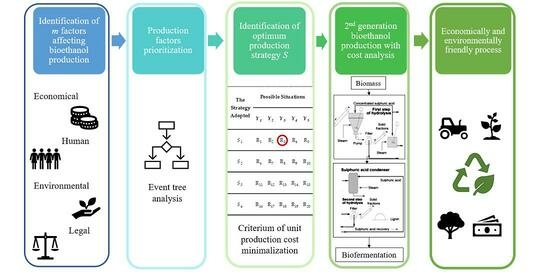

3.3. Prioritizing the Factors Influencing the Economic Effectiveness of Second-Generation Bioethanol Production in Poland

As presented in the literature [

24,

25,

26], an ultimate indicator of a correctly adopted spirit fuel production strategy may be the minimum energy unit manufacturing cost, which requires the right balance of production factors in a changing economic and social environment. However, the mix of various economic, social, and political factors influencing the development of second-generation bioethanol production in Poland represents a heterogenous group of elements that can significantly complicate the identification of the most cost-effective production strategy. To provide a mathematical method enabling analysis of the identified incoherent group of factors, we applied the expert mathematical method. This tool enables investigating diverse factors, and the results obtained by this method differ slightly from other methods in the range of 6–8% [

16,

17]. To provide simplification of the expert analysis resulting in more structured and reliable output data, the idea of event tree analysis (ETA) was applied (

Figure 4).

In the ETA analysis, the importance of 5 level II factors (

C2) and 20 level III factors (

C3), determining the possibility of bioethanol production in Poland (

C1), were estimated. The level II factors included the option of fuel production from different organic materials, including wood, straw, maize, grass, and catch crops (

Figure 4,

Table 2). The level III factors assessed the cost, technical, and environmental aspects of second-generation bioethanol production in Poland. Data obtained from an expert survey was used to identify the most important factors based on the so-called “local’ priority criterion. Local priorities were obtained by the sum of points given by experts and extrapolation to the value of 100. This approach enabled the identification of the share of each factor in the structure of the given group. This approach enabled the identification of the “importance” of level II factors in all sets of elements rated by the experts by the value of local priority

mj (

Table 2).

As presented in

Table 2, the most important factor determining the possibilities of developing the production of second-generation bioethanol in Poland is the availability of raw materials from the forestry and wood processing industries. Their share in the significance hierarchy in bioethanol production represents a value of 41 (41%), and it is almost twice as significant as the next most probable feedstock (maize) with a share of 21 points (21%). According to experts’ assay, the least likely second-generation bioethanol production could be realized from catch crops, which account for only 7 points (7%). The presented concordance coefficient with the value of 0.624 enabled the quantitative assessment of experts’ agreement and met the applied compliance criterion in expert method analysis as presented previously in the literature [

27].

To identify more detailed elements that can affect the level II (

C2) factors, which, as a consequence, may also have an indirect impact on second-generation bioethanol production in Poland, the systemic priorities values of level III factors (

C3) were also determined (

Figure 5). For that purpose, for each identified II level (

C2) factor, four III (

C3) level subfactors were distinguished (

Figure 1) expressing the potential role of the II level (

C2) group and indirectly on the opportunities for the energy production process. In the level III (

C3) factors, the availability and purchasing costs of raw materials and the economic aspects of possible EU and Polish government subsidies and tax rates of production held in Poland were identified (

Figure 5). For level III factors (

C3), the system priorities were calculated as a product of the local priorities from the lowest branch in the event tree to the level located at the top of the tree, with the standardization condition based on the sum of system priorities at a given level equal to 100. The largest share in the second-generation bioethanol production costs from all the analyzed raw materials was represented by the costs of raw materials acquisition, whose values vary from 28.0 to 52.0 points (local priority values). Contrarily, the possible production taxation possessed the lowest impact on estimates, with values ranging from 13.0 to 17.0 points. This factor also revealed the lowest impact on production efficacy in the system priority approach, from 1.1 to 16.0 points for the taxation of catch crops and wood acquisition, respectively.

Following the factor prioritization methodology, the elements affecting bioethanol process production were divided into four ranges of significance (“weights”), that is, high, higher than average, average, and lower than average (

Table 3). The size of the priorities system varied from 1.10 to 16.00 points, with the average value of one factor to 5.00 points (100:20 = 5.00). By dividing the total range of the system priorities size into four groups and including 5.00 points as the average size, the implementation significance ranges can be assessed as follows: 1—high (12.25–16.00), 2—higher than average (8.49–12.24), 3—average (4.73–8.48), 4—lower than average (1.10–4.72). To determine the significance of the influence of each group on the achievement of the main objective, all the factors considered were grouped according to ranges of the size of the system priorities (

Table 3).

Among level III factors, the purchasing cost of raw material from wood (

C311) was found to have the highest significance (

Table 3). Therefore, this element represents the factor of the greatest possible influence on the economic efficiency of second-generation bioethanol production in Poland. Piwowar A. and Dzikuć M. reported that between 2015 and 2019, the main feedstock for bioethanol production in Poland was maize [

23]. However, as presented previously by Kheybari et al. [

28], agricultural waste including wood appears to be competitive from an economic and environmental point of view, primarily due to their high hemicellulose content and adequate amounts of lignin to balance energy demands during bioethanol production. Other materials, such as grass or maize, may not be economically attractive primarily due to lignin deficiency, which cannot meet the energy needs of the spirit fuel production process. As presented in a report analyzing the energy RES transition in Poland [

29], the availability of waste wood raw materials is constantly growing. Wieruszewski et al. [

30] indicated that the average volume of wood assortment harvested each year between 2018 and 2020 reached 12 million m

3, which corresponds to approximately 25% of the total wood harvested annually. Polish sawmills produce approximately 8 million m

3 of wood stocks annually for the production of wood materials and energy biomass, which accounts for approximately 20% of the total production of this raw material. For this reason, the use of wood waste for bioethanol production in Poland seems particularly interesting.

The second distinguished group included one factor (

C312) regarding possible EU subsidies for raw material acquisition, which may also be regarded as a relatively significant factor affecting bioethanol production in Poland. The EU program “Infrastructure and Environment”, established for 2016–2020, included subsidies for the production of biofuels. Within the framework of competition No. 1/PO IiS/9.5/2009, PLN 66.9 million was distributed to the beneficiary for this purpose, with the total cost of the winning project amounting to PLN 135.3 million [

31]. Subsidies for renewable energy sources are also implemented for companies and farms. This includes investing in building new facilities and increasing the capacity of units that generate electricity and heat from biomass. Co-financing was provided by the European Regional Development Fund within the framework of Priority Axis V. All these activities were important from the point of view of Poland’s climate policy and the development strategy of a CO

2-neutral economy [

23]. In 2022, The European Commission approved another investment framework for subsidies worth more than EUR 380 million for 168 new projects under the LIFE program, representing a 27% increase over the previous program’s figures. EU funding under LIFE will mobilize this investment of over EUR 562 million in projects targeting nature, the environment, climate action, and the clean energy transition. Actions will take place in almost all EU Member States. Therefore, the next tranche of grant funding may significantly increase the interest of local companies and international entities in investing in the construction of installations for the production of bioethanol.

In the third group, six factors, namely,

C314,

C313,

C322,

C331,

C332, and

C341, were identified. This different group included factors of waste material production taxation, as well as Polish subsidies for the purchase of different raw materials (wood, straw, maize, and grass). In line with previous reports [

23], the biofuel taxation law regulations represent a significant aspect that may affect the development of spirit fuel production in Poland. The Minister of Finance Decree of 23 December 2003 on Excise Tax was issued to facilitate the production and blending of biofuel fuels. The profitability of using biofuels comes from low excise rates to support farmers’ income, environmental protection, job creation, and fuel safety. Therefore, in Poland, liquid biofuels are less expensive than fuel oils with excise duty. Poland’s renewable energy transport policy focuses on biofuels. Under the Energy Policy Review, Poland has targeted the increase to a 10% renewable energy share in transport by 2020 and 14% by 2030, whereas the real percentage share in 2020 was 6.6% [

32]. Similar to many EU Members, Poland’s main policy mechanism for achieving its RES targets is the biofuel blending obligation. It requires all companies that manufacture or import transport fuels to minimize their share of biofuels according to the energy content of their annual fuel turnover for all modes of transport. Companies that reach 85% of the required mix ratio are eligible to pay a replacement fee in exchange for fully achieving the target. Biofuels are taxed at the same rate as blended fuels. Therefore, Poland aims to maximize local production of biofuels as part of its goal of promoting domestic energy sources. Bioethanol production in 2020 was approximately 0.3 Mt, compared to 0.2 Mt in 2015, and the capacity was approximately 0.7 Mt. Biodiesel production was approximately 0.9 Mt, compared to 0.75 Mt in 2015, with a production capacity of approximately 1.4 Mt., which covers most of the domestically produced Polish biofuel needs.

Twelve factors were included in the last group, whose “system priority weight” of the whole range is quite significant, but the range significance resulted solely from the large number of factors included in this range. The average value of the fourth range significance factor was only 2.81 points, implying no major effect on the economic effects of the production of second-generation bioethanol in Poland.

3.4. Game Theory as an Optimal Tool in the Selection of an Optimum Production Strategy for Second-Generation Bioethanol in Poland

The most rational direction for solving the problem of economic efficiency of the production of second-generation bioethanol was the selection of an optimum strategy for its production. As a result of expert mathematical analysis, the economic efficiency of the production of bioethanol may be primarily affected by the cost of acquisition of raw materials and the amounts of the EU subsidies for the production of raw materials. To analyze the most cost-effective production strategies in the incoherent economic and social environment, the game theory was applied. Three main production scenarios have been highlighted from unfavorable Y2 through to average Y3 and favorable Y4. To ensure the full orthogonality of the considered interval, it was additionally extended by 21.5% to very unfavorable Y1 and very favorable Y5 states. The production costs of second-generation bioethanol from different raw materials were calculated in all distinguished scenarios from very pessimistic (Y1) to very optimistic (Y5).

The pessimistic and optimistic variants were determined through the expert mathematical method (

Table 4), with the index of the increase in the production cost for the pessimistic cases and the decrease in this index for the optimistic variants in comparison with the basic case.

Based on the index of an increase or decrease in the cost of production of second-generation bioethanol in Poland (

Table 4), the costs of production of this fuel have been determined for individual raw materials and possible conditions of the economic and social environment that the producers of second-generation bioethanol may face in Poland (

Table 5).

To determine the optimum economic efficiency of the production of second-generation bioethanol from the raw materials analyzed in Poland, in consideration of a diversified economic and social environment, ranging from extremely favorable to extremely unfavorable, five individual selection criteria were used, i.e., maximum mean reward, minimum mean risk, maximum pessimism, minimum risk, and pessimism-optimism. For this purpose, the unit costs of bioethanol production were transformed by the methodology of the individual choice theory into unit cost indices for the three criteria under consideration and risk size indices for the two remaining criteria (

Figure 6).

The optimum strategy of bioethanol production in Poland was adopted as the one with the largest number of indications in the individual criteria with the minimum identified production costs or minimum risk of increase in production costs depending on changes in the economic and social environment. After the comparison of individual strategies, the final strategy of bioethanol production should be based on the minimal possible production costs and minimal possible risk of production costs increase. The data presented in

Figure 6 indicate that the production of second-generation bioethanol in Poland from wood waste represents the optimum production scenario. According to three main choice criteria, i.e., the criterion of maximum win, the criterion of maximum risk, and the criterion of optimism-pessimism, the possible bioethanol unit production costs represent the lowest value among all analyzed raw materials. Furthermore, according to the fourth criterion—maximum average risk—the production of second-generation bioethanol seems to be optimal. According to the fifth criterion, in the changing economic and social environments analyzed, the production of this fuel is equivalent to that of all the raw materials analyzed. The production of bioethanol from other feedstocks such as maize, catch crops, straw, and grasses is very similar in terms of the possibility of changes in the costs of their production, as well as the size of the risk of these changes, according to all five criteria of individual choice.

3.5. Second-Generation Bioethanol Cost Production Estimation in Poland—Study Case

A case study of bioethanol cost production in Poland was adopted both in technical preferences regarding the installation design (presented in

Section 3.1) and economic parameters of fixed and variable costs, of which the simulation is presented below. Based on the proposed installation scheme, the production line with a capacity of 315 L of spirits per hour was used to analyze the costs of spirits fuel production. As an optimal raw material for the production strategy, the wood chips were selected, based on the prepared expert mathematical method with elements of game theory.

Production line. The proposed production line for bioethanol production included the following elements: A chipper, belt conveyor, tank with a stirrer, pump, drum filter, chromatographic separator, fermenter, membrane module, pipes, sulphuric acid condenser, tank for the finished product, and scales. The individual elements of the production line for the production of second-generation spirit fuel together with their number and price were selected by the analysis of commercial offers of suppliers operating in the Polish market (

Table 6).

The total cost of the production line for the production of second-generation bioethanol amounts to EUR 264,399 (

Table 6). For the proposed installation, depreciation costs can be determined assuming the number of years of use of the production line. To depreciate fixed assets, we assumed a 20-year period of their use, which means that the annual depreciation costs will amount to EUR 13,220. It is worth mentioning that the purchase price of the primary equipment was obtained from local equipment suppliers. However, if the suppliers and proposed equipment type did not match, the estimated costs of the proposed technological components may be different. Data presented in

Table 6 indicate the favorable level of production installation costs. The studies previously reported in the literature show that estimated installation investment can vary from 340,000 up to over 57,200,000 EUR, depending on the production equipment capacities and advancement of line automation [

33,

34]. Nevertheless, we envisage that the bioethanol industry practice concentrates on decreasing the investment outlays by multiplying the total installation purchase by a minimum of three times, which allows for obtaining a total value investment almost 50% lower [

33]. Thus, there is still space for further optimization of the installation purchase expenditures of the proposed technological line for second-generation bioethanol production.

Cost of rent and security of production area. To calculate the cost of renting the premises, the necessary technological space has been identified and characterized into four distinguished production zones: (1) Pre-treatment, where the wood chipper and raw material storage will be located; (2) hydrolysis, where a tank with a stirrer, pump, drum filter, tank with a stirrer, pump, drum filter, chromatograph, tank with a stirrer, and centrifuge will be; (3) fermentation: Fermentation tanks and membrane module; and (4) warehouse for finished products, with a tank with the finished product. In the pre-treatment area, space for the chipper and a stock of raw material is needed. Assuming wood deliveries are made regularly every week, a weekly storage place for the stock should be determined. According to the demand of the production line, 1500 kg of wood is used within 1 h, while the weekly demand, including 20% of the stock, is 152,000 kg. The necessary storage area for the weekly storage of such a quantity of wood is S

1 = 40 m

2. The second zone must include three tanks with an agitator, two pumps, two drum filters, a chromatograph, and a centrifuge. Summing up the necessary areas for the installation of the above-mentioned machines, we obtain the area of 24 m

2, and upon adding the area required for paths for employees of 10 m

2 to this, we obtain the total area of the second zone of 34 m

2. In zone three, space should be provided for a fermenter and a membrane module to concentrate the ethanol solution. The total area of this zone, including the added area for technical paths, is 37.25 m

2. The fourth zone is the storage area. It was assumed that the quantity of bioethanol produced in a month would be 226,800 L with the necessary storage area of 100 m

2. By summing up the areas of all zones, the total production and storage area is 240 m

2. For technological space, the average monthly rental cost in Poland amounts to 660 EUR per month, which will amount to ca. 8000 EUR/year. The production of spirit fuel in Poland is subject to excise tax. To be able to store and produce such material, it is necessary to obtain a permit for a tax warehouse. Concerning the specific legal requirements and Polish tax policy, the average annual costs of monitoring can be settled at 11,265 EUR with the total cost of renting a production hall of 19,155 EUR/year. The analysis of fixed production costs of bioethanol based on published data shows that the spatial organization of the production of second-generation bioethanol, together with the costs of purchasing production equipment and auxiliary materials, is a variable issue, depending on the geographical and geopolitical location of the production site [

15]. In line with previously reported bioethanol production models, our assumptions are based on official statistical reports of the cost of raw materials and energy published by local government institutions, as well as personal communication with suppliers of production solutions [

35]. For this reason, the analysis of various geographical conditions of bioethanol production can be a very variable element, and the analysis of its variance can be an interesting aspect of further research.

Variable costs. In the proposed installation for second-generation bioethanol production, variable costs include the costs of raw materials, costs of purchasing water and sulphuric acid, labor costs, and costs of electricity. Cost of materials. To determine the costs of all necessary raw materials, the aforementioned costs have to be calculated: (1) The amount of wood, which will be based on the technological demand for lignin-cellulose content (the content of lignin-cellulose in wood is approximately 95%, which differs for various waste biomass); (2) the purchase cost of sulphuric acid, which is a one-off expense because it is recovered in the production process; (3) technological medium cost (water). Lignin. Lignin is not subject to hydrolysis and is therefore disposed of into the environment during processing. Only wood with cellulose and hemicellulose content of approximately 75% can be used for fermentation. Cellulose. The hydrolysis process has to be recalculated separately for cellulose and hemicellulose because, during hydrolysis, each substance is converted into different sugars. In the case of cellulose, it hydrolyses by converting it into glucose. The efficiency of the hydrolysis process must be taken into account. During single hydrolysis, an efficiency of approximately 67% can be achieved. When hydrolysis occurs twice, the yield is increased to approximately 89% [

9]). By recalculating the capacity, it is possible to determine the amounts of the obtained components capable of further fermentation. For ease of use, all calculations will be calculated for the conversion of 1 kg of wood. The amount of glucose produced from 1 kg of wood is 0.445 kg. It can also be assumed that this is the amount of hexose produced, because glucose, having six carbon atoms in its molecule, belongs to this group of sugars. Hemicellulose. In the case of hemicellulose, it hydrolyses into pentose and hexose sugars. Each hydrolysis should be considered separately since pentoses and hexoses have different molecular masses [

13]. Hemicellulose consists of pentosanes (approximately 60%) and hexosanes (40%). The total amount of hexose obtained should be calculated by summing up the amount of glucose obtained from cellulose and pentoses from pentosanes from 1 kg of wood to 0.565 kg. The total amount of ethanol obtained from 1 kg of wood is 0.33 kg. Since the easiest method is to calculate the cost of fuel per unit of volume, i.e., in liters, the amount obtained should be converted taking into account the density of the product. Thanks to the final thickening stage, ethanol with a concentration of approximately 99% can be achieved. At this concentration, the density of ethanol is 0.79243 g/cm

3, which is 0.42 L.

Material flow during the production process. Analyzing the selected installation and hydrolysis reaction rate makes it possible to assume an input material flow of 500 L/h. Taking into account the bulk density of wood, it is possible to calculate the amount of input material for 750 kg/h, which results in an annual demand of 6,480,000 kg of wood, and its annual cost is EUR 228,100. The same methodology was used to calculate the costs of other raw materials (

Table 7).

The costs of purchasing raw materials for the production of second-generation bioethanol range from 228,170 EUR to 496,900 EUR (

Table 5). The presented empirical ethanol production effectiveness ranged from 0.28 to 0.33 kg/kg of raw material used, which represents values similar to those previously reported in the literature [

36,

37]. According to the analysis of literature data, the production of ethanol from wood waste may be one of the most cost-effective production solutions, despite the greatest difficulties with the hydrolysis of the input material [

38,

39].

Our findings from the cost analysis supported by the selection of production conditions via game theory confirmed that an appropriately high ratio of lignin-cellulose with the lowest purchasing price from analyzed materials represents the most cost-efficient raw material from second-generation bioethanol in Poland. The most effective ethanol production unit was obtained from wood chips (0.33 kg/kg of wood used) with the total annual row material purchasing price that can be positively compared to previously reported studies on bioethanol production costs from different materials [

40]. Water, as a technological medium, is necessary both in the hydrolysis process and in the HPLC chromatography as an eluent. To calculate the amount of water required, the amount of water needed for hydrolysis of cellulose and hemicellulose 1036.8 tonnes/year should be added up, which, at the price of 0.6 EUR per tonne, gives a total of 632 EUR/year. Waste wood is a valued resource that may be used either for material recycling or energy production, depending on the quality grade. The waste wood is available in large volumes as wood residue chips (from untreated wood residues, recycled wood, and off-cuts), forest chips (from forested areas), short rotation forestry chips (from energy crops), and sawing residue chips (from sawmill residues) [

41]. The rising cost of waste material disposal and the growing consciousness of the environment also contribute to the increasing importance of waste wood recycling. In Poland, the average purchase price per kilogram of wood is approximately 0.1 EUR/kg [

29]. In the case of tonnage purchases, the purchase price can even be reduced to 0.04 EUR/kg (this price of wood was used for further calculations). Converting this quantity into liters results in 0.1 EUR/L of raw material.

Labor cost. In the presented technological line for second-generation bioethanol production, the very process of production is automatic, so an employee is not needed for every position. Since the product can operate for 24 h, shift work should be added. Considering that the day is 24 h old, the working time of a quality control specialist should be converted into three shifts of eight hours each. In the case of a technologist, two shifts of eight hours will suffice. To summarize, four quality control specialists and three technologists should be recruited. In

Table 8, the total monthly subsistence costs of the staff are presented. Thus, the monthly labor costs of people amount to EUR 9160, while annual labor costs amount to EUR 110,000 (detailed data are presented in

Table 8).

Electricity costs. Electricity in the production line of second-generation spirit fuels is necessary to drive working elements and heat or cool down individual machines. Electricity will also be needed to illuminate the production premises and as a source of energy in control equipment. It is estimated that, on average, machines and equipment will consume 65 kWh of energy per hour, which represents 569,400 kWh of energy annually. The current price of 1 kWh of energy for medium-sized enterprises is 0.11 EUR/kWh, so the annual costs of electricity consumption will amount to 61,485 EUR/year.

The annual costs of second-generation bioethanol production in Poland. Annual production costs of second-generation spirit fuel, assuming production of 315 L/h, amount to ca. 433,150 EUR/year (

Table 9). In the structure of these costs, fixed costs constitute 7.47%, while variable costs constitute 92.53%. In the structure of variable costs, the highest item is the cost of raw material (used wood) at 52.82%, which is more than twice as high as labor costs.

The production costs of 1 L of second-generation ethanol were determined based on the production line capacity of 315 L/h, while the annual operating time was 8600 h.

The presented unit production cost of 1 L of second-generation spirit fuel is EUR 0.16. The use of wood chips obtained from forestry or post-production waste products allowed the production of 0.33kg/kg of raw wood chips with a unit production cost of 0.16 EUR/L g when using the production line capacity of 315 L/h, which represents lower production costs than previously reported in the literature. As presented by Randelli et al., the costs per liter of bioethanol production can vary from 0.24 for sugarcanes to 0.57 for sugar beets [

43]. Tran and Yanagida proposed the unit cost of bioethanol produced from banana grass with a minimum value of 0.18 USD/L [

44], which is similar to but still above the value proposed for production in Poland. At this point, it should be noted that the assumptions used in the calculations are based on average prices for wood, water, and electricity in 2021 in Poland. In the case of changes in the average prices of the variable cost elements, the unit cost of production of 1 L of bioethanol will change proportionally; however, the methodology presented above will still be a universal tool allowing quick estimation of the adjusted unit cost of production. Thus, the proposed work entails an advance toward the production of hemicellulose-based ethanol from wood chips. The presented methodology allows for the identification of the most favorable production conditions from various raw materials and presents a universal tool for estimating the cost of bioethanol production from various sources.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}