Towards Economic Corporate Sustainability in Reporting: What Does Earnings Management around Equity Offerings Mean for Long-Term Performance?

Abstract

:1. Introduction

2. Earnings Quality around Going Public: The Existing Evidence

3. Sample and Methodology

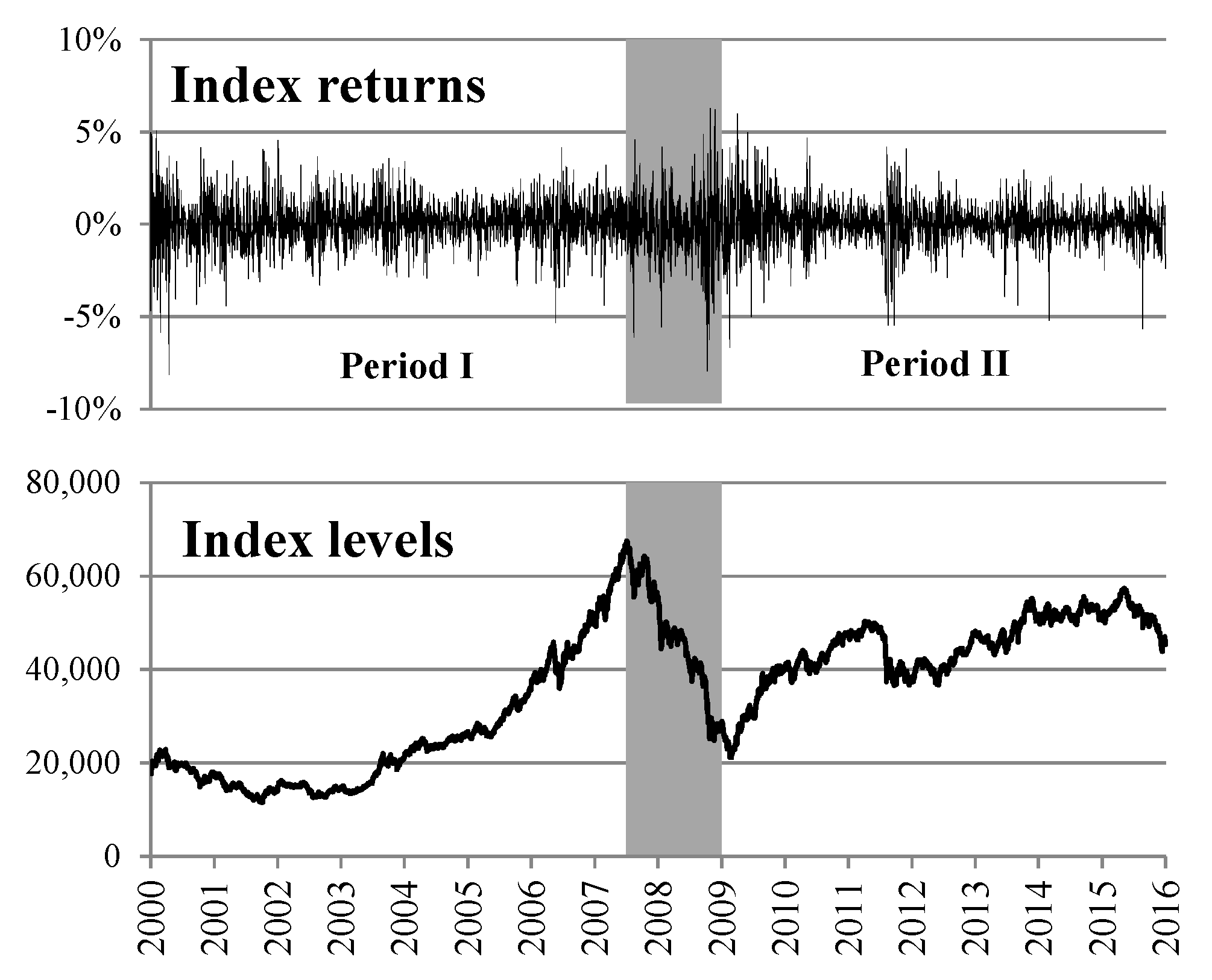

3.1. Sample Description

3.2. Methodology

4. Results and Discussions

4.1. Earnings Management around IPO

4.2. Long-Term IPO Performance

4.3. The Relation between Earnings Quality and Market Performance

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Sustainability Accounting and Reporting; Schaltegger, S.; Bennett, M.; Burritt, R. (Eds.) Springer: Dordrecht, The Netherlands, 2006. [Google Scholar]

- Clark, G.L.; Feiner, A.; Viehs, M. From the Stockholder to the Stakeholder: How Sustainability Can Drive Financial Outperformance. SSRN J. 2014. [Google Scholar] [CrossRef]

- Herzig, C.; Schaltegger, S. Corporate Sustainability Reporting. An Overview. In Sustainability Accounting and Reporting; Schaltegger, S., Bennett, M., Burritt, R., Eds.; Springer: Dordrecht, The Netherlands, 2006; pp. 301–324. [Google Scholar]

- Berglof, E. Reforming corporate governance: Redirecting the European agenda. Econ. Policy 1997, 12, 91–123. [Google Scholar] [CrossRef]

- Berglof, E. What do Firms Disclose and Why? Enforcing Corporate Governance and Transparency in Central and Eastern Europe. Oxf. Rev. Econ. Pol. 2005, 21, 178–197. [Google Scholar] [CrossRef]

- Jiang, Y.; Yu, M.; Hashmi, S. The Financial Crisis and Co-Movement of Global Stock Markets—A Case of Six Major Economies. Sustainability 2017, 9, 260. [Google Scholar] [CrossRef]

- Aharony, J.; Lin, C.-J.; Loeb, M.P. Initial Public Offerings, Accounting Choices, and Earnings Management. Contemp. Account. Res. 1993, 10, 61–81. [Google Scholar] [CrossRef]

- Friedlan, J.M. Accounting Choices of Issuers of Initial Public Offerings. Contemp. Account. Res. 1994, 11, 1–31. [Google Scholar] [CrossRef]

- Teoh, S.H.; Welch, I.; Wong, T.J. Earnings Management and the Long-Run Market Performance of Initial Public Offerings. J. Financ. 1998, 53, 1935–1974. [Google Scholar] [CrossRef] [Green Version]

- Teoh, S.H.; Wong, T.J.; Rao, G.R. Are Accruals during Initial Public Offerings Opportunistic? Rev. Account. Stud. 1998, 3, 175–208. [Google Scholar] [CrossRef]

- DuCharme, L.L.; Malatesta, P.H.; Sefcik, S.E. Earnings Management: IPO Valuation and Subsequent Performance. J. Account. Aud. Financ. 2001, 16, 369–396. [Google Scholar] [CrossRef] [Green Version]

- Ahmad-Zaluki, N.A.; Campbell, K.; Goodacre, A. Earnings management in Malaysian IPOs: The East Asian crisis, ownership control, and post-IPO performance. Int. J. Account. 2011, 46, 111–137. [Google Scholar] [CrossRef] [Green Version]

- Ritter, J.R. The Long-Run Performance of initial Public Offerings. J. Financ. 1991, 46, 3–27. [Google Scholar] [CrossRef]

- Loughran, T.; Ritter, J.R. The New Issues Puzzle. J. Financ. 1995, 50, 23–51. [Google Scholar] [CrossRef] [Green Version]

- Brav, A.; Gompers, P.A. Myth or Reality? The Long-Run Underperformance of Initial Public Offerings: Evidence from Venture and Nonventure Capital-Backed Companies. J. Financ. 1997, 52, 1791–1821. [Google Scholar] [CrossRef]

- Stehle, R.; Ehrhardt, O.; Przyborowsky, R. Long-run stock performance of German initial public offerings and seasoned equity issues. Eur. Financ. Manag. 2000, 6, 173–196. [Google Scholar] [CrossRef] [Green Version]

- Drobetz, W.; Kammermann, M.; Wälchli, U. Long-Run Performance of Initial Public Offerings: The Evidence for Switzerland. Schmalenbach Bus. Rev. 2005, 57, 253–275. [Google Scholar] [CrossRef] [Green Version]

- Hotchkiss, E.S.; Strickland, D. Does Shareholder Composition Matter? Evidence from the Market Reaction to Corporate Earnings Announcements. J. Financ. 2003, 58, 1469–1498. [Google Scholar] [CrossRef]

- Francis, J.; Schipper, K.; Vincent, L. Expanded Disclosures and the Increased Usefulness of Earnings Announcements. Account. Rev. 2002, 77, 515–546. [Google Scholar] [CrossRef]

- Bernard, V.L.; Thomas, J.K. Post-Earnings-Announcement Drift: Delayed Price Response or Risk Premium? J. Account. Res. 1989, 27, 1. [Google Scholar] [CrossRef]

- Francis, J.; Lafond, R.; Olsson, P.; Schipper, K. Information Uncertainty and Post-Earnings-Announcement-Drift. J. Bus. Financ. Account. 2007, 34, 403–433. [Google Scholar] [CrossRef]

- Pevzner, M.; Xie, F.; Xin, X. When firms talk, do investors listen? The role of trust in stock market reactions to corporate earnings announcements. J. Financ. Econ. 2015, 117, 190–223. [Google Scholar] [CrossRef]

- Dechow, P.M.; Schrand, C.M. Earnings Quality; The Research Foundation of CFA Institute: Charlottesville, VA, USA, 2004. [Google Scholar]

- Healy, P.M. The effect of bonus schemes on accounting decisions. J. Account. Econ. 1985, 7, 85–107. [Google Scholar] [CrossRef]

- Guidry, F.; Leone, A.J.; Rock, S. Earnings-based bonus plans and earnings management by business-unit managers. J. Account. Econ. 1999, 26, 113–142. [Google Scholar] [CrossRef]

- DeFond, M.L.; Jiambalvo, J. Debt covenant violation and manipulation of accruals. J. Account. Econ. 1994, 17, 145–176. [Google Scholar] [CrossRef]

- Kasznik, R. On the Association between Voluntary Disclosure and Earnings Management. J. Account. Res. 1999, 37, 57. [Google Scholar] [CrossRef]

- Kothari, S.P. Capital markets research in accounting. J. Account. Econ. 2001, 31, 105–231. [Google Scholar] [CrossRef] [Green Version]

- Fields, T.D.; Lys, T.Z.; Vincent, L. Empirical research on accounting choice. J. Account. Econ. 2001, 31, 255–307. [Google Scholar] [CrossRef]

- Healy, P.M.; Wahlen, J.M. A Review of the Earnings Management Literature and Its Implications for Standard Setting. Account. Horiz. 1999, 13, 365–383. [Google Scholar] [CrossRef]

- Chan, K.; Chan, L.K.; Jegadeesh, N.; Lakonishok, J. Earnings quality and stock returns. J. Bus. 2001, 79, 1041–1082. [Google Scholar] [CrossRef]

- Davis-Friday, P.Y.; Eng, L.L.; Liu, C.-S. The effects of the Asian crisis, corporate governance and accounting system on the valuation of book value and earnings. Int. J. Account. 2006, 41, 22–40. [Google Scholar] [CrossRef]

- Ahmed, K.; Godfrey, J.M.; Saleh, N.M. Market perceptions of discretionary accruals by debt renegotiating firms during economic downturn. Int. J. Account. 2008, 43, 114–138. [Google Scholar] [CrossRef]

- Kirkpatrick, G. The corporate governance lessons from the financial crisis. Financ. Mark. Trends 2009, 1, 1–30. [Google Scholar] [CrossRef]

- Choi, J.-H.; Kim, J.-B.; Lee, J.J. Value relevance of discretionary accruals in the Asian financial crisis of 1997–1998. J. Account. Public Policy 2011, 30, 166–187. [Google Scholar] [CrossRef]

- Gajdka, J. Kształtowanie zysków w przedsiębiorstwach w kontekście kryzysu finansowego. Zesz. Nauk. Uniw. Szczec. Finans. Rynk. Finans. Ubezpieczenia 2012, nr 51, 303–311. [Google Scholar]

- Filip, A.; Raffournier, B. Financial Crisis And Earnings Management: The European Evidence. Int. J. Account. 2014, 49, 455–478. [Google Scholar] [CrossRef]

- Gómez-Bezares, F.; Przychodzen, W.; Przychodzen, J. Corporate Sustainability and Shareholder Wealth—Evidence from British Companies and Lessons from the Crisis. Sustainability 2016, 8, 276. [Google Scholar] [CrossRef]

- Cheung, A.W.K. Do Stock Investors Value Corporate Sustainability? Evidence from an Event Study. J. Bus. Ethics 2011, 99, 145–165. [Google Scholar] [CrossRef]

- Ziegler, A. Is it Beneficial to be Included in a Sustainability Stock Index? A Panel Data Study for European Firms. Environ. Resour. Econ. 2012, 52, 301–325. [Google Scholar] [CrossRef]

- Moneva, J.M.; Ortas, E. Are stock markets influenced by sustainability matter? Evidence from European companies. IJSE 2008, 1, 1. [Google Scholar] [CrossRef]

- Lassala, C.; Apetrei, A.; Sapena, J. Sustainability Matter and Financial Performance of Companies. Sustainability 2017, 9, 1498. [Google Scholar] [CrossRef]

- Oh, S.; Hong, A.; Hwang, J. An Analysis of CSR on Firm Financial Performance in Stakeholder Perspectives. Sustainability 2017, 9, 1023. [Google Scholar] [CrossRef]

- Marti, C.P.; Rovira-Val, M.R.; Drescher, L.G.J. Are Firms that Contribute to Sustainable Development Better Financially? Corp. Soc. Responsib. Environ. Manag. 2015, 22, 305–319. [Google Scholar] [CrossRef]

- Hong, N.Y.; San, O.T. Assessing the relationship among corporate governance, sustainability disclosure and financial performance. Asia Pac. Manag. Account. J. 2016, 11, 129–146. [Google Scholar]

- Maciková, L.; Smorada, M.; Dorčák, P.; Beug, B.; Markovič, P. Financial Aspects of Sustainability: An Evidence from Slovak Companies. Sustainability 2018, 10, 2274. [Google Scholar] [CrossRef]

- Wagner, M. The role of corporate sustainability performance for economic performance: A firm-level analysis of moderation effects. Ecol. Econ. 2010, 69, 1553–1560. [Google Scholar] [CrossRef]

- Stoll, H.R.; Curley, A.J. Small Business and the New Issues Market for Equities. J. Financ. Quant. Anal. 1970, 5, 309. [Google Scholar] [CrossRef]

- Ibbotson, R.G. Price performance of common stock new issues. J. Financ. Econ. 1975, 2, 235–272. [Google Scholar] [CrossRef]

- Chan, P.T.; Moshirian, F.; Ng, D.; Wu, E. The underperformance of the growth enterprise market in Hong Kong. Res. Int. Bus. Financ. 2007, 21, 428–446. [Google Scholar] [CrossRef] [Green Version]

- Cai, X.; Liu, G.S.; Mase, B. The long-run performance of initial public offerings and its determinants: The case of China. Rev. Quant. Financ. Account. 2008, 30, 419–432. [Google Scholar] [CrossRef]

- Paudyal, K.; Saadouni, B.; Briston, R. Privatisation initial public offerings in Malaysia: Initial premium and long-term performance. Pac. Basin Financ. J. 1998, 6, 427–451. [Google Scholar] [CrossRef]

- Xinping, X.; Yixia, W. The Long-run Performance of Initial Public Offerings in China. J. Emerg. Mark. Financ. 2003, 2, 181–205. [Google Scholar] [CrossRef]

- Omran, M. Underpricing and long-run performance of share issue privatizations in the Egyptian stock market. J. Financ. Res. 2005, 28, 215–234. [Google Scholar] [CrossRef]

- Banu Durukan, M. The relationship between IPO returns and factors influencing IPO performance: Case of Istanbul Stock Exchange. Manag. Financ. 2002, 28, 18–38. [Google Scholar] [CrossRef]

- Corhay, A.; Teo, S.; Tourani Rad, A. The long run performance of Malaysian initial public offerings (IPO): Value and growth effects. Manag. Financ. 2002, 28, 52–65. [Google Scholar] [CrossRef]

- Aussenegg, W. Privatization versus Private Sector Initial Public Offerings in Poland. Multinatl. Financ. J. 2000, 4, 69–99. Available online: https://ssrn.com/abstract=2627710 (accessed on 4 January 2018). [CrossRef] [Green Version]

- Jelic, R.; Briston, R. Privatisation Initial Public Offerings: The Polish Experience. Eur. Financ. Manag. 2003, 9, 457–484. [Google Scholar] [CrossRef]

- Lyn, E.O.; Zychowicz, E.J. The performance of new equity offerings in Hungary and Poland. Glob. Financ. J. 2003, 14, 181–195. [Google Scholar] [CrossRef]

- Jewartowski, T.; Lizińska, J. Short- and Long-Term Performance of Polish IPOs. Emerg. Mark. Financ. Trade 2012, 48, 59–75. [Google Scholar] [CrossRef]

- Lizińska, J.; Czapiewski, L. Performance of Polish IPO firms: Size and profitability effect. Gospod. Narodowa 2014, 1, 53–71. [Google Scholar]

- Lizińska, J.; Czapiewski, L. Is the IPO Anomaly in Poland Only Apparent or Real? In The Essence and Measurement of Organizational Efficiency; Dudycz, T., Osbert-Pociecha, G., Brycz, B., Eds.; Springer: Cham, Switzerland, 2016; pp. 175–194. [Google Scholar]

- Teoh, S.H.; Wong, T.J. Analysts’ Credulity about Reported Earnings and Overoptimism in New Equity Issues. SSRN J. 1997. [Google Scholar] [CrossRef]

- Bradshaw, M.T.; Richardson, S.A.; Sloan, R.G. Do Analysts and Auditors Use Information in Accruals? J. Account. Res. 2001, 39, 45–74. [Google Scholar] [CrossRef] [Green Version]

- Beneish, M.D. Discussion of “Are accruals during initial public offerings opportunistic?”. Rev. Account. Stud. 1998, 3, 209–221. [Google Scholar] [CrossRef]

- Ball, R.; Shivakumar, L. Earnings quality in UK private firms: Comparative loss recognition timeliness. J. Account. Econ. 2005, 39, 83–128. [Google Scholar] [CrossRef]

- Ball, R.; Shivakumar, L. Earnings quality at initial public offerings. J. Account. Econ. 2008, 45, 324–349. [Google Scholar] [CrossRef]

- Fan, Q. Earnings Management and Ownership Retention for Initial Public Offering Firms: Theory and Evidence. Account. Rev. 2007, 82, 27–64. [Google Scholar] [CrossRef]

- Armstrong, C.; Foster, G.; Taylor, D.J. Earnings management around initial public offerings: A re-examination. SSRN Electron. J. 2009. [Google Scholar] [CrossRef]

- Subramanyam, K.R. The pricing of discretionary accruals. J. Account. Econ. 1996, 22, 249–281. [Google Scholar] [CrossRef]

- Xie, H. The Mispricing of Abnormal Accruals. Account. Rev. 2001, 76, 357–373. [Google Scholar] [CrossRef]

- Wójtowicz, P. Wiarygodność sprawozdań finansowych wobec aktywnego kształtowania wyniku finansowego; Uniwersytet Ekonomiczny Kraków: Kraków, Poland, 2010. [Google Scholar]

- Brzeszczyński, J.; Gajdka, J.; Schabek, T. Earnings Management in Polish Companies. Comp. Econ. Res. 2011, 14, 55. [Google Scholar] [CrossRef]

- Czajor, P.; Michalak, J.; Waniak-Michalak, H. Influence of Economy Growth on Earnings Quality of Listed Companies in Poland. Soc. Sci. 2014, 82. [Google Scholar] [CrossRef]

- Wójtowicz, P. Earnings management to achieve positive earnings surprises in case of medium size companies listed in Poland. Int. J. Account. Econ. Stud. 2015, 3, 141–147. [Google Scholar] [CrossRef]

- Lizińska, J.; Czapiewski, L. IPO Firms’ Earnings Quality in Poland around the Crisis. Zesz. Nauk. Uniw. Szczec. Finans. Rynk. Finans. Ubezpieczenia 2016, 4, 201–212. [Google Scholar] [CrossRef]

- Lizińska, J.; Czapiewski, L. Manipulowanie zyskami przez spółki debiutujące na GPW. Ruch Praw. Èkon. I Socjol. 2016, 78, 197. [Google Scholar] [CrossRef] [Green Version]

- Lizińska, J.; Czapiewski, L. Earnings Management and the Long-Term Market Performance of Initial Public Offerings in Poland. In Finance and Sustainability: Proceedings from the Finance and Sustainability Conference, Wroclaw 2017; Bem, A., Daszyńska-Żygadło, K., Hajdíková, T., Juhász, P., Eds.; Springer International Publishing: Cham, Switzerland, 2018; pp. 121–134. [Google Scholar]

- Mizerka, J.; Lizińska, J.; Czapiewski, L.; Jewartowski, T.; Kałdoński, M. Pierwsze Oferty Publiczne w Polsce i na Świecie. Kontrowersje Wokół Anomalii Rynkowych; CeDeWu: Warszawa, Poland, 2017. [Google Scholar]

- Ljungqvist, A.; Nanda, V.; Singh, R. Hot Markets, Investor Sentiment, and IPO Pricing. J. Bus. 2006, 79, 1667–1702. [Google Scholar] [CrossRef]

- Helwege, J.; Liang, N. Initial Public Offerings in Hot and Cold Markets. J. Financ. Quant. Anal. 2004, 39, 541. [Google Scholar] [CrossRef] [Green Version]

- Tucker, J.W.; Zarowin, P.A. Does Income Smoothing Improve Earnings Informativeness? Account. Rev. 2006, 81, 251–270. [Google Scholar] [CrossRef] [Green Version]

- Sloan, R.G. Do stock prices fully reflect information in accruals and cash flows about future earnings? Account. Rev. 1996, 71, 289–315. [Google Scholar]

- Basu, S. The conservatism principle and the asymmetric timeliness of earnings1. J. Account. Econ. 1997, 24, 3–37. [Google Scholar] [CrossRef] [Green Version]

- Burgstahler, D.; Dichev, I.D. Earnings management to avoid earnings decreases and losses. J. Account. Econ. 1997, 24, 99–126. [Google Scholar] [CrossRef]

- Jones, J.J. Earnings Management during Import Relief Investigations. J. Account. Res. 1991, 29, 193. [Google Scholar] [CrossRef]

- Ronen, J.; Yaari, V. Earnings Management: Emerging Insights in Theory, Practice, and Research; Springer: New York, NY, USA, 2008. [Google Scholar]

- DeAngelo, L.E. Accounting numbers as market valuation substitutes: A study of management buyouts of public stockholders. Account. Rev. 1986, 61, 400–420. [Google Scholar]

- Dechow, P.M.; Sloan, R.G.; Sweeney, A.P. Detecting Earnings Management. Account. Rev. 1995, 70, 193–225. [Google Scholar]

- Kothari, S.P.; Leone, A.J.; Wasley, C.E. Performance matched discretionary accrual measures. J. Account. Econ. 2005, 39, 163–197. [Google Scholar] [CrossRef] [Green Version]

- Dechow, P.M.; Dichev, I.D. The Quality of Accruals and Earnings: The Role of Accrual Estimation Errors. Account. Rev. 2002, 77, 35–59. [Google Scholar] [CrossRef]

- McNichols, M.F. Discussion of the quality of accruals and earnings: Multiples. J. Account. Res. 2002, 40, 135–172. [Google Scholar]

- McNichols, M.F. Research design issues in earnings management studies. J. Account. Public Policy 2000, 19, 313–345. [Google Scholar] [CrossRef] [Green Version]

- Venkataraman, R.; Weber, J.P.; Willenborg, M. What if Auditing was Not ‘Low-Margin Business’? Auditors and Their IPO Clients as a Natural Experiment. SSRN J. 2004. [Google Scholar] [CrossRef]

- Dyllick, T.; Hockerts, K. Beyond the business case for corporate sustainability. Bus. Strat. Environ. 2002, 11, 130–141. [Google Scholar] [CrossRef]

- Fauzi, H.; Svensson, G.; Rahman, A.A. “Triple Bottom Line” as “Sustainable Corporate Performance”: A Proposition for the Future. Sustainability 2010, 2, 1345–1360. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

| 2000–2012 with Crisis Years | 2000–2012 without Crisis Years | Period I | Period II | |

|---|---|---|---|---|

| Manufacturing | 70 | 47 | 39 | 8 |

| Construction | 13 | 7 | 4 | 3 |

| Petroleum and Related Industries | 12 | 9 | 4 | 5 |

| Retail Trade | 23 | 20 | 17 | 3 |

| Wholesale Trade | 19 | 17 | 14 | 3 |

| Non-Financial services | 70 | 56 | 41 | 15 |

| Finance, Insurance and Related Business | 40 | 33 | 16 | 17 |

| Sum: Non-financial Industries | 207 | 156 | 119 | 37 |

| Sum: All Industries | 247 | 189 | 135 | 54 |

| Y − 2 | Y − 1 | Y0 | Y + 1 | Y + 2 | Y + 3 | Y + 4 | |

|---|---|---|---|---|---|---|---|

| Panel A: McNichols Model | |||||||

| Mean | −0.1058 | −0.0487 | 0.0594 | −0.0104 | −0.0134 | −0.0163 | −0.0062 |

| Median | −0.0421 | −0.0197 | 0.0461 | 0.0000 | −0.0122 | −0.0196 | −0.0097 |

| p-value (t-stud) | 0.0774 | 0.2016 | 0.0074 | 0.6265 | 0.3619 | 0.2056 | 0.7016 |

| * | *** | ||||||

| p-value (Wilc.) | 0.0452 | 0.0852 | 0.0007 | 0.4218 | 0.2624 | 0.2161 | 0.1226 |

| ** | * | *** | |||||

| p-value (CvM) | 0.0000 | 0.0000 | 0.0000 | 0.0001 | 0.0000 | 0.0062 | 0.0000 |

| *** | *** | *** | *** | *** | *** | *** | |

| St.dev. | 0.4676 | 0.4570 | 0.2623 | 0.2628 | 0.1770 | 0.1434 | 0.1747 |

| Skewness | −0.93 | −0.76 | −0.11 | 0.18 | −0.31 | −0.09 | 0.72 |

| Kurtosis | 4.28 | 7.50 | 2.14 | 2.89 | 3.36 | 0.99 | 3.83 |

| Observations | 63 | 145 | 144 | 153 | 147 | 125 | 116 |

| Panel B: Kothari, Leone, Wasley Model | |||||||

| Mean | −0.1215 | −0.0501 | 0.0406 | −0.0421 | −0.0207 | −0.0319 | −0.0029 |

| Median | −0.0902 | −0.0175 | 0.0538 | −0.0261 | −0.0144 | −0.0307 | −0.0139 |

| t-stud | ** | ** | ** | * | *** | ||

| Wilc. | *** | * | ** | ** | ** | *** | |

| CvM | *** | *** | *** | *** | *** | ** | *** |

| Observations | 64 | 140 | 147 | 157 | 158 | 141 | 132 |

| Panel C: Modified Jones Model | |||||||

| Mean | −0.0877 | 0.0132 | 0.0694 | −0.0289 | −0.0153 | −0.0233 | 0.0015 |

| Median | −0.0203 | −0.0002 | 0.0576 | −0.0127 | −0.0156 | −0.0207 | −0.0123 |

| t-stud | *** | ** | * | ** | |||

| Wilc. | ** | *** | ** | ** | |||

| CvM | *** | *** | *** | *** | *** | *** | *** |

| Observations | 130 | 149 | 149 | 158 | 159 | 143 | 134 |

| Panel D: Jones Model | |||||||

| Mean | −0.0561 | −0.0228 | 0.0708 | −0.0343 | −0.0139 | −0.0262 | −0.0033 |

| Median | −0.0271 | −0.0038 | 0.0592 | −0.0181 | −0.0164 | −0.0241 | −0.0121 |

| t-stud | ** | ** | ** | ||||

| Wilc. | ** | *** | * | * | ** | ||

| CvM | *** | *** | *** | *** | *** | *** | *** |

| Observations | 138 | 148 | 157 | 160 | 164 | 145 | 134 |

| Average for models | −0.0850 | −0.0266 | 0.0603 | −0.0291 | −0.0158 | −0.0247 | −0.0026 |

| Period I—before the Crisis | Period II—after the Crisis | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Y − 2 | Y − 1 | Y0 | Y + 1 | Y + 2 | Y + 3 | Y + 4 | Y − 2 | Y − 1 | Y0 | Y + 1 | Y + 2 | Y + 3 | Y + 4 | |

| Panel A: McNichols Model | ||||||||||||||

| Mean | −0.0592 | −0.0039 | 0.0513 | −0.0385 | −0.0223 | −0.0099 | −0.0102 | −0.0466 | −0.1457 | 0.0779 | −0.0095 | −0.0240 | −0.0152 | 0.0069 |

| Median | −0.0294 | −0.0154 | 0.0413 | −0.0352 | −0.0060 | −0.0047 | −0.0117 | −0.0432 | −0.0257 | 0.0597 | 0.0063 | −0.0259 | −0.0292 | 0.0149 |

| p-value (t-stud) | 0.3355 | 0.9287 | 0.0807 | 0.2650 | 0.2153 | 0.5404 | 0.5613 | 0.5758 | 0.1259 | 0.0074 | 0.7072 | 0.3885 | 0.3604 | 0.7303 |

| * | *** | |||||||||||||

| p-value (Wilc.) | 0.1673 | 0.3748 | 0.0312 | 0.2634 | 0.3674 | 0.5308 | 0.0739 | 0.3488 | 0.1048 | 0.0019 | 0.9493 | 0.2449 | 0.4389 | 0.7344 |

| ** | * | *** | ||||||||||||

| p-value (CvM) | 0.0000 | 0.0000 | 0.0014 | 0.0000 | 0.0000 | 0.0091 | 0.0000 | 0.0027 | 0.0000 | 0.0248 | 0.2358 | 0.3071 | 0.1027 | 0.6740 |

| *** | *** | *** | *** | *** | *** | *** | *** | *** | ** | |||||

| St.dev. | 0.3888 | 0.4327 | 0.2906 | 0.3605 | 0.1890 | 0.1611 | 0.1796 | 0.3661 | 0.6117 | 0.1840 | 0.1667 | 0.1624 | 0.0800 | 0.0580 |

| Skewness | 0.03 | 0.55 | −0.14 | −1.06 | −1.18 | 0.09 | 0.75 | 0.48 | −4.65 | 0.73 | −0.52 | 0.44 | 0.16 | −0.03 |

| Kurtosis | 4.28 | 5.37 | 1.56 | 4.47 | 4.76 | 0.89 | 3.70 | 5.24 | 26.06 | 2.70 | −0.09 | 1.23 | −0.53 | −1.33 |

| Observations | 41 | 101 | 100 | 110 | 112 | 101 | 106 | 20 | 43 | 44 | 44 | 35 | 24 | 9 |

| Panel B: Kothari, Leone, Wasley Model | ||||||||||||||

| Mean | −0.1871 | −0.0408 | 0.0258 | −0.0944 | −0.0243 | −0.0249 | −0.0133 | 0.0936 | −0.0430 | 0.0520 | 0.0133 | −0.0009 | −0.0387 | 0.0071 |

| Median | −0.1152 | −0.0142 | 0.0599 | −0.0430 | −0.0260 | −0.0224 | −0.0204 | 0.0155 | −0.0343 | 0.0332 | 0.0111 | −0.0037 | −0.0351 | 0.0047 |

| t-stud | *** | *** | * | * | *** | |||||||||

| Wilc. | *** | * | *** | ** | * | * | * | *** | ||||||

| CvM | *** | *** | *** | *** | *** | ** | *** | *** | *** | *** | ** | |||

| Observations | 41 | 99 | 103 | 114 | 114 | 106 | 108 | 20 | 42 | 43 | 44 | 45 | 33 | 24 |

| Panel C: Modified Jones Model | ||||||||||||||

| Mean | −0.0981 | 0.0245 | 0.0492 | −0.0651 | −0.0243 | −0.0180 | −0.0080 | −0.0063 | −0.0447 | 0.0528 | 0.0087 | −0.0031 | −0.0300 | 0.0105 |

| Median | −0.0171 | 0.0070 | 0.0751 | −0.0447 | −0.0321 | −0.0196 | −0.0163 | −0.0477 | −0.0147 | 0.0403 | 0.0143 | 0.0020 | −0.0212 | 0.0155 |

| t-stud | ** | ** | * | * | ** | ** | ||||||||

| Wilc. | ** | ** | ** | * | * | ** | * | |||||||

| CvM | *** | *** | *** | *** | ** | *** | *** | *** | ** | *** | ||||

| Observations | 92 | 103 | 103 | 114 | 113 | 107 | 109 | 39 | 43 | 44 | 43 | 45 | 35 | 23 |

| Panel D: Jones Model | ||||||||||||||

| Mean | −0.0693 | −0.0335 | 0.0518 | −0.0711 | −0.0225 | −0.0194 | −0.0099 | −0.0224 | −0.0244 | 0.0549 | 0.0131 | 0.0003 | −0.0302 | 0.0129 |

| Median | −0.0161 | −0.0030 | 0.0682 | −0.0402 | −0.0257 | −0.0155 | −0.0150 | −0.0556 | −0.0075 | 0.0437 | 0.0157 | 0.0000 | −0.0277 | 0.0140 |

| t-stud | *** | ** | ** | |||||||||||

| Wilc. | ** | ** | ** | * | ** | ** | ** | |||||||

| CvM | *** | *** | *** | *** | ** | ** | *** | *** | ** | ** | ||||

| Observations | 99 | 104 | 111 | 116 | 118 | 108 | 109 | 39 | 45 | 44 | 44 | 45 | 35 | 24 |

| Average for models | −0.0952 | −0.0133 | 0.0446 | −0.0675 | −0.0233 | −0.0182 | −0.0103 | −0.0015 | −0.0641 | 0.0594 | 0.0064 | −0.0059 | −0.0295 | 0.0098 |

| Y1 | Y1.5 | Y2 | Y2.5 | Y3 | Y3.5 | Y4 | |

|---|---|---|---|---|---|---|---|

| Specification A (P0) | |||||||

| Panel A: 2000–2012 | |||||||

| Mean [%] | −10.76 | −8.90 | 0.49 | −16.48 | −15.39 | −16.86 | −18.35 |

| Median [%] | −11.52 | −21.28 | −17.60 | −22.50 | −28.55 | −33.94 | −36.71 |

| p-value (t-stud) | 0.0013 | 0.0657 | 0.9485 | 0.0074 | 0.0166 | 0.0118 | 0.0142 |

| *** | * | *** | ** | ** | ** | ||

| p-value (Wilc.) | 0.0003 | 0.0005 | 0.0064 | 0.0000 | 0.0006 | 0.0002 | 0.0000 |

| *** | *** | *** | *** | *** | *** | *** | |

| p-value (CvM) | 0.2208 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| *** | *** | *** | *** | *** | *** | ||

| St.dev. [%] | 44.70 | 65.58 | 102.94 | 80.59 | 84.21 | 85.81 | 93.92 |

| Skewness | 0.39 | 1.34 | 2.42 | 1.13 | 0.72 | 0.93 | 1.33 |

| Kurtosis | 0.31 | 3.15 | 8.49 | 2.47 | 0.84 | 1.38 | 2.84 |

| Observations | 183 | 186 | 186 | 176 | 175 | 168 | 161 |

| Panel B: Period I | |||||||

| Mean [%] | −7.69 | −7.18 | 11.22 | −14.77 | −12.27 | −18.26 | −19.36 |

| Median [%] | −13.26 | −20.50 | −14.99 | −25.66 | −28.62 | −33.94 | −35.80 |

| t-stud | * | * | ** | ** | |||

| Wilc. | ** | *** | * | *** | *** | *** | *** |

| CvM | * | *** | *** | *** | *** | *** | *** |

| Observations | 131 | 132 | 133 | 124 | 126 | 126 | 123 |

| Panel C: Period II | |||||||

| Mean [%] | −15.36 | −22.70 | −19.36 | −17.37 | −23.85 | −27.57 | −31.14 |

| Median [%] | −10.77 | −25.05 | −21.20 | −18.05 | −29.61 | −37.80 | −48.68 |

| t-stud | *** | *** | ** | ** | *** | *** | ** |

| Wilc. | *** | *** | ** | ** | ** | *** | *** |

| CvM | * | ||||||

| Observations | 53 | 51 | 52 | 52 | 48 | 41 | 36 |

| Specification B (P3M) | |||||||

| Panel A: 2000–2012 | |||||||

| Mean [%] | −8.99 | −13.44 | −12.50 | −16.04 | −21.69 | −27.85 | −34.00 |

| Median [%] | −11.46 | −15.07 | −14.09 | −21.65 | −30.70 | −36.17 | −39.26 |

| t-stud | *** | *** | *** | *** | *** | *** | *** |

| Wilc. | *** | *** | *** | *** | *** | *** | *** |

| CvM | ** | ** | *** | *** | *** | ||

| Observations | 182 | 172 | 171 | 168 | 155 | 153 | 139 |

| Panel B: Period I | |||||||

| Mean [%] | −10.31 | −12.48 | −12.23 | −21.17 | −27.09 | −25.74 | −30.08 |

| Median [%] | −13.47 | −14.81 | −14.13 | −25.44 | −31.83 | −34.39 | −38.56 |

| t-stud | *** | *** | ** | *** | *** | *** | *** |

| Wilc. | *** | *** | *** | *** | *** | *** | *** |

| CvM | * | *** | *** | *** | *** | ||

| Observations | 128 | 122 | 120 | 117 | 105 | 113 | 111 |

| Panel C: Period II | |||||||

| Mean [%] | −10.14 | −15.79 | −13.14 | −10.46 | −12.68 | −16.81 | −44.97 |

| Median [%] | −7.53 | −20.22 | −13.62 | −18.91 | −26.36 | −38.02 | −39.99 |

| t-stud | * | ** | * | *** | |||

| Wilc. | * | ** | * | * | *** | ||

| CvM | ** | ** | |||||

| Observations | 52 | 50 | 51 | 49 | 43 | 42 | 27 |

| Panel A: IPOs during 2000–2012 | ||||||||||||

| Specification A | Specification B | |||||||||||

| KLW | McN | Av | KLW | McN | Av | |||||||

| P0 | P3M | P0 | P3M | P0 | P3M | P0 | P3M | P0 | P3M | P0 | P3M | |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | (12) | |

| DACC | −0.3388 | −0.4019 | −0.5720 | −0.8733 | −0.3669 | −0.5895 | ||||||

| p-value | 0.2150 | 0.1582 | 0.0931 | 0.0130 | 0.1314 | 0.0247 | ||||||

| * | ** | ** | ||||||||||

| DACC_DISC | −0.2962 | −0.2548 | −0.3291 | −0.4271 | −0.2378 | −0.321 | ||||||

| p-value | 0.0691 | 0.1447 | 0.0372 | 0.0086 | 0.1481 | 0.0737 | ||||||

| * | ** | *** | * | |||||||||

| SIZE | 0.1057 | 0.0608 | 0.1040 | 0.0342 | 0.0916 | 0.0411 | 0.1141 | 0.0653 | 0.1125 | 0.0620 | 0.0981 | 0.0449 |

| p-value | 0.0718 | 0.3207 | 0.0854 | 0.5758 | 0.1196 | 0.5156 | 0.0461 | 0.2739 | 0.0482 | 0.2862 | 0.0934 | 0.4734 |

| * | * | ** | ** | * | ||||||||

| UNDERPR | −0.2898 | −0.3142 | −0.1231 | −0.0945 | −0.4108 | −0.4884 | −0.3216 | −0.3378 | −0.2460 | −0.2509 | −0.4468 | −0.5335 |

| p-value | 0.4426 | 0.4301 | 0.7423 | 0.8052 | 0.2733 | 0.2305 | 0.3845 | 0.3924 | 0.4982 | 0.5048 | 0.2330 | 0.1919 |

| NI_CHANGE | 1.6927 | 1.1949 | 1.9575 | 1.8152 | 1.8692 | 1.6748 | 1.6020 | 0.9305 | 1.5080 | 1.1021 | 1.6139 | 1.2463 |

| p-value | 0.0674 | 0.2655 | 0.0286 | 0.0708 | 0.0417 | 0.1254 | 0.0519 | 0.3166 | 0.0631 | 0.2258 | 0.0507 | 0.1973 |

| * | ** | * | ** | * | * | * | ||||||

| LEV | −0.7499 | −0.2895 | −0.9004 | −0.4533 | −0.6346 | −0.1645 | −0.6671 | −0.2620 | −0.6400 | −0.2229 | −0.5311 | −0.1024 |

| p-value | 0.0692 | 0.5009 | 0.0317 | 0.2856 | 0.1194 | 0.7064 | 0.0922 | 0.5289 | 0.1029 | 0.5798 | 0.1801 | 0.8101 |

| * | ** | * | ||||||||||

| HH | −0.0945 | −0.0334 | −0.1763 | −0.2473 | −0.2860 | −0.3247 | −0.0957 | −0.0610 | −0.1384 | −0.1097 | −0.2700 | −0.3169 |

| p-value | 0.8560 | 0.9506 | 0.7328 | 0.6338 | 0.5831 | 0.5601 | 0.8507 | 0.9079 | 0.7840 | 0.8309 | 0.6020 | 0.5666 |

| Constant | −1.0079 | −0.7111 | −0.9105 | −0.3028 | −0.8498 | −0.4511 | −0.9894 | −0.6257 | −0.9627 | −0.5184 | −0.8529 | −0.3418 |

| p-value | 0.1479 | 0.3341 | 0.1983 | 0.6764 | 0.2181 | 0.5471 | 0.1452 | 0.3877 | 0.1530 | 0.4555 | 0.2206 | 0.6499 |

| Observations | 108 | 103 | 104 | 99 | 113 | 108 | 111 | 106 | 111 | 106 | 115 | 110 |

| Adjusted R2 | 0.0364 | −0.0159 | 0.0598 | 0.0339 | 0.0366 | 0.0200 | 0.0542 | −0.0111 | 0.0636 | 0.0369 | 0.0388 | 0.0056 |

| F Statistic | 1.6743 | 0.7342 | 2.0919 * | 1.5729 | 1.7092 | 1.3644 | 2.0511 * | 0.8087 | 2.2459 ** | 1.6696 | 1.7677 | 1.1019 |

| Panel B: IPOs before the peak of the crisis | ||||||||||||

| Specification A | Specification B | |||||||||||

| KLW | McN | Av | KLW | McN | Av | |||||||

| P0 | P3M | P0 | P3M | P0 | P3M | P0 | P3M | P0 | P3M | P0 | P3M | |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | (12) | |

| DACC | −0.5099 | −0.3876 | −0.7465 | −0.9073 | −0.4678 | −0.5337 | ||||||

| p-value | 0.0913 | 0.1664 | 0.0507 | 0.0086 | 0.0769 | 0.0419 | ||||||

| * | * | *** | * | ** | ||||||||

| DACC_DISC | −0.5299 | −0.4044 | −0.4031 | −0.4852 | −0.4636 | −0.4858 | ||||||

| p-value | 0.0058 | 0.0274 | 0.0273 | 0.0038 | 0.0164 | 0.0113 | ||||||

| *** | ** | ** | *** | ** | ** | |||||||

| SIZE | 0.1574 | 0.1426 | 0.1499 | 0.1017 | 0.1421 | 0.1200 | 0.1680 | 0.1400 | 0.1561 | 0.1337 | 0.1553 | 0.1304 |

| p-value | 0.0234 | 0.0315 | 0.0358 | 0.1188 | 0.0426 | 0.0894 | 0.0099 | 0.0255 | 0.0183 | 0.0292 | 0.0213 | 0.0551 |

| ** | ** | ** | ** | * | *** | ** | ** | ** | ** | * | ||

| UNDERPR | −0.3266 | −0.1668 | −0.0659 | 0.0431 | −0.4289 | −0.3666 | −0.4186 | −0.2997 | −0.1941 | −0.0915 | −0.5117 | −0.4800 |

| p-value | 0.4368 | 0.6742 | 0.8751 | 0.9097 | 0.3059 | 0.3818 | 0.2963 | 0.4373 | 0.6265 | 0.8030 | 0.2118 | 0.2417 |

| NI_CHANGE | 1.5756 | 0.3201 | 1.9968 | 1.2440 | 1.8437 | 0.8541 | 1.3122 | 0.4227 | 1.2565 | 0.5640 | 1.5145 | 0.7684 |

| p-value | 0.1726 | 0.7648 | 0.0713 | 0.2078 | 0.1051 | 0.4446 | 0.1809 | 0.6480 | 0.2084 | 0.5347 | 0.1259 | 0.4320 |

| * | ||||||||||||

| LEV | −0.7440 | −0.1254 | −0.8817 | −0.3662 | −0.5987 | −0.0005 | −0.7467 | −0.1851 | −0.6331 | −0.0949 | −0.5309 | 0.0352 |

| p-value | 0.1359 | 0.7864 | 0.0848 | 0.4196 | 0.2180 | 0.9992 | 0.1101 | 0.6739 | 0.1804 | 0.8246 | 0.2533 | 0.9388 |

| * | ||||||||||||

| HH | −0.1923 | −0.0311 | −0.3029 | −0.2599 | −0.3935 | −0.3193 | −0.1756 | −0.0589 | −0.3152 | −0.1961 | −0.3793 | −0.3529 |

| p-value | 0.7402 | 0.9542 | 0.6026 | 0.6182 | 0.5029 | 0.5825 | 0.7510 | 0.9107 | 0.5757 | 0.7022 | 0.5068 | 0.5340 |

| Constant | −1.5207 | −1.7158 | −1.3813 | −1.0985 | −1.3680 | −1.4116 | −1.3072 | −1.3811 | −1.3497 | −1.3563 | −1.2627 | −1.2331 |

| p-value | 0.0740 | 0.0379 | 0.1100 | 0.1701 | 0.1050 | 0.1016 | 0.0955 | 0.0744 | 0.0920 | 0.0710 | 0.1181 | 0.1332 |

| Observations | 83 | 83 | 79 | 79 | 87 | 87 | 85 | 85 | 85 | 85 | 88 | 88 |

| Adjusted R2 | 0.0710 | 0.0175 | 0.0940 | 0.0650 | 0.0674 | 0.0387 | 0.1274 | 0.0569 | 0.096 | 0.0991 | 0.0977 | 0.0645 |

| F Statistic | 2.0440 * | 1.2438 | 2.3484 ** | 1.9042 * | 2.0353 * | 1.5770 | 3.0433 *** | 1.8454 | 2.4869 ** | 2.5392 ** | 2.5706 ** | 1.9990 * |

| Panel C: IPOs after the peak of the crisis | ||||||||||||

| Specification A | Specification B | |||||||||||

| KLW | McN | Av | KLW | McN | Av | |||||||

| P0 | P3M | P0 | P3M | P0 | P3M | P0 | P3M | P0 | P3M | P0 | P3M | |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | (12) | |

| DACC | 0.6119 | −0.3509 | 0.2482 | −1.3024 | 1.0802 | −0.3377 | ||||||

| p-value | 0.4517 | 0.6732 | 0.8144 | 0.2986 | 0.2469 | 0.7641 | ||||||

| DACC_DISC | 0.2318 | −0.0694 | 0.0762 | −0.266 | 0.3002 | 0.051 | ||||||

| p-value | 0.4801 | 0.8252 | 0.8672 | 0.5411 | 0.4321 | 0.898 | ||||||

| SIZE | −0.0492 | 0.2990 | −0.0646 | 0.2858 | −0.0617 | 0.1670 | 0.0197 | 0.3251 | −0.0016 | 0.3166 | 0.0325 | 0.2128 |

| p-value | 0.7531 | 0.1188 | 0.6821 | 0.1204 | 0.6642 | 0.3218 | 0.9052 | 0.0870 | 0.9924 | 0.0913 | 0.8438 | 0.2219 |

| * | * | |||||||||||

| UNDERPR | 1.2633 | 3.0578 | 1.6399 | 2.8446 | 0.8579 | 1.3777 | 0.0815 | 2.1310 | 0.2611 | 2.3408 | −0.0932 | 0.9094 |

| p-value | 0.4611 | 0.1601 | 0.3254 | 0.1706 | 0.5624 | 0.4523 | 0.9588 | 0.2548 | 0.8717 | 0.2153 | 0.9472 | 0.5701 |

| NI_CHANGE | 0.1365 | 3.4746 | 0.0279 | 4.5896 | 0.0241 | 2.6635 | 0.7470 | 4.7335 | 0.8079 | 5.4876 | 1.0272 | 3.4781 |

| p-value | 0.9373 | 0.4099 | 0.9878 | 0.2805 | 0.9883 | 0.5425 | 0.6811 | 0.2213 | 0.6612 | 0.1717 | 0.5658 | 0.3637 |

| LEV | −0.1808 | −2.2085 | 0.0138 | −2.5688 | −0.0986 | −1.7246 | 0.0019 | −2.2622 | 0.0211 | −2.3766 | −0.0436 | −1.7762 |

| p-value | 0.8325 | 0.0552 | 0.9876 | 0.0272 | 0.9025 | 0.1110 | 0.9984 | 0.0458 | 0.9818 | 0.0381 | 0.9601 | 0.0913 |

| * | ** | ** | ** | * | ||||||||

| HH | −1.0258 | −1.8309 | −0.8982 | −1.6923 | −1.2295 | −2.0300 | −0.5406 | −2.1641 | −0.7031 | −2.1572 | −0.9301 | −2.2132 |

| p-value | 0.3619 | 0.1604 | 0.4328 | 0.1770 | 0.2564 | 0.1350 | 0.6441 | 0.0938 | 0.5551 | 0.0880 | 0.4183 | 0.0897 |

| * | * | * | ||||||||||

| Constant | 0.5268 | −2.3261 | 0.5767 | −1.9912 | 0.6518 | −0.9515 | −0.5832 | −2.4767 | −0.2343 | −2.1759 | −0.6733 | −1.4561 |

| p-value | 0.7536 | 0.2158 | 0.7363 | 0.2735 | 0.6669 | 0.5665 | 0.7524 | 0.1950 | 0.8997 | 0.2595 | 0.7177 | 0.4502 |

| Observations | 24 | 18 | 24 | 18 | 25 | 19 | 25 | 19 | 25 | 19 | 26 | 20 |

| Adjusted R2 | −0.1813 | 0.1122 | −0.2184 | 0.1852 | −0.1218 | −0.0235 | −0.2510 | 0.0764 | −0.2851 | 0.1020 | −0.2239 | −0.0206 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lizińska, J.; Czapiewski, L. Towards Economic Corporate Sustainability in Reporting: What Does Earnings Management around Equity Offerings Mean for Long-Term Performance? Sustainability 2018, 10, 4349. https://doi.org/10.3390/su10124349

Lizińska J, Czapiewski L. Towards Economic Corporate Sustainability in Reporting: What Does Earnings Management around Equity Offerings Mean for Long-Term Performance? Sustainability. 2018; 10(12):4349. https://doi.org/10.3390/su10124349

Chicago/Turabian StyleLizińska, Joanna, and Leszek Czapiewski. 2018. "Towards Economic Corporate Sustainability in Reporting: What Does Earnings Management around Equity Offerings Mean for Long-Term Performance?" Sustainability 10, no. 12: 4349. https://doi.org/10.3390/su10124349

APA StyleLizińska, J., & Czapiewski, L. (2018). Towards Economic Corporate Sustainability in Reporting: What Does Earnings Management around Equity Offerings Mean for Long-Term Performance? Sustainability, 10(12), 4349. https://doi.org/10.3390/su10124349