Estimation of Tax Expenditures Stimulating the Energy Sector Development and the Use of Alternative Energy Sources in OECD Countries

, ,

, ,

Abstract

1. Introduction

2. Literature Review

2.1. Theoretical Background

2.2. Empirical Literature

3. Materials and Methods

3.1. Data

3.2. Methodology

4. Results

5. Discussion

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Tax Expenditures: Current Issues and Five-Year Budget Projections for Fiscal Years 1984–1988. The Congress of the United States. Congressional Budget Office; 25 October 1983. Available online: https://www.cbo.gov/sites/default/files/98th-congress-1983-1984/reports/doc26a.pdf (accessed on 15 January 2023).

- Surrey, S.S.; McDaniel, P.R. The Tax Expenditure Concept: Current Developments and Emerging Issues. Boston Coll. Law Rev. 1979, 20, 225. Available online: https://www.semanticscholar.org/paper/The-Tax-Expenditure-Concept%3A-Current-Developments-Surrey-McDaniel/528ac53eaac085edb9761c0475569b4290d6ffab (accessed on 9 January 2023).

- Thuronyi, V. Tax Expenditures: A Reassessment. Duke Law J. 1988, 37, 1182. Available online: https://scholarship.law.duke.edu/cgi/viewcontent.cgi?article=3057&context=dlj (accessed on 10 January 2023). [CrossRef]

- Tyson, J. Reforming Tax Expenditures in Italy: What, Why, and How? IMF Work. 2014, 14, 4. Available online: http://reforming.it/doc/635/taxexpenditureinitaly.pdf (accessed on 15 January 2023). [CrossRef]

- Best Practice Guidelines—Off Budget and Tax Expenditures. OECD J. Budg. 2004, 4, 121–142.

- Sokolovska, A.; Zatonatska, T. Debatable aspects of the concept of tax expenditures. Ekonomika 2022, 101, 109–124. [Google Scholar] [CrossRef]

- Grisolia, G.; Fino, D.; Lusia, U. Biomethanation of rice straw: A Sustainable perspective for the valorisation of a field residue in the energy sector. Sustainability 2022, 14, 5679. [Google Scholar] [CrossRef]

- Demidova, S.; Balog, M.; Chircova, T.; Kulachinskaya, A.; Zueva, S.; Akhmetova, I.; Ilyashenko, S. Development of methodology and assessment of ecological safety of the EAEU and CIS regions in the context of sustainable development. Economies 2021, 9, 100. [Google Scholar] [CrossRef]

- Villela, L.A. Tax Expenditures Budgets: Concepts and Challenges for Implementation; IDB Working Paper Series: 131. HJ4642.V55; Inter-American Development Bank: Washington, DC, USA, 2021. [Google Scholar]

- Bertrand, L.; Caldeira, E.; Quatrebarbes, C.; Bouterige, Y. Tax Expenditure Assessment: From Principles to Practice Methodological Guide; under the supervision of Anne-Marie Geourjon; Fondation pour les Études et Recherches sur le Développement International (Ferdi): Clermont-Ferrand, France, 2018; ISBN 978-2-9550779-5-5. [Google Scholar]

- Barrios, S.; Figari, F.; Gandullia, L.; Riscado, S. The Fiscal and Equity Impact of Tax Expenditures in the EU. JRC Working Papers on Taxation and Structural Reforms. 2016. Available online: https://joint-research-centre.ec.europa.eu/system/files/2016-12/jrc104176.pdf (accessed on 10 January 2023).

- Kakaulina, M.O.; Gorlov, D.R. Assessment of the impact of tax incentives on investment activity in special economic zones of the Russian Federation. J. Appl. Econ. Res. 2021, 21, 282–324. [Google Scholar] [CrossRef]

- Mosquera, I.; Lesage, D.; Lips, W. Taxation, International Cooperation and the 2030 Sustainable Development Agenda; Springer International Publishing: Cham, Switzerland, 2021; pp. 173–193. ISBN 978-3-030-64857-2. [Google Scholar] [CrossRef]

- Haldenwang, C.; Redonda, A. Tax Expenditures: The Hidden Side of Government Spending, VoxEU.org—CEPR’s Policy Portal. 2021. Available online: https://cepr.org/voxeu/columns/tax-expenditures-hidden-side-government-spending (accessed on 28 January 2023).

- Redonda, A.; Sarralde, S.; Hallerberg, M.; Johnson, L.; Melamud, A.; Rozemberg, R.; Schwab, J.; Haldenwang, C. Tax expenditure and the treatment of tax incentives for investment. Economics: The Open-Access. Open-Assess. E-J. 2019, 13, 1–11. [Google Scholar] [CrossRef]

- Beer, S.; Benedek, D.; Erard, B.; Loeprick, J. How to Evaluate Tax Expenditures; How to Note (International Monetary Fund); International Monetary Fund: Washington, DC, USA, 2022; Available online: https://www.imf.org/en/Publications/Fiscal-Affairs-Department-How-To-Notes/Issues/2022/11/How-to-Evaluate-Tax-Expenditures-525166 (accessed on 10 January 2023).

- Fedorova, E.; Lapshina, N.; Borodin, A.; Lazarev, M. Impact of information in press releases on the financial performance of Russian companies. Ekon. Polit. 2021, 3, 138–157. [Google Scholar] [CrossRef]

- Inventory of Estimated Budgetary Support and Tax Expenditures for Fossil Fuels; OECD Publishing: Paris, France, 2011; Available online: https://www.oecd.org/fossil-fuels/48805150.pdf (accessed on 9 January 2023).

- Zehir, C.; Zehir, M.; Borodin, A.; Mamedov, Z.F.; Qurbanov, S. Tailored Blockchain Applications for the Natural Gas Industry: The Case Study of SOCAR. Energies 2022, 15, 6010. [Google Scholar] [CrossRef]

- Borodin, A.; Zaitsev, V.; Mamedov, Z.F.; Panaedova, G.; Kulikov, A. Mechanisms for Tax Regulation of CO2-Equivalent Emissions. Energies 2022, 15, 7111. [Google Scholar] [CrossRef]

- Crippa, M.; Guizzardi, D.; Banja, M.; Solazzo, E.; Muntean, M.; Schaaf, E.; Pagani, F.; Monforti-Ferrario, F.; Olivier, J.; Quadrelli, R.; et al. CO2 Emissions of all World Countries; EUR 31182 EN; Publications Office of the European Union: Luxembourg, 2022. [Google Scholar] [CrossRef]

- Benzarti, Y.; Carloni, D. Who really benefits from consumption tax cuts? Evidence from a large VAT reform in France. Am. Econ. J. Econ. Policy 2019, 11, 38–63. [Google Scholar] [CrossRef]

- Kronfol, H.; Steenbergen, V. Evaluating the Costs and Benefits of Corporate Tax Incentives. Methodological Approaches and Policy Considerations; World Bank: Washington, DC, USA, 2020; Available online: http://documents1.worldbank.org/curated/en/180341583476704729/pdf/Evaluating-the-Costs-and-Benefits-of-Corporate-Tax-Incentives-Methodological-Approaches-and-Policy-Considerations.pdf (accessed on 29 December 2022).

- Shedding Light on Worldwide Tax Expenditures. GTED Flagship Report. 2021. Available online: http://www.GTED.net (accessed on 9 January 2023).

- Ziyadin, S.; Streltsova, E.; Borodin, A.I.; Kiseleva, N.; Yakovenko, I.; Baimukhanbetova, E. Assessment of Investment Attractiveness of Projects on the Basis of Environmental Factors. Sustainability 2019, 11, 2544. [Google Scholar] [CrossRef]

- Energy Efficiency Trends and Policies in Austria; Austrian Energy Agency: Vienna, Austria, 2021; Available online: https://www.odyssee-mure.eu/publications/national-reports/energy-efficiency-austria.pdf (accessed on 15 January 2023).

- Renewable Energy Sources as a New Development Step for Oil and Gas Companies. 2019. Available online: www.assets.kpmg/content/dam/kpmg/ru/pdf/2019/12/ru-ru-renewable-energy-sources-for-oil-and-gas.pdf (accessed on 20 December 2022).

- Makarova, A.A.; Mitrova, T.A.; Kulagina, V.A. (Eds.) Forecast for the Development of Energy in the World and Russia 2019; M.: ERI RAS—Moscow School of Management SKOLKOVO: Moscow, Russia, 2019; 210p, ISBN 978-5-91438-029-5. [Google Scholar]

- Gole, I.; Dumitrache, V.-M.; Bălu, F.O. Assessment of a decade of greenhouse gas emissions. In Proceedings of the International Conference on Economics and Social Sciences, Bucharest, Romania, 2020; Springer: Berlin/Heidelberg, Germany, 2020; pp. 332–340. [Google Scholar] [CrossRef]

- Kotlikoff, L.; Polbin, A.; Zubarev, A. Will Paris accord accelerate climate change? Econ. Policy 2021, 16, 8–37. [Google Scholar]

- Valko, D. Impact of renewable energy and tax regulation on reducing greenhouse gas emissions in OECD Countries: CS-ARDL Approach. Econ. Policy 2021, 16, 40–61. (In Russian) [Google Scholar] [CrossRef]

- Stepanov, I.A. Energy taxes and their contribution to greenhouse gas emissions reduction. HSE Econ. J. 2022, 23, 290–313. [Google Scholar] [CrossRef]

- Golovanova, A.E.; Polaeva, G.B.; Nurmatova, E.A. European Union energy policy in renewable energy. Innov. Investig. 2018, 11, 52–55. (In Russian) [Google Scholar]

- Kilsedar, C.; Patani, S.; Olsson, M.; Girardi, J.; Mubareka, S. EU Bioeconomy Monitoring System Dashboards: Extended with Trade-Related Indicators; Publications Office of the European Union: Luxembourg, 2022; ISBN 978-92-76-61625-2. [Google Scholar] [CrossRef]

- A European Green Deal. Available online: https://commission.europa.eu/strategy-and-policy/priorities-2019-2024/european-green-deal_en#actions (accessed on 12 November 2022).

- Statistical Pocketbook 2022. Available online: https://op.europa.eu/en/publication-detail/-/publication/7d9ae428-3ae8-11ed-9c68-01aa75ed71a1/language-en/format-PDF/source-279588540 (accessed on 15 January 2023).

- OECD Investment Tax Incentives Database—2022 Update: Tax Incentives for Sustainable Development (Brochure); OECD Publishing: Paris, France, 2022; Available online: www.oecd.org/investment/investment-policy/oecd-investment-tax-incentives-database-2022-update-brochure.pdf (accessed on 22 January 2023).

- Steshenko, J.A.; Tikhonova, A.V. An integral approach to evaluating the effectiveness of tax incentives. J. Tax Reform 2018, 4, 157–173. [Google Scholar] [CrossRef]

- Mamedov, Z.F.; Qurbanov, S.H.; Streltsova, E.; Borodin, A.; Yakovenko, I.; Aliev, A. Mathematical models for assessing the investment attractiveness of oil companies. SOCAR Proc. 2021, 4, 102–114. [Google Scholar] [CrossRef]

- Country Profile—Sweden. European Environment Agency (Energy Support 2005–2012). Available online: https://webcache.googleusercontent.com/search?q=cache:GLvkJyidDjkJ:https://www.eea.europa.eu/publications/energy-support-measures/sweden-country-profile&cd=10&hl=ru&ct=clnk&gl=ru&client=safari (accessed on 15 January 2023).

- Bashir, M.F.; Benjiang, M.A.; Bashir, M.A.; Radulescu, M.; Shahza, U. Investigating the role of environmental taxes and regulations for renewable energy consumption: Evidence from developed economies. Econ. Res.-Ekon. Istrazĭvanja 2022, 35, 1262–1284. [Google Scholar] [CrossRef]

- Ministry of Finance of the Russian Federation. The Main Directions of the Bbudget, Tax and Customs Tariff Policy for 2019 and the Planning Period of 2020 and 2021. Annex 1—Tax Expenditures of the Russian Federation 2015–2021. (In Russisan). Available online: https://minfin.gov.ru/ru/perfomance/budget/policy/osnov?id_65=124752-osnovnye_napravleniya_byudzhetnoi_nalogovoi_i_tamozhenno-tarifnoi_politiki_na_2019_god_i_na_planovyi_period_2020_i_2021_godov (accessed on 10 January 2023).

- Report of the Working Group on Energy Taxation Reform: A Proposal for Implementing the Intentions and Goals of the Government Program and for Further Development of Energy Taxation; VN/11347/2019; Publications of the Ministry of Finance: Helsinki, Finland, 2021; ISBN 978-952-367-508-7. Available online: http://urn.fi/URN:ISBN:978-952-367-508-7 (accessed on 10 January 2023).

- South Korea. Survey of Global Investment and Innovation Incentive. 2020. Available online: https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Tax/dttl-tax-survey-of-global-investment-and-innovation-incentives-southkorea-2020.pdf (accessed on 10 February 2023).

- Holmberg, R. How Are the Swedish Taxes on Energy and Carbon Dioxide Related to Energy Efficiency? Odyssee-Mure Project. 2020. Available online: https://www.odyssee-mure.eu/publications/policy-brief/swedish-taxes-energy-carbon.pdf (accessed on 10 January 2023).

- Ptak, M. Incentives to Promote the Development of Renewable Energy in Poland. Economic and Environmental Studies (E&ES). Econ. Environ. Stud. 2014, 14, 427–439. Available online: https://www.econstor.eu/bitstream/10419/178869/1/ees_14_4_05.pdf (accessed on 14 January 2023).

- Lusia, U.; Fino, D.; Grisolia, G. A thermo-economic indicator for the sustainable development with social considerations: A thermo-economy for sustainable society. Environ. Dev. Sustain. 2021, 24, 2022–2036. [Google Scholar] [CrossRef]

- Bressan, M.; Campagnoli, E.; Ferro, C.G.; Giaretto, V. Rice straw: A waste with a remarkable green energy potential. Energies 2022, 15, 1355. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Year | Austria | India | Spain | South Korea | Russia | France | Sweden |

|---|---|---|---|---|---|---|---|

| % of GDP | |||||||

| 2018 | 0.04 | 0.07 | 0.002 | 0.01 | 0.1 | 0.01 | 0.005 |

| 2019 | 0.04 | 0.08 | 0.002 | 0.01 | 0.1 | 0.01 | 0.005 |

| 2020 | 0.04 | 0.09 | 0.002 | 0.01 | 0.13 | 0.01 | 0.005 |

| % of tax revenues of the consolidated budget | |||||||

| 2018 | 0.14 | 0.59 | 0.01 | 0.02 | 0.52 | 0.1 | 0.02 |

| 2019 | 0.13 | 0.6 | 0.01 | 0.02 | 0.94 | 0.1 | 0.01 |

| 2020 | 0.12 | 0.6 | 0.01 | 0.02 | 1.1 | 0.1 | 0.01 |

| Country | Year | Tax Expenditures Related to Increased Use of Renewable Energy Sources | Tax Expenditures Related to Energy Efficiency Improvements | ||

|---|---|---|---|---|---|

| % of GDP | % of Tax Revenues of the Consolidated Budget | % of GDP | % of Tax Revenues of the Consolidated Budget | ||

| Germany | 2018 | 0.01 | 0.05 | - | - |

| 2019 | 0.01 | 0.13 | - | - | |

| 2020 | 0.03 | 0.15 | - | - | |

| Denmark | 2018 | 0.25 | 0.77 | - | - |

| 2019 | 0.24 | 0.72 | - | - | |

| 2020 | 0.25 | 0.7 | - | - | |

| Ireland | 2018 | - | - | 0.001 | 0.01 |

| 2019 | - | - | 0.001 | 0.01 | |

| 2020 | - | - | 0.001 | 0.01 | |

| Spain | 2018 | - | - | 0.02 | 0.1 |

| 2019 | - | - | 0.02 | 0.1 | |

| 2020 | - | - | 0.01 | 0.07 | |

| Italy | 2018 | 0.0027 | 0.01 | - | - |

| 2019 | 0.003 | 0.013 | - | - | |

| 2020 | 0.0036 | 0.016 | - | - | |

| Netherlands | 2018 | 0.03 | 0.12 | 0.03 | 0.14 |

| 2019 | 0.03 | 0.13 | 0.03 | 0.11 | |

| 2020 | 0.04 | 0.15 | 0.03 | 0.1 | |

| Mexico | 2018 | 0.012 | 0.1 | - | - |

| 2019 | 0.02 | 0.12 | - | - | |

| 2020 | 0.025 | 0.14 | - | - | |

| Poland | 2018 | 0.01 | 0.07 | - | - |

| 2019 | 0.015 | 0.09 | - | - | |

| 2020 | 0.015 | 0.1 | - | - | |

| South Korea | 2018 | 0.004 | 0.02 | 0.01 | 0.05 |

| 2019 | 0.004 | 0.02 | 0.01 | 0.08 | |

| 2020 | 0.004 | 0.02 | 0.01 | 0.1 | |

| Finland | 2018 | 0.01 | 0.01 | 0.33 | 1.58 |

| 2019 | 0.01 | 0.02 | 0.3 | 1.46 | |

| 2020 | 0.01 | 0.02 | 0.29 | 1.41 | |

| France | 2018 | 0.01 | 0.02 | 0.09 | 0.51 |

| 2019 | 0.01 | 0.02 | 0.05 | 0.3 | |

| 2020 | 0.01 | 0.02 | 0.05 | 0.3 | |

| Sweden | 2018 | - | - | 0.16 | 0.68 |

| 2019 | - | - | 0.23 | 1.04 | |

| 2020 | - | - | 0.25 | 1.1 | |

| Country | Tax Expenditures Related to Increased Use of Renewable Energy | Tax Expenditures Related to Energy Efficiency Improvements | ||

|---|---|---|---|---|

| % | Ranking | % | Ranking | |

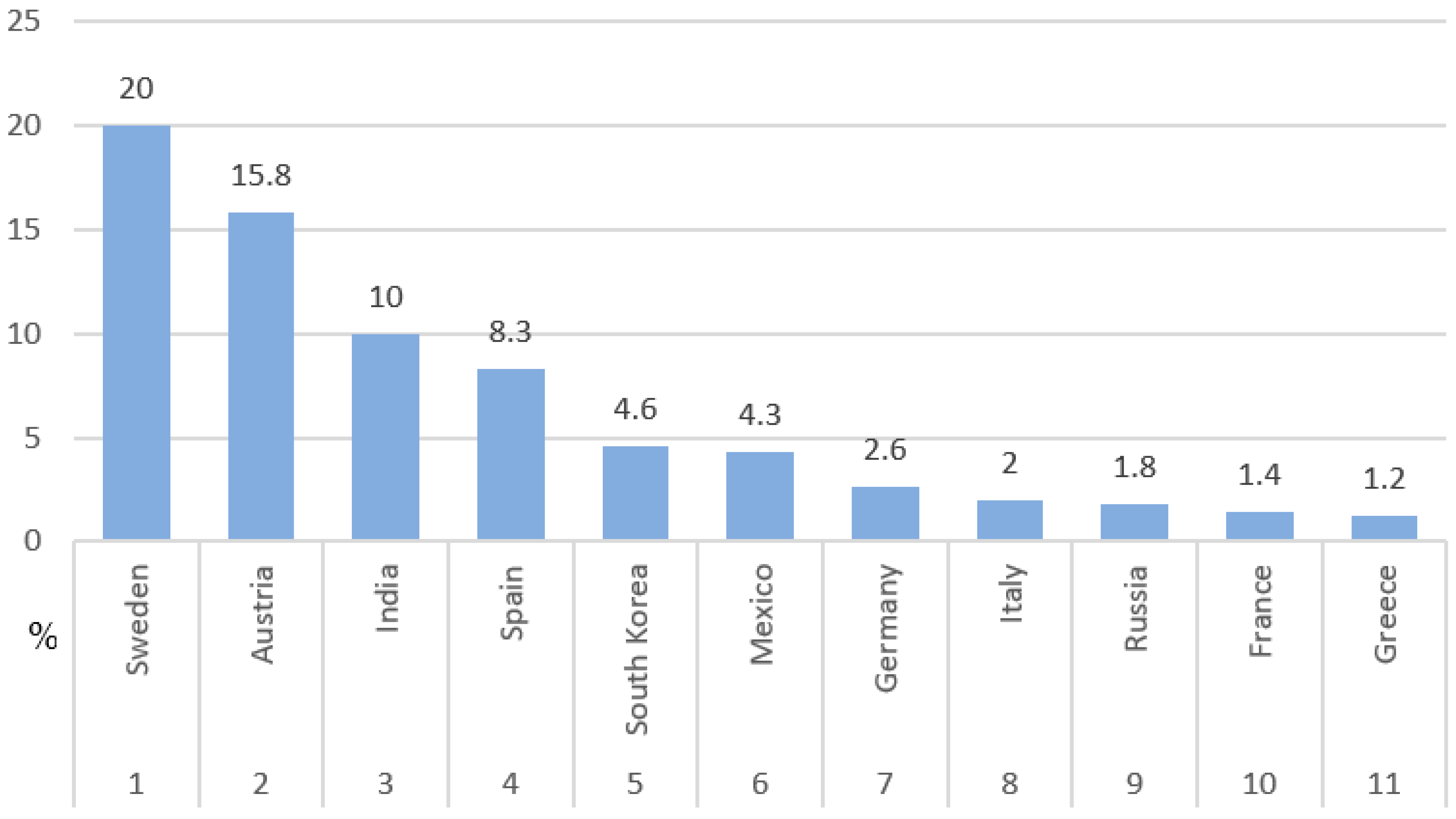

| Poland | 83.3 | 1 | - | - |

| Germany | 38.1 | 2 | 9.5 | 9 |

| Sweden | 33.3 | 3 | 33.3 | 4 |

| Italy | 33.3 | 3 | 16.7 | 6 |

| Denmark | 30 | 4 | 10 | 8 |

| Finland | 28.6 | 5 | 42.9 | 3 |

| Mexico | 25 | 6 | - | - |

| Netherlands | 19.4 | 7 | 8.3 | 10 |

| South Korea | 17.6 | 8 | 52.9 | 1 |

| France | 17.6 | 8 | 26.5 | 5 |

| Latvia | 4.3 | 9 | - | - |

| Ireland | - | - | 50 | 2 |

| Spain | - | - | 33.3 | 4 |

| Russia | - | - | 12.5 | 7 |

| Level of tax expenditures for energy efficiency (b) | high | Finland (+/−) | |||

| average | Sweden (+) | France (c/−) | |||

| low | Spain (−) Ireland (c) | South Korea (c/+) | Netherlands (+/−) | ||

| na | Italy (+) | Germany (+) Poland (+) Mexico (+) | Denmark (−) | ||

| na | low | average | high | ||

| Level of tax expenditures for increasing renewable energy (a) | |||||

| Country | Tax Expenditures Stimulating the Energy Sector Development | Tax Expenditures Related to Increased Use of Renewable Energy Sources | Tax Expenditures Related to Energy Efficiency Improvements | Number of Indicators | Integrated Indicator Reflecting Rating (Multivariate Average) | |||

|---|---|---|---|---|---|---|---|---|

| % of GDP | % of Tax Revenue | % of GDP | % of Tax Revenue | % of GDP | % of Tax Revenue | |||

| Spain | 0.002 | 0.01 | - | - | 0.01 | 0.07 | 4 | 0.2030 |

| South Korea | 0.01 | 0.02 | 0.004 | 0.02 | 0.01 | 0.1 | 6 | 0.4954 |

| France | 0.01 | 0.1 | 0.01 | 0.02 | 0.05 | 0.3 | 6 | 1.0663 |

| Sweden | 0.005 | 0.01 | - | - | 0.25 | 1.1 | 4 | 1.3783 |

| Netherlands | - | - | 0.04 | 0.15 | 0.03 | 0.1 | 4 | 1.4583 |

| Finland | - | - | 0.01 | 0.02 | 0.29 | 1.41 | 4 | 1.6179 |

| Average value | 0.0068 | 0.0350 | 0.0160 | 0.0525 | 0.1067 | 0.5133 | - | - |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tyurina, Y.; Frumina, S.; Demidova, S.; Kairbekuly, A.; Kakaulina, M. Estimation of Tax Expenditures Stimulating the Energy Sector Development and the Use of Alternative Energy Sources in OECD Countries. Energies 2023, 16, 2652. https://doi.org/10.3390/en16062652

Tyurina Y, Frumina S, Demidova S, Kairbekuly A, Kakaulina M. Estimation of Tax Expenditures Stimulating the Energy Sector Development and the Use of Alternative Energy Sources in OECD Countries. Energies. 2023; 16(6):2652. https://doi.org/10.3390/en16062652

Chicago/Turabian StyleTyurina, Yuliya, Svetlana Frumina, Svetlana Demidova, Aidyn Kairbekuly, and Maria Kakaulina. 2023. "Estimation of Tax Expenditures Stimulating the Energy Sector Development and the Use of Alternative Energy Sources in OECD Countries" Energies 16, no. 6: 2652. https://doi.org/10.3390/en16062652

APA StyleTyurina, Y., Frumina, S., Demidova, S., Kairbekuly, A., & Kakaulina, M. (2023). Estimation of Tax Expenditures Stimulating the Energy Sector Development and the Use of Alternative Energy Sources in OECD Countries. Energies, 16(6), 2652. https://doi.org/10.3390/en16062652