1. Introduction

Greenhouse gas emissions have increased the Earth’s temperature by 1.9 degrees Fahrenheit and the sea level by 7 inches. Researchers provide evidence that, even if all emissions are halted from today, the already stored emission levels are enough to adversely impact future life on Earth [

1]. Due to the significant socioeconomic impacts of climate change, the United Nations (UN) requires countries to formulate policies to adapt to climate change’s adverse impacts while also considering steps to mitigate emission levels [

2]. The United Nations currently uses territorial-based carbon emissions (TBEs) accounting to hold countries responsible for their mitigation, where such mechanisms only consider emissions produced in a country’s territory [

3,

4]. Such a conventional mechanism allows developed countries to comply with emissions mitigation requirements by transferring energy-intensive industries to other parts of the world, thus protecting themselves from carbon accountability [

5].

This practice, known as carbon leakage, occurs when businesses relocate to other countries to cap emissions while importing the produced products [

6,

7,

8]. Due to the apparent failure of TBEs to capture carbon leakage, consumption-based carbon emissions (CBEs) are gaining momentum, addressing this shortcoming [

9,

10,

11,

12]. CBEs account for the total emissions associated with a country’s consumption by including emissions embodied in imports and excluding those in exports. Researchers increasingly advocate for the adoption of CBEs as a more accurate framework in assigning emissions mitigation responsibilities, particularly for emissions embedded in international trade [

12,

13].

Numerous studies provide evidence of the relationship between trade and carbon emissions [

14,

15,

16,

17]; however, such studies primarily rely on TBEs, which overlook carbon leakage. Prior studies that have examined the relationship between trade and TBEs have largely ignored the individual impacts of imports and exports on TBEs [

14,

15,

18]. Furthermore, CBEs also challenge the argument of emissions convergence, known as the Environmental Kuznets Curve hypothesis (EKCH), where an inverted-U-shaped relationship exists between economic growth and TBEs [

19,

20,

21,

22]. Considering the role of trade in a country’s economic growth, ignoring the emissions embodied in trade to assess the EKCH provides an over-optimistic belief that further economic growth can reduce emissions [

23].

A growing number of studies are examining the individual impact of trade on CBEs. However, past studies have focused on a group of countries, like the OECD, the European Union, oil-exporting countries, or a combination of developed and developing economies [

23,

24,

25,

26], while ignoring the impact of the disaggregate level of trade for an individual country. Moreover, past studies have only examined the symmetric impact of trade on CBEs. No study has examined the asymmetric relationship between exports and imports and CBEs for an individual country. Due to this apparent gap, this study’s objective is to examine the symmetric and asymmetric impacts of the disaggregate level of trade on the CBEs of the two greatest energy consumers of the world, namely the People’s Republic of China (PRC) and the United States of America (USA).

The PRC and the USA are two major economies globally, representing 25% of global trade while holding top positions among their peer groups in trade [

27]. Both these economies are the most significant consumers of energy and the greatest producers of emissions globally, where the PRC relies on coal and the USA relies on oil to fulfill its growing energy demand [

28]. Although innovation has rendered the whole production process more efficient, at the same time, it has allowed countries to increase their production outputs, thus consuming more energy and producing higher emissions levels [

29,

30,

31]. Thus, considering the sheer extent of the energy consumption and trade volumes of the PRC and the USA, they are excellent candidates to strengthen the argument for embodied emissions in trade.

For analysis, this study considers the period from 1990 to 2018, which was selected to ensure stable trade patterns unaffected by large structural breaks. In 2019, two major disruptions emerged: the intensified US–China trade war and the global COVID-19 pandemic. Both events significantly altered trade flows and emissions patterns [

32,

33], introducing volatility that would compromise long-run equilibrium analysis. Therefore, this timeframe ensures consistency and robustness in the econometric modeling. This study extends the current line of literature in the following ways. Firstly, this study performs a comparative analysis by examining the long- and short-run impact of exports and imports on the CBEs of the PRC and the USA by employing the autoregressive distributed lag (ARDL) methodology. Secondly, beyond symmetric analysis, this study also explores the asymmetric impact of the disaggregate level of trade on CBEs by employing a non-linear autoregressive distributed lag (NARDL) approach, revealing nuanced dynamics in trade and emissions relationships. Thirdly, besides exports and imports, this study also examines the EKC hypothesis, highlighting its limitations when assessed using territorial-based emissions (TBEs). It underscores the importance of adopting CBEs as a more accurate metric, particularly for economies with substantial trade volumes. Control variables such as economic growth, oil prices, financial development and industry value addition are also incorporated to comprehensively analyze the factors influencing CBEs. Lastly, this study applies the dynamic ordinary least squares (DOLS) methodology for robustness analysis, while also utilizing Granger causality to assess the flow of causality among the study variables.

This study’s findings indicate that exports diminish and imports augment CBEs in both the short and long term for the PRC and the USA, with the PRC exhibiting greater coefficient magnitudes due to its accelerated trade expansion and dependence on energy-intensive imports. The findings do not corroborate the EKC theory, suggesting that economic expansion exacerbates CBEs in both economies. The findings regarding the error correction term indicate that the PRC requires a 2.64 times longer duration than the USA to achieve equilibrium after a short-run shock, highlighting systemic rigidity in its emissions systems. These findings offer new perspectives on the trade–emissions relationship, highlighting the necessity of tailored and nation-specific carbon reduction policies.

The remaining parts of this study are organized in the following manner:

Section 2 discusses the literature review, while

Section 3 describes the model and methodological element.

Section 4 covers the results and discussion, and

Section 5 provides the conclusions and policy implications.

2. Literature Review

Industrialization and globalization, supplemented by the formation of the World Trade Organization (WTO), raised international trade among countries by streamlining the overall global trade structure during the 20th century. Although the growing trade volume has enabled both developed and developing economies to enhance their economic growth, such growth has also adversely impacted the environment [

34,

35,

36]. Multiple works of literature have examined the relationship between trade and carbon emissions, but they provide mixed findings. For instance, Shahbaz, M., S. Nasreen, K. Ahmed and S. Hammoudeh [

16] investigated the impact of trade openness on the carbon emissions of 105 economies and found the relationship to be positive. Meanwhile Kim, D.-H., Y.-B. Suen and S.-C. Lin [

37] studied the relationship between trade and carbon emissions in the North–North, South–South, North–South and South–North contexts; they found that trade with the North intensified while trade with the South reduced emission levels.

Furthermore, they analyzed the effect of trade on emissions by splitting the data of developed and developing countries. They noticed that developed countries trade with either the North or the South to reduce their emission levels. In contrast, developing countries’ trade with the North intensifies emissions, while trade with the South mitigates their emission levels. They underlined that developed economies’ companies, in order to remain competitive, have shifted their production to developing economies, which has also benefited them in reducing their emissions. Similarly, Al-Mulali, U., I. Ozturk and S.A. Solarin [

38] also provide evidence that trade openness intensifies carbon emissions in the Americas, Sub-Saharan Africa, South Asia and Eastern and Central Europe, while mitigating Western Europe’s emissions. Gozgor, G. [

39] examined the impact of trade openness on carbon emissions by using data from 35 member countries of the Organization for Economic Cooperation and Development (OECD) and found a negative relationship between trade openness and carbon emissions in the long run. Sharif Hossain, M. [

40], using data from newly industrialized economies from 1971 to 2007, found that trade openness amplifies carbon emissions in the long run due to higher energy consumption.

Energy consumption has long been identified as a principal driver of carbon dioxide (CO

2) emissions, especially in countries relying heavily on fossil fuels. Numerous empirical studies support the positive relationship between energy use and carbon emissions. For instance, Ang, B. W. and B. Su [

41] found that increases in energy consumption directly correlate with higher emissions across both developing and developed economies. Similarly, Shahbaz, M., H. H. Lean and M. S. Shabbir [

42] demonstrated, using ARDL bounds testing for South Africa, that energy usage contributes substantially to environmental degradation. In fast-developing countries, the energy mix plays a crucial role, where countries like China and India, which rely heavily on coal, have experienced significant emission growth despite economic modernization [

43]. Lin, B. and I. Ahmad [

44] also argue that, while economic expansion contributes to rising emissions, the energy structure (renewables vs. fossil fuels) is an even more significant determinant. Moreover, the Environmental Kuznets Curve (EKC) hypothesis has often been tested in this context. It posits that emissions initially rise with energy-fueled economic growth but later fall as economies mature and adopt cleaner energy sources [

45,

46,

47]. However, evidence for the EKC remains mixed, especially when energy consumption remains carbon-intensive [

48,

49].

Technological innovation plays a dual role in carbon emissions: it can either increase efficiency and reduce emissions or spur further energy use and have rebound effects. Innovation that enhances energy efficiency tends to lower emissions. Popp, D. [

29] emphasizes the importance of “directed technical change”, where research and development (R&D) focuses on clean technologies, which significantly contributes to reducing the carbon intensity of an economy. A panel study of OECD countries by Töbelmann, D. and T. Wendler [

50] found that green patents and clean technology investments correlate negatively with carbon emissions. Similarly, Mohamued, E. A., M. Ahmed, P. Pypłacz, K. Liczmańska-Kopcewicz and M. A. Khan [

51] provided evidence that innovation reduces the energy intensity and subsequently carbon emissions in oil-exporting countries.

Conversely, the rebound effect—where efficiency gains lead to increased energy use—remains a critical concern. For example, Gillingham, K., D. Rapson and G. Wagner [

52] noted that efficiency-induced reductions in cost could incentivize more energy consumption, potentially offsetting the emission savings. Furthermore, technological spillovers through trade and foreign direct investment (FDI) also influence emissions. Dauda, L., X. Long, C. N. Mensah, M. Salman, K. B. Boamah, S. Ampon-Wireko and C. S. Kofi Dogbe [

53] argue that countries engaging in technology transfers via trade agreements show better carbon efficiency metrics, although the benefits are more substantial in higher-income economies.

Studies increasingly emphasize the combined influence of the energy structure and technological innovation on carbon mitigation. Renewable energy deployment, supported by innovation in storage and grid management, has proven effective in reducing emissions in European countries [

54]. In addition, innovation-focused climate policies—like carbon pricing coupled with R&D subsidies—create long-term incentives for decarbonization [

55]. Therefore, effective carbon mitigation requires not just reducing energy consumption but shifting to cleaner energy sources and fostering innovative ecosystems that support sustainable technologies.

A substantial body of literature supports the view that financial development contributes to environmental degradation. Shahbaz, M., Q. M. A. Hye, A. K. Tiwari and N. C. Leitão [

56] found that financial development in Indonesia leads to increased CO

2 emissions through higher energy demands. Similarly, Sadorsky, P. [

57] argues that improved access to finance boosts industrial outputs, vehicle ownership and energy consumption, especially in emerging economies, thereby accelerating emissions. Zhang, Y.-J. [

58], using data from China, also reported a positive link between financial sector growth and CO

2 emissions. The rationale is that financial development lowers borrowing constraints, encourages consumption and investment in energy-intensive sectors and ultimately leads to greater environmental degradation.

In contrast, other studies suggest that financial development can facilitate carbon mitigation by easing capital constraints for clean energy investments and improving the resource allocation efficiency. Tamazian, A. and B. B. Rao [

59] demonstrated that, in transitional economies, financial sector efficiency and institutional development contribute to environmental quality improvement by promoting green technologies. Similarly, Javid, M. and F. Sharif [

60] argue that developed financial markets play a crucial role in environmental sustainability by mobilizing capital toward renewable energy and low-carbon projects. They also posit that financial openness may attract foreign direct investment (FDI) in environmentally efficient industries, further aiding emission reduction.

Although previous works of literature provide evidence of how and when trade, energy sources, financial development and technological innovations impact carbon emissions, such studies utilize territorial-based carbon emissions (TBEs), ignoring carbon leakage [

16,

61,

62]. Furthermore, most studies have examined the accumulated effect of imports and exports in the form of trade; only a handful of studies have examined the individual impacts of imports and exports on carbon emissions [

63,

64]. Due to the failure of TBEs to capture carbon leakage, recent studies have not only focused on consumption-based carbon emissions (CBEs), as they capture carbon leakage embodied in international trade.

For instance, Liddle, B. [

25] examined the impacts of exports and imports on CBEs using 102 countries’ data from 1990 to 2013 and found that exports reduce CBEs, while imports enhance CBEs. Khan, Z., M. Ali, L. Jinyu, M. Shahbaz and Y. Siqun [

23], using data from nine oil-exporting countries from 1990 to 2018, also found that imports have a positive and statistically significant relationship with CBEs, while exports have a negative and statistically significant relationship with CBEs. Hasanov, F. J., B. Liddle and J. I. Mikayilov [

24] also found that exports mitigate CBEs, while imports amplify CBEs, using data from 117 countries from 1990 to 2013. Knight, K. W. and J. B. Schor [

26] also provide similar findings using 29 high-income countries’ data from 1991 to 2008. Lamb, W. F., J. K. Steinberger, A. Bows-Larkin, G. P. Peters, J. T. Roberts and F. R. Wood [

65], using data from five high-income countries, examined the relationship between exports and CBEs and found that the relationship was negative and statistically significant.

The Gross Domestic Product (GDP) is a gauge for a country’s economic health. Thus, higher growth would result in higher consumption, government spending and overall trade, leading to higher CBEs [

23,

66]. Safi, A., Y. Chen, S. Wahab, S. Ali, X. Yi and M. Imran [

67] suggest that financial instability in Emerging 7 (E-7) countries hinders economic growth, restricting the financial sector from providing necessary liquidity to the consumer, thus limiting overall consumption and CBEs. However, they also discovered that economic growth has a positive relation with CBEs, but higher technological innovation has the ability to reduce CBEs in the long run. Meanwhile, Kirikkaleli, D., H. Güngör and T. S. Adebayo [

68] highlight the importance of government policies in the case of Chile, which, when used effectively, can allow for financial development to reduce CBEs.

Abbasi, K. R., K. Hussain, A. M. Haddad, A. Salman and I. Ozturk [

69] argue that it is vital to understand the major source of energy consumption of a country; where countries rely solely on non-renewable energy, higher economic growth will always lead to higher CBEs. They found that, in the case of Pakistan, factors like financial development, energy consumption and economic growth intensify CBEs. Qin, L., M. Y. Malik, K. Latif, Z. Khan, A. W. Siddiqui and S. Ali [

70] found similar evidence in the case of N-11 economies, where higher economic growth leads to higher CBEs, due to the dependency of N-11 economies on non-renewable energy. They additionally found that industry value addition also enhances CBEs, but changes in oil price have a negative relationship with CBEs, as higher oil costs reduce non-renewable energy consumption, resulting in a reduction in CBEs.

5. Conclusions and Implications

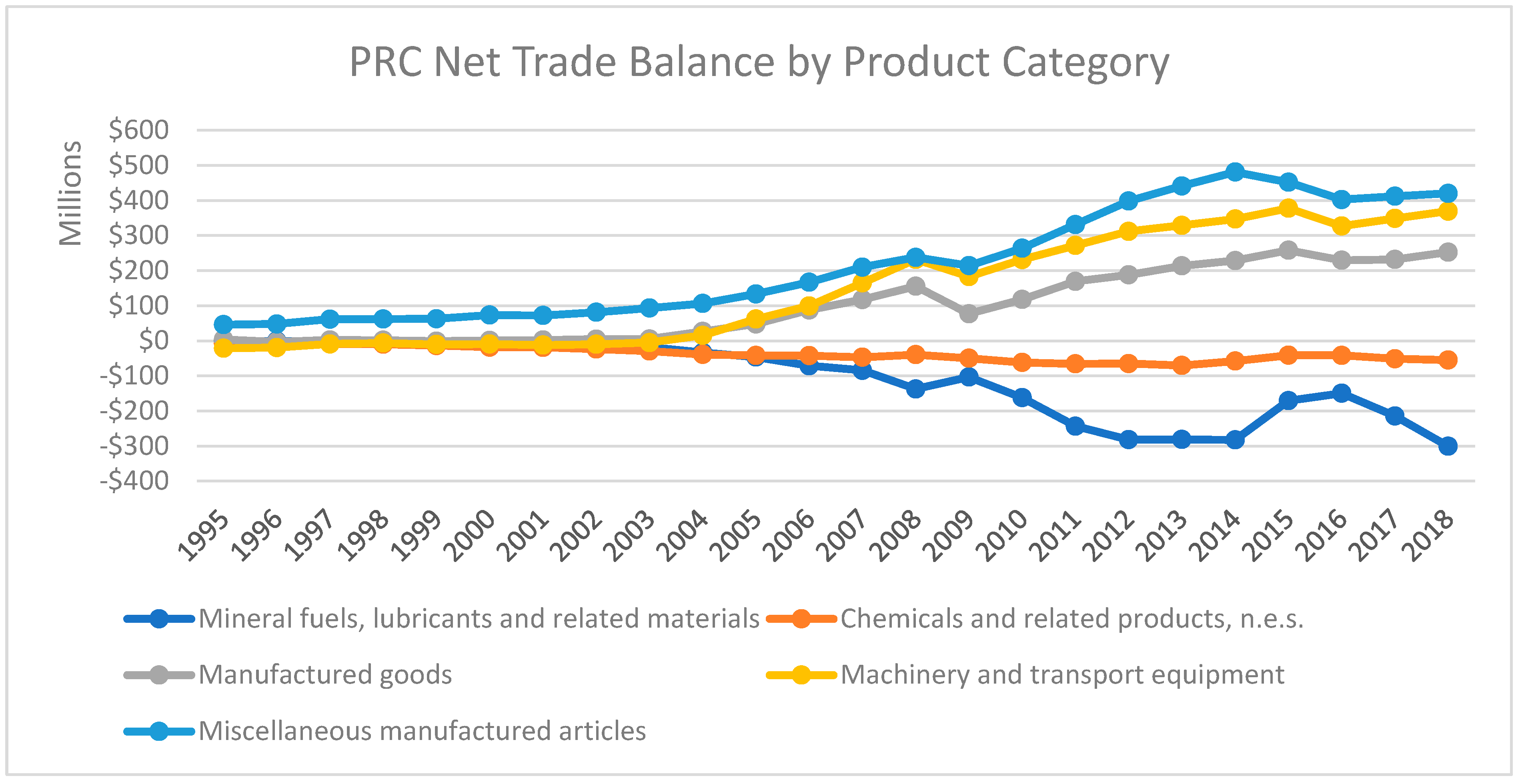

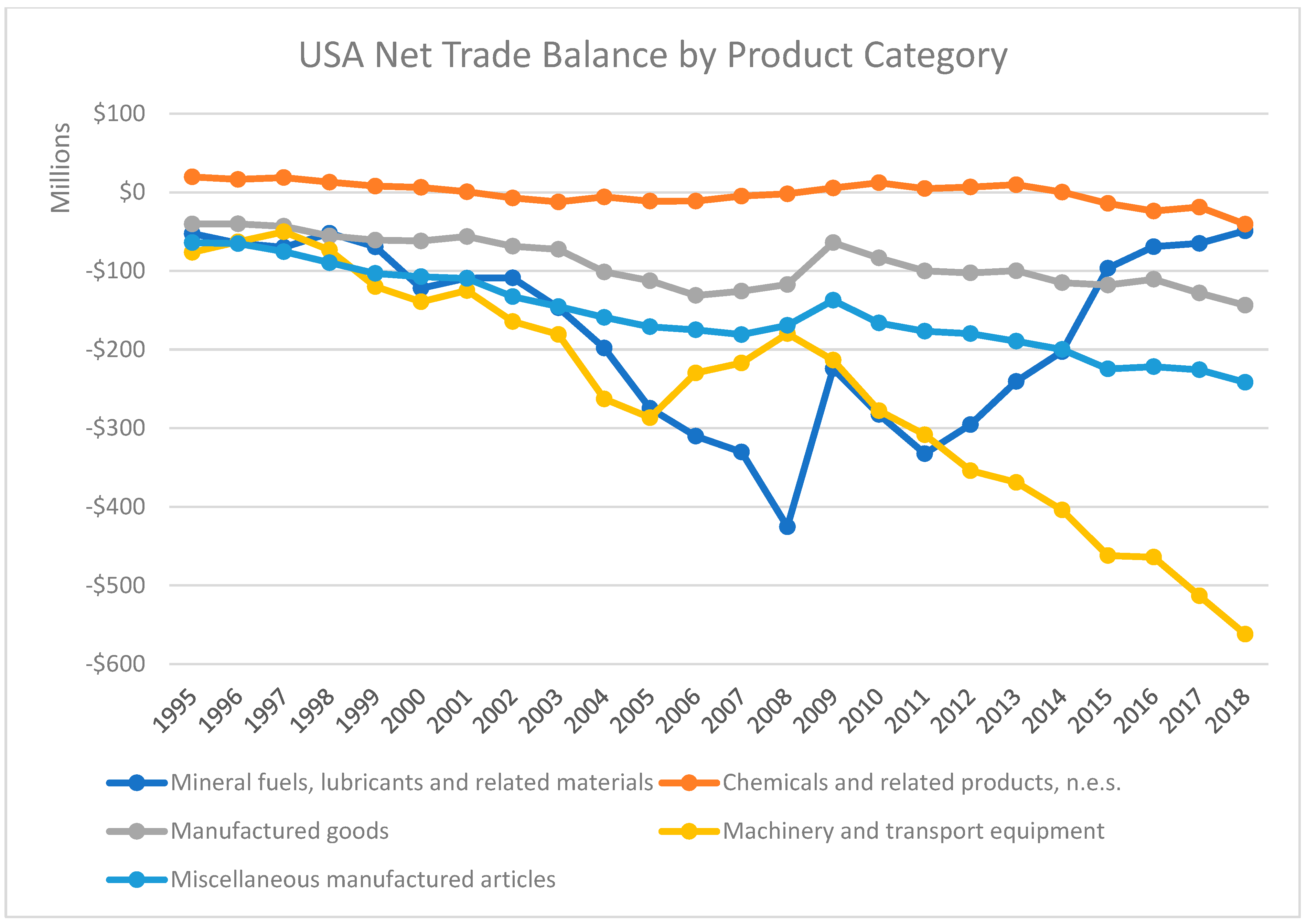

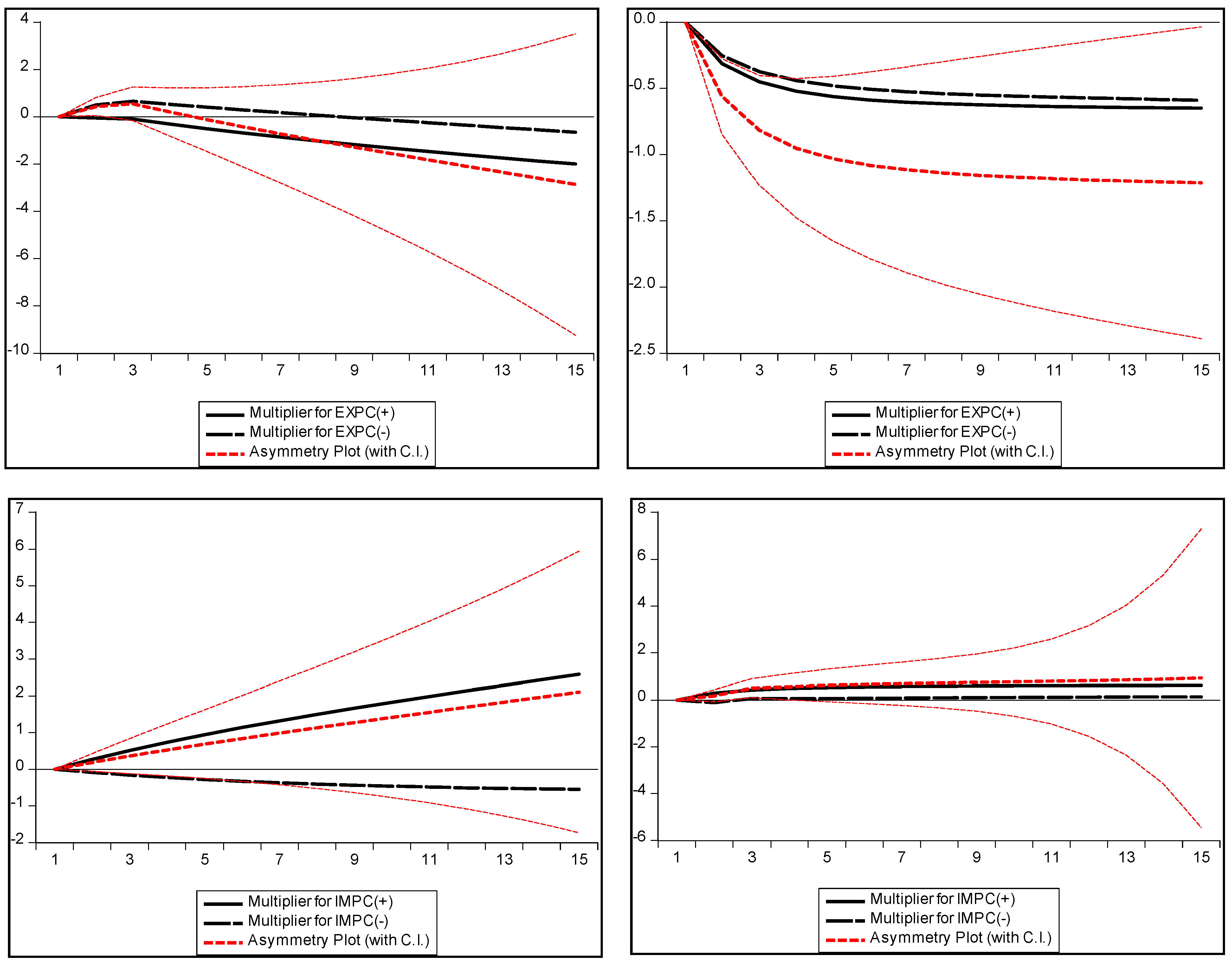

This study analyzes the symmetric and asymmetric effects of imports and exports on CBEs, utilizing data from two energy superpowers, the PRC and the USA, from 1990 to 2018. The ARDL and NARDL techniques are used to analyze the long-term and short-term correlations among the study variables. This study is the inaugural examination of the symmetric and asymmetric links between imports and exports for the two principal energy consumers globally, revealing, through the ARDL results, that exports diminish while imports augment CBEs in both the long and short term for the PRC and the USA. The long-term NARDL estimates indicate that an increase in exports diminishes CBEs, but increases in imports augment CBEs, for both economies. Meanwhile, the short-term estimates from NARDL indicate that an increase in imports boosts CBEs in both nations; however, a fall in exports enhances CBEs in the USA, while reducing CBEs in the PRC. This is attributed to the structural characteristics of the supply chain within each country.

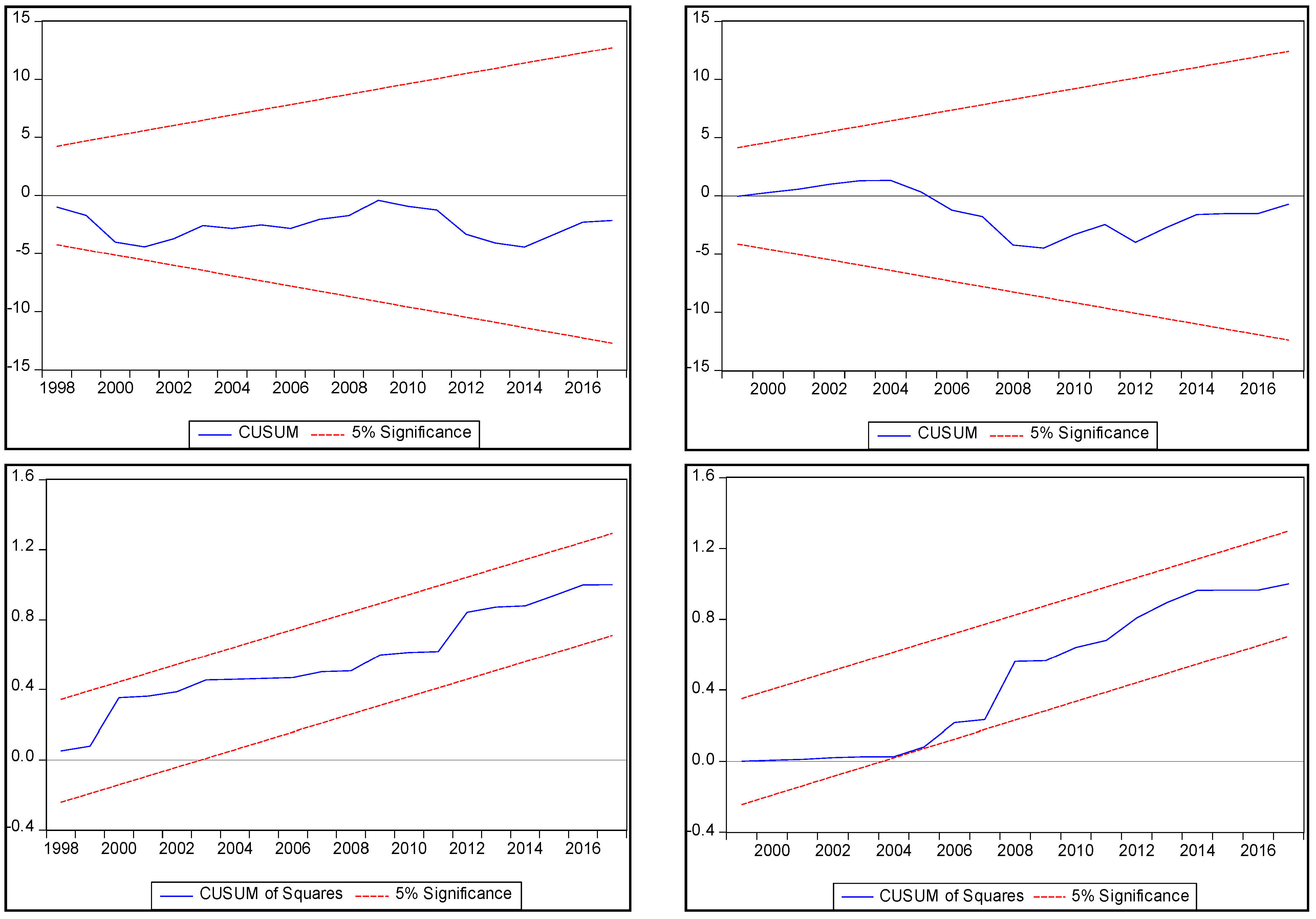

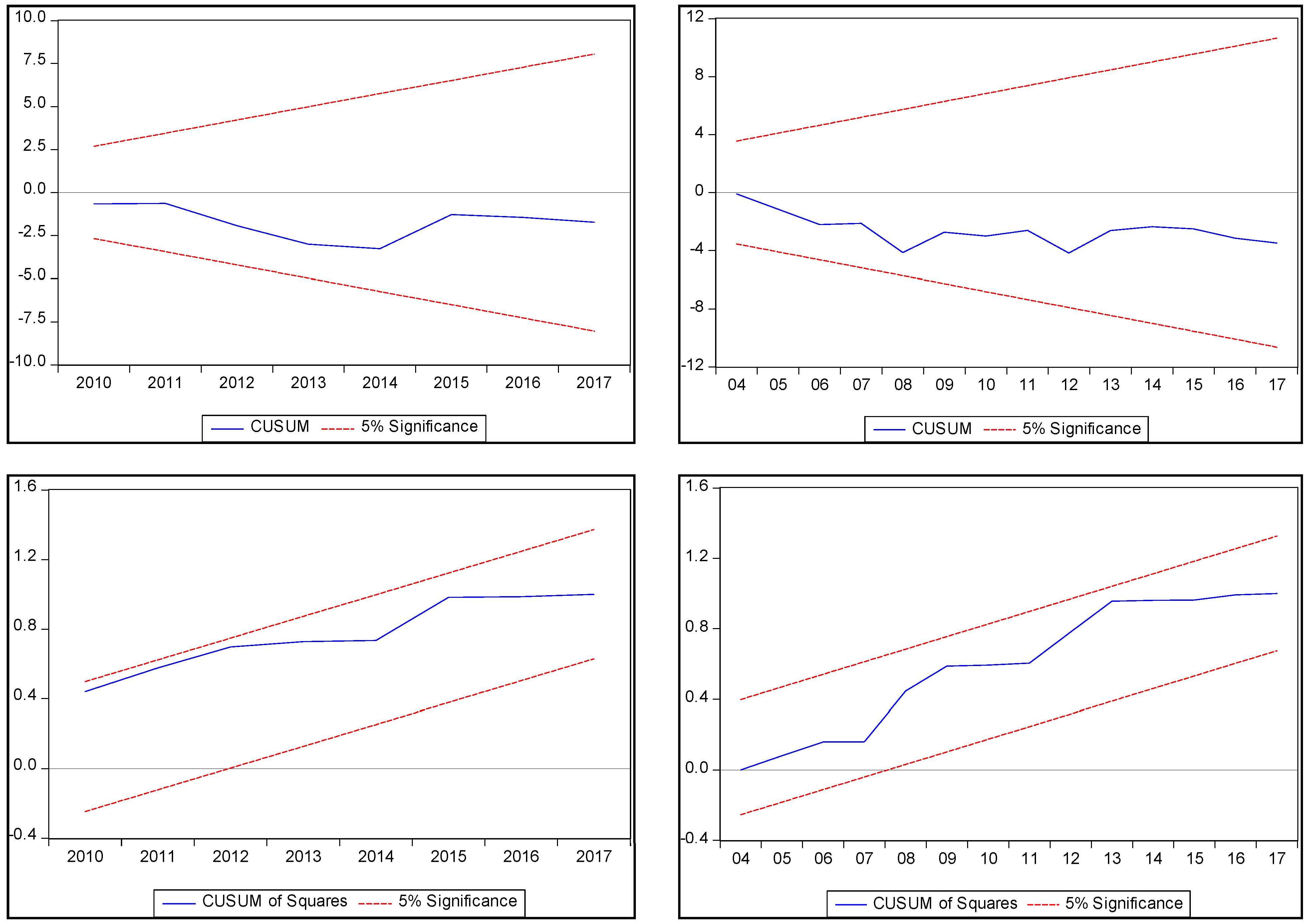

Moreover, in the long run, the magnitude of the overall coefficients for the PRC surpasses that of the USA due to the overall pace of growth in trade and the reliance on energy-intensive imports in the PRC. The error correction term indicates that, following a shock in the short run, the PRC takes 2.6 times longer to return to an equilibrium state in the long run compared to the USA, reflecting the systemic rigidity of the PRC’s emissions and industrial systems. The data do not substantiate the Environmental Kuznets Curve (EKC) theory, which posits an inverted U-shaped correlation between economic expansion and emissions. This deviation from the EKC hypothesis might be ascribed to the neglect of emissions embedded in international commerce when evaluating the growth–emissions correlation. The dependence on consumption-based emissions underscores the necessity of a more holistic carbon accounting method, especially for economies with substantial trade volumes. Robustness checks, including dynamic ordinary least squares (DOLS) analysis and Granger causality tests, validate the consistency of these findings.

This study proposes the following subsequent policy implications derived from its findings. This study shows that higher economic growth intensifies CBEs, emphasizing the importance of decoupling economic growth from carbon emissions through structural reforms and low-carbon technologies. We recommend that both the PRC and the USA use energy-efficient technologies and augment the proportion of renewable energy in their overall energy portfolio to diminish their products’ energy intensity and emission levels. Imposing a carbon price on energy-intensive products will enable consumers to transition to less energy-intensive alternatives while incentivizing firms to decrease their energy intensity to remain competitive globally. Trade policies must concurrently account for the carbon footprints of traded items, necessitating strategies to assist domestic enterprises in diminishing the carbon footprints of their offerings. Transitioning from production-based to consumption-based accounting in international agreements can distribute emissions responsibility more equally. This would urge importing countries to consider the emissions inherent in their consumption habits, promoting shared responsibility.

In a manner analogous to tags that display energy consumption on electronic devices, energy-intensity labels ought to be affixed to all products, enabling consumers to factor in the energy intensity of the product in their decision-making processes. Furthermore, collaborative trade agreements should incorporate carbon standards, fostering mutual accountability and collective innovation in low-carbon technologies. Moreover, customized policies for high-emission industries, including heavy industry and transportation, like encouraging electrification in transportation and enhancing energy efficiency in manufacturing, can substantially decrease emissions associated with commerce. Lastly, the dependence on economic growth as a catalyst for carbon reductions, as suggested by the EKC, may prove inadequate. Both nations require creative policy instruments, like carbon border adjustments, green subsidies and more stringent emissions limits, to attain substantial reductions without depending exclusively on growth.

These policy actions highlight the importance of a comprehensive approach to managing trade-related emissions and ensuring sustainable growth for the PRC and the USA. This study’s methodological framework serves as a crucial resource for policymakers aiming to evaluate the long-term and short-term impacts of economic activity on carbon emissions. Future studies ought to broaden this analysis to include additional significant trading nations and examine sector-specific impacts to improve global carbon mitigation strategies.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}