The European Market for Guarantees of Origin for Green Electricity: A Scenario-Based Evaluation of Trading under Uncertainty

Abstract

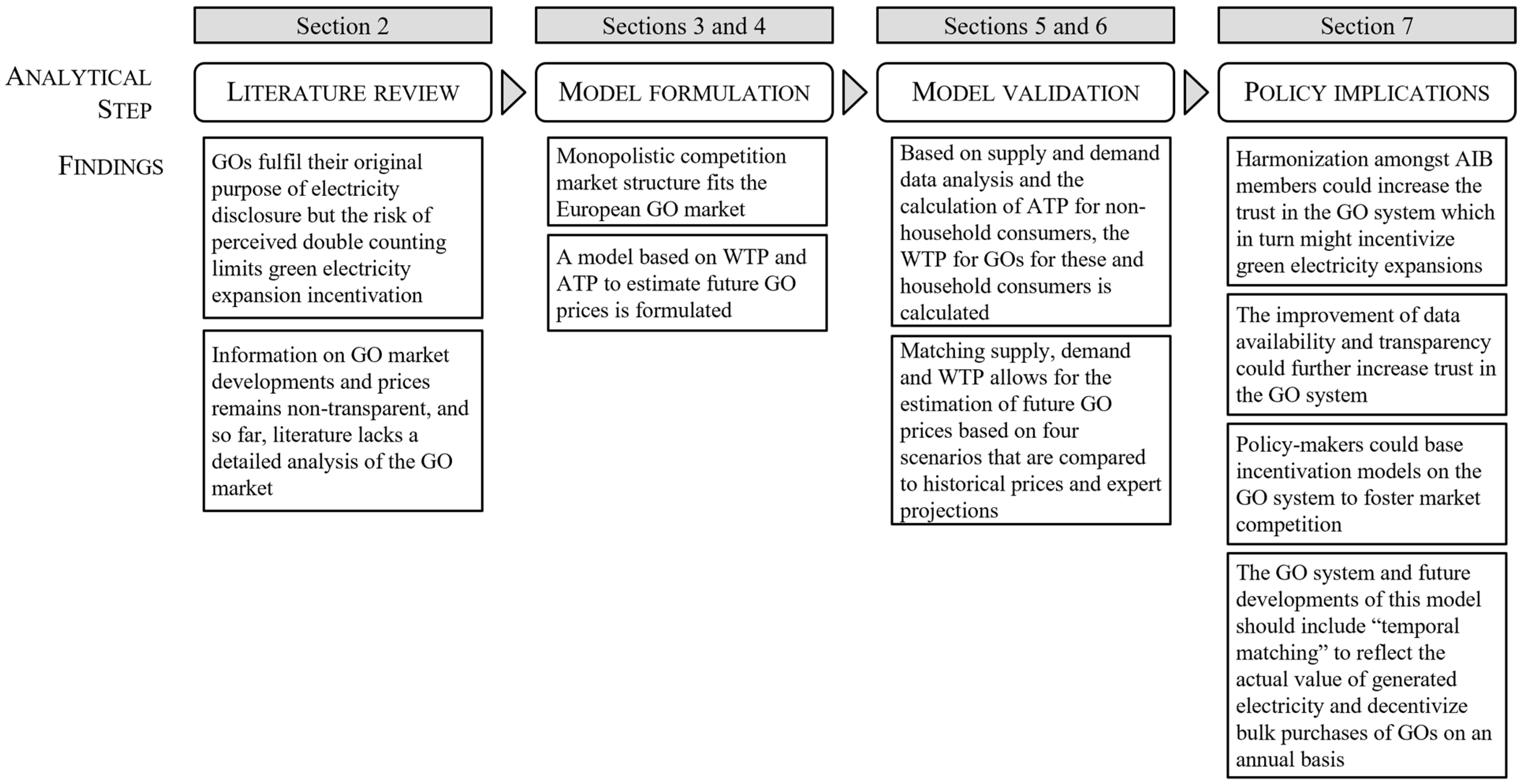

:1. Introduction

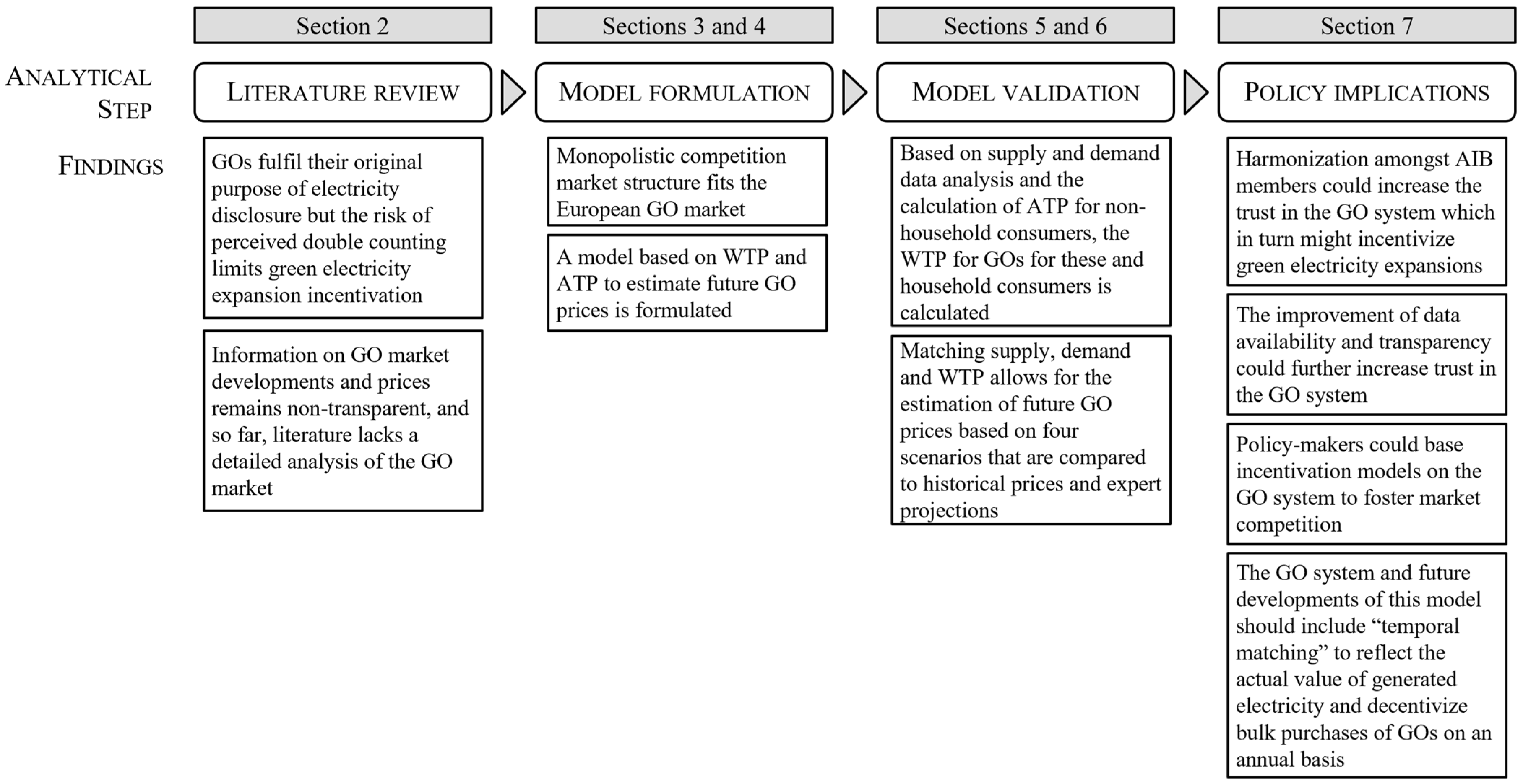

2. Literature Review

2.1. Critical Evaluation of GOs

2.2. Price Information and Evaluation

2.3. Willingness to Pay for Green Electricity

2.4. Interim Conclusion on Literature

3. Theoretical Background

3.1. Monopolistic Competition

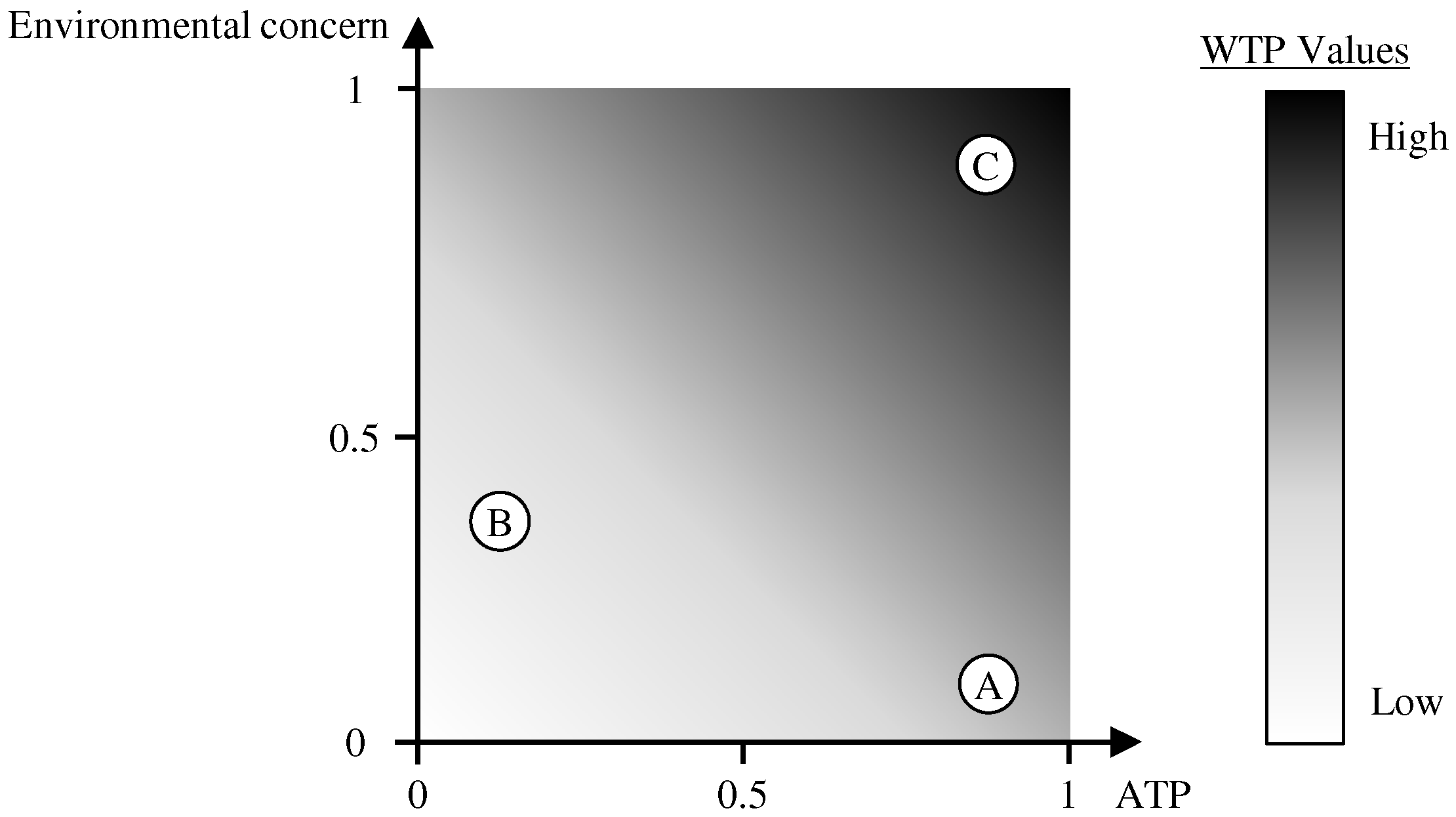

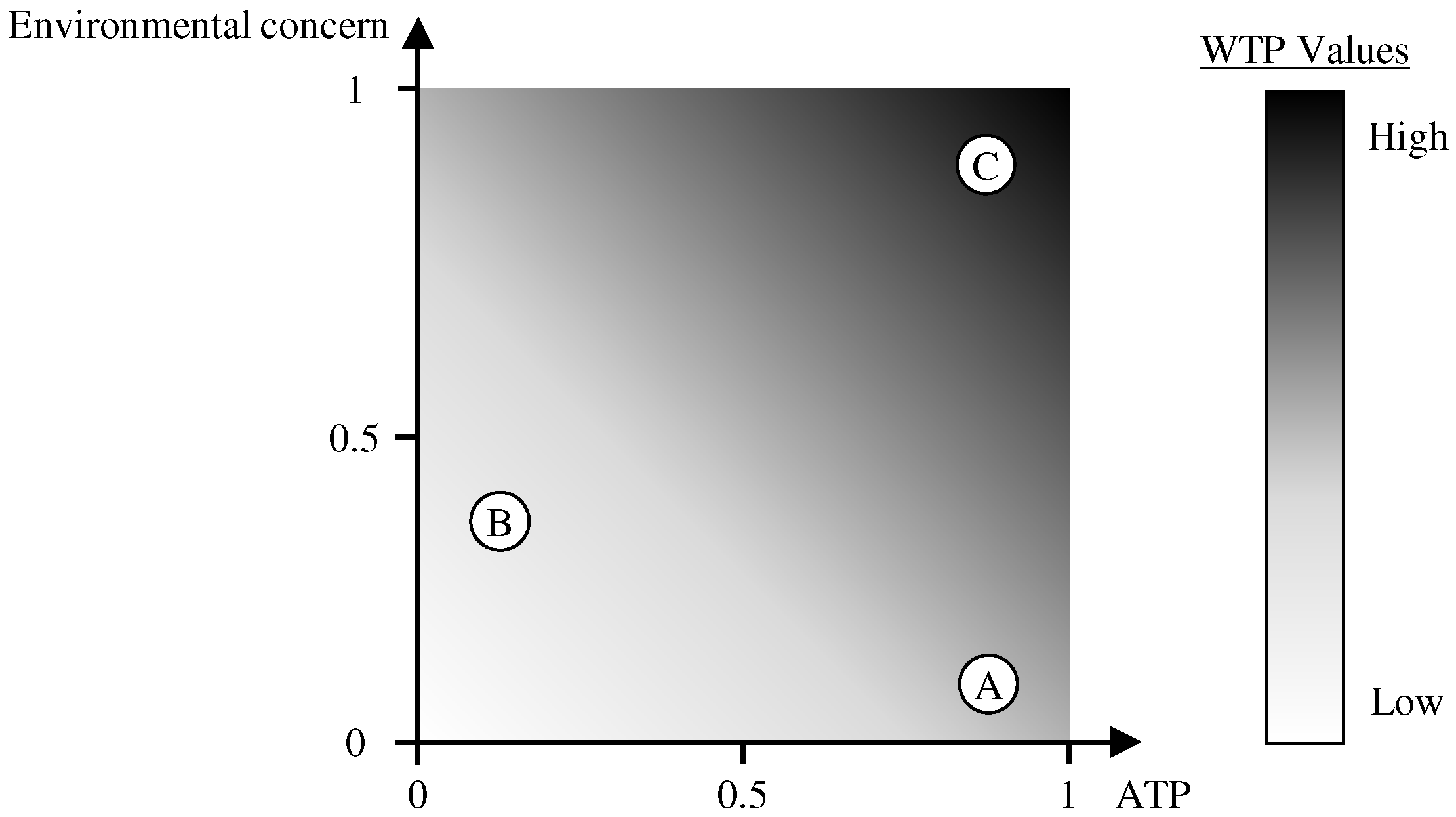

3.2. Willingness and Ability to Pay and Environmental Concern

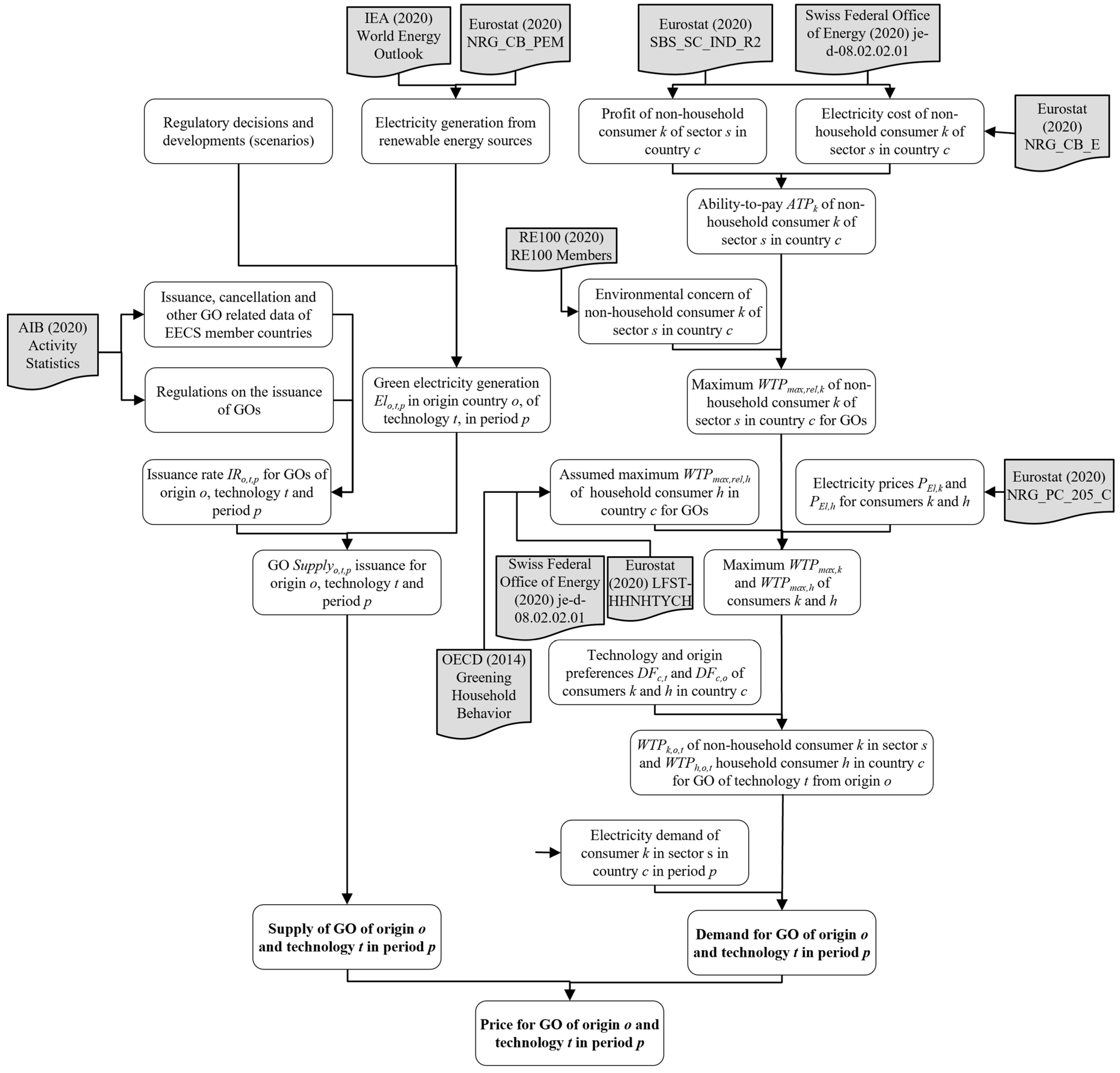

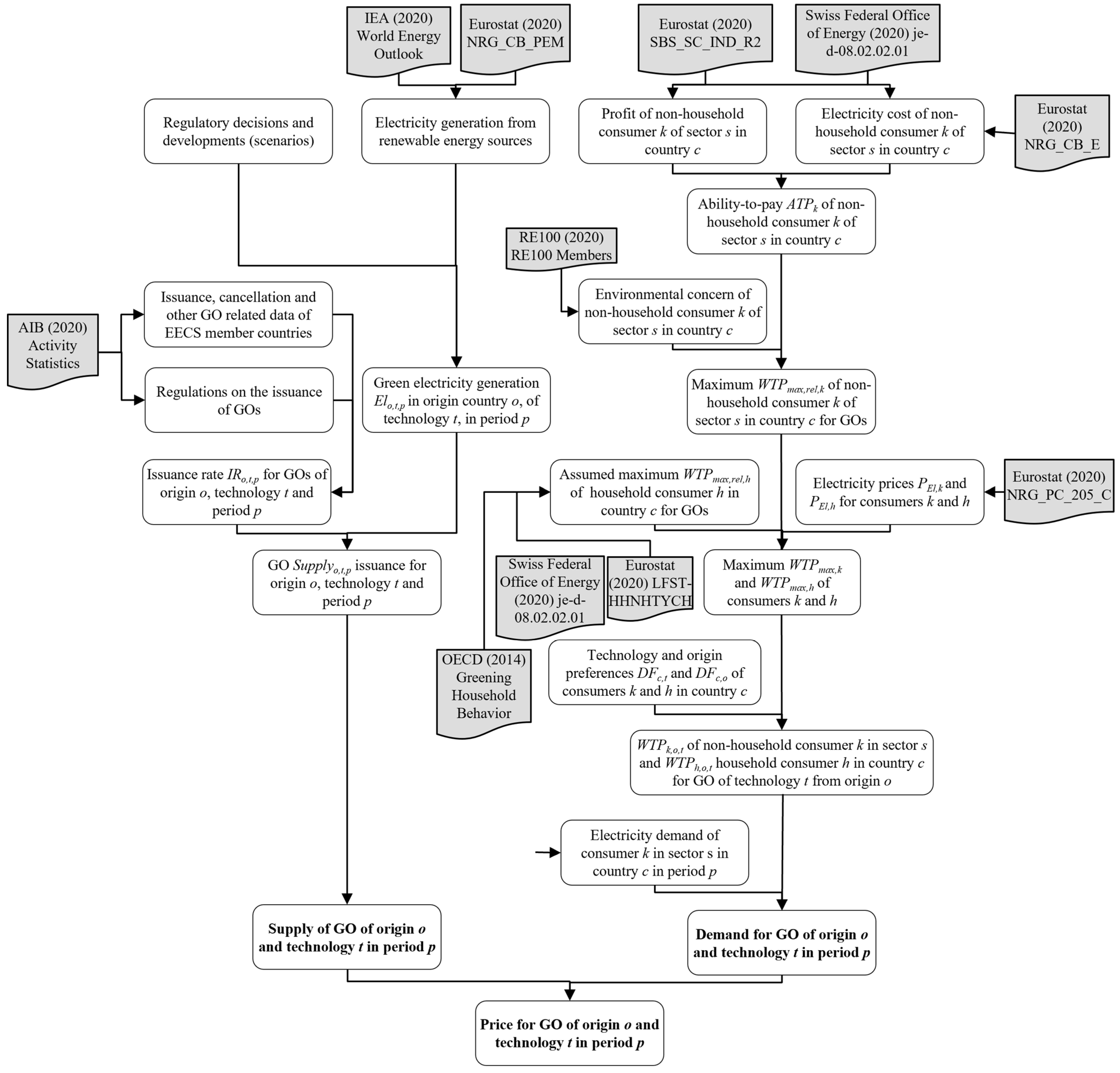

4. Model Specification

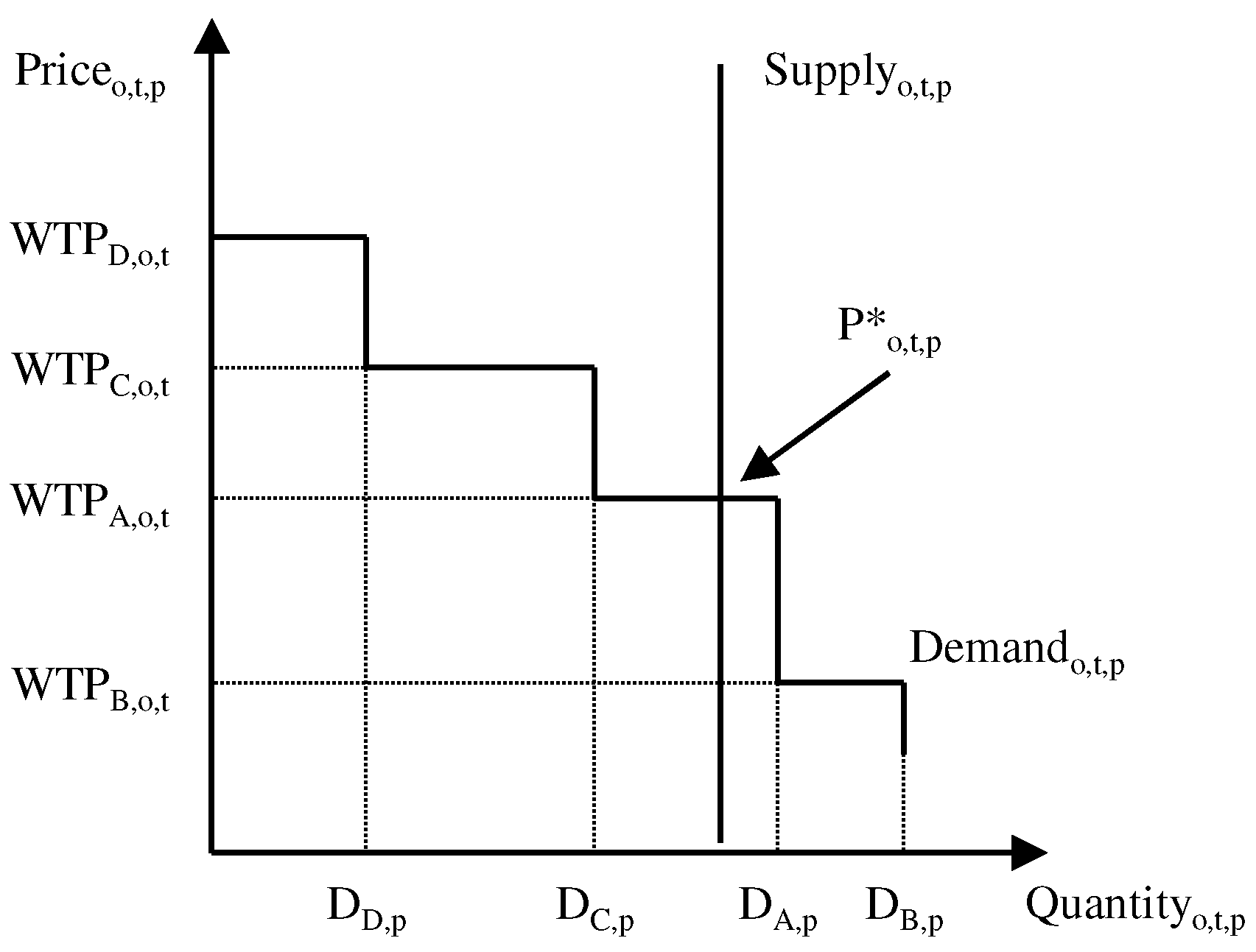

4.1. Modeling of GO Supply

4.2. Modeling of GO Demand

4.3. Model Assumptions and Limitations

5. Data and Scenarios

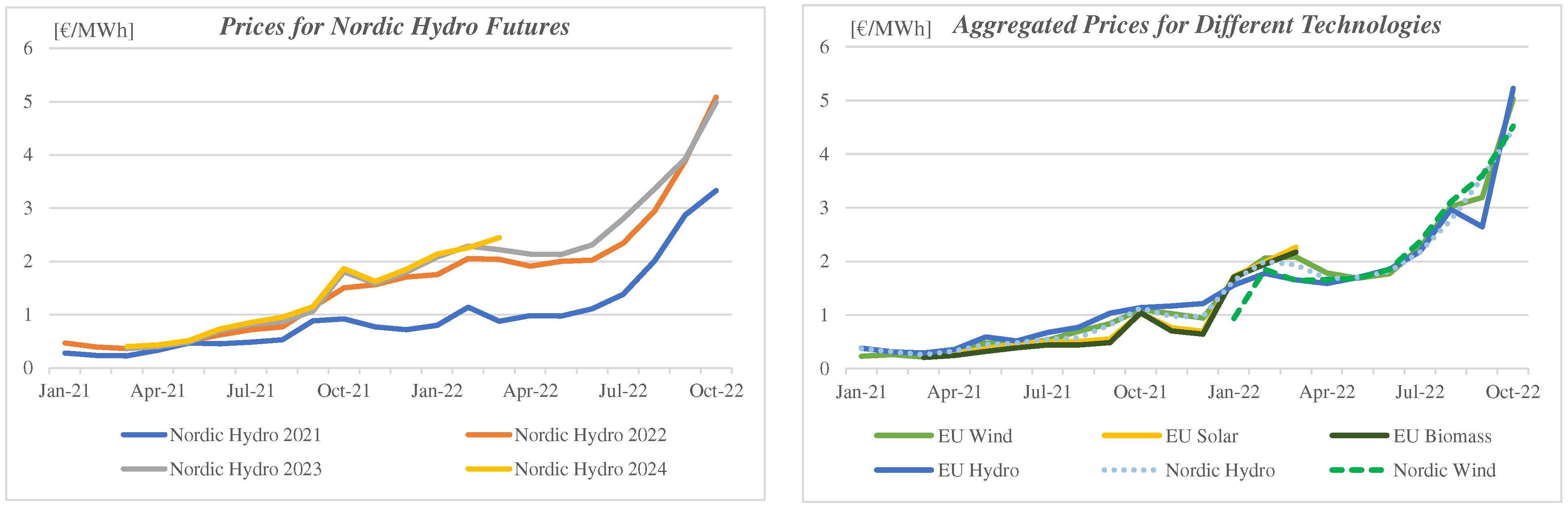

5.1. GO Data

5.2. ATP-WTP Data

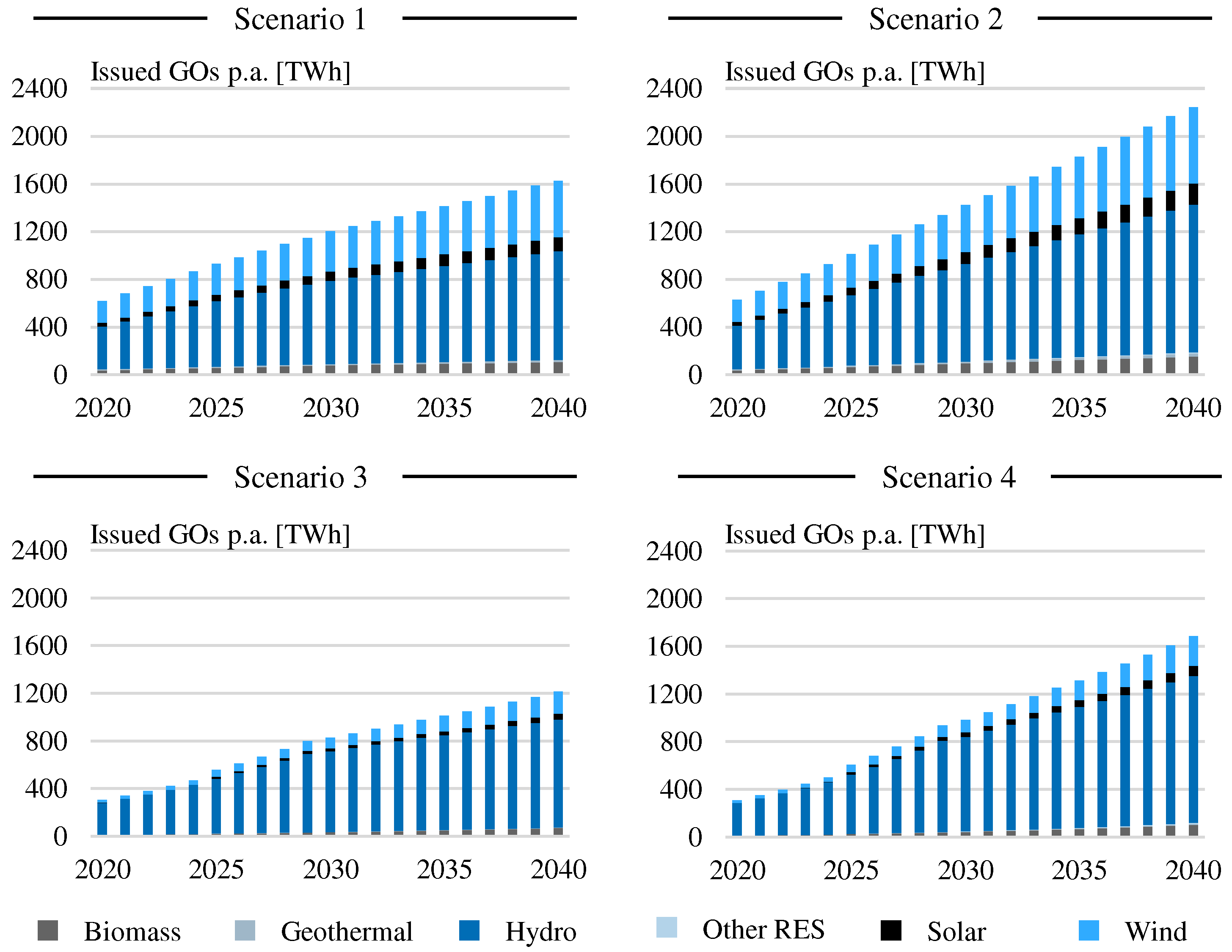

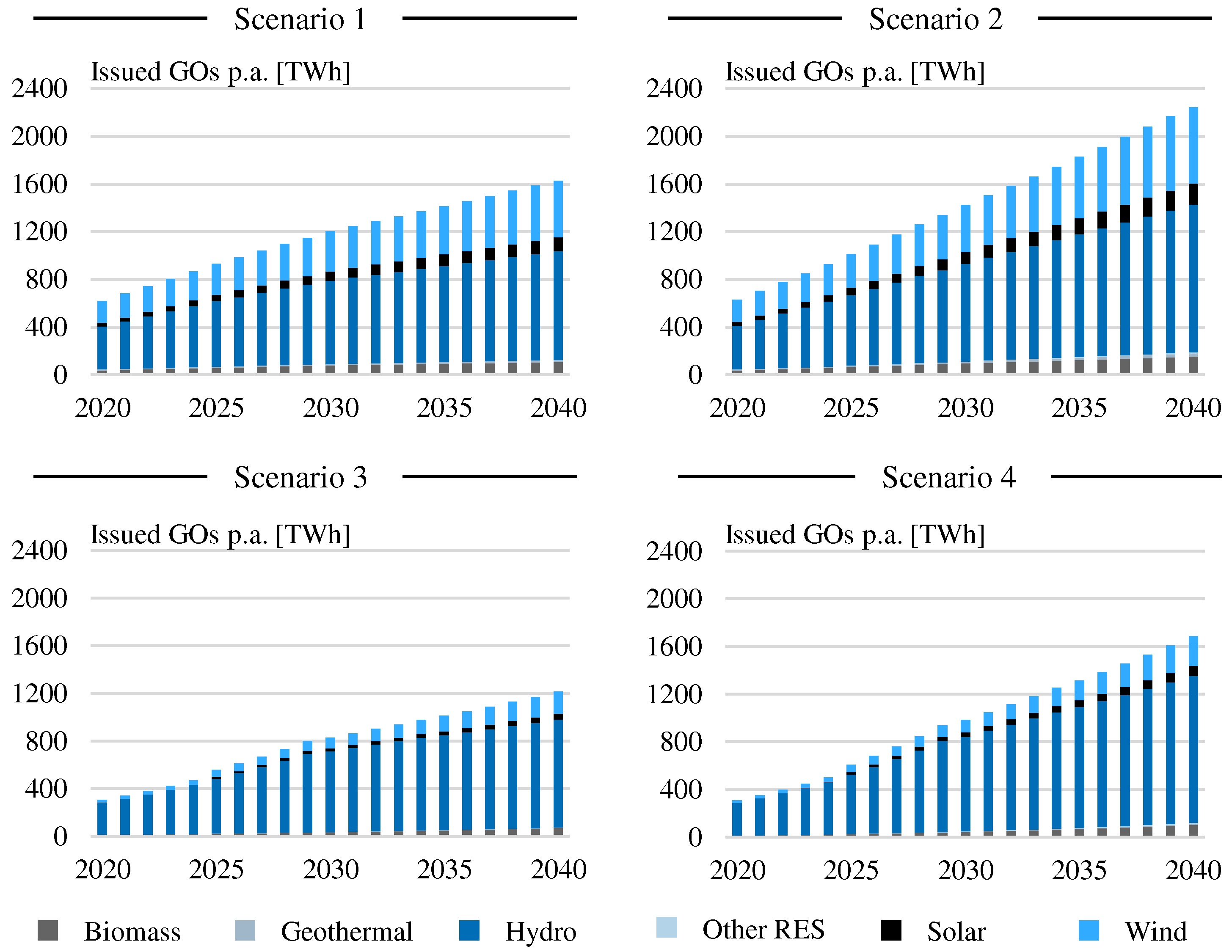

5.3. Scenario Description

6. Results and Discussion

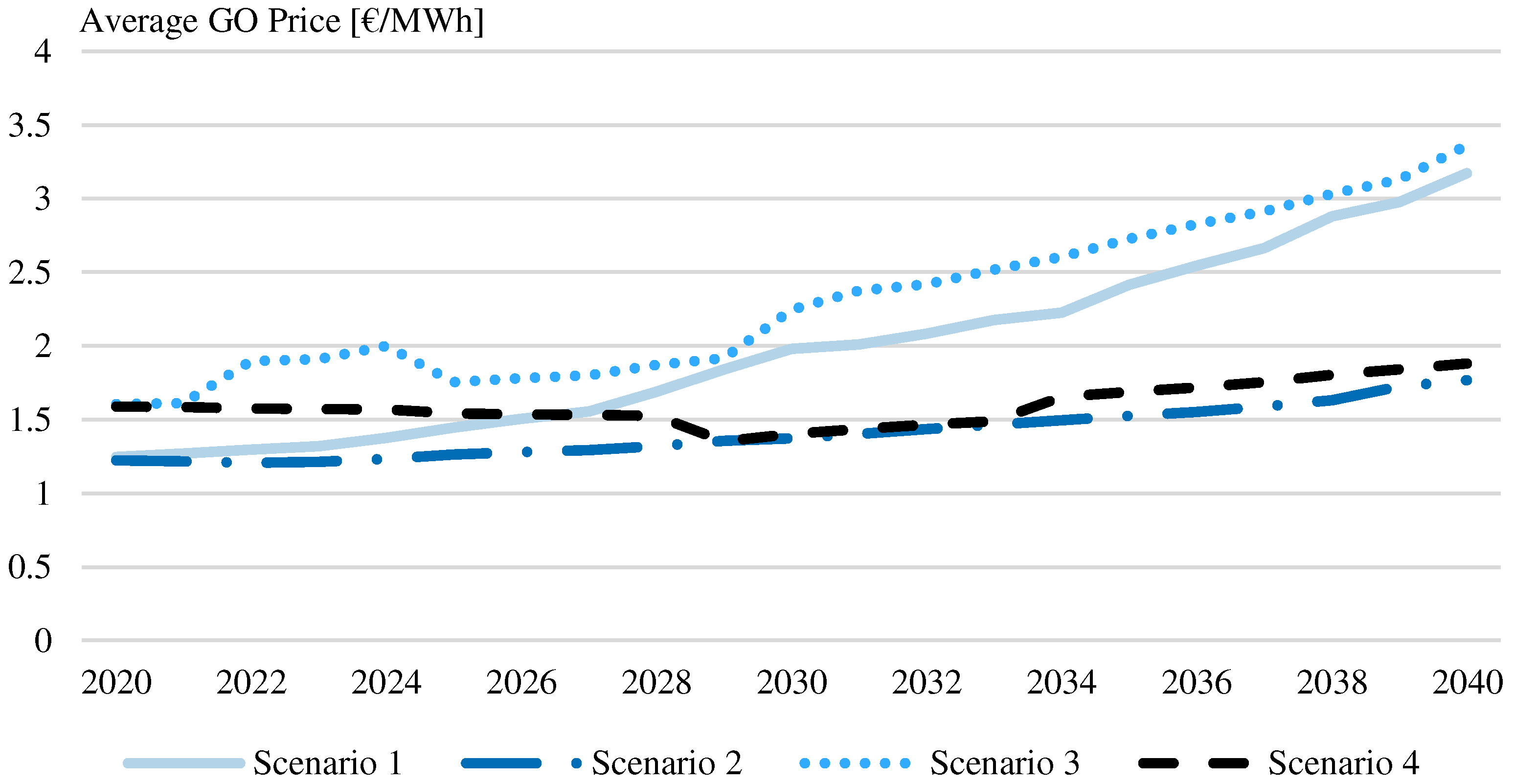

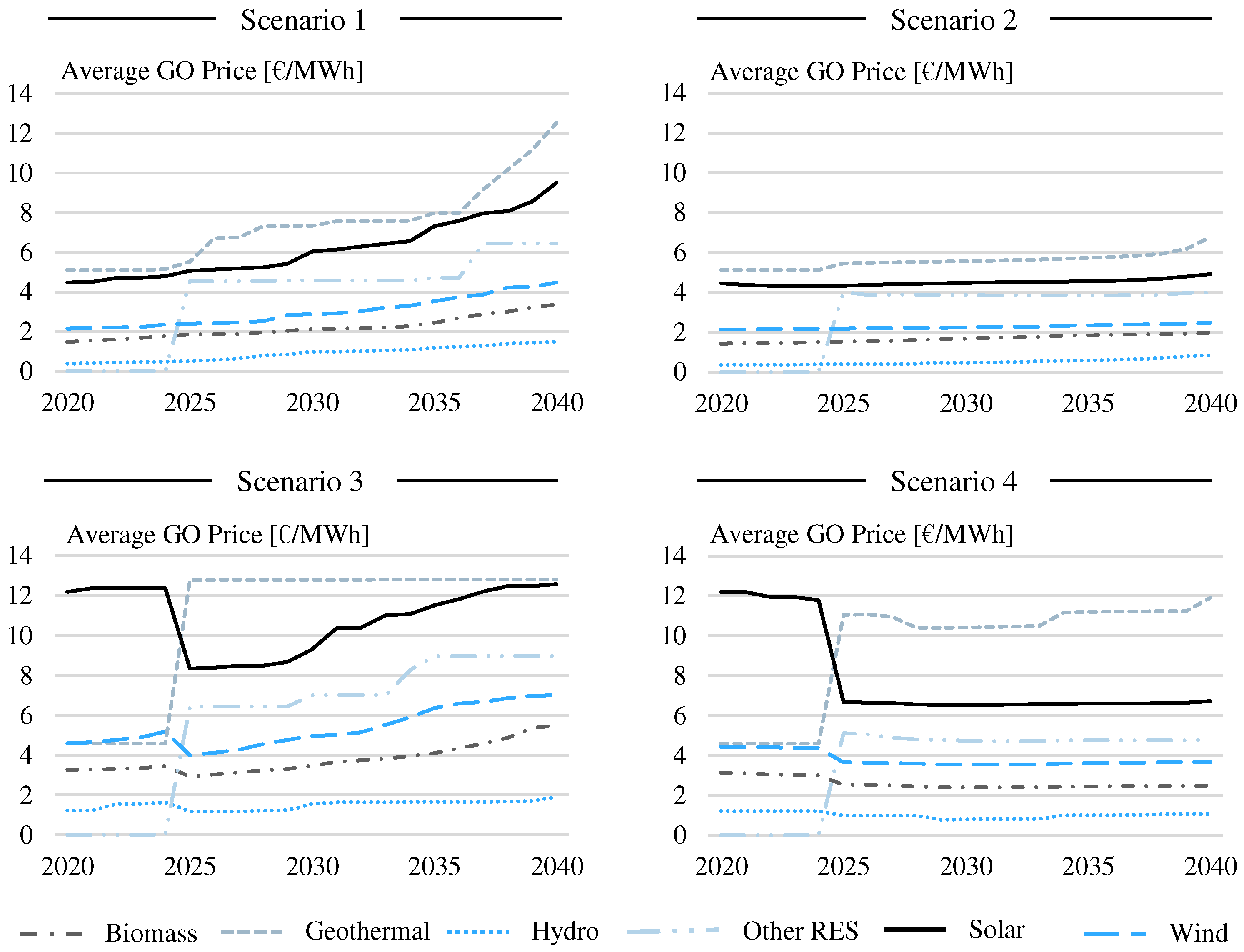

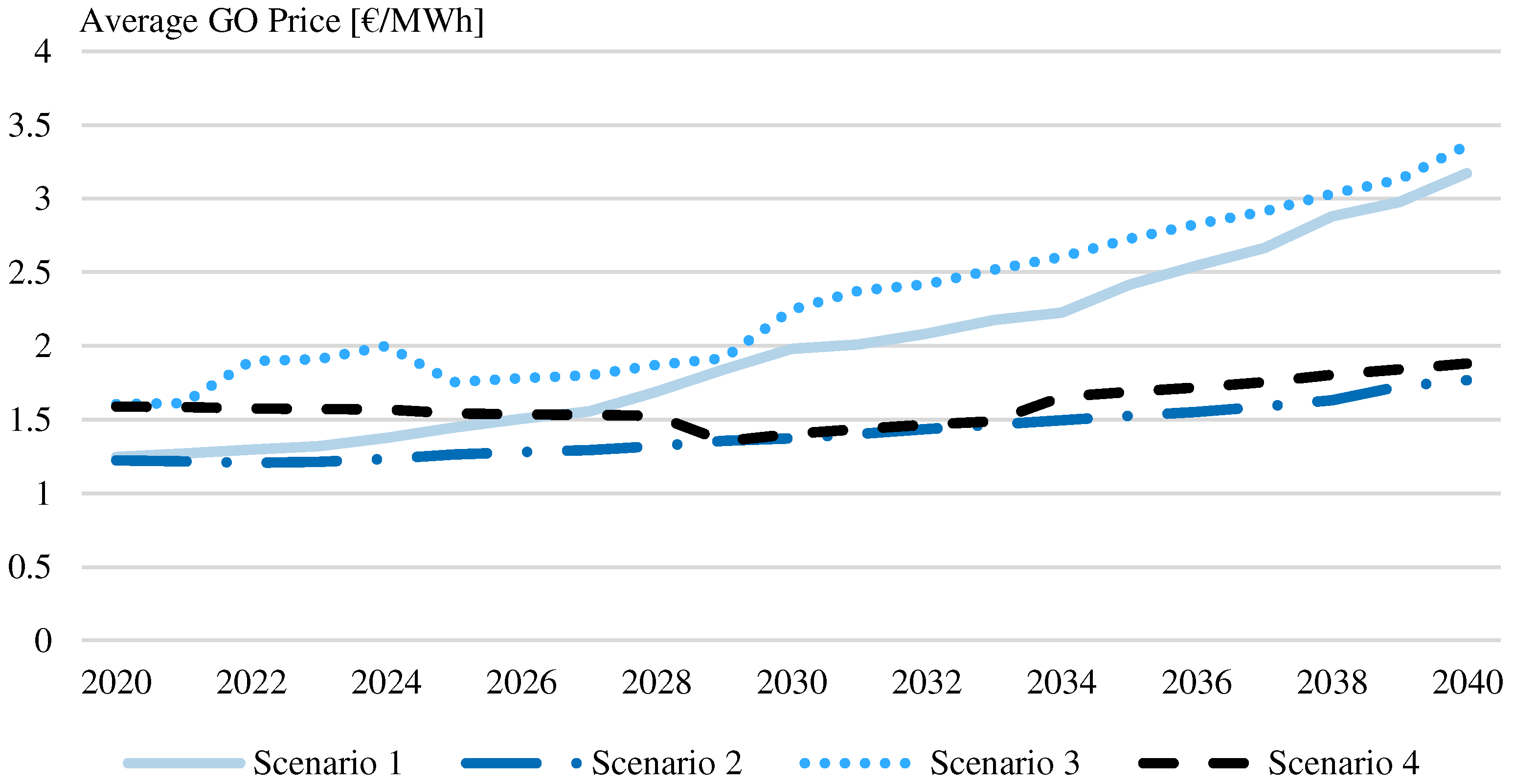

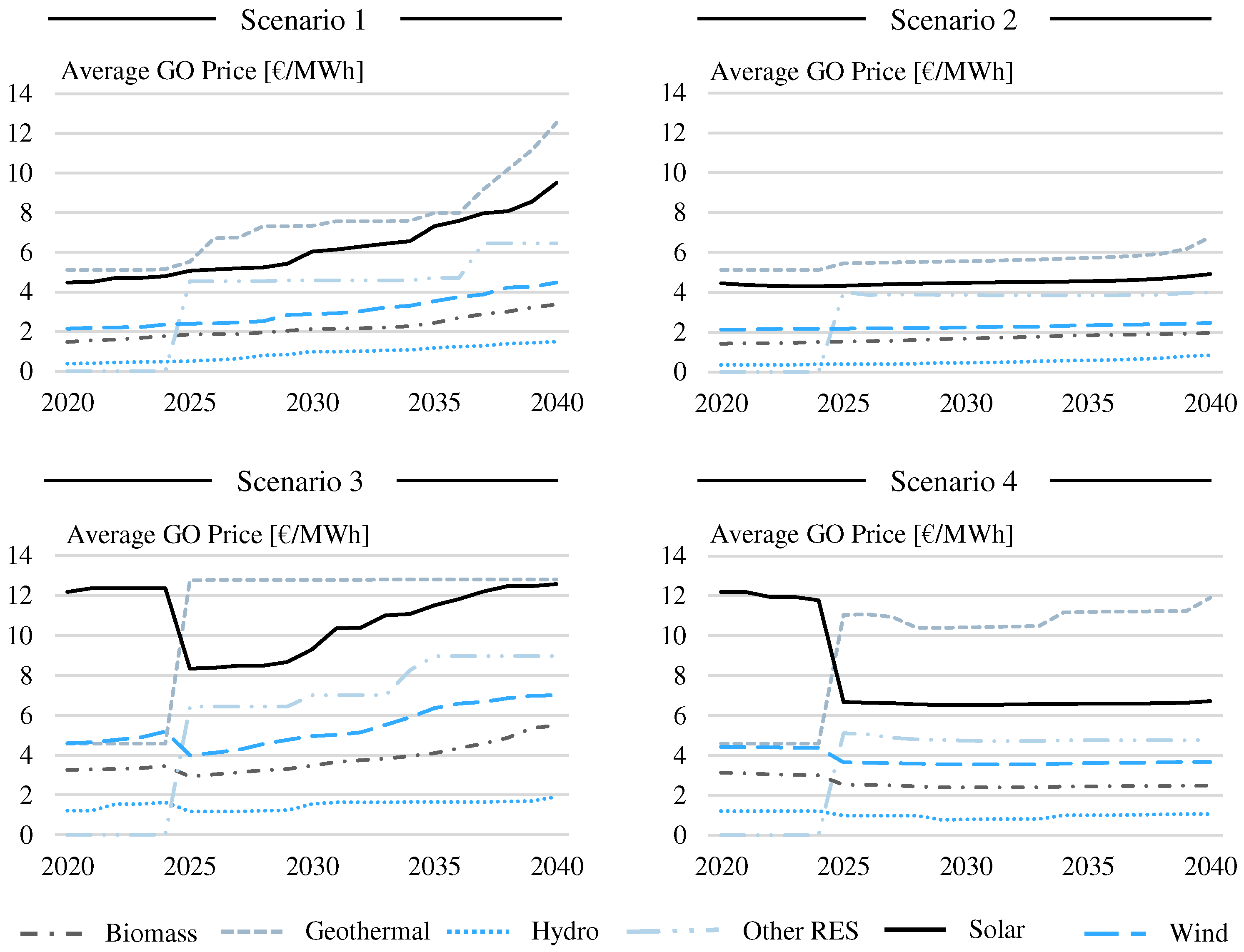

6.1. Scenario Comparison

6.2. Validation of Results

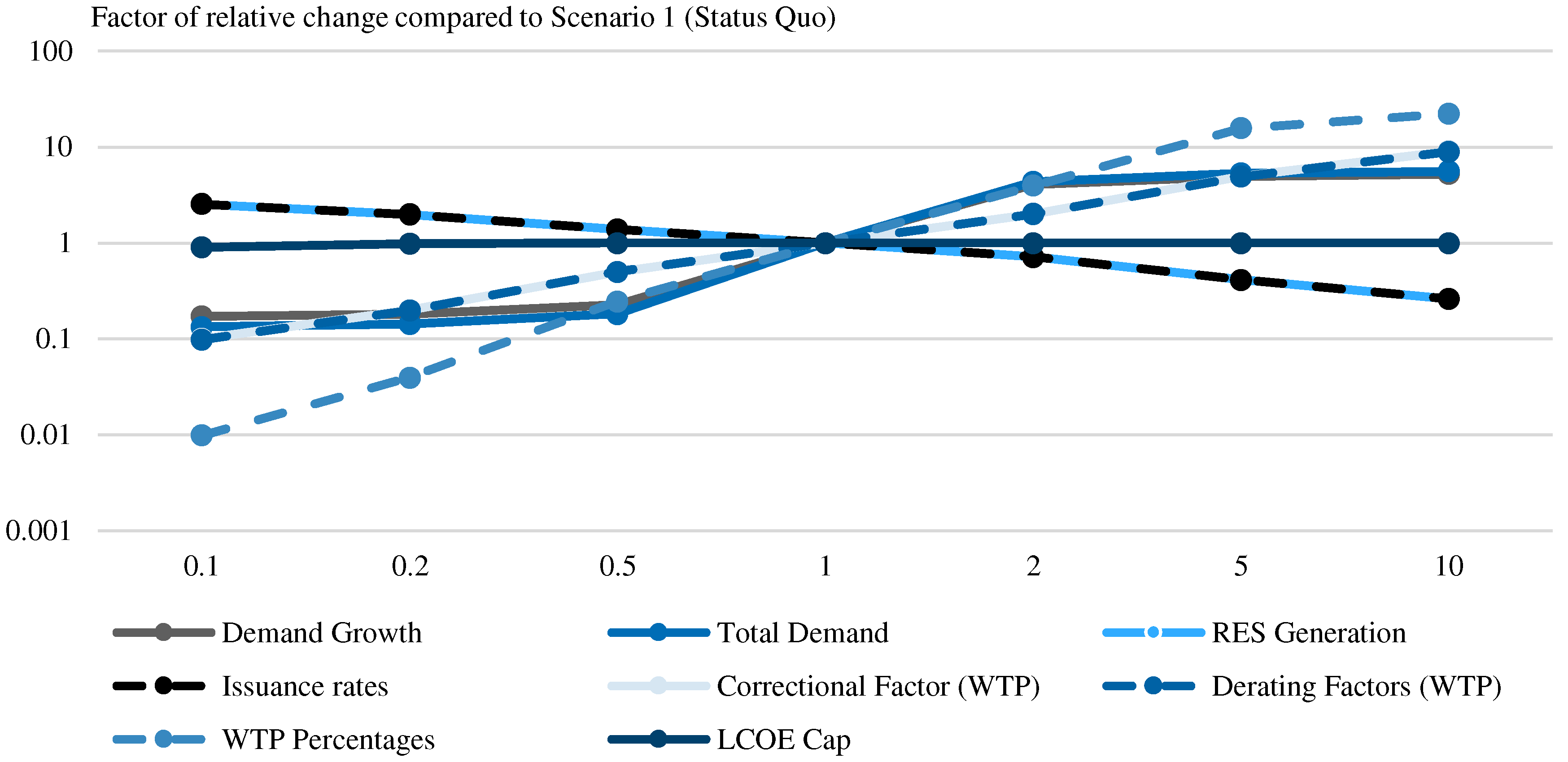

6.3. Sensitivity Analysis

6.4. Limitations of the Model

7. Conclusions and Policy Implications

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| AIB | Association of Issuing Bodies |

| ATP | Ability to pay |

| CAGR | Compound annual growth rate |

| EECS | European Energy Certificate System |

| EEX | European Energy Exchange |

| EPEX | European Power Exchange |

| EU | European Union |

| GHG | Greenhouse gases |

| GO | Guarantee of Origin |

| IEA | International Energy Agency |

| LCOE | Levelized cost of electricity |

| MWh | Megawatt-hour |

| NACE | Statistical Classification of Economic Activities in the European Community (nomenclature statistique des activités économiques dans la Communauté européenne) |

| OECD | Organisation for Economic Co-operation and Development |

| PPA | Power purchase agreement |

| RED | Renewable Energy Directive |

| RES | Renewable energy sources |

| WAVG | Weighted average |

| WTP | Willingness to pay |

Appendix A. Exemplary WTP Calculation

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Consumer | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | |

|---|---|---|---|---|---|---|---|---|---|

| A | Profits in EUR | 767,893.40 | 710,532.00 | 687,090.53 | 677,405.95 | 812,933.47 | 1,039,870.53 | 1,060,647.87 | 1,271,280.00 |

| Electricity cost in EUR | 818,437.58 | 690,850.18 | 744,681.60 | 757,992.45 | 789,018.15 | 874,278.53 | 790,451.80 | 856,901.92 | |

| ATP | 0.94 | 1.03 | 0.92 | 0.89 | 1.03 | 1.19 | 1.34 | 1.48 | |

| B | Profits in EUR | 15,436.30 | 18,209.15 | 12,350.88 | 18,455.85 | 20,502.86 | 23,950.27 | 19,967.06 | 23,164.93 |

| Electricity cost in EUR | 26,412.85 | 29,174.22 | 28,129.60 | 39,799.36 | 40,521.65 | 39,919.53 | 34,994.40 | 24,292.21 | |

| ATP | 0.58 | 0.62 | 0.44 | 0.46 | 0.51 | 0.60 | 0.57 | 0.95 |

| Consumer | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | |

|---|---|---|---|---|---|---|---|---|---|

| A | ATP | 0.94 | 1.03 | 0.92 | 0.89 | 1.03 | 1.19 | 1.34 | 1.48 |

| Environmental concern | 0.40 | 0.40 | 0.40 | 0.40 | 0.40 | 0.40 | 0.40 | 0.40 | |

| WTPmax,rel | 0.25 | 0.25 | 0.25 | 0.25 | 0.25 | 0.25 | 0.25 | 0.25 | |

| Electricity price in EUR/MWh | 60.10 | 62.15 | 63.95 | 63.25 | 64.30 | 66.45 | 60.95 | 58.90 | |

| WTPmax in EUR/MWh | 15.03 | 15.54 | 15.99 | 15.81 | 16.08 | 16.61 | 15.24 | 14.73 | |

| B | ATP | 0.58 | 0.62 | 0.44 | 0.46 | 0.51 | 0.60 | 0.57 | 0.95 |

| Environmental concern | 0.65 | 0.65 | 0.65 | 0.65 | 0.65 | 0.65 | 0.65 | 0.65 | |

| WTPmax,rel | 0.28 | 0.34 | 0.28 | 0.28 | 0.28 | 0.34 | 0.28 | 0.40 | |

| Electricity price in EUR/MWh | 144.95 | 146.30 | 151.45 | 148.20 | 136.40 | 133.50 | 130.25 | 94.45 | |

| WTPmax in EUR/MWh | 39.86 | 49.38 | 41.65 | 40.76 | 37.51 | 45.06 | 35.82 | 37.78 |

| Consumer | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | Average |

|---|---|---|---|---|---|---|---|---|---|

| A | 6.01 | 6.22 | 6.40 | 6.33 | 6.43 | 6.65 | 6.10 | 5.89 | 6.25 |

| B | 19.13 | 23.70 | 19.99 | 19.56 | 18.00 | 21.63 | 17.19 | 18.13 | 19.67 |

Appendix B. Additional Information and Data

| Type of GO | Period | Price/Price Range (in EUR/MWh, unless Otherwise Specified) | Source |

|---|---|---|---|

| Alpine Hydro Power | 2017 | 0.2 | [86] |

| Austrian (unspecif.) | 2018 | 0.9–1.45 | [11] |

| Austrian Hydro (age unspecif.) | 2019 | 1.32 | [92] |

| Dutch Wind | September 2018 | 8 | [23] |

| EU Biomass (unspecif.) | 2018 | 1.62 | [92] |

| EU Hydro (age unspecif.) | 2018 | 1.24–1.25 | [11] |

| EU Hydro (unspecif.) | 2020 | 0.15–0.21 | [93] |

| EU Hydro (unspecif.) | 2018–2020 | 0.49–1.98 | [92] |

| EU (average 2021) | September 2021 | 0.75 | [42] |

| EU (average 2022) | September 2021 | 1.25 | [42] |

| German (unspecif.) | 2018 | 0.8–1.6 | [11] |

| Italian Wind Auction (weighted average) | January 2022/ March 2022/ June 2022/ October 2022/ December 2022 | 1/ 1.32/ 1.88/ 5.01/ 5.93 | [22] |

| Italian Unspecified Technology Auction (weighted average) | January 2022/ March 2022/ June 2022/ October 2022/ December 2022 | 1.03/ 1.65/ 1.93/ 5.28/ 6.42 | [22] |

| Italian Solar Auction (weighted average) | January 2022/ March 2022/ June 2022/ October 2022/ December 2022 | 1.11/ 2.01/ 2.22/ 5.32/ 6.52 | [22] |

| Italian Hydro Auction (weighted average) | January 2022/ March 2022/ June 2022/ October 2022/ December 2022 | 0.89/ 1.46/ 1.99/ 5.60/ 6.28 | [22] |

| Large Nordic Hydro | 2007–2015 | 0.05–0.6 | [41] |

| Nordic (unspecif.), new | 2018 | 2–2.7 | [11] |

| Nordic (unspecif.), new | 2018 | 2.34–3.4 | [11] |

| Nordic (unspecif.), old | 2018 | 0.55 | [11] |

| Nordic (unspecif.), retrofitted | 2018 | 1–1.9 | [11] |

| Nordic Hydro (age unspecif.) | 2015 | 0.05–0.5 | [94] |

| Nordic Hydro (age unspecif.) | 2017 | 0.22–0.38 | [11] |

| Nordic Hydro (age unspecif.) | September 2018–December 2018 | 1.24–2 | [23] |

| Nordic Hydro | 2017 | 0.31 | [86] |

| Northern Continental Europe Wind Power | 2017 | 0.45 | [86] |

| Swiss (unspecif.) | 2018 | 1.5–4 | [11] |

| Swiss Hydro | 2017–2018 | 1–4 CHF/MWh * | [23] |

| Swiss PV (unspecif.) | 2018 | 14.30 | [92] |

| WTPs for Green Electricity | |||||

|---|---|---|---|---|---|

| 0% | >0% | >25% | >50% | >75% | |

| France | 28.5 | 56 | 10.5 | 4.5 | 0.5 |

| Netherlands | 32 | 56 | 8.5 | 3 | 0.5 |

| Spain | 28 | 56 | 11 | 4 | 1 |

| Sweden | 23 | 62 | 10 | 4 | 1 |

| Switzerland | 8.5 | 72 | 15 | 4 | 0.5 |

| EU Average | 24 | 60.4 | 11 | 3.9 | 0.7 |

| Reduced WTP for GOs (% of total electr. price) | 0 | 3.75 | 11.25 | 18.75 | 24 |

| Sector Description | NACE Code | Environmental Concern | Source |

|---|---|---|---|

| Mining of coal and lignite | B05 | 0.1 | Own estimation |

| Extraction of crude petroleum and natural gas | B06 | 0.1 | Own estimation |

| Mining of metal ores | B07 | 0.2 | Own estimation |

| Other mining and quarrying | B08 | 0.15 | Own estimation |

| Mining support service activities | B09 | 0.2 | Own estimation |

| Manufacture of food products | C10 | 0.65 | [81] |

| Manufacture of beverages | C11 | 0.75 | [81] |

| Manufacture of tobacco products | C12 | 0.4 | Own estimation |

| Manufacture of textiles | C13 | 0.7 | [81] |

| Manufacture of apparel | C14 | 0.55 | Own estimation |

| Manufacture of leather and related products | C15 | 0.6 | Own estimation |

| Manufacture of wood and of products of wood and cork, except furniture; manufacture of articles of straw and plaiting materials | C16 | 0.65 | Own estimation |

| Manufacture of paper and paper products | C17 | 0.4 | [81] |

| Printing and reproduction of recorded media | C18 | 0.4 | Own estimation |

| Manufacture of coke and refined petroleum products | C19 | 0.1 | Own estimation |

| Manufacture of chemicals and chemical products | C20 | 0.5 | [81] |

| Manufacture of basic pharmaceutical products and pharmaceutical preparations | C21 | 0.4 | [81] |

| Manufacture of rubber and plastic products | C22 | 0.3 | Own estimation |

| Manufacture of other non-metallic mineral products | C23 | 0.35 | Own estimation |

| Manufacture of basic metals | C24 | 0.4 | Own estimation |

| Manufacture of fabricated metal products, except machinery and equipment | C25 | 0.5 | Own estimation |

| Manufacture of computer, electronic, and optical products | C26 | 0.3 | [81] |

| Manufacture of electrical equipment | C27 | 0.4 | Own estimation |

| Manufacture of machinery and equipment n.e.c. | C28 | 0.4 | [81] |

| Manufacture of motor vehicles, trailers and semi-trailers | C29 | 0.45 | [81] |

| Manufacture of other transport equipment | C30 | 0.35 | Own estimation |

| Manufacture of furniture | C31 | 0.7 | Own estimation |

| Other manufacturing | C32 | 0.5 | Own estimation |

| Repair and installation of machinery and equipment | C33 | 0.4 | Own estimation |

| Water collection, treatment, and supply | E36 | 0.7 | Own estimation |

| Sewerage | E37 | 0.5 | [81] |

| Waste collection, treatment, and disposal activities; materials recovery | E38 | 0.7 | Own estimation |

| Remediation activities and other waste management services | E39 | 0.6 | [81] |

| Wholesale and retail trade and repair of motor vehicles and motorcycles | G45 | 0.4 | Own estimation |

| Wholesale trade, except of motor vehicles and motorcycles | G46 | 0.6 | [81] |

| Retail trade, except of motor vehicles and motorcycles | G47 | 0.7 | [81] |

| Accommodation | I55 | 0.5 | [81] |

| Food and beverage service activities | I56 | 0.5 | Own estimation |

| Publishing activities | J58 | 0.5 | Own estimation |

| Motion picture, video, and television program production, sound recording, and music publishing activities | J59 | 0.6 | Own estimation |

| Programming and broadcasting activities | J60 | 0.4 | Own estimation |

| Telecommunications | J61 | 0.8 | [81] |

| Computer programming, consultancy, and related activities | J62 | 0.8 | [81] |

| Information service activities | J63 | 0.75 | [81] |

| Legal and accounting activities | M69 | 0.3 | [81] |

| Activities of head offices; management consultancy activities | M70 | 0.65 | [81] |

| Architectural and engineering activities; technical testing and analysis | M71 | 0.45 | [81] |

| Scientific research and development | M72 | 0.65 | Own estimation |

| Advertising and market research | M73 | 0.8 | [81] |

| Other professional, scientific, and technical activities | M74 | 0.6 | Own estimation |

| Veterinary activities | M75 | 0.4 | Own estimation |

| Rental and leasing activities | N77 | 0.6 | Own estimation |

| Employment activities | N78 | 0.4 | Own estimation |

| Travel agency, tour operator and other reservation service, and related activities | N79 | 0.5 | Own estimation |

| Security and investigation activities | N80 | 0.2 | Own estimation |

| Services to buildings and landscape activities | N81 | 0.6 | Own estimation |

| Office administrative, office support, and other business support activities | N82 | 0.6 | Own estimation |

| Repair of computers and personal and household goods | S95 | 0.4 | Own estimation |

| Country (or Country Area) | Competent Body | Subsidy Category | Fees | National Certificate System | International Trade | Own Domestic Platform |

|---|---|---|---|---|---|---|

| Austria | E-Control | Cat. 1 | No | No | Yes | Yes |

| Belgium (Federal) | CREG | Cat. 4 | No | No | Yes | Yes |

| Belgium Brussels | Brugel | Cat. 4 | No | No | Yes | Yes |

| Belgium Flanders | VREG | Cat. 4 | Yes | Yes | Yes | Yes |

| Belgium Wallonia | SPW Energie/CWaPE | Cat. 4 | No | Yes | Yes | Yes |

| Switzerland | Pronovo | Cat. 1 | Yes | No | Yes | Yes |

| Cyprus | TSOC | Cat. 3 | Yes | Yes | Yes | Yes |

| Czech Republic | OTE | Cat. 4 | Yes | No | Yes | Yes |

| Germany | UBA | Cat. 5 | Yes | Yes | Yes | Yes |

| Denmark | Energinet | Cat. 1 | Yes | No | Yes | No (CMO.grexel) |

| Estonia | Elering | Cat. 1 | Yes | No | Yes | Yes |

| Spain | CNMC | Cat. 4 | No | Yes | Separation of GOs intended for import and export | Yes |

| Finland | Finextra | Cat. 1 | Yes | Yes | Yes | Yes |

| France | EEX | Cat. 2 | Yes | No | Yes | Yes |

| Greece | DAPEEP/HEDNO/CRES | Cat. 4 | No | Yes | Yes | Yes |

| Croatia | HROTE | Cat. 4 | Yes | No | Yes | No (CMO.grexel) |

| Ireland | SEMO | Cat. 5 | No | No | Yes | No (CMO.grexel) |

| Iceland | Landsnet | Cat. 6 | Yes | No | Yes | No (CMO.grexel) |

| Italy | GSE | Cat. 1 | Yes | No | Yes | Yes |

| Lithuania | Litgrid AB | Cat. 3 | Yes | Yes | Only import | No (CMO.grexel) |

| Luxembourg | ILR | Cat. 2 | Yes | No | Yes | No (CMO.grexel) |

| Netherlands | CertiQ | Cat. 4 | Yes | No | Yes | Yes |

| Norway | Statnett | Cat. 4 | Yes | No | Yes | Yes |

| Portugal | Rede Eléctrica Nacional, S.A. (REN) | Cat. 1 | Yes | Yes | Yes | Yes |

| Serbia | EMS | Cat. 5 | Yes | No | Yes | Yes |

| Sweden | Energimyndigheten | Cat. 4 | Yes | Yes | Yes | Yes |

| Slovenia | Energy Agency/Borzen | Cat. 2 | Yes | Yes | Yes | Yes |

| Slovakia | OKTE | Cat. 2 | Yes | No | Yes | Yes |

| Country (Or Country area) | Trade balance (2015–2019) | Trade hub (2015–2019) | Consumption (2015–2019) | Proportion of issuance (2019) | Proportion of cancel. (2019) | Shifted prop. of cancel. (2019) |

| Austria | Negative | Yes | Consumer | 0.021424047 | 0.037883179 | 0.032454632 |

| Belgium (Federal) | Negative | Yes | Consumer | 0.016463224 | 0.039611106 | 0.035522748 |

| Belgium Brussels | Lack of data | Lack of data | Lack of data | 0 | 0 | 0 |

| Belgium Flanders | Lack of data | Lack of data | Lack of data | 0 | 0 | 0 |

| Belgium Wallonia | Lack of data | Lack of data | Lack of data | 0 | 0 | 0 |

| Switzerland | Negative | No | Consumer | 0.095128656 | 0.088430042 | 0.083808439 |

| Cyprus | Lack of data | Lack of data | Producer | 0.000337672 | 0 | 0 |

| Czech Republic | Positive | No | Producer | 0.008335271 | 0.000983337 | 0.001864038 |

| Germany | Negative | No | Consumer | 0.022031789 | 0.173304752 | 0.158670194 |

| Denmark | Positive | No | Producer | 0.028931447 | 0.014841155 | 0.013331771 |

| Estonia | Positive | Yes | Producer | 0.004086356 | 0.000471532 | 0.000578586 |

| Spain | Positive | No | Producer | 0.143756032 | 0.125417968 | 0.120358496 |

| Finland | Positive | No | Producer | 0.040907033 | 0.04149955 | 0.037288875 |

| France | Positive | No | Producer | 0.079916686 | 0.067765929 | 0.075425313 |

| Greece | Lack of data | Lack of data | Lack of data | 0 | 0 | 0 |

| Croatia | Positive | No | Producer | 0.007435576 | 0.002644953 | 0.003194225 |

| Ireland | Negative | No | Consumer | 0.003198566 | 0.011490545 | 0.011640314 |

| Iceland | Positive | No | Producer | 0.023687093 | 0.006319384 | 0.004605022 |

| Italy | Positive | No | Producer | 0.129264574 | 0.077423193 | 0.080583479 |

| Lithuania | Negative | No | Consumer | 0.000415937 | 0.002066573 | 0.002100529 |

| Luxembourg | Negative | Yes | Consumer | 0.000665903 | 0.005062893 | 0.006328675 |

| Netherlands | Negative | No | Consumer | 0.081629158 | 0.087323332 | 0.092680187 |

| Norway | Positive | Yes | Producer | 0.188048895 | 0.109938713 | 0.105441595 |

| Portugal | Negative | Yes | Consumer | 0 | 0 | 0 |

| Serbia | Lack of data | Lack of data | Producer | 9.94 × 10−6 | 1.10 × 10−5 | 6.34 × 10−5 |

| Sweden | Negative | No | Producer | 0.099308569 | 0.106162988 | 0.09557441 |

| Slovenia | Positive | No | Producer | 0.005017581 | 0.001347882 | 0.001196152 |

| Slovakia | Lack of data | Lack of data | Lack of data | 0 | 0 | 0 |

| AT | BE | DK | FI | FR | DE | UK | IT | IE | NL | NO | PO | ES | SW | CH | HR | CY | CZ | ET | GR | IC | LI | LU | SE | SK | SL | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| AT | 1 | 0.7 | 0.6 | 0.6 | 0.7 | 0.9 | 0.4 | 0.9 | 0.2 | 0.6 | 0.2 | 0.4 | 0.4 | 0.6 | 0.9 | 0.7 | 0.4 | 0.9 | 0.7 | 0.6 | 0.3 | 0.4 | 0.5 | 0.6 | 0.9 | 0.9 |

| BE | 0.7 | 1 | 0.8 | 0.7 | 0.9 | 0.9 | 0.7 | 0.5 | 0.5 | 0.9 | 0.3 | 0.5 | 0.5 | 0.6 | 0.7 | 0.5 | 0.3 | 0.6 | 0.5 | 0.3 | 0.3 | 0.5 | 0.9 | 0.5 | 0.6 | 0.6 |

| DK | 0.6 | 0.8 | 1 | 0.8 | 0.6 | 0.9 | 0.6 | 0.5 | 0.5 | 0.7 | 0.3 | 0.4 | 0.4 | 0.8 | 0.6 | 0.4 | 0.3 | 0.6 | 0.7 | 0.3 | 0.4 | 0.7 | 0.7 | 0.4 | 0.5 | 0.5 |

| FI | 0.6 | 0.7 | 0.8 | 1 | 0.5 | 0.7 | 0.5 | 0.5 | 0.4 | 0.7 | 0.4 | 0.3 | 0.4 | 0.9 | 0.6 | 0.4 | 0.2 | 0.5 | 0.9 | 0.3 | 0.5 | 0.9 | 0.6 | 0.3 | 0.5 | 0.5 |

| FR | 0.7 | 0.9 | 0.6 | 0.5 | 1 | 0.9 | 0.8 | 0.9 | 0.5 | 0.6 | 0.2 | 0.6 | 0.7 | 0.4 | 0.8 | 0.6 | 0.4 | 0.5 | 0.4 | 0.6 | 0.4 | 0.5 | 0.9 | 0.4 | 0.5 | 0.6 |

| DE | 0.9 | 0.9 | 0.9 | 0.7 | 0.9 | 1 | 0.7 | 0.7 | 0.5 | 0.9 | 0.2 | 0.4 | 0.4 | 0.5 | 0.9 | 0.6 | 0.4 | 0.9 | 0.6 | 0.5 | 0.4 | 0.6 | 0.9 | 0.5 | 0.6 | 0.6 |

| UK | 0.4 | 0.7 | 0.6 | 0.5 | 0.8 | 0.7 | 1 | 0.6 | 0.9 | 0.8 | 0.3 | 0.5 | 0.5 | 0.4 | 0.8 | 0.4 | 0.3 | 0.5 | 0.3 | 0.2 | 0.6 | 0.3 | 0.6 | 0.4 | 0.5 | 0.5 |

| IT | 0.9 | 0.5 | 0.5 | 0.5 | 0.9 | 0.7 | 0.6 | 1 | 0.5 | 0.6 | 0.2 | 0.6 | 0.7 | 0.4 | 0.9 | 0.9 | 0.4 | 0.5 | 0.3 | 0.7 | 0.4 | 0.3 | 0.6 | 0.7 | 0.6 | 0.9 |

| IE | 0.2 | 0.5 | 0.5 | 0.4 | 0.5 | 0.5 | 0.9 | 0.5 | 1 | 0.8 | 0.3 | 0.5 | 0.5 | 0.4 | 0.6 | 0.4 | 0.2 | 0.4 | 0.3 | 0.3 | 0.7 | 0.3 | 0.5 | 0.3 | 0.4 | 0.4 |

| NL | 0.6 | 0.9 | 0.7 | 0.7 | 0.6 | 0.9 | 0.8 | 0.6 | 0.8 | 1 | 0.2 | 0.4 | 0.4 | 0.4 | 0.6 | 0.5 | 0.3 | 0.5 | 0.5 | 0.3 | 0.5 | 0.4 | 0.8 | 0.4 | 0.5 | 0.5 |

| NO | 0.2 | 0.3 | 0.3 | 0.4 | 0.2 | 0.2 | 0.3 | 0.2 | 0.3 | 0.2 | 1 | 0.2 | 0.3 | 0.5 | 0.3 | 0.2 | 0.1 | 0.2 | 0.3 | 0.2 | 0.4 | 0.3 | 0.2 | 0.2 | 0.2 | 0.2 |

| PO | 0.4 | 0.5 | 0.4 | 0.3 | 0.6 | 0.4 | 0.5 | 0.6 | 0.5 | 0.4 | 0.2 | 1 | 0.9 | 0.5 | 0.6 | 0.5 | 0.3 | 0.5 | 0.3 | 0.5 | 0.2 | 0.3 | 0.4 | 0.4 | 0.4 | 0.4 |

| ES | 0.4 | 0.5 | 0.4 | 0.4 | 0.7 | 0.4 | 0.5 | 0.7 | 0.5 | 0.4 | 0.3 | 0.9 | 1 | 0.5 | 0.7 | 0.6 | 0.4 | 0.5 | 0.3 | 0.6 | 0.3 | 0.3 | 0.5 | 0.4 | 0.5 | 0.5 |

| SW | 0.6 | 0.6 | 0.8 | 0.9 | 0.4 | 0.5 | 0.4 | 0.4 | 0.4 | 0.4 | 0.5 | 0.5 | 0.5 | 1 | 0.6 | 0.6 | 0.4 | 0.3 | 0.5 | 0.7 | 0.4 | 0.5 | 0.7 | 0.5 | 0.3 | 0.4 |

| CH | 0.9 | 0.7 | 0.6 | 0.6 | 0.8 | 0.9 | 0.8 | 0.9 | 0.6 | 0.6 | 0.3 | 0.6 | 0.7 | 0.6 | 1 | 0.6 | 0.3 | 0.7 | 0.4 | 0.6 | 0.3 | 0.4 | 0.8 | 0.5 | 0.5 | 0.5 |

| HR | 0.7 | 0.5 | 0.4 | 0.4 | 0.6 | 0.6 | 0.4 | 0.9 | 0.4 | 0.5 | 0.2 | 0.5 | 0.6 | 0.4 | 0.6 | 1 | 0.4 | 0.6 | 0.4 | 0.7 | 0.3 | 0.4 | 0.5 | 0.9 | 0.8 | 0.9 |

| CY | 0.4 | 0.3 | 0.3 | 0.2 | 0.4 | 0.4 | 0.3 | 0.4 | 0.2 | 0.3 | 0.1 | 0.3 | 0.4 | 0.3 | 0.3 | 0.4 | 1 | 0.3 | 0.3 | 0.8 | 0.1 | 0.3 | 0.3 | 0.4 | 0.4 | 0.4 |

| CZ | 0.9 | 0.6 | 0.6 | 0.5 | 0.5 | 0.9 | 0.5 | 0.5 | 0.4 | 0.5 | 0.2 | 0.5 | 0.5 | 0.5 | 0.7 | 0.6 | 0.3 | 1 | 0.6 | 0.4 | 0.4 | 0.6 | 0.7 | 0.5 | 0.9 | 0.6 |

| ET | 0.7 | 0.5 | 0.7 | 0.9 | 0.4 | 0.6 | 0.3 | 0.3 | 0.3 | 0.5 | 0.3 | 0.3 | 0.3 | 0.7 | 0.4 | 0.4 | 0.3 | 0.6 | 1 | 0.3 | 0.3 | 0.9 | 0.5 | 0.4 | 0.5 | 0.5 |

| GR | 0.6 | 0.3 | 0.3 | 0.3 | 0.6 | 0.5 | 0.2 | 0.7 | 0.3 | 0.3 | 0.2 | 0.5 | 0.6 | 0.4 | 0.6 | 0.7 | 0.8 | 0.4 | 0.3 | 1 | 0.1 | 0.4 | 0.4 | 0.7 | 0.6 | 0.6 |

| IC | 0.3 | 0.3 | 0.4 | 0.5 | 0.4 | 0.4 | 0.6 | 0.4 | 0.7 | 0.5 | 0.4 | 0.3 | 0.3 | 0.5 | 0.3 | 0.3 | 0.1 | 0.4 | 0.3 | 0.1 | 1 | 0.3 | 0.3 | 0.2 | 0.2 | 0.2 |

| LI | 0.4 | 0.5 | 0.7 | 0.9 | 0.5 | 0.6 | 0.3 | 0.3 | 0.3 | 0.4 | 0.3 | 0.3 | 0.3 | 0.7 | 0.4 | 0.4 | 0.3 | 0.6 | 0.9 | 0.4 | 0.3 | 1 | 0.4 | 0.4 | 0.5 | 0.5 |

| LU | 0.5 | 0.9 | 0.7 | 0.6 | 0.9 | 0.9 | 0.6 | 0.6 | 0.5 | 0.8 | 0.2 | 0.4 | 0.5 | 0.5 | 0.8 | 0.5 | 0.3 | 0.7 | 0.5 | 0.4 | 0.3 | 0.4 | 1 | 0.4 | 0.5 | 0.6 |

| SE | 0.6 | 0.5 | 0.4 | 0.3 | 0.4 | 0.5 | 0.4 | 0.7 | 0.3 | 0.4 | 0.2 | 0.4 | 0.4 | 0.3 | 0.5 | 0.9 | 0.4 | 0.5 | 0.4 | 0.7 | 0.2 | 0.4 | 0.4 | 1 | 0.7 | 0.7 |

| SK | 0.9 | 0.6 | 0.5 | 0.5 | 0.5 | 0.6 | 0.5 | 0.6 | 0.4 | 0.5 | 0.2 | 0.4 | 0.5 | 0.4 | 0.5 | 0.8 | 0.4 | 0.9 | 0.5 | 0.6 | 0.2 | 0.5 | 0.5 | 0.7 | 1 | 0.9 |

| SL | 0.9 | 0.6 | 0.5 | 0.5 | 0.6 | 0.6 | 0.5 | 0.9 | 0.4 | 0.5 | 0.2 | 0.4 | 0.5 | 0.4 | 0.5 | 0.9 | 0.4 | 0.6 | 0.5 | 0.6 | 0.2 | 0.5 | 0.6 | 0.7 | 0.9 | 1 |

| Technology t | Derating Factor Dt |

|---|---|

| Biomass | 0.7 |

| Geothermal | 1 |

| Hydro | 0.5 |

| Solar | 0.9 |

| Wind | 0.8 |

| Other | 0.8 |

References

- Hainsch, K.; Löffler, K.; Burandt, T.; Auer, H.; del Granado, P.C.; Pisciella, P.; Zwickl-Bernhard, S. Energy transition scenarios: What policies, societal attitudes, and technology developments will realize the EU Green Deal? Energy 2022, 239, 122067. [Google Scholar] [CrossRef]

- Kendziorski, M.; Göke, L.; Hirschhausen, C.; von Kemfert, C.; Zozmann, E. Centralized and decentral approaches to succeed the 100% Energiewende in Germany in the European context—A model-based analysis of generation, network, and storage investments. Energy Policy 2022, 167, 113039. [Google Scholar] [CrossRef]

- Mulder, M.; Zomer, S.P. Contribution of green labels in electricity retail markets to fostering renewable energy. Energy Policy 2016, 99, 100–109. [Google Scholar] [CrossRef]

- Directive 96/92/EC of the European Parliament and of the Council of 19 December 1996 concerning Common Rules for the Internal Market in Electricity. 1996. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:31996L0092 (accessed on 18 December 2023).

- Langeraar, J.; Devos, R. Guarantee of Origin: The proof of the pudding is in the eating. Refocus 2003, 4, 62–63. [Google Scholar] [CrossRef]

- IRENA. Corporate Sourcing of Renewables: Market and Industry Trends—REmade Index 2018; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2018. [Google Scholar]

- RE100. Annual Report.: Going 100% Renewable: How Committed Companies Are Demanding a Faster Market Response. 2019. Available online: https://www.there100.org/sites/re100/files/2020-09/RE100ProgressandInsightsAnnualReport2019.pdf (accessed on 18 December 2023).

- Markard, J.; Holt, E. Disclosure of electricity products—Lessons from consumer research as guidance for energy policy. Energy Policy 2003, 31, 1459–1474. [Google Scholar] [CrossRef]

- Directive 2001/77/EC of the European Parliament and of the Council of 27 September 2001 on the Promotion of Electricity Produced from Renewable Energy Source in the Internal Electricity Market: Directive 2001/77/EC 2001 Oct 27. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32001L0077 (accessed on 18 December 2023).

- Gkarakis, K.; Dagoumas, A. Assessment of the implementation of Guarantees of Origin (GOs) in Europe. In Power Systems, Energy Markets and Renewable Energy Sources in South-Eastern Europe; Németh, B., Mavromatakis, F., Siderakis, K., Eds.; Trivent Publishing: Budapest, Hungary, 2016. [Google Scholar]

- Hauser, E.; Heib, S.; Hildebrand, J.; Rau, I.; Weber, A.; Welling, J.; Güldenberg, J.; Maaß, C.; Mundt, J.; Werner, R.; et al. Marktanalyse Ökostrom II: Marktanalyse Ökostrom und HKN, Weiterentwicklung des Herkunftsnachweissystems und der Stromkennzeichnung; Abschlussbericht: Dessau-Roßlau, Germany, 2019; Available online: https://www.umweltbundesamt.de/publikationen/marktanalyse-oekostrom-ii (accessed on 18 December 2023).

- AIB. EECS Rules: Release 7: Association of Issuing Bodies. 2020. Available online: https://www.aib-net.org/eecs/eecsr-rules (accessed on 8 October 2020).

- Raadal, H.L.; Dotzauer, E.; Hanssen, O.J.; Kildal, H.P. The interaction between Electricity Disclosure and Tradable Green Certificates. Energy Policy 2012, 42, 419–428. [Google Scholar] [CrossRef]

- AIB. AIB Members: Association of Issuing Bodies. 2023. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/aib-members (accessed on 17 January 2023).

- Finjord, F.; Hagspiel, V.; Lavrutich, M.; Tangen, M. The impact of Norwegian-Swedish green certificate scheme on investment behavior: A wind energy case study. Energy Policy 2018, 123, 373–389. [Google Scholar] [CrossRef]

- Ganhammar, K. The effect of regulatory uncertainty in green certificate markets: Evidence from the Swedish-Norwegian market. Energy Policy 2021, 158, 112583. [Google Scholar] [CrossRef]

- EPEX SPOT. Successful start of Pan-European Spot Market for Guarantees of Origin: First Auction Completed by EPEX SPOT with Clearing and Delivery through ECC and EEX. 2022. Available online: https://www.epexspot.com/en/news/successful-start-pan-european-spot-market-guarantees-origin (accessed on 17 January 2023).

- Frei, F.; Loder, A.; Bening, C.R. Liquidity in green power markets—An international review. Renew. Sustain. Energy Rev. 2018, 93, 674–690. [Google Scholar] [CrossRef]

- Hulshof, D.; Jepma, C.; Mulder, M. Performance of markets for European renewable energy certificates. Energy Policy 2019, 128, 697–710. [Google Scholar] [CrossRef]

- Robert, L. Guarantees of Origin Market Developments: October 2022—GO Market Review. 2022. Available online: https://portal.greenfact.com/News/2154/October-2022---GO-Market-Overview (accessed on 18 December 2023).

- Argus Media. Voluntary Renewable Power and Gas Markets: European Guarantee of Origin Trade Increases. 2022. Argus Insight. Available online: https://www.argusmedia.com/-/media/Files/white-papers/2022/european-guarantee-of-origin-trade-increase.ashx (accessed on 17 January 2023).

- GME. GSE GO Auctions. 2022. Available online: https://mercatoelettrico.org/En/Esiti/GO/EsitiGOAste.aspx (accessed on 17 January 2023).

- Münzer, A. 2018—A Historic Year for Green Energy in Europe. 2019. Available online: https://www.linkedin.com/pulse/2018-historic-year-green-energy-europe-alexandra-m%C3%BCnzer/ (accessed on 18 December 2023).

- Brander, M.; Gillenwater, M.; Ascui, F. Creative accounting: A critical perspective on the market-based method for reporting purchased electricity (scope 2) emissions. Energy Policy 2018, 112, 29–33. [Google Scholar] [CrossRef]

- Nordenstam, L.; Djuric Ilic, D.; Ödlund, L. Corporate greenhouse gas inventories, guarantees of origin and combined heat and power production—Analysis of impacts on total carbon dioxide emissions. J. Clean. Prod. 2018, 186, 203–214. [Google Scholar] [CrossRef]

- Hufen, J. Cheat Electricity?: The Political Economy of Green Electricity Delivery on the Dutch Market for Households and Small Business. Sustainability 2017, 9, 16. [Google Scholar] [CrossRef]

- Hamburger, Á. Is guarantee of origin really an effective energy policy tool in Europe? A critical approach. Soc. Econ. 2019, 41, 487–507. [Google Scholar] [CrossRef]

- Hast, A.; Syri, S.; Jokiniemi, J.; Huuskonen, M.; Cross, S. Review of green electricity products in the United Kingdom, Germany and Finland. Renew. Sustain. Energy Rev. 2015, 42, 1370–1384. [Google Scholar] [CrossRef]

- Ragwitz, M.; del Río González, P.; Resch, G. Assessing the advantages and drawbacks of government trading of guarantees of origin for renewable electricity in Europe. Energy Policy 2009, 37, 300–307. [Google Scholar] [CrossRef]

- AIB. European Residual Mixes: Results of the Calculation of Residual Mixes for the Calendar Year 2021: Association of Issuing Bodies. 2022. Available online: https://www.aib-net.org/sites/default/files/assets/facts/residual-mix/2021/AIB_2021_Residual_Mix_Results_1_1.pdf (accessed on 17 January 2023).

- Winther, T.; Ericson, T. Matching policy and people? Household responses to the promotion of renewable electricity. Energy Effic. 2013, 6, 369–385. [Google Scholar] [CrossRef]

- Aasen, M.; Westskog, H.; Wilhite, H.; Lindberg, M. The EU electricity disclosure from the business perspective—A study from Norway. Energy Policy 2010, 38, 7921–7928. [Google Scholar] [CrossRef]

- Directive 2009/28/EC of the European Parliament and of the Council of 23 April 2009 on the Promotion of the Use of Energy from Renewable Sources and Amending and Subsequently Repealing Directives 2001/77/EC and 2003/30/EC: Directive 2009/28/EC 2009 Apr 23. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32009L0028 (accessed on 18 December 2023).

- Sundt, S.; Rehdanz, K. Consumers’ willingness to pay for green electricity: A meta-analysis of the literature. Energy Econ. 2015, 51, 1–8. [Google Scholar] [CrossRef]

- Markard, J.; Truffer, B. The promotional impacts of green power products on renewable energy sources: Direct and indirect eco-effects. Energy Policy 2006, 34, 306–321. [Google Scholar] [CrossRef]

- AIB. AIB 2020 Member Tariffs: Association of Issuing Bodies. 2020. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/aib-member-tariffs (accessed on 21 August 2020).

- Velazquez Abad, A.; Dodds, P.E. Green hydrogen characterisation initiatives: Definitions, standards, guarantees of origin, and challenges. Energy Policy 2020, 138, 111300. [Google Scholar] [CrossRef]

- Jansen, J.; Drabik, E.; Egenhofer, C. The Disclosure of Guarantees of Origin: Interactions with the 2030 Climate and Energy Framework; CEPS Special Report: Brussels, Belgium, 2016. [Google Scholar]

- Chuang, J.; Lien, H.-L.; Den, W.; Iskandar, L.; Liao, P.-H. The relationship between electricity emission factor and renewable energy certificate: The free rider and outsider effect. Sustain. Environ. Res. 2018, 28, 422–429. [Google Scholar] [CrossRef]

- Nikolay, J. An Overview of the Development of the Guarantee of Origin Market; University of Greenwich: London, UK, 2020. [Google Scholar]

- Oslo Economics. Analysis of the Trade in Guarantees of Origin: Economic Analysis for Energy Norway; OE-report 2017-58; Oslo, Norway. 2018. Available online: https://dokumen.tips/documents/analysis-of-the-trade-in-guarantees-of-origin-analysis-of-the-trade-in-guarantees.html?page=2 (accessed on 18 December 2023).

- Di Sario, F. GOs Contango Deepens as Demand-Supply Gap Shrinks. 2021. ICIS Editorial. Available online: https://www.icis.com/explore/resources/news/2021/09/20/10686145/gos-contango-deepens-as-demand-supply-gap-shrinks/ (accessed on 17 February 2023).

- Roe, B.; Teisl, M.F.; Levy, A.; Russell, M. US consumers’ willingness to pay for green electricity. Energy Policy 2001, 29, 917–925. [Google Scholar] [CrossRef]

- Breidert, C. Estimation of Willingness-to-Pay: Theory, Measurement, Application, 1st ed.; DUV Deutscher Universitäts-Verlag: Wiesbaden, Germany, 2006. [Google Scholar] [CrossRef]

- Calikoglu, U.; Aydinalp Koksal, M. Green electricity and Renewable Energy Guarantees of Origin demand analysis for Türkiye. Energy Policy 2022, 170, 113229. [Google Scholar] [CrossRef]

- OECD. Greening Household Behaviour: Overview from the 2011 Survey; OECD Publishing: Paris, France, 2014. [Google Scholar] [CrossRef]

- Yang, Y.; Solgaard, H.S.; Haider, W. Value seeking, price sensitive, or green? Analyzing preference heterogeneity among residential energy consumers in Denmark. Energy Res. Soc. Sci. 2015, 6, 15–28. [Google Scholar] [CrossRef]

- Soon, J.-J.; Ahmad, S.-A. Willingly or grudgingly? A meta-analysis on the willingness-to-pay for renewable energy use. Renew. Sustain. Energy Rev. 2015, 44, 877–887. [Google Scholar] [CrossRef]

- Rowlands, I.H.; Scott, D.; Parker, P. Consumers and green electricity: Profiling potential purchasers. Bus. Strat. Env. 2003, 12, 36–48. [Google Scholar] [CrossRef]

- Bollino, C.A. The Willingness to Pay for Renewable Energy Sources: The Case of Italy with Socio-demographic Determinants. Energy J. 2009, 30, 81–96. [Google Scholar] [CrossRef]

- Diaz-Rainey, I.; Ashton, J.K. Profiling potential green electricity tariff adopters: Green consumerism as an environmental policy tool? Bus. Strat. Env. 2011, 20, 456–470. [Google Scholar] [CrossRef]

- Knapp, L.; O’Shaughnessy, E.; Heeter, J.; Mills, S.; DeCicco, J.M. Will consumers really pay for green electricity? Comparing stated and revealed preferences for residential programs in the United States. Energy Res. Soc. Sci. 2020, 65, 101457. [Google Scholar] [CrossRef]

- Grilli, G. Renewable energy and willingness to pay: Evidences from a meta-analysis. Econ. Policy Energy Environ. 2017, 1, 253–271. [Google Scholar] [CrossRef]

- Borchers, A.M.; Duke, J.M.; Parsons, G.R. Does willingness to pay for green energy differ by source? Energy Policy 2007, 35, 3327–3334. [Google Scholar] [CrossRef]

- Andor, M.A.; Frondel, M.; Vance, C. Germany’s Energiewende: A Tale of Increasing Costs and Decreasing Willingness-to-Pay. Energy J. 2017, 38, 211–228. [Google Scholar] [CrossRef]

- Yevdokimov, Y.; Getalo, V.; Shukla, D.; Sahin, T. Measuring willingness to pay for electricity: The case of New Brunswick in Atlantic Canada. Energy Environ. 2019, 30, 292–303. [Google Scholar] [CrossRef]

- Bigerna, S.; Polinori, P. Italian households’ willingness to pay for green electricity. Renew. Sustain. Energy Rev. 2014, 34, 110–121. [Google Scholar] [CrossRef]

- Robinson, J. The Economics of Imperfect Competition; MacMillan: London, UK, 1933. [Google Scholar]

- Woeckener, B. Volkswirtschaftslehre; Springer: Berlin/Heidelberg, Germany, 2019. [Google Scholar]

- AIB. Activity Statistics: Association of Issuing Bodies. 2020. Available online: https://www.aib-net.org/facts/market-information/statistics/activity-statistics-all-aib-members (accessed on 27 August 2020).

- Parkin, M.; Powell, M.; Matthews, K. Economics, 5th ed.; Addison-Wesley: Boston, MA, USA, 2003. [Google Scholar]

- Jansen, J. Does the EU Renewable Energy Secotr Still Need a Guarantees of Origin Market? CEPS Energy Climate House: Brussels, Belgium, 2017; Policy Insights 2017-27; Available online: https://cdn.ceps.eu/wp-content/uploads/2017/07/CEPS%20Policy%20Insights%202017-25%20Guarantees%20of%20Origin%20J%20Jansen.pdf (accessed on 18 December 2023).

- Russell, S. Ability to pay for health care: Concepts and evidence. Health Policy Plan 1996, 11, 219–237. [Google Scholar] [CrossRef] [PubMed]

- Goodspeed, T.J. A re-examination of the use of ability to pay taxes by local governments. J. Public Econ. 1989, 38, 319–342. [Google Scholar] [CrossRef]

- Pederzini, Ò.M. Integrating Energy Demand and Ability to Pay in the Design of Decentralised Energy Supply: A Case Study in Rural Nepal. Master’s Thesis, School of Engineering Sciences, KTH Royal Institute of Technology, Stockholm, Sweden, 2019. [Google Scholar]

- Fankhauser, S.; Tepic, S. Can poor consumers pay for energy and water? An affordability analysis for transition countries. Energy Policy 2007, 35, 1038–1049. [Google Scholar] [CrossRef]

- Bose, R.K.; Shukla, M. Electricity tariffs in India: An assessment of consumers’ ability and willingness to pay in Gujarat. Energy Policy 2001, 29, 465–478. [Google Scholar] [CrossRef]

- European Commission. Proposal for a Directive of the European Parliament and of the Council on Corporate Sustainability Due Diligence and Amending Directive (EU) 2019/1937; European Commission: Brussels, Belgium, 2022; Feb 23 COM/2022/71. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52022PC0071 (accessed on 20 June 2023).

- Fatras, N.; Ma, Z.; Duan, H.; Jørgensen, B.N. A systematic review of electricity market liberalisation and its alignment with industrial consumer participation: A comparison between the Nordics and China. Renew. Sustain. Energy Rev. 2022, 167, 112793. [Google Scholar] [CrossRef]

- IRENA. Global Energy Transformation: A Roadmap to 2050, 2019th ed.; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2019. [Google Scholar]

- IRENA. Renewable Power Generation Costs in 2019; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2020. [Google Scholar]

- Eurostat. Net Electricity Generation by Type of Fuel—Monthly Data; NRG_CB_PEM. 2020. Available online: https://ec.europa.eu/eurostat/statistics-explained/index.php?oldid=515664 (accessed on 18 December 2023).

- IEA. World Energy Outlook 2020; International Energy Agency: Paris, Italy, 2020.

- Eurostat. Number of Private Households by Household Composition, Number of Children and Age of Youngest Child (1000). LFST-HHNHTYCH. 2020. Available online: https://ec.europa.eu/eurostat/web/products-datasets/-/LFST_HHNHTYCH (accessed on 20 October 2020).

- Eurostat. Supply, Transformation and Consumption of Electricity. NRG_CB_E. 2020. Available online: https://ec.europa.eu/eurostat/databrowser/view/nrg_cb_e/default/table?lang=en (accessed on 10 October 2020).

- Eurostat. Electricity Prices Components for Non-Household Consumers—Annual Data (from 2007 Onwards). NRG_PC_205_C. 2020. Available online: https://ec.europa.eu/eurostat/databrowser/view/nrg_pc_205_c/default/table?lang=en (accessed on 10 October 2020).

- Eurostat. Industry by Employment Size Class (NACE Rev. 2, B-E). SBS_SC_IND_R2. 2020. Available online: https://ec.europa.eu/eurostat/databrowser/view/sbs_sc_ind_r2/default/table?lang=en (accessed on 10 October 2020).

- Swiss Federal Office of Energy. Elektrizitätserzeugung: 1970–2019. je-d-08.02.02.01. 2020. Available online: https://www.bfs.admin.ch/bfs/de/home/statistiken/energie.assetdetail.13667566.html (accessed on 27 August 2020).

- Kuronen, A.; Lehtovaara, M. Development of the Guarantees of Origin Market: Key Facts Report. 2017 Update. 2017. Available online: https://recs.org/download/?file=development-of-the-guarantees-of-origin-market-2016-key-facts-report.pdf&file_type=documents&file_type=documents (accessed on 18 June 2023).

- Eurostat. Energy Balance Guide: Methodology Guide for the Construction of Energy Balances & Operational Guide for the Energy Balance Builder Tool; Eurostat: Brussels, Belgium, 2019.

- RE100. RE100 Members. 2020. Available online: https://www.there100.org/re100-members (accessed on 20 October 2020).

- Göke, L.; Weibezahn, J.; von Hirschhausen, C. A collective blueprint, not a crystal ball: How expectations and participation shape long-term energy scenarios. Energy Res. Soc. Sci. 2023, 97, 102957. [Google Scholar] [CrossRef]

- Krey, V.; Guo, F.; Kolp, P.; Zhou, W.; Schaeffer, R.; Awasthy, A.; Bertram, C.; de Boer, H.-S.; Fragkos, P.; Fujimori, S.; et al. Looking under the hood: A comparison of techno-economic assumptions across national and global integrated assessment models. Energy 2019, 172, 1254–1267. [Google Scholar] [CrossRef]

- Greenfact. The Greenfact Market Survey 2020: Current Status and Outlook within the GO Market; Greenfact: Oslo, Norway, 2020. [Google Scholar]

- Köpke, R. PPA-Barometer 2020: Gekommen, um zu bleiben. Available online: https://enervis.de/wp-content/uploads/2020/06/PPA-Barometer-2020-Energie-Management.pdf (accessed on 18 December 2023).

- Dagoumas, A.S.; Koltsaklis, N.E. Price Signal of Tradable Guarantees of Origin for Hedging Risk of Renewable Energy Sources Investments. Int. J. Energy Econ. Policy 2017, 7, 59–67. [Google Scholar]

- Linnemann, M. Post-EEG-Anlagen in der Energiewirtschaft; Springer Fachmedien: Wiesbaden, Germany, 2021. [Google Scholar]

- AIB. FaStGo: Facilitating Standards for Guarantees of Origin: Association of Issuing Bodies. 2019. Available online: https://www.aib-net.org/news-events/aib-projects-and-consultations/fastgo (accessed on 28 October 2020).

- European Commission. Proposal for a Directive of the European Parliament and of the Council Amending Directive (EU) 2018/2001 of the European Parliament and of the Council, Regulation (EU) 2018/1999 of the European Parliament and of the Council and Directive 98/70/EC of the European Parliament and of the Council as Regards the Promotion of Energy from Renewable Sources, and Repealing Council Directive (EU) 2015/652: European Commission. 2021. Available online: https://eur-lex.europa.eu/resource.html?uri=cellar:dbb7eb9c-e575-11eb-a1a5-01aa75ed71a1.0001.02/DOC_1&format=PDF (accessed on 27 June 2023).

- European Commission. Guidance to Member States on Good Practices to Speed up Permit-Granting Procedures for Renewable Energy Projects and on Facilitating Power Purchase Agreements: Accompanying the Document “Commission Recommendation on Speeding up Permit-Granting Procedures for Renewable Energy Projects and Facilitating Power Purchase Agreements”; European Commission: Brussels, Belgium, 2022. Available online: https://ec.europa.eu/info/law/better-regulation/have-your-say/initiatives/13334-Renewable-energy-projects-permit-granting-processes-power-purchase-agreements_en (accessed on 8 October 2023).

- ENTSO-E. Views on a Future-Proof Market Design for Guarantees of Origin. 2022. ENTSO-E Position Paper. Available online: https://eepublicdownloads.blob.core.windows.net/public-cdn-container/clean-documents/Publications/Position%20papers%20and%20reports/2022/entso-e_pp_guarantees_of_origin_220715%20for%20publication.pdf (accessed on 8 October 2023).

- Advantag Services GmbH. Herkunftsnachweise. 2019. Available online: https://advantag.de/de/category/co2-marktberichte/herkunftsnachweise (accessed on 10 September 2020).

- Nvalue, A.G. EU HKN Preise [€/MWh]. 2020. Available online: https://archive.org/details/nvalue-go-o-prices-03092020 (accessed on 18 December 2023).

- Klimscheffskij, M.; Van Craenenbroeck, T.; Lehtovaara, M.; Lescot, D.; Tschernutter, A.; Raimundo, C.; Seebach, D.; Timpe, C. Residual Mix Calculation at the Heart of Reliable Electricity Disclosure in Europe—A Case Study on the Effect of the RE-DISS Project. Energies 2015, 8, 4667–4696. [Google Scholar] [CrossRef]

- CREG. EECS Electricity Domain Protocol for Belgium (Offshore): Commissie voor de Regulering van de Elektriciteit en het Gas. 2018. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/domain-protocols (accessed on 25 August 2020).

- E-Control. EECS Electricity Domain Protocol for Austria. 2019. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/domain-protocols (accessed on 25 August 2020).

- BRUGEL. EECS Electricity Domain Protocol for Brussels. 2013. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/domain-protocols (accessed on 25 August 2020).

- VREG. EECS Electricity Domain Protocol for Flanders: Vlaamse Regulator van de Elektriciteits- en Gasmarkt. 2017. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/domain-protocols (accessed on 25 August 2020).

- CaWaPE. EECS Electricity Domain Protocol for Wallonia, Belgium: Commsion Wallone pour l’Energie. 2017. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/domain-protocols (accessed on 25 August 2020).

- Pronovo Ltd. EECS Electricity Domain Protocol for Switzerland. 2018. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/domain-protocols (accessed on 25 August 2020).

- Transmission System Operator (Cyprus). EECS Electricity Scheme Domain Protocol for Cyprus. 2012. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/domain-protocols (accessed on 25 August 2020).

- Operator trhu s elektrinou, a.s. (OTE). EECS Electricity Domain Protocol for Czech Republic. 2018. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/domain-protocols (accessed on 25 August 2020).

- Energienet, D.K. EECS Electricity Domain Protocol for Denmark. 2016. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/domain-protocols (accessed on 25 August 2020).

- Elering, A.S. EECS Electricity Domain Protocol for Estonia. 2015. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/domain-protocols (accessed on 25 August 2020).

- CNMC. EECS Electricity Domain Protocol for Spain: Comisión Nacional de los Mercados y la Competencia. 2017. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/domain-protocols (accessed on 25 August 2020).

- Finextra, O.Y. EECS Electricity Domain Protocol for Finland. 2017. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/domain-protocols (accessed on 25 August 2020).

- Powernext SAS. EECS Electricity Domain Protocol for France. 2019. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/domain-protocols (accessed on 25 August 2020).

- DAPEEP S.A. EECS Electricity Domain Protocol for Interconnected System—Greece. 2013. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/domain-protocols (accessed on 25 August 2020).

- Hrote. EECS Electricity Domain Protocol for Croatia: Hrvatski Operator Trzista Energije. 2016. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/domain-protocols (accessed on 25 August 2020).

- SEMO. EECS Electricity Domain Protocol for Ireland: Single Electricity Market Operator. 2019. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/domain-protocols (accessed on 25 August 2020).

- Landsnet, H.F. EECS Electricity Domain Protocol for Iceland. 2015. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/domain-protocols (accessed on 25 August 2020).

- GSE. EECS Electricity Domain Protocol for Italy: Gestore dei Servizi Energetici. 2015. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/domain-protocols (accessed on 25 August 2020).

- LITGRID AB. EECS Electricity Domain Protocol for Lithuania. 2018. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/domain-protocols (accessed on 25 August 2020).

- Institut Luxembourgeois de Régulation. EECS Electricity Domain Protocol for Luxembourg. 2018. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/domain-protocols (accessed on 25 August 2020).

- CertiQ, B.V. EECS Electricity Domain Protocol for the Netherlands. 2018. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/domain-protocols (accessed on 25 August 2020).

- Statnett, S.F. EECS Electricity Domain Protocol for Statnett SF. 2018. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/domain-protocols (accessed on 25 August 2020).

- Rede Eléctrica Nacional, S.A. (REN). EECS Electricity Domain Protocol for Portugal. 2020. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/domain-protocols (accessed on 25 August 2020).

- Elektromreža Srbije JSC Belgrade. Domain Protocol for Serbia. 2019. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/domain-protocols (accessed on 25 August 2020).

- Energimyndigheten. EECS Electricity Domain Protocol for Sweden. 2019. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/domain-protocols (accessed on 25 August 2020).

- OKTE, a. EECS Electricity Domain Protocol for OKTE. a.s. 2019. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/domain-protocols (accessed on 25 August 2020).

- Agencija Za Energijo. EECS Electricity Domain Protocol for Slovenia. 2017. Available online: https://www.aib-net.org/facts/aib-member-countries-regions/domain-protocols (accessed on 25 August 2020).

| GO Type | Period | Price/Price Range (EUR/MWh) |

|---|---|---|

| Nordic Hydro | 2015–2018 | 0.05–3.40 |

| German (Unspecified) | 2018 | 0.8–1.6 |

| Austrian (Unspecified) | 2018–2019 | 0.9–1.45 |

| EU Hydro | 2018–2020 | 0.15–1.98 |

| EU (Average), 2022 Futures | September 2021 | 1.25 |

| EU (All) | Spring 2022 | 1.7–2.3 |

| Technology/Green Electricity Source | WTP (USD per Month) | Reference/s |

|---|---|---|

| Mixed source/“green” | 13.10 | [53] |

| Mixed source/“green” | 8.44–17.00 (Mean) | [54] |

| Mixed source/“green” | 5.10 (Low)–7.38 (High) | [52] |

| Solar | 14.40 | [53] |

| Solar | 14.68–21.54 (Mean) | [54] |

| Wind | 14.14 | [53] |

| Wind | 6.14–15.47 (Mean) | [54] |

| Biomass | 11.02 | [53] |

| Biomass | −2.22–10.59 (Mean) | [54] |

| Hydropower | 9.57 | [53] |

| Geothermal | 36.90 | [53] |

| Category | Description | Countries |

|---|---|---|

| 1 | Issuance of GOs for subsidized electricity, but disclosure of subsidy reception on GOs | Austria, Denmark, Estonia, Finland, Italy, Portugal, Switzerland |

| 2 | Subsidized GOs are auctioned | France, Luxembourg, Slovenia, the Slovak Republic |

| 3 | Subsidized GOs are immediately canceled | Cyprus, Lithuania |

| 4 | No regulations on subsidies | Belgium, Croatia, the Czech Republic, Greece, the Netherlands, Norway, Spain, Sweden |

| 5 | Subsidized electricity production may not issue any GOs | Germany, Ireland, Serbia |

| 6 | No subsidy system in place | Iceland |

| Category | 1 | 2 | 3 | 4 | 5 | 6 |

|---|---|---|---|---|---|---|

| Biomass | 0.64 | 0.26 | 0.08 | 0.49 | 0.21 | No GO issuance |

| Geothermal | 0.52 | 0.03 | No GO issuance | No GO issuance | No GO issuance | 0.92 |

| Hydro | 0.78 | 0.49 | 0.35 | 0.6 | 0.63 | 0.98 |

| Solar | 0.53 | 0.05 | No GO issuance | 0.37 | 0.02 | No GO issuance |

| Wind | 0.68 | 0.28 | 0.5 | 0.73 | 0.09 | No GO issuance |

| No. | Data Set | Contents | Used for… | Source |

|---|---|---|---|---|

| 1 | Household characteristics | Household distributions | WTP, demand | [74] |

| 2 | Nrg_cb_e | Electricity consumption | ATP, demand | [75] |

| 3 | Nrg_pc_205 | Electricity prices | ATP, WTP | [76] |

| 4 | Sbs_sc_ind_r2 | Structural data on European industry, i.e., average revenue and number of companies per NACE sector and size | Profit, demand, ATP | [77] |

| 5 | Swiss Electricity Statistics | Electricity consumption and prices in Switzerland | ATP, demand, WTP | [78] |

| Environmental Concern | ATP | ||||

|---|---|---|---|---|---|

| x ≤ 20% | 20% < x ≤ 40% | 40% < x ≤ 60% | 60% < x ≤ 80% | 80% < x ≤ 100% | |

| y ≤ 20% | 0 | 0.025 | 0.05 | 0.075 | 0.1 |

| 20% < y ≤ 40% | 0.025 | 0.05625 | 0.0875 | 0.11875 | 0.15 |

| 40% < y ≤ 60% | 0.075 | 0.11875 | 0.1625 | 0.20625 | 0.2 |

| 60% < y ≤ 80% | 0.15 | 0.2125 | 0.275 | 0.3375 | 0.25 |

| 80% < y ≤ 100% | 0.1 | 0.15 | 0.2 | 0.25 | 0.3 |

| Scenario 1 | Scenario 2 | |||||

|---|---|---|---|---|---|---|

| Technology | 2020 | 2030 | 2040 | 2020 | 2030 | 2040 |

| Biomass | 1.47 | 2.12 | 3.36 | 1.44 | 1.67 | 1.98 |

| Geothermal | 5.13 | 7.33 | 12.54 | 5.13 | 5.56 | 6.77 |

| Hydro | 0.4 | 0.99 | 1.51 | 0.37 | 0.47 | 0.82 |

| Other RES | 0 | 4.59 | 6.45 | 0 | 3.86 | 3.98 |

| Solar | 4.46 | 6.03 | 9.5 | 4.43 | 4.46 | 4.91 |

| Wind | 2.15 | 2.88 | 4.47 | 2.14 | 2.22 | 2.47 |

| Scenario 3 | Scenario 4 | |||||

| Technology | 2020 | 2030 | 2040 | 2020 | 2030 | 2040 |

| Biomass | 3.26 | 3.46 | 5.51 | 3.13 | 2.41 | 2.49 |

| Geothermal | 4.59 | 12.8 | 12.82 | 4.59 | 10.41 | 11.91 |

| Hydro | 1.23 | 1.55 | 1.93 | 1.23 | 0.8 | 1.06 |

| Other RES | 0 | 7 | 8.97 | 0 | 4.73 | 4.77 |

| Solar | 12.19 | 9.3 | 12.57 | 12.19 | 6.53 | 6.72 |

| Wind | 4.59 | 4.96 | 7 | 4.44 | 3.54 | 3.66 |

| Observed Year | 2025 | 2030 |

|---|---|---|

| Survey | 1.6 | 2.02 |

| Scenario 1 | 1.03 | 1.73 |

| Scenario 2 | 0.81 | 0.83 |

| Scenario 3 | 3.32 | 3.8 |

| Scenario 4 | 3.18 | 3.17 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wimmers, A.; Madlener, R. The European Market for Guarantees of Origin for Green Electricity: A Scenario-Based Evaluation of Trading under Uncertainty. Energies 2024, 17, 104. https://doi.org/10.3390/en17010104

Wimmers A, Madlener R. The European Market for Guarantees of Origin for Green Electricity: A Scenario-Based Evaluation of Trading under Uncertainty. Energies. 2024; 17(1):104. https://doi.org/10.3390/en17010104

Chicago/Turabian StyleWimmers, Alexander, and Reinhard Madlener. 2024. "The European Market for Guarantees of Origin for Green Electricity: A Scenario-Based Evaluation of Trading under Uncertainty" Energies 17, no. 1: 104. https://doi.org/10.3390/en17010104

APA StyleWimmers, A., & Madlener, R. (2024). The European Market for Guarantees of Origin for Green Electricity: A Scenario-Based Evaluation of Trading under Uncertainty. Energies, 17(1), 104. https://doi.org/10.3390/en17010104