The Social Efficiency for Sustainability: European Cooperative Banking Analysis

Abstract

1. Introduction

2. Literature Review and Framework

2.1. Country-Effect Studies in Banking

2.2. Type-Effect Studies in Banking

2.3. The Purpose of Our Study in Banking

3. Hypothesis, Sample and Methodology

3.1. Hypothesis

3.2. Sample

3.3. Methodology

3.3.1. Two-Stage DEA Analysis

3.3.2. Second Stage: Factorial Analysis of Variance

4. Results

4.1. European Social Efficiency Analysis: A Path for Sustainability in Financial Area

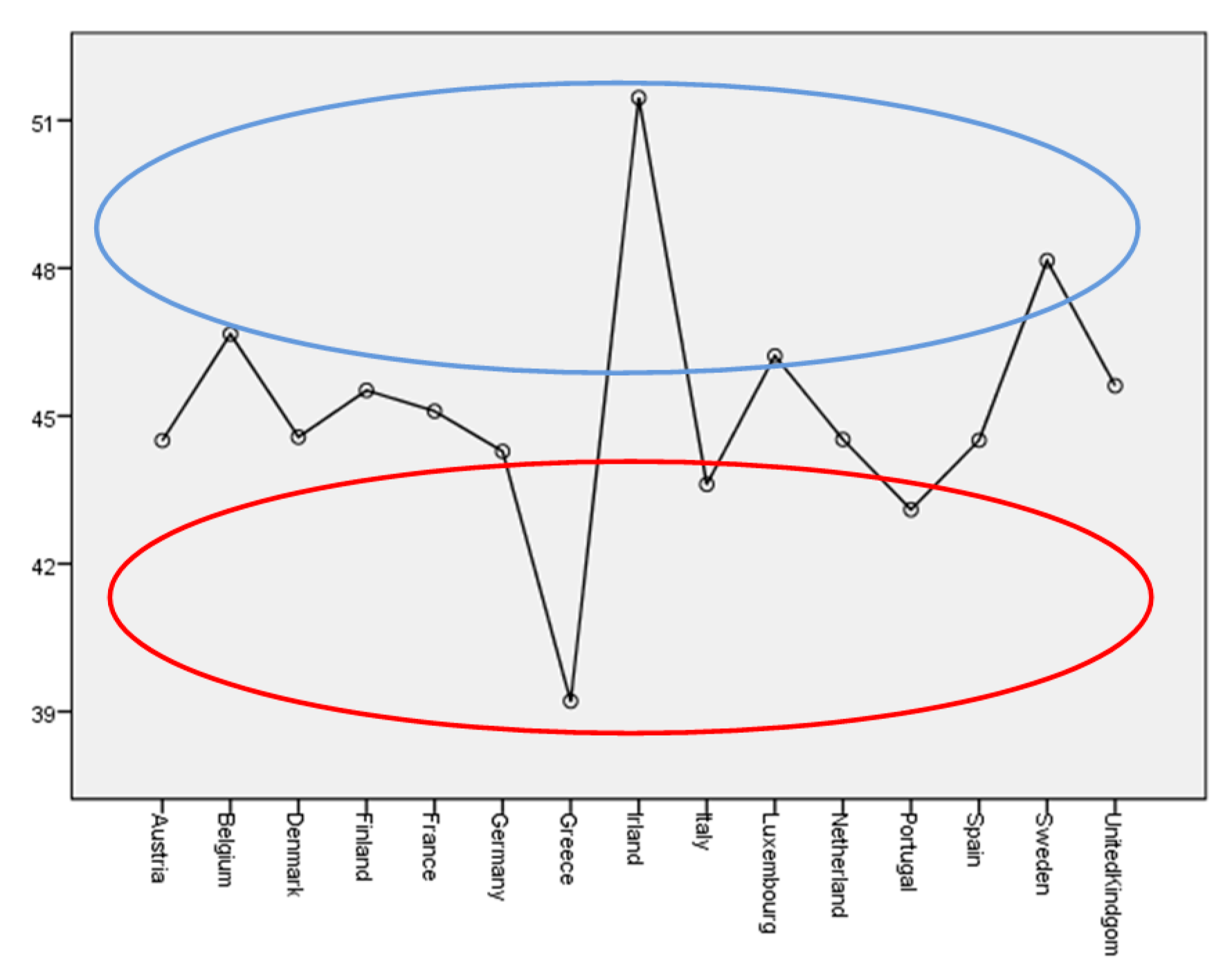

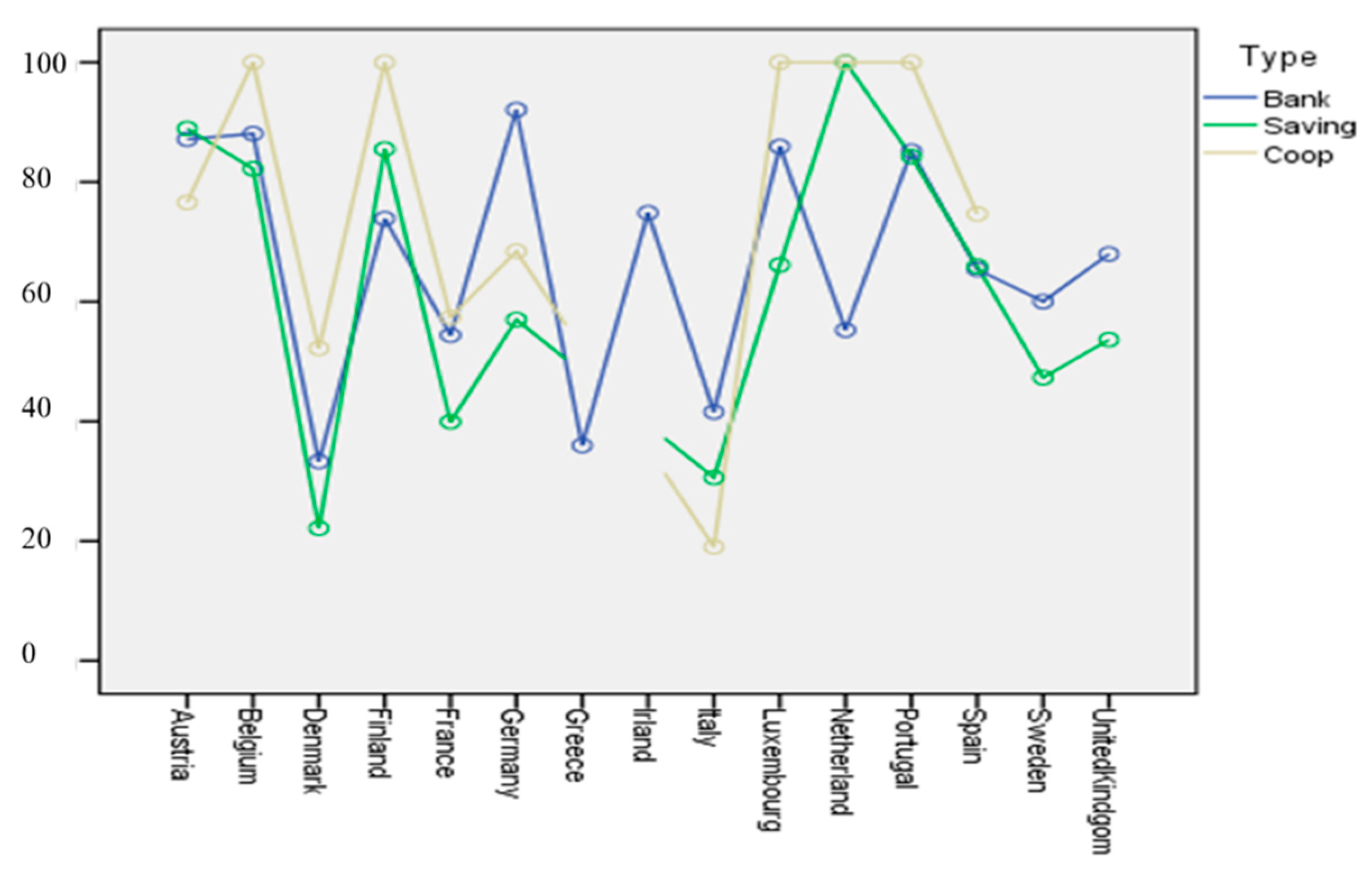

4.2. Country Effect in Social Efficiency for Sustainability between Banks and Cooperatives

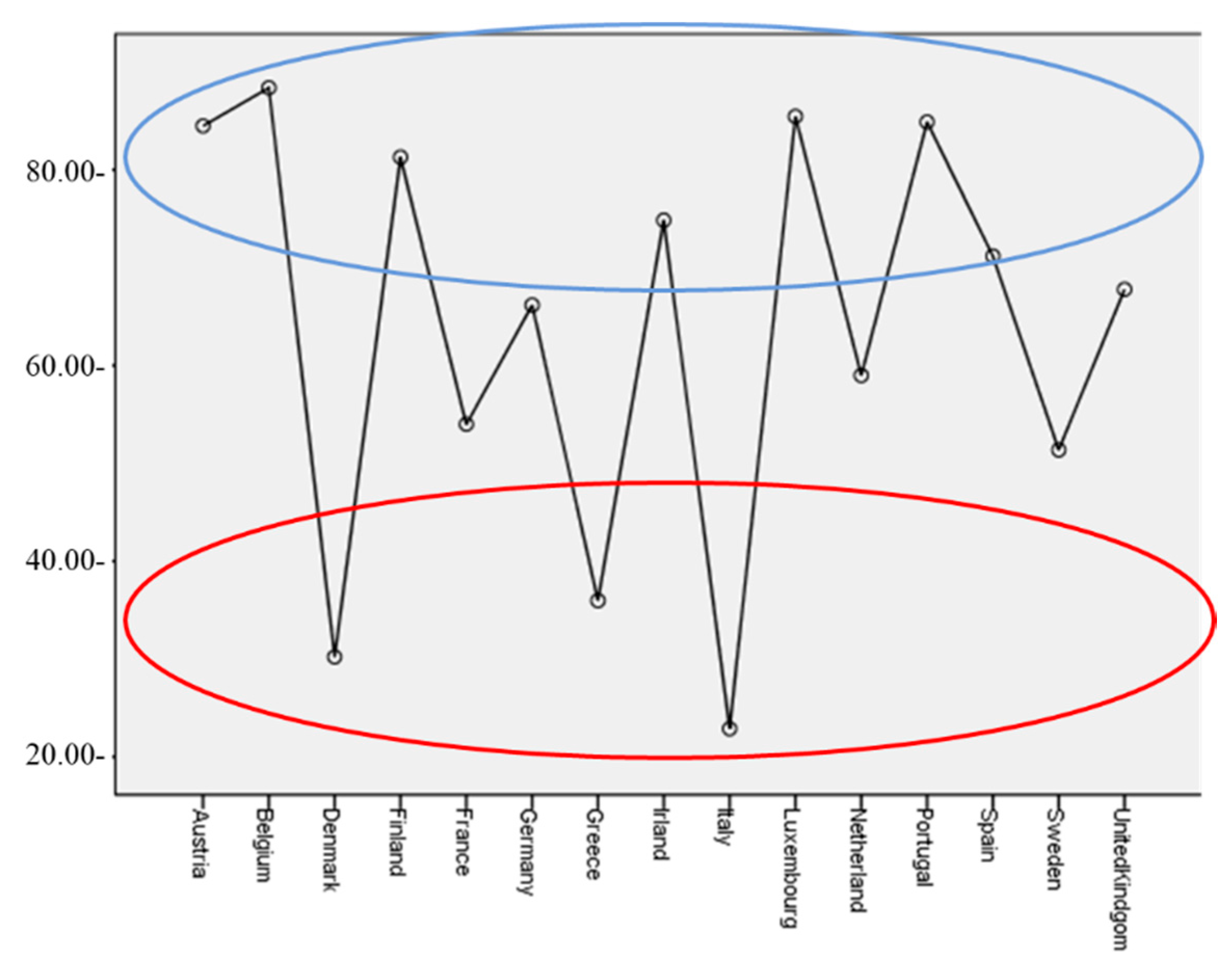

4.3. Analysis of Credit Cooperatives’ Social Efficiency Across European Countries

4.4. Country Effect of Cooperative Bank Efficiency

4.5. Hypothesis Testing

5. Discussion

6. Conclusions, Limitations, and Future Research

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Test/Variable | Profitability | Social Efficiency | ||

|---|---|---|---|---|

| Type-Effect | Country-Effect | Type-Effect | Country-Effect | |

| Welch | 2.961 | 15.593 *** | 24.103 *** | 80.930 *** |

| Brown-Forsythe | 4.191 * | 5.752 *** | 22.994 *** | 68.427 *** |

Appendix B

| Social Efficiency: Type-Effect | p | 95% Confidence Level | ||||

| Games-Howell | Bank | Saving | 10.585 | 2.122 | 0.000 | 5.61 |

| Coop | 13.133 | 1.911 | 0.000 | 8.65 | ||

| Saving | Bank | −10.585 | 2.122 | 0.000 | −15.56 | |

| Coop | 2.549 | 1.790 | 0.329 | −1.65 | ||

| Coop | Bank | −13.133 | 1.911 | 0.000 | −17.62 | |

| Saving | −2.549 | 1.790 | 0.329 | −6.75 | ||

| Profitability: type-effect | p | 95% confidence level | ||||

| Games-Howell | Bank | Saving | 0.658 | 0.278 | 0.048 | 0.01 |

| Coop | 0.549 | 0.274 | 0.112 | −0.10 | ||

| Saving | Bank | −0.658 | 0.278 | 0.048 | −1.31 | |

| Coop | −0.109 | 0.102 | 0.536 | −0.35 | ||

| Coop | Bank | −0.549 | 0.274 | 0.112 | −1.19 | |

| Saving | 0.109 | 0.102 | 0.536 | −0.13 | ||

| Social Efficiency: country-effect | Mean Differences | Standard Error | p | |||

| Games-Howell Test. | F | p | ||||

| Austria | 0.925 | 0.402 | Bank-Saving | −1.792 | 8.943 | 0.978 |

| Coop-Bank | 10.556 | 9.519 | 0.516 | |||

| Coop-Saving | 12.347 | 11.238 | 0.522 | |||

| Belgium | 0.374 | 0.693 | Bank-Saving | 5.884 | 18.644 | 0.948 |

| Coop-Bank | −11.916 | 5.545 | 0.113 | |||

| Coop-Saving | 17.800 | 17.800 | 0.645 | |||

| Denmark | 3.526 | 0.036 | Bank-Saving | 11.128 | 6.977 | 0.260 |

| Coop-Bank | −18.907 | 18.316 | 0.580 | |||

| Coop-Saving | −30.035 | 17.618 | 0.274 | |||

| Finland | 0.797 | 0.461 | Bank-Saving | −11.607 | 12.772 | 0.640 |

| Coop-Bank | −26.120 | 10.002 | 0.055 | |||

| Coop-Saving | 14.513 | 7.942 | 0.199 | |||

| France | 1.968 | 0.143 | Bank-Saving | 14.484 | 6.852 | 0.101 |

| Coop-Bank | −2.968 | 5.655 | 0.859 | |||

| Coop-Saving | 17.452 * | 6.852 | 0.039 | |||

| Germany | 38.708 | 0.000 | Bank-Saving | 35.071 * | 2.751 | 0.000 |

| Coop-Bank | 23.639 * | 2.473 | 0.000 | |||

| Coop-Saving | 11.433 * | 2.189 | 0.000 | |||

| Italy | 24.645 | 0.000 | Bank-Saving | 10.946 | 6.649 | 0.233 |

| Coop-Bank | 22.540 * | 4.635 | 0.000 | |||

| Coop-Saving | −11.594 | 5.028 | 0.069 | |||

| Luxemburg | 0.601 | 0.552 | ||||

| Netherland | 1.197 | 0.322 | ||||

| Portugal | 0.405 | 0.668 | Bank-Saving | 0.903 | 8.666 | 0.994 |

| Coop-Bank | −14.837 | 7.985 | 0.187 | |||

| Coop-Saving | −15.739 * | 3.367 | 0.000 | |||

| Spain | 0.566 | 0.570 | Bank-Saving | −0.514 | 12.426 | 0.999 |

| Coop-Bank | −9.270 | 9.205 | 0.577 | |||

| Coop-Saving | −8.756 | 11.474 | 0.729 | |||

| Sweden | 1.873 | 0.176 | ||||

| United Kingdom | 0.148 | 0.702 | ||||

| When there are less than two entities is not possible to apply this test. | ||||||

References

- Ayadi, R.; Groen, W.P.D. Stress Testing, Transparency, and Uncertainty in European Banking. Oxf. Handb. Econ. Inst. Transpar. 2014. [Google Scholar] [CrossRef]

- San-Jose, L.; Retolaza, J.L.; Torres Pruñonosa, J. Efficiency in Spanish banking: A multistakeholder approach analysis. J. Int. Financ. Mark. Inst. Money 2014, 32, 240–255. [Google Scholar] [CrossRef]

- Ayadi, R.; Llewellyn, D.T.; Schmidt, R.H.; Arbak, E.; De Groen, W.P. Investigating Diversity in the Banking Sector in Europe: Key Developments, Performance and Role of Cooperative Banks; CEPS: Brussels, Belgium, 2010; ISBN 978-94-6138-042-5. [Google Scholar]

- Berger, A.N.; Humphrey, D.B. Efficiency of financial institutions: International survey and directions for future research. Eur. J. Oper. Res. 1997, 98, 175–212. [Google Scholar] [CrossRef]

- Fiordelisi, F.; Marques-Ibanez, D.; Molyneux, P. Efficiency and risk in European banking. J. Bank. Financ. 2011, 35, 1315–1326. [Google Scholar] [CrossRef]

- Ramly, Z.; Chan, S.-G.; Mustapha, M.Z.; Sapiei, N.S. Women on boards and bank efficiency in ASEAN-5: The moderating role of the independent directors. Rev. Manag. Sci. 2017, 11, 225–250. [Google Scholar] [CrossRef]

- Manetti, G.; Magnoli, L. Mutual and social efficiency of italian co-operative banks: An empirical analysis. Ann. Public Coop. Econ. 2013, 84, 289–308. [Google Scholar] [CrossRef]

- Lebovics, M.; Hermes, N.; Hudon, M. Are Financial and Social Efficiency Mutually Exclusive? A Case Study of Vietnamese Microfinance Institutions. Ann. Public Coop. Econ. 2016, 87, 55–77. [Google Scholar] [CrossRef]

- Pava, M.L.; Krausz, J. The association between corporate social-responsibility and financial performance: The paradox of social cost. J. Bus. Ethics 1996, 15, 321–357. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. Creating Shared Value. How to reinvent capitalism—And unleash a wave of innovation and growth. Harv. Bus. Rev. 2011, 89, 62–77. [Google Scholar]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Pitman: Boston, MA, USA, 1984; ISBN 978-0-273-01913-8. [Google Scholar]

- Elkington, J. Partnerships from cannibals with forks: The triple bottom line of 21st-century business. Environ. Qual. Manag. 1998, 8, 31–51. [Google Scholar] [CrossRef]

- Fiordelisi, F. Shareholder value efficiency in European banking. J. Bank. Financ. 2007, 31, 2151–2171. [Google Scholar] [CrossRef]

- Belke, A.; Haskamp, U.; Setzer, R. Regional bank efficiency and its effect on regional growth in “normal” and “bad” times. Econ. Model. 2016, 58, 413–426. [Google Scholar] [CrossRef]

- Wijesiri, M.; Martínez-Campillo, A.; Wanke, P. Is there a trade-off between social and financial performance of public commercial banks in India? A multi-activity DEA model with shared inputs and undesirable outputs. Rev. Manag. Sci. 2017, 1–26. [Google Scholar] [CrossRef]

- Elkington, J. Towards the sustainable corporation: Win-win-win business strategies for sustainable development. Calif. Manag. Rev. Berkeley 1994, 36, 90. [Google Scholar] [CrossRef]

- Tsionas, E.G.; Mamatzakis, E.C. Adjustment costs in the technical efficiency: An application to global banking. Eur. J. Oper. Res. 2017, 256, 640–649. [Google Scholar] [CrossRef]

- Gutierrez-Goiria, J.; San-Jose, L.; Retolaza, J.L. Social Efficiency in Microfinance Institutions: Identifying How to Improve It. J. Int. Dev. 2017, 29, 259–280. [Google Scholar] [CrossRef]

- Bibi, U.; Balli, H.O.; Matthews, C.D.; Tripe, D.W.L. Impact of gender and governance on microfinance efficiency. J. Int. Financ. Mark. Inst. Money 2018, 53, 307–319. [Google Scholar] [CrossRef]

- Chang, H.F. A Liberal Theory of Social Welfare: Fairness, Utility, and the Pareto Principle. Yale Law J. 2000, 110, 173–235. [Google Scholar] [CrossRef]

- Casu, B.; Molyneux, P. A comparative study of efficiency in European banking. Appl. Econ. 2003, 35, 1865–1876. [Google Scholar] [CrossRef]

- Gorton, G.; Pennacchi, G. Financial Intermediaries and Liquidity Creation. J. Financ. 1990, 45, 49–71. [Google Scholar] [CrossRef]

- Chortareas, G.E.; Girardone, C.; Ventouri, A. Financial freedom and bank efficiency: Evidence from the European Union. J. Bank. Financ. 2013, 37, 1223–1231. [Google Scholar] [CrossRef]

- Lozano-Vivas, A.; Pastor, J.T.; Pastor, J.M. An Efficiency Comparison of European Banking Systems Operating under Different Environmental Conditions. J. Product. Anal. 2002, 18, 59–77. [Google Scholar] [CrossRef]

- Galema, R.; Koetter, M. European Bank Efficiency and Performance: The Effects of Supranational Versus National Bank Supervision. In The Palgrave Handbook of European Banking; Palgrave Macmillan: London, UK, 2016; pp. 257–292. ISBN 978-1-137-52143-9. [Google Scholar]

- Fijałkowska, J.; Zyznarska-Dworczak, B.; Garsztka, P.; Fijałkowska, J.; Zyznarska-Dworczak, B.; Garsztka, P. Corporate Social-Environmental Performance versus Financial Performance of Banks in Central and Eastern European Countries. Sustainability 2018, 10, 772. [Google Scholar] [CrossRef]

- Alam, N.; Rizvi, S.A.R. Empirical Research in Islamic Banking: Past, Present, and Future. In Islamic Banking; Palgrave CIBFR Studies in Islamic Finance; Palgrave Macmillan: Cham, Switzerland, 2017; pp. 1–13. ISBN 978-3-319-45909-7. [Google Scholar]

- Widiarto, I.; Emrouznejad, A. Social and financial efficiency of Islamic microfinance institutions: A Data Envelopment Analysis application. Socioecon. Plan. Sci. 2015, 50, 1–17. [Google Scholar] [CrossRef]

- Johnes, J.; Izzeldin, M.; Pappas, V.; Tsionas, M. Measuring Efficiency Convergence in Islamic and Conventional Banks: Cross-Country Evidence. 2017. Available online: https://ssrn.com/abstract=2960018 (accessed on 30 August 2018).

- Tabak, B.M.; Miranda, R.B.; Fazio, D.M. A geographically weighted approach to measuring efficiency in panel data: The case of US saving banks. J. Bank. Financ. 2013, 37, 3747–3756. [Google Scholar] [CrossRef]

- Cuesta, R.A.; Orea, L. Mergers and technical efficiency in Spanish savings banks: A stochastic distance function approach. J. Bank. Financ. 2002, 26, 2231–2247. [Google Scholar] [CrossRef]

- Lang, G.; Welzel, P. Mergers Among German Cooperative Banks: A Panel-based Stochastic Frontier Analysis. Small Bus. Econ. 1999, 13, 273–286. [Google Scholar] [CrossRef]

- Bos, J.W.B.; Kool, C.J.M. Bank efficiency: The role of bank strategy and local market conditions. J. Bank. Finance 2006, 30, 1953–1974. [Google Scholar] [CrossRef]

- Minto, A. The spirit of the law over its letter: The role of culture and social norms in shielding cooperative banks from systemic shocks. Law Financ. Mark. Rev. 2016, 10, 16–26. [Google Scholar] [CrossRef]

- Bal, H.; Gölcükcü, A.; Bal, H.; Gölcükcü, A. Data Envelopment Analysis: An Application to Turkish Banking Industry. Math. Comput. Appl. 2002, 7, 65–72. [Google Scholar] [CrossRef]

- Freeman, R.E. The New Story of Business: Towards a More Responsible Capitalism. Bus. Soc. Rev. 2017, 122, 449–465. [Google Scholar] [CrossRef]

- Freeman, R.E.; Ginena, K. Rethinking the Purpose of the Corporation: Challenges from Stakeholder Theory. Notizie di Politeia 2015, 31, 9–18. [Google Scholar]

- San-Jose, L.; Retolaza, J.L.; Freeman, R.E. Stakeholder Engagement at Extanobe: A Case Study of the New Story of Business. In Stakeholder Engagement: Clinical Research Cases; Issues in Business Ethics; Springer: Cham, Switzerland, 2017; pp. 285–310. ISBN 978-3-319-62784-7. [Google Scholar]

- Gray, R. Rob Social, environmental and sustainability reporting and organisational value creation? Whose value? Whose creation? Account. Audit. Account. J. 2006, 19, 793–819. [Google Scholar] [CrossRef]

- Amonarriz, C.A.; Landart, C.I.; Cantín, L.N. Cooperatives proactive social responsibility in crisis time: How to behave? REVESCO Rev. Estud. Coop. 2017. [Google Scholar] [CrossRef]

- Richez-Battesti, N.; Leseul, G. Cooperative Banks in France: Emergence, Mutations and Issues. In Credit Cooperative Institutions in European Countries; Contributions to Economics; Springer: Cham, Switzerland, 2016; pp. 55–81. ISBN 978-3-319-28783-6. [Google Scholar]

- Demsetz, H. Toward a Theory of Property Rights. In Classic Papers in Natural Resource Economics; Palgrave Macmillan: London, UK, 1974; pp. 163–177. ISBN 978-1-349-41750-6. [Google Scholar]

- Jensen, M.C.; Meckling, W.H. Theory of the firm: Managerial behavior, agency costs and ownership structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef]

- Galbraith, J.K. The New Industrial State; Princeton University Press: Princeton, NJ, USA, 2015; ISBN 978-1-4008-7318-0. [Google Scholar]

- Jensen, M.C. Value Maximization, Stakeholder Theory, and the Corporate Objective Function. Bus. Ethics Q. 2002, 12, 235–256. [Google Scholar] [CrossRef]

- Parmar, B.L.; Keevil, A.; Wicks, A.C. People and Profits: The Impact of Corporate Objectives on Employees’ Need Satisfaction at Work. J. Bus. Ethics 2017. [Google Scholar] [CrossRef]

- Asmild, M.; Zhu, M. Controlling for the use of extreme weights in bank efficiency assessments during the financial crisis. Eur. J. Oper. Res. 2016, 251, 999–1015. [Google Scholar] [CrossRef]

- Hughes, J.P.; Lang, W.W.; Mester, L.J.; Moon, C.-G.; Pagano, M.S. Do bankers sacrifice value to build empires? Managerial incentives, industry consolidation, and financial performance. J. Bank. Financ. 2003, 27, 417–447. [Google Scholar] [CrossRef]

- Luo, Y.; Tanna, S.; De Vita, G. Financial openness, risk and bank efficiency: Cross-country evidence. J. Financ. Stable 2016, 24, 132–148. [Google Scholar] [CrossRef]

- Reckwitz, A. Toward a Theory of Social Practices: A Development in Culturalist Theorizing. Eur. J. Soc. Theory 2002, 5, 243–263. [Google Scholar] [CrossRef]

- Freeman, R.E.; Harrison, J.S.; Wicks, A.C.; Parmar, B.L.; Colle, S.D. Stakeholder Theory: The State of the Art; Cambridge University Press: Cambridge, MA, USA, 2010; ISBN 978-1-139-48411-4. [Google Scholar]

- Kalmi, P. The Role of Stakeholder Banks in the European Banking Sector. In Institutional Diversity in Banking; Palgrave Macmillan Studies in Banking and Financial Institutions; Palgrave Macmillan: Cham, Switzerland, 2017; pp. 33–50. ISBN 978-3-319-42072-1. [Google Scholar]

- Monzon, J.L.; Chaves, R. The European social Economy: Concept and dimensions of the third sector. Ann. Public Coop. Econ. 2008, 79, 549–577. [Google Scholar] [CrossRef]

- Transparency International. Corruption Perceptions Index-Transparency 278 International’s Corruption. Available online: https://www.transparency.org (accessed on 5 September 2018).

- Boston Consulting Group. Welfare data (Wealth-279 to-Well-Being Coefficient and Growth-to-Well-Being Coefficient, as Static and Improvement 280 Coefficient of Welfare). Available online: https://www.bcg.com/ (accessed on 1 July 2018).

- Mauro, P. Corruption and Growth. Q. J. Econ. 1995, 110, 681–712. [Google Scholar] [CrossRef]

- Stolp, C. Strengths and weaknesses of data envelopment analysis: An urban and regional perspective. Comput. Environ. Urban Syst. 1990, 14, 103–116. [Google Scholar] [CrossRef]

- McGuire, J.B.; Sundgren, A.; Schneeweis, T. Corporate Social Responsibility and Firm Financial Performance. Acad. Manag. J. 1988, 31, 854–872. [Google Scholar] [CrossRef]

- Preston, L.E.; O’Bannon, D.P. The Corporate Social-Financial Performance Relationship: A Typology and Analysis. Bus. Soc. 1997, 36, 419–429. [Google Scholar] [CrossRef]

- Cowton, C.J.; San-Jose, L. On the Ethics of Trade Credit: Understanding Good Payment Practice in the Supply Chain. J. Bus. Ethics 2017, 140, 673–685. [Google Scholar] [CrossRef]

- Gutiérrez-Nieto, B.; Serrano-Cinca, C.; Molinero, C.M. Social efficiency in microfinance institutions. J. Oper. Res. Soc. 2009, 60, 104–119. [Google Scholar] [CrossRef]

- Everitt, P.D.; Landau, S.; Everitt, B.S.; Landau, S.L.; Everitt, D. A Handbook of Statistical Analyses Using SPSS; Taylor & Francis: Abingdon, UK, 2004; ISBN 978-1-58488-369-2. [Google Scholar]

| COUNTRY | TYPE | N | Equity | Deposits | Asset | Loan | Labor | Taxes | Risk | Profit |

|---|---|---|---|---|---|---|---|---|---|---|

| France | Banks | 79 | 11,826 | 74,306 | 272,855 | 97,700 | 4956 | 362 | 1450 | 773 |

| Savings | 18 | 5639 | 43,552 | 71,487 | 39,844 | 1717 | 156 | 318 | 327 | |

| Cooperatives | 65 | 20,790 | 114,126 | 378,549 | 141,292 | 7435 | 493 | 1235 | 1133 | |

| Spain | Banks | 18 | 55,545 | 365,233 | 761,873 | 427,455 | 22,327 | 1306 | 10,418 | 3527 |

| Savings | 14 | 9520 | 83,080 | 155,008 | 78,666 | 3196 | 203 | 5467 | 354 | |

| Cooperatives | 51 | 516 | 4887 | 6795 | 3563 | 209 | 4 | 71 | 25 | |

| Germany | Banks | 99 | 7438 | 60,928 | 149,962 | 53,575 | 2532 | 127 | 598 | 254 |

| Savings | 503 | 3114 | 24,988 | 42,113 | 23,894 | 1550 | 85 | 97 | 100 | |

| Cooperatives | 909 | 394 | 3167 | 5847 | 2837 | 187 | 13 | 25 | 22 | |

| Italy | Banks | 66 | 9488 | 62,522 | 148,561 | 81,743 | 4879 | 266 | 5205 | 380 |

| Savings | 31 | 2153 | 15,631 | 50,069 | 40,795 | 1115 | 71 | 1499 | 52 | |

| Cooperatives | 382 | 785 | 4247 | 9715 | 5762 | 309 | 6 | 479 | 14 | |

| Austria | Banks | 36 | 4210 | 30,123 | 56,079 | 32,972 | 3021 | 111 | 717 | 282 |

| Savings | 14 | 910 | 8114 | 13,098 | 8878 | 403 | 15 | 130 | 49 | |

| Cooperatives | 20 | 2631 | 14,004 | 37,343 | 18,372 | 914 | 26 | 541 | 29 | |

| Portugal | Banks | 15 | 5873 | 48,710 | 82,291 | 51,937 | 3235 | 87 | 18 | 25 |

| Savings | 79 | 820 | 11,514 | 13,060 | 5568 | 115 | 1 | 1 | 2 | |

| Cooperatives | 3 | 1918 | 16,340 | 23,189 | 11,100 | 1451 | 60 | 14 | 44 | |

| Belgium | Banks | 16 | 10,705 | 97919 | 184,819 | 92,915 | 3196 | 331 | 2574 | 979 |

| Savings | 3 | 2761 | 46,869 | 55,820 | 37,353 | 269 | 67 | 145 | 288 | |

| Cooperatives | 2 | 1004 | 6282 | 7499 | 4283 | 39 | 0 | 0 | 87 | |

| Denmark | Banks | 26 | 7709 | 36,334 | 159,356 | 92,389 | 1616 | 131 | 1449 | 362 |

| Savings | 29 | 287 | 1769 | 2310 | 1291 | 116 | 2 | 127 | 14 | |

| Cooperatives | 7 | 215 | 1107 | 1535 | 935 | 72 | 0 | 112 | 7 | |

| Finland | Banks | 13 | 6085 | 33,763 | 157,186 | 43,221 | 1133 | 144 | 331 | 581 |

| Savings | 14 | 158 | 1313 | 1807 | 1306 | 49 | 3 | 1 | 11 | |

| Cooperatives | 2 | 26,512 | 148,147 | 414,478 | 228,474 | 8930 | 1036 | 0 | 2649 |

| INPUTS | OUTPUTS | |

|---|---|---|

| Social Efficiency for sustainability (SE) Definition: it is the balance between resources (input) and generation of value (outputs) for the society with those resources (inputs), being sustainable socially. | Equity (E) Deposits (D) | Customer Loans (CC) Labor (L) * Social Contribution/Taxes (SCT) Risk (R) ** |

| Economic Efficiency (EE) Profitability Definition: it is the balance between the resources (assets) used to obtain the net profit. | Total Assets (TA) | Net Profit (P) *** |

| Variables/Data | Equation |

|---|---|

| j = number of DMUs θ = efficiency rating yrj = amount of output r used by j unit [Customer Loans CC, Labor L, Social Contribution-Taxes SCT and Risk R) Xij = amount of input i used by j unit (Equity E and Deposits D) r = number of outputs from 1 to s i = number of inputs from 1 to m ur = coefficient or weight assigned by DEA to output r vi = coefficient or weight assigned by DEA to input i | For each DMU from 1 to n the Social Efficiency (maximizing the outputs) is shown as: |

| Origin | Type III of Sum of Squares | df | Quadratic Means | F | Sig. | Partial to Squared Eta |

|---|---|---|---|---|---|---|

| Corrected Model | 3443.086 | 38 | 90.608 | 8.088 | 0.000 | 0.102 |

| Intersection | 319,453.149 | 1 | 319,453.149 | 28,517.022 | 0.000 | 0.913 |

| Type | 35.510 | 2 | 17.755 | 1.585 | 0.205 | 0.001 *** |

| Country | 1876.861 | 14 | 134.061 | 11.967 | 0.000 | 0.058 |

| Type * Country | 861.991 | 22 | 39.181 | 3.498 | 0.000 | 0.028 ** |

| Error | 30,357.940 | 2710 | 11.202 | |||

| Total | 5,453,484.370 | 2749 | ||||

| Total corrected | 33,801.026 | 2748 |

| Origin | Type III of Sum of Squares | df | Quadratic Means | F | Sig. | Partial to Squared Eta |

|---|---|---|---|---|---|---|

| Corrected Model | 1132,242.643 | 38 | 29,795.859 | 24.510 | 0.000 | 0.256 |

| Intersection | 718,533.603 | 1 | 718,533.603 | 591.069 | 0.000 | 0.179 |

| Type | 3223.202 | 2 | 1611.601 | 1.326 | 0.266 | 0.001 *** |

| Country | 377,493.668 | 14 | 26,963.833 | 22.181 | 0.000 | 0.103 |

| Type * Country | 81,397.755 | 22 | 3699.898 | 3.044 | 0.000 | 0.024 ** |

| Error | 3,294,415.588 | 2710 | 1215.652 | |||

| Total | 13,873,241.818 | 2749 | ||||

| Total corrected | 4,426,658.231 | 2748 |

| COUNTRY | TYPE | N | Mean Social Efficiency (SD) | Levene | F (Sign) (Inter-Groups) | Tamhane (Three Types, But Banks vs. Coop Shown Only) |

|---|---|---|---|---|---|---|

| France | Banks | 79 | 54.406 (35.542) | 9.695 *** | 1.968 (0.143) | No Sign. |

| Cooperatives | 65 | 57.374 (32.239) | ||||

| Spain | Banks | 18 | 65.397 (31.103) | 2.117 * | 0.566 (0.570) | No Sign. |

| Cooperatives | 51 | 74.667 (39.751) | ||||

| Germany | Banks | 99 | 92.064 (20.980) | 306.977 *** | 38.708 (0.000) | Sign. *** |

| Cooperatives | 909 | 68.425 (38.932) | ||||

| Italy | Banks | 66 | 41.555 (36.515) | 32.982 *** | 24.645 (0.000) | Sign. *** |

| Cooperatives | 382 | 19.015 (22.112) | ||||

| Austria | Banks | 36 | 87.144 (28.237) | 3.400 ** | 0.925 (0.402) | No Sign. |

| Cooperatives | 20 | 76.589 (37.001) | ||||

| Portugal | Banks | 15 | 85.163 (30.927) | 2.857 * | 0.405 (0.668) | No Sign. |

| Cooperatives | 3 | 100.000 (0.000) | ||||

| Belgium | Banks | 16 | 88.083 (22.179) | 1.997 | 0.374 (0.693) | No Sign. |

| Cooperatives | 2 | 100.000 (0.000) | ||||

| Denmark | Banks | 26 | 33.277 (30.964) | 10.621 * | 3.526 (0.036) | No Sign. |

| Cooperatives | 7 | 52.184 (45.718) | ||||

| Finland | Banks | 13 | 73.880(36.061) | 4.034 * | 0.797 (0.461) | No Sign |

| Cooperatives | 2 | 100.000 (0.000) |

| Country/Country | N | Mean | SD | I | D | Fr | G | S | A | B | Fi | P |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Italy | 382 | 19.015 | 22.112 | 1 | 0.980 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| Denmark | 7 | 52.184 | 45.718 | 1 | 1.00 | 1.00 | 1.00 | 1.00 | 0.696 | 0.696 | 0.696 | |

| France | 65 | 57.374 | 32.239 | 1 | 0.311 | 0.382 | 0.814 | 0.000 | 0.000 | 0.000 | ||

| Germany | 909 | 68.425 | 38.932 | 1 | 1.00 | 1.00 | 0.000 | 0.000 | 0.000 | |||

| Spain | 51 | 74.667 | 39.751 | 1 | 1.00 | 0.001 | 0.001 | 0.001 | ||||

| Austria | 20 | 76.589 | 37.001 | 1 | 0.321 | 0.321 | 0.321 | |||||

| Belgium | 2 | 100 | 0 | 1 | 1.00 | 1.00 | ||||||

| Finland | 2 | 100 | 0 | 1 | 1.00 | |||||||

| Portugal | 3 | 100 | 0 | 1 | ||||||||

| Total | 1441 | 55.237 | 41.237 |

| Indexes of Nine Countries: Italy, Denmark, France, Germany, Spain, Austria, Belgium, Finland, Portugal | Mean (Deviation) | Correlations Statistics (Pearson) with Social Efficiency 72.02 (26.946) | Significance |

|---|---|---|---|

| Corruption level (measure by the inverse of Corruption Perceptions Index- taken from Transparency International Corruption index) + | 21.11 (19.601) | −6.22 | *** |

| Wealth-to-Well-Being Coefficient | 1.083 (0.070) | 0.799 | *** |

| Growth-to-Well-Being Coefficient | 0.96 (0.221) | 0.721 | *** |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

San-Jose, L.; Retolaza, J.L.; Lamarque, E. The Social Efficiency for Sustainability: European Cooperative Banking Analysis. Sustainability 2018, 10, 3271. https://doi.org/10.3390/su10093271

San-Jose L, Retolaza JL, Lamarque E. The Social Efficiency for Sustainability: European Cooperative Banking Analysis. Sustainability. 2018; 10(9):3271. https://doi.org/10.3390/su10093271

Chicago/Turabian StyleSan-Jose, Leire, Jose Luis Retolaza, and Eric Lamarque. 2018. "The Social Efficiency for Sustainability: European Cooperative Banking Analysis" Sustainability 10, no. 9: 3271. https://doi.org/10.3390/su10093271

APA StyleSan-Jose, L., Retolaza, J. L., & Lamarque, E. (2018). The Social Efficiency for Sustainability: European Cooperative Banking Analysis. Sustainability, 10(9), 3271. https://doi.org/10.3390/su10093271