1. Introduction

Typically, the economic literature highlights the effects of free capital mobility and the sensitivity of capital flows to any changes in the structural and fiscal factors that national governments undertake (see, for example [

1,

2], including in terms of politics (see [

3]) and sustainable community development [

4]. Thus, in their efforts to compete with other countries—in particular to gain competitiveness through costs, governments should take part in a “race-to-the-bottom” battle that could lead to both a decline of taxation rates and/or a reduction of the tax base in order to attract foreign companies and to ease fiscal pressure.

Therefore, as the level of government revenue collected by tax authorities decreases, levels of both government spending in general and social spending, in particular, diminish [

5]. In addition, some scholars conclude that in developing countries pressure is exerted on labor standards as multinationals invest in countries with lower regulatory standards [

6,

7,

8].

In this paper we aim to highlight:

- (1)

the challenges that may arise to the harmonious and inclusive economic development of EU member states from Central and Eastern Europe in the larger context of the European Common Market and the free movement of capital; and

- (2)

some explanatory inconsistencies in the relationship between social (in)equality, freedom of capital mobility and favoring of the attraction of foreign direct investment (FDI), especially if the latter obtains a large share of the value added or a nodal position in a country.

This inconsistency has been presented in the form of the “social trilemma” concept to describe some European Union member states—especially the New Member States from Central and Eastern Europe (CEE), which have a lower level of economic development compared to Western Europe and are more dependent on foreign capital—given their need to implement policies that contribute to sustainable, harmonious and socially inclusive economic growth.

The main contribution of the paper at the general debate regarding development is that there exists a trilemma for countries in terms of economic policy, based on the fact that a country cannot simultaneously possess social equity, free capital movement and a high share of FDI. This is relevant for developing/emergent countries, where the role of FDI companies is relatively important and cost competitiveness weighs significantly on economic attractiveness. Moreover, we consider that the current economic model followed by CEE countries is characterized by the social trilemma, with consequences in terms of social development.

We divided the study into four parts. The first part of the study presents the theoretical framework of structural dependence on international capital and race-to-the-bottom competition. Here we performed a critical analysis of the scientific literature, highlighting the consequences of free movement of capital in relation to economic development, social performance and government policies. The second part of the study comprises the theoretical framework of the social trilemma, starting from the two concepts mentioned above. In addition, in this section we briefly present the indicators and databases used to build the empirical evidence of the so-called social trilemma.

In the third part of the article we provide the empirical evidence that supports the social trilemma, analyzing some aspects, such as the evolution of corporate income tax rates, the share of remuneration of employees in gross domestic product (GDP), gross operating surplus and salaries as shares of value added at factor costs, trade unions’ density evolution, and the share of foreign companies in total value added in several economic sectors. The last part of the article comprises conclusions and further research directions for this topic.

2. Theoretical Framework of Structural Dependence and Race-to-the-Bottom Competition

Different authors (see [

9]) asserts that, very often, partial or total opening of the capital account and the free mobility of capital were processes associated with the so-called Washington Consensus, which was built around liberalization processes, privatization and macro-stabilization. Its scope was to reconnect post-communist Europe to the market economy and, ultimately, to global markets [

10]. On the other hand, the author concludes that countries with a low level of local financial development may be negatively affected when they want to provide greater capital account openness.

In general, the forces of globalization, the liberalization of capital accounts, and the reduction of transaction costs, have drawn states into a competition for lower taxation/tax rates to which companies are subject (e.g., corporate income tax or turnover tax), a race rooted in the literature under the concept of a “race to the bottom”. These factors may, theoretically, lead to a reduction in government revenue and government spending, with additional pressures to restrict social protection benefits and the redistributive function of governments.

Addressing the issue to the European Union, there are some researchers considering that the EU may turn to a “generalized reconstruction” of the social model in the context of increasing capital mobility in the post-launch period of the European single currency in order to lower the level of social protection and labor market regulation [

11]. This occurs as multinational companies are gradually implementing aggressive “social dumping” strategies to diminish the bargaining power of employees, especially if governments face a prolonged recession and rising unemployment, factors that can also reduce the bargaining power of trade unions in the labor market. The pressures on governments will be more powerful in the context of the emerging wave of the Fourth Industrial Revolution, digitalization and the large-scale use of automatization in the manufacturing sector, even in CEE countries [

12], leading to several challenges for the labor market.

Addressing the issue of social fairness and the race-to-the-bottom competition in emerging economies, Nita Rudra considers that relatively higher growth rates in these countries compared to developed countries is not necessarily synonymous with increasing social fairness, which can lead to an intensification of the tensions between winning groups and those who lose from globalization and market liberalization (see [

13]). Citing the works previously published by [

14,

15], the author states that the logic of the race to the bottom implies that taxes on capital incomes will gradually decrease and governments will rely more and more on categories of taxes on labor and consumption.

In addition, the race in which states are engaged will affect the middle class more than the underlying social pyramid classes, because the classical welfare models in emerging economies were not originally designed to take care of low-income classes, but were designed to take care of the middle class [

14]. In addition, from a social perspective, the author asserts that the deepening of income inequalities and rising relative poverty are developments closely related to the phenomenon of globalization, because a national economy that wants to become internationally competitive will find itself in a position in which it is not easy to implement redistributive policies to improve the living conditions of low-income classes.

“Financial globalization triggers a race-to-the-bottom tax competition” and, consequently, the erosion in the tax base shrinks the fiscal finances [

16]. According to [

16], “the tax burden shifts from the highly mobile factors (e.g., capital and top-skilled labor) to the weakly mobile factors (e.g., low-skilled labor)”. Thus, a country that imposes high tax rates may determine a migration of mobile factors (e.g., capital outflows), eroding its own tax base and lowering domestic economic activity at the same time.

3. The Thesis of Structural Dependence

Both globalization and the integration process of the emerging countries of CEE in the European Union foster the interconnection of economies and involve the opening of domestic capital markets (alongside labor, goods and services) to foreign entities in search of profitable investment opportunities, about which decisions are typically adopted exclusively based on return on investment criteria.

The defining elements of this process are represented by the liberalization and/or deregulation policies of all types of markets (capital, labor, goods and services) and, in particular, the complete liberalization of the capital account.

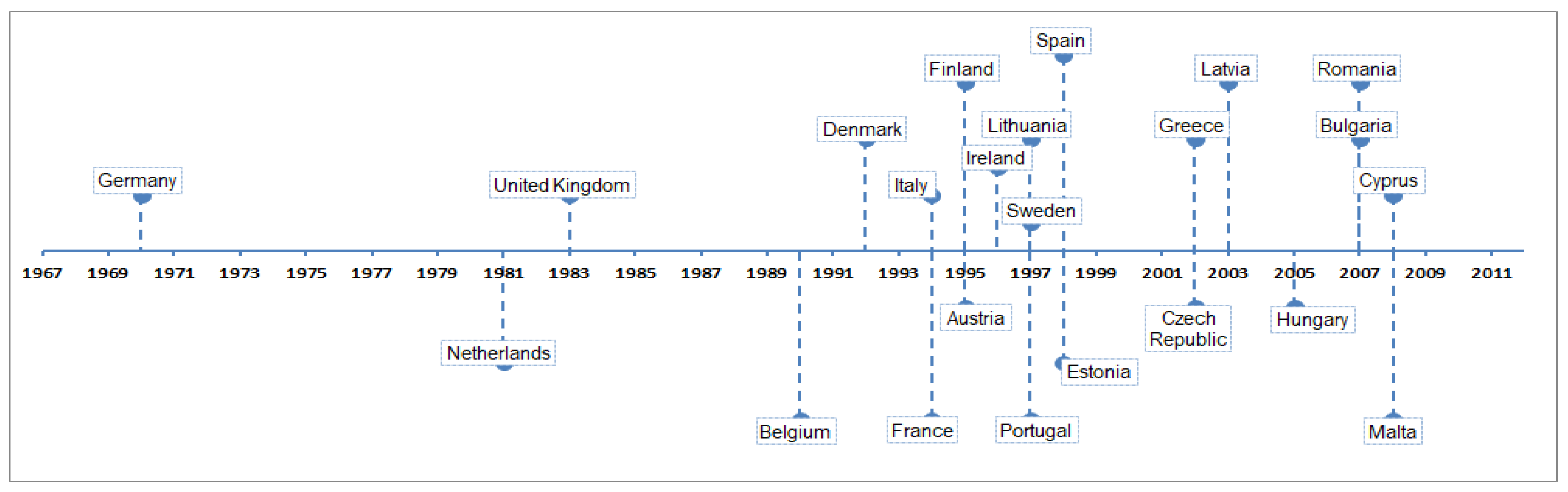

As the figure below shows, there have been several periods during which the capital account was completely liberalized in Europe, beginning with Germany in 1970, followed by the Netherlands in 1981 and the United Kingdom in 1983. The last wave of complete capital account liberalization in the EU occurred in 2007–2008 in Romania, Bulgaria, Malta and Cyprus (see

Figure 1).

At the same time, due to the strong impact generated by the free mobility of foreign capital, some dependence of governmental decisions on capital preferences may also arise, this theory being known as the “thesis of structural dependence”.

The thesis of structural dependence is based on the assumption that the whole society depends on the allocation of resources, a function which is mostly carried out by the capital owners [

17]. The authors also believe that investment decisions by the private sector can determine future production opportunities, employment rates and consumer opportunities that characterize a society.

Thus, when pursuing their “material interests” (e.g., asking for higher wages), all social groups involved (e.g., employees) will have to take into account the effects their actions will have on the future investment decisions of capital owners, decisions that depend in a decisive way on the profitability of the investments [

17].

In a society organized on capitalist principles, the authors assert, there will always be a trade-off between the present and future consumption of all, which initially passes through a trade-off between the consumption of those who own capital and profits (the shareholders of the companies). If we look at this dependence from the perspective of a single group—the labor force—it can be concluded that salaries and profits will always be correlated as a faithful reflection of the compromise between the consumption of employees and the consumption of the shareholders.

Another idea underlined by [

17] is that national governments, even if they want to intervene to improve employee conditions and social fairness, will have to always keep in mind the dynamics of future private investment; if private firms are responding to potential government constraints on wage growth by reducing investment, then wages and future employment will also be affected, and workers’ current wage demands should be more modest. Governments will thus have to avoid policies that dramatically modify the distribution of income and wealth.

According to them, the state’s de facto structural dependence on capital owners means that no government can simultaneously reduce profits and increase investment. Because firms always get to invest according to what they anticipate in the future, government policies that transfer income from equity owners to other social groups will reduce the return on investment and hence the future volume of investment.

Based on these assumptions, the central thesis of structural dependence is that governments will always have to make a trade-off between redistribution (social fairness) and growth stimulation (private investment), which will considerably limit the space to maneuver for policies built to improve economic equality.

As Matthew Watson et al. [

18] points out, with regard to the thesis of structural dependence presented in the terms of the two above-mentioned authors, the state is capital-dependent because the owners of the capital make decisions related to employment, inflation and the income of voters. Thus, politicians—who want to be re-elected—are capital-dependent because their voters are, and this will automatically lead to government measures that provide favorable conditions for investment and capital accumulation [

19]. In addition, at a time when capital mobility is significant, Matthew Watson et al. [

18] argues, political parties that promote economic intervention and state strengthening will be “under considerable constraints”.

At the same time, Matthew Watson et al. [

18] states that capital owners will tend to associate the choice of a socially-oriented administration with a higher taxation level, which, in a globally integrated economy that enjoys perfect capital mobility, is likely to manifest itself as a rapid and destabilizing exodus of capital under a social-democratic government.

Therefore, policy-makers need to adapt their policies to capital-owners’ interests and accept their demands for a lower tax on profit/turnover, labor market flexibility (through deregulation of labor relations), and restriction of social protection systems or austerity, otherwise they may experience periods of disinvestment, currency speculation/depreciation or an economic crisis.

From the perspective of taxation, other studies (see, for example, [

20]) analyze the development of taxes on corporate income in EU and G7 countries over the 1980s and the 1990s. They conclude that tax revenues on profitable investments had fallen. In particular, taxes on income earned by multinational firms are subject to tax competition forces. Tim Besley et al. and Sebastian Krautheim et al. [

21,

22] provided supplementary empirical support and additional evidence related to international tax competition for relatively mobile investments, so that a country with more mobility has lower capital tax rates.

4. Materials and Methods

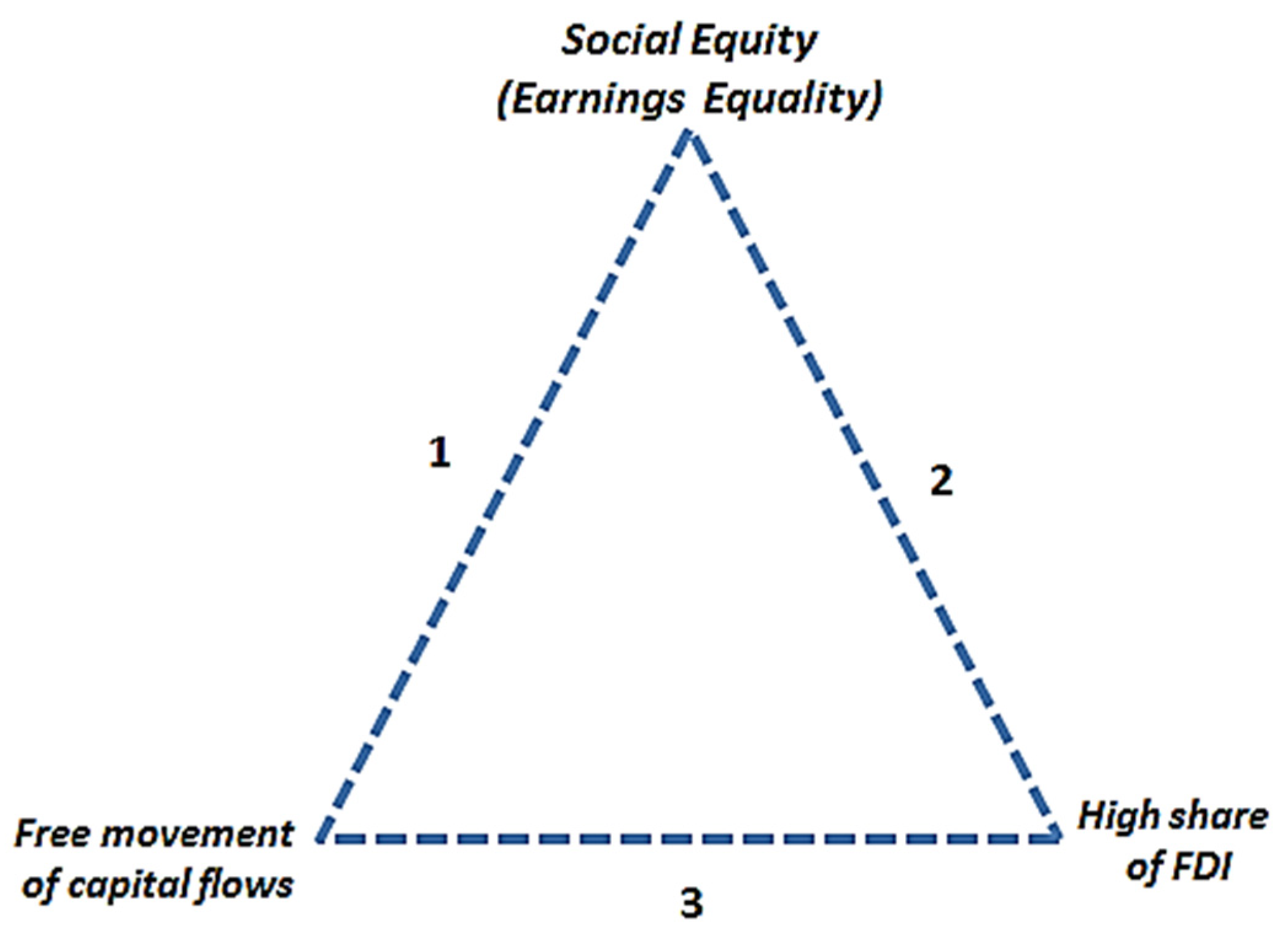

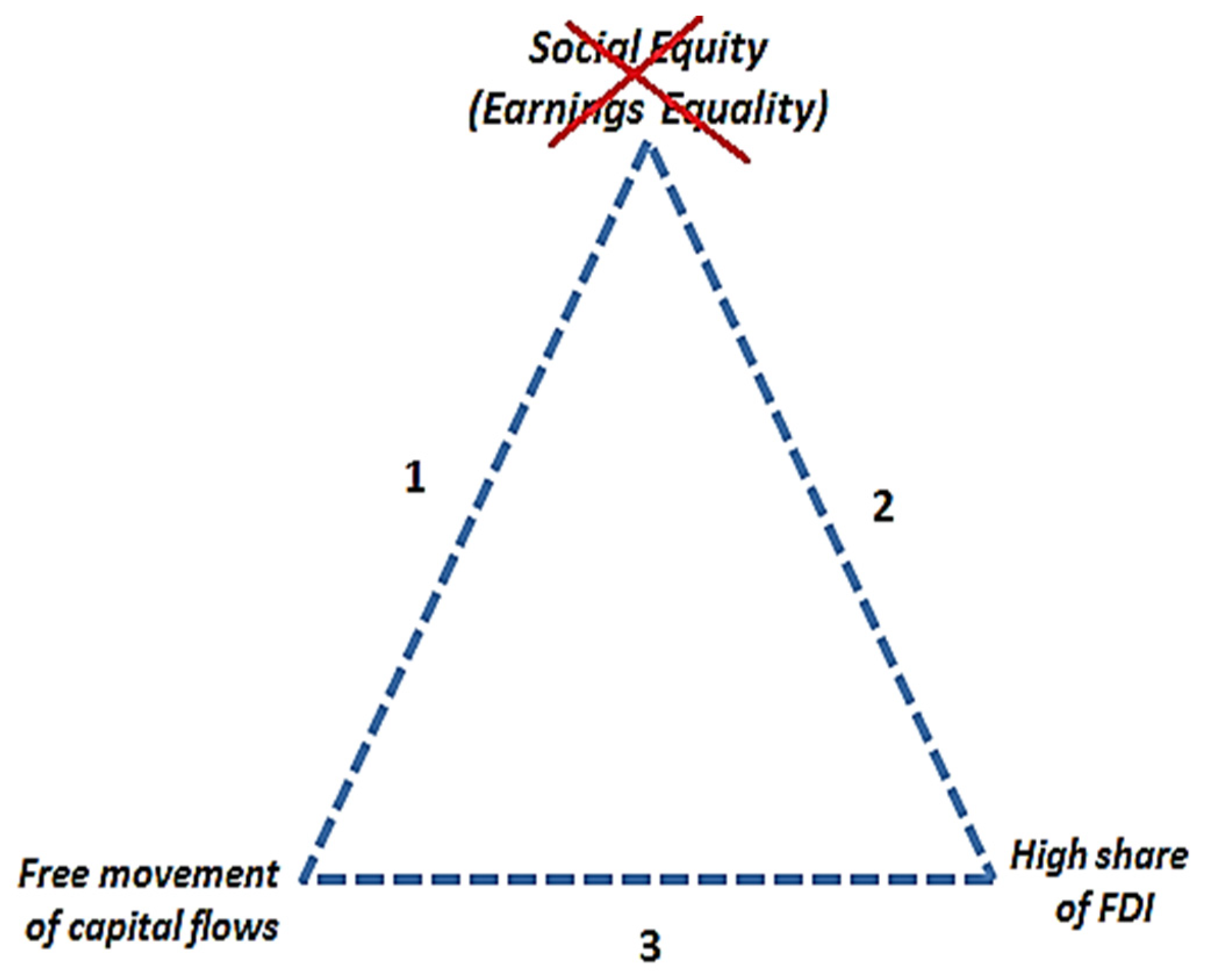

The social trilemma that we discuss in this paper essentially refers to the structural, social and fiscal-budgetary consequences of the free movement of capital and, respectively, to the fiscal efforts to improve economic competitiveness, and their impact on social fairness.

Thus, we argue that national governments, in order to improve the living conditions of individuals (i.e., to increase labor protection, and to reduce income inequality and/or the poverty rate) in an economic context dominated by perfect capital mobility and a large share of foreign investment companies, find themselves in a trilemma while considering that the three objectives cannot be achievable at the same time (see

Figure 2). Further, we present our theory explaining the links between every pillar of the trilemma.

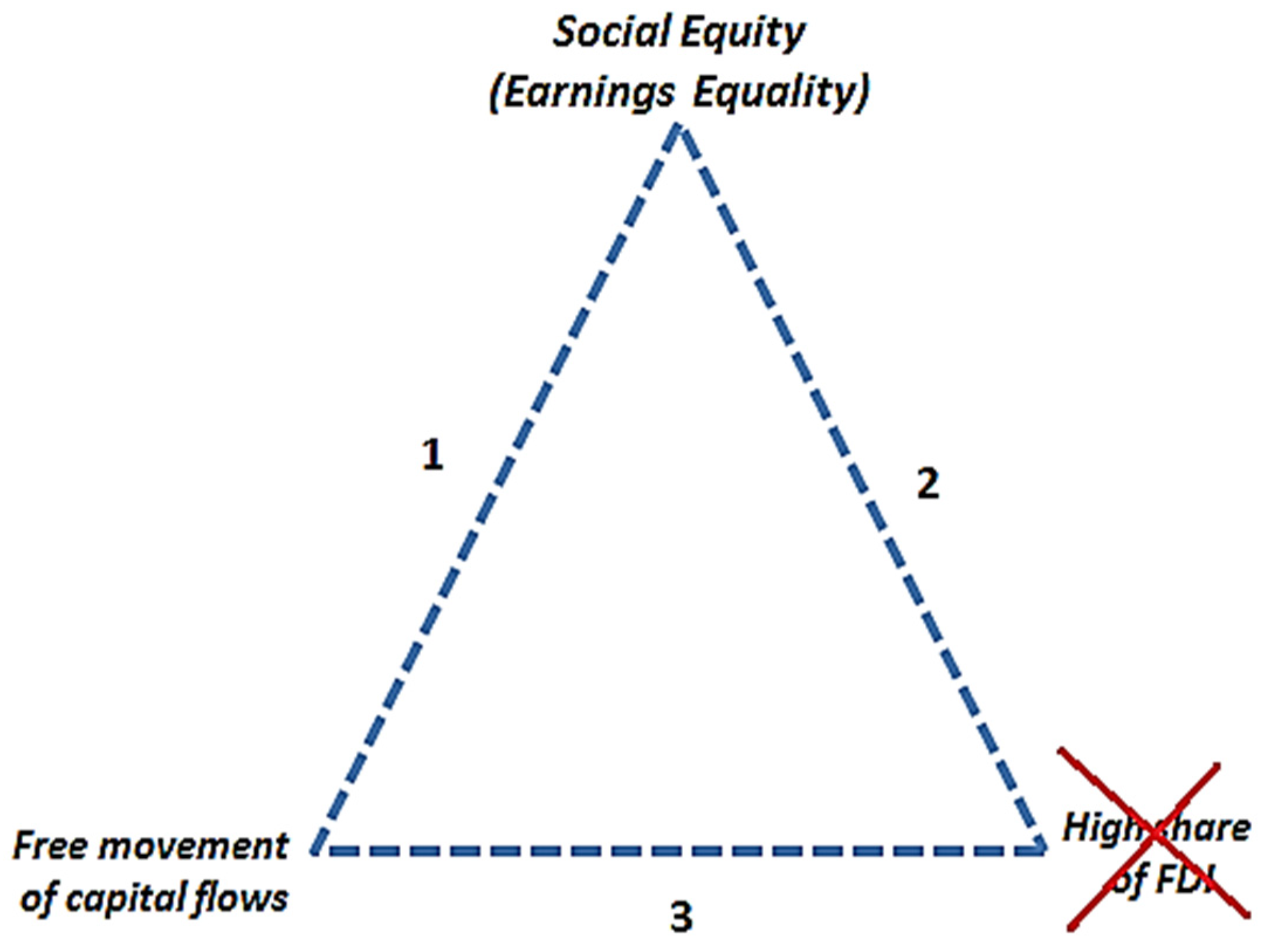

- (1)

As can be seen in

Figure 2, we have positioned social equity at the top of the triangle, being the central stake of the European model of economy. This represents a “footprint” of the European model of the economy in the global landscape—aiming to reduce the development gaps between European Union countries and regions. However, this objective can be achieved in the context of the free movement of capital, but not when there is a high share of FDI companies (see

Figure 3).

Any attempt to improve individuals’ living conditions by increasing government intervention will lead to capital migration due to diminishing private capital returns. If the economy is not strongly integrated into global/European value chains and if there are still strong domestic companies at the national level, this is not a socially significant development.

However, if the share of foreign companies is high in the economy, including in terms of contribution to national external trade, the impact of an increase in taxation and/or tightening regulation to support employees will also lead to an outflow of foreign companies, thus influencing the level of employment and wages for a large part of the economy (see

Figure 4).

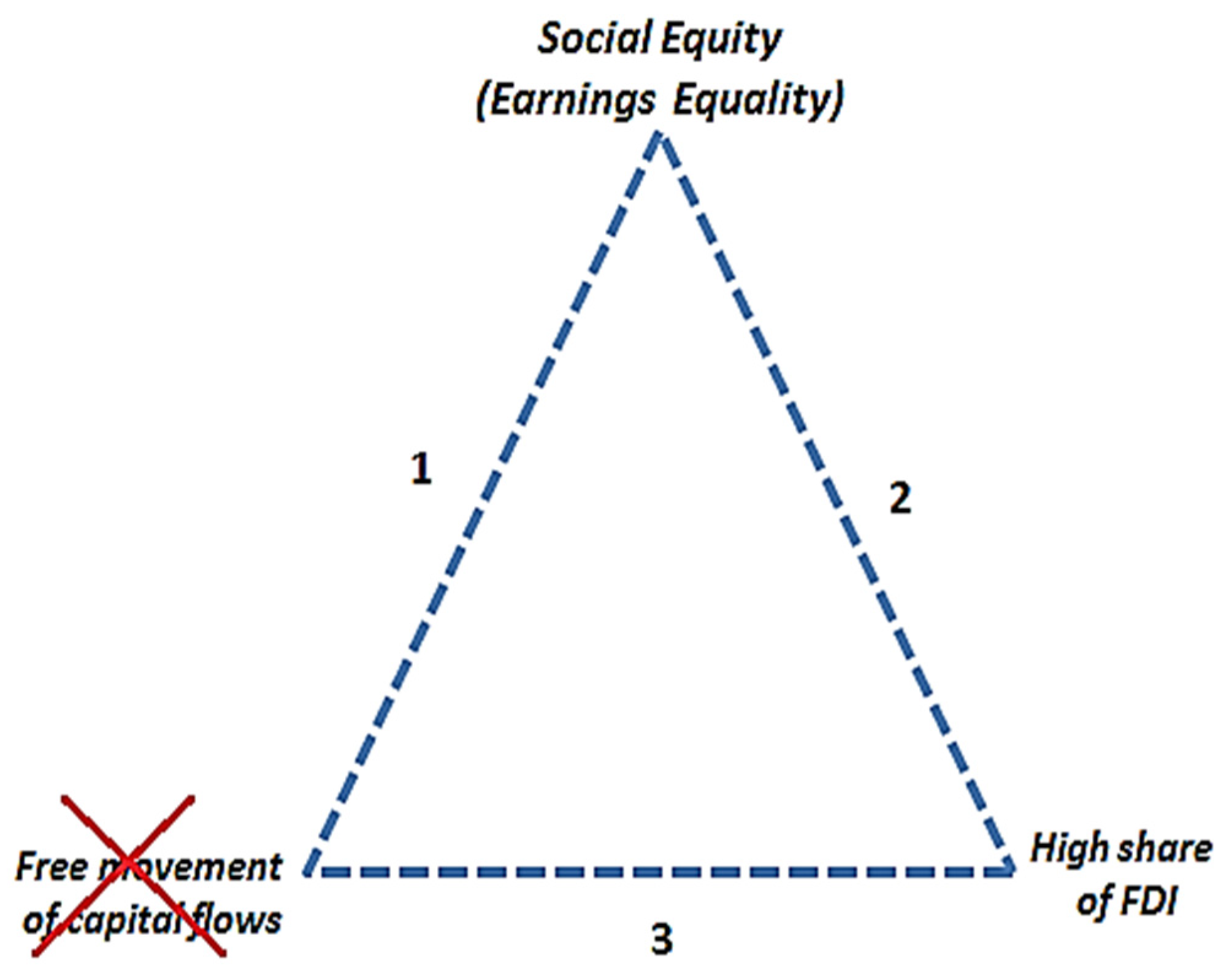

- (2)

On the one hand, increasingly stronger integration of European economies implies an increasing flow of pan-European greenfield FDI or mergers and acquisitions, which, in many New Member States, has led to a consolidation of a high share of foreign companies in most sectors of the economy (in terms of value added created). On the other hand, the existence of a significant (majority) share of companies in the economy as a whole or in important activity sectors, created as a result of FDI, will restrict the maneuvering space of governmental authorities to increase social equity.

Firstly, as we noted above, any fiscal and budgetary measures (in terms of redistribution/market intervention) to improve living conditions will lead to a loss of external competitiveness and to a migration of FDI (delocalization) and capital outflows. Secondly, such measures can still be achieved—albeit, most likely only in the short term—if there is control over the flow of capital entering and leaving an economy. However, even in this case of partial or total control of capital movements by national authorities (government, central bank), the impact of possible interventions will be quite small, especially if the “bridge links” created between FDI companies and local providers are limited in number and size.

- (3)

In a context where the national government wants to improve the social conditions of individuals by increasing government spending (which in the short term can be financed by increasing public deficits, and will eventually lead to some tax increases) and/or by changing the structure of redistribution systems by, for example, introducing a progressive tax, ceteris paribus, the economy will have to cope with a capital outflow (due to a loss of cost competitiveness), a depreciation of the national currency, and inevitably a decrease in the stock of FDI that is attracted.

In addition, if capital flows are perfectly mobile and the objective is to increase the stock of FDI that is attracted, the government should improve external competitiveness through reduction of corporate income or labor taxes. The reduction of labor taxes will have significant consequences, especially in labor-intensive economies and/or in countries with lower productivity, where national governments impose lower taxation rates to compensate.

As a result of these constraints, which will reduce fiscal revenues, the adoption of such policies will undermine social equity and the state’s capacity to implement social policies to improve the living conditions of those with lower incomes, either through passive policy measures (various forms of social benefits, such as housing heating aid and unemployment benefits), or regulatory measures, such as introducing or raising minimum wages (see

Figure 5).

In the next section of the paper we present the empirical evidence of the above-mentioned trilemma based on different indicators from Central and Eastern Europe countries, such as: corporate taxation rates, the share of remuneration of employees in GDP, gross operating surplus and salaries as share of value added at factor costs, inequality and trade union evolution, and the share of foreign companies in total value added in several economic sectors.

Our analysis chiefly uses descriptive statistics in order to examine some relationships between variables relevant to our topic. The main data sources were Eurostat, the Organization for Economic Co-operation and Development, the World Bank and the International Labor Organization, accessed in May–June 2019. Concerning the limitations of this research, due to restrictions of the available data, the methodology was supported by descriptive statistics. It is recommended that additional information is gathered to allow the application of more advanced statistical methods to achieve more detailed results and research conclusions.

5. Results: Empirical Evidence of the Social Trilemma in CEE Countries

More than other European Union member states, Central and Eastern European countries (Bulgaria, Croatia, Czech Republic, Lithuania, Latvia, Estonia, Hungary, Poland, Romania, Slovakia, Slovenia) make efforts in terms of cost and non-cost competitiveness in order to attract foreign capital inflows and to increase the pace of convergence towards developed states.

The important role of foreign companies can be seen in the share of value added they generate in CEE countries compared with developed countries, such as Germany, France, Italy, Austria or Spain, where the share of foreign companies is lower. According to Eurostat, the share of foreign companies (of the total number of companies) in CEE countries is between 0.8%, in Slovakia, and 24.5%, in Estonia (

Table 1).

However, despite the relatively small share of foreign companies in the total number of companies (except Estonia), their importance to national economies is strong. For example, in Slovakia, the 0.8% of companies that are foreign contribute more than 48% of value added at factor cost, while in Hungary around 3% of companies are foreign and create more than 51% of value added.

In addition, it appears that in Poland and Estonia domestic companies are more important for the economy: although these countries have a higher share of foreign companies, their contribution is smaller compared with Romania, Bulgaria, Hungary, Latvia, Lithuania and Czech Republic.

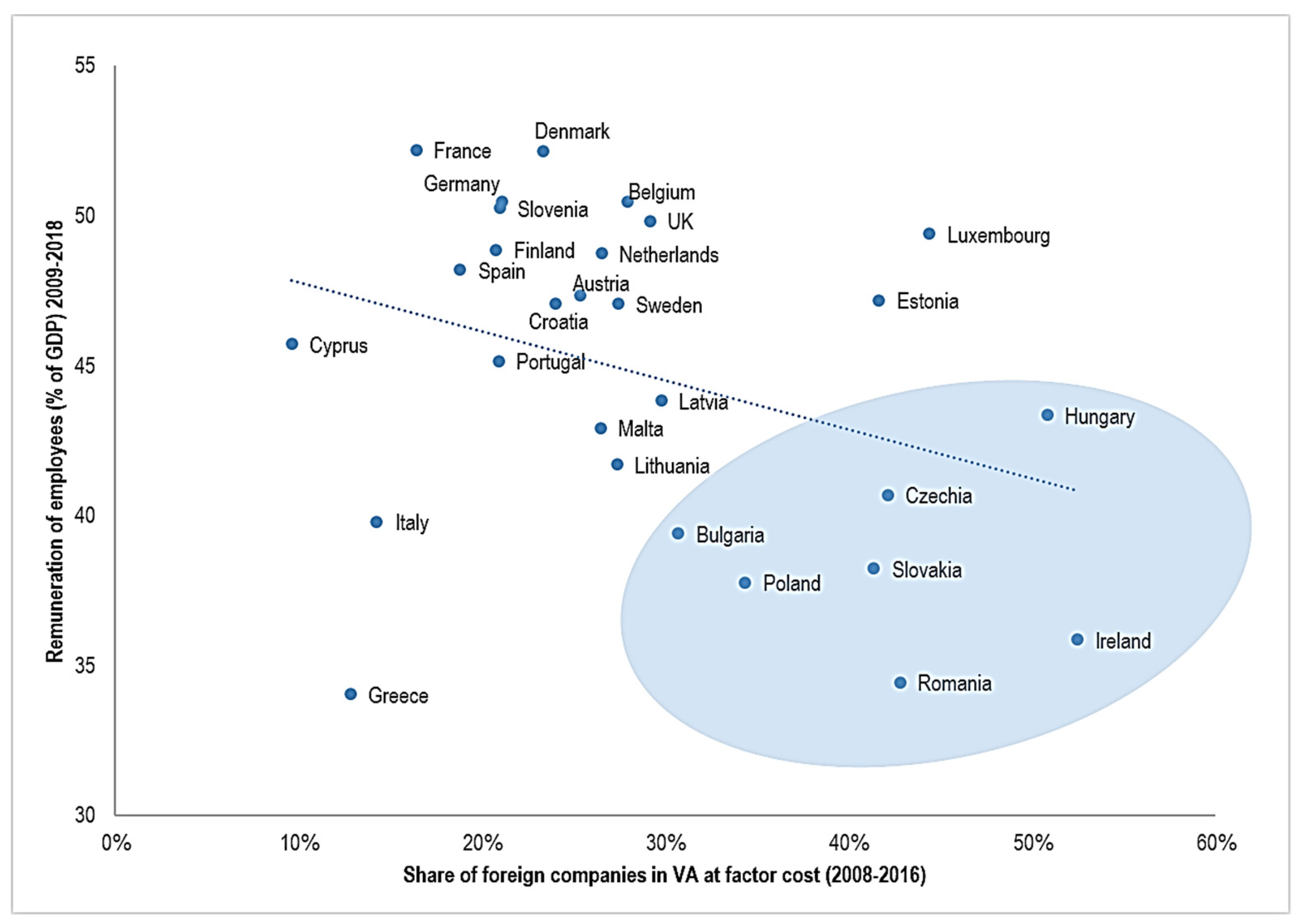

Furthermore, we see that there is a reverse relationship between the importance of foreign companies and the share of remuneration of employees in total GDP.

Figure 6 shows that in CEE countries, in general, the share of foreign companies, even if small in terms of the total number of companies, has an essential role in terms of value added. The relationship between, on the one hand, the lower cost of labor and the lower unionization rate, and on the other hand, the (small) share of the remuneration of employees, suggests that the former variables explain the results of the latter. For example, in this period, the shares of remuneration of employees in Romania and Ireland were the lowest in EU, around 35% of GDP. Close to Romania are Poland, Slovakia, Bulgaria and Czech Republic. In Greece, notably, GDP decreased by approximatively 25% after the financial crisis, capital outflows and austerity measures, while the contribution of foreign companies to value added was relatively low, below 15%.

Finally, we observe that the most developed countries, such as France, Germany, Denmark, Finland and UK, have both a higher share of remuneration of employees in GDP and a smaller proportion of value added generated by foreign capital companies. The only CEE countries that approach developed countries are Slovenia and Croatia, due to a stronger value chain integration, especially with Germany [

23].

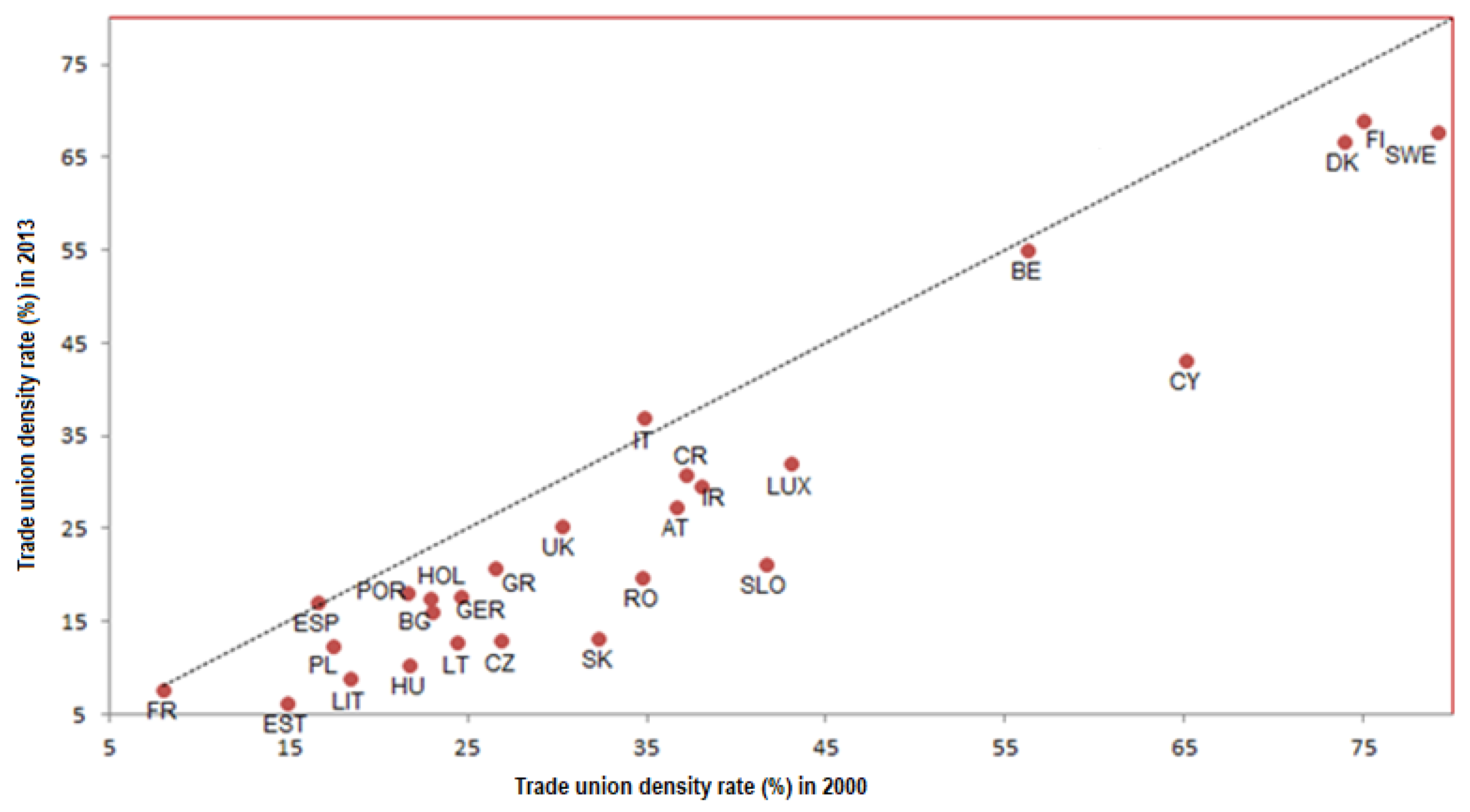

Moreover, it seems that competition between countries was translated into reduction of the degree of unionization and coverage of collective bargaining, especially after the 2000s, which became more pronounced after the financial crisis from 2008 [

24].

Figure 7 and

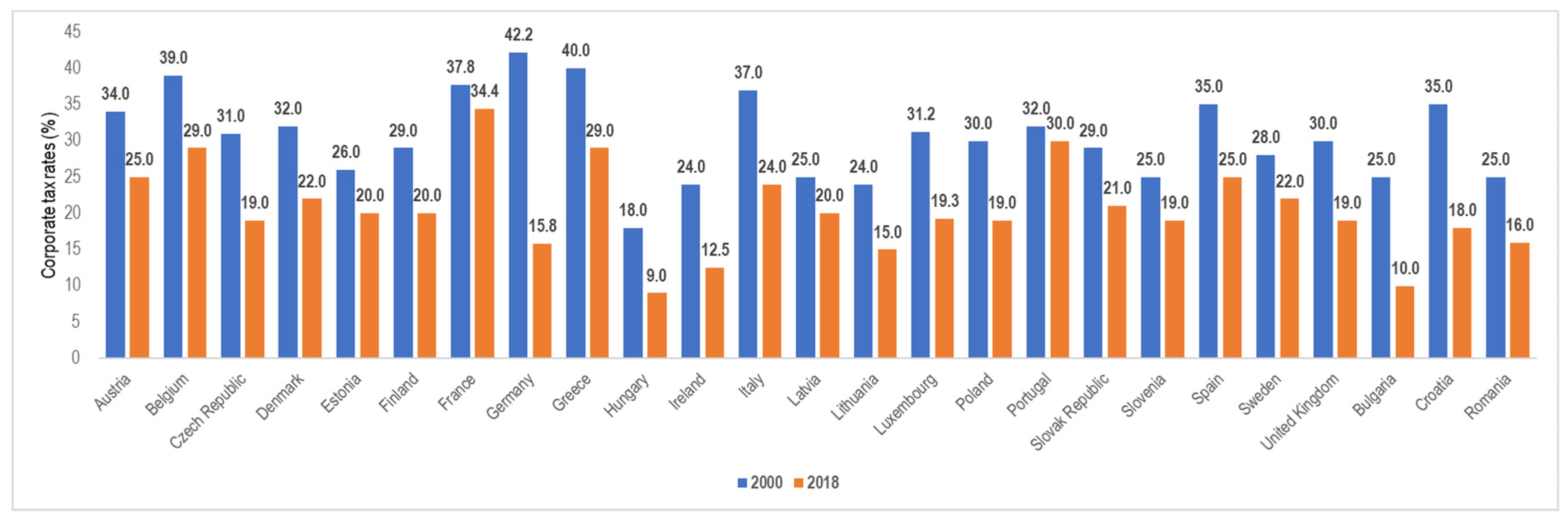

Figure 8 show that in most European countries, trade union density decreased between 2000 and 2013, except in Italy, Belgium, France and Spain, while the most significant reduction was in CEE countries. In turn, as the mobility of capital flows increased, the corporate income tax (CIT) decreased during the last 19 years due to states’ efforts to attract capital. Among the CEE analyzed countries, the most important CIT rate reductions between 2000 and 2018 were in Croatia (−17 percentage points.), Bulgaria (−15 percentage points), Czech Republic(−12 percentage points) and Romania, Lithuania and Hungary (−9 percentage points). This is consistent with the results of other studies, as noted in

Section 2 regarding the race-to-the-bottom theoretical framework, such as [

20], who analyzed the evolution of CITs during the 1980s and 1990s.

From our perspective, the evolution of CIT rates and the decrease of the density union rate during recent decades are a significant reflection of the preference of governments to internalize capital preferences. In addition, the favorable treatment of capital owners attracts foreign companies, linked especially with low labor costs (reflected also in the share of value added retained by employees).

Moreover, it is known that a large part of the competitiveness of a country is derived not only by lowering taxes, but also by raising productivity. As it is very difficult to increase physical productivity in the short term (especially among Small and Medium Enterprises), Central and Eastern European countries, which have a significant productivity gap compared with the EU average [

12], are forced to adopt race-to-the-bottom competition policies to increase their attractiveness until the gap gradually closes. At the end of 2016, the value added generated by an employee of a private enterprise (excluding financial and insurance activities) in the CEEgroup registered productivity of EUR 22,500 per employee, representing around 50% of the EU average.

Thus, another important fact in explaining the social trilemma is the presence of foreign companies in relation to lower labor costs, smaller density of trade unions and the share of value added retained in the form of gross operating surplus. As noted in

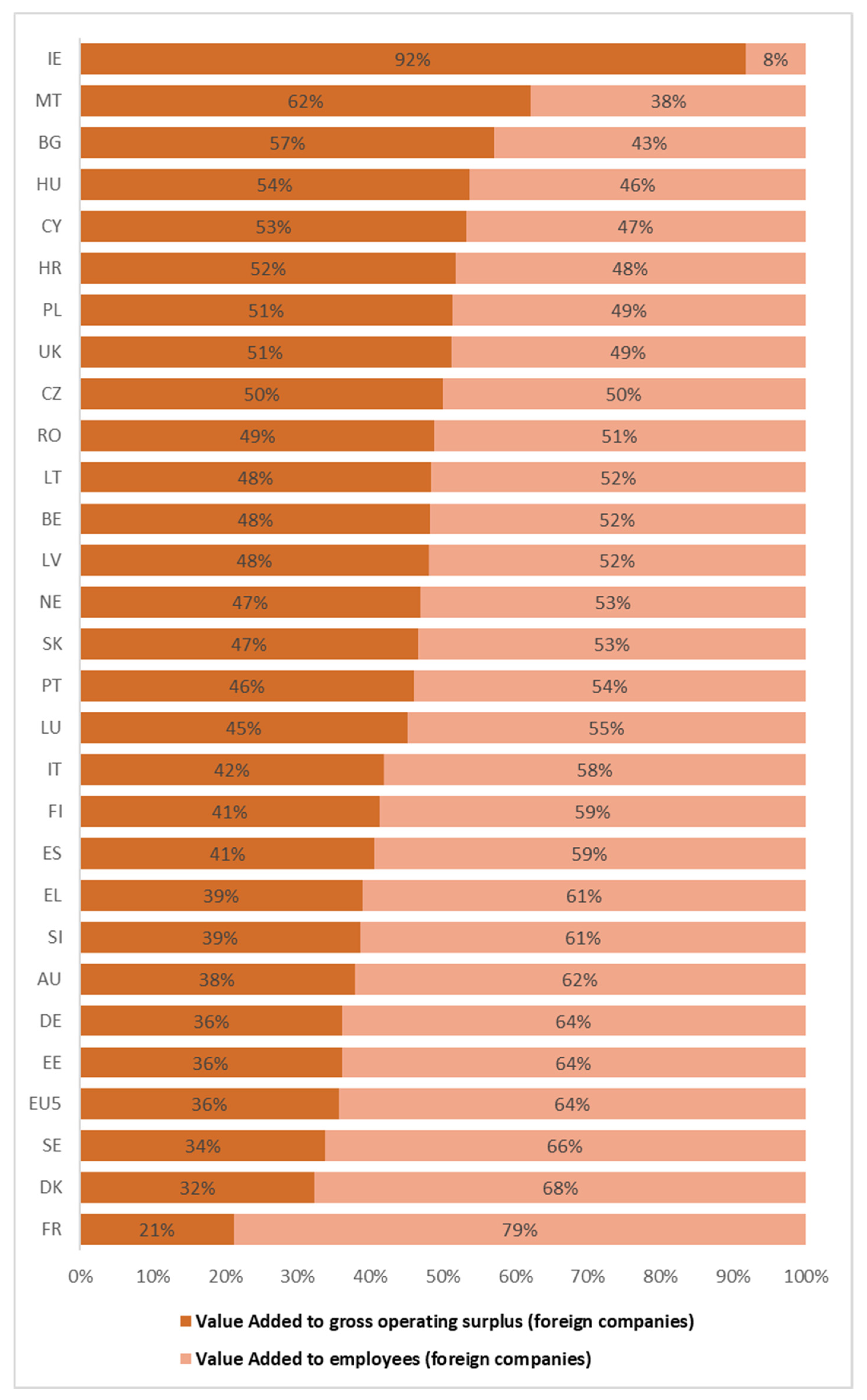

Section 3, there is always a trade-off between the benefits of workers (salaries) and benefits of capital owner (profits). Using data from Eurostat we highlight in

Figure 9 the trade-off using the distribution of value added at factor cost between gross operating surplus and remuneration of employees in foreign companies.

In the European Union, the share of gross operating surplus in value added at factor cost generated by foreign companies from the non-financial sector is between 21% in France and 92% in Ireland. In the most developed countries, such as Germany, United Kingdom, France, Austria and Denmark, the average of gross operating surplus in value added is around 36%, while remuneration of employees represents 64%.

Among CEE countries, only Estonia and Slovenia (the latter with 38.6%), are close to the average. For the other nine CEE countries, the average is above 50% (close to UK), varying from 46.6% in Slovakia to 57.1% in Bulgaria.

In addition, in

Table 2 we emphasize the same distribution among domestic companies from CEE and other countries from the EU. According to our analysis, the situation is more balanced among domestic capital companies. For the entire EU sample, the distribution between gross operating surplus and remuneration of employees is 43%/57% in foreign capital companies, and 46%/54% for domestic capital companies. Moreover, in nine of 28 states, the distribution of value added between gross operating surplus and remuneration of employees is more unbalanced among domestic companies (Denmark, Germany, Estonia, France, Italy, Austria, Slovenia, Slovakia, and Sweden). In these countries, the share of remuneration of employees in value added is lower in domestic companies relative to foreign companies.

In addition, in the CEE sample, with the exception of Estonia, Slovenia and Slovakia, the share of value added retained by employees from domestic companies is higher than by employees from foreign companies.

6. Discussion and Conclusions

Our paper analyzes the challenges that may arise to the harmonious and inclusive economic development of EU member states from Central and Eastern Europe in the larger context of the European Common Market and the free movement of capital.

The theoretical framework on which this paper is based is represented using the concept of the so-called social trilemma. More specifically, we explore some consequences arising from the social cohesion perspective, pointing out that a country cannot simultaneously have (1) a high degree of social equity; (2) free movement of capital, amid structural consequences that manifest themselves as a result of this freedom; and (3) a robust position of foreign companies as a share of value added.

The main empirical evidence that supports the theory is related to the translation of strong competition between countries into several phenomena, including a reduction of the degree of unionization and collective bargaining coverage, while the corporate income tax decreased significantly during the period of study. Among the analyzed CEE countries, the most substantial reductions of the rate of CIT between 2000 and 2018 were in Croatia (−17 p.p.), Bulgaria (−15 p.p.), Czech Republic (−12 p.p.) and Romania, Lithuania and Hungary (−9 p.p.).

Furthermore, there is a negative relationship between the importance of foreign companies and the share of remuneration of employees in total GDP: countries with a high share of foreign companies in value added have a smaller share of remuneration of employees.

For the entire EU sample, the distribution between gross operating surplus and remuneration of employees is 43%/57% in foreign capital companies, and 46%/54% for domestic capital companies. In addition, in nine of 28 states the distribution of value added between gross operating surplus and remuneration of employees is more unbalanced among domestic companies. In these countries, the share of remuneration of employees in value added is lower in domestic companies relative to foreign companies. Moreover, in the CEE sample, with the exception of Estonia, Slovenia and Slovakia, the share of value added retained by employees from domestic companies is higher compared with employees from foreign companies.

The main conclusions of the article can be useful for government in order to reduce the social effects of the trilemma and to customize proper economic policies for development. In addition, the article raises the question of how a national economy can benefit more from the presence of foreign companies, alongside domestic companies, by maximizing their impact on citizen welfare. In our opinion, the main efforts of policymakers should be oriented towards the links between foreign capital and domestic capital, and the support of domestic companies to integrate into global value chains, on the one hand, and encouraging investment in human capital, on the other. Human capital investment is one of the most important policy targets to increase productivity and to achieve balance between cost and non-cost competitiveness.

As a further research direction, we recommend a complementary sectoral approach, especially focusing on various sectors from manufacturing (transport equipment, textiles, rubber, plastics, food, beverages, wood, apparel, etc.), for a more in-depth analysis. The sectoral approach is also essential to emphasize the impact of automation and digitalization within different industries that are moving from human intensive activities to capital intensive activities, given that most emerging countries in Europe are labor-intensive economies, and the digitalization/automatization processes will increase the need for social transfers to vulnerable groups (at least in the short term).

In addition, another research field could encompass the features of economic models and policies implemented by governments from countries, such as Slovenia, Croatia or Estonia, that can be used as good practice models for other CEE countries (i.e., Romania, Poland, Bulgaria), where the share of remuneration of employees is lower, in order to improve economic development. However, in line with other authors (see [

25]) we have referred to a literature review to suggest possible causations that could explain the identified relationships between the studied variables. Further quantitative research with the adoption of more sophisticated statistical methods could be adopted to confirm these conclusions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}