Well-Governed Sustainability and Financial Performance: A New Integrative Approach

,

,

and

and

Abstract

1. Introduction

2. Conceptual Framework of Analysis

2.1. Corporate Social Responsibility (CSR)

2.2. Corporate Governance (CG)

2.3. Financial Performance (FP)

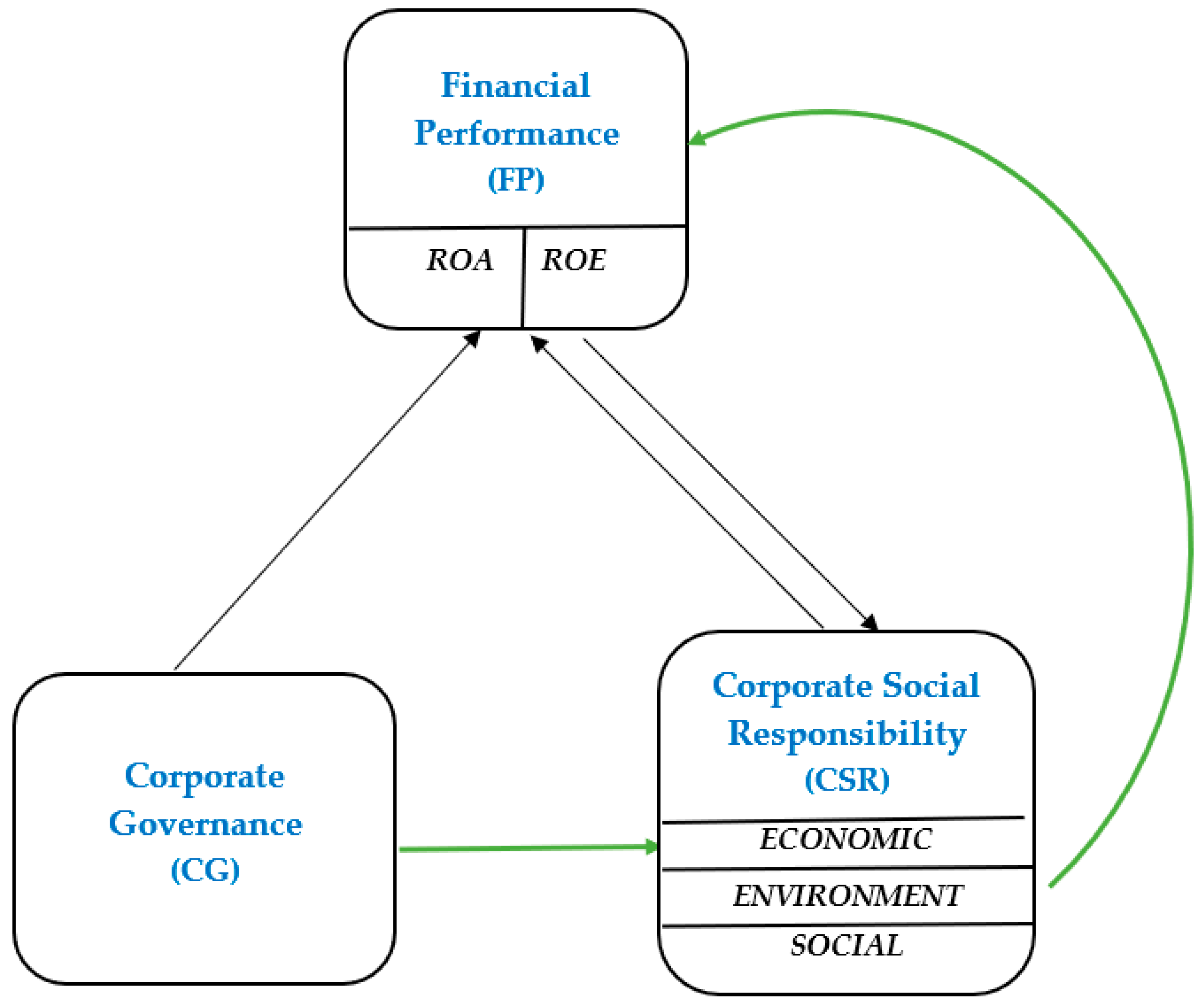

2.4. Applied Model and Interlinkages among CSR-FP-CG

2.4.1. General Conceptual Model

2.4.2. Bidirectional Linkages between CSR-FP

2.4.3. Interlinkages among CG-CSR-FP and CG-FP

3. Materials and Methods

3.1. Data and Sample Construction

3.2. Variables

3.3. Empirical Approach

4. Results and Discussions

4.1. Panel Processing

- the bidirectional relationship between the dimensions of CSR (economic, environmental, social) and the financial performance (ROA, ROE);

- the influence exerted by corporate governance (CG) on financial performance (ROA, ROE) both indirectly, as mediating factor for the CSR-FP relationship, and as a direct factor of influence;

- the total, direct, and indirect dependencies among the three categories of variables, namely CSR (economic, environmental, social), financial performance (ROA, ROE), and corporate governance (CG).

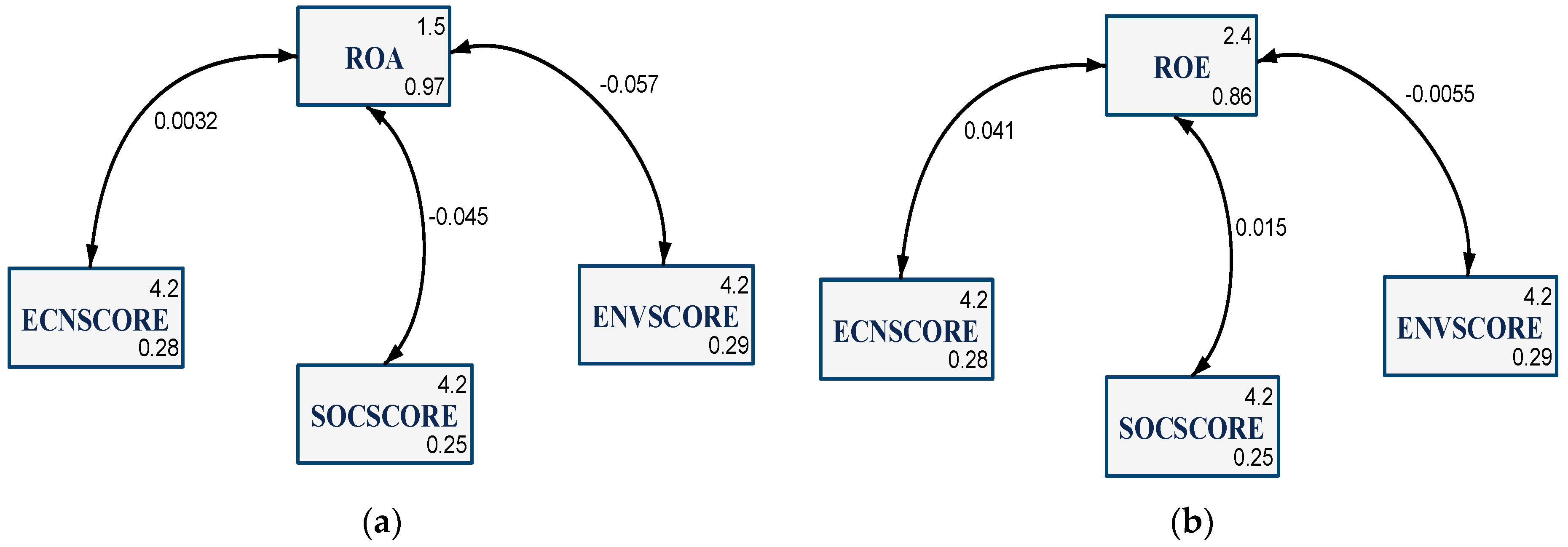

4.2. Bidirectional Relationship CSR-FP

- ROA is positively bi-correlated with the economic dimension of CSR (coefficient = 0.0032), however the link is not significant from a statistical point of view. At the same time, ROA is negatively bi-correlated with the social dimension of CSR (estimated coefficient = −0.045, statistically representative for the 0.1% threshold), but also with the environmental dimension (−0.057 coefficient, statistically representative at the same threshold of 0.1%). These dependencies disprove the first set of hypotheses, regarding a significantly positive bidirectional link among the variables (H1 and H2). In other words, the alternative hypothesis, the one concerning a negative bidirectional link, or an inversely proportional one, an evolution in opposite directions of the analyzed variables is being confirmed. Through an economic lens, the trajectory of these dependencies suggests that the involvement of companies in social and environmental actions leads to a decrease in profitability, as a result of the costs associated with this endeavor;

- ROE is positively bi-correlated with the economic dimension of CSR (the estimated coefficient of 0.041 being statistically representative for the 0.1% threshold). The estimated coefficient of the linkage between ROE and the social dimension (SOCSCORE) is a positive one (0.015), but also insignificant from a statistical point of view. Likewise, insignificant is the estimated coefficient corresponding to the bidirectional dependence between ROE and the environmental dimension of CSR. We must observe that this negative coefficient (−0.0055), implies that the trajectory of this relationship is inversely proportional. In the case of using ROE as the measurement of financial performance, the first set of hypotheses is partially validated, a significant, positive, bidirectional link is only validated in the case of the relationship between the economic dimension of CSR (ECNSCOR) and ROE. From an economic standpoint, this connection implies that a more adequate satisfaction of the clients and associates of a company (as components of the ECNSCORE) leads to an increase in ROE and vice versa, a company with superior profitability is much more involved in the satisfaction of its clients’ and shareholders’ needs.

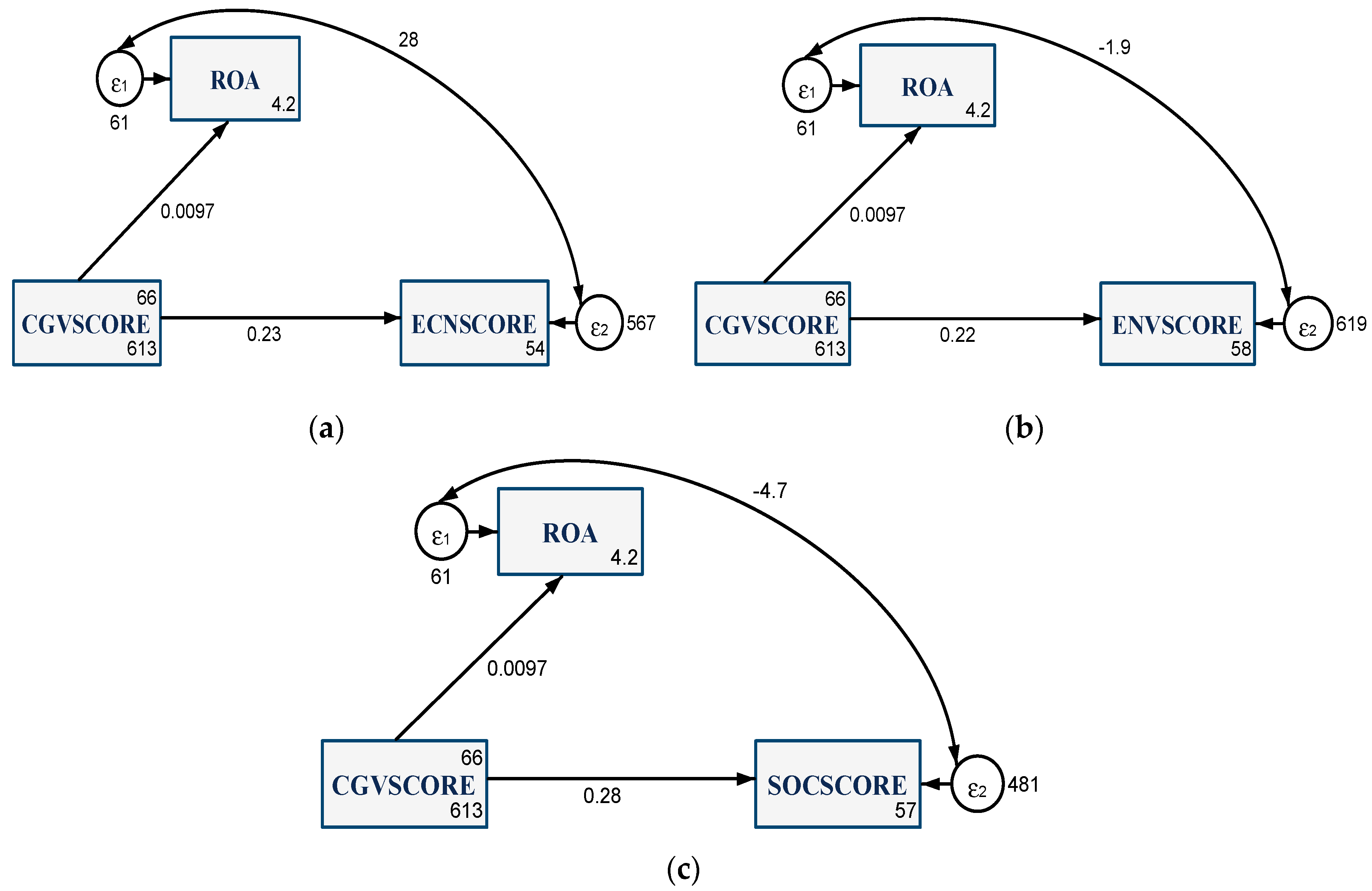

4.3. CG Influence on the CSR-FP Relationship

- indirect positive influence (through a statistically significant coefficient of 0.23) of CG on the bidirectional ROA-ECNSCORE (a coefficient of 28) dependence (Figure 3a). An increase in the value of the coefficient associated with this link from 0.0032 (in the case of the isolated dependence between the variables) (Figure 2a) to 28 (in the case of a link mediated by CG) highlights the major role that CG has in consolidating the link between the two categories of variables;

- the indirect positive influence, suggested by the 0.22 coefficient, that CG has over the ROA-ENVSCORE dependence (a coefficient of −1.9 reiterates the reverse bidirectional link between these variables) (Figure 3b). Moreover, we observe the growth in size of this coefficient and, implicitly, in the power of the link between the variables;

- the indirect positive influence, with an estimated coefficient of 0.28, that CG exerts over the negative, bidirectional dependence between ROA-SOCSCORE (a coefficient of −4.7 consolidates this dependence) (Figure 3c).

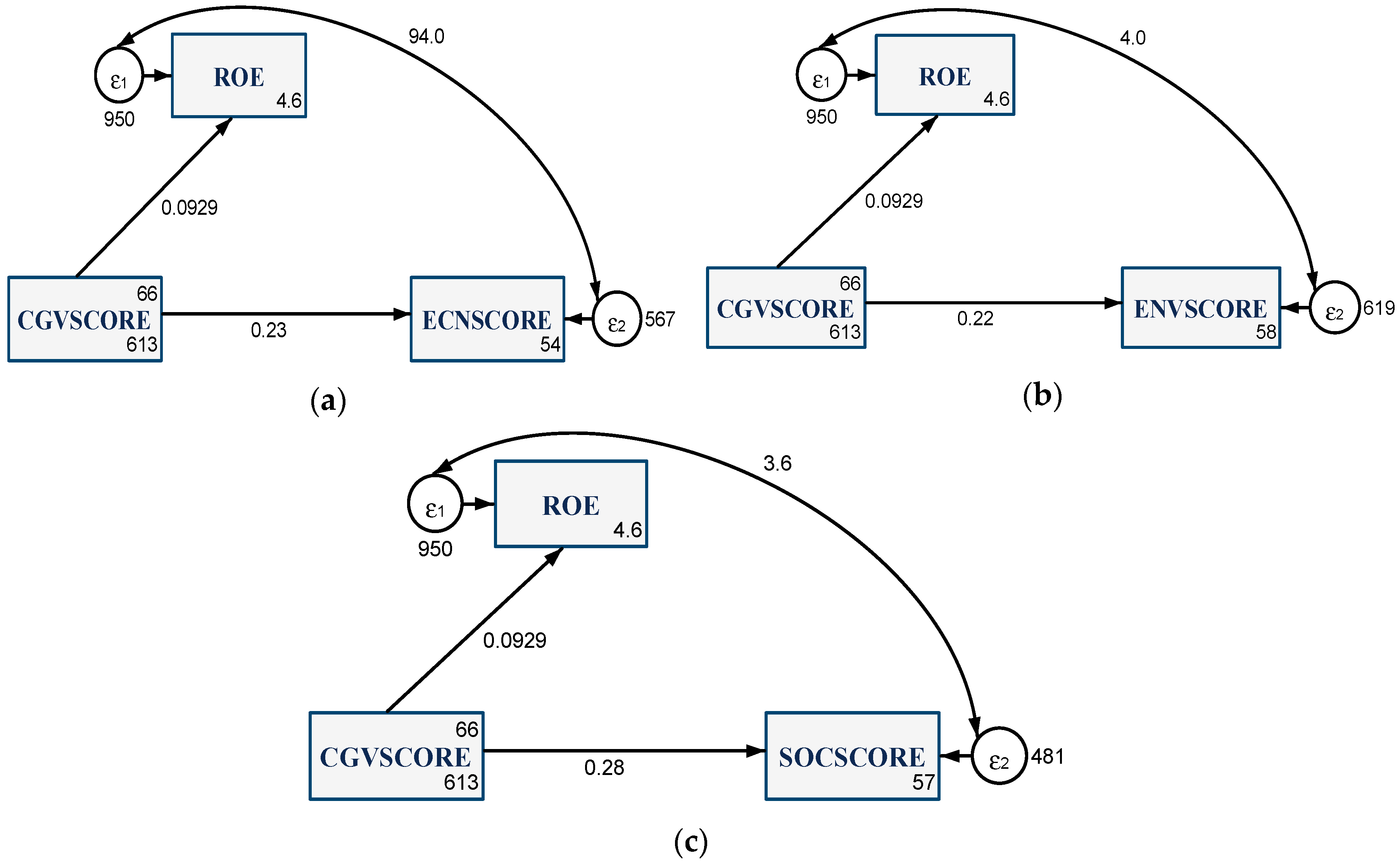

- the indirect positive influence, expressed by a coefficient of 0.23, over the ROE-ECNSCORE (the estimated coefficient registering the same growth tendency as in the case of ROA, up to a value of 94) confirms the role of mediator that CG also has in relation to this link (Figure 4a);

- the indirect and positive influence, determined by a coefficient of 0.22 concerning the ROE-ENVSCORE dependence (Figure 4b). We must take into account that the bidirectional link between these variables is a positive one (the estimated coefficient being 4), unlike in the analysis of the variables of the ROE-ENVSCORE dependence by themselves, where the results showed a negative link (with a coefficient of −0.0055) (Figure 2b). The economic implications of this connection point out the role that CG can have in improving the relationship between financial performance and the environmental policy of a company. Adopting adequate environmental strategies, with controlled costs, can lead to the growth of ROE;

- the direct positive influence (a coefficient of 0.28) of CG over the bidirectional ROE-SOCSCORE dependence (the coefficient of 3.6 confirming this link) (Figure 4c).

4.4. Global Model of Equations

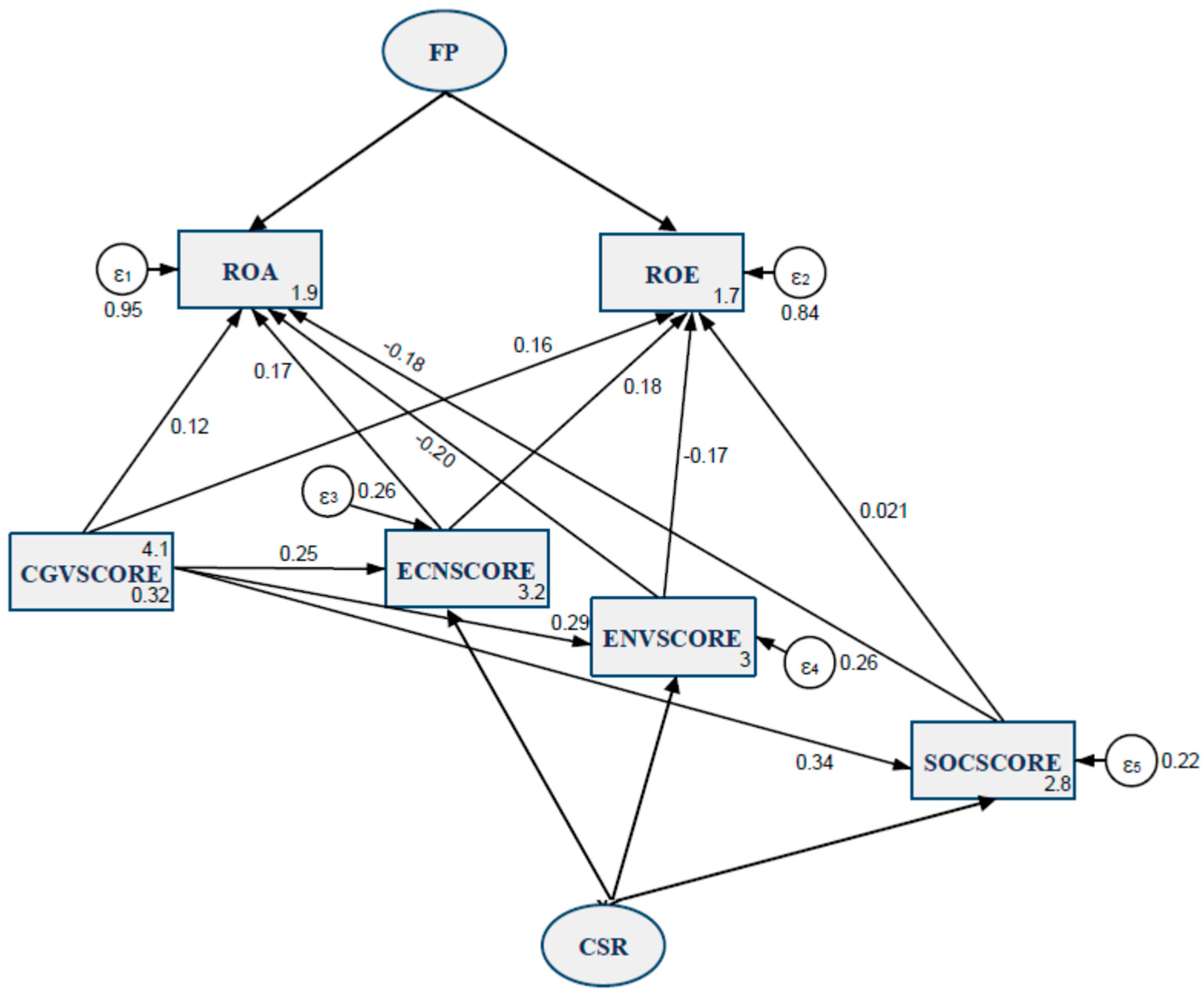

- ENCSCORE-ROA shows a positive, unidirectional dependence (the estimated coefficient of 0.17 is very significant from a statistical point of view, at the 0.1% threshold). The economic dimension of CSR significantly influences ROA, in the direction of its growth, proving that a good policy concerning the satisfaction of clients and shareholders leads to a superior profitability of the company’s assets. The influence of CG (with a statistically significant coefficient of 0.25) is included in the dependence, as an indirect factor or mediator of the mechanism, through which management strategies determine the increase of ROA, as a consequence of adequate economic policies;

- ENVSCORE-ROA reflects a negative, unidirectional dependence (the estimated coefficient being −0.2, very statistically significant at the 0.1% threshold). This influence implies that the involvement and implementation into environmental actions leads to a decrease in the profitability of a company’s assets. Likewise, we also observe the indirect, positive influence of CG (with an estimated coefficient of 0.29, which is very statistically significant);

- SOCSCORE-ROA shows a negative, unidirectional dependence (through the estimated coefficient of −0.18, significant at the 0.1% threshold). Thus, the social dimension of CSR significantly contributes to a decrease in ROA, through any increased involvement in social and societal policies (employees, clients, suppliers, community, etc.). An important role in this dependence is attributed to corporate governance, as a factor of influence of the second degree, which mediates the adoption of strategies that concern social policy and their integration in the global business strategy of a company;

- CG-ROA reflects a direct positive dependence (with an estimated coefficient of 0.12 being very statistically significant), thus corporate governance influences ROA in a favorable way;

- ECNSCORE-ROE, positive, unidirectional dependence (the estimated coefficient of 0.18 is very statistically significant at the 0.1% threshold), through which the profitability of a company’s equity is positively influenced by the economic dimension of CSR. The growth in ROE under the influence of the ECNSCORE is also attributed to the indirect influence of CG, namely the way in which policies regarding the satisfaction of the clients and shareholders is implemented at the level of the company;

- ENVSCORE-ROE, negative, unidirectional dependence (the estimated coefficient being −0.17 and statistically significant at the 0.1% threshold), the environmental dimension of CSR exerting a negative influence on ROE, leading to a decrease in its size, as a consequence of the increased involvement in this kind of policies. The mediating influence of CG is statistically significant as well as positive in the case of this dependence, the decision to reduce pollution and implement innovative, environmentally-friendly product strategies belonging to the governing body of the company;

- SOCSCORE-ROE, positive, unidirectional dependence (with an estimated coefficient of 0.021 being statistically significant), the social dimension exerts a positive influence over ROE, generating its growth, while the influence registered over ROA has proven negative. This dependence suggests that the involvement of a company in social and societal actions is positively appreciated by the present and potential shareholders of the company, leading to an increase in the profitability of a company’s assets. Elements pertaining to CG confirm their mediating role for this dependence (the estimated coefficient being 0.34 and statistically significant);

- CG-ROE, direct, positive dependence (the estimated coefficient of 0.16 being statistically significant), corporate governance influencing ROE in the direction of its growth.

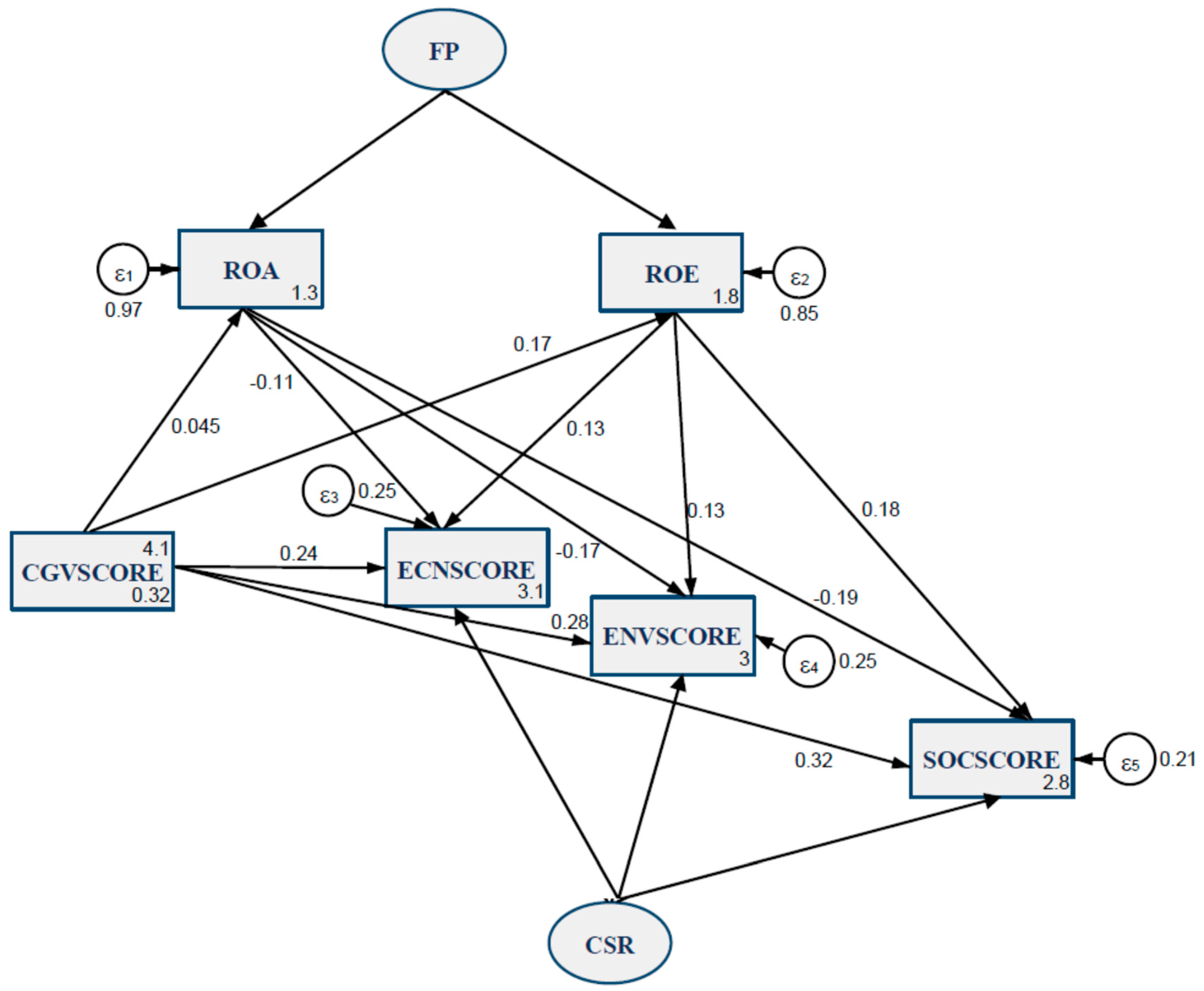

- ROA-ENCSCORE, negative, unidirectional dependence (the estimated coefficient of −0.11 being statistically significant at the 0.1% threshold), ROA influences the economic dimension of CSR in a negative way, showing that a greater profitability of a company’s assets does not represent a guarantee of the involvement of thecompany in economic policies. The dependence is also being mediated by the indirect influence of CG on the economic dimension of CSR (with a coefficient of 0.045, yet statistically insignificant);

- ROA-ENVSCORE, negative, unidirectional dependence (the estimated coefficient being −0.17 and statistically significant at the 0.1% threshold). The economic profitability of assets significantly influences the environmental dimension of CSR, leading it to a decrease. When observing this dependency, we also note a positive, indirect influence on the part of CG;

- ROA-SOCSCORE, the negative, unidirectional dependence (with an estimated coefficient of −0.19, representative at the 0.1% threshold). The social dimension of CSR is also negatively influenced by ROA, under the indirect influence of corporate governance;

- In the case of CG-ROA, we confirm a direct, positive dependence, with an estimated coefficient of 0.045, although not very significant from a statistical point of view;

- ROE-ECNSCORE, positive, unilateral dependence (the estimated coefficient being 0.13, very statistically significant at the 0.1% threshold), the profitability of a company’s assets positively influencing the economic dimension of CSR and implying that an increase in ROE generates better involvement on the part of the company in CSR actions. This dependence is also indirectly amplified by CG (with a coefficient of 0.17 being statistically significant);

- ROE-ENVSCORE, positive, unilateral dependence (the estimated coefficient being 0.13 and statistically representative at the 0.1% threshold). The environmental dimension of CSR is positively influenced by ROE, showing that higher profitabily of assets leads to an increase in the involvement in actions concerning environmental protection. Likewise, we notice the mediating influence of CG over ROE;

- ROE-SOCSCORE, positive, unidirectional dependence (with an estimated coefficient of 0.18, statistically representative). ROE exerts a positive influence over the social dimension of CSR, generating its growth. Likewise, elements pertaining to CG confirm their mediating role regarding this dependence;

- CG-ROE, positive, direct dependence (estimated coefficient of 0.17 being statistically representative), corporate governance influencing ROE in the direction of its growth;

- In both situations (ROA and ROE), we notice the favorable, direct influence of CG over ECNSCORE (the 0.24 coefficient is very statistically significant), ENVSCORE (statistically significant coefficient of 0.28), and also SOCSCORE (estimated coefficient of 0.32 being statistically significant).

5. Concluding Remarks

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| (a) | |||

| Variables | Chi2 | Df | p-Value |

| Log_ROA | 59.93 | 4 | 0.0000 |

| Log_ROE | 54.41 | 4 | 0.0000 |

| Log_ECNSCORE | 216.13 | 1 | 0.0000 |

| Log_ENVSCORE | 280.86 | 1 | 0.0000 |

| Log_SOCSCORE | 468.77 | 1 | 0.0000 |

| H0: all coefficients excluding the intercepts are 0. We can thus reject that null hypothesis for each equation. | |||

| (b) | |||

| Variables | Chi2 | Df | p-Value |

| Log_ROA | 1.77 | 1 | 0.1835 |

| Log_ROE | 27.71 | 1 | 0.0000 |

| Log_ECNSCORE | 257.07 | 3 | 0.0000 |

| Log_ENVSCORE | 369.85 | 3 | 0.0000 |

| Log_SOCSCORE | 607.44 | 3 | 0.0000 |

| H0: all coefficients excluding the intercepts are 0. We can thus reject that null hypothesis for each equation, with limited action on ROA. | |||

| (a) CG-CSR-FP | ||

| Fit Statistic | Value | Description |

| Likelihood ratio | ||

| chi2_ms (26) | 6623.286 | Model vs. saturated |

| p > chi2 | 0.000 | |

| chi2_bs (38) | 7643.061 | Baseline vs. saturated |

| p > chi2 | 0.000 | |

| Population error | ||

| RMSEA | 0.788 | Root mean squared error of approximation |

| 90% CI, lower bound | 0.000 | |

| upper bound | - | |

| Pclose | 0.000 | Probability RMSEA <= 0.05 |

| Information criteria | ||

| AIC | 30,527.643 | Akaike’s information criterion |

| BIC | 30,651.282 | Bayesian information criterion |

| Baseline comparison | ||

| CFI | 0.132 | Comparative fit index |

| TLI | −2.254 | Tucker-Lewis index |

| Size of residuals | ||

| SRMR | 0.237 | Standardized root mean squared residual |

| CD | 0.274 | Coefficient of determination |

| (b) CG-FP-CSR | ||

| Fit Statistic | Value | Description |

| Likelihood ratio | ||

| chi2_ms (26) | 6474.796 | Model vs. saturated |

| p > chi2 | 0.000 | |

| chi2_bs (38) | 7643.061 | Baseline vs. saturated |

| p > chi2 | 0.000 | |

| Population error | ||

| RMSEA | 0.779 | Root mean squared error of approximation |

| 90% CI, lower bound | 0.000 | |

| upper bound | - | |

| pclose | 0.000 | Probability RMSEA <= 0.05 |

| Information criteria | ||

| AIC | 30,379.152 | Akaike’s information criterion |

| BIC | 30,502.791 | Bayesian information criterion |

| Baseline comparison | ||

| CFI | 0.152 | Comparative fit index |

| TLI | −2.181 | Tucker–Lewis index |

| Size of residuals | ||

| SRMR | 0.299 | Standardized root mean squared residual |

| CD | 0.255 | Coefficient of determination |

References

- Brown-Liburd, H.; Cohen, J.; Zamora, V.L. CSR Disclosure Items Used as Fairness Heuristics in the Investment Decision. J. Bus. Ethics 2018, 152, 275289. [Google Scholar] [CrossRef]

- García-Sánchez, I.M.; Noguera-Gámez, L. Integrated Reporting and Stakeholder Engagement: The Effect on Information Asymmetry. Corp. Soc. Responsib. Environ. Manag. 2017, 24, 395–413. [Google Scholar] [CrossRef]

- Maqbool, S.; Bakr, A. The curvilinear relationship between corporate social performance and financial performance: Evidence from Indian companies. J. Glob. Responsib. 2019, 10, 87–100. [Google Scholar] [CrossRef]

- Adeneye, Y.B.; Ahmed, M. Corporate social responsibility and company performance. J. Bus. Stud. Q. 2015, 7, 151–166. [Google Scholar]

- Oh, W.; Park, S. The Relationship Between Corporate Social Responsibility and Corporate Financial Performance in Korea. Emerg. Mark. Financ. Trade 2015, 51, 85–94. [Google Scholar]

- Waworuntu, S.R.; Wantah, M.D.; Rusmanto, T. CSR and financial performance analysis: Evidence from top ASEAN listed companies. Procedia Soc. Behav. Sci. 2014, 164, 493–500. [Google Scholar] [CrossRef]

- Hirigoyen, G.; Poulain-Rehm, T. Causal relationships between corporate social responsibility and financial performance: An international approach. Gestion 2014, 31, 143. [Google Scholar]

- Garcia-Castro, R.; Arino, M.A.; Canela, M.A. Does social performance really lead to financial performance? Accounting for endogeneity. J. Bus. Ethics 2010, 921, 107–126. [Google Scholar] [CrossRef]

- Muzhar, J.; Amir, R.M.; Ghulam, H. Well-governed responsibility spurs performance. J. Clean. Prod. 2017, 166, 1059–1073. [Google Scholar]

- Moazzem, H.M.; Mohammed, A.; Manzuru, A. The mediating role of corporate governance and corporate image on the CSR-FP link. J. Gen. Manag. 2016, 41, 33–51. [Google Scholar]

- Sahut, J.-M.; Mili, M.; Teulon, F. Gouvernance, RSE et performance financière: Vers une compréhension globale de leurs relations. Revue Manag. Avenir 2018, 101, 39–59. [Google Scholar] [CrossRef]

- Thomson Reuters database. Available online: www.thomsonreuters.com (accessed on 2 March 2019).

- Bowen, H.R. Social Responsibilities of the Businessman; Harper & Row: New York, NY, USA, 1953. [Google Scholar]

- Wood, D.J. Corporate social performance revisited. Acad. Manage. Rev. 1991, 16, 691–718. [Google Scholar] [CrossRef]

- Silberhorn, D.; Warren, R.C. Defining corporate social responsibility: A view from big companies in Germany and UK. Eur. Bus. Rev. 2007, 19, 352–357. [Google Scholar] [CrossRef]

- Wood, D.J. Measuring Corporate Social Performance: A Review. Int. J. Manag. Rev. 2010, 12, 50–54. [Google Scholar]

- Carroll, A.B. A three-dimensional conceptual model of corporate performance. Acad. Manage. Rev. 1979, 4, 497–505. [Google Scholar] [CrossRef]

- Carroll, A.B. The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Bus. Horiz. 1991, 34, 39–48. [Google Scholar] [CrossRef]

- Aupperle, K.E. An empirical measure of corporatesocial orientation. In Research in Corporate Social Performance and Policy; Preston, L.E., Ed.; JAI Press: Greenwich, CT, USA, 1984; Volume 6, pp. 27–54. [Google Scholar]

- Wilson, M. Corporate Sustainability: What is it and where does it come from? Ivey Bus. J. 2003, 67, 1–5. [Google Scholar]

- Rodriguez-Fernandez, M. Social responsibility and financial performance: The role of good corporate governance. Bus. Res. Q. 2016, 19, 137–151. [Google Scholar] [CrossRef]

- Simionescu, L.N. Responsabilitatea Sociala si Performanta Financiara a Companiilor; Editura ASE Bucharest: Romania, Bucharest, 2018. [Google Scholar]

- Ntim, C.G.; Soobaroyen, T. Black Economic Empowerment Disclosures by South African Listed Corporations: The Influence of Ownership and Board Characteristics. J. Bus. Ethics 2013, 116, 121–138. [Google Scholar] [CrossRef]

- Turnbull, S. Defining and Achieving Good Governance. Available online: http://dx.doi.org/10.2139/ssrn.2557254 (accessed on 29 January 2015).

- El-Kassar, A.N.; ElGammal, W.; Fahed-Sreih, J. Engagement of family members, corporate governance and social responsibility in family-owned enterprises. J. Organ. Chang. Manag. 2018, 31, 215–229. [Google Scholar] [CrossRef]

- Kuang-Hua, H.; Sin-Jin, L.; Ming-Fu, H. A Fusion Approach for Exploring the Key Factors of Corporate Governance on Corporate Social Responsibility Performance. Sustainability 2018, 10, 1582. [Google Scholar] [CrossRef]

- Money, K.; Schepers, H. Are CSR and corporate governance converging: A view from boardroom directors and company secretaries in FTSE100 companies in the UK. J. Gen. Manag. 2007, 33, 1–11. [Google Scholar] [CrossRef]

- Hirigoyen, G.; Poulain-Rehm, T. Relationships between Corporate Social Responsibility and Financial Performance: What is the Causality. J. Bus. Manag. 2015, 4, 18–43. [Google Scholar] [CrossRef]

- Siminica, M.; Ionascu, C.; Sichigea, M. Corporate Social Performance versus Financial Performance of the Romanian Firms. Prague Econ. Pap. 2019, 28, 49–69. [Google Scholar] [CrossRef]

- KPMG. The KPMG Survey of Corporate Responsibility Reporting 2017. Available online: https://assets.kpmg.com/content/dam/kpmg/xx/pdf/2017/10/kpmg-survey-of-corporate-responsibility-reporting-2017.pdf (accessed on 5 May 2019).

- Woon Leong Lin, W.L.; LawaJ, S.H.; Ho, J.A.; Sambasivanb, M. The causality direction of the corporate social responsibility—Corporate financial performance Nexus: Application of Panel Vector Autoregression approach. N. Am. Econ. Financ. 2019, 48, 401–418. [Google Scholar]

- Javeed, S.H.; Lefen, L. An Analysis of Corporate Social Responsibility and Firm Performance with Moderating Effects of CEO Power and Ownership Structure: A Case Study of the Manufacturing Sector of Pakistan. Sustainability 2019, 11, 248. [Google Scholar] [CrossRef]

- Achim, M.V.; Borlea, S.N.; Mare, C. Corporate Governance and Business Performance: Evidence for the Romanian Economy. J. Bus. Econ. Manag. 2016, 17, 458–474. [Google Scholar] [CrossRef]

- Galant, A.; Cadez, S. Corporate social responsibility and financial performance relationship: A review of measurement approaches. Ekon. Istraz. 2017, 30, 676–693. [Google Scholar] [CrossRef]

- Manta, A.G.; Bădîrcea, R.M.; Pîrvu, R. The Correlation between Corporate Governance and Financial Performances in the Romanian Banks. In Current Issues in Corporate Social Responsibility; Idowu, S., Sitnikov, C., Simion, D., Bocean, C., Eds.; CSR Sustainable, Ethics, Government and Springer: Cham, Switzerland, 2018. [Google Scholar]

- Azman, N.A.N.N.; Roslan, F.I.; Hamzah, N.A.R.; Azmi, N.A.H.M.; Manaf, N.F.A. The Effect of Firm and Corporate Governance Characteristics towards Online CSR Disclosure in Malayasia. Glob. Bus. Manag. Res. Int. J. 2018, 10, 75–84. [Google Scholar]

- Shahzad, A.M.; Rutherford, M.A.; Sharfman, M.P. Stakeholder-Centric Governance and Corporate Social Performance: A Cross-National Study. Corp. Soc. Responsib. Environ. Manag. 2016, 23, 100–112. [Google Scholar] [CrossRef]

- Directive 2014/95/EU of the European Parliament and of the Council of 22 October 2014 amending Directive 2013/34/EU as regards disclosure of non-financial and diversity information by certain large undertakings and groups. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32014L0095 (accessed on 12 June 2019).

- Venturelli, A.; Caputo, F.; Cosma, S.; Leopizzi, R.; Pizzi, S. Directive 2014/95/EU: Are Italian companies already compliant. Sustainability 2017, 9, 1385. [Google Scholar] [CrossRef]

- Dumay, J.; La Torre, M.; Farneti, F. Developing trust through stewardship: Implications for intellectual capital, integrated reporting, and the EU Directive 2014/95/EU. J. Intellect. Cap. 2019, 20, 11–39. [Google Scholar] [CrossRef]

- La Torre, M.; Sabelfeld, S.; Blomkvist, M.; Tarquinio, L.; Dumay, J. Harmonising non-financial reporting regulation in Europe: Practical forces and projections for future research. Med. Account. Res. 2018, 26, 598–621. [Google Scholar] [CrossRef]

- Hox, J.J.; Bechger, T.M. An introduction to structural equation modeling. Fam. Sci. Rev. 1989, 11, 354–373. [Google Scholar]

- Akdoğan, A.A.; KöksaL, O.; Cingöz, A. The Mediating Role of Corporate Reputation in the Effect of Perceived Corporate Social Responsibility on Contextual Performance. In Proceedings of the 14th International Strategic Management Conference, Prague, Czech Republic, 12–14 July 2018. [Google Scholar]

| Country | No. of Companies | Country | No. of Companies |

|---|---|---|---|

| Austria | 9 | Ireland | 23 |

| Belgium | 20 | Italy | 24 |

| Cyprus | 1 | Luxembourg | 7 |

| Czech Republic | 2 | Netherlands | 32 |

| Denmark | 17 | Poland | 13 |

| Finland | 23 | Portugal | 6 |

| France | 73 | Spain | 31 |

| Germany | 63 | Sweden | 36 |

| Greece | 8 | United Kingdom (UK) | 223 |

| Hungary | 3 |

| Category | Name | Symbol | Type |

|---|---|---|---|

| Corporate Social Responsibility (CSR) | Economic dimension | ECNSCORE | Score (Scale: 0–100) |

| Environmental dimension | ENVSCORE | Score (Scale: 0–100) | |

| Social dimension | SOCSCORE | Score (Scale: 0–100) | |

| Corporate governance (CG) | Corporate governance | CGVSCORE | Score (Scale: 0–100) |

| Financial performance (FP) | Return on assets | ROA | Net result/Total assets |

| Return on equity | ROE | Net result/Equity |

| Variables | N | Mean | Standard Deviation (sd) | Min | Max |

|---|---|---|---|---|---|

| ECNSCORE | 3070 | 69.75725 | 24.49642 | 1.26 | 98.52 |

| ENVSCORE | 3070 | 72.40101 | 25.46606 | 8.38 | 95.5 |

| SOCSCORE | 3070 | 74.97696 | 23.01117 | 3.77 | 97.49 |

| CGVSCORE | 3070 | 65.86599 | 24.76057 | 2.12 | 98 |

| ROA | 3070 | 4.85738 | 7.818485 | −55.944 | 67.931 |

| ROE | 3070 | 10.67942 | 30.91214 | −656.566 | 274.653 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Siminica, M.; Cristea, M.; Sichigea, M.; Noja, G.G.; Anghel, I. Well-Governed Sustainability and Financial Performance: A New Integrative Approach. Sustainability 2019, 11, 4562. https://doi.org/10.3390/su11174562

Siminica M, Cristea M, Sichigea M, Noja GG, Anghel I. Well-Governed Sustainability and Financial Performance: A New Integrative Approach. Sustainability. 2019; 11(17):4562. https://doi.org/10.3390/su11174562

Chicago/Turabian StyleSiminica, Marian, Mirela Cristea, Mirela Sichigea, Gratiela Georgiana Noja, and Ion Anghel. 2019. "Well-Governed Sustainability and Financial Performance: A New Integrative Approach" Sustainability 11, no. 17: 4562. https://doi.org/10.3390/su11174562

APA StyleSiminica, M., Cristea, M., Sichigea, M., Noja, G. G., & Anghel, I. (2019). Well-Governed Sustainability and Financial Performance: A New Integrative Approach. Sustainability, 11(17), 4562. https://doi.org/10.3390/su11174562