Implementation Barriers for a System of Environmental-Economic Accounting in Developing Countries and Its Implications for Monitoring Sustainable Development Goals

Abstract

:1. Introduction

- Tier 1: The indicator is conceptually clear and has an internationally established methodology; its standards are available, and its data are regularly produced by countries for at least 50 percent of countries and for the population in every region where the indicator is relevant (104 indicators).

- Tier 2: The indicator is conceptually clear, has an internationally established methodology, and standards are available, but data are not regularly produced by countries (88 indicators).

- Tier 3: No internationally established methodology or standards are yet available for the indicator, but the methodology/standards are being (or will be) developed or tested (34 indicators).

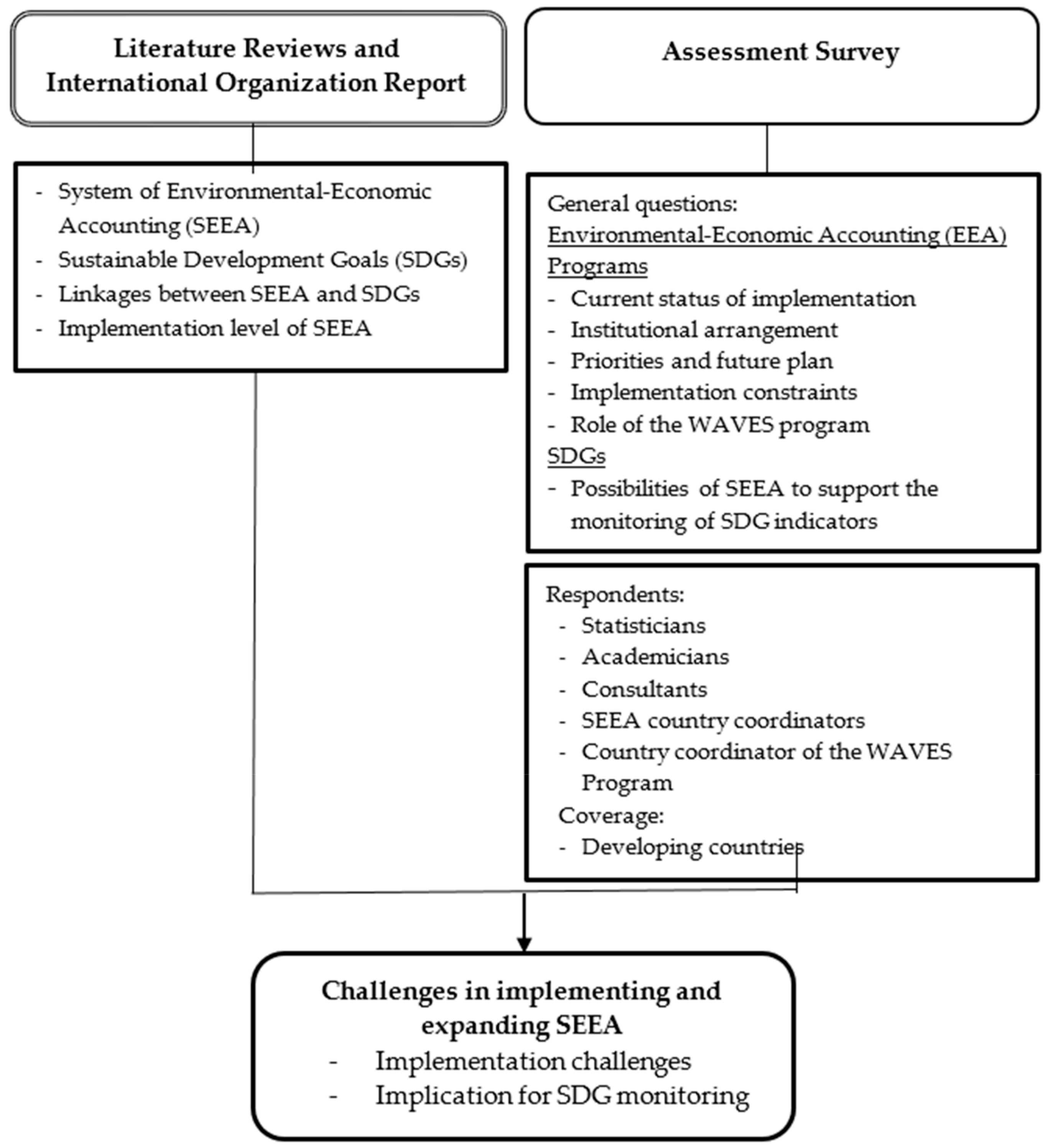

2. Methods of the Study

- Assess the current status of the national implementation of environmental-economics accounting programs

- Assess institutional arrangements for the compilation of environmental-economic Accounts

- Identify priorities and future plans for the compilation of Environmental-economic Accounts

- Identify the constraints in starting the compilation and developing of environmental-economic Accounts

- Identify the role of the WAVES program in compiling and developing of environmental-economic accounts

- Identify the possibilities of Environmental–Economic Accounts to support the monitoring of SDG indicators

3. Literature Review and Report Analysis from International Organizations on SEEA and the SDGs

3.1. Overview of SEEA

- The summary of information in the SEEA (available in the form of aggregates and indicators) can provide information about environmental issues and conditions that are the focus of decision makers.

- More detailed information in the SEEA, for example the main driver of changes in environmental conditions, can be used to provide a deeper understanding of the policy to be taken.

- The data contained in the SEEA can be used to build models and scenarios that can be used to assess different policy scenarios for national and international environmental impacts within a country, between countries, and at the global level.

3.2. SDGs and Their Coverage by SEEA

- (1)

- Policy relevance and utility. Indicators are supported by detailed and organized information, which promotes a detailed understanding of the factors that drive change.

- (2)

- Analytical and methodological soundness. SEEA acts as a vehicle for harmonizing methodological inconsistencies across the environmental data production process and enables a coherent comparison of environment statistics with economic statistics.

- (3)

- Measurability and practicality. SEEA can create efficiencies in the data production process [11].

3.3. Assessment Survey of the Potential for the SEEA to Support SDG Indicator Monitoring

3.4. Conclusions about the Relationship between SEEA and SDGs

4. Implementation Levels of SEEA

4.1. Introduction to the Implementation of SEEA

4.2. Literature Review and International Reports on SEEA Implementation

4.2.1. General Literature Review

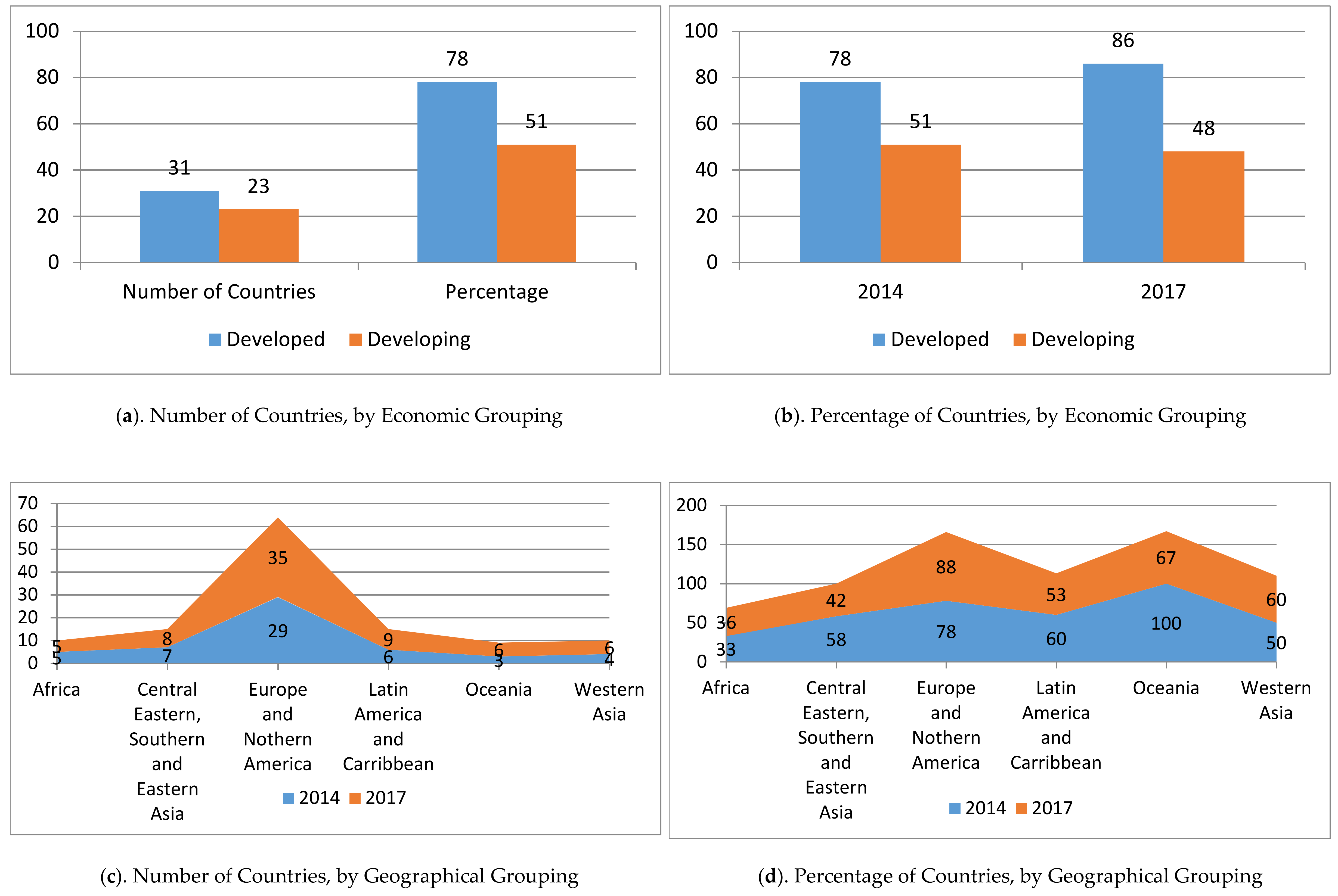

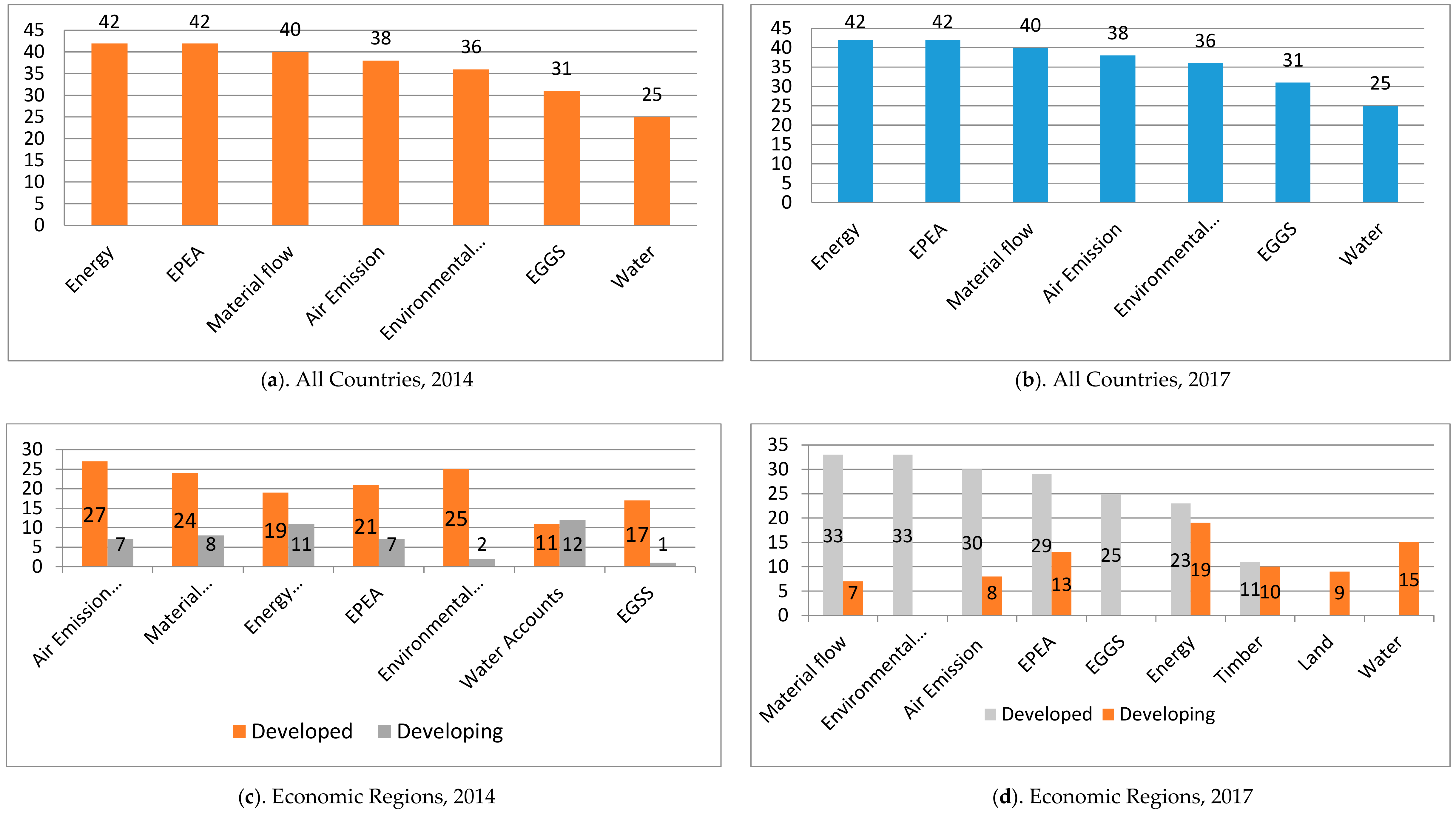

4.2.2. United Nation Statistical Division Global Assessment of Environmental-Economic Accounting

4.2.3. Experiences of the WAVES Program Relevant for SEEA Implementation

4.3. Assessment of SEEA Implementation in Selected Developing Countries via an Assessment Survey

4.4. Conclusions on the Implementation of SEEA

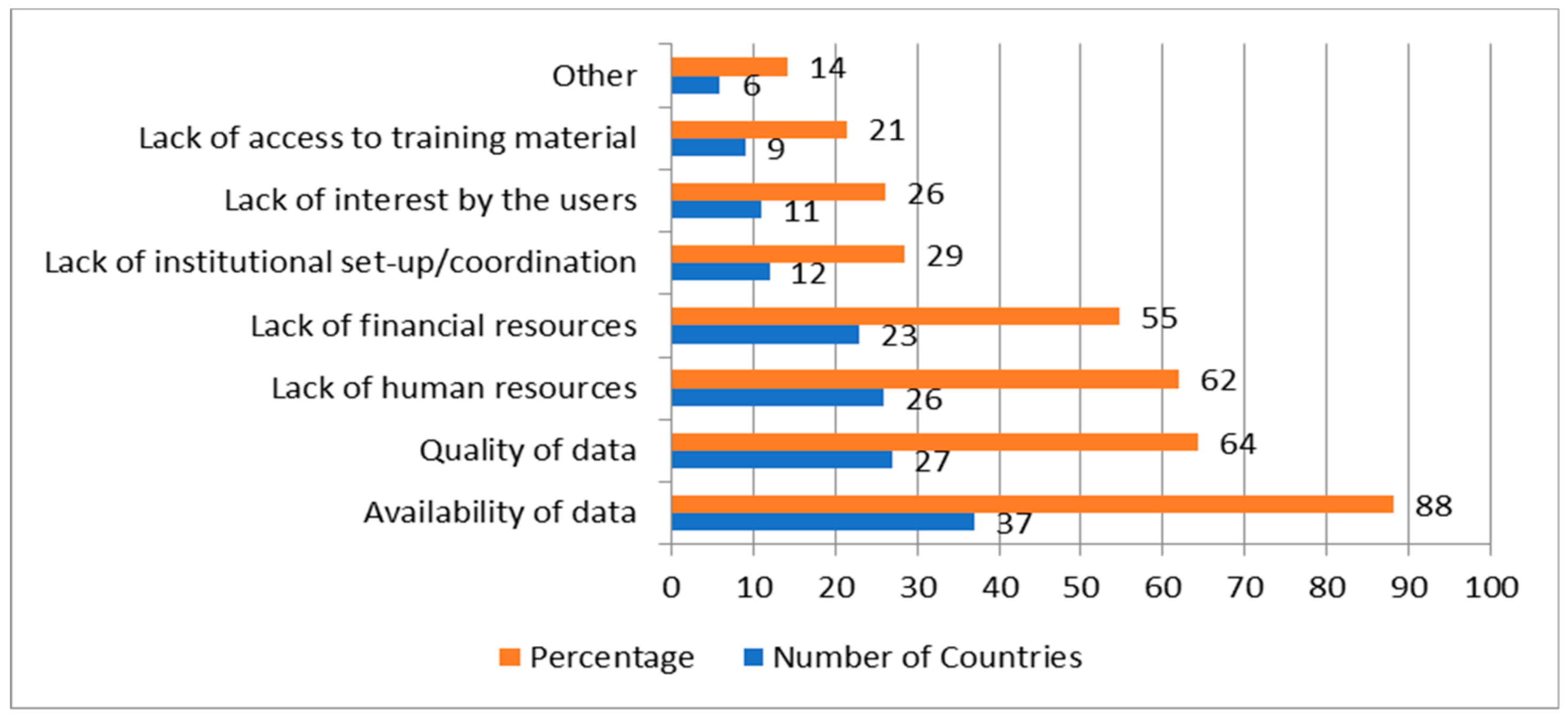

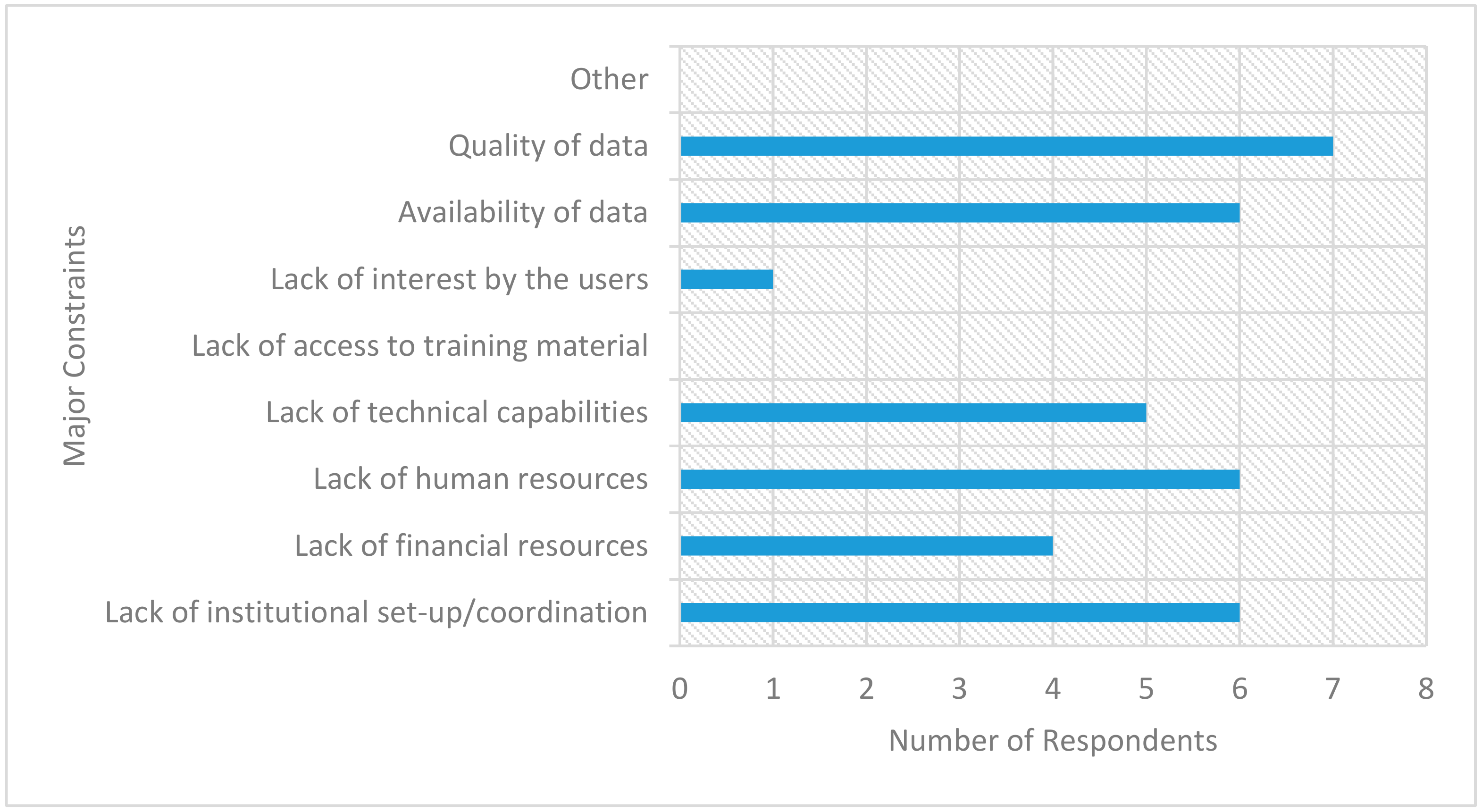

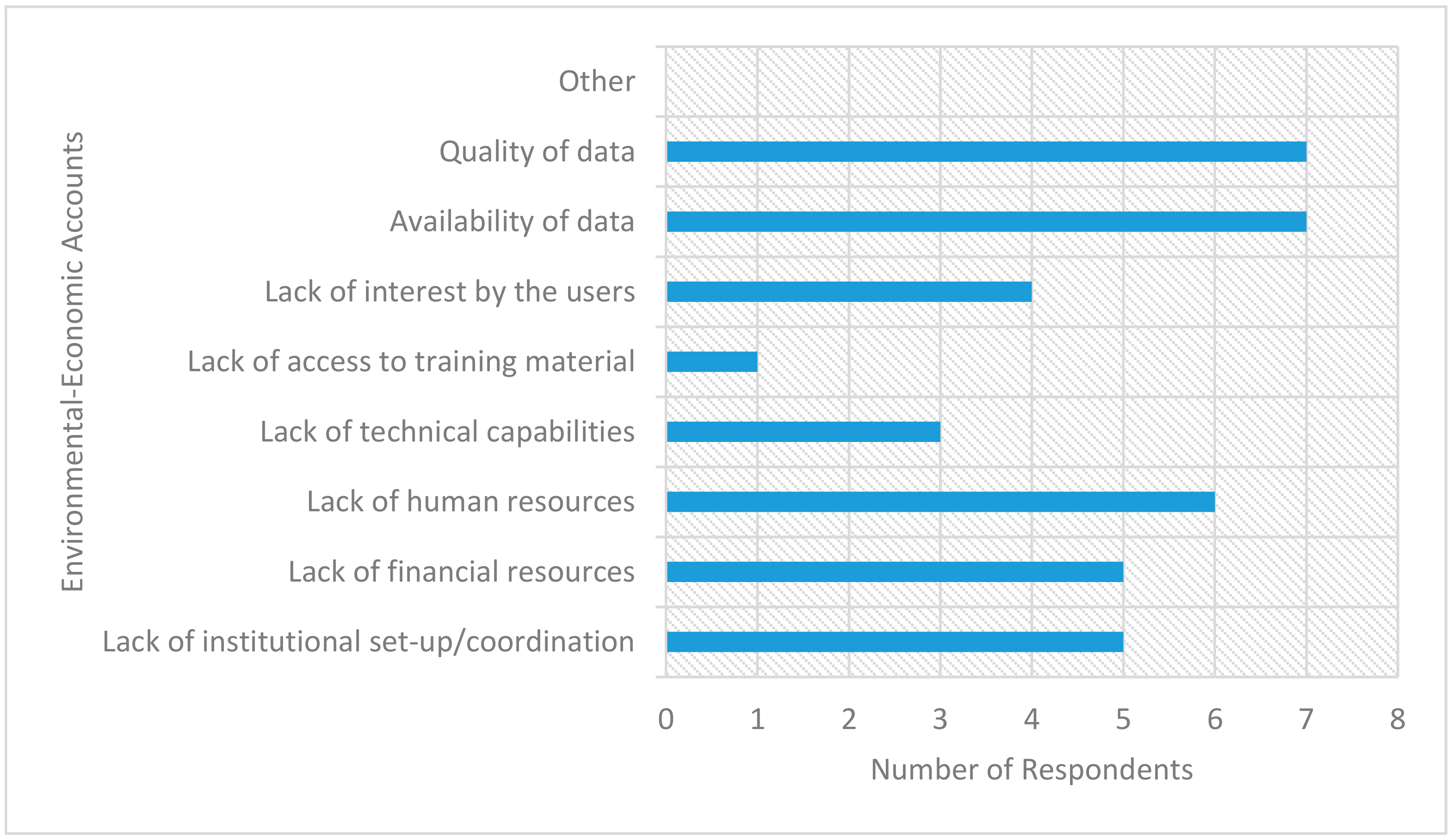

5. Challenges in Implementing and Expanding of SEEA

5.1. Implementation Challenges from the Literature and Survey

5.2. Potential Approaches to Addressing Implementation Challenges

5.3. Implication for SDG Monitoring

6. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A. Questionnaire on Assessment of Environmental-Economic Accounting in Developing Countries

- (a)

- Assessing the current status of national implementation of Environmental-Economic Accounting Programs in developing countries

- (b)

- Assessing institutional arrangements for the compilation of Environmental-Economic Accounts in developing countries

- (c)

- Identifying priorities and future plans for the compilation of Environmental-Economic Accounts

- (d)

- Identifying the constraints in starting the compilation and developing Environmental-Economic Accounts

- (e)

- Identifying the role of WAVES program in compiling and developing Environmental-Economic Accounts

- (f)

- Identifying the possibilities of Environmental-Economic Account to support the monitoring of SDG Indicators

- Does country have a program on Environmental-Economic Accounting that is compiling data for, or developing SEEA-based accounting?[ ] Yes[ ] No → skip to question 18

- If your country have a program on Environmental-Economic Accounting, is the program is a yearly/routine program?[ ] Yes[ ] No

- After 2012, did the program already adopt SEEA-CF 2012 from UN?[ ] Yes[ ] No

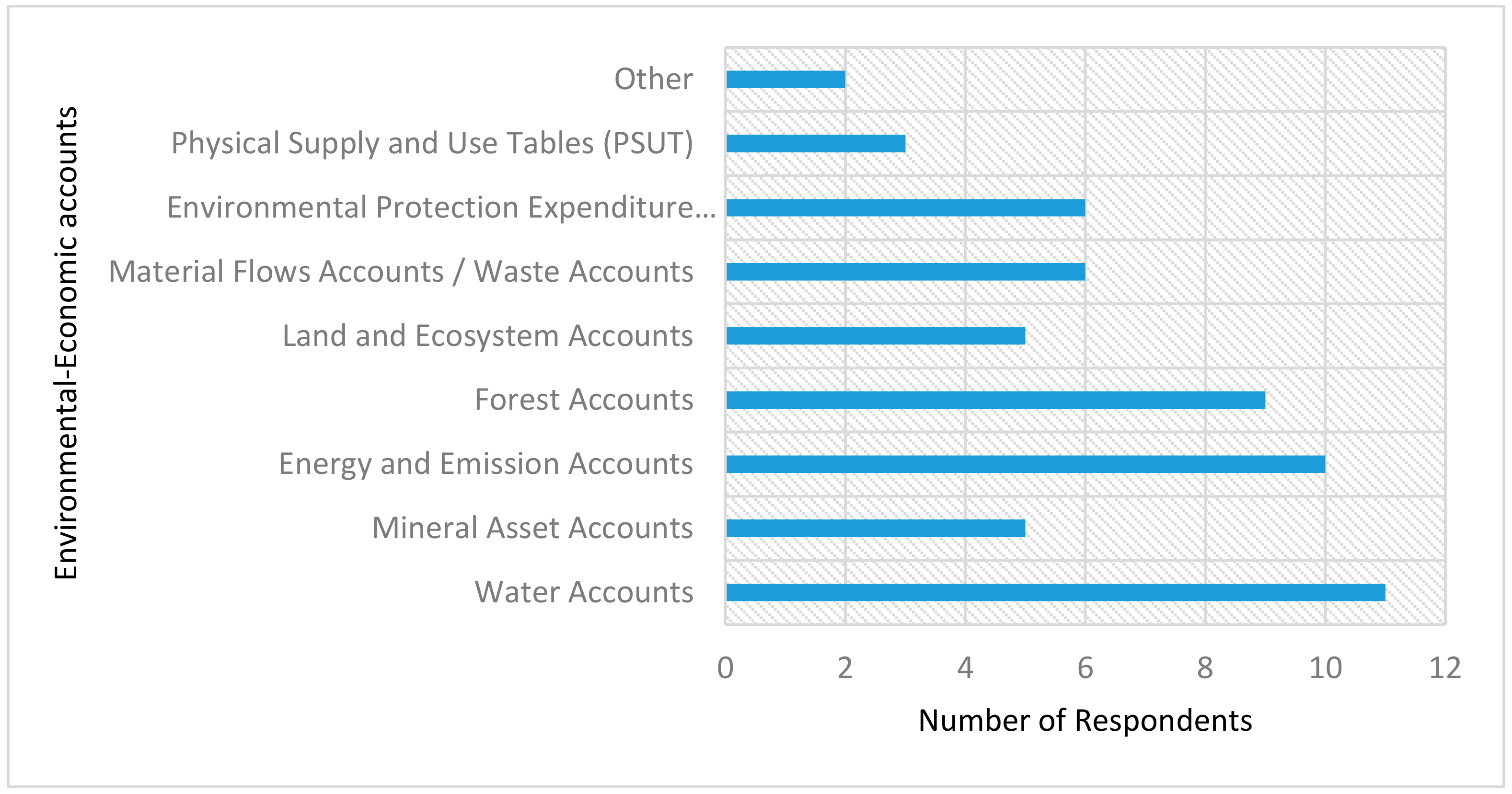

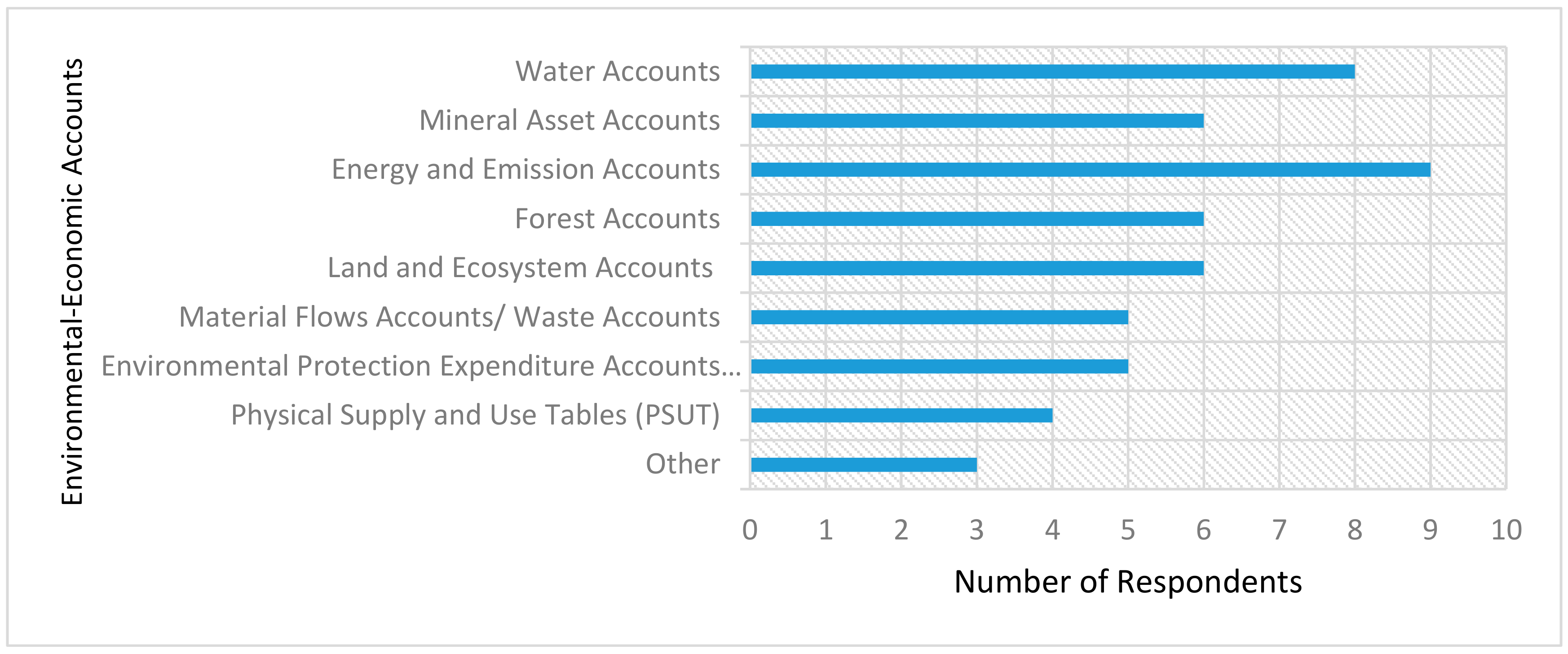

- Which modules of Environmental-Economic Accounting are compiled by your country?[ ] Water Accounts[ ] Mineral Asset Accounts[ ] Energy and Emission Accounts[ ] Forest Accounts[ ] Land and Ecosystem Accounts[ ] Material Flows Accounts/Waste Accounts[ ] Environmental Protection Expenditure Accounts (EPEA)[ ] Physical Supply and Use Tables (PSUT)[ ] Other → Please specify (there is no limit in number of characters): environmental services

- In compiling Environmental-Economic Accounts, has your institution/agency made use of the following:5a. Training material, methodological guidelines or country experiences?[ ] Yes → Please specify (e.g. 1993 SNA, SEEA 2003, etc.): _______[ ] No5b. Technical assistance from international organizations or countries?[ ] Yes → Please describe (e.g. during which period, nature of assistance, etc):[ ] No

- In compiling Environmental-Economic Accounts, your institution/agency funded by:[ ] Government funding[ ] External funding → Please specify (e.g. during which period, from which sources, etc): _________

- In compiling Environmental-Economic Accounts, your institution/agency has regular funding?[ ] Yes → Please specify (e.g. how many professional/supporting staff covered, ranges of funds, government or external sources, etc): _______[ ] No

- In compiling Environmental-Economic Accounts, is WAVES program has a significant role?[ ] Yes → Please give a brief explanation: _________[ ] No

- Which modules/accounts is the most impacted by the existence of WAVES program?[ ] Water Accounts[ ] Mineral Asset Accounts[ ] Energy and Emission Accounts[ ] Forest Accounts[ ] Land and Ecosystem Accounts[ ] Material Flows Accounts/Waste Accounts[ ] Environmental Protection Expenditure Accounts (EPEA)[ ] Physical Supply and Use Tables (PSUT)[ ] Other → Please specify (there is no limit in number of characters): environmental services

- If the World Bank stops the WAVES Program, is your institution/agency will continue to compile the Environmental-Economic Accounts?[ ] Yes[ ] No

- Are there plans to continue compiling the current Environmental-Economic Accounts in your institution/agency?[ ] Yes[ ] No

- Are there plans to expand the compilation of Environmental-Economic Accounts in your institution/agency?[ ] Yes → Which modules?[ ] Water Accounts[ ] Mineral Asset Accounts[ ] Energy and Emission Accounts[ ] Forest Accounts[ ] Land and Ecosystem Accounts[ ] Material Flows Accounts/Waste Accounts[ ] Environmental Protection Expenditure Accounts (EPEA)[ ] Physical Supply and Use Tables (PSUT)[ ] Other → Please specify (there is no limit in number of characters): _______[ ] No

- In relation with SDGs, do your institution/agency think that Environmental-Economic Accounting database is possible to support the SDG Indicators monitoring?[ ] Yes → Please continue to the next questions[ ] No → Skip to question 21

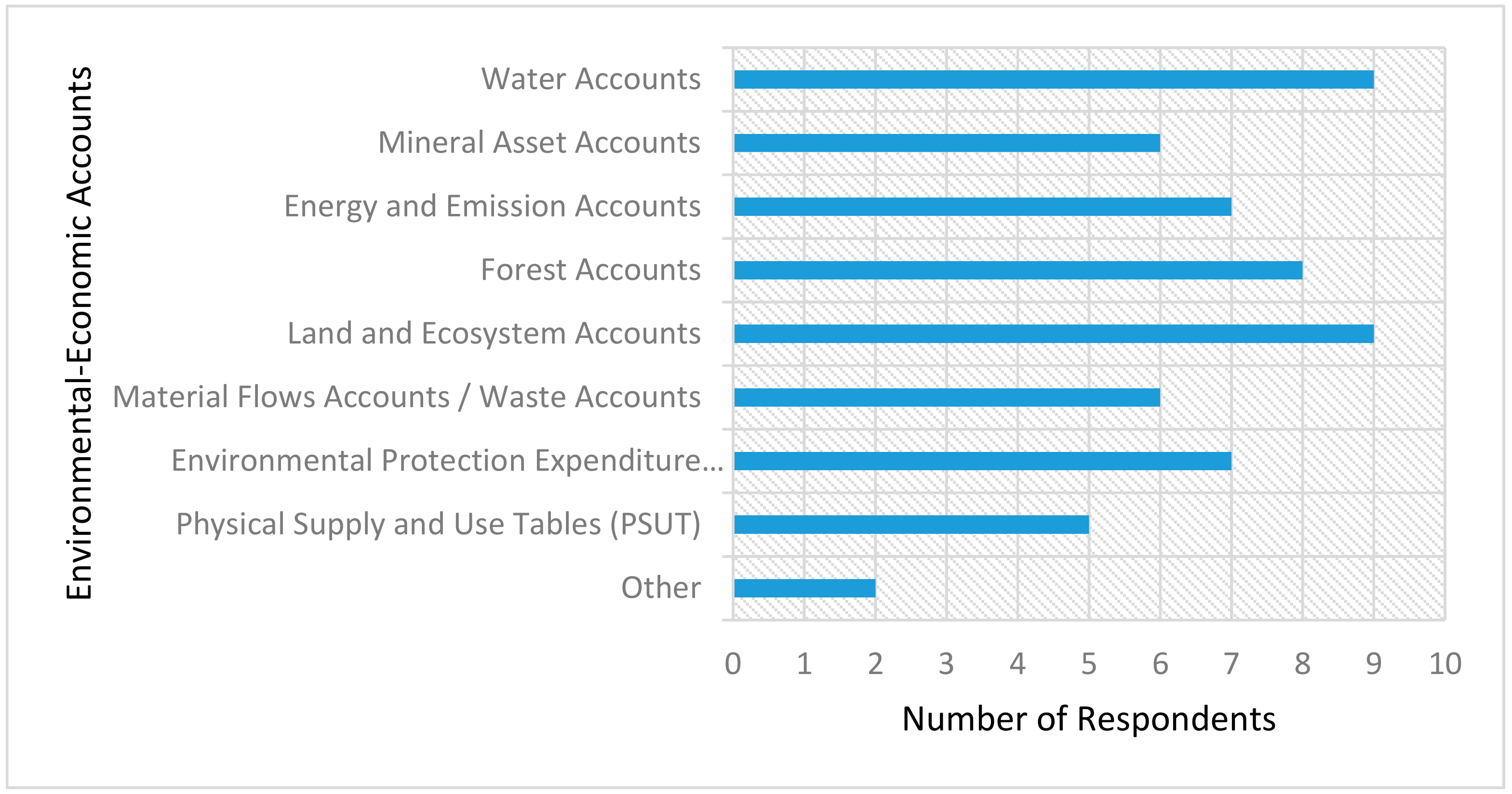

- Which modules/accounts in your view can support SDG Indicators monitoring?[ ] Water Accounts[ ] Mineral Asset Accounts[ ] Energy and Emission Accounts[ ] Forest Accounts[ ] Land and Ecosystem Accounts[ ] Material Flows Accounts/Waste Accounts[ ] Environmental Protection Expenditure Accounts (EPEA)[ ] Physical Supply and Use Tables (PSUT)[ ] Other → Please specify (there is no limit in number of characters): _______

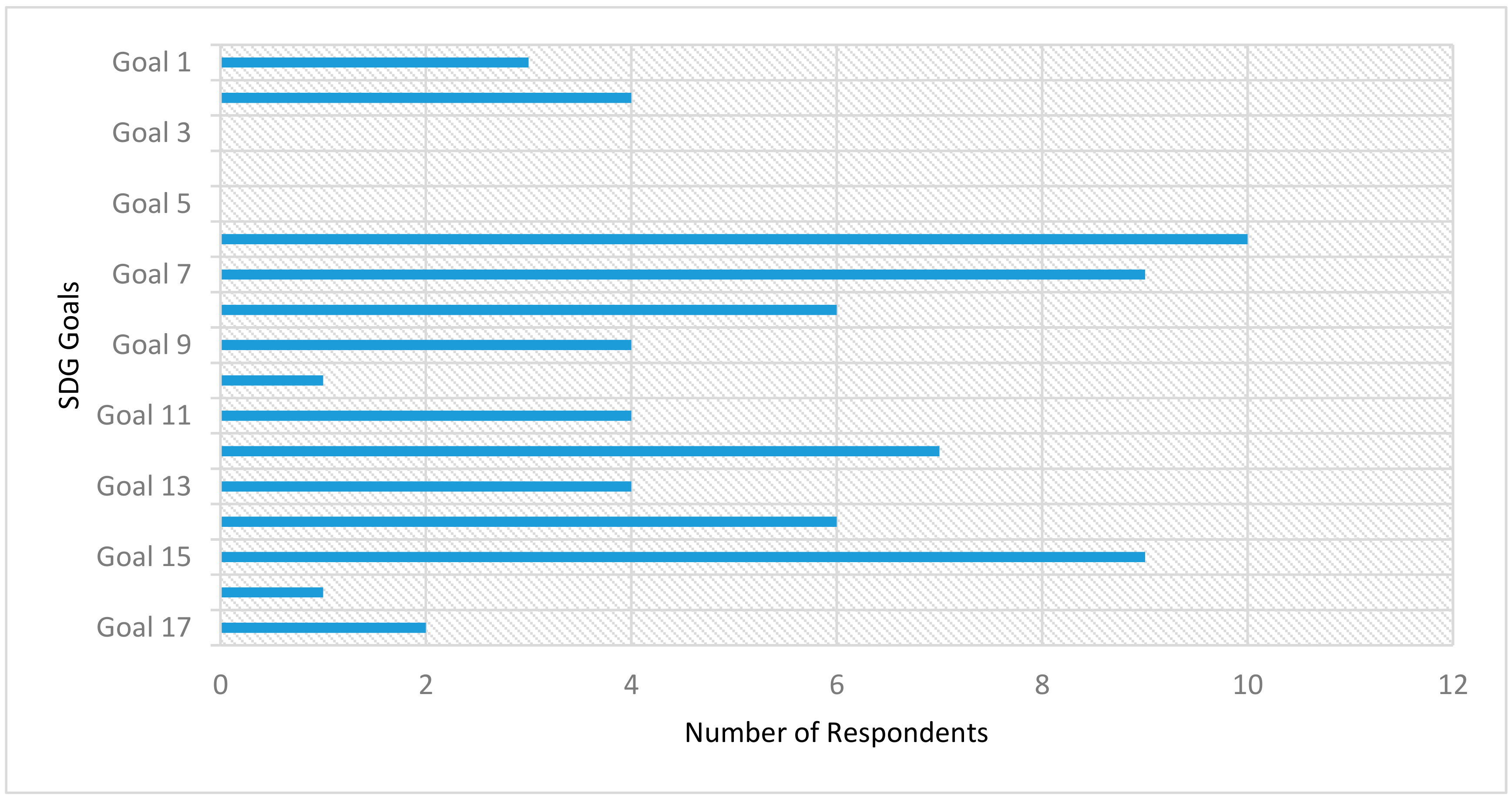

- Which goal of SDGs in your view can support by the existence of the Environmental-Economic Accounts?

[ ] Goal 1 End poverty in all its forms everywhere [ ] Goal 2 End hunger, achieve food security and improved nutrition and promote sustainable agriculture [ ] Goal 3 Ensure healthy lives and promote well-being for all at all ages [ ] Goal 4 Ensure inclusive and equitable quality education and promote lifelong learning opportunities for all [ ] Goal 5 Achieve gender equality and empower all women and girls [ ] Goal 6 Ensure availability and sustainable management of water and sanitation for all [ ] Goal 7 Ensure access to affordable, reliable, sustainable and modern energy for all [ ] Goal 8 Promote sustained, inclusive and sustainable economic growth, full and productive employment and decent work for all [ ] Goal 9 Build resilient infrastructure, promote inclusive and sustainable industrialization and foster innovation [ ] Goal 10 Reduce inequality within and among countries [ ] Goal 11 Make cities and human settlements inclusive, safe, resilient and sustainable [ ] Goal 12 Ensure sustainable consumption and production patterns [ ] Goal 13 Take urgent action to combat climate change and its impacts* [ ] Goal 14 Conserve and sustainably use the oceans, seas and marine resources for sustainable development [ ] Goal 15 Protect, restore and promote sustainable use of terrestrial ecosystems, sustainably manage forests, combat desertification, and halt and reverse land degradation and halt biodiversity loss [ ] Goal 16 Promote peaceful and inclusive societies for sustainable development, provide access to justice for all and build effective, accountable and inclusive institutions at all levels [ ] Goal 17 Strengthen the means of implementation and revitalize the global partnership for sustainable development - Which is the most potential goal of SDGs can support by Environmental-Economic Accounts?

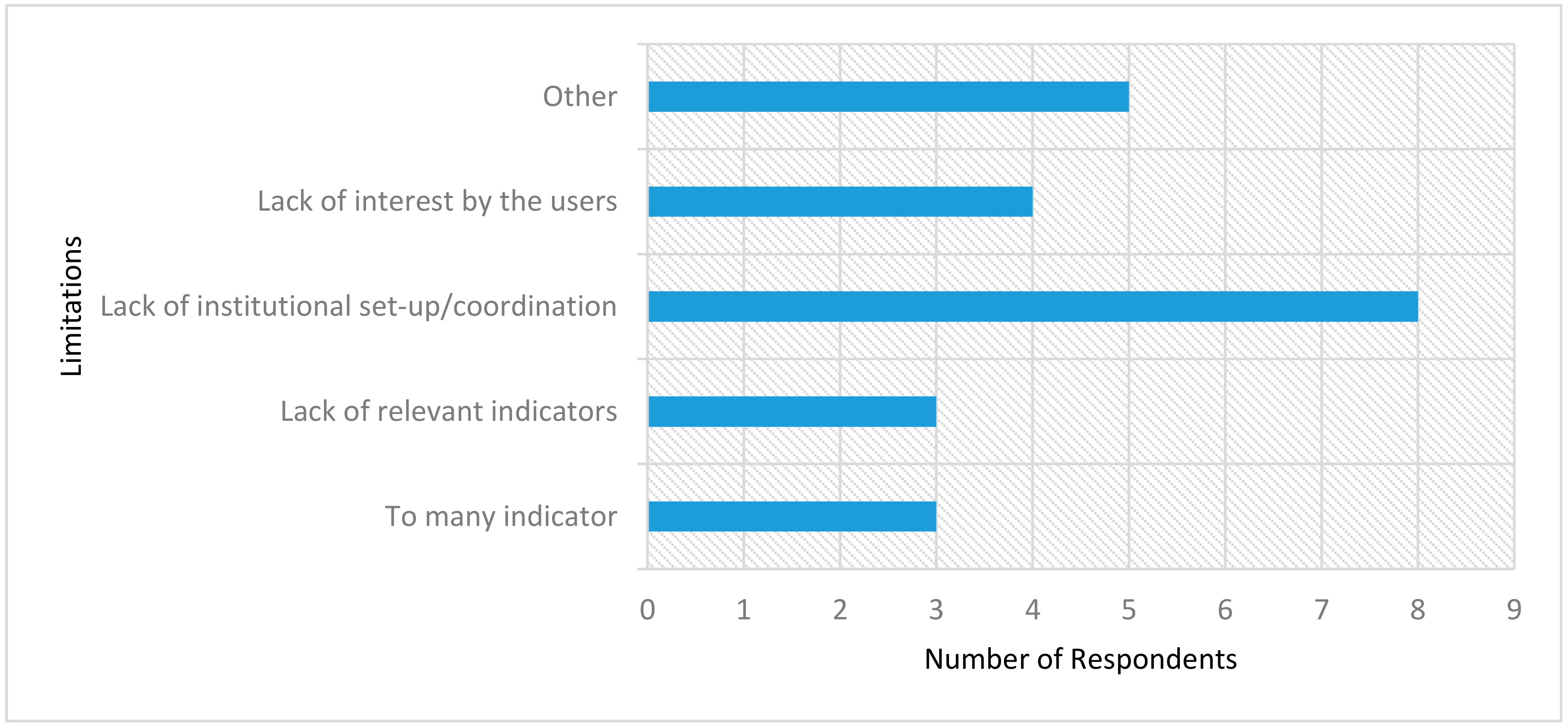

[ ] Goal 1 End poverty in all its forms everywhere [ ] Goal 2 End hunger, achieve food security and improved nutrition and promote sustainable agriculture [ ] Goal 3 Ensure healthy lives and promote well-being for all at all ages [ ] Goal 4 Ensure inclusive and equitable quality education and promote lifelong learning opportunities for all [ ] Goal 5 Achieve gender equality and empower all women and girls [ ] Goal 6 Ensure availability and sustainable management of water and sanitation for all [ ] Goal 7 Ensure access to affordable, reliable, sustainable and modern energy for all [ ] Goal 8 Promote sustained, inclusive and sustainable economic growth, full and productive employment and decent work for all [ ] Goal 9 Build resilient infrastructure, promote inclusive and sustainable industrialization and foster innovation [ ] Goal 10 Reduce inequality within and among countries [ ] Goal 11 Make cities and human settlements inclusive, safe, resilient and sustainable [ ] Goal 12 Ensure sustainable consumption and production patterns [ ] Goal 13 Take urgent action to combat climate change and its impacts* [ ] Goal 14 Conserve and sustainably use the oceans, seas and marine resources for sustainable development [ ] Goal 15 Protect, restore and promote sustainable use of terrestrial ecosystems, sustainably manage forests, combat desertification, and halt and reverse land degradation and halt biodiversity loss [ ] Goal 16 Promote peaceful and inclusive societies for sustainable development, provide access to justice for all and build effective, accountable and inclusive institutions at all levels [ ] Goal 17 Strengthen the means of implementation and revitalize the global partnership for sustainable development - What are the limitation of comprehensive Environmental-Economic Accounts to support SDG indicators monitoring?[ ] To many indicator[ ] Lack of relevant indicators[ ] Lack of institutional set-up/coordination[ ] Lack of interest by the users[ ] Other → Please specify (there is no limit in number of characters): _______

- What were the major constraints in starting the compilation of the (current) Environmental-Economic Accounts in your country? (Please check all that apply)[ ] Lack of institutional set-up/coordination[ ] Lack of financial resources[ ] Lack of human resources[ ] Lack of technical capabilities[ ] Lack of access to training material[ ] Lack of interest by the users[ ] Availability of data[ ] Quality of data[ ] Other → Please specify (there is no limit in number of characters): _______

- What have been the major constraints further expanding the Environmental-Economic Accounting Program?[ ] Lack of institutional set-up/coordination[ ] Lack of financial resources[ ] Lack of human resources[ ] Lack of technical capabilities[ ] Lack of access to training material[ ] Lack of interest by the users[ ] Availability of data[ ] Quality of data[ ] Other → Please specify (there is no limit in number of characters): _______

- Are there plans to compile any modules of the Environmental-Economic Accounts in your country in the near future?[ ] Yes → Which modules?[ ] Water Accounts[ ] Mineral Asset Accounts[ ] Energy and Emission Accounts[ ] Forest Accounts[ ] Land and Ecosystem Accounts[ ] Material Flows Accounts/Waste Accounts[ ] Environmental Protection Expenditure Accounts (EPEA)[ ] Physical Supply and Use Tables (PSUT)[ ] Other → Please specify (there is no limit in number of characters): _______[ ] No

Appendix B.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| No. | Country | Affiliation | Position |

|---|---|---|---|

| 1 | Columbia | National Administrative Department of Statistics (DANE) | Coordinator Indicators and Environmental Accounts |

| 2 | Chile | Ministry of the Environment | Manager—Unit of Environmental Accounts and Indicators |

| 3 | Brasil | Instituto Brasileiro de Geografia e Estatística | técnico em informações geográficas e estatística |

| 4 | Curacao | Central Bureau of Statistics (CBS) | Analyst, Head Business and Environmental Statistics |

| 5 | Guatemala | Universidad Rafael Landívar/IARNA | Academic research associate/Sr. Environmental Economist WAVES |

| 6 | Costa Rica | Banco Central de Costa Rica (BCCR) | Coordinator of Environmental Statistics Unit |

| 7 | Bangladesh | Bangladesh Bureau of Statistics (BBS) | Deputy Director |

| 8 | Philipines | Resources, Environment and Economics Center for Studies | President/ Resoure Economict |

| 9 | Indonesia | Central Bureau of Statistics (CBS) | Head of Sub-directorate on Regional Production Account |

| 10 | Iran | Statistical Centre of Iran | Director General, Office of the Head, Public Relations and International cooperation |

| 11 | Fiji | Fiji Bureau of Statistics | Government statistician |

| 12 | South Africa | Statistics South Africa | Deputy Director: Application of National Accounts |

| 13 | Botswana | Ministry of Finance & economic Development | Chief Economist/Coordinator of WAVES Program for Botswana |

| 14 | Jamaica | Science and Technology Development Planner/SIDS | Dock National Coordinator Planning Institute of Jamaica (PIOJ) |

Appendix C

| Goals and Targets | Indicators | Account | Type of Account | Tier |

|---|---|---|---|---|

| Goal 2. End hunger, achieve food security and improved nutrition and promote sustainable agriculture | ||||

| 2.3 By 2030, double the agricultural productivity and incomes of small-scale food producers, in particular women, indigenous peoples, family farmers, pastoralists and fishers, including through secure and equal access to land, other productive resources and inputs, knowledge, financial services, markets and opportunities for value addition and non-farm employment | 2.3.1 Volume of production per labour unit by classes of farming/pastoral/forestry enterprise size | Agriculture, Forestry and Fisheries | All | Tier II |

| 2.4 By 2030, ensure sustainable food production systems and implement resilient agricultural practices that increase productivity and production, that help maintain ecosystems, that strengthen capacity for adaptation to climate change, extreme weather, drought, flooding and other disasters and that progressively improve land and soil quality | 2.4.1 Proportion of agricultural area under productive and sustainable agriculture | Land + Agriculture, Forestry and Fisheries | Asset accounts | Tier II |

| 2.a Increase investment, including through enhanced international cooperation, in rural infrastructure, agricultural research and extension services, technology development and plant and livestock gene banks in order to enhance agricultural productive capacity in developing countries, in particular least developed countries | 2.a.1 The agriculture orientation index for government expenditures | SNA + Environmental activities | All | Tier I |

| Goal 6. Ensure availability and sustainable management of water and sanitation for all | ||||

| 6.1 By 2030, achieve universal and equitable access to safe and affordable drinking water for all | 6.1.1 Proportion of population using safely managed drinking water services | Water | PSUT + Economic Accounts | Tier II |

| 6.2 By 2030, achieve access to adequate and equitable sanitation and hygiene for all and end open defecation, paying special attention to the needs of women and girls and those in vulnerable situations | 6.2.1 Proportion of population using safely managed sanitation services, including a hand-washing facility with soap and water | Water | PSUT + Economic Accounts | Tier II |

| 6.3 By 2030, improve water quality by reducing pollution, eliminating dumping and minimizing release of hazardous chemicals and materials, halving the proportion of untreated wastewater and substantially increasing recycling and safe reuse globally | 6.3.1 Proportion of wastewater safely treated | Water | PSUT | Tier II |

| 6.3.2 Proportion of bodies of water with good ambient water quality | Materials | Emmission Accounts | Tier II | |

| 6.4 By 2030, substantially increase water-use efficiency across all sectors and ensure sustainable withdrawals and supply of freshwater to address water scarcity and substantially reduce the number of people suffering from water scarcity | 6.4.1 Change in water-use efficiency over time | SNA + Water | PSUT + All | Tier II |

| 6.4.2 Level of water stress: freshwater withdrawal as a proportion of available freshwater resources | Water | Tier I | ||

| 6.5 By 2030, implement integrated water resources management at all levels, including through transboundary cooperation as appropriate | 6.5.1 Degree of integrated water resources management implementation (0-100) | Water | PSUT + Physical asset accounts | Tier I |

| 6.6 By 2020, protect and restore water-related ecosystems, including mountains, forests, wetlands, rivers, aquifers and lakes | 6.6.1 Change in the extent of water-related ecosystems over time | Ecosystems | Ecosystems extent accounts | Tier II |

| 6.a By 2030, expand international cooperation and capacity-building support to developing countries in water- and sanitation-related activities and programmes, including water harvesting, desalination, water efficiency, wastewater treatment, recycling and reuse technologies | 6.a.1 Amount of water- and sanitation-related official development assistance that is part of a government-coordinated spending plan | Water | PSUT + Economic Accounts | Tier I |

| Goal 7. Ensure access to affordable, reliable, sustainable and modern energy for all | ||||

| 7.1 By 2030, ensure universal access to affordable, reliable and modern energy services | 7.1.1 Proportion of population with access to electricity | Energy | PSUT+Economic Accounts+Asset accounts | Tier I |

| 7.1.2 Proportion of population with primary reliance on clean fuels and technology | Energy | PSUT+Economic Accounts+Asset accounts | Tier I | |

| 7.2 By 2030, increase substantially the share of renewable energy in the global energy mix | 7.2.1 Renewable energy share in the total final energy consumption | Energy | PSUT | Tier I |

| 7.3 By 2030, double the global rate of improvement in energy efficiency | 7.3.1 Energy intensity measured in terms of primary energy and GDP | SNA + Energy | PSUT+Value added from SNA | Tier I |

| 7.b By 2030, expand infrastructure and upgrade technology for supplying modern and sustainable energy services for all in developing countries, in particular least developed countries, small island developing States and landlocked developing countries, in accordance with their respective programmes of support | 7.b.1 Investments in energy efficiency as a percentage of GDP and the amount of foreign direct investment in financial transfer for infrastructure and technology to sustainable development services | SNA + Energy | PSUT+ value added from SNA | Tier III |

| Goal 8. Promote sustained, inclusive and sustainable economic growth, full and productive employment and decent work for all | ||||

| 8.4 Improve progressively, through 2030, global resource efficiency in consumption and production and endeavor to decouple economic growth from environmental degradation, in accordance with the 10-Year Framework of Programmes on Sustainable Consumption and Production, with developed countries taking the lead | 8.4.1 Material footprint, material footprint per capita, and material footprint per GDP | Materials | Material flow accounts | Tier II |

| 8.4.2 Domestic material consumption, domestic material consumption per capita, and domestic material consumption per GDP | Materials | Material flow accounts | Tier I | |

| 8.9 By 2030, devise and implement policies to promote sustainable tourism that creates jobs and promotes local culture and products | 8.9.1 Tourism direct GDP as a proportion of total GDP and in growth rate | SNA | Tourism satellite account | Tier II |

| 8.9.2 Number of jobs in tourism industries as a proportion of total jobs and growth rate of jobs, by sex | SNA | Tourism satellite account | Tier III | |

| Goal 9. Build resilient infrastructure, promote inclusive and sustainable industrialization and foster innovation | ||||

| 9.4 By 2030, upgrade infrastructure and retrofit industries to make them sustainable, with increased resource-use efficiency and greater adoption of clean and environmentally sound technologies and industrial processes, with all countries taking action in accordance with their respective capabilities | 9.4.1 CO2 emission per unit of value added | Materials | Air emission accounts + SNA | Tier I |

| Goal 11. Make cities and human settlements inclusive, safe, resilient and sustainable | ||||

| 11.3 By 2030, enhance inclusive and sustainable urbanization and capacity for participatory, integrated and sustainable human settlement planning and management in all countries | 11.3.1 Ratio of land consumption rate to population growth rate | Land | Asset accounts | Tier II |

| 11.4 Strengthen efforts to protect and safeguard the world’s cultural and natural heritage | 11.3.2 Total expenditure (public and private) per capita spent on the preservation, protection and conservation of all cultural and natural heritage, by type of heritage (cultural, natural, mixed and World Heritage Centre designation), level of government (national, regional and local/municipal), type of expenditure (operating expenditure/investment) and type of private funding (donations in kind, private non-profit sector and sponsorship) | Environmental activities | Env. Protection expenditure accounts + Resource management expenditure accounts | Tier III |

| 11.6 By 2030, reduce the adverse per capita environmental impact of cities, including by paying special attention to air quality and municipal and other waste management | 11.6.1 Proportion of urban solid waste regularly collected and with adequate final discharge out of total urban solid waste generated, by cities | Materials | Solid waste accounts | Tier II |

| 11.c Support least developed countries, including through financial and technical assistance, in building sustainable and resilient buildings utilizing local materials | 11.c.1 Proportion of financial support to the least developed countries that is allocated to the construction and retrofitting of sustainable, resilient and resource-efficient buildings utilizing local materials | Environmental activities | Env. Protection expenditure accounts | Tier III |

| Goal 12. Ensure sustainable consumption and production patterns | ||||

| 12.2 By 2030, achieve the sustainable management and efficient use of natural resources | 12.2.1 Material footprint, material footprint per capita, and material footprint per GDP | Materials | Material flow accounts | Tier II |

| 12.2.2 Domestic material consumption, domestic material consumption per capita, and domestic material consumption per GDP | Materials | Material flow accounts | Tier I | |

| 12.4.2 Hazardous waste generated per capita and proportion of hazardous waste treated, by type of treatment | Materials | Solid waste accounts | Tier III | |

| 12.5 By 2030, substantially reduce waste generation through prevention, reduction, recycling and reuse | 12.5.1 National recycling rate, tons of material recycled | Materials | Solid waste accounts | Tier III |

| 12.c Rationalize inefficient fossil-fuel subsidies that encourage wasteful consumption by removing market distortions, in accordance with national circumstances, including by restructuring taxation and phasing out those harmful subsidies, where they exist, to reflect their environmental impacts, taking fully into account the specific needs and conditions of developing countries and minimizing the possible adverse impacts on their development in a manner that protects the poor and the affected communities | 12.c.1 Amount of fossil-fuel subsidies per unit of GDP (production and consumption) and as a proportion of total national expenditure on fossil fuels | Energy | Energy accounts and Environmental taxes and subsidies accounts | Tier II |

| Goal 14. Conserve and sustainably use the oceans, seas and marine resources for sustainable development | ||||

| 14.4 By 2020, effectively regulate harvesting and end overfishing, illegal, unreported and unregulated fishing and destructive fishing practices and implement science-based management plans, in order to restore fish stocks in the shortest time feasible, at least to levels that can produce maximum sustainable yield as determined by their biological characteristics | 14.4.1 Proportion of fish stocks within biologically sustainable levels | Aquatic resources | Asset accounts | Tier I |

| 14.5 By 2020, conserve at least 10 per cent of coastal and marine areas, consistent with national and international law and based on the best available scientific information | 14.5.1 Coverage of protected areas in relation to marine areas | Land | Asset accounts | Tier I |

| 14.7 By 2030, increase the economic benefits to small island developing States and least developed countries from the sustainable use of marine resources, including through sustainable management of fisheries, aquaculture and tourism | 14.7.1 Sustainable fisheries as a percentage of GDP in small island developing States, least developed countries and all countries | Agriculture, Forestry and Fisheries | All | Tier I |

| 14.a Increase scientific knowledge, develop research capacity and transfer marine technology, taking into account the Intergovernmental Oceanographic Commission Criteria and Guidelines on the Transfer of Marine Technology, in order to improve ocean health and to enhance the contribution of marine biodiversity to the development of developing countries, in particular small island developing States and least developed countries | 14.a.1 Proportion of total research budget allocated to research in the field of marine technology | Environmental activities | Env. Protection expenditure accounts | Tier II |

| Goal 15. Protect, restore and promote sustainable use of terrestrial ecosystems, sustainably manage forests, combat desertification, and halt and reverse land degradation and halt biodiversity loss | ||||

| 15.1 By 2020, ensure the conservation, restoration and sustainable use of terrestrial and inland freshwater ecosystems and their services, in particular forests, wetlands, mountains and drylands, in line with obligations under international agreements | 15.1.1 Forest area as a proportion of total land area | Land | Asset accounts | Tier I |

| 15.1.2 Proportion of important sites for terrestrial and freshwater biodiversity that are covered by protected areas, by ecosystem type | Land | Asset accounts | Tier I | |

| 15.3 By 2030, combat desertification, restore degraded land and soil, including land affected by desertification, drought and floods, and strive to achieve a land degradation-neutral world | 15.1.3 Proportion of land that is degraded over total land area | Ecosystems | Condition accounts | Tier II |

| 15.4 By 2030, ensure the conservation of mountain ecosystems, including their biodiversity, in order to enhance their capacity to provide benefits that are essential for sustainable development | 15.4.1 Coverage by protected areas of important sites for mountain biodiversity | Land | Asset accounts | Tier I |

| 15.4.2 Mountain Green Cover Index | Land | Asset accounts | Tier I | |

| 15.5 Take urgent and significant action to reduce the degradation of natural habitats, halt the loss of biodiversity and, by 2020, protect and prevent the extinction of threatened species | 15.5.1 Red List Index | Ecosystems | Biodiversity accounts | Tier I |

| 15.9 By 2020, integrate ecosystem and biodiversity values into national and local planning, development processes, poverty reduction strategies and accounts | 15.9.1 Progress towards national targets established in accordance with Aichi Biodiversity Target 2 of the Strategic Plan for Biodiversity 2011-2020 | Ecosystems | Condition accounts + Ecosystem service account + Biodiversity accounts | Tier III |

| 15.a Mobilize and significantly increase financial resources from all sources to conserve and sustainably use biodiversity and ecosystems | 15.a.1 Official development assistance and public expenditure on conservation and sustainable use of biodiversity and ecosystems | Environmental activities | Env. Protection expenditure accounts | Tier I/III |

| 15.b Mobilize significant resources from all sources and at all levels to finance sustainable forest management and provide adequate incentives to developing countries to advance such management, including for conservation and reforestation | 15.b.1 Official development assistance and public expenditure on conservation and sustainable use of biodiversity and ecosystems | Environmental activities | Env. Protection expenditure accounts | Tier I/III |

| Goal 17. Strengthen the means of implementation and revitalize the Global Partnership for Sustainable Development | ||||

| 17.1 Strengthen domestic resource mobilization, including through international support to developing countries, to improve domestic capacity for tax and other revenue collection | 17.1.1 Total government revenue as a proportion of GDP, by source | Environmental activities | Env. Protection expenditure accounts | Tier I |

| 17.1.2 Proportion of domestic budget funded by domestic taxes | Environmental activities | Env. Protection expenditure accounts | Tier I | |

| : Indicator as currently proposed can be informed by the SEEA Accounts | |

| : Either current wording and concepts of indicator needs to be aligned to be SEEA compliant; or indicator needs to be further defined to ensure SEEA compliance (i.e., detailed definitions added) | |

| : While the indicator cannot be informed by the SEEA, either; a) the SEEA can provide important contextual information and the indicator should be developed with the SEEA approach in mind; or b) there is some overlap with SEEA methodology which should be considered when formulating this indicator. |

Appendix D

References

- Alisjahbana, A.S.; Murniningtyas, E. Tujuan Pembangunan Berkelanjutan di Indonesia: Konsep, Target dan Strategi Implementasi; UNPAD Press: West Java, Indonesia, 2018. [Google Scholar]

- Nicolai, S.; Hoy, C.; Berliner, T.; Aedy, T. Projecting Progress: Reaching the SDGs by 2030. In Development Progress Research Report; ODI: London, UK, 2015. [Google Scholar]

- Sachs, J.; Schmidt-Traub, G.; Kroll, C.; Durand-Delacre, D.; Teksoz, K. SDG Index and Dashboards Report 2017; Bertelsmann Stiftung and Sustainable Development Solutions Network (SDSN): New York, NY, USA, 2017. [Google Scholar]

- March, R. Greening GDP: Overcoming Challenges in Natural Capital Accounting. Ph.D. Thesis, Bard College, Dutchess, NY, USA, May 2015. [Google Scholar]

- Alfsen, K.H.; Greaker, M. From natural resources and environmental accounting to construction of indicators for sustainable development. Ecol. Econ. 2007, 61, 600–610. [Google Scholar] [CrossRef]

- United Nations Statistics Division (UNSD). SDG Indicators Metadata; UNSD: New York, NY, USA, 2017. [Google Scholar]

- Smith, R. Development of the SEEA 2003 and its implementation. Ecol. Econ. 2007, 61, 592–599. [Google Scholar] [CrossRef]

- Palm, V.; Larsson, M. Economic instruments and the environmental accounts. Ecol. Econ. 2007, 61, 684–692. [Google Scholar] [CrossRef]

- Nahman, A.; Mahumani, B.K.; de Lange, W.J. Beyond GDP: Towards a Green Economy Index. Dev. South. Afr. 2016, 3, 215–233. [Google Scholar] [CrossRef]

- United Nation. System of Environmental Economic Accounting. 2016. Available online: http://unstats.un.org/unsd/envaccounting/seea.asp (accessed on 4 November 2018).

- United Nations Statistics Division (UNSD). SEEA and Transforming Global and National Statistical Systems for Monitoring SDG Indicators. In Proceedings of the Tenth Meeting of the UN Committee of Experts on Environmental Economic Accounting, New York, NY, USA, 24–26 June 2015. [Google Scholar]

- United Nations Statistics Division (UNSD). The SEEA as the Statistical Framework in Meeting Data Quality Criteria for SDG Indicators; UNSD: New York, NY, USA, 2015. [Google Scholar]

- Bann, C. Natural capital accounting and the Sustainable Development Goals. WAVES Policy Briefing. 2016, 1, 1–8. [Google Scholar]

- United Nations Committee of Experts on Environmental-Economic Accounting (UNCEEA). Broad-Brush Analysis of SEEA Relevant SDG Indicators; New York, 22–24 June 2016. Available online: https://unstats.un.org/unsd/envaccounting/ceea/meetings/eleventh_meeting/lod11.htm.

- World Bank. Natural Capital Accounting; World Bank: Washington, DC, USA, 2016; pp. 1–4. [Google Scholar]

- Vardon, M.; Lange, G.M.; Johansson, S. Achievements and Lessons from the Waves First 5 Core Implementing Countries; World Bank: Washington, DC, USA, 2016. [Google Scholar]

- WAVES. Natural Capital Accounting and Policy Costa Rica. Available online: https://www.wavespartnership.org/sites/waves/files/kc/Costa%20Rica%20offer%20doc_FINAL.pdf (accessed on 25 May 2018).

- United Nations Statistics Division (UNSD). Revision of the System of Environmental-Economic Accounting (SEEA) SEEA Central Framework; UNSD: New York, NY, USA, 2012. [Google Scholar]

- UNSD. Global Assessment of Environment Statistics and Environmental-Economic Accounting; UNSD: New York, NY, USA, 2007. [Google Scholar]

- UNSD. Global Assessment of Environmental-Economic Accounting and Supporting Statistics 2014; UNSD: New York, NY, USA, 2015. [Google Scholar]

- UNSD. Global Assessment of Environmental-Economic Accounting and Supporting Statistics 2017; UNSD: New York, NY, USA, 2018. [Google Scholar]

- Edens, B.; de Haan, M.; Shenau, S. Initiating a SEEA Implementation Program—A First Investigation of Possibilities. United Nations Department of Economic and Social Affairs, Statistics Division. Sixth Meeting of the UN Committee of Experts on Environmental Economic Accounting, New York, ESA/STAT/AC.238, UNCEEA/6/19. Available online: http://unstats.un.org/unsd/envaccounting/ceea/meetings/UNCEEA-6-19.pdf (accessed on 17 June 2018).

- Aoki-Suzuki, C.; Bengtsson, M.; Hotta, Y. International comparison and suggestions for capacity development in industrializing countries: Policy application of economy-wide material flow accounting. J. Ind. Ecol. 2012, 16, 467–480. [Google Scholar] [CrossRef]

- Naidu, S. Implementation of System of Environmental-Economic Accounting in the Pacific: Achievements and Lessons; United Nations Economic and Social Commission for Asia and the Pacific (ESCAP): Bangkok, Thailand, 2017. [Google Scholar]

| Category | Relevant Indicators |

|---|---|

| Indicator as currently proposed can be informed by the SEEA accounts. | 11 indicators |

| Either current wording and concepts of the indicator need to be aligned to be SEEA compliant or the indicator needs to be further defined to ensure SEEA compliance (i.e., detailed definitions added). | 23 indicators |

| While the indicator cannot be informed by the SEEA, either: (a) the SEEA can provide important contextual information, and the indicator should be developed with the SEEA approach in mind; or (b) there is some overlap with the SEEA methodology that should be considered when formulating this indicator. | 12 indicators |

| Account | Type of Account | Goal 2 | Goal 6 | Goal 7 | Goal 8 | Goal 9 | Goal 11 | Goal 12 | Goal 14 | Goal 15 | Goal 17 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Land | Asset accounts | √ | √ | √ | √ | ||||||

| Energy | Physical Supply and Use Tables (PSUT) | √ | √ | ||||||||

| Economic accounts | √ | √ | |||||||||

| Asset accounts | √ | ||||||||||

| Water | PSUT + Economic accounts | √ | |||||||||

| Asset accounts | √ | ||||||||||

| Materials | Material flow accounts | √ | √ | √ | √ | ||||||

| Emissions accounts | √ | ||||||||||

| Air Emissions accounts | √ | √ | |||||||||

| Solid Waste accounts | √ | √ | |||||||||

| Aquatic resources | Asset accounts | √ | |||||||||

| Agriculture, forestry, and fisheries | All | √ | √ | ||||||||

| Environmental Activities | Environmental protection Expenditure account | √ | √ | √ | √ | ||||||

| Resource management expenditure accounts | √ | ||||||||||

| Environmental taxes and subsidies accounts | √ | √ | |||||||||

| Ecosystem | Condition accounts | √ | |||||||||

| Ecosystem extent accounts | √ | √ | |||||||||

| Ecosystem services accounts | √ | ||||||||||

| Biodiversity accounts | √ | ||||||||||

| UN-SNA | All | √ | √ | √ | √ | ||||||

| Value added | √ | ||||||||||

| Tourism | √ | √ |

| Indicators | Account | Tier |

|---|---|---|

| 2.4.1 Proportion of agricultural area under productive and sustainable agriculture | Land + Agriculture, Forestry and Fisheries | Tier 2 |

| 2.a.1 The agriculture orientation index for government expenditures | SNA + Environmental Activities | Tier 1 |

| 6.3.1 Proportion of wastewater safely treated | Water | Tier 2 |

| 6.4.2 Level of water stress: freshwater withdrawal as a proportion of available freshwater resources | Water | Tier 1 |

| 7.1.1 Proportion of population with access to electricity | Energy | Tier 1 |

| 7.3.1 Energy intensity measured in terms of primary energy and GDP | SNA + Energy | Tier 1 |

| 8.4.1 Material footprint, material footprint per capita, and material footprint per GDP | Materials | Tier 2 |

| 8.9.1 Direct tourism GDP as a proportion of the total GDP and growth rate | SNA | Tier 2 |

| 9.4.1 CO2 emissions per unit of value added | Materials | Tier 1 |

| 11.3.1 Ratio of land consumption rate to population growth rate | Land | Tier 2 |

| 11.6.1 Proportion of urban solid waste regularly collected and with adequate final discharge out of the total urban solid waste generated by cities | Materials | Tier 2 |

| 12.2.1 Material footprint, material footprint per capita, and material footprint per GDP | Materials | Tier 2 |

| 12.5.1 National recycling rate; tons of material recycled | Materials | Tier 3 |

| 14.4.1 Proportion of fish stocks within biologically sustainable levels | Aquatic Resources | Tier 1 |

| 14.7.1 Sustainable fisheries as a percentage of GDP in small island developing states in the least developed countries and all countries | Agriculture, Forestry and Fisheries | Tier 1 |

| 15.1.1 Forest area as a proportion of the total land area | Land | Tier 1 |

| 15.a.1 Official development assistance and public expenditure on conservation and sustainable use of biodiversity and ecosystems | Environmental Activities | Tier 1/3 |

| 17.1.1 Total government revenue as a proportion of GDP by source | Environmental Activities | Tier 1 |

| 17.1.2 Proportion of domestic budget funded by domestic taxes | Environmental Activities | Tier 1 |

| Ch3 | Ch4 | Ch5 | Ch6 | |

|---|---|---|---|---|

| Flows a) | Monetary b) | Assets c) | Sequence d) | |

| Australia | x | x | x | x |

| Botswana | x | |||

| Brazil | x | |||

| Canada | x | x | x | x |

| China | x | x | ||

| Colombia | x | x | x | |

| India | x | x | x | |

| Indonesia | x | x | x | |

| Japan | x | x | x | x |

| Jordan | x | x | ||

| Mexico | x | x | x | |

| Namibia | x | |||

| New Zealand | x | x | x | |

| Philippines | x | x | x | |

| Korea | x | |||

| South Africa | x | x | ||

| USA | x | x | x | |

| EU | x | x | x | x |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Pirmana, V.; Alisjahbana, A.S.; Hoekstra, R.; Tukker, A. Implementation Barriers for a System of Environmental-Economic Accounting in Developing Countries and Its Implications for Monitoring Sustainable Development Goals. Sustainability 2019, 11, 6417. https://doi.org/10.3390/su11226417

Pirmana V, Alisjahbana AS, Hoekstra R, Tukker A. Implementation Barriers for a System of Environmental-Economic Accounting in Developing Countries and Its Implications for Monitoring Sustainable Development Goals. Sustainability. 2019; 11(22):6417. https://doi.org/10.3390/su11226417

Chicago/Turabian StylePirmana, Viktor, Armida Salsiah Alisjahbana, Rutger Hoekstra, and Arnold Tukker. 2019. "Implementation Barriers for a System of Environmental-Economic Accounting in Developing Countries and Its Implications for Monitoring Sustainable Development Goals" Sustainability 11, no. 22: 6417. https://doi.org/10.3390/su11226417

APA StylePirmana, V., Alisjahbana, A. S., Hoekstra, R., & Tukker, A. (2019). Implementation Barriers for a System of Environmental-Economic Accounting in Developing Countries and Its Implications for Monitoring Sustainable Development Goals. Sustainability, 11(22), 6417. https://doi.org/10.3390/su11226417