Parametric Estimation in the Vasicek-Type Model Driven by Sub-Fractional Brownian Motion

{kind=link}

Abstract

1. Introduction

2. Preliminaries

3. The Consistency of the Least Squares Estimator

- (1)

- , as T tends to infinity, almost surely.

- (2)

- , as T tends to infinity, almost surely.

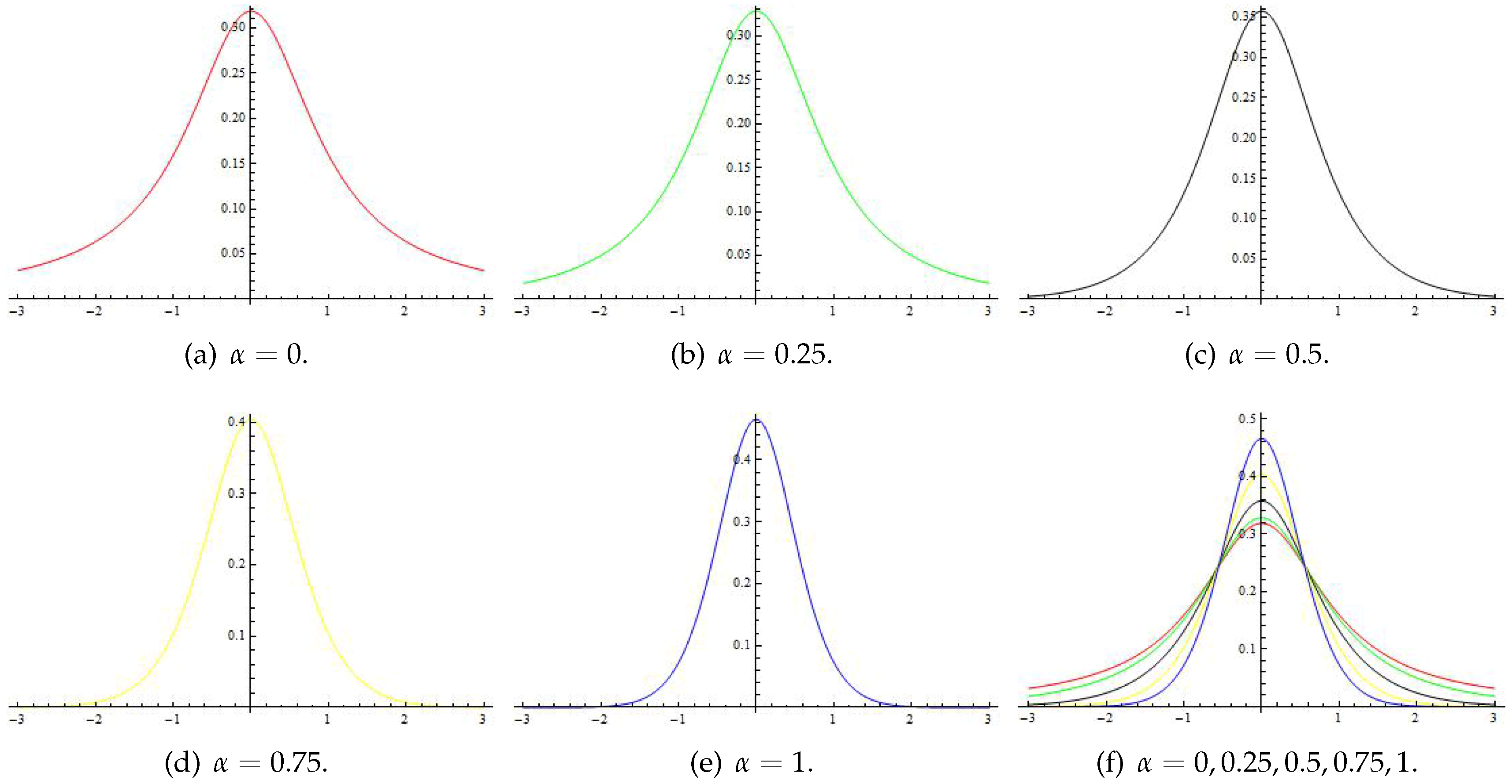

4. Asymptotic Distribution of the Least Squares Estimator

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Bishwal, J.P. Parameter Estimation in Stochastic Differential Equations; Springer: Berlin/Heidelberg, Germany, 2008. [Google Scholar]

- Iacus, S.M. Simulation and Inference for Stochastic Differential Equations; Springer: Berlin/Heidelberg, Germany, 2008. [Google Scholar]

- Kutoyants, Y.A. Statistical Inference for Ergodic Diffusion Processes; Springer: Berlin/Heidelberg, Germany, 2004. [Google Scholar]

- Liptser, R.S.; Shiryaev, A.N. Statistics of Random Processes II: Applications. In Applications of Mathematics; Springer: Berlin/Heidelberg, Germany, 2001. [Google Scholar]

- Prakasa Rao, B.L.S. Statistical Inference for Diffusion type Processes; Oxford University Press: New York, NY, USA, 1999. [Google Scholar]

- Berzin, C.; Latour, A.; Leon, J.R. Inference on the Hurst Parameter and the Variance of Diffusions Driven by Fractional Brownian Motion; Springer: Berlin/Heidelberg, Germany, 2014. [Google Scholar]

- Es-Sebaiy, K. Berry-Esséen bounds for the least squares estimator for discretely observed fractional Ornstein-Uhlenbeck processes. In Malliavin Calculus and Stochastic Analysis; Springer: Berlin/Heidelberg, Germany, 2013; pp. 2372–2385. [Google Scholar]

- Es-Sebaiy, K.; Nourdin, I. Parameter estimation for α fractional bridges. Springer Proc. Math. Stat. 2013, 34, 385–412. [Google Scholar]

- Hu, Y.Z.; Nualart, D.; Zhou, H.J. Parameter estimation for fractional Ornstein–Uhlenbeck processes of general Hurst parameter. arXiv, 2017; arXiv:1703.09372. [Google Scholar]

- Hu, Y.Z.; Nualart, D. Parameter estimation for fractional Ornstein-Uhlenbeck processes. Stat. Prob. Lett. 2010, 80, 1030–1038. [Google Scholar] [CrossRef]

- Kleptsyna, M.L.; Le Breton, A. Statistical analysis of the fractional Ornstein-Uhlenbeck type processes. Stat. Inference Stoch. Process. 2002, 5, 229–248. [Google Scholar] [CrossRef]

- Prakasa Rao, B.L.S. Statistical Inference for Fractional Diffusion Processes; John Wiley & Sons: Hoboken, NJ, USA, 2010. [Google Scholar]

- Mendy, I. Parametric estimation for sub-fractional Ornstein-Uhlenbeck process. J. Stat. Plan. Infer. 2013, 143, 663–674. [Google Scholar] [CrossRef]

- Machkouri, E.; Es-Sebaiy, K.; Ouknine, Y. Least squares estimator for non-ergodic Ornstein-Uhlenbeck processes driven by Gaussian processes. J. Korean Stat. Soc. 2016, 45, 329–341. [Google Scholar] [CrossRef]

- Fouque, J.P.; Papanicolaou, G.; Sircar, R.; Sølna, K. Multiscale Stochastic Volatility for Equity, Interest Rate, and Credit Derivatives; Cambridge University Press: Cambridge, UK, 2011. [Google Scholar]

- Bojdecki, T.; Gorostiza, L.G.; Talarczyk, A. Sub-fractional Brownian motion and its relation to occupation times. Stat. Probab. Lett. 2004, 69, 405–419. [Google Scholar] [CrossRef]

- Bojdecki, T.; Gorostiza, L.G.; Talarczyk, A. Limit theorems for occupation time fluctuations of branching systems (I): Long-range dependence. Stochastic. Process. Appl. 2006, 116, 1–18. [Google Scholar] [CrossRef]

- Bojdecki, T.; Gorostiza, L.G.; Talarczyk, A. Some extension of fractional Brownian motion and sub-fractional Brownian motion related to particle systems. Elect. Comm. Probab. 2007, 12, 161–172. [Google Scholar] [CrossRef]

- Li, Y.; Xiao, Y. Occupation time fluctuations of weakly degenerate branching systems. J. Theo. Probab. 2012, 25, 1119–1152. [Google Scholar] [CrossRef]

- Shen, G.; Yan, L. Estimators for the drift of sub-fractional Brownian motion. Comm. Stat. Theory Methods 2014, 43, 1601–1612. [Google Scholar] [CrossRef]

- Sun, X.; Yan, L. Weak convergence to a class of multiple stochastic integrals. Comm. Stat. Theory Methods 2017, 46, 8355–8368. [Google Scholar] [CrossRef]

- Sun, X.; Yan, L. A central limit theorem associated with sub-fractional Brownian motion and an application. Sci. Sin. Math. 2017, 47, 1055–1076. (In Chinese) [Google Scholar] [CrossRef]

- Tudor, C. Some properties of the sub-fractional Brownian motion. Stochastics 2007, 79, 431–448. [Google Scholar] [CrossRef]

- Tudor, C. Inner product spaces of integrands associated to sub-fractional Brownian motion. Stat. Probab. Lett. 2008, 78, 2201–2209. [Google Scholar] [CrossRef]

- Tudor, C. Some aspects of stochastic calculus for the sub-fractional Brownian motion. Ann. Univ. Bucuresti Math. 2007, 199–230. Available online: http://fmi.unibuc.ro/ro/anale/matematica/mate_anul_LVII_2008_nr_2_art_7.pdf (accessed on 1 November 2018).

- Tudor, C. On the Wiener integral with respect to a sub-fractional Brownian motion on an interval. J. Math. Anal. Appl. 2009, 351, 456–468. [Google Scholar] [CrossRef]

- Yan, L.; He, K.; Chen, C. The generalized Bouleau-Yor identity for a sub-fBm. Sci. China Math. 2013, 56, 2089–2116. [Google Scholar] [CrossRef]

- Yan, L.; Shen, G. On the collision local time of sub-fractional Brownian Motions. Stat. Probab. Lett. 2010, 80, 296–308. [Google Scholar] [CrossRef]

- Alós, E.; Mazet, O.; Nualart, D. Stochastic calculus with respect to Gaussian processes. Ann. Probab. 2001, 29, 766–801. [Google Scholar]

- Nualart, D. Malliavin Calculus and Related Topics; Springer: Berlin/Heidelberg, Germany, 2006. [Google Scholar]

- Samko, S.G.; Kilbas, A.A.; Marichev, O.I. Fractional Integrals and Fractional Derivatives; Gordan and Breach Science: Yverdon, Switzerland, 1993. [Google Scholar]

- Bertoin, J. Sur une intégrale pour les processus á α-variation borné. Ann. Probab. 1989, 17, 1521–1535. (In French) [Google Scholar] [CrossRef]

- FöIllmer, H. Calcul d’Itô sans probabilités. In Séinaire de Probabilités XV; Springer: Berlin/Heidelberg, Germany, 1981. (In French) [Google Scholar]

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Li, S.; Dong, Y. Parametric Estimation in the Vasicek-Type Model Driven by Sub-Fractional Brownian Motion. Algorithms 2018, 11, 197. https://doi.org/10.3390/a11120197

Li S, Dong Y. Parametric Estimation in the Vasicek-Type Model Driven by Sub-Fractional Brownian Motion. Algorithms. 2018; 11(12):197. https://doi.org/10.3390/a11120197

Chicago/Turabian StyleLi, Shengfeng, and Yi Dong. 2018. "Parametric Estimation in the Vasicek-Type Model Driven by Sub-Fractional Brownian Motion" Algorithms 11, no. 12: 197. https://doi.org/10.3390/a11120197

APA StyleLi, S., & Dong, Y. (2018). Parametric Estimation in the Vasicek-Type Model Driven by Sub-Fractional Brownian Motion. Algorithms, 11(12), 197. https://doi.org/10.3390/a11120197