The Impact of Competitive Strategies on Performance of Banking Sector; The Mediating Role of Corporate Social Responsibility and Operational Excellence

Abstract

1. Introduction

2. Literature Review

2.1. Theoretical Background

2.2. Cost-Sensitive Strategy and Performance

2.3. Differentiation Strategy and Performance

2.4. Competitive Strategy and Performance: The Role of CSR Practices

2.5. Competitive Strategy and Performance: The Role of Operational Excellence

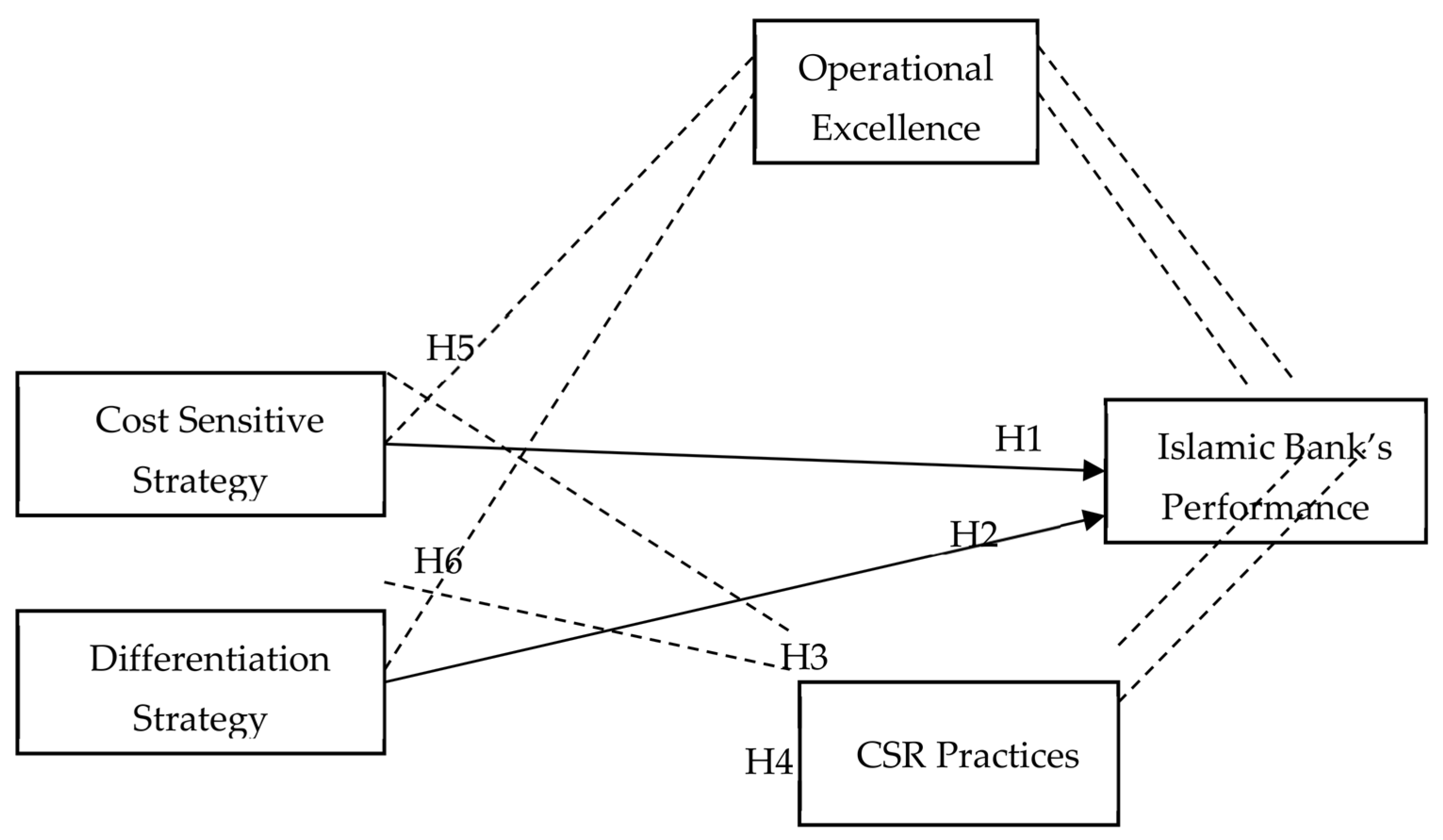

3. Materials and Methods

3.1. Sample Selection and Data

3.2. Measures

4. Results

4.1. Preliminary Analysis

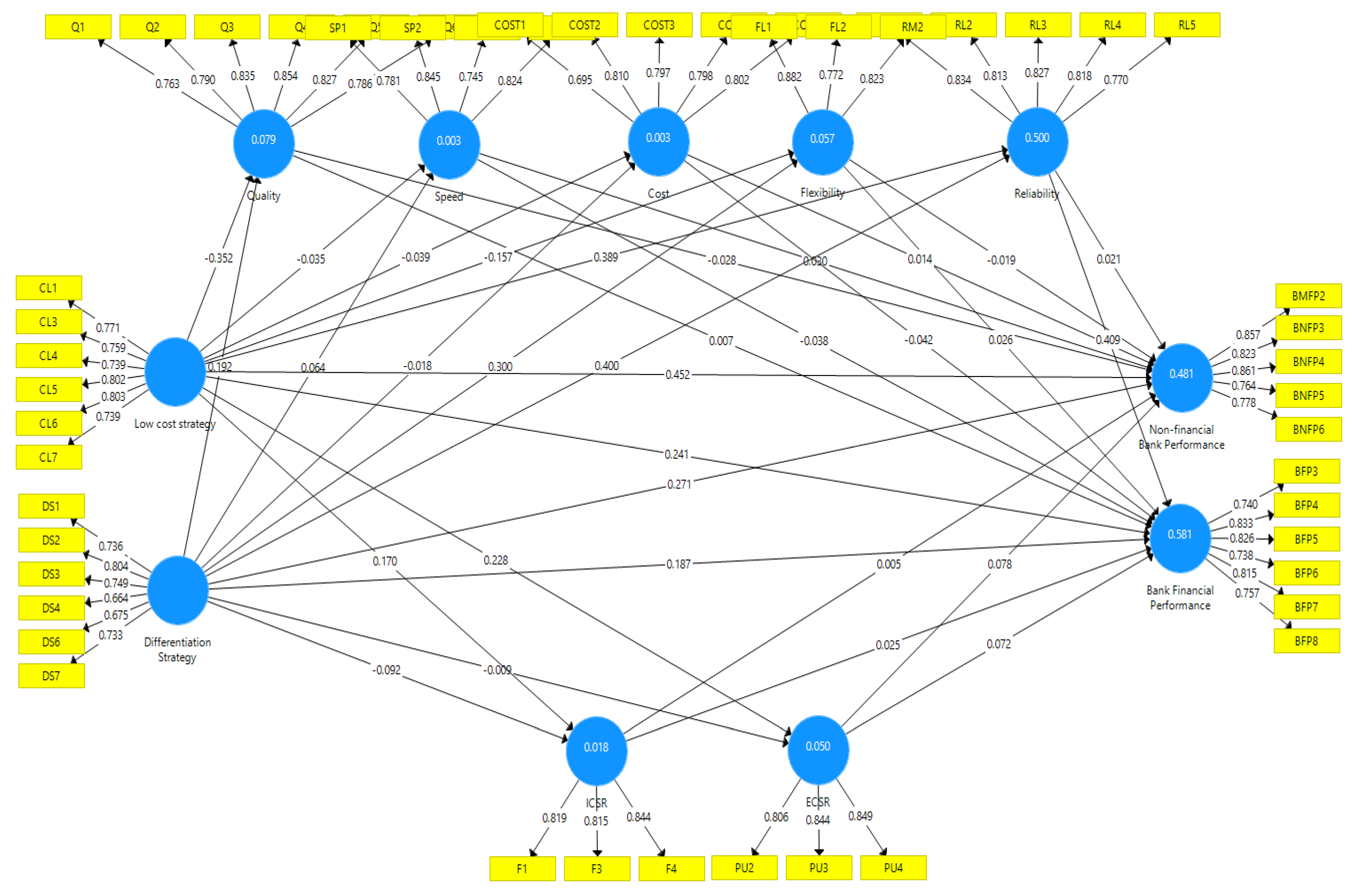

4.2. Assessment of Measurement Model

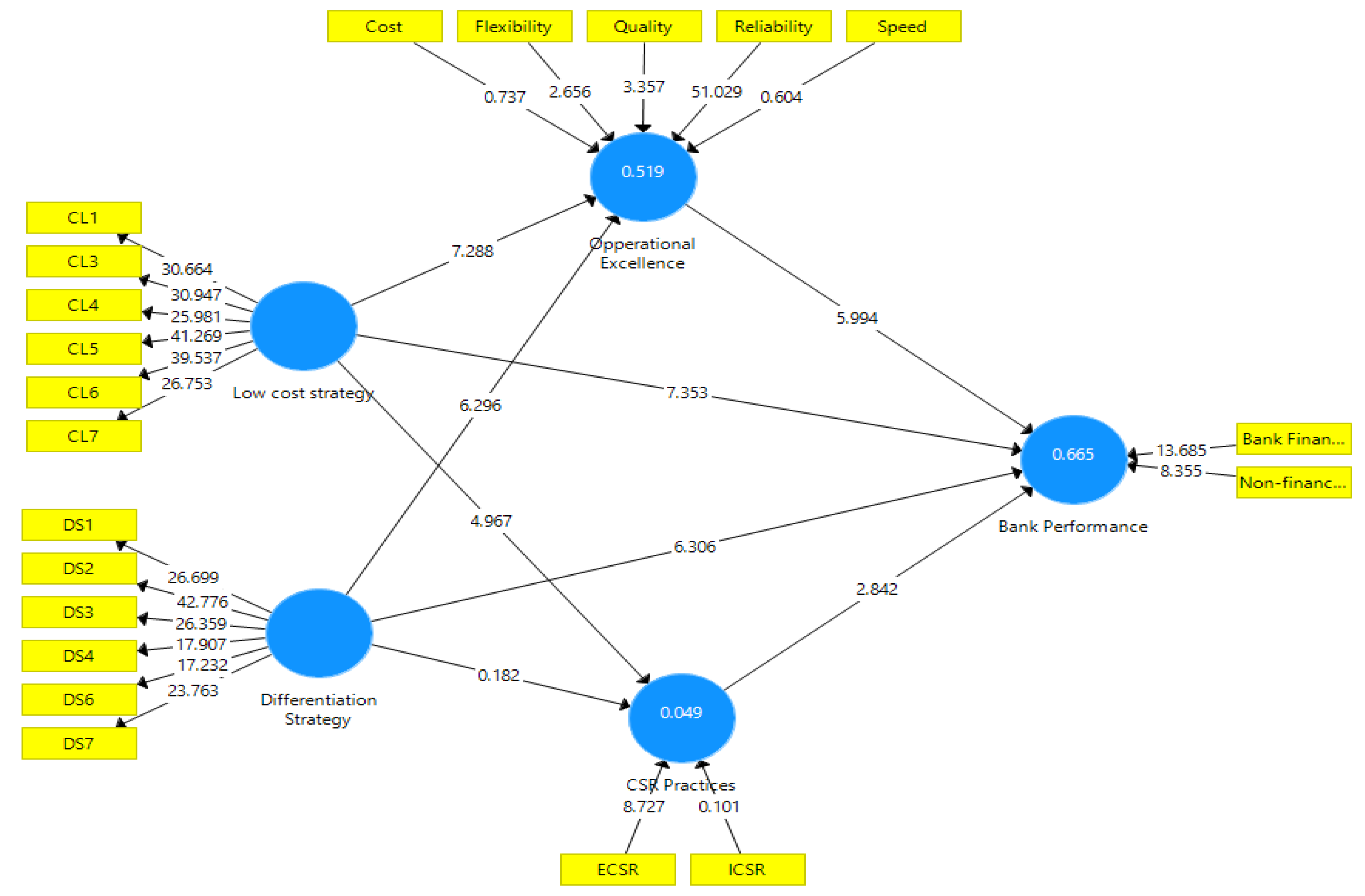

4.3. Structural Model Assessment

4.4. Robustness Test

5. Discussion

6. Conclusions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Ali, W.; Alasan, I.I.; Khan, M.H.; Ali, S.; Cheah, J.-H.; Ramayah, T. Competitive strategies-performance nexus and the mediating role of enterprise risk management practices: A multi-group analysis for fully fledged Islamic banks and conventional banks with Islamic window in Pakistan. Int. J. Islam. Middle East. Finance Manag. 2022, 15, 125–145. [Google Scholar] [CrossRef]

- Beck, T.; De Jonghe, O.; Schepens, G. Bank competition and stability: Cross-country heterogeneity. J. Financ. Intermediation 2013, 22, 218–244. [Google Scholar] [CrossRef]

- Clark, E.; Radić, N.; Sharipova, A. Bank competition and stability in the CIS markets. J. Int. Financial Mark. Inst. Money 2018, 54, 190–203. [Google Scholar] [CrossRef]

- Ijaz, S.; Hassan, A.; Tarazi, A.; Fraz, A. Linking bank competition, financial stability, and economic growth. J. Bus. Econ. Manag. 2020, 21, 200–221. [Google Scholar] [CrossRef]

- Abedifar, P.; Molyneux, P.; Tarazi, A. Risk in Islamic banking. Rev. Financ. 2013, 17, 2035–2096. [Google Scholar] [CrossRef]

- Ali, W.; Alasan, I.I.; Khan, M.H.; Ramayah, T. Strategy Is All About Deliberately Making Choices and Trade-Offs: Analogy Betweenfully-Fledged Islamic Banks and Conventional Banks with Islamic Windows. Acad. Entrep. J. 2021, 27, 1–15. [Google Scholar]

- Hunjra, A.I.; Boubaker, S.; Arunachalam, M.; Mehmood, A. How does CSR mediate the relationship between culture, religiosity and firm performance? Financ. Res. Lett. 2021, 39, 101587. [Google Scholar] [CrossRef]

- Barney, J.B.; Clark, D.N. Resource-Based Theory: Creating and Sustaining Competitive Advantage; OUP Oxford: Oxford, UK, 2007. [Google Scholar]

- Karam, C.M.; Jamali, D. A Cross-Cultural and Feminist Perspective on CSR in Developing Countries: Uncovering Latent Power Dynamics. J. Bus. Ethics 2017, 142, 461–477. [Google Scholar] [CrossRef]

- Jamali, D.; Neville, B. Convergence Versus Divergence of CSR in Developing Countries: An Embedded Multi-Layered Institutional Lens. J. Bus. Ethics 2011, 102, 599–621. [Google Scholar] [CrossRef]

- Lui, T.K.; Zainuldin, M.H.; Wahidudin, A.N.; Foo, C.C. Corporate social responsibility disclosures (CSRDs) in the banking industry: A study of conventional banks and Islamic banks in Malaysia. Int. J. Bank Mark. 2021, 39, 541–570. [Google Scholar] [CrossRef]

- Porter, M.E. The Contributions of Industrial Organization to Strategic Management. Acad. Manag. Rev. 1981, 6, 609–620. [Google Scholar] [CrossRef]

- Becker, J.-M.; Klein, K.; Wetzels, M. Hierarchical Latent Variable Models in PLS-SEM: Guidelines for Using Reflective-Formative Type Models. Long Range Plan. 2012, 45, 359–394. [Google Scholar] [CrossRef]

- Bayraktar, C.A.; Hancerliogullari, G.; Cetinguc, B.; Calisir, F. Competitive strategies, innovation, and firm performance: An empirical study in a developing economy environment. Technol. Anal. Strat. Manag. 2017, 29, 38–52. [Google Scholar] [CrossRef]

- Islami, X.; Mustafa, N.; Latkovikj, M.T. Linking Porter’s generic strategies to firm performance. Futur. Bus. J. 2020, 6, 1–15. [Google Scholar] [CrossRef]

- Rehman, A.U.; Anwar, M. Mediating role of enterprise risk management practices between business strategy and SME performance. Small Enterp. Res. 2019, 26, 207–227. [Google Scholar] [CrossRef]

- Barney, J.B. Firm Resources and Sustained Competitive Advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Barney, J.B. Is the Resource-Based “View” a Useful Perspective for Strategic Management Research? Yes. Acad. Manag. Rev. 2001, 26, 41. [Google Scholar] [CrossRef]

- Sun, L.-Y.; Pan, W. Differentiation strategy, high-performance human resource practices, and firm performance: Moderation by employee commitment. Int. J. Hum. Resour. Manag. 2011, 22, 3068–3079. [Google Scholar] [CrossRef]

- Prajogo, D.; Sohal, A.S. The relationship between organization strategy, total quality management (TQM), and organization performance—The mediating role of TQM. Eur. J. Oper. Res. 2006, 168, 35–50. [Google Scholar] [CrossRef]

- Tatoglu, E.; Frynas, J.G.; Bayraktar, E.; Demirbag, M.; Sahadev, S.; Doh, J.; Koh, S.C.L. Why do Emerging Market Firms Engage in Voluntary Environmental Management Practices? A Strategic Choice Perspective. Br. J. Manag. 2020, 31, 80–100. [Google Scholar] [CrossRef]

- Porter, M.E.; Strategy, C. Techniques for Analyzing Industries and Competitors. Competitive Strategy; Free Press: New York, NY, USA, 1980. [Google Scholar]

- Porter, M.E. Competitive Strategy. Measuring Business Excellence; MCB UP Ltd.: Bingley, UK, 1997. [Google Scholar]

- Kankam-Kwarteng, C.; Osman, B.; Donkor, J. Innovative low-cost strategy and firm performance of restaurants. Asia Pac. J. Innov. Entrep. 2019, 13, 266–281. [Google Scholar] [CrossRef]

- Yuliansyah, Y.; Rammal, H.G.; Rose, E. Business strategy and performance in Indonesia’s service sector. J. Asia Bus. Stud. 2016, 10, 164–182. [Google Scholar] [CrossRef]

- Birjandi, H.; Jahromi, N.M.; Darabi, S.A.; Birjandi, M. The effect of cost leadership strategy on ROA and future perfor-mance of accepted companies in Tehran Stock Exchange. Res. J. Financ. Account. 2014, 5, 152–159. [Google Scholar]

- Teeratansirikool, L.; Siengthai, S.; Badir, Y.; Charoenngam, C. Competitive strategies and firm performance: The mediating role of performance measurement. Int. J. Prod. Perform. Manag. 2013, 62, 168–184. [Google Scholar] [CrossRef]

- Semuel, H.; Siagian, H.; Octavia, S. The Effect of Leadership and Innovation on Differentiation Strategy and Company Performance. Procedia Soc. Behav. Sci. 2017, 237, 1152–1159. [Google Scholar] [CrossRef]

- Li, J.J.; Zhou, K.Z. How foreign firms achieve competitive advantage in the Chinese emerging economy: Managerial ties and market orientation. J. Bus. Res. 2010, 63, 856–862. [Google Scholar] [CrossRef]

- Soltanizadeh, S.; Rasid, S.Z.A.; Golshan, N.M.; Ismail, W.K.W. Business strategy, enterprise risk management and organizational performance. Manag. Res. Rev. 2016, 39, 1016–1033. [Google Scholar] [CrossRef]

- Ascarya, A.; Yumanita, D. Mencari Solusi Rendahnya Pembiayaan Bagi Hasil di Perbankan Syariah Indonesia. Bul. Èkon. Monet. Perbank. 2005, 8, 7–43. [Google Scholar] [CrossRef]

- Laela, S.F.; Rossieta, H.; Wijanto, S.H.; Ismal, R. Management accounting-strategy coalignment in Islamic banking. Int. J. Islam. Middle East. Financ. Manag. 2018, 11, 667–694. [Google Scholar] [CrossRef]

- Rachmawati, E.; Syamsulhakim, E. Factors affecting mudaraba deposits in Indonesia. In Proceedings of the Third International Islamic Banking and Finance Conference, Karachi, Pakistan, 27–28 October 2008. [Google Scholar]

- Hafez. Measuring the impact of corporate social responsibility practices on brand equity in the banking industry in Bangladesh. Int. J. Bank Mark. 2018, 36, 806–822. [Google Scholar] [CrossRef]

- Falcón, J.P.; Asis, R.; Arana, V.; Muñoz, E.; Raza, M. Corporate Social Responsibility and Socio-Environmental Conflicts in Peruvian Mining Company. J. Environ. Manag. Tour. 2022, 13, 1251–1258. [Google Scholar] [CrossRef] [PubMed]

- Droppert, H.; Bennett, S. Corporate social responsibility in global health: An exploratory study of multinational pharmaceutical firms. Glob. Health 2015, 11, 15. [Google Scholar] [CrossRef] [PubMed]

- Luu, D.T. The effect of internal corporate social responsibility practices on pharmaceutical firm’s performance through employee intrapreneurial behaviour. J. Organ. Chang. Manag. 2020, 33, 1375–1400. [Google Scholar] [CrossRef]

- Waheed, A.; Zhang, Q.; Zafar, A.U.; Zameer, H.; Ashfaq, M.; Nusrat, A. Impact of internal and external CSR on organizational performance with moderating role of culture: Empirical evidence from Chinese banking sector. Int. J. Bank Mark. 2021, 39, 499–515. [Google Scholar] [CrossRef]

- Carmeli, A.; Gilat, G.; Waldman, D.A. The Role of Perceived Organizational Performance in Organizational Identification, Adjustment and Job Performance. J. Manag. Stud. 2007, 44, 972–992. [Google Scholar] [CrossRef]

- Lichtenstein, D.R.; Drumwright, M.E.; Braig, B.M. The Effect of Corporate Social Responsibility on Customer Donations to Corporate-Supported Nonprofits. J. Mark. 2004, 68, 16–32. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D.S.; Wright, P.M. Corporate Social Responsibility: International Perspectives. SSRN 2006, 900834. [Google Scholar] [CrossRef]

- Siegel, D.S.; Vitaliano, D.F. An Empirical Analysis of the Strategic Use of Corporate Social Responsibility. J. Econ. Manag. Strat. 2007, 16, 773–792. [Google Scholar] [CrossRef]

- Flammer, C. Competing for government procurement contracts: The role of corporate social responsibility. Strat. Manag. J. 2018, 39, 1299–1324. [Google Scholar] [CrossRef]

- Flynn, B.B.; Flynn, E. An exploratory study of the nature of cumulative capabilities. J. Oper. Manag. 2004, 22, 439–457. [Google Scholar] [CrossRef]

- Kannan, V.R.; Jayaram, J.; Narasimhan, R. Acquisition of operations capability: A model and test across US and European firms. Int. J. Prod. Res. 2004, 42, 833–851. [Google Scholar] [CrossRef]

- Dutta, S.; Narasimhan, O.; Rajiv, S. Success in High-Technology Markets: Is Marketing Capability Critical? Mark. Sci. 1999, 18, 547–568. [Google Scholar] [CrossRef]

- Evans, J.; Lindsay, W. The Management and Control of Quality, South-Western, Cengage Learning. ISBN 2011, 13, 978–1002. [Google Scholar]

- Porter, M.E. What is strategy? Harv. Bus. Rev. 1996, 74, 61–78. [Google Scholar]

- Andersson, C.; Bellgran, M. On the complexity of using performance measures: Enhancing sustained production improvement capability by combining OEE and productivity. J. Manuf. Syst. 2015, 35, 144–154. [Google Scholar] [CrossRef]

- Eisenhardt, K.; Martin, J. Dynamic Capabilities. What are they? Strateg. Manag. J. 2000, 21, 1105–1121. [Google Scholar] [CrossRef]

- Wu, S.J.; Melnyk, S.A.; Flynn, B.B. Operational Capabilities: The Secret Ingredient. Decis. Sci. 2010, 41, 721–754. [Google Scholar] [CrossRef]

- Teece, D.J. The Foundations of Enterprise Performance: Dynamic and Ordinary Capabilities in an (Economic) Theory of Firms. Acad. Manag. Perspect. 2014, 28, 328–352. [Google Scholar] [CrossRef]

- Sehnem, S.; Jabbour, C.J.C.; Pereira, S.C.F.; de Sousa Jabbour, A.B.L. Improving sustainable supply chains performance through operational excellence: Circular economy approach. Resour. Conserv. Recycl. 2019, 149, 236–248. [Google Scholar] [CrossRef]

- Perona, M.; Miragliotta, G. Complexity management and supply chain performance assessment. A field study and a conceptual framework. Int. J. Prod. Econ. 2004, 90, 103–115. [Google Scholar] [CrossRef]

- Hassan, S.S.U.; Hussain, M.A.; Sajid, S. The effectiveness of anti-money laundering legislation in Islamic banking of Pakistan: Experts’ opinion. J. Money Laund. Control 2022, 25, 135–149. [Google Scholar] [CrossRef]

- Johansen, M.B.; Frederiksen, J.T. Ethically important moments—A pragmatic-dualist research ethics. J. Acad. Ethics 2021, 19, 279–289. [Google Scholar] [CrossRef]

- Emmerling, S.A.; Astroth, K.S.; Kim, M.J.; Woith, W.M.; Dyck, M.J. A comparative study of social capital and hospital readmission in older adults. Geriatr. Nurs. 2019, 40, 25–30. [Google Scholar] [CrossRef] [PubMed]

- Santa, R.; MacDonald, J.B.; Ferrer, M. The role of trust in e-Government effectiveness, operational effectiveness and user satisfaction: Lessons from Saudi Arabia in e-G2B. Gov. Inf. Q. 2019, 36, 39–50. [Google Scholar] [CrossRef]

- Tehseen, S.; Ramayah, T.; Sajilan, S. Testing and Controlling for Common Method Variance: A Review of Available Methods. J. Manag. Sci. 2017, 4, 142–168. [Google Scholar] [CrossRef]

- Fischer, D.G.; Fick, C. Measuring Social Desirability: Short Forms of the Marlowe-Crowne Social Desirability Scale. Educ. Psychol. Meas. 1993, 53, 417–424. [Google Scholar] [CrossRef]

- Hair, F.H., Jr.; Hult, G.T.M., Jr.; Ringle, C.M.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM); Sage Publications: New York, NY, USA, 2021. [Google Scholar]

- Wisetsri, W.; Chuaytukpuan, T.; Prompanyo, M.; Raza, M.; Cavaliere, L.P.L.; Akhter, S. Impact of Psychological Capital and Technology Adaptation on Performance of Teachers. J. Posit. Sch. Psychol. 2022, 8784–8793. [Google Scholar]

- Ringle, C.M.; Wende, S.; Becker, J.-M. SmartPLS 3. Boenningstedt SmartPLS GmbH 2015, 3, 584. [Google Scholar]

- Faul, F.; Erdfelder, E.; Buchner, A.; Lang, A.-G. Statistical power analyses using G*Power 3.1: Tests for correlation and regression analyses. Behav. Res. Methods 2009, 41, 1149–1160. [Google Scholar] [CrossRef]

- Chin, W.W.; Thatcher, J.B.; Wright, R.T.; Steel, D. Controlling for Common Method Variance in PLS Analysis: The Measured Latent Marker Variable Approach. In New Perspectives in Partial Least Squares and Related Methods; Springer: Berlin/Heidelberg, Germany, 2013; pp. 231–239. [Google Scholar] [CrossRef]

- Cohen, J. A Power Primer (Methodological Issues and Strategies in Clinical Research), 4th ed.; American Psychological Association: Washington, DC, USA, 2016; pp. 279–284. [Google Scholar]

- Dijkstra, T.K.; Henseler, J. Consistent and asymptotically normal PLS estimators for linear structural equations. Comput. Stat. Data Anal. 2015, 81, 10–23. [Google Scholar] [CrossRef]

- Hair, J.; Hollingsworth, C.L.; Randolph, A.B.; Chong, A.Y.L. An updated and expanded assessment of PLS-SEM in information systems research. Ind. Manag. Data Syst. 2017, 117, 442–458. [Google Scholar] [CrossRef]

- Hair, J.F.; Ringle, C.M.; Sarstedt, M. PLS-SEM: Indeed a silver bullet. J. Mark. Theory Pract. 2011, 19, 139–152. [Google Scholar] [CrossRef]

- Hair, J.F.; Risher, J.J.; Sarstedt, M.; Ringle, C.M. When to use and how to report the results of PLS-SEM. Eur. Bus. Rev. 2019, 31, 2–24. [Google Scholar] [CrossRef]

- Fornell, C.; Larcker, D.F. Structural equation models with unobservable variables and measurement error: Algebra and statistics. J. Mark. Res. 1981, 18, 382–388. [Google Scholar] [CrossRef]

- Henseler, J.; Ringle, C.M.; Sarstedt, M. A new criterion for assessing discriminant validity in variance-based structural equation modeling. J. Acad. Mark. Sci. 2015, 43, 115–135. [Google Scholar] [CrossRef]

- Ahrholdt, D.C.; Gudergan, S.P.; Ringle, C.M. Enhancing loyalty: When improving consumer satisfaction and delight matters. J. Bus. Res. 2019, 94, 18–27. [Google Scholar] [CrossRef]

- Benitez, J.; Henseler, J.; Castillo, A.; Schuberth, F. How to perform and report an impactful analysis using partial least squares: Guidelines for confirmatory and explanatory IS research. Inf. Manag. 2019, 57, 103168. [Google Scholar] [CrossRef]

- Sarstedt, M.; Ringle, C.M.; Cheah, J.-H.; Ting, H.; I Moisescu, O.; Radomir, L. Structural model robustness checks in PLS-SEM. Tour. Econ. 2020, 26, 531–554. [Google Scholar] [CrossRef]

- Hult, G.T.M.; Hair, J.F.; Proksch, D.; Sarstedt, M.; Pinkwart, A.; Ringle, C.M. Addressing Endogeneity in International Marketing Applications of Partial Least Squares Structural Equation Modeling. J. Int. Mark. 2018, 26, 1–21. [Google Scholar] [CrossRef]

- De Los Salmones, M.D.M.G.; Crespo, A.H.; Del Bosque, I.R. Influence of Corporate Social Responsibility on Loyalty and Valuation of Services. J. Bus. Ethics 2005, 61, 369–385. [Google Scholar] [CrossRef]

- Kang, J.; Hustvedt, G. Building Trust Between Consumers and Corporations: The Role of Consumer Perceptions of Transparency and Social Responsibility. J. Bus. Ethics 2014, 125, 253–265. [Google Scholar] [CrossRef]

- Bugandwa, T.C.; Kanyurhi, E.B.; Akonkwa, D.B.M.; Mushigo, B.H. Linking corporate social responsibility to trust in the banking sector: Exploring disaggregated relations. Int. J. Bank Mark. 2021, 39, 592–617. [Google Scholar] [CrossRef]

- Cheah, J.-H.; Ting, H.; Ramayah, T.; Memon, M.A.; Cham, T.-H.; Ciavolino, E. A comparison of five reflective–formative estimation approaches: Reconsideration and recommendations for tourism research. Qual. Quant. 2019, 53, 1421–1458. [Google Scholar] [CrossRef]

- van Riel, A.; Henseler, J.; Kemény, I.; Sasovova, Z. Estimating hierarchical constructs using consistent partial least squares. Ind. Manag. Data Syst. 2017, 117, 459–477. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Relationship | Original Path | MLMV–CLC Path | Endogenous Constructs | Original R2 | MLMV–CLC R2 |

|---|---|---|---|---|---|

| CSRP ≥ BP | 0.069 | 0.066 | BP | 0.665 | 0.668 |

| DS ≥ BP | 0.267 | 0.270 | CSRP | 0.049 | 0.052 |

| DS ≥ CSRP | −0.011 | −0.007 | OE | 0.519 | 0.519 |

| DS ≥ OE | 0.387 | 0.387 | |||

| LCS ≥ BP | 0.353 | 0.336 | |||

| LCS ≥ CSRP | 0.229 | 0.212 | |||

| LCS ≥ OE | 0.417 | 0.413 | |||

| OE ≥ BP | 0.296 | 0.293 |

| α | ρA | ρC | AVE | BFP | Cost | DS | ESCR | Flex | ICSR | LCS | NBFP | Quality | Reliab. | Speed | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| BFP | 0.876 | 0.877 | 0.906 | 0.618 | |||||||||||

| Cost | 0.843 | 0.862 | 0.887 | 0.611 | 0.106 | ||||||||||

| DS | 0.823 | 0.831 | 0.871 | 0.530 | 0.706 | 0.071 | |||||||||

| ECSR | 0.780 | 0.781 | 0.872 | 0.694 | 0.287 | 0.060 | 0.188 | ||||||||

| Flex | 0.774 | 0.830 | 0.866 | 0.684 | 0.123 | 0.059 | 0.247 | 0.177 | |||||||

| ICSR | 0.768 | 0.775 | 0.866 | 0.682 | 0.172 | 0.077 | 0.114 | 0.670 | 0.148 | ||||||

| LCS | 0.862 | 0.862 | 0.897 | 0.592 | 0.727 | 0.065 | 0.708 | 0.270 | 0.060 | 0.140 | |||||

| NBFP | 0.876 | 0.881 | 0.910 | 0.669 | 0.631 | 0.042 | 0.654 | 0.277 | 0.054 | 0.134 | 0.748 | ||||

| Quality | 0.896 | 0.914 | 0.919 | 0.656 | 0.120 | 0.057 | 0.096 | 0.422 | 0.615 | 0.258 | 0.256 | 0.190 | |||

| Relib. | 0.871 | 0.873 | 0.907 | 0.661 | 0.799 | 0.074 | 0.745 | 0.223 | 0.141 | 0.138 | 0.727 | 0.564 | 0.097 | ||

| Speed | 0.827 | 0.874 | 0.876 | 0.640 | 0.066 | 0.059 | 0.057 | 0.099 | 0.033 | 0.044 | 0.073 | 0.056 | 0.109 | 0.034 |

| Linear Relationship | Inverted U-Shaped Test | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Path | t-Value | p Values | Confidence Interval | Path | t-Value | p Values | Confidence Interval | |||

| LLCI | ULCI | LLCI | ULCI | |||||||

| CSRP -> BP | 0.069 | 2.842 | 0.005 | [0.021], [0.116] | −0.019 | 0.935 | 0.350 | [−0.057], [0.022] | ||

| DS -> BP | 0.267 | 6.306 | 0.000 | [0.185], [0.350] | 0.019 | 0.657 | 0.511 | [−0.033], [0.076] | ||

| DS -> CSRP | −0.011 | 0.182 | 0.855 | [−0.132], [0.109] | 0.046 | 1.145 | 0.252 | [−0.045], [0.114] | ||

| DS -> OE | 0.387 | 6.296 | 0.000 | [0.267], [0.507] | −0.040 | 0.919 | 0.358 | [−0.125], [0.049] | ||

| LCS -> BP | 0.353 | 7.353 | 0.000 | [0.255], [0.444] | −0.005 | 0.179 | 0.858 | [−0.063], [0.050] | ||

| LCS -> CSRP | 0.229 | 4.967 | 0.000 | [0.137], [0.318] | −0.007 | 0.187 | 0.852 | [−0.077], [0.070] | ||

| LCS -> OE | 0.417 | 7.288 | 0.000 | [0.301], [0.526] | 0.007 | 0.140 | 0.889 | [−0.090], [0.096] | ||

| OE -> BP | 0.296 | 5.994 | 0.000 | [0.195], [0.390] | 0.003 | 0.096 | 0.923 | [−0.055], [0.059] | ||

| DS -> CSRP-> BP | −0.001 | 0.176 | 0.860 | [−0.010], [0.008] | 0.004 | 1.037 | 0.300 | [−0.004], [0.010] | ||

| LCS -> OE -> BP | 0.123 | 4.665 | 0.000 | [0.074], [0.177] | 0.002 | 0.139 | 0.890 | [−0.026], [0.032] | ||

| DS -> OE -> BP | 0.115 | 4.359 | 0.000 | [0.069], [0.173] | −0.012 | 0.873 | 0.383 | [−0.042], [0.013] | ||

| LCS -> CSRP -> BP | 0.016 | 2.284 | 0.022 | [0.004], [0.031] | −0.001 | 0.172 | 0.864 | [−0.007], [0.006] | ||

| Pre-Specified Groups | Relative Groups Size | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Fit Indices | K = 2 | K = 3 | K = 4 | K = 5 | K = 1 | K = 2 | K = 3 | K = 4 | K = 5 | |

| AIC | 3275.000 | 3209.726 | 3189.000 | 3156.560 | K = 2 | 0.592 | 0.408 | |||

| AIC3 | 3298.000 | 3244.726 | 3236.000 | 3215.560 | K = 3 | 0.535 | 0.252 | 0.213 | ||

| AIC4 | 3321.000 | 3279.726 | 3283.000 | 3274.560 | K = 4 | 0.474 | 0.301 | 0.207 | 0.018 | |

| BIC | 3372.482 | 3358.067 | 3388.201 | 3406.621 | K = 5 | 0.431 | 0.213 | 0.184 | 0.091 | 0.082 |

| CAIC | 3395.482 | 3393.067 | 3435.201 | 3465.621 | ||||||

| HQ | 3313.213 | 3267.876 | 3267.087 | 3254.584 | ||||||

| MDL5 | 3946.408 | 4231.433 | 4561.006 | 4878.865 | ||||||

| LnL | −1614.500 | −1569.863 | −1547.500 | −1519.280 | ||||||

| EN | 0.415 | 0.493 | 0.581 | 0.554 | ||||||

| NFI | 0.483 | 0.490 | 0.523 | 0.486 | ||||||

| NEC | 299.634 | 259.571 | 214.780 | 228.537 | ||||||

| Relationship | Original | K1 | K2 | K3 | K4 | (K1–K2) * | (K1–K3) * | (K1–K4) * | (K2–K3) * | (K2–K4) * | (K3–K4) * | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Path Coefficient | DS ≥ BP | 0.267 | 0.016 | −0.119 | 0.665 | 0.467 | 0.136 | −0.649 | −0.451 | −0.785 | −0.586 | 0.198 |

| LCS ≥ BP | 0.353 | 0.272 | 0.186 | 0.309 | 0.881 | 0.085 | −0.037 | −0.609 | −0.122 | −0.694 | −0.571 | |

| DS ≥ CSRP | −0.011 | 0.346 | 0.016 | −0.226 | −0.169 | 0.330 | 0.572 | 0.515 | 0.241 | 0.184 | −0.056 | |

| LCS ≥ CSRP | 0.229 | 0.111 | 0.181 | 0.102 | 0.539 | −0.070 | 0.009 | −0.428 | 0.079 | −0.357 | −0.437 | |

| DS ≥ OE | 0.387 | 0.193 | −0.225 | 0.398 | 0.248 | 0.417 | −0.204 | −0.055 | −0.622 | −0.472 | 0.149 | |

| LCS ≥ OE | 0.417 | 0.481 | −0.225 | 0.460 | 0.718 | 0.705 | 0.021 | −0.236 | −0.684 | −0.942 | −0.258 | |

| CSRP ≥ BP | 0.069 | 0.310 | −0.225 | 0.025 | 0.367 | 0.534 | 0.284 | −0.057 | −0.249 | −0.591 | −0.341 | |

| OE ≥ BP | 0.296 | 0.600 | 0.923 | 0.075 | −0.639 | −0.322 | 0.524 | 1.239 | 0.847 | 1.562 | 0.714 | |

| R-square (Weighted R-square) | BP | 0.664 (0.849) | 0.920 | 0.833 | 0.909 | 0.768 | ||||||

| CSRP | 0.049 (0.121) | 0.184 | 0.036 | 0.032 | 0.204 | |||||||

| OE | 0.519 (0.611) | 0.393 | 0.563 | 0.608 | 0.802 | |||||||

| Relative sample size (%) | 22.46 | 23.04 | 22.85 | 31.64 |

| Model | Exog. | Path | Sign | Boot | Model | Exog. | Path | Sign | Boot | Model | Exog. | Path | Sign | Boot |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Org. Model | DS | 0.267 | 0.000 | - | CSRP | 0.094 | 0.145 | 0.053 | DSC | 0.098 | 0.424 | 0.475 | ||

| LCS | 0.353 | 0.000 | - | OE | 0.300 | 0.000 | 0.000 | LCSC | 0.115 | 0.259 | 0.322 | |||

| CSRP | 0.069 | 0.000 | - | DSC | 0.164 | 0.129 | 0.152 | CSRPC | −0.018 | 0.636 | 0.503 | |||

| OE | 0.296 | 0.000 | - | CSRPC | −0.018 | 0.637 | 0.502 | Model 12 | DS | 0.126 | 0.375 | 0.486 | ||

| Model 1 | DS | 0.103 | 0.355 | 0.428 | Model 7 | DS | 0.078 | 0.566 | 0.649 | LCS | 0.211 | 0.076 | 0.128 | |

| LCS | 0.351 | 0.000 | 0.000 | LCS | 0.352 | 0.000 | 0.000 | CSRP | 0.069 | 0.010 | 0.004 | |||

| CSRP | 0.066 | 0.013 | 0.006 | CSRP | 0.066 | 0.013 | 0.006 | OE | 0.390 | 0.011 | 0.018 | |||

| OE | 0.299 | 0.000 | 0.000 | OE | 0.333 | 0.023 | 0.041 | DSC | 0.137 | 0.312 | 0.395 | |||

| DSC | 0.162 | 0.123 | 0.140 | DSC | 0.186 | 0.152 | 0.225 | LCSC | 0.133 | 0.212 | 0.267 | |||

| Model 2 | DS | 0.265 | 0.000 | 0.000 | OEC | −0.035 | 0.807 | 0.816 | OEC | −0.089 | 0.556 | 0.566 | ||

| LCS | 0.195 | 0.053 | 0.089 | Model 8 | DS | 0.263 | 0.000 | 0.000 | Model 13 | DS | 0.263 | 0.000 | 0.000 | |

| CSRP | 0.070 | 0.008 | 0.004 | LCS | 0.185 | 0.073 | 0.110 | LCS | 0.177 | 0.119 | 0.167 | |||

| OE | 0.302 | 0.000 | 0.000 | CSRP | 0.102 | 0.112 | 0.035 | CSRP | 0.102 | 0.111 | 0.036 | |||

| LCSC | 0.146 | 0.091 | 0.110 | OE | 0.304 | 0.000 | 0.000 | OE | 0.327 | 0.019 | 0.018 | |||

| Model 3 | DS | 0.265 | 0.000 | 0.000 | LCSC | 0.154 | 0.086 | 0.100 | LCSC | 0.162 | 0.111 | 0.136 | ||

| LCS | 0.352 | 0.000 | 0.000 | CSRPC | −0.021 | 0.589 | 0.439 | CSRPC | −0.021 | 0.588 | 0.433 | |||

| CSRP | 0.100 | 0.097 | 0.056 | Model 9 | DS | 0.265 | 0.000 | 0.000 | OEC | −0.024 | 0.862 | 0.856 | ||

| OE | 0.298 | 0.000 | 0.000 | LCS | 0.177 | 0.120 | 0.167 | Model 14 | DS | 0.082 | 0.548 | 0.634 | ||

| CSRPC | −0.020 | 0.571 | 0.456 | CSRP | 0.071 | 0.008 | 0.004 | LCS | 0.351 | 0.000 | 0.000 | |||

| Model 4 | DS | 0.268 | 0.000 | 0.000 | OE | 0.324 | 0.020 | 0.016 | CSRP | 0.094 | 0.146 | 0.053 | ||

| LCS | 0.350 | 0.000 | 0.000 | LCSC | 0.164 | 0.107 | 0.126 | OE | 0.333 | 0.024 | 0.041 | |||

| CSRP | 0.068 | 0.011 | 0.005 | OEC | −0.022 | 0.869 | 0.860 | DSC | 0.181 | 0.166 | 0.243 | |||

| OE | 0.217 | 0.076 | 0.076 | Model 10 | DS | 0.266 | 0.000 | 0.000 | CSRPC | −0.018 | 0.641 | 0.506 | ||

| OEC | 0.081 | 0.496 | 0.467 | LCS | 0.349 | 0.000 | 0.000 | OEC | −0.034 | 0.814 | 0.823 | |||

| Model 5 | DS | 0.162 | 0.205 | 0.301 | CSRP | 0.102 | 0.111 | 0.032 | Model 15 | DS | 0.130 | 0.362 | 0.470 | |

| LCS | 0.227 | 0.049 | 0.091 | OE | 0.221 | 0.072 | 0.072 | LCS | 0.210 | 0.077 | 0.125 | |||

| CSRP | 0.068 | 0.011 | 0.005 | CSRPC | −0.023 | 0.556 | 0.379 | CSRP | 0.096 | 0.136 | 0.047 | |||

| OE | 0.302 | 0.000 | 0.000 | OEC | 0.079 | 0.510 | 0.481 | OE | 0.390 | 0.011 | 0.017 | |||

| DSC | 0.103 | 0.401 | 0.455 | Model 11 | DS | 0.165 | 0.197 | 0.289 | DSC | 0.132 | 0.332 | 0.411 | ||

| LCSC | 0.115 | 0.259 | 0.321 | LCS | 0.226 | 0.050 | 0.093 | LCSC | 0.132 | 0.213 | 0.265 | |||

| Model 6 | DS | 0.100 | 0.381 | 0.456 | CSRP | 0.096 | 0.136 | 0.049 | CSRPC | −0.018 | 0.645 | 0.512 | ||

| LCS | 0.350 | 0.000 | 0.000 | OE | 0.304 | 0.000 | 0.000 | OEC | −0.087 | 0.563 | 0.574 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ivascu, L.; Ali, W.; Khalid, R.; Raza, M. The Impact of Competitive Strategies on Performance of Banking Sector; The Mediating Role of Corporate Social Responsibility and Operational Excellence. Energies 2023, 16, 297. https://doi.org/10.3390/en16010297

Ivascu L, Ali W, Khalid R, Raza M. The Impact of Competitive Strategies on Performance of Banking Sector; The Mediating Role of Corporate Social Responsibility and Operational Excellence. Energies. 2023; 16(1):297. https://doi.org/10.3390/en16010297

Chicago/Turabian StyleIvascu, Larisa, Waqas Ali, Rimsha Khalid, and Mohsin Raza. 2023. "The Impact of Competitive Strategies on Performance of Banking Sector; The Mediating Role of Corporate Social Responsibility and Operational Excellence" Energies 16, no. 1: 297. https://doi.org/10.3390/en16010297

APA StyleIvascu, L., Ali, W., Khalid, R., & Raza, M. (2023). The Impact of Competitive Strategies on Performance of Banking Sector; The Mediating Role of Corporate Social Responsibility and Operational Excellence. Energies, 16(1), 297. https://doi.org/10.3390/en16010297