Hydrogen: Prospects and Criticalities for Future Development and Analysis of Present EU and National Regulation

Abstract

1. Introduction

2. The EU Policy on Hydrogen and National Provisions

2.1. European Regulation

- Support to the investments,

- Support for production and demand,

- Creation of a market and infrastructure for hydrogen,

- Boost to research and cooperation,

- Stimulation of an international cooperation.

- As agreed by the Member States, 42% of hydrogen used in industry should come from renewable fuels of non-biological origin by 2030 and 60% by 2035;

- The combined share of advanced biofuels and biogas produced from feedstocks and renewable fuels of non-biological origin (RFNBOs) in the energy supplied to the transport sector should be at least 1% in 2025 and 5.5% in 2030 (furthermore, by 2030, at least 1% must come from RFNBOs);

- Energy from RFNBOs is counted towards Member States’ renewable energy share and sectoral targets only if the reduction in greenhouse gas emissions resulting from the use of such fuels is at least 70%.

- All hydrogen refueling should be located either on the Trans-European Transport network (TEN-T) road network, including the most important connections between the main cities and urban nodes (i.e., an urban area where there is TEN-T network infrastructures, such as ports, including passenger terminals, airports, railway stations, logistics platforms and freight terminals, both within and surrounding the urban area), or within a road distance of 10 km from the nearest exit of a TEN-T road;

- All hydrogen-refueling stations should be in urban nodes;

- For urban hubs, public authorities should evaluate the possibility of establishing hydrogen-refueling stations within intermodal hubs (i.e., logistics platform specialized in combined transport) and could also supply hydrogen to other modes of transport, such as rail and internal navigation;

- To this end, member states shall ensure that, by 31 December 2030, publicly accessible hydrogen-refueling stations are installed along the TEN-T core network at a maximum distance of 200 km from each other, designed for a minimum cumulative capacity of 1 ton per day and equipped with at least one 700 bar distributor and in each urban node.

- The additionality requirement: The idea of additionality is to ensure that the increase in hydrogen production goes hand in hand with the increase in renewable electricity generation. To this end, the rules require hydrogen producers to stipulate power purchase agreements (PPAs) only with new and not already-supported renewable electricity generation capacity.

- The temporal and geographical correlation criteria: These criteria ensure that hydrogen is produced only when and where renewable electricity is available. The criteria aim to prevent the demand for renewable electricity used for hydrogen production from incentivizing greater electricity production from fossil sources since this would have negative consequences on greenhouse gas emissions, demand for fossil fuels, and related gas and electricity prices.

- Domestic pillar: to support the expansion of the hydrogen production market within the European Economic Area and connect the supply of renewable hydrogen with demand;

- Hydrogen Bank Auctions: The first European-wide auction awarded almost €720 million to 7 renewable hydrogen projects across Europe under the Innovation Fund. Announced in April 2024, the winning projects were selected by the European Climate, Infrastructure, and Environment Executive Agency (CINEA [18]), which assessed 132 bids submitted to the auction between November 2023 and February 2024 and ranked them based on the offer price;

- International pillar: to promote a coordinated EU strategy on renewable hydrogen imports;

- Transparency and coordination: to ensure transparency and coordination of information to support market and infrastructure development and improve coordination of existing support instruments of the EU and EU countries, including technical assistance and support to investments inside and outside the EU.

2.2. National Regulations

- Two reforms concerning the administrative simplification and reduction in regulatory obstacles to the diffusion of hydrogen, aimed at defining a legal framework to promote hydrogen as a source of renewable energy, and fiscal measures to incentivize production and use of hydrogen.

- Two investments for the production and use of hydrogen on two areas: hydrogen production in disused industrial areas (hydrogen valleys) and use of hydrogen in hard-to-abate sectors.

- I is the incentive due (expressed in €/kg of hydrogen)

- Pagg is the award price (strike price)

- Prif is the price of the counterfactual fuel replaced (reference tariff)

- VGO/ETS is the value of the GOs and the ETS

- R is a reduction term applied in the case other incentives are received

- O is the value of the system charges.

- Natural gas, when hydrogen is used in the industrial sector: in this case, the reference price is the average price of natural gas, expressed in €/smc, weighted by quantities, recorded on the day-ahead natural gas market and on the intraday natural gas market in the month of collection;

- Diesel, when hydrogen is used in the transport sector to replace it: in this case, the reference price is the price, expressed in €/liter, published monthly by the Fuel Observatory on the institutional website of the Ministry,

- Gray hydrogen, when hydrogen (renewable or biohydrogen) is used in industry sectors that use hydrogen as a raw material in processes: in this case, the reference price is indexed to the average methane price of the previous month in the virtual hub representing the place of exchange and sale of natural gas on the national network, taking into account the typical efficiency of the thermochemical processes for the production of gray hydrogen.

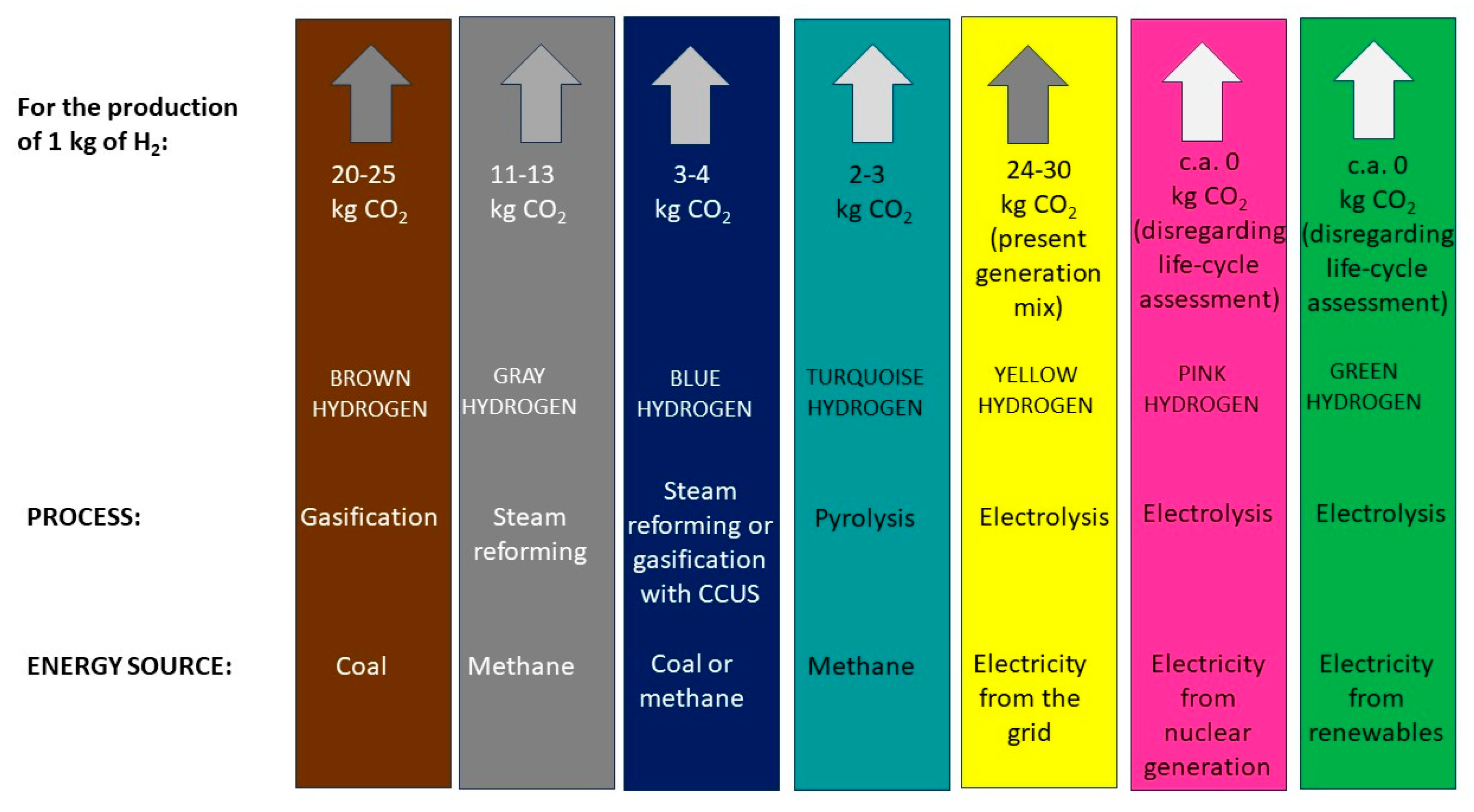

3. Hydrogen as a Feedstock

4. Hydrogen as an Energy Vector

4.1. Industry Sector

- steel production and processing,

- foundries (steel, cast iron, and non-ferrous metals),

- cement,

- glass,

- ceramics,

- paper,

- transport.

- increasing energy efficiency, especially through the recovery of energy from thermal waste;

- electrification of the processes, particularly by exploiting availability of electricity from renewable sources;

- use of alternative fuels (from biomass and recycled materials) to replace fossil fuels;

- circular economy practices that reduce both raw material consumption and the amount of byproducts to be disposed, along with the associated emissions;

- carbon capture and sequestration;

- use of hydrogen-based technologies to replace materials and fossil fuels;

- sector analysis.

- Hydrogen has a high flame speed compared to carbon-containing fuels and a non-luminous flame, making optical monitoring difficult. These challenges can be partially overcome by using hydrogen/ammonia mixtures, as ammonia burns at a much slower rate and with a visible flame, also helping to reduce nitrogen oxide emissions [39,40,41,42].

- Hydrogen flames achieve relatively low heat transfer by radiation compared to other fuels, necessitating the introduction of other carbon-free fluids. In the cement industry, for instance, clinker dust is used in the fuel stream. It may be necessary to redesign current burners to handle any new additives introduced (e.g., to manage the abrasive properties of clinker dust) [43,44].

- Hydrogen causes corrosion and embrittlement when in contact with certain metals, requiring new coatings and other protective measures [45].

- optimize solutions to be competitive with conventional solutions,

- assess the advantages and disadvantages of current and developing technological solutions to choose the most convenient one based on production goals and decarbonization needs.

4.2. Transportation Sector

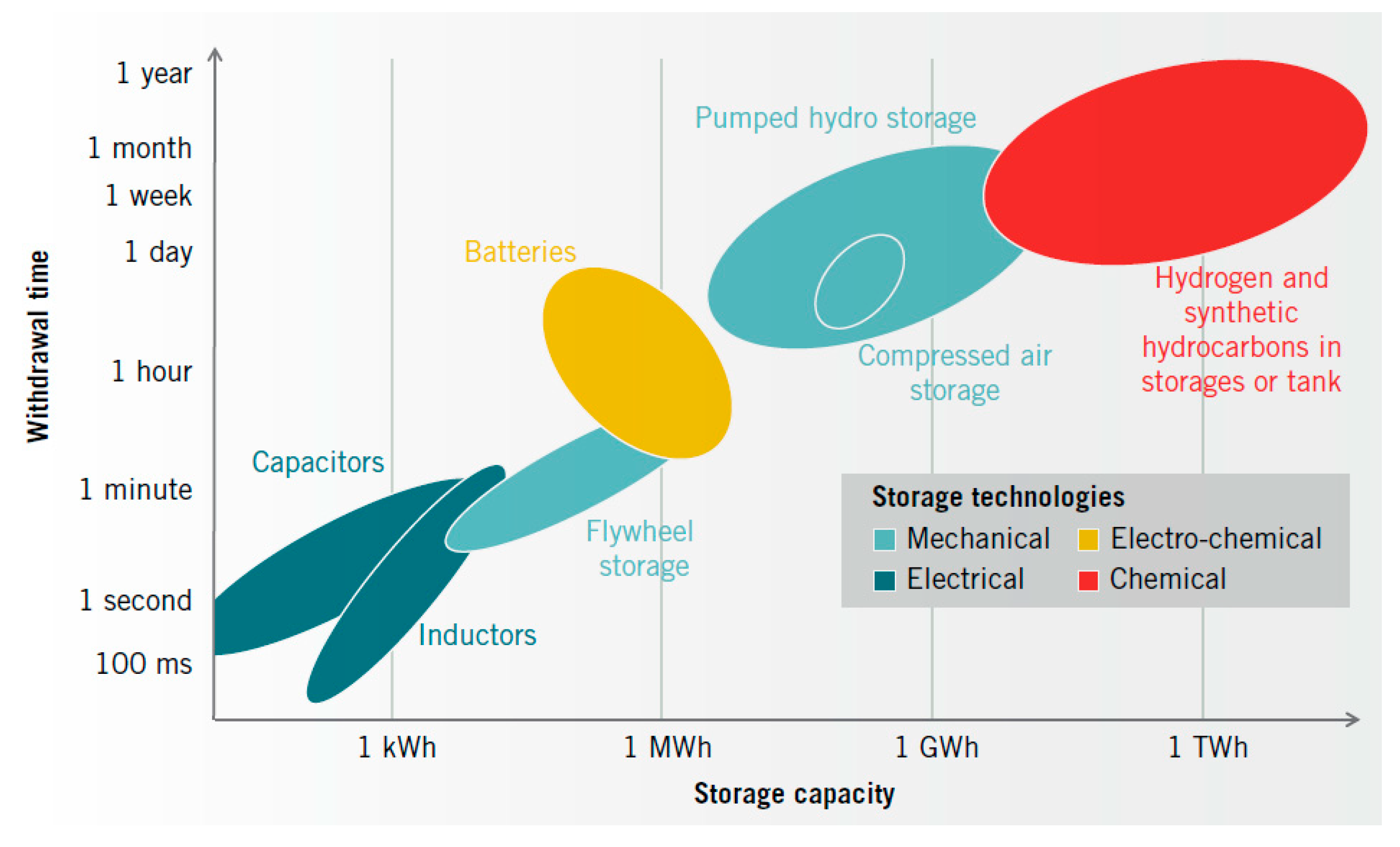

5. Hydrogen Storage and Interaction with the Electric Grid

- Europe benefits from a significant hydrogen storage potential due to the presence of important geological salt structures across the continent; these are particularly concentrated in the north of Europe.

- The estimated technical storage potential of 85,000 TWh significantly exceeds expected H2 production from curtailed VRES in 2030 (17 to 33 TWh), but also third-party estimates of required H2 storage in the same period are up to 70 TWh.

- However, the majority of possible sites are currently not in use and are located offshore, which may require both significant investments and medium-term timeframes before they can be commissioned. This introduces a certain degree of uncertainty about actually available storage volume by 2030.

- In addition, storage and VRES potential are unevenly distributed across Europe. Although the location of salt cavern large-scale storage sites largely coincides with Northern offshore wind potential, there are very few viable sites in the south of Europe, where the most significant PV generation potential is located.

- This could have important implications for the integration of VRES generation into existing networks in these areas, as the flexibility provided by large-scale hydrogen storage in salt caverns would be reduced and/or rely on appropriate power and/or hydrogen infrastructure to link electrolyzers with demand centers and/or storage sites.

- Hydrogen is characterized by a Lower Heating Value (LHV) of approximately 120 MJ/kg, greater, for example, than both methane (approximately 50 MJ/kg) and petrol (approximately 45 MJ/kg). Unlike the latter, however, as it has a low density under atmospheric conditions (approximately 0.089 kg/m3), it has a lower LHV per unit of volume, equal to approximately 10.8 MJ/Nm3 (0.010 MJ/L). In the context of storage, hydrogen requires larger volumes than traditional fossil fuels due to its low density. To overcome this shortcoming, hydrogen can be compressed, liquefied, or incorporated into energy carriers such as ammonia, methanol, and other liquid organic carriers (so-called LOHC: Liquid Organic Hydrogen Carriers) [87]. However, the transformation of hydrogen in LOHC is subject to very low conversion efficiency (e.g., the efficiency of the transformation of hydrogen into ammonia is only 29%), which further reduces the already low efficiency of electrolyzers—see next point.

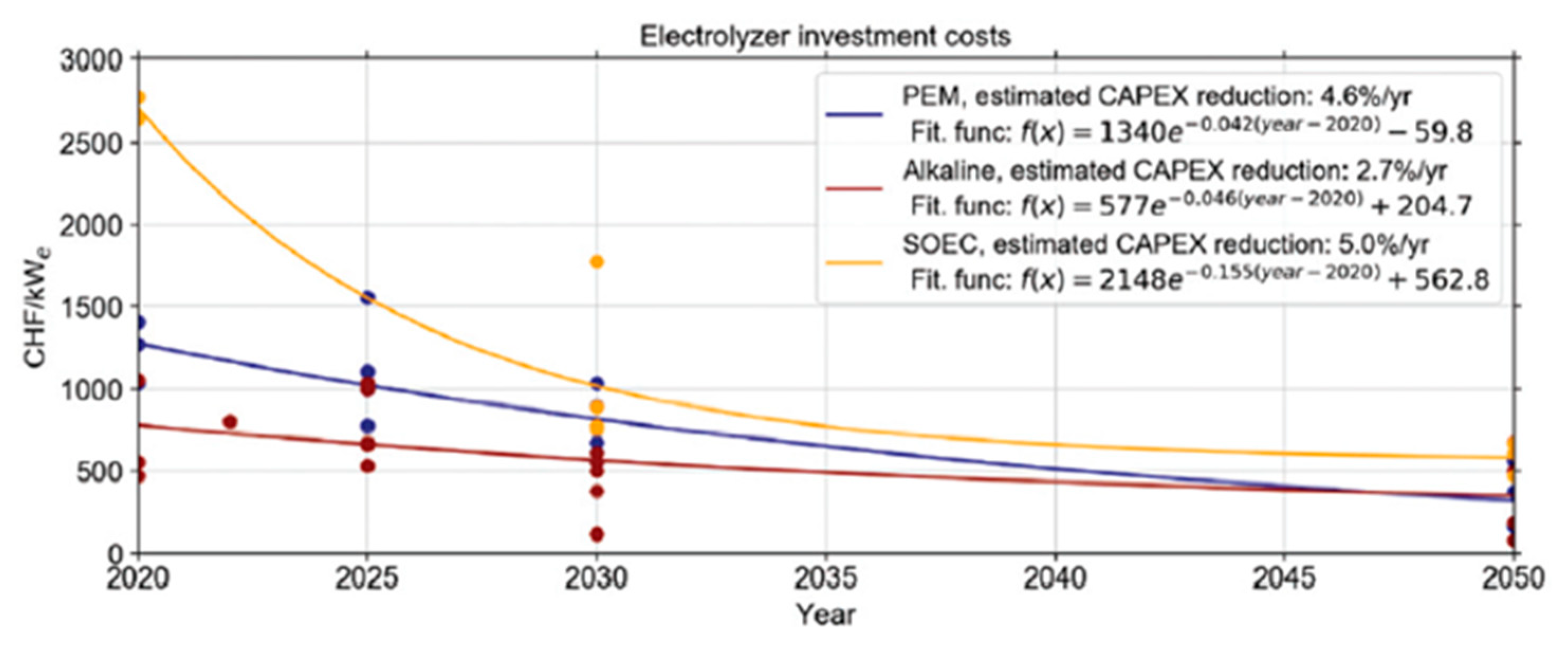

- The transformation from electric carrier to hydrogen and vice versa occurs through electrolysis and fuel cells, respectively. As it already happened in the renewables sector, technologies costs are rapidly decreasing. In fact, the cost of the electrolyzers has dropped by over 60% in the last ten years and is expected to halve further by 2030, thanks to technological developments and economies of scale [88,89]. However, the efficiency of the conversion process implemented by the electrolyzers is very low (currently 64% according to the IEA), and there are thermodynamic limits that suggest that it is not possible to achieve strong increases in efficiency with the current technologies. The efficiency of the conversion process from hydrogen to electricity, implemented by fuel cells, is also very low (around 30%). Therefore, a conversion from the electric carrier to hydrogen for storage and then back to electricity would be affected by an overall efficiency equal to the product of the efficiencies of the two processes applied in cascade (i.e., 38%). All this strongly advises against the accumulation of electrical energy in the form of hydrogen if it is then necessary to implement the reverse transformation into electrical energy unless there will be strong technological improvements in the medium to long term. In the case of electrical sectors where it is necessary to both power an electrical load and supply hydrogen as a raw material, the best option from an energy point of view is to decouple the storage elements, installing both electrolyzers and batteries in parallel.

6. Evolution of Hydrogen Supply

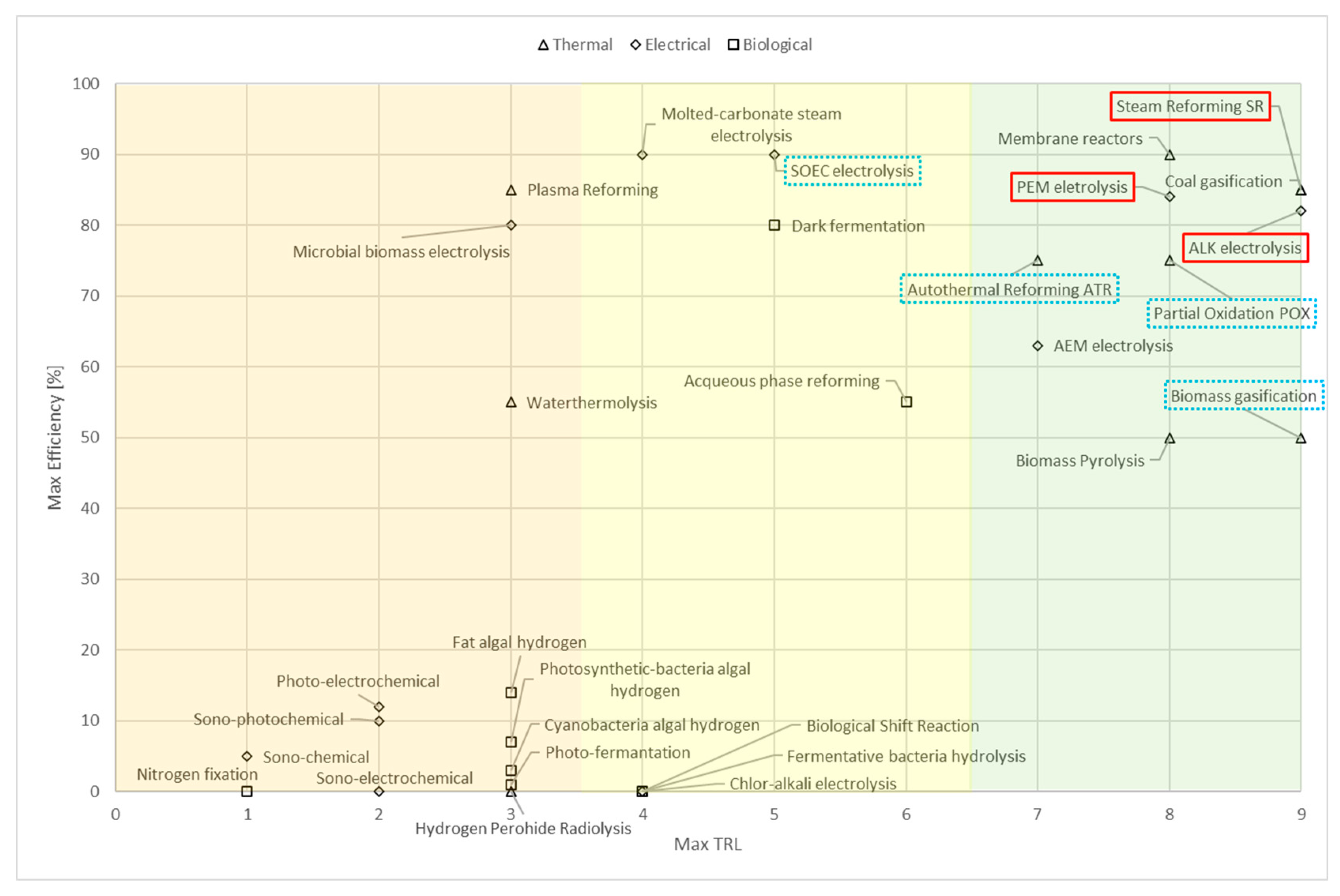

- technology readiness level TRL (which is a widely recognized classification method for estimating the maturity of technologies [99]),

- real carbon emissions and impact,

- produced hydrogen purity level.

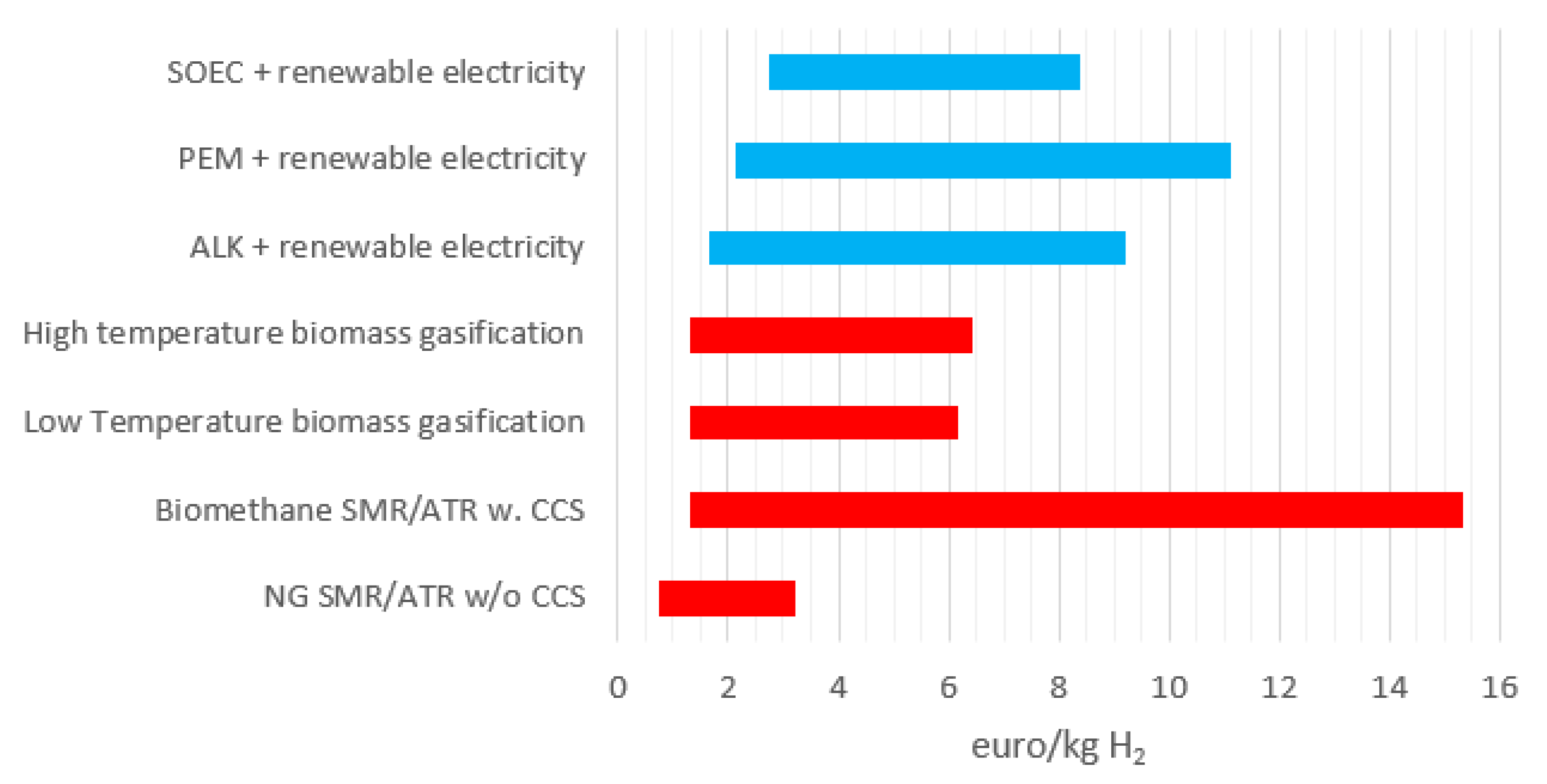

- Thermal processes: Steam Methane Reforming (SMR) is the most common technology globally used for hydrogen production, involving the reforming of methane gas with steam. Variations in this process include the use of air or oxygen, as seen in emerging solutions such as Partial Oxidation (POX) and Auto-Thermal Reforming (ATR). In 2022, 99.7% of the global hydrogen production has been achieved using SMR [38]. The extent of low-carbon emissions from SMR, POX, or ATR largely depends on future advancements in Carbon Capture, Usage, and Storage (CCUS) technologies [105]. Many national strategies consider the transition from “grey” to “blue” hydrogen as a necessary preliminary step toward decarbonizing modern hydrogen production [92,93,94,95]. “Blue” hydrogen production, in particular, offers a commercially viable solution that is ready for deployment, requiring fewer critical raw materials (mainly nickel as a catalyst, absent in POX) [114,119]. Biomass gasification, a well-established technology originally investigated for coal gasification, has recently been proposed for hydrogen production. This process involves separating H2 from the resulting Syngas mixture, utilizing various gasifier configurations (entrained bed, fixed bed, fluidized bed, etc.) Despite being an intriguing solution due to its potential for a negative carbon emission balance, biomass gasification faces challenges. Pyrolysis within the reactor can produce liquid components such as tar [120], a mixture of compounds like benzene, toluene, aromatics hydrocarbons which can obstructs post-gasification ducts of the plant. This obstruction requires frequent substitution of filters and other components leading to increased maintenance costs and operational interruptions. These challenges currently limit the broader implementation of biomass gasification and justify the ongoing development of solutions for these issues [102,120,121,122]:

- Electrical processes: Considered as the main low carbon emitting technologies for hydrogen production, the earliest electrolyzers were based on the Alkaline ALK technology. This production solution was developed in the XIX century, and it has been further refined to achieve yields up to 80%, thanks to the enhancement of the electrolytic solution’s reactivity through the addition of KOH or NaOH at a 30% molar concentration (55 kWh/kg H2) [104,114,123]. ALK electrolyzers are less expensive than membrane electrolyzers, such us proton exchange membrane (PEM). Nickel-based electrodes are the only components classified as “critical raw materials” by the European Commission [124]. In contrast, PEM electrolyzers, while more costly, offer ALK comparable performances (58 kWh/kg H2) but produce hydrogen with a higher degree of purity. However, they contain several critical materials, including Iridium Ir and Platinium Pt for the electrodes and Titanium Ti for the double-polarized layer [124,125]. Although electrolysis is a well-established solution, ALK technology suffers from efficiency drops due to rippling in the input electricity, resulting from low-efficiency rectification processes. This issue can reduce plant yield by up to 20% under low-load conditions [126,127,128]. Conversely, PEM performances are less compromised at variable load conditions [125]. AEM (Anion Exchange Membrane) electrolyzers represent a promising hybrid solution, combining technical advantages of ALK and PEM technologies: high purity levels, high electrolysis reactivity under fluctuant input loads, with higher efficiency (53 kWh/kg H2). However, AEM technology is still under development, with only a few examples currently available on the market [106].

- Although only a small group of technologies is mentioned in today’s national strategies compared to the total number being investigated for hydrogen production, the most promising technologies in the medium-term are those that leverage synergies with already mature technologies, allowing for performance improvements (such as the combination with electrolysis and/or gasification processes). Moreover, the general trend in decreasing prices for technologies with advanced TRL in the long term makes the implementation of these ‘synergistic methods’ even more promising. The strategies already demonstrate how reforming methods are excellent commercially viable solutions for CCS solutions, enabling the decarbonization of existing production and subsequently allowing the implementation of other solutions, such as coupling electrolysis (coupling with sonolysis and/or photolysis) and biomass gasification.

- It is not necessarily required to achieve the highest levels of purity for the use of the produced hydrogen. In fact, there are differences shown in Table 5 that display varying levels of purity between hydrogen produced for research purposes and hydrogen produced for applications in civilian sectors. Although this may be an inclusive factor for technologies other than PEM, improvements still need to be made to enable all technologies considered to produce hydrogen with purity levels such that it can be used without additional costs for post-production treatments (an example is biomass gasification).

- Critical materials are a risk factor for every technology involved in hydrogen production, and technologies that enable higher purity levels contain various critical materials (e.g., PEM). Despite the potential for coupling electrolysis with other phenomena, it is evident that efforts must be made to reduce the quantities of critical materials by investigating alternative materials that do not compromise the performance of the plant.

- Biomass-based production offers promising prospects in the long term, allowing for negative emissions in the lifecycle of the raw material. Nonetheless, the technology must address greater technical definition and consider that the feedstock is limited and regulated by the availability of biomass [134]. Similarly, other technologies based on renewable electrolysis also have limitations defined by the geomorphological context and geographical location (amount of wind and sunlight). This suggests that a heterogeneous technological approach, based on enhanced electrolysis and biomass, could allow for a diversification of supply, making it as dependent as possible on the seasonality of renewables and economically sustainable.

7. Hydrogen as a Commodity

- as a series of cascading auctions some on the day ahead and some closer to real time,

- as a continuous market managed with peer-to-peer techniques.

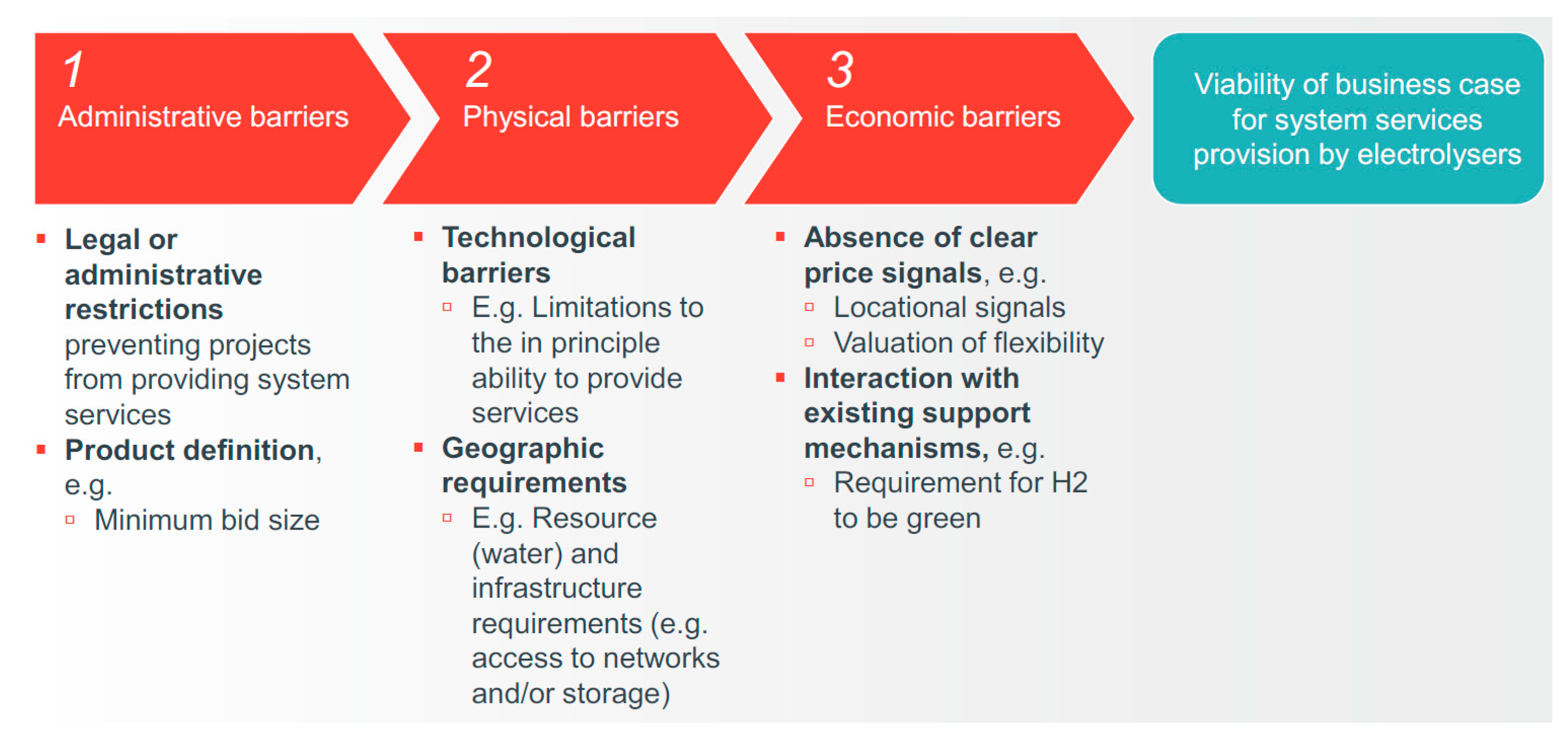

- As electricity is a key input for an electrolyzer (to be provided either locally or, more likely, from the grid), electricity prices are an important element to define the profitability for those who will invest in electrolyzers. The possibility for an electrolyzer to be useful to provide services to the electric grid strongly depends on its geographic location. Also, the availability of spare capacity beyond what has to be provided to industrial clients with which PPAs have been stipulated is of course important. Both these factors are potentially strongly influenced by possible support mechanisms hydrogen producers will perceive, impacting strategic decisions like location, plant size, and key revenue source. A business case focusing on system services may be characterized by a very high degree of uncertainty and therefore be a less viable business case with respect to other ones focused on decarbonization needs for specific industrial users.

- There are several kinds of barriers that could limit the viability of a business case tied to the provision of ancillary services by hydrogen storage owners (see Figure 17): administrative barriers, physical barriers, economic barriers.

8. Research Needs for the Next Years

- development of catalysts, currently primarily based on platinum group metals (PGM), with low quantities or free from critical raw materials for electrolyzers and fuel cells;

- research on advanced materials for hydrogen storage (e.g., carbon fibers, H2 carriers, etc.);

- study for an advanced understanding of the performance and durability mechanisms of electrolyzers and fuel cells.

8.1. Production

- Increasing the efficiency and robustness of the stack and developing high-pressure technology to reduce/eliminate the subsequent compression phase.

- Developing innovative components to optimize and reduce losses and costs.

- Conducting R&D activities on low-carbon hydrogen production technologies other than electrolysis:

- Production of “blue” hydrogen from hydrocarbons, with carbon capture, utilization, and storage (CCUS).

- Flexible coproduction of electricity, heat, and hydrogen from woody biomass.

- Production from biomass with negative emissions.

- Methane pyrolysis with carbon black storage.

- Fostering the development of emerging technologies:

- Anion exchange membrane electrolysis (AEMEL) and proton-conducting ceramic electrolysis (PCCEL) processes.

- Developing innovative materials and devices for photoelectrolysis, photoelectrocatalysis, and phonocatalysis of water (solar energy + ultrasonic mechanical stimulation) based on non-critical materials, for the direct conversion of solar energy into hydrogen or hydrogen carriers.

8.2. Storage

- To support the development of compression, liquefaction, absorption on solids, and new materials technologies, while for long-term storage, the study of efficient, stable, and safe solutions for injection into salt caverns, depleted gas fields, marine deposits, and resolving local methanation issues due to microorganisms in the presence of fossil carbon is required;

- To develop innovative materials for the creation of more economical and safer cryogenic tanks and cryo-compressed hydrogen technology with effective integration between fuel cells and onboard hydrogen storage in vehicles, ships, trains, and airplanes;

- To optimize and improve the efficiency of hydrogen transformation into other energy carriers such as ammonia, methanol, and e-fuels.

8.3. Transport

8.4. Utilization

- Development of technologies for the use of hydrogen as a raw material in place of fossil fuels, particularly in steel production (where the technology has already reached TRL 8);

- Development of technical solutions for adapting the use of hydrogen as an energy carrier in high-temperature processes in “hard to abate” sectors (upgrade and development of new burners, furnaces, etc.);

- Definition of new industrial processes and prototypes involving the use of hydrogen and identification of necessary components;

- Development of products in the micro-CHP (residential) and mini-CHP (commercial/tertiary) sectors that can be powered transitorily by biogas, syngas, ammonia, natural gas (blended with H2), and in perspective, with fully renewable fuels or carriers;

- Research of efficient and economical applications for residential heating;

- For maritime transport: development of modular and high-power density fuel cells, as SOFC (Solid Oxide Fuel Cell) and MCFC (Molten Carbonate Fuel Cell) capable of using a diversified range of fuels and study suitable refueling solutions in ports (liquid hydrogen, hydrides, other carriers);

- For air transport: development of efficient solutions for the production of e-fuels;

- For rail and road transport: development of fuel cell technologies to increase efficiency, modularity, and cost-effectiveness.

9. Conclusions

Funding

Conflicts of Interest

References and Note

- Technologies to Decarbonise the EU Steel Industry. Available online: https://publications.jrc.ec.europa.eu/repository/handle/JRC127468 (accessed on 11 June 2024).

- Cavaliere, P. Clean Ironmaking and Steelmaking Processes: Efficient Technologies for Greenhouse Emissions Abatement; Springer Nature: Cham, Switzerland, 2019; ISBN 978-3-030-21209-4. [Google Scholar] [CrossRef]

- Italian Ministry of Transport. Decarbonising Transport. April 2022. Available online: https://www.mit.gov.it/nfsmitgov/files/media/notizia/2022-06/STEMI_Decarbonising%20Transport_ENG.pdf (accessed on 8 July 2024).

- European Council. Fit for 55. Available online: https://www.consilium.europa.eu/en/policies/green-deal/fit-for-55 (accessed on 11 June 2024).

- European Commission. REPowerEU at a Glance. Available online: https://commission.europa.eu/strategy-and-policy/priorities-2019-2024/european-green-deal/repowereu-affordable-secure-and-sustainable-energy-europe_en (accessed on 11 June 2024).

- Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions—A Hydrogen Strategy for a Climate-Neutral Europe. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52020DC0301 (accessed on 11 June 2024).

- European Commission. Key Actions of the EU Hydrogen Strategy. Available online: https://energy.ec.europa.eu/topics/energy-systems-integration/hydrogen/key-actions-eu-hydrogen-strategy_en (accessed on 11 June 2024).

- Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions—Powering a Climate-Neutral Economy: An EU Strategy for Energy System Integration. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=COM:2020:0299:FIN (accessed on 11 June 2024).

- Communication from the Commission Criteria for the Analysis of the Compatibility with the Internal Market of State Aid to Promote the Execution of Important Projects of Common European Interest. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?toc=OJ%3AC%3A2021%3A528%3ATOC&uri=uriserv%3AOJ.C_.2021.528.01.0010.01.ENG (accessed on 11 June 2024).

- Clean Hydrogen Partnership. Available online: https://www.clean-hydrogen.europa.eu/index_en (accessed on 11 June 2024).

- Directive (EU) 2023/2413 of the European Parliament and of the Council of 18 October 2023 amending Directive (EU) 2018/2001, Regulation (EU) 2018/1999 and Directive 98/70/EC as Regards the Promotion of Energy from Renewable Sources, and Repealing Council Directive (EU) 2015/652. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32023L2413 (accessed on 11 June 2024).

- Regulation (EU) 2023/2405 of the European Parliament and of the Council of 18 October 2023 on Ensuring a Level Playing Field for Sustainable air Transport (ReFuelEU Aviation). Available online: https://eur-lex.europa.eu/eli/reg/2023/2405/oj (accessed on 11 June 2024).

- Regulation (EU) 2023/1805 of the European Parliament and of the Council of 13 September 2023 on the Use of Renewable and Low-Carbon Fuels in Maritime Transport, and Amending Directive 2009/16/EC (Text with EEA Relevance). Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32023R1805 (accessed on 10 September 2024).

- Regulation (EU) 2023/1804 of the European Parliament and of the Council of 13 September 2023 on the Deployment of Alternative Fuels Infrastructure, and Repealing Directive 2014/94/EU (Text with EEA Relevance). September 2023. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32023R1804 (accessed on 8 July 2024).

- Commission Delegated Regulation (EU) 2023/1184 of 10 February 2023 Supplementing Directive (EU) 2018/2001 of the European Parliament and of the Council by Establishing a Union Methodology Setting out Detailed Rules for the Production of Renewable Liquid and Gaseous Transport fuels of Non-Biological Origin. Available online: https://eur-lex.europa.eu/eli/reg_del/2023/1184/oj (accessed on 11 June 2024).

- Commission Delegated Regulation (EU) 2023/1185 of 10 February 2023 Supplementing Directive (EU) 2018/2001 of the European Parliament and of the Council by Establishing a Minimum Threshold for Greenhouse Gas Emissions Savings of Recycled Carbon Fuels and by Specifying a Methodology for Assessing Greenhouse Gas Emissions Savings from Renewable Liquid and Gaseous Transport Fuels of Non-Biological Origin and from Recycled Carbon Fuels. Available online: https://eur-lex.europa.eu/eli/reg_del/2023/1185/oj (accessed on 24 June 2024).

- Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions on the European Hydrogen Bank. Available online: https://eur-lex.europa.eu/legal-content/EN/ALL/?uri=COM%3A2023%3A156%3AFIN (accessed on 11 June 2024).

- European Climate, Infrastructure and Environment Executive Agency. Available online: https://cinea.ec.europa.eu/index_en (accessed on 11 June 2024).

- Directive of the European Parliament and of the Council on Common Rules for the Internal Markets for Renewable Gas, Natural Gas and Hydrogen, Amending Directive (EU) 2023/1791 and Repealing Directive 2009/73/EC (Recast). Available online: https://data.consilium.europa.eu/doc/document/PE-104-2023-INIT/en/pdf (accessed on 11 June 2024).

- Regulation of the European Parliament and of the Council on the Internal Markets for Renewable Gas, Natural Gas and Hydrogen, Amending Regulations (EU) No 1227/2011, (EU) 2017/1938, (EU) 2019/942 and (EU) 2022/869 and Decision (EU) 2017/684 and Repealing Regulation (EC) No 715/2009 (Recast). Available online: https://data.consilium.europa.eu/doc/document/PE-105-2023-INIT/en/pdf (accessed on 11 June 2024).

- ENTSO-E Ten-Year Network Development Plan. Available online: https://tyndp.entsoe.eu/ (accessed on 12 June 2024).

- ENTSOG Ten-Year Network Development Plan. Available online: https://www.entsog.eu/tyndp (accessed on 12 June 2024).

- ENTSO-E. Available online: https://www.entsoe.eu/ (accessed on 12 June 2024).

- ENTSOG. Available online: https://www.entsog.eu/ (accessed on 12 June 2024).

- Agency for the Cooperation of Energy Regulators (ACER). Available online: https://www.acer.europa.eu/ (accessed on 12 June 2024).

- Strategia Nazionale Idrogeno—Linee Guida Preliminari. Available online: https://www.mimit.gov.it/images/stories/documenti/Strategia_Nazionale_Idrogeno_Linee_guida_preliminari_nov20.pdf (accessed on 12 June 2023).

- Piano Nazionale Integrato per l’Energia e Clima (PNIEC). Available online: https://www.mase.gov.it/comunicati/pubblicato-il-testo-definitivo-del-piano-energia-e-clima-pniec (accessed on 12 June 2024).

- Piano Nazionale di Ripresa e Resilienza (PNRR). Available online: https://www.italiadomani.gov.it/content/sogei-ng/it/it/home.html (accessed on 12 June 2024).

- Consultazione Pubblica Decreto Sugli Incentivi Alla Produzione di Idrogeno Rinnovabile. Available online: https://www.mase.gov.it/sites/default/files/02_Consultaz%20pubblica%20schema%20DM%20Incentivi%20H2.pdf (accessed on 12 June 2024).

- Hydrogen Europe, Hydrogen Roadmap Europe—A Sustainable Pathway for the European Energy Transition. 2019. Available online: https://www.clean-hydrogen.europa.eu/media/publications/hydrogen-roadmap-europe-sustainable-pathway-european-energy-transition_en (accessed on 10 September 2024).

- European Union, COM(2020) 301 Final “A Hydrogen Strategy for a Climate-Neutral EUROPE”. 2020. Available online: https://eur-lex.europa.eu/legal-content/IT/TXT/?uri=CELEX%3A52020DC0301 (accessed on 10 September 2024).

- Ministère de l’économie des Finances et de la Souveraineté Industrielle et Numérique. Stratégie Nationale Pour le Développement de L’hydrogène Décarboné en France. 2020. Available online: https://www.entreprises.gouv.fr/fr/strategies-d-acceleration/strategie-nationale-pour-developpement-de-l-hydrogene-decarbone-france (accessed on 10 September 2024).

- Bundesministerium für Wirtschaft und Klimaschutz. Die Nationale Wasserstoffstrategie. 2020. Available online: https://www.bmwk.de/Redaktion/DE/Publikationen/Energie/die-nationale-wasserstoffstrategie.pdf?__blob=publicationFile (accessed on 10 September 2024).

- NWP Nationaal Waterstof Programma. Government Strategy on Hydrogen. 2020. Available online: https://nationaalwaterstofprogramma.nl/default.aspx (accessed on 10 September 2024).

- Ministerio Para la Transición Ecológica y el Reto Demográfico. Hydrogen Roadmap: A Commitment to Renewable Hydrogen. 2020. Available online: https://www.miteco.gob.es/en/energia/novedades/publicacion-hoja-de-ruta-del-hidrogeno-apuesta-hidrogeno-renovable.html (accessed on 10 September 2024).

- Norwegian Ministry of Climate and Environment. The Norwegian Government’s Hydrogen Strategy. 2021. Available online: https://www.regjeringen.no/contentassets/40026db2148e41eda8e3792d259efb6b/y-0127e.pdf (accessed on 10 September 2024).

- GOV.UK, Department for Energy Security and Net Zero. UK Hydrogen Strategy. 2021. Available online: https://www.gov.uk/government/publications/uk-hydrogen-strategy (accessed on 10 September 2024).

- IEA, Global Hydrogen Review 2023. Available online: https://www.iea.org/reports/global-hydrogen-review-2023 (accessed on 10 September 2024).

- Vetkin, A.V.; Suris, A.L.; Litvinova, O.A. Investigation of combustion characteristics of methane-hydrogen fuels. Therm. Eng. 2014, 62, 64–67. [Google Scholar] [CrossRef]

- Menzies, M. Hydrogen: The Burning Question. CEng MIChemE. 23 September 2019. Available online: https://www.thechemicalengineer.com/features/hydrogen-the-burning-question/ (accessed on 10 September 2024).

- Faraci, E.; Nastro, F.; Greguoldo, J.; Kemminger, A. Developing and Enabling H2 Burner Utilization to Produce Liquid Steel in EAF. 2023. Available online: https://www.devh2eaf.eu/downloads/Developing%20and%20Enabling%20H2%20Burner%20Utilization%20to%20Produce%20Liquid%20Steel%20in%20EAF%20(Paper).pdf (accessed on 10 September 2024).

- GREENSTEEL. Green Steel for Europe: Supports the EU towards Achieving the 2030 Climate and Energy Targets and the 2050 Long-Termstrategy for a Climate Neutral Europe, with Effective Solutions for Clean Steelmaking. [EP-PP-CLEAN-STEEL—882151]. 2020. Available online: https://www.estep.eu/projects/estep-projects/green-steel-for-europe (accessed on 10 September 2024).

- GREENEAF2. Biochar for a Sustainable EAF Steel Production. RFSP-CT-2014-00003, 01/07/2014-30/06/2016. Available online: https://op.europa.eu/en/publication-detail/-/publication/7198c147-22b2-11e9-8d04-01aa75ed71a1/language-en (accessed on 10 September 2024).

- GREENEAF. Sustainable EAF Steel Production. Final Report, EUR 26208. 2013. Available online: https://op.europa.eu/en/publication-detail/-/publication/e7dc500c-82de-4c2d-8558-5e24a2d335fb/language-en (accessed on 10 September 2024).

- Li, J.; Huang, H.; Kobayashi, N.; He, Z.; Nagai, Y. Study on using hydrogen and ammonia as fuels: Combustion characteristics and NOx formation. Int. J. Energy Res. 2014, 38, 1214–1223. [Google Scholar] [CrossRef]

- Verhelst, S. Recent progress in the use of hydrogen as a fuel for internal combustion engines. Int. J. Hydrogen Energy 2014, 39, 1071–1085. [Google Scholar] [CrossRef]

- Hoenig, V.; Hoppe, H.; Emberger, B. Carbon capture technology—Options and potentials for the cement industry. Int. J. Energy Res. 2014, 3022, 98. [Google Scholar]

- CEMBUREAU. 2050 Carbon Neutrality Roadmap. 2019. Available online: https://cembureau.eu/media/w0lbouva/cembureau-2050-roadmap_executive-summary_final-version_web.pdf (accessed on 10 September 2024).

- Mineral Products Association. Options for Switching UK Cement Production Sites to Near Zero CO2 Emission Fuel: Technical and Financial Feasibility. 2019. Available online: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/866365/Phase_2_-_MPA_-_Cement_Production_Fuel_Switching.pdf (accessed on 10 September 2024).

- Duarte, P. Hydrogen-Based Steelmaking. Millennium Steel. 2019, pp. 18–22. Available online: https://www.millennium-steel.com/hydrogen-based-steelmaking/ (accessed on 10 September 2024).

- Sadoway, D. Decarbonizing the Production of Steel. Webinar. LowCarbonFuture Project, EU Grant Agreement N. 800643. 2019. Available online: https://www.youtube.com/watch?v=zFDFHXujWEI (accessed on 10 September 2024).

- Hydrogen Council. Path to Hydrogen Competitiveness—A Cost Perspective. 2020. Available online: https://hydrogencouncil.com/wp-content/uploads/2020/01/Path-to-Hydrogen-Competitiveness_Full-Study-1.pdf (accessed on 10 September 2024).

- Ministry of Economy, Trade and Industry of Japan. Basic Hydrogen Strategy. 2023. Available online: https://www.meti.go.jp/shingikai/enecho/shoene_shinene/suiso_seisaku/pdf/20230606_5.pdf (accessed on 10 September 2024).

- Tenova. Progetto “Dalmine Zero Emissions”. 2019. Available online: https://www.siderweb.com/articoli/news/708648-tenaris-dalmine-verso-l-acciaio-a-idrogeno (accessed on 10 September 2024).

- AITEC, Federbeton. La Strategia di Decarbonizzazione del Settore del Cemento. 2021. Available online: https://www.federbeton.it/Portals/0/PubDoc/Pubblicazioni/Rapporti/La_strategia_di_decarbonizzazione_del_settore_del_cemento_brief.pdf?ver=4A-WdgbS7dzcTlxX7gC0dA%3D%3D (accessed on 10 September 2024).

- Perilli, D. Green Hydrogen for Grey Cement, Global Cement. 2020. Available online: https://www.globalcement.com/news/item/11061-green-hydrogen-for-grey-cement (accessed on 10 September 2024).

- Morris, G. Hydrogen Consortium Aims to Reduce Glass Emissions. 2020. Available online: https://www.glass-international.com/news/hydrogen-consortium-aims-to-reduce-glass-emissions (accessed on 10 September 2024).

- Boningari, T.; Smirniotis, P.G. Impact of nitrogen oxides on the environment and human health: Mn-based materials for the NOx abatement. Curr. Opin. Chem. Eng. 2016, 13, 133–141. [Google Scholar] [CrossRef]

- Dimitriades, B. Effects of hydrocarbon and nitrogen oxides on photochemical smog formation. Environ. Sci. Technol. 1972, 6, 253–260. [Google Scholar] [CrossRef]

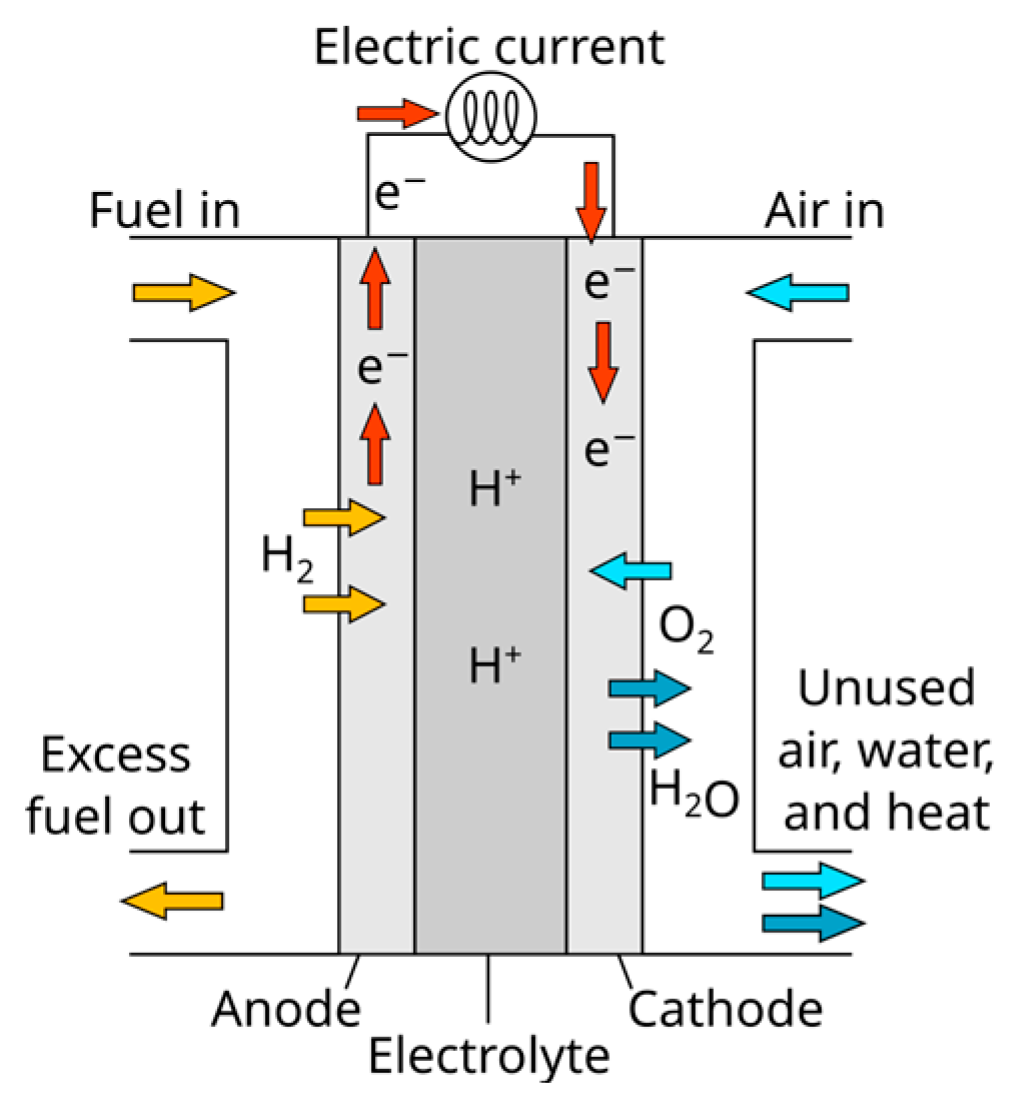

- Wang, Y.; Chen, K.S.; Mishler, J.; Cho, S.C.; Adroher, X.C. A review of polymer electrolyte membrane fuel cells: Technology, applications, and needs on fundamental research. Appl. Energy 2010, 88, 981–1007. [Google Scholar] [CrossRef]

- Wikipedia: Proton-Exchange Membrane Fuel Cell. Available online: https://en.wikipedia.org/wiki/Proton-exchange_membrane_fuel_cell (accessed on 5 September 2024).

- BMW. Electric Cars and Plug-in Hybrid Explained. 2024. Available online: https://www.bmw.com/content/dam/bmw/marketBMWCOM/bmw_com/categories/Innovation/evs-explained/neu/ee-04-media-hd-en.png?imwidth=1920 (accessed on 10 September 2024).

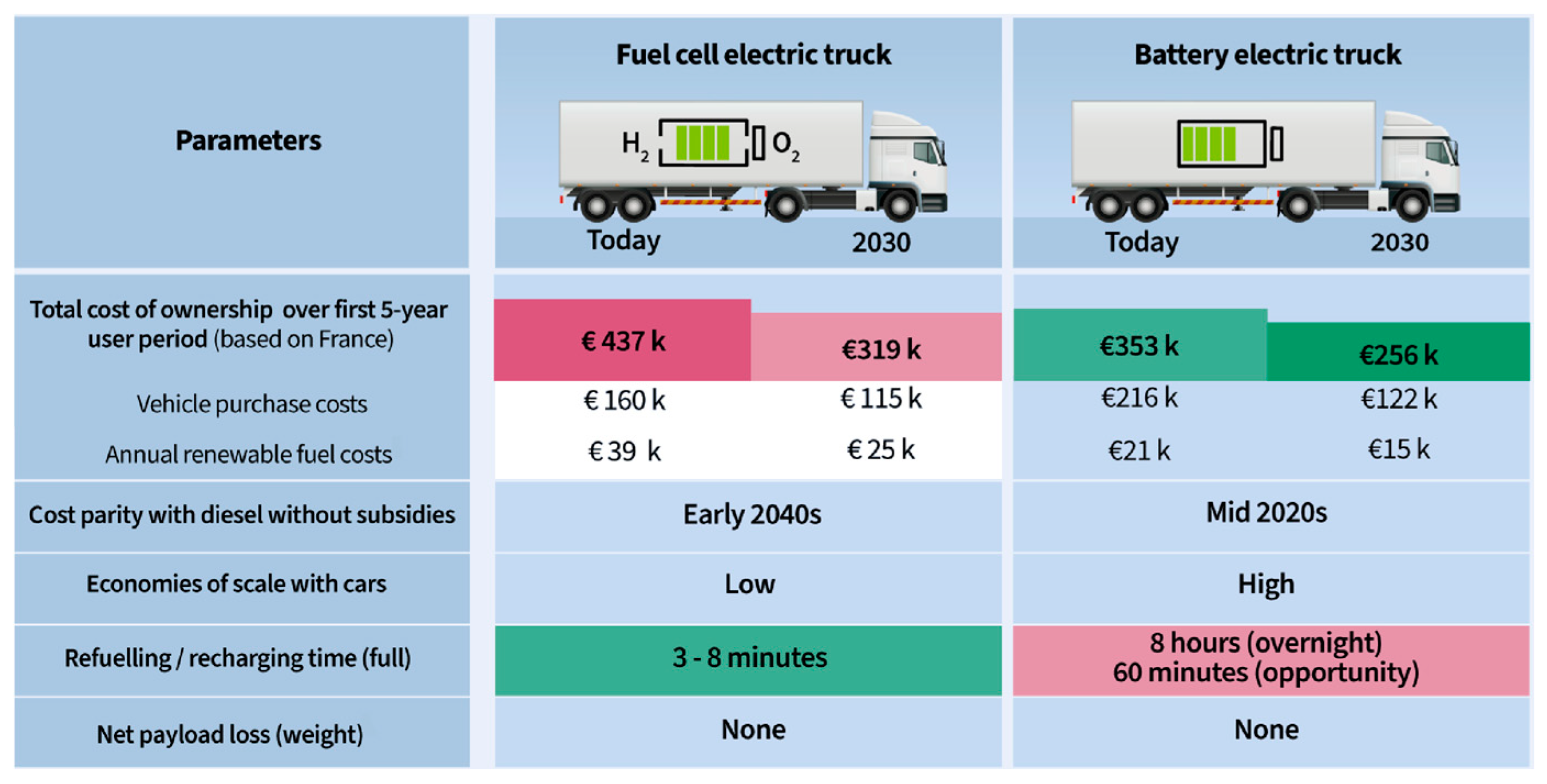

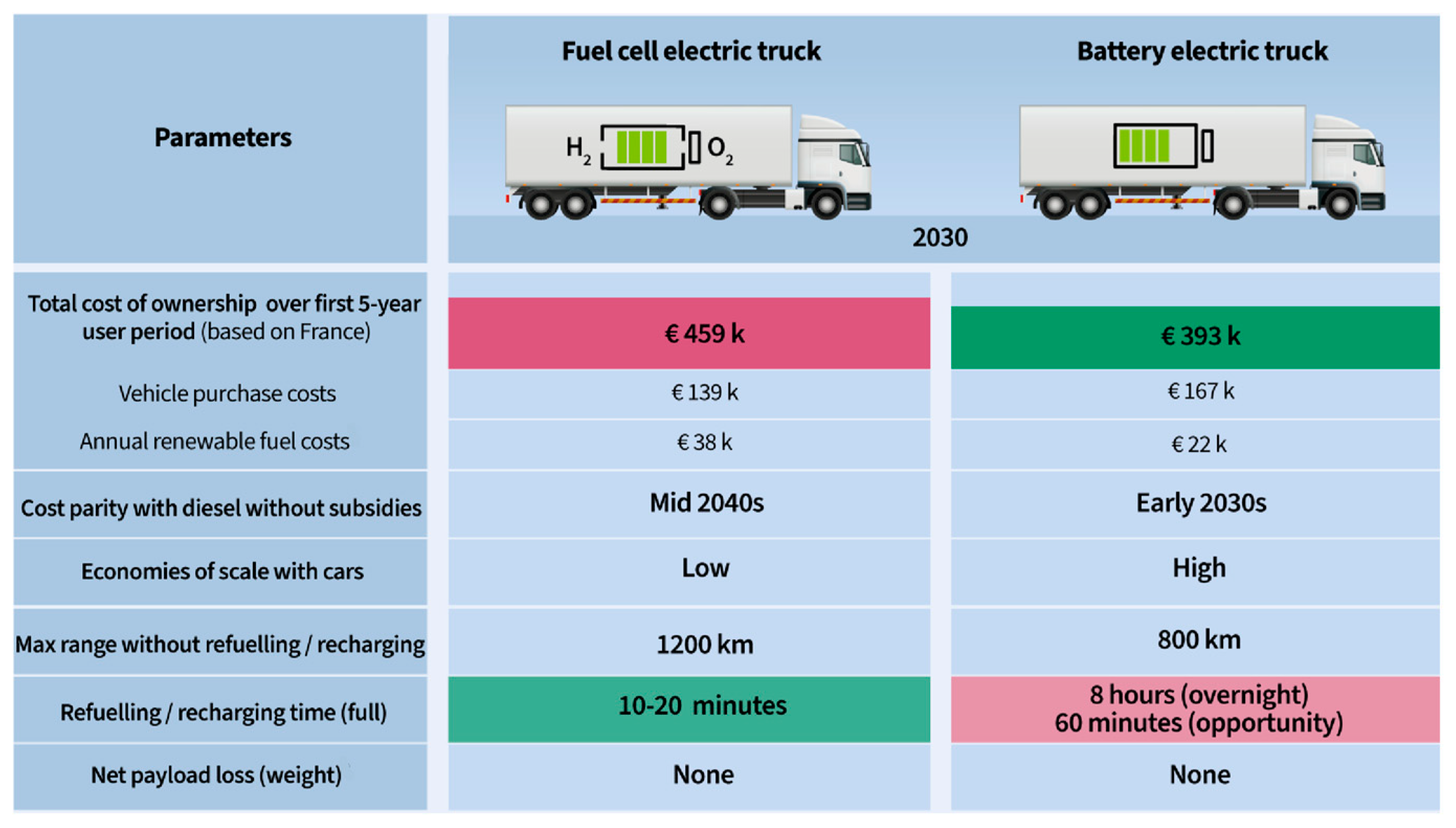

- Transport & Environment, Comparing Hydrogen and Battery Electric Trucks. 2020. Available online: https://www.transportenvironment.org/articles/comparing-hydrogen-and-battery-electric-trucks (accessed on 5 August 2024).

- California Energy Commission, Joint Agency Staff Report on Assembly Bill 8: 2016 Assessment of Time and Cost Needed to Attain 100 Hydrogen Refueling Stations in California. 2017. Available online: https://www.energy.ca.gov/sites/default/files/2021-04/CEC-600-2015-016.pdf (accessed on 10 September 2024).

- Hydrogen Mobility Europe. EMERGING CONCLUSIONS. 2024. Available online: https://h2me.eu/wp-content/uploads/2024/04/D7.20-H2ME-emerging-conclusions-Final-Version.pdf (accessed on 10 September 2024).

- Deloitte, Fueling the Future of Mobility Hydrogen and Fuel Cell Solutions for Transportation. 2020. Available online: https://www2.deloitte.com/content/dam/Deloitte/cn/Documents/finance/deloitte-cn-fueling-the-future-of-mobility-en-200101.pdf (accessed on 10 September 2024).

- International Energy Agency, Fuel Cell Vehicles and Hydrogen Refueling Station Stock by Region. 2020. Available online: https://www.iea.org/data-and-statistics/charts/fuel-cell-vehicles-and-hydrogen-refueling-station-stock-by-region-2020 (accessed on 10 September 2024).

- Clean Technology System. Hydrogen Valley Project Officially Kicks off. September 2023. Available online: https://www.ctsh2.com/news/prende-il-via-ufficiale-al-progetto-transfrontaliero-della-valle-dellidrogeno (accessed on 8 July 2024).

- Vado e Torno Edizioni, Idrogeno, Prospettive e Potenzialità della Propulsione a Zero Emissioni, Autobus, 2019. (In Italian)

- Bloomberg, Electric Vehicle Outlook, BloombergNEF. 2024. Available online: https://assets.bbhub.io/professional/sites/24/847354_BNEF_EVO2024_ExecutiveSummary.pdf (accessed on 10 September 2024).

- Euregio; Hydrogen Masterplan. 2021. Available online: https://www.europaregion.info/fileadmin/downloads/3_Aktuelles_Files/Publikationen/202101-H2-Euregio-Masterplan-IT.pdf (accessed on 8 July 2024). (In Italian).

- H2IT, National Plan for Hydrogen Mobility Development. 2019. Available online: https://www.h2it.it/wp-content/uploads/2019/12/Piano-Nazionale_Mobilita-Idrogeno_integrale_2019_FINALE.pdf (accessed on 8 July 2024). (In Italian).

- Roland Berger, Fuel Cell Electric Buses—Potential for Sustainable Public Transport in Europe A Study for the Fuel Cells and Hydrogen Joint Undertaking, FCH. 2015. Available online: https://www.rolandberger.com/publications/publication_pdf/roland_berger_fuel_cell_electric_buses_20151105.pdf (accessed on 10 September 2024).

- Railway Technology. HYDROFLEX Hydrogen Train. 2019. Available online: https://www.railway-technology.com/projects/hydroflex-hydrogen-train/ (accessed on 8 July 2024).

- RINA. From Today to 2050: Challenges and Opportunities for the Maritime Industry. 2023. Available online: https://scresources.rina.org/media/From-Today-to-2050-Challenges-and-Opportunities-for-the-Maritime-Industry.pdf (accessed on 8 July 2024).

- DNV. Five-Lessons-to-Learn-on-Hydrogen-as-Ship-Fuel. 2021. Available online: https://www.dnv.com/expert-story/maritime-impact/Five-lessons-to-learn-on-hydrogen-as-ship-fuel/ (accessed on 10 September 2024).

- IEEFA. Green vs. Blue Hydrogen: Market, Tech, and Cost Realities. 2022. Available online: https://ieefa.org/events/green-vs-blue-hydrogen-market-tech-and-cost-realities-livestreamed (accessed on 5 August 2024).

- IRENA. Hydrogen from Renewable Power: Technology Outlook for the Energy Transition. International Renewable Energy Agency. 2018. Available online: https://www.irena.org/publications/2018/Sep/Hydrogen-from-renewable-power (accessed on 5 August 2024).

- Odenweller, A.; Ueckerdt, F.; Nemet, G.F.; Jensterle, M.; Luderer, G. Probabilistic feasibility space of scaling up green hydrogen supply. Nat. Energy 2022, 7, 854–865. Available online: https://econpapers.repec.org/article/natnatene/v_3a7_3ay_3a2022_3ai_3a9_3ad_3a10.1038_5fs41560-022-01097-4.htm (accessed on 10 September 2024). [CrossRef]

- World Energy Council, Hydrogen on the Horizon: Hydrogen Demand and Cost Dynamics. World Energy Council. 2021. Available online: https://www.worldenergy.org/assets/downloads/Working_Paper_-_Hydrogen_Demand_And_Cost_Dynamics_-_September_2021.pdf (accessed on 10 September 2024).

- Aarskog, F.G.; Danebergs, J.; Strømgren, T.; Ulleberg, Ø. Energy and cost analysis of a hydrogen driven high speed passenger ferry. Int. Shipbuild. Prog. 2020, 67, 97–123. [Google Scholar] [CrossRef]

- Ricardo Energy & Environment. Study on the Readiness and Availability of Low- and Zero-Carbon Ship Technology and Marine Fuels. 2023. Available online: https://wwwcdn.imo.org/localresources/en/OurWork/Environment/Documents/FFT%20Project/Study%27s%20technical%20proosal_Ricardo_DNV.pdf (accessed on 5 August 2024).

- DNV. Alternative Fuels Insights for the Shipping Industry—AFI Platform. 2023. Available online: https://afi.dnv.com (accessed on 5 September 2024).

- European Union Aviation Safety Agency (EASA). Hydrogen and Its Potential in Aviation. 2024. Available online: https://www.easa.europa.eu/en/light/topics/hydrogen-and-its-potential-aviation (accessed on 22 July 2024).

- Bhaskar, A.; Assadi, M.; Nikpey Somehsaraei, H. Decarbonization of the Iron and Steel Industry with Direct Reduction of Iron Ore with Green Hydrogen. Energies 2020, 13, 758. [Google Scholar] [CrossRef]

- Frontier Economics and ENTSO-E—Potential of P2H2 Technologies to Provide System Services. June 2022. Available online: https://www.entsoe.eu/2022/06/28/entso-e-publishes-a-study-on-flexibility-from-power-to-hydrogen-p2h2/ (accessed on 17 June 2024).

- International Renewable Energy Agency (IRENA) Hydrogen: A Renewable Energy Perspective. Available online: https://www.irena.org/publications/2019/Sep/Hydrogen-A-renewable-energy-perspective (accessed on 13 June 2024).

- International Renewable Energy Agency (IRENA) Innovation Trends in Electrolysers for Hydrogen Production. Available online: https://www.irena.org/publications/2022/May/Innovation-Trends-in-Electrolysers-for-Hydrogen-Production (accessed on 13 June 2024).

- Fraunhofer Institute Cost Forecast for Low Temperature Electrolysis—Technology Driven Bottom-Up Prognosis for Pem and Alkaline Water Electrolysis Systems. Available online: https://www.ise.fraunhofer.de/content/dam/ise/de/documents/publications/studies/cost-forecast-for-low-temperature-electrolysis.pdf (accessed on 13 June 2024).

- Clean Hydrogen Partnership Mission Innovation Hydrogen Valleys Platform. Available online: https://www.clean-hydrogen.europa.eu/get-involved/mission-innovation-hydrogen-valleys-platform_en (accessed on 13 June 2024).

- European Hydrogen Backbone Initiative. Available online: https://www.ehb.eu/files/downloads/EHB-Supply-corridors-presentation-ExecSum.pdf (accessed on 13 June 2024).

- BMWK, German National Hydrogen Strategy Update. 2023. Available online: https://www.bmwk.de/Navigation/DE/Home/home.html (accessed on 9 July 2024).

- Department for Energy Security & Net Zero. UK Hydrogen Strategy Delivery Update. 2023. Available online: https://assets.publishing.service.gov.uk/media/65841578ed3c3400133bfcf7/hydrogen-strategy-update-to-market-december-2023.pdf (accessed on 5 September 2024).

- Department of Energy. U.S. National Clean Hydrogen Strategy and Roadmap. 2023. Available online: https://www.hydrogen.energy.gov/docs/hydrogenprogramlibraries/pdfs/us-national-clean-hydrogen-strategy-roadmap.pdf?sfvrsn=c425b44f_5 (accessed on 5 September 2024).

- COAG Energy Council Hydrogen Working Group. Australia’s National Hydrogen Strategy. 2019. Available online: https://www.dcceew.gov.au/sites/default/files/documents/australias-national-hydrogen-strategy.pdf (accessed on 10 September 2024).

- GFA/ALCOR. Stratégie Nationale Pour Le Développement De L’hydrogène Vert Et Ses Dérivés En Tunisie. 2024. Available online: https://www.energiemines.gov.tn/fileadmin/docs-u1/Re%CC%81sume%CC%81_stratei%CC%80gie_nationale_MIME-WEB.pdf (accessed on 10 September 2024).

- Hydrogen Economy Roadmap of Korea Government of Korea-2. 2019. Available online: https://h2council.com.au/wp-content/uploads/2022/10/KOR-Hydrogen-Economy-Roadmap-of-Korea_REV-Jan19.pdf (accessed on 5 September 2024).

- Da Silva Veras, T.; Mozer, T.S.; da Costa Rubim Messeder dos Santos, D.; da Silva César, A. Hydrogen: Trends, production and characterization of the main process worldwide. Int. J. Hydrogen Energy 2017, 42, 2018–2033. [Google Scholar] [CrossRef]

- Dawood, F.; Anda, M.; Shafiullah, G.M. Hydrogen Production for Energy: An Overview. Int. J. Hydrogen Energy 2020, 45, 3847–3869. [Google Scholar] [CrossRef]

- Dincer, I.; Acar, C. Review and evaluation of hydrogen production methods for better sustainability. Int. J. Hydrogen Energy 2015, 40, 11094–11111. [Google Scholar] [CrossRef]

- Dincer, I.; Acar, C. Innovation in hydrogen production. Int. J. Hydrogen Energy 2017, 42, 14843–14864. [Google Scholar] [CrossRef]

- El-Emam, R.S.; Özcan, H. Comprehensive review on the techno-economics of sustainable large-scale clean hydrogen production. J. Clean. Prod. 2019, 220, 593–609. [Google Scholar] [CrossRef]

- Global Hydrogen Review 2021. Available online: https://www.oecd-ilibrary.org/energy/global-hydrogen-review-2021_39351842-en (accessed on 10 September 2024).

- Islam, M.H.H.; Burheim, O.S.; Pollet, B.G. Sonochemical and sonoelectrochemical production of hydrogen. Ultrason. Sonochemistry 2019, 51, 533–555. [Google Scholar] [CrossRef]

- van der Spek, M.; Banet, C.; Bauer, C.; Gabrielli, P.; Goldthorpe, W.; Mazzotti, M.; Munkejord, S.T.; Røkke, N.A.; Shah, N.; Sunny, N.; et al. Perspective on the hydrogen economy as a pathway to reach net-zero CO2 emissions in Europe. Energy Environ. Sci. 2022, 15, 1034–1077. [Google Scholar] [CrossRef]

- Benghanem, M.; Mellit, A.; Almohamadi, H.; Haddad, S.; Chettibi, N.; Alanazi, A.M.; Dasalla, D.; Alzahrani, A. Hydrogen Production Methods Based on Solar and Wind Energy: A Review. Energies 2023, 16, 757. [Google Scholar] [CrossRef]

- Acar, C.; Dincer, I. Investigation of a novel photoelectrochemical hydrogen production system. Chem. Eng. Sci. 2018, 197, 74–86. [Google Scholar] [CrossRef]

- Arifin, K.; Majlan, E.H.; Daud, W.R.W.; Kassim, M.B. Bimetallic complexes in artificial photosynthesis for hydrogen production: A review. Int. J. Hydrogen Energy 2012, 37, 3066–3087. [Google Scholar] [CrossRef]

- Domenighini, P.; Costantino, F.; Gentili, P.L.; Donnadio, A.; Nocchetti, M.; Macchioni, A.; Rossi, F.; Cotana, F. Future perspectives in green hydrogen production by catalyzed sono-photolysis of water. Sustain. Energy Fuels 2024, 8, 3001–3014. [Google Scholar] [CrossRef]

- Zeng, K.; Zhang, D. Recent progress in alkaline water electrolysis for hydrogen production and applications. Prog. Energy Combust. Sci. 2010, 36, 307–326. [Google Scholar] [CrossRef]

- Eroglu, E.; Melis, A. Microalgal hydrogen production research. Int. J. Hydrogen Energy 2016, 41, 12772–12798. [Google Scholar] [CrossRef]

- Khetkorn, W.; Rastogi, R.P.; Incharoensakdi, A.; Lindblad, P.; Madamwar, D.; Pandey, A.; Larroche, C. Microalgal hydrogen production—A review. Bioresour. Technol. 2017, 243, 1194–1206. [Google Scholar] [CrossRef] [PubMed]

- Kosourov, S.; Murukesan, G.; Seibert, M.; Allahverdiyeva, Y. Evaluation of light energy to H 2 energy conversion efficiency in thin films of cyanobacteria and green alga under photoautotrophic conditions. Algal Res. 2017, 28, 253–263. [Google Scholar] [CrossRef]

- Nikolaidis, P.; Poullikkas, A. A comparative overview of hydrogen production processes. Renew. Sustain. Energy Rev. 2017, 67, 597–611. [Google Scholar] [CrossRef]

- Budhraja, N.; Pal, A.; Mishra, R. Plasma reforming for hydrogen production: Pathways, reactors and storage. Int. J. Hydrogen Energy 2023, 48, 2467–2482. [Google Scholar] [CrossRef]

- Hu, L. Molten Carbonate Fuel Cells for Electrolysis. Ph.D. Dissertation, KTH Royal Institute of Technology, Stockholm, Sweden, 2016. [Google Scholar]

- Hu, L.; Lindbergh, G.; Lagergren, C. Performance and Durability of the Molten Carbonate Electrolysis Cell and the Reversible Molten Carbonate Fuel Cell. J. Phys. Chem. C 2016, 120, 13427–13433. [Google Scholar] [CrossRef]

- Coronado, I.; Stekrova, M.; Reinikainen, M.; Simell, P.; Lefferts, L.; Lehtonen, J. A review of catalytic aqueous-phase reforming of oxygenated hydrocarbons derived from biorefinery water fractions. Int. J. Hydrogen Energy 2016, 41, 11003–11103. [Google Scholar] [CrossRef]

- El-Shafie, M.; Kambara, S.; Hayakawa, Y. Hydrogen Production Technologies Overview. J. Power Energy Eng. 2019, 7, 107–154. [Google Scholar] [CrossRef]

- Sikarwar, V.S.; Zhao, M.; Clough, P.; Yao, J.; Zhong, X.; Memon, M.Z.; Shah, N.; Anthony, E.J.; Fennell, P.S. An overview of advances in biomass gasification. Energy Environ. Sci. 2016, 9, 2939–2977. [Google Scholar] [CrossRef]

- Antonini, C.; Treyer, K.; Moioli, E.; Bauer, C.; Schildhauer, T.J.; Mazzotti, M. Hydrogen from wood gasification with CCS—A techno-environmental analysis of production and use as transport fuel. Sustain. Energy Fuels 2021, 5, 2602–2621. [Google Scholar] [CrossRef]

- Antonini, C.; Treyer, K.; Streb, A.; van der Spek, M.; Bauer, C.; Mazzotti, M. Hydrogen production from natural gas and biomethane with carbon capture and storage—A techno-environmental analysis. Sustain. Energy Fuels 2020, 4, 2967–2986. [Google Scholar] [CrossRef]

- Parra, D.; Valverde, L.; Pino, F.J.; Patel, M.K. A review on the role, cost and value of hydrogen energy systems for deep decarbonisation. Renew. Sustain. Energy Rev. 2019, 101, 279–294. [Google Scholar] [CrossRef]

- European Commission, Directorate-General for Internal Market, Industry, Entrepreneurship and SMEs, Grohol, M., Veeh, C., Study on the critical raw materials for the EU 2023—Final report, Publications Office of the European Union. 2023. Available online: https://data.europa.eu/doi/10.2873/725585 (accessed on 5 September 2024).

- Sayed-Ahmed, H.; Toldy, I.; Santasalo-Aarnio, A. Dynamic operation of proton exchange membrane electrolyzers—Critical review. Renew. Sustain. Energy Rev. 2024, 189, 113883. [Google Scholar] [CrossRef]

- Dobó, Z.; Palotás, B. Impact of the current fluctuation on the efficiency of Alkaline Water Electrolysis. Int. J. Hydrogen Energy 2017, 42, 5649–5656. [Google Scholar] [CrossRef]

- Speckmann, F.-W.; Bintz, S.; Birke, K.P. Influence of rectifiers on the energy demand and gas quality of alkaline electrolysis systems in dynamic operation. Appl. Energy 2019, 250, 855–863. [Google Scholar] [CrossRef]

- Du, N.; Roy, C.; Peach, R.; Turnbull, M.; Thiele, S.; Bock, C. Anion-Exchange Membrane Water Electrolyzers. Chem. Rev. 2022, 122, 11830–11895. [Google Scholar] [CrossRef]

- Midilli, A.; Kucuk, H.; Topal, M.E.; Akbulut, U.; Dincer, I. A comprehensive review on hydrogen production from coal gasification: Challenges and Opportunities. Int. J. Hydrogen Energy 2021, 46, 25385–25412. [Google Scholar] [CrossRef]

- Rezaei, M.; Akimov, A.; Gray, E.M. Economics of renewable hydrogen production using wind and solar energy: A case study for Queensland, Australia. J. Clean. Prod. 2024, 435, 140476. [Google Scholar] [CrossRef]

- Howes, J.; German, L.; Robson, P.; Taylor, R. Innovation Needs Assessment for Biomass Heat. Final Report. 2018. Available online: https://assets.publishing.service.gov.uk/media/5acf7a81e5274a76be66c1d3/BE2_Innovation_Needs_Final_report_Jan18.pdf (accessed on 10 September 2024).

- Parkinson, B.; Tabatabaei, M.; Upham, D.C.; Ballinger, B.; Greig, C.; Smart, S.; McFarland, E. Hydrogen production using methane: Techno-economics of decarbonizing fuels and chemicals. Int. J. Hydrogen Energy 2018, 43, 2540–2555. [Google Scholar] [CrossRef]

- ISO 14687:2019; Hydrogen Fuel Quality—Product Specification. ISO: Geneva, Switzerland, 2019. Available online: https://www.iso.org/standard/69539.html (accessed on 30 July 2024).

- Regulation—2018/841—EN—EUR-Lex. (n.d.). Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32018R0841 (accessed on 30 July 2024).

- Agora Energiewende—What Actually Are Carbon Contracts for Difference? Available online: https://www.bmwk-energiewende.de/EWD/Redaktion/EN/Newsletter/2020/11/Meldung/direkt-account.html (accessed on 17 June 2024).

- ENTSO-E—Balancing Platforms Stakeholders’ Workshop. December 2022. Available online: https://www.entsoe.eu/events/2022/12/08/balancing-platforms-stakeholders-workshop/ (accessed on 17 June 2024).

- Pototschnig, A. European Gas Transmission Tariffication: Is It Really Fit for an Internal Gas Market? Available online: https://fsr.eui.eu/european-gas-transmission-tariffication-is-it-really-fit-for-an-internal-gas-market/ (accessed on 17 June 2024).

- EU. European Open Science Cloud (EOSC Executive Board), Strategic Research and Innovation Agenda (SRIA). 2022. Available online: https://op.europa.eu/it/publication-detail/-/publication/f9b12d1d-74ea-11ec-9136-01aa75ed71a1 (accessed on 10 September 2024).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| European Union [30,31] | Decarbonization of large shares of EU consumption using hydrogen as vector for renewable energy storage and transport, ensuring back-up for seasonal variations and connecting production locations to more distant demand centers. Replace fossil fuels in some carbon intensive industrial processes, such as in the steel or chemical sectors, lowering greenhouse gas emissions and further strengthening global competitiveness for those industries. Solutions for hard-to-abate parts of the transport system, in addition to what can be achieved through electrification and other renewable and low-carbon fuels. |

| France [32] | Environmental issues: hydrogen provides many solutions for decarbonizing industry and transport. Energy security issues: to reduce dependence on hydrocarbon imports. Challenges of technological independence: to enhance the strengths in global competition. |

| Germany [33] | Accelerated transition to a sustainable energy economy. Reduce greenhouse gas emissions by 80 to 95% by 2050 compared to 1990 levels. |

| The Netherlands [34] | H2 crucial to the energy transition. Hydrogen specifically has the added benefit of contributing to better air quality. The rapid development of hydrogen will be a top priority for industry. A portion of German demand will have to be met through imports through the Netherlands. |

| Spain [35] | Hydrogen as main asset for Spain to become one of the European powers in renewable generation. The deployment of green hydrogen will encourage the development of innovative industrial value chains, generating employment and economic activity, contributing to the reactivation of a green economy with high added value. Accelerating renewable deployment, with positive effects on electricity prices and on industrial competitiveness. Development of smart grids and storage of renewable energy on a large scale and on a seasonal basis, providing flexibility to the system. Potential of renewable hydrogen to favor the decarbonization of isolated energy systems, with special attention to islands (highly dependent on air and sea transport). Renewable hydrogen will be promoted to help prevent rural depopulation and achieve the demographic challenge objectives |

| Norway [36] | The government pursues a broad set of policies aimed at zero emission solutions in the transport sector. This also includes hydrogen. |

| United Kingdom [37] | Electricity pathway. Hydrogen pathway: 2050 hydrogen would provide a majority of heating for heating homes (62%) and commercial and public buildings (56%), power all cars and vans, and play a significant role in industrial firing processes. Emissions removal pathway. The transport sector was responsible for 24% of UK carbon emissions in 2014. The UK government has set a target for all new cars and vans to be zero-emission by 2040. |

| European Union | EU industry is rising to the challenge and has developed an ambitious plan to reach 2 × 40 GW of electrolyzers by 2030. Generating 2250 TWh of hydrogen within Europe by 2050 (approximately 24% of final energy demand). Decarbonize various sectors, especially the gas grid, through blending and limited conversion to 100% hydrogen. Transportation through adoption of fuel cells in vehicles and shipping and synthetic fuel in aviation. Use in industry as a substitute for natural gas for high-grade process heat and as a feedstock in processes, either directly or with CO2 as a synfuel or electrofuel. |

| France | Strategy based on large consultation of stakeholders in order to: Accelerate the ecological transition and create a dedicated industrial sector, both domestic on a European scale Install enough electrolyzers to make a significant contribution to the decarbonization of the economy (objective 6.5 GW) Develop clean mobility, in particular for heavy vehicles: save more than 6 Mt of CO2 by 2030. Build industrial sector that creates jobs and guarantees technological leadership: generate between 50,000 and 150,000 direct and indirect jobs. Hydrogen production by electrolysis for industry, in mobility as a complement to battery vehicles, and to assist the stabilization of energy networks. |

| Germany | By 2030: Hydrogen demand is set to experience an initial increase—especially in the industrial sector (chemicals, petrochemicals, steel) and, to a lesser extent, in the transport sector). The demand in industry will rise by 10 TWh. Growing demand is expected to come from fuel-cell-driven electric vehicles. Other consumers (e.g., parts of the heating sector, in the long term) might follow. By 2050: The forecast consumption of electricity-based energy sources will be between 110 TWh—and roughly 380 TWh. Alongside the industrial and transport sectors, long-term demand will also arise in the transformation sector. Focus on close to commercial and on sectors hard to be decarbonized. Existing technologies will be insufficient; innovative technological solutions will be required. Strategy: speed up rollout of H2 technologies in Germany, encouraging other countries to adopt H2 by example. TIMING IS IMPORTANT: to avoid misallocated investments transformation process must be oriented to the demand expected in view of the 2050 decarbonization |

| The Netherlands | The government must meet the necessary preconditions, while businesses and knowledge institutions must start investing in scalable applications and innovation. Key concepts are upscaling, cost reduction (in an international context) and innovation. Presenting an ambitious policy agenda and taking the essential steps needed to realize the infrastructure and other framework conditions, the government wishes to send a clear signal. By national strategy the government underlines the unique starting position of the Netherlands. Hydrogen imports will also take up a key role as a global market begins to emerge. Alignment with the decisions and developments in the regions of our Northwest European energy market. |

| Spain | Potential of renewable hydrogen to decarbonize sectors or processes with greater decarbonization complexity, such as air transport or industrial processes that require high temperatures and power generation. Green hydrogen key to achieve climate neutrality and a 100% renewable electricity system by 2050. The renewable hydrogen will activate the development of the value chains. The Roadmap identifies this energy vector as a key sustainable solution for the decarbonization of the economy and the development of industrial value chains and RD and I, Role of hydrogen in the next three decades will allow Spain to lead a country project towards a decarbonized economy, fostering the innovative value chain, the applied knowledge of the industry, the development of pilot projects throughout the national territory and support for transition. This document is aligned with the Annual Sustainable Growth Strategy for 2021 published by the European Commission. |

| Norway | Hydrogen is currently not competitive in many of the areas of application that could be of interest. Energy losses generated by producing hydrogen and the cost of storing it make the utilization of clean hydrogen less profitable compared with fossil energy sources or other low and zero emission solution. More stringent emissions trading market, combined with the increase in the CO2 tax announced by the government, will make emission-intensive solutions more expensive. Technologies are not yet mature: Technology development and innovation in a value chain perspective could assist in drawing on potential synergies between industries: developing and demonstrating energy-efficient and cost-efficient methods and value chains for the production, transport, storage and use of clean hydrogen. Uncertainties regarding the opportunities for H2 in Norway: the technology for several of these applications is at an early stage. Several of the applications being considered in other countries are of little relevance to Norway. Open issues: In addition to the price of input factors such as electricity or gas, factors such as distance from producer to consumer, the need for storage, demand, and the costs and energy losses associated with chemical conversion matter. For hydrogen used in vehicles/vessels, it is important to emphasize that the combined weight of fuel, tanker, propulsion system and space required will also be significant. Pilots: there are few projects operating with end-user experience in the use of hydrogen. PILOT-E: 71MNOK complete supply chain for H2. |

| United Kingdom | Blue Hydrogen: This type of hydrogen is preferred because: Total hydrogen production would reach approximately 700 TWh in 2050. The main form of production would be steam-methane reforming with carbon capture, usage, and storage. A key aim of the Hydrogen Supply Program is to overcome the cost differential between low-carbon hydrogen and natural gas. SMR (4 × 256 MW capacity) was chosen, as it is a proven technology, has a relatively smaller footprint, and can be integrated into the existing natural gas supply chain. As this approach involves the production of carbon emissions, carbon capture technology would be included to capture 90% of emissions for subsequent sequestration (1.5 million tons per annum). Green Hydrogen: Production using electrolysis was not considered practical due to various factors: limited availability of curtailed electricity. cost of existing bulk grid electricity leading to “expensive” hydrogen production cost. substantial land requirements for dedicated renewable energy supply (i.e., wind) and electrolyzers (400 × 2.6 MW units). additional storage requirements to accommodate variability of wind power and additional costs of associated electrical infrastructure. Assuming a bulk electricity cost of 6 p/kWh, the cost of producing hydrogen at the electrolyzer was estimated to be 10 p/kWh, excluding transmission and storage costs. |

| Vehicle Type | Autonomy | Operation Flexibility | Refuel/ Recharging Time | Passenger Capacity |

|---|---|---|---|---|

| Electric overnight | +/− | +/− | − | − |

| Electric opportunity charging | + | −/+ | +/− | −/+ |

| Trolleybus | + | - | + | + |

| Fuel cell | + | + | + | + |

| Area | Barrier |

|---|---|

| Knowledge of hydrogen behavior: hydrogen handling, storage and bunkering | Uncertainties about the behavior of liquid hydrogen and the detonation thresholds in the event of leaks in closed spaces. |

| Definition of rigorous risk mitigation measures: minimum sizing of spaces, positioning of fans/ventilation shafts, detectors in case of leak. | |

| Safety | The experience gained with natural gas cannot simply be transferred to hydrogen. The unique characteristics of hydrogen make it very different from natural gas. |

| Difficulty in containing hydrogen due to the lightness of the atoms. It can cause materials that are safe for natural gas to become brittle. | |

| Necessity to use certain types of steel and welded rather than fileted connections. | |

| Greater flammability than natural gas. | |

| Use in variable environmental conditions and in small spaces. | |

| Difficulty in evacuating personnel in the event of leaks/spills. | |

| Rules/Regulations | Gaps in authorization procedures, regulations and standards regarding bunkering and the use of hydrogen as a fuel on board vessels. |

| Minimum Purity Level | Application |

|---|---|

| 98.00% | Internal combustion engines ICE for transport, residential and commercial combustion applications |

| 99.90% | Industrial fuel (heat and power generation) |

| 99.97% | Vehicular fuel cells |

| 99.99% | Zero grade (fuel cell) |

| 99.995% | Aircraft and space-vehicle ground support systems |

| 99.999% | Ultra-high purity grade—semiconductors applications |

| 99.9999% | Hydrogen for research-grade purposes |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Migliavacca, G.; Carlini, C.; Domenighini, P.; Zagano, C. Hydrogen: Prospects and Criticalities for Future Development and Analysis of Present EU and National Regulation. Energies 2024, 17, 4827. https://doi.org/10.3390/en17194827

Migliavacca G, Carlini C, Domenighini P, Zagano C. Hydrogen: Prospects and Criticalities for Future Development and Analysis of Present EU and National Regulation. Energies. 2024; 17(19):4827. https://doi.org/10.3390/en17194827

Chicago/Turabian StyleMigliavacca, Gianluigi, Claudio Carlini, Piergiovanni Domenighini, and Claudio Zagano. 2024. "Hydrogen: Prospects and Criticalities for Future Development and Analysis of Present EU and National Regulation" Energies 17, no. 19: 4827. https://doi.org/10.3390/en17194827

APA StyleMigliavacca, G., Carlini, C., Domenighini, P., & Zagano, C. (2024). Hydrogen: Prospects and Criticalities for Future Development and Analysis of Present EU and National Regulation. Energies, 17(19), 4827. https://doi.org/10.3390/en17194827