Abstract

This study investigates the relationship between disclosures related to Sustainable Development Goal 7 (SDG 7) and the financial profitability of Romanian commercial banks during the 2017–2023 period. Using an unbalanced panel dataset of 17 banks and applying fixed-effects regression models, the paper examines how transparency around energy-related sustainability practices influences various dimensions of bank profitability: recurring earning power (REP), loan yield (LY), return on assets (ROA), and return on equity (ROE). Macroeconomic energy indicators, such as the energy intensity level of primary energy (EnInt) and renewable energy consumption (REnC), are also controlled for. The findings indicate that SDG 7.1 disclosures are negatively associated with all profitability measures, except for LY, suggesting potential short-term trade-offs between sustainability transparency and financial outcomes. In contrast, SDG 7.2 disclosures positively impact REP, ROA, and ROE, underscoring the financial relevance of renewable energy financing. SDG 7.a disclosures show no significant relationship with profitability, indicating limited operational involvement in global energy cooperation. Additionally, higher energy intensity negatively affects REP and LY, supporting existing evidence that energy efficiency improves banking performance. These findings have implications for banking strategy, emphasizing the need to align sustainability disclosures with business priorities while recognizing the long-term benefits of green finance and energy efficiency.

1. Introduction

Sustainability has become increasingly important in the business world, emerging as a decisive factor in evaluating a financial success in business [1]. The development of the energy system through innovation and the assurance of energy security are central themes in the debates on sustainable development, aligning with global commitments outlined in the United Nations 2030 Agenda for Sustainable Development, the Paris Agreement on climate change, and the European Union’s goal of achieving climate neutrality (net-zero greenhouse gas emissions) by 2050.

Access to energy is a prerequisite for economic development, without which economic, social, and environmental disparities are perpetuated [2]. Faced with the challenges confronting the planet, the United Nations established SDG 7, “Affordable and Clean Energy,” defining specific targets (7.1, 7.2, 7.3, 7.a, 7.b) and corresponding indicators as part of a global plan to ensure universal access to reliable energy services and affordable clean energy by 2030. Enhancing energy efficiency, replacing fossil fuels (“black energy”) with renewable energy sources (such as wind, solar, hydro, geothermal, and biomass), “strengthening international cooperation to facilitate access to clean energy research and technology,” and “expanding infrastructure and upgrading technology for providing modern and sustainable energy services in developing countries” are viewed as potential solutions for the global transition to low-carbon green energy systems and for addressing global climate change [3]. Thus, SDG 7 underscores the urgent need for all United Nations member states to develop and implement policies, initiatives, and investments in energy infrastructure and clean energy technologies to ensure equitable access to modern energy sources. Zarghami [4], in a study involving 41 OECD and European countries, highlights among the various combinations of economic policies contributing to the achievement of SDG 7 targets the role of government initiatives in implementing international financial regulations—such as tax exemptions, financial incentives, low-interest green mortgages, and financial support for research and technological development in the field of renewable energy—as mechanisms to facilitate energy investments.

As financial intermediaries, banks play a key role in shaping the future of sustainable energy worldwide, bearing the responsibility of supporting the ongoing sustainable “energy revolution” in the EU by financing projects aligned with SDG 7. At the request of regulatory and supervisory authorities, banks integrate sustainability dimensions—including SDG 7—into their risk management and governance frameworks. This integration should be reflected in improved banking performance, reduced systemic risks associated with energy insecurity, and increased borrower and market resilience, all of which confer legitimacy benefits to the banks involved. According to Ozili [5], bank engagement in SDG-related actions is beneficial to the institutions themselves, as it opens opportunities to lend to new markets and offer fee-based services, ultimately enhancing banking profitability. Wu and Broadstock [6] emphasize the ability of banks to mitigate information asymmetry based on their knowledge of clients (borrowers/lenders) and to redirect financing from less energy-efficient and non-renewable energy projects towards renewable energy investments. This can result in lower business operating costs, improved efficiency, and reduced risks associated with renewable energy projects. The potential benefits anticipated by banks are contingent, among other factors, upon the degree of transparency with which they disclose to stakeholders their involvement in financing the transition toward energy-efficient systems aimed at achieving the targets of SDG 7 and, consequently, enhancing societal well-being.

This study contributes to existing literature in three ways. Firstly, despite the increasing relevance of this topic, there is a relative paucity of research exploring how the reporting of progress toward the Sustainable Development Goals—particularly in the banking sector—may influence financial performance [7,8,9,10,11,12]. The majority of existing studies have focused on SDG-related reporting within non-financial corporations. Given the important role of banks in achieving the SDGs by financing sustainable initiatives and facilitating access to financial resources for responsible economic and social development, more studies are needed to shed more light on the relationship between reporting information on SDG achievement and bank financial performance.

Secondly, less attention has been paid to SDG reporting in developing countries. These countries have different corporate reporting systems, experiencing delays in integrating the concept of sustainability into basic management and reporting practices [13]. Eastern European companies, including banks, have been involved in sustainability reporting later and less than those in developed countries, which makes sustainability reporting inferior in terms of the quantity and quality of information disclosed [14]. More studies are therefore needed to help policy makers and bank managers catch up on this gap.

Thirdly, research specifically examining the impact of SDG 7 reporting on banking performance remains significantly underrepresented in the recent literature [15,16]. This research conducted on 17 Romanian commercial banks during the 2017–2023 period aims to contribute to filling the existing gap in the academic literature regarding the potential interdependencies between banks’ reporting on their involvement in achieving SDG 7 targets and their financial performance. Therefore, the study of sustainability initiatives within the banking sector of emerging countries—where investments for the transition to a healthier energy future far exceed public financing capacity—represents a topic of interest in the global effort to achieve SDG 7.

Beyond this introductory overview of the importance and timeliness of the subject under discussion, the structure of the paper includes a literature review section, which forms the basis for the research hypotheses; the research methodology, describing the data sources and the variables involved in the developed models; a discussion of the results, including robustness checks; and a summary of conclusions, implications, and limitations of the present study.

2. Literature Review and Development of Research Hypotheses

2.1. Theoretical Framework

Literature explaining the motivations behind sustainability reporting by banks and other companies is based on several theories, such as stakeholder theory, resource dependency theory, agency theory, and legitimacy theory. Therefore, these studies use multi-theoretical analysis as a conceptual framework.

Stakeholder theory, seen as a lens through which the relationship between the organization and stakeholders is analyzed [17], postulates that corporations should not only take into account the interests of the most important and powerful stakeholders, the shareholders, but must balance the conflicting interests of all of them [18,19,20,21]. Disclosure of non-financial information related to their environmental and social performance demonstrates a focus on diverse stakeholders and consideration of the needs and expectations of non-financial ones. Reporting SDG information shows the organization’s responsibility for social well-being and environmental care, alignment with social and environmental ethics, and the desire to gain the trust and approval of various stakeholders [17,21,22,23]. Buniamin et al., 2021 [24] state that the disclosure of energy-related information based on SDG 7 is evidence of corporate responsibility and communication to achieve the well-being of various stakeholder groups.

According to resource dependency theory, companies rely on external resources to survive and grow [18]. Acquiring strategic external resources influences economic, social, and environmental performance; increases efficiency, and enables firms to engage in sustainable practices. Providing information about the SDGs can be a valid way to obtain vital external sources of resources, which provide legitimacy and competitive advantages to banks [17]. Agency theory plays a critical role in overseeing and regulating managerial actions taken on behalf of shareholders (as principals) [18]. By providing information about SDGs, it leads to the reduction in information asymmetry between the principals and managers (agents), which ensures trust and transparency [22]. SDG reporting allows managers to align their interests with those of stakeholders, improving banks’ reputation and reducing agency costs of monitoring [20].

Legitimacy theory suggests that businesses should align their practices with the values, norms, and social expectations of the communities they serve, thereby conveying to stakeholders their commitment to meeting societal expectations [17,20]. As per [1], legitimacy theory serves as a framework for evaluating voluntary disclosure practices, guiding companies in their decisions to voluntarily share environmental and social information with stakeholders. Datta and Goyal, 2022 [19] explain that legitimacy is a social contract between a company and society, which obliges the company to adhere to social and cultural norms. Accordingly, banks disclose details about the adoption and implementation of the SDGs, demonstrating that they operate in a socially and environmentally responsible manner, in line with societal expectations [20].

2.2. Bank Profitability and SDG Reporting

The debate on sustainable business practices has the banking sector at the center of attention due to its role in directing financial resources towards sustainable activities. In this context, the question that arises goes beyond the practical implications of sustainability practices on the economy and businesses and focuses on the banks themselves and the impact of sustainable financing on their performance. Bank performance, usually operationalized through profitability measures like return on assets (ROA), return on equity (ROE), and net interest margin (NIM) [10], is considered to decisively influence their ability to finance sustainable investments. The literature tries to answer the question: does sustainable finance contribute to achieving the SDGs but also to making profits for banks? On a sample of 713 banks from 75 countries during 2013–2015, Nizam et al., 2019, [25] find that if banks increase their financing for projects with environmental impact, they are likely to improve their financial performance measured by ROE. By conducting a panel analysis of bank data from 48 countries, Torre Olmo et al., 2021 [26] find that banks that adopt sustainable practices, by adhering to the UNEP Finance Initiative’s Principles for Responsible Banking, have higher profitability and lower risk profiles, which justifies the focus on sustainability to increase profitability and maintain operational efficiency. Chen et al., 2024 [16] note that promoting investments in sustainable energy improves the profitability of the banking industry, making it necessary to expand green lending operations, as a functioning credit market is indispensable, especially in regions with limited access to energy. Chen et al., 2023 [27], on a sample of banks in BRICS countries, for the period 2011–2021, conclude that banks heavily involved in renewable investments show improved profitability and greater loan portfolio stability, which is an encouraging signal for making increasing renewable financing a strategic priority. In the same vein, Choudhury et al., 2023 [15] state that banks that provide loans for renewable energy projects benefit from a lower risk of default because companies that adopt renewable energy solutions tend to be more profitable and have higher creditworthiness.

Another significant stream of the literature investigates the role of sustainability disclosures in improving bank performance. The study of Jan et al., 2019 [8] evaluates the link between sustainability efforts (measured through disclosure scores) and financial profitability of Islamic banks from three perspectives: management, shareholders, and market. Their results reveal a significant positive relationship with financial performance, especially from the management (ROA) and shareholders (ROE) perspectives. This validates the stakeholder’s theory, which assumes a positive connection between sustainability practices and financial performance. A study by Jan et al., 2023 [11] assesses the impact of corporate sustainability practices (CSP) of Islamic banks in Malaysia and Indonesia on financial performance (ROA and ROE). The findings show that CSP has a significant positive effect on ROA and ROE, while economic sustainability positively influences ROA and ROE in Indonesia but has no significant impact in Malaysia. Environmental sustainability positively affects ROA and ROE, and social sustainability has no significant impact. The study conducted by Buallay et al., 2023 [9] examines the relationship between the levels of sustainability reporting (measured by ESG score) and the performance of banks and financial services (ROA, ROE, and Tobin’s Q) in 60 countries over the period 2008–2017, documenting a negative relationship between ESG scores and operational, financial, and market performance.

Another branch of literature explores how disclosures on the achievement of the Sustainable Development Goals (SDGs) contribute to enhancing bank performance, emphasizing that a high quality of disclosures also implies good progress towards attaining the SDGs [10]. A study by Ozili, 2023 [10] examines the impact of achieving certain SDGs on the profitability of banks in 28 countries. The results show that some SDGs, such as promoting health and well-being, can increase net interest income, while others, such as combating climate change, can decrease return on assets. In addition, increasing the quality of education and promoting clean and affordable energy sources (SDG 7) positively impact return on equity. Galeazzo et al., 2024 [28] examine how companies (including banks) respond to institutional pressures to engage with the SDGs (based on different SDG disclosure measures) and the financial implications of such engagement. Analyzing data from the 100 most sustainable companies globally (2017–2020), the study finds that financial performance (ROA) generally improves only when companies engage with either the full set of SDGs or a frequently cited subset, but environmental SDGs (which include SDG 7) do not have a positive and significant impact on ROA.

In the context of these mixed results from the literature, it is hypothesized that there is a significant relationship between the disclosure of energy-related SDG7 information and the financial performance of Romanian banks, without making a priori statements on the sign of this relationship.

H1.

There is a significant impact of the disclosures of SDG7-related information on affordable and clean energy on the financial profitability of Romanian banks.

This main hypothesis can be further developed to consider each profitability measure separately.

H1a.

There is a significant impact of the disclosures of SDG7-related information on affordable and clean energy on the recurring earning power (REP) of Romanian banks.

H1b.

There is a significant impact of the disclosures of SDG7-related information on affordable and clean energy on the loan yield (LY) of Romanian banks.

H1c.

There is a significant impact of the disclosures of SDG7-related information on affordable and clean energy on the management performance (ROA) of Romanian banks.

H1d.

There is a significant impact of the disclosures of SDG7-related information on affordable and clean energy on the stockholders’ performance (ROE) of Romanian banks.

3. Research Methodology

This section details the data sources and the sample, as well as the variables used in the models.

3.1. Data Sources and Sample

The analyzed sample included 17 commercial banks, out of a total of 21, according to the 2023 Annual Report of the National Bank of Romania, for which non-financial reports were available [29], four banks being eliminated precisely for lack of information. The analyzed period began with 2017, the first year of application by Romanian banks of the European regulations on non-financial reporting and spanned seven years (2023 included). The final number of annual observations was 110, the sample being unbalanced. After constructing the lead structure for the dependent variables (t + 1), the final estimation sample used in all regression models included 93 complete year-pairs, which ensures full alignment between dependent and independent variables. Of the 17 banks in the sample, four had majority Romanian capital in 2023 (24%), and two were state owned (12%). Also, of the 110 annual observations, 48% came from banks with foreign capital, 37% had mixed capital, and 15% had Romanian capital.

Non-financial data were collected through manual content analysis conducted by the authors. To capture the nuanced and context-specific nature of sustainability disclosures, manual content analysis is employed. Each researcher independently reviewed all reports twice, with no significant differences between the two rounds. Subsequently, the reports were cross-checked by a second researcher, and any discrepancies were resolved through consultation with a third reviewer. This multi-step process was designed to enhance the reliability and consistency of the coding, ensuring a rigorous and transparent evaluation of the qualitative content. Financial data were downloaded from BankFocus—Bureau van Dijk and Moody’s Analytics databases—and the macroeconomic data on energy-related indicators from the WorldBank databases.

3.2. Variables and Models

3.2.1. Dependent and Independent Variables

The variables used to capture the financial performance of banks are accounting-based measures [9]. Market-based measures could not be used as only three Romanian banks are listed. Thus, banking performance is depicted by the following profitability metrics:

- Recurring earning power (REP), computed as pre-impairment operating earnings over total assets, shows the bank’s ability to achieve profitability in a constant and sustainable manner, avoiding risks related to profitability [30]. The lack of risk exposure is highlighted in the numerator of the indicator, which takes into account pre-impairment operating profit. This rate is used in the literature as a proxy for earnings stability because it assumes that all current operating conditions remain constant [31,32].

- Loans yield (LY), calculated as net interest income over net loans, is a profitability measure that shows a bank’s ability to generate earnings from its lending activities [30]. Indicators that take into account net interest income are considered a more robust performance measure, superior to alternative ratios such as ROA and ROE, because they assess the efficiency of banks’ use of their interest-bearing assets [27]. Conversely, ROA and ROE represent the overall performance that encompasses both loans and market investments.

- Return on assets (ROA), extensively used in the literature to capture management performance [8,33,34,35], is calculated as total net income over total assets. A high ROA helps strengthen the bank’s reputation, which attracts new depositors and borrowers, reduces early withdrawals, and increases working capital by using accumulated profits [36].

- Return on equity (ROE), calculated as net income over equity, shows the return to stockholders and is influenced by leverage [22,24,35,37,38]. Unlike ROA, which is influenced solely by the income-generating capacity of assets, ROE is also affected by the methods used to finance these assets [26] and shows stockholders’ perspective [8].

The reporting of information on the progress in achieving SDG 7 by Romanian banks was analyzed from a quantitative and qualitative perspective through four of the five SDG 7-associated targets, respectively 7.1, 7.2, 7.3, and 7.a. These were selected considering the specifics of banking activity as a financial intermediary of companies investing in energy structure and clean energy technology, but also as an energy consumer. Content analysis of sustainability reports, a methodology widely used in studies that assess the level and quality of disclosures about the SDGs [23,28], allowed the coding of narrative data with 1 point and numerical data with 2 points, as well as 0 points for no data, in accordance with other papers [8,39]. Thus, reporting scores (RS) were calculated for each target. These scores represent the main independent variables in the models developed based on Equations (1)–(3).

The control variables included in the models, after careful analysis of the existing literature, include:

- indicators related to energy consumption (REnC) and energy intensity level of primary energy (EnInt). Renewable energy consumption is the share of total energy consumption, while the energy intensity level of primary energy (EnInt) is the ratio between energy supply and gross domestic product measured at purchasing power parity. They are also used in other studies such as [15,40,41,42] and have a mixed impact on bank profitability;

- bank size (size), calculated as the logarithm of total assets [20], is a good indicator of the adaptation of banks’ balance sheets to sustainable development, with larger banks expected to have more resources to transition to renewable energy and be subject to more pressure from stakeholders to implement the SDGs [35]. However, the current literature has not agreed on the type of influence exerted by size, which has an uncertain impact [26,35,43,44];

- deposit-taking activity (DA), determined as total deposits over total assets, is expected to have a positive effect on financial performance [38,43], as deposits are a cheap and stable financial resource when compared to other financing alternatives [44]. However, government-provided insurance protections make deposit demand a significant contributor to agency problems, which might negatively affect profitability [44];

- banking corporate governance structures (CEO gender—CEO and shareholder structure—own). CEO is a dummy variable, coded as 1 when the CEO is a female and 0 otherwise, and is expected to have a mixed impact, based on existing literature [45,46]. Own is a categorical variable, with 3 categories: 1—Romanian ownership, 2—foreign ownership, and 3—mixed ownership. It is expected from foreign investors to show greater concern and to demand more transparency from the companies in which they have invested [18].

To verify the robustness of the model and capture the multidimensional nature of bank financial performance, a composite index was calculated by including all four individual variables used in the paper (REP, LY, ROA, and ROE) and following the methodology described by Mazziotta and Pareto (2017) [47]. This process involved the normalization of the four individual variables, necessary to eliminate fluctuations in the indicators’ values [48], through standardization (Z scores). Principal component analysis (PCA) was used to aggregate the normalized values [47]. The adequacy of the PCA method was verified by applying the Kaiser–Meyer–Olkin statistical test. A value of 0.758 was obtained, which is considered acceptable [49]. The weighing of the individual indicators was made by using the first component (with an eigenvalue greater than 1), which explained 79.23% of the variation in the original variables. Finally, the internal consistency and reliability of the index obtained was validated using Cronbach’s alpha, with a value of 0.9084, above the threshold of 0.80, considered very good for empirical studies [50]. The composite index was then used as the dependent variable in the model in Equation (1).

For more robustness checks, the share of women directors in the board of directors (WBoD) and capital ratio (CpR) are used as control variables. Several studies [17,18,45] show that female board members (WBoD) reduce information asymmetry, contribute new perspectives and skills, and increase the board’s focus on stakeholders, thereby influencing corporate engagement with the SDGs and promoting greater transparency. CpR, calculated as book value of equity capital divided by total assets [44] and serving as an inverse measure of leverage, is a bank-specific determinant that may also be partly influenced by the regulatory framework [44]. It is expected to positively impact profitability [22,34].

3.2.2. Models

Four models are developed based on Equation (1) to capture the financial performance of banks based on four proxies.

where y = the dependent variable, which measures bank financial performance (REP, LY, ROA, ROE), t = the period of time (year); i = the bank at time t; SDG7_1, SDG7_2, SDG7_a = disclosure scores for 3 of the goals related to SDG7 selected in this paper. EnInt = Energy Intensity level of primary energy; REnC = renewable energy consumption; size = bank size; DA = ratio of total deposits over total assets; own = ownership structure; CEO = gender of CEO; year fixed effects (δt), which capture unobserved macroeconomic shocks or institutional factors affecting all banks in a given year; the error term (εit) that captures unobserved, time-varying factors that affect the financial performance of each bank but are not included among the explanatory variables.

yit+1 = α0 + α1 × SDG7_1it + α2 × SDG7_2it + α3 × SDG7_ait + α4 × EnIntit + α5 × REnCit + α6 × Sizeit + α7 × DAit + α8 × Ownit + α9 × CEOit + δt + εit,

A robustness test based on Equation (1) is applied to verify the consistency of the results by replacing the dependent variables with the composite index of bank performance (fpc), which combines all four profitability measures into a single variable.

For further robustness checks, Equations (2) and (3) are applied:

where WBoD is the share of women directors in the Board of Directors.

where CpR is the capital ratio.

yit+1 = α0 + α1 × SDG7_1it + α2 × SDG7_2it + α3 × SDG7_ait + α4 × EnIntit + α5 × REnCit + α6 × Sizeit + α7 × DAit + α8 × Ownit + α9 × CEOit + α10 × WBoDit + δt + εit,

yit+1 = α0 + α1 × SDG7_1it + α2 × SDG7_2it + α3 × SDG7_ait + α4 × EnIntit + α5 × REnCit + α6 × Sizeit + α7 × DAit + α8 × CpRit + δt + εit,

A fixed-effect estimation was used in panel data regression analysis, based on the results of the Hausman test. For reasons of collinearity, only three of the four analyzed targets (7.1, 7.2, and 7.a) are included in the models. Following [28], the dependent variable is forwarded by one year to reflect the causal impact of SDG disclosure in year t on the observed financial performance in year t + 1. This structure reflects the assumption that sustainability disclosures in a given year influence bank financial performance in the subsequent year. To maintain strict one-to-one correspondence between predictors and outcomes, any observations with missing dependent variable values at time t + 1 were excluded. Corresponding independent variables from year t were also removed in such cases to preserve temporal consistency and panel integrity. This procedure ensures that the data structure supports causal interpretation and prevents bias from mismatched or incomplete year-pairs.

To account for unobserved heterogeneity across time and to control for macroeconomic shocks or institutional changes that may influence bank performance, year dummies (2017–2023) are included in all model specifications. These time-fixed effects help isolate the impact of the explanatory variables by absorbing year-specific influences such as policy shifts, economic crises, or global events like the COVID-19 pandemic and the energy crisis, thereby enhancing the robustness and interpretability of the regression results.

4. Results

This section presents descriptive statistics, correlations, and empirical analyses.

4.1. Descriptive Analysis and Correlation Matrix

Table 1 and Table 2 show the descriptive statistics. Note that the number of observations differs between the variables because the dependent variable is specified as a lead (year t + 1) variable.

Table 1.

Descriptive statistics.

Before commenting on the results in Table 2, it is important to briefly describe the background of the research: the Romanian banking system. Official data from the National Bank of Romania for the period 2017–2023 show that the Romanian banking sector has experienced constant growth and stability, but also a good capacity to adapt to economic fluctuations and regulatory changes. During this period, total assets doubled, demonstrating the sustained expansion of lending and investment activities; profitability, measured by ROA and ROE, increased, driven by improved digitalization practices [51]; and asset quality increased due to the lowering of the non-performing loan rate (2.46% in 2023), because of effective risk management strategies [27]. The ownership structure was predominantly foreign, with international banks holding over 75% of total assets [27]. The presence of foreign shareholders is considered to have a positive effect on the adoption of corporate governance and sustainability practices, but also on the transparency of sustainability reports [18,52]. Thus, Zyznarska-Dworczak et al. (2023) [13], in a study on three Eastern European countries, found a significant improvement in the efficiency of Romanian banks in terms of social and environmental performance but showed that there were still important steps to be taken to integrate sustainability into banking operations. Progress is also needed in sustainability reporting. Recent studies [53] document that information provided by the sustainability reports of Romanian banks suffers in terms of comparability of content, level of detail, and numerical indicators used, with an emphasis on the presentation of philanthropic and charitable activities made rather for marketing purposes than for real strategic transformation.

The descriptive statistics confirm this general evolution and provide more insight into the sample, reflecting a diverse and evolving banking sector in Romania, characterized by modest but steadily growing profitability, a reliance on deposit-based funding, limited engagement in sustainability reporting, and persistent gaps in gender diversity at the executive level. Profitability is measured through four distinct indicators, each capturing a different aspect of performance. The mean REP is 1.62, indicating that, on average, Romanian banks have maintained a relatively stable ability to generate sustainable pre-impairment earnings relative to their total assets. The LY, with a mean of 0.04, reflects a moderate capacity of banks to earn from their core lending operations. On average, for every monetary unit of net loans granted, Romanian banks generate 0.04 monetary units of net interest income. This indicator is particularly relevant in assessing efficiency in the use of interest-bearing assets, and its low standard deviation suggests consistency across the sector. In contrast, traditional profitability indicators such as ROA and ROE report lower mean values (0.01 and 0.09, respectively), with negative minimums indicating that a portion of the sample operated at a loss during the study period. Sustainability disclosure is captured through four SDG7-related targets—7.1, 7.2, 7.3, and 7.a. The content analysis reveals low overall reporting levels. Average scores for the four targets—SDG7_1 (0.80), SDG7_2 (0.97), SDG7_3 (0.87), and SDG7_a (0.67)—suggest that most banks provide either limited or narrative-only information, with few offering detailed quantitative disclosures.

The deposit-to-asset ratio (DA) averages 0.76, underscoring the banks’ heavy reliance on deposits as a primary funding source. While deposits are typically viewed as stable and cost-effective, this dependence also poses potential risks related to agency problems and moral hazard, especially in the context of government-backed deposit guarantees [54]. Bank size varies across the sample (mean = 16.61), indicating the inclusion of both medium and large institutions with differing capacities for sustainability investment. Based on Table 2, female representation in executive leadership (CEO) is notably low, with only 12.73% of banks in the sample led by female CEOs. This underrepresentation reflects broader gender imbalances in the Romanian financial sector [55]. Finally, the ownership structure (Own) ranges from domestic to foreign or mixed ownership, with the highest concentration in category 2, implying a strong presence of foreign capital, which is generally associated with higher transparency standards and greater stakeholder pressure for SDG compliance.

Table 2.

Descriptive statistics for categorical variables.

Table 2.

Descriptive statistics for categorical variables.

| Categories | 0 | 1 | 2 | 3 |

|---|---|---|---|---|

| CEO | ||||

| -frequency | 96 | 14 | ||

| -percentage | 87.27 | 12.73 | ||

| Own | ||||

| -frequency | 16 | 53 | 41 | |

| -percentage | 14.55 | 48.18 | 37.27 |

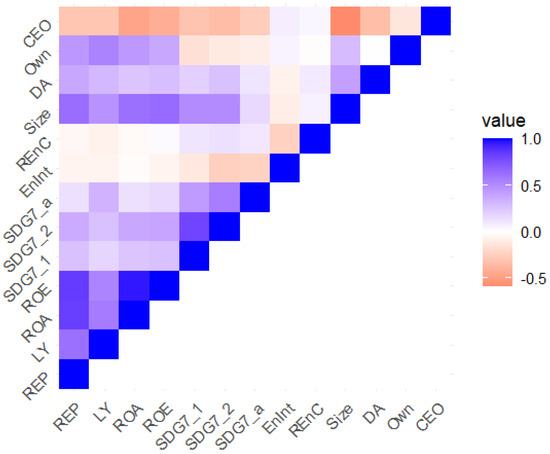

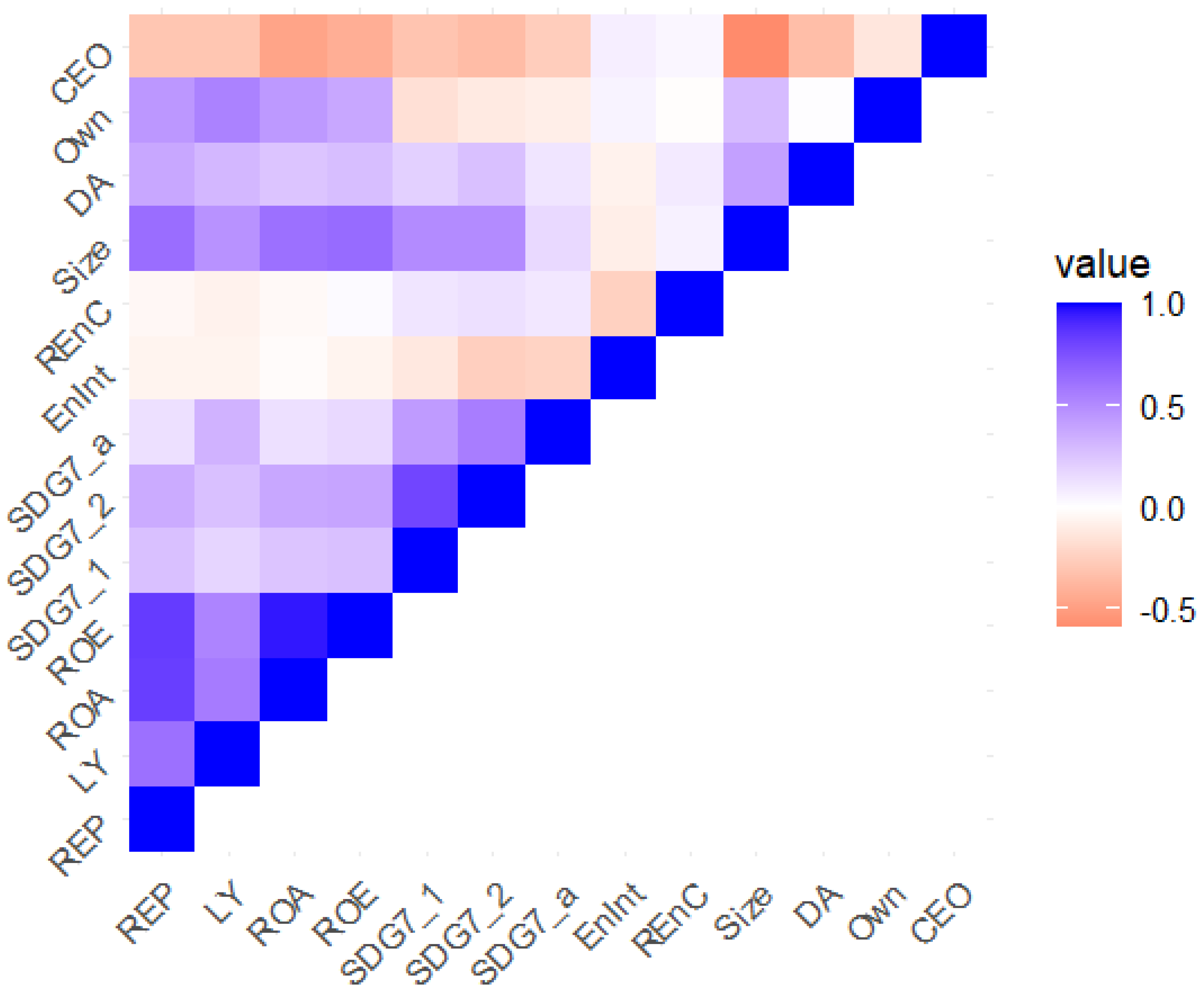

All correlation coefficients between variables remain below the 0.80 threshold (Figure 1 and Table A1), meaning that multi-collinearity is not a concern and ensuring the reliability of subsequent regression analysis.

Figure 1.

Correlation analysis.

Variance inflation factors (VIF) below the 5 threshold (Table 1) [56] support the Pearson’s correlation matrix.

4.2. Empirical Analysis

Table 3 presents the results of the fixed-effect estimation, based on Equation (1).

Table 3.

Results of the regression analysis.

Table 3.

Results of the regression analysis.

| Variables | REP | LY | ROA | ROE |

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| SDG7_1 | −0.4660 *** | −0.0026 | −0.0041 ** | −0.0272 * |

| SDG7_2 | 0.3115 ** | −0.0009 | 0.0032 ** | 0.0208 * |

| SDG7_a | 0.0526 | 0.0016 | 0.0001 | 0.0015 |

| EnInt | −1.0040 ** | −0.0141 *** | −0.0075 | −0.0831 * |

| REnC | 0.5775 | −0.0110 | 0.0106 | 0.1599 * |

| Size | −0.8658 ** | −0.0009 | −0.0067 | −0.0669 * |

| DA | −2.2832 *** | −0.0032 | −0.0302 *** | −0.2902 *** |

| Own | 0.7112 * | 0.0023 | 0.0198 *** | 0.1771 *** |

| CEO | −0.4195 | 0.0026 | −0.0050 * | −0.0453 * |

| constant | 5.1816 | 0.3471 | −0.1295 | −2.5146 |

| R-squared | 0.4272 | 0.3911 | 0.5073 | 0.5326 |

| Obs | 93 | 93 | 93 | 93 |

| Year Dummies | yes | yes | yes | yes |

*** p < 0.01, ** p < 0.05, * p < 0.1.

The regression results presented in Table 3 offer compelling insights into the relationship between sustainability reporting—specifically on SDG 7 targets—and the financial performance of Romanian banks during the 2017–2023 period. The findings reveal both statistically significant and nuanced effects of different SDG 7 disclosure scores across four key performance measures: REP, LY, ROA, and ROE.

Disclosure related to SDG 7.1—ensuring universal access to affordable, reliable, and modern energy services—is negatively and significantly associated with all financial performance indicators, except for LY. This suggests that greater transparency and reporting on this target corresponds with weaker short-term profitability for Romanian banks. Greater disclosure related to SDG 7.1 is associated with a significant decrease in the bank’s reputation score. This could be due to the perception that investments in energy access initiatives are costly and may not yield immediate benefits. A likely explanation lies in the developmental and social nature of energy access projects, which often involve financing initiatives with low or delayed financial returns, such as rural electrification, energy access for marginalized communities, or infrastructure development in less profitable regions. These activities may align with public interest and sustainability goals but are not immediately revenue generating.

This finding is in line with Buallay et al. [9], who observed that ESG disclosures in banking are often negatively correlated with profitability metrics like ROA and ROE, particularly in regions where ESG frameworks are still evolving. They point out that the costs associated with sustainability adoption—such as compliance, training, and stakeholder engagement—often outweigh short-term financial gains, leading to inefficient resource allocation in the eyes of shareholders. Additionally, these outcomes are supported by another recent study [9] investigating the effects of ESG disclosure in the manufacturing and banking sectors across 80 countries. The findings revealed a significant negative relationship between ESG reporting and firm performance in the banking sector, as measured by ROA, ROE, and Tobin’s Q. The author suggests that ESG activities can sometimes divert focus from core financial goals, leading to inefficiencies and reduced firm value—an outcome aligned with classical economic views such as those of Friedman.

This outcome aligns with agency theory, which holds that management may allocate resources to fulfill broader social goals, potentially diverging from shareholder wealth maximization [57]. From the lens of resource dependency theory, such reporting may help banks cultivate legitimacy or gain access to new, underserved markets, even at the cost of immediate financial returns. Moreover, legitimacy theory emphasizes that such disclosures are part of a bank’s strategy to maintain its “social license to operate,” rather than a driver of profitability [58]. Sustainability reporting on access to clean energy seems to carry symbolic rather than economic value in the short run.

While SDG 7.1 initiatives may pose short-term financial challenges, other energy-related disclosures can enhance reputation and financial metrics, as shown by the results obtained. In contrast to the negative effects observed for SDG 7.1, disclosure related to SDG 7.2—promoting the use of renewable energy—exhibits a positive and statistically significant association with banks’ reputation (REP), return on assets (ROA), and return on equity (ROE). These findings suggest that Romanian banks’ transparency around renewable energy initiatives is perceived favorably by stakeholders and can act as a lever for improving financial performance. This outcome aligns with the growing literature emphasizing the strategic importance of green finance and sustainability disclosure in value creation. For instance, Liu and Wu [59], in their systematic review, emphasize that firms engaging in green finance and sustainability disclosure generally experience improved financial performance, lower costs of capital, and enhanced risk management, highlighting the economic advantages of transparent environmental reporting. Steuer and Tröger [60] argue that transparency and disclosure regulations in green finance can trigger market discipline, reallocating capital toward sustainable activities, thus supporting socially optimal climate targets and enhancing firms’ financial performance. Additionally, Buallay et al. [61] investigate the impact of Environmental, Social, and Governance (ESG) disclosures on the performance of 59 MENA banks over 10 years. They find that ESG disclosures significantly improve operational, financial, and market performance, with higher ESG scores leading to better stakeholder trust, while also indicating that banks disclosing more non-financial information are likely to attract a premium on their stocks. The results are further reinforced by Beretta et al. [62], who emphasize that while sustainability performance alone may not directly influence financial performance (measured by ROE), the transparency and comprehensiveness of SDG disclosures can enhance this relationship. By effectively communicating their sustainability efforts, banks can build credibility and trust among stakeholders, leading to better financial outcomes. These results are consistent with legitimacy theory, suggesting that by publicly emphasizing support for renewable energy, banks strengthen their social license to operate and build trust among key stakeholders. From a resource dependence perspective, engagement with the renewable energy sector enables banks to access innovative, rapidly growing markets and diversify their revenue streams, enhancing operational efficiency and profitability. Therefore, disclosures related to SDG 7.2 should be seen not only as fulfilling social expectations but also as a strategic move offering tangible financial benefits.

In contrast, SDG7_a—corresponding to Target 7.a, which relates to international cooperation and investment in clean energy technologies—does not have a statistically significant relationship with any of the financial performance indicators. This may indicate that, at the current stage, Romanian banks’ involvement in this area is either too limited or too disconnected from core business operations to influence financial outcomes measurably. Romanian banks are only marginally involved in global clean energy networks or lack the operational capabilities to contribute to international projects in a measurable way. Significant clean energy projects in Romania often depend on financing from international entities. For instance, the European Investment Bank (EIB) committed up to EUR 30 million for a major wind-power project in Romania [63], highlighting the role of external funding in advancing the country’s green transition. Under legitimacy theory, this form of disclosure may serve a symbolic function [64]—demonstrating alignment with global agendas—but lacks the operational integration required to affect profitability.

This comparative analysis of the regression coefficients across the four financial performance indicators allowed us to explore the heterogeneous effects of SDG 7 disclosures on different dimensions of bank profitability. Notably, while SDG 7.2 disclosures consistently exhibited a positive and statistically significant impact on REP, ROA, and ROE, their effect on LY was negligible. This divergence suggests that renewable energy-related transparency may enhance overall profitability and stakeholder trust more than it directly influences interest income from lending. Conversely, the negative impact of SDG 7.1 disclosures was more pronounced on REP and ROE, indicating that banks engaging in energy access initiatives may face reputational or cost-related trade-offs that disproportionately affect long-term earnings and shareholder returns. To explore potential socioeconomic drivers behind these variations, the interaction between ownership structure and disclosure effects is examined. Foreign-owned banks, which dominate the Romanian banking landscape, appear more responsive to global sustainability norms, potentially amplifying the financial relevance of SDG 7.2 disclosures. These findings underscore the importance of contextual factors—such as ownership, regulatory expectations, and stakeholder pressure—in shaping the financial implications of sustainability reporting.

Regarding the control variables, negative influences on the various measures of bank financial performance are generally observed. An increase in the deposit rate (DA) leads to a significant decrease in REP, ROA, and ROE and has no effect on LY, confirming other results from the literature [43,65]. This relationship can be explained, for Romanian banks, by increased costs for maintaining deposits, lower interest rate margins, stricter regulation, or unfavorable economic conditions. The negative association between bank profitability (ROA, ROE) and female CEOs is usually linked to differences in leadership styles and risk preferences. Thus, female CEOs tend to adopt more conservative and risk-averse strategies compared to their male counterparts, which may also limit opportunities for higher profitability [46]. The negative impact of bank size, statistically significant only for REP and ROE, also found in other papers [22,43] shows that large banks do not benefit from economies of scale. The only positive connection appears between the structure of ownership (own) and REP/ROA/ROE. According to the literature [52], foreign ownership improves banks’ profitability (ROA, ROE) by introducing advanced technology, efficient management practices, and global expertise, allowing better access to international capital markets and improved risk management, which ultimately increases operational efficiency and reduces non-performing loans.

The regression analysis reveals a complex interplay between energy-related macroeconomic variables and bank profitability. The energy intensity of primary energy (EnInt) exerts a statistically significant negative effect on REP, LY, and ROE, while its influence on ROA is negative but not statistically significant. Higher energy intensity reflects lower energy efficiency, suggesting an economy that consumes more energy relative to its output. This inefficiency may negatively affect the financial environment in which banks operate. These findings are consistent with Adom [66], who found that a 10% increase in energy intensity would cause a 10.38% decline in commercial banks’ profitability in Sub-Saharan Africa. According to the author, improvements in energy efficiency reduce the financial burden on households and businesses, freeing up resources for other expenditures such as loan repayments, thereby improving bank performance by reducing non-performing loans. Additionally, better environmental quality resulting from improved energy efficiency can enhance worker productivity, further benefiting financial institutions [67]. Conversely, the share of renewable energy consumption (REnC) in total energy usage shows a statistically significant positive effect on ROE, while its relationship with other profitability indicators (REP, LY, ROA) remains statistically insignificant.

4.3. Robustness Checks

To address potential heterogeneity in the financial performance indicators (REP, LY, ROA, and ROE) and to capture a more integrated view of bank profitability, a composite index (fpc) is constructed using PCA. This index consolidates the four measures into a single variable that captures their common variance structure, offering a robust representation of overall financial performance. The regression results using the composite index as the dependent variable (Table 4) and the model in Equation (1) reaffirm the earlier findings. Specifically, SDG 7.1 disclosures remain significantly negatively associated with overall performance, while SDG 7.2 disclosures show a significant positive impact, reinforcing the conclusion that transparency around renewable energy initiatives enhances bank performance. The consistent lack of significance for SDG 7.a is preserved. Importantly, this integrated approach highlights that while each indicator captures distinct aspects of profitability, the general directional effects of SDG disclosures are robust across performance dimensions. These findings strengthen our interpretation and mitigate concerns about selective significance across isolated indicators.

Table 4.

Results of the robustness analysis using a composite index.

Table 4.

Results of the robustness analysis using a composite index.

| Variable | fpc |

|---|---|

| SDG7_1 | −0.7377 *** |

| SDG7_2 | 0.4976 ** |

| SDG7_a | 0.0759 |

| EnInt | −1.8938 ** |

| REnC | 1.8477 |

| Size | −1.4368 ** |

| DA | −5.1507 *** |

| Own | 2.8869 *** |

| CEO | −0.8667 * |

| constant | −17.1611 |

| R-squared | 0.5160 |

| Obs | 93 |

| Year Dummies | yes |

*** p < 0.01, ** p < 0.05, * p < 0.1.

Results of additional robustness tests, based on Equation (2)—col. 1–4 and Equation (3)—col. 5–8, are presented in Table 5, which depicts similar relationships between variables to those in the initial models (Table 3), validating the findings.

Table 5.

Results of the robustness analysis based on Equations (2) and (3).

Table 5.

Results of the robustness analysis based on Equations (2) and (3).

| Variable | REP | LY | ROA | ROE | REP | LY | ROA | ROE |

|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

| SDG7_1 | −0.4635 *** | −0.0025 | −0.0041 ** | −0.0272 * | −0.4806 *** | −0.0022 | −0.0043 ** | −0.0310 * |

| SDG7_2 | 0.3183 ** | −0.0008 | 0.0032 ** | 0.0207 * | 0.3410 *** | −0.0007 | 0.0043 *** | 0.0303 ** |

| SDG7_a | 0.0426 | 0.0013 | 0.0001 | 0.0016 | 0.0197 | 0.0014 | −0.0006 | −0.0039 |

| EnInt | −1.0368 ** | −0.0152 *** | −0.0075 | −0.0827 * | −0.9246 ** | −0.0090 * | −0.0017 | −0.0481 |

| REnC | 0.7093 | −0.0067 | 0.0106 | 0.1580 | 0.5278 | −0.0245 ** | −0.0009 | 0.0991 |

| Size | −0.8956 ** | −0.0018 | −0.0067 | −0.0664 * | −0.8790 * | 0.0085 | −0.0010 | −0.0492 |

| DA | −2.2708 *** | −0.0028 | −0.0302 *** | −0.2904 *** | −2.4439 *** | −0.0045 | −0.0359 *** | −0.3409 *** |

| Own | 0.7261 * | 0.0028 | 0.0198 *** | 0.1768 *** | ||||

| CEO | 0.3912 | −0.0035 | 0.0050 | 0.0457 * | ||||

| WBoD | −0.2421 | −0.0078 | 0.001 | 0.0035 | ||||

| CpR | −3.7201 | 0.1137 ** | −0.0089 | −0.4816 | ||||

| constant | 2.2894 | 0.2697 *** | −0.1339 | −2.2542 | 8.4328 | 0.4913 ** | 0.0810 | −0.9897 |

| R-squared | 0.4294 | 0.4120 | 0.5073 | 0.5327 | 0.3732 | 0.4312 | 0.3125 | 0.3548 |

| Obs | 93 | 93 | 93 | 93 | 93 | 93 | 93 | 93 |

| Year Dummies | yes | yes | yes | yes | yes | yes | yes | yes |

*** p < 0.01, ** p < 0.05, * p < 0.1.

It is worth noting that the new control variable introduced (WBoD) does not have an impact on any of the measures of banking performance [22,68].

5. Conclusions

This study offers valuable insights into the relationship between SDG 7-related disclosures and the financial performance of Romanian banks. The findings reveal that while sustainability reporting, especially in affordable and clean energy areas, can enhance stakeholder trust and attract investments, its impact on financial performance is complex. Disclosures related to SDG 7.1 (universal access to affordable energy) are negatively associated with short-term profitability measures like REP, LY, ROA, and ROE, suggesting that investments in energy access may not yield immediate financial returns. In contrast, SDG 7.2 (promoting renewable energy) disclosures positively influence financial performance, emphasizing the importance of green finance. However, SDG 7.a (international cooperation in clean energy) has no significant impact, likely due to limited involvement by Romanian banks in global clean energy initiatives. These results suggest that while sustainability reporting improves reputation and trust, the financial benefits are more pronounced for certain types of disclosures, encouraging banks to focus on sustainability areas aligned with their core business operations.

The negative association between SDG 7.1 disclosures and performance metrics suggests that banks should carefully consider the costs and benefits of investing in energy access initiatives, which may require significant upfront capital with delayed returns. While these initiatives contribute to social development, banks should transparently communicate the long-term value of these investments to stakeholders to mitigate any potential negative perceptions. On the other hand, disclosures related to SDG 7.2—promoting renewable energy—should be viewed as a strategic opportunity. As the results indicate, these disclosures positively influence stakeholder trust and financial performance. Therefore, banks should prioritize green finance initiatives and enhance transparency around renewable energy projects, which can improve their reputation, attract investments, and support sustainable growth. Macroeconomic variables further reinforce the analysis: higher energy intensity (EnInt) is negatively associated with performance, affirming that economies with lower energy efficiency constrain banking sector growth. Conversely, renewable energy consumption (REnC) appears to have limited short-term profitability benefits, echoing prior research that emphasizes the delayed economic returns of green transitions.

This study contributes to the growing literature on sustainable finance by providing empirical evidence on how energy-related SDG 7 disclosures and macroeconomic energy indicators influence bank profitability. It offers novel insights from an emerging economy context, highlighting the differentiated financial impacts of various sustainability dimensions. Romanian banks should strategically enhance transparency around renewable energy initiatives while carefully managing stakeholder expectations for disclosures related to energy access. Regulatory bodies and financial institutions alike should recognize the differentiated impact of various sustainability dimensions and tailor their strategies accordingly. The negative link between SDG 7.1 disclosures and profitability highlights the need for public incentives—such as green loan guarantees or tax breaks—to support socially beneficial but less profitable initiatives. The positive impact of SDG 7.2 disclosures implies that aligning financial regulation with green finance goals can enhance both sustainability and bank performance; thus, standardized SDG reporting and ESG frameworks should be promoted. Lastly, the lack of financial impact from SDG 7.a indicates a need for policies that encourage international collaboration and improve banks’ capacity to finance cross-border clean energy projects.

Despite its contributions, this study has several limitations. It focuses solely on Romanian commercial banks, limiting the generalizability of the findings to other contexts. The use of content analysis for SDG 7 disclosures may introduce interpretation bias and may not fully capture SDG disclosure quality. National-level energy indicators (EnInt and REnC) may not reflect individual bank strategies, and the relatively short study period (2017–2023) may miss long-term effects of energy investments. Finally, due to data and methodological constraints, potential endogeneity—such as reverse causality—could not be fully addressed. While the analysis reveals a significant negative correlation between renewable energy consumption and loan yield, consistent with short-term economic costs, it is also acknowledged that renewable energy adoption may improve firms’ financial health by reducing default risk. Due to data constraints, this potential indirect effect could not be examined. Future research incorporating firm-level default rates or credit risk measures would help clarify the pathways through which renewable energy consumption influences loan pricing. Moreover, future studies should explore long-term effects and the role of regulatory environments in amplifying or moderating these relationships. Future studies might also incorporate more granular bank-level data on actual green lending portfolios or energy-related exposures, which would allow for a more direct measurement of sustainability integration into core banking operations.

Author Contributions

Conceptualization, M.C., M.C.H. and M.M.; methodology, M.C., M.C.H. and F.O.B.; software, M.C. and M.C.H.; validation, F.Z., F.O.B. and M.M.; formal analysis, M.C., M.C.H. and F.O.B.; investigation, M.C., M.C.H. and M.M.; resources, F.Z., F.O.B. and M.M.; data curation, M.C.H., F.Z. and F.O.B.; writing—M.C., M.C.H. and M.M.; writing—review and editing, F.Z. and F.O.B.; visualization, F.Z., F.O.B. and M.M.; supervision, M.C. and M.C.H.; project administration, M.C.H. and F.Z.; funding acquisition, M.C.H. and M.M. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by the Executive Unit for Financing Higher Education, Research, Development and Innovation (UEFISCDI) through grants no. PN-IV-P2-2.2-MC-2024-0179 and PN-IV-P2-2.2-MC-2024-0183.

Data Availability Statement

The data presented in this study are available on request from the corresponding author. The data are not publicly available due to them being part of an ongoing study and used in planned future publications.

Conflicts of Interest

The authors declare no conflicts of interest. The funders had no role in the design of the study; in the collection, analyses, or interpretation of data; in the writing of the manuscript; or in the decision to publish the results.

Appendix A

Table A1.

Correlation analysis.

Table A1.

Correlation analysis.

| Variable | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | REP | 1.00 | ||||||||||||

| 2 | LY | 0.62 | 1.00 | |||||||||||

| 3 | ROA | 0.83 | 0.57 | 1.00 | ||||||||||

| 4 | ROE | 0.84 | 0.53 | 0.96 | 1.00 | |||||||||

| 5 | SDG7_1 | 0.27 | 0.18 | 0.25 | 0.27 | 1.00 | ||||||||

| 6 | SDG7_2 | 0.36 | 0.27 | 0.38 | 0.39 | 0.80 | 1.00 | |||||||

| 7 | SDG7_a | 0.13 | 0.33 | 0.13 | 0.16 | 0.43 | 0.56 | 1.00 | ||||||

| 8 | EnInt | −0.06 | −0.06 | −0.02 | −0.06 | −0.12 | −0.25 | −0.23 | 1.00 | |||||

| 9 | REnC | −0.04 | −0.07 | −0.03 | 0.02 | 0.11 | 0.13 | 0.10 | −0.24 | 1.00 | ||||

| 10 | Size | 0.63 | 0.47 | 0.62 | 0.64 | 0.50 | 0.50 | 0.16 | −0.09 | 0.06 | 1.00 | |||

| 11 | DA | 0.38 | 0.31 | 0.25 | 0.28 | 0.20 | 0.27 | 0.11 | −0.07 | 0.09 | 0.41 | 1.00 | ||

| 12 | Own | 0.45 | 0.54 | 0.44 | 0.38 | −0.16 | −0.11 | −0.09 | 0.05 | −0.01 | 0.29 | 0.01 | 1.00 | |

| 13 | CEO | −0.30 | −0.30 | −0.47 | −0.42 | −0.31 | −0.35 | −0.26 | 0.07 | 0.04 | −0.59 | −0.34 | −0.13 | 1.00 |

References

- Sebastião, A.M.; Tavares, M.C.; Azevedo, G. Evolution and Challenges of Sustainability Reporting in the Banking Sector: A Systematic Literature Review. Adm. Sci. 2024, 14, 333. [Google Scholar] [CrossRef]

- Manko, K.; Watkins, T.A. Microfinance and SDG 7: Financial impact channels for mitigating energy poverty. Dev. Pract. 2022, 32, 1036–1048. [Google Scholar] [CrossRef]

- Al Frijat, Y.S.; Al-Msiedeen, J.M.; Elamer, A.A. How Green Credit Policies and Climate Change Practices Drive Banking Financial Performance. Bus. Strat. Dev. 2025, 8, e70090. [Google Scholar] [CrossRef]

- Zarghami, S.A. The role of economic policies in achieving sustainable development goal 7: Insights from OECD and European countries. Appl. Energy 2025, 377, 124558. [Google Scholar] [CrossRef]

- Ozili, P.K. Circular Economy, Banks, and Other Financial Institutions: What’s in It for Them? Circ. Econ. Sust. 2021, 1, 787–798. [Google Scholar] [CrossRef]

- Wu, L.; Broadstock, D.C. Does economic, financial and institutional development matter for renewable energy consumption? Evidence from emerging economies. IJEPEE 2015, 8, 20–39. [Google Scholar] [CrossRef]

- Avrampou, A.; Skouloudis, A.; Iliopoulos, G.; Khan, N. Advancing the Sustainable Development Goals: Evidence from leading European banks. Sustain. Dev. 2019, 27, 743–757. [Google Scholar] [CrossRef]

- Jan, A.; Marimuthu, M.; Mat Isa, M.P.B.M. The nexus of sustainability practices and financial performance: From the perspective of Islamic banking. J. Clean. Prod. 2019, 228, 703–717. [Google Scholar] [CrossRef]

- Mohamed Buallay, A.; Al Marri, M.; Nasrallah, N.; Hamdan, A.; Barone, E.; Zureigat, Q. Sustainability reporting in banking and financial services sector: A regional analysis. J. Sustain. Financ. Invest. 2023, 13, 776–801. [Google Scholar] [CrossRef]

- Ozili, P.K. Sustainable Development Goals and bank profitability: International evidence. Mod. Financ. 2023, 1, 70–92. [Google Scholar] [CrossRef]

- Jan, A.; Rahman, H.U.; Zahid, M.; Salameh, A.A.; Khan, P.A.; Al-Faryan, M.A.S.; Che Aziz, R.B.; Ali, H.E. Islamic corporate sustainability practices index aligned with SDGs towards better financial performance: Evidence from the Malaysian and Indonesian Islamic banking industry. J. Clean. Prod. 2023, 405, 136860. [Google Scholar] [CrossRef]

- Barone, M.; Fraccalvieri, I.; Cuoccio, M.; Bussoli, C. Answering the call to action: An empirical analysis of SDG performance in global banks. Meas. Bus. Excell. 2024. [Google Scholar] [CrossRef]

- Zyznarska-Dworczak, B.; Fijałkowska, J.; Garsztka, P.; Mamić Sačer, I.; Mokošová, D.; Săndulescu, M.-S. Sustainability performance efficiency in the banking sector. Econ. Res.-Ekon. Istraživanja 2023, 36, 2218473. [Google Scholar] [CrossRef]

- Albu, C.-N.; Albu, N.; Dumitru, M.; Fota, M.-S.; Guşe, R.G. Sustainability reporting in Central and Eastern European countries. In Research Handbook on Sustainability Reporting; Rimmel, G., Aras, G., Baboukardos, D., Krasodomska, J., Nielsen, C., Schiemann, F., Eds.; Edward Elgar Publishing: Cheltenham, UK, 2024; pp. 400–417. ISBN 978-1-0353-1626-7. [Google Scholar]

- Choudhury, T.; Kamran, M.; Djajadikerta, H.G.; Sarker, T. Can Banks Sustain the Growth in Renewable Energy Supply? An International Evidence. Eur. J. Dev. Res. 2023, 35, 20–50. [Google Scholar] [CrossRef] [PubMed]

- Chen, J.M.; Umair, M.; Hu, J. Green finance and renewable energy growth in developing nations: A GMM analysis. Heliyon 2024, 10, e33879. [Google Scholar] [CrossRef]

- Zampone, G.; Nicolò, G.; Sannino, G.; De Iorio, S. Gender diversity and SDG disclosure: The mediating role of the sustainability committee. J. Appl. Account. Res. 2024, 25, 171–193. [Google Scholar] [CrossRef]

- Mazumder, M.M.M. An empirical analysis of SDG disclosure (SDGD) and board gender diversity: Insights from the banking sector in an emerging economy. Int. J. Discl. Gov. 2024, 22, 47–63. [Google Scholar] [CrossRef]

- Datta, S.; Goyal, S. Determinants of SDG Reporting by Businesses: A Literature Analysis and Conceptual Model. Vis. J. Bus. Perspect. 2022, 09722629221096047. [Google Scholar] [CrossRef]

- Bidari, G.; Djajadikerta, H.G. Factors influencing corporate social responsibility disclosures in Nepalese banks. Asian J. Account. Res. 2020, 5, 209–224. [Google Scholar] [CrossRef]

- Bose, S.; Khan, H.Z.; Bakshi, S. Determinants and consequences of sustainable development goals disclosure: International evidence. J. Clean. Prod. 2024, 434, 140021. [Google Scholar] [CrossRef]

- Al-Homaidi, E.A.; Tabash, M.I.; Farhan, N.H.S.; Almaqtari, F.A. Bank-specific and macro-economic determinants of profitability of Indian commercial banks: A panel data approach. Cogent Econ. Financ. 2018, 6, 1548072. [Google Scholar] [CrossRef]

- Erin, O.A.; Olojede, P. Do nonfinancial reporting practices matter in SDG disclosure? An exploratory study. Meditari Account. Res. 2024, 32, 1398–1422. [Google Scholar] [CrossRef]

- Buniamin, S.; Jaffar, R.; Ahmad, N.; Johari, N.H. Exploring SDGs Disclosure among Public Listed Companies in Malaysia: A Case of Energy-related SDGs. Glob. Bus. Manag. Res. 2021, 13, 762–776. [Google Scholar]

- Nizam, E.; Ng, A.; Dewandaru, G.; Nagayev, R.; Nkoba, M.A. The impact of social and environmental sustainability on financial performance: A global analysis of the banking sector. J. Multinatl. Financ. Manag. 2019, 49, 35–53. [Google Scholar] [CrossRef]

- Torre Olmo, B.; Cantero Saiz, M.; Sanfilippo Azofra, S. Sustainable Banking, Market Power, and Efficiency: Effects on Banks’ Profitability and Risk. Sustainability 2021, 13, 1298. [Google Scholar] [CrossRef]

- Chen, Z.; Umar, M.; Su, C.-W.; Mirza, N. Renewable energy, credit portfolios and intermediation spread: Evidence from the banking sector in BRICS. Renew. Energy 2023, 208, 561–566. [Google Scholar] [CrossRef]

- Galeazzo, A.; Miandar, T.; Carraro, M. SDGs in corporate responsibility reporting: A longitudinal investigation of institutional determinants and financial performance. J. Manag. Gov. 2024, 28, 113–136. [Google Scholar] [CrossRef]

- BNR. Banca Naţională a României Raport Anual 2023. 2023. Available online: https://www.bnro.ro/Raport-anual-2023-28053-Mobile.aspx (accessed on 22 May 2025).

- Huian, M.C.; Mironiuc, M.; Mihai, O.I. Studying banking performance from an accounting perspective: Evidence from Europe. Theor. Appl. Econ. 2018, XXV, 5–26. [Google Scholar]

- De Haan, J.; Scholtens, B.; Shehzad, C.T. Growth and Earnings Persistence in Banking Firms: A Dynamic Panel Investigation. SSRN J. 2009. [Google Scholar] [CrossRef]

- Ozili, P.K.; Uadiale, O. Ownership concentration and bank profitability. Future Bus. J. 2017, 3, 159–171. [Google Scholar] [CrossRef]

- Eltweri, A.; Sawan, N.; Al-Hajaya, K.; Badri, Z. The Influence of Liquidity Risk on Financial Performance: A Study of the UK’s Largest Commercial Banks. JRFM 2024, 17, 580. [Google Scholar] [CrossRef]

- Le, T.D.; Ngo, T. The determinants of bank profitability: A cross-country analysis. Cent. Bank Rev. 2020, 20, 65–73. [Google Scholar] [CrossRef]

- Caby, J.; Ziane, Y.; Lamarque, E. The impact of climate change management on banks profitability. J. Bus. Res. 2022, 142, 412–422. [Google Scholar] [CrossRef]

- Nguyen, H.T.V.; Vo, D.V. Determinants of Liquidity of Commercial Banks: Empirical Evidence from the Vietnamese Stock Exchange. J. Asian Financ. Econ. Bus. 2021, 8, 699–707. [Google Scholar] [CrossRef]

- Naili, M.; Lahrichi, Y. The determinants of banks’ credit risk: Review of the literature and future research agenda. Int. J. Fin. Econ. 2022, 27, 334–360. [Google Scholar] [CrossRef]

- Bilal, Z.; AlGhazali, A.; Samour, A. GCC banks liquidity and financial performance: Does the type of financial system matter? Futur. Bus. J. 2024, 10, 57. [Google Scholar] [CrossRef]

- Tsalis, T.A.; Malamateniou, K.E.; Koulouriotis, D.; Nikolaou, I.E. New challenges for corporate sustainability reporting: United Nations’ 2030 Agenda for sustainable development and the sustainable development goals. Corp. Soc. Responsib. Environ. 2020, 27, 1617–1629. [Google Scholar] [CrossRef]

- Sueyoshi, T.; Goto, M. Energy Intensity, Energy Efficiency and Economic Growth among OECD Nations from 2000 to 2019. Energies 2023, 16, 1927. [Google Scholar] [CrossRef]

- Pereira, R.; Sequeira, T.; Cerqueira, P. Renewable energy consumption and economic growth: A note reassessing panel data results. Environ. Sci. Pollut. Res. 2021, 28, 19511–19520. [Google Scholar] [CrossRef]

- Anton, S.G.; Afloarei Nucu, A.E. The effect of financial development on renewable energy consumption. A panel data approach. Renew. Energy 2020, 147, 330–338. [Google Scholar] [CrossRef]

- Antoun, R.; Coskun, A.; Georgievski, B. Determinants of financial performance of banks in Central and Eastern Europe. Bus. Econ. Horiz. 2018, 14, 513–529. [Google Scholar] [CrossRef]

- Saona, P. Intra- and extra-bank determinants of Latin American Banks’ profitability. Int. Rev. Econ. Financ. 2016, 45, 197–214. [Google Scholar] [CrossRef]

- Huian, M.C.; Curea, M.; Apostol, C. The association between governance mechanisms and engagement in commercialisation and entrepreneurship of Romanian public research institutes. Heliyon 2024, 10, e34909. [Google Scholar] [CrossRef] [PubMed]

- Palvia, A.; Vähämaa, E.; Vähämaa, S. Are Female CEOs and Chairwomen More Conservative and Risk Averse? Evidence from the Banking Industry During the Financial Crisis. J. Bus. Ethics 2015, 131, 577–594. [Google Scholar] [CrossRef]

- Mazziotta, M.; Pareto, A. Synthesis of Indicators: The Composite Indicators Approach. In Complexity in Society: From Indicators Construction to their Synthesis; Maggino, F., Ed.; Social Indicators Research Series; Springer International Publishing: Cham, Switzerland, 2017; Volume 70, pp. 159–191. ISBN 978-3-319-60593-7. [Google Scholar]

- Mazziotta, M.; Pareto, A. Principal component analysis for constructing socio-economic composite indicators: Theoretical and empirical considerations. SN Soc. Sci. 2024, 4, 114. [Google Scholar] [CrossRef]

- Kaiser, H.F.; Rice, J. Little Jiffy, Mark Iv. Educ. Psychol. Meas. 1974, 34, 111–117. [Google Scholar] [CrossRef]

- Nunnally, J.; Bernstein, I. Psychometric Theory, 3rd ed.; McGraw-Hill: New York, NY, USA, 1994. [Google Scholar]

- Ionașcu, A.E.; Gheorghiu, G.; Spătariu, E.C.; Munteanu, I.; Grigorescu, A.; Dănilă, A. Unraveling Digital Transformation in Banking: Evidence from Romania. Systems 2023, 11, 534. [Google Scholar] [CrossRef]

- Farisyi, S.; Musadieq, M.A.; Utami, H.N.; Damayanti, C.R. A Systematic Literature Review: Determinants of Sustainability Reporting in Developing Countries. Sustainability 2022, 14, 10222. [Google Scholar] [CrossRef]

- Tăchiciu, L.; Fulop, M.T.; Marin-Pantelescu, A.; Oncioiu, I.; Topor, D.I. Non-Financial reporting and reputational risk in the Romanian financial sector. Amfiteatru Econ. 2020, 22, 668–691. [Google Scholar] [CrossRef]

- Allen, F.; Carletti, E.; Goldstein, I.; Leonello, A. Moral Hazard and Government Guarantees in the Banking Industry. J. Financ. Regul. 2015, 1, 30–50. [Google Scholar] [CrossRef]

- Bunea, M.; Dinu, V. The impact of the gender diversity on the Romanian banking system performance. Transform. Bus. Econ. 2018, 17, 42–59. [Google Scholar]

- Studenmund, A.H. Using Econometrics: A Practical Guide, 7th ed.; Pearson: London, UK, 2016. [Google Scholar]

- Jensen, M.C.; Meckling, W.H. Theory of the firm: Managerial behavior, agency costs and ownership structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef]

- Suchman, M.C. Managing legitimacy: Strategic and institutional approaches. Acad. Manag. Rev. 1995, 20, 571–610. [Google Scholar] [CrossRef]

- Liu, C.; Wu, S.S. Green finance, sustainability disclosure and economic implications. Fulbright Rev. Econ. Policy 2023, 3, 1–24. [Google Scholar] [CrossRef]

- Steuer, S.; Tröger, T.H. The Role of Disclosure in Green Finance. J. Financ. Regul. 2022, 8, 1–50. [Google Scholar] [CrossRef]

- Buallay, A.; Fadel, S.M.; Al-Ajmi, J.Y.; Saudagaran, S. Sustainability reporting and performance of MENA banks: Is there a trade-off? Meas. Bus. Excel. 2020, 24, 197–221. [Google Scholar] [CrossRef]

- Beretta, V.; Demartini, M.C.; Trucco, S. From sustainability to financial performance: The role of SDG disclosure. Meas. Bus. Excell. 2024, 29, 237–255. [Google Scholar] [CrossRef]

- European Investment Bank Romania to Expand Clean Energy Production with EUR30 Million EIB Support for Major New Wind Farm. Available online: https://www.eib.org/en/press/all/2025-139-romania-to-expand-clean-energy-production-with-eur30-million-eib-support-for-major-new-wind-farm (accessed on 22 May 2025).

- Michelon, G.; Pilonato, S.; Ricceri, F. CSR reporting practices and the quality of disclosure: An empirical analysis. Crit. Perspect. Account. 2015, 33, 59–78. [Google Scholar] [CrossRef]

- Rachdi, H. What Determines the Profitability of Banks During and before the International Financial Crisis? Evidence from Tunisia. Int. J. Econ. Financ. Manag. 2013, 2, 330–337. [Google Scholar]

- Adom, P.K.; Amuakwa-Mensah, F.; Amuakwa-Mensah, S. Degree of Financialization and Energy Efficiency in Sub-Saharan Africa: Do Institutions Matter? Financ. Innov. 2020, 6, 33. [Google Scholar] [CrossRef]

- Neidell, M. Air pollution and worker productivity. IZA World Labor 2017. [Google Scholar] [CrossRef]

- Pizzi, S.; Rosati, F.; Venturelli, A. The determinants of business contribution to the 2030 Agenda: Introducing the SDG Reporting Score. Bus. Strat. Environ. 2021, 30, 404–421. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).