Current Trends in Research on Social Responsibility in State-Owned Enterprises: A Review of the Literature from 2000 to 2017

Abstract

1. Introduction

2. The Relevance of CSR in SOEs

3. Methods

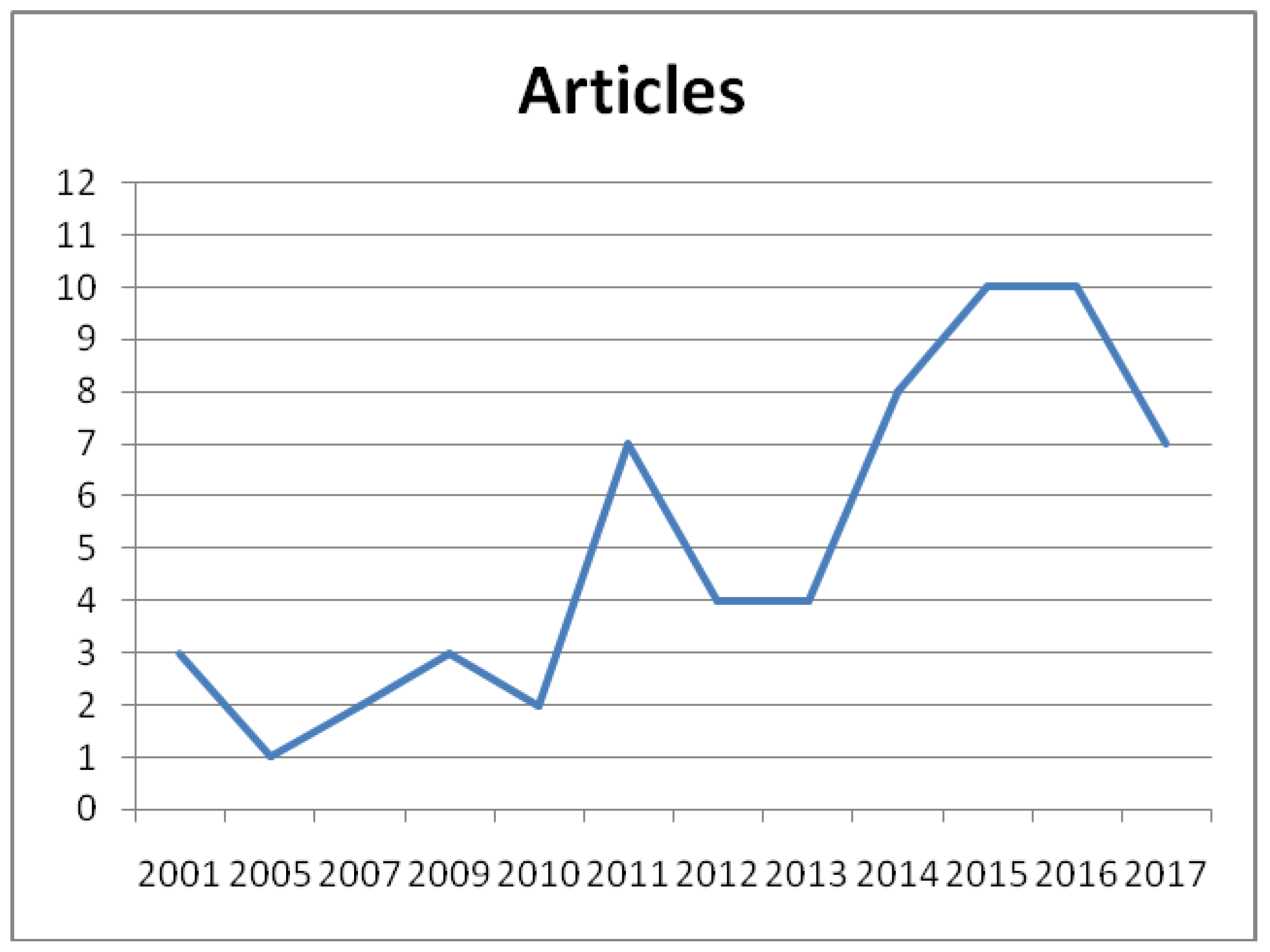

3.1. Scope of the Review

3.2. Screening Process

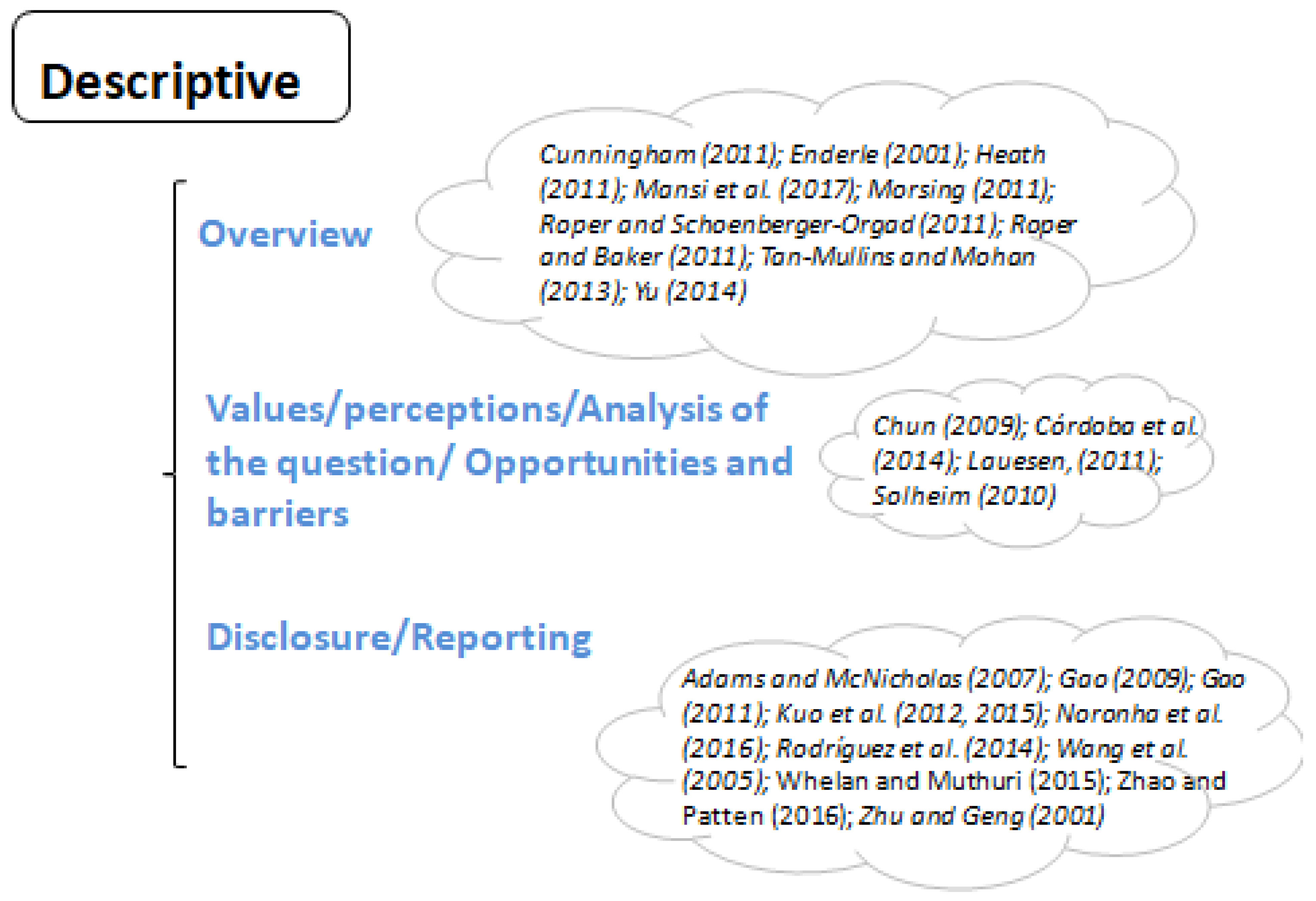

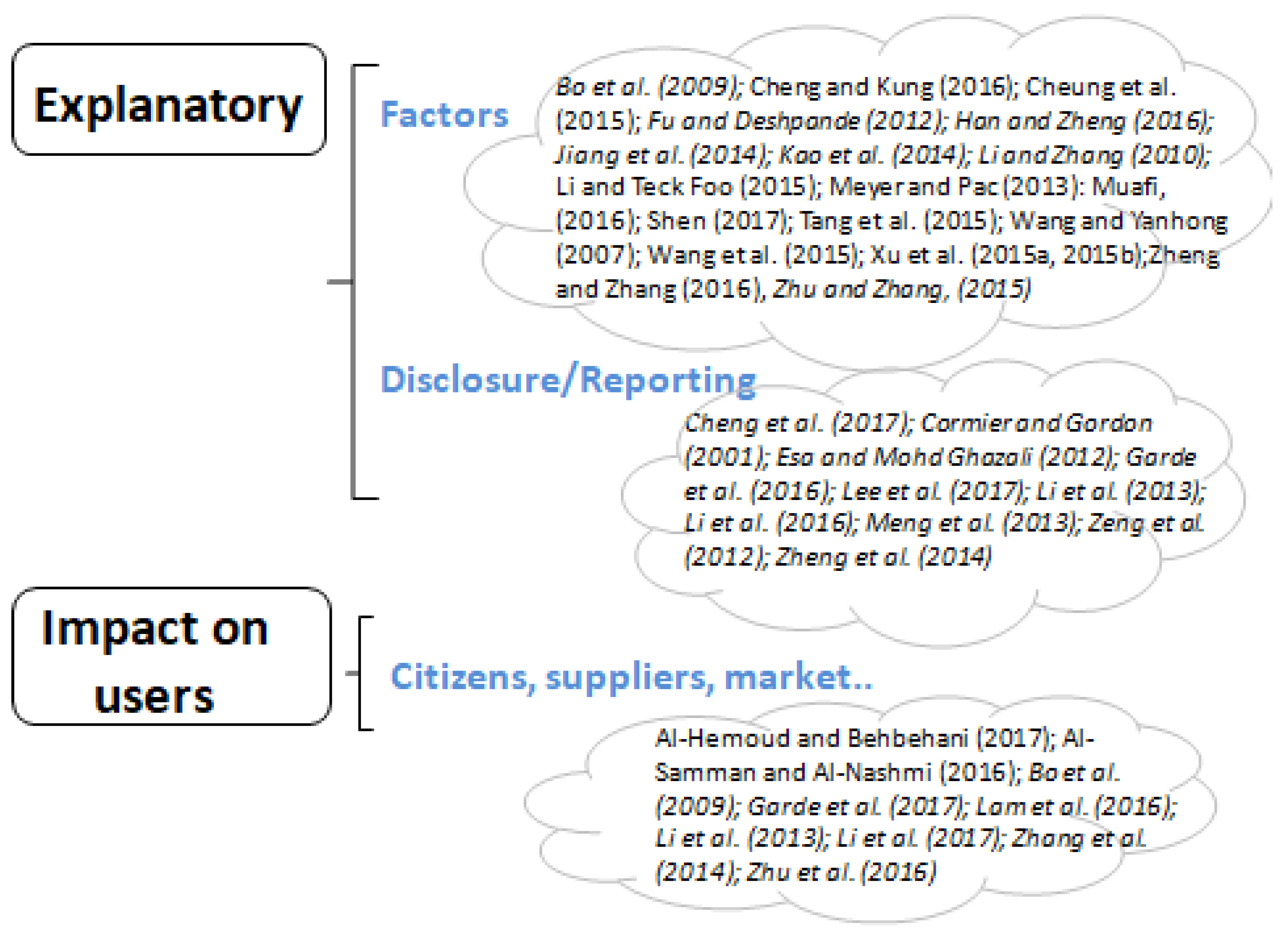

4. Research into CSR in State-Owned Enterprises

5. Theoretical Approaches to Justify CSR in SOEs

6. The Practice of Corporate Social Responsibility in State Owned Enterprises

7. Discussion and Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Bowen, H.R. Social Responsibilities of the Business Man; Harper & Row: New York, NY, USA, 1953. [Google Scholar]

- World Commission on Environment and Development. Our Common Future; Brundtland Report; Oxford University Press: Oxford, UK, 1987. [Google Scholar]

- European Commission. Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions: A renewed EU strategy 2011–14 for Corporate Social Responsibility; Commission of the European Communities; European Commission: Brussels, Belgium, 2011. [Google Scholar]

- Ball, A.; Grubnic, S. Sustainability accounting and accountability in the public sector. In Sustainability Accounting and Accountability; Unerman, J., Bebbington, J., O’Dwyer, B., Eds.; Routledge: London, UK, 2007; pp. 243–265. [Google Scholar]

- Ball, A.; Bebbington, J. Editorial: Accounting and reporting for sustainable development in public service organizations. Public Money Manag. 2008, 28, 323–326. [Google Scholar] [CrossRef]

- Roper, J.; Schoenberger-Orgad, M. State-owned enterprises: Issues of accountability and legitimacy. Manag. Commun. Q. 2011, 25, 693–709. [Google Scholar] [CrossRef]

- Rocheleau, B.; Wu, L. Public versus private information systems: Do they differ in important ways? A review and empirical test. Am. Rev. Public Adm. 2002, 32, 349–397. [Google Scholar] [CrossRef]

- Piotrowski, S.J.; Van Ryzing, G.G. Citizen attitudes toward transparency in local government. Am. Rev. Public Adm. 2007, 37, 306–323. [Google Scholar] [CrossRef]

- Reich, R.B. The new meaning of corporate social responsibility. Calif. Manag. Rev. 1998, 40, 8–17. [Google Scholar]

- Peterson, R.T. Small business manager attitudes relating to the significance of social responsibility issues: A longitudinal study. J. Appl. Manag. Entrepreneurship 2006, 11, 32–50. [Google Scholar]

- Margolis, J.; Walsh, J. People and Profits? The Search for a Link between a Company’s Social and Financial Performance; Lawrence Erlbaum: Mahwah, NJ, USA, 2001. [Google Scholar]

- Chen, C.; Tsai, D. How do destination image and evaluative factors affect behavioral intentions? Tour. Manag. 2007, 28, 1115–1122. [Google Scholar] [CrossRef]

- Deegan, C.; Rankin, M.; Tobin, J. An examination of the corporate social and environmental disclosures of BHP from 1983–1997: A test of legitimacy theory. Account. Audit. Account. J. 2002, 15, 312–343. [Google Scholar] [CrossRef]

- Deephouse, D.L.; Carter, S.M. An examination of differences between organizational legitimacy and organizational reputation. J. Manag. Stud. 2005, 42, 329–360. [Google Scholar] [CrossRef]

- Garde Sánchez, R.; Rodríguez Bolívar, M.P.; López-Hernández, A.M. Online disclosure of university social responsibility: A comparative study of public and private US universities. Environ. Educ. Res. 2013, 19, 709–746. [Google Scholar] [CrossRef]

- Garde Sánchez, R.; Rodríguez Bolívar, M.P.; López-Hernández, A.M. Divulgación online de información de responsabilidad social en lasuniversidadesespañolas. Rev. Educ. Número Extraordin. 2013, 1–24. [Google Scholar] [CrossRef]

- Rodríguez Bolívar, M.P.; Garde Sánchez, R.; López Hernández, A.M. Online disclosure of corporate social responsibility information in leading Anglo-American Universities. J. Environ. Policy Plan. 2013, 15, 551–575. [Google Scholar] [CrossRef]

- Córdoba Pachón, J.R.; Garde Sánchez, R.; Rodríguez Bolívar, M.P. A systemic view of corporate social responsibility (CSR) in state-owned enterprises (SOEs). Knowl. Process Manag. 2014, 21, 206–219. [Google Scholar] [CrossRef]

- Rodríguez Bolívar, M.P.; Garde Sánchez, R.; López Hernández, A.M. Managers as drivers of CSR in state-owned enterprises. J. Environ. Plan. Manag. 2014, 58, 777–801. [Google Scholar] [CrossRef]

- Heath, J.; Norman, W. Stakeholder theory, corporate governance and public management: What can the history of state-run enterprises teach us in the post-Enron era? J. Bus. Ethics 2004, 53, 247–265. [Google Scholar] [CrossRef]

- Cunningham, M. State-owned enterprises: Pursuing responsibility in corporate social responsibility. Manag. Commun. Q. 2011, 25, 718–724. [Google Scholar] [CrossRef]

- Reverte, C. Determinants of Corporate Social Responsibility Disclosure Ratings by Spanish Listed Firms. J. Bus. Ethics 2009, 88, 351–366. [Google Scholar] [CrossRef]

- Maon, F.; Lindgreen, A.; Swaen, V. Organizational stages and cultural phases: A critical review and a consolidative model of corporate social responsibility development. Int. J. Manag. Rev. 2010, 12, 20–38. [Google Scholar] [CrossRef]

- Wilson, D.; Game, C. Local Government in the United Kingdom; Palgrave: Basingstoke, UK, 2011. [Google Scholar]

- Jones, G.; Stewart, J. New development: Accountability in public partnerships-the case of local strategic partnerships. Public Money Manag. 2009, 29, 59–64. [Google Scholar] [CrossRef]

- OECD. Guidelines on Corporate Governance of State-Owned Enterprises; OECD: Paris, France, 2005; ISBN 92-64-00942-6. [Google Scholar]

- Dewenter, K.L.; Malatesta, P.H. State-owned and privately owned firms: An empirical analysis of profitability, leverage and labor intensity. Am. Econ. Rev. 2001, 91, 320–334. [Google Scholar] [CrossRef]

- OECD. The Size and Composition of the SOE Sector in OECD Countries, Corporate Governance Working Papers, No.5; OECD: Paris, France, 2011; Available online: http:// www.oecd.org/daf/corporateaffairs/wp (accessed on 30 June 2018).

- Tranfield, D.; Denyer, D.; Smart, P. Towards a methodology for developing evidence-informed management knowledge by means of systematic review. Br. J. Manag. 2003, 14, 207–222. [Google Scholar] [CrossRef]

- Rousseau, D.; Manning, J.; Denyer, D. Evidence in management and organizational science: Assembling the field’s full weight of scientific knowledge through syntheses. Acad. Manag. Ann. 2008, 2, 475–515. [Google Scholar] [CrossRef]

- Baumann, H.; Boons, F.; Bragd, A. Mapping the green product development field: Engineering, policy and business perspectives. J. Clean. Prod. 2002, 10, 409–425. [Google Scholar] [CrossRef]

- Kitchenham, B.; Brereton, O.; Budgen, D.; Turner, M.; Bailey, J.; Linkman, S. Systematic literature reviews in software engineering: A systematic literature review. Inf. Softw. Technol. 2009, 51, 7–15. [Google Scholar] [CrossRef]

- De Bellis, N. Bibliometrics and Citation Analysis: From the Science Citation Index to Cybermetrics; The Scarecrow Press, Inc.: Lanham, MD, USA, 2009. [Google Scholar]

- Stallings, R.A.; Ferris, J.M. Public administration research: Work in PAR, 1940–1984. Public Adm. Rev. 1988, 48, 580–587. [Google Scholar] [CrossRef]

- Pina Martínez, V.; Torres Pradas, L. Evaluación del rendimientos de los Departamentos de Contabilidad de lasUniversidadesEspañolas. Hacienda Pública Esp. 1995, 135, 183–190. [Google Scholar]

- Legge, J.S.; Devore, J. Measuring productivity in U.S. public administration and public affairs programs 1981–1985. Adm. Soc. 1987, 19, 147–156. [Google Scholar] [CrossRef]

- Organization for Economic Cooperation and Development. OECD Principles of Corporate Governance; Organization for Economic Cooperation and Development: Paris, France, 2004. [Google Scholar]

- Barki, H.; Rivard, S.; Talbot, J. An information systems keyword classification scheme. MIS Q. 1998, 12, 299–322. [Google Scholar] [CrossRef]

- Lan, Z.; Anders, K.K. A paradigmatic view of contemporary public administration research: An empirical test. Adm. Soc. 2000, 32, 138–165. [Google Scholar] [CrossRef]

- Plümber, T.; Radaelli, C.M. Publish or perish? Publications and citations of Italian scientists in international political science journals, 1990–2002. J. Eur. Public Policy 2004, 11, 1112–1127. [Google Scholar] [CrossRef]

- Adams, C.A.; McNicholas, P. Making a difference. Sustainability reporting, accountability and organisational change. Account. Audit. Account. J. 2007, 20, 382–402. [Google Scholar] [CrossRef]

- Al-Hemoud, A.; Behbehani, W. Workplace environmental demands and energizers at two Kuwait oil companies. Int. J. Environ. Sci. Technol. 2017, 14, 983–992. [Google Scholar] [CrossRef]

- Al-Samman, E.; Al-Nashmi, M.M. Effect of corporate social responsibility on nonfinancial organizational performance: Evidence from Yemeni for-profit public and private enterprises. Soc. Responsib. J. 2016, 21, 247–262. [Google Scholar] [CrossRef]

- Bo, H.; Li, T.; Toolsema, L.A. Corporate social responsibility investment and social objectives: An examination on social welfare investment of Chinese state owned enterprises. Scott. J. Polit. Econ. 2009, 56, 267–295. [Google Scholar] [CrossRef]

- Cheng, C.L.; Kung, F.H. The effects of mandatory corporate social responsibility policy on accounting conservatism. Rev. Account. Financ. 2016, 15, 2–20. [Google Scholar] [CrossRef]

- Cheng, Z.; Wang, F.; Keung, C.; Bai, Y. Will Corporate Political Connection Influence the Environmental Information Disclosure Level? Based on the Panel Data of A-Shares from Listed Companies in Shanghai Stock Market. J. Bus. Ethics 2017, 143, 209–221. [Google Scholar] [CrossRef]

- Cheung, Y.L.; Kong, D.; Tan, W.; Wang, W. Being Good When Being International in an Emerging Economy: The Case of China. J. Bus. Ethics 2015, 130, 805–817. [Google Scholar] [CrossRef]

- Chun, R. Ethical values and environmentalism in China: Comparing employees from state-owned and private firms. J. Bus. Ethics 2009, 84, 341–348. [Google Scholar] [CrossRef]

- Cormier, D.; Gordon, I.M. An examination of social and environmental reporting strategies. Account. Audit. Account. J. 2001, 14, 587–617. [Google Scholar] [CrossRef]

- Enderle, G. Integrating the ethical dimension into the analytical framework for the reform of state-owned enterprises in China’s socialist market economy: A proposal. J. Bus. Ethics 2001, 30, 261–276. [Google Scholar] [CrossRef]

- Esa, E.; MohdGhazali, N.A. Corporate social responsibility and corporate governance in Malaysian government-linked companies. Corp. Gov. 2012, 12, 292–305. [Google Scholar] [CrossRef]

- Fu, W.; Deshpande, S.P. Factors impacting ethical behavior in a Chinese state-owned steel company. J. Bus. Ethics 2012, 105, 231–237. [Google Scholar] [CrossRef]

- Gao, Y. Corporate Social Performance in China: Evidence from Large Companies. J. Bus. Ethics 2009, 89, 23–35. [Google Scholar] [CrossRef]

- Gao, Y. CSR in an emerging country: A content analysis of CSR reports of listed companies. Balt. J. Manag. 2011, 6, 263–291. [Google Scholar] [CrossRef]

- Garde Sánchez, R.; Rodríguez Bolívar, M.P.; López-Hernández, A.M. Corporate and managerial characteristics as drivers of social responsibility disclosure by state-owned enterprises. Rev. Manag. Sci. 2016, 11, 633–659. [Google Scholar] [CrossRef]

- Garde Sánchez, R.; Rodríguez Bolívar, M.P.; López-Hernández, A.M. Perceptions of stakeholder pressure for supply-chain social responsibility and information disclosure by state-owned enterprises. Int. J. Logist. Manag. 2017, 28, 1027–1053. [Google Scholar] [CrossRef]

- Han, Y.; Zheng, E. Why Firms Perform Differently in Corporate Social Responsibility? Firm Ownership and the Persistence of Organizational Imprints. Manag. Organ. Rev. 2016, 12, 605–629. [Google Scholar] [CrossRef]

- Heath, J. State-owned enterprises: CSR solution or just another bump in the road. Manag. Commun. Q. 2011, 25, 725–731. [Google Scholar] [CrossRef]

- Jiang, L.; Lin, C.; Lin, P. The determinants of pollution levels: Firm-level evidence from Chinese manufacturing. J. Comp. Econ. 2014, 42, 118–142. [Google Scholar] [CrossRef]

- Kao, E.H.; Hung-Gay, F.; Qingdi, L. What Explains Corporate Social Responsibility Engagement in Chinese Firms? Chin. Econ. 2014, 47, 50–80. [Google Scholar]

- Kuo, L.; Yeh, C.; Yu, H.C. Disclosure of Corporate Social Responsibility and Environmental Management: Evidence from China. Int. J. Bus. Soc. 2012, 19, 273–287. [Google Scholar] [CrossRef]

- Kuo, L.; Yu, H.C.; Chang, B.G. The signals of green governance on mitigation of climate change—Evidence from Chinese firms. Int. J. Clim. Chang. Strateg. Manag. 2015, 7, 154–171. [Google Scholar] [CrossRef]

- Lam, K.S.; Yeung, C.L.; Cheng, T.C.E.; Humphreys, P.K. Corporate environmental initiatives in the Chinese context: Performance implications and contextual factor. Int. J. Prod. Econ. 2016, 180, 48–56. [Google Scholar] [CrossRef]

- Lauesen, L.M. CSR in publicly owned enterprises: Opportunities and barriers. Soc. Responsib. J. 2011, 7, 558–577. [Google Scholar] [CrossRef]

- Lee, E.; Walker, M.; Zeng, C. Do Chinese state subsidies affect voluntary corporate social responsibility disclosure? J. Account. Public Policy 2017, 36, 179–200. [Google Scholar] [CrossRef]

- Li, C.K.; Luo, J.; Soderstrom, N.S. Market response to expected regulatory costs related to haze. J. Account. Public Policy 2017, 36, 201–219. [Google Scholar] [CrossRef]

- Li, Q.; Luo, W.; Wang, Y.; Wu, L. Firm performance, corporate ownership, and corporate social responsibility disclosure in China. Bus. Ethics 2013, 22, 159–173. [Google Scholar] [CrossRef]

- Li, W.; Zhang, R. Corporate social responsibility, ownership structure, and political interference: Evidence from China. J. Bus. Ethics 2010, 96, 631–645. [Google Scholar] [CrossRef]

- Li, Y.; Teck Foo, C. A sociological theory of corporate finance: Societal responsibility and cost of equity in China. Chin. Manag. Stud. 2015, 9, 269–294. [Google Scholar] [CrossRef]

- Li, D.; Xin, L.; Sun, Y.; Huang, M.; Ren, S. Assessing Environmental Information Disclosures and the Effects of Chinese Nonferrous Metal Companies. Polish J. Environ. Stud. 2016, 25, 663–671. [Google Scholar] [CrossRef]

- Mansi, M.; Pandey, R.; Ghauri, E. CSR focus in the mission and vision statements of public sector enterprises: Evidence from India. Manag. Audit. J. 2017, 32, 356–377. [Google Scholar] [CrossRef]

- Meng, X.H.; Zeng, S.X.; Tam, C.M. From Voluntarism to Regulation: A Study on Ownership, Economic Performance and Corporate Environmental Information Disclosure in China. J. Bus. Ethics 2013, 116, 217–232. [Google Scholar] [CrossRef]

- Meyer, A.; Pac, G. Environmental performance of state-owned and privatized eastern European energy utilities. Energy Econ. 2013, 36, 205–214. [Google Scholar] [CrossRef]

- Morsing, M. State-owned enterprises: A corporatization of governments? Manag. Commun. Q. 2011, 25, 710–717. [Google Scholar] [CrossRef]

- Muafi, M. Analyzing Fit in CSR Strategy Research in State-Owned Enterprises: Indonesia Context. J. Ind. Eng. Manag. 2016, 9, 179–206. [Google Scholar]

- Noronha, C.; Leung, T.C.H.; Lei, O.L. Corporate social responsibility disclosure in Chinese railway companies: Corporate response after a major train accident. Sustain. Account. Manag. Policy J. 2015, 6, 446–474. [Google Scholar] [CrossRef]

- Roper, J.; Barker, J.R. Forum Introduction: State-owned enterprises, corporate social responsibility, and organizational communication. Manag. Commun. Q. 2011, 25, 690–692. [Google Scholar] [CrossRef]

- Shen, W. Who drives China’s renewable energy policies? Understanding the role of industrial corporations. Environ. Dev. 2017, 21, 87–97. [Google Scholar] [CrossRef]

- Solheim, L.Y. Inclusive working life and value conflict in Norway. Int. J. Sociol. Soc. Policy 2010, 30, 399–411. [Google Scholar] [CrossRef]

- Tang, S.; Li, P.H.; Fryxell, G.E.; Lo, C.W. Enterprise-Level Motivations, Regulatory Pressures, and Corporate Environmental Management in Guangzhou, China. Environ. Manag. 2015, 56, 777–790. [Google Scholar] [CrossRef] [PubMed]

- Tan-Mullins, M.; Mohan, G. The potential of corporate environmental responsibility of Chinese state-owned enterprises in Africa. Environ. Dev. Sustain. 2013, 5, 265–284. [Google Scholar] [CrossRef]

- Wang, H.; Yanhong, J. Industrial Ownership and Environmental Performance: Evidence from China. Environ. Resour. Econ. 2007, 36, 255–273. [Google Scholar] [CrossRef]

- Wang, S.; Huang, W.; Gao, Y.; Ansett, S.; Xu, S. Can socially responsible leaders drive Chinese firm performance? Leadersh. Organ. Dev. J. 2015, 36, 435–450. [Google Scholar] [CrossRef]

- Wang, Y.; Wang, Y.; Bramley, G. Chinese housing reform in state owned enterprises and its impacts on different social groups. Urban Stud. 2005, 42, 1859–1878. [Google Scholar] [CrossRef]

- Whelan, G.; Muthuri, J. Chinese State-Owned Enterprises and Human Rights: The Importance of National and Intra-Organizational Pressures. Bus. Soc. 2015, 56, 738–781. [Google Scholar] [CrossRef]

- Xu, E.; Yang, H.; Quan, J.M.; Lu, Y. Organizational slack and corporate social performance: Empirical evidence from China’s public firms. Asia Pac. J. Manag. 2015, 32, 181–198. [Google Scholar] [CrossRef]

- Xu, S.; Liu, D.; Huang, J. Corporate social responsibility, the cost of equity capital and ownership structure: An analysis of Chinese listed firms China. J. Manag. 2015, 40, 245–276. [Google Scholar]

- Yu, S. The impact of corporate governance of state-owned enterprises on social responsibility activities. J. Bus. Resear. 2014, 67, 2768–2776. [Google Scholar]

- Zeng, S.; Xu, X.; Yin, H.; Tam, C. Factors that Drive Chinese Listed Companies in Voluntary Disclosure of Environmental Information. J. Bus. Ethics 2012, 109, 309–321. [Google Scholar] [CrossRef]

- Zhang, M.; Ma, L.; Su, J.; Zhang, W. Do suppliers applaud corporate social performance? J. Bus. Ethics 2014, 121, 543–557. [Google Scholar] [CrossRef]

- Zhao, N.; Patten, D.M. An exploratory analysis of managerial perceptions of social and environmental reporting in China: Evidence from state-owned enterprises in Beijing. Sustain. Account. Manag. Policy J. 2016, 7, 80–98. [Google Scholar] [CrossRef]

- Zheng, H.; Zhang, Y. Do SOEs outperform private enterprises in CSR? Evidence from China. Chin. Manag. Stud. 2016, 10, 435–457. [Google Scholar] [CrossRef]

- Zheng, L.; Balsara, N.; Huang, H. Regulatory pressure, blockholders and corporate social responsibility (CSR) disclosures in China. Soc. Responsib. J. 2014, 10, 226–245. [Google Scholar] [CrossRef]

- Zhu, Q.; Geng, Y. Integrating Environmental Issues into Supplier Selection and Management. Greener Manag. Int. 2001, 35, 27–40. [Google Scholar] [CrossRef]

- Zhu, Q.; Liu, J.; Lai, K. Corporate social responsibility practices and performance improvement among Chinese national state-owned enterprises. Int. J. Econ. Prod. 2016, 171, 417–426. [Google Scholar] [CrossRef]

- Zhu, Q.; Zhang, Q. Evaluating practices and drivers of corporate social responsibility: The Chinese context. J. Clean. Prod. 2015, 100, 315–324. [Google Scholar] [CrossRef]

- Roper, J.; Weymes, E. Reinstating the collective: A Confucian approach to well-being and social capital development in a globalised economy. J. Corp. Citizsh. 2007, 26, 135–144. [Google Scholar] [CrossRef]

- Goetzmann, W.; Koll, E. The History of Corporate Ownership in China: State Patronage, Company Legislation, and the Issue of Control; National Bureau of Economic Research: Cambridge, MA, USA, 2004. [Google Scholar]

- McWilliams, A.; Siegel, D. Corporate social responsibility: A theory of the firm perspective. Acad. Manag. Rev. 2001, 26, 117–127. [Google Scholar] [CrossRef]

- Doh, J.P.; Guay, T.R. Corporate social responsibility, public policy, and NGO activism in Europe and the United States: An institutional-stakeholder perspective. J. Manag. Stud. 2006, 43, 47–73. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Pitman Press: Boston, MA, USA, 1984. [Google Scholar]

- Pedersen, E.R.; Neergaard, P. What matters to managers? The whats, whys, and hows of corporate social responsibility in a multinational corporation. Manag. Decis. 2009, 47, 1261–1280. [Google Scholar] [CrossRef]

- Clarkson, M.B.E. A stakeholder framework for analyzing and evaluating corporate social performance. Acad. Manag. Rev. 1995, 20, 92–116. [Google Scholar] [CrossRef]

- Donaldson, T.; Preston, L. The stakeholder theory of the modern corporation: Concepts, evidence and implications. Acad. Manag. Rev. 1995, 20, 65–91. [Google Scholar] [CrossRef]

- Pedersen, E.R. Making corporate social responsibility (CSR) operable: How companies translate stakeholder dialogue into practice. Bus. Soc. Rev. 2011, 111, 137–163. [Google Scholar] [CrossRef]

- Dowling, J.; Pfeffer, J. Organization legitimacy: Social values and organizational behaviour. Pac. Sociol. Rev. 1975, 28, 122–136. [Google Scholar] [CrossRef]

- Cho, D.H.; Patten, D.M. The role of environmental disclosures as a tool of legitimacy: A research note. Account. Organ. Soc. 2007, 32, 639–647. [Google Scholar] [CrossRef]

- Hooghiemstra, R. Corporate communication and impression management: New perspectives why companies engage in corporate social reporting. J. Bus. Ethics 2000, 27, 55–68. [Google Scholar] [CrossRef]

- Meyer, J.; Rowan, B. Institutionalized organizations: Formal structure as mythand ceremony. Am. J. Sociol. 1977, 83, 340–363. [Google Scholar] [CrossRef]

- DiMaggio, P.J.; Powell, W.W. The Iron Cage Revisited: Institutional Isomorphism and Collective Rationality in Organization Fields. In The New Institutionalism in Organizational Analysis; Powell, W.W., DiMaggio, P.J., Eds.; University of Chicago Press: Chicago, IL, USA, 1991. [Google Scholar]

- Egels-Zandén, N.; Wahlqvist, E. Post-partnership strategies for Refining corporate responsibility: The business social compliance initiative. J. Bus. Ethics 2007, 70, 175–189. [Google Scholar] [CrossRef]

- Suchman, M.C. Managing Legitimacy: Strategic and Institutional Approaches. Acad. Manag. Rev. 1995, 20, 571–610. [Google Scholar] [CrossRef]

- Zucker, L. The role of institutionalization in culture persistence. Am. Sociol. Rev. 1977, 42, 726–743. [Google Scholar] [CrossRef]

- Scott, W.R. Institutions and Organizations, 3rd ed.; Sage: Thousand Oaks, CA, USA, 2007. [Google Scholar]

- Sen, S.; Cowley, J. The relevance of stakeholder theory and social capital theory in the context of CSR in SMEs: An Australian perspective. J. Bus. Ethics 2013, 118, 413–427. [Google Scholar] [CrossRef]

- Barney, J.; Hesterly, W.S. Strategic Management and Competitive Advantages; Pearson Prentice Hall: Upper Saddle River, NJ, USA, 2008; ISBN 0-13-613520-X. [Google Scholar]

- Wang, L.; Juslin, H. The impact of Chinese culture on corporate social responsibility: The harmony approach. J. Bus. Ethics 2009, 88, 433–451. [Google Scholar] [CrossRef]

- Lin, L.W. Corporate social responsibility in China: Window dressing or structural change? Berkeley J. Int. Law 2010, 28, 64–100. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Authors | Year | Country | Journal | Data Collection And Methodology |

|---|---|---|---|---|

| Adams, C.A.; McNicholas, P. [41] | 2007 | Australia | Accounting, Auditing & Accountability Journal | Survey/Descriptive analysis. |

| Al-Hemoud, A.; Behbehani, W. [42] | 2017 | Kuwait | International Journal of Environmental Science and Technology | Survey/DEI methodology |

| Al-Samman, E.; Al-Nashmi, M.M. [43] | 2016 | Yemen | Social Responsibility Journal | Survey/Multiple regression |

| Bo, H.; Li, T.; Toolsema, L.A. [44] | 2009 | China | Scottish Journal of Political Economy | Survey/Theoretical model |

| Cheng, C.L.; Kung, F.H. [45] | 2016 | China | Review of Accounting and Finance | Database/Descriptive analysis/Regression analysis |

| Cheng, Z.; Wang, F.; Keung, C.; Bai, Y. [46] | 2017 | China | Journal of Business Ethics | Database/Regression analysis |

| Cheung, Y.L.; Kong, D.; Tan, W.; Wang, W. [47] | 2015 | China | Journal of Business Ethics | Database/Regression analysis |

| Chun, R. [48] | 2009 | China | Journal of Business Ethics | Questionnaires/Descriptive analysis |

| Córdoba Pachón, J.R.; Garde Sánchez, R.; Rodríguez Bolívar, M.P. [18] | 2014 | Spain | Knowledge and Process Management | Survey/Descriptive analysis |

| Cormier, D.; Gordon, I.M. [49] | 2001 | Canada | Accounting, Auditing & Accountability Journal | Environmental Disclosure Index/Regression analysis |

| Cunningham, M. [21] | 2011 | Canada | Management Communication Quarterly | Case study |

| Enderle, G. [50] | 2001 | China | Journal of Business Ethics | Case study |

| Esa. E.; MohdGhazali, N.A. [51] | 2012 | Malaysian | Corporate Governance: The International Journal of Business in Society | Content analysis/Multiple regression analysis |

| Fu, W.; Deshpande, S.P. [52] | 2012 | China | Journal of Business Ethics | Survey/Regression analysis |

| Gao, Y. [53] | 2009 | China | Journal of Business Ethics | Content Analysis/Descriptive analysis |

| Gao, Y. [54] | 2011 | China | Baltic Journal of Management | Content analysis/Descriptive analysis |

| Garde Sánchez, R., Rodríguez Bolívar, M.P.; López-Hernández, A.M. [55] | 2016 | Spain | Review of Managerial Science | Survey/Regression analysis |

| Garde Sánchez, R., Rodríguez Bolívar, M.P.; López-Hernández, A.M. [56] | 2017 | Spain | The International Journal of Logistics Management | Survey/Structural equation modelling |

| Han, Y.; Zheng, E. [57] | 2016 | China | Management and Organization Review | Survey/Hierarchical linear modelling |

| Heath, J. [58] | 2011 | United States | Management Communication Quarterly | Case study |

| Jiang, L.; Lin, C.; Lin, P. [59] | 2014 | China | Journal of Comparative Economics | Database/Regression analysis |

| Kao, E.H.; Hung-Gay F., Qingdi L. [60] | 2014 | China | The Chinese Economy | Database/Regression Model |

| Kuo, L.; Yeh, C.; Yu, H.C. [61] | 2012 | China | The International Journal of Business in Society | Content analysis/Descriptive analysis |

| Kuo, L.; Yu, H.C.; Chang, B.G. [62] | 2015 | China | International Journal of Climate Change Strategies and Management | Content analysis/Descriptive analysis |

| Lam, K.S.; Yeung, C.L.; Cheng, T.C.E.; Humphreys, P.K. [63] | 2016 | China | International Journal of Production Economics | Content analysis/Cross-sectional regression analysis |

| Lauesen, L.M. [64] | 2011 | Denmark | Social Responsibility Journal | Case study |

| Lee, E.; Walker, M.; Zeng, C. [65] | 2017 | China | Journal of Accounting and Public Policy | Content analysis/Regression analysis |

| Li, C.K.; Luo, J.; Soderstrom, N.S. [66] | 2017 | China | Journal of Accounting and Public Policy | Content analysis/Regression analysis |

| Li, Q.; Luo, W.; Wang, Y.; Wu, L. [67] | 2013 | China | Business Ethics: A European Review | Database/Regression analysis |

| Li, W.; Zhang, R. [68] | 2010 | China | Journal of Business Ethics | Database/Regression analysis |

| Li, Y.; Teck Foo, C. [69] | 2015 | China | Chinese Management Studies | Database/Regression models |

| Li, D.; Xin, L.; Sun, Y.; Huang, M.; Ren, S. [70] | 2016 | China | Polish Journal of Environmental Studies | Database/Regression analysis |

| Mansi, M.; Pandey, R.; Ghauri, E. [71] | 2017 | India | Managerial Auditing Journal | Content analysis/Descriptive analysis |

| Meng, X.H.; Zeng, S.X.; Tam, C.M. [72] | 2013 | China | Journal of Business Ethics | Data base/Regression analysis |

| Meyer, A.; Pac; G. [73] | 2013 | Eastern Europe | Energy Economics | Database/Regression analysis |

| Morsing, M. [74] | 2011 | Scandinavia/Denmark | Management Communication Quarterly | Case study |

| Muafi, M. [75] | 2016 | Indonesia | Journal of Industrial Engineering and Management | Survey/Regression analysis |

| Noronha, C.; Cheng Han Leung, T.; Lei, O.L. [76] | 2015 | China | Sustainability Accounting, Management and Policy Journal | Content analysis/Descriptive analysis |

| Rodríguez Bolívar, M.P.; Garde Sánchez, R.; López Hernández, A.M. [19] | 2014 | Spain | Journal of Environmental Planning and Management | Survey/Descriptive analysis |

| Roper, J.; Schoenberger-Orgad, M. [6] | 2011 | New Zealand | Management Communication Quarterly | Case study |

| Roper, J.; Barker, J.R. [77] | 2011 | New Zealand | Management Communication Quarterly | Forum Introduction |

| Shen, W. [78] | 2017 | China | Environmental Development | Case study |

| Solheim, L.Y. [79] | 2010 | Norway | The International Journal of Sociology and Social Policy | Case study |

| Tang, S.; Li, Pansy, H.; Fryxell, G.E; Lo, C.W. [80] | 2015 | China | Environmental Management | Surveys/Descriptive statistics/Structural equation modelling |

| Tan-Mullins, M.; Mohan, G. [81] | 2013 | China | Environment, Development and Sustainability | Case study |

| Wang, H.; Yanhong, J. [82] | 2007 | China | Environmental and Resource Economics | Survey/Regression analysis |

| Wang, S.; Huang, W.; Gao, Y.; Ansett, S.; Xu, S. [83] | 2015 | China | Leadership & Organization Development Journal | Survey/Ordinary least squares |

| Wang, Y.; Wang, Y.; Bramley, G. [84] | 2005 | China | Urban Studies | Content analysis/Descriptive analysis |

| Whelan, G.; Muthuri, J. [85] | 2015 | China | Business & Society | Content analysis/Descriptive analysis |

| Xu, E.; Yang, H.; Quan, J.M.; Lu, Y. [86] | 2015 | China | Asia Pacific Journal of Management | Content analysis/Regression analysis |

| Xu, S.; Liu, D.; Huang, J. [87] | 2015 | China | Australian Journal of Management | Database/Multivariate regression analysis |

| Yu, S. [88] | 2014 | China | Journal of Business Research | Forum Introduction |

| Zeng, S.; Xu, X.; Yin, H.; Tam, C. [89] | 2012 | China | Journal of Business Ethics | Database/Regression analysis |

| Zhang, M.; Ma, L.; Su, J.; Zhang, W. [90] | 2014 | China | Journal of Business Ethics | Database/Regression analysis |

| Zhao, N.; Patten, D.M. [91] | 2016 | China | Sustainability Accounting, Management and Policy Journal | Interviews/Descriptive statistics |

| Zheng, H; Zhang, Y. [92] | 2016 | China | Chinese Management Studies | Survey/Structural equation modelling |

| Zheng, L.; Balsara, N.; Huang, H. [93] | 2014 | China | Social Responsibility Journal | Database/Regression analysis |

| Zhu, Q.; Geng, Y. [94] | 2001 | China | Greener Management International | Survey/Descriptive statistics |

| Zhu, Q.; Liu, J.; Lai, K. [95] | 2016 | China | International Journal of Production Economics | Content analysis/Multiple regression analysis |

| Zhu, Q.; Zhang, Q. [96] | 2015 | China | Journal of Cleaner Production | Exploratory factor analysis/Structural Equation Model |

| Theory | Explanation | References |

|---|---|---|

| Stakeholder theory (N = 21/60) | The entities take into account not only the shareholders but the diverse groups of interest or stakeholders. Firms consider the demands and requirement of stakeholders to establish their strategies and commitments. | Al-Samman and Al-Nashmi (2016); Cheng and Kung (2016); Cheng et al. (2017); Garde et al. (2016, 2017); Kao et al. (2012, 2014); Lauesen (2011); Lee et al. (2017); Li et al. (2013); Li and Teck Foo (2015); Mansi et al. (2017); Meng et al. (2013); Noronha et al. (2015); Rodríguez et al. (2015); Tang et al. (2015); Wang and Yanhong (2007); Xu et al. (2015); Zeng et al. (2012); Zhao and Patten (2016); Zheng and Zhang (2016) |

| Legitimacy theory (N = 12/60) | Companies can operate if society legitimizes them. There is a “contract” between the company and society to operate. It is necessary that society considers adequate the performance that the entity develops. | Cormier and Gordon (2001); Enderle (2001); Garde et al. (2016, 2017); Heath (2011); Lauesen (2011); Lee et al. (2017); Li et al. (2016); Meng et al. (2013); Noronha et al. (2015); Rodríguez et al. (2015); Roper and Schoenberger-Orgad (2011) |

| Institutional theory (N = 9/60) | Analyses the processes by which organisations acquire social acceptance and approval as a result of compliance with standards and the institutional environment | Cheng, Z. et al. (2017); Cheung, et al. (2015); Noronha et al. (2015); Wang et al. (2005); Yu (2014); Zhang et al. (2014); Zhao and Patten (2016); Zheng and Zhang (2016); Zhu et al. (2016) |

| Agency theory (N = 3/60) | Shareholders entrust management tasks to agents, in the understanding that their interests will be protected | Cheng and Kung (2016); Cheng et al. (2017); Li and Zhang (2010) |

| Stewardship theory (N = 1/60) | The board wishes to be a good administrator of the entity and do a good job in managing the company’s resources properly | Rodríguez et al. (2015) |

| Organisational and economic theories (N = 10/60) | Organisational approach Job characteristics theory Organisational imprinting theory Coasian theory Signalling theory | Adams and McNicholas (2007) Al-Hemoud and Behbehani (2017) Han and Zheng (2016) Jiang et al. (2014) Kuo et al. (2015); Lam et al. (2016) |

| Performance impression theory Contingency theory | Meng et al. (2013) Mufaci (2016) | |

| Social capital theory Classic economic theory, shareholder theory, behavioural theory | Rodríguez et al. (2015) Whelan and Muthuri (2015) |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Garde-Sanchez, R.; López-Pérez, M.V.; López-Hernández, A.M. Current Trends in Research on Social Responsibility in State-Owned Enterprises: A Review of the Literature from 2000 to 2017. Sustainability 2018, 10, 2403. https://doi.org/10.3390/su10072403

Garde-Sanchez R, López-Pérez MV, López-Hernández AM. Current Trends in Research on Social Responsibility in State-Owned Enterprises: A Review of the Literature from 2000 to 2017. Sustainability. 2018; 10(7):2403. https://doi.org/10.3390/su10072403

Chicago/Turabian StyleGarde-Sanchez, Raquel, María Victoria López-Pérez, and Antonio M. López-Hernández. 2018. "Current Trends in Research on Social Responsibility in State-Owned Enterprises: A Review of the Literature from 2000 to 2017" Sustainability 10, no. 7: 2403. https://doi.org/10.3390/su10072403

APA StyleGarde-Sanchez, R., López-Pérez, M. V., & López-Hernández, A. M. (2018). Current Trends in Research on Social Responsibility in State-Owned Enterprises: A Review of the Literature from 2000 to 2017. Sustainability, 10(7), 2403. https://doi.org/10.3390/su10072403