The Financial Results of Energy Sector Companies in Europe and Their Involvement in Hydrogen Production

, , , ,

, , , ,

Abstract

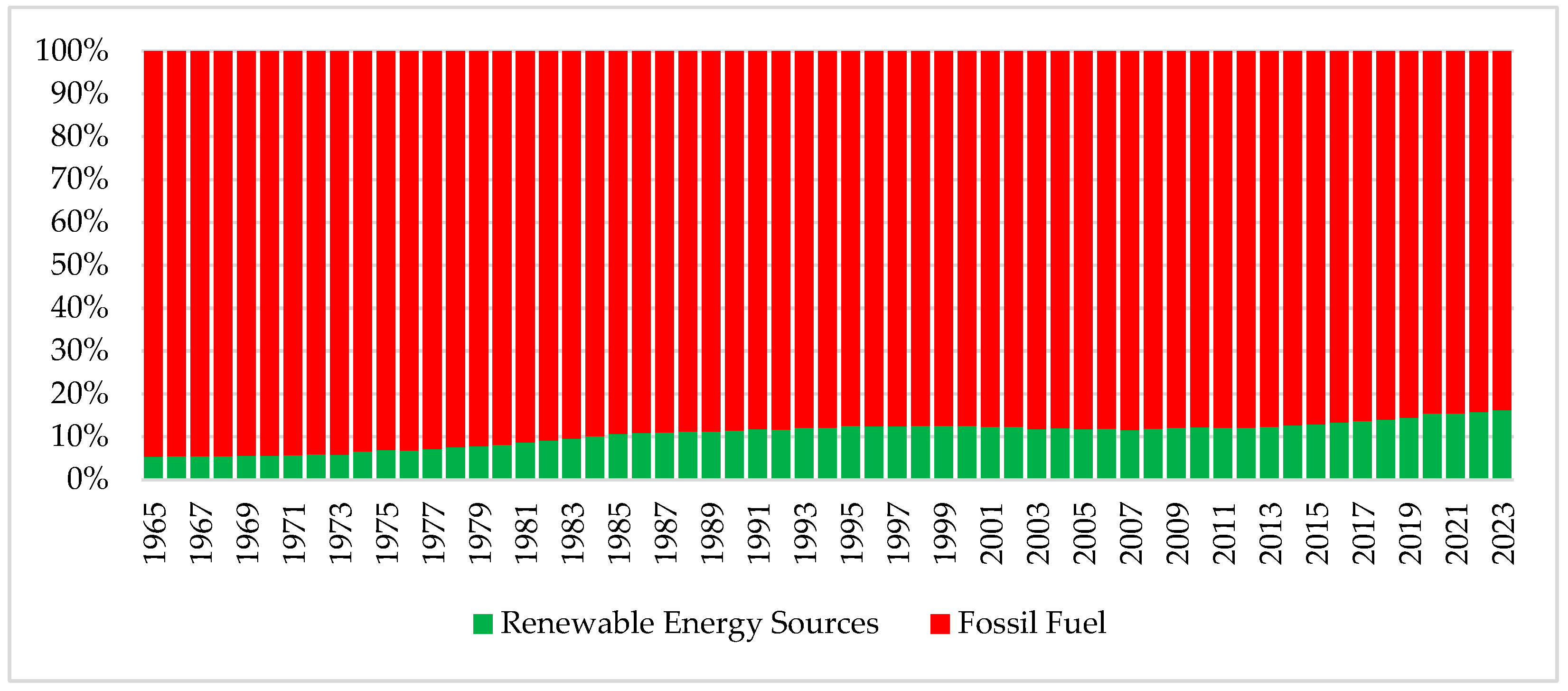

1. Introduction

2. Materials and Methods

3. Results and Discussion

3.1. Hydrogen Engagement Impact on a Company’s Financial Performance

3.2. Hydrogen Engagement Impact on a Company’s Market Value

3.3. Robustness Check

4. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Abbreviations and Nomenclature

| Abbreviation | Name |

| Adj. R2 | Adjusted R2 |

| BLUE | Blue hydrogen production |

| CR | Current ratio |

| FEs | Fixed effects |

| F-stat. | F statistics |

| FSTR | Financial structure |

| GRAY | Gray hydrogen production |

| GREEN | Green hydrogen production |

| GROW | Company growth |

| HYDRO | Hydrogen production engaging company |

| i | Company |

| MV/BV | Market-to-book value ratio |

| N | Number of observations |

| N | Variable |

| PROD | Hydrogen production |

| RES | Renewable energy sources |

| ROA | Return on assets ratio |

| ROE | Return on equity |

| SIZE | Company size |

| Std. err. | Standard error |

| STOR | Hydrogen storage |

| t | Year |

| TQ | Tobin’s Q |

| t-stat. | t statistics |

| UHS | Underground hydrogen storage |

| UGS | Underground gas storage |

References

- Manowska, A.; Bluszcz, A.; Chomiak-Orsa, I.; Wowra, R. Towards Energy Transformation: A Case Study of EU Countries. Energies 2024, 17, 1778. [Google Scholar] [CrossRef]

- Nasser, M.; Hassan, H. Green hydrogen production mapping via large scale water electrolysis using hybrid solar, wind, and biomass energies systems: 4E evaluation. Fuel 2024, 371, 131929. [Google Scholar] [CrossRef]

- Gajdzik, B.; Jaciow, M.; Wolniak, R.; Wolny, R.; Grebski, W.W. Assessment of Energy and Heat Consumption Trends and Forecasting in the Small Consumer Sector in Poland Based on Historical Data. Resources 2023, 12, 111. [Google Scholar] [CrossRef]

- Energy Institute. Statistical Review of World Energy 2024. Available online: https://www.energyinst.org/statistical-review (accessed on 6 September 2024).

- Elaheh Mohammadi, V.; Yosoon, C. Utilization of solar and wind power-generation systems in the mining industry: Recent trends and future prospects. J. Sustain. Min. 2024, 23, 1–10. [Google Scholar] [CrossRef]

- Al-Orabi, A.M.M.; Osman, G.; Sedhom, B.E. Analysis of the economic and technological viability of producing green hydrogen with renewable energy sources in a variety of climates to reduce CO2 emissions: A case study in Egypt. Appl. Energy 2023, 338, 120958. [Google Scholar] [CrossRef]

- Magdziarczyk, M.; Chmiela, A.; Su, W.; Smolinski, A. Green Transformation of Mining towards Energy Self-Sufficiency in a Circular Economy—A Case Study. Energies 2024, 17, 3771. [Google Scholar] [CrossRef]

- Więckowski, J.; Kizielewicz, B.; Sałabun, W. A multi-dimensional sensitivity analysis approach for evaluating the robustness of renewable energy sources in European countries. J. Clean. Prod. 2024, 469, 143225. [Google Scholar] [CrossRef]

- Zivar, D.; Kumar, S.; Foroozesh, J. Underground hydrogen storage: A comprehensive review. Int. J. Hydrogen Energy 2021, 46, 23436–23462. [Google Scholar] [CrossRef]

- Lackey, G.; Freeman, G.M.; Buscheck, T.A.; Haeri, F.; White, J.A.; Huerta, N.; Goodman, A. Characterizing hydrogen storage potential in U.S. underground gas storage facilities. Geophys. Res. Lett. 2023, 50, e2022GL101420. [Google Scholar] [CrossRef]

- Melaina, M.W.; Antonia, O.; Penev, M. Blending Hydrogen Into Natural Gas Pipeline Networks: A Review of Key Issues (NREL/TP-5600-51995); National Renewable Energy Laboratory: Golden, CO, USA, 2013.

- Doppfel, N.; Jansen, S.; Gerritse, J. Microbial side effects of underground hydrogen storage—Knowledge gaps, risks and opportunitiesfor successful implementation. Int. J. Hydrogen Energy 2021, 46, 8606–8954. [Google Scholar] [CrossRef]

- Ghadiani, H.; Farhat, Z.; Alam, T.; Islam, M.A. Assessing hydrogen embrittlement in pipeline steels for natural gas-hydrogen blends: Implications for existing infrastructure. Solids 2024, 5, 375–393. [Google Scholar] [CrossRef]

- Nazar, S.; Lipiec, S.; Proverbio, E. FEM modelling of hydrogen embrittlement in API 5L X65 steel for safe hydrogen transportation. J. Mater. Sci. Mater. Eng. 2025, 20, 9. [Google Scholar] [CrossRef]

- Frischmuth, T.; Götz, J.; Kremmer, M. Fracture toughness assessment of pipeline steels under hydrogen exposure for blended gas applications. Metals 2024, 15, 29. [Google Scholar] [CrossRef]

- Gajdzik, B.; Wolniak, R.; Nagaj, R.; Grebski, W.W.; Romanyshyn, T. Barriers to Renewable Energy Source (RES) Installations as Determinants of Energy Consumption in EU Countries. Energies 2023, 16, 7364. [Google Scholar] [CrossRef]

- Smoliński, A.; Howaniec, N. Hydrogen energy, electrolyzers and fuel cells—The future of modern energy sector. Int. J. Hydrogen Energy 2020, 45, 5607. [Google Scholar] [CrossRef]

- Alanzi, S.S.; Aldalali, B.; Kamel, R.M. Effects of sandstorms on hybrid renewable energy sources and load demand in arid desert climates: A case study. Energy Sustain. Dev. 2024, 81, 101473. [Google Scholar] [CrossRef]

- Doorga, J.R.S.; Hall, J.W.; Eyre, N. Geospatial multi-criteria analysis for identifying optimum wind and solar sites in Africa: Towards effective power sector decarbonization. Renew. Sustain. Energy Rev. 2022, 158, 112107. [Google Scholar] [CrossRef]

- Manowska, A.; Dylong, A.; Tkaczyk, B.; Manowski, J. Analysis and Monitoring of Maximum Solar Potential for Energy Production Optimization Using Photovoltaic Panels. Energies 2024, 17, 72. [Google Scholar] [CrossRef]

- Smoliński, A.; Howaniec, N. Experimental investigation and chemometric analysis of gasification and co-gasification of olive pomace and Sida Hermaphrodita blends with sewage sludge to hydrogen-rich gas. Energy 2023, 284, 129208. [Google Scholar] [CrossRef]

- Smoliński, A.; Wojtacha-Rychter, K.; Krol, M.; Magdziarczyk, M.; Polański, J.; Howaniec, N. Co-gasification of refuse-derived fuels and bituminous coal with oxygen/steam blend to hydrogen rich gas. Energy 2022, 254, 124210. [Google Scholar] [CrossRef]

- Zdeb, J.; Howaniec, N.; Smoliński, A. Utilization of Carbon Dioxide in Coal Gasification—An Experimental Study. Energies 2019, 12, 140. [Google Scholar] [CrossRef]

- Cui, S.; Zhu, G.; He, L.; Wang, X.; Zhang, X. Analysis of the fire hazard and leakage explosion simulation of hydrogen fuel cell vehicles. Therm. Sci. Eng. Prog. 2023, 41, 101754. [Google Scholar] [CrossRef]

- Moradi, R.; Groth, K.M. Hydrogen storage and delivery: Review of the state of the art technologies and risk and reliability analysis. Int. J. Hydrogen Energy 2019, 44, 12254–12269. [Google Scholar] [CrossRef]

- Abramov, Y.; Basmanov, O.; Krivtsova, V.; Mikhayluk, A.; Makarov, Y. Determining the functioning efficiency of a fire safety subsystem when operating the hydrogen storage and supply system. East.-Eur. J. Enterp. Technol. 2024, 2, 75–84. [Google Scholar] [CrossRef]

- Abramov, Y.; Kryvtsova, V.; Mikhailyuk, A. Justification of the characteristics of the fire-safe condition control system of the storage system and hydrogen supply. Eng. Sci. Archit. 2023, 1, 125–130. [Google Scholar] [CrossRef]

- Tarkowski, R. Underground hydrogen storage: Characteristics and prospects. Renew. Sustain. Energy Rev. 2019, 104, 86–94. [Google Scholar] [CrossRef]

- Talukdar, M.; Blum, P.; Heinemann, N.; Miocic, J. Techno-economic analysis of underground hydrogen storage in Europe. iScience 2024, 27, 108771. [Google Scholar] [CrossRef]

- Alms, K.; Berndsen, M.; Groeneweg, A.; Graf, M.; Nehler, M.; Ahrens, B. Underground hydrogen storage in the Bunter Sandstone Formation in the North German Basin: Capacity assessment and geochemical modeling. Energy Technol. 2023, 13, 2300847. [Google Scholar] [CrossRef]

- Heinemann, N.; Alcalde, J.; Miocic, J.M.; Hangx, S.J.T.; Kallmeyer, J.; Ostertag-Henning, C.; Hassanpouryouzband, A.; Thaysen, E.M.; Strobel, G.J.; Schmidt-Hattenberger, C.; et al. Enabling large-scale hydrogen storage in porous media—The scientific challenges. Energy Environ. Sci. 2021, 14, 853–864. [Google Scholar] [CrossRef]

- Graczyk, A.M.; Kusterka-Jefmańska, M.; Jefmański, B.; Graczyk, A. Pro-Ecological Energy Attitudes towards Renewable Energy Investments before the Pandemic and European Energy Crisis: A Segmentation-Based Approach. Energies 2023, 16, 707. [Google Scholar] [CrossRef]

- Gado, M.G.; Nasser, M.; Hassan, H. Potential of solar and wind-based green hydrogen production frameworks in African countries. Int. J. Hydrogen Energy 2024, 68, 520–536. [Google Scholar] [CrossRef]

- Banda, F.M.; Edriss, A.-K. What Factors Influence the Profitability of Firms in Malawi? Evidence from the Non-Financial Firms Listed on the Malawi Stock Exchange. Int. J. Financ. Issues 2022, 12, 86–91. [Google Scholar] [CrossRef]

- Al-Jafari, M.K.; Al Samman, H. Determinants of Profitability: Evidence from Industrial Companies Listed on Muscat Securities Market. Rev. Eur. Stud. 2015, 7, 303–311. [Google Scholar] [CrossRef]

- Hossain, T. Determinants of profitability: A study on manufacturing companies listed on the Dhaka Stock Exchange. Asian Econ. Financ. Rev. 2020, 10, 1496–1508. [Google Scholar] [CrossRef]

- Al-Najjar, B.; Anfimiadou, A. Environmental Policies and Firm Value. Bus. Strategy Environ. 2011, 21, 49–59. [Google Scholar] [CrossRef]

- Squadrito, G.; Maggio, G.; Nicita, A. The green hydrogen revolution. Renew. Energy 2023, 216, 119041. [Google Scholar] [CrossRef]

- Gupta, J. Application of Green Management in Business Processes. Natl. J. Leg. Res. Innov. Ideas 2023, 3, 84–97. Available online: https://www.scribd.com/document/682030095/Application-of-Green-Management-in-Business-Processes-NJLRII-compressed (accessed on 4 May 2025).

- Gawęda, A. Does environmental, social, and governance performance elevate firm value? International evidence. Financ. Res. Lett. 2025, 73, 106639. [Google Scholar] [CrossRef]

- Tokarski, S.; Magdziarczyk, M.; Smoliński, A. Risk management scenarios for investment program delays in the Polish power industry. Energies 2021, 14, 5210. [Google Scholar] [CrossRef]

- Tokarski, S.; Magdziarczyk, M.; Smoliński, A. An Analysis of Risks and Challenges to the Polish Power Industry in the Year 2024. Energies 2024, 17, 1044. [Google Scholar] [CrossRef]

- Zwickl-Bernhard, S.; Auer, H. Green hydrogen from hydropower: A non-cooperative modeling approach assessing the profitability gap and future business cases. Energy Strategy Rev. 2022, 43, 100912. [Google Scholar] [CrossRef]

- Tudor, C. Enhancing Sustainable Finance through Green Hydrogen Equity Investments: A Multifaceted Risk-Return Analysis. Risks 2023, 11, 212. [Google Scholar] [CrossRef]

- Cheilas, P.T.; Daglis, T.; Xidonas, P.; Michaelides, P.G.; Konstantakis, K.N. Financial dynamics, green transition and hydrogen economy in Europe. Int. Rev. Econ. Financ. 2024, 94, 103370. [Google Scholar] [CrossRef]

- Okafor, A.; Adusei, M.; Adeleye, B.N. Corporate social responsibility and financial performance: Evidence from US tech firms. J. Clean. Prod. 2021, 292, 126078. [Google Scholar] [CrossRef]

- Barros, V.; Verga, M.P.; Miranda, S.J.; Rino, V.P. M&A activity as a driver for better ESG performance. Technol. Forecast. Soc. Change 2022, 175, 121338. [Google Scholar] [CrossRef]

- Torres-Reyna, O. Panel Data Using R-Slides; Princeton University: Princeton, NJ, USA, 2010; Available online: https://www.princeton.edu/~otorres/Panel101R.pdf (accessed on 4 May 2025).

- Mervelskemper, L.; Streit, D. Enhancing Market Valuation of ESG Performance: Is Integrated Reporting Keeping its Promise? Bus. Strategy Environ. 2017, 26, 536–549. [Google Scholar] [CrossRef]

- White, H. A heteroscedasticity consistent covariance matrix estimator and a direct test for heteroscedasticity. Econometrica 1980, 48, 817–838. [Google Scholar] [CrossRef]

- Kao, C. Spurious regression and residual-based tests for cointegration in panel data. J. Econom. 1999, 90, 1–44. [Google Scholar] [CrossRef]

- Sánchez-Ballesta, J.P.; Yagüe, J. Tax avoidance and debt maturity in SMEs. J. Int. Financ. Manag. Account. 2024, 35, 429–464. [Google Scholar] [CrossRef]

- Cho, W.; Lee, J.; Park, J. Higher highs and lower lows: Investor valuation of ESG and financial performance. Appl. Econ. Lett. 2023, 31, 1482–1487. [Google Scholar] [CrossRef]

- Abdi, Y.; Li, X.; Camara-Tutull, X. Exploring the impact of sustainability (ESG) disclosure on firm value and financial performance (FP) in airline industry: The moderating role of size and age. Environ. Dev. Sustain. 2022, 24, 5052–5079. [Google Scholar] [CrossRef]

- Zaiane, S.; Ellouze, D. Corporate social responsibility and firm financial performance: The moderating effects of size and industry sensitivity. J. Manag. Gov. 2023, 27, 1147–1187. [Google Scholar] [CrossRef]

- Gupta, J. Role Of United Nations Environment Programme. in: Addressing the Issue of Climate Change. Bharat Manthan Multidiscip. Res. J. 2023, 3, 83–91. Available online: https://www.thebharatmanthan.in/archives#h.f3hsf5vsh3l0 (accessed on 4 May 2025).

- Sadiq, M.; Khan, M.S.; Abid, M.; Alkahtani, M.; Xiaoming, B. Exergo-economic analysis of a solar-driven multigeneration system for power, ammonia production, and cooling. Renew. Energy 2025, 248, 123072. [Google Scholar] [CrossRef]

{kind=link}

| Country of Headquarters | Number of Companies |

|---|---|

| Austria | 2 |

| Belgium | 4 |

| Bosnia and Herzegovina | 8 |

| Bulgaria | 3 |

| Croatia | 2 |

| Cyprus | 6 |

| Denmark | 2 |

| Estonia | 1 |

| Faroe Islands | 1 |

| Finland | 3 |

| France | 15 |

| Germany | 11 |

| Greece | 9 |

| Guernsey | 4 |

| Hungary | 1 |

| Iceland | 2 |

| Ireland | 9 |

| Isle of Man | 1 |

| Italy | 9 |

| Jersey | 6 |

| Lithuania | 1 |

| Luxembourg | 3 |

| Macedonia | 2 |

| Monaco | 2 |

| Netherlands | 5 |

| Norway | 33 |

| Poland | 15 |

| Portugal | 2 |

| Republic of Montenegro | 1 |

| Republic of Serbia | 1 |

| Romania | 14 |

| Russia | 13 |

| Slovenia | 1 |

| Spain | 2 |

| Sweden | 16 |

| Switzerland | 2 |

| Ukraine | 3 |

| United Kingdom | 72 |

| Variables | Name | Abbreviated Name | Definition |

|---|---|---|---|

| Dependent | Return on assets ratio | ROA | EBIT/Year-average total assets |

| Market-to-book value ratio | MV/BV | Market capitalization/(Total assets − Total debt) | |

| Explanatory | Hydrogen production-engaging company | HYDRO | Dummy equals 1 if a company is engaged in hydrogen-related activities and 0 otherwise |

| Hydrogen production | PROD | Dummy equals 1 if a company is engaged in hydrogen production and 0 otherwise | |

| Hydrogen storage | STOR | Dummy equals 1 if a company is engaged in hydrogen storage and 0 otherwise | |

| Green hydrogen production | GREEN | Dummy equals 1 if a company is engaged in green hydrogen production and 0 otherwise | |

| Blue hydrogen production | BLUE | Dummy equals 1 if a company is engaged in blue hydrogen production and 0 otherwise | |

| Gray hydrogen production | GRAY | Dummy equals 1 if a company is engaged in gray hydrogen production and 0 otherwise | |

| Control | Company size | SIZE | ln(Total assets) |

| Company growth | GROW | (Sales revenue for the year − Sales revenue of the previous year)/Sales revenue of the previous year | |

| Current Ratio | CR | Current assets/Current liabilities | |

| Financial structure | FSTR | Total debt/Total assets |

| Variable | Mean | Median | Minimum | Maximum | Std. dev. |

|---|---|---|---|---|---|

| ROA | −0.031 | 0.012 | −1.604 | 0.985 | 0.282 |

| MV/BV | 2.693 | 1.005 | −12.734 | 47.906 | 7.151 |

| SIZE | 7822.786 | 131.574 | 1.225 | 253,245.800 | 32,978.859 |

| GROW | 0.156 | 0.063 | −0.081 | 7.212 | 0.962 |

| CR | 4.246 | 1.371 | 0.031 | 93.385 | 11.602 |

| FSTR | 0.605 | 0.520 | 0.001 | 6.282 | 0.7671 |

| Variables | ROA | MV/BV | SIZE | GROW | CR | FSTR |

|---|---|---|---|---|---|---|

| ROA | 1.000 | |||||

| MV/BV | −0.086 *** | 1.000 | ||||

| SIZE | 0.443 *** | −0.170*** | 1.000 | |||

| GROW | −0.051 * | 0.098 *** | −0.02 | 1.000 | ||

| CR | −0.006 | −0.016 | 0.132 *** | 0.075 ** | 1.000 | |

| FSTR | −0.335 *** | −0.075 ** | 0.151 *** | −0.024 | −0.201 *** | 1.000 |

| Model | Baseline Regression | With Control Variables | ||||||

|---|---|---|---|---|---|---|---|---|

| (1) | (1) | |||||||

| β | Std. Err. | t-Stat. | p-Value | β | Std. Err. | t-Stat. | p-Value | |

| HYDRO | −0.151 | 0.027 | −5.511 | 0.005 | −0.150 | 0.012 | −12.194 | 0.000 |

| SIZE | – | – | – | – | 0.044 | 0.002 | 26.369 | 0.000 |

| GROW | – | – | – | – | −0.001 | 0.001 | −0.766 | 0.086 |

| CR | – | – | – | – | 0.0010 | 0.000 | 1.240 | 0.083 |

| FSTR | – | – | – | – | −0.109 | 0.019 | −5.806 | 0.004 |

| ε | −0.089 | 0.012 | −7.745 | 0.002 | −0.232 | 0.031 | −7.533 | 0.002 |

| Country FEs | Yes | Yes | ||||||

| Year FEs | Yes | Yes | ||||||

| F-stat. (p-value) | 8.539 (0.000) | 27.018 (0.000) | ||||||

| Adj. R2 | 0.180 | 0.454 | ||||||

| N | 1440 | 1440 | ||||||

| Model | Baseline Regression | With Control Variables | ||||||

|---|---|---|---|---|---|---|---|---|

| (2) | (2) | |||||||

| β | Std. Err. | t-Stat. | p-Value | β | Std. Err. | t-Stat. | p-Value | |

| PROD | −0.178 | 0.026 | −5.405 | 0.006 | −0.155 | 0.011 | −14.274 | 0.000 |

| STOR | −0.141 | 0.032 | −5.527 | 0.005 | −0.137 | 0.023 | −5.997 | 0.004 |

| SIZE | – | – | – | – | 0.044 | 0.002 | 26.607 | 0.000 |

| GROW | – | – | – | – | −0.001 | 0.001 | −0.771 | 0.084 |

| CR | – | – | – | – | 0.000 | 0.000 | 1.240 | 0.083 |

| FSTR | – | – | – | – | −0.109 | 0.019 | −5.803 | 0.004 |

| ε | −0.089 | 0.012 | −7.739 | 0.002 | −0.232 | 0.031 | −7.578 | 0.002 |

| Country FEs | Yes | Yes | ||||||

| Year FEs | Yes | Yes | ||||||

| F-stat. (p-value) | 8.347 (0.000) | 26.431 (0.000) | ||||||

| Adj. R2 | 0.180 | 0.454 | ||||||

| N | 1440 | 1440 | ||||||

| Model | Baseline Regression | With Control Variables | ||||||

|---|---|---|---|---|---|---|---|---|

| (3) | (3) | |||||||

| β | Std. Err. | t-Stat. | p-Value | β | Std. Err. | t-Stat. | p-Value | |

| GREEN | −0.193 | 0.042 | −4.602 | 0.010 | −0.168 | 0.020 | −8.195 | 0.001 |

| BLUE | −0.018 | 0.022 | −0.819 | 0.059 | −0.105 | 0.028 | −3.807 | 0.019 |

| GRAY | −0.072 | 0.008 | −8.800 | 0.001 | −0.143 | 0.008 | −17.747 | 0.000 |

| SIZE | – | – | – | – | 0.044 | 0.002 | 28.275 | 0.000 |

| GROW | – | – | – | – | −0.001 | 0.001 | −0.870 | 0.433 |

| CR | – | – | – | – | 0.000 | 0.000 | 1.251 | 0.279 |

| FSTR | – | – | – | – | −0.108 | 0.018 | −5.888 | 0.004 |

| ε | −0.093 | 0.012 | −7.785 | 0.002 | −0.237 | 0.030 | −7.929 | 0.001 |

| Country FEs | Yes | Yes | ||||||

| Year FEs | Yes | Yes | ||||||

| F-stat. (p-value) | 8.018 (0.000) | 25.408 (0.000) | ||||||

| Adj. R2 | 0.177 | 0.449 | ||||||

| N | 1440 | 1440 | ||||||

| Model | Baseline Regression | With Control Variables | ||||||

|---|---|---|---|---|---|---|---|---|

| (4) | (4) | |||||||

| β | Std. Err. | t-Stat. | p-Value | β | Std. Err. | t-Stat. | p-Value | |

| HYDRO | 4.454 | 0.808 | 5.515 | 0.005 | 3.604 | 0.841 | 4.287 | 0.013 |

| SIZE | – | – | – | – | −0.508 | 0.064 | −7.988 | 0.001 |

| GROW | – | – | – | – | 0.962 | 0.457 | 2.105 | 0.093 |

| CR | – | – | – | – | −0.043 | 0.005 | −7.953 | 0.001 |

| FSTR | – | – | – | – | −0.903 | 0.061 | −14.875 | 0.000 |

| ε | 1.390 | 0.230 | 6.055 | 0.004 | 4.274 | 0.525 | 8.145 | 0.001 |

| Country FEs | Yes | Yes | ||||||

| Year FEs | Yes | Yes | ||||||

| F-stat. (p-value) | 4.100 (0.000) | 5.815 (0.000) | ||||||

| Adjusted R2 | 0.083 | 0.133 | ||||||

| N | 1440 | 1440 | ||||||

| Model | Baseline Regression | With Control Variables | ||||||

|---|---|---|---|---|---|---|---|---|

| (5) | (5) | |||||||

| β | Std. Err. | t-Stat. | p-Value | β | Std. Err. | t-Stat. | p-Value | |

| PROD | 2.984 | 0.846 | 3.526 | 0.024 | 2.737 | 0.750 | 3.648 | 0.022 |

| STOR | 8.352 | 3.111 | 2.685 | 0.055 | 7.568 | 3.047 | 2.484 | 0.068 |

| SIZE | – | – | – | – | −0.525 | 0.067 | −7.883 | 0.001 |

| GROW | – | – | – | – | 0.042 | 0.021 | 1.953 | 0.093 |

| CR | – | – | – | – | −0.044 | 0.005 | −8.312 | 0.001 |

| FSTR | – | – | – | – | −1.019 | 0.098 | −10.390 | 0.001 |

| ε | 1.384 | 0.233 | 5.930 | 0.004 | 4.619 | 0.401 | 11.505 | 0.000 |

| Country FEs | Yes | Yes | ||||||

| Year FEs | Yes | Yes | ||||||

| F-stat. (p-value) | 4.336 (0.000) | 5.552 (0.000) | ||||||

| Adj. R2 | 0.091 | 0.129 | ||||||

| N | 1440 | 1440 | ||||||

| Model | Baseline Regression | With Control Variables | ||||||

|---|---|---|---|---|---|---|---|---|

| (6) | (6) | |||||||

| β | Std. Err. | t-Stat. | p-Value | β | Std. Err. | t-Stat. | p-Value | |

| GREEN | 3.379 | 1.223 | 2.763 | 0.051 | 2.974 | 1.114 | 2.221 | 0.091 |

| BLUE | 1.841 | 0.543 | 3.388 | 0.028 | 2.455 | 0.480 | 6.156 | 0.004 |

| GRAY | 0.968 | 1.020 | 0.950 | 0.396 | 1.556 | 0.922 | 1.688 | 0.097 |

| SIZE | – | – | – | – | −0.559 | 0.054 | −10.337 | 0.001 |

| GROW | – | – | – | – | 0.044 | 0.021 | 2.128 | 0.100 |

| CR | – | – | – | – | −0.045 | 0.005 | −8.953 | 0.001 |

| FSTR | – | – | – | – | −1.077 | 0.097 | −11.089 | 0.000 |

| ε | 1.610 | 0.159 | 10.125 | 0.001 | 5.032 | 0.228 | 22.072 | 0.000 |

| Country FEs | Yes | Yes | ||||||

| Year FEs | Yes | Yes | ||||||

| F-statistics (p-value) | 3.187 (0.000) | 4.510 (0.000) | ||||||

| Adj. R2 | 0.063 | 0.105 | ||||||

| N | 1440 | 1440 | ||||||

| Model | Dependent Variable: ROE | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | ||||||||||

| β | Std. Err. | t-Stat. | p-Value | β | Std. Err. | t-Stat. | p-Value | β | Std. Err. | t-Stat. | p-Value | |

| HYDRO | −0.244 | 0.052 | −4.679 | 0.010 | – | – | – | – | – | – | – | – |

| PROD | – | – | – | – | −0.247 | 0.137 | −1.803 | 0.146 | – | – | – | – |

| STOR | – | – | – | – | −0.236 | 0.270 | −0.872 | 0.432 | – | – | – | – |

| GREEN | – | – | – | – | – | – | – | – | −0.240 | 0.204 | −1.178 | 0.304 |

| BLUE | – | – | – | – | – | – | – | – | −0.226 | 0.074 | −3.072 | 0.037 |

| GRAY | – | – | – | – | – | – | – | – | −0.301 | 0.049 | −6.166 | 0.004 |

| Error term | Yes | Yes | Yes | |||||||||

| Control variables | Yes | Yes | Yes | |||||||||

| Country FEs | Yes | Yes | Yes | |||||||||

| Year FEs | Yes | Yes | Yes | |||||||||

| F-stat. (p-value) | 3.761 (0.000) | 3.678 (0.000) | 3.550 (0.000) | |||||||||

| Adj R2 | 0.081 | 0.080 | 0.078 | |||||||||

| N | 1440 | 1440 | 1440 | |||||||||

| Model | Dependent Variable: TQ | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (4) | (5) | (6) | ||||||||||

| β | Std. Err. | t-Stat. | p-Value | β | Std. Err. | t-Stat. | p-Value | β | Std. Err. | t-Stat. | p-Value | |

| HYDRO | 2.407 | 0.302 | 7.960 | 0.001 | – | – | – | – | – | – | – | – |

| PROD | – | – | – | – | 2.059 | 0.396 | 5.199 | 0.007 | – | – | – | – |

| STOR | – | – | – | – | 3.334 | 0.170 | 19.638 | 0.000 | – | – | – | – |

| GREEN | – | – | – | – | – | – | – | – | 2.205 | 0.498 | 4.431 | 0.011 |

| BLUE | – | – | – | – | – | – | – | – | 1.437 | 0.237 | 6.056 | 0.004 |

| GRAY | – | – | – | – | – | – | – | – | 1.249 | 0.218 | 5.738 | 0.005 |

| Error term | Yes | Yes | Yes | |||||||||

| Control variables | Yes | Yes | Yes | |||||||||

| Country FEs | Yes | Yes | Yes | |||||||||

| Year FEs | Yes | Yes | Yes | |||||||||

| F-stat. (p-value) | 14.308 (0.000) | 14.168 (0.000) | 12.396 (0.000) | |||||||||

| Adj R2 | 0.298 | 0.301 | 0.275 | |||||||||

| N | 1440 | 1440 | 1440 | |||||||||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chmiela, A.; Gawęda, A.; Barszczowska, B.; Howaniec, N.; Pysz, A.; Smoliński, A. The Financial Results of Energy Sector Companies in Europe and Their Involvement in Hydrogen Production. Energies 2025, 18, 3385. https://doi.org/10.3390/en18133385

Chmiela A, Gawęda A, Barszczowska B, Howaniec N, Pysz A, Smoliński A. The Financial Results of Energy Sector Companies in Europe and Their Involvement in Hydrogen Production. Energies. 2025; 18(13):3385. https://doi.org/10.3390/en18133385

Chicago/Turabian StyleChmiela, Andrzej, Adrian Gawęda, Beata Barszczowska, Natalia Howaniec, Adrian Pysz, and Adam Smoliński. 2025. "The Financial Results of Energy Sector Companies in Europe and Their Involvement in Hydrogen Production" Energies 18, no. 13: 3385. https://doi.org/10.3390/en18133385

APA StyleChmiela, A., Gawęda, A., Barszczowska, B., Howaniec, N., Pysz, A., & Smoliński, A. (2025). The Financial Results of Energy Sector Companies in Europe and Their Involvement in Hydrogen Production. Energies, 18(13), 3385. https://doi.org/10.3390/en18133385