Managerial Humanistic Attention and CSR: Do Firm Characteristics Matter?

Abstract

1. Introduction

2. Literature Review and Research Hypothesis

2.1. Managerial Humanistic Attention and CSR

2.2. Moderating Role of Firm Characteristics

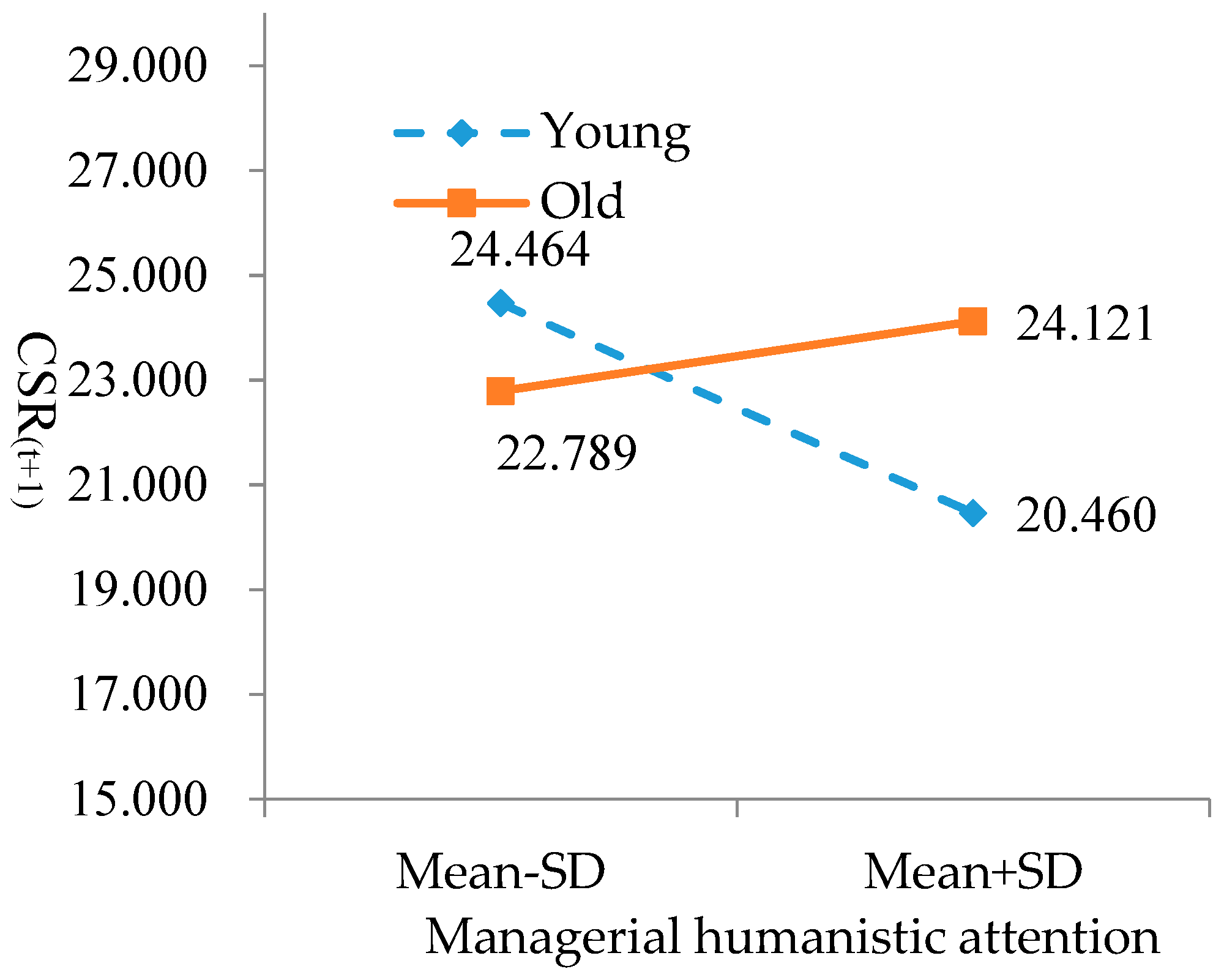

2.2.1. Firm Age

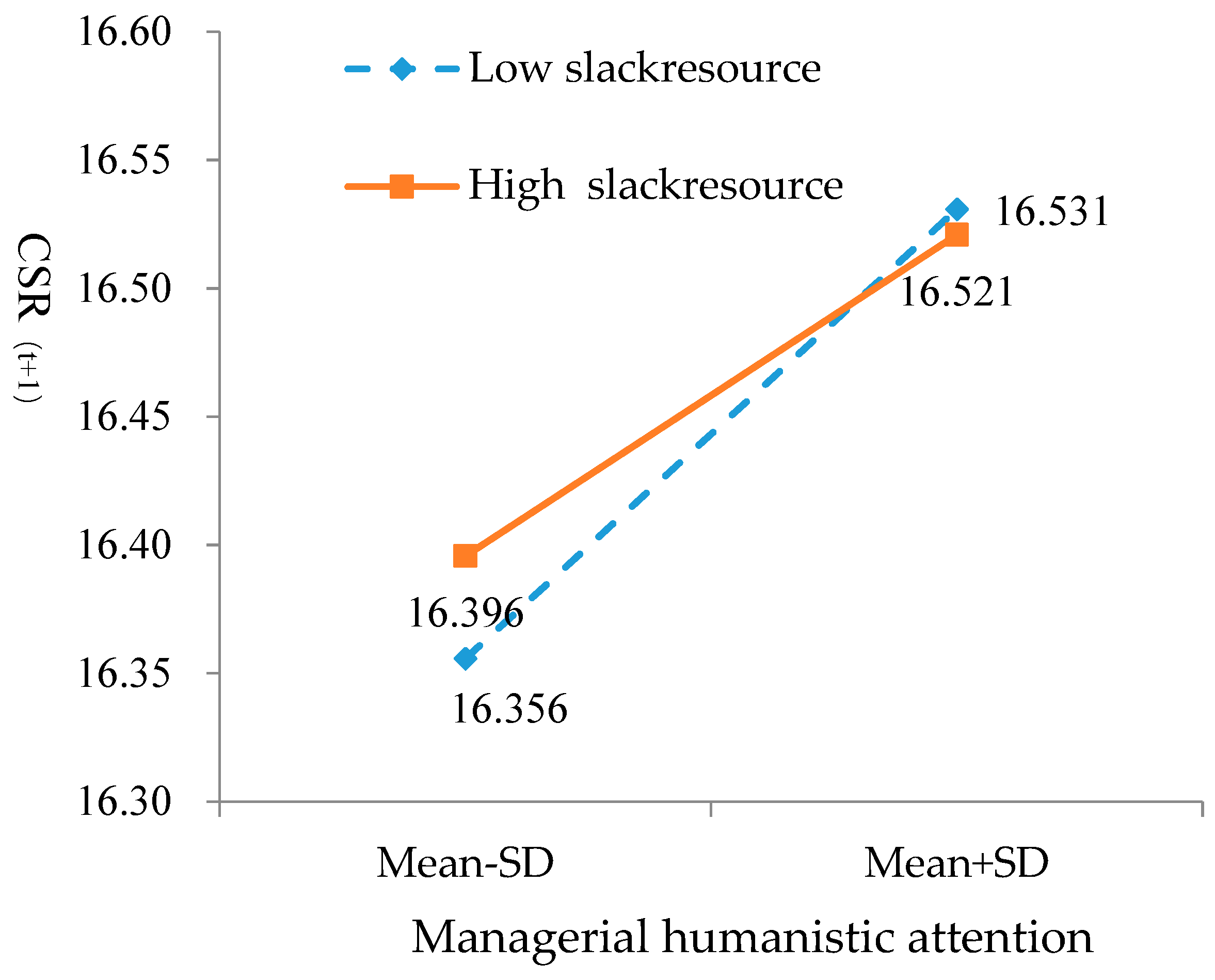

2.2.2. Slack Resources

2.2.3. Firm Size

3. Research Methodology

3.1. Sample Description and Data Resource

3.2. Definition of Main Variables

3.2.1. Managerial Humanistic Attention

3.2.2. Corporate Social Responsibility

3.2.3. Managerial Discretion

3.2.4. Control Variables

3.3. Empirical Model

4. Results and Discussion

4.1. Descriptive Statistics and Correlation Analysis

4.2. Regression Analysis

4.2.1. Managerial Humanistic Attention and CSR

4.2.2. Managerial Attention to Human, Managerial Discretion, and CSR

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Aguinis, H.; Glavas, A. What we know and don’t know about corporate social responsibility: A review and research agenda. J. Manag. 2012, 38, 932–968. [Google Scholar] [CrossRef]

- Hambrick, D.C.; Mason, P.A. Upper echelons: The organization as a reflection of its top managers. Acad. Manag. Rev. 1984, 9, 193–206. [Google Scholar] [CrossRef]

- Godos-Díez, J.L.; Martínez-Campillo, A. How Important Are CEOs to CSR Practices? An Analysis of the Mediating Effect of the Perceived Role of Ethics and Social Responsibility. J. Bus. Ethics 2011, 98, 531–548. [Google Scholar] [CrossRef]

- Groves, K.S.; LaRocca, M.A. An empirical study of leader ethical values, transformational and transactional leadership, and follower attitudes toward corporate social responsibility. J. Bus. Ethics 2011, 103, 511–528. [Google Scholar] [CrossRef]

- Muller, A.; Whiteman, G. Corporate philanthropic responses to emergent human needs: The role of organizational attention focus. J. Bus. Ethics 2016, 137, 299–314. [Google Scholar] [CrossRef]

- Agle, B.R.; Mitchell, R.K.; Sonnenfeld, J.A. Who matters to Ceos? An investigation of stakeholder attributes and salience, corpate performance, and Ceo values. Acad. Manag. J. 1999, 42, 507–525. [Google Scholar] [CrossRef]

- Zhao, X.; Chen, S.; Xiong, C. Organizational attention to corporate social responsibility and corporate social performance: The moderating effects of corporate governance. Bus. Ethics Eur. Rev. 2016, 25, 386–399. [Google Scholar] [CrossRef]

- Lerner, L.D.; Fryxell, G.E. CEO stakeholder attitudes and corporate social activity in the Fortune 500. Bus. Soc. 1994, 33, 58–81. [Google Scholar] [CrossRef]

- Mattingly, J.E. Stakeholder salience, structural development, and firm performance: Structural and performance correlates of sociopolitical stakeholder management strategies. Bus. Soc. 2004, 43, 97–114. [Google Scholar] [CrossRef]

- Flammer, C. Does corporate social responsibility lead to superior financial performance? A regression discontinuity approach. Manag. Sci. 2015, 61, 2549–2568. [Google Scholar] [CrossRef]

- Ocasio, W. Towards an attention-based view of the firm. Strateg. Manag. J. 1997, 18, 187–206. [Google Scholar] [CrossRef]

- Smith, W.K.; Tushman, M.L. Managing strategic contradictions: A top management model for managing innovation streams. Org. Sci. 2005, 16, 522–536. [Google Scholar] [CrossRef]

- Simon, H.A. Technology and environment. Manag. Sci. 1973, 19, 1110–1121. [Google Scholar] [CrossRef]

- Baysinger, B.D.; Kosnik, R.D.; Turk, T.A. Effects of board and ownership structure on corporate R&D strategy. Acad. Manag. J. 1991, 34, 205–214. [Google Scholar] [CrossRef]

- Hoskisson, R.E.; Hitt, M.A.; Johnson, R.A.; Grossman, W. Conflicting voices: The effects of institutional ownership heterogeneity and internal governance on corporate innovation strategies. Acad. Manag. J. 2002, 45, 697–716. [Google Scholar] [CrossRef]

- Kochhar, R.; David, P. Institutional investors and firm innovation: A test of competing hypotheses. Strateg. Manag. J. 1996, 17, 73–84. [Google Scholar] [CrossRef]

- Di Fabio, A. The psychology of sustainability and sustainable development for wellbeing in organizations. Front. Psychol. 2017, 8, 1534. [Google Scholar] [CrossRef] [PubMed]

- Di Fabio, A. Positive Healthy Organizations: Promoting well-being, meaningfulness, and sustainability in organizations. Front. Psychol. 2017, 8, 1938. [Google Scholar] [CrossRef] [PubMed]

- Cassirer, E.; Kristeller, P.O.; Randall, J.H. The Renaissance Philosophy of Man; University of Chicago Press: Chicago, IL, USA, 1948. [Google Scholar]

- Bantel, K.A.; Jackson, S.E. Top management and innovations in banking: Does the composition of the top team make a difference? Strateg. Manag. J. 1989, 10, 107–124. [Google Scholar] [CrossRef]

- Cho, T.S.; Hambrick, D.C. Attention as the mediator between top management team characteristics and strategic change: The case of airline deregulation. Org. Sci. 2006, 17, 453–469. [Google Scholar] [CrossRef]

- Mitchell, R.K.; Agle, B.R.; Wood, D.J. Toward a theory of stakeholder identification and salience: Defining the principle of who and what really counts. Acad. Manag. Rev. 1997, 22, 853–886. [Google Scholar] [CrossRef]

- Grant, A.M.; Dutton, J.E.; Rosso, B.D. Giving commitment: Employee support programs and the prosocial sensemaking process. Acad. Manag. J. 2008, 51, 898–918. [Google Scholar] [CrossRef]

- Madden, L.T.; Duchon, D.; Madden, T.M.; Plowman, D.A. Emergent organizational capacity for compassion. Acad. Manag. Rev. 2012, 37, 689–708. [Google Scholar] [CrossRef]

- Brickson, S.L. Organizational identity orientation: Forging a link between organizational identity and organizations’ relations with stakeholders. Adm. Sci. Q. 2005, 50, 576–609. [Google Scholar] [CrossRef]

- Rousseau, D.M.; Wade-Benzoni, K.A. Linking strategy and human resource practices: How employee and customer contracts are created. Hum. Res. Manag. 1994, 33, 463–489. [Google Scholar] [CrossRef]

- Orlitzky, M. Corporate social responsibility, noise, and stock market volatility. Acad. Manag. Perspect. 2013, 27, 238–254. [Google Scholar] [CrossRef]

- Mackey, A.; Mackey, T.B.; Barney, J.B. Corporate social responsibility and firm performance: Investor preferences and corporate strategies. Acad. Manag. Rev. 2007, 32, 817–835. [Google Scholar] [CrossRef]

- Cyert, R.M.; March, J.G. A Behavioral Theory of the Firm; Prentice Hall: Englewood Cliffs, NJ, USA, 1963; Volume 2, pp. 169–187. [Google Scholar]

- Nadkarni, S.; Barr, P.S. Environmental context, managerial cognition, and strategic action: An integrated view. Strateg. Manag. J. 2008, 29, 1395–1427. [Google Scholar] [CrossRef]

- Ocasio, W. Attention to attention. Org. Sci. 2011, 22, 1286–1296. [Google Scholar] [CrossRef]

- Yadav, M.S.; Prabhu, J.C.; Chandy, R.K. Managing the future: CEO attention and innovation outcomes. J. Mark. 2007, 71, 84–101. [Google Scholar] [CrossRef]

- Greve, J. Healthcare in developing countries and the role of business: A global governance framework to enhance the accountability of pharmaceutical companies. Int. J. Bus. Soc. 2008, 8, 490–505. [Google Scholar] [CrossRef]

- Kaplan, S. Cognition, capabilities, and incentives: Assessing firm response to the fiber-optic revolution. Acad. Manag. J. 2008, 51, 672–695. [Google Scholar] [CrossRef]

- Boeker, W. Strategic change: The influence of managerial characteristics and organizational growth. Acad. Manag. J. 1997, 40, 152–170. [Google Scholar] [CrossRef]

- Finkelstein, S.; Hambrick, D.C. Top-management-team tenure and organizational outcomes: The moderating role of managerial discretion. Adm. Sci. Q. 1990, 484–503. [Google Scholar] [CrossRef]

- Bigoness, W.J.; Blakely, G.L. A cross-national study of managerial values. J. Int. Bus. Stud. 1996, 27, 739–748. [Google Scholar] [CrossRef]

- Singhapakdi, A.; Marta, J.K.; Rallapalli, K.C.; Rao, C.P. Toward an understanding of religiousness and marketing ethics: An empirical study. J. Bus. Ethics 2000, 27, 305–319. [Google Scholar] [CrossRef]

- Fritzsche, D.J. Personal values: Potential keys to ethical decision making. J. Bus. Ethics 1995, 14, 909–922. [Google Scholar] [CrossRef]

- Beach, L.R.; Mitchell, T.R. A contingency model for the selection of decision strategies. Acad. Manag. Rev. 1978, 3, 439–449. [Google Scholar] [CrossRef]

- Hage, J.; Dewar, R. Elite values versus organizational structure in predicting innovation. Adm. Sci. Q. 1973, 279–290. [Google Scholar] [CrossRef]

- Marbaniang, D. Developing the Spirit of Patriotism and Humanism in Children for Peace and Harmony; Domenic Marbaniang: Bangalore, India, 2009; pp. 474–490. [Google Scholar]

- Brodley, J.F. Massive Industrial Size, Classical Economics, and the Search for Humanistic Value. Stanf. Law Rev. 1972, 24, 1155–1178. [Google Scholar] [CrossRef]

- Spratlen, T.H. The challenge of a humanistic value orientation in marketing. In Society and Marketing: An Unconventional View; Kangun, N., Ed.; Harper and Row: New York, NY, USA, 1972; pp. 403–413. [Google Scholar]

- Du, S.; Bhattacharya, C.B.; Sen, S. Corporate social responsibility and competitive advantage: Overcoming the trust barrier. Manag. Sci. 2011, 57, 1528–1545. [Google Scholar] [CrossRef]

- Kahneman, D. Attention and Effort, 1st ed.; Prentice-Hall: Englewood Cliffs, NJ, USA, 1973; ISBN 0130505188. [Google Scholar]

- Weick, K.E.; Sutcliffe, K.M. Mindfulness and the quality of organizational attention. Org. Sci. 2006, 17, 514–524. [Google Scholar] [CrossRef]

- Hambrick, D.C. Upper echelons theory: An update. Acad. Manag. Rev. 2007, 32, 334–343. [Google Scholar] [CrossRef]

- Li, J.; Tang, Y.I. CEO hubris and firm risk taking in China: The moderating role of managerial discretion. Acad. Manag. J. 2010, 53, 45–68. [Google Scholar] [CrossRef]

- Jain, T.; Jamali, D. Strategic approaches to corporate social responsibility. In Development-Oriented Corporate Social Responsibility; Greenleaf Publishing: Sheffield, UK, 2015; p. 2. [Google Scholar]

- Hannan, M.T.; Freeman, J. Structural inertia and organizational change. Am. Soc. Rev. 1984, 49, 149–164. [Google Scholar] [CrossRef]

- Lavie, D.; Rosenkopf, L. Balancing exploration and exploitation in alliance formation. Acad. Manag. J. 2006, 49, 797–818. [Google Scholar] [CrossRef]

- Barron, D.N.; West, E.; Hannan, M.T. A time to grow and a time to die: Growth and mortality of credit unions in New York City, 1914–1990. Am. J. Soc. 1994, 100, 381–421. [Google Scholar] [CrossRef]

- Bourgeois, L.J., III. On the measurement of organizational slack. Acad. Manag. Rev. 1981, 6, 29–39. [Google Scholar] [CrossRef]

- Hambrick, D.C.; Finkelstein, S. Managerial discretion: A bridge between polar views of organizational outcomes. Res. Org. Behav. 1987, 9, 369–406. [Google Scholar]

- Heeley, M.B.; Matusik, S.F.; Jain, N. Innovation, appropriability, and the underpricing of initial public offerings. Acad. Manag. J. 2007, 50, 209–225. [Google Scholar] [CrossRef]

- Ling, Y.A.; Simsek, Z.; Lubatkin, M.H.; Veiga, J.F. Transformational leadership’s role in promoting corporate entrepreneurship: Examining the CEO-TMT interface. Acad. Manag. J. 2008, 51, 557–576. [Google Scholar] [CrossRef]

- Garcia-Morales, V.J.; Llorens-Montes, F.J.; Verdú-Jover, A.J. Antecedents and consequences of organizational innovation and organizational learning in entrepreneurship. Ind. Manag. Data Syst. 2006, 106, 21–42. [Google Scholar] [CrossRef]

- Anderson, A.R.; Li, J.H.; Harrison, R.T.; Robson, P.J. The increasing role of small business in the Chinese economy. J. Small. Bus. Manag. 2003, 41, 310–316. [Google Scholar] [CrossRef]

- Barr, P.S.; Stimpert, J.L.; Huff, A.S. Cognitive Change, Strategic Action, and Organizational Renewal. Strateg. Manag. J. 1992, 13, 15–36. [Google Scholar] [CrossRef]

- Duriau, V.J.; Reger, R.K.; Pfarrer, M.D. A Content Analysis of the Content Analysis Literature in Organization Studies: Research Themes, Data Sources, and Methodological Refinements. Org. Res. Methods 2007, 10, 5–34. [Google Scholar] [CrossRef]

- Kaplan, S.; Murray, F.; Henderson, R. Discontinuities and senior management: Assessing the role of recognition in pharmaceutical firm response to biotechnology. Ind. Corpor. Chang. 2003, 12, 203–233. [Google Scholar] [CrossRef]

- Roger, R.K.; Grant, J. Content Analysis of Information Cited in Reports of Sell-Side Financial Analysts. J. Financ. Statement Anal. 1997, 3, 17–30. [Google Scholar]

- Clarkson, P.M.; Kao, J.L.; Richardson, G.D. Evidence that management discussion and analysis (MD&A) is a part of a firm’s overall disclosure package. Contemp. Account. Res. 1999, 16, 111–134. [Google Scholar] [CrossRef]

- Barr, P.S. Adapting to unfamiliar environmental events: A look at the evolution of interpretation and its role in strategic change. Org. Sci. 1998, 9, 644–669. [Google Scholar] [CrossRef]

- Yang, J.; Park, K.M. The Effects of Performance Feedback, Past Temporal Orientation, and Interaction on R&D Intensity. Acad. Manag. 2017, 1, 17526. [Google Scholar] [CrossRef]

- Cole, C.J.; Jones, C.L. Management discussion and analysis: A review and implications for future research. J. Account. Lit. 2005, 24, 135–174. [Google Scholar]

- Kohut, G.F.; Segars, A.H. The president’s letter to stockholders: An examination of corporate communication strategy. J. Bus. Commun. 1992, 29, 7–21. [Google Scholar] [CrossRef]

- Li, F. Survey of the Literature. J. Account. Lit. 2010, 29, 143–165. [Google Scholar]

- Sapir, E. Grading, a study in Semantics. Philos. Sci. 1944, 11, 93–116. [Google Scholar] [CrossRef]

- Whorf, B.L. Language, Thought, and Reality: Selected Writings; Technology Press of Massachusetts Institute of Technology: Cambridge, MA, USA, 1956. [Google Scholar]

- Pennebaker, J.W.; Francis, M.E.; Booth, R.J. Linguistic inquiry and word count: LIWC 2001. Lawrence Erlbaum Assoc. 2001, 71, 1–22. [Google Scholar]

- Zheng, G.; Wang, S.; Xu, Y. Monetary Stimulation, Bank Relationship and Innovation: Evidence from China. J. Bank. Finaanc. 2018, 89, 237–248. [Google Scholar] [CrossRef]

- Chandler, G.N.; Hanks, S.H. Measuring the performance of emerging businesses: A validation study. J. Bus. Ventur. 1993, 8, 391–408. [Google Scholar] [CrossRef]

- Xu, E.; Yang, H.; Quan, J.M.; Lu, Y. Organizational slack and corporate social performance: Empirical evidence from China’s public firms. Asia Pac. J. Manag. 2015, 32, 181–198. [Google Scholar] [CrossRef]

- Wiseman, R.M.; Bromiley, P. Toward a Model of Risk in Declining Organizations: An Empirical Examination of Risk, Performance and Decline. Org. Sci. 1996, 7, 524–543. [Google Scholar] [CrossRef]

- Iyer, D.N.; Miller, K.D. Performance Feedback, Slack, and the Timing of Acquisitions. Acad. Manag. J. 2008, 51, 808–822. [Google Scholar] [CrossRef]

- Seifert, B.; Morris, S.A.; Bartkus, B.R. Having, Giving, and Getting: Slack Resources, Corporate Philanthropy, and Firm Financial Performance. J. Bus. Soc. 2004, 43, 135–161. [Google Scholar] [CrossRef]

- Aiken, L.S.; West, S.G. Multiple Regression: Testing and Interpreting Interactions—Institute for Social and Economic Research (ISER); Sage: Thousand Oaks, CA, USA, 1991; Volume 14, pp. 167–168. [Google Scholar]

- Lu, C.; Zhao, X.; Dai, J. Corporate Social Responsibility and Insider Trading: Evidence from China. Sustainability 2018, 10, 3163. [Google Scholar] [CrossRef]

- Cohen, W.M.; Levinthal, D.A. Innovation and Learning: The Two Faces of R & D. Econ. J. 1989, 99, 569–596. [Google Scholar] [CrossRef]

- Dess, G.G.; Beard, D.W. Dimensions of Organizational Task Environments. Adm. Sci. Q. 1984, 52–73. [Google Scholar] [CrossRef]

- Sapienza, H.J.; Smith, K.G.; Gannon, M.J. Using Subjective Evaluations of Organizational Performance in Small Business Research. Am. J. Small Bus. 1988, 12, 45–54. [Google Scholar] [CrossRef]

- Arora, P.; Dharwadkar, R. Corporate governance and corporate social responsibility (CSR): The moderating roles of attainment discrepancy and organization slack. Corpor. Gov. Int. Rev. 2011, 19, 136–152. [Google Scholar] [CrossRef]

- Shin, I.; Hur, W.-M.; Kang, S. Employees’ Perceptions of Corporate Social Responsibility and Job Performance: A Sequential Mediation Model. Sustainability 2016, 8, 493. [Google Scholar] [CrossRef]

- Lee, S.-Y.; Seo, Y.W. Corporate Social Responsibility Motive Attribution by Service Employees in the Parcel Logistics Industry as a Moderator between CSR Perception and Organizational Effectiveness. Sustainability 2017, 9, 355. [Google Scholar] [CrossRef]

- Pérez, S.; Fernández-Salinero, S.; Topa, G. Sustainability in Organizations: Perceptions of Corporate Social Responsibility and Spanish Employees’ Attitudes and Behaviors. Sustainability 2018, 10, 3423. [Google Scholar] [CrossRef]

- Wooldridge, J.M. Introductory Econometrics: A Modern Approach; Nelson Education: Scarborough, ON, Canada, 2015; ISBN 978-0-324-58162-1. [Google Scholar]

{kind=link}

{kind=link}

| Year | 2010 | 2011 | 2012 | 2013 | 2014 | Total |

|---|---|---|---|---|---|---|

| Sample size | 440 | 464 | 479 | 484 | 480 | 2347 |

| Variable | Symbol | Variable Definitions |

|---|---|---|

| Dependent Variable | ||

| Corporate Social Responsibility | CSR | The comprehensive score of five first-class CSR indexes calculated by the weighted average method, range from 0 to 100 |

| Independent variable | ||

| Managerial humanistic attention | MH_A | The ratio of the keywords appearing in the MD&A part of an annual report |

| Moderator | ||

| Firm Age | Age | Listing age, defined as the number of years a firm’s stocks have been listed |

| Firm Size | Size | The natural logarithm of sales |

| Slack Resource | Slack | The ratio of cash flow to total assets of the firm |

| Control variable | ||

| Market munificence | Market | Average growth in net sales and growth in operating income in dominant industry |

| Research and Development Intensity | R&D | Corporate R&D expenditures divided by sales |

| Rate of Return on Asset | ROA | The ratio of net profit to total assets |

| N | Mean | SD | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 CSR | 2347 | 27.31 | 21.62 | 1.00 | - | - | - | - | - | - | - |

| 2 MH_A | 2347 | 2.59 | 1.57 | 0.01 | 1.00 | - | - | - | - | - | - |

| 3 ROA | 2347 | 0.04 | 0.49 | 0.35 ** | 0.02 | 1.00 | - | - | - | - | - |

| 4 Market | 2347 | 0.01 | 0.13 | 0.02 | −0.12 ** | −0.05 | 1.00 | - | - | - | - |

| 5 R&D | 2347 | 0.01 | 0.01 | 0.12 ** | −0.01 | 0.22 ** | 0.15 ** | 1.00 | - | - | - |

| 6 Age | 2347 | 13.99 | 4.09 | −0.00 | −0.02 | 0.05 | −0.02 | 0.03 | 1.00 | - | - |

| 7 Size | 2347 | 9.39 | 0.69 | 0.07 ** | −0.04 | 0.08 ** | −0.06 ** | 0.11 ** | −0.05 | 1.00 | - |

| 8 Slack | 2347 | 0.01 | 0.09 | 0.07 ** | 0.05 | 0.18 ** | −0.02 | 0.03 | 0.01 | −0.01 | 1.00 |

| Corporate Social Responsibility | ||||||

|---|---|---|---|---|---|---|

| Variable | (1) | (2) | (3) | (4) | (5) | (6) |

| MH_A | - | 1.378 *** (0.26) | 1.417 *** (0.26) | 1.393 *** (0.26) | 1.446 *** (0.26) | 1.506 ** (0.26) |

| ROA | 0.015 *** (0.00) | 0.015 *** (0.00) | 0.014 *** (0.00) | 0.015 *** (0.00) | 0.014 *** (0.00) | 0.015 *** (0.00) |

| Market | 0.029 ** (0.01) | 0.036 *** (0.01) | 0.035 *** (0.01) | 0.035 *** (0.01) | 0.036 *** (0.01) | 0.035 *** (0.01) |

| R&D | −0.015 *** (0.00) | −0.014 ***0.00) | −0.014 *** (0.00) | −0.014 *** (0.00) | −0.014 *** (0.00) | −0.014 *** (0.00) |

| Age | −0.472 *** (0.13) | −0.434 * (0.13) | −0.432 ** (0.13) | −0.439 ** (0.13) | −0.438 ** (0.13) | −0.434 ** (0.13) |

| Size | 0.002 * (0.00) | 0.002 * (0.00) | 0.002 * (0.00) | 0.002 * (0.00) | 0.002 * (0.00) | 0.002 * (0.00) |

| Slack | 0.002 (0.00) | 0.002 (0.00) | 0.002 (0.00) | 0.002 (0.00) | 0.002 (0.00) | 0.002 (0.00) |

| MH_A Age | - | - | 0.094 * (0.05) | - | - | 0.102 * (45.01) |

| MH_A Slack | - | - | - | 0.001 * (0.00) | - | 0.001 * (0.00) |

| MH_A Size | - | - | - | - | 0.000 + (0.00) | 0.000 + (0.00) |

| Constant | 22.358 *** (2.38) | 18.158 *** (2.05) | 18.142 *** (2.49) | 17.871 *** (2.49) | 17.843 *** (2.50) | 17.512 *** (2.50) |

| Year | Yes | Yes | Yes | Yes | Yes | Yes |

| Observation | 2347 | 2347 | 2347 | 2347 | 2347 | 2347 |

| R2 | 0.04 | 0.03 | 0.03 | 0.03 | 0.03 | 0.04 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hu, Y.; Chen, S.; Wang, J. Managerial Humanistic Attention and CSR: Do Firm Characteristics Matter? Sustainability 2018, 10, 4029. https://doi.org/10.3390/su10114029

Hu Y, Chen S, Wang J. Managerial Humanistic Attention and CSR: Do Firm Characteristics Matter? Sustainability. 2018; 10(11):4029. https://doi.org/10.3390/su10114029

Chicago/Turabian StyleHu, Yuanyuan, Shouming Chen, and Jian Wang. 2018. "Managerial Humanistic Attention and CSR: Do Firm Characteristics Matter?" Sustainability 10, no. 11: 4029. https://doi.org/10.3390/su10114029

APA StyleHu, Y., Chen, S., & Wang, J. (2018). Managerial Humanistic Attention and CSR: Do Firm Characteristics Matter? Sustainability, 10(11), 4029. https://doi.org/10.3390/su10114029