The Differential Effects of Oil Prices on the Development of Renewable Energy in Oil-Importing and Oil-Exporting Countries in Africa

Abstract

:1. Introduction

2. Literature Review

3. Methodology

3.1. Data Sources

3.2. Econometric Model

3.3. Econometric Technique: P-VECM Approach

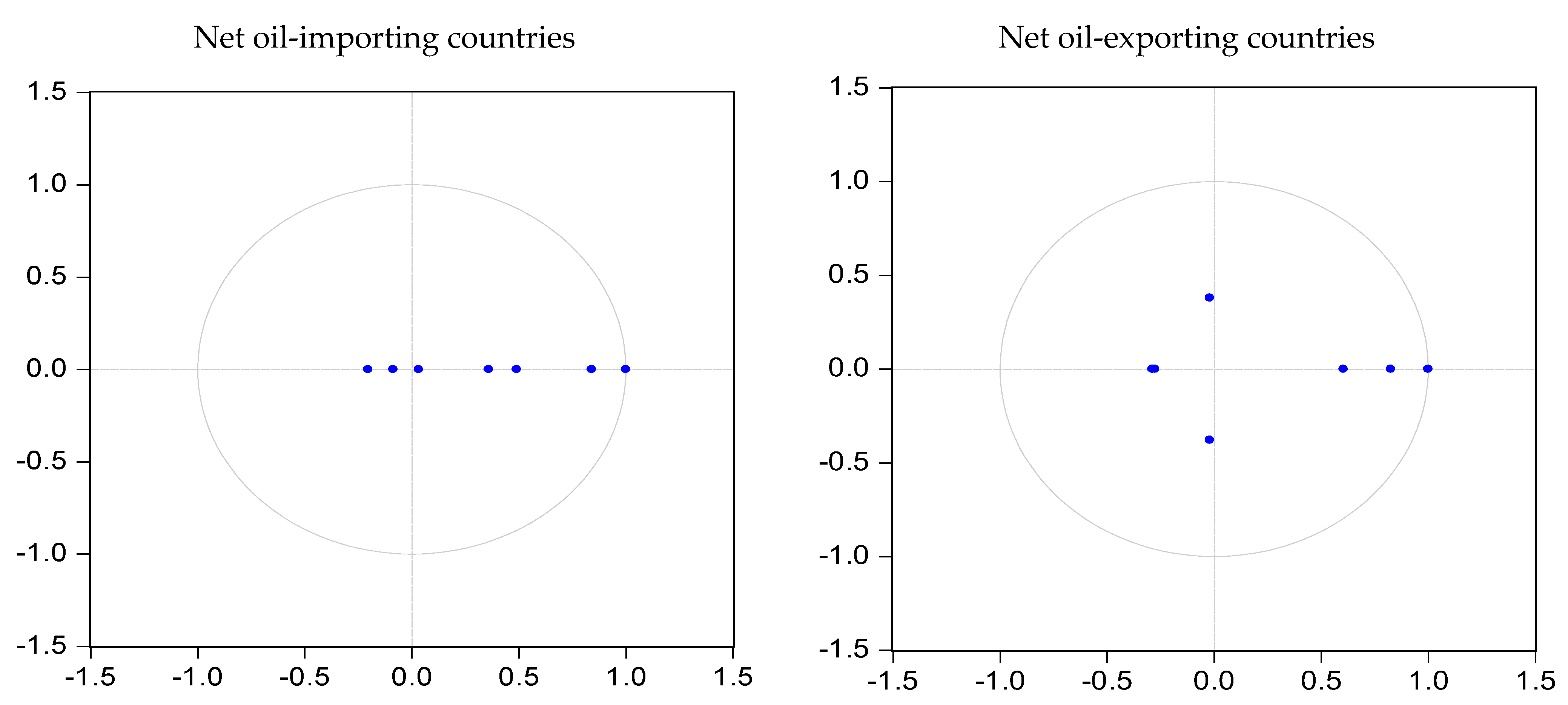

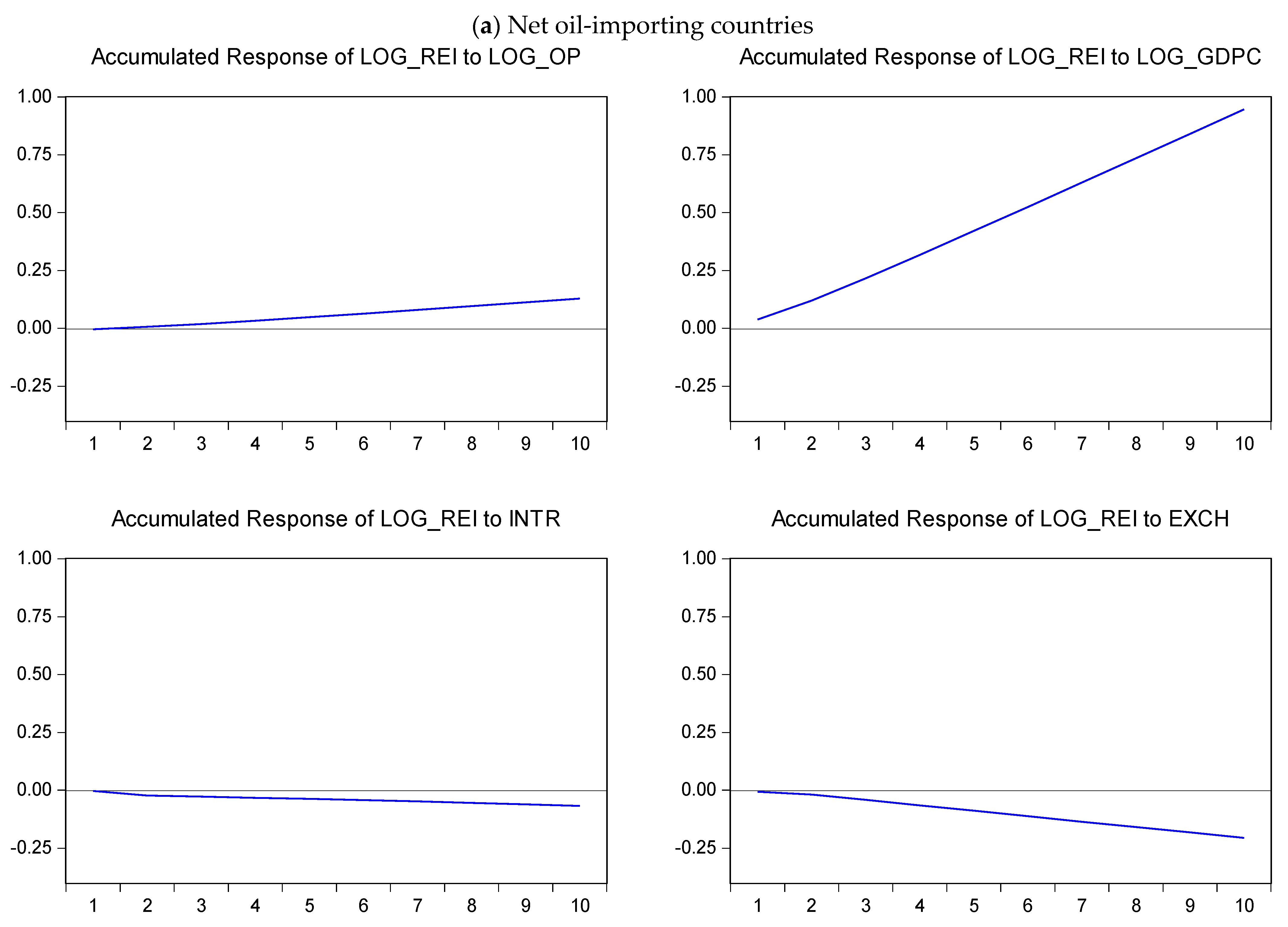

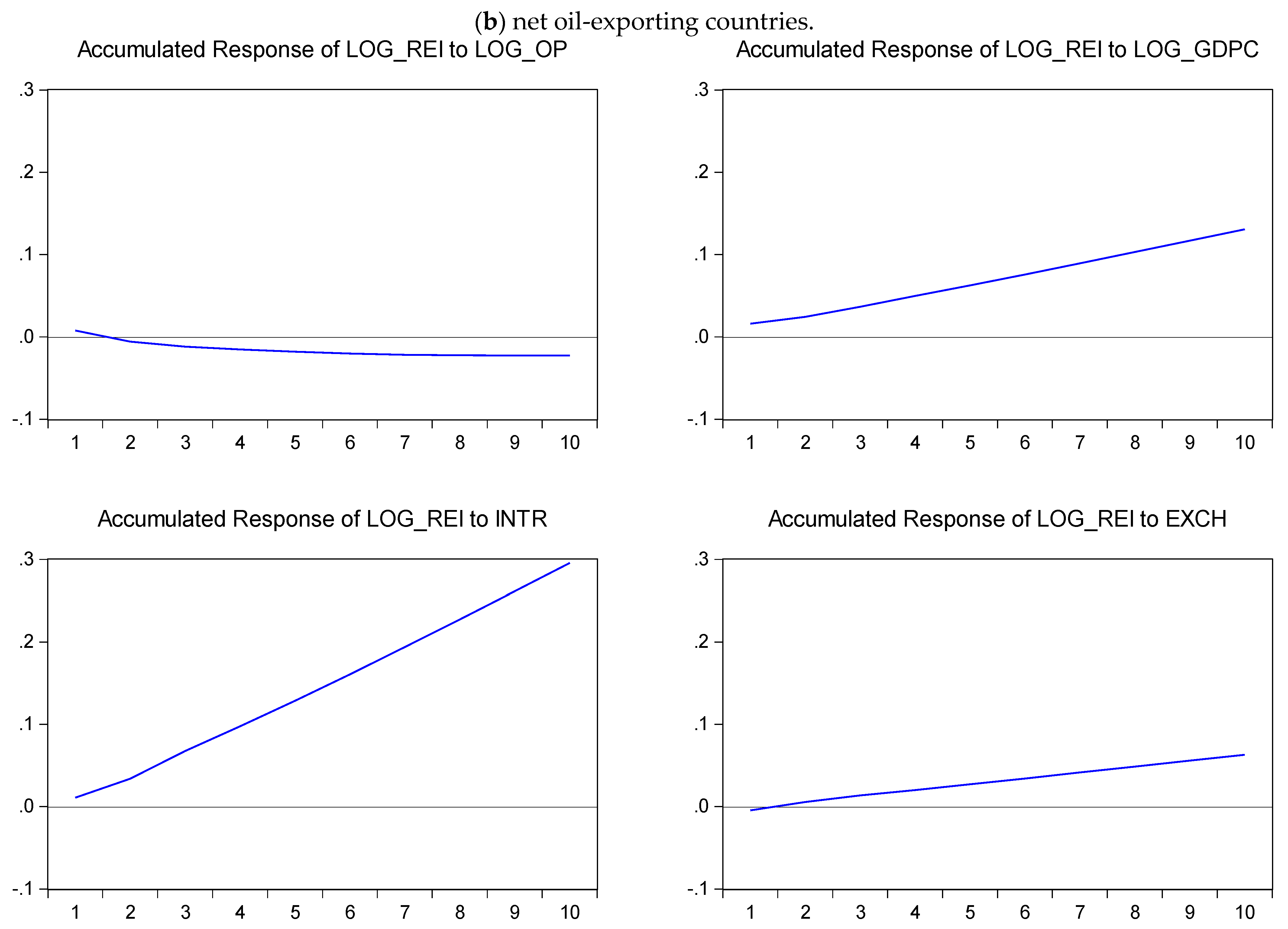

4. Empirical Analysis

Robustness Checks

5. Discussion and Implications

6. Concluding Remarks

6.1. Contributions

6.2. Policy Recommendations

- Encouragement of investment in renewable energy: Policymakers in oil-importing countries should encourage the development of renewable energy by offering financial incentives, such as tax breaks, subsidies, or low-interest loans, to potential investors. This will help to make renewable energy more economically competitive, particularly when oil prices are high.

- Promotion of economic growth: Policymakers should implement policies that promote economic growth, such as infrastructure development and job creation, which will drive the growth of renewable energy. This can be achieved through public–private partnerships or government-led initiatives.

- Reduction of interest rates: Policymakers should reduce interest rates to encourage investment in renewable energy in net oil-importing countries. High-interest rates may discourage investors from pursuing renewable energy projects, particularly in the early stages, when returns on investment may be uncertain.

- Management of exchange rates: Policymakers should manage exchange rates carefully to promote the development of renewable energy in the oil-importing countries. This can be conducted through measures, such as currency stabilization funds, which can help to reduce volatility and make investment in renewable energy more predictable.

- Support of technology transfer: Policymakers should facilitate the transfer of renewable energy technology to net oil-importing countries to help them overcome technological barriers to the development of renewable energy. This can be conducted through partnerships with technology providers or through capacity-building programs.

6.3. Limitations and Future Research Directions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Assessment R Report 6. Climate Change 2022 Impacts, Adaptation and Vulnerability Summary for Policymakers. Working Group II Contribution to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change. 2022. Available online: https://www.ipcc.ch/report/ar6/wg2/ (accessed on 2 March 2023).

- IEA. Global Energy Review; IEA: Paris, France, 2021. [Google Scholar]

- Tambari, I.T.; Dioha, M.O.; Failler, P. Renewable energy scenarios for sustainable electricity supply in Nigeria. Energy Clim. Change 2020, 1, 100017. [Google Scholar] [CrossRef]

- Oyewo, A.S.; Aghahosseini, A.; Ram, M.; Breyer, C. Just transition towards defossilised energy systems for developing economies: A case study of Ethiopia. Renew. Energy 2021, 176, 346–365. [Google Scholar] [CrossRef]

- Jia, Z.; Wen, S.; Lin, B. The effects and reacts of COVID-19 pandemic and international oil price on energy, economy, and environment in China. Appl. Energy 2021, 302, 117612. [Google Scholar] [CrossRef] [PubMed]

- Manama, B. Economic Diversification in Oil-Exporting Arab Countries. In Annual Meeting of Arab Ministers of Finance; International Monetary Fund: Washington, DC, USA, 2016. [Google Scholar]

- Aloui, D.; Goutte, S.; Guesmi, K.; Hchaichi, R. COVID-19′s impact on crude oil and natural gas S&P GS Indexes. HAL SHS Sci. Hum. Soc. 2020, 16, 1–6. [Google Scholar]

- Gozgor, G.; Kumar, M.; Demir, E.; Padhan, H. The impact of economic globalization on renewable energy in the OECD countries. Energy Policy 2020, 139, 111365. [Google Scholar] [CrossRef]

- Aleluia, J.; Tharakan, P.; Chikkatur, A.P.; Shrimali, G.; Chen, X. Accelerating a clean energy transition in Southeast Asia: Role of governments and public policy. Renew. Sustain. Energy Rev. 2022, 159, 112226. [Google Scholar] [CrossRef]

- Borzuei, D.; Moosavian, S.F.; Ahmadi, A. Investigating the dependence of energy prices and economic growth rates with emphasis on the development of renewable energy for sustainable development in Iran. Sustain. Dev. 2022, 30, 848–854. [Google Scholar] [CrossRef]

- Mukhtarov, S.; Mikayilov, J.I.; Maharramov, S.; Aliyev, J. Higher oil prices, are they good or bad for renewable energy consumption: The case of Iran? Renew. Energy 2022, 186, 411–419. [Google Scholar] [CrossRef]

- IEA. For the First Time in Decades, the Number of People without Access to Electricity Is Set to Increase in 2022; IEA: Paris, France, 2022; Available online: https://www.iea.org/commentaries/for-the-first-time-in-decades-the-number-of-people-without-access-to-electricity-is-set-to-increase-in-2022 (accessed on 15 March 2023).

- US Department of Commerce. Egypt-Electricity and Renewable Energy; US International Trade Administration: Washington, DC, USA, 2022. Available online: https://www.trade.gov/country-commercial-guides/egypt-electricity-and-renewable-energy (accessed on 10 March 2023).

- United State Department of State. Secretary Antony, J. Blinken Remarks at the Virtual Kenya-U.S. Interagency Clean Energy Event; US Department of State: Washington, DC, USA, 2021. Available online: https://www.state.gov/secretary-antony-j-blinken-remarks-at-the-virtual-kenya-u-s-interagency-clean-energy-event/ (accessed on 17 March 2023).

- Morisset, J.; Mariano, S. Future Development: 2 Reasons Why Climate Skeptics Should Support South Africa’s Just Energy Transition; Brookings Institution: Washington, DC, USA, 2022; Available online: https://www.brookings.edu/blog/future-development/2022/11/17/two-reasons-why-climate-skeptics-should-support-south-africas-just-energy-transition/ (accessed on 2 March 2023).

- Inuwa, N.; Adamu, S.; Hamza, Y.; Bello, M. Does dichotomy between resource dependence and resource abundance matters for resource curse hypothesis ? New evidence from quantiles via moments. Resour. Policy 2023, 81, 103295. [Google Scholar] [CrossRef]

- Miamo, W.C.; Achuo, E.D. Can the resource curse be avoided? An empirical examination of the nexus between crude oil price and economic growth. SN Bus. Econ. 2022, 2, 5. [Google Scholar] [CrossRef]

- Oludimu, S.; Alola, A.A. Does crude oil output aid economy boom or curse in Nigeria? An inference from “Dutch disease.” Manag. Environ. Qual. Int. J. 2022, 33, 185–201. [Google Scholar]

- Wang, Q.; Li, S.; Pisarenko, Z. Heterogeneous effects of energy ef fi ciency, oil price, environmental pressure, R&D investment, and policy on renewable energy—Evidence from the G20 countries. Energy 2020, 209, 118322. [Google Scholar] [CrossRef]

- Mukhtarov, S.; Mikayilov, J.I.; Humbatova, S.; Muradov, V. Do High Oil Prices Obstruct the Transition to Renewable Energy Consumption? Sustainability 2020, 12, 4689. [Google Scholar] [CrossRef]

- Rasheed, Q.M.; Abdul, R.; Tomiwa, H.; Adebayo, S.; Ahmed, Z.; Ahmad, M. The long—Run relationship between energy consumption, oil prices, and carbon dioxide emissions in European countries. Environ. Sci. Pollut. Res. 2022, 29, 24234–24247. [Google Scholar] [CrossRef]

- Olanipekun, I.O.; Ozkan, O.; Olasehinde-Williams, G. Is renewable energy use lowering resource-related uncertainties? Energy 2023, 271, 126949. [Google Scholar] [CrossRef]

- Mukhtarov, S.; Humbatova, S.; Hajiyev, N.G.-O. Is the transition to renewable energy consumption hampered by high oil prices ? Is the Transition to Renewable Energy Consumption Hampered by High Oil Prices? Int. J. Energy Econ. Policy 2021, 11, 377–380. [Google Scholar] [CrossRef]

- Guo, Y.; Yu, C.; Zhang, H.; Cheng, H. Asymmetric between oil prices and renewable energy consumption in the G7 countries. Energy 2021, 226, 120319. [Google Scholar] [CrossRef]

- Murshed, M.; Tanha, M.M. Oil price shocks and renewable energy transition: Empirical evidence from net oil-importing South Asian economies. Energy Ecol. Environ. 2021, 6, 183–203. [Google Scholar] [CrossRef]

- Sahu, P.K.; Solarin, S.A.; Al-mulali, U.; Ozturk, I. Investigating the asymmetry effects of crude oil price on renewable energy consumption in the United States. Environ. Sci. Pollut. Res. 2022, 29, 817–827. [Google Scholar] [CrossRef]

- Guo, L.; She, C.; Kong, D.; Yan, S.; Xu, Y. Prediction of the effects of climate change on hydroelectric generation, electricity demand, and emissions of greenhouse gases under climatic scenarios and optimized ANN model. Energy Rep. 2021, 7, 5431–5445. [Google Scholar] [CrossRef]

- Cheng, Y.; Awan, U.; Ahmad, S.; Tan, Z. How do technological innovation and fiscal decentralization affect the environment? A story of the fourth industrial revolution and sustainable growth. Technol. Forecast. Soc. Change 2021, 162, 120398. [Google Scholar] [CrossRef]

- Zhao, Y.; Zhang, Y.; Wei, W. Quantifying international oil price shocks on renewable energy development in China. Appl. Econ. 2021, 53, 329–344. [Google Scholar] [CrossRef]

- Lin, B.; Wang, S. Mechanism analysis of the influence of oil price uncertainty on strategic investment of renewable energy enterprises. Int. J. Financ. Econ. 2022, 28, 1–18. [Google Scholar]

- Royal, S.; Singh, K. A nexus between renewable energy, FDI, oil prices, oil rent and CO2 emission: Panel data evidence from G7 economies. OPEC Energy Rev. 2022, 46, 208–227. [Google Scholar] [CrossRef]

- Escoffier, M.; Hache, E.; Mignon, V.; Paris, A. Determinants of solar photovoltaic deployment in the electricity mix: Do oil prices really matter? Energy Econ. 2021, 97, 105024. [Google Scholar] [CrossRef]

- Husaini, H.D.; Lean, H.H. Renewable and non-renewable electricity-growth nexus in Asia: The role of private power plants and oil price threshold effect. Resour. Policy 2022, 78, 102850. [Google Scholar] [CrossRef]

- Zaghdoudi, T.; Tissaoui, K.; Hakimi, A.; Ben, L. Dirty versus renewable energy consumption in China: A comparative analysis between conventional and non-conventional approaches. Ann. Oper Res. 2023, 18, 3–12. [Google Scholar] [CrossRef]

- Kazemzadeh, E.; Fuinhas, J.A.; Koengkan, M.; Shadmehri, M.T.A. Relationship between the share of renewable electricity consumption, economic complexity, financial development, and oil prices: A two-step club convergence and PVAR model approach. Int. Econ. 2023, 173, 260–275. [Google Scholar] [CrossRef]

- Deka, A.; Cavusoglu, B.; Dube, S.; Rukani, S.; Omotola, M. Examining the effect of renewable energy on exchange rate in the emerging economies with dynamic ARDL bounds test approach. Renew. Energy Focus 2023, 44, 237–243. [Google Scholar] [CrossRef]

- Murshed, M. Efficacies of technological progress and renewable energy transition in amplifying national electrification rates: Contextual evidence from developing countries. Util. Policy 2023, 81, 101512. [Google Scholar] [CrossRef]

- Tambari, I.; Failler, P. Determining if oil prices significantly affect renewable energy investment in african countries with energy security concerns. Energies 2020, 13, 6740. [Google Scholar] [CrossRef]

- Ali, M.; Tursoy, T.; Samour, A.; Moyo, D.; Konneh, A. Testing the impact of the gold price, oil price, and renewable energy on carbon emissions in South Africa: Novel evidence from bootstrap ARDL and NARDL approaches. Resour. Policy 2022, 79, 102984. [Google Scholar] [CrossRef]

- Sims, C.A.; Stock, J.H.; Watson, M.W. Inference in Linear Time Series Models with some Unit Roots. Econometrica 1990, 58, 113. [Google Scholar] [CrossRef]

- Dunne, J.P.; Smith, R.P. Military expenditure and granger causality: A critical review. Def. Peace Econ. 2010, 21, 427–441. [Google Scholar] [CrossRef]

- Sheytanova, T. The Accuracy of the Hausman Test in Panel Data: A Monte Carlo Study. 2014. Available online: http://oru.diva-portal.org/smash/get/diva2:805823/FULLTEXT01.pdf (accessed on 23 March 2023).

- Mehrara, M.; Rezaei, S.; Razi, D.H. Determinants of Renewable Energy Consumption among ECO countries; Based on Bayesian Model Averaging and Weighted-Average Least Square. Int. Lett. Soc. Humanist Sci. 2015, 54, 96–109. [Google Scholar] [CrossRef]

- Xin-Gang, Z.; Yu-Qiao, Z. Analysis of the effectiveness of Renewable Portfolio Standards: A perspective of shared mental model. J. Clean. Prod. 2021, 278, 124276. [Google Scholar] [CrossRef]

- Apergis, N.; Payne, J.E. Renewable energy consumption and economic growth: Evidence from a panel of OECD countries. Energy Policy 2010, 38, 656–660. [Google Scholar] [CrossRef]

- Henriques, I.; Sadorsky, P. Oil prices and the stock prices of alternative energy companies. Energy Econ. 2008, 30, 998–1010. [Google Scholar] [CrossRef]

- Shah, I.H.; Hiles, C.; Morley, B. How do oil prices, macroeconomic factors and policies affect the market for renewable energy? Appl. Energy 2018, 215, 87–97. [Google Scholar] [CrossRef]

- Apergis, N.; Payne, J.E. Renewable energy, output, carbon dioxide emissions, and oil prices: Evidence from South America. Energy Sources Part B Econ. Plan. Policy 2015, 10, 281–287. [Google Scholar] [CrossRef]

- Brini, R.; Amara, M.; Jemmali, H. Renewable energy consumption, International trade, oil price and economic growth inter-linkages: The case of Tunisia. Renew. Sustain. Energy Rev. 2017, 76, 620–627. [Google Scholar] [CrossRef]

- Tiwari, A.K. Comparative performance of renewable and nonrenewable energy source on economic growth and CO2 emissions of europe and eurasian countries: A PVAR approach. Econ. Bull. 2011, 31, 2356–2372. [Google Scholar]

- Johansen, S.; Juselius, K. Testing structural hypotheses in a multivariate cointegration analysis of the PPP and the UIP for UK. J. Econ. 1992, 53, 211–244. [Google Scholar] [CrossRef]

- Chen, Y.; Liu, L. Data cleaning and data preprocessing for big data: A survey. Mob. Netw. Appl. 2018, 23, 375–382. [Google Scholar] [CrossRef]

- Kim, K.; Park, H.; Kim, H. Real options analysis for renewable energy investment decisions in developing countries. Renew. Sustain. Energy Rev. 2017, 75, 918–926. [Google Scholar] [CrossRef]

- Im, K.S.; Pesaran, M.H.; Shin, Y. Testing for unit roots in heterogeneous panels. J. Econ. 2003, 115, 53–74. [Google Scholar] [CrossRef]

- Levin, A.; Lin, C.F.; Chu, C.S.J. Unit root tests in panel data: Asymptotic and finite-sample properties. J. Econ. 2002, 108, 1–24. [Google Scholar] [CrossRef]

- Pedroni, P. Panel Cointegration; Asymptotic and Finite Sample Properties of Pooled Time Series Tests, with an Application to the PPP Hypothesis; Indiana University Bloomington: Bloomington, IN, USA, 1995. [Google Scholar]

- Pedroni, P. Panel Cointegration: Asymptotic and finite sample properties of pooled time series tests with an application to the ppp hypothesis. Econ. Theory 2004, 20, 597–625. Available online: https://www.cambridge.org/core/journals/econometric-theory/article/abs/panel-cointegration-asymptotic-and-finite-sample-properties-of-pooled-time-series-tests-with-an-application-to-the-ppp-hypothesis/F31DA49F3109F20315298A97EB46A47E (accessed on 18 March 2023). [CrossRef]

- Abrigo, R.M.M.; Love, I. Estimation of panel vector autoregression in Stata. Stata J. 2016, 16, 778–804. [Google Scholar] [CrossRef]

- Pesaran, H.H.; Shin, Y. Generalized impulse response analysis in linear multivariate models. Econ. Lett. 1998, 58, 17–29. [Google Scholar] [CrossRef]

- Arellano, M.; Bond, S. Some Tests of Specification for Panel Data: Monte Carlo Evidence and an Application to Employment Equations. Rev. Econ. Stud. 1990, 58, 277–297. [Google Scholar] [CrossRef]

- Hwang, J.; Sun, Y. Testing for panel data unit roots in the presence of serially correlated errors: Finite sample results. J. Econ. 2018, 204, 29–46. [Google Scholar]

- Kripfganz, S. A Stata package for the linear GMM estimator for dynamic panel data models. Stata J. 2019, 19, 322–344. [Google Scholar]

- Obonyo, R.; The Push for Renewables: How Africa is Building a Different Energy Pathway. Countries Accelerate Use of Renewable Energy and Are Leading Energy Transition Efforts. United Nations—Africa Renewal. 2021. Available online: https://www.un.org/africarenewal/magazine/january-2021/push-renewables-how-africa-building-different-energy-pathway (accessed on 18 March 2023).

- Satti, S.L.; Farooq, A.; Loganathan, N.; Shahbaz, M. Empirical evidence on the resource curse hypothesis in oil abundant economy. Econ. Model. 2014, 42, 421–429. [Google Scholar] [CrossRef]

- Ozcan, B.; Ozturk, I. Renewable energy consumption-economic growth nexus in emerging countries: A bootstrap panel causality test. Renew. Sustain. Energy Rev. 2019, 104, 30–37. [Google Scholar] [CrossRef]

- Evans, O. The investment dynamics in renewable energy transition in Africa: The asymmetric role of oil prices, economic growth and ICT. Int. J. Energy Sect. Manag. 2023, 14, 8–21. [Google Scholar] [CrossRef]

- Evans, O. Information and communication technologies and economic development in Africa in the short and long run. Int. J. Technol. Manag. Sustain. Dev. 2019, 18, 127–146. [Google Scholar] [CrossRef]

- Kocaarslan, B.; Soytas, U. Asymmetric pass-through between oil prices and the stock prices of clean energy firms: New evidence from a nonlinear analysis. Energy Rep. 2019, 5, 117–125. [Google Scholar] [CrossRef]

- Shahbaz, M.; Zakaria, M.; Shahzad, S.J.H.; Mahalik, M.K. The energy consumption and economic growth nexus in top ten energy-consuming countries: Fresh evidence from using the quantile-on-quantile approach. Energy Econ. 2018, 71, 282–301. [Google Scholar] [CrossRef]

- Qadir, A.S.; Al-Motairi, H.; Tahir, F.; Al-Fagih, L. Incentives and strategies for financing the renewable energy transition: A review. Energy Rep. 2021, 7, 3590–3606. [Google Scholar] [CrossRef]

- Deka, A.; Cavusoglu, B. Examining the role of renewable energy on the foreign exchange rate of the OECD economies with dynamic panel GMM and Bayesian VAR model. SN Bus. Econ. 2022, 2, 119. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Author (s) | Country/Area | Period | Method | Results |

|---|---|---|---|---|

| Wang et al. (2020) [19] | G-20 | 1990–2017 | Cointegration | Oil price plays a positive role in promoting renewable energy. |

| Mukhtarov et al. (2020) [20] | Azerbaijan | 1992–2015 | STSM | A negative nexus exists between oil prices and REC. |

| Chen et al. (2021) [28] | 97 countries | 1995–2015 | Panel threshold model | Increases in real oil prices lead to increased REC in less democratic countries but there are no significant effects in more democratic countries. |

| Sahu et al. (2021) [26] | United States | 1970–2018 | NARDL | Increased oil prices lead to increased renewable energy in both the short and long term. |

| Murshed and Taha (2021) [25] | 4 Asia net oil-importing economies | 1990–2018 | Cross-sectional dependency | Oil price fluctuations influence movements in REC and in total final energy consumption and aggregate production. |

| Mukhtarov et al. (2021) [23] | Kazakhstan | 1992–2015 | FMOLS and CCR | Oil prices have negative effects on REC. |

| Guo et al. (2021) [24] | G-7 Countries | 1980–2018 | NARDL | There is positive and negative nexus between oil price and REC (heterogeneity between the countries). |

| Zhao and Wei (2021) [29] | China | 42 sectors in 2015 | CGE | Increasing oil prices can advance renewable energy investment. |

| Lin and Wang (2022) [30] | China | GMM | Oil price uncertainty will increase the market’s expectation of renewable enterprises and, thus, stimulate their investment. | |

| Rasheed et al. (2022) [21] | 30 European countries | 1997–2017 | FMOLS and the Driscoll–Kraay regression tests | Rise in oil prices increases the usage of renewable energy. |

| Royal et al. (2022) [31] | G 7 Countries | 1971–2019 | FMOLS and DOLS | Oil prices are one of the major drivers of REC in the long run. |

| Mukhatarov et al. (2022) [11] | Iran | 1980–2019 | GETS | Oil prices have a significant and negative impact on REC. |

| Escoffier et al. (2022) [32] | OECD and BRICS | 1997–2016 | PSTR model | Higher oil prices increase investment in renewable energy. |

| Husaini and Lean (2022) [33] | 8 Asian countries | 1980–2017 | Panel threshold regression | High oil prices increase public electricity generation. |

| Zaghdoudi et al. (2023) [34] | China | 1970–2019 | NARDL | Oil price fluctuations have significant effects on REC. |

| Kazemzadeh et al. (2023) [35] | 49 countries worldwide | 1985–2017 | Club convergence and PVAR | A granger causal relationship exists between GDP, REC, and oil price. |

| Deka et al. (2023) [36] | Brazil, China, Indonesia, India, Mexico, Rusia and Turkey | 1990–2019 | ARDL | GDP, interest rates, and renewable energy promote exchange rate appreciation. |

| Murshed (2023) [37] | 74 developing countries | 2000–2018 | DCCE-MG | Oil prices hike undermining macroeconomic factors and renewable electrification rate. |

| Olanipekun et al. (2023) [22] | Global analysis | 2004–2019 | Wavelet-coherence and quantile regression | Renewable energy use leads to a significant fall in geopolitical oil prices. |

| Tambari and Failler (2020) [38] | 6 African countries | 1990–2018 | VAR | Oil price has positive impact on investment in renewable energy. |

| Ali (2022) [39] | South Africa | 1990–2019 | ARDL and NARDL | Negative shocks in oil prices increase demands for RE. |

| Variable | Variable Description | Unit of Measurement | Expected Sign According to Economic Theory | Source of Data |

|---|---|---|---|---|

| Renewable energy generation | Renewable energy total generation from hydroelectricity, solar, wind, biomass and waste, hydroelectric pumped storage, non-hydroelectric renewables, geothermal, tides, and waves. | Per capita billions of kilowatt hours. | U.S. Energy Information Administration. http://www.eia.doe.gov/fuelrenewable.html (accessed on 15 March 2023) | |

| Oil prices | The nominal oil price series is the petroleum (Dubai, Brent, Nigerian, and West Texas Intermediate) average crude prices. | The real oil price is calculated from the nominal oil price which is deflated by the inherent consumer price index of the individual countries. USA dollars per barrel. | Positive/negative | The nominal oil price data is taken from the British Petroleum (BP) annual statistical review (1985, 1990, 1996, 2001, 2007, 2012, 2018, and 2022) report and the individual country consumer price index from the International Monetary Fund’s International Energy Agency, International Financial Statistics (IFS). |

| Per capita GDP | The real gross domestic product series is divided by population. | units: per caita US dollars at constant 2015 price; scale: billions. | positive | The United Nations economic database. http://unstats.un.org/unsd/snaama/Introduction.asp (accessed on 15 March 2023) |

| Interest rate | The real interest is defined as the lending interest rate adjusted for inflation. | Measured as a percentage by the GDP deflator. | negative | World Bank Development Indicator, and the IFS. |

| Exchange rate | International Monetary Fund exchange rate. | USD exchange rate against national currencies. | negative | The United Nations economic database. http://unstats.un.org/unsd/snaama/Introduction.asp (accessed on 15 March 2023) |

| (a) Group Descriptive Statistics (1990–2021) | |||||

|---|---|---|---|---|---|

| REI | OP | GDPC | INTR | EXCH | |

| Net oil-importing countries | |||||

| Mean | 1.66 × 10−7 | 0.635 | 1585.957 | 8.827 | 145.510 |

| Median | 1.15 × 10−7 | 0.642 | 575.110 | 8.369 | 21.218 |

| Maximum | 7.50 × 10−7 | 2.660 | 6259.064 | 29.583 | 1989.391 |

| Minimum | 3.43 × 10−9 | 0.107 | 203.864 | −17.122 | 2.39 × 10−9 |

| Std. Dev. | 1.91 × 10−7 | 0.329 | 1956.954 | 12.483 | 354.583 |

| Net oil-exporting countries | |||||

| Mean | 8.30 × 10−8 | 11,743,685.000 | 3618.246 | −2.828 | 74.097 |

| Median | 5.42 × 10−8 | 0.708 | 3153.474 | 1.606 | 39.294 |

| Maximum | 3.40 × 10−7 | 1.04 × 109 | 13,263.490 | 38.978 | 631.442 |

| Minimum | 9.24 × 10−10 | 0.109 | 1433.522 | −93.513 | 2.99 × 10−8 |

| Std. Dev. | 7.99 × 10−8 | 96,861,240.000 | 2026.834 | 22.992 | 103.631 |

| (b) The Average Values of Each Variable for the 10 Countries (1990–2021) | |||||

| REI | OP | GDPC | INTR | Exch | |

| Net oil-importing countries | |||||

| Congo | 1.21 × 10−7 | 0.530 | 461.678 | 22.994 | 603.667 |

| Ethiopia | 5.64 × 10−8 | 0.629 | 402.027 | −5.735 | 13.451 |

| Kenya | 1.38 × 10−7 | 0.777 | 1306.227 | 7.956 | 74.808 |

| Mozambique | 4.44 × 10−7 | 0.663 | 406.894 | 13.809 | 27.521 |

| South Africa | 6.91 × 10−8 | 0.575 | 5352.960 | 5.111 | 8.101 |

| Net oil-exporting countries | |||||

| Algeria | 9.18 × 10−9 | 0.582 | 3579.938 | 0.747 | 72.839 |

| Angola | 1.35 × 10−7 | 51,378,620.000 | 3172.026 | −21.229 | 105.908 |

| Egypt | 1.74 × 10−7 | 0.618 | 3580.606 | 3.826 | 6.776 |

| Libya | 1.20 × 10−9 | 0.453 | 10,624.700 | −1.843 | 1.069 |

| Nigeria | 4.48 × 10−8 | 1.379 | 2008.383 | 3.138 | 138.052 |

| Net Oil-Importing Countries | ||||

|---|---|---|---|---|

| LLC | IPS | |||

| Level | First Difference | Level | First Difference | |

| log_rei | −1.224 * | −8.766 *** | −1.727 ** | −7.480 *** |

| log_op | −0.628 | −3.462 *** | −0.378 | −8.079 *** |

| log_gdpc | −0.654 | −8.297 *** | −1.472 * | −9.501 *** |

| Intr | −4.031 *** | −9.408 *** | −3.522 *** | −8.012 *** |

| Exch | −0.139 | −8.455 *** | −0.940 | −9.247 *** |

| Net oil-exporting countries | ||||

| log_rei | −1.395 * | −3.621 *** | −1.391 * | −8.630 *** |

| log_op | −0.266 | −8.710 *** | −0.284 | −6.035 *** |

| log_gdpc | −0.125 | −3.269 *** | −0.806 | −8.514 *** |

| Intr | −3.900 *** | −6.401 *** | −3.990 *** | −7.352 *** |

| Exch | −0.528 | −7.811 *** | −0.672 | −9.348 *** |

| Net Oil-Importing Countries | Net Oil-Exporting Countries | ||||

|---|---|---|---|---|---|

| Statistic | Weighted Statistic | Statistic | Weighted Statistic | ||

| within-dimension | Panel v-Statistic | −1.011 | −1.797 | −2.150 | −2.322 |

| Panel rho-Statistic | −4.753 *** | −4.528 *** | −2.696 *** | −1.038 | |

| Panel PP-Statistic | −12.784 *** | −10.257 *** | −14.366 *** | −7.271 *** | |

| Panel ADF-Statistic | −3.192 *** | −3.589 *** | −6.975 *** | −3.588 *** | |

| between-dimension | Group rho-Statistic | −2.740 *** | −0.698 | ||

| Group PP-Statistic | −10.726 *** | −12.288 *** | |||

| Group ADF-Statistic | −3.429 *** | −4.386 *** | |||

| Net Oil-Exporting Countries | ||||||

|---|---|---|---|---|---|---|

| Lag | LogL | LR | FPE | AIC | SC | HQ |

| 0 | −732.110 | NA | 5.400 | 26.742 | 26.872 | 26.795 |

| 1 | −722.059 | 1146.894 | 2.087 * | 14.802 * | 15.822 * | 15.357 * |

| 2 | −695.700 | 46.921 | 2.291 | 15.014 | 16.447 | 15.594 |

| 3 | −674.321 | 35.916 | 2.487 | 15.086 | 17.171 | 15.930 |

| Net Oil-Importing Countries | ||||||

| Lag | LogL | LR | FPE | AIC | SC | HQ |

| 0 | −780.766 | NA | 2.215 | 29.763 | 29.879 | 29.810 |

| 1 | −773.814 | 1913.209 | 0.420 * | 13.397 | 14.093 * | 13.679 * |

| 2 | −751.822 | 39.953 | 0.477 | 13.447 | 14.725 | 13.966 |

| 3 | −718.858 | 57.138 | 0.509 | 13.314 * | 15.173 | 14.069 |

| Net Oil-Importing Countries | Net Oil-Exporting Countries | |||

|---|---|---|---|---|

| Estimates | Std. Error | Estimates | Std. Error | |

| dlog_rei(−1) | 0.181 ** | 0.081 | 0.256 *** | 0.084 |

| dlog_op(−1) | 0.203 * | 0.114 | −0.058 | 0.065 |

| dlog_gdpc(−1) | 1.393 * | 0.710 | 0.044 * | 0.025 |

| d_intr(−1) | −0.057 * | 0.004 | 0.003 * | 0.002 |

| d_exch(−1) | −0.015 ** | 0.007 | 0.056 *** | 0.010 |

| c | 0.080 *** | 0.032 | 0.064 ** | 0.032 |

| ECM | −0.019 *** | 0.005 | −0.043 *** | 0.009 |

| Adjusted R-squared | 0.858 | 0.774 | ||

| F-statistic | 147.878 *** | 172.211 *** | ||

| VEC Residual Serial Correlation LM Tests | 69.521 [0.532] | 77.098 [0.309] | ||

| VEC Residual Heteroskedasticity Tests | 117.290 [0.551] | 426.387 [0.226} | ||

| (a) Net Oil-Importing Countries | ||||||

|---|---|---|---|---|---|---|

| Period | S.E. | LOG_REI | LOG_OP | LOG_GDPC | INTR | EXCH |

| 1 | 0.349 | 100.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| 5 | 0.699 | 96.352 | 0.219 | 3.148 | 0.064 | 0.217 |

| 10 | 0.979 | 95.186 | 0.309 | 4.193 | 0.038 | 0.275 |

| 15 | 1.195 | 94.746 | 0.354 | 4.576 | 0.032 | 0.293 |

| 20 | 1.378 | 94.512 | 0.381 | 4.775 | 0.030 | 0.303 |

| (b) Net Oil-Exporting Countries | ||||||

| Period | S.E. | LOG_REI | LOG_OP | LOG_GDPC | INTR | EXCH |

| 1 | 0.305 | 100.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| 5 | 0.568 | 98.984 | 0.211 | 0.006 | 0.703 | 0.096 |

| 10 | 0.785 | 98.796 | 0.150 | 0.009 | 0.937 | 0.108 |

| 15 | 0.954 | 98.698 | 0.116 | 0.010 | 1.061 | 0.114 |

| 20 | 1.098 | 98.637 | 0.096 | 0.011 | 1.138 | 0.118 |

| Net Oil-Importing Countries | Net Oil-Exporting Countries | |

|---|---|---|

| Log-rei | 0.395 *** (0.018) | 0.482 *** (0.012) |

| Log_op | 0.015 *** (0.004) | 0.018 (0.014) |

| Log_gdpc | 0.058 ** (0.027) | 0.079 ** (0.038) |

| Intr | −0.023 * (0.012) | 0.003 (0.002) |

| Exch | −0.059 *** (0.018) | 0.092 *** (0.027) |

| C | −0.261 *** (0.015) | 0.182 *** (0.017) |

| Arellano–Bond test for AR(1) | −1.664 [0.095] | −1.116 [0.262] |

| Arellano–Bond test for AR(2) | −0.565 [0.573] | −0.482 [0.631] |

| Hansen J-test | 27.793 [0.248] | 30.187 [0.159] |

| Net Oil-Importing Countries | |||||

|---|---|---|---|---|---|

| Congo | Ethiopia | Kenya | Mozambique | South Africa | |

| dlog_rei(−1) | 0.511 *** | 0.245 *** | 0.190 *** | 0.428 *** | 0.382 *** |

| dlog_op(−1) | 0.092 ** | 0.082 ** | 0.038 * | 0.087 ** | 0.093 ** |

| dlog_gdpc(−1) | 0.088 ** | 0.079 ** | 0.012 * | 0.019 * | 0.065 ** |

| d_intr(−1) | −0.043 | −0.074 ** | −0.045 * | 0.004 | −0.021 * |

| d_exch(−1) | −0.013 * | −0.068 ** | −0.077 ** | −0.053 *** | −0.064 ** |

| c | −0.418 *** | −0.396 * | 0.878 *** | 0.739 ** | 0.277 * |

| Ecm | −0.081 *** | −0.029 *** | −0.007 * | −0.036 ** | −0.096 *** |

| Adjusted R-squared | 0.836 | 0.763 | 0.962 | 0.868 | 0.794 |

| F-statistic | 142.995 *** | 256.793 *** | 377.808 *** | 175.973 *** | 278.161 *** |

| Net Oil-Exporting Countries | |||||

| Algeria | Angola | Egypt | Libya | Nigeria | |

| dlog_rei(−1) | 0.855 *** | 0.130 *** | 0.224 *** | 0.212 *** | 0.663 *** |

| dlog_op(−1) | −0.032 | 0.076 *** | −0.070 | −0.056 | −0.025 |

| dlog_gdpc(−1) | 0.039 * | 0.044 * | 0.006 * | 0.029 * | 0.058 * |

| d_intr(−1) | 0.004 | 0.013 * | 0.008 * | 0.016 * | 0.024 * |

| d_exch(−1) | 0.055 ** | −0.021 * | 0.033 * | 0.072 *** | 0.049 * |

| c | 0.965 *** | 0.769 ** | 0.972 *** | 0.650 ** | 0.704 ** |

| Ecm | −0.078 *** | −0.047 ** | −0.059 *** | −0.038 * | −0.024 * |

| Adjusted R-squared | 0.764 | 0.922 | 0.735 | 0.863 | 0.895 |

| F-statistic | 278.161 *** | 108.548 *** | 176.044 *** | 324.915 *** | 385.711 *** |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tambari, I.J.T.; Failler, P.; Jaffry, S. The Differential Effects of Oil Prices on the Development of Renewable Energy in Oil-Importing and Oil-Exporting Countries in Africa. Energies 2023, 16, 3803. https://doi.org/10.3390/en16093803

Tambari IJT, Failler P, Jaffry S. The Differential Effects of Oil Prices on the Development of Renewable Energy in Oil-Importing and Oil-Exporting Countries in Africa. Energies. 2023; 16(9):3803. https://doi.org/10.3390/en16093803

Chicago/Turabian StyleTambari, Ishaya Jonah Tegina, Pierre Failler, and Shabbar Jaffry. 2023. "The Differential Effects of Oil Prices on the Development of Renewable Energy in Oil-Importing and Oil-Exporting Countries in Africa" Energies 16, no. 9: 3803. https://doi.org/10.3390/en16093803

APA StyleTambari, I. J. T., Failler, P., & Jaffry, S. (2023). The Differential Effects of Oil Prices on the Development of Renewable Energy in Oil-Importing and Oil-Exporting Countries in Africa. Energies, 16(9), 3803. https://doi.org/10.3390/en16093803