Shaking Stability: COVID-19 Impact on the Visegrad Group Countries’ Financial Markets

, ,

, ,  ,

,

Abstract

1. Introduction

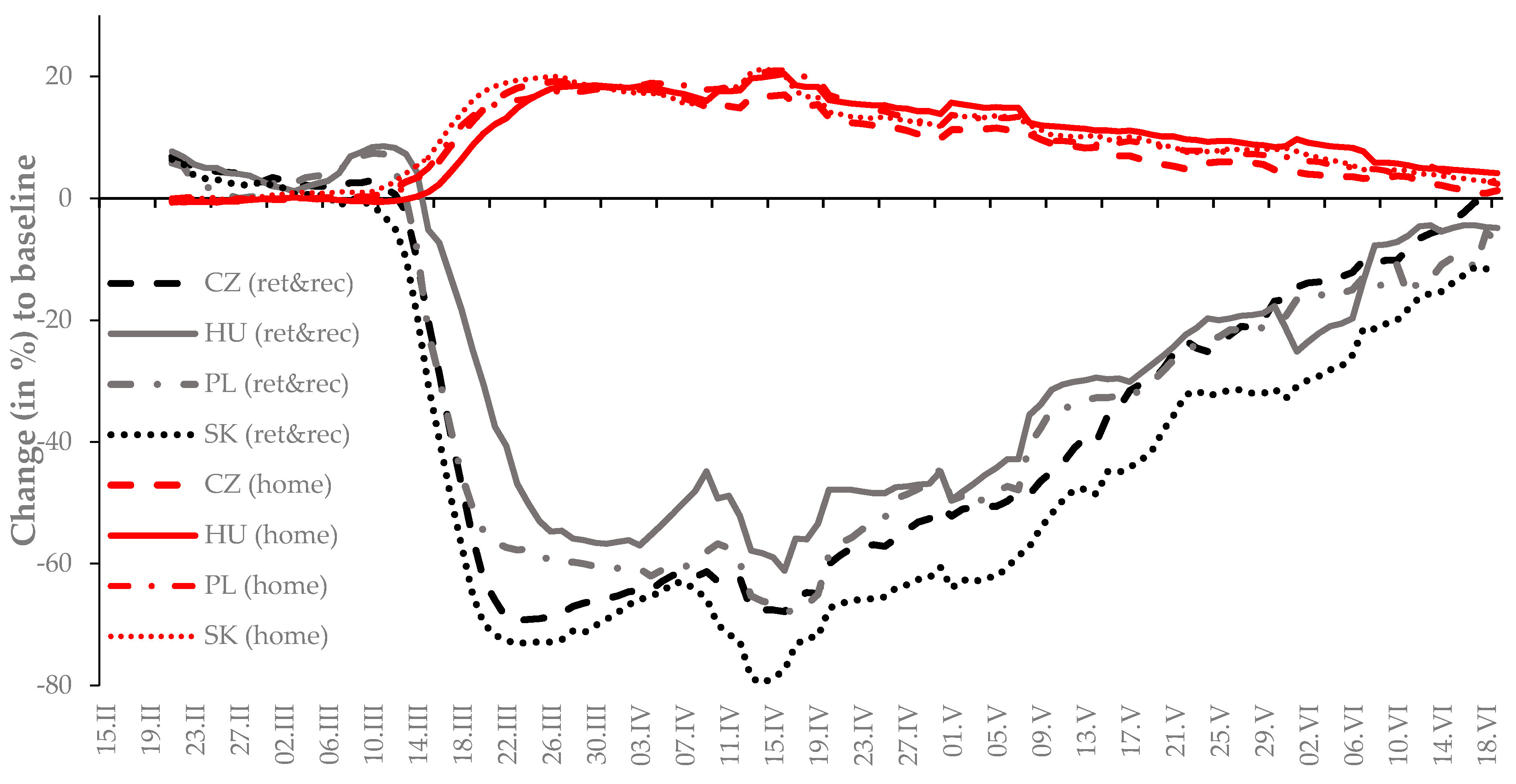

2. COVID-19 Pandemic Development in the Visegrad Group Countries and Its Effect on Their Economies

3. Methodology

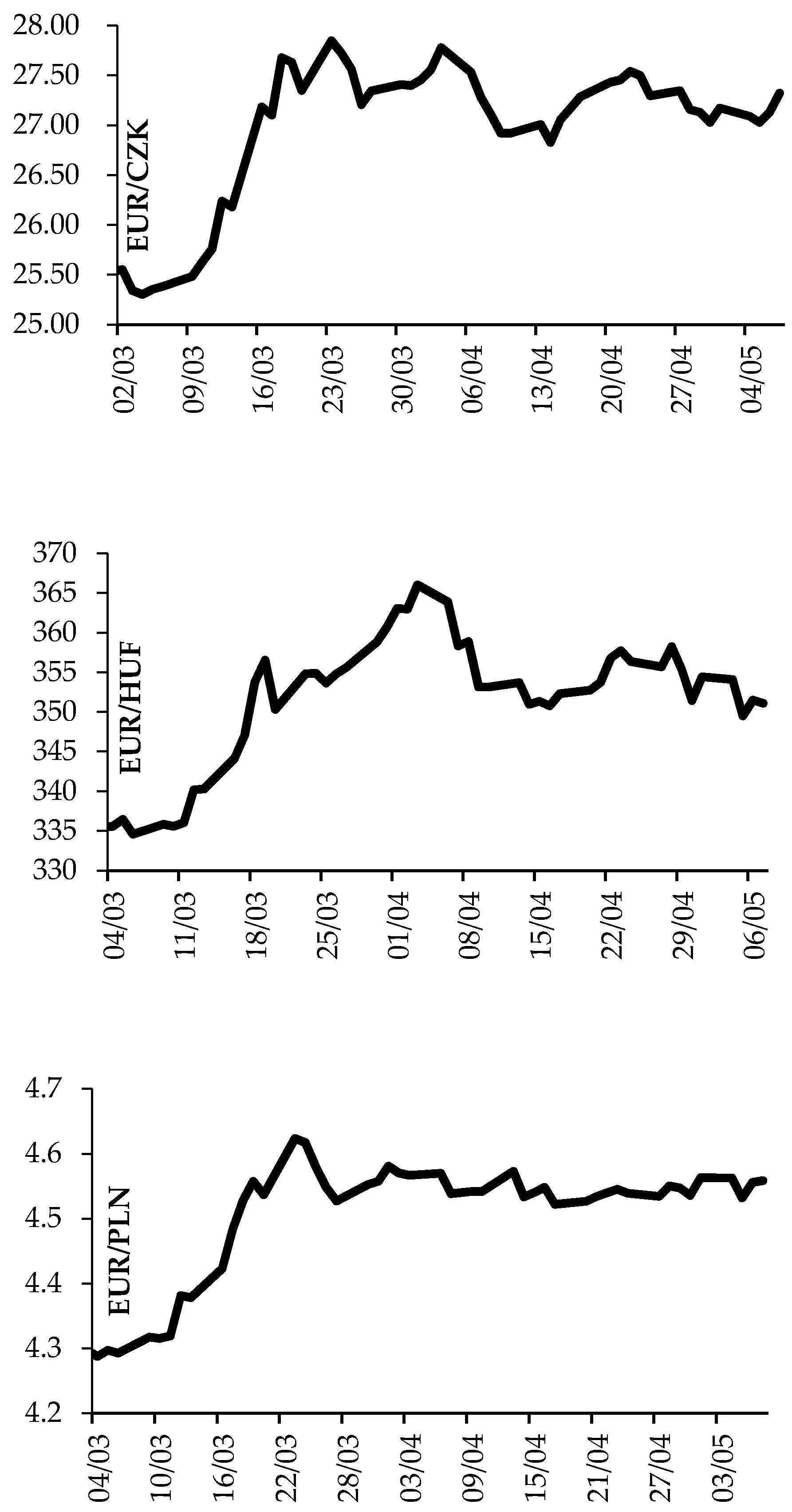

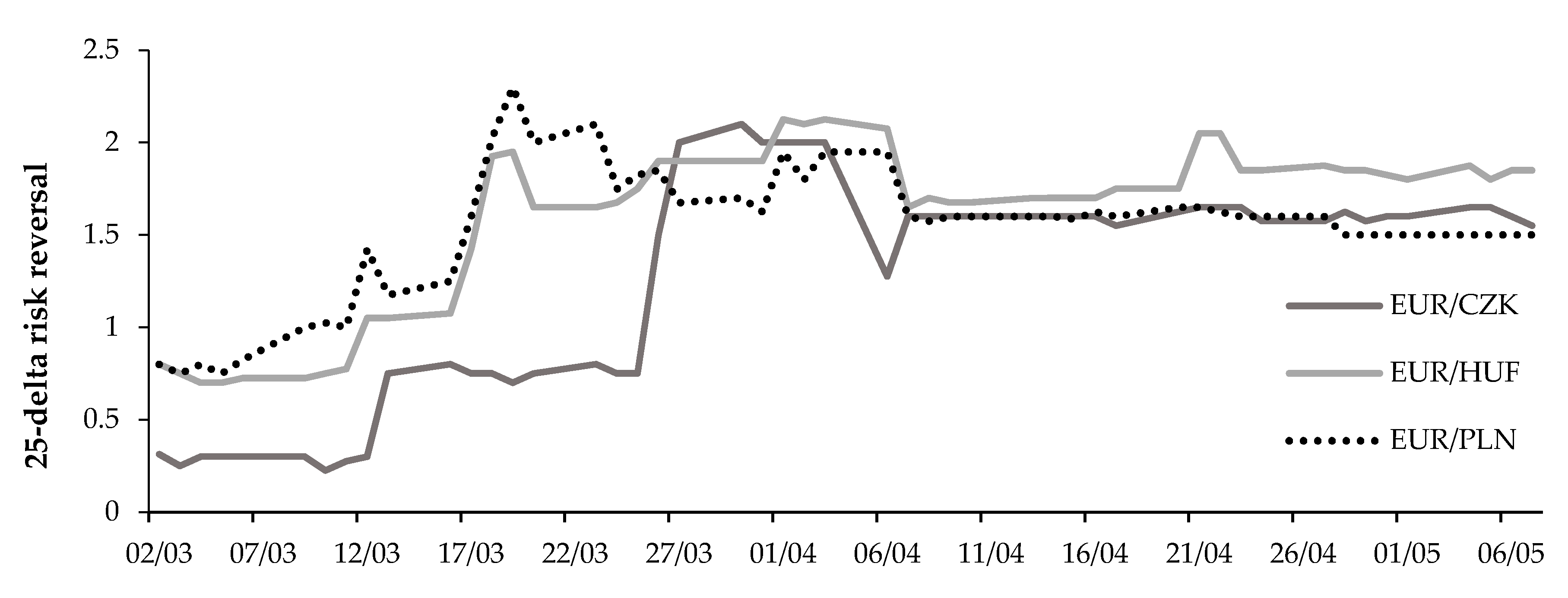

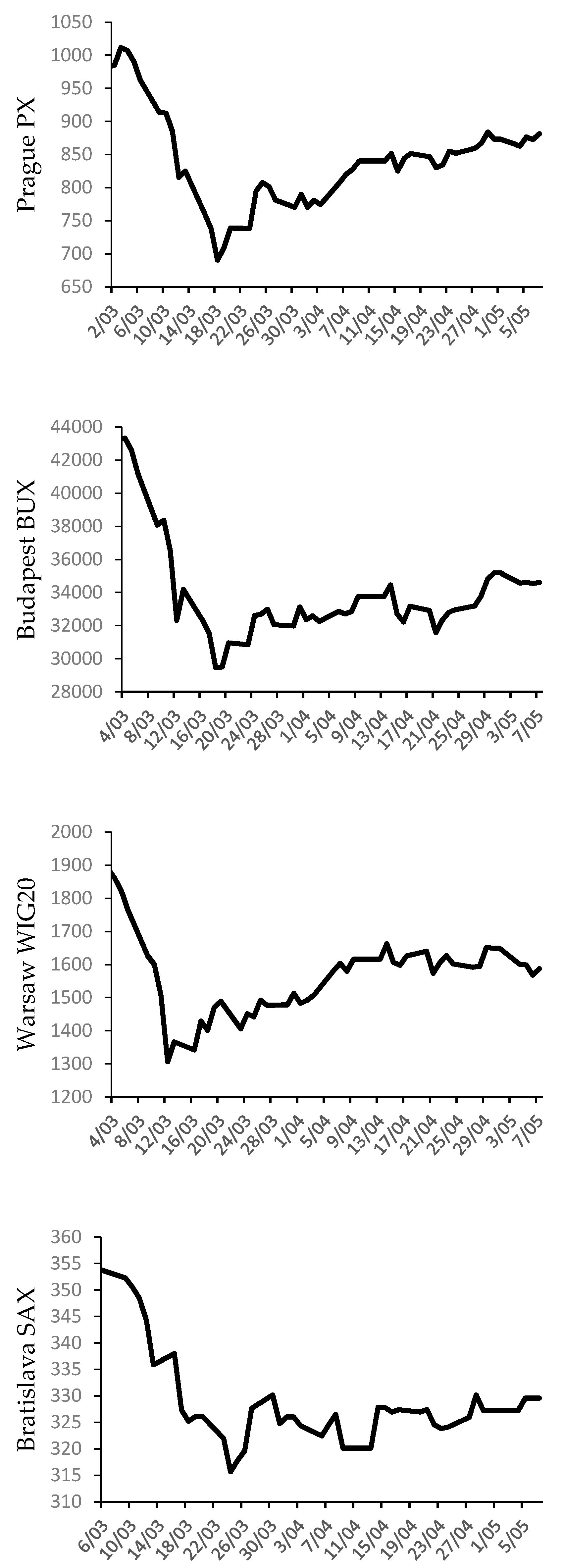

4. The Impact of COVID-19 Cases on the Financial Markets of the Visegrad Group Countries

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A

References

- Goodell, J.W. COVID-19 and finance: Agendas for future research. Financ. Res. Lett. 2020, 35, 101512. [Google Scholar] [CrossRef]

- Maier, B.F.; Brockmann, D. Effective containment explains subexponential growth in recent confirmed COVID-19 cases in China. Science 2020, 368, 742–746. [Google Scholar] [CrossRef]

- Verikios, G.; Sullivan, M.; Stojanovski, P.; Giesecke, J.; Woo, G. The Global Economic Effects of Pandemic Influenza; Centre of Policy Studies: Clayton, Australia, 2011. [Google Scholar]

- Andersen, K.G.; Rambaut, A.; Lipkin, W.I.; Holmes, E.C.; Garry, R.F. The proximal origin of SARS-CoV-2. Nat. Med. 2020, 26, 450–452. [Google Scholar] [CrossRef]

- Corman, V.M.; Muth, D.; Niemeyer, D.; Drosten, C. Hosts and sources of endemic human coronaviruses. In Advances in Virus Research; Academic Press Inc.: Cambridge, MA, USA, 2018; Volume 100, pp. 163–188. ISBN 9780128152010. [Google Scholar]

- Ge, X.; Li, Y.; Yang, X.; Zhang, H.; Zhou, P.; Zhang, Y.; Shi, Z. Metagenomic analysis of viruses from bat fecal samples reveals many novel viruses in insectivorous bats in China. J. Virol. 2012, 86, 4620–4630. [Google Scholar] [CrossRef]

- Ge, X.Y.; Li, J.L.; Yang, X.L.; Chmura, A.A.; Zhu, G.; Epstein, J.H.; Mazet, J.K.; Hu, B.; Zhang, W.; Peng, C.; et al. Isolation and characterization of a bat SARS-like coronavirus that uses the ACE2 receptor. Nature 2013, 503, 535–538. [Google Scholar] [CrossRef]

- Johns Hopkins University COVID-19 Map—Johns Hopkins Coronavirus Resource Center. Available online: https://coronavirus.jhu.edu/map.html (accessed on 29 June 2020).

- Walker, P.; Whittaker, C.; Watson, O.; Baguelin, M.; Ainslie, K.; Bhatia, S.; Bhatt, S.; Boonyasiri, A.; Boyd, O.; Cattarino, L.; et al. Report 12: The Global Impact of COVID-19 and Strategies for Mitigation and Suppression; Imperial College London: London, UK, 2020. [Google Scholar]

- Laing, T. The economic impact of the Coronavirus 2019 (Covid-2019): Implications for the mining industry. Extr. Ind. Soc. 2020, 7, 580. [Google Scholar] [CrossRef]

- European Institute for European Policy Is the COVID-19 Pandemic the Hungarian Democracy’s Coup de Grace—EUROPEUM Institute for European Policy. Available online: https://europeum.blogactiv.eu/2020/04/23/covid-19-pandemic-the-coup-de-grace-hungarian-democracy/ (accessed on 28 June 2020).

- Zambrano-Monserrate, M.A.; Ruano, M.A.; Sanchez-Alcalde, L. Indirect effects of COVID-19 on the environment. Sci. Total Environ. 2020, 728, 138813. [Google Scholar] [CrossRef]

- Mitra, A.; Chaudhuri, T.R.; Mitra, A.; Pramanick, P.; Zaman, S. Impact of COVID-19 related shutdown on atmospheric carbon dioxide level in the city of Kolkata. Parana J. Sci. Educ. 2020, 6, 84–92. [Google Scholar] [CrossRef]

- Crawford, J.; Butler-Henderson, K.; Rudolph, J.; Malkawi, B.; Glowatz, M.; Burton, R.; Magni, P.A.; Lam, S. View of COVID-19: 20 countries’ higher education intra-period digital pedagogy responses. J. Appl. Learn. Teach. 2020, 3, 9–28. [Google Scholar]

- Toquero, C.M. Challenges and opportunities for higher education amid the COVID-19 pandemic: The Philippine context. Pedagog. Res. 2020, 5, em0063. [Google Scholar] [CrossRef]

- Zhang, W.; Wang, Y.; Yang, L.; Wang, C. Suspending classes without stopping learning: China’s education emergency management policy in the COVID-19 outbreak. J. Risk Financ. Manag. 2020, 13, 55. [Google Scholar] [CrossRef]

- Alon, T.M.; Doepke, M.; Olmstead-Rumsey, J.; Tertilt, M. The Impact of COVID-19 on Gender Equality; National Bureau of Economic Research: Cambridge, MA, USA, 2020. [Google Scholar]

- Mahler, D.G.; Lakner, C.; Castaneda Aguilar, A.R.; Wu, H. Updated estimates of the impact of COVID-19 on global poverty. Available online: https://blogs.worldbank.org/opendata/updated-estimates-impact-covid-19-global-poverty (accessed on 28 June 2020).

- Sumner, A.; Hoy, C.; Ortiz-Juarez, E. Estimates of the Impact of COVID-19 on Global Poverty. WIDER Working Paper, 43rd ed.; UNU-WIDER: Helsinki, Finland, 2020; Volume 2020, ISBN 978-92-9256-800-9. [Google Scholar]

- Tokic, D. Long-term consequences of the 2020 coronavirus pandemics: Historical global-macro context. J Corp. Account. Financ. 2020. [Google Scholar] [CrossRef]

- Mckibbin, W.; Fernando, R. The Global Macroeconomic Impacts of COVID-19: Seven Scenarios; Centre for Economic Policy Research: London, UK, 2020. [Google Scholar]

- Loayza, N.V.; Pennings, S. Macroeconomic Policy in the Time of COVID-19: A Primer for Developing Countries. Research and Policy Briefs; World Bank: Washington, DC, USA, 2020. [Google Scholar]

- Baldwin, R.E.; Tomiura, E. Thinking ahead about the trade impact of COVID-19. In Economics in the Time of COVID-19; Centre for Economic Policy Research: London, UK, 2020; pp. 59–71. [Google Scholar]

- Nicola, M.; Alsafi, Z.; Sohrabi, C.; Kerwan, A.; Al-Jabir, A.; Iosifidis, C.; Agha, M.; Agha, R. The socio-economic implications of the coronavirus pandemic (COVID-19): A review. Int. J. Surg. 2020, 78, 185–193. [Google Scholar] [CrossRef] [PubMed]

- Eichenbaum, M.S.; Rebelo, S.; Trabandt, M. The Macroeconomics of Epidemics; NBER Working Paper: Cambridge, MA, USA, 2020. [Google Scholar]

- Yu, K.D.S.; Aviso, K.B. Modelling the economic impact and ripple effects of disease outbreaks. Process Integr. Optim. Sustain. 2020, 4, 183–186. [Google Scholar] [CrossRef]

- Boot, A.; Carletti, E.; Kotz, H.-H.; Krahnen, J.P.; Pelizzon, L.; Subrahmanyam, M. The Coronavirus and Financial Stability. Available online: https://voxeu.org/content/coronavirus-and-financial-stability (accessed on 15 July 2020).

- Aslam, F.; Mohti, W.; Ferreira, P. Evidence of intraday multifractality in european stock markets during the recent coronavirus (COVID-19) outbreak. Int. J. Financ. Stud. 2020, 8, 31. [Google Scholar] [CrossRef]

- Yu, L.; Du, J.; Dang, H. Special issue on FDI and integration of Chinese economy. China Econ. Rev. 2020, 61, 101460. [Google Scholar] [CrossRef]

- Rodeck, D. The Shape of the COVID-19 Recession—Forbes Advisor. Available online: https://www.forbes.com/advisor/investing/covid-19-coronavirus-recession-shape/ (accessed on 28 June 2020).

- Engelhardt, N.; Krause, M.; Neukirchen, D.; Posch, P. What drives stocks during the corona-crash? News attention vs. rational expectation. Sustainability 2020, 12, 5014. [Google Scholar] [CrossRef]

- Barro, R.J.; Ursua, J.F.; Weng, J. The Coronavirus and the Great Influenza Epidemic—Lessons from the “Spanish Flu” for the Coronavirus’s Potential Effects on Mortality and Economic Activity; CESifo Working Paper Series CESifo: Munich, Germany, 2020. [Google Scholar]

- Ramelli, S.; Wagner, A.F. Feverish Stock Price Reactions to COVID-19; Social Science Research Network: Rochester, NY, USA, 2020. [Google Scholar]

- Malec, K.; Gebeltova, Z.; Maitah, M. Volatility and liquidity of cme corn market. In Agrarian Perspectives Xxvii—Food Safety—Food Security; Tomsik, K., Ed.; Czech University Life Sciences Prague: Prague, Czechia, 2018; pp. 159–166. ISBN 978-80-213-2890-7. [Google Scholar]

- Goniewicz, K.; Khorram-Manesh, A.; Hertelendy, A.J.; Goniewicz, M.; Naylor, K.; Burkle, F.M. Current response and management decisions of the European union to the COVID-19 outbreak: A review. Sustainability 2020, 12, 3838. [Google Scholar] [CrossRef]

- Gössling, S.; Scott, D.; Hall, C.M. Pandemics, tourism and global change: A rapid assessment of COVID-19. J. Sustain. Tour. 2020, 1–20. [Google Scholar] [CrossRef]

- Haacker, M. The Impact of HIV/AIDS on Government Finance and Public Services; International Monetary Fund: Washington, DC, USA, 2004; ISBN 978-1-58906-360-0. [Google Scholar]

- McKibbin, W.; Roshen, F. The economic impact of COVID-19. In Economics in the Time of COVID-19; Centre for Economic Policy Research: London, UK, 2020; pp. 45–52. ISBN 978-1-912179-28-2. [Google Scholar]

- Zhang, D.; Hu, M.; Ji, Q. Financial markets under the global pandemic of COVID-19. Financ. Res. Lett. 2020, 101528. [Google Scholar] [CrossRef]

- Baker, S.R.; Bloom, N.; Davis, S.J.; Kost, K.J.; Sammon, M.C.; Viratyosin, T. The Unprecedented Stock Market Impact of COVID-19; National Bureau of Economic Research: Cambridge, MA, USA, 2020. [Google Scholar]

- Okorie, D.I.; Lin, B. Stock markets and the COVID-19 fractal contagion effects. Financ. Res. Lett. 2020, 101640. [Google Scholar] [CrossRef]

- Sansa, N.A. The impact of the COVID-19 on the financial markets: Evidence from China and USA. Electron. Res. J. Soc. Sci. Humanit. 2020, 2, 29–39. [Google Scholar] [CrossRef]

- He, Q.; Liu, J.; Wang, S.; Yu, J. The impact of COVID-19 on stock markets. Econ. Political Stud. 2020, 1–14. [Google Scholar] [CrossRef]

- Ammy-Driss, A.; Garcin, M. Efficiency of the financial markets during the COVID-19 crisis: Time-varying parameters of fractional stable dynamics. arXiv 2020, arXiv:2007.10727. [Google Scholar]

- Garcin, M.; Klein, J.; Laaribi, S. Estimation of time-varying kernel densities and chronology of the impact of COVID-19 on financial markets. arXiv 2020, arXiv:2007.09043. [Google Scholar]

- Topcu, M.; Gulal, O.S. The impact of COVID-19 on emerging stock markets. Financ. Res. Lett. 2020, 101691. [Google Scholar] [CrossRef]

- Liu, H.; Manzoor, A.; Wang, C.; Zhang, L.; Manzoor, Z. The COVID-19 outbreak and affected countries stock markets response. Int. J. Environ. Res. Public Health 2020, 17, 2800. [Google Scholar] [CrossRef]

- Ali, M.; Alam, N.; Rizvi, S.A.R. Coronavirus (COVID-19)—An epidemic or pandemic for financial markets. J. Behav. Exp. Financ. 2020, 27, 100341. [Google Scholar] [CrossRef]

- Ashraf, B.N. Stock markets’ reaction to COVID-19: Cases or fatalities? Res. Int. Bus. Financ. 2020, 54, 101249. [Google Scholar] [CrossRef]

- De Bock, R.; de Carvalho Filho, I. The behavior of currencies during risk-off episodes. J. Int. Money Financ. 2015, 53, 218–234. [Google Scholar] [CrossRef]

- Ranaldo, A.; Söderlind, P. Safe haven currencies. Rev. Financ. 2010, 14, 385–407. [Google Scholar] [CrossRef]

- Grisse, C.; Nitschka, T. On financial risk and the safe haven characteristics of Swiss franc exchange rates. J. Empir. Financ. 2015, 32, 153–164. [Google Scholar] [CrossRef]

- Habib, M.M.; Stracca, L. Getting beyond carry trade: What makes a safe haven currency? J. Int. Econ. 2012, 87, 50–64. [Google Scholar] [CrossRef]

- Gilmore, S.; Hayashi, F. Emerging market currency excess returns. Am. Econ. J. Macroecon. 2011, 3, 85–111. [Google Scholar] [CrossRef]

- Gunay, S. A New form of financial contagion: COVID-19 and stock market responses. SSRN J. 2020. [Google Scholar] [CrossRef]

- Benzid, L.; Chebbi, K. The impact of COVID-19 on exchange rate volatility: Evidence through GARCH model. SSRN J. 2020. [Google Scholar] [CrossRef]

- Salathé, M.; Althaus, C.L.; Neher, R.; Stringhini, S.; Hodcroft, E.; Fellay, J.; Zwahlen, M.; Senti, G.; Battegay, M.; Wilder-Smith, A.; et al. COVID-19 epidemic in Switzerland: On the importance of testing, contact tracing and isolation. Swiss Med. Wkly. 2020. [Google Scholar] [CrossRef]

- Berger, D.; Herkenhoff, K.; Mongey, S. An SEIR Infectious Disease Model with Testing and Conditional Quarantine; National Bureau of Economic Research: Cambridge, MA, USA, 2020; p. w26901. [Google Scholar]

- Worldometer Coronavirus Update (Live): 10,352,387 Cases and 506,364 Deaths from COVID-19 Virus Pandemic. Available online: https://www.worldometers.info/coronavirus/ (accessed on 29 June 2020).

- Hale, T.; Webster, S.; Petherick, A.; Phillips, T.; Kira, B. Oxford COVID-19 Government Response Tracker. Available online: https://www.bsg.ox.ac.uk/research/publications/variation-government-responses-covid-19 (accessed on 29 June 2020).

- Correia, S.; Luck, S.; Verner, E. Pandemics depress the economy, public health interventions do not: Evidence from the 1918 flu. SSRN J. 2020. [Google Scholar] [CrossRef]

- Google LLC COVID-19 Community Mobility Report. Available online: https://www.google.com/covid19/mobility?hl=en (accessed on 29 June 2020).

- Oxford Economics Economic and Political Risk Evaluator. A Framework for Forecasting Economic and Geopolitical Risks. Available online: https://www.oxfordeconomics.com/economic-and-political-risk-evaluator (accessed on 29 June 2020).

- OECD OECD Economic Outlook, June 2020. Available online: http://www.oecd.org/economic-outlook/june-2020/ (accessed on 29 June 2020).

- Macroeconomic Policy in the Time of COVID-19: A Primer for Developing Countries. Available online: https://documents.worldbank.org/en/publication/documents-reports/documentdetail (accessed on 29 June 2020).

- Cochrane, J.H. Coronavirus monetary policy. In Economics in the Time of COVID-19; Centre for Economic Policy Research: London, UK, 2020; pp. 105–108. ISBN 978-1-912179-28-2. [Google Scholar]

- World Trade Organisations Trade Set to Plunge as COVID-19 Pandemic Upends Global Economy. Available online: https://www.wto.org/english/news_e/pres20_e/pr855_e.htm (accessed on 29 June 2020).

- Eurostat Comext Datasets. Available online: http://epp.eurostat.ec.europa.eu/newxtweb/ (accessed on 29 June 2020).

- European Commission The impact of COVID Confinement Measures on EU Labour Market. Available online: https://ec.europa.eu/jrc/sites/jrcsh/files/jrc.120585_policy.brief_impact.of_.covid-19.on_.eu-labour.market.pdf (accessed on 29 June 2020).

- Eurostat Eurostat—Data Explorer. Available online: https://appsso.eurostat.ec.europa.eu/nui/show.do?dataset=une_rt_m&lang=en (accessed on 29 June 2020).

- Beck, T. Finance in the times of coronavirus. CEPR, 73–76. In Economics in the Time of COVID-19; Centre for Economic Policy Research: London, UK, 2020; pp. 73–76. ISBN 978-1-912179-28-2. [Google Scholar]

- Refinitiv Datastream Macroeconomic Analysis. Available online: http://solutions.refinitiv.com/datastream-macroeconomic-analysis (accessed on 29 June 2020).

- Beber, A.; Breedon, F.; Buraschi, A. Differences in beliefs and currency risk premiums. J. Financ. Econ. 2010, 98, 415–438. [Google Scholar] [CrossRef]

- Campa, J.M.; Chang, P.H.K.; Reider, R.L. Implied exchange rate distributions: Evidence from OTC option markets. J. Int. Money Financ. 1998, 17, 117–160. [Google Scholar] [CrossRef]

- Gunay, S. COVID-19 Pandemic versus global financial crisis: Evidence from currency market. SSRN J. 2020. [Google Scholar] [CrossRef]

- Engle, R.F. Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica 1982, 50, 987. [Google Scholar] [CrossRef]

- Bollerslev, T. Modelling the coherence in short-run nominal exchange rates: A multivariate generalized arch model. Rev. Econ. Stat. 1990, 72, 498. [Google Scholar] [CrossRef]

- Bekaert, G.; Wu, G. Asymmetric volatility and risk in equity markets. Rev. Financ. Stud. 2000, 13, 1–42. [Google Scholar] [CrossRef]

- Wang, J.; Yang, M. Asymmetric volatility in the foreign exchange markets. J. Int. Financ. Mark. Inst. Money 2009, 19, 597–615. [Google Scholar] [CrossRef]

- Ning, C.; Xu, D.; Wirjanto, T.S. Is volatility clustering of asset returns asymmetric? J. Bank. Financ. 2015, 52, 62–76. [Google Scholar] [CrossRef]

- Lim, C.M.; Sek, S.K. Comparing the performances of GARCH-type models in capturing the stock market volatility in Malaysia. Procedia Econ. Financ. 2013, 5, 478–487. [Google Scholar] [CrossRef]

- Ausloos, M.; Zhang, Y.; Dhesi, G. Stock index futures trading impact on spot price volatility. The CSI 300 studied with a TGARCH model. Expert Syst. Appl. 2020, 160, 113688. [Google Scholar] [CrossRef]

- Sabiruzzaman, M.; Monimul, H.M.; Beg, R.A.; Anwar, S. Modeling and forecasting trading volume index: GARCH versus TGARCH approach. Q. Rev. Econ. Financ. 2010, 50, 141–145. [Google Scholar] [CrossRef]

- Glosten, L.R.; Jagannathan, R.; Runkle, D.E. On the relation between the expected value and the volatility of the nominal excess return on stocks. J. Financ. 1993, 48, 1779–1801. [Google Scholar] [CrossRef]

- Nelson, D.B. Conditional heteroskedasticity in asset returns: A new approach. Econometrica 1991, 59, 347–370. [Google Scholar] [CrossRef]

- Hamilton, J.D. Time Series Analysis; Princeton Unviersity Press: Princeton, NJ, USA, 1994. [Google Scholar]

- Sharif, A.; Aloui, C.; Yarovaya, L. COVID-19 pandemic, oil prices, stock market, geopolitical risk and policy uncertainty nexus in the US economy: Fresh evidence from the wavelet-based approach. Int. Rev. Financ. Anal. 2020, 70, 101496. [Google Scholar] [CrossRef]

- Dickey, D.A.; Fuller, W.A. Distribution of the estimators for autoregressive time series with a unit root. J. Am. Stat. Assoc. 1979, 74, 427–431. [Google Scholar] [CrossRef]

- Akaike, H. Canonical correlation analysis of time series and the use of an information criterion. In Mathematics in Science and Engineering; Mehra, R.K., Lainiotis, D.G., Eds.; Elsevier: New York, NY, USA, 1976; Volume 126, pp. 27–96. [Google Scholar]

- Ma, X.; Yang, R.; Zou, D.; Liu, R. Measuring extreme risk of sustainable financial system using GJR-GARCH model trading data-based. Int. J. Inf. Manag. 2020, 50, 526–537. [Google Scholar] [CrossRef]

- Yeh, Y.H.; Lee, T.S. The interaction and volatility asymmetry of unexpected returns in the greater China stock markets. Glob. Financ. J. 2000, 11, 129–149. [Google Scholar] [CrossRef]

- Enders, W. Applied Econometric Time Series, 4th ed.; John Willey & Sons: Hoboken, NJ, USA, 2014. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Country | Czechia | Hungary | Poland | Slovakia |

|---|---|---|---|---|

| First case | 01.03.2020 | 04.03.2020 | 04.03.2020 | 07.03.2020 |

| Number of cases | 11,604 | 4145 | 34,154 | 1665 |

| Number of cases/1M pop | 1084 | 429 | 902 | 305 |

| No. of deaths | 348 | 585 | 1444 | 28 |

| No. of deaths/1M pop | 32 | 61 | 38 | 5 |

| Total tests | 545,873 | 273,897 | 1,493,993 | 208,966 |

| Total tests/1M pop | 50,983 | 28,353 | 39,475 | 38,275 |

| Deaths/cases | 0.030 | 0.141 | 0.042 | 0.017 |

| Population | 10,708,097 | 9,661,388 | 37,848,394 | 5,459,526 |

| Factors | Czechia | Hungary | Poland | Slovakia | ||||

|---|---|---|---|---|---|---|---|---|

| Nov. 2019 | May 2020 | Nov. 2019 | May 2020 | Nov. 2019 | May 2020 | Nov. 2019 | May 2020 | |

| Economic risk index (ERI) (1–10) | 2.9 | 2.8 | 3.8 | 3.8 | 3.3 | 3.2 | 3.2 | 3.1 |

| Rank out of 164 (ERI) | 16 | 12 | 39 | 42 | 30 | 26 | 26 | 23 |

| Dependent Variables | TGARCH (1,1) | TGARCH (2,1) | TGARCH (1,2) | TGARCH (2,2) |

|---|---|---|---|---|

| EUR/CZK | −10.732 | −10.732 | −10.731 | −10.718 |

| Prague PX | −7012 | −7010 | −7011 | −7011 |

| EUR/HUF | −8666 | −8665 | −8664 | −8664 |

| Budapest BUX | −6397 | −6396 | −6393 | −6395 |

| EUR/PLN | −8821 | −8821 | −8820 | −8820 |

| Warsaw WIG20 | −6290 | −6291 | −6289 | −6289 |

| Bratislava SAX | −6536 | −6540 | −6535 | −6544 |

| Parameters | EUR/CZK | PX | EUR/HUF | BUX | EUR/PLN | WIG20 | SAX |

|---|---|---|---|---|---|---|---|

| β | 0.01 *** | −0.02 ** | 0.01 ** | −0.02 ** | 0.01 *** | −0.02 ** | −0.01 *** |

| α0 | 0.01 *** | 0.01 *** | 0.01 * | 0.01 *** | 0.01 *** | 0.01 *** | 0.01 *** |

| α1 | 0.48 *** | 0.03 | 0.08 *** | 0.03 * | 0.13 *** | −0.04 * | 0.09 *** |

| α2 | - | - | - | - | - | 0.05 * | −0.07 *** |

| γ | −0.28 *** | 0.15 *** | −0.06 *** | 0.13 *** | −0.08 *** | 0.10 *** | −0.02 *** |

| φ1 | 0.80 *** | 0.85 *** | 0.94 *** | 0.85 *** | 0.87 *** | 0.90 *** | 1.67 *** |

| φ2 | - | - | - | - | - | - | −0.69 *** |

| ω | 0.78 *** | 1.25 *** | 1.63 *** | 1.32 *** | 1.36 *** | 1.23 *** | 1.57 *** |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Czech, K.; Wielechowski, M.; Kotyza, P.; Benešová, I.; Laputková, A. Shaking Stability: COVID-19 Impact on the Visegrad Group Countries’ Financial Markets. Sustainability 2020, 12, 6282. https://doi.org/10.3390/su12156282

Czech K, Wielechowski M, Kotyza P, Benešová I, Laputková A. Shaking Stability: COVID-19 Impact on the Visegrad Group Countries’ Financial Markets. Sustainability. 2020; 12(15):6282. https://doi.org/10.3390/su12156282

Chicago/Turabian StyleCzech, Katarzyna, Michał Wielechowski, Pavel Kotyza, Irena Benešová, and Adriana Laputková. 2020. "Shaking Stability: COVID-19 Impact on the Visegrad Group Countries’ Financial Markets" Sustainability 12, no. 15: 6282. https://doi.org/10.3390/su12156282

APA StyleCzech, K., Wielechowski, M., Kotyza, P., Benešová, I., & Laputková, A. (2020). Shaking Stability: COVID-19 Impact on the Visegrad Group Countries’ Financial Markets. Sustainability, 12(15), 6282. https://doi.org/10.3390/su12156282