The Impact of Supply Chain Integration and Internal Control on Financial Performance in the Jordanian Banking Sector

Abstract

1. Introduction

2. Literature Review

2.1. Supply Chain Management Practices

2.2. Supply Chain Integration

2.2.1. Supplier Integration

2.2.2. Customer Integration

2.2.3. Internal Integration

2.3. Internal Control

2.4. Performance and Financial Performance

2.5. The Banking Sector in Jordan

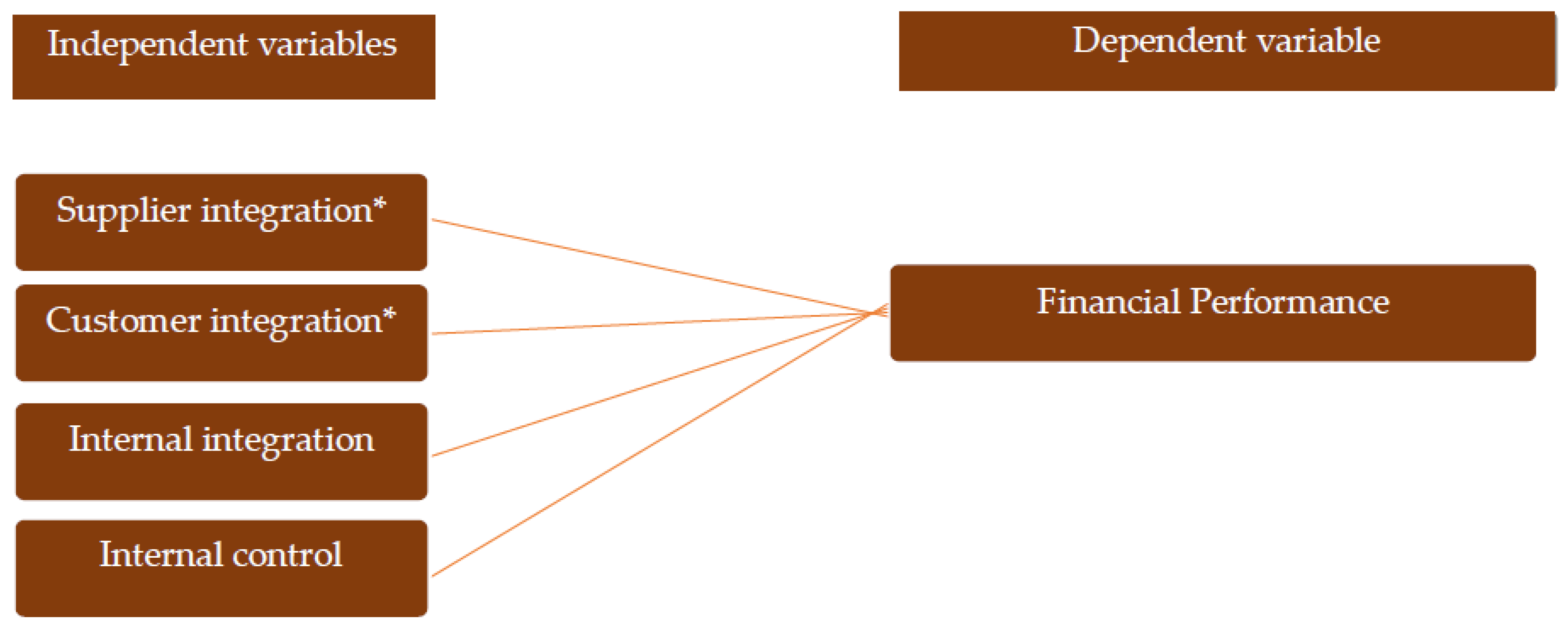

3. Conceptual Model and Research Hypotheses

3.1. Conceptual Model

3.2. Hypotheses Development

3.2.1. The Effect of Supply Chain Integration on Financial Performance

3.2.2. Internal Control and Financial Performance

3.3. Supply Chain Integration and Internal Control

3.3.1. Independent Variables

3.3.2. Dependent Variable

4. Material and Methods

4.1. Questionnaire Design

4.2. Research Population and Sample

4.3. Techniques for Data Analysis

5. Results and Discussion

5.1. Results

5.1.1. The Relationship between Supply Chain Integration, Internal Control, and Financial Performance

5.1.2. Exploring the Structure of Items

5.1.3. Promax Rotation

5.1.4. Reliability Test

5.1.5. The New Model after Rotation

5.2. Discussion

5.2.1. The Impact of Supply Chain Integration on Financial Performance

5.2.2. Customer Integration Influence on Financial Performance

5.2.3. Supplier Integration Influence on Financial Performance

5.2.4. Internal Integration Influence on Financial Performance

5.2.5. The Impact of Internal Control on Financial Performance

6. Conclusions

7. Recommendations

Supplementary Materials

Author Contributions

Funding

Conflicts of Interest

References

- Sroka, W.; Szántó, R. Corporate Social Responsibility and Business Ethics in Controversial Sectors: Analysis of Research Results. J. Entrep. Manag. Innov. 2018, 14, 111–126. [Google Scholar] [CrossRef]

- Sroka, W.; VVeinhardt, J. Nepotism and favouritism in the steel industry: A case study analysis. Forum Sientiae Oecon. 2018, 6, 31–45. [Google Scholar]

- Turkulainen, V.; Roh, J.; Whipple, J.M.; Swink, M. Managing Internal Supply Chain Integration: Integration Mechanisms and Requirements. J. Bus. Logist. 2017, 38, 290–309. [Google Scholar] [CrossRef]

- Sweeney, E. Innovation for Competing in Highly Competitive Markets in Supply Chain Innovation for Competing in Highly Competitive Markets: Challenges and Solutions; National Institute of Transport and Logistics: Dublin, Ireland, 2012. [Google Scholar]

- Oláh, J.; Karmazin, G.; Pető, K.; Popp, J. Information technology developments of logistics service providers in Hungary. Int. J. Logist. Res. Appl. 2018, 21, 332–344. [Google Scholar] [CrossRef]

- Flynn, B.B.; Huo, B.; Zhao, X. The impact of supply chain integration on performance: A contingency and configuration approach. J. Oper. Manag. 2010, 28, 58–71. [Google Scholar] [CrossRef]

- Kot, S. Sustainable Supply Chain Management in Small and Medium Enterprises. Sustainability 2018, 10, 1143. [Google Scholar] [CrossRef]

- Schoenherr, T.; Swink, M. Revisiting the arcs of integration: Cross-validations and extensions. J. Oper. Manag. 2012, 30, 99–115. [Google Scholar] [CrossRef]

- Ataseven, C.; Nair, A. Assessment of supply chain integration and performance relationships: A meta-analytic investigation of the literature. Int. J. Prod. Econ. 2017, 185, 252–265. [Google Scholar] [CrossRef]

- Haddad, H. Internal Controls in Jordanian Banks and Compliance Risk. Res. J. Financ. Acc. 2016, 7, 17–31. [Google Scholar]

- Lutz, J. Committee of Sponsoring Organizations of the Treadway Commission: Internal Control; Integrated Framework Mit Besonderer Berücksichtigung der Änderungen in der Neuauflage 2013. Master’s Thesis, Hochschule Mittweida, Mittweida, Germany, 2015. [Google Scholar]

- De Souza Miguel, P.L.; Brito, L.A.L. Supply Chain Management measurement and its influence on Operational Performance. J. Oper. Suppl. Chain Manag. 2011, 4, 56–70. [Google Scholar] [CrossRef]

- Abdallah, A.B.; Obeidat, B.Y.; Aqqad, N.O. The impact of supply chain management practices on supply chain performance in Jordan: The moderating effect of competitive intensity. Int. Bus. Res. 2014, 7, 13. [Google Scholar] [CrossRef]

- Jabbour, A.B.L.; Filho, A.G.A.; Viana, A.B.N.; Jabbour, C.J.C. Measuring supply chain management practices. Meas. Bus. Excell. 2011, 15, 18–31. [Google Scholar] [CrossRef]

- Lotfi, Z.; Mukhtar, M.; Sahran, S.; Zadeh, A.T. Information sharing in supply chain management. Procedia Technol. 2013, 11, 298–304. [Google Scholar] [CrossRef]

- Wong, C.W.; Wong, C.Y.; Boon-itt, S. The combined effects of internal and external supply chain integration on product innovation. Int. J. Prod. Econ. 2013, 146, 566–574. [Google Scholar] [CrossRef]

- Slusarczyk, B.; Smolag, K.; Kot, S. The Supply Chain of a Tourism Product. Actual Probl. Econ. 2016, 197–207. Available online: http://nbuv.gov.ua/UJRN/ape_2016_5_23 (accessed on 26 February 2019).

- Lii, P.; Kuo, F.-I. Innovation-oriented supply chain integration for combined competitiveness and firm performance. Int. J. Prod. Econ. 2016, 174, 142–155. [Google Scholar] [CrossRef]

- Qi, Y.; Huo, B.; Wang, Z.; Yeung, H.Y.J. The impact of operations and supply chain strategies on integration and performance. Int. J. Prod. Econ. 2017, 185, 162–174. [Google Scholar] [CrossRef]

- Ince, H.; Imamoglu, S.Z.; Keskin, H.; Akgun, A.; Efe, M.N. The impact of ERP systems and supply chain management practices on firm performance: Case of Turkish companies. Procedia-Soc. Behav. Sci. 2013, 99, 1124–1133. [Google Scholar] [CrossRef]

- Silvestro, R.; Lustrato, P. Integrating financial and physical supply chains: The role of banks in enabling supply chain integration. Int. J. Oper. Prod. Manag. 2014, 34, 298–324. [Google Scholar] [CrossRef]

- Yang, C.-C.; Wei, H.-H. The effect of supply chain security management on security performance in container shipping operations. Suppl. Chain Manag. Int. J. 2013, 18, 74–85. [Google Scholar] [CrossRef]

- Kim, D.-Y. Relationship between supply chain integration and performance. Oper. Manag. Res. 2013, 6, 74–90. [Google Scholar] [CrossRef]

- Danese, P. Supplier integration and company performance: A configurational view. Omega 2013, 41, 1029–1041. [Google Scholar] [CrossRef]

- Oláh, J.; Bai, A.; Karmazin, G.; Balogh, P.; Popp, J. The role played by trust and its effect on the competiveness of logistics service Providers in Hungary. Sustainability 2017, 9, 2303. [Google Scholar] [CrossRef]

- Lau, A.K.; Yam, R.C.; Tang, E.P. Supply chain integration and product modularity: An empirical study of product performance for selected Hong Kong manufacturing industries. Int. J. Oper. Prod. Manag. 2010, 30, 20–56. [Google Scholar] [CrossRef]

- Koufteros, X.; Verghese, A.J.; Lucianetti, L. The effect of performance measurement systems on firm performance: A cross-sectional and a longitudinal study. J. Oper. Manag. 2014, 32, 313–336. [Google Scholar] [CrossRef]

- Narasimhan, R.; Narayanan, S.; Srinivasan, R. Explicating the mediating role of integrative supply management practices in strategic outsourcing: A case study analysis. Int. J. Prod. Res. 2010, 48, 379–404. [Google Scholar] [CrossRef]

- Kotcharin, S.; Eldridge, S.; Freeman, J. Investigating the relationships between internal integration and external integration and their impact on combinative competitive capabilities. In Proceedings of the 17th International Working Seminar on Production Economics, Innsbruck, Austria, 20–24 February 2012; pp. 1–12. [Google Scholar]

- Ayoub, H.F.; Abdallah, A.B.; Suifan, T.S. The effect of supply chain integration on technical innovation in Jordan: The mediating role of knowledge management. Benchmarking 2017, 24, 594–616. [Google Scholar] [CrossRef]

- Länsiluoto, A.; Jokipii, A.; Eklund, T. Internal control effectiveness–a clustering approach. Manag. Audit. J. 2016, 31, 5–34. [Google Scholar] [CrossRef]

- Pallant, J. SPSS Survival Manual, 2nd ed.; Open University Press: Berkshire, UK, 2005. [Google Scholar]

- Ayagre, P.; Appiah-Gyamerah, I.; Nartey, J. The effectiveness of Internal Control Systems of banks. The case of Ghanaian banks. Int. J. Acc. Financ. Rep. 2014, 4, 377–389. [Google Scholar] [CrossRef]

- IIA Institute of Internal Auditors: Lake Mary, USA. 2013. Available online: https://global.theiia.org/Pages/globaliiaHome.aspx (accessed on 26 February 2019).

- Wheelen, T.L.; Hunger, J.D.; Hoffman, A.N.; Bamford, C.E. Strategic Management and Business Policy: Toward Global Sustainability; Pearson Education Inc.: London, UK, 2017; ISBN 978-0132153225. [Google Scholar]

- Huo, B. The impact of supply chain integration on company performance: An organizational capability perspective. Suppl. Chain Manag. Int. J. 2012, 17, 596–610. [Google Scholar] [CrossRef]

- Appiah-Adu, K. Market orientation and performance: Empirical tests in a transition economy. J. Strateg. Mark. 1998, 6, 25–45. [Google Scholar] [CrossRef]

- Jitpaiboon, T.; Dobrzykowski, D.D.; Ragu-Nathan, T.; Vonderembse, M.A. Unpacking IT use and integration for mass customisation: A service-dominant logic view. Int. J. Prod. Res. 2013, 51, 2527–2547. [Google Scholar] [CrossRef]

- Chang, W.; Ellinger, A.E.; Kim, K.K.; Franke, G.R. Supply chain integration and firm financial performance: A meta-analysis of positional advantage mediation and moderating factors. Eur. Manag. J. 2016, 34, 282–295. [Google Scholar] [CrossRef]

- Mafini, C.; Pooe, D.R. The relationship between employee satisfaction and organisational performance: Evidence from a South African government department. SA J. Ind. Psychol. 2013, 39. [Google Scholar] [CrossRef]

- Mele, C.; Russo Spena, T.; Colurcio, M. Co-creating value innovation through resource integration. Int. J. Qual. Serv. Sci. 2010, 2, 60–78. [Google Scholar] [CrossRef]

- Zhao, X.; Huo, B.; Selen, W.; Yeung, J.H.Y. The impact of internal integration and relationship commitment on external integration. J. Oper. Manag. 2011, 29, 17–32. [Google Scholar] [CrossRef]

- Kliestik, T.; Misankova, M.; Valaskova, K.; Svabova, L. Bankruptcy Prevention: New Effort to Reflect on Legal and Social Changes. Sci. Eng. Ethics 2018, 24, 791–803. [Google Scholar] [CrossRef] [PubMed]

- Zhang, C.; Gunasekaran, A.; Wang, W.Y.C. A comprehensive model for supply chain integration. Benchmarking 2015, 22, 1141–1157. [Google Scholar] [CrossRef]

- Yu, W.; Jacobs, M.A.; Salisbury, W.D.; Enns, H. The effects of supply chain integration on customer satisfaction and financial performance: An organizational learning perspective. Int. J. Prod. Econ. 2013, 146, 346–358. [Google Scholar] [CrossRef]

- Msimangira, K.A.; Venkatraman, S. Supply chain management integration: Critical problems and solutions. Oper. Suppl. Chain Manag. 2014, 7, 23–31. [Google Scholar] [CrossRef]

- Demeter, K.; Szász, L.; Rácz, B.-G. The impact of subsidiaries’ internal and external integration on operational performance. Int. J. Prod. Econ. 2016, 182, 73–85. [Google Scholar] [CrossRef]

- Kliestik, T.; Kovacova, M.; Podhorska, I.; Kliestikova, J. Searching for key sources of goodwill creation as new global managerial challenge. Pol. J. Manag. Stud. 2018, 17, 144–154. [Google Scholar] [CrossRef]

- Hannah, N. The Effect of Internal Controls on Revenue Generation: A Case Study of the University of Nairobi Enterprise and Services Limited. Master’s Thesis, University of Nairobi, Nairobi, Kenya, 2013. [Google Scholar]

- Brunswicker, S.; Chesbrough, H. The Adoption of Open Innovation in Large Firms: Practices, Measures, and Risks A survey of large firms examines how firms approach open innovation strategically and manage knowledge flows at the project level. Res. Technol. Manag. 2018, 61, 35–45. [Google Scholar] [CrossRef]

- Werner, M.; Gehrke, N. Identifying the Absence of Effective Internal Controls-An Alternative Approach for Internal Control Audits. J. Inf. Syst. 2018. [Google Scholar] [CrossRef]

- Carnes, R.R.; Christensen, D.M.; Lamoreaux, P.T. Investor Demand for Internal Control Audits of Large US Companies: Evidence from a Regulatory Exemption for M&A Transactions. Acc. Rev. 2018. [Google Scholar] [CrossRef]

- Cheng, B.-L. Service quality and the mediating effect of corporate image on the relationship between customer satisfaction and customer loyalty in the Malaysian hotel industry. Gadjah Mada Int. J. Bus. 2013, 15, 99–112. [Google Scholar] [CrossRef]

- Sekaran, U.; Bougie, R. Research Methods for Business: A Skill Building Approach; John Wiley & Sons: Hoboken, NJ, USA, 2016; p. 1119165555. [Google Scholar]

- Garson, D.G. Factor Analysis: Statnotes. 2008. Available online: https://www.encorewiki.org/download/attachments/25657/Factor+Analysis_+Statnotes+from+North+Carolina+State+University.pdf (accessed on 27 February 2019).

- Nunnally, J. Psychometric Theory; McGraw-Hill: New York, NY, USA, 1978. [Google Scholar]

- Richey, R.G., Jr.; Roath, A.S.; Whipple, J.M.; Fawcett, S.E. Exploring a governance theory of supply chain management: Barriers and facilitators to integration. J. Bus. Logist. 2010, 31, 237–256. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| SCM Practices | References |

|---|---|

| Customer integration | Abdallah et al. [13], Flynn et al. [6], Jabbour et al. [14], Lotfi et al. [15], Wong et al. [16], Slusarczyk et al. [17], Lii and Kuo [18] |

| Supplier integration | Abdallah et al. [13], Flynn et al. [6], Jabbour et al. [14], Lotfi et al. [15], Wong et al. [16], Lii and Kuo [18] |

| Internal integration | Abdallah et al. [13]; Flynn et al. [6], Jabbour et al. [14], Lotfi et al. [15], Wong et al. [16], Lii and Kuo [18] |

| Postponement | Abdallah et al. [13], Jabbour et al. [14] |

| Continuous process flow | Flynn et al. [6] |

| Information sharing | Abdallah et al. [13], Flynn et al. [6], Jabbour et al. [14], |

| Lean | Qi et al. [19] |

| Variables | Number of Items | Cronbach Alpha |

|---|---|---|

| Independent variable | 34 | 0.969 |

| Customer integration | 8 | 0.902 |

| Supplier integration | 8 | 0.921 |

| Internal integration | 10 | 0.937 |

| Internal control | 8 | 0.885 |

| Dependent variable | 6 | 0.887 |

| Financial performance | 6 | 0.887 |

| Overall | 40 | 0.975 |

| Overall average | 5 | 0.946 |

| Variables | Original Number of Items | Items after Deletion | Cronbach’s Alpha | Final Number of Items |

|---|---|---|---|---|

| Internal integration (II) | 10 | 8 | 0.934 | 9 |

| Supplier integration (SI) | 8 | 6 | 0.910 | 8 |

| Customer integration (CI) | 8 | 6 | 0.872 | 5 |

| Internal control (IC) | 8 | 7 | 0.858 | 5 |

| Total/overall Cronbach’s | 34 | 27 | 0.848 | 27 |

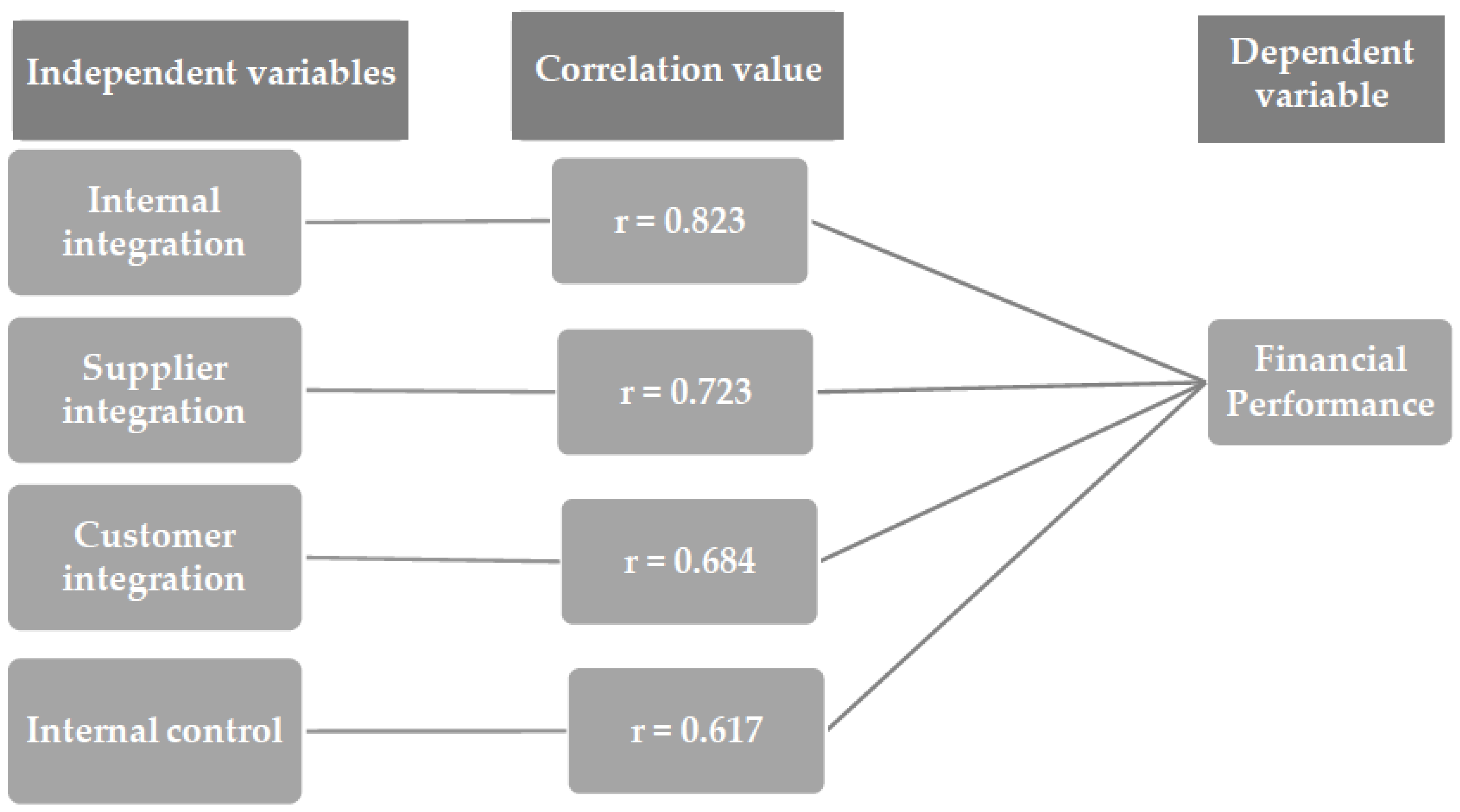

| Financial Performance | Internal Integration | Supplier Integration | Internal Control | Customer Integration | |||

|---|---|---|---|---|---|---|---|

| Spearman’s rho | Financial performance | Correlation coefficient | 1.000 | 0.823 ** | 0.723 ** | 0.617 ** | 0.684 ** |

| Sig. (two-tailed) | 0.000 | 0.000 | 0.000 | 0.000 | |||

| N | 249 | 249 | 249 | 249 | |||

| Internal integration | Correlation coefficient | 0.823 ** | 1.000 | 0.691 ** | 0.539 ** | 0.606 ** | |

| Sig. (two-tailed) | 0.000 | 0.000 | 0.000 | 0.000 | |||

| N | 249 | 249 | 249 | 249 | |||

| Supplier integration | Correlation coefficient | 0.723 ** | 0.691 ** | 1.000 | 0.514 ** | 0.602 ** | |

| Sig. (two-tailed) | 0.000 | 0.000 | 0.000 | 0.000 | |||

| N | 249 | 249 | 249 | 249 | |||

| Internal control | Correlation coefficient | 0.617 ** | 0.539 ** | 0.514 ** | 1.000 | 0.540 ** | |

| Sig. (two-tailed) | 0.000 | 0.000 | 0.000 | 0.000 | |||

| N | 249 | 249 | 249 | 249 | |||

| Customer integration | Correlation coefficient | 0.684 ** | 0.606 ** | 0.602 ** | 0.540 ** | 1.000 | |

| Sig. (two-tailed) | 0.000 | 0.000 | 0.000 | 0.000 | |||

| N | 249 | 249 | 249 | 249 | |||

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Pakurár, M.; Haddad, H.; Nagy, J.; Popp, J.; Oláh, J. The Impact of Supply Chain Integration and Internal Control on Financial Performance in the Jordanian Banking Sector. Sustainability 2019, 11, 1248. https://doi.org/10.3390/su11051248

Pakurár M, Haddad H, Nagy J, Popp J, Oláh J. The Impact of Supply Chain Integration and Internal Control on Financial Performance in the Jordanian Banking Sector. Sustainability. 2019; 11(5):1248. https://doi.org/10.3390/su11051248

Chicago/Turabian StylePakurár, Miklós, Hossam Haddad, János Nagy, József Popp, and Judit Oláh. 2019. "The Impact of Supply Chain Integration and Internal Control on Financial Performance in the Jordanian Banking Sector" Sustainability 11, no. 5: 1248. https://doi.org/10.3390/su11051248

APA StylePakurár, M., Haddad, H., Nagy, J., Popp, J., & Oláh, J. (2019). The Impact of Supply Chain Integration and Internal Control on Financial Performance in the Jordanian Banking Sector. Sustainability, 11(5), 1248. https://doi.org/10.3390/su11051248