3.3. Model Establishment

Assumption 1: The two participating groups in the game model are governments and private investors and both of them are bounded rational groups. The governments’ strategy set is (weak supervision, strong supervision); while the private investors’ strategy for defaulting behaviors set is (default, no to default). As it is known to all, behaviors which default laws, regulations and contracts exert negative impact on the outcome of PPP projects. Players from both groups make independent decisions based on their own judgments after comparing the values of different strategies. During the entire game process, players make adjustments to their strategy choices.

Assumption 2: is assumed as the project output of private investors when the private investors do not conduct defaulting behaviors, the income of the private investors is expressed as , where means subsidy and fixed payment given by the governments when certain basic conditions are satisfied. means the sharing ratio of project output for private investors and . In some PPP projects, apart from the fixed payment, the private investors can also gain a certain sharing ratio of the output of projects. Therefore, the output assigned to the governments is . It should be noticed that when only fixed payments is included and no income sharing is offered to the private investors in the signed contracts, is 0 here.

Assumption 3: If private investors conduct defaulting behaviors, the governments may discover them in supervision, or may not. If the defaulting behaviors are known by the governments, the private investors will be punished. However, because of the informational asymmetry, it is possible that the governments may never discover the defaulting behaviors which have been conducted by the private investors.

is assumed as the profit that the private investors gain by conducting defaulting behaviors in PPP projects and the damage coefficient is . The output of private investors in the project will decrease by because of defaulting behaviors and therefore the output of private investors can be expressed as .

Assumption 4: Consider the incomes of both parties when the private investors conduct defaulting behaviors. When defaulting behaviors conducted by private investors are not known by the governments, the income of private investors is . However, it is also possible that the governments find the defaulting behaviors of private investors in some way. In such case, the income of private investors in this project can be expressed by , where represents the penalty coefficient of the defaulting behaviors and is a new but lower subsidies or payments offered by the governments after discovering defaulting behaviors. It can be easily known from the practice that , indicating that there is a penalty on the private investors for the defaulting behaviors discovered by the governments. This parameter in the model can be set as different values as needed. When is smaller than , there exists a fixed penalty on the fixed payment. However, when the penalty is only related to the damage of defaulting behaviors to the output of PPP project () and the penalty coefficient (), is equal to and the penalty of defaulting behaviors is .

Assumption 5: When the governments strengthen supervision in PPP projects, the probability of discovering defaulting behaviors by the governments should be higher but in the meanwhile the strong supervision cause an increase in the supervision cost (including the human, physical and financial cost). Suppose that the governmental supervision cost under weak supervision is , the cost under strong supervision is and that .

Assumption 6: It is assumed that strong supervision may generate additional benefits for the governments as a result of hard work, such as some certain subsidies, award, or higher work efficiency which will bring other material or spiritual rewards, higher recognition and even promotion opportunities. Here, means the sum of the encouragement for strong supervision, including all sorts of material and spiritual reward and subsidies. If there is no reward or subsidy, should be set as 0. Generally speaking, is not equal to 0 in reality.

When the private investors do not conduct defaulting behaviors and the governmental supervision is weak, the income of the governments is . While the supervision of the governments is strong and the private investors choose not to perform defaulting behaviors, there will be no defaulting behavior discovered, so the income of the governments will be .

Assumption 7: The discovering probability of defaulting behaviors is closely related to the governments’ supervisory measures. The different discovering probabilities of defaulting behaviors under weak governmental supervision and strong governmental supervision are respectively assumed as and and it is obvious that is smaller than .

Assumption 8: The public participation in supervision is also considered in this model. The probability of the defaulting behaviors discovered by some citizens is assumed as . When some citizens find the defaulting behaviors, they will use new media to publish news related to the discovered defaulting behaviors so as to expose the private investors and protect the public benefit and then the governments and the public will also know the defaulting behaviors. The private investors will also be punished. Only if the defaulting behaviors are neither discovered by the governments nor published by the new media, the private investors will not be punished.

According to the Assumptions 7 and 8, it can be derived that when the private investors conduct defaulting behaviors and the governments conduct weak supervision, the probability that both of the governments and citizens fail to discover defaulting behaviors is , representing that the conducted defaulting behaviors are not found, there will be no punishment on private investors. Under such situation, private investors successfully make unjust benefit. If there is no defaulting behavior discovered under weak supervision, the income of the governments is expressed as .

On the contrary, if the defaulting behaviors are found by the governments, various measures will be taken to punish the private investors. When the defaulting behaviors are discovered first by some citizens, after they publish news though new media, the governments and the public will know the defaulting behaviors from the news. The possibility of this case under weak supervision is , representing that the public knows the defaulting behaviors first from the new media rather than governments. At this time, the public will be skeptical about the supervision efficiency of the governments, so it will impair the reputation and public trust of the governments. The reputation lost value is assumed as . After discovering the defaulting behaviors, the governments will punish private investors and publish relevant news and the income of the governments under weak supervision will be . If the governments find and expose the defaulting behaviors not later than the new media, there will be no reputation lost. The possibility of this situation is and the income of the governments under weak supervision is . According to the above analysis, when the defaulting behaviors are performed by private investors under weak governmental supervision and public supervision, the mean income of governments is expressed as . Similarly, under strong governmental supervision and public supervision, the mean income of governments is .

When the private investors conduct defaulting behaviors under weak governmental supervision and public supervision, it can be derived that the expected income of private investors is and that the expected income of private investors when conducting defaulting behaviors under strong governmental supervision and public supervision is .

Assumption 9: In addition, and respectively mean the proportions of strong governmental supervision and weak governmental supervision. is the proportion that private investors do not carry out defaulting behaviors in PPP projects and therefore the probability of conducting defaulting behaviors is . It can be known from the definitions of and that and .

Based on the above analysis, the mean incomes of both governments and private investors can be analyzed when different strategies are adopted. When making the decisions about supervision strategy, the governments do not know whether private investors will carry out defaulting behaviors. Therefore, each of the two strategies is likely to be chosen. If strong supervision is adopted, the governments can discover private investors’ defaulting behaviors with a higher probability. Penalties on private investors can compensate for the loss caused by the defaulting behaviors to some extent. However, it is also possible that after strengthening supervision and paying higher supervision costs, the governments still do not discover the defaulting behaviors of the private investors in this project. Suppose that

represents the expected income when the governments choose weak supervision,

indicates the expected income of the governments under strong supervision and the overall mean income of governments is

. The three parameters can be respectively calculated by Equations (1)–(3).

The private investors are in pursuit of maximization of personal profits, which motivates the private investors in the PPP project to obtain unjust profits by engaging in defaulting behaviors. Meanwhile, private investors also know that the governments will supervise their behavior but on one hand the private investors are not sure whether the governments will adopt weak supervision or strong supervision; and on the other hand, even if the governments adopt strong supervision, it is possible that the defaulting behaviors are not discovered. If the governments discover the defaulting behaviors, there will be punishment on the private investors. When the defaulting behaviors are not discovered, the private investors can benefit from the defaulting behaviors, so the private investors may still have a fluky psychology to perform defaulting behaviors. Suppose that

denotes the expected income of private investors that can be obtained when not conducting defaulting behaviors,

is the expected income of private investors when conducting defaulting behaviors and

represents the overall mean income of private investors.

,

and

can be calculated according to Equations (4)–(6).

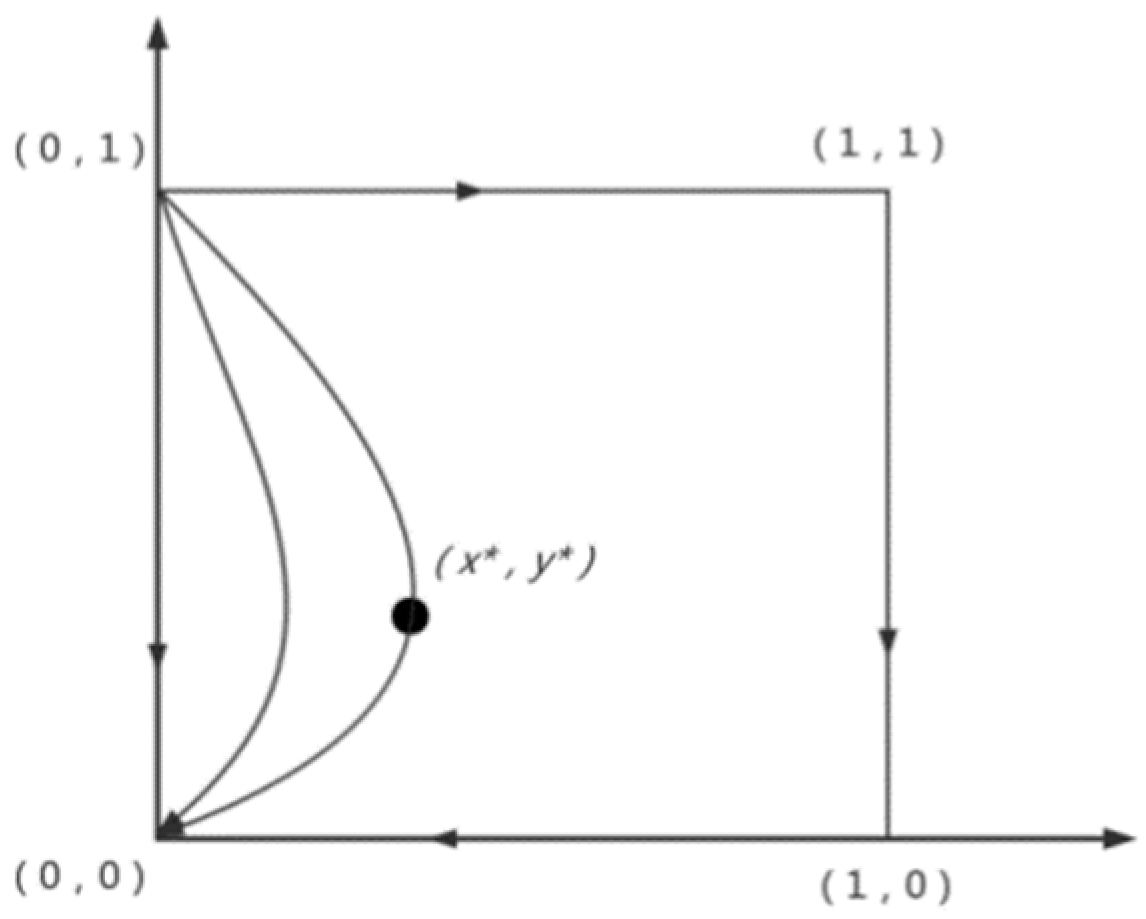

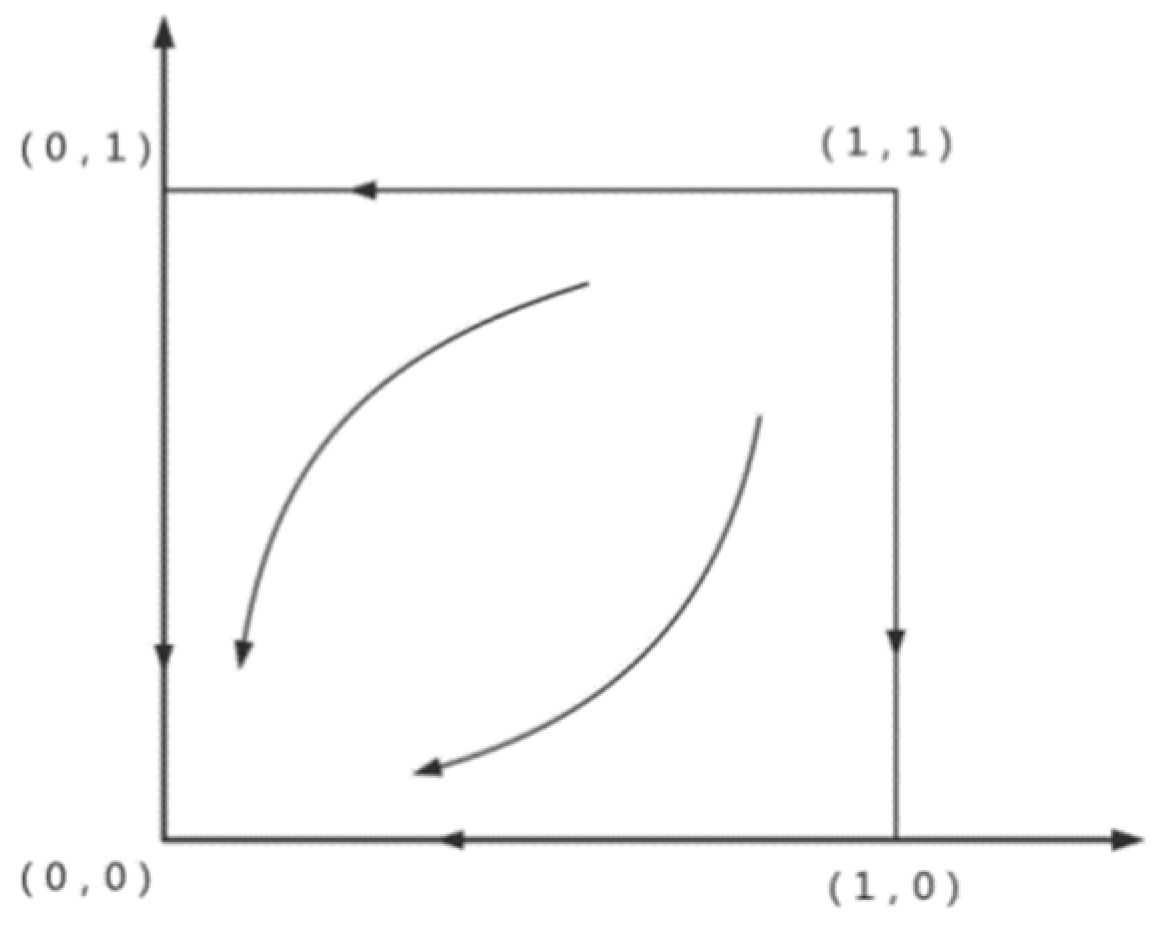

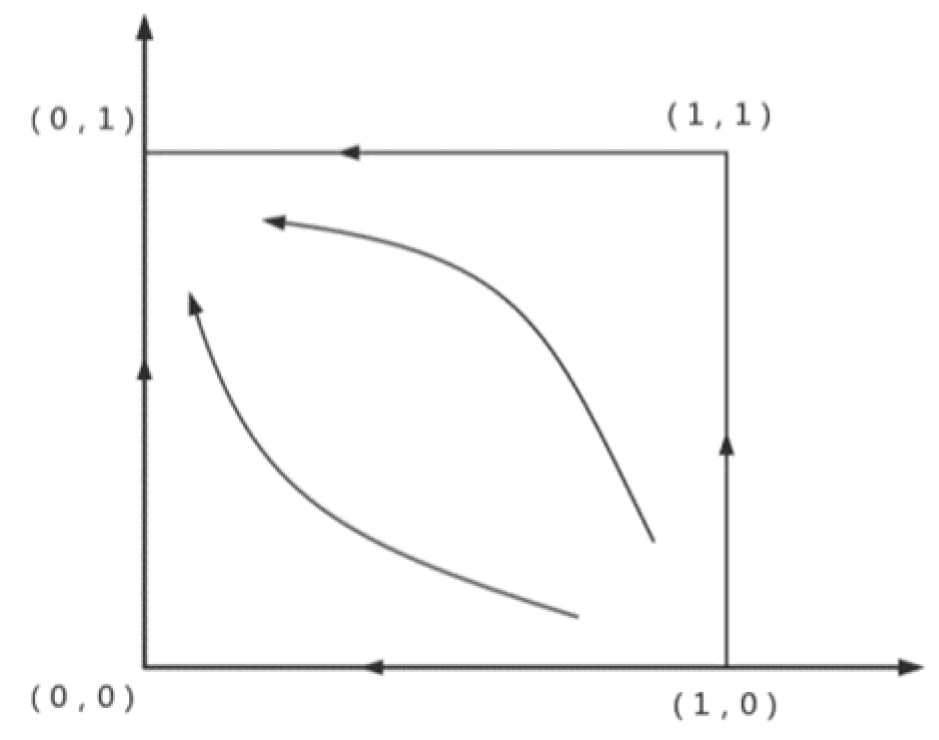

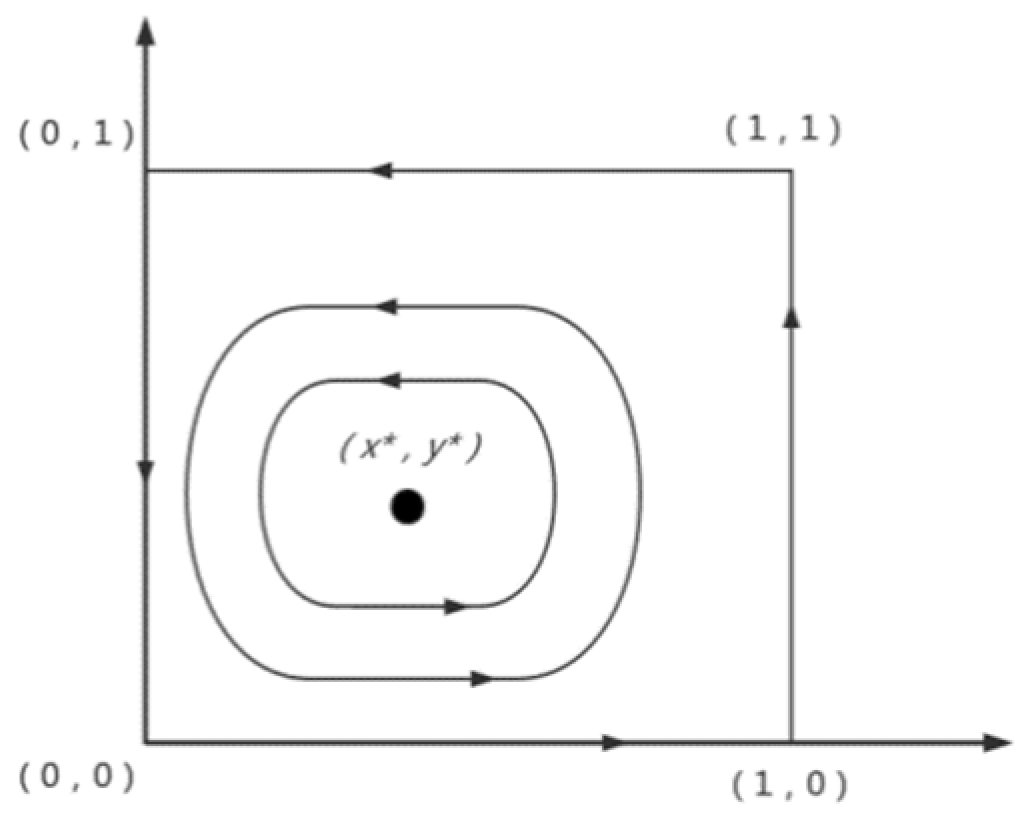

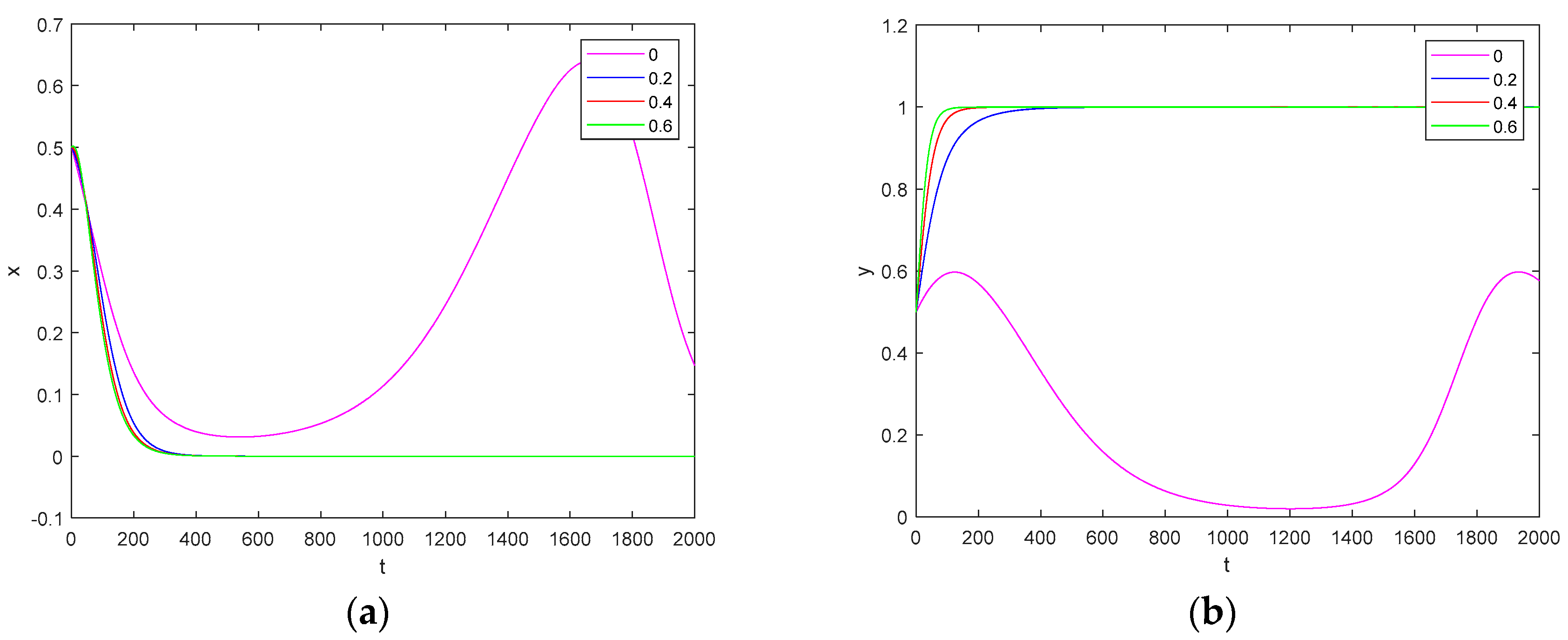

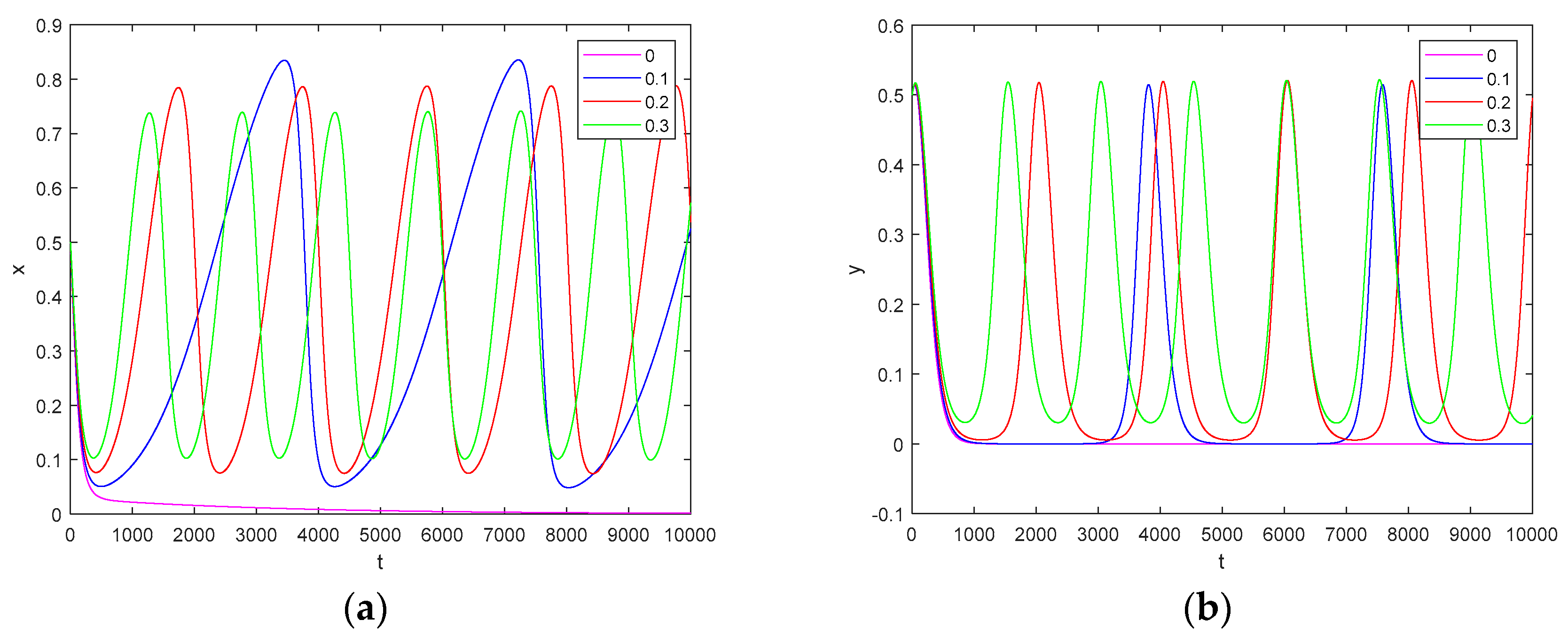

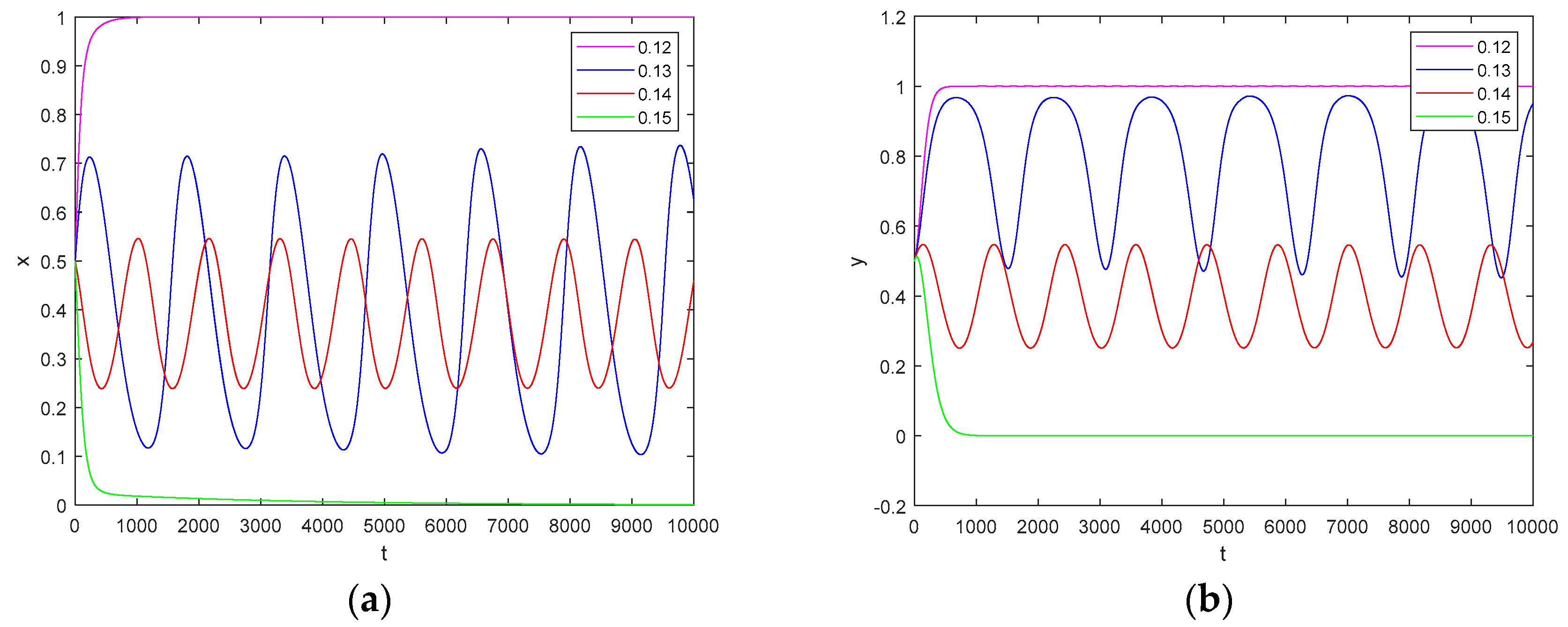

The dynamic changes in the proportions of different strategies chosen by the both parties throughout the entire process are the core of the evolutionary game theory. The change rates of proportions can represent the main feature of the dynamic change. The replicator dynamic equation that determines the proportion of strong governmental supervision can be expressed as Equation (7), where

denotes time and

means the change rate of proportion of strong supervision chosen by the governments (

).

Likewise, as for the private investors, the replicator dynamic equation that determines the change in the proportion of not conducting defaulting behaviors is expressed as Equation (8).

Based on the above analysis, a two-dimensional dynamic system can be derived, as shown in Equation (9).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}