Perspective of Local Government on the Performance Assessment of District Sports and Leisure Centers

Abstract

:1. Introduction

2. Public Administration on the District Local Sports and Leisure Centers in Taiwan

3. Literature Review

3.1. The Theoretical Background Evolutionary Theory

3.2. Performance Assessment for Sport and Leisure Centres

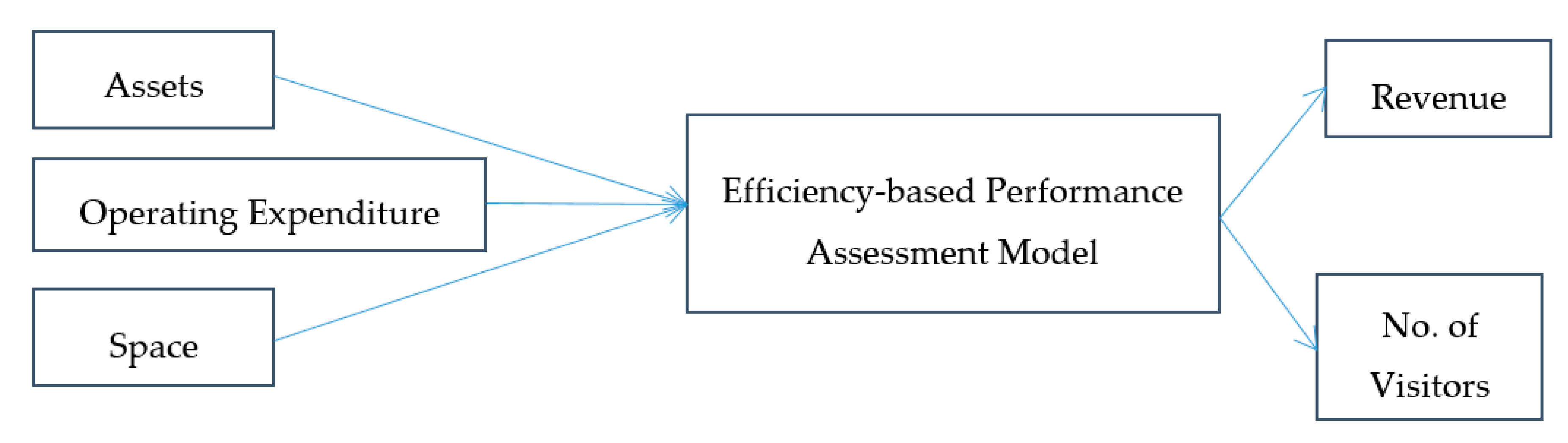

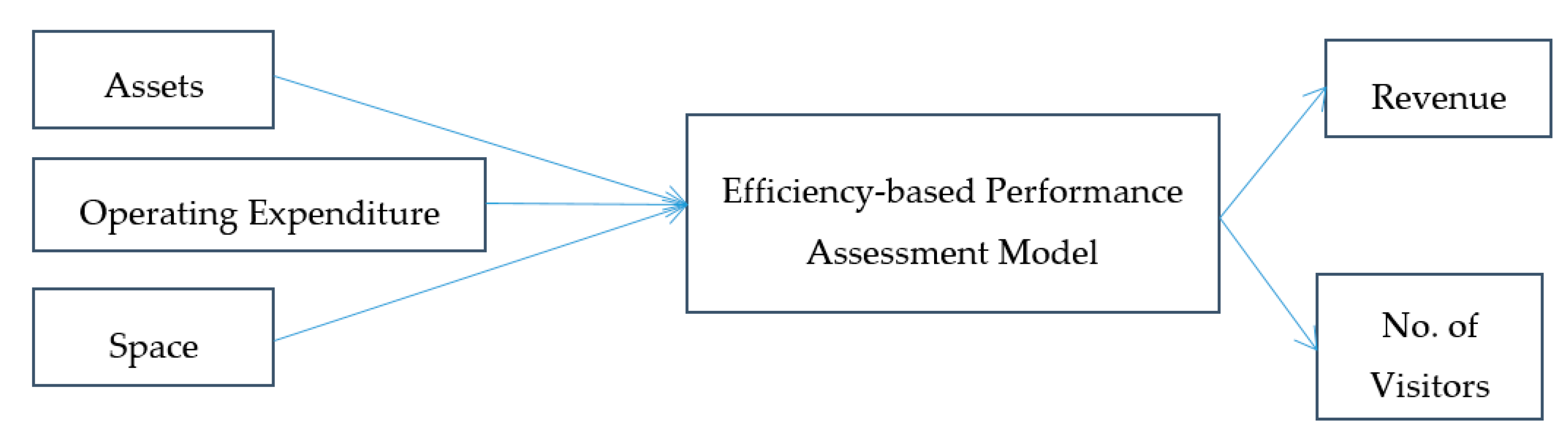

3.3. The Application of Total-Factor Framework

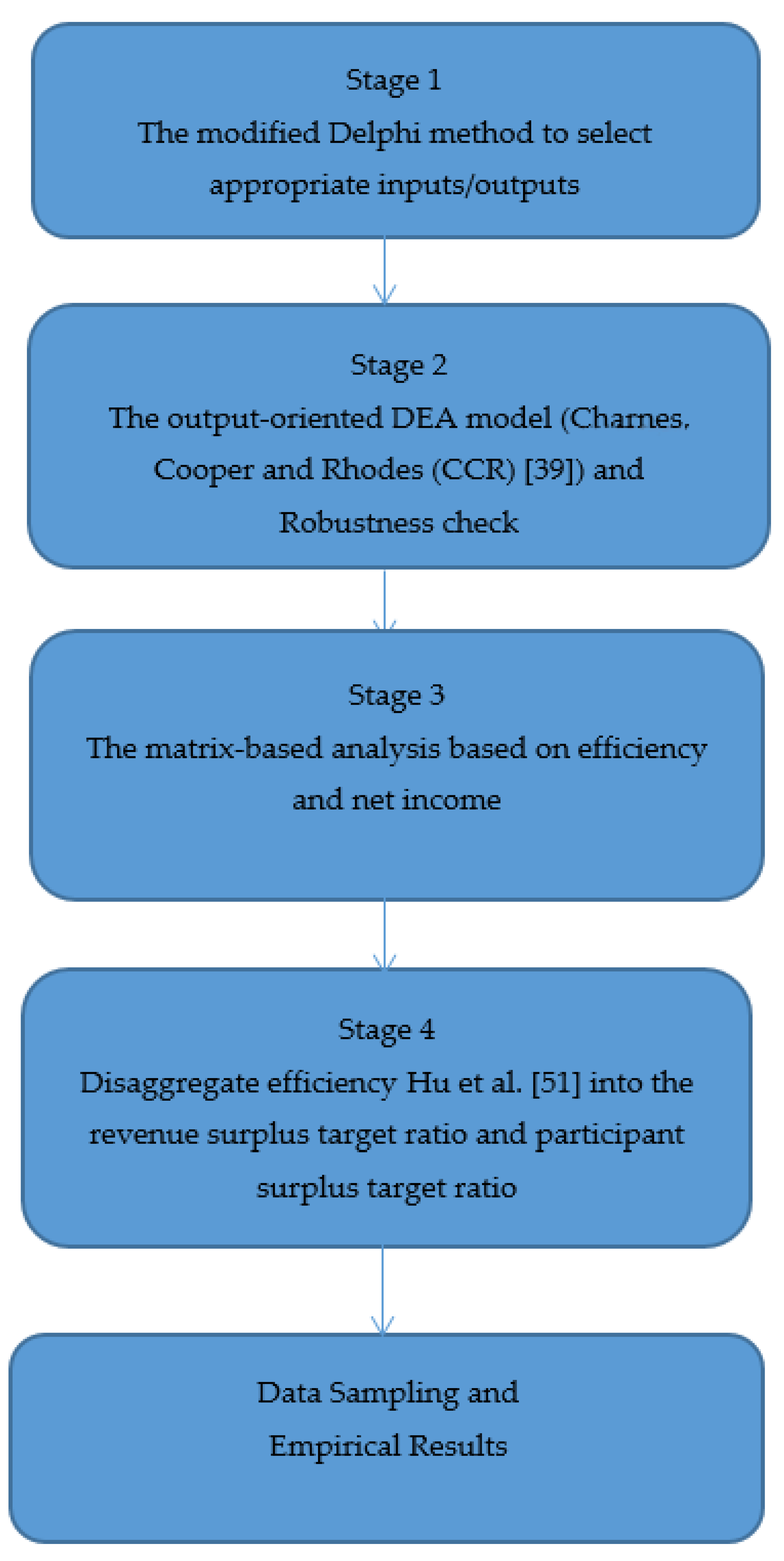

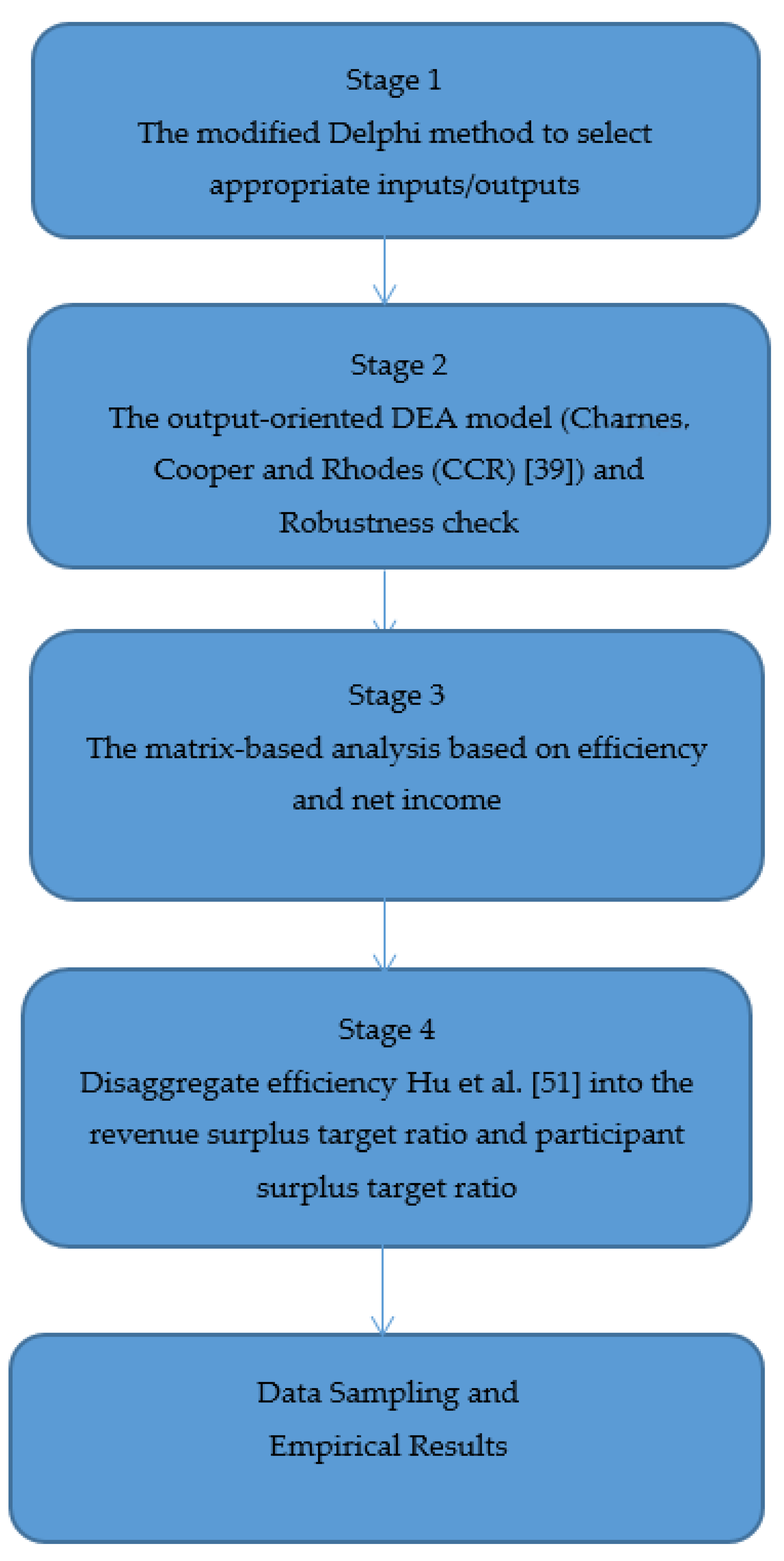

4. Materials and Methods

4.1. The Modified Delphi Method

4.2. DEA Model

4.3. Estimate the Output Surplus Target Ratio (OSTR) Using the Total-Factor Framework

4.4. Data Sampling

5. Results

5.1. Descriptive Statistics

5.2. Efficiency Score from the DEA Model

5.3. Robustness Validation

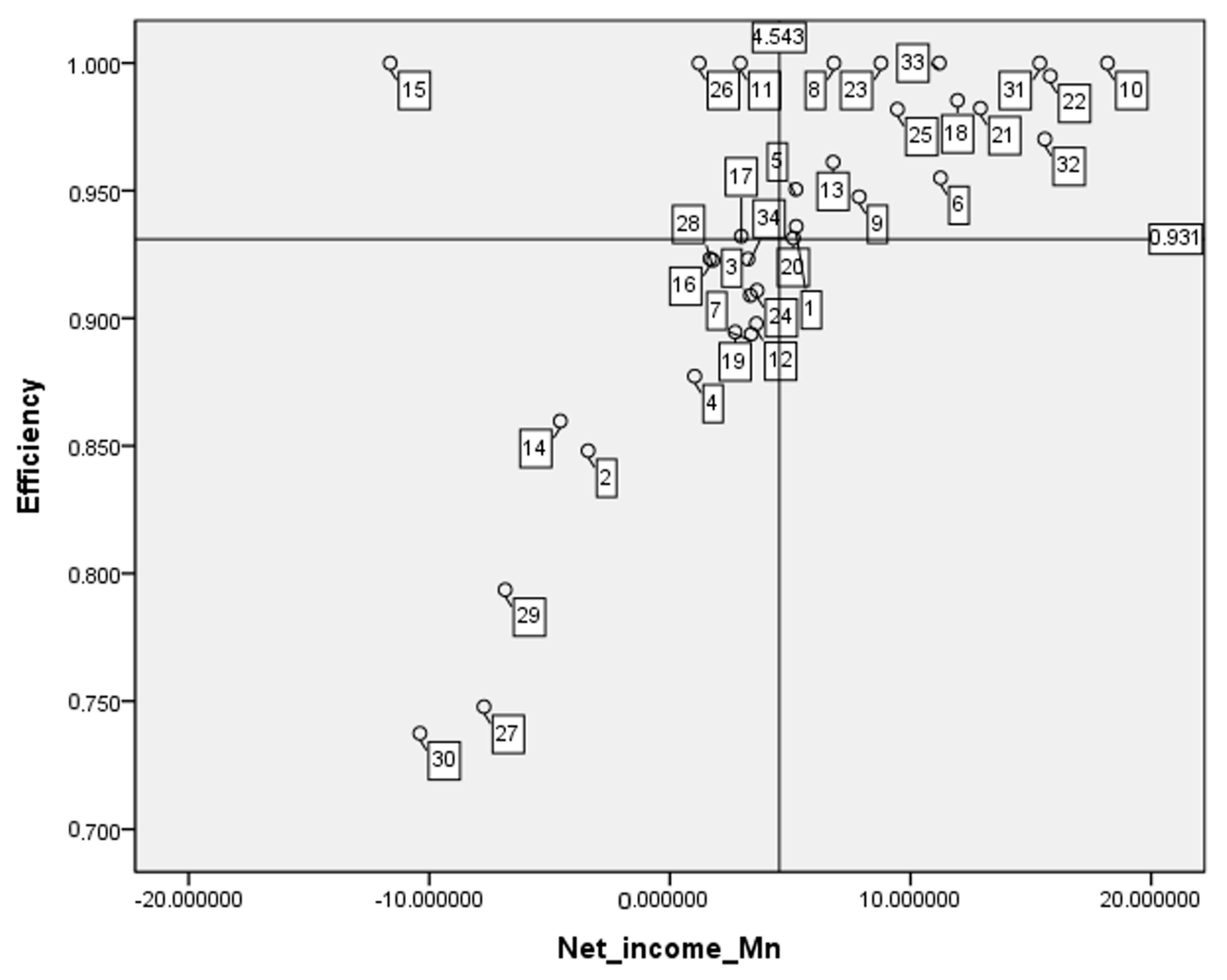

5.4. The Quadrant-Based Matrix Based on Efficiency Score and Net Income

5.5. Total-Factor Output Efficiency

6. Discussion and Implications

6.1. Discussion

6.2. Theoretical Implications

6.3. Managerial Implications

7. Conclusions, Limitations, and Future Research

Funding

Conflicts of Interest

References

- Afonso, A.; Venâncio, A. Local territorial reform and regional spending efficiency. Local Gov. Stud. 2019, 1–23. [Google Scholar] [CrossRef] [Green Version]

- Pérez-López, G.; Prior, D.; Zafra-Gómez, J.L. Rethinking new public management delivery forms and efficiency: Long-term effects in Spanish local government. J. Public Adm. Res. Theory 2015, 25, 1157–1183. [Google Scholar] [CrossRef]

- Lawson, H.A. Empowering people, facilitating community development, and contributing to sustainable development: The social work of sport, exercise, and physical education programs. Sport Educ. Soc. 2005, 10, 135–160. [Google Scholar] [CrossRef]

- Howat, G.; Assaker, G. Outcome quality in participant sport and recreation service quality models: Empirical results from public aquatic centres in Australia. Sport Manag. Rev. 2016, 19, 520–535. [Google Scholar] [CrossRef]

- Kung, S.P.; Taylor, P. The effect of management types on the performance of English public sports centres. Int. J. Sport Policy Politics 2010, 2, 303–326. [Google Scholar] [CrossRef]

- Liu, Y.-D.; Taylor, P.; Shibli, S. Sport Equity: Benchmarking the Performance of English Public Sport Facilities. Eur. Sport Manag. Q. 2009, 9, 3–21. [Google Scholar] [CrossRef]

- Rossi, L.; Breuer, C.; Feiler, S. Determinants of non-profit sports clubs’ perceived competition from commercial sports providers. Sport Manag. Rev. 2020, 23, 736–749. [Google Scholar] [CrossRef]

- Alexandris, K.; Zahariadis, P.; Tsorbatzoudis, C.; Grouios, G. An empirical investigation of the relationships among service quality, customer satisfaction and psychological commitment in a health club context. Eur. Sport Manag. Q. 2004, 4, 36–52. [Google Scholar] [CrossRef]

- Howat, G.; Murray, D.; Crilley, G. The relationships between service problems and perceptions of service quality, satisfaction, and behavioural intentions of Australian public sports and leisure centre customers. J. Park Recreat. Adm. 1999, 17, 42–64. [Google Scholar]

- Murray, D.; Howat, G. The relationships among service quality, value, satisfaction, and future intentions of customers at an Australian sports and leisure centre. Sport Manag. Rev. 2002, 5, 25–43. [Google Scholar] [CrossRef]

- Vieira, E.R.M.; Ferreira, J.J. Strategic framework of fitness clubs based on quality dimensions: The blue ocean strategy approach. Total Qual. Manag. Bus. Excell. 2018, 29, 1648–1667. [Google Scholar] [CrossRef]

- Iversen, E.B. Does size matter when public management tools meet (the voluntary) reality in sports facilities? World Leis. J. 2017, 59, 54–69. [Google Scholar] [CrossRef]

- Barney, J.B. Resource-based theories of competitive advantage: A ten-year retrospective on the resource-based view. J. Manag. 2001, 27, 643–650. [Google Scholar] [CrossRef]

- Nelson, R.; Winter, G. An Evolutionary Theory of Economic Change; Harvard University Press: Cambridge, MA, USA, 1982; ISBN 9780674272286. [Google Scholar]

- Donnellan, J.; Rutledge, W.L. A case for resource-based view and competitive advantage in banking. Manag. Decis. Econ. 2019, 40, 728–737. [Google Scholar] [CrossRef]

- Amit, R.; Schoemaker, P.J.H. Strategic assets and organizational rent: Strategic assets. Strat. Manag. J. 1993, 14, 33–46. [Google Scholar] [CrossRef]

- Donthu, N.; Yoo, B. Cultural influences on service quality expectations. J. Serv. Res. 1998, 1, 178–186. [Google Scholar] [CrossRef]

- Capron, L. The long-term performance of horizontal acquisitions. Strateg. Manag. J. 1999, 20, 987–1018. [Google Scholar] [CrossRef]

- Seiford, L.M.; Zhu, J. Profitability and marketability of the top 55 U.S. commercial banks. Manag. Sci. 1999, 45, 1270–1288. [Google Scholar] [CrossRef] [Green Version]

- Bagozzi, R.P.; Phillips, L.W. Representing and testing organizational theories: A holistic construal. Adm. Sci. Q. 1982, 27, 459. [Google Scholar] [CrossRef]

- Chakravarthy, B.S. Measuring strategic performance. Strat. Manag. J. 1986, 7, 437–458. [Google Scholar] [CrossRef]

- Hong, S.-J.; Jeon, M. The technical efficiency of French regional airports and low-cost carrier terminals. Sustainability 2019, 11, 5107. [Google Scholar] [CrossRef] [Green Version]

- Lo, S.-F. Performance evaluation for sustainable business: A profitability and marketability framework. Corp. Soc. Respons. Environ. Manag. 2010, 17, 311–319. [Google Scholar] [CrossRef]

- Ortiz-de-Mandojana, N.; Bansal, P. The long-term benefits of organizational resilience through sustainable business practices: The long-term benefits of sustainable business practices. Strat. Manag. J. 2016, 37, 1615–1631. [Google Scholar] [CrossRef]

- Porter, E.; Mark, R. Creating shared value. Manag. Sustain. Bus. 2019, 323–346. [Google Scholar] [CrossRef]

- Fang, C.Y.; Peng, P.Y.; Pan, W.T. Does using an a la carte or combo set menu affect the performance of a teppanyaki-style restaurant? Int. J. Contemp. Hosp. Manag. 2013, 25, 491–509. [Google Scholar] [CrossRef]

- Honma, S.; Hu, J.-L. Industry-level total-factor energy efficiency in developed countries: A Japan-centered analysis. Appl. Energy 2014, 119, 67–78. [Google Scholar] [CrossRef]

- Hu, J.-L.; Wang, S.-C. Total-factor energy efficiency of regions in China. Energy Policy 2006, 34, 3206–3217. [Google Scholar] [CrossRef]

- Liu, Y.-D.; Taylor, P.; Shibli, S. The operational efficiency of English public sport facilities. Manag. Leis. 2007, 12, 251–272. [Google Scholar] [CrossRef]

- Department of Sports, The Taipei City Government. 2020. Available online: https://english.sports.gov.taipei/News_Content.aspx?n=B3572EB30821B61C&sms=37F5ADE5D6397558&s=A3DFB7BE7B4794E1 (accessed on 10 October 2020).

- Du, Y.; Fang, J.; Ke, Y.; Philbin, S.P.; Zhang, J. Developing a revenue sharing method for an operational transfer-operate-transfer project. Sustainability 2019, 11, 6436. [Google Scholar] [CrossRef] [Green Version]

- Scandizzo, P.L.; Venturab, M. Sharing risk through concession contracts. Eur. J. Oper. Res. 2010, 207, 363–370. [Google Scholar] [CrossRef] [Green Version]

- Yong Kim, B.; Oh, H. How do hotel firms obtain a competitive advantage? Int. J. Contemp. Hosp. Manag. 2004, 16, 65–71. [Google Scholar] [CrossRef]

- Song, M.; Di Benedetto, C.A.; Nason, R.W. Capabilities and financial performance: The moderating effect of strategic type. J. Acad. Mark. Sci. 2007, 35, 18–34. [Google Scholar] [CrossRef]

- Lieberman, M.B.; Dhawan, R. Assessing the resource base of Japanese and U.S. auto producers: A stochastic frontier production function approach. Manag. Sci. 2005, 51, 1060–1075. [Google Scholar] [CrossRef] [Green Version]

- Nath, P.; Nachiappan, S.; Ramanathan, R. The impact of marketing capability, operations capability and diversification strategy on performance: A resource-based view. Ind. Mark. Manag. 2010, 39, 317–329. [Google Scholar] [CrossRef]

- Coelli, T.J. Recent developments in frontier modelling and efficiency measurement. Aust. J. Agric. Econ. 1995, 39, 219–245. [Google Scholar] [CrossRef] [Green Version]

- Gomes, C.F.; Yasin, M.M. An assessment of performance-related practices in service operational settings: Measures and utilization patterns. Serv. Ind. J. 2013, 33, 73–97. [Google Scholar] [CrossRef]

- Charnes, A.; Cooper, W.W.; Rhodes, E. Measuring the efficiency of decision making units. Eur. J. Oper. Res. 1978, 2, 429–444. [Google Scholar] [CrossRef]

- Kim, S.; Chung, J. Enhancing visitor return rate of national museums: Application of data envelopment analysis to millennials. Asia Pac. J. Tour. Res. 2020, 25, 76–88. [Google Scholar] [CrossRef]

- Reynolds, D. Hospitality-productivity assessment using data-envelopment analysis. Cornell Hotel Restaur. Adm. Q. 2003, 44, 8. [Google Scholar] [CrossRef]

- Donthu, N.; Hershberger, E.K.; Osmonbekov, T. Benchmarking marketing productivity using data envelopment analysis. J. Bus. Res. 2005, 58, 1474–1482. [Google Scholar] [CrossRef]

- Sherman, H.D.; Zhu, J. Analyzing performance in service organizations. MIT Sloan Manag. Rev. 2013, 54, 37–42. [Google Scholar]

- Terrien, M.; Andreff, W. Organisational efficiency of national football leagues in Europe. Eur. Sport Manag. Q. 2020, 20, 205–224. [Google Scholar] [CrossRef]

- O’Boyle, I.; Hassan, D. Performance management and measurement in national-level non-profit sport organisations. Eur. Sport Manag. Q. 2014, 14, 299–314. [Google Scholar] [CrossRef]

- Macintosh, E.; Doherty, A. Reframing the service environment in the fitness industry. Manag. Leis. 2007, 12, 273–289. [Google Scholar] [CrossRef]

- Rafoss, K.; Troelsen, J. Sports facilities for all? The financing, distribution and use of sports facilities in Scandinavian countries. Sport Soc. 2010, 13, 643–656. [Google Scholar] [CrossRef]

- Hu, J.-L.; Kao, C.-H. Efficient energy-saving targets for APEC economies. Energy Policy 2007, 35, 373–382. [Google Scholar] [CrossRef]

- Honma, S.; Hu, J.-L. Total-factor energy efficiency for sectors in Japan. Energy Sources Part B Econ. Plan. Policy 2013, 8, 130–136. [Google Scholar] [CrossRef]

- Lee, Y.-C.; Hu, J.-L.; Kao, C.-H. Efficient saving targets of electricity and energy for regions in China. Int. J. Electr. Power Energy Syst. 2011, 33, 1211–1219. [Google Scholar] [CrossRef]

- Hu, J.L.; Li, Y.; Tung, H.J.; Feng, J.T. Total-factor output efficiencies of ASEAN airports. Airl. Econ. Asia 2018, 7. [Google Scholar] [CrossRef]

- The Sport Administration. Ministry of Education. Available online: https://www.sa.gov.tw/ (accessed on 21 June 2020).

- Lo, Y.C.; Fang, C.-Y. Facebook marketing campaign benchmarking for a franchised hotel. J. Contemp. Hosp. Manag. 2018, 30, 1705–1723. [Google Scholar] [CrossRef]

- Department of Health, Taipei City Government. Available online: https://health.gov.taipei (accessed on 28 June 2020).

- Department of Sports, Taipei City Government. Available online: https://sports.gov.taipei (accessed on 28 June 2020).

- Al Rabadi, W. The effect of using the aqua yoga exercises on the improvement of breathing and relaxation operations by beginners in swimming sport. Najah Univ. J. Res. 2009, 23, 527–564. Available online: http://hdl.handle.net/20.500.11888/2400 (accessed on 28 June 2020).

- Kantyka, J.; Herman, D.; Roczniok, R.; Kuba, L. Effects of aqua aerobics on body composition, body mass, lipid profile, and blood count in middle-aged sedentary women. Hum. Mov. 2015, 16, 9–14. [Google Scholar] [CrossRef]

- Wakefield, K.L.; Barnes, J.H. Retailing hedonic consumption: A model of sales promotion of a leisure service. J. Retail. 1996, 72, 409–427. [Google Scholar] [CrossRef]

- Gómez-Baya, D.; Calmeiro, L.; Gaspar, T.; Marques, A.; Loureiro, N.; Peralta, M.; Mendoza, R.; Gaspar de Matos, M. Longitudinal Association between Sport Participation and Depressive Symptoms after a Two-Year Follow-Up in Mid-Adolescence. Int. J. Environ. Res. Public Health 2020, 17, 7469. [Google Scholar] [CrossRef] [PubMed]

- Hayes, D.K.; Miller, A.A. Revenue Management for the Hospitality Industry; Wiley: Hoboken, NJ, USA, 2011; ISBN 9780470393086. [Google Scholar]

- Barney, J. Firm resources and sustained competitive advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Wernerfelt, B. The resource-based view of the firm: Ten years after. Strat. Manag. J. 1995, 16, 171–174. [Google Scholar] [CrossRef]

- McDougall, G.H.G.; Levesque, T. Customer satisfaction with services: Putting perceived value into the equation. J. Serv. Mark. 2000, 14, 392–410. [Google Scholar] [CrossRef]

- Osterwalder, A.; Pigneur, Y.; Clark, T. Business Model Generation: A Handbook for Visionaries, Game Changers, and Challengers; Wiley: Hoboken, NJ, USA, 2010; ISBN 9780470876411. [Google Scholar]

- Verma, V.K.; Chandra, B. An application of theory of planned behavior to predict young Indian consumers’ green hotel visit intention. J. Clean. Prod. 2018, 172, 1152–1162. [Google Scholar] [CrossRef]

- Hsu, B.Y.; Wu, Y.F.; Chen, H.W.; Cheung, M.L. How Sport Tourism Event Image Fit Enhances Residents’ Perceptions of Place Image and Their Quality of Life. Sustainability 2020, 12, 8227. [Google Scholar] [CrossRef]

- Waterlander, W.E.; Steenhuis, I.H.M.; de Vet, E.; Schuit, A.J.; Seidell, J.C. Expert views on most suitable monetary incentives on food to stimulate healthy eating. Eur. J. Public Health 2010, 20, 325–331. [Google Scholar] [CrossRef]

- Wang, Y.; Fesenmaier, D.R. Modeling Participation in an online travel community. J. Travel Res. 2004, 42, 261–270. [Google Scholar] [CrossRef]

- Kang, M.; Schuett, M.A. Determinants of sharing travel experiences in social media. J. Travel Tour. Mark. 2013, 30, 93–107. [Google Scholar] [CrossRef]

- Hoekman, R.; Breedveld, K.; Kraaykamp, G. Sport participation and the social and physical environment: Explaining differences between urban and rural areas in the Netherlands. Leis. Stud. 2017, 36, 357–370. [Google Scholar] [CrossRef] [Green Version]

- Roman, M.; Roman, M.; Niedziółka, A. Spatial Diversity of Tourism in the Countries of the European Union. Sustainability 2020, 12, 2713. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Input/Output | Mean | St Dev | Max | Min |

|---|---|---|---|---|

| Assets (NT$) | 70,305,603.08 | 103,449,855.38 | 404,522,793.00 | 8,758,876.00 |

| Operating Expenses (NT$) | 67,019,457.46 | 16,402,754.61 | 97,155,200.00 | 23,029,903.00 |

| Space (square-meter) | 18,168.07 | 15,358.13 | 66,310.00 | 6121.00 |

| Revenue (NT$) | 71,958,128.00 | 20,283,514.29 | 113,833,802.00 | 19,634,285.00 |

| No. of Visitors | 915,860.00 | 200,051.33 | 1,363,118.00 | 384,819.00 |

| No. | DMU | Score | Revenue | REV_Projection | Revenue_Surplus | RSTR (%) | No of Participant | NOP_Projection | NOP_Surplus | PSTR (%) |

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | SLC1_1st_yr | 0.94 | 68,650,453 | 73,343,428 | 4,692,975 | 6.8 | 878,885 | 938,966 | 60,081 | 6.8 |

| 2 | SLC2_1st_yr | 0.85 | 19,634,285 | 23,150,847 | 3,516,562 | 17.9 | 384,819 | 453,741 | 68,922 | 17.9 |

| 3 | SLC3_1st_yr | 0.91 | 94,788,891 | 104,285,864 | 9,496,973 | 10.0 | 1,227,955 | 1,350,985 | 123,030 | 10.0 |

| 4 | SLC4_1st_yr | 0.88 | 60,499,744 | 68,964,332 | 8,464,588 | 14.0 | 773,922 | 882,202 | 108,280 | 14.0 |

| 5 | SLC5_1st_yr | 0.95 | 59,596,290 | 62,697,830 | 3,101,540 | 5.2 | 776,276 | 816,675 | 40,399 | 5.2 |

| 6 | SLC6_1st_yr | 0.96 | 85,022,564 | 89,030,527 | 4,007,963 | 4.7 | 908,487 | 1,000,083 | 91,596 | 10.1 |

| 7 | SLC7_1st_yr | 0.89 | 87,747,697 | 98,173,452 | 10,425,755 | 11.9 | 1,021,488 | 1,163,509 | 142,021 | 13.9 |

| 8 | SLC8_1st_yr | 1.00 | 61,956,210 | 61,956,210 | 0 | 0.0 | 996,361 | 996,361 | 0 | 0.0 |

| 9 | SLC9_1st_yr | 0.95 | 81,136,425 | 85,621,758 | 4,485,333 | 5.5 | 1,005,821 | 1,061,424 | 55,603 | 5.5 |

| 10 | SLC10_1st_yr | 1.00 | 113,833,802 | 113,833,802 | 0 | 0.0 | 1,298,340 | 1,298,340 | 0 | 0.0 |

| 11 | SLC11_1st_yr | 1.00 | 64,885,634 | 64,885,634 | 0 | 0.0 | 1,053,550 | 1,053,550 | 0 | 0.0 |

| 12 | SLC12_1st_yr | 0.90 | 65,644,648 | 73,109,258 | 7,464,610 | 11.4 | 736,114 | 887,867 | 151,753 | 20.6 |

| 13 | SLC1_2nd_yr | 0.96 | 72,324,693 | 75,247,968 | 2,923,275 | 4.0 | 944,480 | 982,655 | 38,175 | 4.0 |

| 14 | SLC2_2nd_yr | 0.86 | 45,050,754 | 52,403,997 | 7,353,243 | 16.3 | 751,131 | 873,732 | 122,601 | 16.3 |

| 15 | SLC3_2nd_yr | 1.00 | 62,206,105 | 62,206,105 | 0 | 0.0 | 807,004 | 807,004 | 0 | 0.0 |

| 16 | SLC4_2nd_yr | 0.92 | 59,374,530 | 64,308,039 | 4,933,509 | 8.3 | 858,959 | 930,331 | 71,372 | 8.3 |

| 17 | SLC5_2nd_yr | 0.93 | 57,522,525 | 61,710,227 | 4,187,702 | 7.3 | 788,819 | 846,246 | 57,427 | 7.3 |

| 18 | SLC6_2nd_yr | 0.99 | 81,487,201 | 82,691,671 | 1,204,470 | 1.5 | 903,156 | 944,524 | 41,368 | 4.6 |

| 19 | SLC7_2nd_yr | 0.89 | 85,831,468 | 95,943,234 | 10,111,766 | 11.8 | 976,590 | 1,148,279 | 171,689 | 17.6 |

| 20 | SLC8_2nd_yr | 0.93 | 59,712,861 | 64,108,947 | 4,396,086 | 7.4 | 848,838 | 911,330 | 62,492 | 7.4 |

| 21 | SLC9_2nd_yr | 0.98 | 84,033,418 | 85,545,537 | 1,512,119 | 1.8 | 961,653 | 978,957 | 17,304 | 1.8 |

| 22 | SLC10_2nd_yr | 0.99 | 112,961,762 | 113,546,085 | 584,323 | 0.5 | 1,363,118 | 1,370,169 | 7,051 | 0.5 |

| 23 | SLC11_2nd_yr | 1.00 | 68,878,589 | 68,878,589 | 0 | 0.0 | 846,530 | 846,530 | 0 | 0.0 |

| 24 | SLC12_2nd_yr | 0.91 | 74,214,523 | 81,472,345 | 7,257,822 | 9.8 | 868,344 | 1,001,975 | 133,631 | 15.4 |

| 25 | SLC1_3rd_yr | 0.98 | 79,296,794 | 80,759,183 | 1,462,389 | 1.8 | 1,003,754 | 1,022,265 | 18,511 | 1.8 |

| 26 | SLC2_3rd_yr | 1.00 | 46,018,650 | 46,018,650 | 0 | 0.0 | 1,042,918 | 1,042,918 | 0 | 0.0 |

| 27 | SLC3_3rd_yr | 0.75 | 71,463,778 | 95,562,528 | 24,098,750 | 33.7 | 826,614 | 1,105,362 | 278,748 | 33.7 |

| 28 | SLC4_3rd_yr | 0.92 | 58,837,222 | 63,762,977 | 4,925,755 | 8.4 | 853,260 | 924,694 | 71,434 | 8.4 |

| 29 | SLC6_3rd_yr | 0.79 | 69,584,894 | 87,687,215 | 18,102,321 | 26.0 | 929,058 | 1,170,750 | 241,692 | 26.0 |

| 30 | SLC7_3rd_yr | 0.74 | 66,857,793 | 90,671,942 | 23,814,149 | 35.6 | 768,160 | 1,067,986 | 299,826 | 39.0 |

| 31 | SLC9_3rd_yr | 1.00 | 87,996,020 | 87,996,020 | 0 | 0.0 | 984,126 | 984,126 | 0 | 0.0 |

| 32 | SLC10_3rd_yr | 0.97 | 121,004,391 | 124,715,882 | 3,711,491 | 3.1 | 1,274,288 | 1,441,609 | 167,321 | 13.1 |

| 33 | SLC11_3rd_yr | 1.00 | 74,119,532 | 74,119,532 | 0 | 0.0 | 877,524 | 877,524 | 0 | 0.0 |

| 34 | SLC12_3rd_yr | 0.92 | 75,773,661 | 82,080,834 | 6,307,173 | 8.3 | 1,003,593 | 1,087,129 | 83,536 | 8.3 |

| Average | 0.93 | 72,880,818 | 78,249,719 | 5,368,901 | 8.03 | 927,763 | 1,007,935 | 80,172 | 9.34 |

| Variables | Original | Model_1 | Model_2 | Model_3 | Model_4 | Model_5 |

|---|---|---|---|---|---|---|

| Inputs | ||||||

| Assets (NT$) | V | V | V | V | V | |

| Operating Expenses (NT$) | V | V | V | V | V | |

| Space (square-meter) | V | V | V | V | V | |

| Outputs | ||||||

| Revenue (NT$) | V | V | V | V | V | |

| No. of Visitors | V | V | V | V | V | |

| Spearman correlation_ Original Model | 1 | 0.848 ** | 0.382 ** | 0.996 ** | 0.576 ** | 0.831 ** |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Fang, C.-Y.F. Perspective of Local Government on the Performance Assessment of District Sports and Leisure Centers. Sustainability 2020, 12, 9094. https://doi.org/10.3390/su12219094

Fang C-YF. Perspective of Local Government on the Performance Assessment of District Sports and Leisure Centers. Sustainability. 2020; 12(21):9094. https://doi.org/10.3390/su12219094

Chicago/Turabian StyleFang, Chin-Yi Fred. 2020. "Perspective of Local Government on the Performance Assessment of District Sports and Leisure Centers" Sustainability 12, no. 21: 9094. https://doi.org/10.3390/su12219094

APA StyleFang, C.-Y. F. (2020). Perspective of Local Government on the Performance Assessment of District Sports and Leisure Centers. Sustainability, 12(21), 9094. https://doi.org/10.3390/su12219094