Assessing the Relevance of Green Banking Practice on Bank Loyalty: The Mediating Effect of Green Image and Bank Trust

Abstract

1. Introduction

2. Theoretical Framework and Hypothesis

2.1. Socially Responsible Investment Theory

2.2. Green Banking Effect

2.3. Green Image Effect

2.4. Bank Trust

2.5. Mediating Role of Green Image and Bank Trust

3. Methods

3.1. Research Design

3.2. Analytical Techniques

4. Results

4.1. Convergent Validity

4.2. Discriminant Validity

4.3. Test of Hypothesis

5. Discussion

6. Conclusions

Limitations

Author Contributions

Funding

Conflicts of Interest

References

- Kassarjian, H.H. Incorporating ecology into marketing strategy: The case of air pollution. J. Mark. 1971, 35, 61–65. [Google Scholar] [CrossRef]

- Polonsky, M.J. Green marketing regulation in the US and Australia: The Australian checklist. Greener Manag. Int. 1994, 5, 44–53. [Google Scholar]

- Jain, S.K.; Kaur, G. Green Marketing: An Indian Perspective. Decision 2004, 31, 168–209. [Google Scholar]

- Lefebvre, R.C. An integrative model for social marketing. J. Soc. Mark. 2011, 1, 54–72. [Google Scholar] [CrossRef]

- Wood, D.J.; Jones, R.E. Stakeholder mismatching: A theoretical problem in empirical research on corporate social performance. Int. J. Org. Anal. 1995, 3, 229–267. [Google Scholar] [CrossRef]

- Biswas, N. Sustainable green banking approach: The need of the hour. Bus. Spectr. 2011, 1, 32–38. [Google Scholar]

- Bahl, S. Green banking-The new strategic imperative. Asian J. Res. Bus. Econ. Manag. 2012, 2, 176–185. [Google Scholar]

- Knörzer, A. The transition from environmental funds to sustainable investment: The practical application of sustainability criteria in investment products in Bouma, M. In Sustainable Banking: The Greening of Finance; Greenleaf Publishing: Sheffield, UK, 2001; pp. 211–221. [Google Scholar]

- Derwall, J.; Guenster, N.; Bauer, R.; Koedijk, K. The eco-efficiency premium puzzle. Financ. Anal. J. 2005, 61, 51–63. [Google Scholar] [CrossRef]

- Courvisanos, J. The political economy of R&D in a global financial context. In Powerful Finance and Innovation Trends in a High-Risk Economy; Springer: Berlin, Germany, 2008; pp. 88–109. [Google Scholar]

- EIM (European Investment Monitor) and Oxford Research. Financing Eco Innovation. Final report. EIM and Oxford Report Research for the European Commission, DG, Environment; EIM (European Investment Monitor) and Oxford Research: London, UK, 2011. [Google Scholar]

- Green Network Bank. Green Network Impact through July 2018. Available online: http://greenbanknetwork.org/gbn-impact/ (accessed on 7 April 2019).

- Masukujjaman, M.; Siwar, C.; Mahmud, M.R.; Alam, S.S. Bankers’ perception of Green Banking: Learning from the experience of Islamic banks in Bangladesh. Geogr.-Malays. J. Soc. Space 2017, 12, 144–153. [Google Scholar]

- Rifat, A.; Nisha, N.; Iqbal, M.; Suvittawat, A. The role of commercial banks in green banking adoption: A Bangladesh perspective. Int. J. Green Econ. 2016, 10, 226–251. [Google Scholar] [CrossRef]

- Iqbal, M.; Nisha, N.; Rifat, A.; Panda, P. Exploring Client Perceptions and Intentions in Emerging Economies: The Case of Green Banking Technology. Int. J. Asian Bus. Inf. Manag. 2018, 9, 14–34. [Google Scholar] [CrossRef]

- Coalition for Green Capital. Growing Clean Energy Market with Green Bank Financing. A Green Bank White Paper; Coalition for Green Capital: Washington, DC, USA, 30 June 2016. [Google Scholar]

- Chen, Y.S.; Lai, S.B.; Wen, C.T. The influence of green innovation performance on corporate advantage in Taiwan. J. Bus. Eth. 2006, 67, 331–339. [Google Scholar] [CrossRef]

- Falcone, P.M.; Morone, P.; Sica, E. Greening of the financial system and fuelling a sustainability transition: A discursive approach to assess landscape pressures on the Italian financial system. Technol. Forecast. Soc. Chang. 2018, 127, 23–37. [Google Scholar] [CrossRef]

- Chen, Y.S. Towards green loyalty: Driving from green perceived value, green satisfaction, and green trust. Sustain. Dev. 2013, 21, 294–308. [Google Scholar] [CrossRef]

- Argenti, P.A. Corporate Communication; McGraw-Hill Higher Education: New York, NY, USA, 2015. [Google Scholar]

- Dick, A.S.; Basu, K. Customer loyalty: Toward an integrated conceptual framework. J. Acad. Mark. Sci. 1994, 22, 99–113. [Google Scholar] [CrossRef]

- Saha, M.; Darnton, G. Green companies or green con-panies: Are companies really green, or are they pretending to be? Bus. Soc. Rev. 2005, 110, 117–157. [Google Scholar] [CrossRef]

- Renneboog, L.; Ter Horst, J.; Zhang, C. Socially responsible investments: Institutional aspects, performance, and investor behavior. J. Bank. Financ. 2008, 32, 1723–1742. [Google Scholar] [CrossRef]

- Revelli, C.; Viviani, J.L. Financial performance of socially responsible investing (SRI): What have we learned? A meta-analysis. Bus. Eth. Eur. Rev. 2015, 24, 158–185. [Google Scholar] [CrossRef]

- Chatzitheodorou, K.; Skouloudis, A.; Evangelinos, K.; Nikolaou, I. Exploring socially responsible investment perspectives: A literature mapping and an investor classification. Sustain. Prod. Consum. 2019, 19, 117–129. [Google Scholar] [CrossRef]

- Junkus, J.; Berry, T.D. Socially responsible investing: A review of the critical issues. Manag. Financ. 2015, 41, 1176–1201. [Google Scholar] [CrossRef]

- Van Dooren, B.; Galema, R. Socially responsible investors and the disposition effect. J. Behav. Exp. Financ. 2018, 17, 42–52. [Google Scholar] [CrossRef]

- Hernandez, D.; Hugger, C. Creating social impact through responsible investing. Benefits Mag. 2016, 53, 14–22. [Google Scholar]

- Sturm, R.R.; Field, C.M. Benchmark error and socially responsible investments. Glob. Financ. J. 2018, 38, 24–29. [Google Scholar] [CrossRef]

- Lee, N.R.; Miller, M. Influencing positive financial behaviors: The social marketing solution. J. Soc. Mark. 2012, 2, 70–86. [Google Scholar] [CrossRef]

- Cervelló-Royo, R.; Guijarro, F.; Martinez-Gomez, V. Social Performance considered within the global performance of Microfinance Institutions: A new approach. Oper. Res. 2019, 19, 737–755. [Google Scholar] [CrossRef]

- Bennett, M.S.; Iqbal, Z. How socially responsible investing can help bridge the gap between Islamic and conventional financial markets. Int. J. Islam. Middle East. Financ. Manag. 2013, 6, 211–225. [Google Scholar] [CrossRef]

- Michelson, G.; Wailes, N.; Van Der Laan, S.; Frost, G. Ethical investment processes and outcomes. J. Bus. Eth. 2004, 52, 1–10. [Google Scholar] [CrossRef]

- Perks, R.W.; Rawlinson, D.H.; Ingram, L. An exploration of ethical investment in the UK. Br. Account. Rev. 1992, 24, 43–65. [Google Scholar] [CrossRef]

- Sparkes, R. Ethical investment: Whose ethics, which investment? Bus. Eth. Eur. Rev. 2001, 10, 194–205. [Google Scholar] [CrossRef]

- Bergek, A.; Mignon, I.; Sundberg, G. Who invests in renewable electricity production? Empirical evidence and suggestions for further research. Energy Policy 2013, 56, 568–581. [Google Scholar] [CrossRef]

- Flammer, C. Corporate social responsibility and shareholder reaction: The environmental awareness of investors. Acad. Manag. J. 2013, 56, 758–781. [Google Scholar] [CrossRef]

- Muñoz, J.I.; de la Nieta, A.A.; Contreras, J.; Bernal-Agustín, J.L. Optimal investment portfolio in renewable energy: The Spanish case. Energy Policy 2009, 37, 5273–5284. [Google Scholar] [CrossRef]

- Dorfleitner, G.; Nguyen, M. Which proportion of SR investments is enough? A survey-based approach. Bus. Res. 2016, 9, 1–25. [Google Scholar] [CrossRef]

- Belghitar, Y.; Clark, E.; Deshmukh, N. Does it pay to be ethical? Evidence from the FTSE4Good. J. Bank. Financ. 2014, 47, 54–62. [Google Scholar] [CrossRef]

- Ziegler, A.; Schröder, M. What determines the inclusion in a sustainability stock index?: A panel data analysis for european firms. Ecol. Econ. 2010, 69, 848–856. [Google Scholar] [CrossRef]

- Korzeb, Z.; Samaniego-Medina, R. Sustainability Performance: A Comparative Analysis in the Polish Banking Sector. Sustainability 2019, 11, 653. [Google Scholar] [CrossRef]

- Bihari, S.C. Green Banking–Socially Responsible Banking in India. India Bank. 2011, 6, 2277–7830. [Google Scholar]

- Statman, M. What do investors want? J. Portf. Manag. 2004, 30, 153–161. [Google Scholar] [CrossRef]

- Borgers, A.C.; Pownall, R.A. Attitudes towards socially and environmentally responsible investment. J. Behav. Exp. Financ. 2014, 1, 27–44. [Google Scholar] [CrossRef]

- Borghesi, R.; Houston, J.F.; Naranjo, A. Corporate socially responsible investments: CEO altruism, reputation, and shareholder interests. J. Corp. Financ. 2014, 26, 164–181. [Google Scholar] [CrossRef]

- Bauer, R.; Smeets, P. Social identification and investment decisions. J. Econ. Behav. Org. 2015, 117, 121–134. [Google Scholar] [CrossRef]

- Riedl, A.; Smeets, P. Why do investors hold socially responsible mutual funds? J. Financ. 2017, 72, 2505–2550. [Google Scholar] [CrossRef]

- Igbudu, N.; Garanti, Z.; Popoola, T. Enhancing Bank Loyalty through Sustainable Banking Practices: The Mediating Effect of Corporate Image. Sustainability 2018, 10, 4050. [Google Scholar] [CrossRef]

- Ballantine, J.; Kelly, M.; Larres, P. Banking for the common good: A Lonerganian perspective. Crit. Perspect. Account. 2018. [Google Scholar] [CrossRef]

- Mullineux, A. Banking for the public good. Int. Rev. Financ. Anal. 2014, 36, 87–94. [Google Scholar] [CrossRef]

- Chen, Z.; Hossen, M.M.; Muzafary, S.S.; Begum, M. Green banking for environmental sustainability-present status and future agenda: Experience from Bangladesh. Asian Econ. Financ. Rev. 2018, 8, 571. [Google Scholar]

- Lalon, R.M. Green banking: Going green. Int. J. Econ. Financ. Manag. Sci. 2015, 3, 34–42. [Google Scholar]

- Falcone, P.M.; Sica, E. Assessing the opportunities and challenges of green finance in Italy: An analysis of the biomass production sector. Sustainability 2019, 11, 517. [Google Scholar] [CrossRef]

- Muhamat, A.A.; Nizam bin Jaafar, M. The Development of Ethical Banking Concept Amongst the Malaysian Islamic banks. Norfaridah, The Development of Ethical Banking Concept Amongst the Malaysian Islamic Banks. In Proceedings of the iCAST 2010, Penang, Malaysia, 24–25 February 2010; pp. 24–25. [Google Scholar]

- Weber, O.; Remer, S. Social Banzks and the Future of Sustainable Finance; Routledge: London, UK, 2011. [Google Scholar]

- Dharwal, M.; Agarwal, A. Green banking: An innovative initiative for sustainable development. ACCMAN Inst. Manag. Artic. 2013, 2, 1–7. [Google Scholar]

- Kennan, H. Banks for Clean Energy. Working Paper, Energy Innovation; Policy and Technology, LLC: San Francisco, CA, USA, 2014. [Google Scholar]

- Mazzucato, M.; Semieniuk, G. Financing renewable energy: Who is financing what and why it matters. Technol. Forecast. Soc. Chang. 2018, 127, 8–22. [Google Scholar] [CrossRef]

- Ji, Q.; Zhang, D. How much does financial development contribute to renewable energy growth and upgrading of energy structure in China? Energy Policy 2019, 128, 114–124. [Google Scholar] [CrossRef]

- United State Department of Energy Report. Energy Investment Partnerships: How State and Local Governments Are Engaging Private Capital to Drive Clean Energy Investment; United State Department of Energy: Washington, DC, USA, 2017. [Google Scholar]

- Falcone, P.M. Green investment strategies and bank-firm relationship: A firm-level analysis. Econ. Bull. 2018, 38, 2225–2239. [Google Scholar]

- Liao, X. Public appeal, environmental regulation and green investment: Evidence from China. Energy Policy 2018, 119, 554–562. [Google Scholar] [CrossRef]

- D’Orazio, P.; Popoyan, L. Fostering green investments and tackling climate-related financial risks: Which role for macroprudential policies? Ecol. Econ. 2019, 160, 25–37. [Google Scholar] [CrossRef]

- Yuan, F.; Gallagher, K.P. Greening Development Lending in the Americas: Trends and Determinants. Ecol. Econ. 2018, 154, 189–200. [Google Scholar] [CrossRef]

- He, L.; Zhang, L.; Zhong, Z.; Wang, D.; Wang, F. Green credit, renewable energy investment and green economy development: Empirical analysis based on 150 listed companies of China. J. Clean. Prod. 2019, 208, 363–372. [Google Scholar] [CrossRef]

- Griffin, A. New York green bank: Introduction to standardization and collaboration. Econ. Financ. 2014. Available online: https://www.slideshare.net/reedhundt/gba-standardization-collaboration-31361631 (accessed on 4 April 2019).

- Browner, C.M.; Baussan, D.; Bovarnick, B.; Hernandez, M.; Kasper, M. Clean Energy Investment in the United States: The View to 2030; Center for American Progress: Washington, DC, USA, 2014. [Google Scholar]

- Pérez, M.E. SEBI index: Measuring the commitment to the principles of social banking. Contaduría y Administración 2017, 62, 1393–1407. [Google Scholar] [CrossRef]

- Chen, Y.S. The drivers of green brand equity: Green brand image, green satisfaction, and green trust. J. Bus. Eth. 2010, 93, 307–319. [Google Scholar] [CrossRef]

- Shrum, L.J.; McCarty, J.A.; Lowrey, T.M. Buyer characteristics of the green consumer and their implications for advertising strategy. J. Advert. 1995, 24, 71–82. [Google Scholar] [CrossRef]

- Cronin, J.J.; Brady, M.K.; Brand, R.R.; Hightower, R., Jr.; Shemwell, D.J. A cross-sectional test of the effect and conceptualization of service value. J. Serv. Mark. 1997, 11, 375–391. [Google Scholar] [CrossRef]

- Tam, J.L. Customer satisfaction, service quality and perceived value: An integrative model. J. Mark. Manag. 2004, 20, 897–917. [Google Scholar] [CrossRef]

- Hagmann, C.; Semeijn, J.; Vellenga, D.B. Exploring the green image of airlines: Passenger perceptions and airline choice. J. Air Transp. Manag. 2015, 43, 37–45. [Google Scholar] [CrossRef]

- McBoyle, G. Green tourism and Scottish distilleries. Tour. Manag. 1996, 17, 255–263. [Google Scholar] [CrossRef]

- Welsch, H.; Kühling, J. How green self image is related to subjective well-being: Pro-environmental values as a social norm. Ecol. Econ. 2018, 149, 105–119. [Google Scholar] [CrossRef]

- Binder, M.; Blankenberg, A.K. Green lifestyles and subjective well-being: More about self-image than actual behavior? J. Econ. Behav. Org. 2017, 137, 304–323. [Google Scholar] [CrossRef]

- Bansal, P. Evolving sustainably: A longitudinal study of corporate sustainable development. Strateg. Manag. J. 2005, 26, 197–218. [Google Scholar] [CrossRef]

- Mayer, R.; Ryley, T.; Gillingwater, D. Passenger perceptions of the green image associated with airlines. J. Transp. Geogr. 2012, 22, 179–186. [Google Scholar] [CrossRef]

- Delmas, M. Stakeholders and competitive advantage: The case of ISO 14001. Prod. Oper. Manag. 2001, 10, 343–358. [Google Scholar] [CrossRef]

- Nair, S.R.; Menon, C.G. An environmental marketing system–a proposed model based on Indian experience. Bus. Strategy Environ. 2008, 17, 467–479. [Google Scholar] [CrossRef]

- Abimbola, T.; Lim, M.; Hillestad, T.; Xie, C.; Haugland, S.A. Innovative corporate social responsibility: The founder’s role in creating a trustworthy corporate brand through “green innovation”. J. Prod. Brand Manag. 2010, 19, 440–451. [Google Scholar]

- Worcester, R.M. Managing the image of your bank: The glue that binds. Int. J. Bank Mark. 1997, 15, 146–152. [Google Scholar] [CrossRef]

- Sallam, M.A. An Investigation of Corporate Image Effect on WOM: The Role of Customer Satisfaction and Trust. Int. J. Bus. Adm. 2016, 7, 27–35. [Google Scholar] [CrossRef]

- Wang, J.; Wang, S.; Xue, H.; Wang, Y.; Li, J. Green image and consumers’ word-of-mouth intention in the green hotel industry: The moderating effect of Millennials. J. Clean. Prod. 2018, 181, 426–436. [Google Scholar] [CrossRef]

- Andreassen, T.W.; Lindestad, B. The effect of corporate image in the formation of customer loyalty. J. Serv. Res. 1998, 1, 82–92. [Google Scholar] [CrossRef]

- Nguyen, N.; Leblanc, G. Corporate image and corporate reputation in customers’ retention decisions in services. J. Retail. Consum. Serv. 2001, 8, 227–236. [Google Scholar] [CrossRef]

- Makanyeza, C.; Chikazhe, L. Mediators of the relationship between service quality and customer loyalty: Evidence from the banking sector in Zimbabwe. Int. J. Bank Mark. 2017, 35, 540–556. [Google Scholar] [CrossRef]

- Blomqvist, K. The many faces of trust. Scand. J. Manag. 1997, 13, 271–286. [Google Scholar] [CrossRef]

- Rousseau, D.M.; Sitkin, S.B.; Burt, R.S.; Camerer, C. Not so different after all: A cross-discipline view of trust. Acad. Manag. Rev. 1998, 23, 393–404. [Google Scholar] [CrossRef]

- Kee, H.W.; Knox, R.E. Conceptual and methodological considerations in the study of trust and suspicion. J. Confl. Resolut. 1970, 14, 357–366. [Google Scholar] [CrossRef]

- McKnight, D.H.; Choudhury, V.; Kacmar, C. The impact of initial consumer trust on intentions to transact with a web site: A trust building model. J. Strateg. Inf. Syst. 2002, 11, 297–323. [Google Scholar] [CrossRef]

- Zhou, T. The effect of initial trust on user adoption of mobile payment. Inf. Dev. 2011, 27, 290–300. [Google Scholar] [CrossRef]

- Martínez, P. Customer loyalty: Exploring its antecedents from a green marketing perspective. Int. J. Contemp. Hosp. Manag. 2015, 27, 896–917. [Google Scholar] [CrossRef]

- Gennaioli, N.; Shleifer, A.; Vishny, R. Money doctors. J. Financ. 2015, 70, 91–114. [Google Scholar] [CrossRef]

- Fungáčová, Z.; Hasan, I.; Weill, L. Trust in banks. J. Econ. Behav. Org. 2019, 157, 452–476. [Google Scholar] [CrossRef]

- Van Esterik-Plasmeijer, P.W.; van Raaij, W. F. Banking system trust, bank trust, and bank loyalty. Int. J. Bank Mark. 2017, 35, 97–111. [Google Scholar] [CrossRef]

- Ennew, C.; Sekhon, H. Measuring trust in financial services: The trust index. Consum. Policy Rev. 2007, 17, 62. [Google Scholar]

- Shao, Z.; Zhang, L.; Li, X.; Guo, Y. Antecedents of trust and continuance intention in mobile payment platforms: The moderating effect of gender. Electron. Commer. Res. Appl. 2019, 33, 100823. [Google Scholar] [CrossRef]

- Shim, S.; Serido, J.; Tang, C. After the global financial crash: Individual factors differentiating young adult consumers’ trust in banks and financial institutions. J. Retail. Consum. Serv. 2013, 20, 26–33. [Google Scholar] [CrossRef]

- Järvinen, R.A. Consumer trust in banking relationships in Europe. Int. J. Bank Mark. 2014, 32, 551–566. [Google Scholar] [CrossRef]

- Filipiak, U. Trusting financial institutions: Out of reach, out of trust? Q. Rev. Econ. Financ. 2016, 59, 200–214. [Google Scholar] [CrossRef][Green Version]

- Ganesan, S. Determinants of long-term orientation in buyer-seller relationships. J. Mark. 1994, 58, 1–9. [Google Scholar] [CrossRef]

- Grayson, K.; Ambler, T. The dark side of long-term relationships in marketing services. J. Mark. Res. 1999, 36, 132–141. [Google Scholar] [CrossRef]

- Moorman, C.; Zaltman, G.; Deshpande, R. Relationships between providers and users of market research: The dynamics of trust within and between organizations. J. Mark. Res. 1992, 29, 314–328. [Google Scholar] [CrossRef]

- Morgan, R.M.; Hunt, S.D. The commitment-trust theory of relationship marketing. J. Mark. 1994, 58, 20–38. [Google Scholar] [CrossRef]

- Flavián, C.; Guinalíu, M.; Gurrea, R. The role played by perceived usability, satisfaction and consumer trust on website loyalty. Inf. Manag. 2006, 43, 1–4. [Google Scholar]

- Walther, J.B. Selective self-presentation in computer-mediated communication: Hyperpersonal dimensions of technology, language, and cognition. Comput. Hum. Behav. 2007, 23, 2538–2557. [Google Scholar] [CrossRef]

- Brislin, R.W. Back-translation for cross-cultural research. J. Cross-cult. Psychol. 1970, 1, 185–216. [Google Scholar] [CrossRef]

- Cortina, J.M. What is coefficient alpha? An examination of theory and applications. J. Appl. Psychol. 1993, 78, 98–104. [Google Scholar] [CrossRef]

- Bagozzi, R.P.; Yi, Y. On the evaluation of structural equation models. J. Acad. Mark. Sci. 1988, 16, 74–94. [Google Scholar] [CrossRef]

- Hair, J.F.; Anderson, R.E.; Babin, B.J.; Black, W.C. Multivariate Data Analysis: A Global Perspective; Pearson: Upper Saddle River, NJ, USA, 2010; Volume 7. [Google Scholar]

- Nunnally, J.C. Psychometric Theory, 2nd ed.; McGraw-Hill: New York, NY, USA, 1978. [Google Scholar]

- Kissi, P.S.; Nat, M.; Armah, R.B. The effects of learning–family conflict, perceived control over time and task-fit technology factors on urban–rural high school students’ acceptance of video-based instruction in flipped learning approach. Educ. Technol. Res. Dev. 2018, 66, 1547–1569. [Google Scholar] [CrossRef]

- Segars, A.H. Assessing the unidimensionality of measurement: A paradigm and illustration within the context of information systems research. Omega 1997, 25, 107–121. [Google Scholar] [CrossRef]

- Yip, A.W.; Bocken, N.M. Sustainable business model archetypes for the banking industry. J. Clean. Prod. 2018, 174, 150–169. [Google Scholar] [CrossRef]

- Peters, R.G.; Covello, V.T.; McCallum, D.B. The determinants of trust and credibility in environmental risk communication: An empirical study. Risk Anal. 1997, 17, 43–54. [Google Scholar] [CrossRef]

- Masukujjaman, M.; Aktar, S. Green banking in Bangladesh: A commitment towards the global initiatives. J. Bus. Technol. 2013, 8, 17–40. [Google Scholar] [CrossRef]

- Sahoo, P.; Nayak, B.P. Green banking in India. Ind. Econ. J. 2007, 55, 82–98. [Google Scholar] [CrossRef]

- Kotler, P.; Armstrong, G. Principles of Marketing; Pearson Education: London, UK, 2010. [Google Scholar]

- Orel, F.D.; Kara, A. Supermarket self-checkout service quality, customer satisfaction, and loyalty: Empirical evidence from an emerging market. J. Retail. Consum. Serv. 2014, 21, 118–129. [Google Scholar] [CrossRef]

- Gupta, S. Bank Loyalty: Challenges, Trends and Opportunities. 2018. Available online: https://www.marketing-interactive.com/features/banking-loyalty-challenges-trends-and-opportunities (accessed on 15 May 2019).

- Khan, B.; Khan, M.; Shagufta, B.; Ahmad, I.; Ilyas, M. Comparison of Islamic and conventional banking practices regarding house finance in Pakistan: A case of hazara division. Acad. Res. Int. 2014, 5, 251. [Google Scholar]

- Fuentes, C. How green marketing works: Practices, materialities, and images. Scand. J. Manag. 2015, 31, 192–205. [Google Scholar] [CrossRef]

- Miroshnychenko, I.; Barontini, R.; Testa, F. Green practices and financial performance: A global outlook. J. Clean. Prod. 2017, 147, 340–351. [Google Scholar] [CrossRef]

- Merli, R.; Preziosi, M.; Acampora, A.; Lucchetti, M.C.; Ali, F. The impact of green practices in coastal tourism: An empirical investigation on an eco-labelled beach club. Int. J. Hosp. Manag. 2019, 77, 471–482. [Google Scholar] [CrossRef]

- Zaid, A.A.; Jaaron, A.A.; Bon, A.T. The impact of green human resource management and green supply chain management practices on sustainable performance: An empirical study. J. Clean. Prod. 2018, 204, 965–979. [Google Scholar] [CrossRef]

- Sellitto, M.A.; Hermann, F.F.; Blezs, A.E., Jr.; Barbosa-Póvoa, A.P. Describing and organizing green practices in the context of Green Supply Chain Management: Case studies. Resour. Conserv. Recycl. 2019, 145, 1–10. [Google Scholar] [CrossRef]

{kind=link}

| Frequency | Percent | |

|---|---|---|

| Gender | ||

| Male | 277 | 50.3 |

| Female | 274 | 49.7 |

| Age | ||

| Below 20 | 25 | 4.5 |

| 21–30 | 327 | 59.3 |

| 31–40 | 147 | 26.7 |

| 41–50 | 59 | 8.9 |

| Above 51 | 3 | 0.5 |

| Education qualification | ||

| PhD. | 44 | 8.0 |

| M.Sc. | 97 | 17.6 |

| B.Sc. | 223 | 40.5 |

| Others | 187 | 33.9 |

| Years of being a customer | ||

| Below 3 | 62 | 11.3 |

| 4–6 | 68 | 12.3 |

| 7–9 | 191 | 34.7 |

| 10–14 | 37 | 6.7 |

| 15 above | 193 | 35 |

| Construct | Measure | Factor Loading |

|---|---|---|

| Green banking | AVE = 0.738, CR = 0.847, α = 0.832 | |

| GB1 | 0.740 | |

| GB2 | 0.964 | |

| GB3 | ||

| GB4 | ||

| GB5 | ||

| Green image | AVE = 0.564, CR = 0.793, α = 0.783 | |

| GI1 | ||

| GI2 | 0.782 | |

| GI3 | 0.619 | |

| GI4 | 0.835 | |

| GI5 | ||

| Bank trust | AVE = 0.796, CR = 0.885, α = 0.815 | |

| BT1 | 0.782 | |

| BT2 | 0.990 | |

| BT3 | ||

| BT4 | ||

| BT5 | ||

| Bank loyalty | AVE = 0.692, CR = 0.871, α = 0.819 | |

| BL1 | ||

| BL2 | 0.814 | |

| BL3 | 0.855 | |

| BL4 | 0.826 |

| Fit Index | Research Model | Recommended Value |

|---|---|---|

| χ2/df | 3.690 | ˂0.04 |

| CFI | 0.970 | >0.800 |

| GFI | 0.963 | >0.800 |

| AGFI | 0.930 | >0.800 |

| RMSEA | 0.070 | ˂0.08 |

| SRMR | 0.04 | ˂0.05 |

| Construct | GB | GI | BT | BL |

|---|---|---|---|---|

| GB | 0.832 | |||

| GI | 0.136 | 0.751 | ||

| BT | −0.057 | 0.290 | 0.892 | |

| BL | 0.046 | 0.658 | 0.386 | 0.832 |

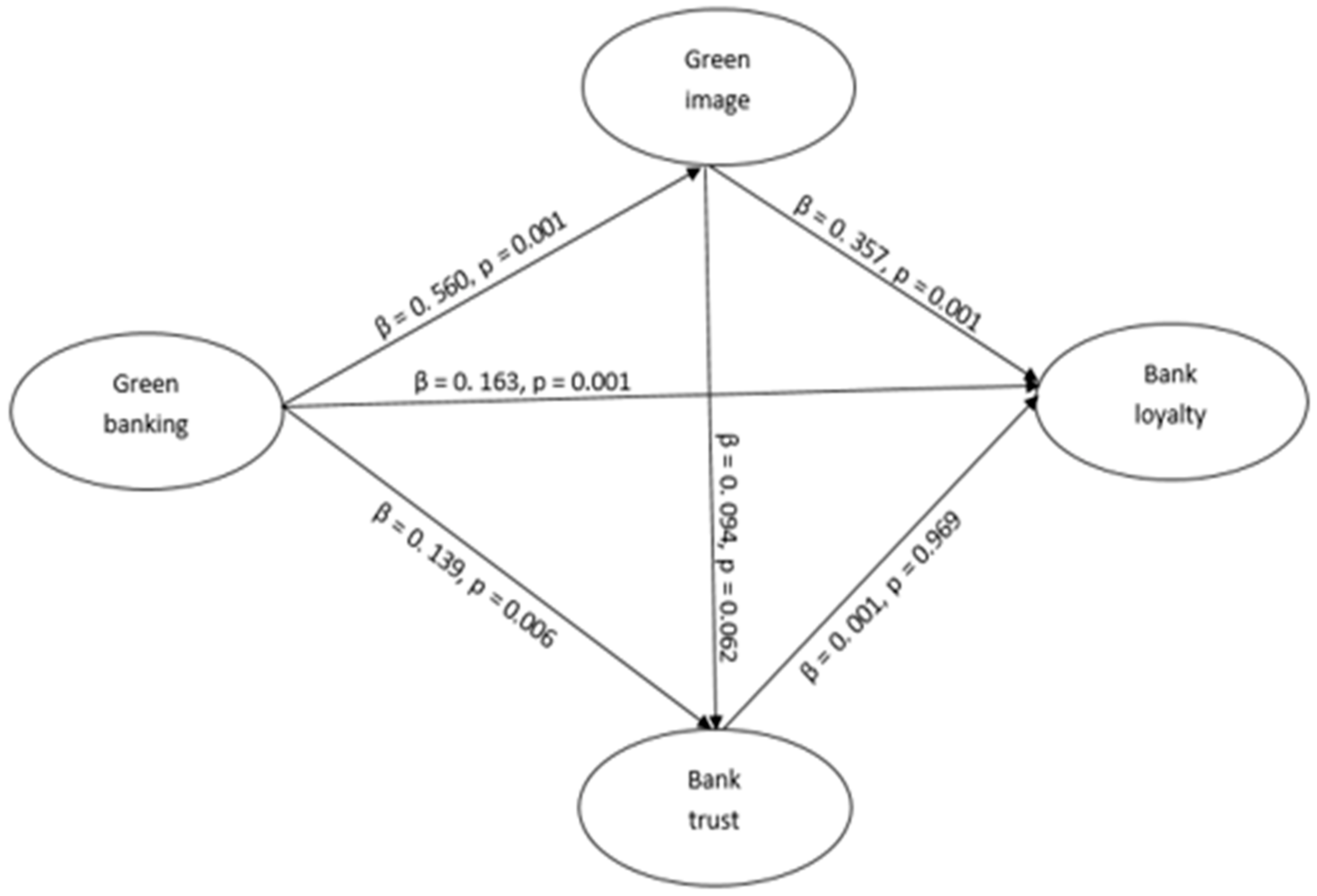

| Hypothesis | Path | Standardized Estimate | Decision |

|---|---|---|---|

| H1 | GB → GI | 0.560 *** | Supported |

| H2 | GB → BT | 0.139 *** | Supported |

| H3 | GB → BL | 0.163 *** | Supported |

| H4 | GI → BT | 0.094 *** | Supported |

| H5 | GI → BL | 0.375 *** | Supported |

| H6 | BT → BT | 0.001 | Not supported |

| Hypothesis | Path | Standardized Estimate | Decision |

|---|---|---|---|

| H7 | GB → GI → BL | 0.346 *** | Supported |

| H8 | GB → BT → BL | −0.001 | Not supported |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ibe-enwo, G.; Igbudu, N.; Garanti, Z.; Popoola, T. Assessing the Relevance of Green Banking Practice on Bank Loyalty: The Mediating Effect of Green Image and Bank Trust. Sustainability 2019, 11, 4651. https://doi.org/10.3390/su11174651

Ibe-enwo G, Igbudu N, Garanti Z, Popoola T. Assessing the Relevance of Green Banking Practice on Bank Loyalty: The Mediating Effect of Green Image and Bank Trust. Sustainability. 2019; 11(17):4651. https://doi.org/10.3390/su11174651

Chicago/Turabian StyleIbe-enwo, Grace, Nicholas Igbudu, Zanete Garanti, and Temitope Popoola. 2019. "Assessing the Relevance of Green Banking Practice on Bank Loyalty: The Mediating Effect of Green Image and Bank Trust" Sustainability 11, no. 17: 4651. https://doi.org/10.3390/su11174651

APA StyleIbe-enwo, G., Igbudu, N., Garanti, Z., & Popoola, T. (2019). Assessing the Relevance of Green Banking Practice on Bank Loyalty: The Mediating Effect of Green Image and Bank Trust. Sustainability, 11(17), 4651. https://doi.org/10.3390/su11174651