Market-Based Instruments for Managing Hazardous Chemicals: A Review of the Literature and Future Research Agenda

Abstract

1. Introduction

2. Materials and Methods

3. Experiences from Using Market-Based Instruments in Chemicals Management

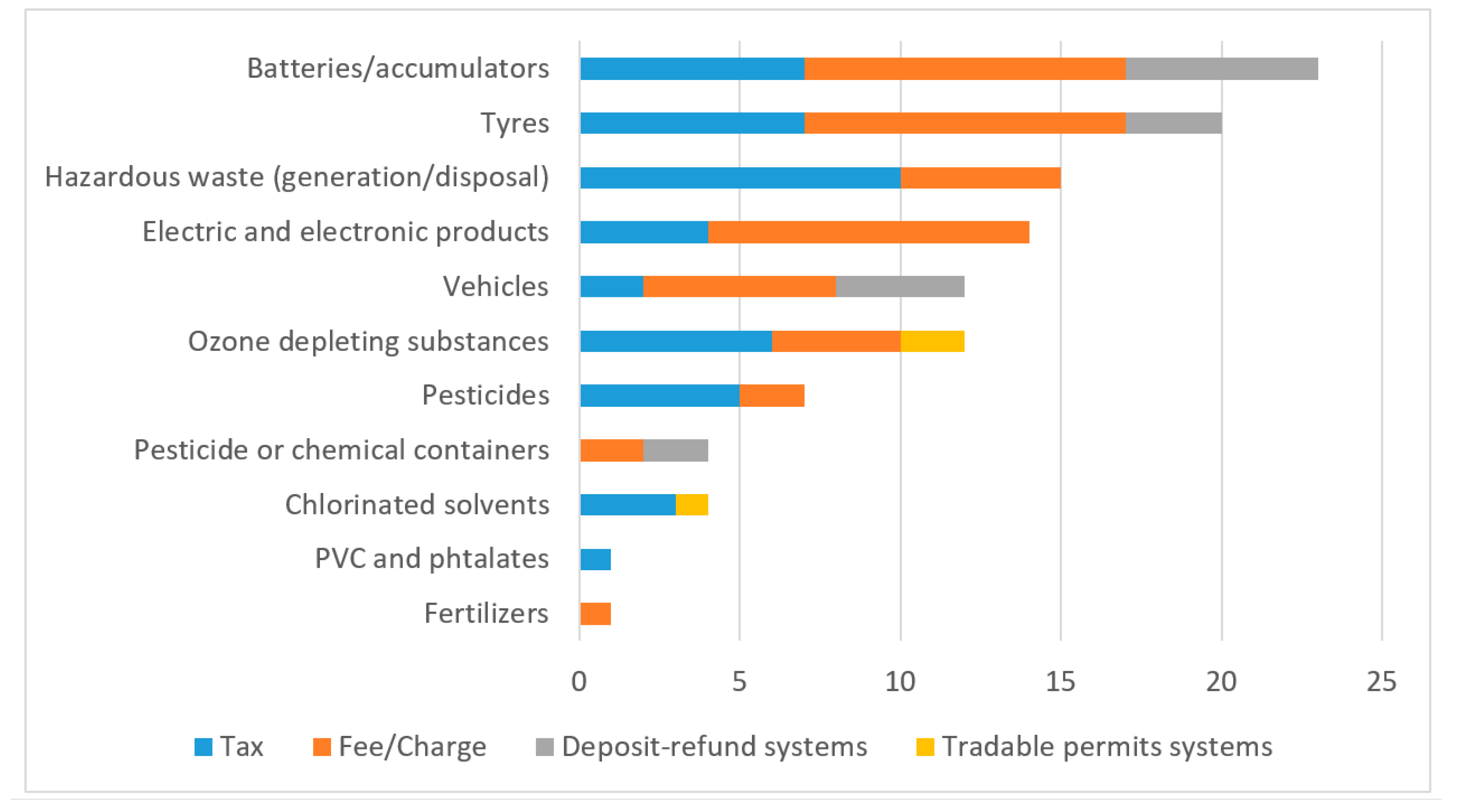

3.1. Limited but Increasing Use of Market-Based Instruments for Managing Hazardous Chemicals

3.2. Taxes on Inputs to Prodution

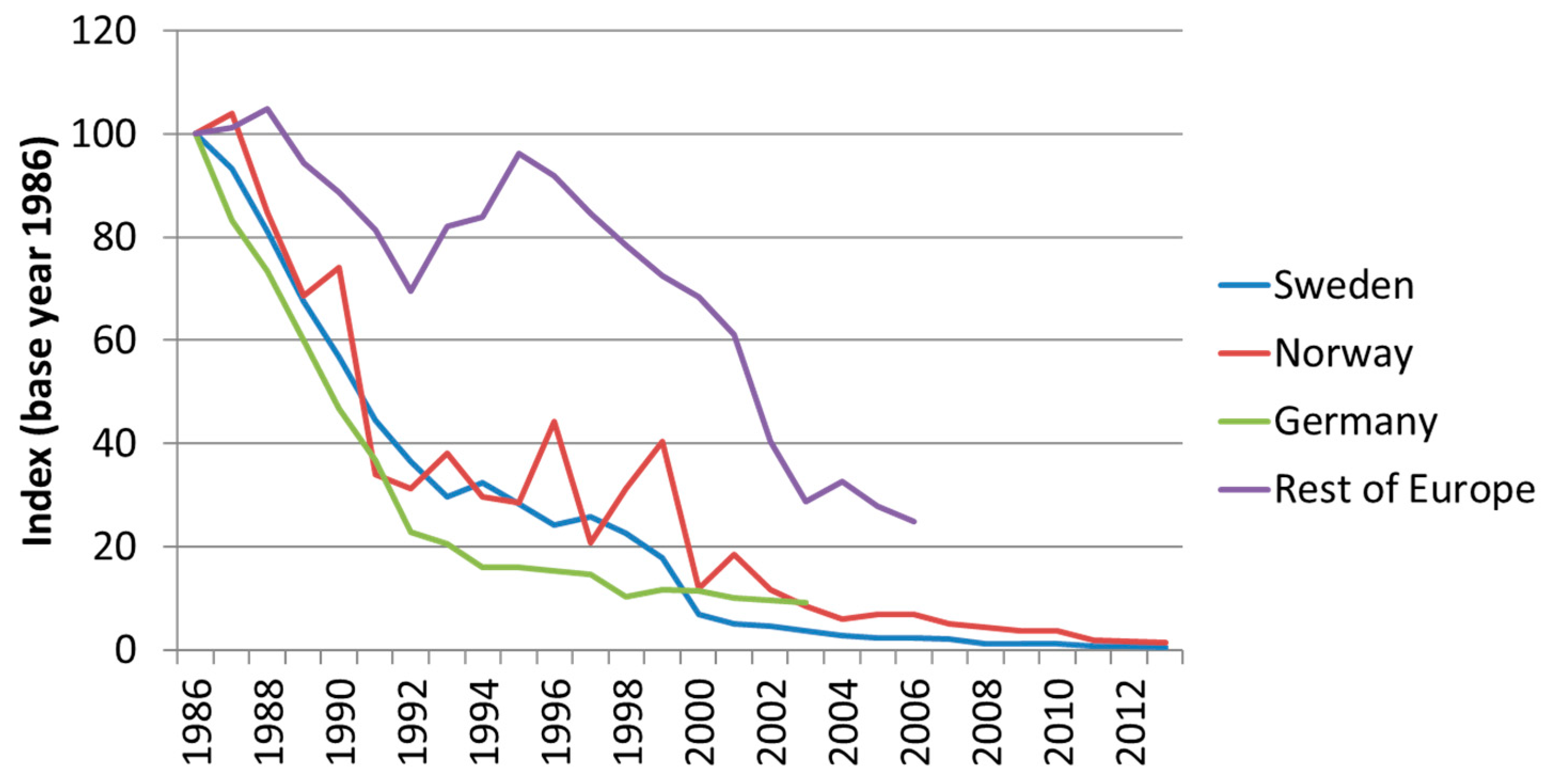

3.2.1. Taxes on Chlorinated Solvents

3.2.2. Taxes on Agrochemicals

3.3. Taxes and Charges on Chemicals in Consumer Products

3.3.1. Tax on Products Containing Phthalates or PVC in Denmark

3.3.2. Tax on Flame Retardants in Electrical and Electronic Products and Hazardous Chemicals in Clothes and Shoes in Sweden

3.4. Tradable Permits in Chemicals Management

3.4.1. The Use of Tradable Permits and Taxes to Phase out Lead in Petrol in the U.S.

3.4.2. Tradable Emission Quotas for Regulating Nitrogen Pollution from Agriculture in New Zealand

3.5. Subsidies and Subsidy Removals

3.5.1. The Fertilizer Subsidy Programme in India

3.6. Charges and Deposit-Refund Instruments for Hazardous Waste Management

3.6.1. Recycling Fees

3.6.2. Deposit-Refund and Refund Systems

3.7. Fiscal Revenue Generation from Market Based-Instruments

4. Discussion

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

- chemic * AND tax * (NOT “taxa”)

- chemic * AND fee

- chemic * AND subsid *

- “chemical pollution” AND tax *

- “chemical pollution” AND fee

- “chemical pollution” AND subsid *

- Pestic * AND tax *

- Pestic * AND fee

- Pestic * AND subsid *

- Fertiliz * AND tax * (NOT “taxa”)

- Fertiliz * AND fee

- Fertiliz * AND subsid *

- Fertiliz * AND tax * (NOT “taxa”)

- Fertiliz * AND fee

- Fertiliz * AND subsid *

- Lead AND tax * and “heavy metals”

- Lead AND fee and “heavy metals”

- Lead AND subsid * and “heavy metals”

- Cadmium AND tax *

- Cadmium AND fee

- Cadmium AND subsid *

- Mercury AND tax *

- Mercury AND fee

- Mercury AND subsid *

- batter * AND tax *

- batter * AND fee

- batter * AND subsid *

- batter * AND refund

- plastic bag * AND tax *

- plastic bag * AND fee

- plastic bag * AND subsid *

- plastic bag * AND refund

Appendix B

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Chemical/Product | Number of Countries | Countries with the Specific Market-Based Instrument | |||

|---|---|---|---|---|---|

| Tax | Fee/Charge | Deposit-Refund Systems | Tradable Permit Systems | ||

| Pesticides | 7 | Denmark, Italy, Norway, Sweden, US | Bulgaria, Canada | ||

| Fertilisers | 1 | Bulgaria | |||

| Ozone depleting substances | 10 | Australia, Czech Republic, Denmark, Spain, US | FYR of Macedonia, Latvia, Montenegro, Serbia | Canada 1, US 2 | |

| Chlorinated solvents | 4 | Denmark, Norway, US | Canada 3 | ||

| Polyvinylcloride and phthalates | 1 | Denmark | |||

| Pesticide or chemical containers | 4 | Canada, Korea | Poland, US | ||

| Tyres a | 15 | Canada, Denmark, Finland, Hungary, Slovenia, South Africa, US | Bulgaria, Canada, Croatia, FYR of Macedonia, Latvia, Lithuania, Malta, Poland, Portugal, US | Canada, Denmark, US | |

| Batteries/accumulators a | 17 | Canada, Denmark, Hungary, Iceland, Liechtenstein, Sweden, US | Austria, Bulgaria, Denmark, FYR of Macedonia, Italy, Korea, Lithuania, Poland, Portugal, Switzerland | Canada, Denmark, Lithuania, Mexico, Poland, US | |

| Electrical and electronic products a | 13 | Canada, Denmark, Hungary, Slovenia | Canada, China, FYR of Macedonia, Korea, Liechtenstein, Lithuania, Malta, Poland, Portugal, Switzerland | ||

| Vehicles a | 10 | Slovenia, Russia | Bulgaria, Czech Republic, Croatia, Finland, Switzerland | Denmark, Finland, Norway, Sweden | |

| Hazardous waste (generation/disposal) | 15 | Belgium, Brazil, Czech Republic, Estonia, Hungary, Iceland, Poland, Portugal, Spain, US | Croatia, Denmark, Germany, Montenegro, Serbia | ||

References

- Weitzman, M.L. Prices vs quantities. Rev. Econ. Stud. 1974, 41, 477–491. [Google Scholar] [CrossRef]

- Bernhardt, E.S.; Rosi, E.J.; Gessner, M.O. Synthetic chemicals as agents of global change. Front. Ecol. Environ. 2017, 15, 84–90. [Google Scholar] [CrossRef]

- Landrigan, P.J.; Fuller, R.; Acosta, N.J.R.; Adeyi, O.; Arnold, R.; Basu, N.; Baldé, A.B.; Bertollini, R.; Bose, O.; Richard, B.S.; et al. The Lancet Commission on pollution and health. Lancet 2018, 391, 462–512. [Google Scholar] [CrossRef]

- Grandjean, P.; Bellanger, M. Calculation of the disease burden associated with environmental chemical exposures: Application of toxicological information in health economic estimation. Environ. Health 2017, 16, 123. [Google Scholar] [CrossRef] [PubMed]

- Goldenman, G.; Fernandes, M.; Holland, M.; Tugran, T.; Nordin, A.; Schoumacher, C.; McNeill, A. The Cost of Inaction: A Socioeconomic Analysis of Environmental and Health Impacts Linked to Exposure to PFAS; Nordisk Ministerråd: Copenhagen, Denmark, 2019. [Google Scholar]

- Olsson, M. The Cost of Inaction: A Socioeconomic Analysis of Costs Linked to Effects of Endocrine Disrupting Substances on Male Reproductive Health; Nordic Council of Ministers: Copenhagen, Denmark, 2014. [Google Scholar]

- Trasande, L.; Zoeller, R.T.; Hass, U.; Kortenkamp, A.; Grandjean, P.; Myers, J.P.; DiGangi, J.; Bellanger, M.; Hauser, R.; Legler, J.; et al. Estimating burden and disease costs of exposure to endocrine-disrupting chemicals in the European Union. J. Clin. Endocrinol. Metabol. 2015, 100, 1245–1255. [Google Scholar] [CrossRef] [PubMed]

- Bellanger, T.M.; Demeneix, T.B.; Grandjean, T.P.; Zoeller, T.R.; Trasande, T.L. Neurobehavioral Deficits, Diseases, and Associated Costs of Exposure to Endocrine-Disrupting Chemicals in the European Union. J. Clin. Endocrinol. Metabol. 2015, 100, 1256–1266. [Google Scholar] [CrossRef] [PubMed]

- Sadler, T. Regulating chemical emissions with risk-based environmental taxation. Int. Adv. Econom. Res. 2000, 6, 287–305. [Google Scholar] [CrossRef]

- Böcker, T.; Finger, R. European Pesticide Tax Schemes in Comparison: An Analysis of Experiences and Developments. Sustainability 2016, 8, 378. [Google Scholar] [CrossRef]

- UN Environment. Global Chemicals Outlook II-From Legacies to Innovative Solutions: Implementing the 2030 Agenda for Sustainable Development; UN Environment: Geneva, Switzerland, 2019. [Google Scholar]

- Söderholm, P. Economic Instruments in Chemicals Policy: Past Experiences and Prospects for Future Use; Nordic Council of Ministers: Copenhagen, Denmark, 2009. [Google Scholar]

- Sterner, T.; Coria, J. Policy Instruments for Environmental and Natural Resource Management, 2nd ed.; RFF Press: Washington, DC, USA, 2012. [Google Scholar]

- Stavins, R.N. Experience with Market-Based Environmental Policy Instruments; Elsevier: Washington, DC, USA, 2001; pp. 355–435. [Google Scholar]

- Baumol, W.J.; Oates, W.E. The Theory of Environmental Policy, 2nd ed.; Oates, W.E., Bawa, V.S., Bradford, D.F., Eds.; Cambridge University Press: Cambridge, UK, 1988. [Google Scholar]

- Macauley, M.K.; Bowes, M.D.; Palmer, K.L. Using Economic Incentives to Regulate Toxic Subst; Future, R.F., Ed.; Resources for the Future: New York, NY, USA, 1992. [Google Scholar]

- Harrington, W.; Morgenstern, R.; Sterner, T. Choosing Environmental Policy, Comparing Instruments and Outcomes in the United States and Europe; RFF press: Washington, DC, USA, 2004. [Google Scholar]

- Bragadóttir, H.; Danielsson, C.v.U.; Magnusson, R.; Seppänen, S.; Stefansdotter, A.; Sundén, D. The Use of Economic Instruments: In Nordic Environmental Policy 2010–2013; Nordisk Ministerråd: Copenhagen, Denmark, 2014; p. 207. [Google Scholar]

- OECD. Environmentally Related Taxes in OECD Countries; Humana Press: Totowa, NJ, USA, 2001. [Google Scholar]

- Swedish Chemicals Agency. Kan Ekonomiska Styrmedel Bidra till en Giftfri Miljö? (Can Economic Policy Instruments Contribute to a Non-Toxic Environment?); Rapport 7/07; KEMI: Stockholm, Sweden, 2007. [Google Scholar]

- Swedish Chemicals Agency. Internationell Förekomst av Ekonomiska Styrmedel på Kemikalieområdet (Economic Policy Instruments in the Area of Chemicals Management in the International Arena); PM 1/11; KEMI: Stockholm, Sweden, 2011. [Google Scholar]

- Swedish Chemicals Agency. När Kan Ekonomiska Styrmedel Komplettera Regleringar Inom Kemikalieområdet? (When Can Economic Instruments Complement Regulations in the Area of Chemicals Management?); Rapport nr 1/13; KEMI: Stockholm, Sweden, 2013. [Google Scholar]

- OECD. Database on Policy Instruments for the Environment. Available online: https://pinedatabase.oecd.org/ (accessed on 11 March 2018).

- Söderholm, P.; Christiernsson, A. Policy effectiveness and acceptance in the taxation of environmentally damaging chemical compounds. Environ. Sci. Policy 2008, 11, 240–252. [Google Scholar] [CrossRef]

- Slunge, D.; Sterner, T. Implementation of Policy Instruments for Chlorinated Solvents: A Comparison of Design Standards, Bans, and Taxes to Phase Out Trichloroethylene. Eur. Environ. 2001, 11, 281–296. [Google Scholar] [CrossRef]

- Gupt, Y.; Sahay, S. Review of extended producer responsibility: A case study approach. Waste Manag. Res. 2015, 33, 595–611. [Google Scholar] [CrossRef]

- OECD. The Political Economy of Biodiversity Policy Reform; Cambridge University Press: Cambridge, UK, 2017. [Google Scholar]

- Massachusetts Budget and Policy Center. Available online: http://children.massbudget.org/tax-break-removal-lead-paint (accessed on 4 December 2018).

- Walls, M. Deposit-Refund Systems in Practice and Theory; Resources for the Future: Washington, DC, USA, 2011; pp. 11–47. [Google Scholar]

- Newell, R.G.; Rogers, K. The U.S. Experience with the Phasedown of Lead in Gasoline; Resources for the Future: Washinton, DC, USA, 2003. [Google Scholar]

- Government of Denmark. Ftalater—reguleringsmæssig status, ftalatafgiftens effekter og overvejelser om differentieret afgift (Phthalates—Regulatory Status, Effects of the Fee on Phthalates and Considerations about a Differentiated Charge); Miljø-og Planlægningsudvalget: Copenhagen, Denmark, 2006; p. 343.

- Rendahl, P. Kemikalieskatt i Sverige? Till Vilket Eller Vilka Ändamål? (Chemical Tax in Sweden? For Which Purpose?); Juristförlaget i Lund: Lund, Sweden, 2017. [Google Scholar]

- Sterner, T. Trichloroethylene in Europe: Ban Versus Tax. 2004. Available online: https://www.taylorfrancis.com/books/e/9781936331468/chapters/10.4324/9781936331468-16 (accessed on 9 August 2019).

- SPIN database. Database on the Use of Substances in Products in the Nordic Countries. Available online: http://spin2000.net/ (accessed on 4 December 2018).

- Shortle, J.S.; Ribaudo, M.; Horan, R.D.; Blandford, D. Reforming agricultural nonpoint pollution policy in an increasingly budget-constrained environment. Environ. Sci. Technol. 2012, 46, 1316. [Google Scholar] [CrossRef]

- OECD. Water Quality and Agriculture: Meeting the Policy Challenge; OECD Publishing: Paris, France, 2012. [Google Scholar]

- Kjäll, K. Hur väl fungerar miljöskatter inom kemikalieområdet? Effekter av miljöskatter på växtskydd och klorerade lösningsmedel i Sverige, Danmark, Norge och Frankrike; KEMI: Stockholm, Sweden, 2012. [Google Scholar]

- Ørum, J.E.; Kudsk, P.; Jørgensen, L.N.; Paaske, K. Behandlingshyppighed og Pesticidbelastning for Solgte Pesticider 2007–2015; University of Copenhagen: Copenhagen, Denmark, 2017. [Google Scholar]

- Government of Sweden. Kemikalieskatt-Skatt på Vissa Konsumentvaror Som Innehåller Kemikalier (Chemical Tax-Tax on Certain Consumer Products Containing Chemicals); Government of Sweden: Stockhgolm, Sweden, 2015.

- Stringer, L. Denmark to scrap tax on PVC and phthalates Chemical Watch Global Risk & Regulation news. 2017. Available online: https://chemicalwatch.com/61121/denmark-to-scrap-tax-on-pvc-and-phthalates. (accessed on 8 October 2018).

- Stringer, L. Sweden’s chemicals tax heavily flawed, say electronics organisations Chemical Watch Global Risk and Regulation news. 2017. Available online: https://chemicalwatch.com/60745/swedens-chemicals-tax-heavily-flawed-say-electronics-organisations. (accessed on 8 October 2018).

- Hammar, H.; Löfgren, Å.; Sterner, T. Political Economy Obstacles to Fuel Taxation. Energy J. 2004, 25, 1–17. [Google Scholar] [CrossRef]

- Greenhalgh, S.; Selman, M. Comparing Water Quality Trading Programs: What Lessons Are There To Learn? J. Reg. Anal. Policy 2012, 42, 104–125. [Google Scholar]

- OECD. The Lake Taupo Nitrogen Market in New Zealand: A Review for Policy Makers; OECD Publishing: Paris, France, 2015. [Google Scholar]

- Gulati, A.; Banerjee, P. Rationalising Fertiliser Subsidy in India: Key Issues and Policy Options. Available online: https://www.econstor.eu/handle/10419/176325 (accessed on 8 August 2019).

- Praveen, K.V. Evolution and Emerging Issues in Fertilizer Policies in India. Econ. Aff. 2014, 59, 163–173. [Google Scholar] [CrossRef]

- Wang, H.D.; Gu, Y.F.; Li, L.Q.; Liu, T.L.; Wu, Y.F.; Zuo, T.Y. Operating models and development trends in the extended producer responsibility system for waste electrical and electronic equipment. Res. Conserv. Recycl. 2017, 127, 159–167. [Google Scholar] [CrossRef]

- Turner, J.M.; Nugent, L.M. Charging up Battery Recycling Policies Extended Producer Responsibility for Single-Use Batteries in the European Union, Canada, and the United States. J. Ind. Ecol. 2016, 20, 1148–1158. [Google Scholar] [CrossRef]

- Favot, M.; Grassetti, L. E-waste collection in Italy: Results from an exploratory analysis. Waste Manag. 2017, 67, 222–231. [Google Scholar] [CrossRef]

- Lim-Wavde, K.; Kauffman, R.J.; Dawson, G.S. Household informedness and policy analytics for the collection and recycling of household hazardous waste in California. Res. Conserv. Recycl. 2017, 120, 88–107. [Google Scholar] [CrossRef]

- Gu, Y.F.; Wu, Y.F.; Xu, M.; Wang, H.D.; Zuo, T.Y. To realize better extended producer responsibility: Redesign of WEEE fund mode in China. J. Clean Prod. 2017, 164, 347–356. [Google Scholar] [CrossRef]

- Awasthi, A.K.; Li, J.H. Management of electrical and electronic waste: A comparative evaluation of China and India. Renew. Sustain. Energy Rev. 2017, 76, 434–447. [Google Scholar] [CrossRef]

- Zeng, X.L.; Duan, H.B.; Wang, F.; Li, J.H. Examining environmental management of e-waste: China’s experience and lessons. Renew. Sustain. Energy Rev. 2017, 72, 1076–1082. [Google Scholar] [CrossRef]

- Pathak, P.; Srivastava, R.R. Assessment of legislation and practices for the sustainable management of waste electrical and electronic equipment in India. Renew. Sustain. Energy Rev. 2017, 78, 220–232. [Google Scholar] [CrossRef]

- Eurostat. End-of-Life Vehicle Statistics; Eurostat: Luxembourg City, Luxembourg, 2016. [Google Scholar]

- Manomaivibool, P. Network management and environmental effectiveness: The management of end-of-life vehicles in the United Kingdom and in Sweden. J. Clean Prod. 2008, 16, 2006–2017. [Google Scholar] [CrossRef]

- Hu, S.H.; Wen, Z.G. Why does the informal sector of end-of-life vehicle treatment thrive? A case study of China and lessons for developing countries in motorization process. Resour. Conserv. Recycl. 2015, 95, 91–99. [Google Scholar] [CrossRef]

- Sun, M.X.; Yang, X.C.; Huisingh, D.; Wang, R.Q.; Wang, Y.T. Consumer behavior and perspectives concerning spent household battery collection and recycling in China: A case study. J. Clean Prod. 2015, 107, 775–785. [Google Scholar] [CrossRef]

- Sun, Z.; Cao, H.B.; Zhang, X.H.; Lin, X.; Zheng, W.W.; Cao, G.Q.; Sun, Y.; Zhang, Y. Spent lead-acid battery recycling in China - A review and sustainable analyses on mass flow of lead. Waste Manag. 2017, 64, 190–201. [Google Scholar] [CrossRef]

- Gu, F.; Guo, J.F.; Yao, X.; Summers, P.A.; Widijatmoko, S.D.; Hall, P. An investigation of the current status of recycling spent lithium-ion batteries from consumer electronics in China. J. Clean Prod. 2017, 161, 765–780. [Google Scholar] [CrossRef]

- Gupt, Y. Economic Instruments and the Efficient Recycling of Batteries in Delhi and the National Capital Region of India. Environ. Dev. Econ. 2014, 20, 236–258. [Google Scholar] [CrossRef]

- Yla-Mella, J.; Keiski, R.L.; Pongracz, E. Electronic waste recovery in Finland: Consumers’ perceptions towards recycling and re-use of mobile phones. Waste Manag. 2015, 45, 374–384. [Google Scholar] [CrossRef]

- OECD. Taxation, Innovation and the Environment; OECD: Paris, France, 2010. [Google Scholar]

- Svenningsen, L.S.; Sørensen, M.M.; Hansen, L.L.; Hansen, T.; Schou, J.; Øyvind, L. Policy Brief: The~Use of Economic Instruments in Nordic Environmental Policy 1990–2017; Nordic Council of Ministers: Stockholm, Sweden, 2018. [Google Scholar]

- Jaffe, A.B.; Newell, R.G.; Stavins, R.N. A tale of two market failures: Technology and environmental policy. Ecol. Econ. 2005, 54, 164–174. [Google Scholar] [CrossRef]

- Finger, R.; Möhring, N.; Dalhaus, T.; Böcker, T. Revisiting Pesticide Taxation Schemes. Ecol. Econ. 2017, 134, 263–266. [Google Scholar] [CrossRef]

- Vatn, A. Input versus emission taxes: Environmental taxes in a mass balance and transaction costs perspective. Land Econ. 1998, 74, 514–525. [Google Scholar] [CrossRef]

- Coria, J. The Economics of Toxic Substance Control and the REACH Directive. Review of Environmental Economics and Policy, Forthcoming. 2019.

- European Commission; DG Health and Food Safety. Ad-Hoc Study on the Trade of Illegal and Counterfeit Pesticides in the EU. Consultancy Report. 2015. Available online: https://ec.europa.eu/food/sites/food/files/plant/docs/pesticides_ppp_illegal-ppps-study.pdf (accessed on 6 August 2019).

- Di John, J. The Political Economy of Taxation and Tax Reform in Developing Countries; Helsinki: United nations university: World Institute for Development Economics Research UNU-WIDER: Helsinki, Finland, 2006. [Google Scholar]

- Slunge, D.; Sterner, T. Environmental Fiscal Reform in East and Southern Africa and its Effects on Income Distribution. Rivista Di Politica Economica 2009, 12. [Google Scholar] [CrossRef]

| Policy Instrument | Description | Example of Application |

|---|---|---|

| Tax | By increasing the price of using a chemical, a tax incentivizes decreased use. Taxes are levied by the state, with proceeds going to the general budget. The level should reflect the damages caused by the production, use and disposal of the chemical, which in the absence of the tax would not be reflected in the market price of the input or final product. | Pesticides [10], inorganic fertilizers [24], chlorinated solvents [25]. |

| Charge/Fee | Similar to a tax but revenues are typically earmarked. The level of a fee should reflect the cost of providing a specific service—such as processing hazardous waste. | Hazardous waste [13], pesticide or chemical containers [23], tyres [26], batteries [26]. |

| Subsidy | A subsidy is the mirror image of a tax. It can provide incentives to increase the use of alternative chemicals that are less hazardous. In particular, authorities may want to subsidise learning and technology development. | Subsidies for organic farming [27], lead paint removal [28]. |

| Subsidy removal | In many cases, subsidies are introduced to deal with distributional concerns, yet may result in unsound practices from a health or environmental perspective. Hence, subsidy removal is considered a policy instrument in its own right. | Removal of subsidies for the use of chemical fertilisers or pesticides [27]. |

| Deposit-Refund | A surcharge is paid when purchasing potentially polluting products. A refund is received when returning the product to an approved centre for recycling or disposal. | Pesticide or chemical containers [23], batteries and tyres [29]. |

| Tradable permits | An overall level of ‘allowable’ pollution is established and allocated among firms in the form of permits. These permits can be traded on a market at market prices | Lead in petrol (trade among refineries) [30], ozone-depleting substances (trade among producers and importers) [17]. |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Slunge, D.; Alpizar, F. Market-Based Instruments for Managing Hazardous Chemicals: A Review of the Literature and Future Research Agenda. Sustainability 2019, 11, 4344. https://doi.org/10.3390/su11164344

Slunge D, Alpizar F. Market-Based Instruments for Managing Hazardous Chemicals: A Review of the Literature and Future Research Agenda. Sustainability. 2019; 11(16):4344. https://doi.org/10.3390/su11164344

Chicago/Turabian StyleSlunge, Daniel, and Francisco Alpizar. 2019. "Market-Based Instruments for Managing Hazardous Chemicals: A Review of the Literature and Future Research Agenda" Sustainability 11, no. 16: 4344. https://doi.org/10.3390/su11164344

APA StyleSlunge, D., & Alpizar, F. (2019). Market-Based Instruments for Managing Hazardous Chemicals: A Review of the Literature and Future Research Agenda. Sustainability, 11(16), 4344. https://doi.org/10.3390/su11164344