Risk Dependence and Risk Spillovers Effect from Crude Oil on the Chinese Stock Market and Gold Market: Implications on Portfolio Management

Abstract

1. Introduction

2. Literature Review

3. Econometric Modeling Framework

3.1. The Marginal Distribution and Copula Models

3.2. Risk Spillover Effects

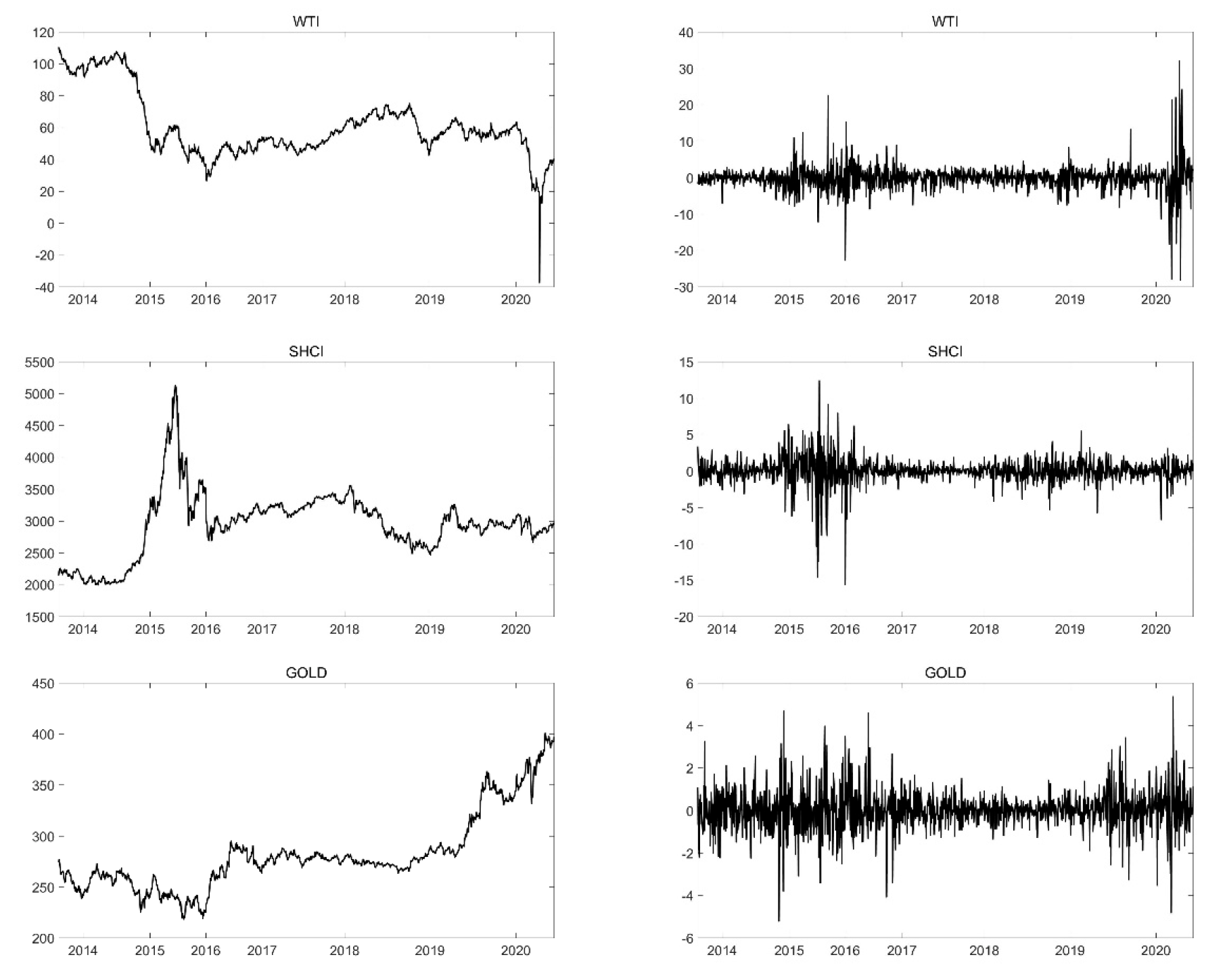

4. Data and Summary Statistics

5. Empirical Analysis

5.1. Marginal Model Analysis

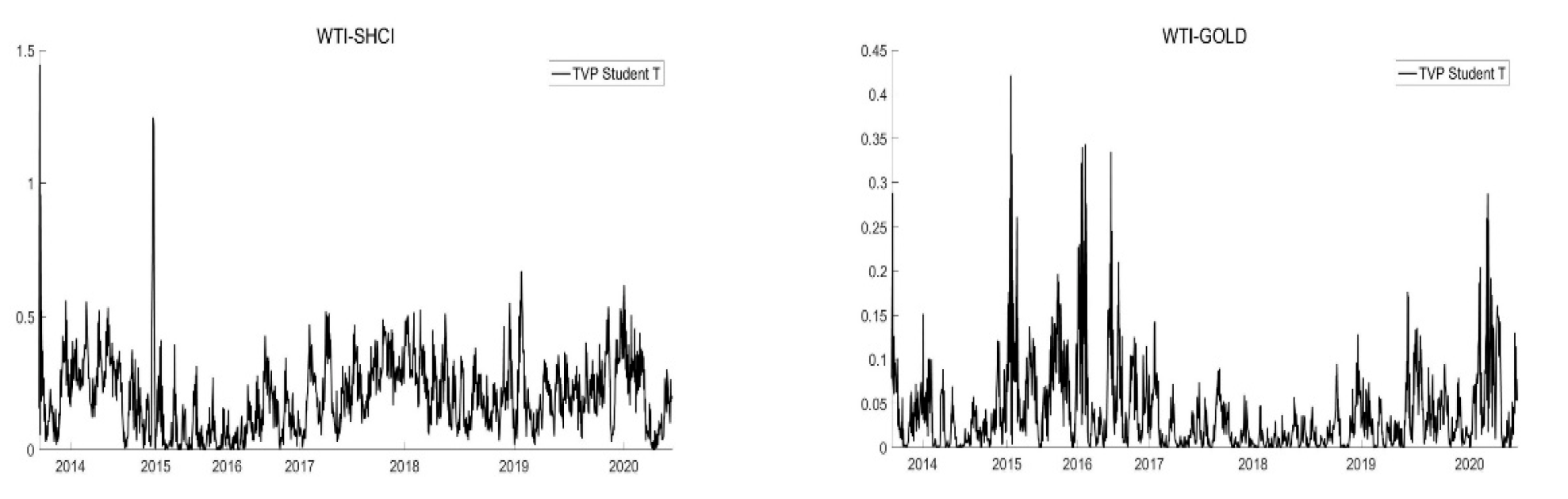

5.2. Copula Model Results

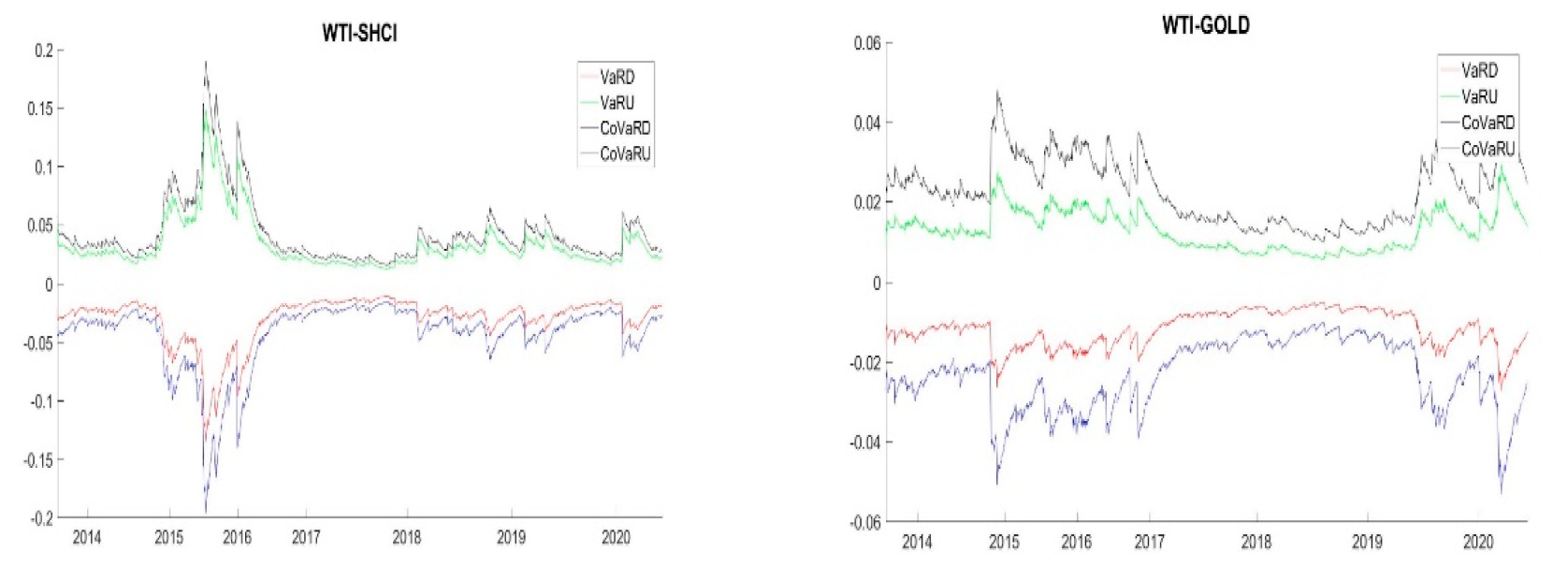

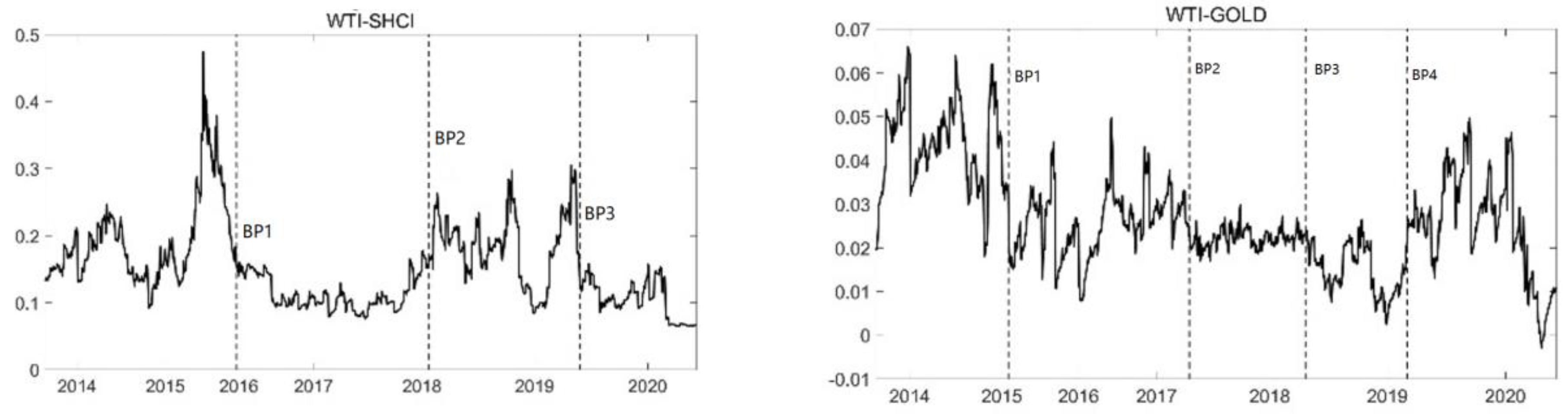

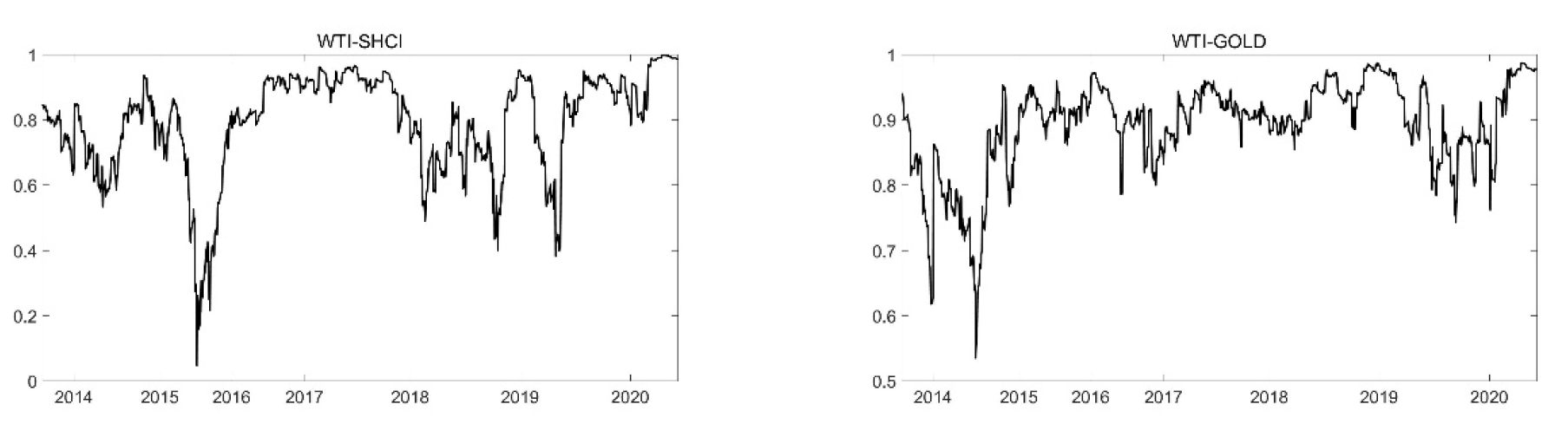

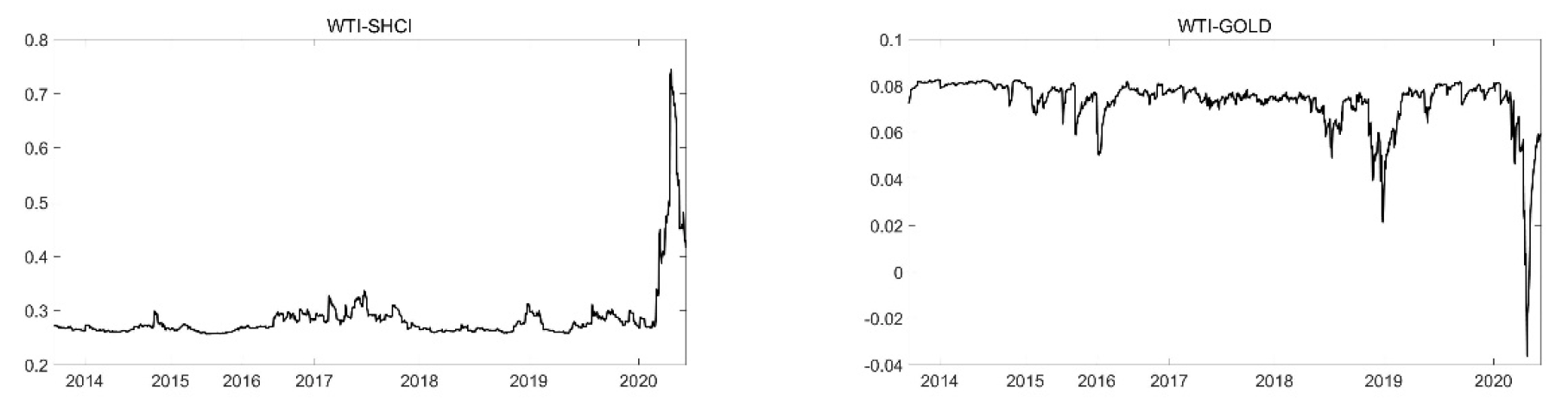

5.3. Spillover Effect Analysis

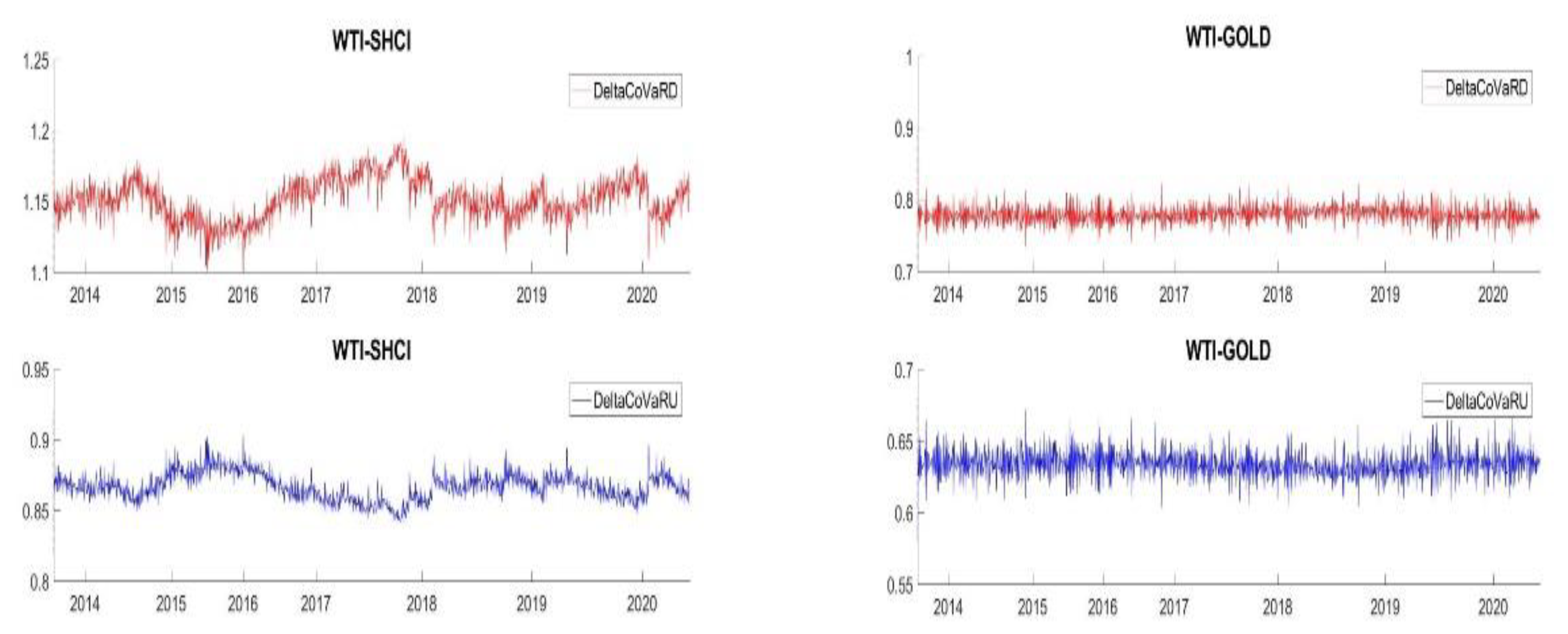

5.4. Asymmetric Risk Spillovers

5.5. Portfolio Implications

6. Implications and Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Fang, S.; Lu, X.; Egan, P.G. Reinvestigating the Oil Price–Stock Market Nexus: Evidence from Chinese Industry Stock Returns. China World Econ. 2018, 26, 43–62. [Google Scholar] [CrossRef]

- Ji, H.; Wang, H.; Zhong, R.; Li, M. China’s liberalizing stock market, crude oil, and safe-haven assets: A linkage study based on a novel multivariate wavelet-vine copula approach. Econ. Model. 2020, 93, 187–204. [Google Scholar] [CrossRef]

- Wei, Y.; Qin, S.; Li, X.; Zhu, S.; Wei, G. Oil price fluctuation, stock market and macroeconomic fundamentals: Evidence from China before and after the financial crisis. Financ. Res. Lett. 2019, 30, 23–29. [Google Scholar] [CrossRef]

- Peng, Y.; Chen, W.; Wei, P.; Yu, G. Spillover effect and Granger causality investigation between China’s stock market and international oil market: A dynamic multiscale approach. J. Comput. Appl. Math. 2020, 367, 112460. [Google Scholar] [CrossRef]

- Zhong, J.; Wang, M.; Drakeford, B.; Li, T. Spillover effects between oil and natural gas prices: Evidence from emerging and developed markets. Green Financ. 2019, 1, 30–45. [Google Scholar] [CrossRef]

- Lin, L.; Kuang, Y.; Jiang, Y.; Su, X. Assessing risk contagion among the Brent crude oil market, London gold market and stock markets: Evidence based on a new wavelet decomposition approach. N. Am. Econ. Financ. 2019, 50, 101035. [Google Scholar] [CrossRef]

- Miller, J.I.; Ratti, R.A. Crude oil and stock markets: Stability, instability, and bubbles. Energy Econ. 2009, 31, 559–568. [Google Scholar] [CrossRef]

- Liu, K.; Luo, C.; Li, Z. Investigating the risk spillover from crude oil market to BRICS stock markets based on Copula-POT-CoVaR models. Quant. Financ. Econ. 2019, 3, 754–771. [Google Scholar] [CrossRef]

- Awan, T.M.; Khan, M.S.; Haq, I.U.; Kazmi, S. Oil and stock markets volatility during pandemic times: A review of G7 countries. Green Financ. 2021, 3, 15–27. [Google Scholar] [CrossRef]

- Yousaf, I.; Hassan, A. Linkages between crude oil and emerging Asian stock markets: New evidence from the Chinese stock market crash. Financ. Res. Lett. 2019, 31. [Google Scholar] [CrossRef]

- Huang, J.; Li, Z.; Xia, X. Network diffusion of international oil volatility risk in China’s stock market: Quantile interconnectedness modelling and shock decomposition analysis. Int. Rev. Econ. Financ. 2021, 76, 1–39. [Google Scholar] [CrossRef]

- Mo, B.; Li, Z.; Meng, J. The dynamics of carbon on green energy equity investment: Quantile-on-quantile and quantile coherency approaches. Environ. Sci. Pollut. Res. 2022, 29, 5912–5922. [Google Scholar] [CrossRef]

- Jiang, K.; Ye, W. Does the asymmetric dependence volatility affect risk spillovers between the crude oil market and BRICS stock markets? Econ. Model. 2022, 117, 106046. [Google Scholar] [CrossRef]

- Zhu, P.; Tang, Y.; Wei, Y.; Lu, T. Multidimensional risk spillovers among crude oil, the US and Chinese stock markets: Evidence during the COVID-19 epidemic. Energy 2021, 231, 120949. [Google Scholar] [CrossRef]

- Mensi, W.; Al Rababa’a, A.R.; Vo, X.V.; Kang, S.H. Asymmetric spillover and network connectedness between crude oil, gold, and Chinese sector stock markets. Energy Econ. 2021, 98, 105262. [Google Scholar] [CrossRef]

- Özdurak, C. Nexus between crude oil prices, clean energy investments, technology companies and energy democracy. Green Financ. 2021, 3, 337–350. [Google Scholar] [CrossRef]

- Ahmed, A.D.; Huo, R. Volatility transmissions across international oil market, commodity futures and stock markets: Empirical evidence from China. Energy Econ. 2021, 93, 104741. [Google Scholar] [CrossRef]

- Zhao, Z.; Wen, H.; Li, K. Identifying bubbles and the contagion effect between oil and stock markets: New evidence from China. Econ. Model. 2021, 94, 780–788. [Google Scholar] [CrossRef]

- Tiwari, A.K.; Trabelsi, N.; Alqahtani, F.; Hammoudeh, S. Analysing systemic risk and time-frequency quantile dependence between crude oil prices and BRICS equity markets indices: A new look. Energy Econ. 2019, 83, 445–466. [Google Scholar] [CrossRef]

- Arouri, M.E.H.; Jouini, J.; Nguyen, D.K. Volatility spillovers between oil prices and stock sector returns: Implications for portfolio management. J. Int. Money Financ. 2011, 30, 1387–1405. [Google Scholar] [CrossRef]

- Adewuyi, A.O.; Awodumi, O.B.; Abodunde, T.T. Analysing the gold-stock nexus using VARMA-BEKK-AGARCH and Quantile regression models: New evidence from South Africa and Nigeria. Resour. Policy 2019, 61, 348–362. [Google Scholar] [CrossRef]

- Basher, S.A.; Sadorsky, P. Hedging emerging market stock prices with oil, gold, VIX, and bonds: A comparison between DCC, ADCC and GO-GARCH. Energy Econ. 2016, 54, 235–247. [Google Scholar] [CrossRef]

- Antonakakis, N.; Cunado, J.; Filis, G.; Gabauer, D.; de Gracia, F.P. Oil and asset classes implied volatilities: Investment strategies and hedging effectiveness. Energy Econ. 2020, 91, 104762. [Google Scholar] [CrossRef]

- Elie, B.; Naji, J.; Dutta, A.; Uddin, G.S. Gold and crude oil as safe-haven assets for clean energy stock indices: Blended copulas approach. Energy 2019, 178, 544–553. [Google Scholar] [CrossRef]

- Mo, B.; Nie, H.; Jiang, Y. Dynamic linkages among the gold market, US dollar and crude oil market. Phys. A 2018, 491, 984–994. [Google Scholar] [CrossRef]

- Dai, X.; Wang, Q.; Zha, D.; Zhou, D. Multi-scale dependence structure and risk contagion between oil, gold, and US exchange rate: A wavelet-based vine-copula approach. Energy Econ. 2020, 88, 104774. [Google Scholar] [CrossRef]

- Junttila, J.; Pesonen, J.; Raatikainen, J. Commodity market based hedging against stock market risk in times of financial crisis: The case of crude oil and gold. J. Int. Financ. Mark. Inst. Money 2018, 56, 255–280. [Google Scholar] [CrossRef]

- Lin, B.; Su, T. Mapping the oil price-stock market nexus researches: A scientometric review. Int. Rev. Econ. Financ. 2020, 67, 133–147. [Google Scholar] [CrossRef]

- Gharib, C.; Mefteh-Wali, S.; Jabeur, S.B. The bubble contagion effect of COVID-19 outbreak: Evidence from crude oil and gold markets. Financ. Res. Lett. 2021, 38, 101703. [Google Scholar] [CrossRef]

- Li, X.; Wei, Y. The dependence and risk spillover between crude oil market and China stock market: New evidence from a variational mode decomposition-based copula method. Energy Econ. 2018, 74, 565–581. [Google Scholar] [CrossRef]

- Li, Z.; Mo, B.; Nie, H. Time and frequency dynamic connectedness between cryptocurrencies and financial assets in China. Int. Rev. Econ. Financ. 2023, in press. [CrossRef]

- Aloui, C.; Jammazi, R. The effects of crude oil shocks on stock market shifts behaviour: A regime switching approach. Energy Econ. 2009, 31, 789–799. [Google Scholar] [CrossRef]

- Henry, O.T. Regime switching in the relationship between equity returns and short-term interest rates in the UK. J. Bank Financ. 2009, 33, 405–414. [Google Scholar] [CrossRef]

- Glosten, L.R.; Jagannathan, R.; Runkle, D.E. On the relation between the expected value and the volatility of the nominal excess return on stocks. J. Financ. 1993, 48, 1779–1801. [Google Scholar] [CrossRef]

- Drost, F.C.; Werker, B.J. Closing the GARCH gap: Continuous time GARCH modeling. J. Econom. 1996, 74, 31–57. [Google Scholar] [CrossRef]

- Bae, K.-H.; Karolyi, G.A. Good news, bad news and international spillovers of stock return volatility between Japan and the US. Pac.-Basin Financ. J. 1994, 2, 405–438. [Google Scholar] [CrossRef]

- Braun, P.A.; Nelson, D.B.; Sunier, A.M. Good news, bad news, volatility, and betas. J. Financ. 1995, 50, 1575–1603. [Google Scholar] [CrossRef]

- Mohamed, A.; Rubi, A. Return performance and leverage effect in Islamic and socially responsible stock indices evidence from Dow Jones (DJ) and Financial Times Stock Exchange (FTSE). Afr. J. Bus. Manag. 2011, 5, 6927–6939. [Google Scholar]

- Jiang, Y.; Jiang, C.; Nie, H.; Mo, B. The time-varying linkages between global oil market and China’s commodity sectors: Evidence from DCC-GJR-GARCH analyses. Energy 2019, 166, 577–586. [Google Scholar] [CrossRef]

- Medovikov, I. When does the stock market listen to economic news? New evidence from copulas and news wires. J. Bank Financ. 2016, 65, 27–40. [Google Scholar] [CrossRef]

- Boubaker, H.; Sghaier, N. Portfolio optimization in the presence of dependent financial returns with long memory: A copula based approach. J. Bank Financ. 2013, 37, 361–377. [Google Scholar] [CrossRef]

- Delatte, A.-L.; Lopez, C. Commodity and equity markets: Some stylized facts from a copula approach. J. Bank Financ. 2013, 37, 5346–5356. [Google Scholar] [CrossRef]

- Nelsen, R.B. Lecture Notes in Statistics. In An Introduction to Copulas; Springer: Berlin/Heidelberg, Germany, 1999; Volume 139, pp. 414–422. [Google Scholar]

- Patton, A.J. Estimation of multivariate models for time series of possibly different lengths. J. Appl. Econom. 2006, 21, 147–173. [Google Scholar] [CrossRef]

- Joe, H. Multivariate Models and Multivariate Dependence Concepts; CRC Press: Boca Raton, FL, USA, 1997. [Google Scholar]

- Tobias, A.; Brunnermeier, M.K. CoVaR. Am. Econ. Rev. 2016, 106, 1705. [Google Scholar]

- Jiang, Y.; Mu, J.; Nie, H.; Wu, L. Time-frequency analysis of risk spillovers from oil to BRICS stock markets: A long-memory Copula-CoVaR-MODWT method. Int. J. Financ. Econ. 2022, 27, 3386–3404. [Google Scholar] [CrossRef]

- Girardi, G.; Ergün, A.T. Systemic risk measurement: Multivariate GARCH estimation of CoVaR. J. Bank Financ. 2013, 37, 3169–3180. [Google Scholar] [CrossRef]

- Li, Z.; Ao, Z.; Mo, B. Revisiting the valuable roles of global financial assets for international stock markets: Quantile coherence and causality-in-quantiles approaches. Mathematics 2021, 9, 1750. [Google Scholar] [CrossRef]

- Lssifuah-Nunoo, E.; Junior, P.O.; Adam, A.M.; Bossman, A. Assessing the safe haven properties of oil in African stock markets amid the COVID-19 pandemic: A quantile regression analysis. Quant. Financ. Econ. 2022, 6, 244–269. [Google Scholar] [CrossRef]

- Li, Z.; Chen, L.; Dong, H. What are bitcoin market reactions to its-related events? Int. Rev. Econ. Financ. 2021, 73, 1–10. [Google Scholar] [CrossRef]

- Li, Z.; Chen, H.; Mo, B. Can digital finance promote urban innovation? Evidence from China. Borsa Istanb. Rev. 2022, in press. [CrossRef]

- Li, Z.; Zou, F.; Mo, B. Does mandatory CSR disclosure affect enterprise total factor productivity? Ekon. Istraz. 2022, 35, 4902–4921. [Google Scholar] [CrossRef]

- Zhang, C.; Chen, X. The impact of global oil price shocks on China’s bulk commodity markets and fundamental industries. Energy Policy 2014, 66, 32–41. [Google Scholar] [CrossRef]

- Chen, P. Global oil prices, macroeconomic fundamentals and China’s commodity sector comovements. Energy Policy 2015, 87, 284–294. [Google Scholar] [CrossRef]

- Luo, J.; Ji, Q. High-frequency volatility connectedness between the US crude oil market and China’s agricultural commodity markets. Energy Econ. 2018, 76, 424–438. [Google Scholar] [CrossRef]

- Meng, J.; Nie, H.; Mo, B.; Jiang, Y. Risk spillover effects from global crude oil market to China’s commodity sectors. Energy 2020, 202, 117208. [Google Scholar] [CrossRef]

- Jiang, Y.; Tian, G.; Mo, B. Spillover and quantile linkage between oil price shocks and stock returns: New evidence from G7 countries. Financ. Innov. 2020, 6, 42. [Google Scholar] [CrossRef]

- Kroner, K.F.; Ng, V.K. Modeling asymmetric comovements of asset returns. Rev. Financ. Stud. 1998, 11, 817–844. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Copula Name | Formula | Tail Dependence |

|---|---|---|

| Normal | zero tail dependence | |

| Student-t | symmetric tail dependence | |

| Clayton | lower tail dependence | |

| Gumbel | upper tail dependence | |

| Rotated Gumbel | lower tail dependence | |

| Frank | zero tail dependence | |

| Placket | zero tail dependence | |

| SJC | upper and lower tail dependence |

| WTI | SHCI | GOLD | |

|---|---|---|---|

| Mean | −0.0297 | 0.0240 | 0.0274 |

| Median | 0.1159 | 0.0546 | 0.0315 |

| Max | 31.9634 | 12.4048 | 5.3570 |

| Min | −28.1796 | −15.6188 | −5.2213 |

| S. D. | 3.4462 | 1.6907 | 0.9229 |

| Skew | 0.5871 | −1.4467 | 0.0830 |

| Kurt | 25.0793 | 21.2358 | 7.7263 |

| Max | 27,601.11 *** | 19,275.95 *** | 1264.6 *** |

| Q (10) | 60.4400 *** | 24.309 ** | 7.1560 |

| [0.0000] | [0.0068] | [0.7106] | |

| Q2 (10) | 666.7100 *** | 416.4287 *** | 178.3176 *** |

| [0.0000] | [0.0000] | [0.0000] | |

| ARCH (10) | 200.5658 *** | 209.6522 *** | 100.1241 *** |

| [0.0000] | [0.0000] | [0.0000] | |

| ADF | −36.7195 *** | −39.3499 *** | −37.5984 *** |

| PP | −36.796 *** | −39.2612 *** | −37.597 *** |

| KPSS | 0.114027 | 0.126658 | 0.302704 |

| correlation | - | 0.1342 *** | 0.0203 *** |

| WTI | SHCI | GOLD | |

|---|---|---|---|

| (p, q) | (1,2) | (2,2) | (1,2) |

| −0.0504 | 0.042 * | 0.0104 | |

| (0.0678) | (0.0678) | (0.0678) | |

| 0.9511 *** | −0.0649 | −0.3187 | |

| (0.0159) | (3.3695) | (0.2943) | |

| 0.026 | |||

| (1.0275) | |||

| −0.9761 *** | 0.0614 | 0.3025 | |

| (0.0333) | (3.3664) | (0.2944) | |

| 0.0317 | −0.0156 | 0.0158 | |

| (0.0292) | (1.1188) | (0.0267) | |

| 0.0757 *** | 0.0139 * | 0.0032 | |

| (0.0285) | (0.0072) | (0.0021) | |

| 0.0116 | 0.0773 *** | 0.0421 ** | |

| (0.0189) | (0.0169) | (0.0185) | |

| 0.9327 *** | 0.9278 *** | 0.9523 *** | |

| (0.0152) | (0.0116) | (0.0153) | |

| 0.1113 *** | −0.0046 | 0.0108 | |

| (0.0283) | (0.0272) | (0.0185) | |

| Asy | −0.1449 *** | −0.0145 | −0.0184 |

| (0.0346) | (0.0334) | (0.0314) | |

| Tail | 3.4338 *** | 3.5077 *** | 4.2185 *** |

| (0.4088) | (0.3763) | (0.4838) | |

| Q (10) | 7.7294 | 11.4798 | 2.5773 |

| [0.3570] | [0.0746] | [0.9211] | |

| Q2 (10) | 5.6827 | 9.1551 | 14.3853 |

| [0.6827] | [0.3293] | [0.0722] | |

| ARCH (10) | 0.5765 | 0.9349 | 1.4388 |

| [0.8342] | [0.4998] | [0.1575] |

| WTI-SHCI | WTI-GOLD | WTI-SHCI | WTI-GOLD | ||||

|---|---|---|---|---|---|---|---|

| Normal | 0.093 *** | 0.0526 * | Time-varying normal | 0.3269 *** | 0.1308 *** | ||

| (0.0270) | (0.0271) | (0.0244) | (0.0167) | ||||

| AIC | −11.7771 | −3.7633 | −0.0806 | 0.1677 ** | |||

| Clayton | 0.1551 *** | 0.0782 ** | (0.0904) | (0.0788) | |||

| (0.0436) | (0.0356) | −1.3134 *** | −0.9195 *** | ||||

| AIC | −26.7061 | −7.5171 | (0.1943) | (0.2484) | |||

| Rotated Clayton | 0.0955 ** | 0.0757 ** | AIC | −12.1243 | −5.5614 | ||

| (0.0399) | (0.0374) | Time-varying rotated Gumbel | 0.0010 | 0.6195 | |||

| AIC | −10.2425 | −6.5720 | (0.0822) | (4.3291) | |||

| Plackett | 1.3936 ** | 1.2058 *** | 0.4885 *** | −0.3382 | |||

| (0.5823) | (0.4191) | (0.1197) | (4.0651) | ||||

| AIC | −13.2232 | −4.4562 | −0.7138 *** | −0.0851 | |||

| Frank | 0.5772 | 0.3378 | (0.1829) | (0.1319) | |||

| (1.0747) | (1.0457) | AIC | −42.9376 | −13.6182 | |||

| AIC | −11.4063 | −4.0183 | Time-varying SJC | −18.1697 *** | 3.1519 *** | ||

| Gumbel | 1.1000 *** | 1.1000 *** | (0.0009) | (1.0540) | |||

| (0.0160) | (0.0161) | −1.8517 *** | −25.0000 *** | ||||

| AIC | −19.5484 | −5.5451 | (0.0001) | (4.7500) | |||

| Rotated Gumbel | 1.1000 *** | 1.1000 *** | −0.0071 *** | −5.0837 *** | |||

| (0.0145) | (0.0158) | (0.0000) | (1.7284) | ||||

| AIC | −34.3998 | −7.1905 | 2.7231 *** | −13.8260 *** | |||

| Student’s t | 0.0911 *** | 0.0590 *** | (0.0000) | (0.1762) | |||

| (0.0000) | (0.0000) | −16.3463 *** | 25.0000 *** | ||||

| 3.6122 *** | 4.8238 *** | (0.0000) | (0.3181) | ||||

| (0.0000) | (0.0006) | −4.4404 *** | −18.4485 *** | ||||

| AIC | −85.8457 | −48.2914 | (0.0000) | (0.1569) | |||

| SJC | 0.0000 | 0.0001 | AIC | −41.2246 | −21.6513 | ||

| (0.4740) | (0.0002) | Time-varying Gumbel | −0.5174 *** | 1.9783 *** | |||

| 0.0639 | 0.0090 | (0.0566) | (0.0513) | ||||

| (0.3039) | (0.0062) | 0.8854 *** | −1.0160 *** | ||||

| AIC | −32.0104 | −10.6824 | (0.0567) | (0.0545) | |||

| −0.4550 *** | −2.2179 *** | ||||||

| (0.1460) | (0.0666) | ||||||

| AIC | −34.6333 | −21.1931 | |||||

| Time-varying T-copula | 0.2976 *** | 0.0626 *** | |||||

| (0.0348) | (0.0169) | ||||||

| −0.0690 | 0.2672 *** | ||||||

| (0.0792) | (0.0944) | ||||||

| −1.0707 *** | −0.8110 *** | ||||||

| (0.3275) | (0.2781) | ||||||

| AIC | −88.4969 | −48.2839 | |||||

| Time-varying Clayton | 1.3950 *** | −0.3872 | |||||

| (0.1258) | (0.4323) | ||||||

| −0.6358 *** | −1.2148 | ||||||

| (0.2111) | (0.8361) | ||||||

| −2.8353 *** | 1.8647 ** | ||||||

| (0.3542) | (0.9663) | ||||||

| AIC | −34.9863 | −8.3209 |

| Best-Fit Copula | Dependence Structure | |

|---|---|---|

| WTI-SHCI | TVP-Student-t | Symmetric tail dependence |

| WTI-GOLD | TVP-Student-t | Symmetric tail dependence |

| Down | Up | |||||

|---|---|---|---|---|---|---|

| VaR | CoVaR | ∆CoVaR | VaR | CoVaR | ∆CoVaR | |

| WTI-SHCI | −2.9520 | −4.3113 | 1.1491 | 3.3550 | 4.2949 | 0.8663 |

| (1.9744) | (2.8680) | (0.1080) | (2.1797) | (2.7977) | (0.0178) | |

| WTI-GOLD | −1.1741 | −2.3340 | 0.7810 | 1.2915 | 2.2921 | 0.6336 |

| (0.4445) | (0.8769) | (0.0816) | (0.4800) | (0.8530) | (0.0138) | |

| H0:

H1: | H0:

H1: | H0:

H1: | H0:

H1: | |

|---|---|---|---|---|

| WTI-SHCI | 0.3765 | 0.2623 | 1.0000 | 0.9992 |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| WTI-GOLD | 0.5696 | 0.5283 | 0.9985 | 0.9985 |

| (0.000) | (0.000) | (0.000) | (0.0000) |

| WTI-SHCI | F Statistics | WTI-GOLD | F Statistics | |

|---|---|---|---|---|

| Number of breaks selected | 3 breaks | 4 breaks | ||

| Break date | 4 December 2015 | 319.3474 *** | 27 January 2015 | 1092.582 *** |

| 22 November 2017 | 126.5677 *** | 28 April 2017 | 59.99245 *** | |

| 30 May 2019 | 383.1022 *** | 25 April 2018 | 91.64415 *** | |

| 06 March 2019 | 84.37587 *** |

| WTI-SHCI | |||||||

|---|---|---|---|---|---|---|---|

| Full Period | Begin-BP1 | BP1-BP2 | BP2-BP3 | BP3-End | |||

| 0.1507 | 0.1919 | 0.1089 | 0.1791 | 0.1035 | |||

| (0.0611) | (0.0656) | (0.0219) | (0.0491) | (0.0273) | |||

| 0.7909 | 0.6871 | 0.8975 | 0.7180 | 0.9092 | |||

| (0.1562) | (0.1707) | (0.0507) | (0.1302) | (0.0608) | |||

| 0.2856 | 0.2656 | 0.2885 | 0.2678 | 0.3402 | |||

| (0.0569) | (0.0065) | (0.0151) | (0.0106) | (0.1157) | |||

| RRE | 0.2513 | 0.3538 | 0.0748 | 0.1954 | −0.1122 | ||

| WTI-GOLD | |||||||

| Full Period | Begin-BP1 | BP1-BP2 | BP2-BP3 | BP3-BP4 | BP4-End | ||

| 0.0267 | 0.0435 | 0.0257 | 0.0222 | 0.0147 | 0.0249 | ||

| (0.0123) | (0.0100) | (0.0074) | (0.0022) | (0.0056) | (0.0120) | ||

| 0.8910 | 0.8009 | 0.9041 | 0.9127 | 0.9526 | 0.8961 | ||

| (0.0711) | (0.0855) | (0.0368) | (0.0238) | (0.0250) | (0.0607) | ||

| 0.0730 | 0.0805 | 0.0751 | 0.0744 | 0.0637 | 0.0692 | ||

| (0.0119) | (0.0019) | (0.0054) | (0.0014) | (0.0109) | (0.0199) | ||

| RRE | 0.1871 | 0.2438 | 0.1684 | 0.1507 | 0.1021 | 0.1771 | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mo, B.; Meng, J.; Wang, G. Risk Dependence and Risk Spillovers Effect from Crude Oil on the Chinese Stock Market and Gold Market: Implications on Portfolio Management. Energies 2023, 16, 2141. https://doi.org/10.3390/en16052141

Mo B, Meng J, Wang G. Risk Dependence and Risk Spillovers Effect from Crude Oil on the Chinese Stock Market and Gold Market: Implications on Portfolio Management. Energies. 2023; 16(5):2141. https://doi.org/10.3390/en16052141

Chicago/Turabian StyleMo, Bin, Juan Meng, and Guannan Wang. 2023. "Risk Dependence and Risk Spillovers Effect from Crude Oil on the Chinese Stock Market and Gold Market: Implications on Portfolio Management" Energies 16, no. 5: 2141. https://doi.org/10.3390/en16052141

APA StyleMo, B., Meng, J., & Wang, G. (2023). Risk Dependence and Risk Spillovers Effect from Crude Oil on the Chinese Stock Market and Gold Market: Implications on Portfolio Management. Energies, 16(5), 2141. https://doi.org/10.3390/en16052141