1. Introduction

Oil price volatility is influenced not only by macroeconomic [

1,

2,

3,

4] and microeconomic [

5,

6] variables, but also by speculative activities and non-economic variables [

7]. The world oil prices have become increasingly volatile since the 1970s of the 20th century. The advent of futures trading caused more speculation in the market. Rising demand in developing countries and increasing supply driven by new production in the United States, have further contributed to price volatility in the last few years [

8]. Moreover, the effects of the COVID-19 pandemic caused unprecedented fluctuations in oil prices. The outbreak of COVID-19 and the lockdowns implemented to hold the spread of the virus caused the economic downturn [

9]. Many countries have significantly reduced transportation, travel and tourism. The total number of commercial flights per day (including passenger, cargo, charter, and some business jet flights) decreased between January 2020 and early April 2020 by almost 70%. As the aviation and transport sectors are responsible for 60% of oil demand, mobility constraints caused the decline in oil consumption. Daily world oil demand fell from 100 million barrels in January 2020 to a level below 75 million barrels in April 2020 [

10]. At the beginning of the COVID-19 pandemic, a sharp drop in oil consumption in the context of still large production (the effect of the “Oil War” between Russia and Saudi Arabia) led to a rapid increase in oil inventories, and a record decline in oil prices [

11].

Lockdowns had also an impact on global supply chains. In the first quarter of 2020, almost 80% of the global floating production, storage, and offloading vessels in the world were under construction in shipyards in China, Korea and Singapore. In addition, the main center for the production of specialized engineering equipment for the oil industry is the Lombardy region, which was one of the most affected Italian regions [

10].

Bildirici et al. [

7] emphasized that “uncertainty and volatility in oil prices due to COVID-19 and the conflict between Russia and Saudi Arabia have impacted the investors’ decisions for portfolio allocation and manufacturers’ decisions for industrial production and economy”. There is literature investigating oil prices, their determinants and volatility during the COVID-19 pandemic. Nyga-Łukaszewska and Aruga [

10] examined the impact of the COVID-19 cases on the crude oil. They concluded that in the U.S. the pandemic had a statistically negative impact on the oil price. Bouri et al. [

9] examined the predictive power of a newspaper-based index of uncertainty associated with infectious diseases (EMVID) for the volatility of crude oil price. They showed that including EMVID into a forecasting setting improved the forecast accuracy of oil realized volatility at different horizons. In turn, de Blasis and Petroni [

12] investigated the behavior of volatility linkages between oil and renewable energy firms by analyzing two crude oil futures prices (the West Texas Intermediate (WTI) crude oil futures contract and the Brent crude oil futures contract), and two indices (the STOXX Europe 600 oil & gas index and the European renewable energy index). They found that volatility for all energy firms increased between March and July 2020 and the ability to forecast their volatility decreased. In our paper we try to model the oil price risk using investor’s expectations embedded in the Crude Oil Volatility Index (OVX).

The Crude Oil Volatility Index was introduced by the Chicago Board Option Exchange in 2007 as a new measure of crude oil expectation of volatility. As it is based on implied volatility it has become a new barometer of investment sentiment with reference to future oil prices [

13,

14].

The results of Benedetto et al. [

15] underline the fact that OVX is a measure of uncertainty related to West Texas Intermediate crude oil, similarly to the relationship of VIX and S&P500. Although many studies find a link between the VIX and OVX [

16,

17,

18,

19,

20], OVX seems to be better than VIX in predicting oil price changes [

21]. Lv [

22] showed that the OVX has a significantly positive impact on oil futures volatility. This finding is in line with [

23] in the post-2009 period, stating a significant role of OVX for supply-side and oil specific demand shocks, as net transmitters of spillover effects. According to Chatziantoniou et al. [

24], OVX is a transmitter of shocks to VIX, especially after the oil price collapse period of 2014–2016. The oil market has become more financialized over recent years and thus the uncertainties between the oil and stock markets tend to become more interlinked. Chen et al. [

25] showed a weak negative relationship between OVX changes and future crude oil price movements, thus extremely high/low levels of OVX cannot predict future negative/positive returns well. OVX serves as an unbiased, but not an efficient estimate of the future realized volatility and it includes information on the future realized volatility. Rising OVX had a greater negative impact on the oil prices than the declining OVX, thus indicating that a long-run, asymmetric cointegration exists between them [

26]. The results of linear Granger causality showed that OVX led the oil price in one direction. However, the nonlinear Granger causality test results confirmed a bidirectional nonlinear causality between OVX and oil prices. Liu et al. [

27] revealed the asymmetric effect of the dependence structure between WTI and OVX and a greater lower-upper tail dependence than the upper-lower one. The result indicates that oil price returns are more sensitive in response to OVX increase relative to the OVX decrease. The asymmetry was also confirmed in the study conducted by Agbeyegbe [

28] and Chen and Zou [

29].

The first research aim of this paper is to verify the tail dependence between OVX and crude oil price. The COVID-19 pandemic has shaken the oil market and exposed the investment risk to an unprecedented extent. The WTI oil price dropped to negative values in April 2020 for the first time in history and OVX hit its maximum, doubling the previous record reached at the time of the Global Financial Crisis (GFC). We attempt to test the strength and asymmetry in the tail dependence between the index and oil prices. The copula approach is used as a research method analyzing the static and dynamic patterns of dependency.

The second research problem of this study is to explore the predictive power of the OVX in the context of tail risk measurement. There is considerable literature studying issues related to tail risks in the financial and commodity markets. Conventional measures include Value at Risk (VaR) and Expected Shortfall (ES) [

30,

31,

32]. Lian et al. [

31] indicated the group of new risk measures of tail risk including co-crash probability [

33,

34], correlation of international equity returns in the upper and lower tails [

35], co-skewness and co-kurtosis [

36,

37], tail risk measure based on Hill’s [

38] power law estimator [

39], systematic tail risk [

40] and CoVaR [

41]. The most commonly used measure of tail risk is Value at Risk. This measure determines the maximum loss of an asset or a portfolio over a specific time period, with a given confidence level. In the oil market, VaR can be used to quantify the maximum oil price change associated with a certain confidence level. The VaR of the oil market has increased more during the COVID-19 era than during the Global Financial Crisis [

42], therefore we can expect that traditional statistical methods of risk measurement may not be appropriate to capture the risk with high accuracy. We assess how much the OVX can improve the VaR forecasts computed with the use of the statistical model. The observed strengthening of the tail dependence during the COVID-19 pandemic time indicates a potential to improve volatility models by implementing the investors’ expectations in GARCH-type models. Christoffersen et al. [

43] found no evidence that VaR estimated using implied volatility is superior to the VaR based on GARCH or historical simulations. In turn, Chong [

44] stated that implied volatility is not effective in estimating VaR, as it tends to overestimate volatility in periods of stability and underestimates risk when the market is more volatile. In their study Kim and Ryu [

45] examined the information content of implied volatilities in the Korean stock market. They found the bad performance of the VaR–VKOSPI model as a tool for risk management. Bongiovanni et al. [

46] showed a poor performance of VIX in VaR measurement of the portfolio replicating the S&P500 index during the most turbulent market phase, thus causing the inadequacy of this model both for the failure rate and the size of losses. Conversely, their performance is significantly better when the market faces more normal conditions, where the lower volatility allows them to reduce the corresponding failure rate and the average losses that occur. These results contrast with the findings of Giot [

47], who analyzed the VIX in the U.S. market. He predicted VaR using implied volatility with a skewed Student’s

t-distributional assumption and concluded that VaR estimates relying exclusively on lagged implied volatility perform as well as VaR estimates based on the volatility forecasts of GARCH family models. Liu et al. [

27] compared the VaR for the WTI returns model conditional on OVX with the ARMA(2,2)-GJR-GARCH(1,1). A comparison between VaR and VaR conditional on OVX indicates that taking the condition of the OVX into account can slightly improve the accuracy of the VaR estimates for WTI returns. However, no essential difference exists between the VaR for WTI and the VaR for WTI conditional on OVX. The predictive power of alternative volatility models, i.e., GARCH, Extreme Value Theory (EVT) and VIX for the S&P500 index, was verified in [

48]. Based on the adjusted determination coefficients they proved that the VIX index performs better than the GARCH and EVT estimators. In this study we resume the considerations on the usefulness of implied volatility in VaR estimation for crude oil under the new extreme situation caused by the COVID-19 pandemic.

We contribute to the existing literature in two ways: (1) we found stronger strength and asymmetry in the tail dependence between OVX changes and negative crude oil returns compering to positive returns during the COVID-19 pandemic. The finding underlies the role of OVX as a fear gauge with reference to crude oil prices. Moreover, comparing to other studies we analyze the dependence between extreme values of OVX changes and WTI returns and thus we focus on the situations where the informative role of the fear index is the most important; (2) In the Arab Spring and COVID-19 health crisis, the expectation factor (OVX) affects oil price volatility. However, the OVX index does not improve the accuracy of Value at Risk forecasts obtained from the statistical GARCH-EVT model.

The rest of the paper is organized as follows.

Section 2 provides methodological details. It introduces the copula methodology and defines the tail dependence concept.

Section 3 shows the results of the empirical study on tail dependence between considered variables.

Section 4 presents empirical results for VaR forecasting, while

Section 5 concludes the study.

3. Tail Dependence between OVX and WTI Oil Price—Empirical Results

In

Figure 2 we present correlation plots for the entire research period and highlight the extreme values of OVX changes and WTI returns. We considered one-day scaled implied volatility, i.e., OVX

. As the extrema we chose exceedances of the 5th and 95th percentiles of distribution. The left panel presents all data points, whereas the right one displays the same pairs, but for clarity we removed the outliers. The upper plots show the dependence between OVX changes and crude oil returns, while the lower ones show the dependence between GARCH volatility changes and crude oil returns. In this study, the selection of the best ARMA-GARCH model from the set of models considered is based on information criteria (the Akaike information criterion and Bayesian information criterion) and properties of the residuals. The Akaike information criterion is the most commonly used method for selecting a model. In turn, the Bayesian information criterion is recommended when the model is used for forecasting, because it allows to obtain better quality of forecasts. We adopted the ARMA(1,1)-GJR-GARCH(1,1) model with skewed Student’s

t-distribution to estimate the WTI oil return volatility. In the upper plots we observed many more exceedances for the negative extreme returns than for the positive ones. It suggests a stronger tail dependence between the index and negative returns than for the positive returns. The same type of asymmetry is documented in [

68] for the index options in Poland. The GARCH volatility and returns pairs behave completely differently, as the correlation plot indicates a symmetry in the lower and upper tails of returns.

In this section we present the calculation results for the tail dependence between WTI oil returns and OVX or GARCH volatility changes. A higher tail dependence is interpreted as a higher co-movement under the extreme events. As we tried to verify the asymmetric behavior of index/volatility changes in the presence of positive and negative price shocks of WTI oil, we estimated the copulas separately for positive and negative returns with OVX/volatility. Two types of dependence are analyzed. First, the co-movement between the variables and second, the tail dependence between oil returns and lagged OVX/volatility. The first approach is to reveal the ability of OVX to be a fear gauge or sentiment indicator. We are particularly interested in the COVID-19 period, which to date has not been included in such considerations. The second relationship to check is the tail dependence between lagged OVX/volatility changes and oil returns. The analysis is to disclose the predictive power of OVX and finally will be implemented in Value at Risk forecasting in the next section.

In order to choose the best copula model for the empirical study the distance between estimated,

C and empirical,

copula must be computed. Genest et al. [

69] proposed to use the Cramér-von Mises statistic:

We used this metric to choose the copula model best fitted to our data. If the model outperformed others only in one tail, we presented the results also in the other one to be able to compare the differences between them.

Table 1 presents the correlation coefficient and the tail dependence (lambda) between negative (-rCL) or positive (rCL) WTI crude oil returns and OVX changes (dOVX). The

t-copula outperforms other models for positive returns, whereas the Joe copula does so for negative ones. The relationship between OVX changes and crude oil returns is significantly negative. The correlation coefficient obtained from the

t-copula between the variables is negative in the entire sample period, as well as in the GFC and COVID-19 sub-periods. It means that a decrease in WTI oil prices is accompanied by an increase in the OVX index. The dependence of extreme values is strongly asymmetrical. The tail dependence increases with negative shocks and shifts to independence when the WTI oil price increases. The same, high level of tail dependence is maintained over the full sample period and in the COVID-19 sub-period. According to the

t-copula, TDC for negative returns in the COVID-19 subperiod is 0.352. The asymmetric Joe copula indicates a very high level of tail dependence, 0.479. In the GFC period the level of dependence is lower, 0.23 for the

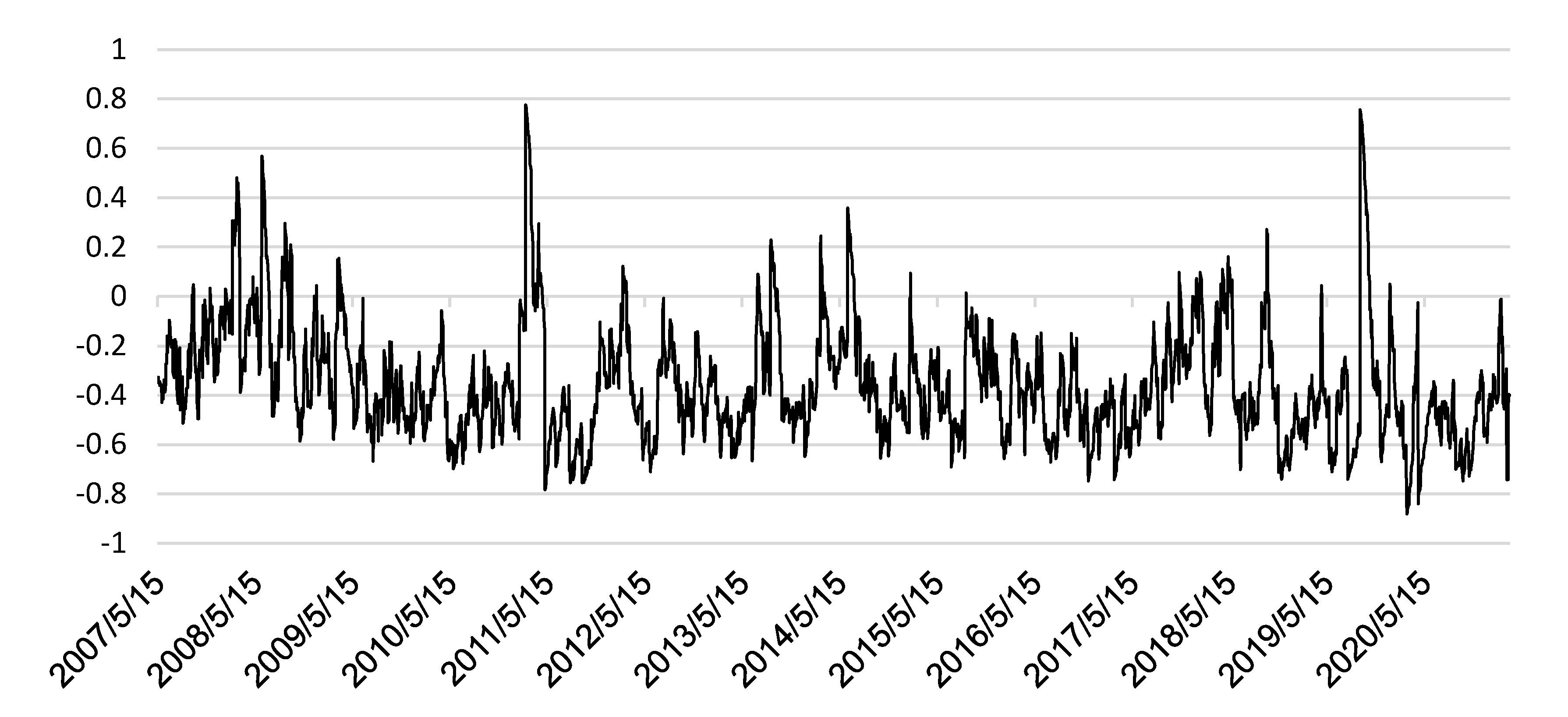

t-copula and 0.328 for the Joe copula. The WTI oil prices behaved differently during GFC than in the COVID-19 crisis. In the GFC period WTI oil price increased from USD 96 in December 2007 and reached the level USD 145 in July 2008 (see

Figure 1). At the same time the OVX index gradually grew. After that, a steep decline in oil prices began together with the increase in the values of the index, reaching the floor USD 34 in December 2008 with the maximum of OVX. The maximum was exceeded as late as the COVID-19 crisis. The findings highlight the early warning character of OVX, which extreme increase is concurrent with an extreme decrease in WTI oil prices. As the OVX index is based on implied volatility, thus on the investors’ expectations towards future oil prices. Hence, we checked further the predictive power of the index to predict the one-day ahead return on crude oil.

Table 2 presents the tail dependence of crude oil returns with one-day lagged changes in the OVX index. In the considered cases the

t-copula is the best fitted copula model to data both for negative and positive returns. The correlation coefficient is non-significant for all sample periods. We can conclude that there is no influence of OVX changes on the future behavior of the oil price. However, we found evidence of the tail dependency in lagged OVX changes and returns in the entire sample period and in the COVID-19 sub-sample period. In the full period the tail dependence is symmetrical for negative and positive returns; however, in the COVID-19 period the dependence for negative returns is twice as big as for positive ones and amounts to 0.239. The finding seems to be promising for the tail risk prediction. The usefulness of the implied volatility in one-day ahead forecasts of the Value at Risk is verified in the next section.

Traditional Value at Risk models use an ex-ante volatility. As it is shown in

Figure 2, this type of volatility behaves differently than implied volatility. The dependence between crude oil returns and volatility changes is not as strong as in the case of implied volatility. Moreover, it does not show the asymmetry in the tail dependence with lower and upper tails of crude oil returns. Such an observation is confirmed by the results presented in

Table 3. The correlation coefficient is non-significant at a 5% significance level in the GFC and entire periods. The tail dependence coefficient is indeed lower than in the OVX case and symmetrical for positive and negative oil price shocks in the full period. The same results were obtained for the GFC period. In the COVID-19 period the dependence seems to be slightly higher for positive returns than for negative ones; however, the level of dependency is only 0.191 for the upper tail comparing to 0.058 for the lower one.

Table 4 presents the relationship between lagged volatility changes and crude oil returns. The results for the tail dependence look similarly to those for OVX presented in

Table 2 for the entire period. In both the GFC and COVID-19 periods the volatility does not point out the predictive power for future returns. The tail dependence coefficient is close to zero. Comparing the results for the OVX index and GARCH volatility a greater relationship is observed in the extrema between crude oil returns and implied volatility than with GARCH volatility. The OVX index seems to be useful in tail risk prediction, especially in times of enormous volatility such as the COVID-19 period.

Results shown above are based on the static model of a copula. To examine the possible evolution of the dependence over time, the conditional copula approach is applied. We chose the

t-copula as this model was most often applied in the previous analyses. Moreover, the

t-copula together with the tail dependence allows to estimate the correlation between variables. The estimation results for the time-varying copula between WTI returns and OVX changes are shown in

Table 5. We adopted the GJR-GARCH(1,1) model with skewed Student’s

t-distribution to estimate the WTI oil return volatility. In the case of OVX changes the best model was the ARMA(1,1)-GARCH(1,1) with skewed Student’s

t-distribution. The conditional correlation coefficient, shown in

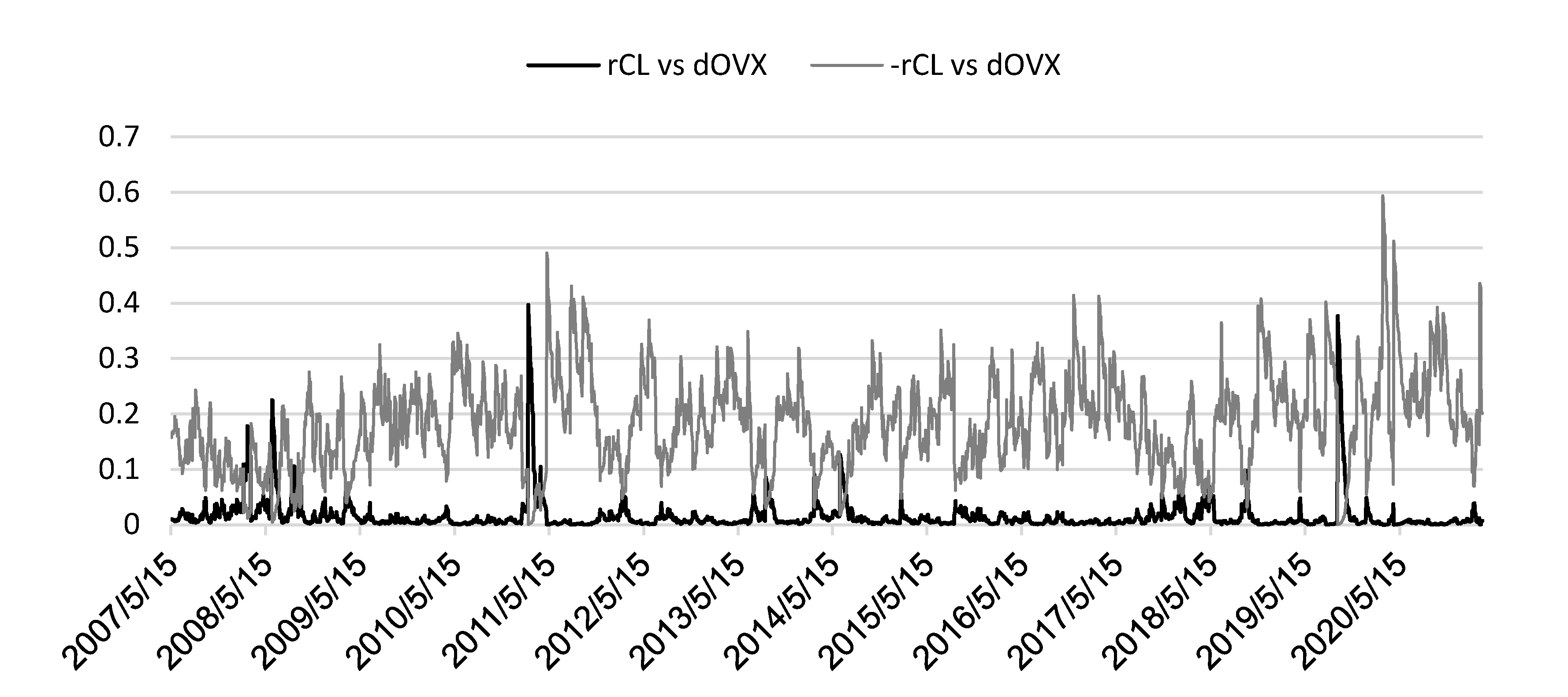

Figure 3, exhibits a time variation and presents a general negative dependence between WTI returns and OVX changes. Thus, when the oil price decreases the OVX index increases, while the oil price increases with OVX drop (

Figure 1). An interesting fact is that during the GFC period the dependence was the weakest. The finding confirms that obtained from the static copula analysis. In the first period of GFC the oil price and OVX moved in the same direction, thus increasing their correlation. The interpretation of the dependence captured by the correlation coefficient does not hold for extreme changes. The asymmetry between positive and negative returns in relation to OVX changes is easy to notice (

Figure 4). The tail dependence between positive returns and OVX changes is approximately zero when excluding the isolated cases, indicating little or no dependence. However, for negative returns the dependence seems to maintain the high level and it reached level 0.6 in the COVID-19 crisis and the level 0.5 in the Arab Spring (the period of the uncertainty in oil supply stemming from the social instability in the Middle East and North Africa). The finding suggests that joint extreme movements of negative oil returns and OVX changes tended to occur most frequently during the COVID-19 crisis. In contrast, the lower tail dependence is observed in the GFC period.

4. Value at Risk Forecasting—Empirical Results

In this section we verify the usefulness of expectations towards oil prices, embedded in the implied volatility index OVX, to predict one-day ahead Value at Risk. As we found a tail dependence between OVX and crude oil returns, we expected that applying OVX could improve VaR forecasts for crude oil computed from the statistical model. As the VaR model we decided to use the conditional Extreme Value model (GARCH-EVT) proposed by McNeil and Frey [

70]. The model guarantees high accuracy of risk estimations [

70,

71,

72,

73,

74]. A GARCH-EVT approach is a two-stage hybrid method that combines a Generalized Autoregressive Conditional Heteroskedasticity (GARCH) filter with the Extreme Value Theory (EVT). In the first stage the GARCH approach is used to estimate empirical oil returns. In our study the GARCH(1,1) model is used:

where:

represents conditional variance of

and

are the standardized residuals. The GARCH-EVT-OVX model exploits the following volatility equation:

where

denote the 1-day scaled implied volatility at time

t.In the second step the Peaks over Threshold (POT) method of EVT is applied to model the tails of standardized residues

obtained from the GARCH model. The POT method is based on the Balkema–de Haan theorem [

75], which states that exceedances (abnormal values of a random variable)

y of a high threshold,

u follow the Generalized Pareto Distribution (GPD) with CDF of the form:

where

are distribution parameters which satisfy

for

and

for

. The

q-quantile of GPD for sample size of length

n is calculated as follows:

where

k is the number of exceedances of the threshold,

u.Using the POT approach requires to pre-specify the threshold,

u which indicates the beginning of the upper distribution tail. The appropriate choice of a threshold level is a considerable challenge. A broad overview on how to choose the threshold may be found in [

76,

77,

78,

79]. The choice of the threshold in the GARCH-EVT model is discussed in [

80]. The authors provide the rationale that the fixed threshold allows to produce VaRs with a similar accuracy as advanced optimization procedures. We set the 90th percentile as the threshold level in the empirical study, because such a selection of the threshold value enables the determination of VaR forecasts for the confidence levels of 95%, 97.5% and 99%. Moreover, for different threshold levels the GARCH-EVT model produces similar Value at Risk estimates [

80].

The Value at Risk for a short position (right tail) in the GARCH-EVT model is calculated with the formula:

where:

—one step ahead forecast of conditional volatility,

—GPD quantile calculated for the standardized residuals

of the GARCH(1,1) model.

To test the forecasting performance of examined VaR models we used rolling windows of 504 returns and computed the VaR forecasts for each moving window. To evaluate the accuracy of forecasts we applied four different backtesting procedures, i.e., the Kupiec failure test,

UC [

81], the conditional coverage Christoffersen’s test,

CC [

82], the duration Christoffersen and Pelletier’s test,

UD [

83] and the dynamic quantile Engle and Manganelli’s test,

DQ (the test included constant, VaR, first five lagged exceedances and one lagged squared return) [

84]. These tests focus on exceedances of VaR forecasts by actual returns and consider it as a violation. The Kupiec test checks the valuation number, whereas the other tests evaluate their independence. An evaluation of the test size for small samples may be found in [

85]. Laporta et al. [

30] used a similar set of tests (Kupiec test, Christoffersen’s test, and Engle and Manganelli’s test) to assess VaR forecasts for daily returns on energy commodities. Marimoutou et al. [

71] applied the loss function proposed by Lopez [

86] as an additional measure of VaR forecasts for returns on WTI and Brent. Furthermore, as goodness-of-fit measures we present mean/maximum absolute deviation between the returns and the quantiles when the valuation occurs

ADmean/

ADmax used by McAleer and Da Veiga [

87] and the loss function

Q described by Gonzalez-Rivera et al. [

88].

Table 6 shows the results of calculations for the GARCH-EVT model. Panels A and B present findings for the full research period, panels C and D for the pre-COVID-19 sample (from May 2007 to the end of November 2019) and panels E and F for the COVID-19 one. All calculations were made for long (left tail) and short (right tail) investors’ positions. The rejection of the null hypothesis at the 5% significance level is marked in bold and thus a failure of the VaR model. The Kupiec test confirms that the number of valuations is consistent with the expected one. However, the other tests display a dependence of VaR valuations. The duration

UD test shows the existence of memory between VaR valuations in the right tail in the pandemic period (

q = 97.5%, 95%) and in the left tail in the entire period (

q = 99%). The dynamic quantile

DQ test indicates that the current valuation is not independent on past processed information available in valuations, VaR and squared return. Based on the

DQ test a dependence was found only in the pre-COVID-19 period in the right tail for

q = 97.5%, 95% and in the left one for

q = 99%. The goodness-of-fit measures, i.e.,

ADmean,

ADmax and the loss function, take higher values for the left tail than for the right one indicating greater difficulties in risk measurement during crude oil price drops.

Comparing the results included in

Table 6 and

Table 7 no significant differences were observed for the results of tests and goodness-of-fit measures. The number of valuations tends to be slightly lower for the model with implied volatility (

Table 7). We can infer that the expectation factor does not improve the accuracy of forecasts received from the statistical model. This finding confirms these cited in the Introduction.

Figure 5 shows the estimates of

in formula (30), which stands for the weight of the OVX in the volatility equation. The values of

are equal to zero for most of the research period. Only in periods of high volatility (the Arab Spring and COVID-19 periods) it is positive, although its value does not exceed 0.08. The impact of expectations in one-day ahead VaR forecasting seems to be negligible. This result may be explained by the tail co-movement between oil returns and OVX and a weak tail dependence between oil returns and lagged OVX. The concurrent reaction of extreme returns and OVX changes does not allow to take advantage the expectations in future risk assessment. Presumably, during an extended crisis time, when the tail dependence enhances the importance of the expectation factor in the volatility equation could play a greater role, but our research period does not allow to verify such a hypothesis.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}