Since its appearance in 2009, the cryptocurrency market has assumed increasing importance in financial and economic systems. The authors of [

1] indicated that the creation of virtual currencies was considered the first step in the digitalization of the financial and economic system. They similarly illustrated that the magnitude of the digital economy is expected to reach a value of 23 trillion USD in 2025. In addition, [

2] added that there are various cryptocurrencies, of which the most popular is Bitcoin. The authors of [

3] also showed that the attraction of investors, financial authorities, and researchers to Bitcoin assets is due to the rapid increase of the price from zero in 2009 to USD 57,668 in 2021. However, they affirmed that this huge fluctuation in Bitcoin price increases concerns amongst policymakers about this asset and illustrates the different risks that can be generated by Bitcoin trading [

3,

4]. First, the fluctuation of the Bitcoin price can destabilize economies and augment uncertainty about the stability of financial and economic systems in the future. Concretely, financial authorities in these countries consider that Bitcoin has no physical presence, and its movement cannot be supervised in worldwide markets because Bitcoins are transferred between individuals and institutions through the Internet using an encrypted database that allows investors to quickly and securely transfer funds outside the conventional central payment system, hence it is not subject to the supervision of central banks and governments. Second, trading in Bitcoin in an illegal manner and outside the control of government contravenes the most important function of monetary authorities, namely money creation, which is based on the analysis of economic growth trends and inflation, and which should rely on a balance of gold, foreign currencies, and financial instruments. Third, Bitcoin is unable to play an important role at the international level as traditional currencies do, because it lacks basic functions as an intermediary for transactions, which are unit of account and store of value. To avoid this limitation, it must have a set of elements that allow it to perform these functions reasonably, the most important of which is the degree of confidence in the economic and political stability of the issuing country of this virtual currency. This is not currently achieved in virtual currencies. In addition to these studies that focused on the different risks of Bitcoin, other studies have tried to investigate different dimensions of Bitcoin, such as return volatility [

5,

6,

7,

8,

9,

10,

11]. Due to the importance of Bitcoin, whether from a negative or positive perspective, recent studies have appeared that are concerned with the relationship between Bitcoin prices (BP), mining, and energy consumption (BEC) [

12,

13,

14,

15]. These studies have shown that Bitcoin mining centers use sophisticated computing hardware and an enormous amount of energy to create and validate new coins. At the beginning of 2017, Bitcoin was using 6.6 terawatt-hours (TWh) of energy annually. In October 2020, it reached 67 TWh. And in the year 2021, the number has almost doubled to 121 TWh. The authors of [

14] noted that the cost of electricity per Bitcoin mining and the price of Bitcoin has a direct impact on the profitability of miners. When the cost of electricity per Bitcoin is lower than Bitcoin prices, miners will make a profit; but when the cost of electricity per Bitcoin mining goes up, energy consumption is higher, and miners will make losses. This strong relationship between BP, energy usage, and the evolution of mining costs may add to growing worries about the energy demand of Bitcoin mining and its growing influence on climate change. In addition to this, the existence of unknowns in the mining process, such as the type of mining hardware employed and the time taken, causes considerable deviations in Bitcoin energy consumption (hereafter BEC) estimates.

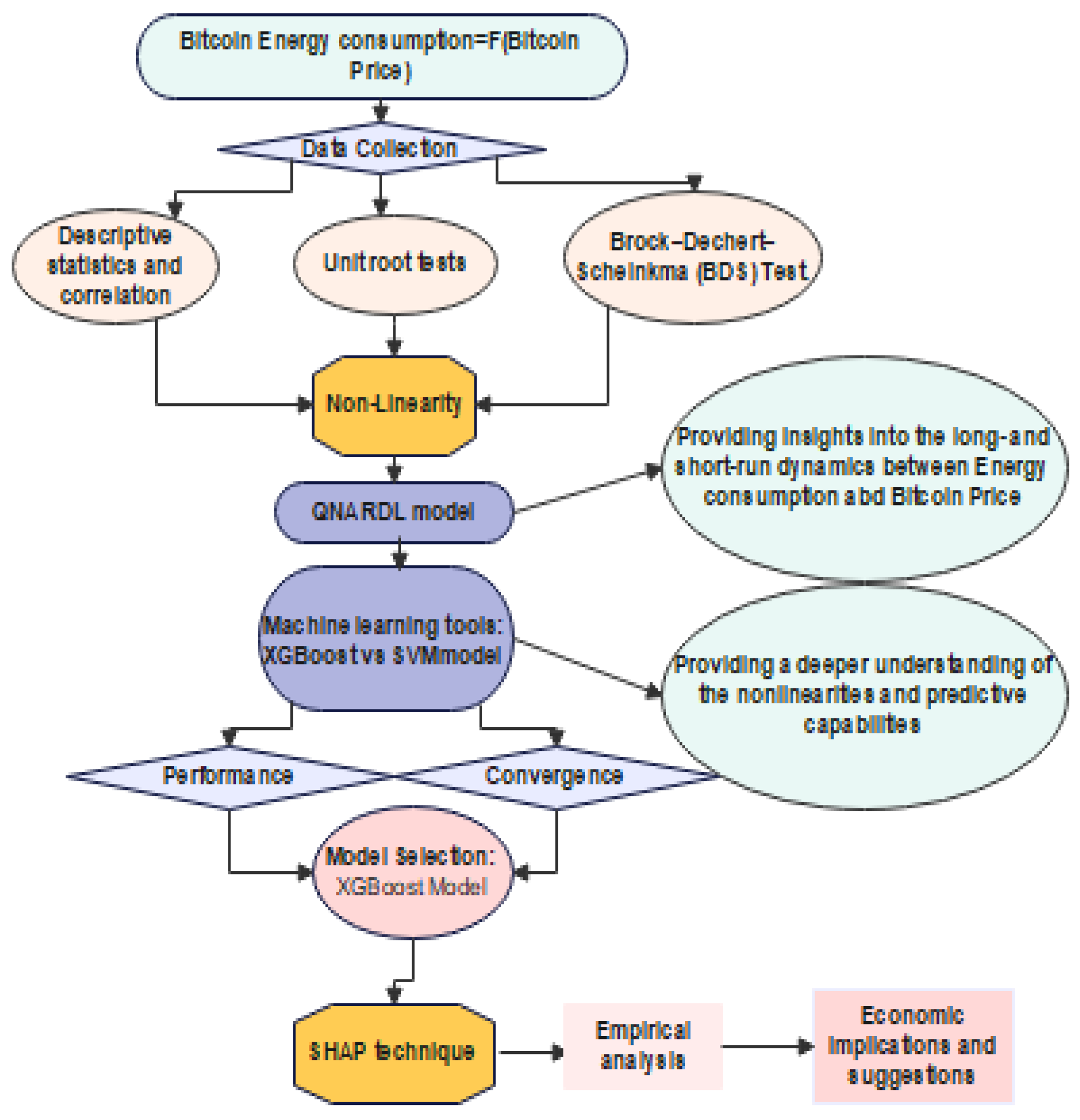

In this paper, we attempt to find out how BEC and BP interact. To do this, we opt for the quantile nonlinear autoregressive distributed lags (hereafter QNARDL) model proposed by [

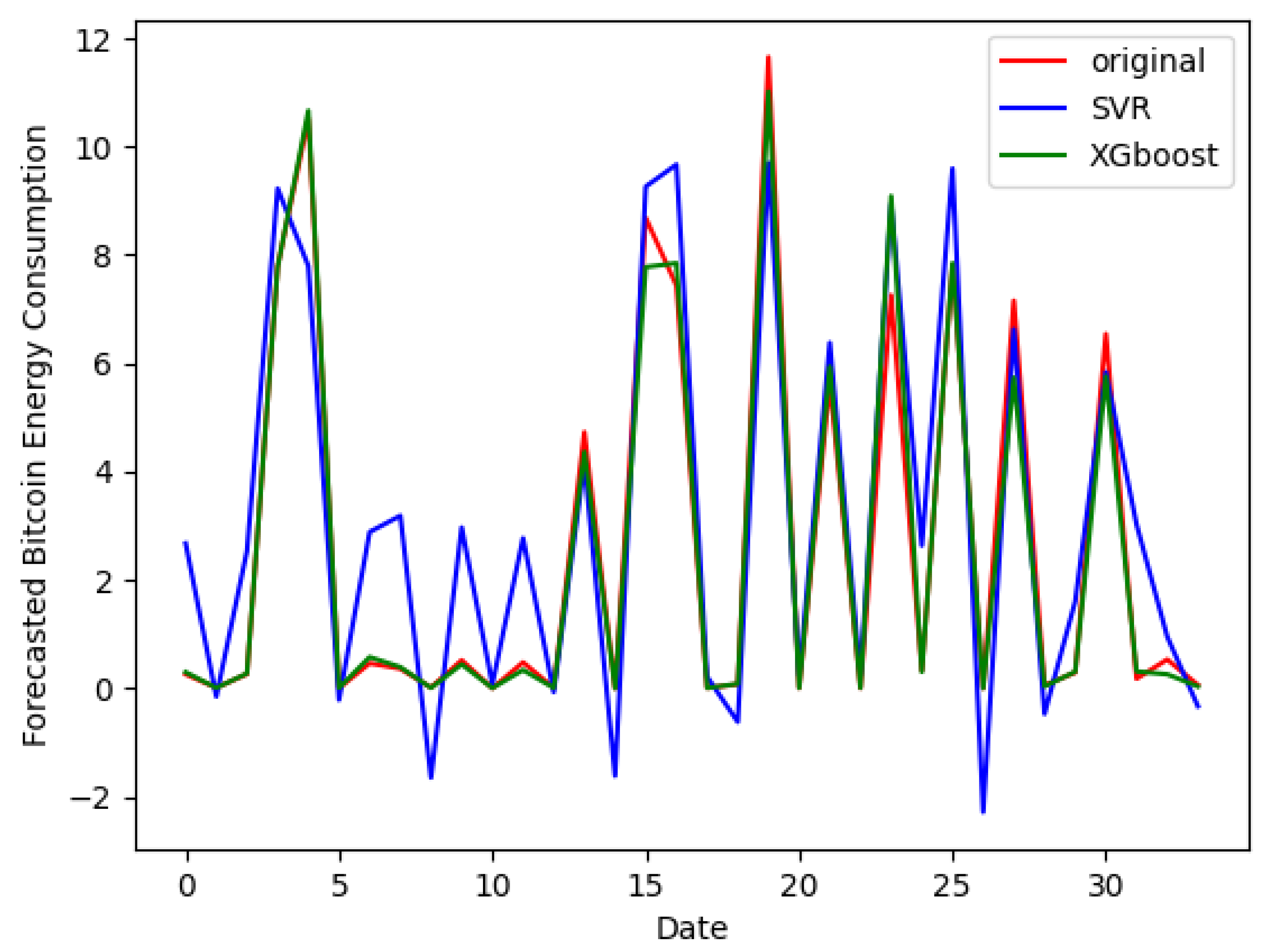

16] to consider chaotic and non-linear anomalies in data. Afterward, we will apply machine learning methods like the Support Vector Machine (SVM) and eXtreme Gradient Boosting (XGBoost) to estimate BEC. Much attention has been paid to Bitcoin’s environmental effect, especially regarding its energy consumption, because of its growing popularity. It is essential to comprehend the connection between energy consumption and Bitcoin pricing to make well-informed decisions on the sustainability of cryptocurrency operations. As a result, the fundamental objective of this study is to look at the nonlinear, long- and short-run distributional asymmetries of Bitcoin prices on Bitcoin energy usage. Our objective is to give new perspectives on this complex connection by combining classic econometric approaches with cutting-edge machine learning features.

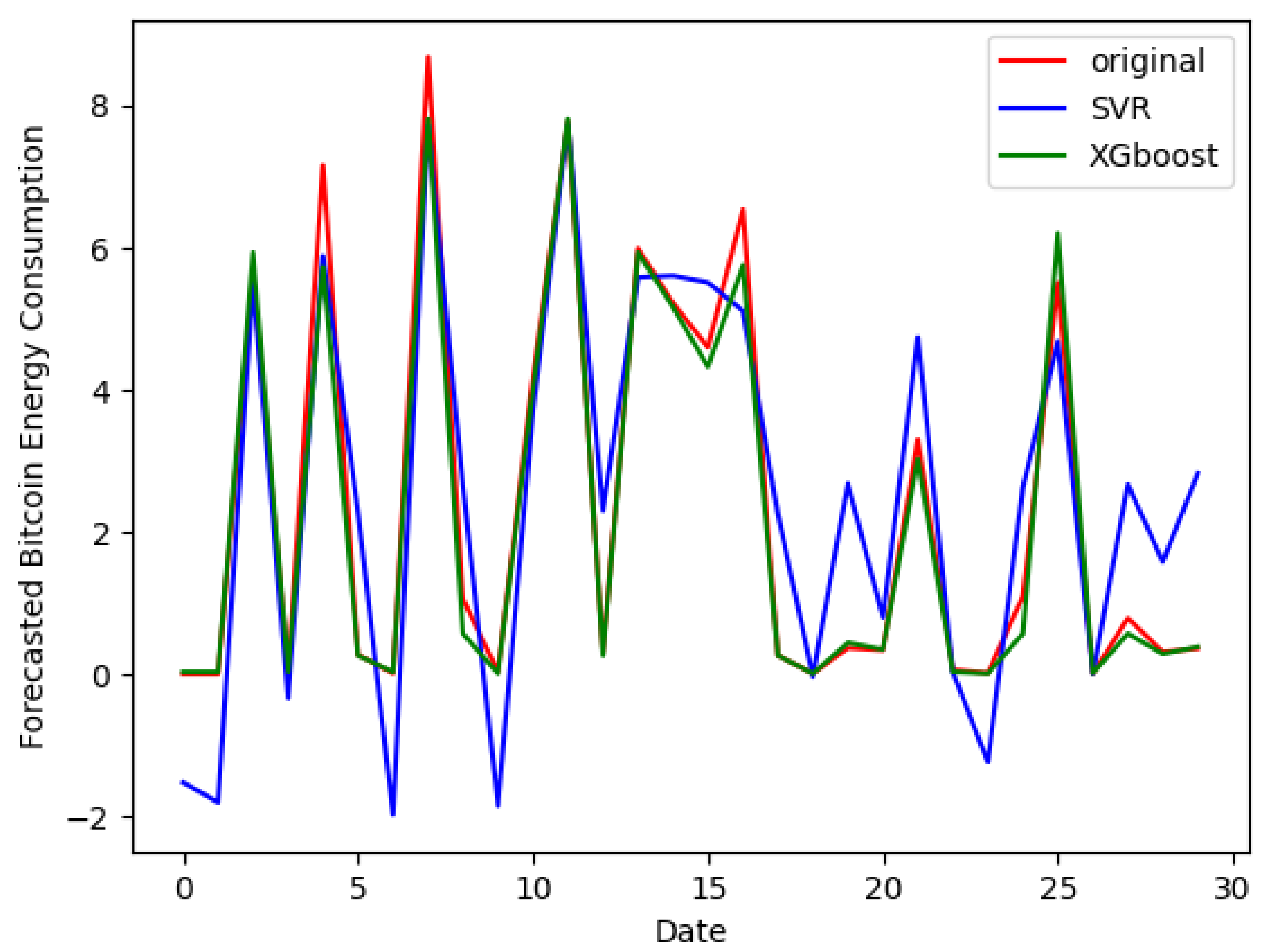

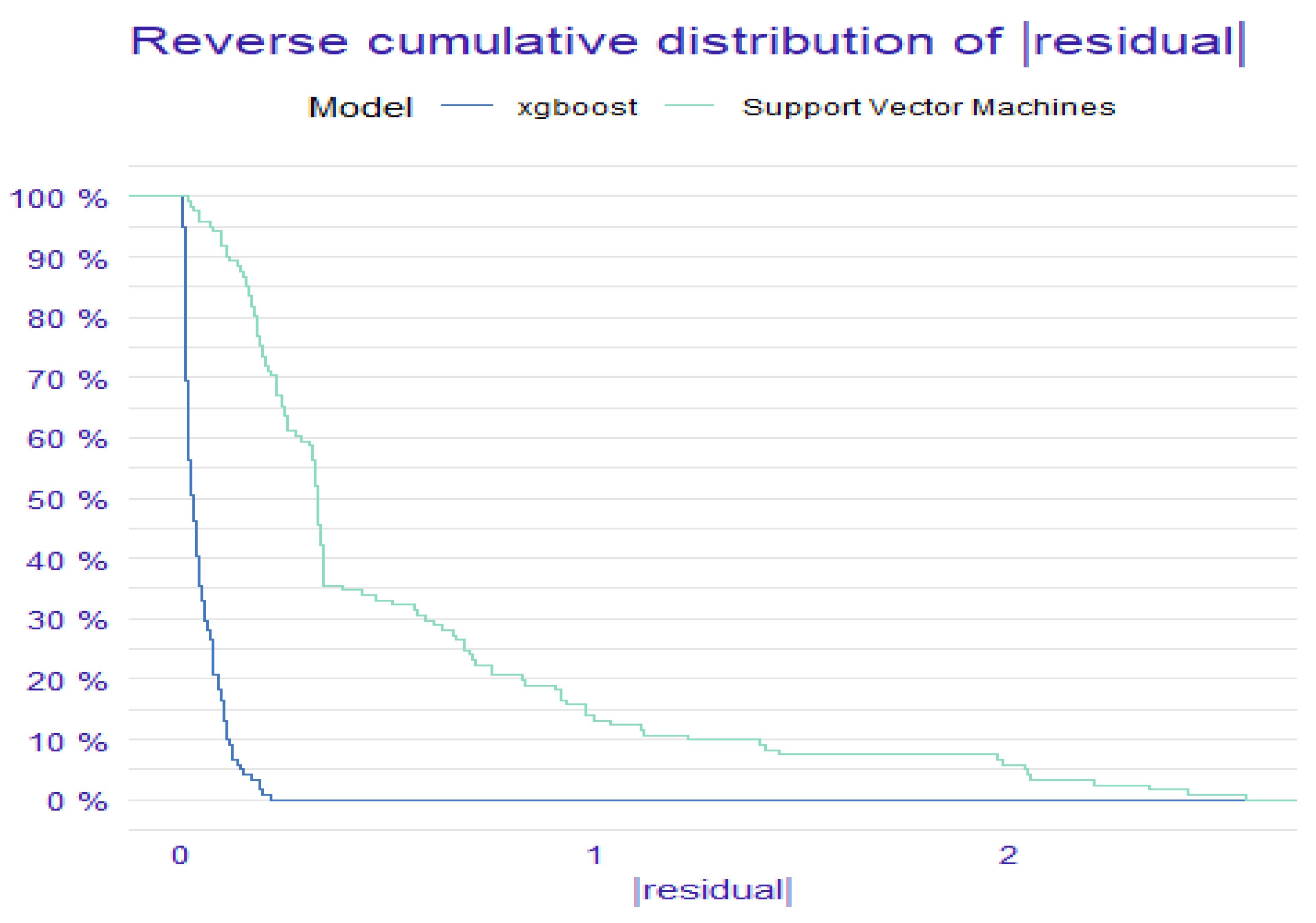

This study’s primary goal is to investigate the asymmetric effects of Bitcoin prices on Bitcoin energy usage using sophisticated approaches. Specifically, we want to use the non-conventional XGBoost machine learning technology in conjunction with the classic Quantile Nonlinear Autoregressive Distributed Lag (QNARDL) model. Through this approach, we want to illuminate the complex relationships between energy use and Bitcoin prices, highlighting disparities in distribution as well as short- and long-term impacts. We hope that our study will add to the current debate on sustainable Bitcoin usage and provide useful information to stakeholders and policymakers.

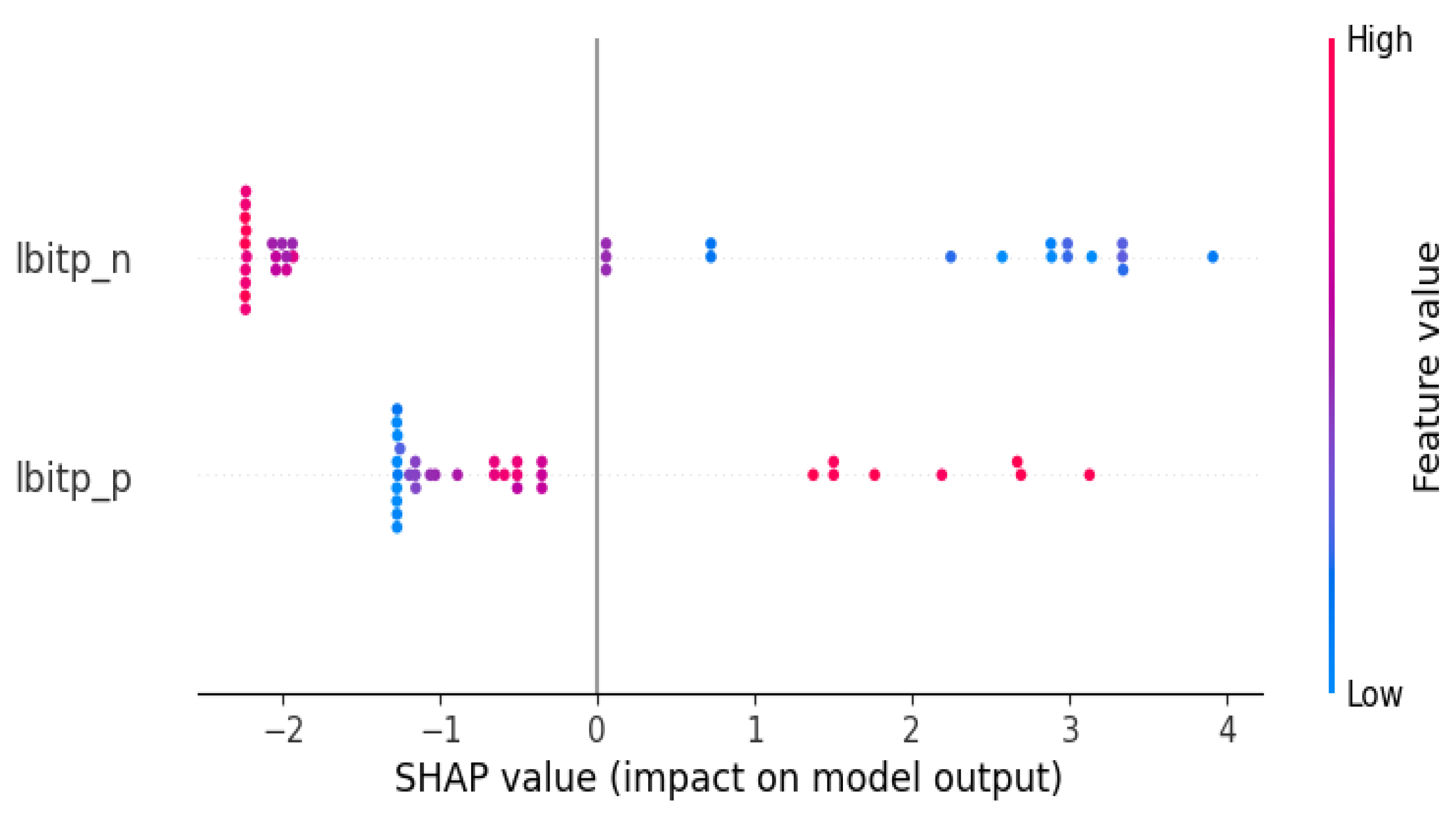

This study’s original element is the use of the QNARDL model and the XGBoost machine learning technology to examine the link between Bitcoin prices and energy use. Although nonlinear effects and distributional asymmetries may be explored using the QNARDL model, the addition of XGBoost improves our analysis’s prediction power. By combining established and innovative approaches, we may get new perspectives on the intricate relationship between energy use and Bitcoin pricing, which may help us better understand how the proliferation of cryptocurrencies will affect the environment.

In many aspects, the current work is different from the preceding literature. First, we attach a new feature to the cryptocurrency energy consumption literature by investigating the short- and long-run asymmetric relationship between BEC and BP. To the best of our knowledge, no research has looked at the dynamic spillover of BEC and BP from a short- and long-run asymmetric point of view. Second, we employ the QNARDL model proposed by [

16] and the nonlinear causality test advanced by [

17]. These methods, which have never been considered before in this context, allow us to study the interaction between BEC and BP over several quantiles. Third, this paper is the pioneer in investigating the forecasting power of negative and positive changes to BP on the BEC by using machine learning methods: Support Vector Machine (SVM) and eXtreme Gradient Boosting (XGBoost). The remainder of this paper is organized as follows.

Section 2 presents the literature review. Data and methodology are reported in

Section 3.

Section 4 shows the model estimation and results, and

Section 5 concludes.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}