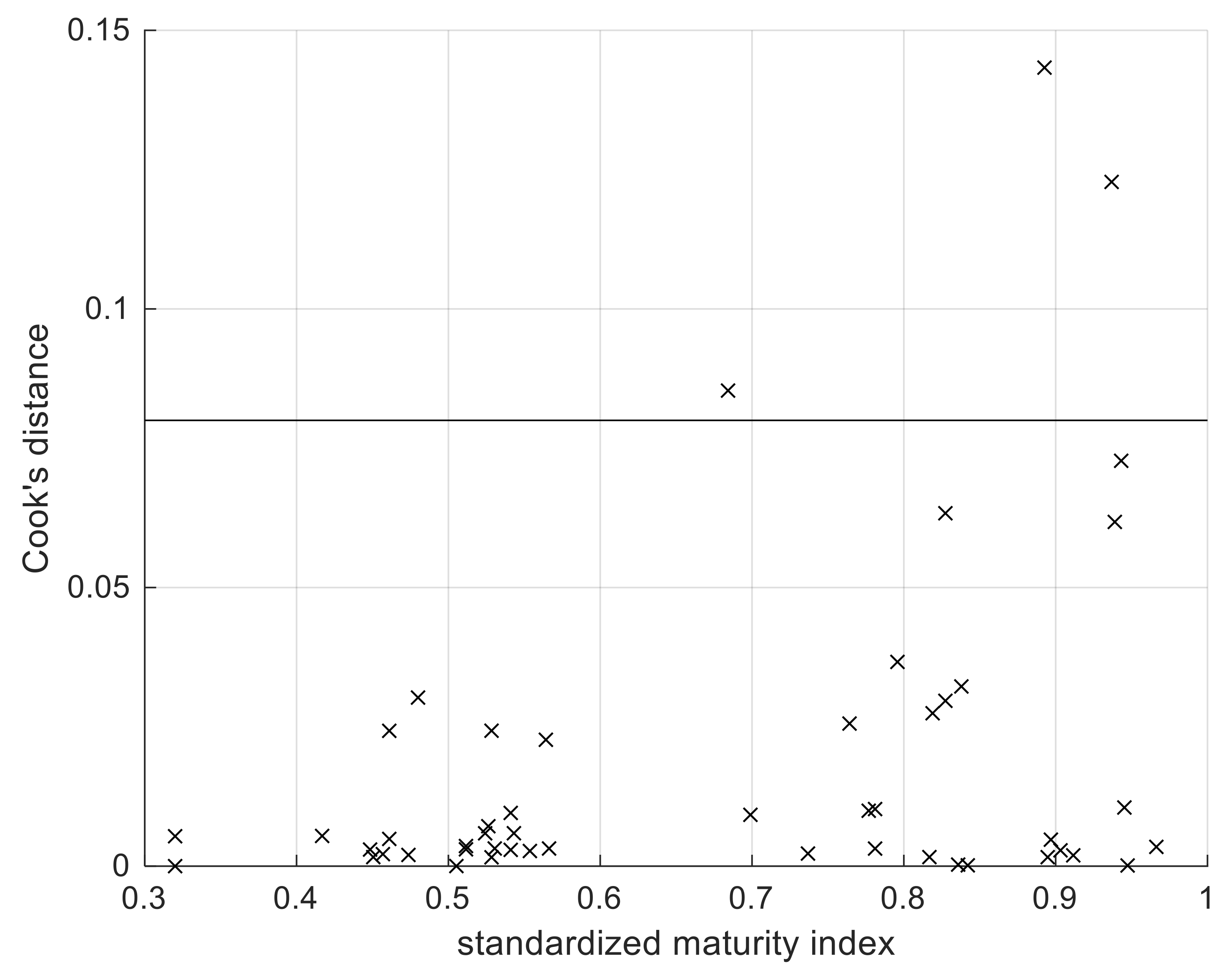

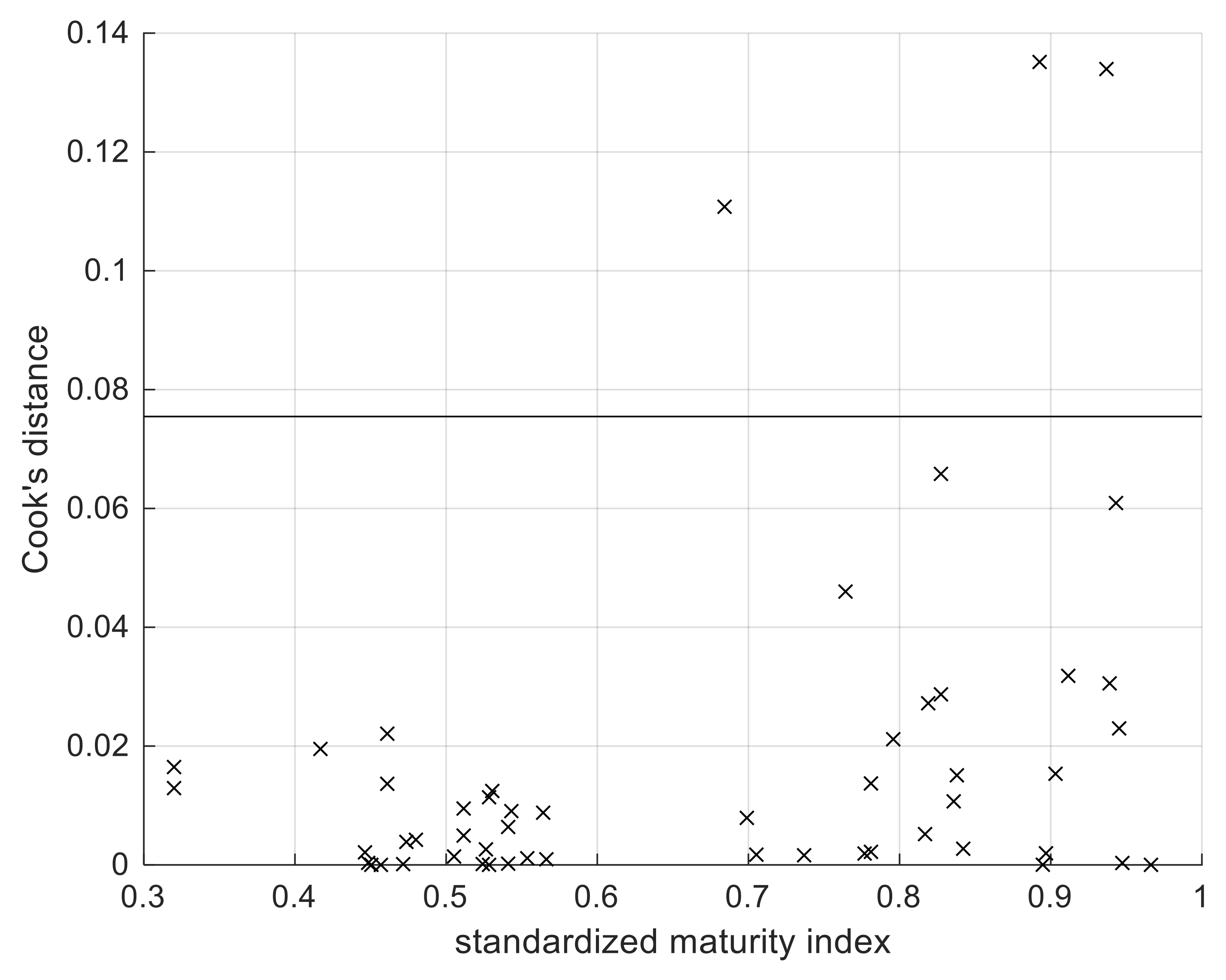

4.3. Outlier Analysis

4.4. Regression

- Simple linear regressions on the original database.

- Simple linear regressions of the database without the influential points.

- Simple robust linear regression on the original database.

5. Discussion

- 1.

- Improved brand image.

- 2.

- Employees’ satisfaction, morale and retention.

- 3.

- Product, service and market innovation.

- 4.

- Business process and model innovation.

- 5.

- Effective risk management.

- 6.

- Enhanced stakeholder relations.

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Co. No. | Company SIC Code | Country 1 | Employees (No.) | Operating Income (AUS $) | Net Margin (%) | EBT (%) | ROA (%) | ROE (%) |

|---|---|---|---|---|---|---|---|---|

| 1 | 6162 | AUS | 41,849 | 7955 | 23.30 | 33.37 | 0.67 | 12.87 |

| 2 | 6162 | GBR | 24,600 | 2443 | 23.80 | 35.41 | 0.52 | 11.66 |

| 3 | 6162 | GBR | 264,000 | 29,706 | 22.60 | 25.04 | 0.52 | 7.35 |

| 4 | 6311 | AUS | 963 | 220 | 11.70 | 17.28 | 8.97 | 12.79 |

| 5 | 6282 | AUS | 1200 | 443 | 32.21 | 35.03 | 9.58 | 18.92 |

| 6 | 6035 | AUS | 503 | 350 | 7.86 | 43.04 | 2.11 | 4.99 |

| 7 | 6311 | AUS | 1600 | 173 | 20.50 | 34.63 | 6.44 | 15.45 |

| 8 | 6321 | AUS | 47 | 38 | 20.06 | 29.73 | 3.95 | 3.97 |

| 9 | 6189 | AUS | 54 | 16 | 26.00 | 23.00 | 9.45 | 15.75 |

| 10 | 6022 | JAM | 2600 | 524.00 | 20.00 | 26.78 | 2.40 | 14.45 |

| 11 | 6162 | JAM | 1600 | 32. | 21.67 | 20.48 | 1.51 | 2.76 |

| 12 | 2711 | JAM | 600 | −2.71 | −7.30 | −7.30 | −16.80 | −32.80 |

| 13 | 2000 | JAM | 1940 | 58.67 | 5.10 | 6.90 | 3.90 | 10.00 |

| 14 | 2080 | JAM | 340 | 29.37 | 18.00 | 23.00 | 22.00 | 24.00 |

| 15 | 2851 | JAM | 126 | 1.41 | 6.00 | 7.00 | 12.00 | 20.00 |

| 16 | 2033 | JAM | 60 | 9.83 | 7.00 | 8.00 | 10.00 | 8.00 |

| 17 | 6199 | JAM | 2292 | 139.73 | 19.00 | 24.00 | 3.30 | 20.00 |

| 18 | 6162 | JAM | 650 | 50.09 | 19.40 | 17.00 | 1.23 | 9.91 |

| 19 | 6199 | JAM | 300 | 26.31 | 11.90 | 13.50 | 1.00 | 10.10 |

| 20 | 3540 | GBR | 238 | 38.20 | 17.85 | 0.10 | −0.45 | −0.54 |

| 21 | 3600 | GBR | 1500 | 51.00 | 0.32 | 43.00 | 0.54 | 0.87 |

| 22 | 3679 | GBR | 190 | 7.12 | 8.79 | 7.69 | 11.31 | 17.21 |

| 23 | 3490 | GBR | 78 | 7.01 | 15.31 | 16.12 | 13.47 | 16.14 |

| 24 | 3679 | GBR | 225 | −0.25 | −66.89 | −70.02 | −47.53 | −85.90 |

| 25 | 3640 | GBR | 343 | −1.64 | −0.14 | −0.34 | −0.22 | −1.03 |

| 26 | 1540 | MHL | 576 | 4.25 | 21 | 21 | 10.00 | 20.00 |

| 27 | 6022 | MHL | 136 | 10.8 | 40.6 | 44.3 | 3.40 | 11.80 |

| 28 | 8700 | MHL | 90 | 31.9 | 86.8 | 88.9 | 86.80 | 85.80 |

| 29 | 6022 | MHL | 20 | 0.255 | 9.6 | 14 | 89.00 | 13.30 |

| 30 | 2711 | MHL | 20 | 0.446 | 15 | 14 | 11.00 | 16.00 |

| 31 | 1540 | MHL | 120 | 4.34 | 55 | 10 | 90.00 | 60.00 |

| 32 | 5140 | MHL | 110 | 16.59 | 35 | 30 | 8.00 | 9.00 |

| 33 | 3490 | ITA | 32 | 5.216 | 3.4 | 4.83 | 3.00 | 1.54 |

| 34 | 7380 | KIR | 5 | 0.0842 | 2.8 | 2.8 | 1.80 | 1.80 |

| 35 | 8741 | KIR | 35 | 6.6 | 2.90 | 3.2 | 1.60 | 1.80 |

| 36 | 0900 | KIR | 280 | 15.44 | 15.00 | 27.50 | 4.00 | 6.50 |

| 37 | 5141 | TUV | 45 | 0.4 | 5 | 8 | 10.00 | 7.00 |

| 38 | 5080 | TUV | 20 | 0.42 | 7 | 10 | 8 | 6 |

| 39 | 5080 | TUV | 5 | 0.32 | 6 | 9 | 9 | 8 |

| 40 | 3640 | GBR | 195 | 8.01 | 9.2 | 7.5 | 13.2 | 18.4 |

| 41 | 3640 | GBR | 1355 | 48.5 | 1.1 | 37.2 | 1.2 | 0.9 |

| 42 | 6199 | GBR | 1233 | 372.3 | 28.1 | 27.3 | 7.6 | 12.3 |

| 43 | 6199 | GBR | 65 | 5.2 | 13.2 | 14.7 | 12.9 | 15.7 |

| 44 | 2870 | ITA | 23 | 0.20652 | 3 | 2 | 1.8 | 2.5 |

| 45 | 3560 | AUS | 1100 | 2.93 | 25.1 | 22.5 | 3.2 | 9.4 |

| 46 | 4941 | AUS | 122 | 4.2 | 35.1 | 10.4 | 27.2 | 16.7 |

| 47 | 6500 | AUS | 162 | 4.8 | 2.2 | −0.4 | −8.4 | −0.23 |

| 48 | 3620 | AUS | 42 | 4.7 | 11.7 | 4.8 | 4.1 | 5.3 |

| 49 | 6199 | AUS | 116 | 4.8 | 2.6 | 3.7 | 2.8 | 1.6 |

| 50 | 6199 | AUS | 204 | 67 | 2.2 | 4.4 | 1.4 | 2 |

| 51 | 3640 | AUS | 167 | 3.2 | 1.9 | 6.9 | 1.5 | 1.8 |

| 52 | 3640 | AUS | 87 | 2.7 | 3 | 3.6 | 0.2 | 1.5 |

| 53 | 6199 | AUS | 52 | 1.9 | 1.1 | 0.2 | 0.3 | 0.6 |

| Company No. | Total CS | Total EC | Total SC | Total HC | Total NC | SMI Total |

|---|---|---|---|---|---|---|

| 1 | 156 | 77 | 55 | 98 | 38 | 424 |

| 2 | 159 | 90 | 57 | 103 | 36 | 445 |

| 3 | 113 | 72 | 41 | 73 | 26 | 325 |

| 4 | 74 | 54 | 23 | 54 | 14 | 219 |

| 5 | 94 | 57 | 28 | 69 | 20 | 268 |

| 6 | 72 | 54 | 21 | 68 | 13 | 228 |

| 7 | 120 | 73 | 37 | 80 | 22 | 332 |

| 8 | 48 | 32 | 15 | 49 | 8 | 152 |

| 9 | 46 | 32 | 17 | 46 | 11 | 152 |

| 10 | 159 | 92 | 56 | 104 | 35 | 446 |

| 11 | 150 | 91 | 58 | 103 | 27 | 429 |

| 12 | 115 | 66 | 47 | 79 | 28 | 335 |

| 13 | 156 | 91 | 60 | 109 | 33 | 449 |

| 14 | 161 | 94 | 58 | 106 | 40 | 459 |

| 15 | 135 | 77 | 41 | 81 | 35 | 369 |

| 16 | 141 | 81 | 51 | 87 | 37 | 397 |

| 17 | 139 | 85 | 51 | 76 | 20 | 371 |

| 18 | 120 | 88 | 54 | 94 | 15 | 371 |

| 19 | 156 | 88 | 57 | 92 | 32 | 425 |

| 20 | 53 | 59 | 25 | 63 | 13 | 213 |

| 21 | 71 | 47 | 20 | 68 | 13 | 219 |

| 22 | 77 | 40 | 18 | 63 | 19 | 217 |

| 23 | 72 | 41 | 24 | 77 | 11 | 225 |

| 24 | 70 | 49 | 22 | 66 | 17 | 224 |

| 25 | 69 | 43 | 25 | 61 | 14 | 212 |

| 26 | 142 | 90 | 56 | 103 | 35 | 426 |

| 27 | 133 | 77 | 57 | 99 | 34 | 400 |

| 28 | 134 | 73 | 53 | 89 | 39 | 388 |

| 29 | 150 | 94 | 58 | 106 | 40 | 448 |

| 30 | 136 | 85 | 48 | 90 | 30 | 389 |

| 31 | 119 | 72 | 47 | 81 | 31 | 350 |

| 32 | 100 | 43 | 39 | 40 | 18 | 240 |

| 33 | 70 | 45 | 18 | 53 | 12 | 198 |

| 34 | 136 | 87 | 43 | 93 | 34 | 393 |

| 35 | 156 | 90 | 55 | 94 | 38 | 433 |

| 36 | 162 | 83 | 58 | 108 | 39 | 450 |

| 37 | 138 | 73 | 53 | 98 | 36 | 398 |

| 38 | 139 | 75 | 45 | 101 | 33 | 393 |

| 39 | 113 | 76 | 50 | 89 | 35 | 363 |

| 40 | 70 | 40 | 21 | 62 | 21 | 214 |

| 41 | 82 | 53 | 24 | 71 | 22 | 252 |

| 42 | 87 | 45 | 31 | 70 | 18 | 251 |

| 43 | 81 | 37 | 31 | 81 | 13 | 243 |

| 44 | 135 | 90 | 31 | 92 | 30 | 378 |

| 45 | 104 | 45 | 35 | 49 | 25 | 258 |

| 46 | 88 | 57 | 32 | 67 | 25 | 269 |

| 47 | 84 | 51 | 31 | 65 | 26 | 257 |

| 48 | 83 | 54 | 31 | 53 | 22 | 243 |

| 49 | 96 | 47 | 29 | 61 | 30 | 263 |

| 50 | 101 | 23 | 33 | 60 | 34 | 251 |

| 51 | 98 | 32 | 45 | 52 | 22 | 249 |

| 52 | 67 | 36 | 42 | 87 | 18 | 250 |

| 53 | 78 | 40 | 39 | 78 | 22 | 257 |

References

- Feil, A.A.; Schreiber, D.; Haetinger, C.; Strasburg, V.J.; Barkert, C.L. Sustainability Indicators for Industrial Organizations: Systematic Review of Literature. Sustainability 2019, 11, 854. [Google Scholar] [CrossRef]

- Hosseini, S.; Barker, K.; Ramirez-Marquez, J.E. A review of definitions and measures of system resilience. Reliab. Eng. Syst. Saf. 2016, 145, 47–61. [Google Scholar] [CrossRef]

- Roostaie, S.; Nawari, N.; Kibert, C.J. Integrated sustainability and resilience assessment framework: From theory to practice. J. Clean. Prod. 2019, 232, 1158–1166. [Google Scholar] [CrossRef]

- Faber, M.H. On sustainability and resilience of engineered systems. In Routledge Handbook of Sustainable and Resilient Infrastructure; Routledge: Abingdon, UK, 2019; pp. 28–49. [Google Scholar]

- Fahimnia, B.; Jabbarzadeh, A. Marrying supply chain sustainability and resilience: A match made in heaven. Transp. Res. Part E Logist. Transp. Rev. 2016, 91, 306–324. [Google Scholar] [CrossRef]

- Milman, A.; Short, A. Incorporating resilience into sustainability indicators: An example for the urban water sector. Glob. Environ. Chang. 2008, 18, 758–767. [Google Scholar] [CrossRef]

- Redman, C.L. Should sustainability and resilience be combined or remain distinct pursuits? Ecol. Soc. 2014, 19, 37. [Google Scholar] [CrossRef]

- Marchese, D.; Reynolds, E.; Bates, M.E.; Morgan, H.; Clark, S.S.; Linkov, I. Resilience and sustainability: Similarities and differences in environmental management applications. Sci. Total Environ. 2018, 613, 1275–1283. [Google Scholar] [CrossRef]

- Herbane, B. A Business Continuity Perspective on Organisational Resilience. In IRGC Resource Guide on Resilience; Florin, M.-V., Linkov, I., Eds.; EPFL International Risk Governance Center (IRGC): Lausanne, Switzerland, 2016; Volume 1. [Google Scholar]

- Francis, R.; Bekera, B. A metric and frameworks for resilience analysis of engineered and infrastructure systems. Reliab. Eng. Syst. Saf. 2014, 121, 90–103. [Google Scholar] [CrossRef]

- Annarelli, A.; Nonino, F. Strategic and operational management of organizational resilience: Current state of research and future directions. Omega 2016, 62, 1–18. [Google Scholar] [CrossRef]

- Bhamra, R.; Dani, S.; Burnard, K. Resilience: The concept, a literature review and future directions. Int. J. Prod. Res. 2011, 49, 5375–5393. [Google Scholar] [CrossRef]

- Lee, A.V.; Vargo, J.; Seville, E. Developing a tool to measure and compare organizations’ resilience. Nat. Hazards Rev. 2013, 14, 29–41. [Google Scholar] [CrossRef]

- D’Agostini, M.; Tondolo, R.D.R.P.; Camargo, M.E.; Dullius, A.I.D.S.; Tondolo, R.D.R.P.; Russo, S.L. Relationship between sustainable operations practices and performance: A meta-analysis. Int. J. Prod. Perform. Manag. 2017, 66, 1020–1042. [Google Scholar] [CrossRef]

- Dalziell, E.P.; Mcmanus, S.T. Resilience, vulnerability, and adaptive capacity: Implications for system performance. Int. Forum Eng. Decis. Mak. 2004, 17. Available online: https://ir.canterbury.ac.nz/handle/10092/2809 (accessed on 25 February 2020).

- Hollnagel, E. Introduction to the Resilience Analysis Grid (RAG). 2015, pp. 1–16. Available online: https://erikhollnagel.com/onewebmedia/RAG%20Outline%20V2.pdf (accessed on 25 February 2020).

- Li, X.; Wu, Q.; Holsapple, C.W.; Goldsby, T. An empirical examination of firm financial performance along dimensions of supply chain resilience. Manag. Res. Rev. 2017, 40, 254–269. [Google Scholar] [CrossRef]

- Yarveisy, R.; Gao, C.; Khan, F. A simple yet robust resilience assessment metrics. Reliab. Eng. Syst. Saf. 2020, 197, 106810. [Google Scholar] [CrossRef]

- De Mandojana, N.O.M.; Bansal, P. The long-term benefits of organizational resilience through sustainable business practices. Strateg. Manag. J. 2015, 37, 1615–1631. [Google Scholar] [CrossRef]

- Macuzić, I.; Tadic, D.; Aleksic, A.; Stefanovic, M. A two step fuzzy model for the assessment and ranking of organizational resilience factors in the process industry. J. Loss Prev. Process. Ind. 2016, 40, 122–130. [Google Scholar] [CrossRef]

- Fiksel, J. Sustainability and resilience: Toward a systems approach. IEEE Eng. Manag. Rev. 2007, 35, 5. [Google Scholar] [CrossRef]

- Parker, D.W.; Loh, A.; Chevers, D.; Minto-Coy, I.; Zeppetella, L. Operations sustainability maturity model: Preliminary findings of financial services in developing and developed countries. Meas. Bus. Excel. 2017, 21, 309–336. [Google Scholar] [CrossRef]

- Magon, R.B.; Thomé, A.M.T.; Ferrer, A.L.C.; Scavarda, L.F. Sustainability and performance in operations management research. J. Clean. Prod. 2018, 190, 104–117. [Google Scholar] [CrossRef]

- Prayag, G.; Chowdhury, M.; Spector, S.; Orchiston, C. Organizational resilience and financial performance. Ann. Tour. Res. 2018, 73, 193–196. [Google Scholar] [CrossRef]

- Gunasekaran, A.; Rai, B.K.; Griffin, M. Resilience and competitiveness of small and medium size enterprises: An empirical research. Int. J. Prod. Res. 2011, 49, 5489–5509. [Google Scholar] [CrossRef]

- Loh, A.; Parker, D. Corporate Sustainability Maturity Model: The Development of a Framework and Standardised Assessment Instrument; Working Paper Series; The University of Queensland: Brisbane, QLD, Australia, 2016. [Google Scholar]

- Goyal, P.; Rahman, Z.; Kazmi, A.A. Corporate sustainability performance and firm performance research: Literature review and future research agenda. Manag. Decis. 2013, 51, 361–379. [Google Scholar] [CrossRef]

- Alshehhi, A.; Nobanee, H.; Khare, N. The Impact of Sustainability Practices on Corporate Financial Performance: Literature Trends and Future Research Potential. Sustainability 2018, 10, 494. [Google Scholar] [CrossRef]

- Aggarwal, P. Impact of Sustainability Performance of Company on its Financial Performance: A Study of Listed Indian Companies. Glob. J. Manag. Bus. Res. Financ. 2013, 13, 61–70. [Google Scholar]

- Lassala, C.; Apetrei, A.; Sapena, J. Sustainability matter and financial performance of companies. Sustainability 2017, 9, 498. [Google Scholar] [CrossRef]

- De Carvalho, A.O.; Ribeiro, I.; Cirani, C.B.S.; Cintra, R.F. Organizational resilience: A comparative study between innovative and non-innovative companies based on the financial performance analysis. Int. J. Innov. 2016, 4, 58–69. [Google Scholar] [CrossRef]

- Springer Nature Switzerland AG. Revisiting Supply Chain Risk; Zsidisin, G.A., Henke, M., Eds.; Springer: Cham, Switzerland, 2019; Volume 7. [Google Scholar]

- Prashar, A.; Sunder M, V. A bibliometric and content analysis of sustainable development in small and medium-sized enterprises. J. Clean. Prod. 2020, 245, 118665. [Google Scholar] [CrossRef]

- Avery, G.C.; Bergsteiner, H. Sustainable leadership practices for enhancing business resilience and performance. Strateg. Leadersh. 2011, 39, 5–15. [Google Scholar] [CrossRef]

- Rajesh, R. On sustainability, resilience, and the sustainable–resilient supply networks. Sustain. Prod. Consum. 2018, 15, 74–88. [Google Scholar] [CrossRef]

- Sabahi, S.; Parast, M.M. Firm innovation and supply chain resilience: A dynamic capability perspective. Int. J. Logist. Res. Appl. 2019, 1–16. [Google Scholar] [CrossRef]

- Golicic, S.L.; Flint, D.J.; Signori, P. Building business sustainability through resilience in the wine industry. Int. J. Wine Bus. Res. 2017, 29, 74–97. [Google Scholar] [CrossRef]

- Carmeli, A.; Dothan, A.; Boojihawon, D.K. Resilience of sustainability-oriented and financially-driven organizations. Bus. Strateg. Environ. 2019, 29, 154–169. [Google Scholar] [CrossRef]

- Berns, M.; Townend, A.; Khayat, Z.; Balagopal, B.; Reeves, M.; Hopkins, M.S.; Kruschwitz, N. The Business of Sustainability: What it Means to Managers Now. MIT Sloan Management Review 2009, 51, 20–26. [Google Scholar]

- Hillman, A.J.; Keim, G.D. Shareholder value, stakeholder management, and social issues: what’s the bottom line? Strateg. Manag. J. 2001, 22, 125–139. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. The Big idea Creating Shared Value how to reinvent capitalism-and unleash a wave of innovation and growth. Harvard Business Review, January–February 2011; 1–17. Available online: https://hbr.org/2011/01/the-big-idea-creating-shared-value (accessed on 25 February 2020).

- Sroufe, R.; Gopalakrishna-Remani, V. Management, Social Sustainability, Reputation, and Financial Performance Relationships: An Empirical Examination of U.S. Firms. Organ. Environ. 2018, 32, 331–362. [Google Scholar] [CrossRef]

| Operations Sustainability Domain | OSSM Items Related to Resilience Indicators and Capabilities | References |

|---|---|---|

| Corporate sustainability | Network perspective | [13] |

| Effective planning | [13] | |

| Staff engagement/sense of teamwork | [10,13,36] | |

| Economic capital | Long-term perspective | [34] |

| Innovation and creativity | [31,32,36] | |

| Flexibility/adaptability | [10] | |

| Information and knowledge | [13] | |

| Societal capital | Organizational connectivity and relationships | [10,13] |

| Stakeholders involvement | [13] | |

| Human capital | Communications and relationship | [37] |

| Information and knowledge | [13] | |

| Natural capital | -- |

| Feature | Influential Points |

|---|---|

| Log(operating income) | 1, 2, 3 |

| Net margin | 24, 28 |

| EBT | 24, 28 |

| Return on assets | 24, 28, 29, 31 |

| Return on equity | 24, 28 |

| Log(Employees) | 1, 2, 3 |

| Feature | Parameter | Estimate | Squared Error | t-Statistic | p-Value |

|---|---|---|---|---|---|

| Log(Operating income) | Intercept | 2.90 | 1.38 | 2.10 | 0.04 |

| Slope | −0.34 | 1.97 | −0.17 | 0.86 | |

| Net margin | Intercept | 1.11 | 9.54 | 0.12 | 0.91 |

| Slope | 18.92 | 13.74 | 1.38 | 0.17 | |

| EBT | Intercept | 3.90 | 10.07 | 0.39 | 0.70 |

| Slope | 18.03 | 14.50 | 1.24 | 0.22 | |

| Return on assets | Intercept | −8.88 | 10.81 | −0.82 | 0.42 |

| Slope | 26.42 | 15.56 | 1.70 | 0.10 | |

| Return on equity | Intercept | −7.49 | 9.97 | −0.75 | 0.46 |

| Slope | 24.61 | 14.35 | 1.71 | 0.09 | |

| Log(Employees) | Intercept | 4.67 | 1.04 | 4.50 | 0.00 |

| Slope | 1.23 | 1.50 | 0.82 | 0.41 |

| Feature | Parameter | Estimate | Squared Error | t-Statistic | p-Value |

|---|---|---|---|---|---|

| Log(Operating income) | Intercept | 3.65 | 1.12 | 3.27 | 0.00 |

| Slope | −2.09 | 1.62 | −1.29 | 0.20 | |

| Net margin | Intercept | 10.36 | 6.25 | 1.66 | 0.10 |

| Slope | 5.28 | 8.99 | 0.59 | 0.56 | |

| EBT | Intercept | 13.64 | 6.75 | 2.02 | 0.05 |

| Slope | 3.81 | 9.71 | 0.39 | 0.70 | |

| Return on assets | Intercept | 5.16 | 3.57 | 1.44 | 0.16 |

| Slope | −0.21 | 5.19 | −0.04 | 0.97 | |

| Return on equity | Intercept | 3.04 | 5.82 | 0.52 | 0.60 |

| Slope | 9.36 | 8.37 | 1.12 | 0.27 | |

| Log(Employees) | Intercept | 5.27 | 0.81 | 6.51 | 0.00 |

| Slope | −0.17 | 1.18 | −0.14 | 0.89 |

| Feature | Parameter | Estimate | Squared Error | t-Statistic | p-Value |

|---|---|---|---|---|---|

| Log(Operating income) | Intercept | 3.02 | 1.36 | 2.22 | 0.03 |

| Slope | −0.93 | 1.93 | −0.48 | 0.63 | |

| Net margin | Intercept | 9.90 | 6.37 | 1.55 | 0.13 |

| Slope | 4.72 | 9.17 | 0.52 | 0.61 | |

| EBT | Intercept | 12.38 | 7.45 | 1.66 | 0.10 |

| Slope | 4.91 | 10.73 | 0.46 | 0.65 | |

| Return on assets | Intercept | 5.24 | 4.04 | 1.30 | 0.20 |

| Slope | −0.71 | 5.81 | −0.12 | 0.90 | |

| Return on equity | Intercept | 3.37 | 4.48 | 0.75 | 0.46 |

| Slope | 8.45 | 6.45 | 1.31 | 0.20 | |

| Log(Employees) | Intercept | 4.79 | 0.96 | 4.97 | 0.00 |

| Slope | 0.80 | 1.39 | 0.58 | 0.57 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Balugani, E.; Butturi, M.A.; Chevers, D.; Parker, D.; Rimini, B. Empirical Evaluation of the Impact of Resilience and Sustainability on Firms’ Performance. Sustainability 2020, 12, 1742. https://doi.org/10.3390/su12051742

Balugani E, Butturi MA, Chevers D, Parker D, Rimini B. Empirical Evaluation of the Impact of Resilience and Sustainability on Firms’ Performance. Sustainability. 2020; 12(5):1742. https://doi.org/10.3390/su12051742

Chicago/Turabian StyleBalugani, Elia, Maria Angela Butturi, Delroy Chevers, David Parker, and Bianca Rimini. 2020. "Empirical Evaluation of the Impact of Resilience and Sustainability on Firms’ Performance" Sustainability 12, no. 5: 1742. https://doi.org/10.3390/su12051742

APA StyleBalugani, E., Butturi, M. A., Chevers, D., Parker, D., & Rimini, B. (2020). Empirical Evaluation of the Impact of Resilience and Sustainability on Firms’ Performance. Sustainability, 12(5), 1742. https://doi.org/10.3390/su12051742