Development of a Streamlined Environmental Life Cycle Costing Model for Buildings in South Korea

Abstract

1. Introduction

2. Environmental Life Cycle Costing

3. Model Development

3.1. Selection of Major Cost Categories

3.2. Selection of Major Building Materials

3.3. Development of ELCC Model

3.3.1. Calculation of Private Costs

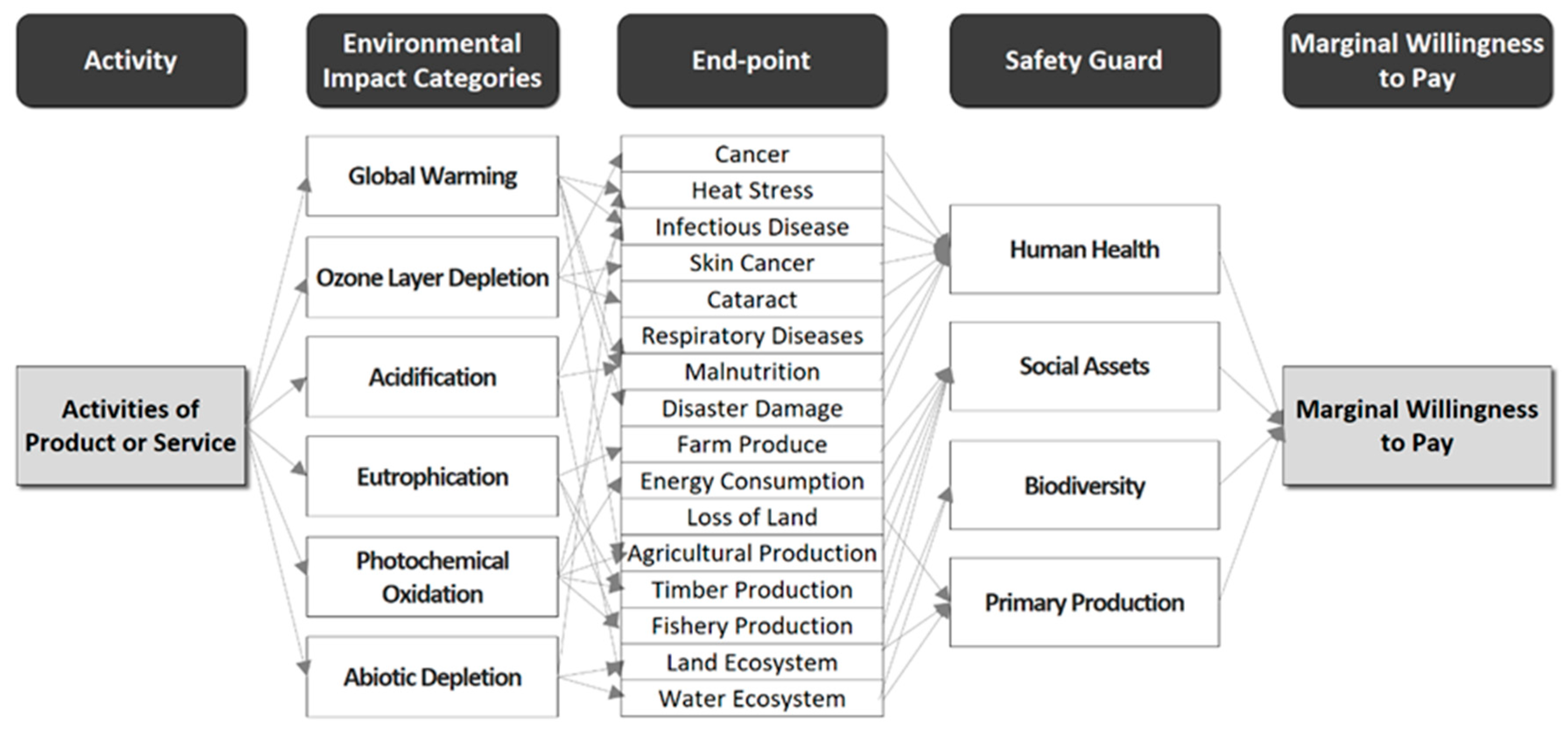

3.3.2. Calculation of External Costs

3.3.3. Application of the ELCC Model Equation

4. Case Study

4.1. Target Selection

4.2. Evaluation Scope

4.3. Data Collection

4.4. Evaluation

4.5. Evaluation Results

4.5.1. Private Costs

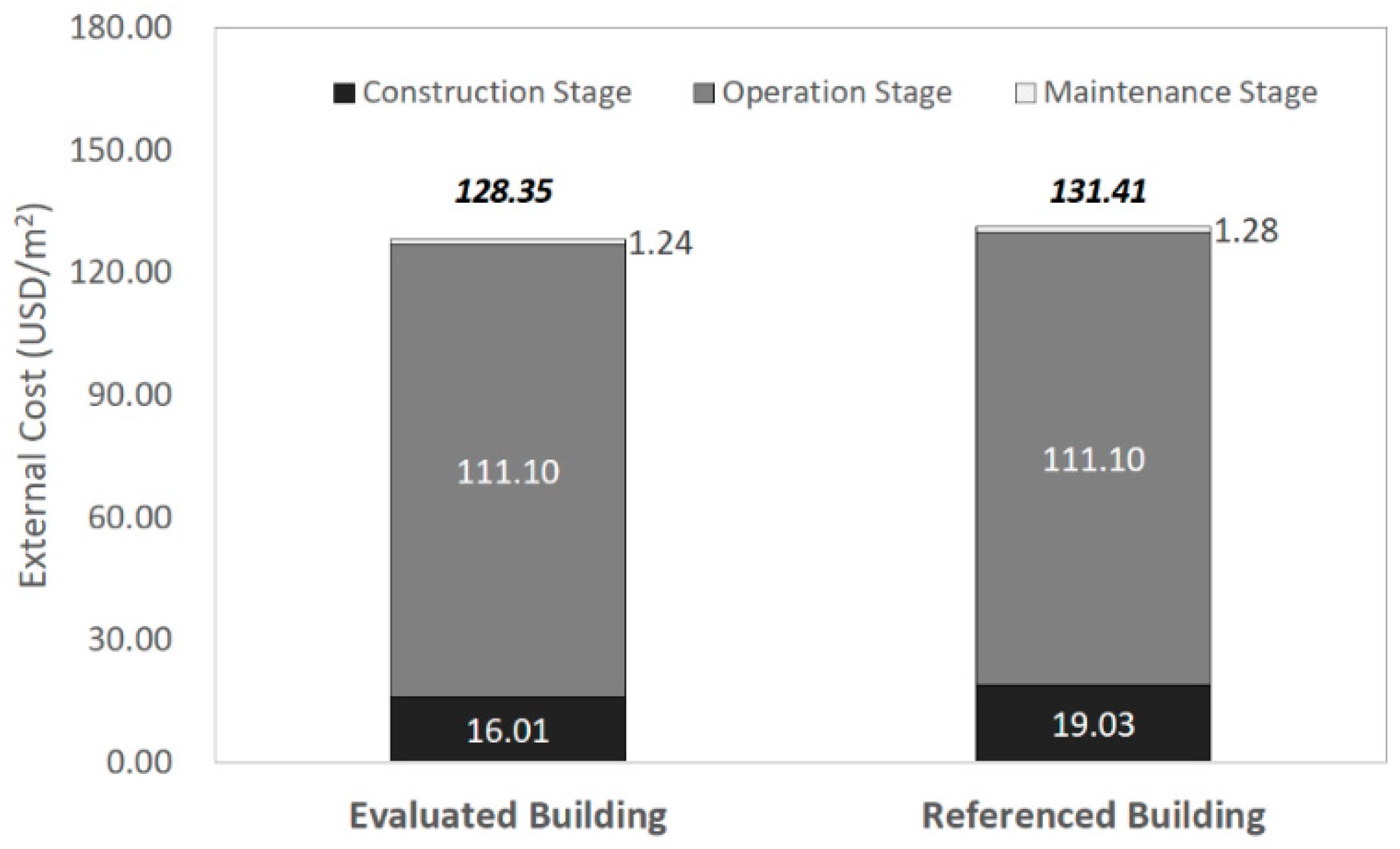

4.5.2. External Costs

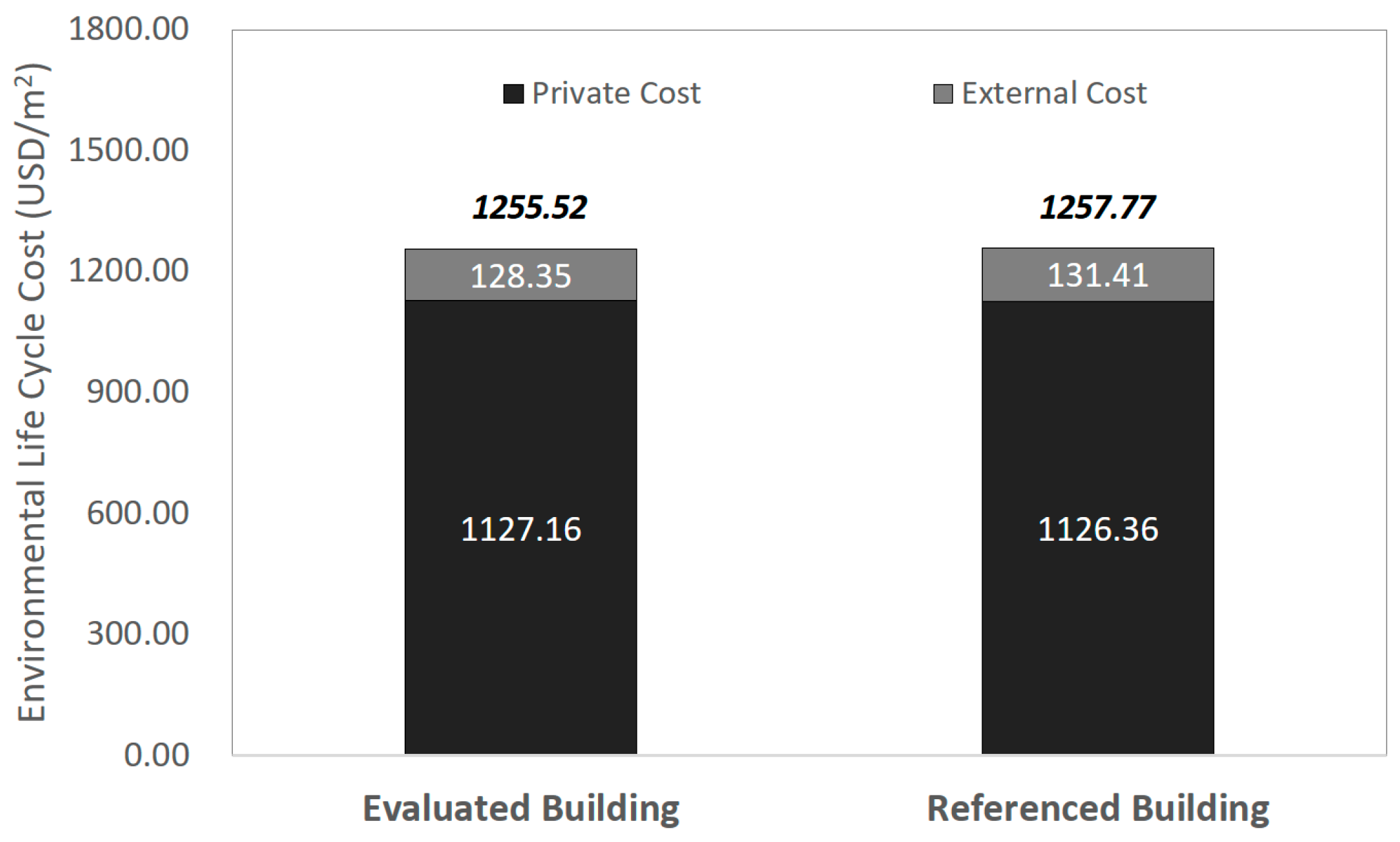

4.5.3. Environmental Life Cycle Cost

5. Discussion

6. Conclusions

- We established an equation for the systematic evaluation of ELCC in the early planning stage of a construction project by considering the MWTP of the KOLID as external costs, and developed a streamlined ELCC model for buildings.

- As the major cost categories for the streamlined ELCC model for buildings in the early planning stage of a construction project, we selected direct construction, operation energy, and maintenance costs as the scope of the private cost evaluation, and the corresponding costs in the construction, operation energy consumption, and maintenance stages as the scope of the external cost evaluation.

- By analyzing the direct construction costs of six buildings constructed in Korea, we extracted 10 building materials that accounted for over 95% of the total direct construction cost: concrete, rebar, glass, concrete brick insulation, gypsum board, window frame, stone, tile, and paint.

- We verified the applicability of the streamlined ELCC model for buildings developed in this study by performing quantitative ELCC evaluations on two apartment buildings with different structure types and compared their private and external costs in a case study.

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Bagheri, A.; Hjorth, P. Planning for Sustainable Development: A Paradigm Shift towards a Process-Based Approach. Sustain. Dev. 2007, 15, 83–96. [Google Scholar] [CrossRef]

- Gorobets, A. Eco-centric policy for sustainable development. J. Clean. Prod. 2014, 64, 654–655. [Google Scholar] [CrossRef]

- Braganca, L.; Mateus, R.; Koukkari, H. Building Sustainability Assessment. Sustainability 2010, 2, 2010–2023. [Google Scholar] [CrossRef]

- Castro Marins, K. Comparative assessment of sustainability strategies applied to urban neighbourhoods in Brazil, Germany and Sweden. Int. J. Sustain. Build. Technol. Urban Dev. 2017, 8, 195–207. [Google Scholar]

- Vrieze, R.; Moll, H. An analytical approach towards sustainability-centered guidelines for Dutch primary school building design. Int. J. Sustain. Build. Technol. Urban Dev. 2017, 8, 93–124. [Google Scholar]

- The World Commission on Environment and Development (WCED). Our Common Future: Report of the World Commission on Environment and Development. Available online: http://www.un-documents.net/our-common-future.pdf (accessed on 26 April 2018).

- Georgiadou, M.; Hacking, T.; Guthrie, P. A conceptual framework for future-proofing the energy performance of buildings. Energy Policy 2012, 47, 145–155. [Google Scholar] [CrossRef]

- Hacking, T.; Guthrie, P. A framework for clarifying the meaning of Triple Bottom-Line, Integrated, and Sustainability Assessment. Environ. Impact Assess. Rev. 2008, 28, 73–89. [Google Scholar] [CrossRef]

- Hu, M.; Kleijn, R.; Bozhilova-Kisheva, K.; Maio, F.D. An approach to LCSA: The case of concrete recycling. Int. J. Life Cycle Assess 2013, 18, 1793–1803. [Google Scholar] [CrossRef]

- Foolmaun, R.; Ramjeawon, T. Life cycle sustainability assessments (LCSA) of four disposal scenarios for used polyethylene terephthalate (PET) bottles in Mauritius. Int. J. Life Cycle Assess 2013, 15, 783–806. [Google Scholar] [CrossRef]

- Vinyes, E.; Oliver-Solà, J.; Ugaya, C.; Rieradevall, J.; Gasol, C. Application of LCSA to used cooking oil waste management. Int. J. Life Cycle Assess 2013, 18, 445–455. [Google Scholar] [CrossRef]

- Finkbeiner, M.; Schau, E.; Lehmann, A.; Traverso, M. Towards Life Cycle Sustainability Assessment. Sustainability 2010, 2, 3309–3322. [Google Scholar] [CrossRef]

- UNEP. Towards a Life Cycle Sustainability Assessment; UNEP: Nairobi, Kenya, 2011. [Google Scholar]

- Hunkeler, D.; Lichtenvort, K.; Rebitzer, G.; Ciroth, A.; Huppers, G.; Klopffer, W.; Rudenauer, I.; Steen, B.; Swarr, T. Environmental Life Cycle Costing; SETAC: New York, NY, USA, 2008. [Google Scholar]

- Swarr, T. Environmental Life Cycle Costing: A Code of Practice; SETAC: New York, NY, USA, 2011. [Google Scholar]

- Rodrigues, C.; Freire, F. Building retrofit addressing occupancy: An integrated cost and environmental life-cycle analysis. Energy Build. 2017, 140, 388–398. [Google Scholar] [CrossRef]

- Robati, M.; McCarthy, T.J.; Kokogiannakis, G. Integrated life cycle cost method for sustainable structural design by focusing on a benchmark office building in Australia. Energy Build. 2018, 166, 525–537. [Google Scholar] [CrossRef]

- Chou, J.S.; Yeh, K.C. Life cycle carbon dioxide emissions simulation and environmental cost analysis for building construction. J. Clean. Prod. 2015, 101, 137–147. [Google Scholar] [CrossRef]

- Islam, H.; Jollands, M.; Setunge, S. Life cycle assessment and life cycle cost implication of residential buildings—A review. Renew. Sustain. Energy Rev. 2015, 42, 129–140. [Google Scholar] [CrossRef]

- Kim, T.H.; Tae, S.H. Proposal of environmental impact assessment method for concrete in South Korea: An application in LCA (life cycle assessment). Int. J. Environ. Res. Public Health 2016, 13, 1074. [Google Scholar] [CrossRef] [PubMed]

- Zuo, J.; Zhao, Z.Y. Green building research–current status and future agenda: A review. Renew. Sustain. Energy Rev. 2014, 30, 271–281. [Google Scholar] [CrossRef]

- Shin, S. Environmental Performance Evaluation and Design Techniques for Environment Friendly Buildings; Kimoondang Publishing: Seoul, Korea, 2007. [Google Scholar]

- Lee, S.; Lee, B.; Kim, J.; Kim, J. A Financing Model to Solve Financial Barriers for Implementing Green Building Projects. Sci. World J. 2013, 2013, 240394. [Google Scholar] [CrossRef] [PubMed]

- Kim, S.; Lee, S.; Na, Y.; Kim, J.T. Conceptual model for LCC-based LCCO2 analysis of apartment buildings. Energy Build 2013, 64, 285–291. [Google Scholar] [CrossRef]

- Korea Exchange. Marketdata. Available online: http://marketdata.krx.co.kr/mdi#document=070301 (accessed on 26 April 2018).

- Anderson, B.; Maria, C. Abatement and Allocation in the Pilot Phase of the EU ETS. Environ. Res. Econ. 2011, 48, 83–103. [Google Scholar] [CrossRef]

- Hintermann, B. Allowance price drivers in the first phase of the EU ETS. J. Environ. Econ. Manag. 2010, 59, 43–56. [Google Scholar] [CrossRef]

- Blyth, W. Coevolution of policy, market and technical price risks in the EU ETS. Energy Policy 2011, 39, 4578–4593. [Google Scholar] [CrossRef]

- Marzouk, M.; Azab, S.; Metawie, M. BIM-based approach for optimizing life cycle costs of sustainable buildings. J. Clean. Prod. 2018, 188, 217–226. [Google Scholar] [CrossRef]

- Kovacic, I.; Zoller, V. Building life cycle optimization tools for early design phases. Energy 2015, 92, 409–419. [Google Scholar] [CrossRef]

- Barg, S.; Flager, F.; Fischer, M. An analytical method to estimate the total installed cost of structural steel building frames during early design. J. Build. Eng. 2018, 15, 41–50. [Google Scholar] [CrossRef]

- Reich, M. Economic assessment of municipal waste management systems—Case studies using a combination of life cycle assessment (LCA) and life cycle costing (LCC). J. Clean. Product. 2005, 13, 253–263. [Google Scholar] [CrossRef]

- Norris, G. Integrating Life Cycle Cost Analysis and LCA. Int. J. Life Cycle Assess 2001, 6, 118–120. [Google Scholar]

- Norris, G. Integrating Economic Analysis into LCA. Environ. Qual. Manag. 2001, 10, 59–64. [Google Scholar] [CrossRef]

- Rebitzer, G.; Hunkeler, D.; Jolliet, O. LCC-The Economic Pillar of Sustainability: Methodology and Application to Wastewater Treatment. Environ. Progr. 2003, 22, 241–249. [Google Scholar] [CrossRef]

- Schmidt, W. Life Cycle Costing as Part of Design for Environment. Int. J. Life Cycle Assess 2003, 8, 167–174. [Google Scholar] [CrossRef]

- Korea Environmental Industry & Technology Institute. Development of Integrated Evaluation Technology on Product Value for Dissemination of Environmentally Preferable Products; Korea Ministry of Environment: Sejong, Korea, 2009.

- Jeon, C. A Study on the Development of Life Cycle Cost Database in Buildings. Master’s Dissertation, Mokwon University, Daejeon, Korea, 2003. [Google Scholar]

- Roh, S.; Tae, S. Building Simplified Life Cycle CO2 Emissions Assessment Tool (B-SCAT) to Support Low-Carbon Building Design in South Korea. Sustainability 2016, 8, 567. [Google Scholar] [CrossRef]

- Korea Public Procurement Service. Korea ON-Line E-Procurement System. Available online: http://www.g2b.go.kr/pt/menu/selectSubFrame.do?framesrc=/pt/menu/framePrice.do?url=http://www.g2b.go.kr/ci/co/priceGuide.do&menuId=000001 (accessed on 26 April 2018).

- Roh, S.; Tae, S.; Suk, S.J.; Ford, G. Evaluating the embodied environmental impacts of major building tasks and materials of apartment buildings in Korea. Renew. Sustain. Energy Rev. 2017, 73, 135–144. [Google Scholar] [CrossRef]

- Yoo, J.; Shin, J. Method for Estimating Energy Consumption Units Derived from Statistic Document–Focused apartment house. Arch. Inst. Korea 2014, 30, 209–217. [Google Scholar] [CrossRef]

- Korea Energy Economics Institute. Korea Energy Statistical Information System. Available online: http://www.kesis.net (accessed on 26 April 2018).

- Korea Housing Act. Korea Ministry of Land, Infrastructure and Transport. Available online: http://elaw.klri.re.kr/kor_service/lawView.do?hseq=25579&lang=ENG (accessed on 26 April 2018).

- Korea Corporate Tax Act: Korea Ministry of Strategy and Finance. Available online: http://elaw.klri.re.kr/kor_service/lawView.do?hseq=28577&lang=ENG (accessed on 26 April 2018).

- Bank of Korea. Korean Stat 100 of Economic Statistics System (ECOS). Available online: http://ecos.bok.or.kr/jsp/vis/keystat/index_e.html#/key (accessed on 26 April 2018).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Classification | Items | ||

|---|---|---|---|

| Initial investment costs | Planning & design costs | Planning costs | Basic design costs |

| Design costs | Execution design costs | ||

| Direct construction costs | Material costs | Materials, equipment, others | |

| Labor costs | Labor costs included in construction costs | ||

| Miscellaneous expenses | Various indirect costs, supervision costs, etc. | ||

| Operation costs | Operation energy costs | Electricity bills | Electricity bills for air conditioning/hot water supply |

| Gas bills | Gas bills for air conditioning/hot water supply | ||

| District heating & cooling bills | District heating & cooling bills | ||

| Water & sewage bills | Water & sewage bills | ||

| Maintenance costs | Repair parts costs | Repair & consumable parts costs | |

| Replacement costs | Replacement costs, such as equipment & piping | ||

| General management costs | Taxes | Acquisition & registration taxes on buildings | |

| Insurance premiums | Fire insurance premium | ||

| Labor costs | Labor costs for general management | ||

| Destruction costs | Destruction costs | Destruction costs | Destruction costs of a building |

| Residual values | Residual values of a building | ||

| Other costs | Support funds | Various support funds | Support funds for electricity provider, etc. |

| Classification | Building “A” | Building “B” | Building “C” | Building “D” | Building “E” | Building “F” |

|---|---|---|---|---|---|---|

| Location | Seoul, Korea | Seoul, Korea | Seoul, Korea | Seoul, Korea | Seoul, Korea | Seoul, Korea |

| Break ground | Jan. 2009 | Oct. 2009 | Jan. 2012 | Jan. 2012 | Oct. 2011 | Jun. 2011 |

| Completion | Jan. 2011 | Sep. 2011 | Jun. 2014 | Jun. 2014 | Jun. 2014 | Dec. 2013 |

| Structure | Reinforced concrete (RC) structure, (Wall type) | RC structure, (Wall type) | RC structure, (Rigid-frame) | RC structure, (Rigid-frame) | RC structure, (Flat plate) | RC structure, (Flat plate) |

| Lot area | 10,780 m2 | 40,424 m2 | 75,115 m2 | 56,336 m2 | 72,608 m2 | 108,163 m2 |

| Building area | 2513 m2 | 10,210 m2 | 19,480 m2 | 16,320 m2 | 14,172 m2 | 18,658 m2 |

| Gross floor area | 83,883 m2 | 68,612 m2 | 227,466 m2 | 208,393 m2 | 190,866 m2 | 267,015 m2 |

| Building coverage ratio | 23% | 25% | 26% | 29% | 20% | 17% |

| Floor area ratio | 564% | 169% | 201% | 239% | 185% | 172% |

| Classification | Unit | Safety Guard | |||

|---|---|---|---|---|---|

| Human Health (DALY/Unit) | Social Assets (USD/Unit) | Biodiversity (EINES/Unit) | Primary Production (NPP/Unit) | ||

| Ready-mixed concrete | m3 | 2.47 × 10−4 | 5.31 × 100 | 1.48 × 10−13 | 4.63 × 101 |

| Rebar | kg | 3.98 × 10−7 | 8.47 × 10−3 | 2.48 × 10−16 | 4.62 × 10−2 |

| Glass | kg | 1.44 × 10−6 | 3.00 × 10−2 | 7.01 × 10−16 | 1.74 × 10−1 |

| Gypsum board | kg | 2.09 × 10−7 | 4.52 × 10−3 | 9.70 × 10−17 | 2.57 × 10−2 |

| Electricity | kWh | 2.72 × 10−7 | 5.92 × 10−3 | 2.86 × 10−16 | 3.26 × 10−2 |

| Safety Guard | Description | Unit | MWTP (USD/Unit) |

|---|---|---|---|

| Human health | Mortality, or diseases or disorders leading to mortality | DALY (disability adjusted life year) | 26,355.14 |

| Social assets | Agricultural products, fishery resources, forestry resources, mineral resources, fossil fuel resources | KRW (Korean Won, economic costs) | 0.000935 |

| Biodiversity | Extinction of vascular plant species water-borne plants | EINES (expected increase in number of extinct species) | 531.78 |

| Primary production | Land plants and marine plankton | NPP (net primary production) | 46.07 |

| Classification | Evaluated Building | Referenced Building |

|---|---|---|

| Purpose | Apartment building | Apartment building |

| Structure | RC structure, flat plate | RC structure, wall type |

| Plane form | Plate-type, 4 units per story | Plate-type, 4 units per story |

| Exclusive area per unit | 59.77 | 59.99 |

| Total exclusive area | 3108.04 | 3119.48 |

| Gross floor area | 4024.17 | 4039.56 |

| Number of stories | 15 | 15 |

| Classification | Unit | Evaluated Building | Referenced Building | |

|---|---|---|---|---|

| Input quantity of major building materials | Ready-mixed concrete | m3/m2 | 0.68 | 0.92 |

| Rebar | kg/m2 | 128.63 | 108.54 | |

| Glass | kg/m2 | 6.92 | 7.18 | |

| Concrete brick | kg/m2 | 88.87 | 86.24 | |

| Insulation | kg/m2 | 1.68 | 1.65 | |

| Gypsum board | kg/m2 | 2.51 | 2.74 | |

| Window frame | kg/m2 | 5.51 | 5.46 | |

| Stone | kg/m2 | 4.68 | 4.84 | |

| Tile | kg/m2 | 5.16 | 5.08 | |

| Paint | kg/m2 | 1.36 | 1.42 | |

| Annual operation energy consumption | Electricity | kWh/m2, year | 27.50 | 27.50 |

| City gas | kWh/m2, year | 99.40 | 99.40 | |

| Year | Fixed Deposit Interest Rate (%) | Inflation Rate (%) | Real Interest Rate (%) |

|---|---|---|---|

| 2008 | 5.67 | 4.70 | 0.93 |

| 2009 | 3.23 | 2.80 | 0.42 |

| 2010 | 3.18 | 3.00 | 0.17 |

| 2011 | 3.69 | 4.00 | −0.30 |

| 2012 | 3.43 | 2.20 | 1.20 |

| 2013 | 2.73 | 1.30 | 1.41 |

| 2014 | 2.43 | 1.30 | 1.12 |

| 2015 | 1.74 | 0.70 | 1.03 |

| 2016 | 1.48 | 1.00 | 0.48 |

| 2017 | 1.56 | 1.90 | −0.33 |

| Average | 2.91 | 2.29 | 0.61 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Roh, S.; Tae, S.; Kim, R. Development of a Streamlined Environmental Life Cycle Costing Model for Buildings in South Korea. Sustainability 2018, 10, 1733. https://doi.org/10.3390/su10061733

Roh S, Tae S, Kim R. Development of a Streamlined Environmental Life Cycle Costing Model for Buildings in South Korea. Sustainability. 2018; 10(6):1733. https://doi.org/10.3390/su10061733

Chicago/Turabian StyleRoh, Seungjun, Sungho Tae, and Rakhyun Kim. 2018. "Development of a Streamlined Environmental Life Cycle Costing Model for Buildings in South Korea" Sustainability 10, no. 6: 1733. https://doi.org/10.3390/su10061733

APA StyleRoh, S., Tae, S., & Kim, R. (2018). Development of a Streamlined Environmental Life Cycle Costing Model for Buildings in South Korea. Sustainability, 10(6), 1733. https://doi.org/10.3390/su10061733