An Empirical Study of the Policy Processes behind Norway’s BEV-Olution

Abstract

1. Introduction

2. Materials and Methods

2.1. Literature Review

2.2. A Brief Overview of Norwegian Politics and Policy Processes

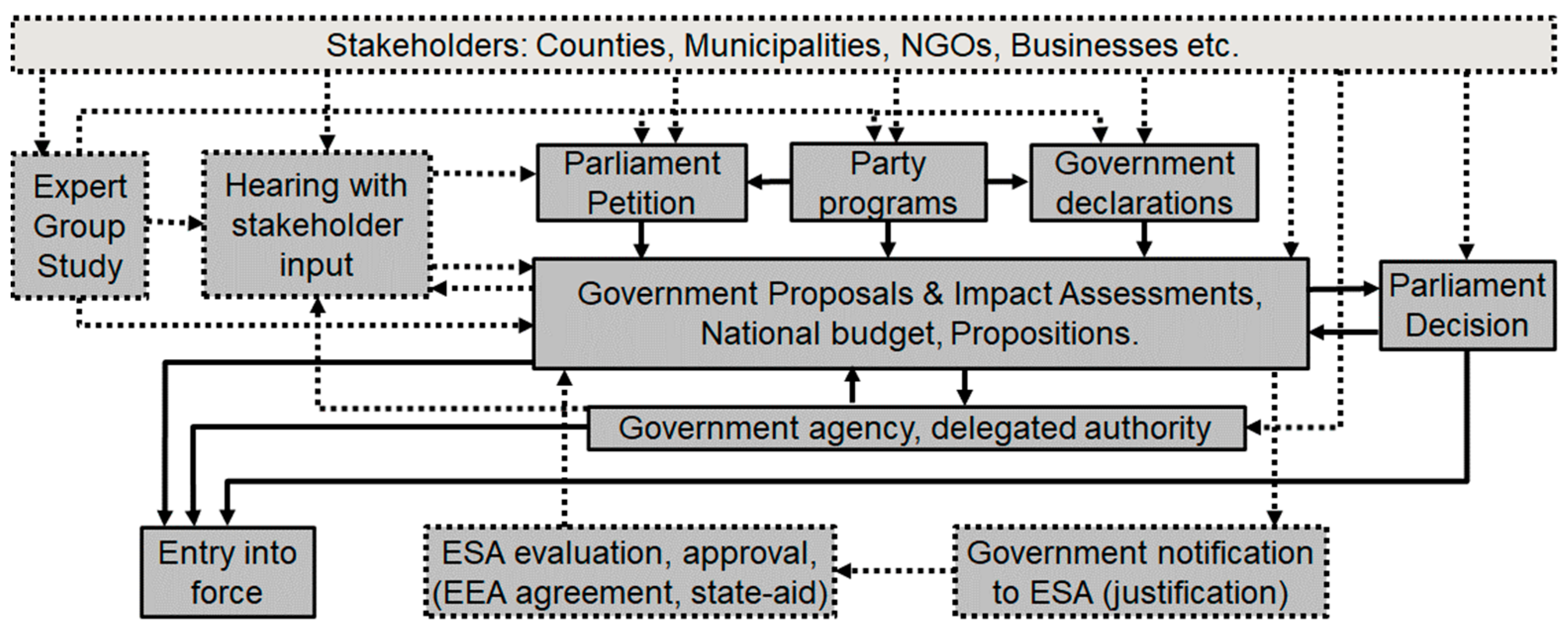

2.3. Method

2.4. Materials

3. Results

3.1. 1990–1997—Policies Enabled Market Experiments to Verify BEVs’ Potential

- Exemption from registration tax and km tax (1990, 1996)

- Exemption and reduction from annual tax (1996)

- Free road tolls (1997)

3.2. 1998–2002—Policies Supported BEV Industrialisation

- Free public parking (1999)

- Reduced company car benefit tax (2000)

- Zero-rate VAT (Value-Added Tax) (2001)

3.3. 2003–2006—Policies Remained in Place as Global BEV Markets Collapsed

- Access to bus lanes (2003/2005)

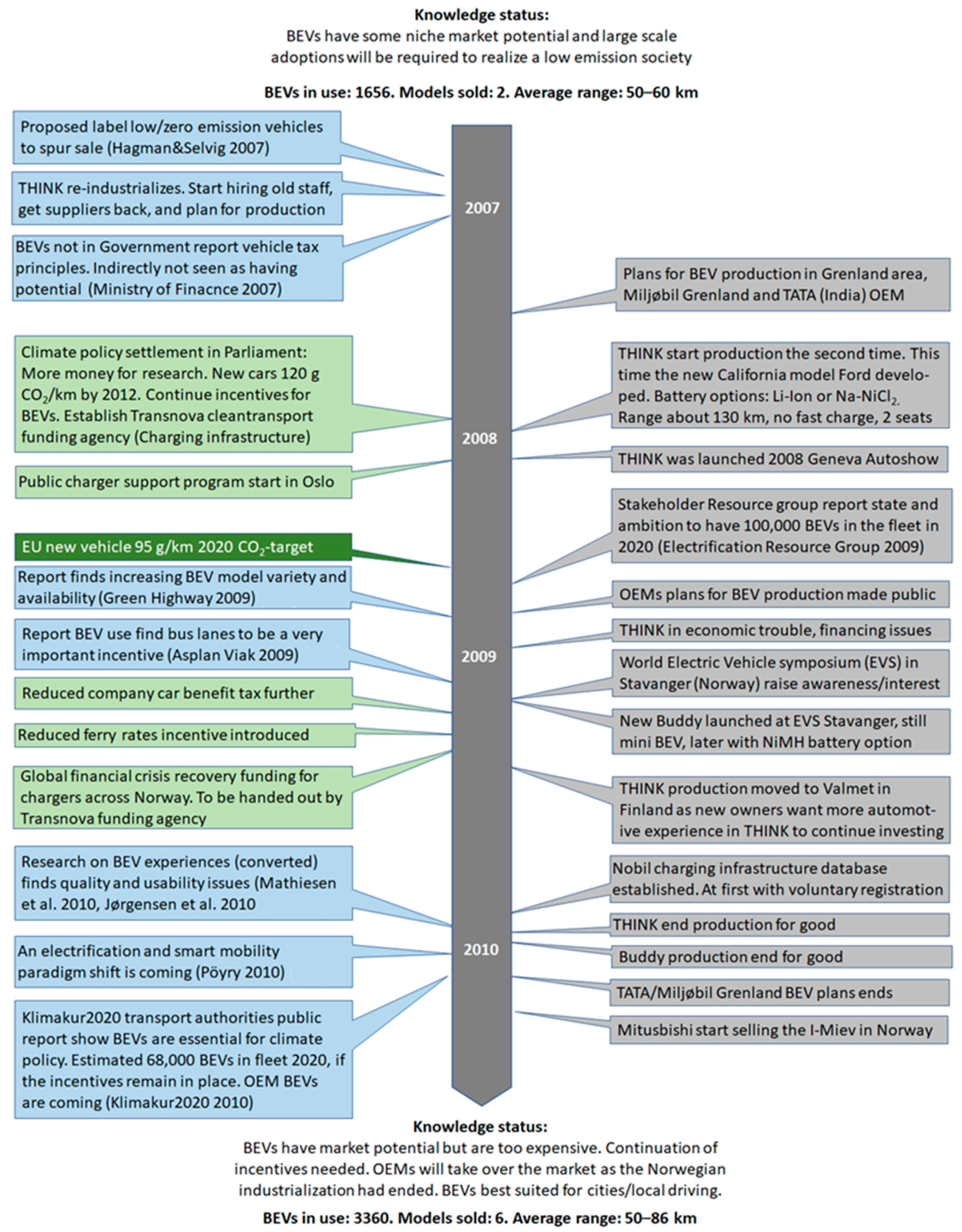

3.4. 2007–2010—Policies Supported BEV Industrialisation in the Global Climate Policy Spur

- Average new vehicle CO2 emissions target of 120 g/km by 2012 (2007)

- Increased vehicle allowance for business trips (2008)

- Reduced ferry rates (2009)

- Transnova funding agency (2009) transport GHG emission reduction measures, first charger support programme

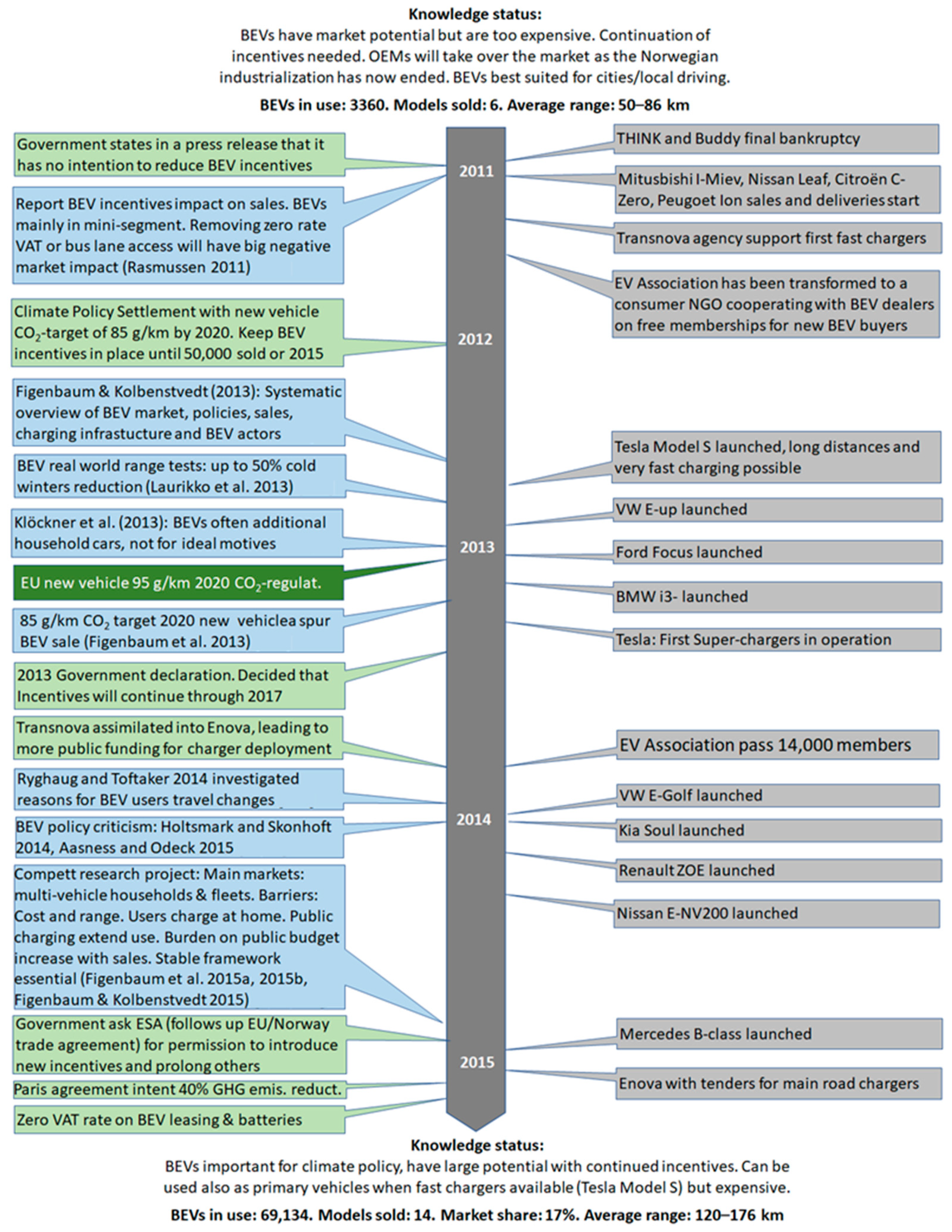

3.5. 2011–2015—Policies Supported the Roll-Out of Increasing Numbers of OEM BEVs

- Average new vehicle CO2 emissions of 85 g/km by 2020 (2012)

- Keep incentives in place until there are 50,000 BEVs in the fleet or through 2015 (2012)

- Keep incentives in place until the end of 2017 (2013)

- Zero-rate VAT for BEV leasing and battery replacement (2015)

- Vehicle taxation policy settlement (2015)

3.6. 2016–2020—Policies Supported the Mass Market to Achieve GHG Emission Reductions

- Keep incentives in place through 2020 (2016/2017)

- Only sell ZEVs from 2025 (2017)

- Exemption from re-registration tax (2018)

- Right to charge for flat owners in joint properties (2018)

- The 50% rule for road tolls, parking fees, and ferry tickets, and acknowledging local authority co-decisions (2018)

- Action plan for infrastructure for alternative fuels in transport (2019)

- Keep incentives in place through 2021 (2020)

- Strategy for post-2025 vehicle taxation (2020)

- Right to charge for flat owners in housing communities (2020)

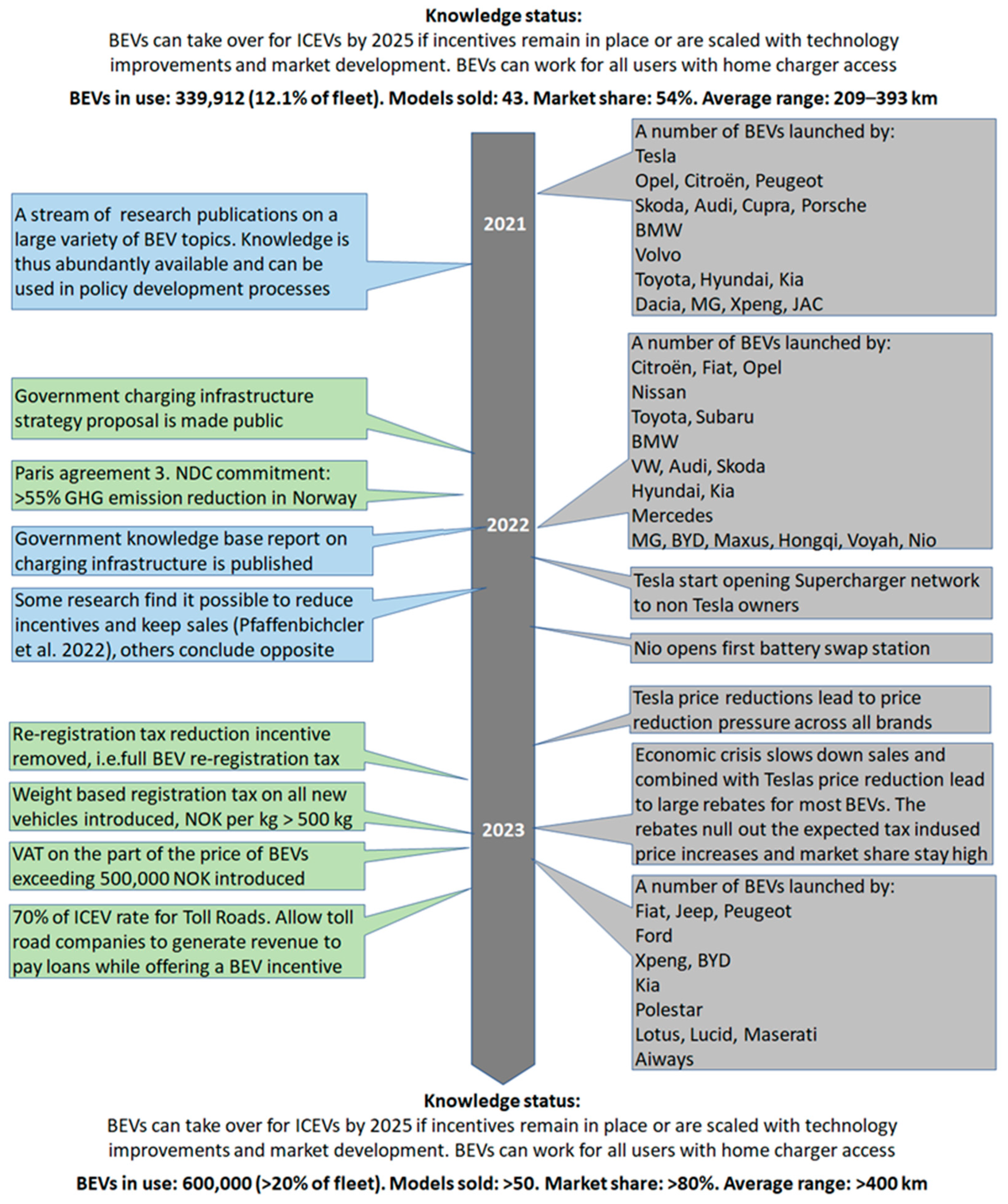

3.7. 2021–2023—Policies Downscaled to Preserve Government Income but Still Meet Targets

- Charging infrastructure strategy proposal (2022)

- Proposal of the removal of zero-rate VAT, to be replaced by a support scheme (2023). VAT to be introduced on the part of the purchase price exceeding NOK 500,000

- New weight tax on all vehicles (2023)

- Removal of reduced re-registration tax incentive (2023)

- Removal of reduced company car benefit tax (2023)

- The 70% rule for toll roads (2023)

3.8. 1990–2023—The Policy Processes from Infancy to Mass Market and Beyond

4. Discussion

5. Conclusions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Socialist | Labour | Centre | Conservative | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Rødt | SV | AP | SP | MDG | V | KRF | H | FRP | |

| The Reds (Socialist) | The Socialist Party | Labour Party Sociodemocrat | Centre Parti (rural/farmers) | The Green Party | The Liberal Party | The Christian Democratic Party | Conservative Party | Progress Party (populist) | |

| 1989–1993 | Stricter emission regulations. Use of natural gas in the transport sector. | Less vehicle use in cities, use road tolls. Emission reductions for diesel cars, BEVs/ZEVs were not mentioned. | Use best available emission reduction technology for all vehicle types. | Not available | Use fuel/other taxes to stimulate a switch over to gas and electricity. No tax on safety/environment equipment. | Differentiate taxes based on emissions. No tax on safety/environment equipment. | Reduce tax on environment equipment (i.e., catalytic converters). | Proposes strong reduction in vehicle taxes to enable people to buy safe and less polluting cars (i.e., new cars). | |

| 1993–1997 | Favourable conditions for BEVs, low fuel consumption vehicles, and biofuels. | BEVs or ZEVs not mentioned. Transfer from vehicles to pub. Transport. New tech. mentioned to reduce pollution but no details. | Favourable conditions for BEVs. Move taxes from purchase to use and exempt BEVS. Work to reduce vehicle use in cities. | Reduce transport as much as possible, prioritise electricity-based transport. Avoid fossil-fuel transport. Introduce restrictions on ICEVs and later bans. | Move taxes from purchase to use, use gas as the main alternative energy carrier. Adjust purchase tax to enable installation of emission-reducing equipment. | No mentions apart from requiring more stringent emission limits. | Stimulate change over to vehicles using less fuel. | Chapter on motor vehicles. Proposes reduction in vehicle taxes. Tax income from transport to be transfer-ed back to the sector. | |

| 1997–2001 | Support use of BEVs to improve air-quality in cities. Increased use of biodiesel, car sharing support, testing of hydrogen. | Stimulate increased testing and change to gas, electricity, or H2 for transport, using vehicle tax system. Increase diesel tax. | BEVs to be 100% exempted from taxes. Reduce vehicle use in cities and increase public transport use. | Reduce vehicle-based transport. Vehicles should be powered by clean electricity and biogas. Develop car sharing with cleaner vehicles. Ban ICEVs in cities in 10 years. | Support increased use of electric vehicles. Move taxes to vehicle usage. Differentiate tax based on fuel consumption. | Norway a front-runner for more environmentally friendly transport. Vehicle users pay real societal costs. Tax system to stimulate BEVs and other low-emission vehicles | No mention of vehicles in particular. A general text on how taxes shall reflect environmentall costs. | Chapter on motor vehicles. Propose strong reduction in vehicle taxes. Tax income from transport to be transferred back to the sector. | |

| 2001–2005 | Use taxes to support low energy use/alternative fuels. Support testing and increase adoption in public fleets. Rebates for car sharing. Less traffic volume with city road tax. | Same as 1997 apart from diesel tax not mentioned. New in 2001: Action plan for large cities that target increased use of ZEVs. | Full-tax-exempt BEVs (VAT, reg. tax, etc.). Continue local incentives (road, toll parking). Support BEV demo projects, H2 in transport. 10% of the fleet to be emission-free by 2005. | Reduction in car-based transport. Vehicles should be powered by clean electricity and biogas. Nat. gas preferred over other fossil options. Car sharing with cleaner vehicles. Higher taxes on ICEVs, later bans. | Stimulate buying, testing, and use of ZEVs. Make use of vehicles in cities more expensive. Move taxes from purchase to vehicle usage. | Norway a front-runner for more environmentally friendly transport. Vehicle users pay real societal costs. Tax system to stimulate BEVs and other low-emission vehicles. Natural gas as alt. fuel. Support H2. | Stimulate use of BEVs and other low- and zero-emission vehicles. Reduce total taxes on vehicles. | Chapter on motor vehicles. Proposes strong reduction in vehicle taxes as measure to renew fleet and reduce emissions. Increased BEV adoption, reduced city pollution. | |

| 2005–2009 | No mention of policies for vehicles other than support the opposite, i.e., public transport. | H2 cars same incentive as BEVs, indirectly support BEV incentives. No mention of new BEV policies. Build H2 fuel stations. | Support increased use of biofuels incl. sales obligation. Support ZEVs and LEVs through the tax system. Keep BEV incentives in place. | Not available. | Focused moved to a hydrogen society as the vision of the future with same tax advantages for hydrogen as BEVs. Biofuels also in focus. | Norway a front-runner for environmentally friendly transport. More focus on use of and research on H2 and other ZEVs. Hydrogen tax exempt. Support biofuel use/prod. | Reduce vehicle taxes to make it easier to buy safe and more environmentally friendly vehicles. | Expand use of NG in transport sector by building infrastructure. Increased use of BEVs/HEVs and fleet renewal to reduce city pollution. | |

| 2009–2013 | Focus on public transport measures and policies for reduction of vehicle-based transport. | 2015 ban on car only using fossil fuel. Plan scaling up sales of ZEVs, incl. importer obligations. Public ZEV procurement. Plan for charging infrastructure deployment. | Reward ZEVs and LEVs in the tax system so that they take over as soon as possible. Also use biogas for transport. | Taxes support ZEVs, PHEVs, LEVs, HEVs, and biofuels. Minimum 20% ZEVs sold 2020, rest LEVs. Build charging infrastructure. H2 available. Scrappage bonus of NOK 40,000 for buying environmentally friendly car. | Ban on gasoline and diesel cars from 2013. Certified biofuels. Registration tax based on CO2 emissions and immediate ban on high emitters. Vehicles OK where public transport does not suffice, but new technology should be used. | Vehicle taxes stim-ulate use of LEVs, BEVs, and FCEVs. Adjust annual (CO2) emission targets for new cars from 2015, ban sale of fossil cars. Public fleets should buy LEVs/ZEVs. Minimum 10% share of biofuel and H2 by 2013. Build more infrastructure for ZEV, H2, and biofuel. | Increased use of hydrogen, HEVs, PHEVs, and BEVs. Increased use of CO2-neutral fuels (biofuels). Public fleets to only procure LEVS or ZEVs. Norway should push for an end to global ICEV production by 2020. | Reduce vehicle taxes to make it easier to buy safe and more environmentally friendly vehicles. Remove taxes on ZEVs. Build alternative fuel and charging infrastructure. | Reduce vehicle taxes. |

| 2013–2017 | BEVs or vehicles not mentioned. Focus on public transport, vehicle-based transport reduction policies. | BEVs compete with ICEVs. Keep incentives. Support other emission-free options and infrastructure, i.e., chargers. 50% of public fleets shall be BEVs/PHEVs. | Continue to use the tax system to reduce emissions from transport. | Reduce GHG emissions from transport, support 2nd-gen. biofuels. Phase in new and environmentally friendly vehicle technology. | All new vehicles BEVs or HEVs, but highest priority is public transport. Use road pricing to curb city traffic. Stimulate car sharing solutions Remove VAT for BEV lease/batteries. Keep/expand BEV incentives to 2020. | Target world’s most environmentally friendly transport. Keep BEV incentives. Build fast chargers between cities. Remove VAT for BEV leasing/batteries. Support 2nd-gen. biofuel development. Strenghten Trans-nova and BEV, H2, and biofuel infrastructure. Expand biofuel and H2. | Increased use of H2, HEVs, PHEVs, BEVs, and biofuels. Public fleets only LEVS or ZEVs. Norway push end of global ICEV production by 2020. Build charging stations. Keep incentives until 10% PEVs on road or 2020. | Continue tax exemption for ZEVs. Build infrastructure for BEVs and hydrogen, use public procurement. Develop biofuel strategy. | Strong reduction in vehicle taxes and increase in scrappage bonus to renew vehicle fleet to make it safer and more environmentally friendly. |

| 2017–2021 | Build good, fast charger capacity in all municipal centres. Focus on public transport measures and vehicle-based transport reduction policies. | Keep BEV incentives in place through 2021. Max half rate of ICEVs for ZEVs for road tolls, parking, and ferries. Biofuel production to be developed. Use 2nd-gen. biofuels in intermedium term. | Pursue ZEVs and biofuels. Build biofuel fueling stations and charging infrastructure. | Continue ZEV support. Keep purchase incentives, slowly phase out local incentives by 2030. Use taxes to get 100% ZEV share by 2025. Stronger focus on biofuels. Intensify building of charging and energy stations. Strong support for H2 use. | Phase out sales of ICEVs by 2020. Public fleets must buy ZEVs. Higher ICEV taxes. Build energy stations to support ZEVs everywhere. Always be cheaper to select a ZEV. Less traffic in cities and support ZEVs in districts. Support charging station building and BEV leasing. Continue ZEV advantages until competitive. | Keep incentives until ZEVs competitive by themselves, at least until 2025. ZEVs have lasting advantage of half price of ICEVs for road tolls/ferries. Ensure good infrastructure for fast/normal charging across the country. Cooperate w. companies on nationwide energy stations with chargers and biofuel and H2 dispensers. Public fleets buy ZEVs (not police). | Emission-free sector by 2030. Increase BEVs, H2, HEVs, PHEVs, and biofuel. Public fleets to only procure LEVs or ZEVs. Norway push end to global ICEV production by 2020. Build charging, hydrogen, and biofuel stations faster. Keep incentives until l10% PEVs on road or 2020. | Zero emission vision for transport. Shall be worthwhile to go for ZEVs. Support for infrastructure. | Proposes strong reduction in vehicle taxes and increase in scrappage bonus to renew vehicle fleet to make it safer and more environmentally friendly. |

| 2021–2025 | References NTP target. Build BEV fast-charging capacity in municipal centres. Maximum-limit BEV subsidies. Tax above limit. Increase H2 efforts. | Reach 2025 target 2 years earlier/2023. Economic to buy a ZEV. Increase BEV tax followed by a larger ICEV tax. VAT price > NOK 600,000. Investigate an ICEV ban and BEV sharing. Tighten ICEV vs. BEV loop-hole leasing. | Reach the 2025 ZEV target. Reduce tax incentives on expensive BEVs and increase CO2 tax on ICEVs. VAT on prices exceeding NOK 600,000. Increase ICEV taxes. Build fast chargers. | Reach the 2025 ZEV target for new vehicles. Avoid single BEV focus due to blackout risk. VAT on price > NOK 600,000. Propose building of 10,000 fast chargers and national plan for charging infrastructure. Gradual reduction in user advantages. | Reach the 2025 ZEV target for new vehicles 2 years earlier/2023. Support rural environmentally friendly transport and BEV leasing and large-scale building of chargers, incl. for flat owners. Stimulate car sharing. Incentives until ZEVs competitive. Increase taxes on ICEVs and CO2. | Reach the 2025 ZEV target for new vehicles. We are the BEV advocate and will ensure BEV advantages through 2025. The advantage must remain until BEVs reach a competitive price. Secure charging infrastructure is available in the whole country. | Reach the 2025 ZEV target for new vehicles. Build charging infrastructure (housing communities and common garages mentioned specifically). Establish a sustainable taxation system ensuring it is economical to buy a BEV over an ICEV. | Follow up the 2025 target for new vehicles. Build fast and ultra-fast chargers incl. for flat owners. Gradually step down ZEV incentives, starting with the most expensive, but always more economic to buy a BEV. | Proposes strong reduction in vehicle taxes in general, BEVs only mentioned as an example. |

| Government | Period | Parties | Support in Parliament | Government Declaration | BEV-Related Topics in Declaration | BEV Incentives and Targets Introduced | ||

|---|---|---|---|---|---|---|---|---|

| Year Decided | Intro Year | Description | ||||||

| Brundtland | 9 May 1986–16 October 1989 | AP | Minority | Brundt-land 1986 “Speech” | No mentions of climate or CO2, no measures within transport related to greenhouse gas emissions. Note that the Brundtland commision (UN) “Our common future” report came in 1987, leading to a higher political focus on environment issues, including climate, following years. | 1989 | 1990 | Temp. registration tax exemption to allow BEV experiments. |

| 1989 | 1990 | Km tax exemption to allow BEV experiments. | ||||||

| Syse | 16 October 1989–3 November 1990 | H, KrF, SP | Minority | Lysebu 1989 | None, CO2 emission reduction of high priority, reforestation to reduce CO2. Reduce local pollution from transport with 3-way catalysts and traffic measures | Carried through the decicions in parliament in late 1989 to provide exemptions from registration and km tax. | ||

| Brundtland 3 | 3 November 1990–25 October 1996 | AP | Minority | Brundt-land 1990 “Speech” | None, prioritise global climate policy agreement, focus on sector overarching environmental policies | 1995 | 1996 | Permanent registration tax exemption. |

| 1995 | 1996 | Annual tax exemption. | ||||||

| Jagland | 25 October 1996–17 October 1997 | AP | Minority | Jagland 1996 | None, but talks about an ecologically sustainable society. | 1996 | 1997 | Road toll exemption. |

| Bondevik 1 | 17 October 1997–17 March 2000 | KrF, SP, V | Minority | Voksenåsen 1997 | None, high priority to reduce greenhouse gases, focus on Kyoto negotations and reaching an agreement. Transportation: Focus on reducing and supporting public transport. | 1997 | 1999 | Free parking. |

| 1999 | 2000 | Reduced imposed benefit tax on disposing a company car, 50% reduction. | ||||||

| Stoltenberg 1 | 17 March 2000–19 October 2001 | AP | Minority | Stoltenberg 2000, “Speech from the throne” | None specific, mentions Kyoto as a breakthrough, Norway being a frontrunner on environmental issues. | 2000 | 2001 | VAT exemption. |

| Bondevik 2 | 19 October 2001–17 October 2005 | KrF, H, V | Minority | Sem 2001 | None, high priority to reduce greenhouse gases, focus on Kyoto negotiations and reaching a global agreement. Transportation: Focus on reducing and supporting public transport. | 2002 | 2003 | Bus lane access test—Greater Oslo. |

| 2004 | Traffic insurance tax moved to annual tax, BEV owners had to pay that tax. | |||||||

| 2005 | 2005 | Bus lane access permanent and national. | ||||||

| Stoltenberg 2 | 17 October 2005–7 October 2009 | AP, SV, SP | Majority | Soria Moria 1 2005 | Follow up Kyoto, work for more ambitious global climate policy agreement, strive for increased use of environmentally friendly vehicles, make it economical to buy low-emission vehicles, biofuel focus. | 2008 | 2009 | Reduced ferry rates. |

| 2008 | 2008 | Increased km allowance for electric car use on business trips. | ||||||

| 2008 | 2012 | Average new vehicle CO2 emissions below 120 g/km by 2012. Broad agreement in parliament. | ||||||

| 2009 | 2009 | Creation of support agency Transnova. | ||||||

| 2009 | 2010 | Financial crisis support programme for chargers. | ||||||

| 7 October 2009–16 October 2013 | AP, SV, SP | Majority | Soria Moria 2 2009 | Work for a strong international climate agreement, exceed Kyoto obligations by 10%, transport policy shall support climate policy, action plan for ZEV/LEV introduction, biofuels support, charging stations to be built. | 2011 | 2011 | First support programme for fast chargers. | |

| 2012 | 2020 | Average new vehicle CO2 emissions below 85 g/km by 2020. | ||||||

| 2012 | 2015 | Keep incentives in place until the end of 2015 or 50,000 BEVs are in the fleet. Broad agreement in parliament. | ||||||

| Solberg | 16 October 2013–17 January 2018 | H, FrP | Minority, supported by V, KrF | Sundvolden 2013 | Continue BEV tax regime until 2017, go through tax policy, follow-up on 2012 climate policy settlement in Stortinget. | 2013 | 2017 | Keep purchase incentives in place until the end of 2017. |

| 2013 | 2015 | Zero VAT rate for leasing and battery replacement. | ||||||

| 2014 | 2015 | Restriction on bus lane access on west corridor to Oslo in rush hour introduced. | ||||||

| 2014 | 2015 | Transnova assimilated into Enova. | ||||||

| Solberg continued | 2015 | 2015–18 | Support programme for fast chargers along major roads. | |||||

| 2016 | 2016 | Restriction on bus lane access on southeast corridor to Oslo in rush hour introduced. | ||||||

| 2016 | 2017 | Only sell ZEVs by 2025. Broad agreement in parliament. | ||||||

| 2016 | 2017 | Re-registration tax exemption. | ||||||

| 2018 | Law change parking: Parking facilities and public parking can charge full rate for BEVs, and must offer up to 6% of spaces with charging access. | |||||||

| 2016 | 2018 | Parliament decide rule that maximum rate for toll roads, parking, and ferries shall be 50% of the rate of ICEVs, local authorities to decide on the level up to the maximum. | ||||||

| 2017 | 2017 | Law change for condominiums to regulate access to charging in common parking facilities. | ||||||

| 2017 | 2018 | Full exemption from annual tax, or rather the tax on insurance that replaced the annual tax. | ||||||

| 17 January 2018–22 January 2019 | H, FrP, V | Minority, KrF support | Jeløya 2018 | 40% greenhouse gas emission reduction by 2030 over 1990, suggest new ambitious target to Paris Agreement. NTP vehicle targets basis for policy (only ZEVs sold from 2025). | 2018 | 2021 | ||

| 22 January 2019–13 January 2020 | H, FrP, V, KrF | Majority | Grana-volden 2019 | More ambitious climate policy target, 50% reduction in transport sector by 2030, NTP vehicle targets (only ZEVs sold from 2025). | 2019 | 2021 | Keep purchase incentives in place until end of 2021. | |

| 2019 | Action plan for alternative fuel infrastructure. | |||||||

| 13 January 2020–end 2021 | H, V, KrF | Minority | Grana-volden 2019 | See above | 2020 | 2020 | Law change for housing communities to regulate access to charging in common parking facilities. | |

| 2020 | 2021–22 | Keep zero-rate VAT through 2022. | ||||||

| 2020 | 2021 | Reduced-rate insurance tax (30% below ICEV rate). | ||||||

| 2020 | 2025 | Future principles for vehicle taxation post-2025 transition period 2022–2025. | ||||||

| Støre | 14 October 2021-This day | A, SP | Minority, with SV primary supporter | Hurdals-platt-formen | More ambitious climate policy target, -55% reduction of Norwegian emissions by 2030 compared to 1990. | |||

| Reduce GHG emissions from transport and contribute to meeting national climate policy goals. | ||||||||

| Make it attractive to select LEVs and ZEVs, 100% of new vehicles fossil-fuel-free from 2025, contribute to ZEVs keeping their competitive advantage vs. ICEVs. | 2022 | Strategy process for charging infrastructure initiated. | ||||||

| Arrange the tax system so that it is fair and contributes to cuts in greenhouse gas emissions. | 2022 | 2023- | Proposal to replace zero-rate VAT with support scheme. | |||||

References

- Figenbaum, E. Norway the World Leader in BEV Adoption. In Who’s Driving Electric Cars; Understanding Consumer Adoption and Use of Plug-in Electric Cars; Springer Nature: Berlin, Germany, 2020; Available online: https://link.springer.com/book/10.1007/978-3-030-38382-4#about (accessed on 16 January 2024).

- Norwegian Vehicle Register; Norwegian Public Roads Administration: Oslo, Norway, 2024.

- Figenbaum, E. The 1990 to 2020 Technology Innovation System (TIS) Supporting Norway’s Bev Revolution. SSRN 2022. Available online: https://ssrn.com/abstract=4061401 (accessed on 20 December 2023). [CrossRef]

- Langeland, O.; George, C.; Figenbaum, E. Technological Innovation System and Transport Innovations: Understanding Vehicle Electrification in Norway. In Innovations in Transport: Success, Failure and Societal Impacts; Edward Elgar: Cheltenham, UK, 2022; Available online: https://www.elgaronline.com/edcollchap-oa/book/9781800373372/book-part-9781800373372-14.xml (accessed on 16 January 2024).

- Figenbaum, E. Perspectives On Norway’s Supercharged Electric Vehicle Policy. Environ. Innov. Soc. Transitions 2017, 25, 14–34. [Google Scholar] [CrossRef]

- Figenbaum, E. Retrospective Total Cost of Ownership Analysis of Battery Electric Vehicles in Norway. Transp. Res. Part D Transp. Environ. 2022, 105, 103246. [Google Scholar] [CrossRef]

- Figenbaum, E.; Kolbenstvedt, M. Competitive Electric Town Transport: Main Results from COMPETT—An Electromobility + Project; Report 1422/2015; Institute of Transport Economics: Oslo, Norway, 2015; Available online: https://www.toi.no/publications/competitive-electric-town-transport-main-results-from-compett-and-electromobility-project-article33368-29.html (accessed on 16 January 2024).

- Figenbaum, E.; Kolbenstvedt, M.; Elvebakk, B. Electric Vehicles–Environmental, Economic and Practical Aspects: As Seen by Current and Potential Users; Compett and TØI report 1329/2014; Institute of Transport Economics: Oslo, Norway, 2014; Available online: https://www.toi.no/publications/electric-vehicles-environmental-economic-and-practical-aspects-as-seen-by-current-and-potential-users-article32644-29.html (accessed on 16 January 2024).

- Figenbaum, E.; Nordbakke, S. Battery Electric Vehicle User Experiences in Norway’s Maturing Market; TØI report 1719/2019; Institute of Transport Economics: Oslo, Norway, 2019; Available online: https://www.toi.no/publications/battery-electric-vehicle-user-experiences-in-norway-s-maturing-market-article35709-29.html?deviceAdjustmentDone=1 (accessed on 16 January 2024).

- Figenbaum, E.; Kolbenstvedt, M. Learning from Norwegian Battery Electric and Plug-In Hybrid Vehicle Users—Results from a Survey of Vehicle Owners; TØI report 1492/2016; Institute of Transport Economics: Oslo, Norway, 2016; Available online: https://www.toi.no/publications/learning-from-norwegian-battery-electric-and-plug-in-hybrid-vehicle-users-results-from-a-survey-of-vehicle-owners-article33869-29.html (accessed on 16 January 2024).

- Figenbaum, E.; Thorne, R.J.; Amundsen, A.H.; Pinchasik, D.R.; Fridstrøm, L. From Market Penetration to Vehicle Scrappage—The Movement of Li-Ion Batteries through the Norwegian Transport Sector; TOI report 1756/2020; Institute of Transport Economics: Oslo, Norway, 2020; Available online: https://www.toi.no/publications/from-market-penetration-to-vehicle-scrappage-the-movement-of-li-ion-batteries-through-the-norwegian-transport-sector-article36209-29.html (accessed on 16 January 2024).

- Transport & Environment. Electric Surge: Carmakers’ BEV Plans across Europe 2019–2025; Transport & Environment: Brûssel, Belgium, 2019; Available online: https://www.transportenvironment.org/publications/electric-surge-carmakers-electric-car-plans-across-europe-2019-2025 (accessed on 16 January 2024).

- Figenbaum, E. Battery Electric Vehicle Fast Charging—Evidence from the Norwegian Market. World Electr. Veh. J. 2020, 11, 38. [Google Scholar] [CrossRef]

- Figenbaum, E.; Wangsness, P.B.; Amundsen, A.H.; Milch, V. Empirical Analysis of the User Needs and the Business Models in the Norwegian Charging Infrastructure Ecosystem. World Electr. Veh. J. 2022, 13, 185. [Google Scholar] [CrossRef]

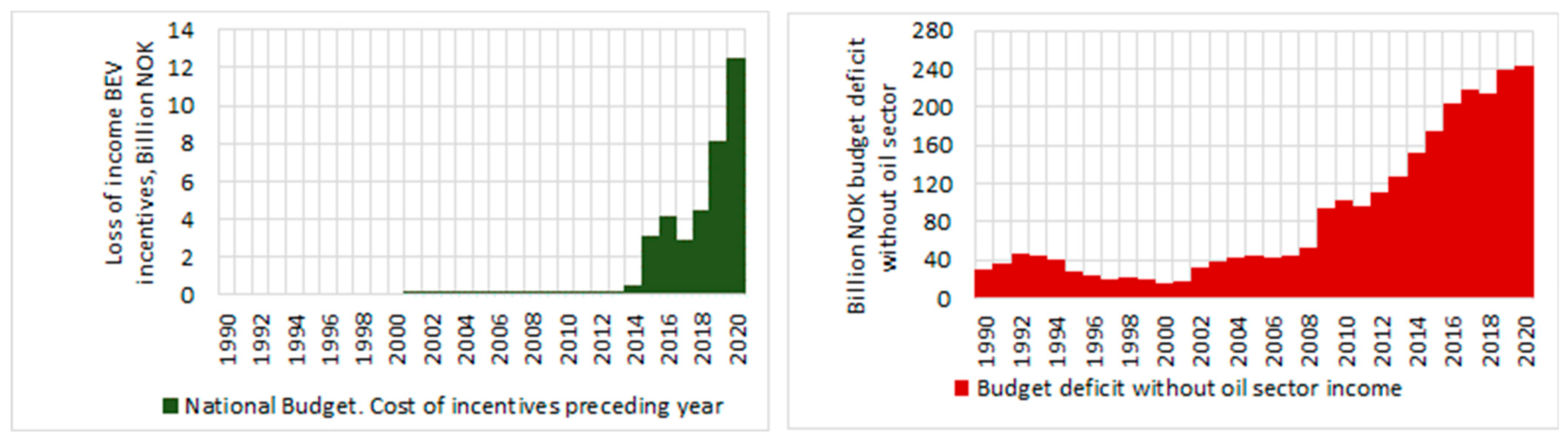

- Ministry of Finance. National Budget Documents 2021. 2020. Available online: https://www.regjeringen.no/no/statsbudsjett/2021/id2741050/ (accessed on 16 January 2024).

- Ryghaug, M.; Skjølsvold, T.M. How policies and actor strategies affect electric vehicle diffusion and wider sustainability transitions. Proc. Natl. Acad. Sci. USA 2023, 120, e2207888119. [Google Scholar] [CrossRef]

- Fevang, E.; Figenbaum, E.; Fridstrøm, L.; Halse, A.H.; Hauge, K.E.; Johansen, B.J.; Raaumm, O. Who goes electric? The anatomy of electric car ownership in Norway. Transp. Res. Part D 2021, 92, 102727. [Google Scholar] [CrossRef]

- Bjerkan, K.Y.; Nørbech, T.E.; Nordtømme, M.E. Incentives for promoting Battery Electric Vehicle (BEV) adoption in Norway. Transp. Res. Part D Transp. Environ. 2016, 43, 169–180. [Google Scholar] [CrossRef]

- Mersky, A.C.; Sprei, F.; Samaras, C.; Qian, Z. Effectiveness of incentives on electric vehicle adoption in Norway. Transp. Res. Part D 2016, 46, 56–68. [Google Scholar] [CrossRef]

- Fridstrøm, L.; Østli, V. The vehicle purchase tax as a climate policy instrument. Transp. Res. Part A 2017, 96, 168–189. [Google Scholar] [CrossRef]

- Fearnley, N.; Pfaffenbichler, P.; Figenbaum, E.; Jellinek, R. E-Vehicle Policies and Incentives—Assessment and Recommendations; TØI-rapport 1421/2015; Transportøkonomisk Institutt: Oslo, Norway, 2015; Available online: https://www.toi.no/publications/e-vehicle-policies-and-incentives-assessment-and-recommendations-article33367-29.html (accessed on 16 January 2024).

- Aurland-Bredesen, K.J. Too green to be good: The efficiency loss of the Norwegian electric vehicle policy. J. Environ. Econ. Policy 2017, 6, 404–414. [Google Scholar] [CrossRef]

- Pfaffenbichler, P.; Emberger, E.; Fearnley, N.; Figenbaum, E. Simulating the effects of tax exemptions for plug-in electric vehicles in norway. In Proceedings of the European Transport Conference, Milan, Italy, 7–9 September 2022. [Google Scholar]

- Figenbaum, E. The contribution of research and knowledge accumulation in the development of the Norwegian battery electric vehicle market. Transp. Res. Procedia 2023, 72, 4127–4134. [Google Scholar] [CrossRef]

- Bjerkan, K.Y.; Bjørge, N.M.; Babri, S. Transforming socio-technical configurations through creative destruction: Local policy, electric vehicle diffusion, and city governance in Norway. Energy Res. Soc. Sci. 2021, 82, 102294. [Google Scholar] [CrossRef]

- Lemphers, N.; Bernstein, S.; Hoffman, M.; Wolfe, D.A. Rooted in place: Regional innovation, assets, and the politics of electric vehicle leadership in California, Norway, and Quebec. Energy Res. Soc. Sci. 2022, 87, 102462. [Google Scholar] [CrossRef]

- Holtsmark, B.; Skonhoft, A. The Norwegian support and subsidy policy of electric cars. Should it be adopted by other countries? Environ. Sci. Policy 2014, 42, 160–168. [Google Scholar] [CrossRef]

- Aasness, M.A.; Odeck, J. The increase of electric vehicle usage in Norway—Incentives and adverse effects. Eur. Transp. Res. Rev. 2015, 7, 34. [Google Scholar] [CrossRef]

- Haustein, S.; Jensen, A.F.; Cherchi, E. Battery electric vehicle adoption in Denmark and Sweden: Recent changes, related factors and policy implications. Energy Policy 2021, 149, 112096. [Google Scholar] [CrossRef]

- Mazur, C.; Contestabile, M.; Offer, G.J.; Brandon, N.P. Assessing and comparing German and UK transition policies for electric mobility. Environ. Innov. Soc. Transit. 2015, 14, 84–100. [Google Scholar] [CrossRef]

- Calef, D.; Goble, R. The allure of technology: How France and California promoted electric and hybrid vehicles to reduce urban air pollution. Policy Sci. 2007, 40, 1–34. [Google Scholar] [CrossRef]

- Haas, T.; Sander, H. Decarbonizing Transport in the European Union: Emission Performance Standards and the Perspectives for a European Green Deal. Sustainability 2020, 12, 8381. [Google Scholar] [CrossRef]

- Kester, J.; Noel, L.; Zarazua de Rubens, G.; Sovacool, B.K. Policy mechanisms to accelerate electric vehicle adoption: A qualitative review from the Nordic region. Renew. Sustain. Energy Rev. 2018, 94, 719–731. [Google Scholar] [CrossRef]

- Collantes, G.; Sperling, D. The origin of California’s zero emission vehicle mandate. Transp. Res. Part A Policy Pract. 2008, 42, 1302–1313. [Google Scholar] [CrossRef]

- California Air Resources Board. Midterm Review Report. Advanced Clean Cars. 2017. Available online: https://ww2.arb.ca.gov/resources/documents/2017-midterm-review-report (accessed on 16 January 2024).

- Commission Staff Working Document Impact Assessment Part 1 Accompanying the Document Proposal for a Regulation of the European Parliament and of the Council amending Regulation (EU) 2019/631 as Regards Strengthening the CO2 Emission Performance Standards for New Passenger Cars and New Light Commercial Vehicles in Line with the Union’s Increased Climate Ambition. Document 52021SC0613. SWS/2021/613 Final. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex%3A52021SC0613 (accessed on 16 January 2024).

- Figenbaum, E.; Fearnley, N.; Pfaffenbichler, P.; Hjorthol, R.; Kolbenstvedt, M.; Emmerling, B.; Jellinek, F.; Bonnema, G.M.; Ramjerdi, F.; Iversen, L.M. Increasing competitiveness of e-vehicles in Europe. Eur. Transp. Res. Rev. 2015, 7, 28. Available online: http://link.springer.com/article/10.1007%2Fs12544-015-0177-1 (accessed on 16 January 2024). [CrossRef]

- Münzel, C.; Plötz, P.; Sprei, F.; Gnann, T. How large is the effect of financial incentives on electric vehicle sales?—A global review and European analysis. Energy Econ. 2019, 84, 104493. Available online: https://www.sciencedirect.com/science/article/pii/S0140988319302749 (accessed on 16 January 2024). [CrossRef]

- Lovdata. Instruks Om Utredning Av Konsekvenser, Foreleggelse Og Høring Ved Arbeidet Med Offentlige Utredninger, Forskrifter, Proposisjoner Og Meldinger Til Stortinget. For-2000-02-18-108. 2000, Revised 2005 and 2016. Available online: https://lovdata.no/dokument/LTI/forskrift/2000-02-18-108 (accessed on 16 January 2024).

- Lovdata. Instruks Om Utredning Av Konsekvenser, Foreleggelse Og Høring Ved Arbeidet Med Offentlige Utredninger, For-Skrifter, Proposisjoner Og Meldinger Til Stortinget. For-1994-12-16-4062. 1994. Available online: https://lovdata.no/dokument/INSO/forskrift/1994-12-16-4062 (accessed on 16 January 2024).

- Lovdata. Regelverksinstruksen. Bestemmelsen Om Arbeidet Med Offentlige Utredninger, Lover, Forskrifter, Stortingsmeldinger Og-Proposisjoner. For-1985-08-30-9952. 1985. Available online: https://lovdata.no/dokument/INSO/forskrift/1985-08-30-9952 (accessed on 16 January 2024).

- Ministry of Finance. Rundskriv R. Prinsipper Og Krav Ved Utarbeidelse Av Samfunnsøkonomiske Analyser. 2021. Available online: https://www.regjeringen.no/globalassets/upload/fin/vedlegg/okstyring/rundskriv/faste/r_109_2021.pdf (accessed on 16 January 2024).

- Ministry of Finance. Prinsipper Og Krav Ved Utarbeidelse Av Samfunnsøkonomiske Analyser MV. R-109/14. Available online: https://www.regjeringen.no/globalassets/upload/fin/vedlegg/okstyring/rundskriv/faste/r_109_2014.pdf?id=2220435 (accessed on 16 January 2024).

- Ministry of Finance. Behandling Av Kalkulasjonsrente, Risiko, Kalkulasjonspriser Og Skattekostnad I Samfunnsøkonomiske Analyser. R-109/2005. Available online: https://www.regjeringen.no/globalassets/upload/fin/vedlegg/okstyring/rundskriv/faste/r_109_2005.pdf (accessed on 16 January 2024).

- Ministry of Finance. Behandling Av Diskonteringsrente, Risiko, Kalkulasjonspriser Og Skattekostnad I Samfunnsøkonomiske Analyser. R-14/99. Available online: https://www.regjeringen.no/globalassets/upload/fin/vedlegg/okstyring/rundskriv/arlige/1999/r_14_1999.pdf (accessed on 16 January 2024).

- Kingdon, J. Agendas, Alternatives and Public Policy, 2nd ed.; Pearson: New York, NY, USA, 2010. [Google Scholar]

- Asphjell, A.; Asphjell, Ø.; Kvisle, H.H. 2013 Elbil på Norsk; Transnova: Hong Kong, 2013; ISBN 978-82-7704-142-1. (In Norwegian) [Google Scholar]

- Ikke Unntak, Faktaboks I Artikkel: Staten Stopper Forskning; News article, Avgift 160000; VG: Oslo, Norway, 1985.

- Figenbaum, E. Elbiler–Teknikk, Forskning og utvikling, Infrastruktur; Marked. Rapport nr. 271 (01) 1993; Teknologisk Institutt: Oslo, Norway, 1993. [Google Scholar]

- Figenbaum, E. Testprogram for Elbiler–Elbiler i Norge–Brukererfaringer; Report; Teknologisk Institutt: Oslo, Norway, 1994. [Google Scholar]

- Figenbaum, E. Norwegian Experience. In Electric & Hybrid Vehicle Technology 95; UK & International Press: London, UK, 1995. [Google Scholar]

- Figenbaum, E. Testprogram for Elbiler–Hovedrapport; Report; Teknologisk Institutt: Oslo, Norway, 1995. [Google Scholar]

- Figenbaum, E. Miljøvennlige Biler i Flåter–Kartlegging av bilflåter; Report; Teknologisk Institutt: Oslo, Norway, 1996. [Google Scholar]

- Figenbaum, E. Miljøvennlige Biler i Flåter–Hovedrapport; Report; Teknologisk Institutt: Oslo, Norway, 1997. [Google Scholar]

- Figenbaum, E. PIVCO Markedsintroduksjon–Ytelsestester; Report; Teknologisk Institutt: Oslo, Norway, 1997. [Google Scholar]

- Berge Lover Nedsatt El-Bilavgift; News article; NTB Tekst: Oslo, Norway, 1989.

- Ministry of Finance. National Budget Documents 1990. St.prp nr. 1 Statsbudsjettet 1990 (1989–1990), Document 1: Statsbudsjettet Medregnet Folketrygden. Document 2: Skatter Og Avgifter Til Statskassen. 1989. Available online: https://stortinget.no/no/Saker-og-publikasjoner/Stortingsforhandlinger/Lesevisning/?p=1989-90&paid=1&wid=a&psid=DIVL801&pgid=a_0271 (accessed on 16 January 2024).

- Parliament. 1990 National Budget Negotiation. Decision in the Parliament to Temporary Exempt BEVs from the Vehicle Registration Taxa s proposed by the Government in: St.prp nr. 1 1989-90, Dokument 1: Statsbudsjettet Medregnet Folketrygden, Dokument 2: Skatter Og Avgifter Til Statskassen. 1989. Available online: https://stortinget.no/no/Saker-og-publikasjoner/Stortingsforhandlinger/Lesevisning/?p=1989-90&paid=1&wid=a&psid=DIVL801&pgid=a_0047 (accessed on 16 January 2024).

- Ministry of Finance. National Budget Vehicle Taxation Reform Document. St prp nr 1 Tillegg nr 3. 1995. Available online: https://www.stortinget.no/no/Saker-og-publikasjoner/Stortingsforhandlinger/Lesevisning/?p=1995-96&paid=1&wid=c&psid=DIVL2868 (accessed on 16 January 2024).

- Parliament. 1995 National Budget Vehicle Reform Negotiation Meeting Minutes. Stortingsbehandling Av Avgiftsvedtak for 1996. Stortinget 8 Desember 1995. Available online: https://www.stortinget.no/no/Saker-og-publikasjoner/Stortingsforhandlinger/Lesevisning/?p=1995-96&paid=7&wid=a&psid=DIVL14&pgid=b_0517&s=True (accessed on 16 January 2024).

- Ministry of Finance. National Budget Documents. 1995. Available online: https://www.stortinget.no/no/Saker-og-publikasjoner/Saker/Sak/?p=7815 (accessed on 24 October 2023).

- Ministry of Finance. National Budget Document 2023. 2022. Available online: https://www.regjeringen.no/no/statsbudsjett/2023/id2927365/ (accessed on 16 January 2024).

- Parliament. Budsjett-Innst. S. NR. 1 (2003–2004) Innstilling Til Stortinget FRA Finanskomiteen st.meld. NR. 1 (2003–2004), st.prp. NR. 1 (2003–2004) OgSt.prp. nr. 1 Tillegg nr. 1-11 (2003–2004); National Budget 2004 Negotiation in the Parliament, Meeting Minutes; Stortinget: Oslo, Norway, 2003. [Google Scholar]

- Parliament. Nyere, Sikrere Og Mer Miljøvennlig Bilpark; Parliament Vehicle Taxation Policy Settlement, Bilavgiftsforlik; Agreement between the Majority of Parties in the Parliament: Oslo, Norway, 2015. [Google Scholar]

- Parliament. Minutes of the National Budget for 2017 Debate in the Parliament. Meeting 5. Des. 2016, 10.00. 1. Finansministerens Redegjørelse Om Regjeringens Forslag Til Statsbudsjett Og Om Nasjonalbudsjettet for 2017 899, 2. Nasjonalbudsjettet 2017 Og Forslag Til Statsbudsjett for 2017. 2016. Available online: https://www.stortinget.no/globalassets/pdf/referater/stortinget/2016-2017/refs-201617-12-05.pdf (accessed on 16 January 2024).

- Ministry of Finance. National Budget Documents 2018. 2017. Available online: https://www.regjeringen.no/no/statsbudsjett/2018/id2570841/ (accessed on 16 January 2024).

- Ministry of Finance. National Budget Documents 2022. 2021. Available online: https://www.regjeringen.no/no/statsbudsjett/2022/id2871447/ (accessed on 16 January 2024).

- Simmones, H.; Thronsen, M. Et Norsk Eventyr: Norsk Elbilforening i 25 år; Dinamo Forlag: Bærum, Norway, 2020. [Google Scholar]

- Gratis Oslo Parkering for Elbiler; News article; Aftenposten: Oslo, Norway, 1997.

- Norske Elbiler Til California; News article; Aftenposten: Oslo, Norway, 1995.

- Parliament. Minutes of Meeting. Decision in the Parliament to Change the Law to Enable the Toll Road Exemption. Stortinget Innst. S. nr. 74. (1996–1997). Innstilling Fra Samferdselskomiteen Om Forslag Fra Stortingsrepresentant Lars Sponheim Om Regelendringer Som Gjør Det Mulig for Lokale Styresmakter å Frita Elektriske Biler for Bompengeavgift. 1996. Available online: https://www.stortinget.no/no/Saker-og-publikasjoner/Publikasjoner/Innstillinger/Stortinget/1996-1997/inns-199697-074/?lvl=0 (accessed on 16 January 2024).

- Figenbaum, E. TH!NK, a Unique Citycar. In Electric & Hybrid Vehicle Technology; UK & International Press: Surrey, UK, 1998; 98p. [Google Scholar]

- Figenbaum, E. PIVCO Markedsintroduksjon-Sluttrapport; Report; Teknologisk Institutt: Oslo, Norway, 1998. [Google Scholar]

- Hoogma, R.; Kemp, R.; Schot, J.; Truffer, B. Experimenting for Sustainable Transport; The Approach of Strategic Niche Management; Chapter 4: Experiments in Electrifying Mobility, The PIVCO Experience: Ecological Product Differentiation; Routledge: Hoboken, NJ, USA, 2002; ISBN 978-0-415-27116-5. [Google Scholar]

- Samferdselsministeren Lokker Me Gratis Parkering: En Trøm Av El-Biler Til Oslo; News article; Aftenposten: Oslo, Norway, 1998.

- Gratis P-Plass for El-Biler; News article; Aftenpostn: Oslo, Norway, 1999.

- Gratis Parkering for El-Drevne Biler; News article; Aftenposten Aften: Oslo, Norway, 1998.

- Lovdata. Law Change Implementation. Forskrift om Offentlig Parkeringsregulering og Parkeringsgebyr (Parkeringsforskriften). FOR-1993-10-01-921. 1993, Revision 19 Jan. 1999, Forskrift 139. Available online: https://lovdata.no/dokument/SFO/forskrift/1993-10-01-921/KAPITTEL_2#KAPITTEL_2 (accessed on 16 January 2024).

- Lovdata. Law Change Implementation. Forskrift Om Endring Av Forskrift Fastsatt Av Finans-Og Tolldepartementet Til Utfylling Og Gjennomføring Mv. Av Skatteloven Av 26. Mars 1999 nr. 14. Kunngjort 03.02.2000. Ikrafttredelse Fra Og Med Inntektsåret. 2000. Available online: https://lovdata.no/dokument/LTI/forskrift/2000-01-10-19 (accessed on 16 January 2024).

- Nye Tiltak for økt Bruk Av Elbiler; Government press release 12.11.1999; Ministry of Trade and Industry: Oslo, Norway, 1999.

- Lovdata. Law Change Implementation. Forskrift Om Endring i Forskrift Til Utfylling Og Gjennomføring Mv. Av Skatteloven Av 26. Mars 1999 nr. 14. Kunngjort 23.12.2004. Ikrafttredelse: Inntektsåret 2004, Inntektsåret 2005. 2004. Available online: https://lovdata.no/dokument/LTI/forskrift/2004-12-17-1709 (accessed on 16 January 2024).

- Lovdata. Law Change Implementation. Forskrift Om Endring i Forskrift Til Utfylling Og Gjennomføring Mv. Av Skatteloven Av 26. Mars 1999 nr. 14. Kunngjort 16.12.2008. Ikrafttredelse 12.12.2008 Med Virkning Fra Og Med Inntektsåret 2009. 2008. Available online: https://lovdata.no/dokument/LTI/forskrift/2008-12-12-1329 (accessed on 16 January 2024).

- Lovdata. Law Change Implementation. Forskrift Om Endring i Forskrift Til Utfylling Og Gjennomføring Av Skatteloven Av 26. Mars 1999 nr. 14. 2017. Available online: https://lovdata.no/dokument/LTI/forskrift/2017-12-14-2101 (accessed on 16 January 2024).

- Parliament. Innst. 3 S (2021–2022). Innstilling Fra Finanskomiteen Om Skatter, Avgifter Og Toll 2022. Includes the Parliament Decision on Changes to Company Car Tax Incentive. 2022. Available online: https://www.stortinget.no/globalassets/pdf/innstillinger/stortinget/2021-2022/inns-202122-003s.pdf (accessed on 7 December 2023).

- Lovdata. Law Change Implementation. Forskrift Om Endring i Forskrift Til Utfylling Og Gjennomføring Mv. Av Skatteloven Av 26. Mars 1999 nr. 14. Kunngjort 11 April 2022. Ikrafttredelse 7 April 2022 Med Virkning Fra Inntektsåret 2004. 2022. Available online: https://lovdata.no/dokument/LTI/forskrift/2022-04-07-564 (accessed on 16 January 2024).

- NOU 1990:11. Generell Merverdiavgift På Omsetning Av Tjenester (nb.no). Available online: https://www.regjeringen.no/no/dokumenter/nou_1990-11/id115324/ (accessed on 16 January 2024).

- Board Meeting Minutes of the EV Association; Norstart—Norsk Elbilforening Møtereferat; EVA: Oslo, Norway, 2000.

- Parliament. Minutes of Meeting in Parliament. 2001 National Budget Agreement. Budsjettavtale for Statsbudsjettet for 2001 Mellom Arbeiderpartiet, Kristelig Folkeparti, Senterpartiet Og Venstre Inngått 18 November 2000. Publisert Av Finansdepartementet. 2000. Published by Ministry of Finance 30.05.2009. Available online: https://www.regjeringen.no/no/dokument/dep/fin/statsbudsjettet/budsjett-2001/budsjettavtale-for-statsbudsjettet-for-2/id411925/ (accessed on 16 January 2024).

- Parliament. Minutes of Meeting in Parliament. Zero VAT-Rate Decision in the Parliament. Innstilling Fra Finanskomiteen Om Lov Om Endringer i Lov 19 June 1969 nr. 66 om Merverdiavgift (Merverdiavgiftsloven) m.v. (Merverdiavgiftsreformen 2001). Innst. O. nr. 24—2000–2001. 2000. Available online: https://www.stortinget.no/globalassets/pdf/innstillinger/odelstinget/2000-2001/inno-200001-024.pdf (accessed on 16 January 2024).

- Ministry of Finance. National Budget Documents 2001. 2000. Available online: https://www.regjeringen.no/no/statsbudsjett/2001/id489537/ (accessed on 16 January 2024).

- Revised National Budget 2015. Ministry of Finance. 2015. Available online: https://www.regjeringen.no/no/statsbudsjett/2015/rnb/id2409228/ (accessed on 16 January 2024).

- ESA. Efta Surveillance Authority Decision of 21 April 2015 on the State Aid Measures in Favour of Electric Vehicles (Norway). EEA EFTA Surveillance Authority Decision. Case No: 76399, Document No: 746191, Decision No: 150/15/COL. 2015. Available online: https://www.eftasurv.int/state-aid/state-aid-register/state-aid-measures-favour-electric-vehicles (accessed on 16 January 2024).

- ESA. EFTA Surveilance Authority Decision. Tax Reductions on Zero Emission Vehicles. EEA EFTA Surveillance Authority, 19 December 2017. Case No: 81341, Document No: 877360, Decision No: 228/17/COL. 2017. Available online: https://www.eftasurv.int/state-aid/state-aid-register/tax-reductions-zero-emission-vehicles (accessed on 16 January 2024).

- ESA. EFTA Surveilance Authority Decision. Prolongation of the Zero VAT Rating for Zero-Emission Vehicles 2021–2022. EEA EFTA Surveillance Authority, 16 December 2020. Case No: 85854, Document No: 1158139, Decision No: 148/20/COL. 2020. Available online: https://www.eftasurv.int/cms/sites/default/files/documents/gopro/College%20Decision%20148%2020%20COL%20-%20State%20aid%20-%20Norway%20-%20Prolongation%20of%20zero%20VAT%20rating%20for%20zero-emission%20vehicles%202021-.pdf (accessed on 16 January 2024).

- RNB. Revised National Budget Document 2022. Ministry of Finance. 2022. Available online: https://www.regjeringen.no/no/statsbudsjett/2022/rnb/id2909908/ (accessed on 16 January 2024).

- Revised National Budget 2022 Agreement in Parliament. Parliament. 2022. Available online: https://www.stortinget.no/no/Saker-og-publikasjoner/Saker/Sak/?p=89362 (accessed on 16 January 2024).

- Low Emission Committee. Et Klimavennlig Norge. Official Norwegian Report (NOU). 2006. Available online: https://www.regjeringen.no/contentassets/56ae831eec35484881c6b237c2e817ac/no/pdfs/nou200620060018000dddpdfs.pdf (accessed on 16 January 2024).

- Minibussene Ut Av Kollektivfeltene; News article; Dagbladet: Oslo, Norway, 2001.

- NITO Og NIF Aksjonerer for Think; News article; Teknisk Ukeblad: Oslo, Norway, 2002.

- Transcript of Radio News Broadcast on Channel P4; News article; P4: Lillehammer, Norway, 2002.

- Elbil i Kollektivfeltene; News article; Teknisk Ukeblad: Oslo, Norway, 2003.

- Står i Kø for å Slippe Køkjøring: Tidoblet Salg Av Elbiler; News article; Aftenposten: Oslo, Norway, 2003.

- Bech, C. Why Think Nordic believes that BEVs are part of the future? Think Nordic 2004. In Proceedings of the 2004 European Ele-Drive Transportation Conference & Exhibition on Urban Sustainable Mobility, Estoril, Portugal, 17–20 March 2004. [Google Scholar]

- Minibusser Ut Av Kollektivfelt Fra Nyttår; News article; VG: Oslo, Norway, 2008.

- El-Biler i Kollektivfeltene i Oslo Og Akershus; Conference Speech, Tale/Innlegg; Ministry of Transport: Oslo, Norway, 2003.

- Ministry of Transport. Nullutslippsbiler: Kan Kjøre i Kollektivfelt Fra 1. Juni; Press release; Samferdselsdepartementet: Oslo, Norway, 2005. [Google Scholar]

- Vil Drøfte Kollektivfeltets Fremtid; News article; cFædrelandsvennen: Oslo, Norway, 2014.

- Vegvesenet Vil Kreve Medpassasjer; Budstikka: Oslo, Norway, 2015.

- Hver Tredje Elbil Er Borte; Budstikka: Oslo, Norway, 2015.

- Ministry of Finance. Bilavgifter. Rapport fra en arbeidsgruppe. Avgitt til Finansdepartementet 30. april 2003. Oslo, Norway. Available online: https://www.regjeringen.no/globalassets/upload/kilde/fin/rap/2003/0003/ddd/pdfv/177320-rapport_bil.pdf (accessed on 16 January 2024).

- Selvig, E.; Stølan, A.; Flugsrud, K. Helse- og Miljønytte av Innfasing av 0-Utslippskjøretøy i Norge; Civitas: Oslo, Norway, 2003. [Google Scholar]

- Elbileiernes Reisevaner; Rapport 2006-040; ECON Analyse: Oslo, Norway, 2006.

- Electrification Resource Group. Handlingsplan for Elektrifisering Av Veitransport. Rapport Fra Ressursgruppe Nedsatt Av Samferdselsdepartementet. 2009. Available online: https://www.regjeringen.no/no/dokumenter/handlingsplan-for-elektrifisering-av-vei/id560916/ (accessed on 16 January 2024).

- Nye Og Ambisiøse Mål Om Reduksjon Av Klimagassutslepp Få Nye Bilar; Press release; Ministry of Transport: Oslo, Norway, 2007.

- Ministry of the Environment. Climate Policy Bill. Norsk Klimapolitikk. St.Meld. nr. 34. 2007. Available online: https://www.regjeringen.no/no/dokumenter/Stmeld-nr-34-2006-2007-/id473411/ (accessed on 17 October 2023).

- Parliament. Climate Policy Settlement. Avtale Om Klimameldingen. 17 January 2008. Arbeiderpartiet, Sosialistisk Venstreparti, Senterpartiet, Høyre, Kristelig Folkeparti Og Venstre er Enige Om Nedenstående Merknader Til St.Meld. nr. 34 (2006–2007) Norsk Klimapolitikk. Utover Det Som Framgår Av Avtalen Slutter Partene Seg Til Klimameldinga. 2008. Available online: https://www.regjeringen.no/contentassets/fbe5a5829a5d468fab6e4eec0a39512d/avtale_klimameldingen_2008_01_17.pdf (accessed on 17 October 2023).

- European Union. Regulation (EC) No 443/2009 of The European Parliament and of the Council of 23 April 2009 Setting Emission Performance Standards for New Passenger Cars as Part of the Community’s Integrated Approach to Reduce CO2 Emissions from Light-Duty Vehicles. Available online: https://www.eumonitor.eu/9353000/1/j9vvik7m1c3gyxp/vitgbgiqypyz (accessed on 16 January 2024).

- Ministry of Government Administration and Reform 2008. Nye Reisesatser for Ansatte i Staten. Fornyings-Og Administrasjonsdepartementet. Pressemelding|Dato: 16 April 2008. Available online: https://www.regjeringen.no/no/dokumentarkiv/stoltenberg-ii/fad_2006-2009/nyheter-og-pressemeldinger/pressemeldinger/2008/nye-reisesatser-for-ansatte-i-staten/id508085/ (accessed on 16 January 2024).

- Ministry of Transport. Gratis Med Elbiler På Riksvegferjer; Press release, Pressemelding Nr: 95/08; Samferdselsdepartementet: Oslo, Norway, 2008. [Google Scholar]

- Gratisferje-Idé Kom Frå Pendlar; News article; Firda: Byrknesøy, Norway, 2008.

- Ministry of Finance. Nye Tiltak for å Bekjempe økt Arbeidsledighet. Ministry of Finance Press Release 11/2009, 26/02/09. 2009. Available online: https://www.regjeringen.no/globalassets/upload/fin/statsbudsjettet/tiltak09/pressehefte_fin.pdf (accessed on 16 January 2024).

- Om Endringer i Statsbudsjettet 2009 Med Tiltak for Arbeid. St. prp. Nr. 37 (2008–2009); Ministry of Finance: Oslo, Norway, 2009.

- Bilnorge. News Article. Zero Lader. 3 March 2009. Available online: https://www.bilnorge.no/artikkel.php?aid=34729 (accessed on 16 January 2024).

- TU. News Article. Statoil Selger Strøm. 17 November 2011. Available online: https://www.tu.no/artikler/statoil-selger-strom/239104 (accessed on 16 January 2024).

- Hagman, R.; Selvig, E. Environmentally Friendly Vehicles. In Experiences and Definitions; TemaNord 2007:531; Nordic Council of Ministers: Copenhagen, Denmark, 2007. [Google Scholar]

- Ministry of Finance. Bilavgifter. Rapport fra en Interdepartemental Arbeidsgruppe. In Hvordan kan en på best Mulig måte Prise de Samfunnsøkonomiske Kostnadene som Veitrafikken Forårsaker; Avgitt til Finansdepartementet 20; Ministry of Finance: Oslo, Norway, 2007. [Google Scholar]

- Green Highway Elbil- Och Laddhybridguide. April 2009. Green Highway Interreg. Project Report. Available online: https://temfunderingar.wordpress.com/2009/04/30/elbil-och-laddhybridguide-fran-april-2009/ (accessed on 16 January 2024).

- SPØRREUNDERSØKELSE OM BRUK AV OG HOLDNINGER TIL ELBILER I NORSKE STORBYER; NOTAT; Asplan Viak: Bærum, Norway, 2009.

- Mathisen, T.A.; Solvoll, G.; Smith, K.H. Bruk av elbiler. In Forventninger og Tilfredshet; SIB rapport nr. 6/2010; Handelshøyskolen i Bodø, Senter for Innovasjon og Bedriftsøkonomi: Bodø, Norway, 2010. [Google Scholar]

- Jørgensen, F.; Mathisen, T.A.; Solvoll, G. Elbil eller Konvensjonell bil? Økonomiske Analyser; SIB rapport nr. 2/2010; Handelshøyskolen i Bodø, Senter for Innovasjon og Bedriftsøkonomi: Bodø, Norway, 2010. [Google Scholar]

- Et nytt Transportparadigme i Emning; Econ Pöyry Report R-2010-095; Econ Pöyry /Ministry of Transport: Oslo, Norway, 2010.

- Klimakur2010. Klimakur2020. Tiltak Og Virkemidler for å Nå Norske Klimamål Mot 2020. Miljødirektoratet TA 2590/2010. Statens Vegvesen, Avinor, Jernbaneverket, Sjøfartsdirektoratet, Kystverket, Klima-Og Forurensningsdirektoratet. 17 March 2010. Available online: https://www.miljodirektoratet.no/ansvarsomrader/klima/klimatiltak/klimakur/klimakur-2020/ (accessed on 16 January 2024).

- Figenbaum, E.; Eskeland, G.S.; Leonardsen, J.A.; Hagman, R. 85 g CO2 per km i 2020—Er Det Mulig? TØI-rapport 1264/2013; Transportøkonomisk institutt: Oslo, Norway, 2013; Available online: https://www.toi.no/publications/85-g-co2-km-in-2020-is-that-achievable-article31927-29.html (accessed on 16 January 2024).

- Ministry of the Environment. Meld. St. 21 (2011–2012). Norsk Klimapolitikk. Det Kongelige Miljøverndepartement. 25 April 2012. Available online: https://www.regjeringen.no/no/dokumenter/meld-st-21-2011-2012/id679374/ (accessed on 16 January 2024).

- European Union. Regulation (EU) no 333/2014 of the European Parliament and of the Council of 11 March 2014 Amending Regulation (EC) No 443/2009 to Define The Modalities for Reaching the 2020 Target to Reduce CO2 Emissions from New Passenger Cars. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=uriserv%3AOJ.L_.2014.103.01.0015.01.ENG (accessed on 16 January 2024).

- Parliament. Climate Policy Settlement. Stortinget. Innst. 390 S (2011–2012). In Innstilling Til Stortinget Fra Energi-Og Miljøkomiteen Meld. St. 21 (2011–2012); Parliament: Oslo, Norway, 2012; Available online: https://www.stortinget.no/no/Saker-og-publikasjoner/Publikasjoner/Innstillinger/Stortinget/2011-2012/inns-201112-390/ (accessed on 16 January 2024).

- Ministry of Finance. News Note on Government Web Page: Feil Om El-Biler; Nyhet: Oslo, Norway, 2011. [Google Scholar]

- Political Platform for a Government Formed by the Conservative Party and the Progress Party. Sundvolden, 7 October 2013. Government Declaration for 2013–2016. 2013. Available online: https://www.regjeringen.no/contentassets/a93b067d9b604c5a82bd3b5590096f74/politisk_platform_eng.pdf (accessed on 16 January 2024).

- Parliament Petition to the Government. Innst. 2 S (2013–2014). In Innstilling Fra Finanskomiteen Om Nasjonalbudsjettet for 2014 Og Forslaget Til Statsbudsjett for 2014; Parliament: Oslo, Norway, 2013; Available online: https://www.stortinget.no/globalassets/pdf/innstillinger/stortinget/2013-2014/inns-201314-002.pdf (accessed on 16 January 2024).

- Parliament Petition to the Government. Innst. 4 L (2013–2014). Innstilling Fra Finanskomiteen Om Skatter, Avgifter Og Toll 2014—Lovsaker. 2013. Available online: https://www.stortinget.no/no/Saker-og-publikasjoner/Publikasjoner/Innstillinger/Stortinget/2013-2014/inns-201314-004/?lvl=0 (accessed on 16 January 2024).

- Thema. Report. Utvikling Og Nedtrapping Av Ladbare Bilers Virkemidler. ZERO November 2013. Available online: https://zero.no/wp-content/uploads/2016/05/utvikling-og-nedtrapping-av-ladbare-bilers-virkemidler.pdf (accessed on 16 January 2024).

- Assum, T.; Kolbenstvedt, M.; Figenbaum, E. The Future of Electromobility in Norway—Some Stakeholder Perceptives; TØI rapport 1385/2014; Institute of Transport Economics: Oslo, Norway, 2014; Available online: https://www.toi.no/publications/the-future-of-electromobility-in-norway-some-stakeholder-perspectives-article33109-29.html (accessed on 16 January 2024).

- Ministry of Finance. Notification (Letter) from the Royal Ministry of Finance to ESA Subject: Notification of VAT Zero Rate for Electric Vehicles. 4 November 2014. Available online: https://www.regjeringen.no/contentassets/0b202c86bcd4423ca6044b81f3590f81/notificationvat_el.pdf (accessed on 16 January 2024).

- The Norwegian Tax Administration. Revidert Nasjonalbudsjett 2015—Endringer i Merverdiavgiftsloven Merverdiavgiftsfritaket for Elbiler. Avgitt 23 June 2015. Available online: https://www.skatteetaten.no/rettskilder/type/skattedirektoratets-meldinger/revidert-nasjonalbudsjett-2015--endringer-i-merverdiavgiftsloven-merverdiavgiftsfritaket-for-elbiler/ (accessed on 16 January 2024).

- Green Tax Committee. NOU 2015: Sett Pris På Miljøet. 2015. Available online: https://www.regjeringen.no/no/dokumenter/nou-2015-15/id2465882/ (accessed on 16 January 2024).

- Nyere, Sikrere Og Mer Miljøvennlig Bilpark; Vehicle Tax Policy Settlement, Bilavgiftsforlik; Parliament: Oslo, Norway, 2015.

- Rasmussen, I. Virkninger av endringer i insentiver for kjøp og bruk av ladbare biler; Rapport 2011/30; Vista Analyse: Oslo, Norway, 2011. [Google Scholar]

- Figenbaum, E.; Kolbenstvedt, M. Electromobility in Norway-Experiences and Opportunities with Electric Vehicles; TØI rapport 1281/2013; Institute of Transport Economics: Oslo, Norway, 2013; Available online: https://www.toi.no/publications/electromobility-in-norway-experiences-and-opportunities-with-electric-vehicles-article32104-29.html (accessed on 16 January 2024).

- Laurikko, J.; Granström, R.; Haakana, A. Realistic estimates of EV range based on extensive laboratory and field tests in Nordic climate conditions. World Electr. Veh. J. 2013, 6, 192–203. [Google Scholar] [CrossRef]

- Klöckner, C.A.; Nayum, A.; Mehmetoglu, M. Positive and negative spillover effects from electric car purchase to car use. Transp. Res. Part 2013, 21, 32–38. [Google Scholar] [CrossRef]

- Ryghaug, M.; Toftaker, M. A Transformative Practice? Meaning, Competence, and Material Aspects of Driving Electric Cars in Norway. Nat. Cult. 2014, 9, 146–163. [Google Scholar] [CrossRef]

- Figenbaum, E.; Assum, T.; Kolbenstvedt, M. Electromobility in Norway-experiences and opportunities. Res. Transp. Econ. 2015, 50, 29–38. [Google Scholar] [CrossRef]

- Klimakur2030. 2020. Tiltak Og Virkemidler Mot 2030. M-1625/2020. Utarbeidet Av: Miljødirektoratet, Enova, Statens Vegvesen, Kystverket, Landbruksdirektoratet, NVE. Utgitt Av: Miljødirektoratet. 2020. Available online: https://www.miljodirektoratet.no/klimakur (accessed on 16 January 2024).

- Bruvoll, A.; Babri, S.; Bråthen, S.; Lilliestråle, A.; Støle, Ø.H. Toll Road Committee. 2020. På Veg Mot Et Bedre Bomsystem. Utfordringer Og Muligheter i Det Grønne Skiftet. Rapport Fra Utvalg. Overlevert Samferdselsministeren. 14 September 2020. Available online: https://www.regjeringen.no/contentassets/cbeb78d09109475aba2bfa9df488971a/1409_utvalgsrapport-framtidige-inntekter-i-bomringene.pdf (accessed on 16 January 2024).

- Subject: Notification of Tax Measures for Electric Vehicles; Letter to EFTA Surveillance Authority 2017; Ministry of Finance: Oslo, Norway, 2017.

- Transport Authorities. National Transport Plan Proposal. Nasjonal Transportplan 2018–2029. Grunnlagsdokument. 2016. Available online: https://www.regjeringen.no/no/dokumenter/grunnlagsdokument-nasjonal-transportplan-2018-2029/id2477391/ (accessed on 16 January 2024).

- Government. UNFCCC Paris Agreement. Norway’s First NDC 2016. Available online: https://unfccc.int/NDCREG?gclid=CjwKCAjw1t2pBhAFEiwA_-A-NJSS5k7rJrSzRZnwq8kC8LeoYWwi1_rknEn9w0eBs2Du2f0iT4vwZxoCS3sQAvD_BwE (accessed on 16 January 2024).

- Norwegian Environment Agency. Report. Kunnskapsgrunnlag for Lavutslippsutvikling. Miljødirektoratet Rapport M229–2014. 2014. Available online: https://www.miljodirektoratet.no/globalassets/publikasjoner/M229/M229.pdf (accessed on 16 January 2024).

- Ministry of Transport. Meld. St. 33 (2016–2017), Nasjonal Transportplan 2018–2029; Samferdselsdepartementet: Oslo, Norway, 2017; Available online: https://www.vegvesen.no/fag/fokusomrader/nasjonal-transportplan/tidligere-nasjonale-transportplaner/nasjonal-transportplan-2018-2029/ (accessed on 16 January 2024).

- Parliament. Innst. 460 S (2016–2017). 2017. Available online: https://www.stortinget.no/no/Saker-og-publikasjoner/Publikasjoner/Innstillinger/Stortinget/2016-2017/inns-201617-460s/?all=true (accessed on 16 January 2024).

- Innspill Til Helhetlig Gjennomgang Av Kjøretøy-Og Drivstoffavgiftene; Sendt til Samferdselsdepartementet 4 August 2014; EVA: Oslo, Norway, 2014.

- Lovdata. Law Change Implementation. Lov Om Eierseksjoner (Eierseksjonsloven). Dato LOV-2017-06-16-65. Ministry of Local Government and Regional Development. 2017. Available online: https://lovdata.no/dokument/NL/lov/2017-06-16-65#KAPITTEL_5 (accessed on 16 January 2024).

- Lovdata. Law Change Implementation. Lov Om Endringar i Burettslagslova mv. (Rett Til å Setje Opp Ladepunkt for Elbil, Samanslåing av Eigarseksjonssameige) Kunngjort 4 December 2020. Ikrafttredelse: Kongen Fastset. Available online: https://lovdata.no/dokument/LTI/lov/2020-12-04-137 (accessed on 16 January 2024).

- Ministry of Transport. Prop. 87 S (2017–2018) Nokre Saker Om Luftfart, Veg, Særskilde Transporttiltak, Kyst Og Post Og Telekommunikasjonar. Tilråding Frå Samferdselsdepartementet 15. Mai 2018, Godkjend i Statsråd Same Dagen. (Regjeringa Solberg). 2018. Available online: https://www.regjeringen.no/contentassets/c6a173c941ca442eb3ffcd4340c9762a/nn-no/pdfs/prp201720180087000dddpdfs.pdf (accessed on 16 January 2024).

- NPRA. Statens Vegvesen. Riksregulativ for Ferjetakster Gjeldende Fra 1 March 2018. Statens Vegvesen. 2018. Available online: https://www.fosennamsos.no/getfile.php/138587-1519810692/FosenNamsos%20Sj%C3%B8/Bilder/Artikkelbilder/Takster/Takstbestemmelser%20010318%20ferje.pdf (accessed on 13 April 2021).

- Elbil.no. News Note. Her Får Du Gratis Elbil-Parkering—Og Her Må Du Betale. Elbil.no Artikkel. 6 January 2022. Available online: https://elbil.no/norge-rundt-fa-oversikt-over-gratis-parkering/ (accessed on 16 January 2024).

- Lovdata. Forskrift Om Vilkårsparkering for Allmennheten Og Håndheving Av Private Parkeringsreguleringer (Parkeringsforskriften). FOR-2016-03-18-260. 2016. Available online: https://lovdata.no/dokument/SF/forskrift/2016-03-18-260 (accessed on 16 January 2024).

- News Notice in Aftenposten 30 November 2008 Stating that the City Council Would Finance 400 Chargers in Oslo up to 2011; Aftenposten: Oslo, Norway, 2008.

- Transnova. Forslag Til: Nasjonal Strategi Og Finansieringsplan for Infrastruktur for Elbiler. Transnova. 2014. Available online: https://www.regjeringen.no/globalassets/upload/sd/vedlegg/transnovas_ladestrategi.pdf (accessed on 16 January 2024).

- Strategi for Ladestasjoner Og Infrastruktur for Elbil 2015–2016; Enova SF: Trondheim, Norway, 2015.

- Civitas Stavn. Helhetlig Utbyggingsplan for Infrastruktur Til Ladbare Biler i Fylkene Akershus, Hedmark, Oppland and Østfold. Civitas Stavn Report; Oslo, Norway. 15 May 2012. Available online: https://www.yumpu.com/no/document/view/19971846/last-ned-og-les-rapporten-her-pdf-civitas (accessed on 16 January 2024).

- Strategi for Ladeinfrastruktur 2014 2020 Oppfølging Av Moss Kommunes Energi Og Klimaplan; Moss Kommune: Moss, Norway, 2014.

- Ladepunktstrategi for Skedsmo kommune 2015–2020; Skedsmo, Norway. 2014. Available online: https://klimaostfold.no/wp-content/uploads/2017/01/Skedsmo-kommune-Ladepunktstrategi.pdf (accessed on 16 January 2024).

- Ministry of Transport. Handlingsplan for Infrastruktur for Alternative Drivstoff i Transport. 2019. Available online: https://www.regjeringen.no/no/dokumenter/handlingsplan-for-infrastruktur-for-alternative-drivstoff-i-transport/id2662448/ (accessed on 16 January 2024).

- European Union. Directive 2014/94/EU of the European Parliament and of the Council of 22 October 2014 on the Deployment of Alternative Fuels Infrastructure). Available online: https://eur-lex.europa.eu/legal-content/en/TXT/?uri=CELEX%3A32014L0094 (accessed on 16 January 2024).

- Jeløya. Government Declaration. Politisk Plattform for En Regjering Utgått Fra Høyre, Fremskrittspartiet Og Venstre. Jeløya. 14 January 2018. Available online: https://www.venstre.no/assets/v-h-frp-politisk-plattform-2018.pdf (accessed on 19 October 2023).

- Notification of Zero Rate VAT for Electric Vehicles; Ministry of Finance: Oslo, Norway, 2020.

- Ministry of Climate and Environment. Meld. St. 13 (2020–2021) Melding Til Stortinget. Klimaplan for 2021–2030. 2021. Available online: https://www.regjeringen.no/no/dokumenter/meld.-st.-13-20202021/id2827405/ (accessed on 16 January 2024).

- Parliament. Minutes of Parliament Debate over Bill to the Parliament on the Right to Charge for Flat Owners. Endringar i Burettslagslova mv. (Rett Til å Setje Opp Ladepunkt for Elbil, Samanslåing Av Eigarseksjonssameige) Prop. 144 L (2019–2020), Innst. 78 L (2020–2021), Lovvedtak 21 (2020–2021). 2020. Available online: https://www.stortinget.no/no/Saker-og-publikasjoner/Saker/Sak/?p=81159 (accessed on 16 January 2024).

- Government. UNFCCC Paris Agreement. Norway’s Second Update to the NDC. 2022. Available online: https://unfccc.int/sites/default/files/NDC/2022-11/NDC%20Norway_second%20update.pdf (accessed on 16 January 2024).

- Parliament. Resolution (Vedtak) 792, during the Discussion of Meld. St. 13 (2020–2021) Klimaplan for 2021–2030. 2021. Available online: https://www.stortinget.no/no/Saker-og-publikasjoner/Vedtak/Vedtak/Sak/?p=82805 (accessed on 16 January 2024).

- Figenbaum, E. Electromobility Status in Norway: Mastering Long Distances—The Last Hurdle to Mass Adoption; TØI 1627/2018; Transportøkonomisk institutt: Oslo, Norway, 2018; Available online: https://www.toi.no/publications/electromobility-status-in-norway-mastering-long-distances-the-last-hurdle-to-mass-adoption-article34903-29.html (accessed on 16 January 2024).

- Videokonferansehøring: Meld. St. 13 (2020-2021) Klimaplan for 2021–2030; Parliament: Oslo, Norway, 2021.

- Resolution (Vedtak) 1232 during the Discussion of Meld. St. 20 (2020-2021) Nasjonal Transportplan 2022–2033; Parliament: Oslo, Norway, 2021.

- SVV. Kunnskapsgrunnlag Om Hurtigladeinfrastruktur for Veitransport. Statens Vegvesen Og Miljødirektoratet 2022. Rapport M-2232 Miljødirektoratet. 1 March 2022. Available online: https://www.miljodirektoratet.no/publikasjoner/2022/mars/kunnskapsgrunnlag-om-hurtigladeinfrastruktur-for-veitransport/ (accessed on 16 January 2024).

- SVV. Invitasjon Til å Bidra Med Innspill Til Regjeringens Ladestrategi. Meeting the 21 March 2022. Available online: https://www.regjeringen.no/no/aktuelt/invitasjon-til-a-bidra-med-innspill-til-regjeringens-ladestrategi/id2902693/ (accessed on 16 January 2024).

- Parliament. Agreement in the Parliament on the Implementation of VAT on BEVs Purchase Price Exceeding 500,000 NOK; Revidert nasjonalbudsjett 2022: Enighet mellom Ap, Sp og SV; Arbeiderpartiet: Oslo, Norway, 2022; Available online: https://www.arbeiderpartiet.no/aktuelt/revidert-nasjonalbudsjett-2022-enighet-mellom-ap-sp-og-sv/ (accessed on 16 January 2024).

- Lovdata. Lov Om Endinger i Merverdiavgiftsloven. Kunngjort 20 December 2022. Ikrafttredelse 1 January 2023. 2022. Available online: https://lovdata.no/dokument/LTI/lov/2022-12-20-108 (accessed on 16 January 2024).

- Parliament. Agreement on the National Budget for 2023; Parliament: Oslo, Norway, 2022; Available online: https://www.stortinget.no/no/Saker-og-publikasjoner/Statsbudsjettet/statsbudsjettet-2023/ (accessed on 16 January 2024).

- Takstretningslinjer for Bompengeprosjekt På Offentlig Veg. Retningslinjer. Fastsatt i Vegdirektoratet Juli 2023. Available online: https://www.autopass.no/siteassets/takstretningslinjer/lars/takstretningslinjer-for-bompengeprosjekt-pa-offentlig-veg---juli-2023.pdf (accessed on 16 January 2024).

- Kunnskapsgrunnlag om Hurtigladeinfrastruktur for Veitransport; Miljødirektoratet og Statens Vegvesen: Oslo, Norway, 2022; Available online: https://www.regjeringen.no/no/aktuelt/kunnskapsgrunnlaget-om-utbygging-av-ladeinfrastruktur-er-klart/id2902606/ (accessed on 16 January 2024).

- Fridstrøm, L.; Alfsen, K. Norway’s Path to Sustainable Transportation. TØI report 1321/2014. 2014. Available online: https://www.toi.no/publications/norway-s-path-to-sustainable-transport-article32521-29.html (accessed on 16 January 2024).

- Jong, W.; van der Linde, V. Clean Diesel and Dirty Scandal: The Echo of Volkswagen’s Dieselgate in an Intra-Industry Setting. Public Relat. Rev. 2022, 48, 102146. [Google Scholar] [CrossRef]

- Samset, K.; Bukkestein, I. Hvordan Stoppe Dårlig Begrunnete Prosjekter På Et Tidlig Tidspunkt. Concept-Programmet Norges Teknisk-Naturvitenskapelige Universitet 7491 NTNU—Trondheim. 2020. Available online: https://www.ntnu.no/documents/1261860271/1261996393/Hvordan+stoppe+d%C3%A5rlig+begrunnete+prosjekter+WEB+%281%29.pdf/6d566e4d-8310-e104-2dec-b748b82c6fc8?t=1606199737906 (accessed on 20 December 2023).

- Ministry of Finance. National Budget Documents 2024. 2023. Available online: https://www.regjeringen.no/no/statsbudsjett/2024/id2994174/ (accessed on 16 January 2024).

- Agreement on National Budget for 2024. Budsjettforlik Mellom Ap/Sp Og SV 2024. Versjon, 3 December 2023., kl. 08:30. Avtaletekst. Available online: https://www.sv.no/wp-content/uploads/2023/12/031223-budsjettforlik-verbaler-beriktiget-041223.pdf (accessed on 19 December 2023).

- Figenbaum, E. Chapter on Norway in the IEA HEV TCP Annual Report 2023. The Electric Drive Ramps Up. Available online: https://ieahev.org/wp-content/uploads/2023/06/Digital_HEVTCP_Annual_Report_2023_v0.3-3-1.pdf (accessed on 19 December 2023).

| Electromobility Norway | Theory/International | Total | |

|---|---|---|---|

| Peer-reviewed research articles | 22 | 18 | 40 |

| Editor-reviewed research articles | 2 | 1 | 3 |

| Monographs (scientific book, PhD thesis) | 3 | 2 | 5 |

| Book chapter in scientific book | 3 | 3 | 6 |

| Scientific research paper | 3 | 3 | 6 |

| Reports—research/scientific | 28 | 3 | 31 |

| Reports—authorities using scientific approach | 2 | 0 | 2 |

| Reports—consultants | 10 | 0 | 10 |

| Reports—organisations | 2 | 1 | 3 |

| Popular science book | 2 | 0 | 2 |

| Press articles | 66 | 9 | 75 |

| Other news articles, websites | 14 | 3 | 17 |

| Private actor documents | 17 | 6 | 23 |

| Public actor documents | 10 | 1 | 11 |

| Political documents | 18 | 0 | 18 |

| Law texts | 1 | 2 | 3 |

| Other references | 4 | 2 | 6 |

| Total | 207 | 54 | 261 |

| Incentive | Introduction | 1st Major Revision | 2nd Major Revision | 3rd Major Revision | 4th Major Revision | 5th Major Revision | Status 2023 |

|---|---|---|---|---|---|---|---|

| Registration tax exemption | 1990, temporary | 1996, permanent | 2023, weight tax element introduced | Weight tax as for ICEVs, other parts exempted | |||

| Annual tax exemption | 1996 | 2004, partial reduction | 2018, BEVs fully exempted, changed to tax on insurance | 2021, partial reduction | 2022, full tax as for ICEVs | Full tax as for ICEVs | |

| Road toll exemption | 1997 | 2018, max 50% of ICEVs, local decision | 2023, max 70% of ICEVs, local decision | Max 70% of ICEVs, local decision | |||

| Parking fee exemption | 1999 | 2017, local authorities can decide | 2018, BEVs 50% of ICEVs | 50% rate still not implemented | |||

| Reduced company car benefit tax | 2000 | 2005, new tax system, BEVs 75% of ICEVs | 2009, 50% of ICEVs | 2018, 60% of ICEV | 2022, 80% of ICEV | 2023, full tax as for ICEVs | Full tax as for ICEVs |

| Zero-rate VAT purchases | 2001 | 2023, full VAT on price above NOK 500,000 | Full VAT on price above NOK 500,000 | ||||

| Reduced ferry rates | 2009, national car ferries | 2018, max 50% of ICEVs, ferry operator to decide, includes county ferries | Max 50% of ICEVs, ferry operator to decide, includes county ferries | ||||

| Zero-rate VAT leasing | 2015 | 2023, full VAT on price above NOK 500,000 | Full VAT on price above NOK 500,000 | ||||

| Re-registration tax exemption | 2018 | 2022, 25% of ICEV rate | 2023, full tax as for ICEVs | Full tax as for ICEVs | |||

| Access to bus lanes | 2003, Oslo area test | 2005, access to all bus lanes in Norway | 2015, passenger in the car in rush hour, local authority decides | 2015, passenger in the car rush hour, local authority decides |

| No. | BEV Policy | Type | Year Decided | Year Initiated | Effect | Market Impact | Impact Assessm. | Process | New BEVs Sold | Market Share | BEV Fleet (Incl. Used) | Average Range km | Public Chargers | Fast Chargers | Press Articles | Reports Articles | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1990–1997 | 1 | Registration tax exemption, temporary | Tax | 1989 | 1990 | Market pull | High | No | National budget doc. | 5 | 0.0% | 5 | 30 | 0 | 0 | - | 1 |

| 2 | Km tax exemption | Tax | 1989 | 1990 | Market pull | Low | No | National budget doc. | 5 | 0.0% | 5 | 30 | 0 | 0 | - | 1 | |

| 3 | Registration tax exemption, permanent | Tax | 1995 | 1996 | Market pull | High | No | Gov. prop. to parliament | 10 | 0.0% | 50 | 60 | 11 | 0 | 27 | 1 | |

| 4 | Annual tax exemption | Tax | 1995 | 1996 | Market pull | Medium | No | National budget debate | 10 | 0.0% | 50 | 60 | 11 | 0 | 27 | 1 | |

| 5 | Toll road exemption | Fee/Law | 1997 | 1997 | Market pull | High | No | Parliament law change | 42 | 0.0% | 147 | 60 | 30 | 0 | 49 | 0 | |

| 1998–2002 | 6 | Parking fee exemption | Fee/Law | 1999 | 1999 | Market pull | Medium | Yes | Law change w. hearing | 101 | 0.0% | 285 | 60 | No data | 0 | 89 | 0 |

| 7 | Reduced company car benefit tax | Tax | 1999 | 2000 | Market pull | Low | No | National budget doc. | 101 | 0.1% | 285 | 60 | No data | 0 | 89 | 0 | |

| 8 | Zero-rate VAT BEV purchase | Tax/Law | 2000 | 2001 | Market pull | High | No | National budget process | 207 | 0.2% | 468 | 60 | No data | 0 | 71 | 0 | |

| 2003 –2006 | 9 | Bus lanes Oslo area (test 2003–2005) | Adm. | 2003 | 2003 | Market pull | High | No | Real-life test | 15 | 0.0% | 1081 | 60 | No data | 0 | 208 | 0 |

| 10 | Bus lanes Norway (Oslo test ok) | Adm. | 2005 | 2005 | Market pull | High | No | Experience from test | 26 | 0.0% | 1320 | 50 | No data | 0 | 285 | 1 | |

| 2007–2010 | 11 | New car average CO2 emis. <120 g/km | Target | 2007 | 2012 | Supporting target | Low | No | Government process | 240 | 0.0% | 1903 | 50 | No data | 0 | 1276 | 2 |

| 12 | Increased car allowance for business trips | Adm. | 2008 | 2008 | Cost compensation | Low | No | Government process | 443 | 0.1% | 2424 | 77 | No data | 0 | 2002 | 1 | |

| 13 | Ferry ticket price reduction | Adm. | 2008 | 2009 | Market pull | Medium | No | Government process | 443 | 0.1% | 2424 | 77 | No data | 0 | 2002 | 1 | |

| 14 | TRANSNOVA funding agency start | Adm. | 2009 | 2010 | Barrier reduction | Medium | Yes | National budget doc. | 295 | 0.1% | 2753 | 56 | No data | 0 | 4482 | 5 | |

| 15 | Transnova support for normal chargers | Adm. | 2009 | 2010 | Barrier reduction | Low | No | Parliament propositon | 295 | 0.1% | 2753 | 56 | No data | 0 | 4482 | 5 | |

| 16 | Transnova support for fast chargers | Adm. | 2010 | 2011 | Barrier reduction | Low | No | Transnova decision | 599 | 0.2% | 3360 | 86 | 1163 | 0 | 4041 | 5 | |

| 2011–2015 | 17 | New car average CO2 emis. <85 g/km | Target | 2012 | 2020 | Supporting target | Medium | No | Government process | 3950 | 2.9% | 9581 | 131 | 3433 | 58 | 4215 | 11 |

| 18 | Keep incentives to 2015/50,000 BEVs | Decision | 2012 | 2015 | Market stability | High | No | Parliament agreement | 3950 | 2.9% | 9581 | 131 | 3433 | 58 | 4215 | 11 | |

| 19 | Keep incentives in place through 2017 | Decision | 2013 | 2017 | Market stability | High | No | Government declaration | 7888 | 5.6% | 18,916 | 185 | 4538 | 131 | 6680 | 19 | |

| 20 | TRANSNOVA merged into ENOVA | Adm. | 2014 | 2015 | More resources | High | Partial | Government process | 16,830 | 13% | 38,652 | 185 | 5744 | 270 | 10,389 | 13 | |

| 21 | ENOVA strategy for fast chargers | Adm. | 2015 | 2016 | Barrier reduction | High | No | ENOVA internal process | 25,785 | 17% | 69,134 | 176 | 6550 | 449 | 10,539 | 14 | |

| 22 | ENOVA support for fast chargers 2015–2022 | Adm. | 2015 | 2016 | Barrier reduction | High | No | Delegated authority | 25,785 | 17% | 69,134 | 176 | 6550 | 449 | 10,539 | 14 | |

| 23 | Zero-rate VAT BEV leasing/batteries | Tax/Law | 2015 | 2015 | Market pull | Low | Yes | Parliament petition | 25,785 | 17% | 69,134 | 176 | 6550 | 449 | 10,539 | 14 | |

| 2016–2020 | 24 | Only sell ZEVs from 2025—proposal | Target | 2016 | 2025 | Proposed target | High | No | National Transport Plan | 24,222 | 16% | 97,532 | 209 | 7830 | 757 | 9196 | 24 |

| 25 | Only sell ZEVs from 2025—decision | Target | 2017 | 2025 | Supporting target | High | No | National Transport Plan | 33,025 | 21% | 138,983 | 301 | 6858 | 1211 | 11,876 | 17 | |

| 26 | Keep incentives in place through 2020 | Decision | 2017 | 2020 | Market stability | High | No | Parliament petition | 33,025 | 21% | 138,983 | 301 | 6858 | 1211 | 11,876 | 17 | |

| 27 | Re-registration tax exemption | Tax | 2017 | 2018 | Market pull | Low | Yes | Parliament petition | 33,025 | 21% | 138,983 | 301 | 6858 | 1211 | 11,876 | 17 | |

| 28 | 50% of ICEV rate parking/road toll/ferry | Fee/Law | 2017 | 2018 | Incentive reduct. | Medium | No | National budget agreement | 33,025 | 21% | 138,983 | 301 | 6858 | 1211 | 11,876 | 17 | |

| 29 | Right to charge, flats/joint properties | Law | 2017 | 2018 | Barrier reduction | Low | Yes | Parliament petition/law revision | 33,025 | 21% | 138,983 | 301 | 6858 | 1211 | 11,876 | 17 | |

| 30 | Action plan for alternative fuels infrastr. | Strategy | 2019 | n/a | Barrier reduction | Low | No | Government strategy | 60,316 | 42% | 260,692 | 397 | 12,132 | 2399 | 18,316 | 44 | |