Corruption and Technological Innovation in Private Small-Medium Scale Companies: Does Female Top Management Play a Role?

Abstract

1. Introduction

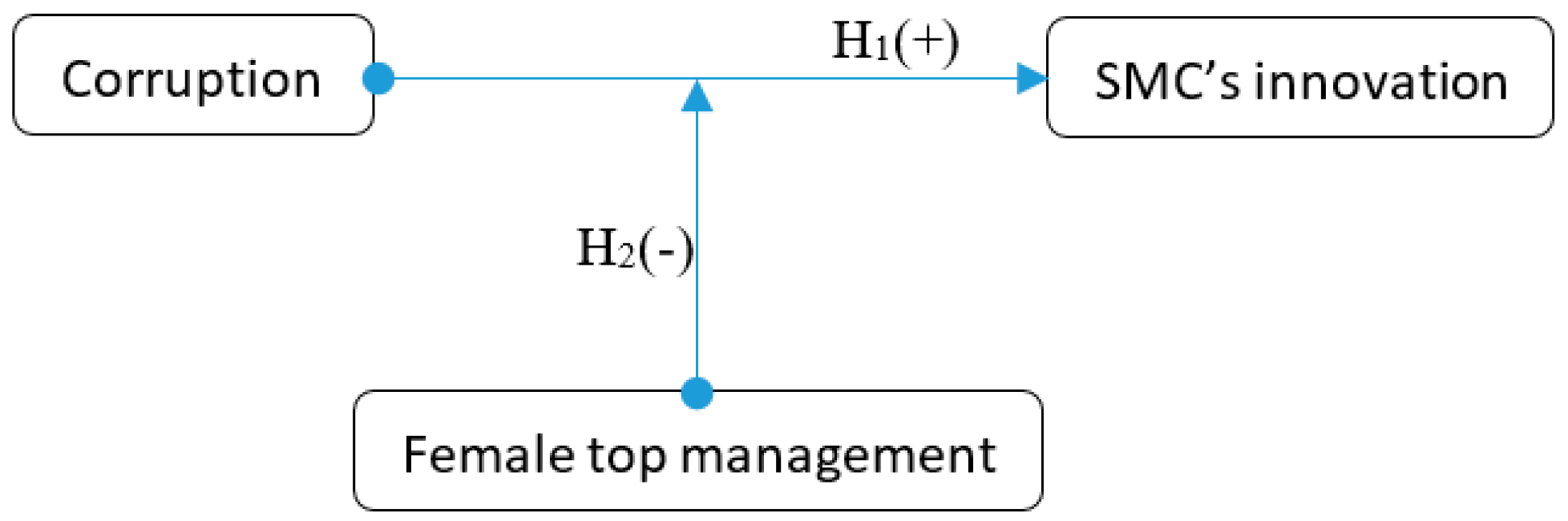

2. Theory and Hypotheses

2.1. Theoretical Framework

2.2. Innovation and Corruption in Privately Owned SMCs

2.3. Female Top Management

3. Research Methodology

3.1. Data and Sample

3.2. Measures

3.2.1. Dependent Variables

3.2.2. Independent Variables

It is said that establishments are sometimes required to make informal payments or gifts to public officials to “get things done” with regard to licenses, regulations, services and so forth. On average, what percentage of total annual sales, or estimated total annual value, do establishments like this one pay in informal payments or gifts to public officials for this purpose?

3.2.3. Control Variables

4. Results

4.1. The Influence of Corruption on SMCs’ Innovation

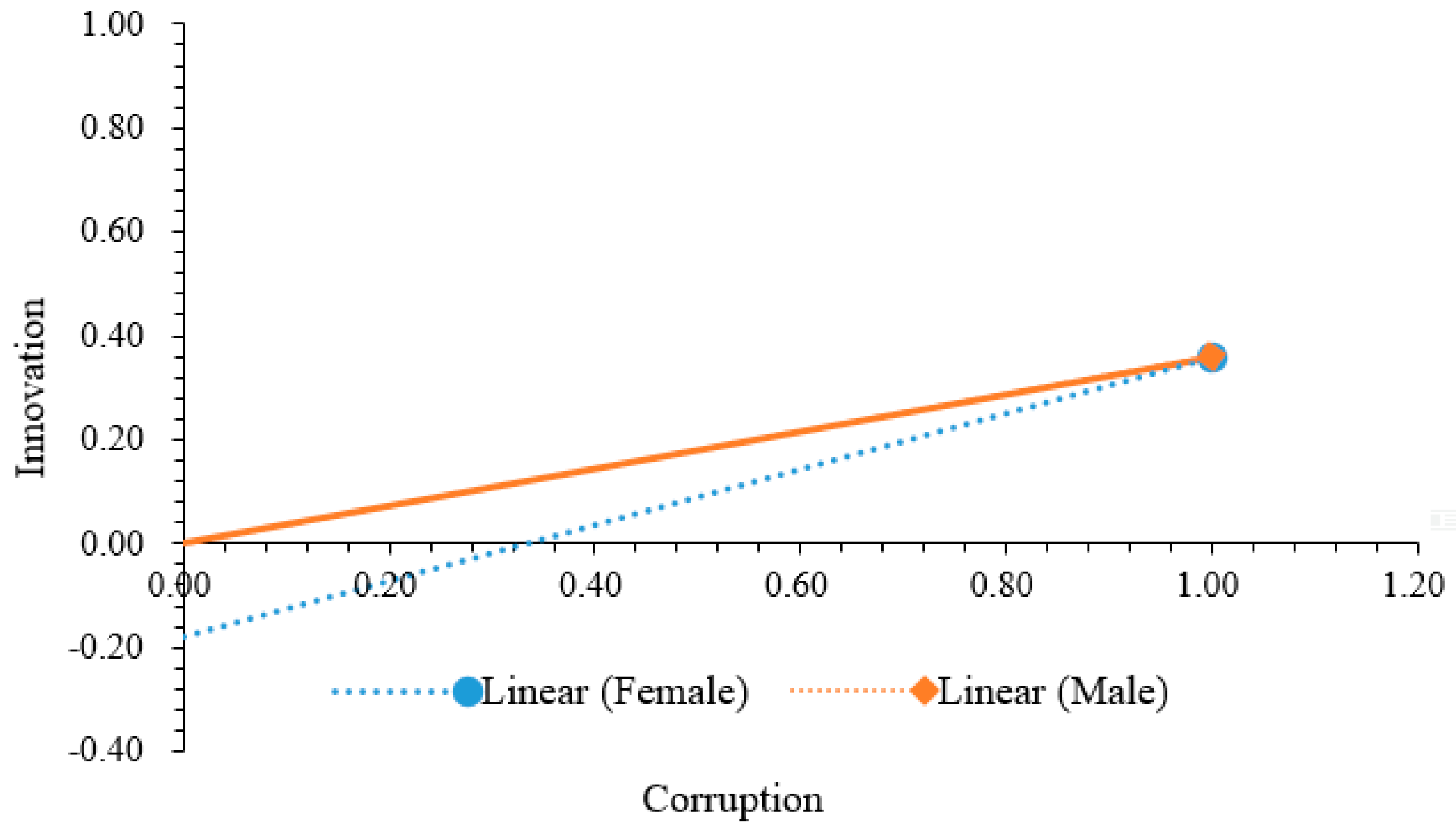

4.2. Corruption and Innovation: Does Gender Play a Role?

5. Robustness and Endogeneity

5.1. Robustness of the Interaction Term

5.2. Endogeneity of Corruption

6. Conclusions and Discussion

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Dollar, D.; Fisman, R.; Gatti, R. Are women really the “fairer” sex? Corruption and women in government. J. Econ. Behav. Organ. 2001, 4, 423–429. [Google Scholar] [CrossRef]

- Collins, J.D.; Uhlenbruck, K.; Rodriguez, P. Why firms engage in corruption: A top management perspective. J. Bus. Ethics 2009, 1, 89–108. [Google Scholar] [CrossRef]

- Hambrick, D.C.; Mason, P.A. Upper echelons: The organization as a reflection of its top managers. Acad. Manag. Rev. 1984, 2, 193–206. [Google Scholar] [CrossRef]

- Jha, C.K.; Sarangi, S. Women and corruption: What positions must they hold to make a difference? J. Econ. Behav. Organ. 2018, 4, 1–15. [Google Scholar] [CrossRef]

- Swamy, A.; Knack, S.; Lee, Y.; Azfar, O. Gender and corruption. J. Dev. Econ. 2001, 1, 25–55. [Google Scholar] [CrossRef]

- Jefferson, G.H.; Huamao, B.; Xiaojing, G.; Xiaoyun, Y. R&D performance in Chinese industry. Econ. Innov. New Technol. 2006, 15, 345–366. [Google Scholar]

- Qijing, Y. The growth of enterprises: To build political connections or capability? Econ. Res. J. 2011, 10, 54–66. [Google Scholar]

- Cai, H.; Fang, H.; Xu, L.C. Eat, drink, firms, government: An investigation of corruption from the entertainment and travel costs of Chinese firms. J. Law Econ. 2011, 1, 55–78. [Google Scholar] [CrossRef]

- Buis, M.L. Stata tip 87: Interpretation of interactions in non-linear models. State J. 2010, 2, 305–308. [Google Scholar]

- Scott, W.R. Institutions and Organizations: Ideas, Interests, and Identities; Sage Publications: Los Angeles, CA, USA, 2013. [Google Scholar]

- Xie, X.; Qi, G.; Zhu, K.X. Corruption and New Product Innovation: Examining Firms’ Ethical Dilemmas in Transition Economies. J. Bus. Ethics 2018, 2, 1–19. [Google Scholar] [CrossRef]

- Bonanno, G.; Haworth, B. The intensity of competition and the choice between product and process innovation. Int. J. Ind. Organ. 1998, 4, 495–510. [Google Scholar] [CrossRef]

- Blake, M.K.; Hanson, S. Rethinking innovation: Context and gender. Environ. Plan. A 2005, 4, 681–701. [Google Scholar] [CrossRef]

- Marlow, S.; McAdam, M. Analyzing the influence of gender upon high-technology venturing within the context of business incubation. Entrep. Theory Pract. 2012, 4, 655–676. [Google Scholar] [CrossRef]

- Méon, P.; Sekkat, K. Does corruption grease or sand the wheels of growth? Public Choice 2005, 122, 69–97. [Google Scholar] [CrossRef]

- Van Vu, H.; Tran, T.Q.; Van Nguyen, T.; Lim, S. Corruption, types of corruption and firm financial performance: New evidence from a transitional economy. J. Bus. Ethics 2016, 4, 847–858. [Google Scholar] [CrossRef]

- Rose-Ackerman, S. Corruption and development. In Annual World Bank Conference on Development Economics; World Bank: Washington, DC, USA, 1998; pp. 35–57. [Google Scholar]

- Kim, E.; Ha, Y.; Kim, S. Public Debt, Corruption and Sustainable Economic Growth. Sustainability 2017, 3, 433. [Google Scholar] [CrossRef]

- Luiz, J.M.; Stewart, C. Corruption, South African multinational enterprises, and institutions in Africa. J. Bus. Ethics 2014, 3, 383–398. [Google Scholar] [CrossRef]

- Habiyaremye, A.; Raymond, W. Transnational Corruption and Innovation in Transition Economies; UNU-MERIT Working Paper; UNU-MERIT: Maastricht, The Netherlands, 2013; pp. 1–37. [Google Scholar]

- Aguilera, R.V.; Vadera, A.K. The dark side of authority: Antecedents, mechanisms, and outcomes of organizational corruption. J. Bus. Ethics 2008, 4, 431–449. [Google Scholar] [CrossRef]

- Anokhin, S.; Schulze, W.S. Entrepreneurship, innovation, and corruption. J. Bus. Ventur. 2008, 5, 465–476. [Google Scholar] [CrossRef]

- Blackburn, K.; Forgues-Puccio, G.F. Why is corruption less harmful in some countries than in others? J. Econ. Behav. Organ. 2009, 3, 797–810. [Google Scholar] [CrossRef]

- De Beer, J.; Fu, K.; Wunsch-Vincent, S. The Informal Economy, Innovation and Intellectual Property-Concepts, Metrics, and Policy Considerations. Economic Research Working Paper; WIPO: Geneva, Switzerland, 2013; Volume 10, pp. 1–76. [Google Scholar]

- Moldovan, A.; Van de Walle, S. Gifts or bribes? Attitudes on informal payments in Romanian health care. Public Integr. 2013, 4, 385–402. [Google Scholar] [CrossRef]

- Iriyama, A.; Kishore, R.; Talukdar, D. Playing dirty or building capability? Corruption and HR training as competitive actions to threats from informal and foreign firm rivals. Strateg. Manag. J. 2016, 10, 2152–2173. [Google Scholar] [CrossRef]

- Acemoglu, D.; Verdier, T. The choice between market failures and corruption. Am. Econ. Rev. 2000, 1, 194–211. [Google Scholar] [CrossRef]

- Adhikari, A.; Derashid, C.; Zhang, H. Public policy, political connections, and effective tax rates: Longitudinal evidence from Malaysia. J. Account. Public Policy 2006, 5, 574–595. [Google Scholar] [CrossRef]

- Viadero, D. Researches mull STEM gender gap. Educ. Week 2009, 35, 1–5. [Google Scholar]

- Gorodnichenko, Y.; Roland, G. Individualism, innovation, and long-run growth. Proc. Natl. Acad. Sci. USA 2011, 108, 21316–21319. [Google Scholar] [CrossRef] [PubMed]

- Jha, C.K.; Panda, B. Individualism and Corruption: A Cross-Country Analysis. Econ. Pap. 2017, 36, 60–74. [Google Scholar] [CrossRef]

- d’Adda, G.; Darai, D.; Pavanini, N.; Weber, R.A. Do leaders affect ethical conduct? J. Eur. Econ. Assoc. 2017, 6, 1177–1213. [Google Scholar] [CrossRef]

- Vian, T.; Grybosk, K.; Sinoimeri, Z.; Hall, R. Informal payments in government health facilities in Albania: Results of a qualitative study. Soc. Sci. Med. 2006, 4, 877–887. [Google Scholar] [CrossRef] [PubMed]

- Ashforth, B.E.; Anand, V. The normalization of corruption in organizations. Res. Organ. Behav. 2003, 25, 1–52. [Google Scholar] [CrossRef]

- Breen, M.; Gillanders, R.; McNulty, G.; Suzuki, A. Gender and corruption in business. J. Dev. Stud. 2017, 9, 1486–1501. [Google Scholar] [CrossRef]

- Cuijpers, M.; Guenter, H.; Hussinger, K. Costs and benefits of inter-departmental innovation collaboration. Res. Policy 2011, 4, 565–575. [Google Scholar] [CrossRef]

- Zhai, Y.M.; Sun, W.Q.; Tsai, S.B.; Wang, Z.; Zhao, Y.; Chen, Q. An Empirical Study on Entrepreneurial Orientation, Absorptive Capacity, and SMEs’ Innovation Performance: A Sustainable Perspective. Sustainability 2018, 2, 314. [Google Scholar] [CrossRef]

- Van de Ven, A.H. Central problems in the management of innovation. Manag. Sci. 1986, 5, 590–607. [Google Scholar] [CrossRef]

- Reinikka, R.; Svensson, J. Using micro-surveys to measure and explain corruption. World Dev. 2006, 2, 359–370. [Google Scholar] [CrossRef]

- Clarke, G.R. How petty is petty corruption? Evidence from firm surveys in Africa. World Dev. 2011, 7, 1122–1132. [Google Scholar] [CrossRef]

- Wang, Y.; You, J. Corruption and firm growth: Evidence from China. China Econ. Rev. 2012, 2, 415–433. [Google Scholar] [CrossRef]

- Ai, C.; Norton, E.C. Interaction terms in logit and probit models. Econ. Lett. 2003, 1, 123–129. [Google Scholar] [CrossRef]

- Cornelißen, T.; Sonderhof, K. Partial effects in probit and logit models with a triple dummy-variable interaction term. Stata J. 2009, 4, 571. [Google Scholar]

- Esarey, J.; Chirillo, G. “Fairer sex” or purity myth? Corruption, gender, and institutional context. Polit. Gend. 2013, 4, 361–389. [Google Scholar] [CrossRef]

- Lee, S.H.; Weng, D.H. Does bribery in the home country promote or dampen firm exports? Strat. Manag. J. 2013, 12, 1472–1487. [Google Scholar] [CrossRef]

- Besley, T.; Burgess, R. Can labor regulation hinder economic performance? Evidence from India. Q. J. Econ. 2004, 1, 91–134. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Aspects | Types of Theories | Core Contents | The Role of Female Top Management |

|---|---|---|---|

| Organizational perspective | Resource dependence | Each organization must seek development resources from an open environment | Providing diverse perspectives and solutions to managerial decisions and bringing more internal support and external resources |

| Principal-agent | The function of the board of directors is to monitor and control the managers | Role of female managers on companies’ access to resources is not clear | |

| Team perspective | Upper Echelons | companies’ outcomes—strategic choices and decisions—are partially forecasted by managerial characteristics | Female executives’ characteristics and ways of doing things have an obvious influence on strategic choices and team performance |

| Social cognition | The minority is subordinate to the majority and the lower level to the higher level | Powerless that cannot play their role | |

| Personal perspective | Human capital | In economic growth, the role of human capital is greater than that of material capital. The economic benefit of investment in human capital is more than that of material investment | The human capital characteristics of female executives are different from that of male top managers and benefit to innovative performance |

| Feminism | In accepting higher education and having the right to vote, women should get equal opportunities with men | It is a woman’s job to nurture and care for the family and that has a negative influence on innovation |

| Options | No Obstacle | Minor Obstacle | Moderate Obstacle | Major Obstacle | Very Severe Obstacle | |

|---|---|---|---|---|---|---|

| Variables | ||||||

| Market competition | 0 | 1 | 2 | 3 | 4 | |

| Access to finance | 0 | 1 | 2 | 3 | 4 | |

| Labor regulations | 0 | 1 | 2 | 3 | 4 | |

| Variables | Obs. | Mean | S.D. | Min. | Max. |

|---|---|---|---|---|---|

| 1. Firm age in log | 1757 | 2.83 | 0.36 | 1.61 | 4.87 |

| 2. Market competition | 1757 | 0.83 | 0.86 | 0 | 4 |

| 3. R&D investment | 1697 | 0.42 | 0.49 | 0 | 1 |

| 4. Innovation | 1517 | 0.37 | 0.48 | 0 | 1 |

| 5. Innovation (alternative measure) | 1697 | 0.63 | 0.48 | 0 | 1 |

| 6. Corruption | 1196 | 0.20 | 0.40 | 0 | 1 |

| 7. Firm size in log | 1757 | 4.44 | 1.34 | 1.61 | 10.82 |

| 8. Labor regulations | 1757 | 0.52 | 0.71 | 0 | 4 |

| 9. Access to finance | 1757 | 0.83 | 0.87 | 0 | 4 |

| 10. Female top manager | 1757 | 0.59 | 0.49 | 0 | 1 |

| 11. c_gender | 1757 | 0.00 | 0.49 | −0.58 | 0.41 |

| 12. c_corruption | 1196 | 0.00 | 0.40 | −0.20 | 0.80 |

| 13. c_ female top manager * c_corruption | 1196 | 0.03 | 0.20 | −0.47 | 0.33 |

| Variables | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. Firm age in log | 1.00 | |||||||||||

| 2. Market competition | −0.00 | 1.00 | ||||||||||

| 3. R&D investment | 0.06 ** | 0.06 ** | 1.00 | |||||||||

| 4. Innovation | −0.02 | −0.01 * | 0.07 *** | 1.00 | ||||||||

| 5. Innovation b | 0.06 ** | 0.10 *** | 0.38 *** | 0.28 *** | 1.00 | |||||||

| 6. Corruption | 0.01 | −0.02 | 0.09 *** | 0.13 *** | 0.13 *** | 1.00 | ||||||

| 7. Firm size in log | 0.26 *** | −0.09 *** | 0.23 *** | 0.04 | 0.17 *** | 0.01 | 1.00 | |||||

| 8. Labor regulations | 0.04 | 0.25 *** | 0.09 *** | 0.02 | 0.11 *** | −0.01 | 0.05 * | 1.00 | ||||

| 9. Access to finance | −0.03 | 0.22 *** | 0.14 *** | 0.02 | 0.14 *** | 0.03 | 0.01 | 0.37 *** | 1.00 | |||

| 10. Female top manager | 0.07 | 0.06 ** | −0.09 *** | −0.17 *** | -0.08 *** | −0.14*** | 0.03 | 0.31 *** | −0.03 | 1.00 | ||

| 11. c_gender | 0.07 | 0.06 ** | −0.09 *** | −0.17 *** | -0.08 *** | −0.14*** | 0.03 | 0.031 *** | −0.03 | 1.00 | 1.00 | |

| 12. c_corruption | 0.01 | −0.02 | 0.09 *** | 0.13 *** | 0.13 *** | 1.00 | 0.01 | −0.01 | 0.03 | −0.14 *** | −0.14 *** | 1.00 |

| 13. c_ female top manager * c_corruption | 0.02 | 0.11 *** | 0.04 | −0.17 *** | −0.05* | −0.25 *** | 0.03 | 0.07 * | 0.03 | 0.04 | 0.04 | −0.25 *** |

| Variables | OLS | Logit | Logit | Logit (Innovation a) | ||

|---|---|---|---|---|---|---|

| Innovation b | Odds Ratio | Average Marginal Effects (dy/dx) | Average Marginal Effects (ey/dx) | |||

| Corruption | 0.0868 ** | 0.4925 ** | 0.7706 *** | 1.6364 ** | 0.0887 ** | 0.2898 ** |

| (0.0358) | (0.2054) | (0.2061) | (0.3412) | (0.0364) | (0.1214) | |

| Firm age in log | −0.0295 | −0.1733 | 0.1754 | 0.8408 | −0.0312 | −0.1021 |

| (0.0409) | (0.2130) | (0.1984) | (0.1749) | (0.0383) | (0.1253) | |

| Market competition | 0.0221 | 0.1248 | 0.1417 | 1.1321 | 0.0225 | 0.0734 |

| (0.0189) | (0.0976) | (0.0897) | (0.1085) | (0.0175) | (0.0574) | |

| R&D investment | 0.0226 | 0.1326 | 1.5318 * | 1.1412 | 0.0238 | 0.0781 |

| (0.0308) | (0.1644) | (0.1553) | (0.1919) | (0.0296) | (0.0967) | |

| Firm size in log | 0.0173 | 0.0956 | 0.1717 *** | 1.1003 | 0.0172 | 0.0563 |

| (0.0125) | (0.0659) | (0.0619) | (0.0699) | (0.0118) | (0.0388) | |

| Labor regulations | 0.0408 * | 0.2404 * | 0.1077 | 1.2717 * | 0.0433 * | 0.1414 * |

| (0.0239) | (0.1293) | (0.1132) | (0.1699) | (0.0231) | (0.0761) | |

| Access to finance | −0.0212 | −0.1306 | 0.0301 | 0.8775 | −0.0235 | −0.0768 |

| (0.0183) | (0.0977) | (0.0892) | (0.0831) | (0.0176) | (0.0574) | |

| Constant | 0.0297 | −2.4174 *** | −1.3595 ** | 0.0891 *** | ||

| (0.1415) | (0.7843) | (0.5771) | (0.0653) | |||

| City/Industry dummies | Y | Y | Y | Y | Y | Y |

| R2 | 0.2557 | |||||

| Pseudo R2 | 0.2100 | 0.1268 | 0.2100 | |||

| p-Value | 0.0000 | 0.0000 | 0.0000 | |||

| Correctly classified | 72.00% | 73.23% | 72.00% | |||

| Observations | 1196 | 1196 | 1196 | 1196 | 1196 | 1196 |

| Variables | OLS | Logit | Logit | Logit (Innovation a) | ||

|---|---|---|---|---|---|---|

| Innovation b | Odds Ratio | Average Marginal Effects (dy/dx) | Average Marginal Effects (ey/dx) | |||

| Female top manager | −0.0730 *** | −0.4023 ** | −0.2946 ** | 0.6688 *** | −0.0742 *** | −0.2546 *** |

| (0.0279) | (0.1459) | (0.1149) | (0.0976) | (0.0265) | (0.0927) | |

| Firm age in log | −0.0427 | −0.2402 | 0.1207 | 0.7864 | −0.0443 | −0.1521 |

| (0.0340) | (0.1795) | (0.1568) | (0.1412) | (0.0330) | (0.1137) | |

| Market competition | 0.0203 | 0.1165 | 0.2209 *** | 1.1235 | 0.0215 | 0.0737 |

| (0.0165) | (0.0835) | (0.0720) | (0.0937) | (0.0153) | (0.0528) | |

| R&D investment | 0.0314 | 0.1776 | 1.6626 *** | 1.1943 | 0.0328 | 0.1125 |

| (0.0264) | (0.1362) | (0.1265) | (0.1627) | (0.0251) | (0.0862) | |

| Firm size in log | 0.0250 ** | 0.1373 *** | 0.1783 *** | 1.1472 *** | 0.0253 *** | 0.0869 *** |

| (0.0097) | (0.0518) | (0.0451) | (0.0594) | (0.0095) | (0.0328) | |

| Labor regulations | 0.0547 *** | 0.3089 *** | 0.1453 | 1.3620 *** | 0.0570 *** | 0.1956 *** |

| (0.0205) | (0.1043) | (0.0957) | (0.1420) | (0.0190) | (0.0662) | |

| Access to finance | 0.0010 | 0.0035 | 0.1558 ** | 1.0035 | 0.0006 | 0.0022 |

| (0.0162) | (0.0839) | (0.0726) | (0.0842) | (0.0155) | (0.0531) | |

| Constant | 0.1010 | −2.0783 *** | −1.3898 *** | 0.1251 *** | ||

| (0.1167) | (0.6692) | (0.4501) | (0.0838) | |||

| City/Industry dummies | Y | Y | Y | Y | Y | Y |

| R2 | 0.2047 | |||||

| Pseudo R2 | 0.1692 | 0.1413 | 0.1692 | |||

| p-Value | 0.0000 | 0.0000 | 0.0000 | |||

| Correctly classified | 72.24% | 67.83% | 72.24% | |||

| Observations | 1757 | 1757 | 1757 | 1757 | 1757 | 1757 |

| Variables | OLS | Logit | Logit | ||

|---|---|---|---|---|---|

| Odds Ratio | Average Marginal Effects (dy/dx) | Average Marginal Effects (ey/dx) | |||

| Female top manager | −1.3715 *** | −0.9641 ** | 0.7962 ** | −0.0154 ** | −0.1546 ** |

| (0.1128) | (0.5413) | (0.0120) | (0.0652) | (0.0771) | |

| Foreign ownership (%) | −3.2781 * | −2.9810 ** | 0.2512 ** | −0.0550 ** | −0.7090 ** |

| (0.0201) | (0.0812) | (0.0379) | (0.1052) | (0.6180) | |

| Exporter Dummy | 3.1039 * | 3.3102 ** | 2.194 ** | 0.4519 ** | 0.5847 ** |

| (0.4103) | (0.6451) | (0.0579) | (0.1110) | (0.2262) | |

| Sales in log | 0.5201 ** | 0.4973 *** | 1.1412 *** | 0.2092 *** | 0.1943 *** |

| (0.0984) | (0.0811) | (0.9014) | (0.0792) | (0.1428) | |

| Constant | −2.1087 ** | −2.0783 *** | 0.1251 *** | ||

| (0.6711) | (0.7021) | (0.8136) | |||

| City/Industry dummies | Y | Y | Y | Y | Y |

| R2 | 0.1943 | ||||

| Pseudo R2 | 0.1023 | 0.1631 | |||

| p-Value | 0.0000 | 0.0000 | |||

| Correctly classified | 69.31% | 69.31% | |||

| Observations | 1196 | 1196 | 1196 | 1196 | 1196 |

| Variables | OLS | Logit | Logit | Logit (Innovation a) | |

|---|---|---|---|---|---|

| Innovation b | Average Marginal Effects (dy/dx) | Average Marginal Effects (ey/dx) | |||

| Corruption | 0.0697 * | 0.3629 * | 0.6147 *** | 0.0648 * | 0.2136 * |

| (0.0366) | (0.2181) | (0.2054) | (0.0386) | (0.1286) | |

| Female top manager | −0.0496 | −0.3053 * | −0.2883 * | −0.0545 * | −0.1796 * |

| (0.0324) | (0.1834) | (0.1478) | (0.0324) | (0.1082) | |

| c_ female top manager * c_corruption | −0.0316 ** | −0.1888 ** | −0.1521* | −0.0338 ** | −0.1111 ** |

| (0.0141) | (0.0808) | (0.0815) | (0.0143) | (0.0476) | |

| Firm age in log | −0.0255 | −0.1709 | 0.1968 | −0.0306 | −0.1006 |

| (0.0409) | (0.2151) | (0.1982) | (0.0384) | (0.1265) | |

| Market competition | 0.0259 | 0.1514 | 0.1702 * | 0.0270 | 0.0891 |

| (0.0188) | (0.0984) | (0.0902) | (0.0175) | (0.0579) | |

| R&D investment | 0.0268 | 0.1643 | 1.5351 *** | 0.0294 | 0.0968 |

| (0.0307) | (0.1658) | (0.1566) | (0.0295) | (0.0974) | |

| Firm size in log | 0.0175 | 0.0977 | 0.1798 *** | 0.0174 | 0.0575 |

| (0.0124) | (0.0663) | (0.0616) | (0.0117) | (0.0389) | |

| Labor regulations | 0.0409 * | 0.2562 * | 0.1313 | 0.0458 * | 0.1508 * |

| (0.0237) | (0.1302) | (0.1155) | (0.0231) | (0.0767) | |

| Access to finance | −0.0204 | −0.1355 | 0.0333 | −0.0242 | −0.0797 |

| (0.0183) | (0.0984) | (0.0893) | (0.0175) | (0.0578) | |

| Constant | 0.0351 | −2.3762 *** | −1.3230 ** | ||

| (0.1422) | (0.7952) | (0.5691) | |||

| City/Industry dummies | Y | Y | Y | Y | Y |

| R2 | 0.2607 | ||||

| Pseudo R2 | 0.2156 | 0.1314 | |||

| p-Value | 0.0000 | 0.0000 | |||

| Correctly classified | 73.05% | 72.97% | |||

| Observations | 1050 | 1050 | 1050 | 1050 | 1050 |

| Corruption × Female Top Manager | Margin | Delta-Method Std. Err. | z | p > z |

| 0 0 | 1.2847 *** | 0.2032 | 9.05 | 0.000 |

| 0 1 | 0.7318 *** | 0.0880 | 10.66 | 0.000 |

| 1 0 | 4.5874 *** | 0.1703 | 5.27 | 0.000 |

| 1 1 | 0.6694 *** | 0.1860 | 4.32 | 0.000 |

| 0. Corruption × 1. Female Top Manager | Coef. | Std. Err. | z | p > z |

| (1) | −0.5528 *** | 0.2045 | −2.70 | 0.007 |

| 1. Corruption × 1. Female Top Manager | Coef. | Std. Err. | z | p > z |

| (1) | −3.9180 *** | 0.1733 | −3.34 | 0.001 |

| First-Stage Regressions (Corruption) | Instrumental Variables Regression (Innovation) | |||||

|---|---|---|---|---|---|---|

| Coef. | Robust Std. Err. | t | Coef. | Robust Std. Err. | z | |

| Corruption | 0.1470 ** | 0.1451 | 2.01 | |||

| Female top manager | −0.0137 | 0.0265 | −0.52 | −0.0451 ** | 0.0322 | −2.40 |

| c_corruption*c_ female top manager | −0.0215 * | 0.2595 | −1.78 | |||

| Firm age in log | 0.0114 | 0.0286 | 0.40 | −0.0284 | 0.0403 | −0.70 |

| Market competition | −0.0161 | 0.0146 | −1.10 | 0.0251 | 0.0185 | 1.36 |

| R&D investment | −0.0242 | 0.0258 | −0.94 | 0.0259 | 0.0309 | 0.84 |

| Firm size in log | −0.0086 | 0.0090 | −0.96 | 0.0183 | 0.0123 | 1.49 |

| Labor regulations | 0.0127 | 0.0199 | 0.64 | 0.0393 | 0.0253 | 1.55 |

| Access to finance | 0.0187 | 0.0156 | 1.20 | −0.0224 | 0.0186 | −1.20 |

| Court system | 0.1532 *** | 0.0195 | 7.87 | |||

| Tax administration | 0.1274 *** | 0.0453 | 2.81 | |||

| c_court system*c_gender | 0.0603 | 0.0389 | 1.55 | |||

| c_tax administration*c_gender | −0.0029 | 0.0667 | −0.04 | |||

| City/Industry dummies | Y | Y | ||||

| _cons | 0.1358 | 0.1012 | 1.34 | 0.0239 | 0.1462 | 0.16 |

| Underidentification test p-value | 0.0000 | |||||

| Cragg-Donald Wald F statistic | 11.44 | |||||

| Kleibergen-Paap rk Wald F statistic | 7.07 | |||||

| Stock-Yogo weak ID test critical values | ||||||

| 5% maximal IV relative bias | 11.04 | |||||

| 10% maximal IV relative bias | 6.56 | |||||

| 20% maximal IV relative bias | 5.57 | |||||

| 30% maximal IV relative bias | 4.73 | |||||

| 10% maximal IV size | 16.87 | |||||

| 15% maximal IV size | 9.93 | |||||

| 20% maximal IV size | 7.54 | |||||

| 25% maximal IV size | 6.28 | |||||

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Xia, H.; Tan, Q.; Bai, J. Corruption and Technological Innovation in Private Small-Medium Scale Companies: Does Female Top Management Play a Role? Sustainability 2018, 10, 2252. https://doi.org/10.3390/su10072252

Xia H, Tan Q, Bai J. Corruption and Technological Innovation in Private Small-Medium Scale Companies: Does Female Top Management Play a Role? Sustainability. 2018; 10(7):2252. https://doi.org/10.3390/su10072252

Chicago/Turabian StyleXia, Houxue, Qingmei Tan, and Junhong Bai. 2018. "Corruption and Technological Innovation in Private Small-Medium Scale Companies: Does Female Top Management Play a Role?" Sustainability 10, no. 7: 2252. https://doi.org/10.3390/su10072252

APA StyleXia, H., Tan, Q., & Bai, J. (2018). Corruption and Technological Innovation in Private Small-Medium Scale Companies: Does Female Top Management Play a Role? Sustainability, 10(7), 2252. https://doi.org/10.3390/su10072252