Development of the Financial Sector and Growth of Microfinance Institutions: The Moderating Effect of Economic Growth

Abstract

1. Introduction

2. Theory and Hypotheses

3. Empirical Analysis

3.1. Characteristics and Composition of the Sample

3.2. Econometric Model

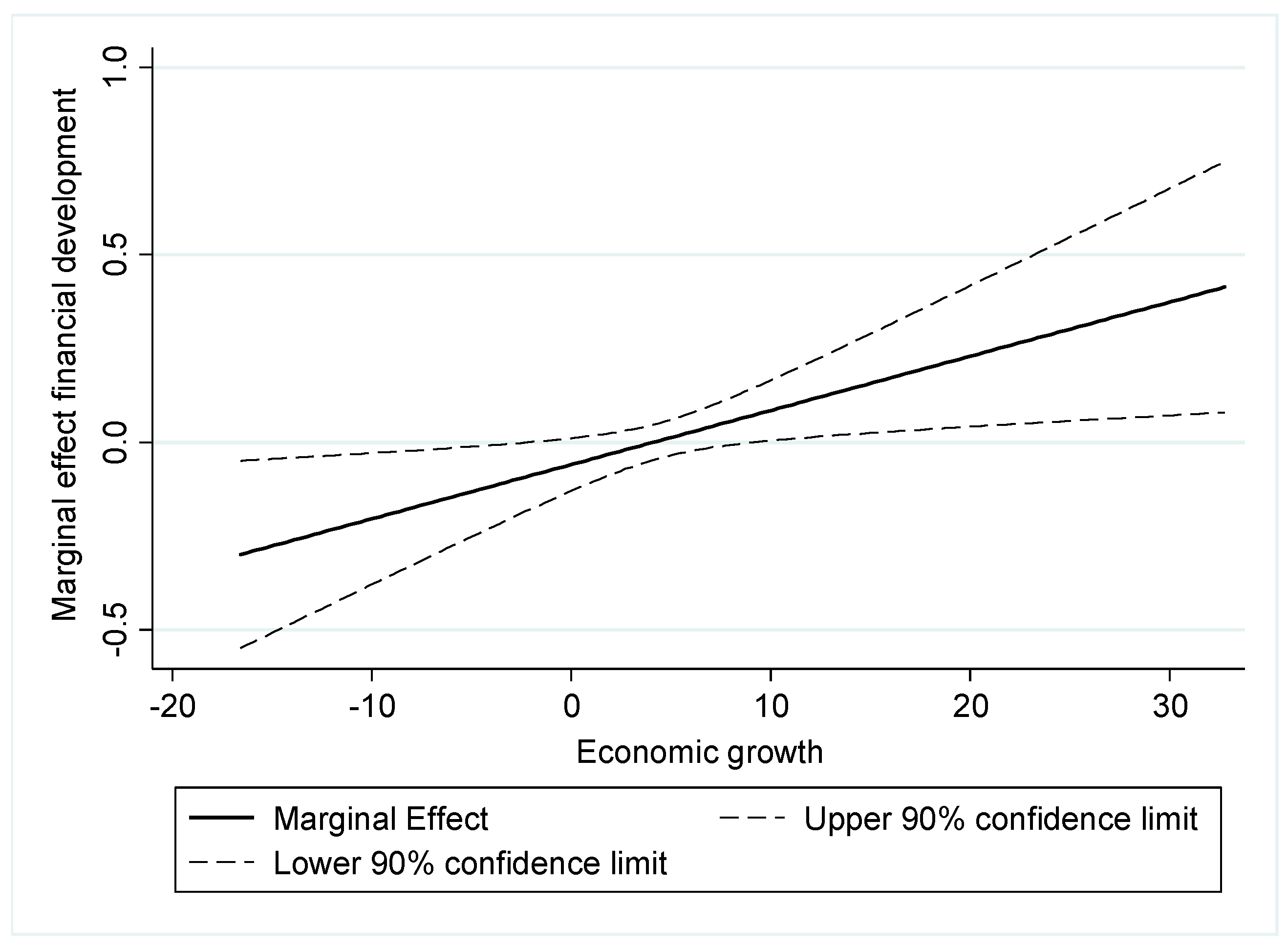

3.3. Results

4. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Cull, R.; Demirgüç-Kunt, A.; Morduch, J. Microfinance meets the market. J. Econ. Perspect. 2009, 23, 167–192. [Google Scholar] [CrossRef]

- Ahlin, C.; Lin, J. Luck or Skill? MFI Performance in Macroeconomic Context; BREAD Working Paper 132; Centre for International Development, Harvard University: Cambridge, MA, USA, 2006. [Google Scholar]

- Hermes, N.; Lensink, R.; Meesters, A. Outreach and efficiency of microfinance institutions. World Dev. 2011, 39, 938–948. [Google Scholar] [CrossRef]

- Bogan, V.L. Capital structure and sustainability: An empirical study of microfinance institutions. Rev. Econ. Stat. 2012, 94, 1045–1058. [Google Scholar] [CrossRef]

- Vanroose, A.; D’Espallier, B. Do microfinance institutions accomplish their mission? Evidence from the relationship between traditional financial sector development and microfinance institutions’ outreach and performance. Appl. Econ. 2013, 45, 1965–1982. [Google Scholar] [CrossRef]

- Adhikary, S.; Papachristou, G. Is There a Trade-off between Financial Performance and Outreach in South Asian Microfinance Institutions? J. Dev. Areas 2014, 48, 381–402. [Google Scholar] [CrossRef]

- Ahlin, C.; Lin, J.; Maio, M. Where does microfinance flourish? Microfinance institution performance in macroeconomic context. J. Dev. Econ. 2011, 95, 105–120. [Google Scholar] [CrossRef]

- Martinez, R. Latin America and the Caribbean 2009: Microfinance Analysis and Benchmarking Report; Microfinance Information Exchange: Washington, DC, USA, 2010. [Google Scholar]

- McIntosh, C.; Wydick, B. Competition and microfinance. J. Dev. Econ. 2005, 78, 271–298. [Google Scholar] [CrossRef]

- Hermes, N.; Lensink, R.; Meesters, A. Financial Development and the Efficiency of Microfinance Institutions; University of Groningen: Groningen, The Netherlands, 2009. [Google Scholar]

- Huijsman, S. The Impact of the Economic and Financial Crisis on MFIs; Planet Finance: Stuttgart, Germany, 2011. [Google Scholar]

- Constantinou, D.; Ashta, A. Financial crisis: Lessons from microfinance. Strateg. Chang. 2011, 20, 187–203. [Google Scholar] [CrossRef]

- Rosenberg, R.; González, A.; Narain, S. The New Moneylenders: Are the Poor Being Exploited by High Microcredit Interest Rates? CGAP: Washington, DC, USA, 2009. [Google Scholar]

- Hamada, M. Commercialization of microfinance in Indonesia: The shortage of funds and the linkage program. Dev. Econ. 2010, 48, 156–176. [Google Scholar] [CrossRef]

- Demirgüç-Kunt, A.; Beck, T.; Honohan, P. Finance for All? Policies and Pitfalls in Expanding Access; World Bank Policy Research Report: Washington, DC, USA, 2008. [Google Scholar]

- Wagner, C.; Winkler, A. The vulnerability of microfinance to financial turmoil: Evidence from the global financial crisis. World Dev. 2013, 51, 71–90. [Google Scholar] [CrossRef]

- Sinclair, S. Financial Exclusion: An Introductory Survey Centre for Research into Socially Inclusive Services; Centre for Research into Socially Inclusive Services, Heriot Watt University: Edimburgo, UK, 2001. [Google Scholar]

- World Bank Group. The Little Data Book on Financial Inclusion 2015. Global Financial Inclusion Database; World Bank: Washington, DC, USA, 2015; ISBN 1464805520. [Google Scholar]

- Barr, M.S. Microfinance and Financial Development. Michigan J. Int. Law 2005, 26, 271–296. [Google Scholar]

- McIntosh, C.; Janvry, A.; Sadoulet, E. How rising competition among microfinance institutions affects incumbent lenders. Econ. J. 2005, 115, 987–1004. [Google Scholar] [CrossRef]

- Bell, C.; Rousseau, P.L. Post-independence India: A case of finance-led industrialization? J. Dev. Econ. 2001, 65, 153–175. [Google Scholar] [CrossRef]

- Isem, J.; Porteous, D. Commercial Banks and Microfinance: Evolving Models of Success; CGAP Focus Note; no. 28; World Bank: Washington, DC, USA, 2005. [Google Scholar]

- De Crombrugghe, A.; Tenikue, M.; Sureda, J. Perfomance analysis for a sample of microfinance institutions in India. Ann. Public Coop. Econ. 2008, 79, 269–299. [Google Scholar] [CrossRef]

- Quayes, S. Depth of outreach and financial sustainability of microfinance institutions. Appl. Econ. 2012, 44, 3421–3433. [Google Scholar] [CrossRef]

- King, R.G.; Levine, R. Finance and Growth: Schumpeter Might Be Right. Q. J. Econ. 1993, 108, 717–737. [Google Scholar] [CrossRef]

- Levine, R. Finance and growth: Theory and evidence. In Handbook of Economic Growth; Aghion, P., Durlauf, S.N., Eds.; Elsevier: Amsterdam, The Netherlands, 2005; Volume 1, pp. 865–934. [Google Scholar]

- Samargandi, N.; Firdmuc, J.; Ghost, S. Is the Relationship Between Financial Development and Economic Growth Monotonic? Evidence from a Sample of Middle-Income Countries. World Dev. 2015, 68, 66–81. [Google Scholar] [CrossRef]

- Durusu-Ciftci, D.; Ispir, M.S.; Hakan, Y. Financial development and economic growth: Some theory and more evidence. J. Policy Model. 2016, 39, 290–306. [Google Scholar] [CrossRef]

- Rousseau, P.L.; Wachtel, P. Financial Intermediation and Economic Performance: Historical Evidence from Five Industrialized Countries. J. Money Credit Bank. 1998, 30, 657–678. [Google Scholar] [CrossRef]

- Bekaert, G.; Harvey, C.R. Capital markets: An engine for economic growth. Brown J. World Aff. 1998, 5, 33–53. [Google Scholar] [CrossRef]

- Berkes, E.; Panizza, U.; Arcand, J.-L. Too Much Finance? International Monetary Fund Working Paper WP/12/161: Washington, DC, USA, 2012. [Google Scholar]

- Cecchetti, S.; Kharroubi, E. Reassessing the Impact of Finance on Growth; Bank for International Settlements Working Paper 381: Basel, Switzerland, 2012. [Google Scholar]

- Law, S.H.; Singh, N. Does too much finance harm economic growth? J. Bank. Financ. 2014, 41, 36–44. [Google Scholar] [CrossRef]

- Patrick, H.T. Financial development and economic growth in underdeveloped countries. Econ. Dev. Cult. Chang. 1966, 14, 174–189. [Google Scholar] [CrossRef]

- Shaw, E.S. Financial Deepening in Economic Development; Oxford University Press: New York, NY, USA, 1973. [Google Scholar]

- Fritz, R.G. Time series evidence of the causal relationship between financial deepening and economic development. J. Econ. Dev. 1984, 9, 91–111. [Google Scholar]

- Jung, W.S. Financial Development and Economic Growth: International Evidence. Econ. Dev. Cult. Chang. 1986, 34, 333–346. [Google Scholar] [CrossRef]

- Demetriades, P.O.; Hussein, K.A. Does financial development cause economic growth? Time-series evidence from 16 countries. J. Dev. Econ. 1996, 51, 387–411. [Google Scholar] [CrossRef]

- Blackburn, K.; Hung, V.T.Y. A theory of growth, financial development and trade. Economica 1998, 65, 107–124. [Google Scholar] [CrossRef]

- Khan, A. Financial Development and Economic Growth. Macroecon. Dyn. 2001, 5, 413–433. [Google Scholar]

- Calderón, C.; Liu, L. The direction of causality between financial development and economic growth. J. Dev. Econ. 2003, 72, 321–334. [Google Scholar] [CrossRef]

- Fung, M.K. Financial development and economic growth: Convergence or divergence? J. Int. Money Financ. 2009, 28, 56–67. [Google Scholar] [CrossRef]

- Hassan, M.K.; Sánchez, B.; Yu, J.-S. Financial development and economic growth: New evidence from panel data. Q. Rev. Econ. Financ. 2011, 51, 88–104. [Google Scholar] [CrossRef]

- Schneider, F.; Enste, D.H. Shadow Economies: Size Causes and Consecuences. J. Econ. Lit. 2000, 38, 77–114. [Google Scholar] [CrossRef]

- Heintz, J.; Pollin, R. Informalization, Economic Growth and the Challenge of Creating Viable Labor Standards in Developing Countries; SSRN Electronic Journal. 10.2139; SSRN: New York, NY, USA, 2003; Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=427683 (accessed on 28 October 2018).

- Lucas, R.E. On the mechanics of economic development. J. Monet. Econ. 1988, 22, 3–42. [Google Scholar] [CrossRef]

- Goodhart, C.A.E. Financial Development and Economic Growth: Explaining the Links; Palgrave Macmillan: Basingstoke, UK, 2004; ISBN 9780230374270. [Google Scholar]

- Robinson, J. The Rate of Interest and Other Essays; Macmillan: London, UK, 1952. [Google Scholar]

- Robinson, J. The Rate of Interest. In The Generalisation of the General Theory and other Essays; Palgrave Macmillan UK: London, UK, 1979; pp. 135–164. [Google Scholar]

- Bell, R.; Harper, A.; Mandivenga, D. Can commercial banks do microfinance? Lessons from the commercial bank of Zimbabwe and the co-operative bank of Kenya. Small Enterp. Dev. 2002, 13, 35–46. [Google Scholar] [CrossRef]

- Isern, J.; Ritchie, A.; Crenn, T.; Brown, M. Review of Commercial Banks and Other Formal Financial Institutions Participation in Microfinance; CGAP: Washington, DC, USA, 2003. [Google Scholar]

- Trigo, J.; Loubière, P.; Devaney, L.; Rhyne, E. Supervising and Regulating Microfinance in the Context of Financial Sector Liberalization: Lessons from Bolivia, Colombia and Mexico; Accion Internacional: Washington, DC, USA, 2004. [Google Scholar]

- Arellano, M.; Bond, S. Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. Rev. Econ. Stud. 1991, 58, 277–297. [Google Scholar] [CrossRef]

- Gutiérrez-Nieto, B.; Serrano-Cinca, C.; Mar Molinero, C. Social efficiency in microfinance institutions. J. Oper. Res. Soc. 2009, 60, 104–119. [Google Scholar] [CrossRef]

- Mersland, R.; Strøm, R.Ø. Microfinance mission drift? World Dev. 2010, 38, 28–36. [Google Scholar] [CrossRef]

- Wagner, C. From Boom to Bust: How Different Has Microfinance Been from Traditional Banking? Dev. Policy Rev. 2012, 30, 187–210. [Google Scholar] [CrossRef]

- Patten, R.H.; Rosengard, J.K.; Johnston, D.J. Microfinance Success Amidst Macroeconomic Failure: The Experience of Bank Rakyat Indonesia During the East Asian Crisis. World Dev. 2001, 29, 1057–1069. [Google Scholar] [CrossRef]

- Vogelgesang, U. Microfinance in Times of Crisis: The Effects of Competition, Rising Indebtedness, and Economic Crisis on Repayment Behavior. World Dev. 2003, 31, 2085–2114. [Google Scholar] [CrossRef]

- Assefa, E.; Hermes, N.; Meesters, A. Competition and the performance of microfinance institutions. Appl. Financ. Econ. 2013, 23, 767–782. [Google Scholar] [CrossRef]

- Rajan, R.G.; Zingales, L. American Economic Association Financial Dependence and Growth. Am. Econ. Rev. 1998, 88, 559–586. [Google Scholar]

- Levine, R.; Loayza, N.; Beck, T. Financial intermediation and growth: Causality and causes. J. Monet. Econ. 2000, 46, 31–77. [Google Scholar] [CrossRef]

- Westley, G.D. Can Financial Market Policies Reduce Income Inequality? Inter-American Development Bank: Washington, DC, USA, 2016. [Google Scholar]

- Demirgüç-Kunt, A.; Levine, R. Financial Structure and Economic Growth: A Cross-Country Comparison of Banks, Markets, and Development; MIT Press: Cambridge, UK, 2004; ISBN 9780262541794. [Google Scholar]

- Gutiérrez Goiria, J. Las Microfinanzas en el Marco de la Financiación del Desarrollo: Compatibilidad y/o Conflicto Entre Objetivos Sociales y Financieros; Universidad del País Vasco–Euskal Herriko Unibertsitatea: Leioa, Spain, 2012. [Google Scholar]

- González, A. Is Microfinance Growing Too Fast? Microfinance Information Exchange: Washington, DC, USA, 2010. [Google Scholar]

- Rozas, D. Weathering the Storm: Hazards, Beacons, and Life Rafts Lessons in Microfinance Crisis Survival from Those Who Have Been There; Center for Financial Inclusion: Washington, DC, USA, 2011. [Google Scholar]

- Hernández-Hernández, E.; Sam, A.G.; González-Vega, C.; Chen, J. Agricultural and Applied Economics Association; Agricultural and Applied Economics Association: Milwaukee, WI, USA, 2009. [Google Scholar]

- Kappel, V.; Krauss, A.; Lontzek, L. Sobreendeudamiento y Microfinanzas Construyendo un índice de alerta Temprana; Center of Microfinance, University of Zurich: Zurich, Switzerland, 2010. [Google Scholar]

- Baquero, G.; Hamadi, M.; Heinen, A. Competition, Loan Rates and Information Dispersion in Microcredit Markets. J. Money Credit Bank. 2018, 50, 893–937. [Google Scholar] [CrossRef]

- Wilhelm, U. Identificando los Principales Riesgos en las Microfinanzas; Standard & Poor’s: New York, NY, USA, 2000. [Google Scholar]

- Reille, X. The Rise, Fall, and Recovery of the Microfinance Sector in Morocco; CGAP: Washington, DC, USA, 2009. [Google Scholar]

- Chen, G.; Rasmussen, S.; Reille, X. Growth and Vulnerabilities in Microfinance; Consultative Group to Assist the Poor (CGAP): Washington, DC, USA, 2010. [Google Scholar]

- Richman, D.; Fred, A.K. Gender Composition, Competition and Sustainability of Micro Finance in Africa: Evidence from Ghana’s Microfinance Inustry; Ghana Institute of Management and Public Administration: Ghana, West Africa, 2010. [Google Scholar]

- Priyadarshee, A.; Ghalib, A.K. The Andhra Pradesh Microfinance Crisis in India: Manifestation, Causal Analysis, and Regulatory Response; Brooks World Poverty Institute Working Paper No. 157: Nueva Delhi, India, 2011. [Google Scholar]

- Bastiaensen, J.; Marchetti, P.; Mendoza Vidaurre, R.; Pérez, F.J. Las paradójicas secuelas del movimiento no pago en las microfinanzas agropecuarias en Nicaragua. Encuentro 2013, 95, 47–68. [Google Scholar]

- Brambor, T.; Clark, W.R.; Golder, M.; Beck, N.; Boehmke, F.; Gilligan, M.; Golder, S.N.; Nagler, J. Understanding Interaction Models: Improving Empirical Analysis. Political Anal. 2006, 14, 63–82. [Google Scholar] [CrossRef]

- Berry, W.D.; Golder, M.; Milton, D. Improving Tests of Theories Positing Interaction. J. Political 2012, 74, 653–671. [Google Scholar] [CrossRef]

- Aiken, L.S.; West, S.G.; Reno, R.R. Multiple Regression: Testing and Interpreting Interactions; Sage Publications: Thousand Oaks, CA, USA, 1991; ISBN 0803936052. [Google Scholar]

{kind=link}

| N | n | Banks | Credit Union/Cooperative | NBFI (Non-Bank Financial Institutions) | NGO (Non-Governmental Organizations) | Rural Bank | |

|---|---|---|---|---|---|---|---|

| Africa | 412 | 66 | 34 | 106 | 118 | 154 | 0 |

| Benin | 23 | 3 | 0 | 0 | 0 | 23 | 0 |

| Burkina Faso | 9 | 1 | 0 | 0 | 9 | 0 | 0 |

| Burundi | 4 | 1 | 0 | 0 | 4 | 0 | 0 |

| Cameroon | 20 | 4 | 0 | 4 | 16 | 0 | 0 |

| Congo, Dem. Rep. | 15 | 3 | 0 | 0 | 0 | 15 | 0 |

| Cote d’Ivoire | 5 | 1 | 0 | 5 | 0 | 0 | 0 |

| Ghana | 46 | 8 | 0 | 0 | 12 | 34 | 0 |

| Kenya | 60 | 8 | 19 | 0 | 34 | 7 | 0 |

| Madagascar | 20 | 4 | 0 | 20 | 0 | 0 | 0 |

| Malawi | 20 | 4 | 6 | 0 | 0 | 14 | 0 |

| Mali | 41 | 6 | 0 | 24 | 0 | 17 | 0 |

| Namibia | 4 | 1 | 0 | 0 | 0 | 4 | 0 |

| Niger | 4 | 1 | 0 | 0 | 4 | 0 | 0 |

| Senegal | 51 | 8 | 0 | 47 | 0 | 4 | 0 |

| Sierra Leone | 4 | 1 | 0 | 0 | 0 | 4 | 0 |

| Swaziland | 4 | 1 | 0 | 0 | 4 | 0 | 0 |

| Tanzania | 36 | 5 | 9 | 0 | 5 | 22 | 0 |

| Togo | 16 | 2 | 0 | 6 | 0 | 10 | 0 |

| Uganda | 23 | 3 | 0 | 0 | 23 | 0 | 0 |

| Zambia | 7 | 1 | 0 | 0 | 7 | 0 | 0 |

| East Asia and the Pacific | 465 | 74 | 23 | 4 | 112 | 196 | 130 |

| Cambodia | 116 | 13 | 13 | 0 | 103 | 0 | 0 |

| China | 28 | 5 | 0 | 0 | 4 | 24 | 0 |

| Indonesia | 62 | 14 | 0 | 4 | 0 | 26 | 32 |

| Philippines | 240 | 39 | 10 | 0 | 0 | 132 | 98 |

| Samoa | 8 | 1 | 0 | 0 | 0 | 8 | 0 |

| Thailand | 5 | 1 | 0 | 0 | 5 | 0 | 0 |

| Timor-Leste | 6 | 1 | 0 | 0 | 0 | 6 | 0 |

| Eastern Europe and Central Asia | 912 | 138 | 144 | 196 | 425 | 147 | 0 |

| Albania | 42 | 5 | 6 | 5 | 31 | 0 | 0 |

| Armenia | 4 | 1 | 0 | 0 | 0 | 4 | 0 |

| Azerbaijan | 88 | 13 | 15 | 7 | 66 | 0 | 0 |

| Bosnia and Herzegovina | 128 | 13 | 6 | 0 | 44 | 78 | 0 |

| Bulgaria | 95 | 17 | 6 | 73 | 16 | 0 | 0 |

| Croatia | 14 | 2 | 0 | 14 | 0 | 0 | 0 |

| Georgia | 56 | 7 | 17 | 0 | 39 | 0 | 0 |

| Kazakhstan | 56 | 10 | 0 | 0 | 49 | 7 | 0 |

| Kosovo | 51 | 7 | 6 | 0 | 16 | 29 | 0 |

| Kyrgyz Republic | 23 | 5 | 4 | 12 | 7 | 0 | 0 |

| Macedonia, FYR | 27 | 4 | 6 | 14 | 0 | 7 | 0 |

| Moldova | 12 | 2 | 0 | 0 | 12 | 0 | 0 |

| Mongolia | 26 | 3 | 20 | 0 | 6 | 0 | 0 |

| Poland | 10 | 2 | 0 | 0 | 10 | 0 | 0 |

| Romania | 40 | 6 | 7 | 0 | 33 | 0 | 0 |

| Russian Federation | 126 | 22 | 17 | 71 | 32 | 6 | 0 |

| Serbia | 19 | 4 | 9 | 0 | 5 | 5 | 0 |

| Tajikistan | 79 | 12 | 19 | 0 | 54 | 6 | 0 |

| Turkey | 5 | 1 | 0 | 0 | 0 | 5 | 0 |

| Ukraine | 11 | 2 | 6 | 0 | 5 | 0 | 0 |

| Latin America and the Caribbean | 1932 | 283 | 183 | 246 | 601 | 902 | 0 |

| Argentina | 42 | 8 | 0 | 0 | 20 | 22 | 0 |

| Bolivia | 173 | 23 | 29 | 10 | 28 | 106 | 0 |

| Brazil | 70 | 13 | 8 | 8 | 8 | 46 | 0 |

| Chile | 15 | 2 | 0 | 0 | 9 | 6 | 0 |

| Colombia | 119 | 19 | 12 | 4 | 11 | 92 | 0 |

| Costa Rica | 57 | 9 | 0 | 0 | 0 | 57 | 0 |

| Dominican Republic | 14 | 2 | 14 | 0 | 0 | 0 | 0 |

| Ecuador | 332 | 45 | 49 | 161 | 11 | 111 | 0 |

| El Salvador | 88 | 12 | 7 | 4 | 42 | 35 | 0 |

| Guatemala | 95 | 15 | 0 | 0 | 0 | 95 | 0 |

| Haiti | 45 | 7 | 0 | 0 | 22 | 23 | 0 |

| Honduras | 87 | 12 | 7 | 0 | 51 | 29 | 0 |

| Mexico | 197 | 35 | 14 | 10 | 156 | 17 | 0 |

| Nicaragua | 165 | 21 | 14 | 10 | 13 | 128 | 0 |

| Panama | 20 | 3 | 0 | 6 | 7 | 7 | 0 |

| Paraguay | 24 | 4 | 6 | 0 | 4 | 14 | 0 |

| Peru | 375 | 51 | 14 | 33 | 214 | 114 | 0 |

| Trinidad and Tobago | 5 | 1 | 0 | 0 | 5 | 0 | 0 |

| Venezuela, RB | 9 | 1 | 9 | 0 | 0 | 0 | 0 |

| Middle East and North Africa | 238 | 31 | 0 | 0 | 49 | 189 | 0 |

| Egypt, Arab Rep. | 70 | 10 | 0 | 0 | 0 | 70 | 0 |

| Iraq | 7 | 1 | 0 | 0 | 0 | 7 | 0 |

| Jordan | 38 | 4 | 0 | 0 | 32 | 6 | 0 |

| Lebanon | 23 | 3 | 0 | 0 | 10 | 13 | 0 |

| Morocco | 63 | 8 | 0 | 0 | 0 | 63 | 0 |

| Sudan | 5 | 1 | 0 | 0 | 0 | 5 | 0 |

| Tunisia | 12 | 1 | 0 | 0 | 0 | 12 | 0 |

| Yemen, Rep. | 20 | 3 | 0 | 0 | 7 | 13 | 0 |

| South Asia | 655 | 101 | 47 | 16 | 220 | 308 | 64 |

| Bangladesh | 100 | 16 | 7 | 0 | 0 | 93 | 0 |

| India | 326 | 50 | 0 | 8 | 177 | 133 | 8 |

| Nepal | 109 | 16 | 13 | 8 | 0 | 32 | 56 |

| Pakistan | 86 | 13 | 27 | 0 | 15 | 44 | 0 |

| Sri Lanka | 34 | 6 | 0 | 0 | 28 | 6 | 0 |

| Total | 4614 | 693 | 828 | 1030 | 2932 | 3638 | 388 |

| Variable | Observations | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| MFIG | 4614 | 0.2261 | 0.4932 | −11.2648 | 5.6116 |

| GROW | 4614 | 3.8943 | 4.2174 | −16.5856 | 33.0305 |

| FD | 4614 | 3.3354 | 0.5450 | 0.6923 | 4.8637 |

| SIZE | 4614 | 16.1813 | 1.7709 | 8.0203 | 22.2021 |

| RISK | 4614 | 0.0778 | 0.1811 | 0.0000 | 10.5350 |

| FDI | 4614 | 4.0507 | 4.7028 | −2.4988 | 53.8108 |

| REM | 4614 | 6.8717 | 7.3769 | 0.0009 | 49.2899 |

| CONC | 4614 | 0.2972 | 0.2405 | 0.0344 | 1.0000 |

| GROW | FD | SIZE | RISK | FDI | REM | CONC | |

|---|---|---|---|---|---|---|---|

| GROW | 1 | ||||||

| FD | −0.0681 | ||||||

| SIZE | −0.0208 | 0.0975 | 1 | ||||

| RISK | −0.1504 | 0.005 | −0.0226 | 1 | |||

| FDI | 0.3608 | −0.1187 | −0.0332 | −0.0485 | 1 | ||

| REM | −0.0627 | 0.0018 | −0.0292 | −0.0063 | 0.0338 | 1 | |

| CONC | 0.0318 | −0.1866 | −0.0963 | −0.0231 | 0.2811 | −0.0726 | 1 |

| Economic Growth ≥ 0 | Economic Growth < 0 | Z | Mean Difference | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| N | Mean | Std. Dev. | Min | Max | N | Mean | Std. Dev. | Min | Max | ||||

| MFIG | 4080 | 0.2447 | 0.4914 | −11.2648 | 5.6116 | 534 | 0.0839 | 0.4847 | −7.0874 | 2.5311 | 9.492 | *** | 2.91 |

| GROW | 4080 | 4.7506 | 3.5048 | 0.0217 | 33.0305 | 534 | −2.6486 | 3.3801 | −16.5856 | −0.0262 | 37.634 | *** | −1.79 |

| FD | 4080 | 3.3438 | 0.5474 | 0.6923 | 4.8637 | 534 | 3.2718 | 0.5220 | 0.9066 | 4.3308 | 4.374 | *** | 1.02 |

| SIZE | 4080 | 16.1694 | 1.7739 | 8.0203 | 22.2021 | 534 | 16.2724 | 1.7469 | 10.5823 | 21.2786 | −1.159 | 0.99 | |

| RISK | 4080 | 0.0712 | 0.0922 | 0.0000 | 1.2000 | 534 | 0.1281 | 0.4648 | 0.0000 | 10.5350 | −10.662 | *** | 0.56 |

| FDI | 4080 | 4.1380 | 4.8835 | −2.4988 | 53.8108 | 534 | 3.3836 | 2.8987 | −0.9247 | 13.6045 | 2.873 | *** | 1.22 |

| REM | 4080 | 6.9094 | 7.3749 | 0.0009 | 49.2899 | 534 | 6.5837 | 7.3929 | 0.0025 | 35.9985 | 2.317 | ** | 1.05 |

| CONC | 4080 | 0.2973 | 0.2414 | 0.0344 | 1.0000 | 534 | 0.2967 | 0.2343 | 0.0371 | 1.0000 | −1.051 | 1.00 | |

| Model 1.a | Model 1.b | |||||||

|---|---|---|---|---|---|---|---|---|

| MFIG | Coefficient | Z | p-Value | Coefficient | Z | p-Value | ||

| GROW | 0.0086 | 1.52 | 0.128 | 0.0780 | 2.59 | 0.010 | *** | |

| FD | 0.0164 | 0.51 | 0.610 | −0.2057 | −0.81 | 0.415 | ||

| SIZE | 0.1167 | 2.70 | 0.007 | *** | −0.0919 | −1.22 | 0.223 | |

| RISK | −1.5183 | −4.80 | 0.000 | *** | −2.1952 | −3.18 | 0.001 | *** |

| FDI | −0.0068 | −2.58 | 0.010 | *** | −0.0342 | −1.92 | 0.055 | * |

| REM | −0.0028 | −1.29 | 0.199 | −0.0046 | −0.41 | 0.682 | ||

| CONC | −0.0783 | −1.11 | 0.267 | 0.3836 | 1.68 | 0.092 | * | |

| REG | 0.0022 | 0.06 | 0.952 | |||||

| AGE1 | −0.2502 | −1.00 | 0.316 | 0.006 | 0.01 | 0.992 | ||

| AGE3 | −0.1296 | −0.47 | 0.635 | −0.0262 | −0.04 | 0.967 | ||

| CONS | −1.2518 | −1.97 | 0.049 | ** | 2.5474 | 2.71 | 0.007 | *** |

| YEAR | 79.84 | 0.000 | *** | 30.78 | 0.002 | *** | ||

| N | 4614 | 714 | ||||||

| n | 693 | 111 | ||||||

| m2 | −0.47 | 0.640 | −0.44 | 0.659 | ||||

| Hansen | 24.48 | 0.378 | 19.36 | 0.308 | ||||

| MFGI | Coefficient | Z | p-Value | |

|---|---|---|---|---|

| GROW | −0.0345 | −1.84 | 0.066 | * |

| FD | −0.0599 | −1.40 | 0.160 | |

| GROW *FD | 0.0145 | 2.03 | 0.042 | ** |

| SIZE | 0.0937 | 2.42 | 0.015 | ** |

| RISK | −1.4790 | −4.10 | 0.000 | *** |

| FDI | −0.0058 | −2.66 | 0.008 | *** |

| REM | −0.0024 | −1.18 | 0.237 | |

| CONC | −0.0598 | −0.92 | 0.357 | |

| AGE1 | −0.1058 | −0.32 | 0.750 | |

| AGE3 | −0.0611 | −0.18 | 0.856 | |

| CONS | −0.7114 | −1.17 | 0.242 | |

| YEAR | 82.73 | 0.000 | *** | |

| N | 4614 | |||

| n | 693 | |||

| m2 | −0.75 | 0.450 | ||

| Hansen | 35.42 | 0.310 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sainz-Fernandez, I.; Torre-Olmo, B.; López-Gutiérrez, C.; Sanfilippo-Azofra, S. Development of the Financial Sector and Growth of Microfinance Institutions: The Moderating Effect of Economic Growth. Sustainability 2018, 10, 3930. https://doi.org/10.3390/su10113930

Sainz-Fernandez I, Torre-Olmo B, López-Gutiérrez C, Sanfilippo-Azofra S. Development of the Financial Sector and Growth of Microfinance Institutions: The Moderating Effect of Economic Growth. Sustainability. 2018; 10(11):3930. https://doi.org/10.3390/su10113930

Chicago/Turabian StyleSainz-Fernandez, Isabel, Begoña Torre-Olmo, Carlos López-Gutiérrez, and Sergio Sanfilippo-Azofra. 2018. "Development of the Financial Sector and Growth of Microfinance Institutions: The Moderating Effect of Economic Growth" Sustainability 10, no. 11: 3930. https://doi.org/10.3390/su10113930

APA StyleSainz-Fernandez, I., Torre-Olmo, B., López-Gutiérrez, C., & Sanfilippo-Azofra, S. (2018). Development of the Financial Sector and Growth of Microfinance Institutions: The Moderating Effect of Economic Growth. Sustainability, 10(11), 3930. https://doi.org/10.3390/su10113930