Costs and Benefits of Citizen Participation in the Energy Transition: Investigating the Economic Viability of Prosumers on Islands—The Case of Mayotte

Abstract

1. Introduction

1.1. Clean Energy Transitions on Islands

1.2. Ambition and Contribution to Research

- Do solar rooftop PV systems for prosumption present a profitable investment option in Mayotte, both today and in the future? How is profitability influenced by the ongoing decarbonization?

- What are the technical, financial, and regulatory drivers of profitability?

- What policy measures can support the profitability of rooftop solar PV systems for prosumption, and which specifically consider issues of affordability and inclusion?

2. Materials and Methods

2.1. Methods

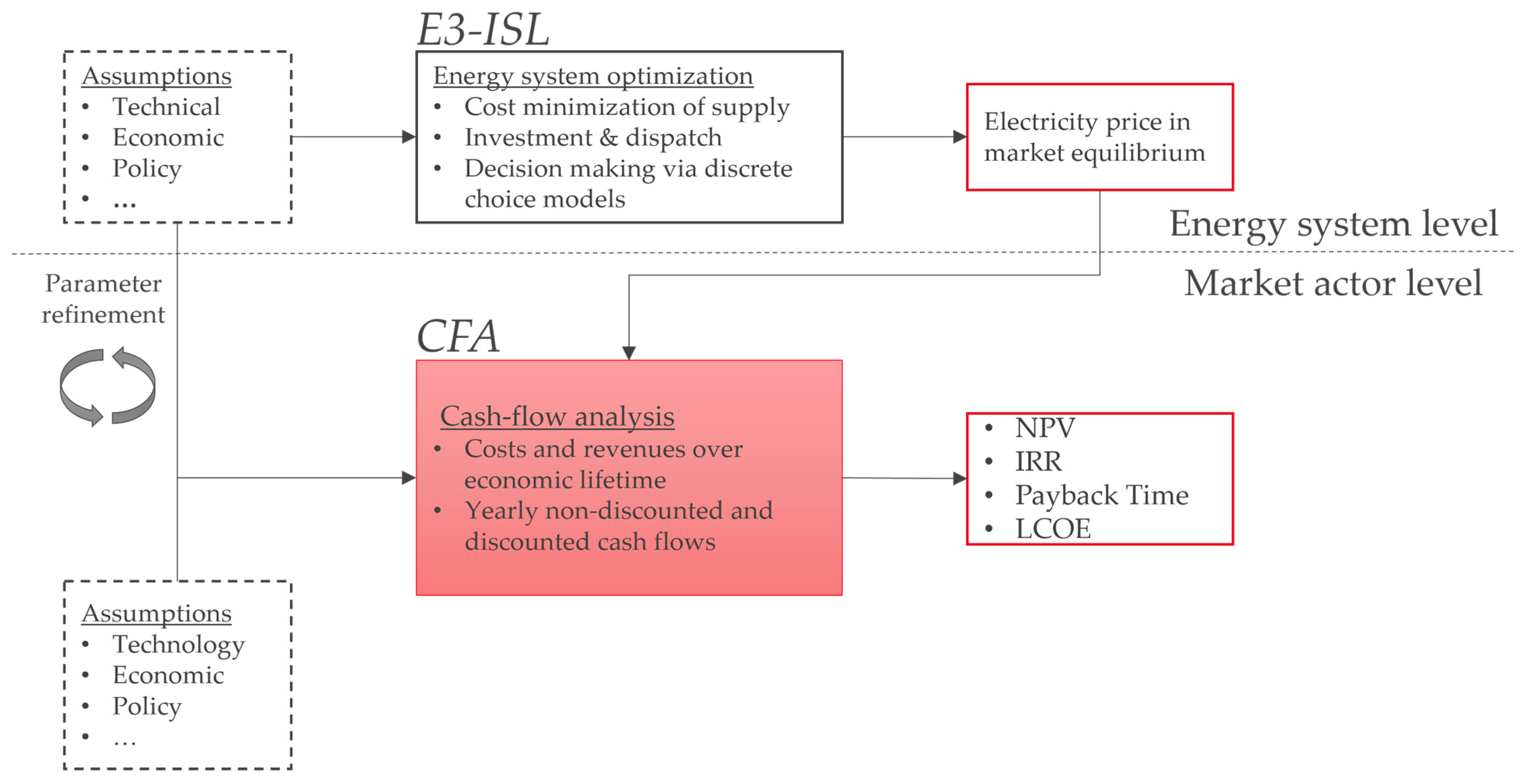

2.1.1. Energy System Modeling

- E3-ISL was developed to obtain consistent projections of the energy system of Mayotte, including forecasting the energy demand by the main sectors (transport, buildings, industries), the fuel and technology mix by sector, planning the power supply sector, and assessing the emissions, energy, and economic consequences of certain political decisions or market developments. The model was specifically tailored to the characteristics of the non-interconnected island energy system of Mayotte, including significant seasonal load variability, high fuel prices, weak electricity grid, and poor energy infrastructure.

- E3-ISL projects electricity prices in the period 2025–2050, as derived from cost minimization on the supply side due to endogenous competition between various power-generating technologies and the price-elastic behaviours of energy consumers, which results in a market equilibrium.

- In our analysis, the base year of the model is set as 2020. The optimization is executed in 5-year time steps up to 2050. Thus, the model’s horizon reaches 2050.

- The results may be exported to a Microsoft Excel-based environment (e.g., Excel 2021, Version 2405), which provides a user-friendly intersection to allow for soft-linking with the CFA modelling, or further processing of results.

- The choices of actors (e.g., energy consumer for fuels used, investments) are determined by decision-making agents via discrete choice models. The choices are influenced by policy drivers (including fuel taxation, RES and energy efficiency targets, subsidies for technologies, regulatory instruments, behavioural changes, and emissions trading) that are set to be defined by the modeller, allowing for flexible scenario formulation.

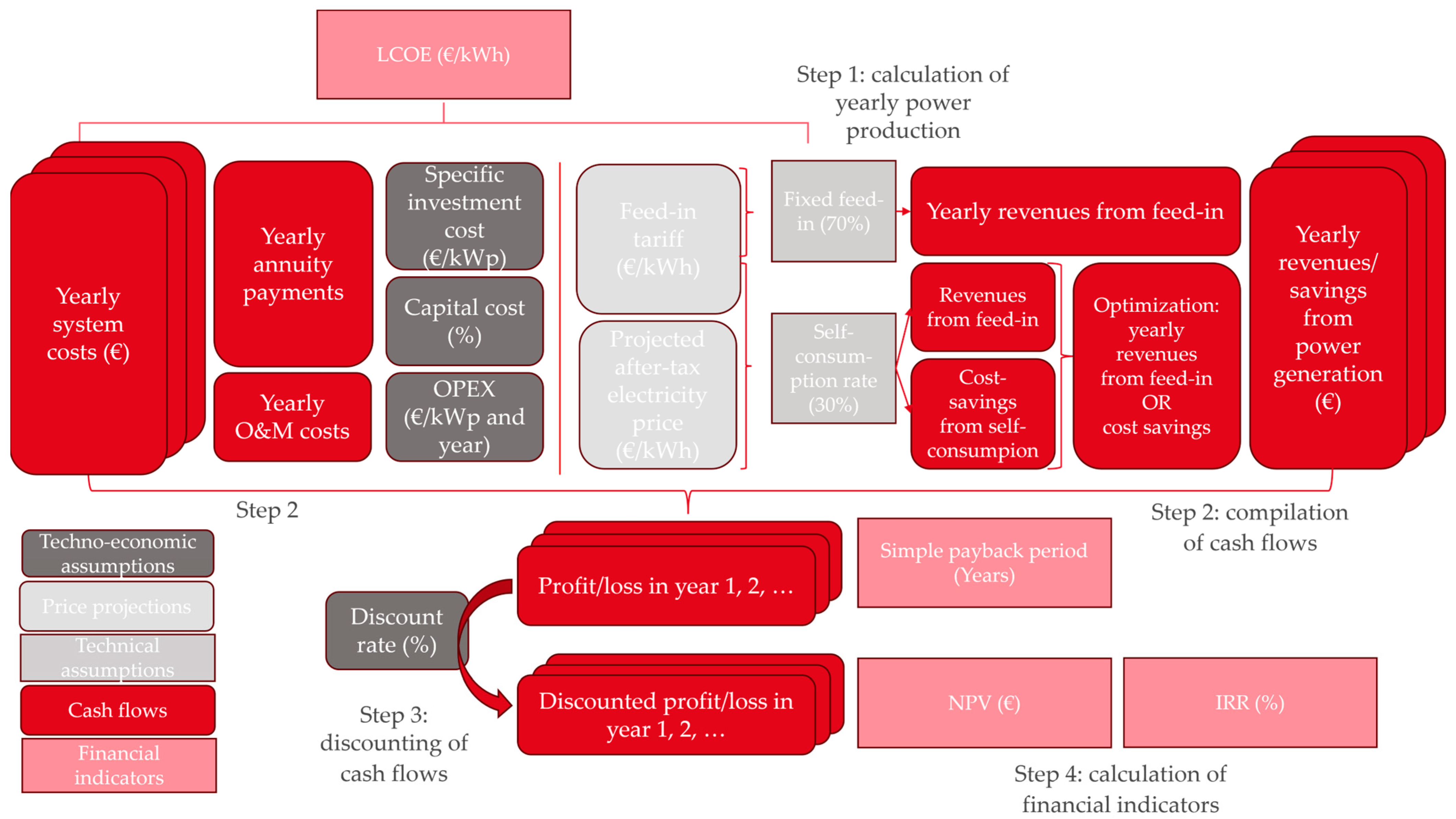

2.1.2. Cash-Flow Analysis

- (1)

- Compilation of technical data: We first compile the technical data needed for the calculation of the yearly power generation of an asset, i.e., installed capacity, yearly runtime, and capacity factor. Technical assumptions are assumed to be constant over the asset’s lifetime as this feature is embedded in specific technological equipment.

- (2)

- Compilation of cash flows: We compile all cash flows over an investment’s lifetime, based on the underlying technical data. This includes capital expenditure (specific investment cost) and cost of capital, operational expenditures (OPEX), and revenues from electricity sales or self-consumption. The data for each 5-year period are assumed for all years during the five-year period, e.g., the specific investment cost for rooftop solar PV in 2020 remains the same for systems installed in the years from 2021 to 2024. For our cash flows, we consider the following factors:

- The specific investment cost represents the total initial investment costs associated with purchasing and installing the power generation assets, such as construction, equipment, and infrastructure costs. It is a one-time cost that relates to the installed power capacity of assets and is thus expressed in €/kWp. The specific investment cost varies between system sizes and time periods (see Table A1), with lower costs for larger systems and systems installed in later time periods, as shown in Section 2.2.2.

- In line with the E3-ISL modelling assumptions, investors are assumed to take on a loan, on which they must pay interest, to finance the specific investment cost, i.e., the cost of capital (8.5% in the reference case, see Section 2.2.2).

- The loan is paid back as an annuity over the investment’s economic lifetime (15 years), resulting in same-sized yearly cash outflows that cover both the repayment of the specific investment cost and the interest rate.

- The OPEX of rooftop solar PV systems is only composed of fixed operation and maintenance (O&M) expenses, which represent the ongoing costs required to maintain and operate the power generation assets, such as expenses for regular maintenance and administrative costs. Fixed O&M costs are calculated based on the installed capacity, i.e., €/kW and year. These per-unit O&M costs are uniform across system sizes but are lower for systems installed in later time periods following the trend of the specific investment costs. The OPEX results in same-sized yearly cash outflows.

- No taxes are included in the analysis. At the time of writing, there is no VAT in Mayotte, and we assume a favorable framework where power generation by prosumers is not taxed. For power producers, taxes on electricity are profit-neutral, as they are passed on to final consumers.

- Finally, producer revenues finally are considered on a pre-tax basis, again in line with modelling assumptions, and assed based on the annual generated power sold to the end consumers of electricity. All power producers receive the pre-tax electricity price, calculated by the E3-ISL model for each unit sold, i.e., €/kWh. In E3-ISL, this price is calculated based on the total electricity costs divided by total energy generation, thereby recovering all system costs, including specific investment cost, OPEX, fuel, and carbon costs. It therefore varies by scenario, changing according to the energy system setup, the technology and investment mix, and the dispatch of power plants.

- The sum of annuity payments and yearly O&M costs result in the yearly system costs, while the sum of revenues from feed-in and electricity bill savings results in the yearly system revenues. The sum of costs and revenues results in the net cash flows, i.e., a profit or loss in a given year.

- (3)

- (4)

- Calculation of financial key performance indicators (KPIs): Finally, we calculate a set of financial indicators, offering different perspectives for evaluating the economic viability of rooftop solar PV investments in Mayotte. In line with the related literature [28], the indicators include the Net Present Value (NPV), the Internal Rate of Return (IRR), the simple payback time, and the levelized cost of electricity (LCOE). All indicators relate to the economic lifetime of assets, which is set to 15 years for all rooftop solar PV systems, again in line with [25,26]. Since the technical lifetime of 20 or even 25 years exceeds the economic lifetime, additional profits might be made if an asset continues to operate after reaching its economic lifetime of 15 years. These additional profits are not considered in the profitability calculations but present an additional potential benefit for prosumers. The calculated KPIs, their purpose, and their interpretation are listed in Table 1.

2.2. Materials and Assumptions

2.2.1. Case Study Description

2.2.2. Data, Assumptions and Projections

Technical Assumptions

Specific Investment Cost

Pre- and After-Tax Electricity Prices

FiT Projection

2.2.3. Market Participants and Behavior

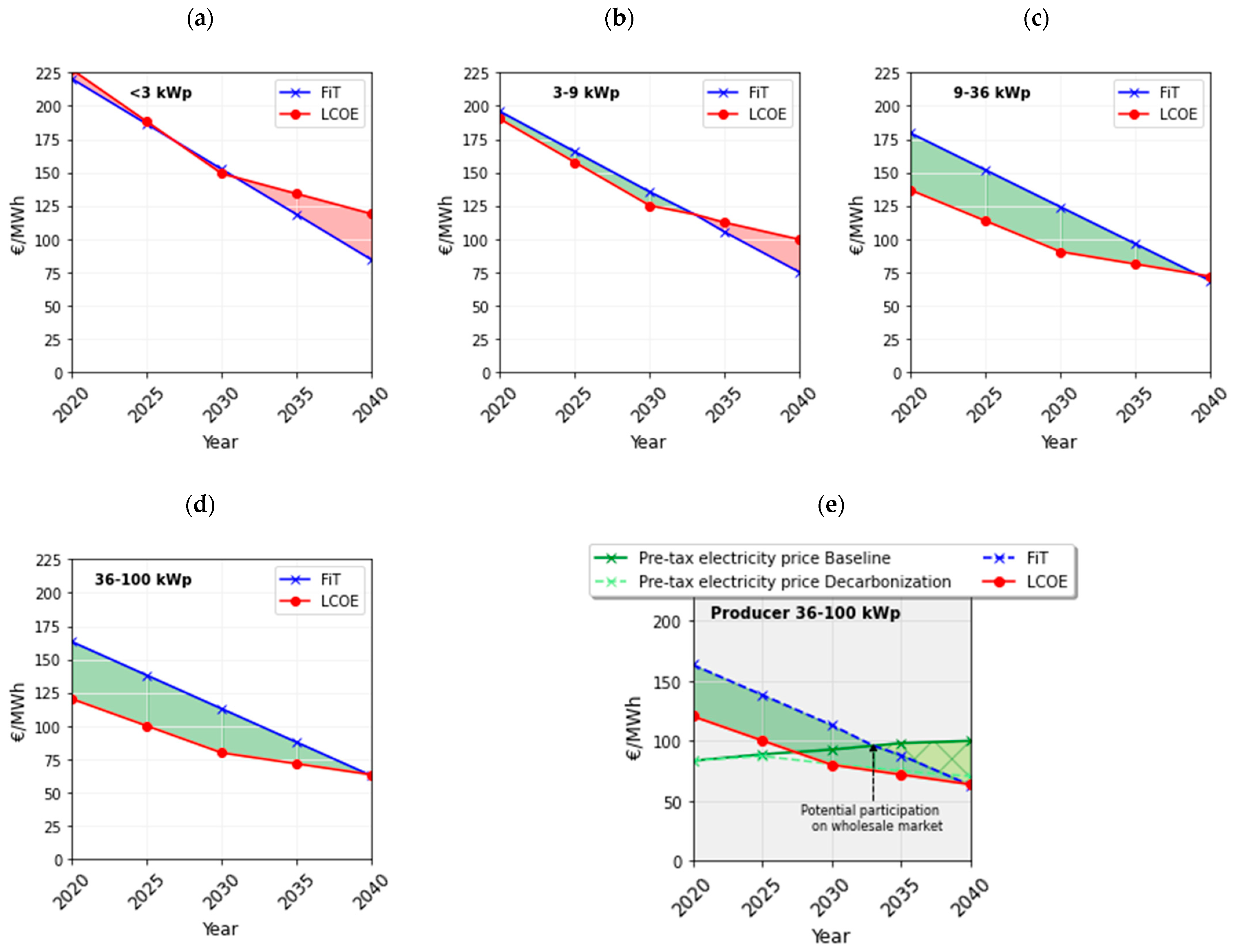

- Producers: In 2035 and 2040 in the baseline and decarbonization scenarios, respectively, the FiT for newly installed systems is lower than the pre-tax electricity price over the following years. Hence, producers may switch to being compensated via the wholesale electricity price rather than FiT. While wholesale prices can exceed the FiT prices and thereby provide additional revenues, they are the result of energy market clearing and fluctuate over time. Producers can thus reasonably project electricity price developments and use these assumptions to inform investment decisions, but cannot plan for guaranteed compensation based on market prices. To achieve such certainty, a power purchasing agreement (PPA) or other form of guaranteed compensation beyond the FiT would be needed, which is beyond the scope of the current study.

- Prosumers: As long as the rate pf FiT compensation is higher than the electricity price, feeding in is always more attractive than self-consumption. Depending on the system size, and scenario (baseline or decarbonization), the point in time for a switch differs. As FiTs gradually decrease, self-consumption becomes more attractive the later a system is installed. This shift happens earlier in the baseline scenario, where the higher costs of (diesel-intense) power generation lead to higher and rising electricity prices, and thereby to more profitable self-consumption.

3. Results and Implications

3.1. Profitability Analysis

3.1.1. Evaluating Cost Recovery

- The cost recovery of the investment depends on the system size, due to the different ratio of FiT to LCOE in different system sizes. With increasing system size, the systems become more profitable—despite the lower FiT. This is due to the decreasing specific investment cost of PV with the increasing system size. According to our analysis, the smallest systems, <3 kWp, are currently not economically viable under the assumptions made. In contrast, according to our analysis, large systems, e.g., with a capacity of 36 kWp, can currently (2024) achieve a difference of around €40/MWh.

- The profitability of the investment depends on the timing of the investment. Both the projected FiT and LCOE are expected to decline in the future for all system sizes, but at different gradients. This could result in varying differences between FiT and LCOE. The trends for larger systems (>9 kWp) therefore show decreasing positive differences, neglecting possible adjustments to the FiT in future in line with the development of the LCOE (see Section 4 for a related discussion). For any size of system observed, the LCOE may exceed the FiT by 2040.

- As can be expected, the LCOE will asymptotically approach stagnation in the future due to limitations in the cost reduction of PV technology. In the case of systems below 9 kWp, we observe that the FiT could fall below the level of the LCOE in the future—if not readjusted (see, for example, from 2033 for systems between 3 and 9 kWp). Consequently, we can conclude that, in order to guarantee the profitability of the systems, either the FiT will have to be adjusted or additional compensation pathways will have to be opened up, i.e., participation in wholesale electricity markets.

3.1.2. Evaluating Profitability

3.2. Sensitivity Analysis

3.2.1. Sensitivity towards Economic Parameters

3.2.2. Sensitivity towards the Self-Consumption Rate

4. Discussion

- (i)

- Summarize the implications of our study in front of the relevant political and regulatory framework, thereby answering the specific research questions RQ1, RQ2 and RQ3 as stated in Section 1.2 (Section 4.1);

- (ii)

- Place our findings in the context of popular and recent concepts of citizen-driven energy transitions (Section 4.2);

- (iii)

- Critically reflect on the scope of application of the analysis and its findings and discuss transferability to other islands and remote settings (Section 4.3).

4.1. Implications of the Findings and Recommendations for Policy and Regulation

- (i)

- The size of the PV system: we considered different PV system sizes that substantially differed in their specific costs and applicable FiT. For smaller systems, e.g., <3 kWp, high specific investment costs cannot be compensated for with the higher FiT, jeopardizing their profitability. Without the PV cost reductions achieved through a growing solar PV industry in Mayotte or other beneficial factors, additional measures will be needed to support the profitability of these systems as a first prerequisite for economic incentives and likely their widespread adoption. For large- and medium-sized systems (9–100 kWp), the guaranteed FiT exceeds the LCOE in most investment periods, resulting in a positive return per kWh. Combined with appropriate insurance and financial solutions, this results in a secured positive return. This security presents a highly attractive opportunity for risk-averse actors, such as municipalities and other public or non-profit actors. In addition to the guaranteed financial returns obtained through feed-in tariffs, the self-consumption of the generated power can result in additional cost savings, increase autonomy from the electricity grid, and protect the respective prosumers from fluctuating energy prices [38]. Still, the financial returns of large- and medium-sized systems might not suffice for profit-oriented investors, as the IRR remains below the assumed discount rate of 8.5% pertaining for most investments. If decision-makers in Mayotte aim for a fast and widespread adoption of rooftop solar PV on the island, further support measures will be needed to increase the profitability and attract private capital. We argue, however, that different support schemes should be weighted and prioritized under consideration of their distributional impacts.

- (ii)

- The time of investment: our analysis considered the projections of declining specific investment costs of the PV assets and simultaneously decreasing FiT. Hence, we observe the profitability of investments in PV to be time-dependent. The more steeply falling gradient of the FiT compared to the declining costs of PV assets leads shrinking profitability for the same system size in future periods. As the specific costs of the PV assets are expected to asymptotically approach a stagnating positive minimum and the FiT—if not adjusted—can fall (linearly) towards 0, it could come to a point in the future where the costs of the PV system can no longer be covered by feeding electricity into the grid. Accordingly, alternative compensation routes would be necessary to provide an economic incentive to invest.

- (iii)

- The level of decarbonization of the entire energy sector: with the ongoing decarbonization of the energy sector of Mayotte, our energy system model predicts that the wholesale electricity prices will decrease. This, in turn, will decrease the potential compensation from selling electricity on the market as a producer and diminish prosumers’ energy bill savings. Ironically, these lower prices are the result of increasing RES penetration into the electricity system, exemplifying a cannibalization effect of RES revenues through their wide-scale deployment. Still, many investments in rooftop solar PV are profitable under decarbonization, allowing prosumers to participate in the energy transition and profit through economic benefits.

- (iv)

- The market behavior: in our analysis, we compare two types of market participants, distinguishing between producers and prosumers, the latter of which may partly self-consume electricity produced. Comparing the two market participants at the same system sizes, we identify that, under perfectly rational behavior, the prosumer would in fact feed in the entire electricity produced—acting as producer only—until 2035, as no economic incentive is given to self-consume electricity. In later periods, this reverses and self-consumption may become more advantageous compared to sole feed-in—however, this only applies when assuming that the market participant may be prevented from selling fed-in electricity at wholesale prices. Here, we observe that producers being compensated for injected electricity at the pre-tax electricity price can achieve higher economic gains compared to prosumers, given the electricity price remains high when still assuming a high share of fossil fuels in the energy mix.

4.2. Significance of the Results for Concepts of a Citizen-Driven Energy Transition

4.3. Critical Reflection on the Scope of Application and Investor Profiles

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Year | 2020 | 2025 | 2030 | 2035 | 2040 | 2045 | 2050 |

|---|---|---|---|---|---|---|---|

| Cost reduction | −17.60% | −21.35% | −9.95% | −11.04% | −9.06% | −9.96% | |

| 36–100 kWp | 1300.00 | 1071.25 | 842.51 | 758.71 | 674.91 | 613.76 | 552.61 |

| 9–36 kWp | 1500.00 | 1236.06 | 972.13 | 875.44 | 778.75 | 708.19 | 637.63 |

| 3–9 kWp | 2150.00 | 1771.69 | 1393.38 | 1254.79 | 1116.20 | 1015.07 | 913.94 |

| <3 kWp | 2600.00 | 2142.51 | 1685.02 | 1517.42 | 1349.83 | 1227.53 | 1105.23 |

| System Size/Year | 2020 | 2025 | 2030 | 2035 | 2040 |

|---|---|---|---|---|---|

| 100 kWp (Producer) | 51,117.81 | 45,256.86 | 39,395.92 | 33,538.28 | 45,402.99 |

| 100 kWp (Prosumer) | 51,117.81 | 45,256.86 | 44,352.08 | 34,413.03 | 22,975.45 |

| 36 kWp | 18,333.79 | 16,367.52 | 14,811.46 | 10,856.98 | 6453.50 |

| 9 kWp | 603.67 | 855.17 | 1106.66 | 38.22 | −871.63 |

| 3 kWp | −246.98 | −65.51 | 115.96 | −430.72 | −739.75 |

| System Size/Year | 2020 | 2025 | 2030 | 2035 | 2040 |

|---|---|---|---|---|---|

| 100 kWp (Producer) | 51,117.81 | 45,256.86 | 39,395.92 | 19,219.64 | 4346.51 |

| 100 kWp (Prosumer) | 51,117.81 | 45,256.86 | 39,395.92 | 23,978.06 | 11,081.13 |

| 36 kWp | 18,333.79 | 16,367.52 | 14,401.24 | 7119.16 | 2171.55 |

| 9 kWp | 603.67 | 855.17 | 1106.66 | −765.77 | −1942.11 |

| 3 kWp | −246.98 | −65.51 | 115.96 | −558.00 | −1096.58 |

References

- Ara Begum, R.; Lempert, R.; Ali, E.; Benjaminsen, T.A.; Bernauer, T.; Cramer, W.; Cui, X.; Mach, K.; Nagy, G.; Stenseth, N.C.; et al. 2022: Point of Departure and Key Concepts. In Climate Change 2022: Impacts, Adaptation and Vulnerability. Contribution of Working Group II to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change; Pörtner, H.-O., Roberts, D.C., Tignor, M., Poloczanska, E.S., Mintenbeck, K., Alegría, A., Craig, M., Langsdorf, S., Löschke, S., Möller, V., et al., Eds.; Cambridge University Press: Cambridge, UK; New York, NY, USA, 2022; pp. 121–196. [Google Scholar] [CrossRef]

- Přívara, A.; Přívarová, M. Nexus between Climate Change, Displacement and Conflict: Afghanistan Case. Sustainability 2019, 11, 5586. [Google Scholar] [CrossRef]

- Tabe, T. Climate Change Migration and Displacement: Learning from Past Relocations in the Pacific. Soc. Sci. 2019, 8, 218. [Google Scholar] [CrossRef]

- Zulhaimi, N.A.; Pereira, J.J.; Muhamad, N. Global Research Landscape of Climate Change, Vulnerability, and Islands. Sustainability 2023, 15, 13064. [Google Scholar] [CrossRef]

- Ioannidis, A.; Chalvatzis, K.J.; Li, X.; Notton, G.; Stephanides, P. The Case for Islands’ Energy Vulnerability: Electricity Supply Diversity in 44 Global Islands. Renew. Energy 2019, 143, 440–452. [Google Scholar] [CrossRef]

- Field, C.B.; Dokken, D.J. Part B: Regional Aspects. Working Group 2 Contribution to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change. In Climate Change 2014: Impacts, Adaptation, and Vulnerability; IPCC: Cambridge, UK, 2014. [Google Scholar]

- Ritchie, H.; Roser, M. CO2 Emissions. Available online: https://ourworldindata.org/co2-emissions (accessed on 17 January 2023).

- United Nations Climate Change The Paris Agreement. Available online: https://unfccc.int/process-and-meetings/the-paris-agreement/the-paris-agreement (accessed on 3 June 2024).

- Zafirakis, D.; Chalvatzis, K.J. Wind Energy and Natural Gas-Based Energy Storage to Promote Energy Security and Lower Emissions in Island Regions. Fuel 2014, 115, 203–219. [Google Scholar] [CrossRef]

- Gils, H.C.; Simon, S. Carbon Neutral Archipelago—100% Renewable Energy Supply for the Canary Islands. Appl. Energy 2017, 188, 342–355. [Google Scholar] [CrossRef]

- Kuang, Y.; Zhang, Y.; Zhou, B.; Li, C.; Cao, Y.; Li, L.; Zeng, L. A Review of Renewable Energy Utilization in Islands. Renew. Sustain. Energy Rev. 2016, 59, 504–513. [Google Scholar] [CrossRef]

- Child, M.; Breyer, C. Transition and Transformation: A Review of the Concept of Change in the Progress towards Future Sustainable Energy Systems. Energy Policy 2017, 107, 11–26. [Google Scholar] [CrossRef]

- European Commission Clean Energy for EU Islands. Available online: https://clean-energy-islands.ec.europa.eu (accessed on 3 June 2024).

- African Union AEEP: Partnering for an African Energy Transition. Available online: https://africa-eu-energy-partnership.org (accessed on 3 June 2024).

- Wahlund, M.; Palm, J. The Role of Energy Democracy and Energy Citizenship for Participatory Energy Transitions: A Comprehensive Review. Energy Res. Soc. Sci. 2022, 87, 102482. [Google Scholar] [CrossRef]

- Johnson, V.; Hall, S. Community Energy and Equity: The Distributional Implications of a Transition to a Decentralised Electricity System. People Place Policy 2014, 8, 149–167. [Google Scholar] [CrossRef]

- Stephens, J.C. Energy Democracy: Redistributing Power to the People Through Renewable Transformation. Environ. Sci. Policy Sustain. Dev. 2019, 61, 4–13. [Google Scholar] [CrossRef]

- Seto, K.C.; Davis, S.J.; Mitchell, R.B.; Stokes, E.C.; Unruh, G.; Ürge-Vorsatz, D. Carbon Lock-In: Types, Causes, and Policy Implications. Annu. Rev. Environ. Resour. 2016, 41, 425–452. [Google Scholar] [CrossRef]

- Jacobsson, S.; Lauber, V. The Politics and Policy of Energy System Transformation—Explaining the German Diffusion of Renewable Energy Technology. Energy Policy 2006, 34, 256–276. [Google Scholar] [CrossRef]

- Tenenbaum, B.; Greacen, C.; Siyambalapitiya, T.; Knuckles, J. From the Bottom Up How Small Power Producers and Mini-Grids Can Deliver Electrification and Renewable Energy in Africa; World Bank Publications: Chicago, IL, USA, 2014. [Google Scholar]

- Ghanem, D.A.; Crosbie, T. The Transition to Clean Energy: Are People Living in Island Communities Ready for Smart Grids and Demand Response? Energies 2021, 14, 6218. [Google Scholar] [CrossRef]

- Schöne, N.; Greilmeier, K.; Heinz, B. Survey-Based Assessment of the Preferences in Residential Demand Response on the Island of Mayotte. Energies 2022, 15, 1338. [Google Scholar] [CrossRef]

- Otte, L.; Schmid, L.; Baerens, T.; Tomboanjara, M.; Ahmed, F.; Heinz, B. An Energy Transition for All: Investigating Determinants of Citizen Support for Energy Community Initiatives in Mayotte. Energy Res. Soc. Sci. 2024, accepted. [Google Scholar]

- Parag, Y.; Sovacool, B.K. Electricity Market Design for the Prosumer Era. Nat. Energy 2016, 1, 16032. [Google Scholar] [CrossRef]

- Flessa, A.; Fragkiadakis, D.; Zisarou, E.; Fragkos, P. Developing an Integrated Energy–Economy Model Framework for Islands. Energies 2023, 16, 1275. [Google Scholar] [CrossRef]

- Flessa, A.; Fragkiadakis, D.; Zisarou, E.; Fragkos, P. Decarbonizing the Energy System of Non-Interconnected Islands: The Case of Mayotte. Energies 2023, 16, 2931. [Google Scholar] [CrossRef]

- Luthander, R.; Widén, J.; Nilsson, D.; Palm, J. Photovoltaic Self-Consumption in Buildings: A Review. Appl. Energy 2015, 142, 80–94. [Google Scholar] [CrossRef]

- Delapedra-Silva, V.; Ferreira, P.; Cunha, J.; Kimura, H. Methods for Financial Assessment of Renewable Energy Projects: A Review. Processes 2022, 10, 184. [Google Scholar] [CrossRef]

- Global Solar Atlas. Mayotte. Available online: https://globalsolaratlas.info/map?s=-12.823048,45.152076&m=site&c=-12.823048,45.152076,11 (accessed on 6 March 2024).

- European Commission; Directorate General for Energy; Directorate General for Climate Action; Directorate General for Mobility and Transport. EU Reference Scenario 2020: Energy, Transport and GHG Emissions: Trends to 2050; Publications Office: Luxembourg, 2021. [Google Scholar]

- European Commission; Directorate General for Energy; E3 Modelling; Ecofys; Tractebel. Technology Pathways in Decarbonisation Scenarios; Publications Office: Luxembourg, 2020. [Google Scholar]

- International Renewable Energy Agency. Energy Profile Mayotte. 2023. Available online: https://www.irena.org/-/media/Files/IRENA/Agency/Statistics/Statistical_Profiles/Africa/Mayotte_Africa_RE_SP.pdf (accessed on 15 April 2024).

- Le Centre National de Ressources sur le Photovoltaïque. Connaître les Coûts et Evaluer la Rentabilité. 2024. Available online: https://www.photovoltaique.info/fr/preparer-un-projet/quelles-demarches-realiser/choisir-son-modele-economique/ (accessed on 15 February 2024).

- Institut National de la Statistique et des Etudes Economiques. The All Employees-Revised Index of Hourly Labour Cost—(ICHTrev-TS). 2022. Available online: https://www.insee.fr/en/statistiques/6541219#consulter (accessed on 30 January 2024).

- Institut National de la Statistique et des Etudes Economiques. Indice de prix de Production de L’industrie Française pour le Marché Français—A10 BE—Ensemble de L’industrie. 2023. Available online: https://www.insee.fr/fr/statistiques/serie/010534796#Tableau (accessed on 30 January 2024).

- Commission de Régulation de L’énergie. Révision Trimestrielle des Paramètres de L’arrêté “PV ZNI”. 2023. Available online: https://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=&cad=rja&uact=8&ved=2ahUKEwis-uaqvLaBAxWkQPEDHcQLBX8QFnoECBAQAQ&url=https%3A%2F%2Fwww.cre.fr%2Fcontent%2Fdownload%2F19601%2F235736&usg=AOvVaw1-v1Y36AhjjPLIqwH1S7zC&opi=89978449 (accessed on 19 September 2023).

- Huld, T.; Ruf, H.; Heilscher, G. Self-Consumption of Electricity by Households, Effects of PV System Size and Battery Storage. In Proceedings of the 29th European Photovoltaic Solar Energy Conference and Exhibition, Amsterdam, The Netherlands, 22–26 September 2014; pp. 4014–4017. [Google Scholar] [CrossRef]

- Dehler, J.; Keles, D.; Telsnig, T.; Fleischer, B.; Baumann, M.; Fraboulet, D.; Faure-Schuyer, A.; Fichtner, W. Self-Consumption of Electricity from Renewable Sources. In Europe’s Energy Transition—Insights for Policy Making; Elsevier: Amsterdam, The Netherlands, 2017; pp. 225–236. ISBN 978-0-12-809806-6. [Google Scholar]

- Guaita-Pradas, I.; Blasco-Ruiz, A. Analyzing Profitability and Discount Rates for Solar PV Plants. A Spanish Case. Sustainability 2020, 12, 3157. [Google Scholar] [CrossRef]

- Shao, X.; Fang, T. Performance Analysis of Government Subsidies for Photovoltaic Industry: Based on Spatial Econometric Model. Energy Strategy Rev. 2021, 34, 100631. [Google Scholar] [CrossRef]

- Del Río, P.; Mir-Artigues, P. Support for Solar PV Deployment in Spain: Some Policy Lessons. Renew. Sustain. Energy Rev. 2012, 16, 5557–5566. [Google Scholar] [CrossRef]

- Hsu, C.-W. Using a System Dynamics Model to Assess the Effects of Capital Subsidies and Feed-in Tariffs on Solar PV Installations. Appl. Energy 2012, 100, 205–217. [Google Scholar] [CrossRef]

- Inês, C.; Guilherme, P.L.; Esther, M.-G.; Swantje, G.; Stephen, H.; Lars, H. Regulatory Challenges and Opportunities for Collective Renewable Energy Prosumers in the EU. Energy Policy 2020, 138, 111212. [Google Scholar] [CrossRef]

- Masson, G.; Kaizuka, I. Trends in Photovoltaic Applications 2021; The International Energy Agency: Paris, France, 2021. [Google Scholar]

- Tongsopit, S.; Junlakarn, S.; Wibulpolprasert, W.; Chaianong, A.; Kokchang, P.; Hoang, N.V. The Economics of Solar PV Self-Consumption in Thailand. Renew. Energy 2019, 138, 395–408. [Google Scholar] [CrossRef]

- López Prol, J.; Steininger, K.W. Photovoltaic Self-Consumption Regulation in Spain: Profitability Analysis and Alternative Regulation Schemes. Energy Policy 2017, 108, 742–754. [Google Scholar] [CrossRef]

- Gautier, A.; Jacqmin, J.; Poudou, J.-C. The Prosumers and the Grid. J. Regul. Econ. 2018, 53, 100–126. [Google Scholar] [CrossRef]

- Eid, C.; Reneses Guillén, J.; Frías Marín, P.; Hakvoort, R. The Economic Effect of Electricity Net-Metering with Solar PV: Consequences for Network Cost Recovery, Cross Subsidies and Policy Objectives. Energy Policy 2014, 75, 244–254. [Google Scholar] [CrossRef]

- Gautier, A.; Hoet, B.; Jacqmin, J.; Van Driessche, S. Self-Consumption Choice of Residential PV Owners under Net-Metering. Energy Policy 2019, 128, 648–653. [Google Scholar] [CrossRef]

- Simshauser, P. Distribution Network Prices and Solar PV: Resolving Rate Instability and Wealth Transfers through Demand Tariffs. Energy Econ. 2016, 54, 108–122. [Google Scholar] [CrossRef]

- Xu, X.; Chen, C.; Zhu, X.; Hu, Q. Promoting Acceptance of Direct Load Control Programs in the United States: Financial Incentive versus Control Option. Energy 2018, 147, 1278–1287. [Google Scholar] [CrossRef]

- Carmichael, R.; Schofield, J.; Woolf, M.; Bilton, M.; Ozaki, R.; Strbac, G. Residential Consumer Attitudes to Time-Varying Pricing; Imperial College London: London, UK, 2014. [Google Scholar]

- Pacudan, R. Feed-in Tariff vs Incentivized Self-Consumption: Options for Residential Solar PV Policy in Brunei Darussalam. Renew. Energy 2018, 122, 362–374. [Google Scholar] [CrossRef]

- Petrichenko, L.; Sauhats, A.; Diahovchenko, I.; Segeda, I. Economic Viability of Energy Communities versus Distributed Prosumers. Sustainability 2022, 14, 4634. [Google Scholar] [CrossRef]

- Roberts, M.B.; Bruce, A.; MacGill, I. A Comparison of Arrangements for Increasing Self-Consumption and Maximising the Value of Distributed Photovoltaics on Apartment Buildings. Sol. Energy 2019, 193, 372–386. [Google Scholar] [CrossRef]

- Roberts, M.B.; Bruce, A.; MacGill, I. Impact of Shared Battery Energy Storage Systems on Photovoltaic Self-Consumption and Electricity Bills in Apartment Buildings. Appl. Energy 2019, 245, 78–95. [Google Scholar] [CrossRef]

- Luthander, R.; Widén, J.; Munkhammar, J.; Lingfors, D. Self-Consumption Enhancement and Peak Shaving of Residential Photovoltaics Using Storage and Curtailment. Energy 2016, 112, 221–231. [Google Scholar] [CrossRef]

- Reis, I.F.; Gonçalves, I.; Lopes, M.A.; Antunes, C.H. Business Models for Energy Communities: A Review of Key Issues and Trends. Renew. Sustain. Energy Rev. 2021, 144, 111013. [Google Scholar] [CrossRef]

- Zhang, H.; Wu, K.; Qiu, Y.; Chan, G.; Wang, S.; Zhou, D.; Ren, X. Solar Photovoltaic Interventions Have Reduced Rural Poverty in China. Nat. Commun. 2020, 11, 1969. [Google Scholar] [CrossRef]

- O’Shaughnessy, E.; Barbose, G.; Wiser, R.; Forrester, S.; Darghouth, N. The Impact of Policies and Business Models on Income Equity in Rooftop Solar Adoption. Nat. Energy 2020, 6, 84–91. [Google Scholar] [CrossRef]

- Institut National de la Statistique et des Etudes Economiques. La France et ses Territoires: Édition 2021. 2021. Available online: https://www.insee.fr/fr/statistiques/5039943?sommaire=5040030 (accessed on 18 September 2023).

- Institut National de la Statistique et des Etudes Economiques. Les Inégalités de Niveau de vie se Sont Creusées. Revenus et Pauvreté à Mayotte en 2018. 2020. Available online: https://www.insee.fr/fr/statistiques/4622454#consulter (accessed on 2 April 2024).

- Institut National de la Statistique et des Etudes Economiques. Unité de Consommation. 2022. Available online: https://www.insee.fr/fr/metadonnees/definition/c1802 (accessed on 16 February 2024).

- United Nations Population Division. Database on Household Size and Composition 2022. 2022. Available online: https://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=&cad=rja&uact=8&ved=2ahUKEwi54vGOwYCFAxXlS_EDHRazBR0QFnoECBkQAQ&url=https%3A%2F%2Fwww.un.org%2Fdevelopment%2Fdesa%2Fpd%2Fsites%2Fwww.un.org.development.desa.pd%2Ffiles%2Fundesa_pd_2022_hh-size-composition.xlsx&usg=AOvVaw0h4EORCnOKRU2944P7Nn2M&opi=89978449 (accessed on 19 March 2024).

- Braito, M.; Flint, C.; Muhar, A.; Penker, M.; Vogel, S. Individual and Collective Socio-Psychological Patterns of Photovoltaic Investment under Diverging Policy Regimes of Austria and Italy. Energy Policy 2017, 109, 141–153. [Google Scholar] [CrossRef]

| KPI | Definition and Purpose | Calculation | Interpretation |

|---|---|---|---|

| LCOE | Average cost of electricity generation for a generation asset over its economic lifetime. Used in our analysis as a first indication of investment decisions. | Dividing the total non-discounted costs of electricity generation, including specific investment cost, capital costs and OPEX, by the total electricity generated over the investment’s economic lifetime. | Minimum revenue or tariff that a given investment would need to receive per unit produced to achieve cost neutrality. |

| NPV | Present value of the future cash flows generated by a project. Applies a discount rate that reflects the minimal acceptable rate of return, e.g., relating to the returns of comparable investments or the cost of capital. | Sum of all discounted cash flows over a project’s economic lifetime, i.e., 15 years. | If NPV > 0: investment is expected to generate a return above the discount rate, and is therefore profitable. If NPV < 0: investment is expected to generate a return below the discount rate, and is not financially attractive. |

| IRR | Estimation of the profitability of an investment using a relative (percentage) value rather than an absolute monetary amount. | Computing the discount rate that will result in the expected NPV of an investment to be zero. | The expected profitability rate of an investment. If the IRR exceeds the cost of capital, the investment is considered profitable. |

| Simple payback time | Time period needed for the investment to recover its initial cost, i.e., the specific investment cost, through subsequent, non-discounted yearly cash flows. | Time period in which the sum of initial expenditures (specific investment cost; negative) and the subsequent non-discounted cash flows (interest payments, OPEX, revenues; ideally net positive) reaches zero. | If payback time > economic lifetime: the initial investment cannot be recovered within the economic lifetime of the asset, indicating that an investment is not economically viable. |

| System Size/Year | 2020 | 2025 | 2030 | 2035 | 2040 | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| Base | DD | Base | DD | Base | DD | Base | DD | Base | DD | |

| 36–100 kWp (Producer) | 7.60 | 7.60 | 8.10 | 8.10 | 9.80 | 8.85 | 8.62 | 6.23 | 6.66 | 3.33 |

| 36–100 kWp (Prosumer) | 7.60 | 7.60 | 8.10 | 8.10 | 9.80 | 8.85 | 8.62 | 6.23 | 6.66 | 3.33 |

| 9–36 kWp | 6.67 | 6.67 | 7.17 | 7.17 | 8.11 | 7.91 | 6.77 | 4.58 | 4.65 | 1.56 |

| 3–9 kWp | 0.69 | 0.69 | 1.18 | 1.18 | 1.91 | 1.91 | 0.12 | −1.59 | −2.22 | −5.17 |

| <3 kWp | −0.73 | −0.73 | −0.23 | −0.23 | 0.51 | 0.51 | −2.21 | −2.98 | −4.80 | −7.62 |

| System Size/Year | 2020 | 2025 | 2030 | 2035 | 2040 | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| Base | DD | Base | DD | Base | DD | Base | DD | Base | DD | |

| 36–100 kWp (Producer) | 9 | 9 | 9 | 9 | 9 | 9 | 9 | 11 | 7 | 14 |

| 36–100 kWp (Prosumer) | 9 | 9 | 9 | 9 | 8 | 9 | 9 | 10 | 10 | 12 |

| 9–36 kWp | 10 | 10 | 10 | 10 | 9 | 9 | 10 | 11 | 11 | 14 |

| 3–9 kWp | 15 | 15 | 14 | 14 | 13 | 13 | 15 | >15 | >15 | >15 |

| <3 kWp | >15 | >15 | >15 | >15 | 15 | 15 | >15 | >15 | >15 | >15 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Otte, L.; Schöne, N.; Flessa, A.; Fragkos, P.; Heinz, B. Costs and Benefits of Citizen Participation in the Energy Transition: Investigating the Economic Viability of Prosumers on Islands—The Case of Mayotte. Energies 2024, 17, 2904. https://doi.org/10.3390/en17122904

Otte L, Schöne N, Flessa A, Fragkos P, Heinz B. Costs and Benefits of Citizen Participation in the Energy Transition: Investigating the Economic Viability of Prosumers on Islands—The Case of Mayotte. Energies. 2024; 17(12):2904. https://doi.org/10.3390/en17122904

Chicago/Turabian StyleOtte, Lukas, Nikolas Schöne, Anna Flessa, Panagiotis Fragkos, and Boris Heinz. 2024. "Costs and Benefits of Citizen Participation in the Energy Transition: Investigating the Economic Viability of Prosumers on Islands—The Case of Mayotte" Energies 17, no. 12: 2904. https://doi.org/10.3390/en17122904

APA StyleOtte, L., Schöne, N., Flessa, A., Fragkos, P., & Heinz, B. (2024). Costs and Benefits of Citizen Participation in the Energy Transition: Investigating the Economic Viability of Prosumers on Islands—The Case of Mayotte. Energies, 17(12), 2904. https://doi.org/10.3390/en17122904