Evaluating the Effectiveness of Investment in Human Capital in E-Business Enterprise in the Context of Sustainability

Abstract

:1. Introduction

2. Literature Review

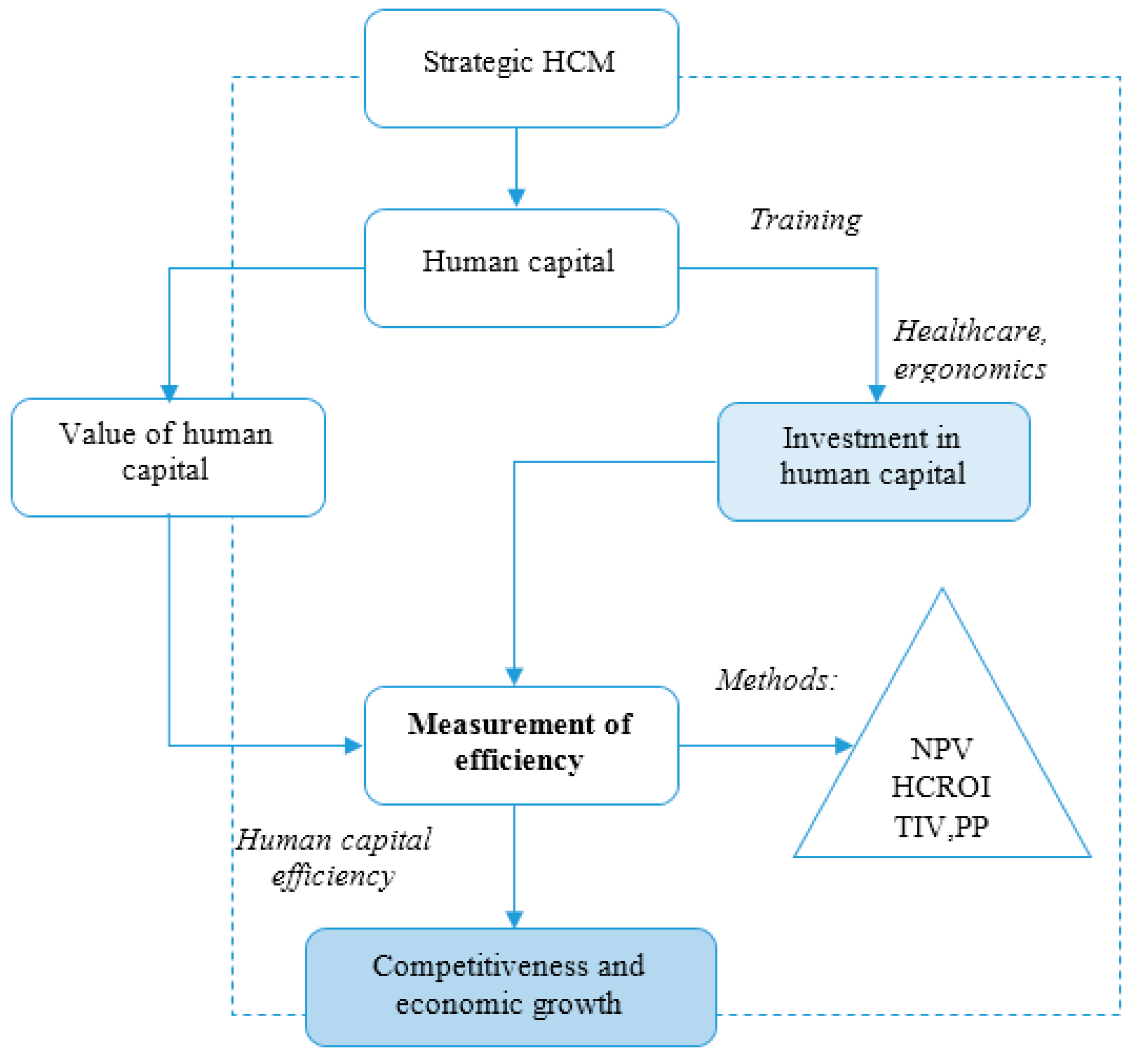

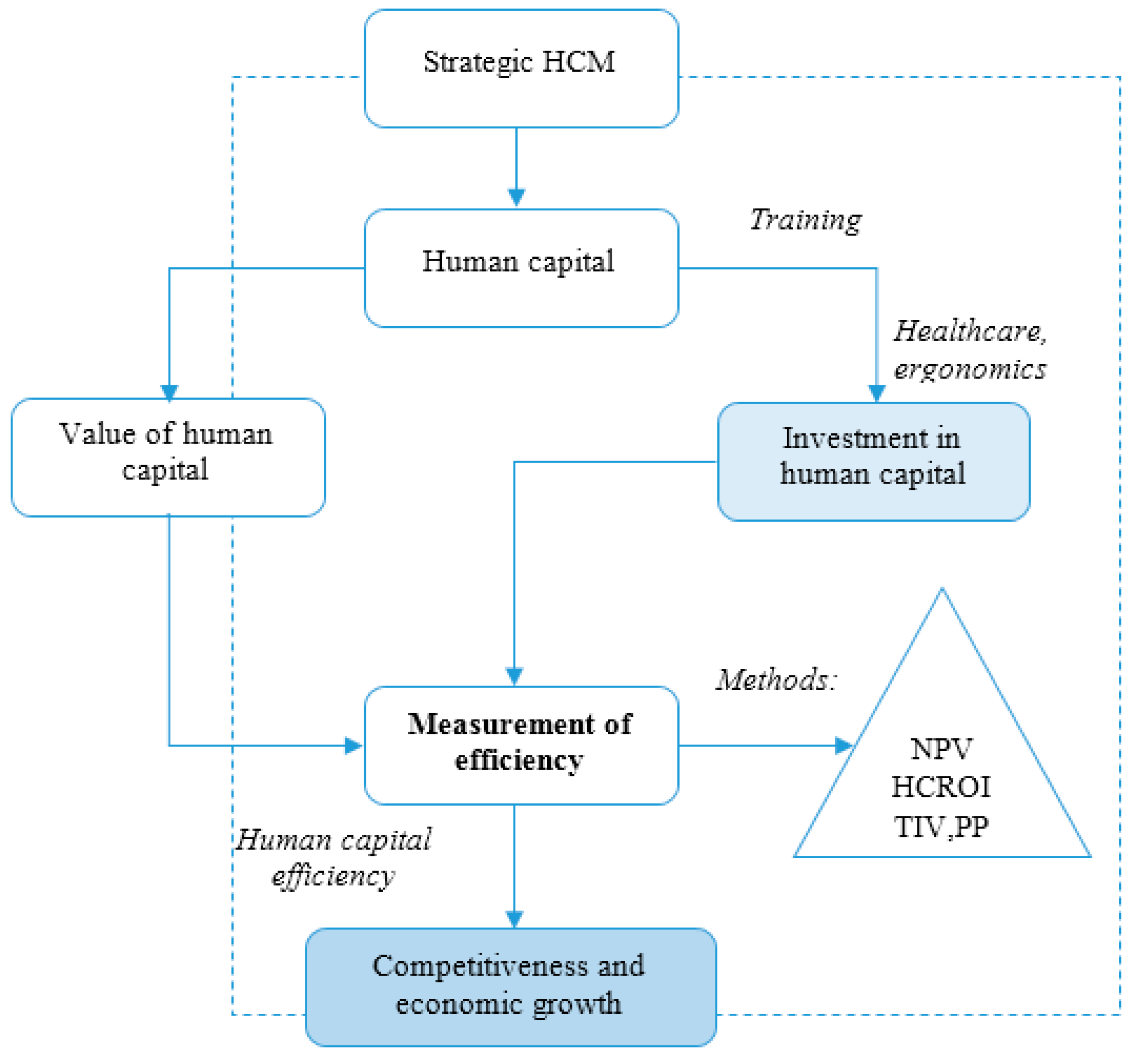

2.1. Human Capital Management

- considers that people are more than the costs,

- understands the measurement as important, which must point to a clear link between HC and business performance,

- determines the mutual relationship between human resources management and business strategy,

- emphasizes the importance of measurement, which points to the fact that the policy of human resources management together with the practice bring excellent results and also serve to determine the direction of human resources, and

- underlines the role of a business partner within the framework of human resources practices, providing different types of advice: what to measure, how to measure it, and how to interpret the results [35].

- more efficient use of resources,

- the provision of realistic personnel projections for the purposes of budget making,

- provision of a clear justification of the expenditures on the training a retraining, development, career counselling and hiring efforts,

- the aid in the maintaining or strengthening of HC, and

- the aid in the preparation of the forming and development of HC.

2.2. Investment in Human Capital in Enterprises within the Area of E-Business

3. Materials and Methods

4. Results—An Example of Implementation of HCM for Effectiveness of Investment in HC

4.1. Human Capital as a Creator of the Enterprise’s Value

4.2. The Effectiveness of Investment in Human Capital

4.2.1. Payback Period of the Investment

4.2.2. Human Capital Return of Investment

Determining the Future Benefits from the Investment

- individual psychological and character attributes of the employees—the ability to utilize the knowledge gained,

- the emergence of new technology—the speed of technological changes, the creation of new versions of software,

- higher satisfaction level of customers—references, new projects, and

- random impacts—occurrence of unexpected situations and events that the enterprise cannot affect.

Calculation of the Human Capital Return of Investment in the Training Activities

4.2.3. The Net Present Value

- the prestige of the certificates for the customers from the public sector,

- informatization of society in the Slovak and Czech Republic, and

- the importance of the efficient project management (fulfilment of the plans, allocation of human resources, people’s management, and so on).

Elimination of Negative Impacts on the Investment in Human Capital

5. Discussion

6. Conclusions

- individuals who expect to increase salaries and social status,

- enterprises, which expect a labor productivity growth, improvement in the quality of production and services, increase in the competitiveness, etc., and

- government or the society expecting an increase in life standards and cultural level.

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Loučanová, E.; Olšiaková, M.; Dzian, M. Open Innovation System in Business Process in the Global Market. In Proceedings of the 17th International Scientific Conference Globalization and Its Socio-Economic Consequences, Rajecké Teplice, Slovakia, 4–5 October 2017; pp. 1347–1353, ISBN 978-80-8154-212-1. [Google Scholar]

- Kampf, R.; Ližbetinová, L.; Tišlerová, K. Management of Customer Service in Terms of Logistics Information Systems. Open Eng. 2017, 7, 26–30. [Google Scholar] [CrossRef]

- Strenitzerová, M.; Gaňa, J. Customer satisfaction and loyalty as a part of customer-based corporate sustainability in the sector of mobile communications services. Sustainability 2018, 10, 1657. [Google Scholar] [CrossRef]

- Madleňáková, L.; Madleňák, R.; Rudawska, A. The Habits and Global Problems of Cross-Border On-Line Shopping. In Proceedings of the 17th International Scientific Conference Globalization and Its Socio-Economic Consequences, Rajecké Teplice, Slovakia, 4–5 October 2017; pp. 1420–1427, ISBN 978-80-8154-212-1. [Google Scholar]

- Ďuračík, M.; Kršák, E.; Hrkút, P. Current trends in source code analysis, plagiarism detection and issues of analysis big datasets. Procedia Eng. 2017, 192, 136–141. [Google Scholar] [CrossRef]

- Zhang, X.; Wang, W.G.; de Pablos, P.O.; Tang, J.; Yan, X.D. Mapping development of social media research through different disciplines: Collaborative learning in management and computer science. Comp. Hum. Behav. 2015, 51, 1142–1153. [Google Scholar] [CrossRef]

- Čorejová, A.; Rostášová, M.; Čorejová, T. Knowledge transfer model and spin-off company set up in significant academic centres in Taiwan. Procedia Eng. 2017, 192, 86–91. [Google Scholar]

- Strenitzerová, M.; Garbárová, M. Identification of the barriers to business in Slovakia. Communications 2017, 19, 56–60. [Google Scholar]

- Ayres, R.U. Sustainability economics: Where do we stand? Ecol. Econ. 2008, 67, 281–310. [Google Scholar] [CrossRef]

- Križanová, A.; Gajanová, L.; Nadanyová, M.; Kramárová, K. Study of green marketing principles and their implementation in the selected Slovak companies. Glob. J. Bus. Econ. Manag. 2016, 6, 78–85. [Google Scholar]

- Choi, Y.; Mai, D.Q. The sustainable role of the E-Trust in the B2C E-Commerce of Vietnam. Sustainability 2018, 10, 291. [Google Scholar] [CrossRef]

- Lee, S.-J.; Ahn, C.; Song, K.M.; Ahn, H. Trust and distrust in E-Commerce. Sustainability 2018, 10, 1015. [Google Scholar] [CrossRef]

- Križanová, A.; Masarová, G.; Štefaniková, L.; Rypáková, M. Building a brand in the context of sustainable development. In Proceedings of the International Conference on Management Engineering and Management Innovation (ICMEMI 2015), Changsha, China, 10–11 January 2015; pp. 79–84. [Google Scholar]

- Jankalová, M.; Jankal, R. The assessment of corporate social responsibility: Aproaches analysis. Entrep. Sustain. Issues 2017, 4, 441–459. [Google Scholar] [CrossRef]

- Hategan, C.-D.; Sirghi, N.; Curea-Pitorac, R.-I.; Hategan, V.-P. Doing well or doing good: The relationship between corporate social responsibility and profit in Romanian companies. Sustainability 2018, 10, 1041. [Google Scholar] [CrossRef]

- Jankalová, M.; Jankal, R. Corporate social responsibility in the context of national awards for social responsibility in the Slovakia and Czech Republic. New Trends Issues Proc. Hum. Soc. Sci. 2017, 3, 190–197. [Google Scholar] [CrossRef]

- Kim, B.-J.; Nurunnabi, M.; Kim, T.-H.; Kim, T. Doing good is not enough, you should have been authentic: Organizational identification, authentic leadership and CSR. Sustainability 2018, 10, 2026. [Google Scholar] [CrossRef]

- Tokarčíková, E.; Falát, L.; Malichová, E. Exploitation of corporate social responsibility reports in manager’s decision making in automotive company. In Proceedings of the 20th International Scientific Conference on Transport Means, Juodkrante, Lithuania, 5–7 October 2016; pp. 259–263. [Google Scholar]

- Lee, Y.-M.; Hu, J.-L. Integrated Approaches for Business Sustainability: The Perspective of Corporate Social Responsibility. Sustainability 2018, 10, 2318. [Google Scholar] [CrossRef]

- Lozano, R. Towards better embedding sustainability into companies’ systems: An analysis of voluntary corporate initiatives. J. Clean. Prod. 2012, 25, 14–26. [Google Scholar] [CrossRef]

- Čorejová, T.; Al Kassiri, M. Knowledge Triangle, Innovation Performance and Global Value Chain. In Proceedings of the 16th International Scientific Conference Globalization and Its Socio-Economic Consequences, Rajecké Teplice, Slovakia, 5–6 October 2016; pp. 329–336, ISBN 978-80-8154-191-9. [Google Scholar]

- Bontis, N.; Dragonetti, N.C.; Jacobsen, K.; Roos, G. The knowledge toolbox: A review of tools available to measure and manage intangible resources. Eur. Manag. J. 1999, 17, 391–402. [Google Scholar] [CrossRef]

- Davenport, T.H.; Prusak, L. Working Knowledge; Harvard Business School Press: Boston, MA, USA, 1998; p. 199. ISBN 1-57851-301-4. [Google Scholar]

- Armstrong, M. A Handbook of Human Resource Management Practice; Cambridge University Press: London, UK, 2006; p. 977. ISBN 0-7494-4631-5. [Google Scholar]

- Schultz, T.W. Investment in Human Capital. Am. Econ. Rev. 1961, 51, 1–17. [Google Scholar]

- Becker, G.S. Human Capital; University of Chicago Press: Chicago, IL, USA, 1964. [Google Scholar]

- Kucharčíková, A. Human Capital—Definitions and approaches. Hum. Resour. Manag. Ergon. 2011, 5, 60–70. [Google Scholar]

- Mankiw, N.G.; Romer, D.; Weil, D.N. Contribution to the empirics of economic growth. Quart. J. Econ. 1992, 107, 407–437. [Google Scholar] [CrossRef]

- Barro, R.J. Human capital and growth. Am. Econ. Rev. 2001, 91, 12–17. [Google Scholar] [CrossRef]

- Romer, P. Endogenous technological change. J. Polit. Econ. 1990, 98, 71–102. [Google Scholar] [CrossRef]

- Edvinsson, L.; Malone, M.S. Intellectual Capital: Realizing Your Company’s True Value by Finding its Hidden Roots; Harper Collins Publishers: New York, NY, USA, 1997. [Google Scholar]

- Sveiby, K.E. The New Organizational Wealth: Managing and Measuring Knowledge-based Assets; Barrett-Kohler Publishers: San Francisco, CA, USA, 1997. [Google Scholar]

- Kearns, P. Evaluating the ROI from Learning; CIPD Publishing: London, UK, 2005; p. 224, ISBN-13 978-1843980780. [Google Scholar]

- The European Public Policy Partnership: Vzdelávací model pre výučbu riadenia ľudského kapitálu vo verejnom sektore. Available online: http://www.jeneweingroup.com/dokumenty/eppp/Vzdelavaci_modul.pdf (accessed on 4 November 2016).

- Martin, J. Key Concepts in Human Resource Management; Saga Publications: London, UK, 2010; p. 304. [Google Scholar]

- Donkin, R. Human Capital Management: A Management Report; Croner: London, UK, 2005. [Google Scholar]

- Nalbantian, H.R. Optimizing rewards: Applying the new science of human capital measurement and management. In Proceedings of the 10th ASHRM Conference, Manama, Bahrain, 29–31 March 2010. [Google Scholar]

- Armstrong, M. Řízení Lidských Zdrojů, 10th ed.; Grada Publishing: Prague, Czech Republic, 2007; p. 800. ISBN 8024714073. [Google Scholar]

- The Search Financial Applications: Human Capital Management (HCM). Available online: http://searchfinancialapplications.techtarget.com/definition/human-capital-management (accessed on 14 December 2016).

- Fitz-Enz, J. The ROI of Human Capital: Measuring the Economic Value of Employee Performance; Amacom: New York, NY, USA, 2009; p. 310. [Google Scholar]

- Archibald, G.A. Regionalizing Competitive Talent: An Exploratory Study of the Role of Human Capital Management in the Context of Economic Integration and Labor Mobility, 1st ed.; Capella University: Minneapolis, MN, USA, 2008; p. 290. ISBN 9780549438861. [Google Scholar]

- The Management Study Guide: Human Capital Management—Meaning and Important Concepts. Available online: http://www.managementstudyguide.com/human-capital-management.htm (accessed on 24 November 2016).

- Ahluwalia, A.K. Human Capital Management (A Comparative Study of Public, Private & Foreign Banks), 1st ed.; Lulu Publication: Raleigh, NC, USA, 2015; p. 106. ISBN 978-1-329-64759-6. [Google Scholar]

- Wyatt, W. Human Capital Index; Towers Watson: London, UK, 2001. [Google Scholar]

- Mayo, A. The Human Value of the Enterprise; Nicholas Brealey Publishing: London, UK, 2001; p. 307. [Google Scholar]

- Andriessen, D. Making Sence of Intellectual Capital; Taylor & Francis Ltd.: New York, NY, USA, 2011; p. 456. [Google Scholar]

- Mathis, R.L.; Jackson, J.H. Human Resource Management. Essential Perspectives, 6th ed.; South-Western, Cengage Learning: Mason, OH, USA, 2012. [Google Scholar]

- Chui, K.T.; Alhalabi, W.; Pang, S.S.H.; Ordóñez de Pablos, P.; Liu, R.W.; Zhao, M.B. Disease Diagnosis in Smart Healthcare: Innovation, Technologies and Applications. Sustainability 2017, 9, 2309. [Google Scholar] [CrossRef]

- Manuti, de Palma, P.D. Why Human Capital Is Important for Organizations: People Come First, 1st ed.; Palgrave Macmillan: London, UK, 2014; p. 198. ISBN 978-1-137-41078-8. [Google Scholar]

- Evans, G. ROI: Measuring the Contribution of Human Capital; Network; Spring; 2007; pp. 33–35. Available online: http://www.wynfordgroup.com/whats_new/Measuring_the_Contribution_of_Human_Capital.pdf (accessed on 24 June 2018).

- Ilin, V.; Ivetić, J.; Simić, D. Understanding the determinants of e-business adoption in ERP-enabled firms and non-ERP enabled firms: A case study of the Western Balkan Peninsula. Technol. Forecast. Soc. Chang. 2017, 125, 206–223. [Google Scholar] [CrossRef]

- Oliveira, T.; Martins, M.F. Understanding e-business adoption across industries in European countries. Ind. Manag. Data Syst. 2010, 110, 1337–1354. [Google Scholar] [CrossRef]

- Evangelista, P.; Sweeney, E. Technology usage in the supply chain: The case small 3PLs. Int. J. Logist. Manag. 2006, 17, 55–74. [Google Scholar] [CrossRef]

- Lawson, R.; Alcock, C.; Cooper, J.; Burgess, L. Factors affecting adoption of electronic commerce technologies by SMEs: An Australian study. J. Small Bus. Enterp. Dev. 2003, 10, 265–276. [Google Scholar] [CrossRef]

- Choi, Y. Digital Business and Sustainable Development—Asian Perspectives; Routledge: New York, NY, USA, 2017; p. 176. ISBN 978-1-138-18954-6. [Google Scholar]

- Bi, R.; Davison, R.M.; Smyrnios, K.X. E-business and fast growth SMEs. Small Bus. Econ. 2017, 48, 559–576. [Google Scholar] [CrossRef]

- Zhu, Z.; Zhao, J.; Tang, X.; Zhang, Y. Leveraging e-business process for business value: A layered structure perspective. Inf. Manag. 2015, 52, 679–691. [Google Scholar] [CrossRef]

- Bernal-Jurado, E.; Medina-Viruel, M.J.; Mozas-Moral, A. Human resource characteristics and e-business: ANfsQCA analysis. Lect. Notes in Bus. Inf. Proc. 2015, 222, 53–63. [Google Scholar]

- EFQM Excellence One Toolbook. EFQM Excellence One Toolbook; EFQM Publications; 2001; p. 150. Available online: http://www.efqm.org/sites/default/files/e1toolbookteaser.pdf (accessed on 10 August 2018).

- Sesil, C.J. Applying Advanced Analytics to HR Management Decision; FT Press: Upper Saddle River, NJ, USA, 2014; p. 224. [Google Scholar]

- Bontis, N.; Fitz-enz, J. Intellectual capital ROI: A causal map of Human Capital Antecedents and Consequents. J. Intellect. Cap. 2002, 3, 223–247. [Google Scholar] [CrossRef]

- Accenture. Available online: https://www.accenture.com/us-en/success-telefonica-digital-hr-model-workday-human-capital-management (accessed on 10 August 2018).

- Bassi, L.; McMurrer, D. Human Capital and Organizational Performance: Next Generation Metrics as a Catalyst for Change. McBassi & Company, Inc., 2007. Available online: http://mcbassi.com/wp/resources/documents/NextGenerationMetrics.pdf (accessed on 10 August 2018).

- Kaplan, R.S.; Norton, D.P. The Balanced Scorecard; HBS Press: Boston, MA, USA, 1996. [Google Scholar]

- Šafránková, J.M.; Šikýř, M. Work expectations and potential employability of millennials and post-millennials on the Czech labor market. Oeconomia Copernicana 2017, 8, 584–596. [Google Scholar] [CrossRef]

- Zhang, X.; Gao, Y.; Yan, X.D.; Ordóñez de Pablos, P.; Sun, Y.Q.; Cao, X.F. From e-learning to social-learning: Mapping development of studies on social media-supported knowledge management. Comp. Hum. Behav. 2015, 51, 803–811. [Google Scholar] [CrossRef]

- Lorincová, S.; Potkány, M. The proposal of innovation support in Small and Medium-sized Enterprises. In Proceedings of the International Conference on Engineering Science and Production Management (ESPM), Bratislava, Slovakia, 16–17 April 2015; pp. 157–161. [Google Scholar]

- Chodasová, Z.; Tekulová, Z. Monitoring of competitiveness indicators of the controlling enterprise. In Proceedings of the International Conference on Engineering Science and Production Management (ESPM), Bratislava, Slovakia, 16–17 April 2015; pp. 101–106. [Google Scholar]

- Malichová, E.; Ďurišová, M.; Tokarčíková, E. Models of Application Economic Value Added in Automotive Company. Transp. Probl. 2017, 12, 93–102. [Google Scholar] [CrossRef]

- Malichová, E.; Ďurišová, M. Evaluation of Financial Performance of Enterprises in IT Sector. Procedia Econ. Financ. 2015, 34, 238–243. [Google Scholar] [CrossRef]

- Lorincová, S.; Schmidtová, J.; Balážová, Z. Perception of the Corporate Culture by Managers and Blue Collar Workers in Slovak Wood-Processing Businesses. Acta Fac. Xylologiae 2016, 58, 149–163. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Metrics | Author | Formula |

|---|---|---|

| HC ROI | Mankiw et al., 1992 | |

| HC ROI | Fitz-enz, 2009 | . |

| HC ROI | Manuti,2014 | |

| TIV | Evans, 2007 | |

| Payback Period | ||

| NPV | r—interest rate n—investment’s lifetime |

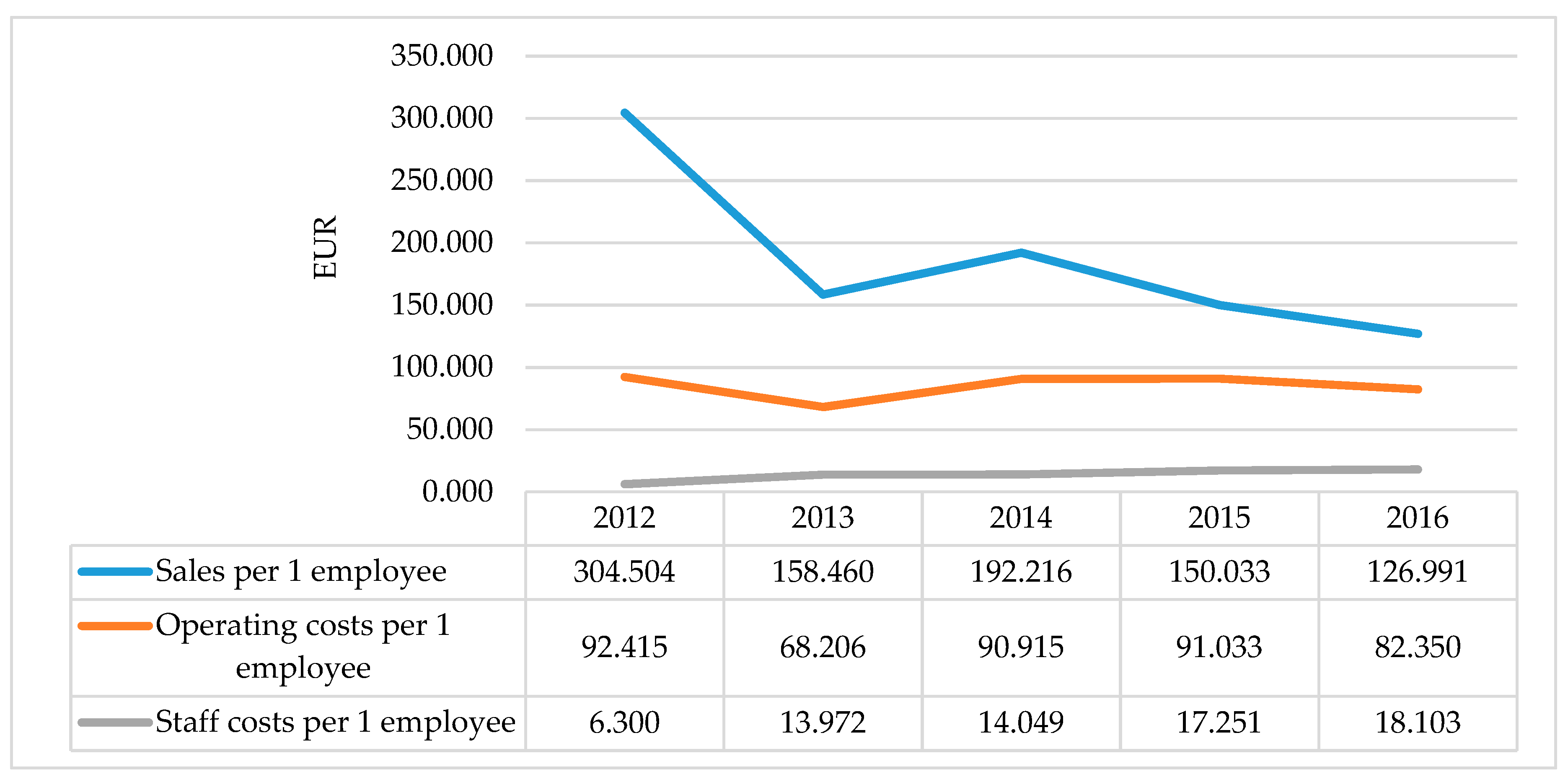

| Indicator | 2012 | 2013 | 2014 | 2015 | 2016 |

|---|---|---|---|---|---|

| Number of employees | 5 | 25 | 45 | 90 | 140 |

| Number of employees (full time) | 5 | 23 | 41 | 78 | 125 |

| % employees: Top management | 20 | 8 | 6.7 | 3.3 | 2.1 |

| % employees: Managers | 20 | 36 | 26.7 | 22.2 | 22.9 |

| % employees: Specialists | 40 | 40 | 53.3 | 63.3 | 67.9 |

| % employees: Administration | 20 | 8 | 13.3 | 8.9 | 7.1 |

| Staff costs (EUR) | 31,500 | 349,310 | 632,210 | 1,552,590 | 2,534,400 |

| Number of trained employees | 0 | 0 | 11 | 24 | 34 |

| Sales (EUR) | 1,522,520 | 3,961,459 | 8,649,730 | 13,502,999 | 17,778,700 |

| Net profit after taxes (EUR) | 889,467 | 14,298,311 | 2,976,720 | 2,589,800 | 2,065,200 |

| Operating costs (EUR) | 462,075 | 1,705,161 | 4,091,172 | 8,192,960 | 11,528,946 |

| Indicator | 2012 | 2013 | 2014 | 2015 | 2016 |

|---|---|---|---|---|---|

| Investment in human capital as % of sales | 0.02 | 0.03 | 0.2 | 0.6 | 0.6 |

| Investment in human capital as % of the operating costs | 0.08 | 0.06 | 0.4 | 1.0 | 0.9 |

| Staff costs as % of revenues | 2.1 | 8.8 | 7.3 | 11.5 | 14.3 |

| Training costs as % of staff costs | 0 | 0 | 1.6 | 3 | 2.3 |

| Year | Training Cost (EUR) | Cash Flow (EUR) | Cumulative Cash Flow (EUR) | Payback Period (Years) |

|---|---|---|---|---|

| 2014 | 10,125 | 3,017,658 | 3,017,658 | 0.003 |

| 2015 | 46,815 | 2,204,651 | 5,222,309 | 0.021 |

| 2016 | 57,699 | 2,018,173 | 7,240,481 | 0.029 |

| Category | 2012 | 2013 | 2014 |

|---|---|---|---|

| Net CF (EUR) | 2,704,651 | 2,218,173 | 2,100,500 |

| Sales from the selling of fixed assets (EUR) | 13,550 | 102,720 | 118,000 |

| Adjusted CF (EUR) | 2,691,101 | 2,115,453 | 1,982,500 |

| Year | Area of the Investment | Investment’s Costs | Lifetime | Significance of the Investment’s Outcome | Revenues from the Investment in 2012 | Revenues from the Investment in 2013 | Revenues from the Investment in 2014 |

|---|---|---|---|---|---|---|---|

| 2014 | IBM certification | 7710 | 3 | 5 | 58,868 | 55,454 | 14,869 |

| IT trends | 2415 | 4 | 3 | 35,321 | 33,273 | 8921 | |

| Together | 10,125 | - | 8 | 94,189 | 88,727 | 23,790 | |

| 2015 | Oracle | 10,915 | 4 | 5 | - | 26,722 | 26,444 |

| Java certification | 5400 | 3 | 5 | - | 26,722 | 26,446 | |

| SAP | 6,780 | 5 | 5 | - | 26,724 | 26,440 | |

| Web applications | 3,720 | 2 | 2 | - | 10,688 | 10,577 | |

| Language courses | 20,000 | - | 1 | - | 5344 | 5288 | |

| Together | 26,815 | - | 18 | - | 96,200 | 95,195 | |

| 2016 | ITIL Foundation certification | 1598 | 4 | 5 | - | - | 33,042 |

| PRINCE2 Foundationcertification | 3960 | 5 | 5 | - | - | 33,043 | |

| Web applications | 15,700 | 3 | 2 | - | - | 13,216 | |

| IT trends | 3572 | 2 | 2 | - | - | 13,216 | |

| Language courses | 24,000 | - | 1 | - | - | 6608 | |

| Together | 24,830 | - | 15 | - | - | 99,125 |

| Area of the Investment | 2015/2014 | 2016/2015 | 2017/2016 |

|---|---|---|---|

| IBM certification | 6.6 | 6.2 | 0.92 |

| IT trends | 13.63 | 12.78 | 2.7 |

| Oracle | – | 1.4 | 1.42 |

| Java certification | – | 3.9 | 3.9 |

| SAP | – | 2.9 | 2.9 |

| Web applications | – | 1.9 | 1.8 |

| Language courses | – | –0.7 | –0.74 |

| ITIL Foundation certification | – | - | 19.7 |

| PRINCE2 Foundation certification | – | - | 7.3 |

| Web applications | – | - | –0.2 |

| IT trends | – | - | 2.7 |

| Language courses | – | - | –0.7 |

| Year of Lifetime | Revenues | Discounting Rate | Discounted Revenues |

|---|---|---|---|

| 1. | 33,043 | 0.93 | 30,730 |

| 2. | 33,043 | 0.87 | 28,747 |

| 3. | 33,043 | 0.82 | 27,095 |

| 4. | 33,043 | 0.76 | 25,113 |

| 5. | 33,043 | 0.71 | 23,461 |

| Together | 165,215 | – | 135,146 |

| Negative Impacts | 2012 | 2013 | 2014 | 2015 | 2016 |

|---|---|---|---|---|---|

| Turnover | 0 | 0 | 1 | 0 | 2 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kucharčíková, A.; Mičiak, M.; Hitka, M. Evaluating the Effectiveness of Investment in Human Capital in E-Business Enterprise in the Context of Sustainability. Sustainability 2018, 10, 3211. https://doi.org/10.3390/su10093211

Kucharčíková A, Mičiak M, Hitka M. Evaluating the Effectiveness of Investment in Human Capital in E-Business Enterprise in the Context of Sustainability. Sustainability. 2018; 10(9):3211. https://doi.org/10.3390/su10093211

Chicago/Turabian StyleKucharčíková, Alžbeta, Martin Mičiak, and Miloš Hitka. 2018. "Evaluating the Effectiveness of Investment in Human Capital in E-Business Enterprise in the Context of Sustainability" Sustainability 10, no. 9: 3211. https://doi.org/10.3390/su10093211

APA StyleKucharčíková, A., Mičiak, M., & Hitka, M. (2018). Evaluating the Effectiveness of Investment in Human Capital in E-Business Enterprise in the Context of Sustainability. Sustainability, 10(9), 3211. https://doi.org/10.3390/su10093211