An Empirical Study on Internet Startup Financing From a Green Financial Perspective

Abstract

1. Introduction

2. Theoretical Analysis

2.1. Research on Crowdfunding

2.2. Research on the Backgrounds of Internet Entrepreneurs

2.3. The Uncertainty Avoidance Tendency in Entrepreneurs’ Cultural Background

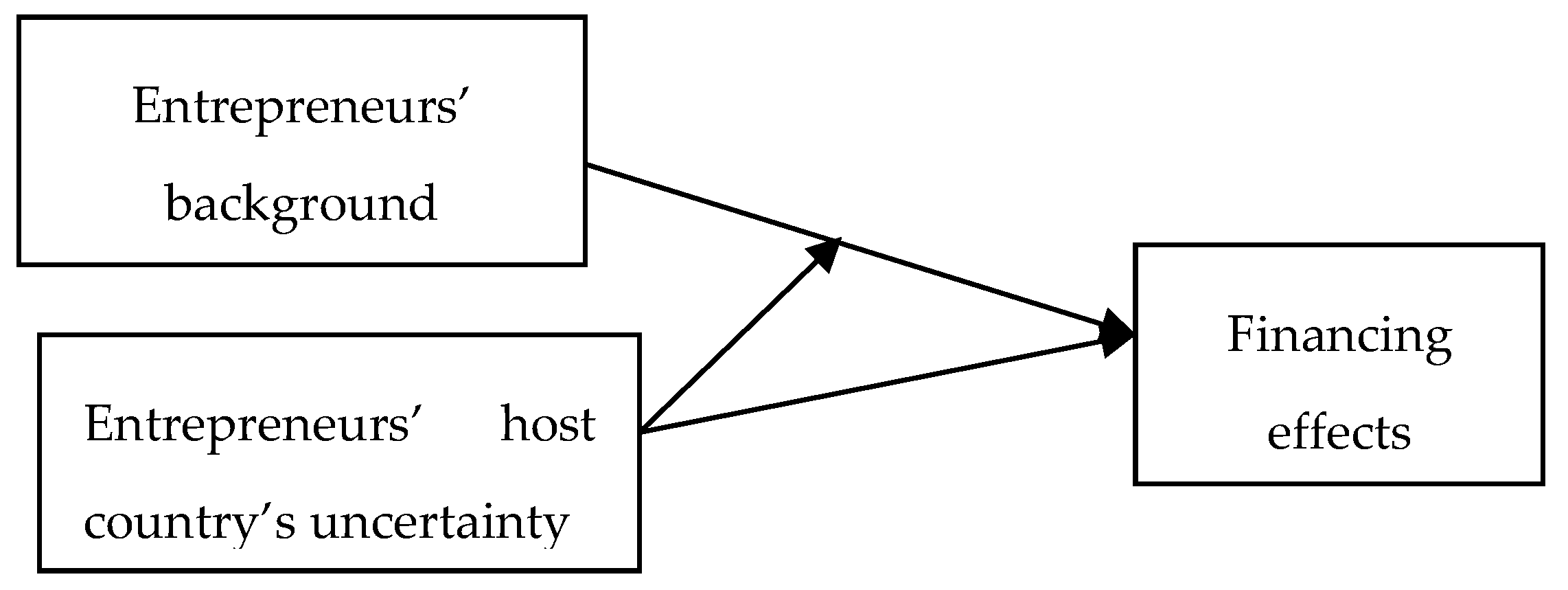

3. Research Hypotheses

3.1. Influence of Entrepreneurs’ Backgrounds on Financing Effect

3.2. Influence of Entrepreneur’s Host Country’s Uncertainty Avoidance on Financing Effects

3.3. Moderating Effects of Entrepreneurs’ Level of Uncertainty Avoidance on Financing Effects

4. Research Design

4.1. Data Collection

4.2. Variable Structures

4.2.1. Dependent Variables

4.2.2. Explanatory Variables

4.2.3. Moderating Variables

4.2.4. Control Variables

5. Findings and Discussion

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Khavul, S. Microfinance: Creating opportunities for the poor? Acad. Manag. Perspect. 2010, 24, 58–72. [Google Scholar] [CrossRef]

- Schwienbacher, A. The entrepreneur’s investor choice: The impact on later-stage firm development. J. Bus. Ventur. 2013, 28, 528–545. [Google Scholar] [CrossRef]

- Moenninghoff, S.C.; Wieandt, A. The future of peer-to-peer finance. Z. Betriebswirtsch. Forsch. 2013, 65, 466–487. [Google Scholar] [CrossRef]

- Lehner, O.M. Crowdfunding social ventures: A model and research agenda. Ventur. Cap. 2013, 15, 289–311. [Google Scholar] [CrossRef]

- Tomczak, A.; Brem, A. A conceptualized investment model of crowdfunding. Ventur. Cap. 2013, 15, 335–359. [Google Scholar] [CrossRef]

- Khavul, S.; Bruton, G.D.; Wood, E. Informal family business in Africa. Entrep. Theory Pract. 2009, 33, 1219–1238. [Google Scholar] [CrossRef]

- Khavul, S.; Chavez, H.; Bruton, G.D. When institutional change outruns the change agent: The contested terrain of entrepreneurial microfinance for those in poverty. J. Bus. Ventur. 2013, 28, 30–50. [Google Scholar] [CrossRef]

- Berger, A.N.; Saunders, A.; Scalise, J.M.; Udell, G.F. The effects of bank mergers and acquisitions on small business lending. J. Financ. Econ. 1998, 50, 187–229. [Google Scholar] [CrossRef]

- Bruton, G.; Khavul, S.; Siegel, D.; Wright, M. New Financial Alternatives in Seeding Entrepreneurship: Microfinance, Crowdfunding, and Peer-to-Peer Innovations. Entrep. Theory Pract. 2015, 39, 9–26. [Google Scholar] [CrossRef]

- Ordanini, A.; Miceli, L.; Pizzetti, M.; Parasuraman, A. Crowd-funding: Transforming customers into investors through innovative service platforms. J. Serv. Manag. 2011, 22, 443–470. [Google Scholar] [CrossRef]

- Belleflamme, P.; Lambert, T.; Schwienbacher, A. Crowdfunding: Tapping the right crowd. J. Bus. Ventur. 2014, 29, 585–609. [Google Scholar] [CrossRef]

- Gerber, E.M.; Hui, J.S.; Kuo, P.Y. Crowdfunding: Why people are motivated to post and fund projects on crowdfunding platforms. In Proceedings of the Computer Supported Cooperative Work 2012, Seattle, WA, USA, 11–15 February 2012. [Google Scholar]

- Storey, D.J.; Tether, B.S. New technology-based firms in the European Union: An introduction. Res. Policy 1998, 26, 933–946. [Google Scholar] [CrossRef]

- Hambrick, D.C.; Mason, P.A. Upper echelons: The organization as a reflection of its top managers. Acad. Manag. Rev. 1984, 9, 193–206. [Google Scholar] [CrossRef]

- Korsgaard, S. Entrepreneurship as translation: Understanding entrepreneurial opportunities through actor-network theory. Entrep. Reg. Dev. 2011, 23, 661–680. [Google Scholar] [CrossRef]

- Meyskens, M.; Paul, K. The evolution of corporate social reporting practices in Mexico. J. Bus. Ethics 2010, 91, 211–227. [Google Scholar] [CrossRef]

- Huckman, R.S.; Staats, B.R. Fluid tasks and fluid teams: The impact of diversity in experience and team familiarity on team performance. Manuf. Serv. Oper. Manag. 2011, 13, 310–328. [Google Scholar] [CrossRef]

- Van Osnabrugge, M. A comparison of business angel and venture capitalist investment procedures: An agency theory-based analysis. Ventur. Cap. 2000, 2, 91–109. [Google Scholar] [CrossRef]

- Pinto, F.; Simões, P.; Marques, R. Raising the bar: The role of governance in performance assessments. Util. Policy 2017, 49, 38–47. [Google Scholar] [CrossRef]

- Kirkman, B.L.; Lowe, K.B.; Gibson, C.B. A quarter century of culture’s consequences: A review of empirical research incorporating Hofstede’s cultural values framework. J. Int. Bus. Stud. 2006, 37, 285–320. [Google Scholar] [CrossRef]

- Gray, S.; Kang, T.; Yoo, Y. National culture and international differences in the cost of equity capital. Manag. Int. Rev. 2013, 53, 899–916. [Google Scholar] [CrossRef]

- Mu, R.; Geng, T. Cultural distance, network centrality and internet entrepreneurial financing—Empirical test based on crowdfunding data. J. Beijing Technol. Bus. Univ. Soc. Sci. 2017, 32, 94–103. [Google Scholar]

- Shane, S. Prior Knowledge and the Discovery of Entrepreneurial Opportunities. Organ. Sci. 2000, 11, 448–469. [Google Scholar] [CrossRef]

- Beckman, C.M.; Burton, M.D. Founding the Future: Path Dependence in the Evolution of Top Management Teams from Founding to IPO. Organ. Sci. 2008, 19, 3–24. [Google Scholar] [CrossRef]

- Zott, C.; Huy, Q.N. How entrepreneurs use symbolic management to acquire resources. Adm. Sci. Q. 2007, 52, 70–105. [Google Scholar] [CrossRef]

- Antarciuc, E.; Zhu, Q.; Almarri, J.; Zhao, S.; Feng, Y.; Agyemang, M. Sustainable Venture Capital Investments: An Enabler Investigation. Sustainability 2018, 10, 1204. [Google Scholar] [CrossRef]

- Mollick, E. The dynamics of crowdfunding: An exploratory study. J. Bus. Ventur. 2014, 29, 1–16. [Google Scholar] [CrossRef]

- Cooper, A.C.; Bruno, A.V. Success among high-technology firms. Bus. Horiz. 1977, 20, 16–22. [Google Scholar] [CrossRef]

- Stuart, R.W.; Abetti, P.A. Impact of entrepreneurial and management experience on early performance. J. Bus. Ventur. 1990, 5, 151–162. [Google Scholar] [CrossRef]

- Jo, H.; Lee, J. The relationship between an entrepreneur’s background and performance in a new ventur. Technovation 1996, 16, 161–211. [Google Scholar] [CrossRef]

- Ramayah, T.; Ahmad, N.H.; Fei, T.H.C. Entrepreneur education: Does prior experience matter? J. Entrep. Educ. 2012, 15, 65. [Google Scholar]

- Zimmerman, M.A. The Influence of Top Management Team Heterogeneity on the Capital Raised through an Initial Public Offering. Entrep. Theory Pract. 2008, 32, 391–414. [Google Scholar] [CrossRef]

- MacMillan, I.C.; Siegel, R.; Narasimha, P.N.S. Criteria used by venture capitalists to evaluate new venture proposals. J. Bus. Ventur. 1986, 1, 119–128. [Google Scholar] [CrossRef]

- Tyebjee, T.T.; Bruno, A.V. A model of venture capitalist investment activity. Manag. Sci. 1984, 30, 1051–1066. [Google Scholar] [CrossRef]

- Erez, M.; Earley, P.C. Culture, Self-Identity, and Work; Oxford University Press: Oxford, UK, 1993. [Google Scholar]

- Mueller, S.L.; Thomas, A.S. Culture and entrepreneurial potential: A nine country study of locus of control and innovativeness. J. Bus. Ventur. 2001, 16, 51–75. [Google Scholar] [CrossRef]

- Baughn, C.C.; Neupert, K.E. Culture and national conditions facilitating entrepreneurial start-ups. J. Int. Entrep. 2003, 1, 313–330. [Google Scholar] [CrossRef]

- Cooper, A.C.; Dunkelberg, W.C. Entrepreneurship and paths to business ownership. Strateg. Manag. J. 1986, 7, 53–68. [Google Scholar] [CrossRef]

- Hofstede, G. Motivation, leadership, and organization: Do American theories apply abroad? Organ. Dyn. 1980, 9, 42–63. [Google Scholar] [CrossRef]

- Hofstede, G. Culture’s Consequences: International Differences in Work-Related Values; Sage: Newcastle upon Tyne, UK, 1984. [Google Scholar]

- Lee, S.M.; Peterson, S.J. Culture, entrepreneurial orientation, and global competitiveness. J. World Bus. 2001, 35, 401–416. [Google Scholar] [CrossRef]

- Shane, S. Cultural influences on national rates of innovation. J. Bus. Ventur. 1993, 8, 59–73. [Google Scholar] [CrossRef]

- Busenitz, L.W.; Gomez, C.; Spencer, J.W. Country institutional profiles: Unlocking entrepreneurial phenomena. Acad. Manag. J. 2000, 43, 994–1003. [Google Scholar]

- Moon, Y.; Hwang, J. Crowdfunding as an Alternative Means for Funding Sustainable Appropriate Technology: Acceptance Determinants of Backers. Sustainability 2018, 10, 1456. [Google Scholar] [CrossRef]

- Shane, S. Uncertainty avoidance and the preference for innovation championing roles. J. Int. Bus. Stud. 1995, 26, 47–68. [Google Scholar] [CrossRef]

- Hoang, H.; Antoncic, B. Network-Based Research in Entrepreneurship: A Critical Review. J. Bus. Ventur. 2003, 18, 165–187. [Google Scholar] [CrossRef]

- Witt, P. Entrepreneurs’ Networks and the Success of Start-Ups. Entrep. Reg. Dev. 2004, 16, 391–412. [Google Scholar] [CrossRef]

- Kwak, H.; Lee, C.; Park, H.; Moon, S. What is Twitter, a social network or a news media? In Proceedings of the 19th international conference on World Wide Web, Raleigh, NC, USA, 26–30 April 2010; pp. 591–600. [Google Scholar]

- Tsai, S.-B. Using the DEMATEL Model to Explore the Job Satisfaction of Research and Development Professionals in China’s Photovoltaic Cell Industry. Renew. Sustain. Energy Rev. 2018, 81, 62–68. [Google Scholar] [CrossRef]

- Lee, Y.C.; Hsiao, Y.C.; Peng, C.F.; Tsai, S.B.; Wu, C.H.; Chen, Q. Using Mahalanobis-Taguchi System, Logistic Regression and Neural Network Method to Evaluate Purchasing Audit Quality. Proc. Inst. Mech. Eng. Part B J. Eng. Manuf. 2015, 229 (Suppl. 1), 3–12. [Google Scholar] [CrossRef]

- Lee, Y.C.; Chen, C.Y.; Tsai, S.B.; Wang, C.T. Discussing green environmental performance and competitive strategies. Pensee 2014, 76, 190–198. [Google Scholar]

- Liu, B.; Li, T.; Tsai, S.B. Low carbon strategy analysis of competing supply chains with different power structures. Sustainability 2017, 9, 835. [Google Scholar] [CrossRef]

- Qu, Q.; Tsai, S.B.; Tang, M.; Xu, C.; Dong, W. Marine ecological environment management based on ecological compensation mechanisms. Sustainability 2016, 8, 1267. [Google Scholar] [CrossRef]

- Lee, Y.C.; Wang, Y.C.; Chien, C.H.; Wu, C.H.; Lu, S.C.; Tsai, S.B.; Dong, W. Applying revised gap analysis model in measuring hotel service quality. SpringerPlus 2016, 5, 1191. [Google Scholar] [CrossRef] [PubMed]

- Wang, J.; Yang, J.M.; Chen, Q.; Tsai, S.B. Collaborative Production Structure of Knowledge Sharing Behavior in Internet Communities. Mob. Inf. Syst. 2016. [Google Scholar] [CrossRef]

- Tsai, S.B.; Lee, Y.C.; Guo, J.J. Using modified grey forecasting models to forecast the growth trends of green materials. Proc. Inst. Mech. Eng. Part B J. Eng. Manuf. 2014, 228, 931–940. [Google Scholar] [CrossRef]

- Tsai, S.B.; Zhou, J.; Gao, Y.; Wang, J.; Li, G.; Zheng, Y.; Ren, P.; Xu, W. Combining FMEA with DEMATEL Models to Solve Production Process Problems. PLoS ONE 2017, 12, e0167710. [Google Scholar] [CrossRef] [PubMed]

- Ge, B.; Jiang, D.; Gao, Y.; Tsai, S.B. The influence of legitimacy on a proactive green orientation and green performance: A study based on transitional economy scenarios in china. Sustainability 2016, 8, 1344. [Google Scholar] [CrossRef]

- Lee, S.C.; Su, J.M.; Tsai, S.B.; Lu, T.L.; Dong, W. A comprehensive survey of government auditors’ self-efficacy and professional Development for improving audit quality. SpringerPlus 2016, 5, 1263. [Google Scholar] [CrossRef] [PubMed]

- Chen, H.M.; Wu, C.H.; Tsai, S.B.; Yu, J.; Wang, J.; Zheng, Y. Exploring key factors in online shopping with a hybrid model. SpringerPlus 2016, 5, 2046. [Google Scholar] [CrossRef] [PubMed]

- Lee, Y.C.; Wang, Y.C.; Lu, S.C.; Hsieh, Y.F.; Chien, C.H.; Tsai, S.B.; Dong, W. An empirical research on customer satisfaction study: A consideration of different levels of performance. SpringerPlus 2016, 5, 1577. [Google Scholar] [CrossRef] [PubMed]

- Wang, J.; Yang, J.; Chen, Q.; Tsai, S.B. Creating the sustainable conditions for knowledge information sharing in virtual community. SpringerPlus 2016, 5, 1019. [Google Scholar] [CrossRef] [PubMed]

- Schwienbacher, A.; Larralde, B. Crowdfunding of small entrepreneurial ventures. In Handbook of Entrepreneurial Finance; Oxford University Press: Oxford, UK, 2010; Forthcoming. [Google Scholar]

- VanderWerf, P.A.; Mahon, J.F. Meta-analysis of the impact of research methods on findings of first-mover advantage. Manag. Sci. 1997, 43, 1510–1519. [Google Scholar] [CrossRef]

{kind=link}

| Mean | s.d. | Min | Max. | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. Financing Proportion | 2.549 | 2.105 | 0 | 27.86 | 1 | ||||||||

| 2. Uncertainty Avoidance | 51.019 | 5.179 | 29 | 92 | −0.106 | 1 | |||||||

| 3. Technical Education Backgrounds | 2.017 | 0.75 | 0 | 6 | 0.413 *** | −0.094 ** | 1 | ||||||

| 4. Marketing Education Backgrounds | 2.185 | 1.651 | 0 | 9 | 0.305 *** | −0.075 ** | 0.318 *** | 1 | |||||

| 5. Online Entrepreneurial Experience | 1.873 | 0.758 | 0 | 5 | 0.238 *** | 0.013 | 0.005 | 0.258 *** | 1 | ||||

| 6. Offline Entrepreneurial Experience | 1.56 | 1.479 | 0 | 6 | 0.351 ** | −0.065 ** | 0.103 ** | 0.095 | 0.270 *** | 1 | |||

| 7. Financing Goal | 3.604 | 3.792 | 0.5 | 25 | −0.184 *** | 0.151 | 0.101 ** | 0.014 | 0.038 * | 0.015 | 1 | ||

| 8. Financing Time Limitation | 26.15 | 7.091 | 10 | 90 | 0.241 *** | 0.261 * | 0.002 | 0.419 | 0.149 * | 0.13 | 0.148 *** | 1 | |

| 9. SNS Recognition | 27.801 | 84.589 | 0 | 791 | 0.414 *** | 0.195 *** | 0.491 *** | 0.210 ** | 0.264 *** | 0.419 *** | 0.172 | 0.079 | 1 |

| 10. Technical Dummy Variables | 0.571 | 0.406 | 0 | 1 | 0.145 ** | 0.208 | 0.213 ** | 0.194 *** | 0.079 ** | 0.185 | 0.015 *** | 0.104 * | 0.231 ** |

| Model 1 | Model 2 | Model 3 | |

|---|---|---|---|

| Uncertainty Avoidance × Technical Educational Backgrounds | −0.002 (0.003) | ||

| Uncertainty Avoidance × Marketing Educational Backgrounds | −0.001 (0.001) | ||

| Uncertainty Avoidance × Online Entrepreneurial Experiences | −0.013 *** (0.001) | ||

| Uncertainty Avoidance × Offline Entrepreneurial Experiences | −0.008 *** (3.14 × 10−5) | ||

| Uncertainty Avoidance | −0.017 (0.035) | −0.015 (0.027) | |

| Technical Educational Backgrounds | 0.237 *** (0.010) | 0.220 *** 0.008 | |

| Marketing Educational Backgrounds | 0.079* (0.038) | 0.085 (0.096) | |

| Online Entrepreneurial Experiences | 0.169 *** (0.009) | 0.172 *** (0.010) | |

| Offline Entrepreneurial Experiences | 0.095 ** (0.011) | 0.105 *** (0.028) | |

| Financing Goal | −0.115 *** (0.006) | −0.127 *** (0.007) | -0.084 *** (0.003) |

| Financing Time Limitation | 0.048 *** (7.89 × 10−4) | 0.011 *** (3.10 × 10−4) | 0.009 *** (1.81 × 10−4) |

| SNS Recognition | 0.004 *** (1.80 × 10−4) | 0.001 *** (1.80 × 10−5) | 0.001 *** (1.80 × 10−5) |

| Technical Dummy Variables | 0.379 *** (0.026) | 0.121 *** (0.005) | 0.116 *** (0.006) |

| Host Country Dummy Variables | Included | Included | Included |

| R-sq | 0.315 | 0.521 | 0.516 |

| F | 88.23 | 195.68 | 187.56 |

| Numbers of Observations | 423 | 423 | 423 |

| Hypothesis | Result | |

|---|---|---|

| Hypothesis 1a | Entrepreneur’s background of technological education has a positive effect on Internet financing. | support |

| Hypothesis 1b | Entrepreneur’s background of marketing education has a positive effect on Internet financing. | |

| Hypothesis 1c | Entrepreneur’s offline entrepreneurial experience has a positive effect on Internet financing. | support |

| Hypothesis 1d | Entrepreneur’s online entrepreneurial experience has a positive effect on Internet financing. | support |

| Hypothesis 2 | The lower the uncertainty avoidance of the entrepreneurs’ host country is, the stronger the promotion on Internet financing is. | |

| Hypothesis 3a | The lower the value of uncertainty avoidance in cultures of the entrepreneurial leaders’ host countries, the stronger the promotion of technical educational backgrounds on Internet financing is. | |

| Hypothesis 3b | The lower the value of uncertainty avoidance in cultures of entrepreneurial leaders’ host countries is, the stronger the promotion of marketing educational backgrounds on Internet financing is. | |

| Hypothesis 3c | The lower the value of uncertainty avoidance in cultures of the entrepreneurial leaders’ host countries is, the stronger the function of offline entrepreneurial experience on Internet financing is. | support |

| Hypothesis 3d | The lower the value of uncertainty avoidance in cultures of the entrepreneurial leaders’ host countries is, the stronger the function of online entrepreneurial experience on Internet financing is. | support |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yan, Z.; Wang, K.; Tsai, S.-B.; Zhou, L. An Empirical Study on Internet Startup Financing From a Green Financial Perspective. Sustainability 2018, 10, 2912. https://doi.org/10.3390/su10082912

Yan Z, Wang K, Tsai S-B, Zhou L. An Empirical Study on Internet Startup Financing From a Green Financial Perspective. Sustainability. 2018; 10(8):2912. https://doi.org/10.3390/su10082912

Chicago/Turabian StyleYan, Zichun, Kai Wang, Sang-Bing Tsai, and Lili Zhou. 2018. "An Empirical Study on Internet Startup Financing From a Green Financial Perspective" Sustainability 10, no. 8: 2912. https://doi.org/10.3390/su10082912

APA StyleYan, Z., Wang, K., Tsai, S.-B., & Zhou, L. (2018). An Empirical Study on Internet Startup Financing From a Green Financial Perspective. Sustainability, 10(8), 2912. https://doi.org/10.3390/su10082912