The Global Surge in Energy Innovation

Abstract

:1. Introduction

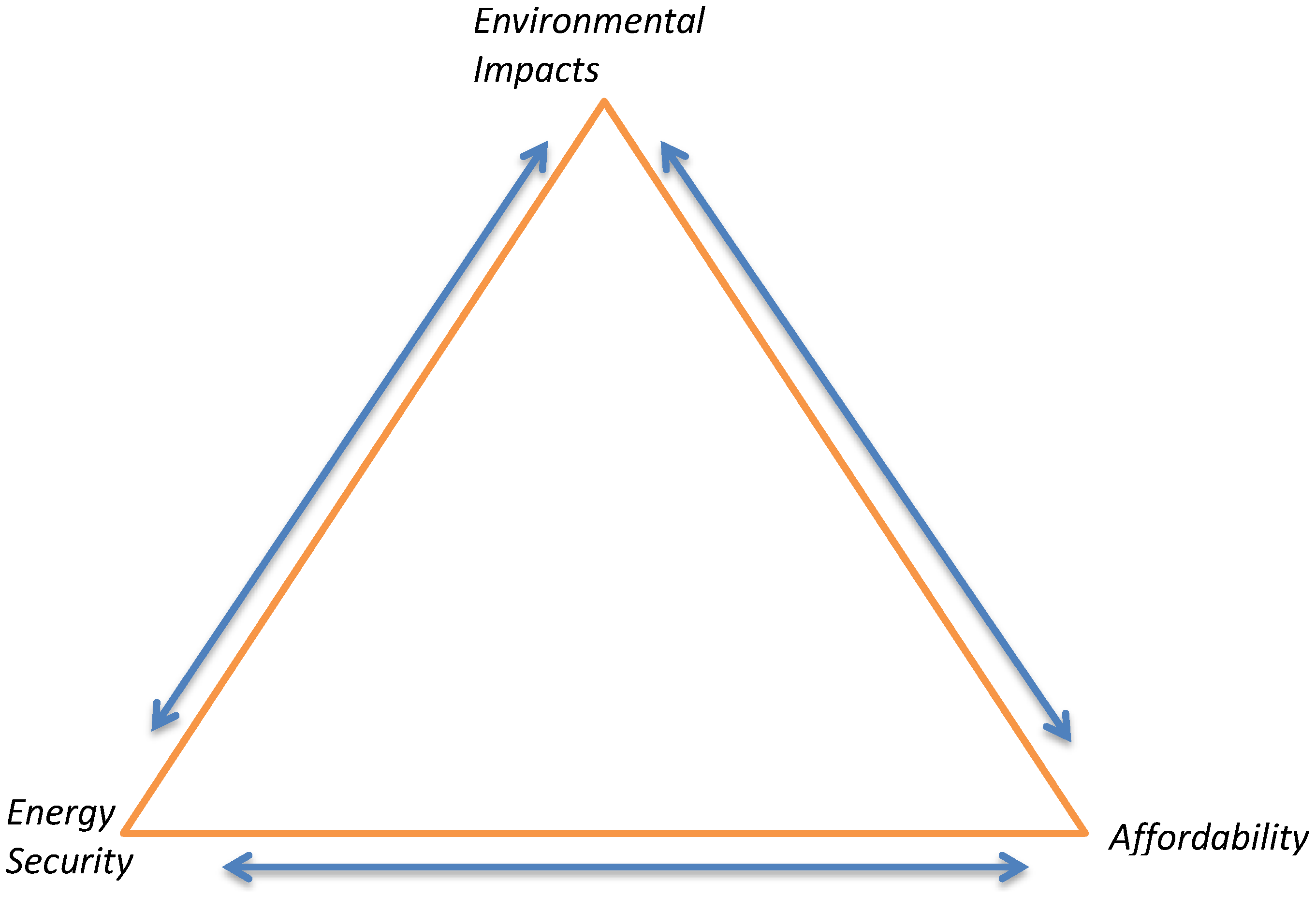

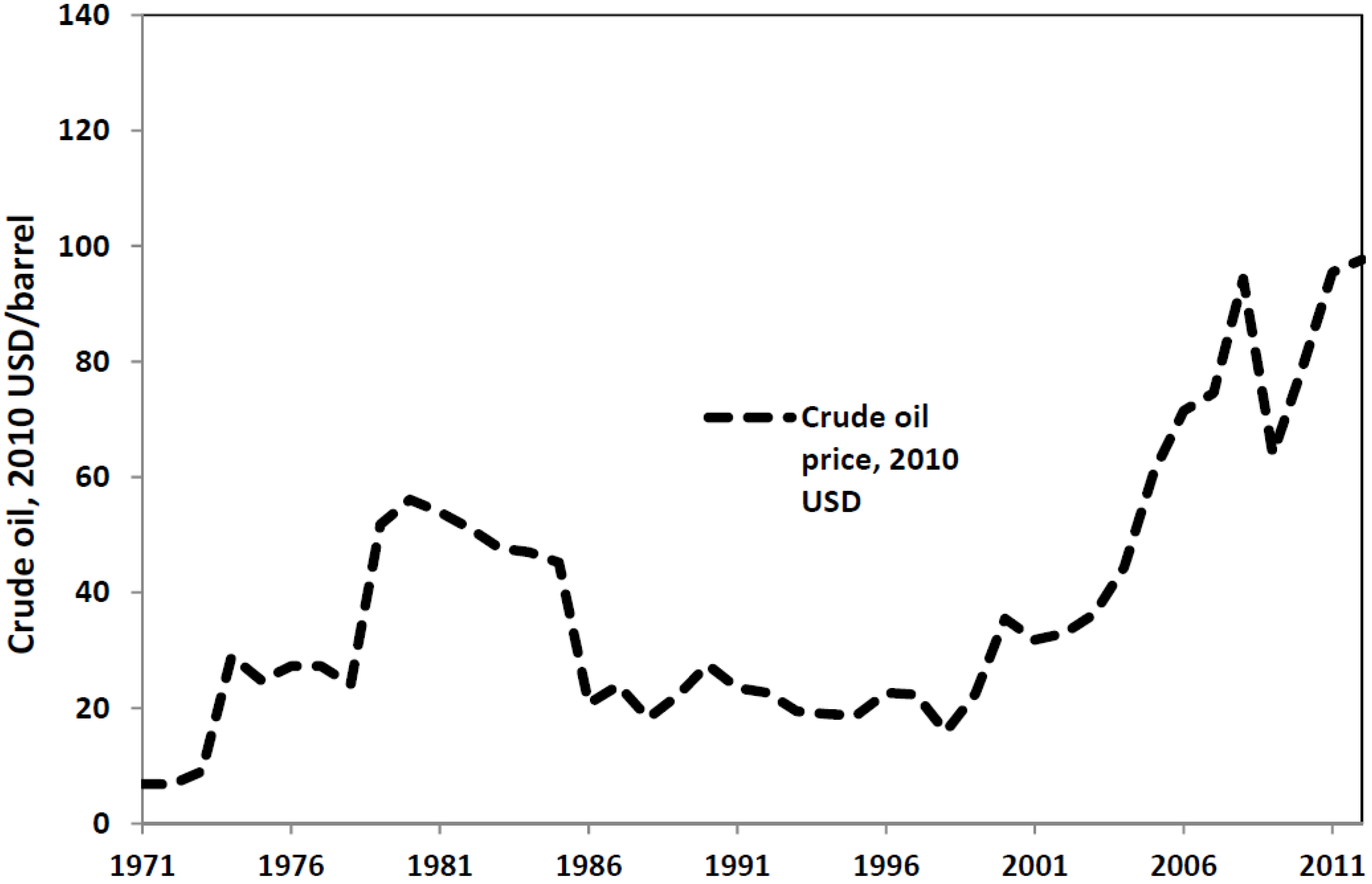

2. The Policy Pull

3. The Science and Technology Push

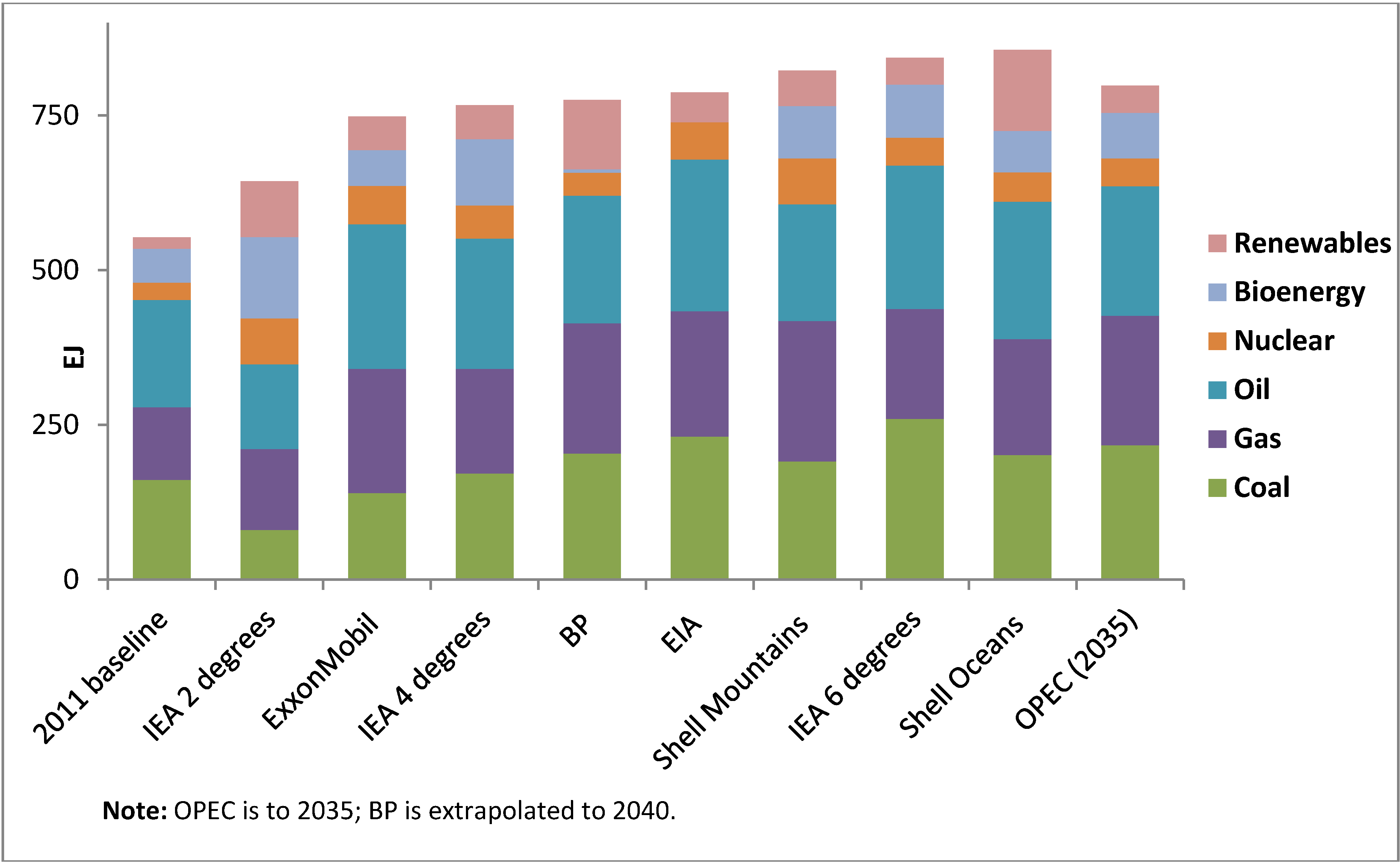

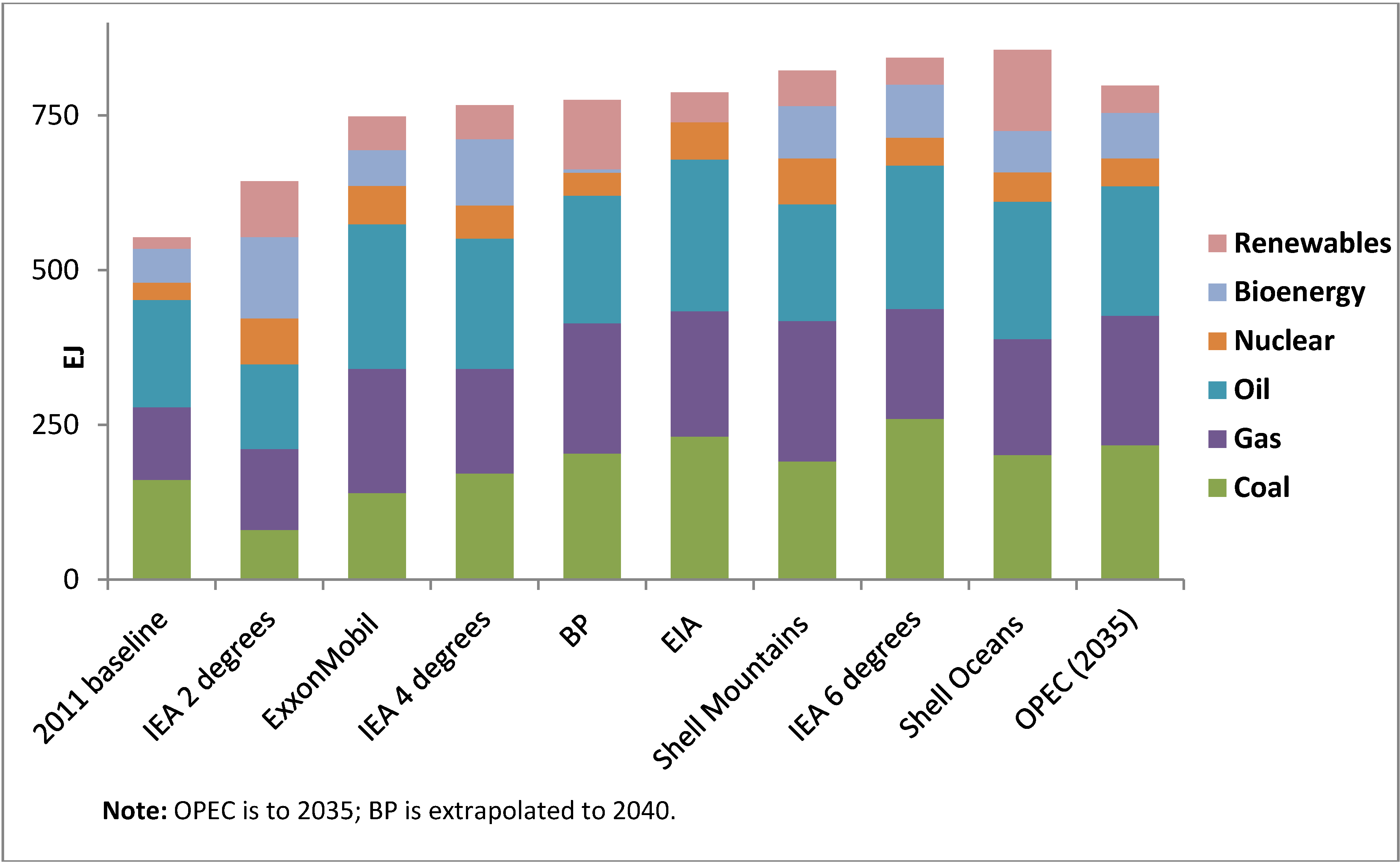

4. Global Projections

| Scenario/Projection | Style | Final Demand for Electricity (EJ) | Energy-Related CO2 Emissions (billion·t) |

|---|---|---|---|

| 2011 baseline | - | 66 | 31 |

| IEA 2 degrees | Normative | 108 | 20 |

| IEA 4 degrees | Adopts Cancún pledges | 120 | 40 |

| IEA 6 degrees | BAU projection | 131 | 52 |

| EIA International Energy Outlook | Outlook | 127 | 45 |

| ExxonMobil Outlook for Energy | Outlook | 124 | 36 |

| Shell Mountains scenario | Exploratory | 131 | 37 |

| Shell Oceans scenario | Exploratory | 159 | 41 |

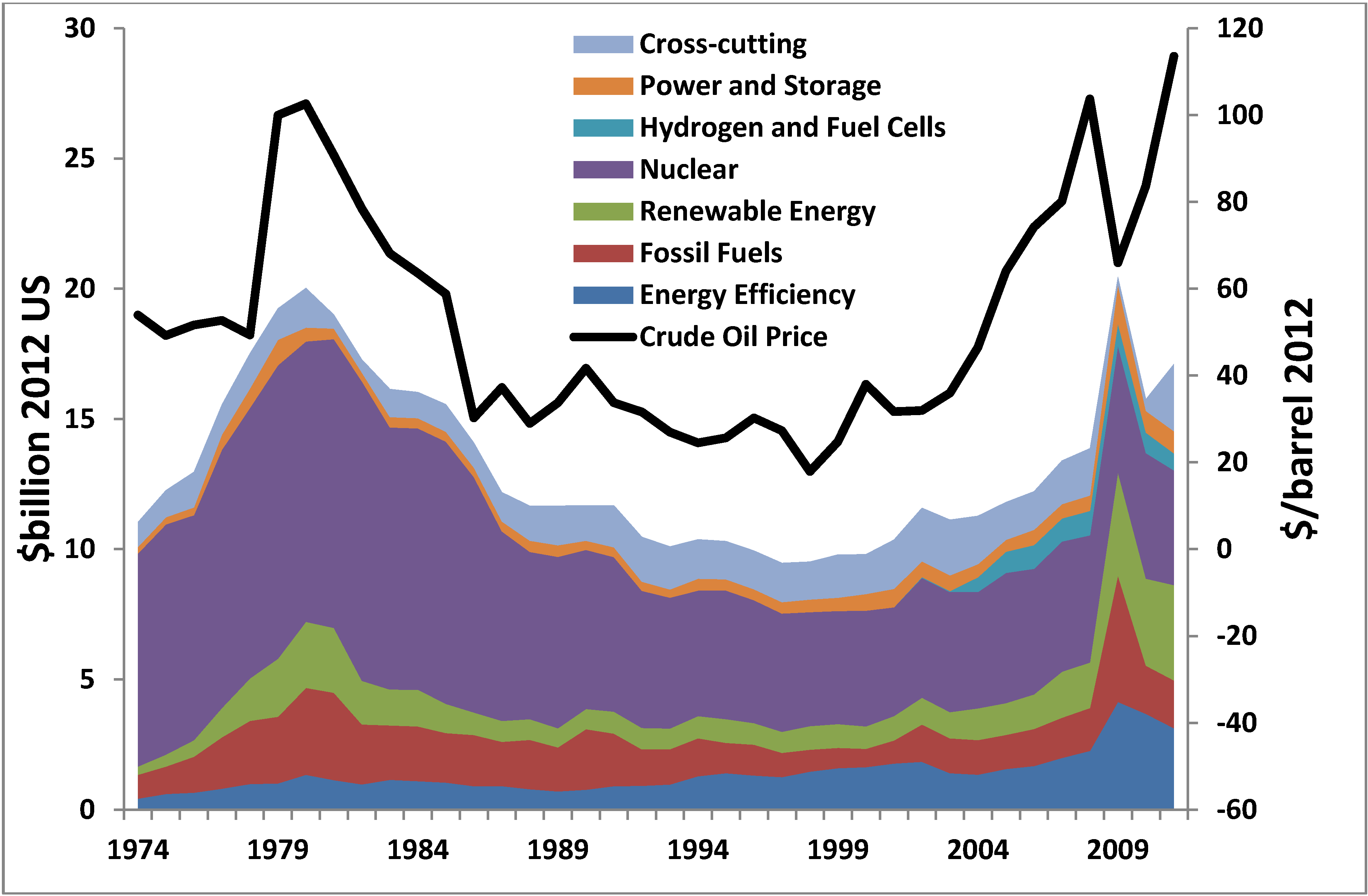

5. RD&D Patterns

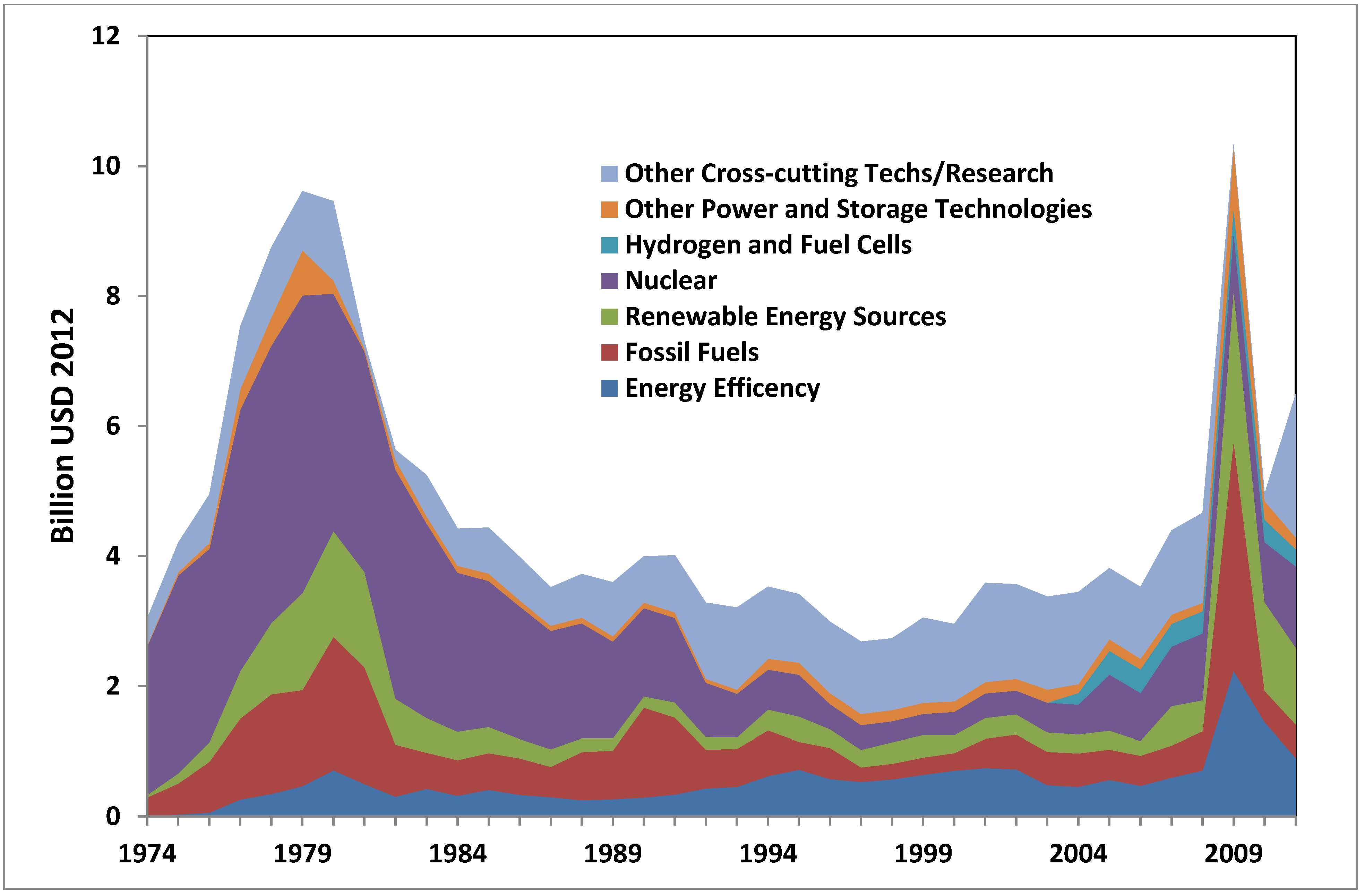

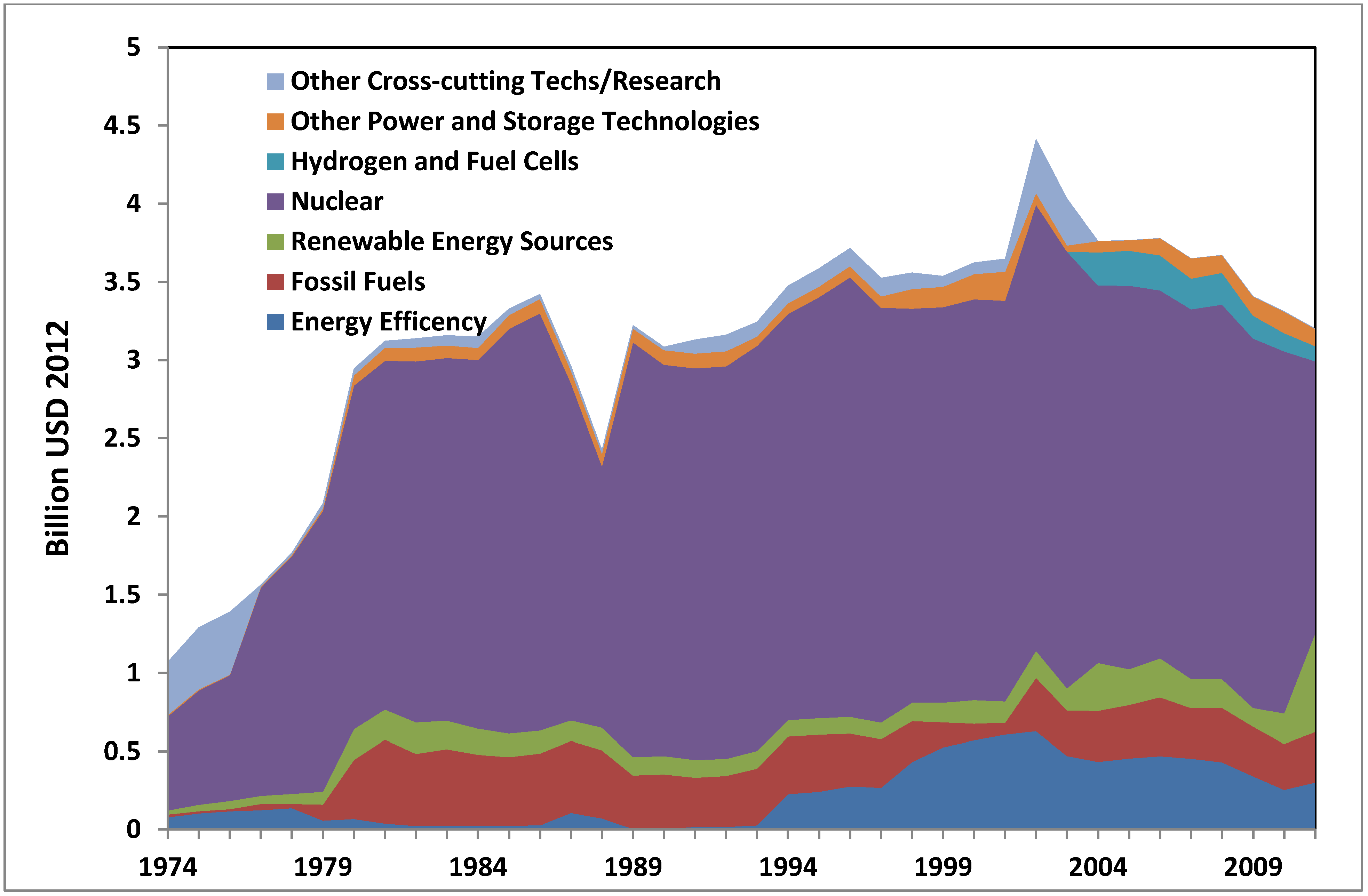

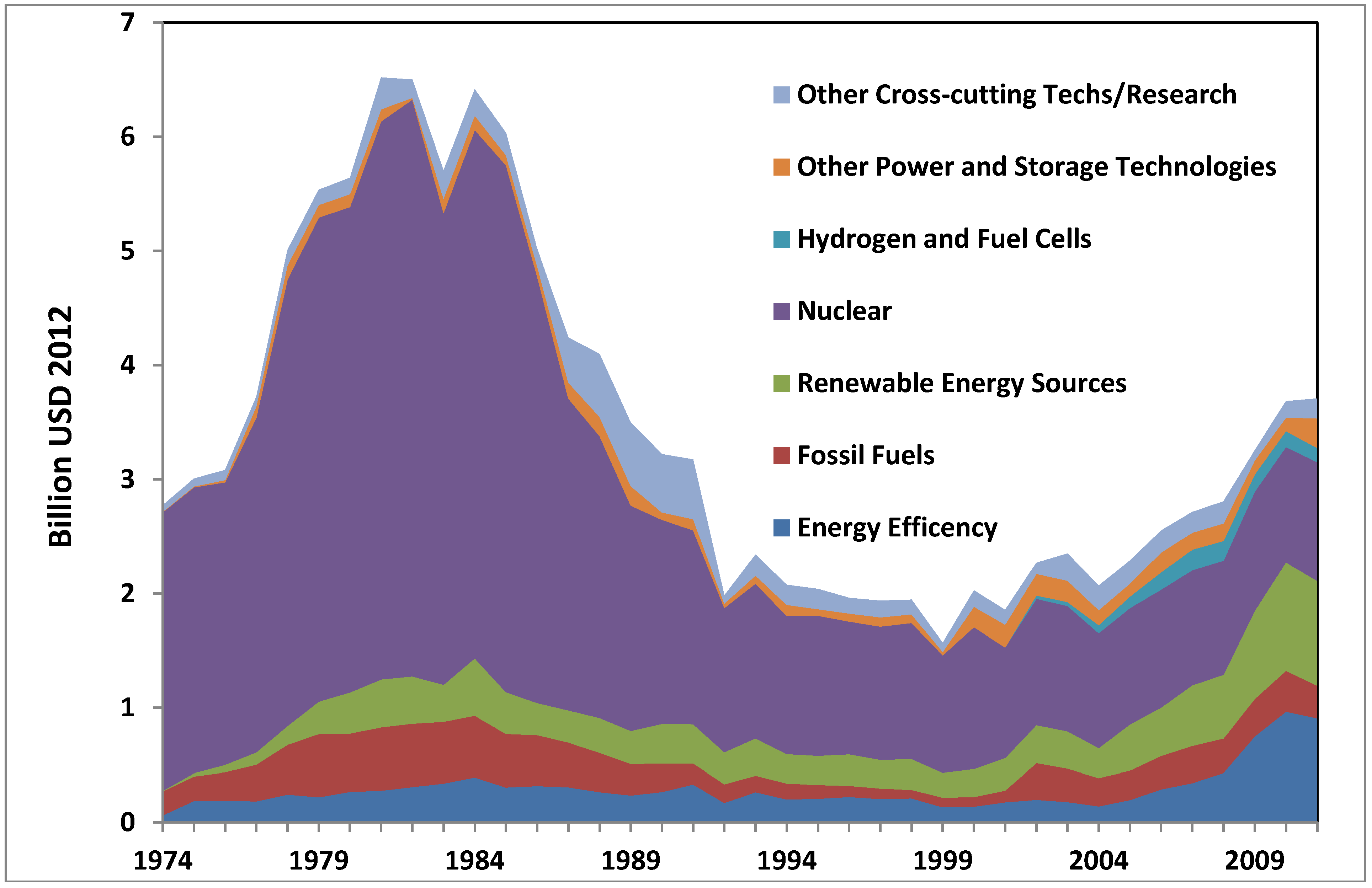

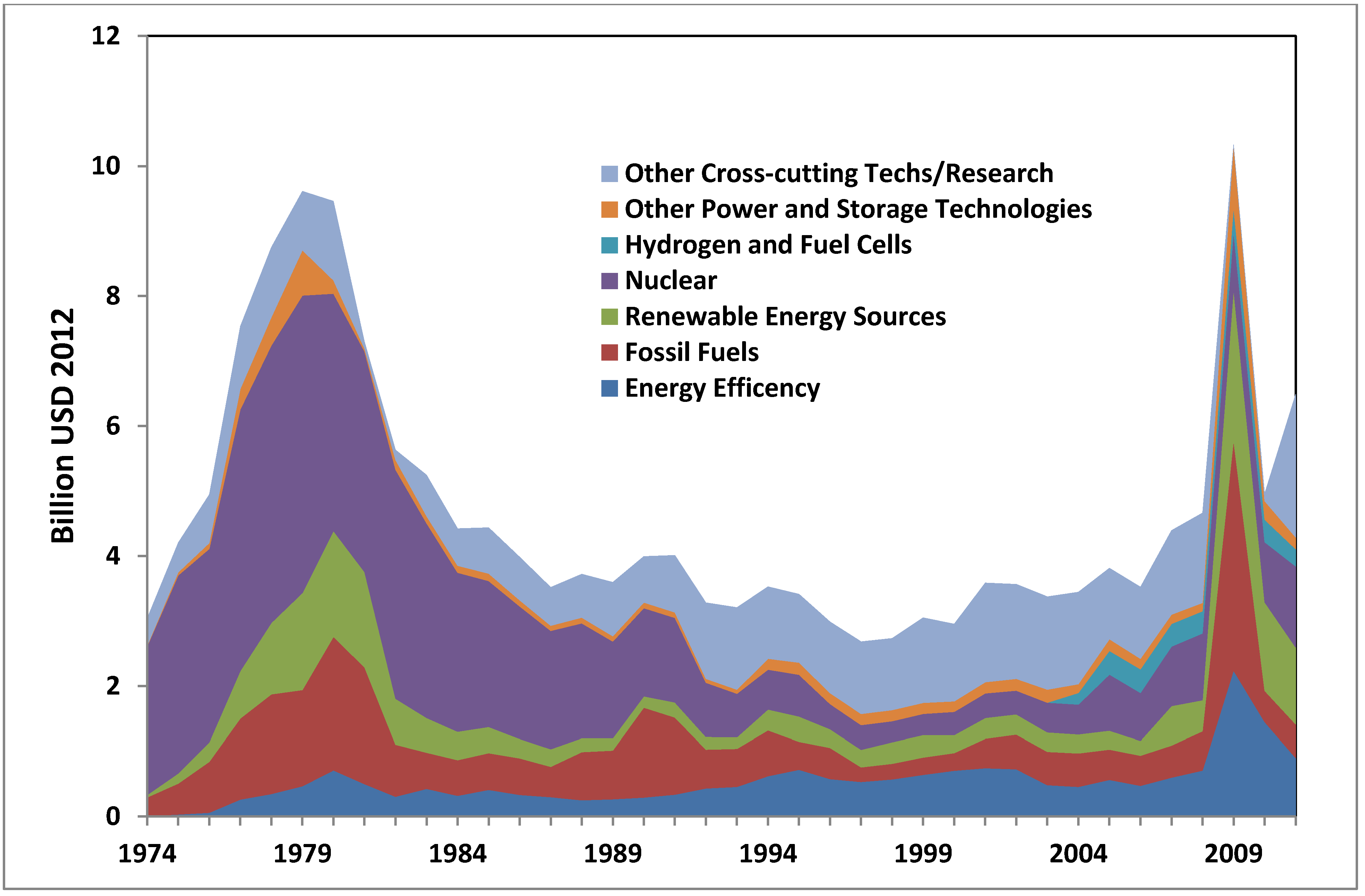

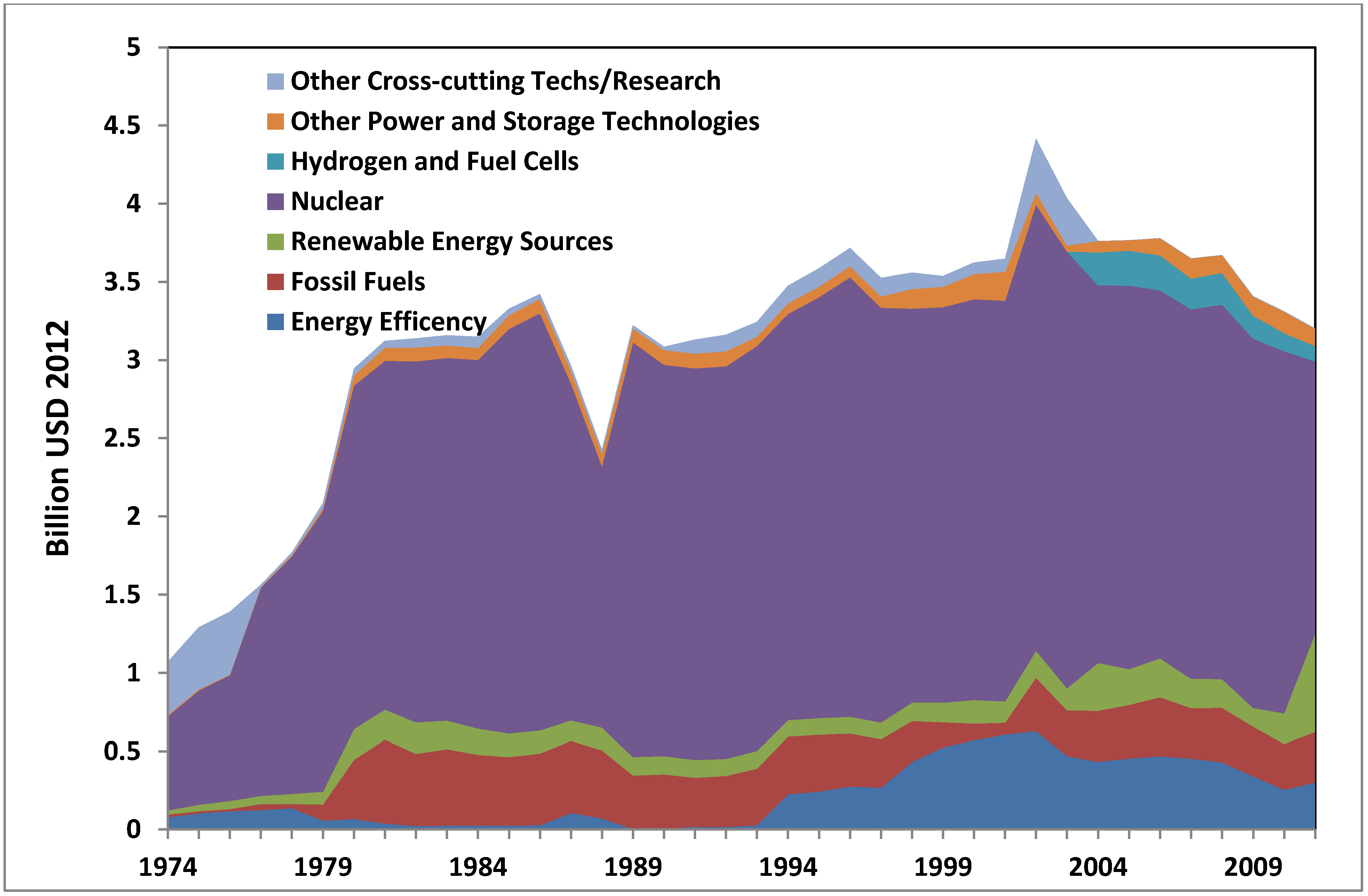

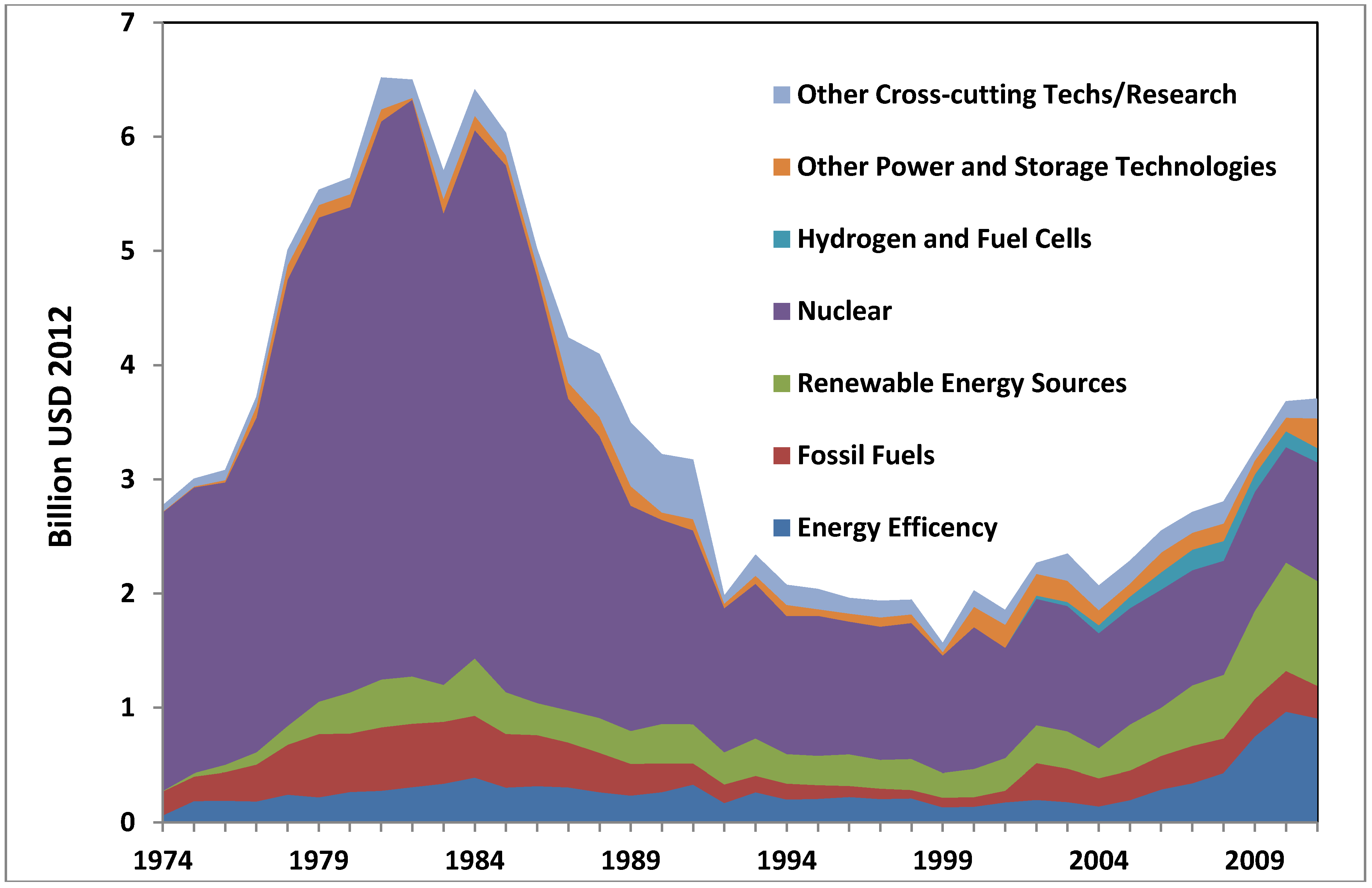

5.1. Public R&D Trends

| Area | Spend |

|---|---|

| Energy Efficiency | 3.1 |

| Fossil Fuels | 1.8 |

| Renewable Energy | 3.7 |

| Nuclear | 4.4 |

| Hydrogen and Fuel Cells | 0.7 |

| Power and Storage | 0.9 |

| Cross-cutting | 2.6 |

| Total | 17.2 |

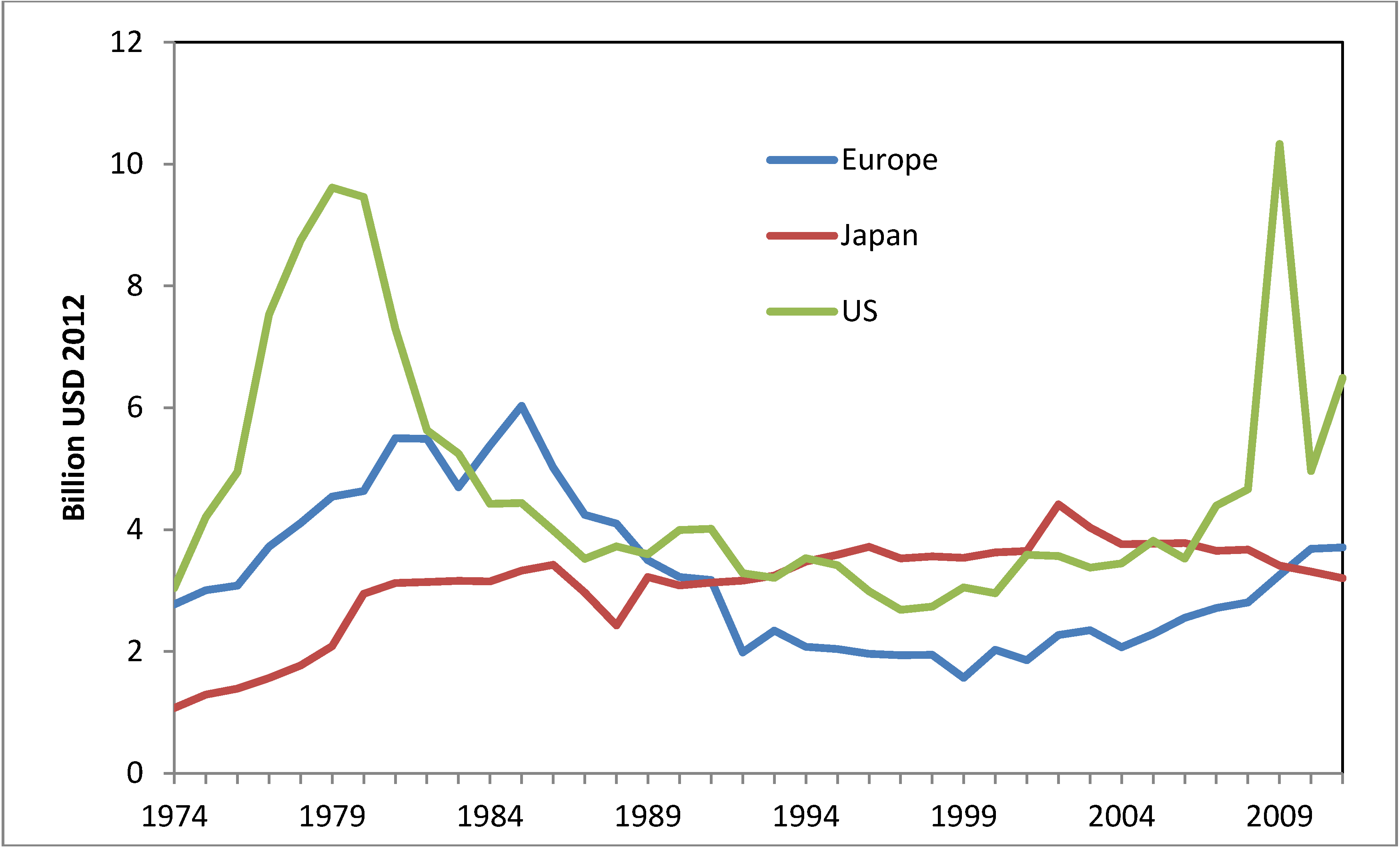

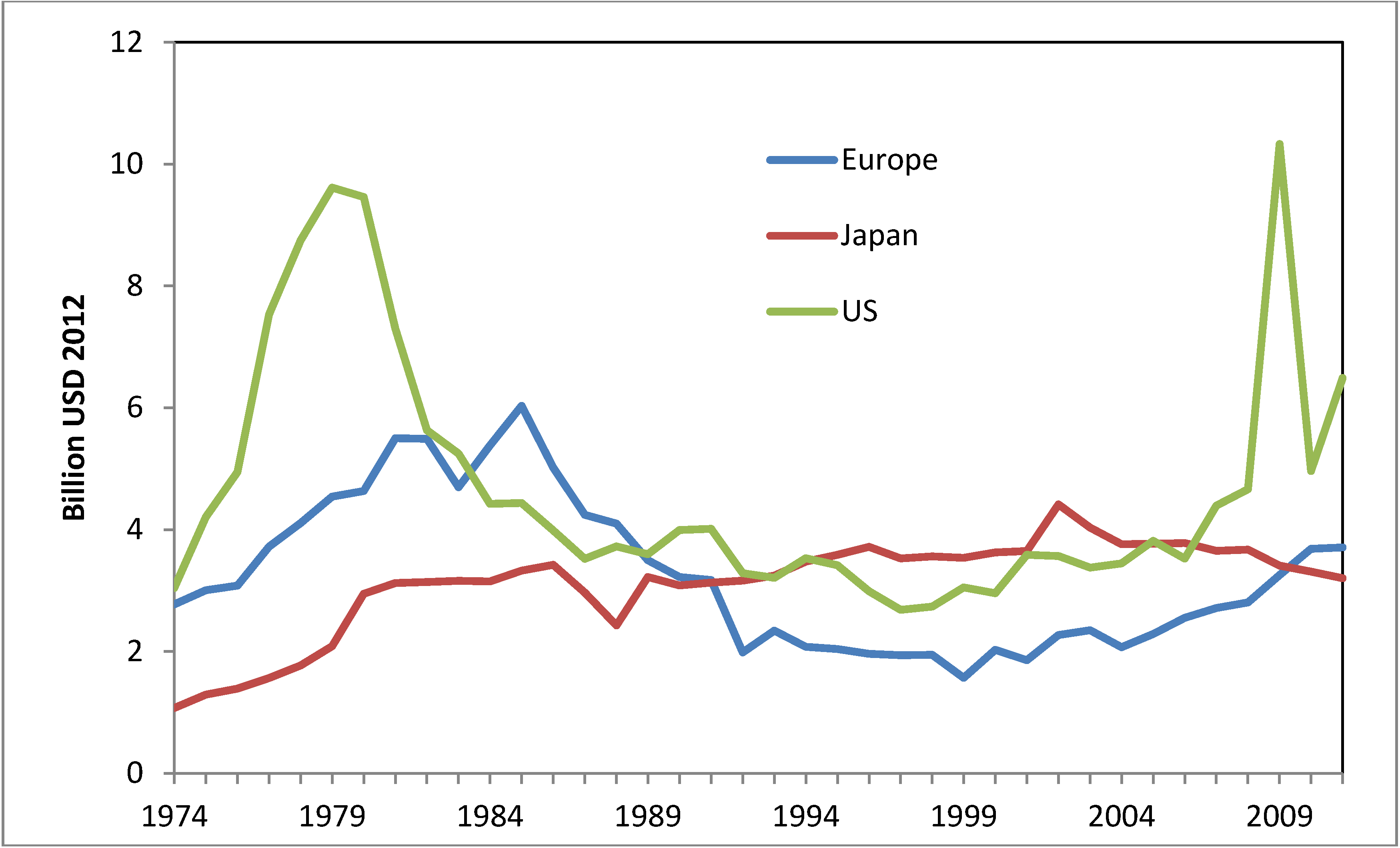

| Research Area | US | Japan | Major European Economies | ||||||

|---|---|---|---|---|---|---|---|---|---|

| 2000 | 2011 | % Change | 2000 | 2011 | % Change | 2000 | 2011 | % Change | |

| 1. Energy Efficiency | 702 | 898 | 128 | 570 | 301 | −47 | 137 | 908 | 664 |

| 2. Fossil Fuels | 270 | 514 | 190 | 106 | 323 | 304 | 84 | 286 | 339 |

| 3. Renewable Energy Sources | 275 | 1182 | 430 | 150 | 627 | 418 | 244 | 918 | 376 |

| 4. Nuclear | 356 | 1248 | 351 | 2563 | 1742 | −32 | 1242 | 1039 | -16 |

| 5. Hydrogen and Fuel Cells | 0 | 265 | - | 0 | 97 | - | 0 | 124 | - |

| 6. Other Power and Storage Technologies | 161 | 182 | 113 | 162 | 110 | −32 | 178 | 258 | 145 |

| 7. Other Cross-cutting research | 1190 | 2200 | 185 | 74 | 2 | −97 | 142 | 174 | 123 |

| Total | 2955 | 6489 | 220 | 3624 | 3203 | −12 | 2021 | 3708 | 183 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

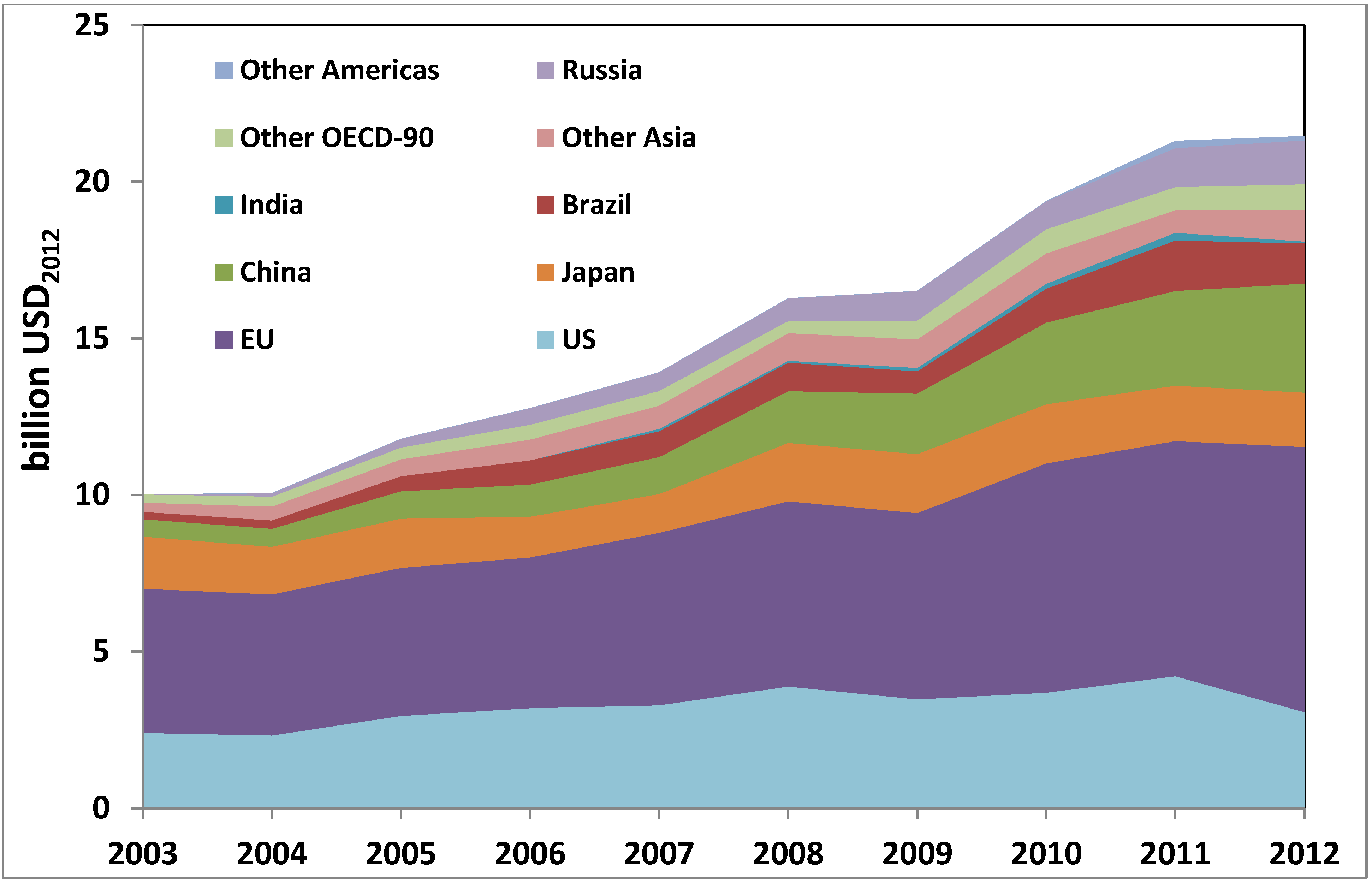

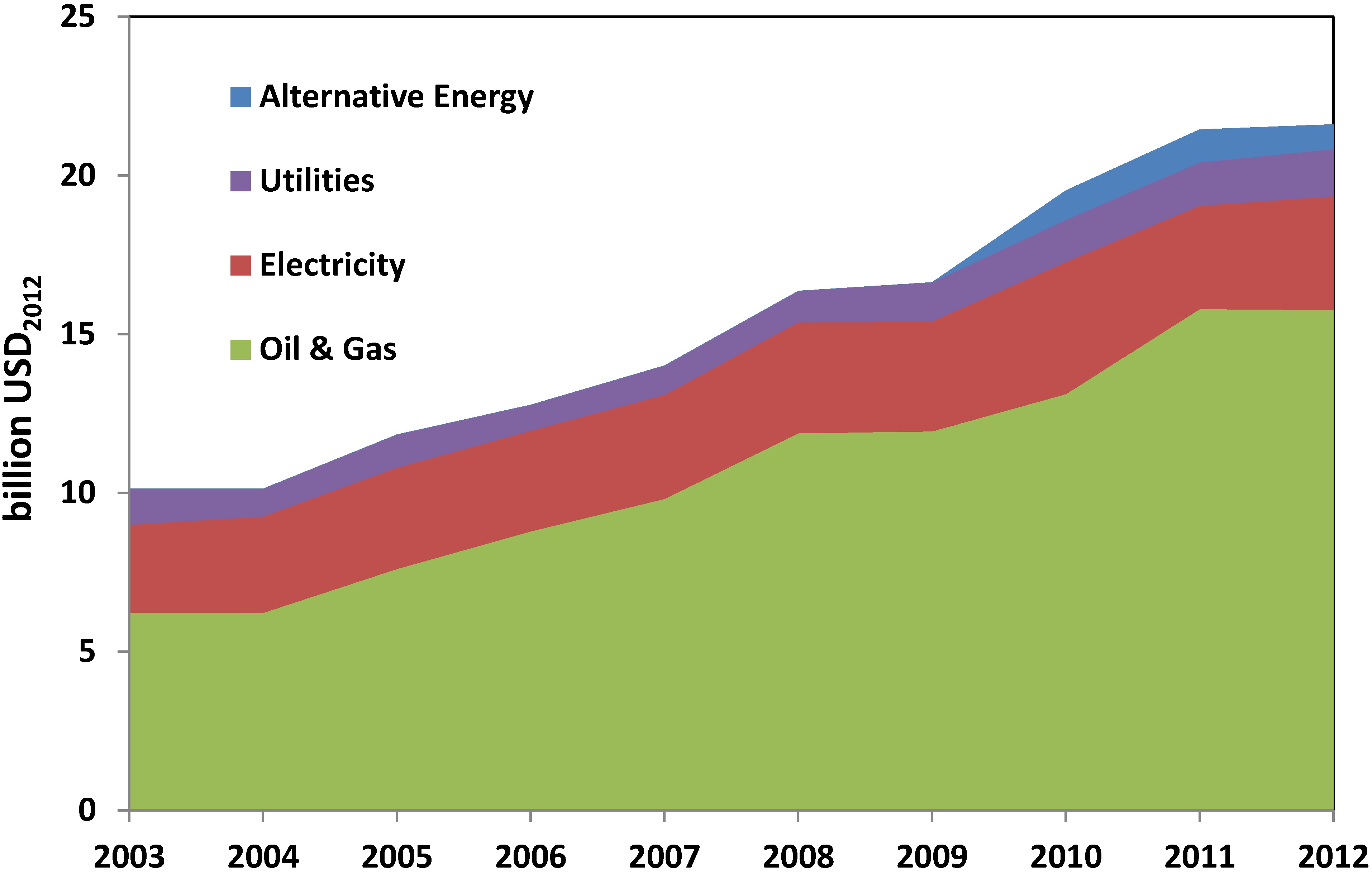

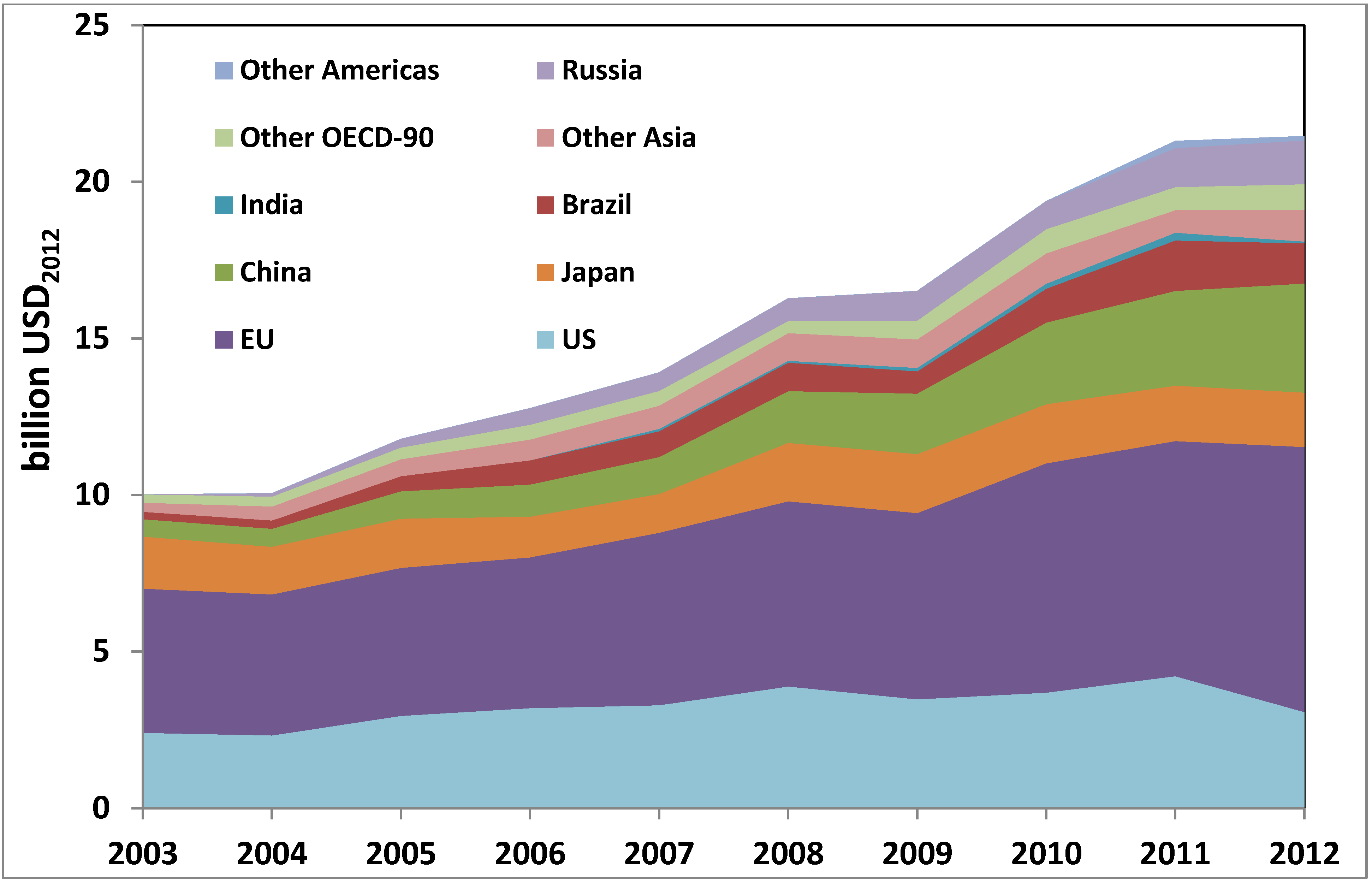

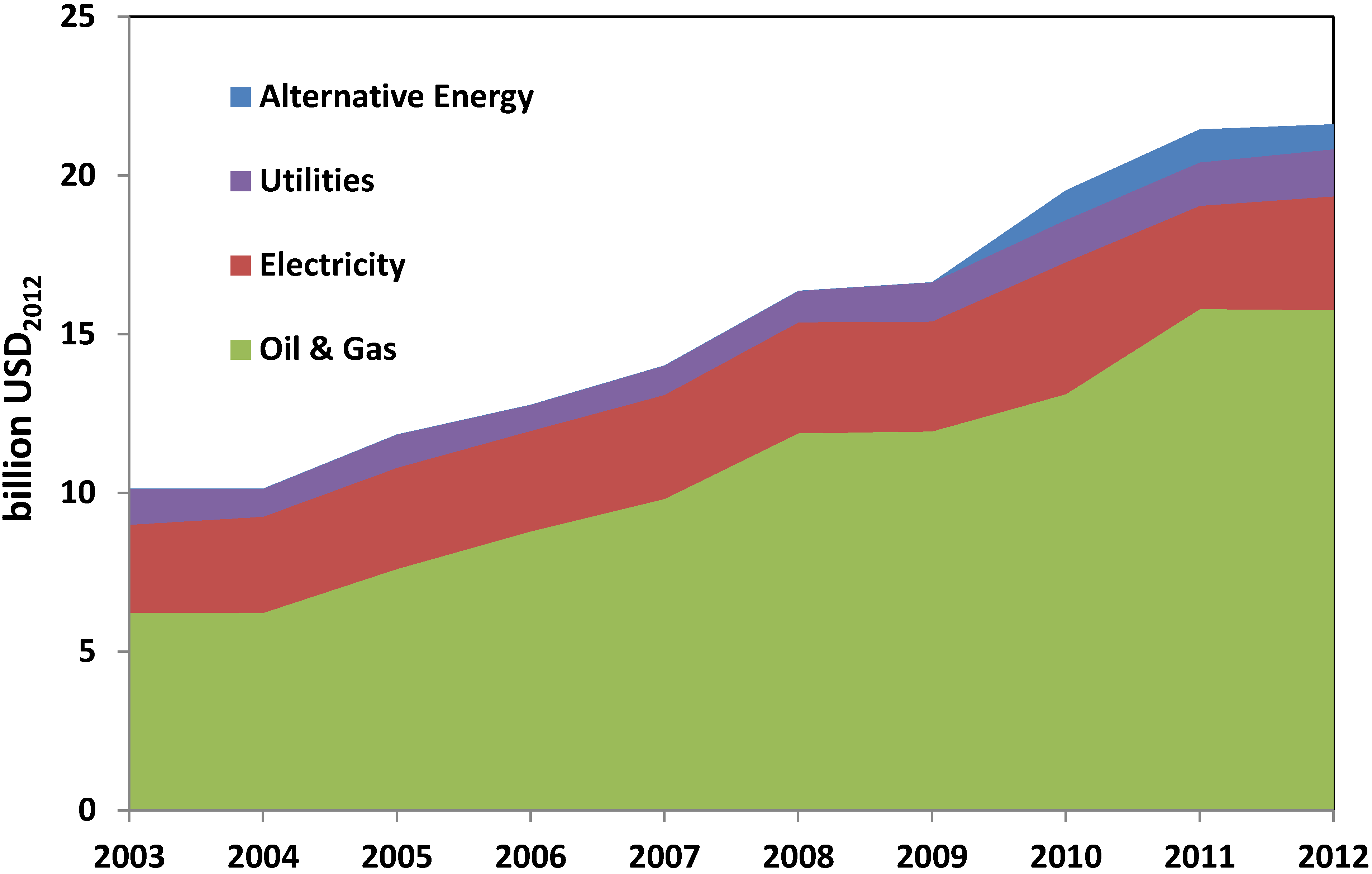

5.2. Private Sector Energy R&D Patterns

- (a)

- While the scoreboard has been published annually since 2004, referring to data in the previous year, the composition of the panel has changed. The number of companies covered has risen, from 1000 in the 2003 survey published in 2004 to 2000 in the 2009 survey published in 2010. Until 2010, the scoreboard covered equal numbers of EU and non-EU companies. Since 2011, a single panel covering both EU and non-EU companies has been used.

- (b)

- It is difficult to attribute all relevant R&D activity specifically to energy. The scoreboard identifies separately: oil and gas producers; oil equipment, services and distribution; electricity; gas, water and multi-utilities; and alternative energy. However, much energy R&D takes place in the electronic and electrical equipment sector and in general industrials (e.g., Siemens, General Electric) which cover products, e.g., transport equipment, extending beyond energy. R&D relevant to energy demand is particularly hard to attribute since it is embedded in wider R&D efforts in sectors such as automobiles and construction. Toyota, for example, is the world’s largest investor in R&D (over $10 billion in 2011). Manufacturers of appliances and electronic equipment are very R&D intensive (spending over 5% of revenue) and the total R&D expenditure of $50 billion vastly exceeds the $3 billion spent on energy efficiency RD&D by the public sector in IEA countries.

| Sector | OECD | Non-OECD | Total |

|---|---|---|---|

| Oil & gas producers | 6.4 | 6.1 | 12.5 |

| Oil equipment, services & distribution | 2.6 | 0.3 | 2.9 |

| Electricity | 2.9 | 0.6 | 3.5 |

| Gas, water & multi-utilities | 1.4 | 0.1 | 1.5 |

| Alternative energy | 0.8 | 0.0 | 0.8 |

6. Discussion

7. Conclusions and Further Questions

Acknowledgments

Author Contributions

Conflicts of Interest

References

- OECD. STAN Database for Structural Analysis. Available online: http://stats.oecd.org/Index.aspx?DataSetCode=STAN08BIS (accessed on 28 May 2014).

- EU Industrial R&D Investment Scoreboard 2013; European Commission, Joint Research Centre: Seville, Spain, 2013.

- International Energy Agency (IEA). Energy Technology Research and Development Database 2013; IEA: Paris, France, 2013. [Google Scholar]

- Gallagher, K.S.; Grübler, A.; Kuhl, L.; Nemet, G.; Wilson, C. The energy technology innovation system. Annu. Rev. Environ. Resour. 2012, 37, 137–162. [Google Scholar]

- McGowan, F. The single energy market and energy policy: Conflicting agendas? Energy Policy 1989, 17, 547–553. [Google Scholar] [CrossRef]

- The World Energy Council (WEC). Time to Get Real—The Case for Sustainable Energy Investment; WEC: London, UK, 2013. [Google Scholar]

- Repert of the Conference of the Parties on its Sixteenth Session, Held in Cancun from 29 November to 10 December 2010. Available online: http://unfccc.int/resource/docs/2010/cop16/eng/07a01.pdf (accessed on 25 August 2014).

- Intergovernmental Panel on Climate Change (IPCC). Climate Change 2014: Mitigation of Climate Change—Summary for Policymakers; IPCC: Geneva, Switzerland, 2014; p. 31. [Google Scholar]

- International Energy Agency (IEA). Energy Technology Perspectives 2012: Pathways to a Clean Energy System; IEA: Paris, France, 2012; pp. 56–59. [Google Scholar]

- International Energy Agency (IEA). Energy Technology Perspectives 2008; IEA: Paris, France, 2008; p. 650. [Google Scholar]

- Cabraal, R. Experiences and lessons from 15 years of World Bank support for photovoltaics for off-grid electrification. In Proceedings of the 2nd International Conference on the Developments in Renewable Energy Technology (ICDRET), Dhaka, Bangladesh, 5–7 January 2012; pp. 1–4.

- International Energy Agency World Energy Balances. Available online: http://www.esds.ac.uk/international/doipages/ieaweb.asp (accessed on 25 August 2014).

- U.S. Energy Information Administration. Short-Term Energy Outlook. Available online: http://www.eia.gov/forecasts/steo/report/prices.cfm (accessed on 30 May 2014).

- British Petroleum (BP). BP Statistical Review of World Energy; BP: London, UK, 2014; p. 48. [Google Scholar]

- Repealing the Carbon Tax. Available online: http://www.environment.gov.au/climate-change/repealing-carbon-tax (accessed on 8 August 2014).

- Foxon, T.J. Technological lock-in and the role of innovation. In Handbook of Sustainable Development; Atkinson, G., Dietz, S., Neumayer, E., Eds.; Edward Elgar Publishing: Cheltenham, UK; p. 140.

- International Energy Agency (IEA). Science for Today’s Energy Challenges: Accelerating Progress for a Sustainable Energy Future; IEA: Paris, France, 2006; p. 20. [Google Scholar]

- UK Energy Research Centre. Transforming Our Energy Future: Meeting Report. Available online: http://www.ukerc.ac.uk (accessed on 18 June 2014).

- International Energy Agency (IEA). Reviewing R&D Policies; IEA: Paris, France, 2007; p. 79. [Google Scholar]

- Freeman, C.; Louçã, F. As Time Goes By: From the Industrial Revolutions to the Information Revolution; Oxford University Press: Oxford, UK, 2001; p. 424. [Google Scholar]

- Teh, N.J.; Rhodes, A. UK Smart Grid Capabilities Development Programme; UK Energy Research Centre: London, UK, 2014; p. 80. [Google Scholar]

- Asmus, P. Microgrids, virtual power plants and our distributed energy future. Electr. J. 2010, 23, 72–82. [Google Scholar]

- Loulou, R. Documentation for the MARKAL Family of Models; International Energy Agency (IEA): Paris, France, 2004. [Google Scholar]

- Rhodes, A.; Skea, J.; Hannon, M. Electrochemical Energy Technologies and Energy Storage: RCUK Energy Strategy Fellowship Energy Research and Training Prospectus Report 6; Imperial College London: London, UK, 2014. [Google Scholar]

- DOE Joint Genome Institute. The First Tree Genome is Published. Available online: http://jgi.doe.gov/news_9_14_06/ (accessed on 25 June 2014).

- Skea, J.; Rhodes, A.; Hannon, M. Bioenergy: RCUK Energy Strategy Fellowship Energy Research and Training Prospectus Report 8; Imperial College London: London, UK, 2014. [Google Scholar]

- Stern, N. Research and Development, Demonstration and Deployment and Skills. In The Stern Review; Government Equalities Office: London, UK, 2006; pp. 216–234. [Google Scholar]

- Sunlight Electric History of Photovoltaics. Available online: http://www.sunlightelectric.com/pvhistory.php (accessed on 5 August 2014).

- U.S. Energy Information Administration. Annual Energy Outlook 2014; U.S. Energy Information Administration (EIA): Washington, DC, USA, 2014; p. 269.

- Organisation of the Petroleum Exporting Countries (OPEC). World Oil Outlook 2013; OPEC: Vienna, Austria, 2013; p. 318. [Google Scholar]

- ExxonMobil. The Outlook for Energy: A View to 2040; ExxonMobil: Irving, TX, USA, 2014; p. 58. [Google Scholar]

- British Petroleum (BP). BP Energy Outlook 2035; BP: London, UK, 2014. [Google Scholar]

- Shell Scenarios Team. Shell New Lens Scenarios; Shell Global: Hague, The Netherlands, 2013. [Google Scholar]

- Global Wind Energy Council (GWEC). Global Wind Statistics 2013; GWEC: Brussels, Belgium, 2014; pp. 2–3. [Google Scholar]

- EurObserv’er. PV Barometer 2012; EurObserv’er: Paris, France, 2012. [Google Scholar]

- Geels, F.W. Technological Transitions and System Innovations; Edward Elgar Publishing: Cheltenham, UK, 2005; p. 318. [Google Scholar]

- Gross, R.; Stern, J.; Charles, C.; Nicholls, J.; Candelise, C.; Heptonstall, P.; Greenacre, P. On Picking Winners: The Need for Targeted Support for Renewable Energy; Imperial College of London: London, UK, 2012; p. 28. [Google Scholar]

- Mazzucato, M. The Entrepreneurial State: Debunking Public vs. Private Sector Myths; Anthem Press: London, UK, 2013; p. 266. [Google Scholar]

- Helm, D. The Carbon Crunch: How We’re Getting Climate Change Wrong—And How to Fix it; Yale University Press: New Haven, CT, USA, 2012. [Google Scholar]

© 2014 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/3.0/).

Share and Cite

Rhodes, A.; Skea, J.; Hannon, M. The Global Surge in Energy Innovation. Energies 2014, 7, 5601-5623. https://doi.org/10.3390/en7095601

Rhodes A, Skea J, Hannon M. The Global Surge in Energy Innovation. Energies. 2014; 7(9):5601-5623. https://doi.org/10.3390/en7095601

Chicago/Turabian StyleRhodes, Aidan, Jim Skea, and Matthew Hannon. 2014. "The Global Surge in Energy Innovation" Energies 7, no. 9: 5601-5623. https://doi.org/10.3390/en7095601

APA StyleRhodes, A., Skea, J., & Hannon, M. (2014). The Global Surge in Energy Innovation. Energies, 7(9), 5601-5623. https://doi.org/10.3390/en7095601