1. Introduction

Due to climate change, natural catastrophes such as flooding are likely to increase in frequency and severity in the future [

1]. For 2019 alone, worldwide economic damage from flooding is estimated at

$82 billion [

2]. However, it is found that the impact of flooding disproportionally affects the world’s poorer regions [

3,

4]. Furthermore, it is argued that the recovery process after a flood can reinforce inequality, as more wealthy households can better access recovery mechanisms, e.g., insurance coverage [

5], which allows them to get back on their feet quicker than those without. Flood insurance helps the insured to recover because it provides a contractual right for compensation after a flood. The resulting indemnity payments can enable a faster recovery, for example to repair damaged property, which may exceed the immediate available resources of a household [

6,

7]. Flood insurance can spread the risk of a large randomly occurring disaster over many households that are paying premiums, which makes a single household less sensitive to income shocks [

8].

In addition to financing recovery, flood insurance systems can also be beneficial for limiting overall risk. For instance, by differentiating premiums according to the risk faced, a price signal of risk is generated. This price signal can encourage households to move away from—or avoid locating in—high-risk areas, or implement risk reduction measures such as dry- or wet-flood-proofing in exchange for premium discounts [

6,

9]. Risk-based premiums are therefore often considered to limit moral hazard, which is the behavioral response of insured individuals to limit effort to reduce risk. However, in the context of natural hazard insurance, evidence suggests that moral hazard is not apparent [

10]. In private flood insurance systems, the premiums are often determined by the insurers themselves based on risk estimates from catastrophe models [

11], like we use in our study for estimating local flood risk as well as for the risk reduction that can be obtained from flood-proofing measures by households. Alternatively, information from catastrophe models can be used by public authorities to regulate flood insurance premiums and premium discounts for risk reduction, as is common practice in public or public–private flood insurance systems. For example, in the National Flood Insurance Program in the US, premiums depend on flood risk zones and policyholders receive lower premiums when they elevate their home [

12].

However, since risk-based premiums initially increase the cost of insurance in areas with high flood risk, the price signal may discourage households from obtaining insurance coverage. This process will be enhanced by climate change, and may lead to increasing social equity issues [

7]. For example, in the US, it is found that risk-based premiums disproportionally impact low-income and minority populations [

13], which can limit fair access to recovery mechanisms. Furthermore, the demand for insurance coverage can decline when premiums increase more rapidly than the perceptions of flood risk by households, which is likely to occur due to rising flood risk as a result of climate change. The result is a widening divergence between what households are willing to pay for insurance, based on their subjectively perceived threat of flooding, and what insurers must charge to remain in business [

14]. This is a recognized issue regarding natural disaster insurance demand, because individuals tend to underestimate risk of events that occur with a low probability, but cause high damage, as is the case for flood risk [

15].

Diminishing demand for flood insurance coverage can enlarge the burden of financing the recovery of flood damage from other sources, such as governmental compensation or private savings, which is especially problematic in the face of rising flood risk. These alternative forms of coverage are often considered inadequate, since for example government compensation, unless made explicit in law, leads to ambiguity regarding the compensation households receive for flood damage and results in unstable government budgets [

16,

17]. Besides this, private savings can be insufficient due to underestimation of flood risk by households, budget constraints [

15], or competing objectives for how these savings should be used.

In a worst-case scenario, the aforementioned inequalities and the resulting lack of insurance uptake may result in a collapse of the flood insurance market in certain areas [

18]. Such a development can also be interpreted as a climate induced socio-economic tipping-point, which is defined as a climate-change induced, abrupt change of a socio-economic system, into a new, fundamentally different state [

19]. In this study, we examine impacts of the interaction between climate- and socio-economic change on the sustainability of flood insurance systems. Polhill et al. [

20] note that while much attention has been placed upon tipping-points within ecological or economic systems independently, analyses of joint socio-environmental tipping-points are scarce, such as the impact of climate change on insurance systems. The relevance of this research topic is motivated by the observation that near collapses, or major reforms, of insurance systems have already been observed in practice. For example, in the UK, where the autumn floods of 2000 marked the potential end of the ‘universally available’ flood insurance coverage [

21]; or in Germany, where the floods of 2002 caused premiums to rise up to 50% and flood insurance penetration to decline by 10% to 20% in some areas [

18]. Such sharp declines in insurance coverage have large negative welfare consequences, since impacts of uncovered flood damage have been associated with (mental) health problems [

22], low regional economic growth rates [

23], and social segregation of income groups [

24].

The objective of this study is to identify areas where the functioning of (regional) private flood insurance markets could be hampered by rising unaffordability and declining demand for flood insurance, and to assess under which conditions of climate- and socio-economic change this occurs. We identify areas where the aforementioned problems with uncovered flood damage are the greatest and examine how policy adaptation can improve future resilience of flood insurance systems. Studied policy changes aim to improve affordability and insurance uptake, to secure the continued provision of flood insurance, and to suitably alter the financial burden upon households and governments. We assess measures ranging from insurance uptake requirements, introducing the government as a reinsurer, and a system with limited risk-based premiums where risk is shared amongst households to a certain degree [

25].

Our study uses an adapted version of the “Dynamic Integrated Flood and Insurance” (DIFI) model, which is a partial economic equilibrium model that integrates flood risk, household behavior, and the insurance sector of different flood insurance systems for EU countries. We build upon the previous work in Hudson et al. [

26] who examine desirable reforms of EU flood insurance systems based on national level DIFI output under a single future risk scenario, using a multi-criteria analysis. Here, we replace the flood risk assessment module in the previous DIFI model version with a more extensive and detailed flood risk dataset, which enables us to project regional inequalities in the impacts of climate change on existing flood insurance systems. While Hudson et al. [

26] projected future flood risk under a high end climate change scenario combined with an average of socio-economic scenarios, the augmented DIFI model makes use of future risk projections under a variety of scenario combinations of climate and socio-economic change. This means that our approach allows for identifying specific future risk conditions under which the functioning of flood insurance systems is impaired. Moreover, we assess relevant DIFI model outcomes at a more spatially detailed regional level instead of the national level and present a more detailed analysis of the affordability and demand of flood insurance.

In the following section of the paper, the modelling approach will be explained, after which the results are presented, and a conclusion is given including policy recommendations.

2. Model Description

The DIFI model combines a riverine flood risk model with an insurance sector and household behavior model, in order to project future levels of unaffordability of premiums and insurance uptake under various existing and proposed flood insurance market structures in Europe. Each component of the model is described here in a separate section.

Section 2.1 explains how flood risk is estimated;

Section 2.2 describes how flood risk affects insurance premiums for various insurance schemes; and

Section 2.3 defines the behavioral model by which unaffordability and uptake of insurance is determined. A list of variables and their definitions that are used in this section is provided in

Appendix G.

This study uses an adapted version of the “Dynamic Integrated Flood Insurance” (DIFI) model developed by Hudson et al. [

26]. The most notable change is the application of more detailed flood risk and socio-economic data, including multiple scenarios, which enables a more elaborate analysis of the occurrence of tipping-points for flood insurance in the EU. As we do not analyze the full spectrum of results produced by the DIFI model, we refer to the article by Hudson et al. [

26] for a full model description. In this section, we specifically describe the process of obtaining unaffordability and market penetration projections that result from increasing flood risk under various flood insurance arrangements and climate change scenarios.

2.1. Flood Risk Model

In the flood risk model, the flood hazard (that is the probability of a flood of a certain magnitude occurring) is combined with the potential impact that can occur from flooding, which enables the estimation of flood risk, expressed as expected annual damage (EAD). EAD is important for the calculation of insurance premiums, as the insurance industry requires averaged expected damage values in order to spread flood risk over time using annual premium income. The data used to calculate the EAD in the current DIFI model version 2.0 are collected from the GLOFRIS model cascade [

27,

28], which is a change from DIFI model version 1.0, where data are obtained from the LISFLOOD model [

29]. An advantage of this change is that the GLOFRIS model provides data using various combinations of climate and socio-economic scenarios, which enables the comparison of outcomes across a range of scenarios and controlling for uncertainty that underlies future projections of climate- and socio-economic change. An extensive validation exercise of the GLOFRIS model has been included in Ward et al. [

27], which showed that the overall performance of the model is adequate and closely matches the LISFLOOD model.

The flood hazard is calculated in the GLOFRIS model for various representative concentration pathways (RCPs), which are scenarios for future levels of greenhouse concentrations. The RCPs are expressed as possible radiative forcing values in 2100, and existing trajectories include 2.6, 4.5, 6.0, and 8.5 W/m

2, respectively [

30]. The model simulates water levels that occur with certain probabilities, which are expressed as return periods (2, 5, 10, 25, 50, 100, 250, 500, and 1000 years). For the baseline, the water level per river basin corresponding to each return period is determined by forcing the hydrological model PCR-GLOBWB [

31,

32] with meteorological fields (precipitation, temperature, radiation), using annual time-series data of maximum flood volumes for 1960–1999 from the EU-WATCH project [

33]. For future projections (2030, 2050, and 2080) the model is run using bias-corrected meteorological data from the CMIP5 global circulation models (GCMs) [

34], provided by the ISIMIP project [

35].

The flood hazard is combined with exposure and vulnerability data in order to derive the potential impact it can cause [

36]. Specifically, inundation maps are overlain with a land use map that identifies urban density, which for the baseline is taken from the HYDE database [

37]. Current and future population data is taken from Huijstee et al. [

38]. As flood insurance is usually organized on a household level, we estimate the number of exposed households by dividing the population by an average number of individuals per household on a country level, which is taken from Eurostat [

39]. The economic value of exposed assets is dependent on national GDP per capita in 2010 [

40]. Future simulations of built-up area are taken from Winsemius et al. [

28], which uses data from the Shared Socio-economic Pathways (SSPs) [

41], taken from IIASA’s SSP database. Furthermore, the economic values of urban areas are determined by adjusting the GDP per capita of exposed population according to the SSP scenarios, which is also taken from the SSP database.

The potential damage a flood event can cause for each urbanized grid cell is then computed based on the extend of inundation, urban density, economic value, and global flood depth–damage functions per occupancy type taken from Huizinga et al. [

42]. The global flood depth–damage functions account for the vulnerability aspect of the flood risk model and consist of stage–-damage curves, which project the impact of flood depth, and is based on the JRC global functions database. At this point, as is common practice, we take the average over the GCMs in order to limit biases originating from these models [

43].

It is assumed that, in our modeling scheme, inundation only takes place when riverine water levels exceed the protection standards, i.e., when the protection standards of a dike are supposed to withstand riverine water levels of a 100-year return period, water levels of a return period lower than 100 years cannot lead to flooding. Regional protection standards are taken from the FLOPROS database [

44], and are assumed to remain constant through time in regions where flood hazard increases. This means that, when flood hazard increases, investments are made in protection standards in order to account for rising water levels per return period, whereas in the case that flood hazard decreases, as a result of a dryer climate, the current protection standards will become higher in the future. In order to simulate the probability of the exceedance of protection standards, a damage probability curve is fitted based on a power-law function. After this, the DIFI model uses a Monte Carlo approach in order to produce estimates of EAD and its variance, by drawing random return periods per region and comparing it to the current and future protection standards.

For further steps, the derived flood risk estimates are aggregated to the NUTS2 level, which is a classification of geographical regions in EU-countries and the UK. For certain countries, the NUTS2 regions comprise of provinces, such as in the Netherlands, Spain, and Italy, whereas for the Baltic states the NUTS2 regions make up the individual countries (Eurostat). Consistent with Hudson et al. [

26], the flood risk module of the DIFI model focuses on households located in 1/100-year flood zones. These high-risk flood zones are most relevant for the focus of this study, since issues with affordability of premiums are most likely to occur, and the relevance of obtaining sufficient flood insurance coverage is highest in these areas. For example, in the US, the 1/100-year flood zones are designated by FEMA (Federal Emergency Management Agency) as “base flood” zones, and it is for households located in these regions that the flood insurance coverage debate is focused on most. For example, flood insurance coverage is mandatory for homeowners located in these regions with a mortgage from a federal lending institution [

45]. While, traditionally in the UK, areas within the 1/75-year floodplain is the demarcation of universal insurance coverage.

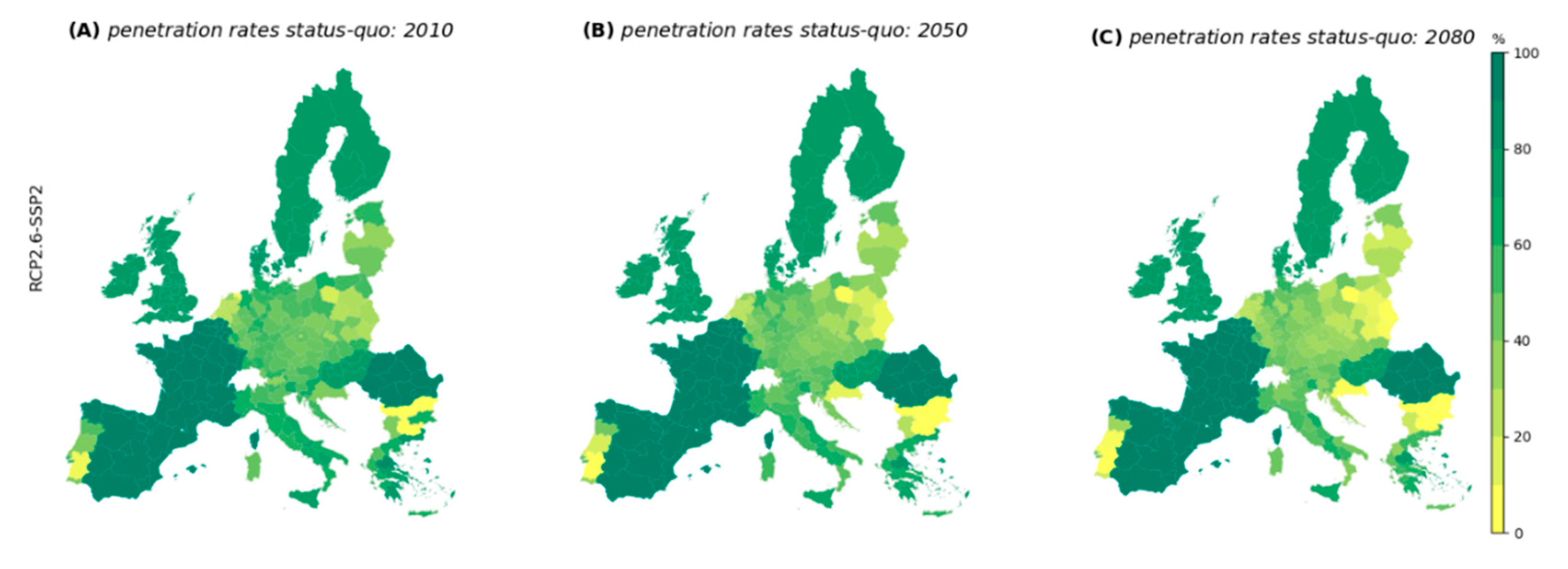

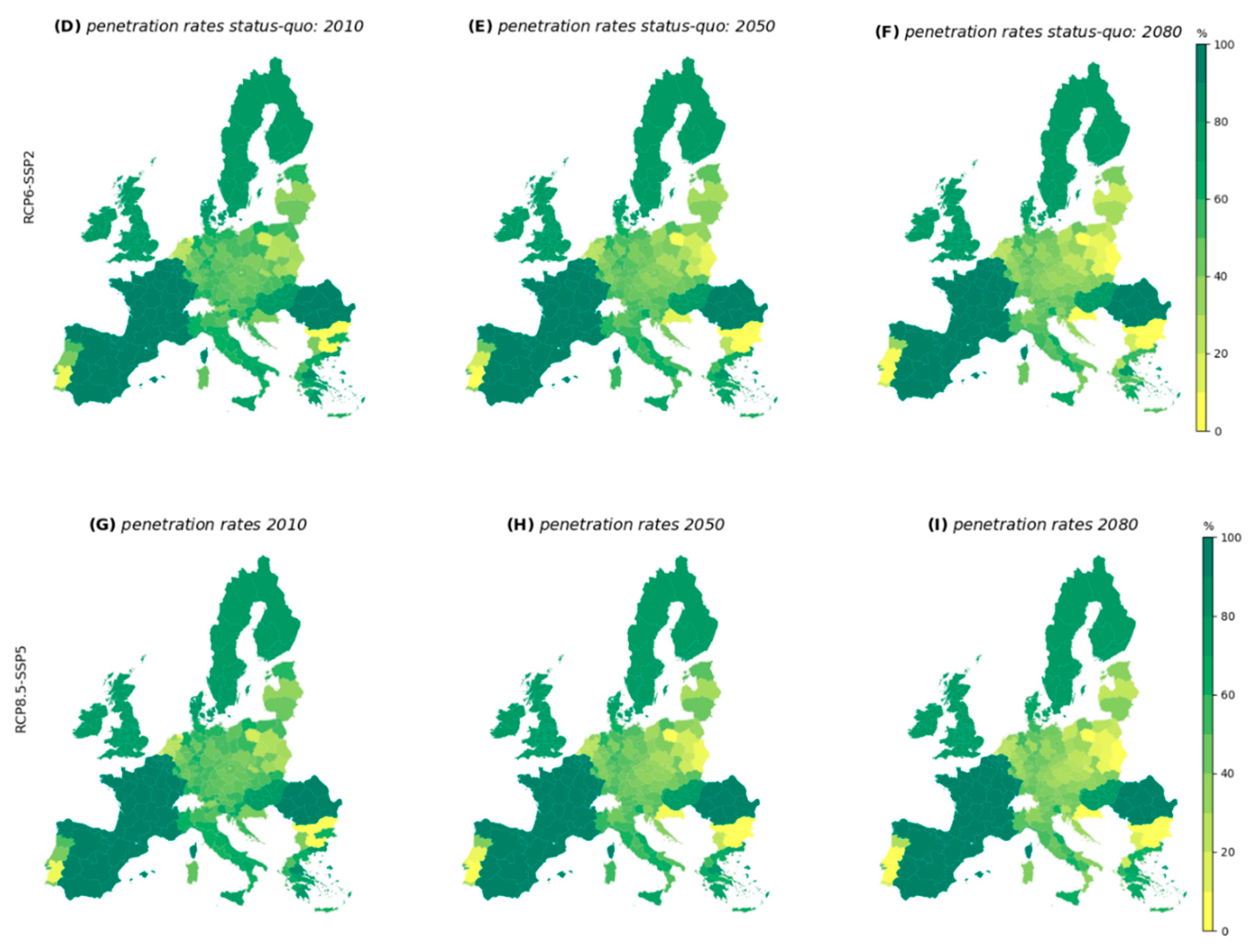

Future climate events do not have an exact known probability distribution, which means that they can be characterized as being uncertain. We account for the uncertainty of future flood risk by assessing multiple scenarios of climate- and socio-economic change. In total, six RCP-SSP combinations are used, in order to examine a plausible range of potential future developments of flood risk. The “middle of the road” SSP2 scenario is assessed in combination with RCP2.6 and RCP6.0, in order to observe differences that arise from maintaining stringent greenhouse gas mitigation efforts (RCP2.6) versus a scenario that is judged to be realistic in the absence of mitigation efforts (RCP6.0).

Furthermore, scenario combinations RCP8.5-SSP3 and RCP2.6-SSP1 are assessed, which are included to compare extreme scenarios of climate risk development. The former combines the highest level of greenhouse gas emissions with an SSP scenario where mitigation and adaptation challenges are deemed difficult to meet due to regional conflicts and low technological advances [

41], while RCP2.6-SSP1 has a strong emphasis on global sustainability.

Finally, RCP8.5-SSP5 is included in order to assess outcomes of differing socio-economic paths under a high climate-change scenario. In particular, SSP5 is considered a scenario representative of business-as-usual, with high socio-economic growth and a high societal dependence on fossil fuels [

46]. We select RCP4.5-SSP2 in order to observe the impact of a scenario broadly aligned with the “Nationally Determined Contributions” (NDCs) of the Paris Climate Agreement [

47]. The comparison of these scenarios provides insight into the potential consequences of failing to meet the climate change mitigation targets that underlie RCP4.5.

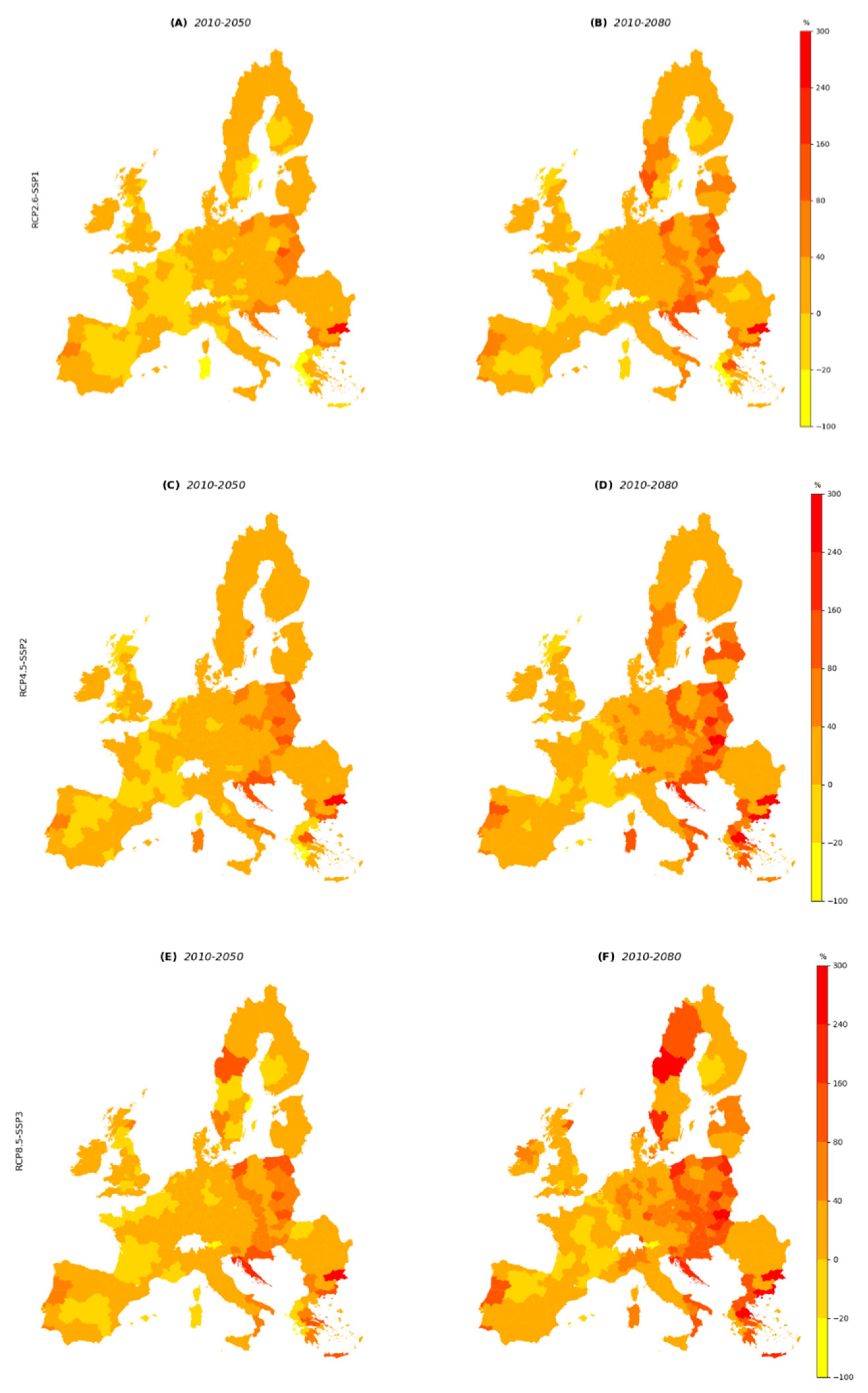

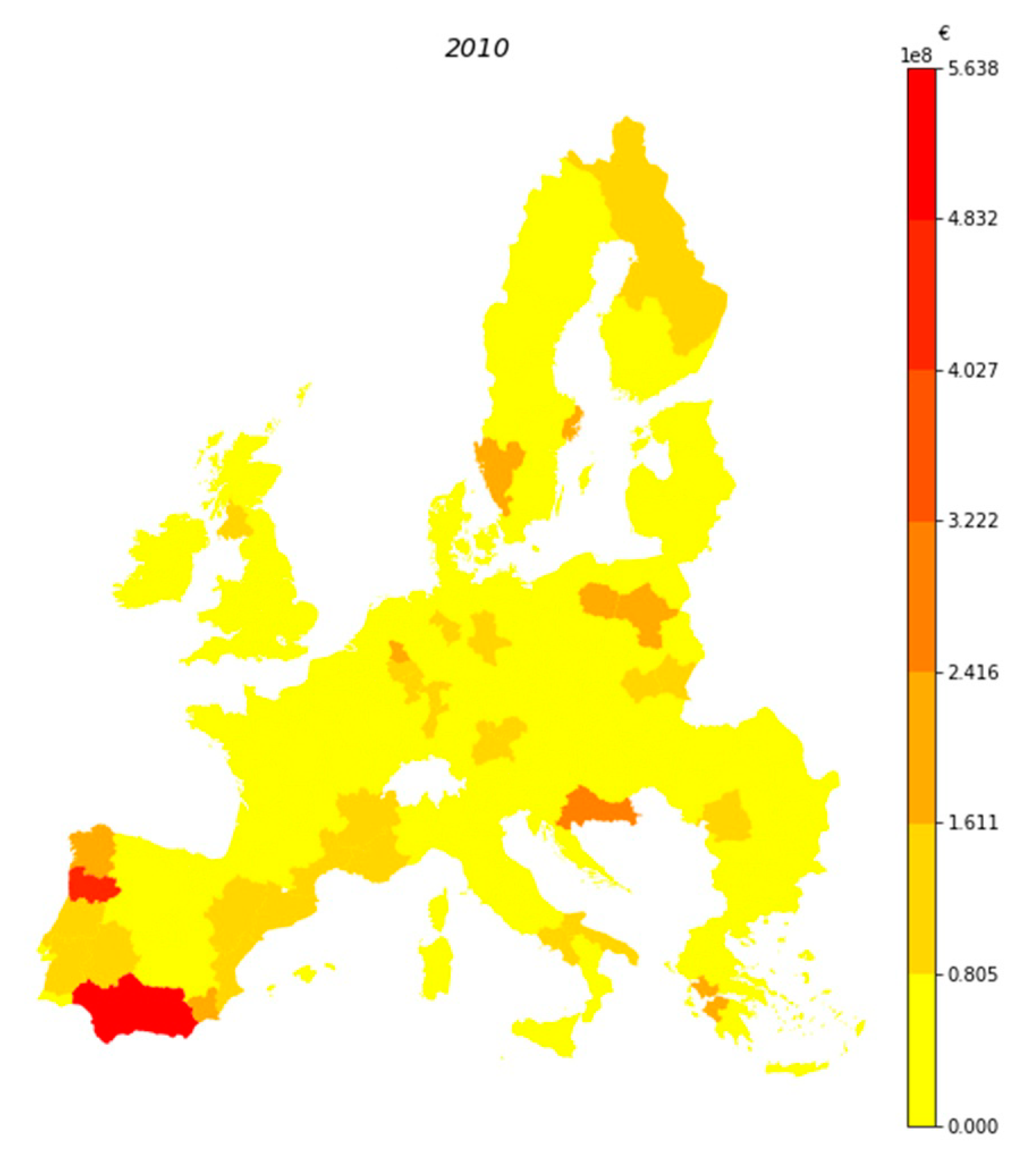

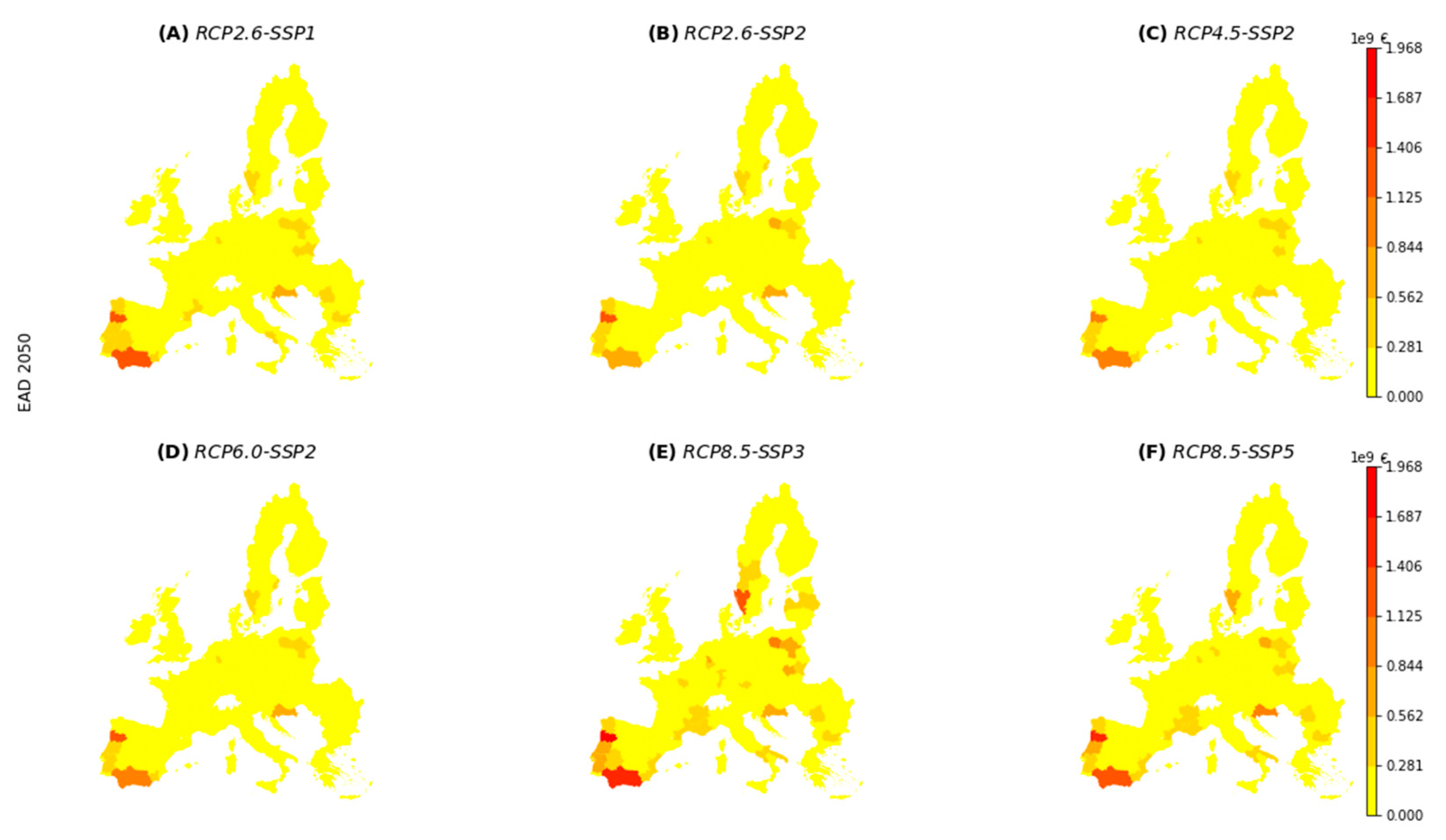

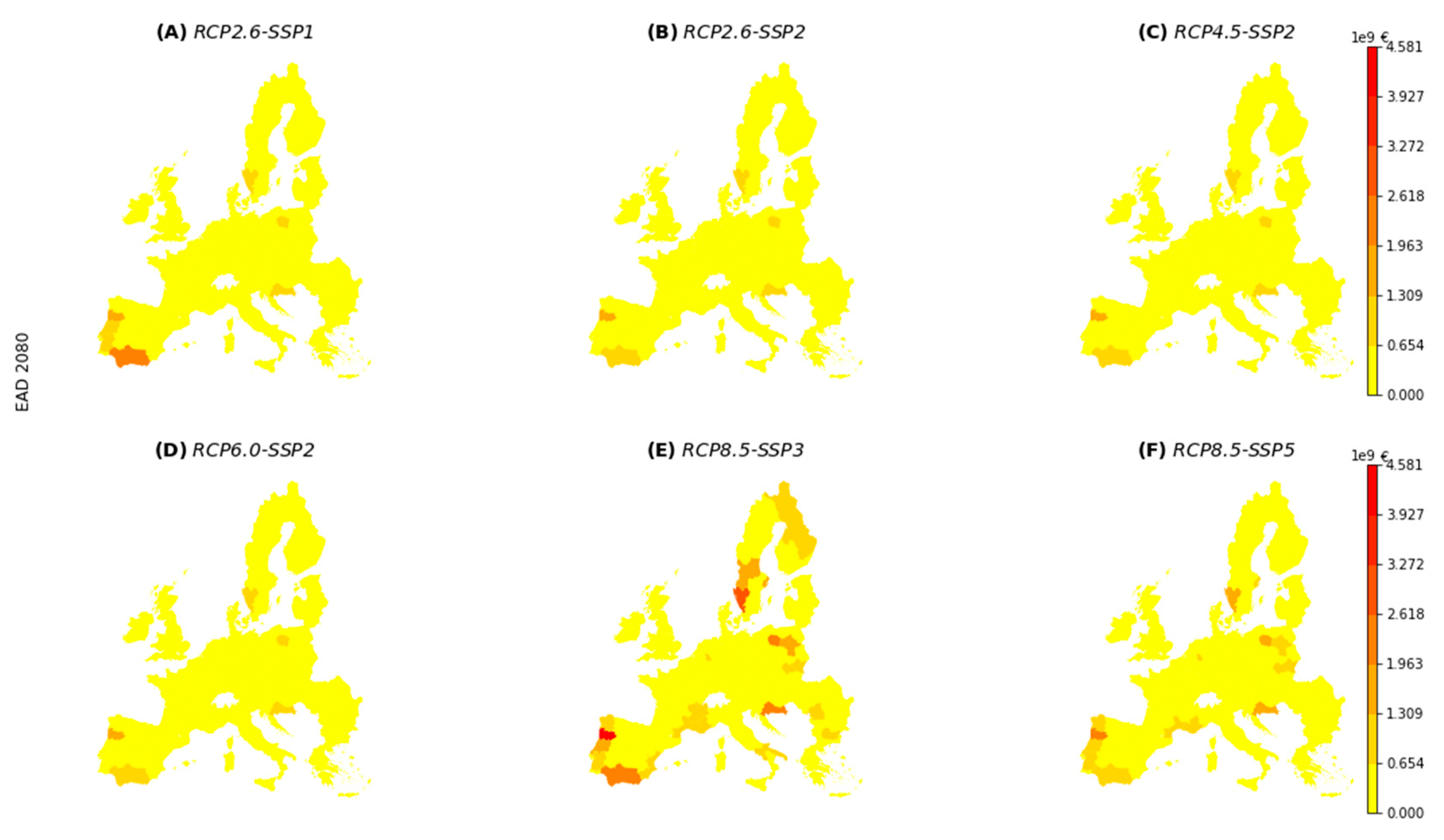

Baseline flood risk and projections of future EAD under the considered scenarios are shown in

Appendix C. In

Figure A3, it can be seen that riverine flood risk in 2010 is highest in southern Spain and northern Portugal, followed by regions in Poland, Croatia, Sweden, and the Mediterranean coast of France and Spain. The projected development of EAD until 2050 and 2080 are displayed in

Figure A4 and

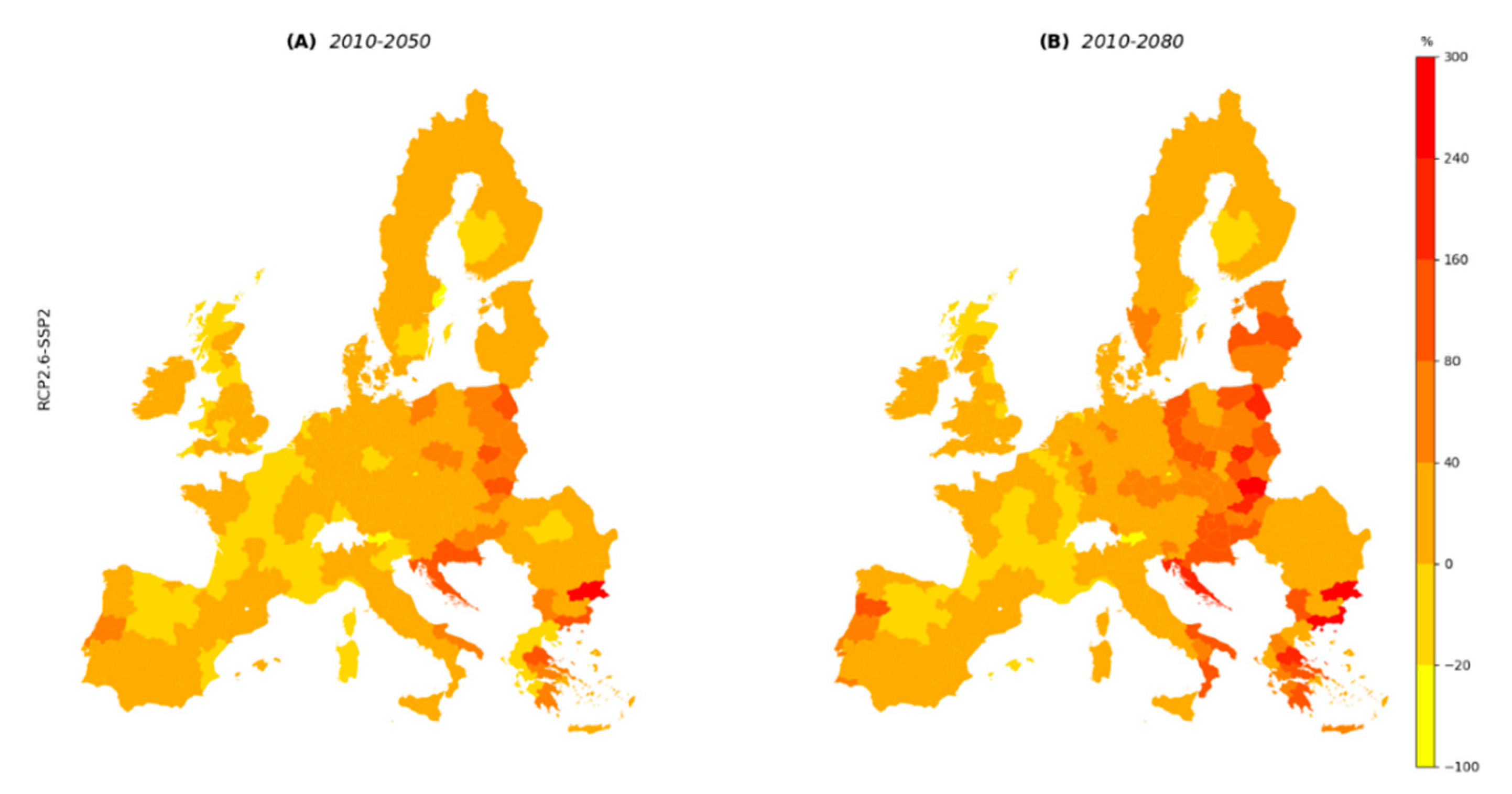

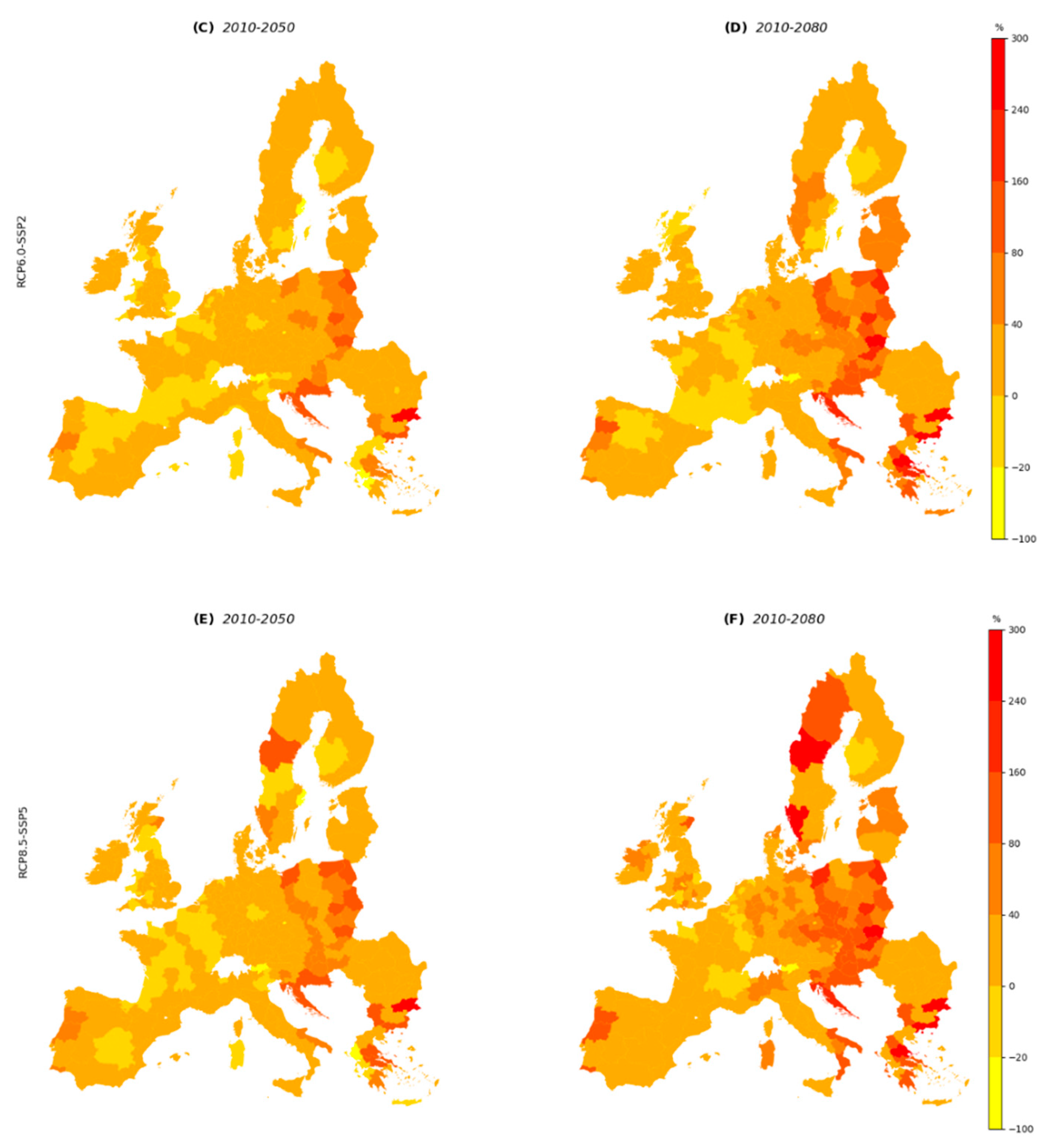

Figure A5 for the six scenarios considered in this study. Flood risk grows most rapidly under the high-end scenarios displayed in panels E and F, while not much difference can be observed between the remaining scenarios. Within the high-end climate change scenario RCP8.5, the highest impact on EAD is projected for the combination with SSP3.

2.2. Insurance Sector Model

The expected annual loss and volatility of losses are converted into insurance premiums for six stylized insurance market structures, which are derived in Hudson et al. [

26] and partly based on Paudel et al. [

48] and Paudel et al. [

25]. Importantly, the current analysis is targeted at home insurance and disregards, for example, flood insurance for businesses or agriculture. The insurance market structures differ in terms of various market features such as purchase requirements, premium differentiation based on risk, and reinsurance arrangements. Selected European countries are allocated to one of these stylized structures, based on their current flood insurance arrangement. Specifics concerning the included stylized insurance systems are presented in

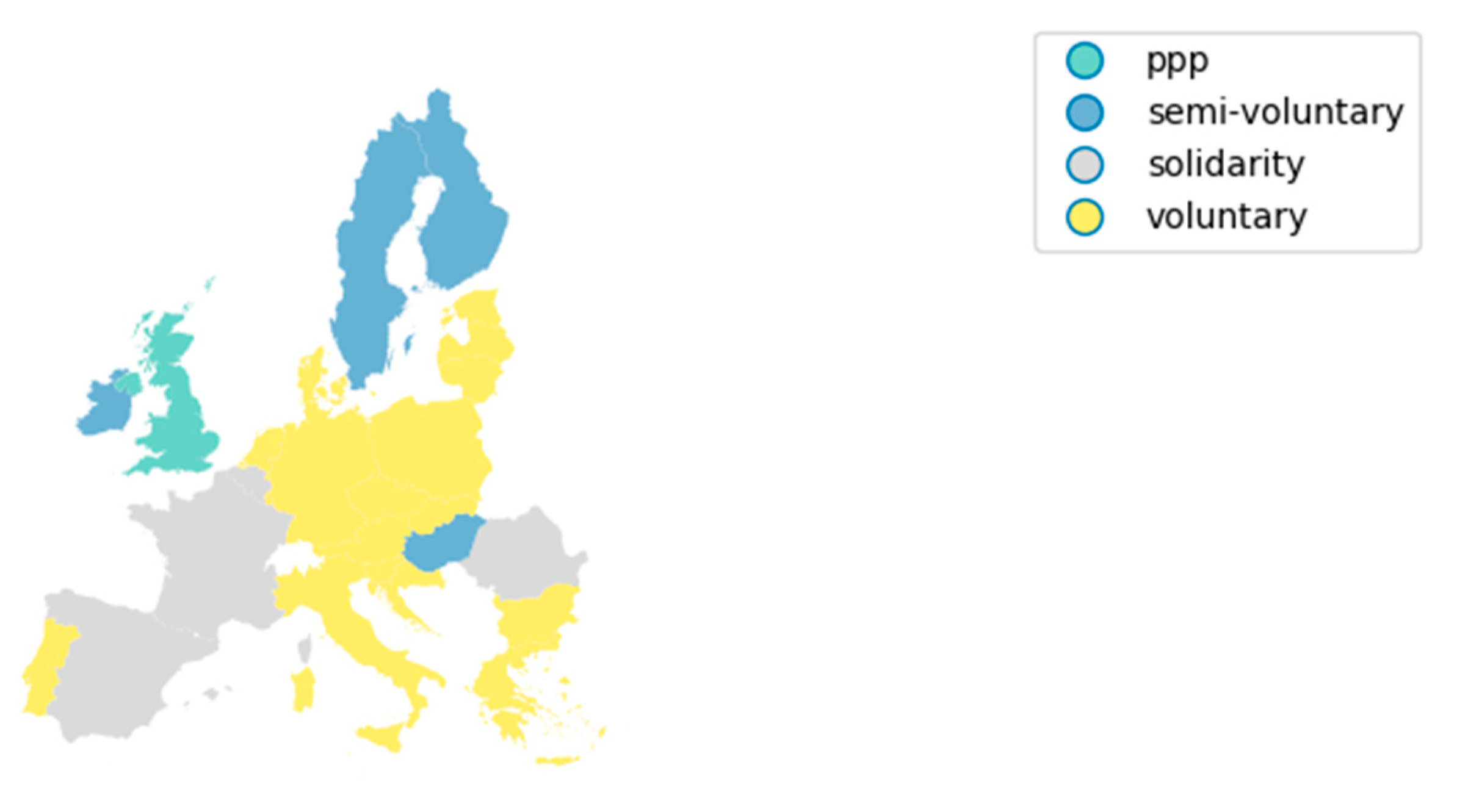

Table 1. The details of insurance arrangements for individual European countries differ from the stylized versions presented here. However, the most important characteristics that distinguish each system are captured by our model, which enables the comparison of the capacity of different insurance arrangements to deal with issues posed by climate change. For example, analyzed differences of flood insurance systems include risk-based premiums versus premiums that are unconnected to risk, voluntary versus mandatory insurance uptake, or a public versus a private reinsurance arrangement.

Each modelled insurance market structure has the same co-insurance style deductible of 15% of claimed loss, which is based on observed deductible levels reported in Paudel et al. [

48]. Therefore, the expected annual loss transferred to the insurer is determined by taking the mean of 85% of the calculated loss for each region, and the volatility of losses is determined by the standard deviation of the transferred loss. The following section explains in detail how the premium is determined for the voluntary insurance system. It can be seen in

Table 1 that this stylized insurance system is considered representative for most European countries. Furthermore, the map in

Appendix D visualizes the allocated stylized insurance systems per country. As this system is also most important for the current analysis on insurance tipping-points, due to its risk-based premiums and voluntary insurance uptake, we discuss its premium structure here and refer to

Appendix A for a description of the premium structures for the remaining insurance systems. We do not explicitly model insolvency of insurers, but we do account for the practice to minimize this risk through reinsurance. Within the EU there is strict supervision regarding the solvency of insurers covering natural or man-made disasters (see [

49] for an overview of this regulatory oversight from the EU). As a result, presently the risk of bankruptcy of individual insurers is unlikely. In particular, the annual insolvency probability should be below 0.5% to comply with the Solvency II European Union legislation.

The text below is based upon that presented in Hudson et al. [

26] and re-presented here in order to briefly describe the model used, of which more details can be found in Hudson et al. [

26].

Voluntary or Semi-Voluntary Market (M2, M3)

Equation (1) shows how the premium is determined for the (semi-)voluntary insurance systems, which follows a flood insurance pricing rule used in various studies [

48,

50,

51]. In this system, there is a full risk signal from insurers to policyholders. The premium is determined at the NUTS2-level hence the subscript

j is introduced, which represents that geographic level. This implies that expected flood damage (

) and the deductible (

) are modelled per high-risk household on the NUTS2-level at time

t.

Specific cost loading factors are introduced for the proportion of risk that is covered by the private primary insurer, or the private reinsurer.

is the cost-loading factor for the primary insurer, which is implemented on country-level as indicated by subscript

c;

is the cost-loading factor for the reinsurer; the superscript

RR indicates the risk transferred from the insurer to the reinsurer;

r, is the risk aversion coefficient of the primary insurers and reinsurers;

, is the volatility of flood damage within a quantile range that is considered insurable [

25].

The loading factors for the primary insurer and reinsurer are determined as follows. For the private primary insurers Bertrand competition is assumed, which means that no company can charge a profit-loading factor. The cost-loading factor for private reinsurers is fixed at

, as the market tends to be more concentrated [

26]. The cost-loading factors are determined on a country-level based on OECD insurance statistics of costs of non-life insurance policies, as is described in detail in Hudson et al. [

26].

The final premiums faced by individuals

is determined as the baseline average risk per household (indicated by subscript

i) for a certain NUTS2 region, which is reduced by the premium discount (

ERDRR) that is determined by the implementation of risk reduction measures (Equation (2)).

2.3. Household Behavior Model

The estimated premiums for the included insurance market structures are then fed into a household behavior model, which projects flood insurance demand, and allows us to derive the level of unaffordability and market penetration, which are the main interest for this study. Moreover, the household behavior module of the DIFI model also involves household decisions to apply risk reduction measures (see Hudson et al., [

26] for details).

The behavioral model representing households at risk of flooding is based on subjective expected utility theory [

52]. The decision to obtain insurance coverage is only made when uptake is voluntary. Each household included in the model purchases insurance if that option yields the highest expected utility, or chooses to remain uninsured if that expected utility is higher instead, as represented by the two elements in Equation (3). The first element

expresses the expected utility of not being insured, in which case the household is faced with uncompensated flood losses with probability

p. The second element

expresses the expected utility of being insured, where the household pays the premium and faces the deductible in the case of flood damage. New terms in Equation (3) includes

Wi,j,t, which symbolizes estimated wealth of household

i in region

j at time

t. Wealth is determined as a fixed ratio of income, which is estimated by taking households’ stock of financial assets as a percentage of disposable income, as indicated by Eurostat [

53].

αi represents the risk aversion of a household and is fixed at

αi = 1, resulting in a logarithmic utility function. Subjective flood occurrence perceptions are included by modelling households to consider flood losses over the probability range [0,

], where

where

is the regional flood protection standard and with

being a distribution of subjective flood occurrence probabilities (see Hudson et al. [

26] for a detailed discussion on how this is done). Therefore, households’ subjective flood probabilities differ from the objective probability determined in the flood risk module.

is a parameter between 0 and 1, which represents how the perceived flood impact differs from the modelled flood impact, which is similarly taken from a generalized Pareto distribution, calibrated using data about flood insurance uptake from the German Insurance Association [

54].

The household, moreover, faces a budget constraint, where it is assumed that no insurance is purchased when the premium is deemed unaffordable, as shown in Equation (4). This budget constraint follows the theory of hierarchy of human needs [

55], where flood insurance may be considered subordinate to primary economic goods such as food and shelter. This is conceptually similar to Bundorf and Pauly [

56], who argue that insurance affordability can be judged as having sufficient income to afford a certain standard of living after purchasing insurance. Unaffordability is measured following Hudson et al. [

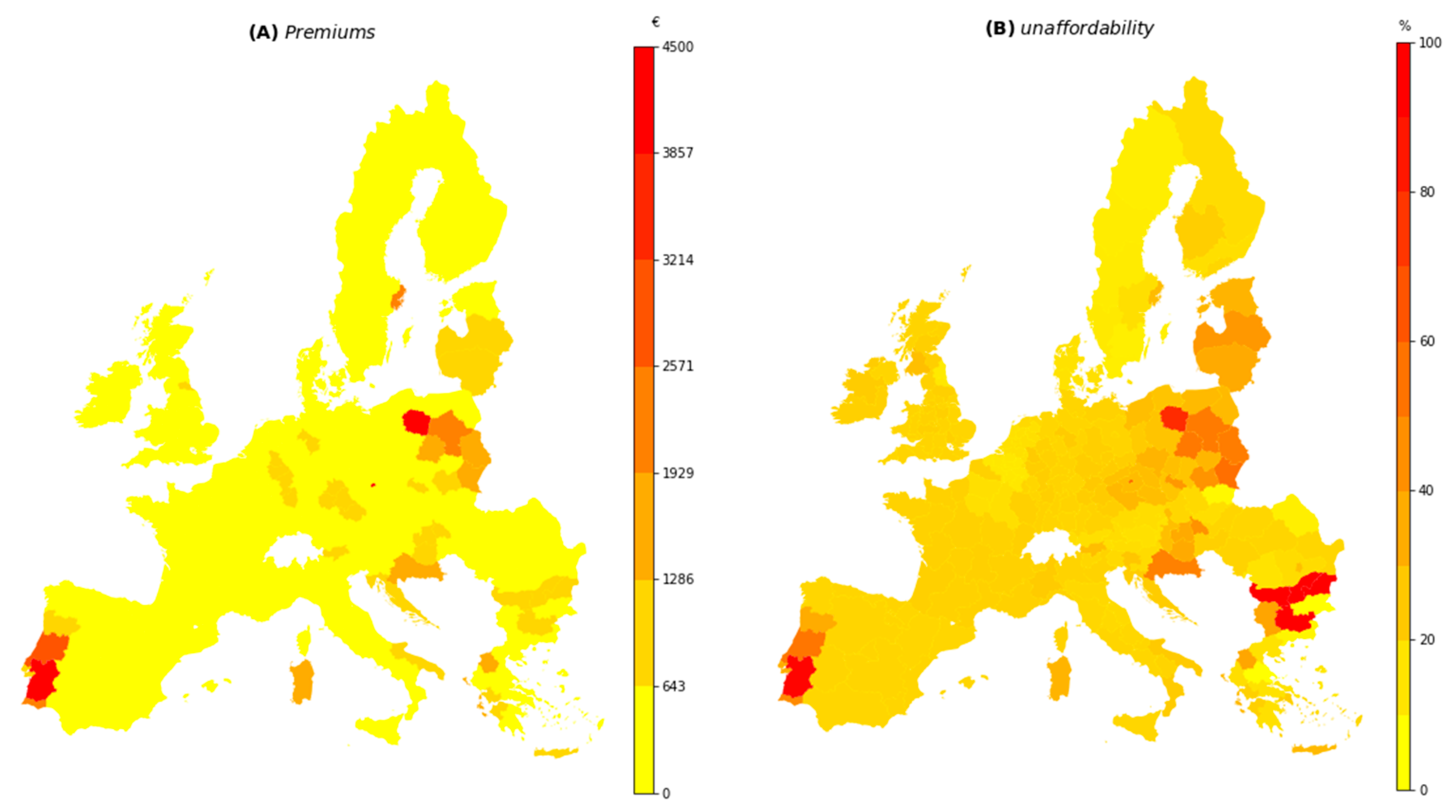

51], where insurance is considered unaffordable when the sum to be paid causes the household’s poverty-adjusted disposable income

to descent below the poverty line

, which is set at 60% of national median income. The magnitude of unaffordability is measured as the regional total value of the unaffordable share of the premium for each household.

Future unaffordability of premiums is dependent on the level of income growth households may experience. In the DIFI model, household income growth is modelled to follow GDP-growth on the NUTS2-level according to the respective SSP scenarios. Therefore, GDP-growth is considered to increase exposure and flood risk, while it is also modelled to increase household income and limit the unaffordability of premiums. For every modelled household, income is determined by randomly drawing from a log-normal income distribution. Although the position of the distribution is calibrated per country and changes over time depending on the SSP-projections, the shape is applied equally for EU countries. This is done because the development of the shape of income distributions is uncertain and is affected by future income redistribution policies, such as through the income tax system and social safety nets.

Equation (4) summarizes the modelled decision framework. Households will buy insurance if it maximizes expected utility, as long as it is affordable to do so.

We realize that affordability is a normative concept [

57], which results in different metrics being proposed for measuring it. Hudson [

58] observes three main affordability metrics regarding flood insurance: Residual income—the purchaser must be left with a certain income after the purchase [

59]; expenditure cap—the purchaser must not spend more than a given percentage of income [

7]; housing burden—the combined expenditure on housing must not exceed a certain percentage of income [

45]. Given the current study’s focus at the European scale, measuring unaffordability following the residual income approach used in Hudson et al. [

51] is most suitable. This is because the at-risk-of-poverty line employed is a pre-existing policy relevant definition across Europe for measuring financial burden [

60]. On the other hand, determining suitable income thresholds for the expenditure and housing burden definitions would require detailed stakeholder consultation within each country studied. Moreover, the residual income approach directly accounts for equity concerns, which is important given the increasing role households play in integrated flood risk management, as noted in international agreements such as the Sendai Framework for Disaster Risk Reduction [

61]. Equity is accounted for by considering a household’s position in the overall income distribution, as well as their available resources.

An elaborate sensitivity analysis of the behavioral module in the DIFI model is performed in Hudson et al. [

26], which includes several alternative assumptions concerning the utility function determining insurance demand. For example, instead of expected utility theory, the model is operated using a household decision function based on prospect theory. Moreover, the sensitivity analysis includes the use of various levels of risk aversion and flood risk perceptions. Overall, the changes in insurance demand caused by the alternative decision theory or behavioral assumptions is limited. Considering the scope of the current study we decided to maintain the utility theory based on subjective expected utility. Instead of focusing on how alternative decision theories or behavioral parameters impact the occurrence of an insurance tipping-point, the main focus of the current study is to analyze the impact of different scenarios of climate and socio-economic change.

4. Discussion

This analysis uses an adapted version of the DIFI model (V2.0), in which flood damage- and socioeconomic data input is acquired from the GLOFRIS framework [

27,

28]. This model adjustment facilitates running the model using various flood hazard and exposure data projections, which are incorporated as RCP-SSP scenario combinations. Previous studies highlight the importance of comparing various risk projections, because these can create large differences in outcomes [

41], meaning that optimal adaptation strategies can differ based on the future scenarios [

27]. For example, Arnell and Lloyd-Hughes [

65] find that the consequences of floods under the same RCP scenario diverge significantly between levels of socio-economic development, with higher adaptation challenges leading to higher impacts. Similarly, we find notable differences between SSP scenarios when holding the RCP scenario constant. The impact of socio-economic development becomes greater for high climate change projections (RCP8.5) compared to low climate change projections (RCP2.6), due to a higher average frequency and intensity of floods in the former [

66].

Whereas the analysis in the current study is sensitive to various future flood risk scenarios, as well as multiple types of flood insurance markets, the household behavioral module based on subjective expected utility theory is the same between households. Although this is a conscious choice of the authors, as the primary interest of this study concerns the performance of various types of flood insurance arrangements under different climatic- and socio-economic scenarios, the inclusion of some additional behavioral theories can also provide interesting insights. For example, an agent-based study found that interaction between individuals, insurance markets, and the environment significantly affects future flood risk due to additional adaptive behavior by heterogenous boundedly rational individuals [

67]. Similarly, an agent-based approach could be applied to model intra-household behavior concerning insurance purchase and the decision to apply risk-reduction measures. Existing research suggests that this type of complexity of within-household decision making concerning consumption exists [

68]. However, to our knowledge no previous studies exist that relate this type of decision making to flood insurance purchase decisions or adaptation to natural hazards. A downside of modelling more complex household behavior on this level, especially using agent-based models, is that it is computationally too demanding on a large scale, such as EU-level.

The unaffordability of flood insurance, as well as the penetration rate, are found to improve when introducing various elements of the Public-Private-Partnership (PPP). Paudel et al. [

69] explains how this type of insurance system can lower premiums by shifting the extreme risk (top 15% in our model) to a public reinsurer that does not charge a profit-loading factor for the transferred risk. This is made possible by its “

non-profit status, low administrative costs and lack of risk load” [

70]. An example of a public reinsurer, although in a slightly different form as described earlier, is Flood Re in the UK, which was able to reduce premiums up to 50% for households with a prior flood claim since 2016 [

71]. Our study found the highest reduction in unaffordability of premiums by incorporating an element of risk-sharing in the form of a premium-cap. In principle, public reinsurance can be combined with a premium-cap in a PPP flood insurance arrangement in order to limit problems with unaffordability of premiums.

In addition to introducing a public reinsurer or premium cap, we include insurance schemes with purchase requirements. This includes a semi-voluntary scheme, where insurance uptake is required for mortgages, such as in Sweden, or included in home and real estate insurance, such as in Finland. As a result of this measure, both of these countries are able to maintain penetration rates above 80% [

72,

73]. Besides conditional purchase requirements we include an insurance scheme that is mandatory for all, as can be found in France, Spain, Belgium, and Romania. All of these countries are able to maintain very high penetration rates, except for Romania, where the enforcement of the insurance purchase mandate is lacking [

72]. These type of insurance policies limit problems with adverse selection compared to a voluntary system, as most households in lower risk areas cannot choose to opt out of insurance. As a result of this, insurers are better able to spread risk, which can enhance insurer solvency and potentially reduce premiums for households [

69]. Moreover, high penetration rates mean that most households are financially protected against flood damage. This limits the impact on private savings after flood events, or the burden for the public budget when the government offers disaster relief to uninsured households, as was, for instance, required after the 2013 floods in Germany [

74].

A relevant implication of introducing insurance purchase requirements is that the total value of unaffordability must be compensated, as forcing households into poverty through mandating coverage may have large socio-economic consequences. An existing measure to tackle the problem of unaffordability is to provide subsidized insurance to low income households, or households residing in high-risk areas [

75]. A subsidy can be either provided directly to households, or to insurers who can then charge premiums below the expected value of loss. A downside of these measures is that households in high-risk areas receive less incentive to mitigate or adapt to flood risk, which can have a negative welfare consequences, as more funding will be required for subsidies due to rising flood risk. Kousky and Kunreuther [

7] propose a voucher mechanism as an alternative, in which means-tested vouchers are coupled with low-cost loans meant for investment in risk-reducing measures. Alternatively, governments can subsidize risk-reduction measures for low-income households. This, in turn, will lower flood risk, which reduces the cost of insurance and limits unaffordability issues. Instead of a lump-sum transfer to cover unaffordability, this measure reduces overall flood risk and, therefore, is more efficient.

Alleviating premium costs for households in high-risk areas is justified from a solidarity perspective. However, it should be considered that it can stimulate economic development and increase exposure to flooding in high-risk areas [

76]. Therefore, premium reductions should be accompanied by incentives to mitigate risk, such as premium discounts when risk-reduction measures are implemented. An example of this type of policy is the community rating system implemented by the National Flood Insurance Program in the US, where households can receive a premium discount based on their community’s effort to reduce risk [

77]. Moreover, individual households can receive additional premium discounts if people elevate the lowest floor of their home, which is a cost-effective way for limiting flood risk especially for newly constructed homes [

78]. A disadvantage of stimulating risk reduction with premium discounts is that it involves administrative costs for the insurance company to determine whether the risk reduction measures are in place. In practice, this can be overcome through external building certification schemes, such as elevation certificates issued in the US.

Relocation to areas that are less prone to flooding can be another way to cope with increasing flood risk and higher flood insurance premiums, besides structural measures that reduce flood risk. Although large-scale migration in response to natural disasters has not been observed in developed countries [

79], some studies suggest this as a viable option to enhance future societal resilience to flooding [

80]. Risk-based insurance premiums can stimulate this type of adaptation when these rise rapidly in high-risk areas. However, insurance policies should beware that this does not disproportionally cause problems for low-income groups, as relocating may be infeasible or too expensive for these groups. If relocation of households from high- to low flood-risk areas will happen on a larger scale towards 2080, then the level of unaffordability of premiums simulated in this study may be overestimated.

The mentioned policy changes considered several potential insurance policy strategies and how they impact unaffordability of premiums and uptake of coverage. Importantly, what we did not address in this study is how an improvement in flood protection standards can impact these outcomes. In the flood risk module, it was assumed that protection standards remain constant in the case flood hazard increases, meaning that governments invest in maintaining protection infrastructure to grow along with the flood hazard. However, additional public spending can be directed to enhance flood protection standards, which can significantly reduce regional flood risk, and therefore reduce insurance premiums without additional changes in insurance strategies. However, relying on this measure may enlarge regional inequality in flood insurance affordability and availability, as enhancing protection standards in the face of increasing flood hazard can be costly, and may be unaffordable for lower income countries.

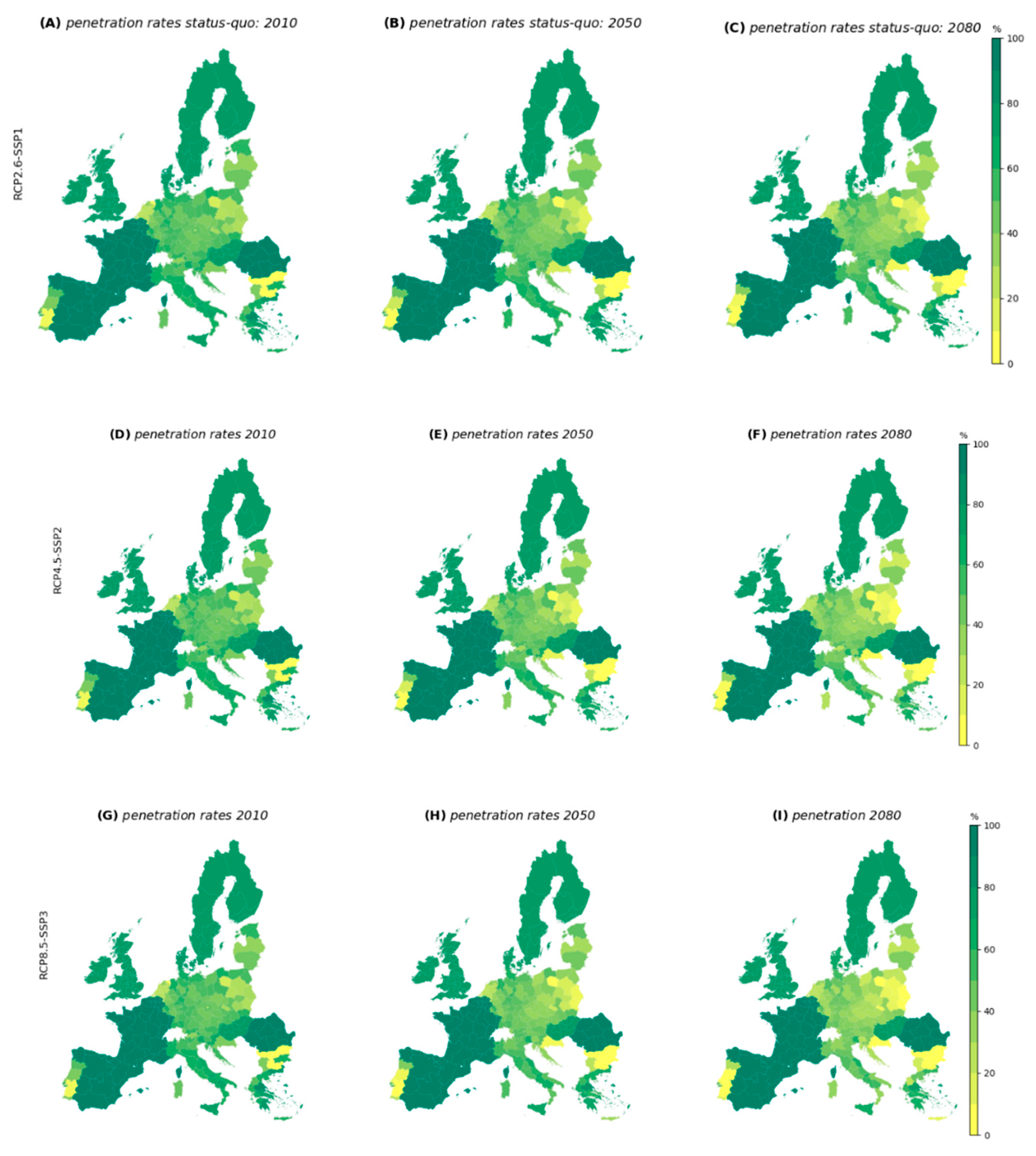

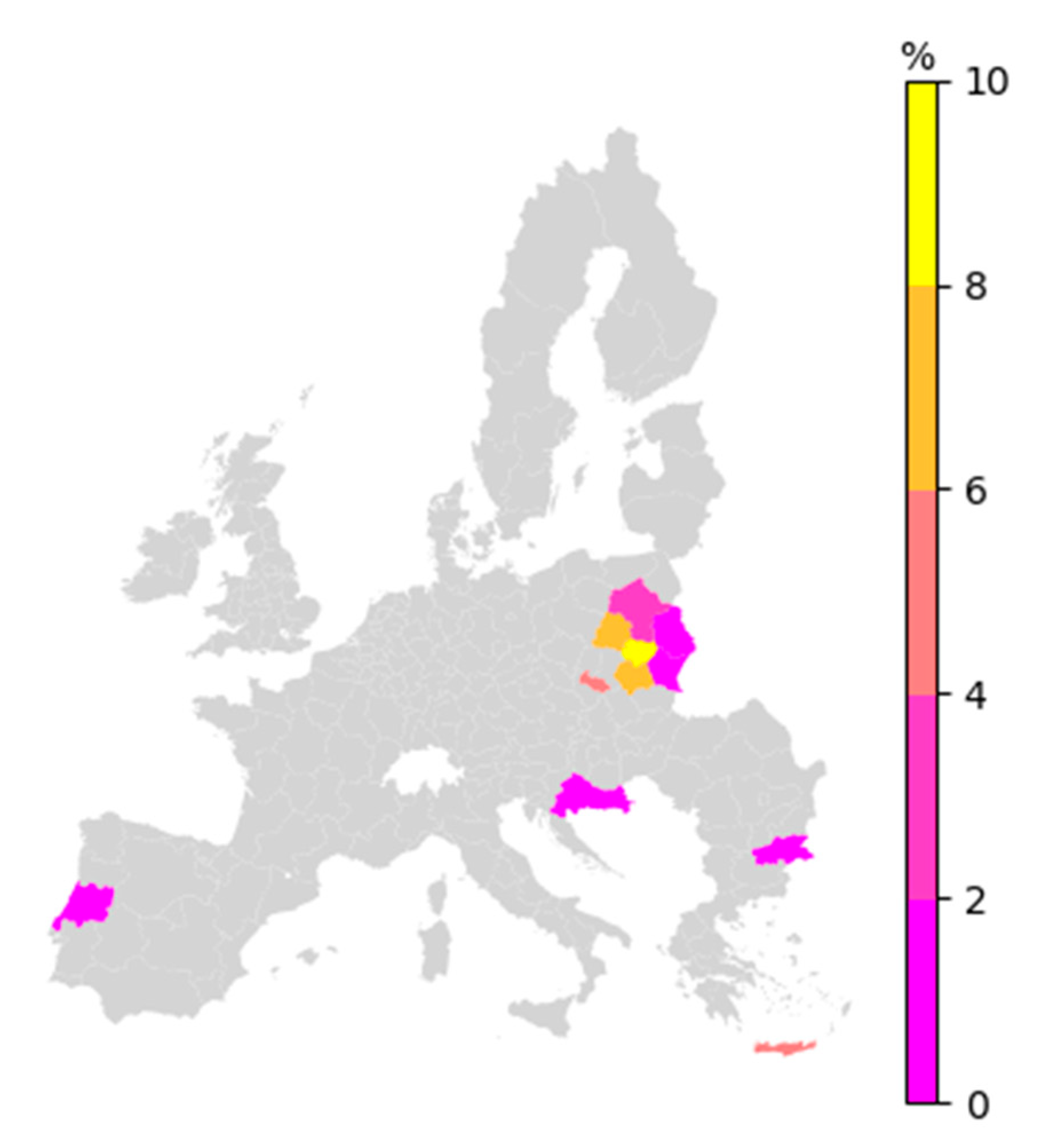

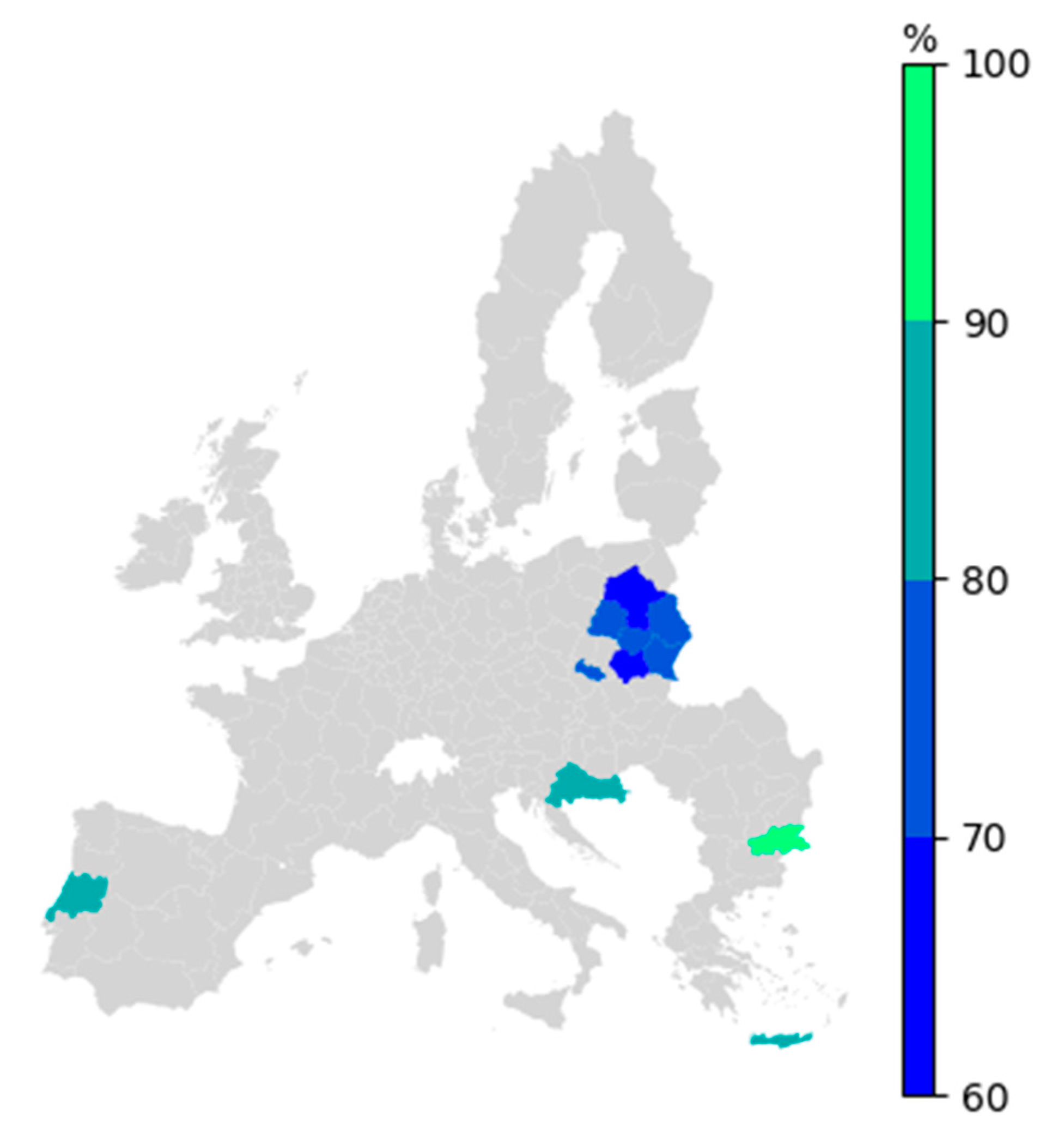

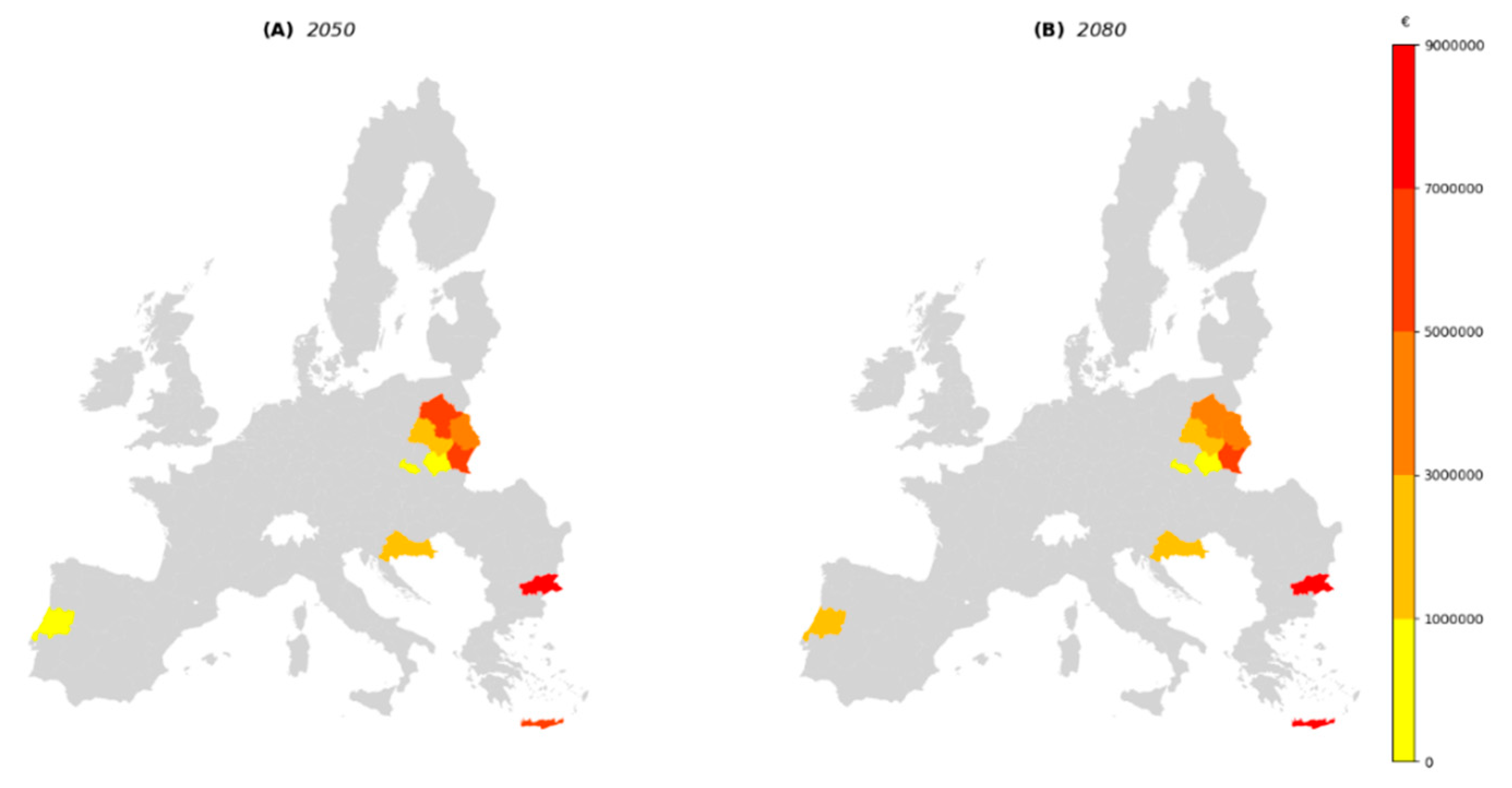

Finally, in this study, we considered which European regions are projected to experience growing unaffordability of premiums and declining uptake of insurance to such an extent that it obstructs the functioning of insurance markets, leaving households to finance flood damage by different means. However, as this analysis focusses on high-risk areas, a perceived regional tipping-point may not lead to a collapse of private flood insurance on a national scale. Instead, the collapse of flood insurance markets was approached from the consumer side, where unwillingness to pay for rapidly increasing premiums by households causes the insurance system to no longer meet its objective, which is to provide financial security for citizens against the growing threat of flooding. Furthermore, tipping-point regions are identified using criteria selected by the authors based on projected insurance penetration rates. The criteria used here define the occurrence of a tipping-point when the penetration rate declines from 20% in 2010 to less than 5% in 2080, which is a selected point where insurance fails to provide coverage for a significant share of households. However, this definition is not absolute, and changing these criteria also affects the number of tipping-point regions.

5. Conclusions

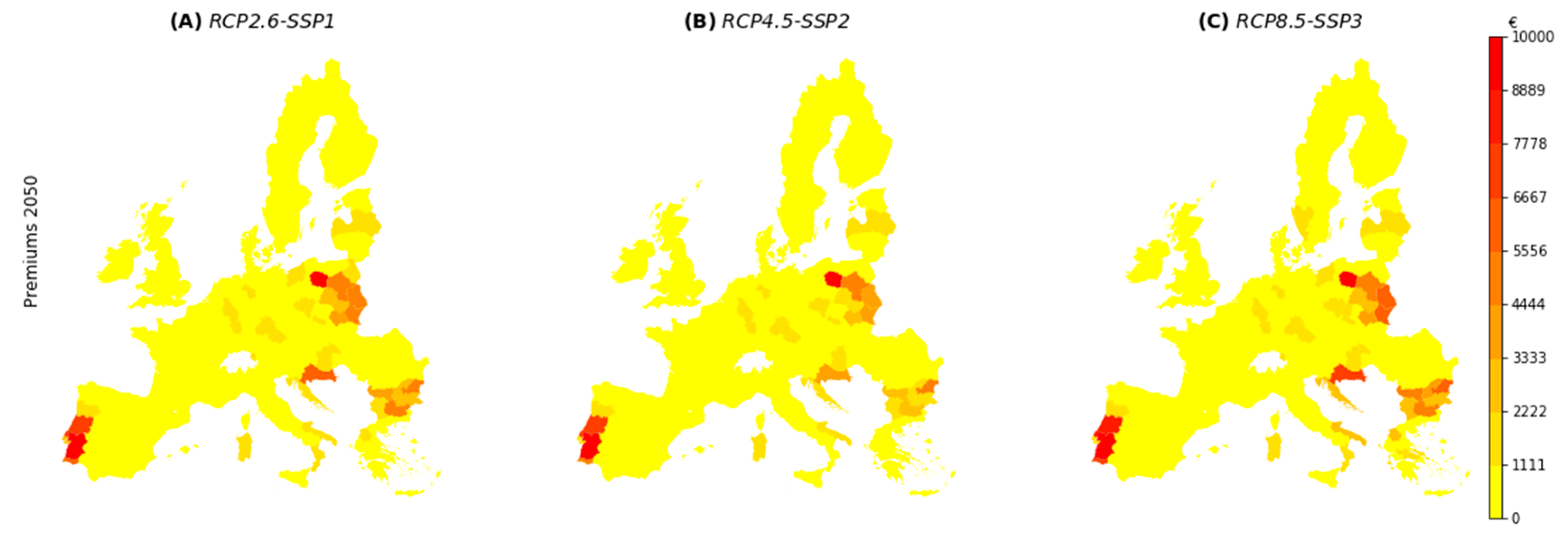

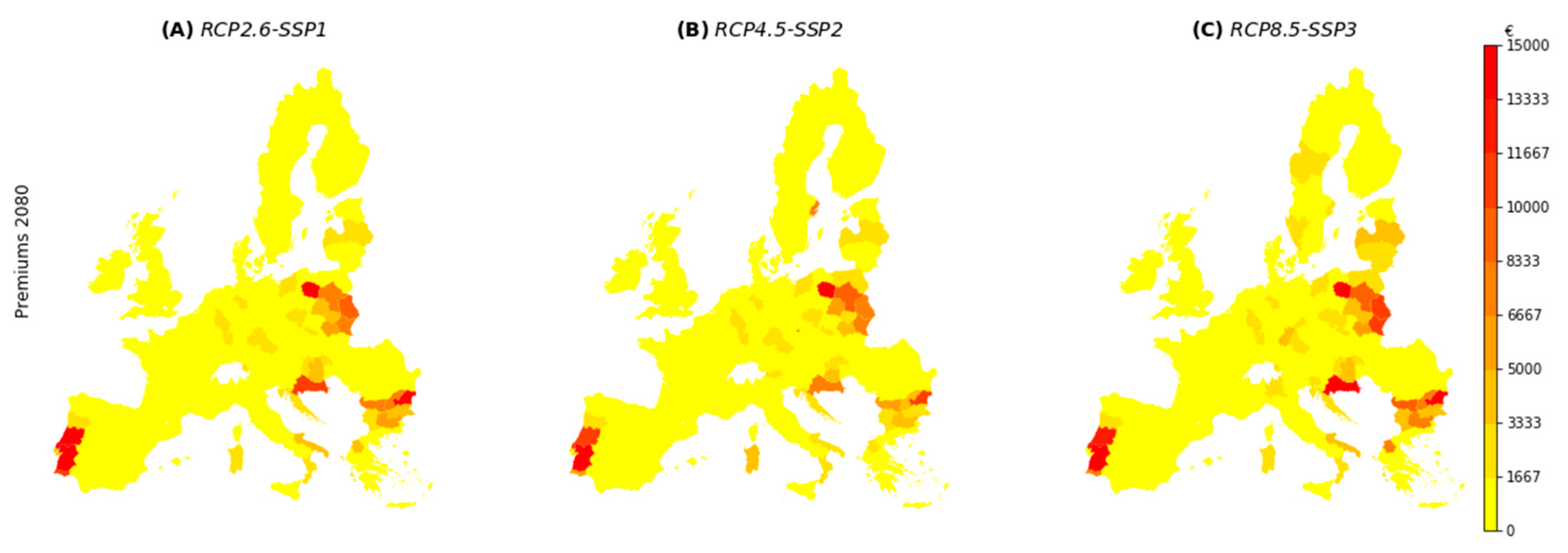

This study showed the possibility of a climate-induced socio-economic tipping-point for flood insurance in Europe, where rising unaffordability and declining uptake of insurance under climate change obstructs the functioning of insurance markets in high-risk areas. As a result, regional inequalities arise in the ability to use flood insurance as an instrument for adapting to increasing flood risk. We observe progressively rising flood insurance premiums over time from the climate change scenarios RCP2.6 to RCP8.5, for countries that maintain risk-based insurance premiums. This causes an increase of unaffordability of insurance, the extent of which depends on the projected socio-economic development in that period. Such unaffordability problems occur particularly in regions with below average income per capita. When insurance uptake is voluntary, the increase of premiums combined with underestimated household risk perceptions causes a decline of insurance demand. This process causes flood insurance demand to almost disappear for several regions in our projections. The number of European regions where this occurs is highest under the RCP8.5-SSP3 scenario, which represents a continued rise in greenhouse gas emissions combined with regional economic inequalities.

This development constitutes a socio-economic tipping-point as the collapse of private flood insurance calls for a shift of flood damage compensation from pre-funded, formal insurance, towards less formal means of financing, such as ex post government compensation or self-insurance. However, ex post government compensation is a contingent liability, which, unless made explicit, is inherently uncertain for both the government’s budget as well as the household. Therefore, we argue in favor of formal insurance, which can be sustained in the face of increasing flood risk by maintaining premiums with limited risk-reflection, as this encourages risk-mitigation while limiting unaffordability of premiums. Furthermore, coverage requirements should increase the covered assets and enhance the ability for insurers to pool the risk. Finally, a government reinsurer can reduce premiums as it is risk neutral and does not seek profit.

We recommend future research to focus on developing a more specific strategy for implementing a voucher mechanism that covers the remaining unaffordability of insurance. This system should alleviate the share of the insurance premium that is considered unaffordable, while giving an incentive for households to implement risk-reduction measures and reduce the premium. We also recognize the importance of investigating the impacts of uncovered flood risk on household and government budgets in future research. A more extensive analysis of household behavior and decision making under scenarios of flood risk is another topic that deserves attention in future research. Research can, for example, focus on the performance of insurance markets or the extend of household-level adaptation to flood risk under multiple theories of individual decision-making, such as decision rules that account for myopia or are based on heuristics.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}