On the Asymmetries of Sovereign Credit Rating Announcements and Financial Market Development in the European Region

Abstract

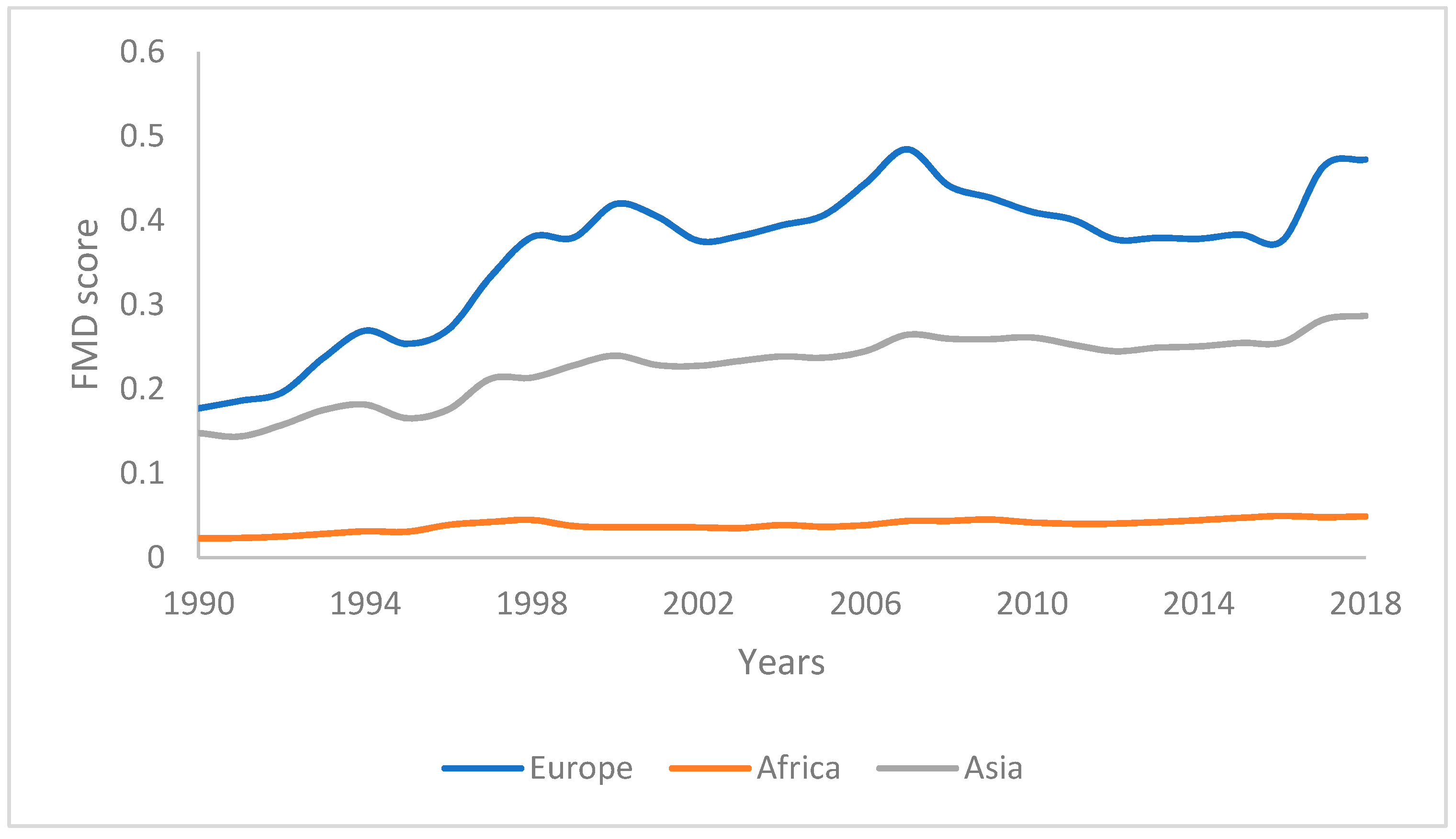

1. Introduction

2. Sovereign Credit Ratings and Financial Markets

3. Materials and Methods

3.1. Symmetric Panel ARDL (PARDL) Framework

3.2. Asymmetric Panel ARDL Framework

4. Results

4.1. Symmetric and Asymmetric Impact of CR on FMD

4.2. Robustness: Using an Alternative Measure

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Yang, C.-C.; Ou, S.-L.; Hsu, L.-C. A Hybrid Multi-Criteria Decision-Making Model for Evaluating Companies’ Green Credit Rating. Sustainability 2019, 11, 1506. [Google Scholar] [CrossRef]

- Shah, S.S.H.; Khan, M.A.; Meyer, N.; Meyer, D.F.; Oláh, J. Does Herding Bias Drive the Firm Value? Evidence from the Chinese Equity Market. Sustainability 2019, 11, 5583. [Google Scholar] [CrossRef]

- Cubas-Díaz, M.; Martínez Sedano, M.J.S. Do Credit Ratings Take into Account the Sustainability Performance of Companies? Sustainability 2018, 10, 4272. [Google Scholar] [CrossRef]

- Schmukler, S. Emerging Markets Instability: Do Sovereign Ratings Affect Country Risk and Stock Returns? The World Bank: Washington, DC, USA, 1999. [Google Scholar] [CrossRef]

- Corbet, S. The contagion effects of sovereign downgrades: Evidence from the European financial crisis. Int. J. Econ. Financ. Issues 2013, 4, 83–92. [Google Scholar]

- Graham, J.R.; Harvey, C.R. The theory and practice of corporate finance: Evidence from the field. J. Financ. Econ. 2001, 60, 187–243. [Google Scholar] [CrossRef]

- McLean, R.D.; Zhang, T.; Zhao, M. Why does the law matter? Investor protection and its effects on investment, finance, and growth. J. Financ. 2012, 67, 313–350. [Google Scholar] [CrossRef]

- Williams, G.; Alsakka, R.; Ap Gwilym, O. The impact of sovereign rating actions on bank ratings in emerging markets. J. Bank. Financ. 2013, 37, 563–577. [Google Scholar] [CrossRef]

- Kliger, D.; Sarig, O. The information value of bond ratings. J. Financ. 2000, 55, 2879–2902. [Google Scholar] [CrossRef]

- Goh, J.C.; Ederington, L.H. Is a bond rating downgrade bad news, good news, or no news for stockholders? J. Financ. 1993, 48, 2001–2008. [Google Scholar] [CrossRef]

- Holthausen, R.W.; Leftwich, R.W. The effect of bond rating changes on common stock prices. J. Financ. Econ. 1986, 17, 57–89. [Google Scholar] [CrossRef]

- Hand, J.R.; Holthausen, R.W.; LEFTWICH, R.W. The effect of bond rating agency announcements on bond and stock prices. J. Financ. 1992, 47, 733–752. [Google Scholar] [CrossRef]

- Poon, W.P.H.; Chan, K.C. An empirical examination of the informational content of credit ratings in China. J. Bus. Res. 2008, 61, 790–797. [Google Scholar] [CrossRef]

- Norden, L.; Weber, M. Informational efficiency of credit default swap and stock markets: The impact of credit rating announcements. J. Bank. Financ. 2004, 28, 2813–2843. [Google Scholar] [CrossRef]

- Jorion, P.; Zhang, G. Information effects of bond rating changes: The role of the rating prior to the announcement. J. Fixed Income Spring 2007, 16, 45–59. [Google Scholar] [CrossRef]

- Pukthuanthong-Le, K.; Elayan, F.A.; Rose, L.C. Equity and debt market responses to sovereign credit ratings announcement. Glob. Financ. J. 2007, 18, 47–83. [Google Scholar] [CrossRef]

- Bremer, M.; Pettway, R.H. Information and the market’s perceptions of Japanese bank risk: Regulation, environment, and disclosure. Pac. Basin Financ. J. 2002, 10, 119–139. [Google Scholar] [CrossRef]

- Klimavičiena, A. Sovereign credit rating announcements and Baltic stock markets. Organ. Mark. Emerg. Econ. 2011, 2, 51–62. [Google Scholar] [CrossRef]

- Michaelides, A.; Milidonis, A.; Nishiotis, G.; Papakyriacou, P. Sovereign Debt Rating Changes and the Stock Market. 2012. Available online: https://ssrn.com/abstract=1988675 (accessed on 5 November 2019).

- Creighton, A.; Gower, L.; Richards, A.J. The impact of rating changes in Australian financial markets. Pac. Basin Financ. J. 2007, 15, 1–17. [Google Scholar] [CrossRef]

- Subaşı, F.Ö. The effect of sovereign rating changes on stock returns and exchange rates. Int. Res. J. Financ. Econ. 2008, 20, 46–54. [Google Scholar]

- Hu, H.; Kaspereit, T.; Prokop, J. The information content of issuer rating changes: Evidence for the G7 stock markets. Int. Rev. Financ. Anal. 2016, 47, 99–108. [Google Scholar] [CrossRef]

- Böninghausen, B.; Zabel, M. Credit ratings and cross-border bond market spillovers. J. Int. Money Financ. 2015, 53, 115–136. [Google Scholar] [CrossRef]

- Li, H.; Jeon, B.N.; Cho, S.-Y.; Chiang, T.C. The impact of sovereign rating changes and financial contagion on stock market returns: Evidence from five Asian countries. Glob. Financ. J. 2008, 19, 46–55. [Google Scholar] [CrossRef]

- Sari, R.; Uzunkaya, M.; Hammoudeh, S. The relationship between disaggregated country risk ratings and stock market movements: An ARDL approach. Emerg. Mark. Financ. Trade 2013, 49, 4–16. [Google Scholar] [CrossRef]

- Galletta, S.; Mazzù, S. Liquidity Risk Drivers and Bank Business Models. Risks 2019, 7, 89. [Google Scholar] [CrossRef]

- Pelizzon, L.; Subrahmanyam, M.G.; Tomio, D.; Uno, J. Sovereign credit risk, liquidity, and European Central Bank intervention: Deus ex machina? J. Financ. Econ. 2016, 122, 86–115. [Google Scholar] [CrossRef]

- Diamond, D.W. Debt Maturity Structure and Liquidity Risk. Q. J. Econ. 1991, 106, 709–737. [Google Scholar] [CrossRef]

- de Souza Murcia, F.C.; Murcia, F.D.-R.; Borba, J.A. The Informational Content of Credit Ratings in Brazil: An Event Study. Braz. Rev. Financ. 2013, 11, 503–526. [Google Scholar] [CrossRef]

- Reisen, H.; Von Maltzan, J. Boom and bust and sovereign ratings. Int. Financ. 1999, 2, 273–293. [Google Scholar] [CrossRef]

- Cantor, R.; Packer, F. Determinants and impact of sovereign credit ratings. Econ. Policy Rev. 1996, 2. [Google Scholar] [CrossRef]

- Chiang, T.C.; Jeon, B.N.; Li, H. Dynamic correlation analysis of financial contagion: Evidence from Asian markets. J. Int. Money Financ. 2007, 26, 1206–1228. [Google Scholar] [CrossRef]

- Ferreira, M.A.; Gama, P.M. Does sovereign debt ratings news spill over to international stock markets? J. Bank. Financ. 2007, 31, 3162–3182. [Google Scholar] [CrossRef]

- Bissoondoyal-Bheenick, E. Do sovereign rating changes trigger spillover effects? Res. Int. Bus. Financ. 2012, 26, 79–96. [Google Scholar] [CrossRef]

- Hooper, V.; Hume, T.; Kim, S.-J. Sovereign rating changes—Do they provide new information for stock markets? Econ. Syst. 2008, 32, 142–166. [Google Scholar] [CrossRef]

- Huang, B.; He, L.; Xiong, S.; Zhang, Y. The impact of bond rating downgrades on common stock prices in China. Econ. Political Stud. 2018, 6, 209–220. [Google Scholar] [CrossRef]

- Charoenwong, C.; Li, X.H.; Visaltanachoti, N. Market Reaction to Credit Rating Announcements in the Irish Stock Market. SSRN Electron. J. 2004. [Google Scholar] [CrossRef]

- Covitz, D.; Downing, C. Liquidity or Credit Risk? The Determinants of Very Short-Term Corporate Yield Spreads. J. Financ. 2007, 62, 2303–2328. [Google Scholar] [CrossRef]

- Odders-White, E.R.; Ready, M.J. Credit Ratings and Stock Liquidity. Rev. Financ. Stud. 2005, 19, 119–157. [Google Scholar] [CrossRef]

- Monfort, A.; Renne, J.-P. Decomposing Euro-Area Sovereign Spreads: Credit and Liquidity Risks*. Rev. Financ. 2013, 18, 2103–2151. [Google Scholar] [CrossRef]

- Hammoudeh, S.; Sari, R.; Uzunkaya, M.; Liu, T. The dynamics of BRICS’s country risk ratings and domestic stock markets, U.S. stock market and oil price. Math. Comput. Simul. 2013, 94, 277–294. [Google Scholar] [CrossRef]

- Borensztein, E.; Cowan, K.; Valenzuela, P. Sovereign ceilings “lite”? The impact of sovereign ratings on corporate ratings. J. Bank. Financ. 2013, 37, 4014–4024. [Google Scholar] [CrossRef]

- Sensoy, A.; Eraslan, V.; Erturk, M. Do sovereign rating announcements have an impact on regional stock market co-movements? The case of Central and Eastern Europe. Econ. Syst. 2016, 40, 552–567. [Google Scholar] [CrossRef]

- Brooks, R.; Faff, R.W.; Hillier, D.; Hillier, J. The national market impact of sovereign rating changes. J. Bank. Financ. 2004, 28, 233–250. [Google Scholar] [CrossRef]

- Bissoondoyal-Bheenick, E. Rating timing differences between the two leading agencies: Standard and Poor’s and Moody’s. Emerg. Mark. Rev. 2004, 5, 361–378. [Google Scholar] [CrossRef]

- Andritzky, J.R.; Bannister, G.J.; Tamirisa, N.T. The impact of macroeconomic announcements on emerging market bonds. Emerg. Mark. Rev. 2007, 8, 20–37. [Google Scholar] [CrossRef]

- Kim, S.-J.; Wu, E. Sovereign credit ratings, capital flows and financial sector development in emerging markets. Emerg. Mark. Rev. 2008, 9, 17–39. [Google Scholar] [CrossRef]

- Kräussl, R. Do credit rating agencies add to the dynamics of emerging market crises? J. Financ. Stab. 2005, 1, 355–385. [Google Scholar] [CrossRef]

- Ismailescu, I.; Kazemi, H. The reaction of emerging market credit default swap spreads to sovereign credit rating changes. J. Bank. Financ. 2010, 34, 2861–2873. [Google Scholar] [CrossRef]

- Afonso, A.; Furceri, D.; Gomes, P. Sovereign credit ratings and financial markets linkages: Application to European data. J. Int. Money Financ. 2012, 31, 606–638. [Google Scholar] [CrossRef]

- Treepongkaruna, S.; Wu, E. Realizing the volatility impacts of sovereign credit ratings information on equity and currency markets: Evidence from the Asian Financial Crisis. Res. Int. Bus. Financ. 2012, 26, 335–352. [Google Scholar] [CrossRef]

- Khan, M.A.; Kong, D.; Xiang, J.; Zhang, J. Impact of Institutional Quality on Financial Development: Cross-Country Evidence based on Emerging and Growth-Leading Economies. Emerg. Mark. Financ. Trade 2019, 1–17. [Google Scholar] [CrossRef]

- Pesaran, M.H.; Shin, Y.; Smith, R.J. Bounds testing approaches to the analysis of level relationships. J. Appl. Econom. 2001, 16, 289–326. [Google Scholar] [CrossRef]

- Pesaran, B.; Pesaran, M.H. Time Series Econometrics Using Microfit 5.0: A User’s Manual; Oxford University Press, Inc.: New York, NY, USA, 2010. [Google Scholar]

- Gkillas, K.; Vortelinos, D.I.; Suleman, T. Asymmetries in the African financial markets. J. Multinatl. Financ. Manag. 2018, 45, 72–87. [Google Scholar] [CrossRef]

- Khan, M.A.; Khan, M.A.; Abdulahi, M.E.; Liaqat, I.; Shah, S.S.H. Institutional quality and financial development: The United States perspective. J. Multinatl. Financ. Manag. 2019, 49, 67–80. [Google Scholar] [CrossRef]

- Khan, M.A.; Ilyas, R.M.A.; Hashmi, S.H. Cointegration between Institutional Quality and Stock Market Development. Int. J. Bus. Manag. 2018, 13, 90–103. [Google Scholar]

- Shin, Y.; Yu, B.; Greenwood-Nimmo, M. Modelling asymmetric cointegration and dynamic multipliers in a nonlinear ARDL framework. In Festschrift in Honor of Peter Schmidt; Springer: Berlin, Germany, 2014; pp. 281–314. [Google Scholar] [CrossRef]

- Afonso, A.; Gomes, P.; Rother, P. Short-and long-run determinants of sovereign debt credit ratings. Int. J. Financ. Econ. 2011, 16, 1–15. [Google Scholar] [CrossRef]

- Chi, G.; Zhang, Z.J.S. Multi criteria credit rating model for small enterprise using a nonparametric method. Sustainability 2017, 9, 1834. [Google Scholar] [CrossRef]

{kind=link}

| S.No. | Country | S.No. | Country |

|---|---|---|---|

| 1 | Albania | 21 | Latvia |

| 2 | Austria | 22 | Lithuania |

| 3 | Belarus | 23 | Luxembourg |

| 4 | Belgium | 24 | Malta |

| 5 | Bosnia and Herzegovina | 25 | Moldova |

| 6 | Bulgaria | 26 | Montenegro |

| 7 | Croatia | 27 | Netherlands |

| 8 | Cyprus | 28 | Norway |

| 9 | Czech Republic | 29 | Poland |

| 10 | Denmark | 30 | Portugal |

| 11 | Estonia | 31 | Romania |

| 12 | Finland | 32 | Russia |

| 13 | France | 33 | Slovakia |

| 14 | Germany | 34 | Slovenia |

| 15 | Greece | 35 | Spain |

| 16 | Hungary | 36 | Sweden |

| 17 | Iceland | 37 | Switzerland |

| 18 | Ireland | 38 | Turkey |

| 19 | Isle of Man | 39 | Ukraine |

| 20 | Italy | 40 | United Kingdom |

| Variable | Obs | Mean | St.Dev. | Min | Max |

|---|---|---|---|---|---|

| CR_M | 1131 | 4.154 | 0.455 | 2.303 | 4.605 |

| CR_S | 1160 | 4.15 | 0.474 | 1.609 | 4.605 |

| FMD | 1131 | 3.061 | 1.346 | −3.687 | 4.605 |

| FMX | 899 | 0.02 | 1.00 | −5.176 | 3.471 |

| BD | 1160 | 4.03 | 0.817 | 0.326 | 5.733 |

| EG | 1160 | 9.799 | 0.799 | 6.86 | 11.625 |

| INF | 1160 | 1.437 | 1.613 | −4.791 | 8.463 |

| OP | 1160 | 4.198 | 0.448 | 2.889 | 5.198 |

| INV | 1160 | 3.076 | 0.217 | 1.503 | 3.669 |

| LLC | IPS | |||

|---|---|---|---|---|

| Level | 1st Difference | Level | 1st Difference | |

| CR_M | −0.70 | −20.23 *** | −0.97 | −4.43 *** |

| CR_S | −8.71 *** | −16.91 *** | −1.15 | −3.83 *** |

| FM_IMF | −10.51 *** | −36.34 *** | −3.35 *** | −5.38 *** |

| FMX | −2.87 *** | −25.01 *** | −1.87 | −4.86 *** |

| BD | −0.82 | −9.48 *** | −1.35 | −3.72 *** |

| EG | −2.54 *** | −17.91 *** | −2.02 | −4.03 *** |

| INF | −8.24 *** | −28.37 *** | −3.22 *** | −5.64 *** |

| OP | −2.51 *** | −26.48 *** | −1.73 | −4.25 *** |

| INV | −7.65 *** | −20.39 *** | −2.00 | −4.59 *** |

| Dependent variable: FMD | ||||

|---|---|---|---|---|

| Symmetry | Asymmetry | |||

| (1) | (2) | (3) | (4) | |

| Variables | CR_S | CR_M | CR_S | CR_M |

| ECT | −0.301 *** | −0.217 *** | −0.317 *** | −0.311 *** |

| (−6.95) | (−5.89) | (−7.45) | (−6.40) | |

| ΔCR | −0.161 | 0.042 | ||

| (−0.75) | (0.26) | |||

| ΔCR_POS | −0.531 | 0.258 | ||

| (−1.54) | (1.39) | |||

| ΔCR_NEG | 0.058 | 0.714 | ||

| (0.18) | (1.09) | |||

| ΔBD | 0.245 ** | 0.194 | 0.232 ** | 0.256 ** |

| (2.14) | (1.64) | (1.99) | (2.09) | |

| ΔEG | 0.117 | 0.251 | 0.079 | 0.179 |

| (0.31) | (0.87) | (0.21) | (0.52) | |

| ΔINF | −0.007 | −0.015 | 0.010 | −0.003 |

| (−0.48) | (−1.14) | (0.67) | (−0.21) | |

| ΔOP | 0.141 | 0.249 ** | 0.072 | 0.198 * |

| (1.09) | (2.03) | (0.51) | (1.67) | |

| ΔINV | 0.164 | 0.190 | 0.235 | 0.109 |

| (0.98) | (1.19) | (1.29) | (0.64) | |

| CR | 0.185 | 0.977 *** | ||

| (1.39) | (5.48) | |||

| CR_POS | −1.102 *** | −0.233 ** | ||

| (−4.45) | (−2.40) | |||

| CR_NEG | 0.341 ** | 0.015 | ||

| (1.97) | (0.17) | |||

| BD | 0.160 *** | −0.102 * | −0.041 | 0.166 *** |

| (3.10) | (−1.86) | (−0.92) | (3.84) | |

| EG | −0.050 | 0.041 | 0.082 * | 0.024 |

| (−1.06) | (0.55) | (1.74) | (0.54) | |

| INF | −0.034 ** | 0.005 | −0.060 *** | −0.053 *** |

| (−1.99) | (0.22) | (−4.91) | (−4.57) | |

| OP | −0.274 *** | −1.132 *** | 0.000 | −0.467 *** |

| (−2.61) | (−6.67) | (0.01) | (−5.01) | |

| INV | 0.338 *** | −0.607 *** | 0.051 | 0.035 |

| (2.95) | (−3.56) | (0.56) | (0.41) | |

| Constant | 1.090 *** | 1.152 *** | 0.807 *** | 1.249 *** |

| (7.01) | (5.79) | (5.96) | (6.12) | |

| Observations | 1064 | 1092 | 1092 | 1092 |

| Hausman | 3.34 | 2.68 | 2.24 | 2.55 |

| Loglikelihood | 508.21 | 521.77 | 562.74 | 546.65 |

| Dependent Variable: FMD | ||||

|---|---|---|---|---|

| Symmetry | Asymmetry | |||

| (1) | (2) | (3) | (4) | |

| Variables | CR_S | CR_M | CR_S | CR_M |

| ECT | −0.312 *** | −0.215 *** | −0.336 *** | −0.300 *** |

| (−5.74) | (−5.01) | (−6.57) | (−5.88) | |

| ΔCR | −0.521 | 0.188 | ||

| (−1.06) | (0.68) | |||

| ΔCR_POS | 0.034 | 0.497 ** | ||

| (0.16) | (2.06) | |||

| ΔCR_NEG | 0.043 | 0.420 | ||

| (0.07) | (1.18) | |||

| ΔBD | 0.502 *** | 0.091 | 0.491 *** | 0.403 *** |

| (2.62) | (0.45) | (2.62) | (2.73) | |

| ΔEG | 0.137 | 0.118 | 0.084 | 0.252 |

| (0.36) | (0.30) | (0.23) | (0.79) | |

| ΔINF | −0.008 | −0.043 ** | −0.009 | −0.012 |

| (−0.40) | (−1.97) | (−0.53) | (−0.70) | |

| ΔOP | −0.090 | −0.055 | −0.236 | −0.111 |

| (−0.75) | (−0.36) | (−1.61) | (−0.74) | |

| ΔINV | 0.341 * | 0.478 ** | 0.330 * | 0.346 * |

| (1.73) | (2.03) | (1.78) | (1.73) | |

| CR | 0.495 *** | 1.883 *** | ||

| (7.06) | (5.66) | |||

| CR_POS | −0.232 | −0.940 *** | ||

| (−1.53) | (−4.41) | |||

| CR_NEG | 0.281 *** | 0.112 | ||

| (3.37) | (0.65) | |||

| BD | −0.123 * | 0.137 ** | −0.012 | 0.221 *** |

| (−1.77) | (2.09) | (−0.16) | (3.02) | |

| EG | −0.153 * | 1.095 *** | −0.158 ** | 0.052 |

| (−1.68) | (7.82) | (−2.17) | (0.60) | |

| INF | −0.144 *** | −0.114 *** | −0.185 *** | −0.169 *** |

| (−4.40) | (−3.80) | (−6.21) | (−5.55) | |

| OP | −0.010 | −1.443 *** | 0.748 *** | 0.181 |

| (−0.10) | (−6.82) | (6.08) | (1.49) | |

| INV | −0.208 | −0.395 | −0.251 * | −0.334 ** |

| (−1.23) | (−1.41) | (−1.72) | (−1.99) | |

| Constant | 0.276 *** | −2.655 *** | −0.051 | −0.232 *** |

| (4.81) | (−4.95) | (−0.95) | (−4.27) | |

| Observations | 868 | 868 | 868 | 868 |

| Hausman | 3.39 | 8.83 | 2.64 | 1.89 |

| LogLikelihood | 287.98 | 273.64 | 311.48 | 288.93 |

| Dependent Variable | FMD_IMF | FMD_X | ||

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| CR_S | CR_M | CR_S | CR_M | |

| Long run asymmetry | 9.49 *** | 11.72 *** | 22.96 *** | 30.5 *** |

| Short run asymmetry | 1.45 | 0.49 | 4.95 *** | 0.01 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Li, C.; Pervaiz, K.; Asif Khan, M.; Ur Rehman, F.; Oláh, J. On the Asymmetries of Sovereign Credit Rating Announcements and Financial Market Development in the European Region. Sustainability 2019, 11, 6636. https://doi.org/10.3390/su11236636

Li C, Pervaiz K, Asif Khan M, Ur Rehman F, Oláh J. On the Asymmetries of Sovereign Credit Rating Announcements and Financial Market Development in the European Region. Sustainability. 2019; 11(23):6636. https://doi.org/10.3390/su11236636

Chicago/Turabian StyleLi, Chunling, Khansa Pervaiz, Muhammad Asif Khan, Faheem Ur Rehman, and Judit Oláh. 2019. "On the Asymmetries of Sovereign Credit Rating Announcements and Financial Market Development in the European Region" Sustainability 11, no. 23: 6636. https://doi.org/10.3390/su11236636

APA StyleLi, C., Pervaiz, K., Asif Khan, M., Ur Rehman, F., & Oláh, J. (2019). On the Asymmetries of Sovereign Credit Rating Announcements and Financial Market Development in the European Region. Sustainability, 11(23), 6636. https://doi.org/10.3390/su11236636