The Inclusion of Socially Irresponsible Companies in Sustainable Stock Indices

,

,  and

and

Abstract

1. Introduction

2. Literature Review

3. Database Description

3.1. The Dow Jones Sustainability Index

3.2. The Selection of Companies

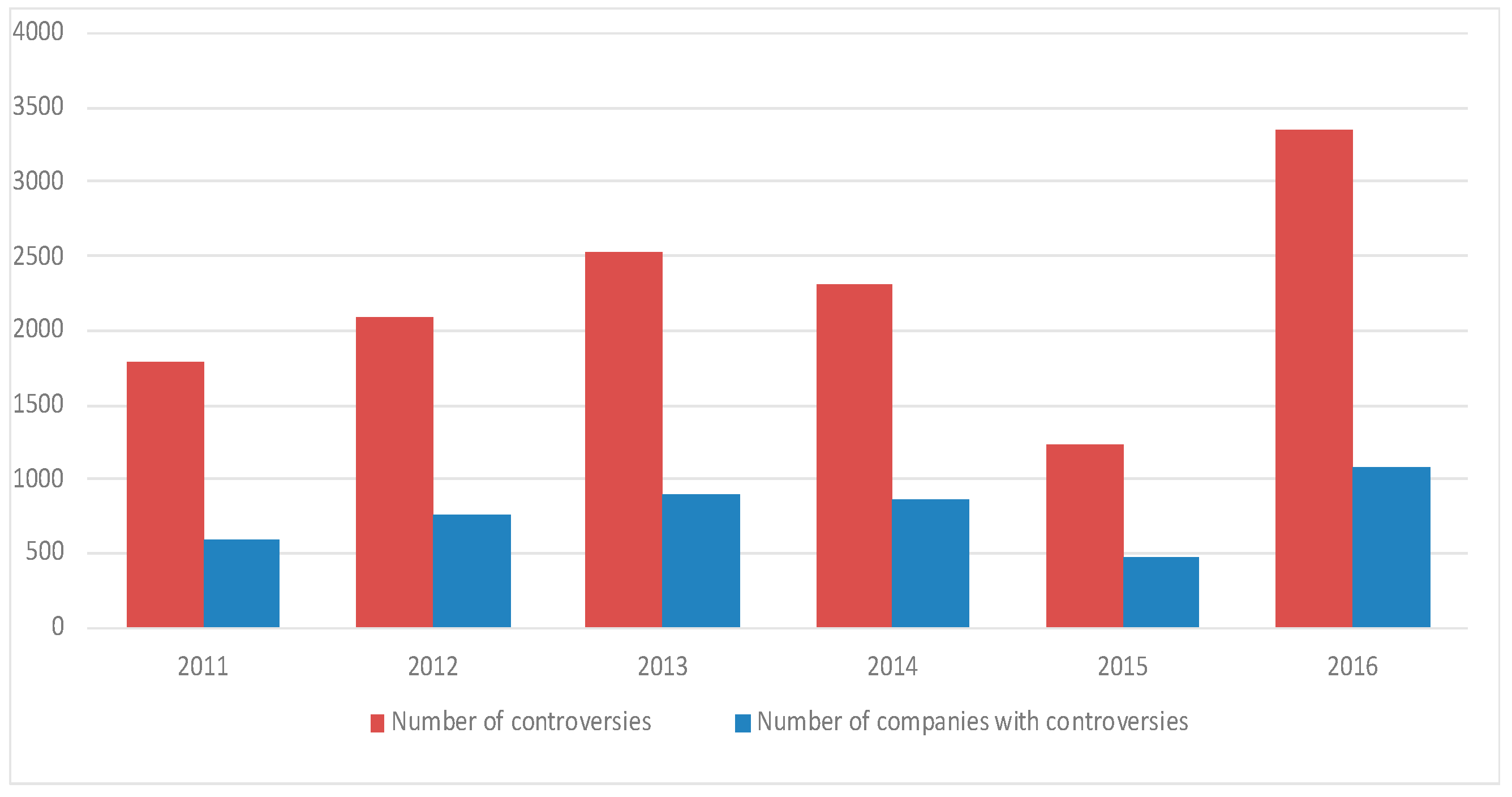

3.3. Controversies in the Thomson Reuters Eikon Database

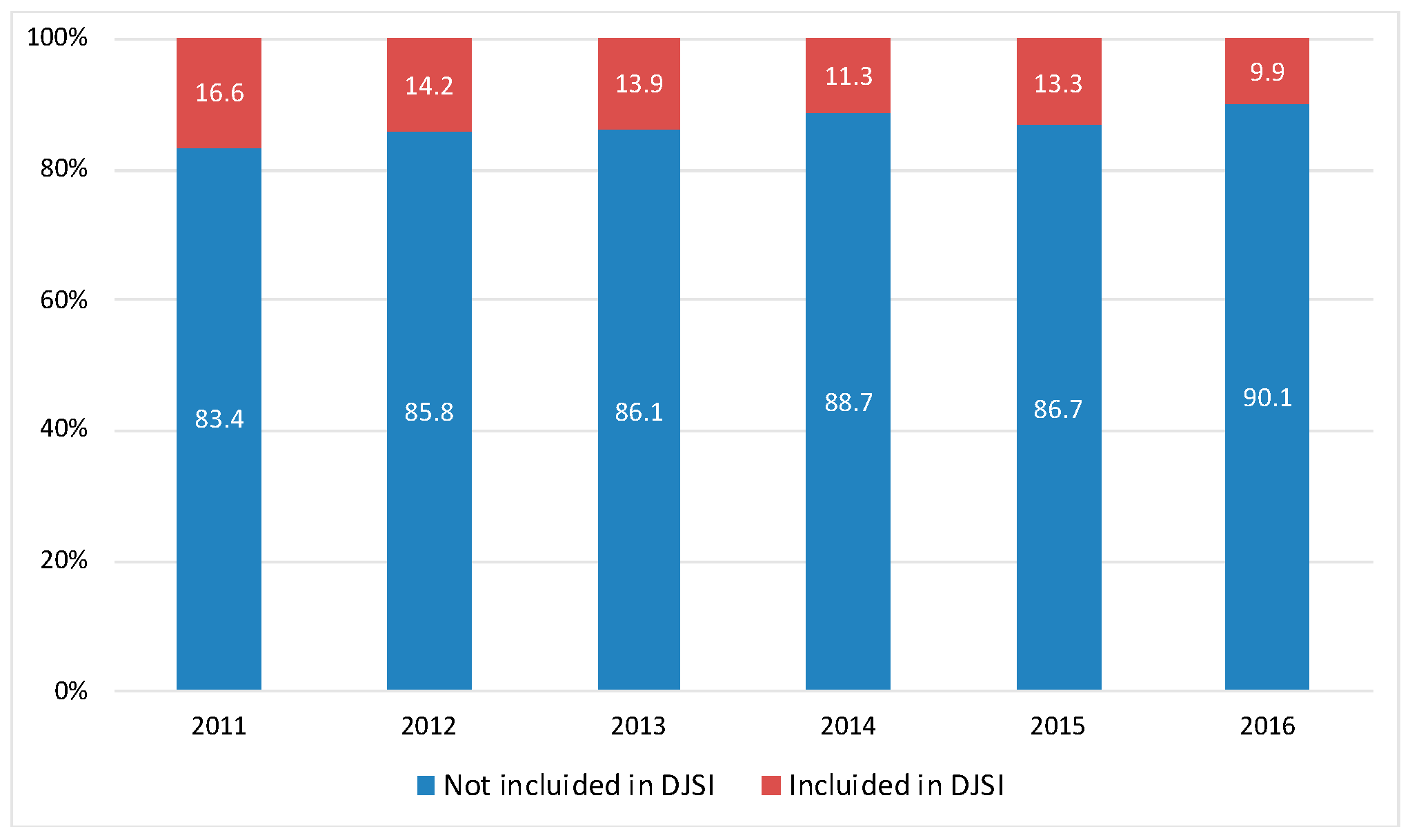

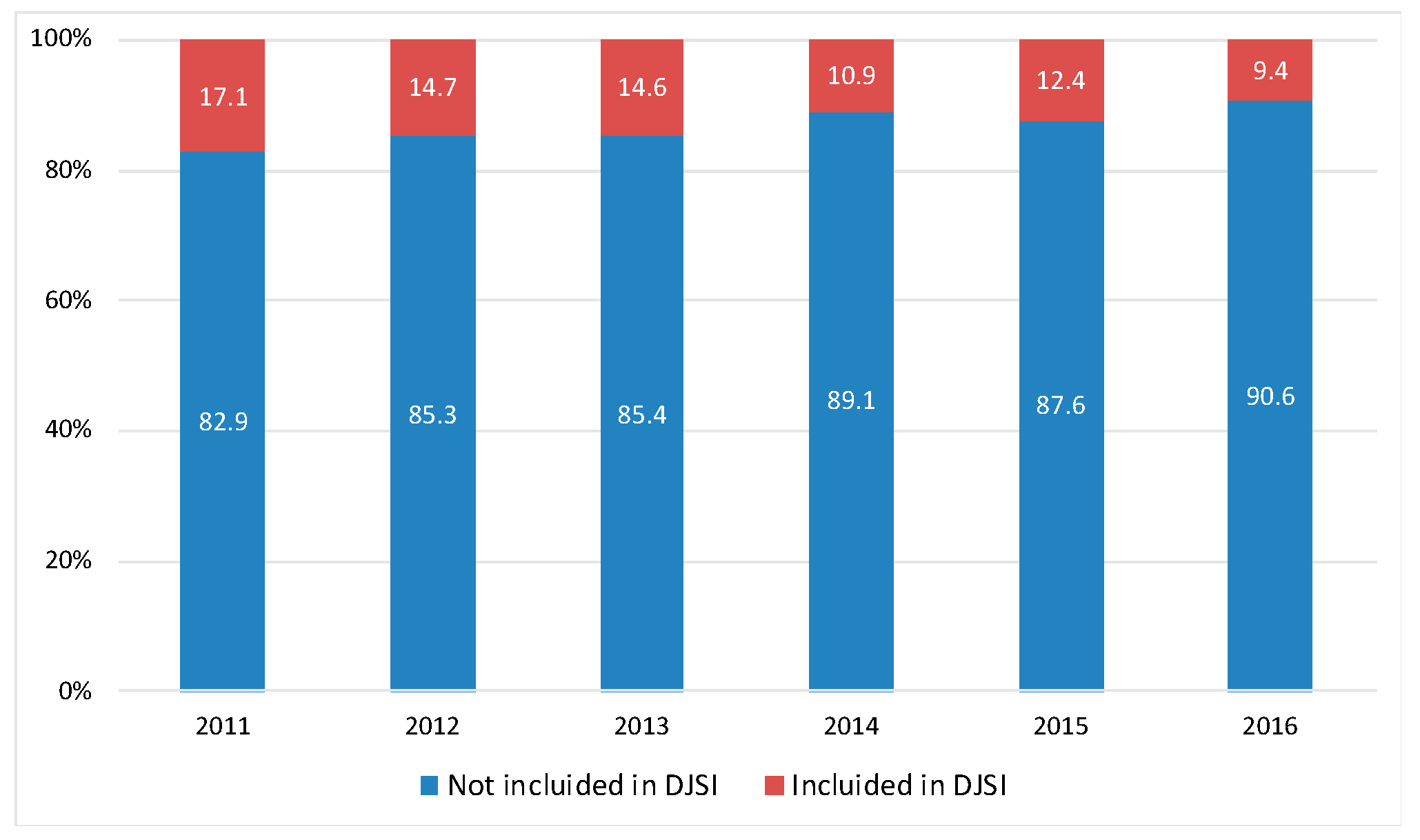

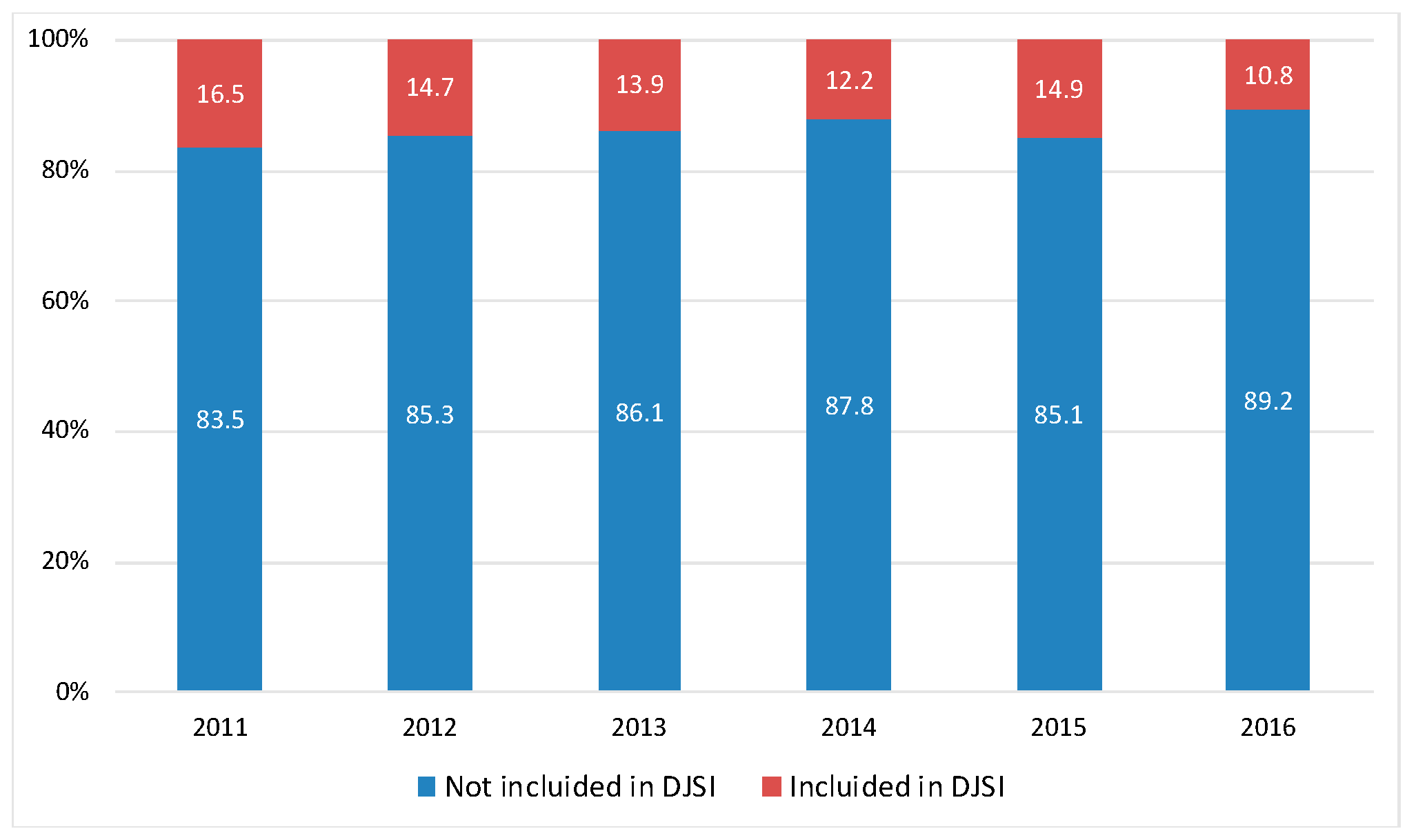

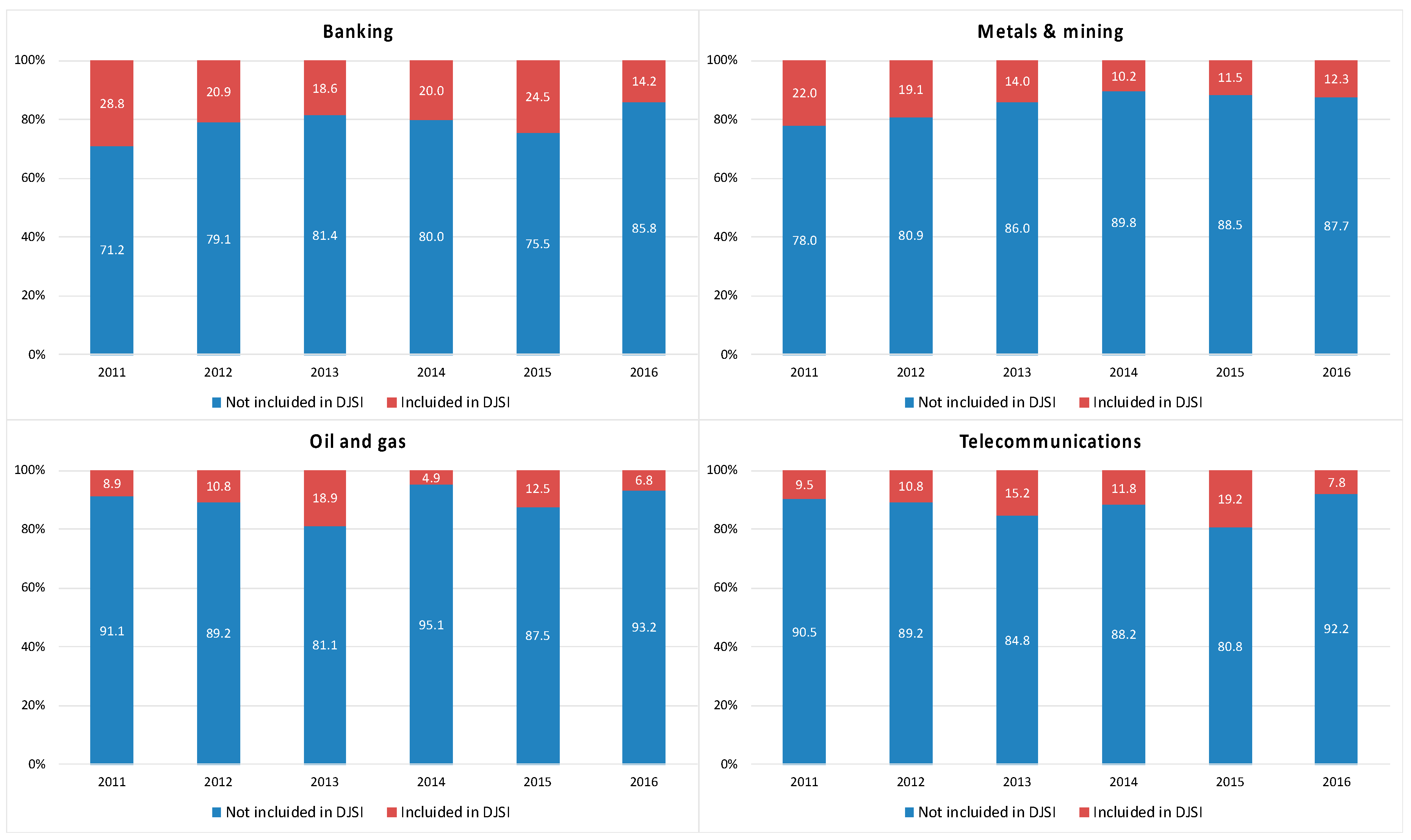

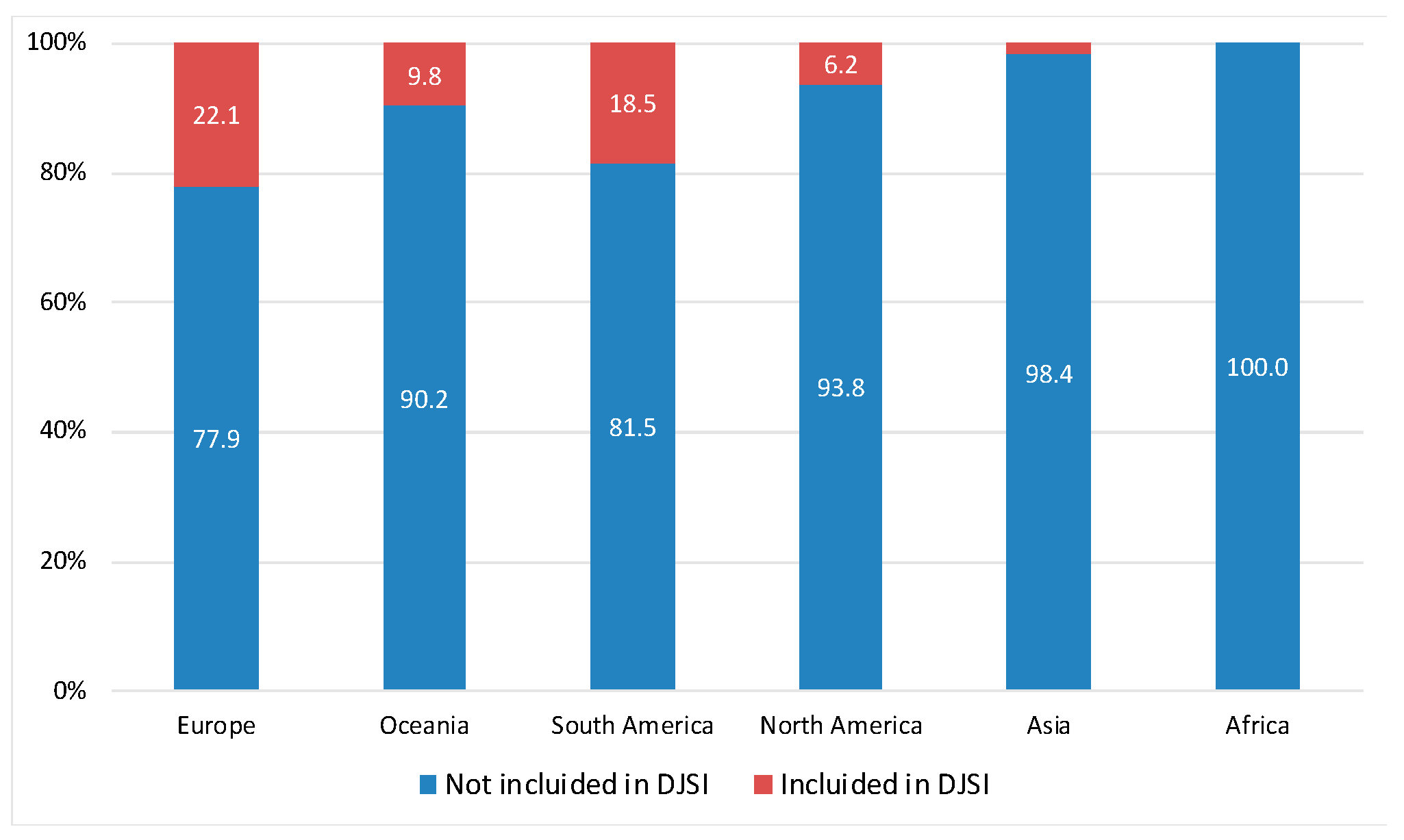

4. Results and Discussion

Analysis of the Controversies Reported in the EIKON Database Relating to Companies Included in the DJSI World Index

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Ou, Y.C. Using a hybrid decision-making model to evaluate the sustainable development performance of high-tech listed companies. J. Bus. Econ. Manag. 2016, 17, 331–346. [Google Scholar] [CrossRef]

- Halkos, G.; Skouloudis, A. Revisiting the relationship between corporate social responsibility and national culture: A quantitative assessment. Manag. Decis. 2017, 55, 595–613. [Google Scholar] [CrossRef]

- Halkos, G.; Skouloudis, A. National CSR and institutional conditions: An exploratory study. J. Clean. Prod. 2016, 139, 1150–1156. [Google Scholar] [CrossRef]

- Skouloudis, A.; Evangelinos, K. A research design for mapping national CSR terrains. J. Sustain. Dev. World Ecol. 2012, 19, 130–143. [Google Scholar] [CrossRef]

- Achim, M.V.; Borlea, S.N.; Mare, C. Corporate governance and business performance: Evidence for the Romanian economy. J. Bus. Econ. Manag. 2016, 17, 458–474. [Google Scholar] [CrossRef]

- Silvestre, W.J.; Antunes, P.; Filho, W.L. The corporate sustainability typology: Analysing sustainability drivers and fostering sustainability at enterprises. Technol. Econ. Dev. Econ. 2018, 24, 513–533. [Google Scholar] [CrossRef]

- Rodriguez-Fernandez, M. Social responsibility and financial performance: The role of good corporate governance. BRQ Bus. Res. Q. 2016, 19, 137–151. [Google Scholar] [CrossRef]

- Tebini, H.; M’Zali, B.; Lang, P.; Perez-Gladish, B. The economic impact of environmentally responsible practices. Corp. Soc. Responsib. Environ. Manag. 2016, 23, 333–344. [Google Scholar] [CrossRef]

- Gherghina, Ş.C.; Vintilă, G. Exploring the impact of corporate social responsibility policies on firm value: The case of listed companies in Romania. Econ. Sociol. 2016, 9, 23–42. [Google Scholar] [CrossRef]

- Li, S.; Ngniatedema, T.; Chen, F. Understanding the impact of green initiatives and green performance on financial performance in the US. Bus. Strateg. Environ. 2017, 79, 776–790. [Google Scholar] [CrossRef]

- Jankalová, M.; Jankal, R. The assessment of corporate social responsibility: Approaches analysis. Entrep. Sustain. Issues 2017, 4, 441–459. [Google Scholar] [CrossRef]

- García-Melón, M.; Pérez-Gladish, B.; Gómez-Navarro, T.; Mendez-Rodriguez, P. Assessing mutual funds’ corporate social responsibility: A multistakeholder-AHP based methodology. Ann. Oper. Res. 2016, 244, 475–503. [Google Scholar] [CrossRef]

- Miralles-Quirós, M.M.; Miralles-Quirós, J.L. Improving diversification opportunities for socially responsible investors. J. Bus. Ethics 2017, 140, 339–351. [Google Scholar] [CrossRef]

- GSIA. Global Sustainable Investment Review 2016; GSIA: Washington, DC, USA, 2016; Available online: http://www.gsi-alliance.org/wp-content/uploads/2017/03/GSIR_Review2016.F.pdf (accessed on 17 October 2018).

- Schwartz, M.S. The “ethics” of ethical investing. J. Bus. Ethics 2003, 43, 195–213. [Google Scholar] [CrossRef]

- Hellsten, S.; Mallin, C. Are “ethical” or “socially responsible” investments socially responsible? J. Bus. Ethics 2006, 66, 393–406. [Google Scholar] [CrossRef]

- Chatterji, A.; Levine, D. Breaking down the wall of codes: Evaluating non-financial performance measurement. Calif. Manag. Rev. 2006, 48, 29–51. [Google Scholar] [CrossRef]

- Renneboog, L.; Ter Horst, J.; Zhang, C. Socially responsible investments: Institutional aspects, performance, and investor behavior. J. Bank. Financ. 2008, 32, 1723–1742. [Google Scholar] [CrossRef]

- Capelle-Blancard, G.; Monjon, S. Trends in the literature on socially responsible investment: Looking for the keys under the lamppost. Bus. Ethics 2012, 21, 239–250. [Google Scholar] [CrossRef]

- Markowitz, H. Portfolio selection. J. Financ. 1952, 7, 77–91. [Google Scholar]

- Markowitz, H. Portfolio Selection: Efficient Diversification of Investments; Yale University Press: New Haven, CT, USA, 1959. [Google Scholar]

- Arribas, I.; Espinós-Vañó, M.D.; García, F.; Tamosiuniene, R. Negative screening and sustainable portfolio diversification. Int. J. Entrep. Sustain. Issues 2019, forthcoming. [Google Scholar]

- Trinks, P.J.; Scholtens, B. The opportunity cost of negative screening in socially responsible investing. J. Bus. Ethics 2017, 140, 193–208. [Google Scholar] [CrossRef]

- Nainggolan, Y.; How, J.; Verhoeven, P. Ethical screening and financial performance: The case of islamic equity funds. J. Bus. Ethics 2016, 137, 83–99. [Google Scholar] [CrossRef]

- Lesser, K.; Rößle, F.; Walkshäusl, C. Socially responsible, green, and faith-based investment strategies: Screening activity matters! Financ. Res. Lett. 2016, 16, 171–178. [Google Scholar] [CrossRef]

- Von Wallis, M.; Klein, C. Ethical requirement and financial interest: A literature review on socially responsible investing. Bus. Res. 2015, 8, 61–98. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Prentice Hall: Boston, MA, USA, 1984. [Google Scholar]

- Girerd-Potin, I.; Jimenez-Garces, S.; Louvet, P. Which dimensions of social responsibility concern financial investors? J. Bus. Ethics 2014, 121, 559–576. [Google Scholar] [CrossRef]

- Bertrand, P.; Lapointe, V. How performance of risk-based strategies is modified by socially responsible investment universe? Int. Rev. Financ. Anal. 2014, 38, 175–190. [Google Scholar] [CrossRef]

- Lean, H.H.; Ang, W.R.; Smyth, R. Performance and performance persistence of socially responsible investment funds in Europe and North America. N. Am. J. Econ. Financ. 2015, 34, 254–266. [Google Scholar] [CrossRef]

- Lyn, E.O.; Zychowicz, E.J. The impact of faith-based screens on investment performance. J. Investig. 2010, 19, 136–143. [Google Scholar] [CrossRef]

- Xiao, Y.; Faff, R.; Gharghori, P. The financial performance of socially responsible investments: Insights from the Intertemporal CAPM. J. Bus. Ethics 2017, 146, 353–364. [Google Scholar] [CrossRef]

- Reddy, K.; Mirza, N.; Naqvi, B.; Fu, M. Comparative risk adjusted performance of Islamic, socially responsible and conventional funds: Evidence from United Kingdom. Econ. Model. 2017, 66, 233–243. [Google Scholar] [CrossRef]

- Muñoz, F.; Vargas, M.; Marco, I. Environmental mutual funds: Financial performance and managerial abilities. J. Bus. Ethics 2014, 124, 551–569. [Google Scholar] [CrossRef]

- Van Duuren, E.; Plantinga, A.; Scholtens, B. ESG integration and the investment management process: Fundamental investing reinvented. J. Bus. Ethics 2016, 138, 525–533. [Google Scholar] [CrossRef]

- Ibikunle, G.; Steffen, T. European green mutual fund performance: A comparative analysis with their conventional and black peers. J. Bus. Ethics 2017, 145, 337–355. [Google Scholar] [CrossRef]

- Revelli, C.; Viviani, J.L. Financial performance of socially responsible investing (SRI): What have we learned? A meta-analysis. Bus. Ethics A Eur. Rev. 2015, 24, 158–185. [Google Scholar] [CrossRef]

- Renneboog, L.; Ter Horst, J.; Zhang, C. Is ethical money financially smart? Nonfinancial attributes and money flows of socially responsible investment funds. J. Financ. Intermed. 2011, 20, 562–588. [Google Scholar] [CrossRef]

- Humphrey, J.E.; Warren, G.J. What is different about socially responsible funds? A holdings-based analysis. J. Bus. Ethics 2016, 138, 263–277. [Google Scholar] [CrossRef]

- Charlo, M.J.; Moya, I.; Muñoz, A.M. Sustainable development in Spanish listed companies: A strategic approach. Corp. Soc. Responsib. Environ. Manag. 2017, 24, 222–234. [Google Scholar] [CrossRef]

- Charlo, M.J.; Moya, I.; Muñoz, A.M. Sustainable development and corporate financial performance: A study based on the FTSE4Good IBEX index. Bus. Strateg. Environ. 2015, 24, 277–288. [Google Scholar] [CrossRef]

- Windolph, S.E. Assessing corporate sustainability through ratings: Challenges and their causes. J. Environ. Sustain. 2011, 1, 1–22. [Google Scholar] [CrossRef]

- Searcy, C.; Elkhawas, D. Corporate sustainability ratings: An investigation into how corporations use the Dow Jones sustainability index. J. Clean. Prod. 2012, 35, 79–92. [Google Scholar] [CrossRef]

- Ziegler, A.; Schröder, M. What determines the inclusion in a sustainability stock index? A panel data analysis for European firms. Ecol. Econ. 2010, 69, 848–856. [Google Scholar] [CrossRef]

- Utz, S.; Wimmer, M. Are they any good at all? A financial and ethical analysis of socially responsible mutual funds. J. Asset Manag. 2014, 15, 72–82. [Google Scholar] [CrossRef]

- Gangi, F.; Varrone, N. Screening activities by socially responsible funds: A matter of agency? J. Clean. Prod. 2018, 197, 842–855. [Google Scholar] [CrossRef]

- Verheyden, T.; De Moor, L. Multi–criteria decision analysis: Methods to define and evaluate socially responsible investments. Int. J. Manag. Decis. Mak. 2014, 14, 44–65. [Google Scholar] [CrossRef]

- Lamata, M.T.; Liern, V.; Pérez-Gladish, B. Doing good by doing well: A MCDM framework for evaluating corporate social responsibility attractiveness. Ann. Oper. Res. 2018, 267, 249–266. [Google Scholar] [CrossRef]

- Escrig-Olmedo, E.; Muñoz-Torres, M.J.; Fernández-Izquierdo, M.Á.; Rivera-Lirio, J.M. Measuring corporate environmental performance: A methodology for sustainable development. Bus. Strateg. Environ. 2017, 26, 142–162. [Google Scholar] [CrossRef]

- Montiel, I.; Delgado-Ceballos, J. Defining and measuring corporate sustainability: Are we there yet? Organ. Environ. 2014, 27, 113–139. [Google Scholar] [CrossRef]

- Pérez-Gladish, B.; Méndez, P.; M’Zali, B. Ranking socially responsible mutual funds. Int. J. Energy Optim. Eng. 2012, 37, 559–594. [Google Scholar] [CrossRef]

- García-Martínez, G.; Guijarro, F.; Poyatos, J.A. Measuring the social responsibility of European companies: A goal programming approach. Int. Trans. Oper. Res. 2017, 26, 1074–1095. [Google Scholar] [CrossRef]

- Cervelló-Royo, R.; Guijarro, F.; Martinez-Gomez, V. Social Performance considered within the global performance of Microfinance Institutions: A new approach. Oper. Res. 2017, 1–19. [Google Scholar] [CrossRef]

- S&P Dow Jones Indices; RobecoSAM. Dow Jones Sustainability Indices. Methodology. Available online: https://www.sustainability-indices.com/ (accessed on 17 October 2018).

- Balcilar, M.; Demirer, R.; Gupta, R. Do sustainable stocks offer diversification benefits for conventional portfolios? An empirical analysis of risk spillovers and dynamic correlations. Sustainability 2017, 9, 1799. [Google Scholar] [CrossRef]

- RobecoSAM. Measuring “Intangibles”. Available online: https://www.robecosam.com/csa/csa-resources/csa-methodology.html (accessed on 15 October 2017).

- Thomson Reuters. Thomson Reuters ESG Scores. Available online: https://www.refinitiv.com/content/dam/marketing/en_us/documents/methodology/esg-scores-methodology.pdf (accessed on 17 October 2018).

- Aouadi, A.; Marsat, S. Do ESG controversies matter for firm value? Evidence from international data. J. Bus. Ethics 2018, 151, 1027–1047. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | |

|---|---|---|---|---|---|---|

| Community | 18.5 | 13.8 | 16.5 | 12.4 | 17.4 | 11.1 |

| Environment | 23.8 | 30.0 | 25.9 | 14.3 | 18.6 | 11.9 |

| Human rights | 20.6 | 21.4 | 33.3 | 7.1 | 9.1 | 27.3 |

| Management | 75.0 | 47.4 | 23.8 | 40.0 | 0.0 | 7.1 |

| Product | 25.6 | 20.6 | 14.7 | 13.0 | 11.0 | 12.1 |

| Shareholders | 20.0 | 16.4 | 13.2 | 13.0 | 15.1 | 11.5 |

| Workforce | 18.4 | 18.5 | 18.4 | 12.6 | 15.2 | 12.1 |

| 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | |

|---|---|---|---|---|---|---|

| Australia | 25.0 | 20.7 | 22.0 | 7.4 | 20.0 | 10.5 |

| Canada | 7.7 | 11.8 | 21.4 | 17.9 | 16.7 | 12.8 |

| China | 13.3 | 10.7 | 9.7 | 6.7 | 13.0 | 10.5 |

| France | 41.4 | 35.7 | 37.5 | 25.9 | 42.9 | 48.1 |

| Germany | 54.5 | 41.7 | 39.3 | 41.7 | 36.4 | 25.0 |

| India | 8.3 | 0.0 | 2.9 | 5.6 | 3.8 | 2.2 |

| Japan | 2.2 | 4.5 | 2.0 | 0.0 | 2.4 | 1.4 |

| South Korea | 13.3 | 10.7 | 9.7 | 6.7 | 13.0 | 10.5 |

| United Kingdom | 34.4 | 34.5 | 20.5 | 23.5 | 28.1 | 18.1 |

| United States | 8.1 | 7.4 | 7.7 | 5.6 | 8.5 | 5.4 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Arribas, I.; Espinós-Vañó, M.D.; García, F.; Morales-Bañuelos, P.B. The Inclusion of Socially Irresponsible Companies in Sustainable Stock Indices. Sustainability 2019, 11, 2047. https://doi.org/10.3390/su11072047

Arribas I, Espinós-Vañó MD, García F, Morales-Bañuelos PB. The Inclusion of Socially Irresponsible Companies in Sustainable Stock Indices. Sustainability. 2019; 11(7):2047. https://doi.org/10.3390/su11072047

Chicago/Turabian StyleArribas, Iván, María Dolores Espinós-Vañó, Fernando García, and Paula Beatriz Morales-Bañuelos. 2019. "The Inclusion of Socially Irresponsible Companies in Sustainable Stock Indices" Sustainability 11, no. 7: 2047. https://doi.org/10.3390/su11072047

APA StyleArribas, I., Espinós-Vañó, M. D., García, F., & Morales-Bañuelos, P. B. (2019). The Inclusion of Socially Irresponsible Companies in Sustainable Stock Indices. Sustainability, 11(7), 2047. https://doi.org/10.3390/su11072047