4.1. National Level Results

The model was constructed to run from 2021 to 2060 for five scenarios (see

Appendix B for detail), under which the life of each plant becomes progressively shorter: 30 years under the “No Transition” (NT) and ”Baseline” (B) scenarios, 25 under “Low-Cost Renewables” (R), 20 under 50% lower emissions than 2015 (C50) and 15 under “80% lower” (C80), respectively.

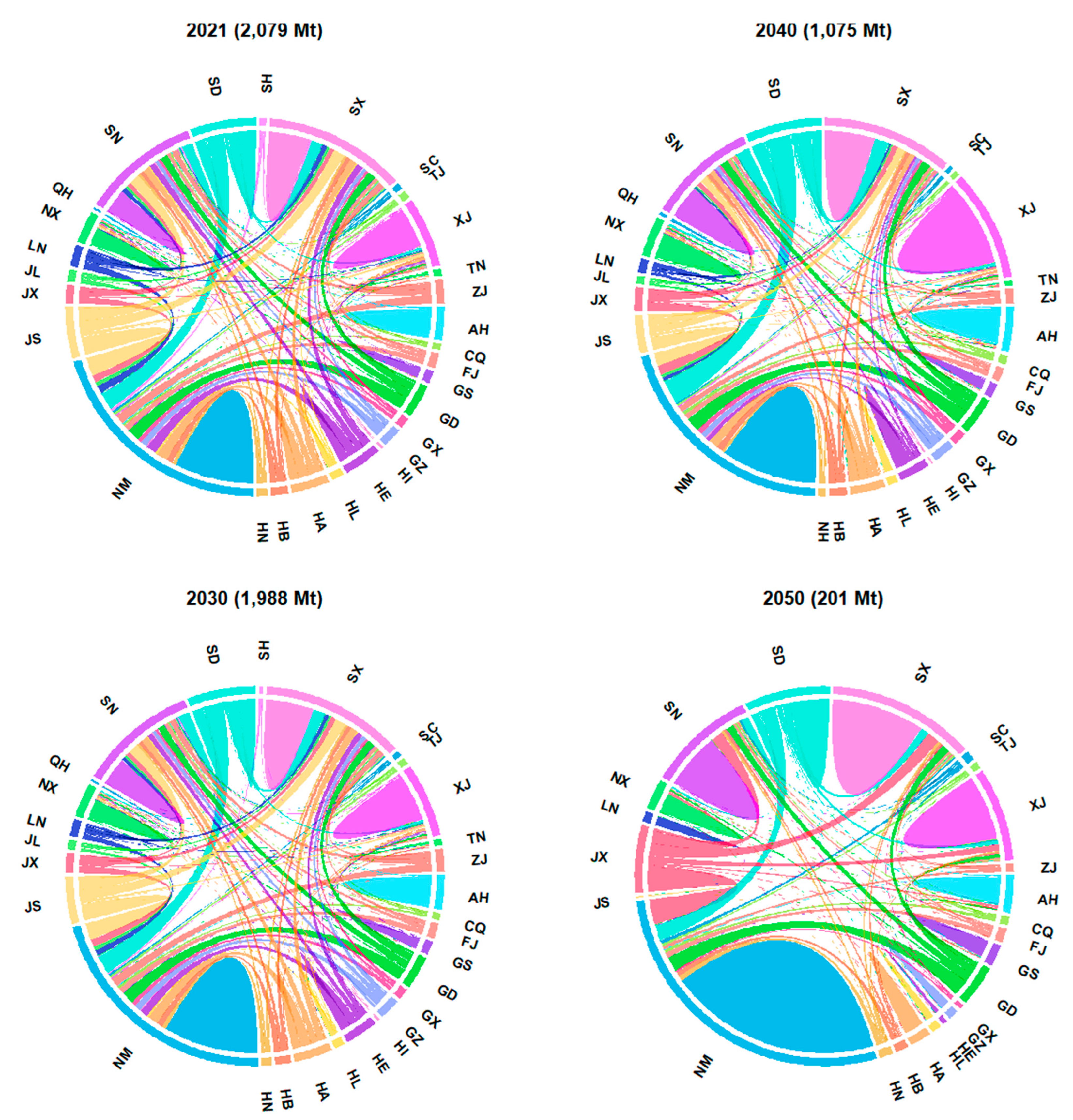

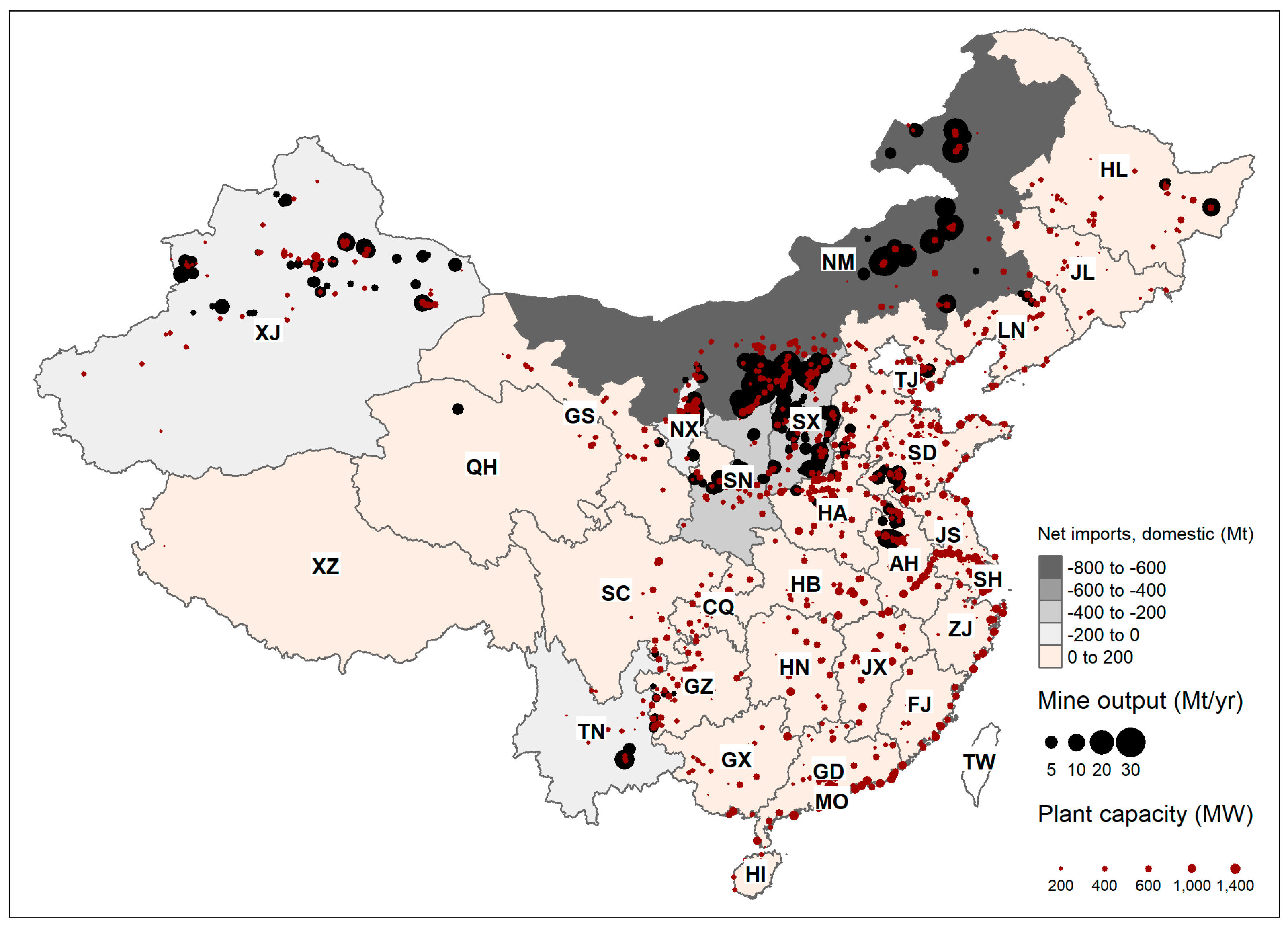

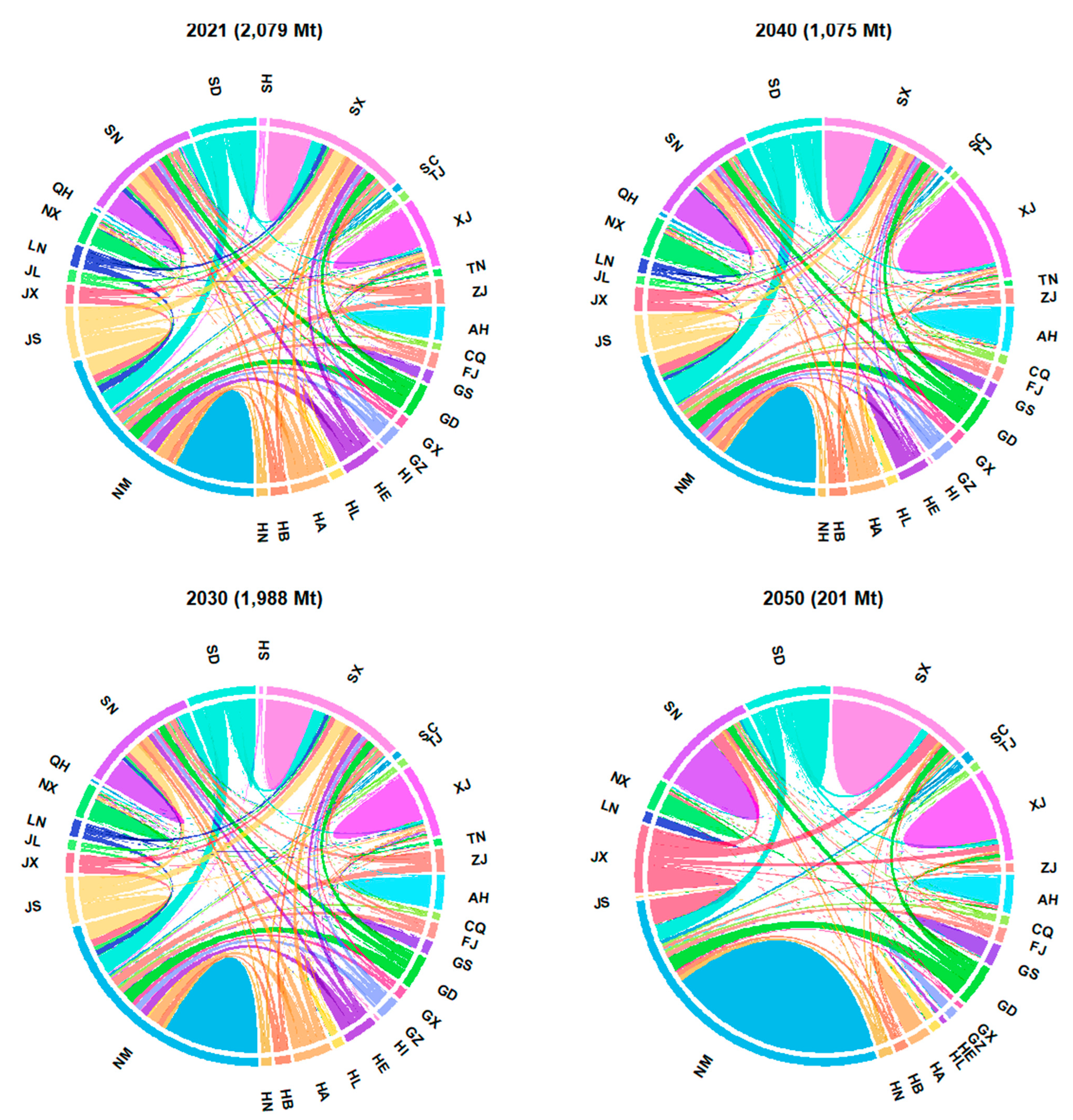

Figure 2 shows the production-consumption relationships of thermal coal of all types between provinces in the B scenario, where each coal-consuming province (outside ring) consumes coal from local mines where it is available, and imports from other provinces where it is not (cross-circle links, where the colour of the link is that of the destination province). The prominence of Inner Mongolia (NM), Shaanxi (SN), and Shanxi (SX) as coal suppliers to many other provinces is clearly visible. All three produce a large amount of coal, consume a significant share of their own coal, and export the rest to other provinces. Inner Mongolia’s and Shanxi’s prominence as both producers and consumers will continue to grow, such that, by 2050, both provinces will dominate coal demand, obtaining the vast majority of coal from their own local mines.

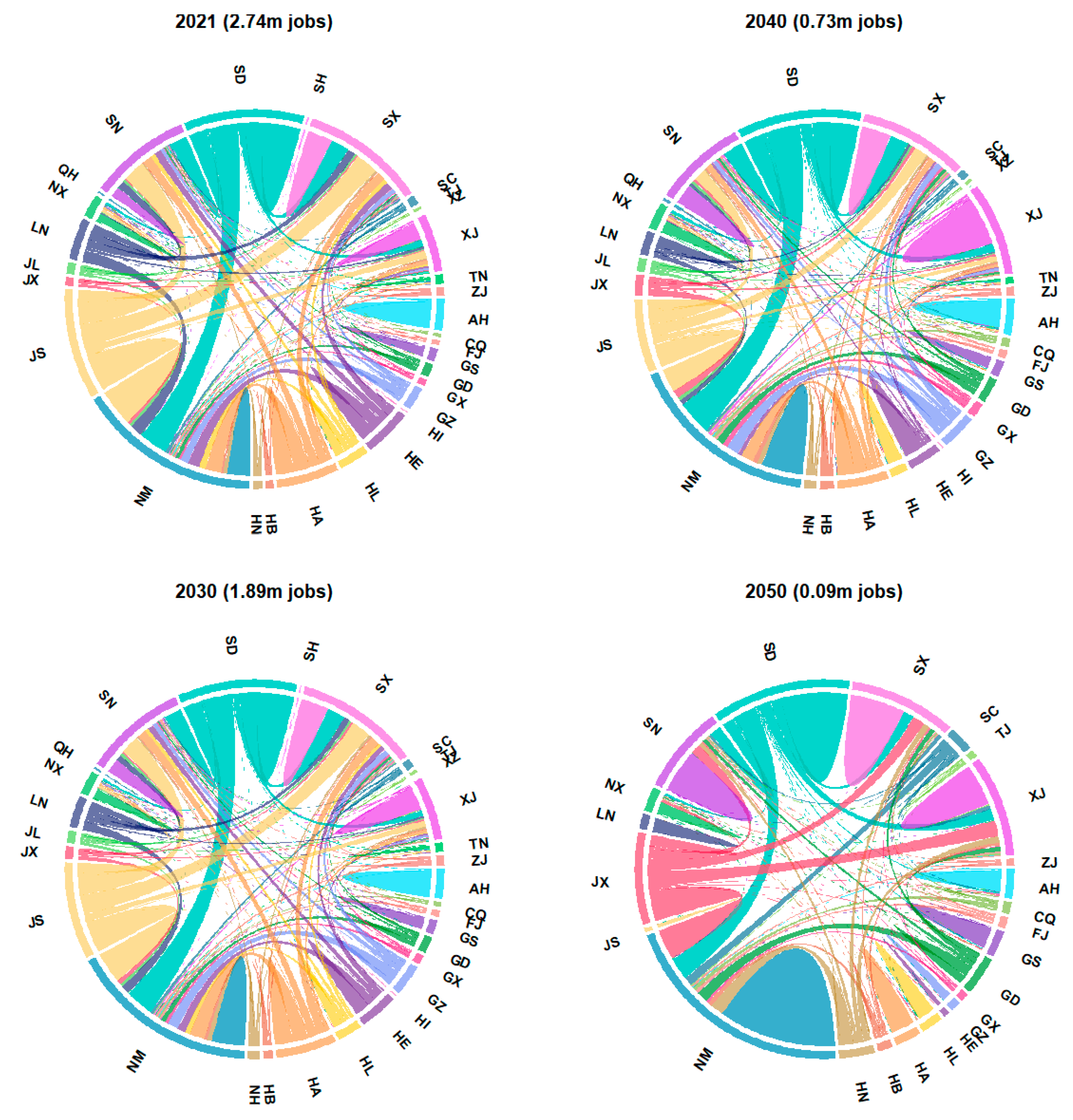

Table 2 summarises the number of jobs supported by each province’s coal fleet, which are also visualised in

Figure 3. This refers to jobs at coal plants in that province, as well as upstream supply chain jobs in mining and transport supported by each plant’s coal consumption. The number of support jobs is determined largely by the labour intensity of mining in the provinces from which the coal is sourced. Provinces themselves are more likely to be home to a greater number of coal jobs (both locally and nationally) when they have a combination of large coal fleets, large mining capacity, and high labour intensity. Coal plants in Shandong, for instance, support 491,200 jobs nationally, both locally and indirectly by importing coal from other provinces. Inner Mongolia’s coal fleet is of a similar size but is supplied entirely by its ultra-efficient domestic mining industry workforce and supports only 102,000 jobs, although coal exports to other provinces supports another 444,000 coal mining jobs in Inner Mongolia’s mines.

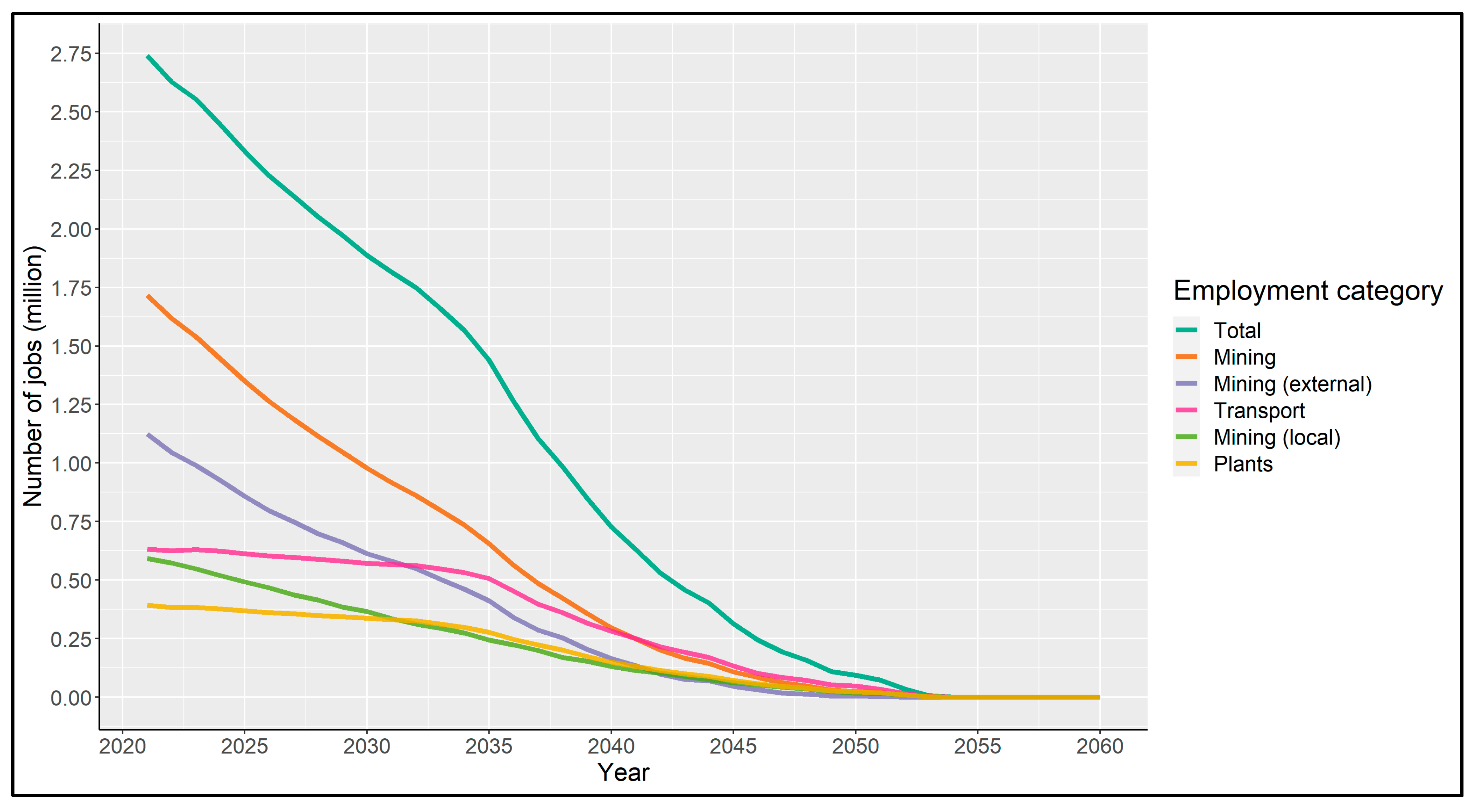

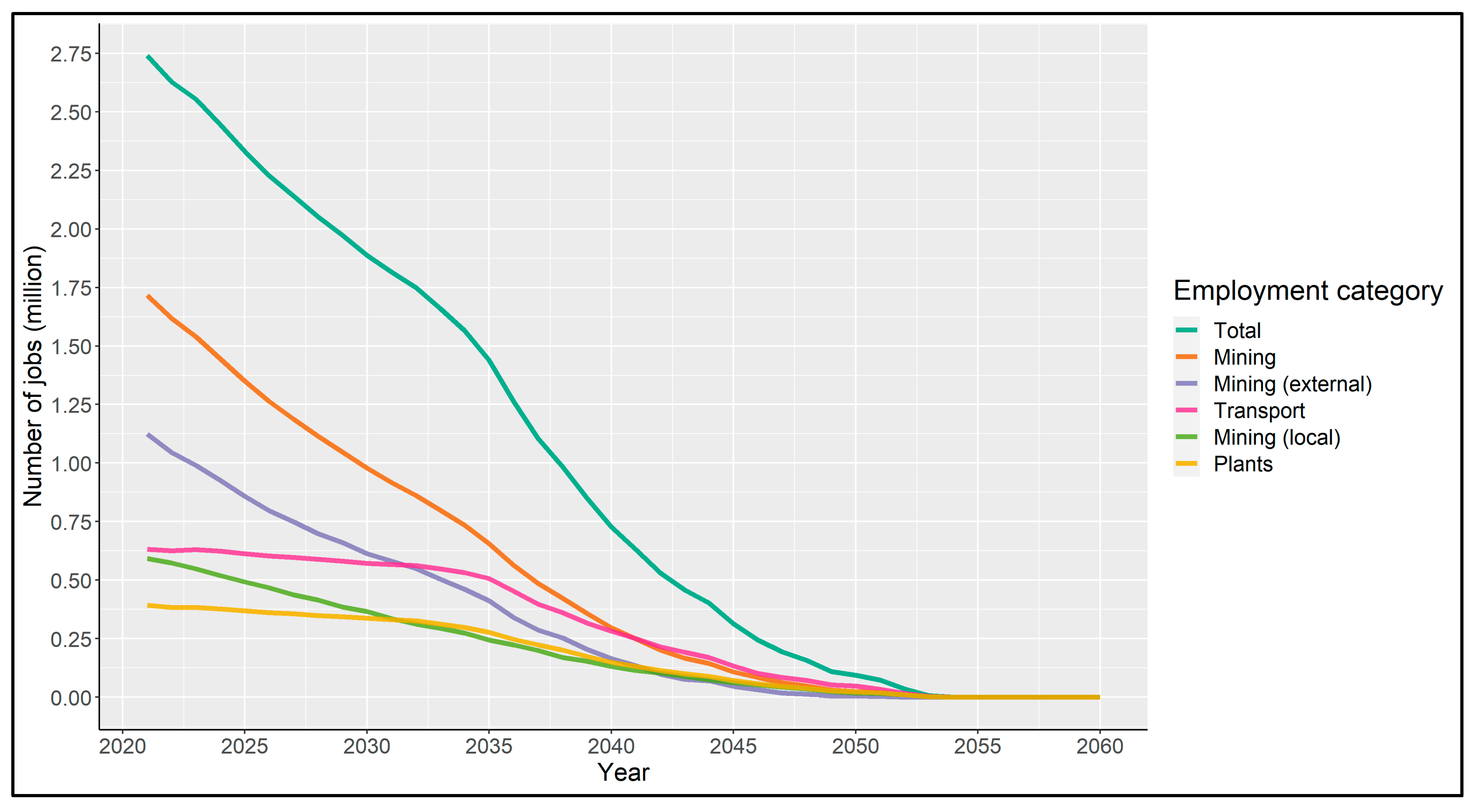

Figure 4 plots baseline scenario estimates for employment in the coal power industry from 2021–2060. Employment in coal mines starts at a higher level (1.72 million) but follows a steep downward trajectory, declining by over 60% to 655,000 by 2035. Employment in plants (starting at 393,000) falls half as fast, by just under 30% to 277,000 in the same period. Transport jobs are proportional to ton-km of coal transported and again fall half as fast as plant jobs: 632,000 in 2021 falling 15% to 238,000 in 2035, reflecting a 15% drop in coal consumption over that period. The sharp fall in mining jobs reflects the extrapolation of past declines in mining labour intensity and the slow pace of plant retirements up to about 2034. From this point onwards, total job losses accelerate as the pace of plant retirements increases and coal demand falls more rapidly, slowing slightly again in the 2040s and declining to zero in 2054 as the wave of plants built in the decade to 2020 reach the end of their operating lifetimes.

Under the baseline scenario, reflecting current policies, total employment supported by the thermal coal power industry is projected to drop from 2.74 million in 2021, to below 1 million by 2038, below 500,000 by 2043, and below 250,000 by 2046 (see

Figure 4). As noted in previous work [

16], the net employment impact of coal closure on the whole economy is unlikely to be significantly negative as other forms of energy production and supporting industries take its place. The public policy challenge is anticipating job losses sufficiently well across space and time to take early action to redeploy workers elsewhere or offer retraining programmes to avoid the potentially very large burden of mass early retirements, or chronic unemployment, on the social security system. Methodologies have been developed to undertake this analysis by identifying green industries and skills that are ‘adjacent’ to emissions-intensive ones [

76], but have not yet been applied in detail to China.

The trajectory of fiscal revenues in the B scenario does not decline as sharply and in fact rises slightly in the short term. Income taxes and social security payments fall with the decline in employment; however, total revenues rise initially from CNY 330 billion to CNY 339 billion in 2023, at which point total coal capacity peaks at 1205 GW. This reflects the tax burden on physical capital (notably resource and environmental pollution taxes, VAT, and surcharges linked to VAT) representing a much greater proportion of total revenue than taxes on labour.

In 2021, VAT contributes CNY 153.7 billion in tax revenues to the national government (95% of the total), about 2.7% of total VAT revenue in 2020 [

77]. Of the remaining national government revenues, income taxes contribute CNY 5.6 billion (3.4%), and mining royalties CNY 2.6 billion (1.6%), and. For subnational governments, pollution taxes on mines generate CNY 52.7 billion (31.3%), VAT, CNY 51.2 billion (30.5%), resource taxes CNY 47.8 billion (28.4%), and pollution taxes on plants, CNY 4.7 billion (2.8%).

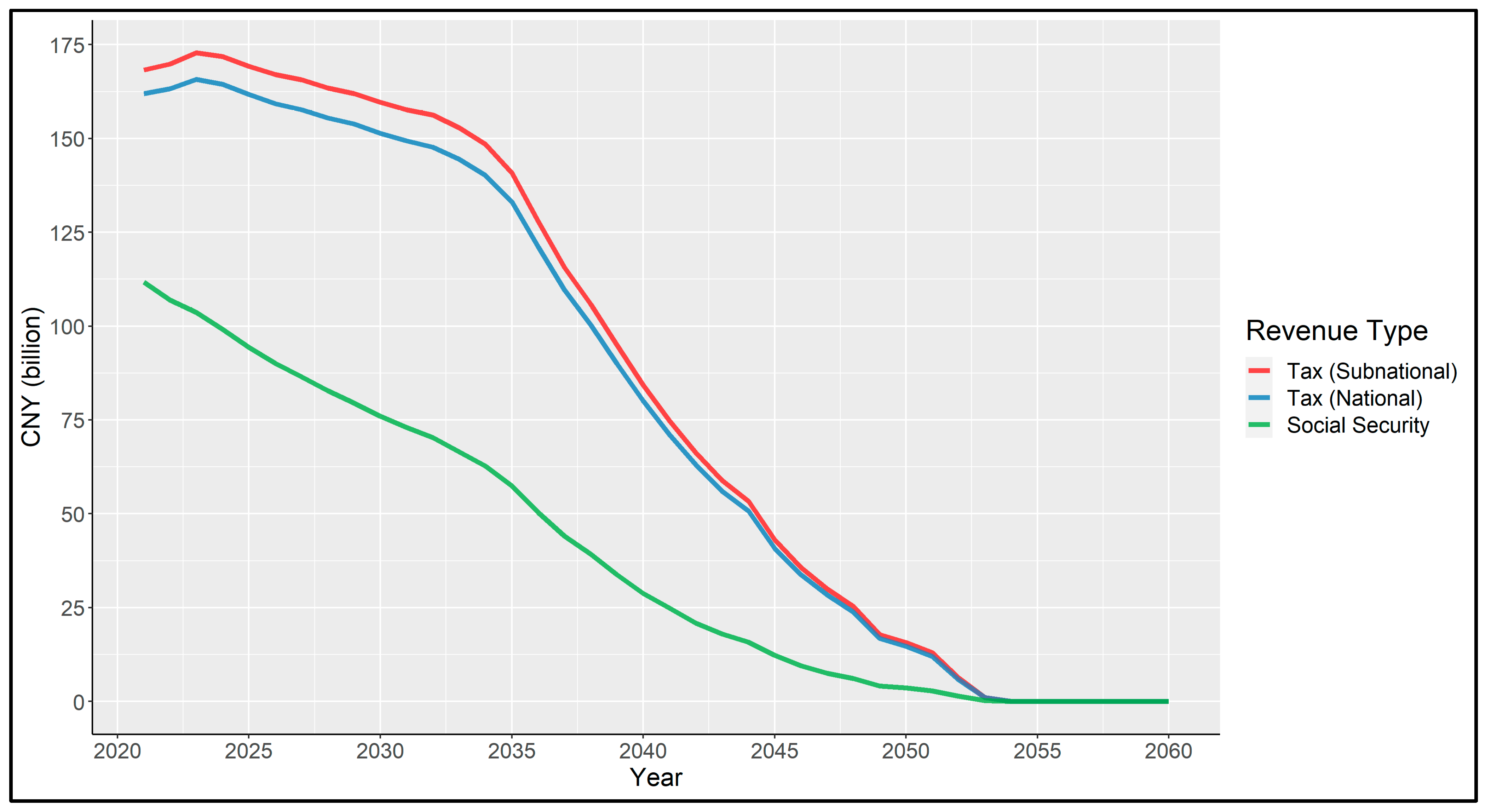

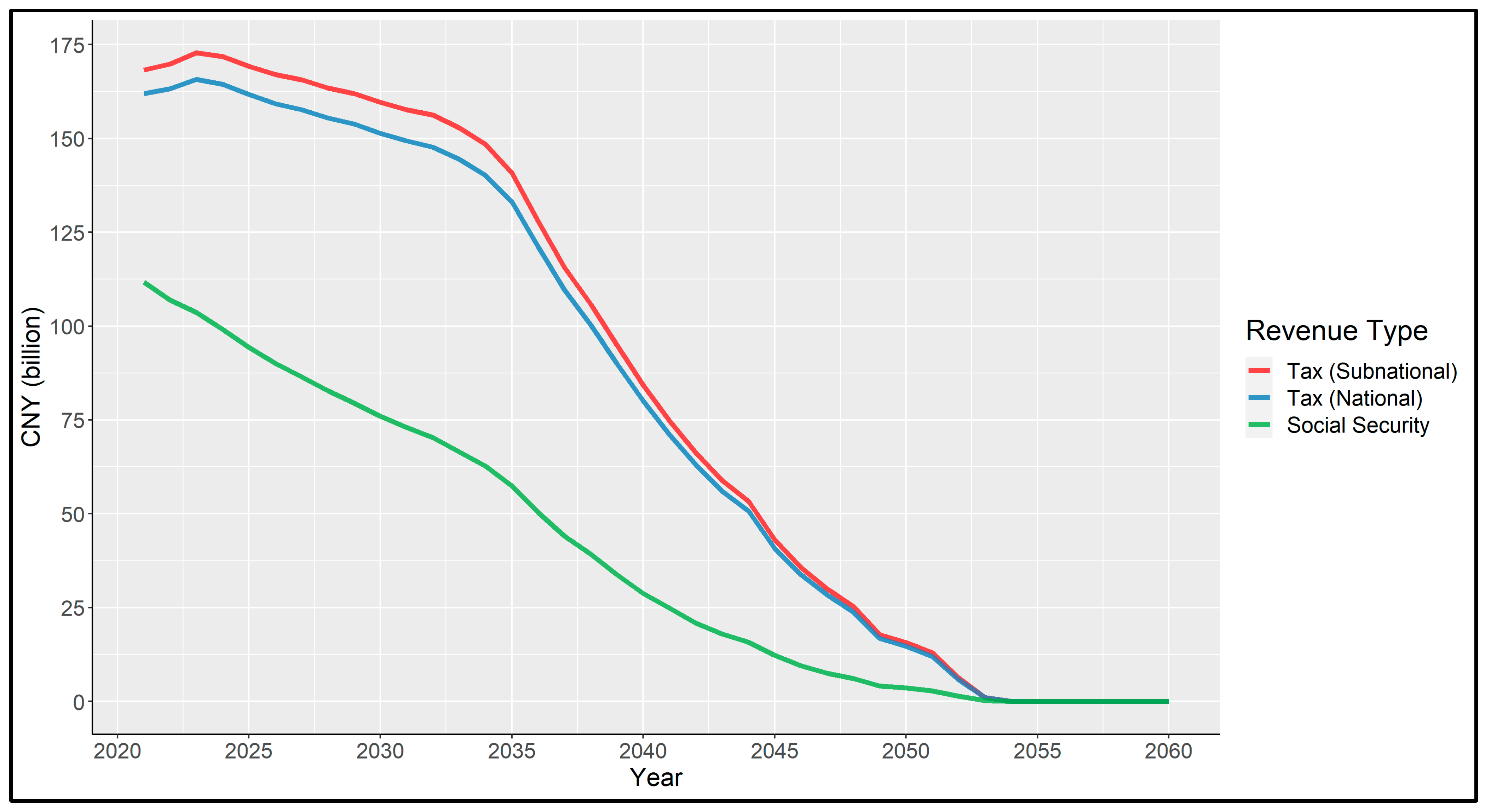

As

Figure 5 shows, despite the difference in composition, absolute revenues flowing to national and subnational governments are very similar and follow a near-identical trajectory. Annual revenues to national/subnational/all levels of government decline slowly by 1–1.5% annually from their CNY 166/173/339 billion peaks in 2023, to CNY 151/160/311 billion in 2030. Tax revenues start to fall steeply around 2034 as plant retirements accelerate, with annual rates of decline in both cases jumping from 3% in 2034, to 5% in 2035 and 9% in 2036, continuing to fall by 9–11% per year until 2044 and significantly faster thereafter. Total tax revenues from the thermal coal industry fall below CNY 100 billion by 2045, and just over CNY 30 billion in 2050. Social security payments (not strictly a tax, but a relevant contribution to publicly managed funds) are also plotted for comparison. The trend in social security revenue, falling from CNY 112 billion in 2021 to CNY 76 billion in 2030 (a 32% decline), and CNY 3.6 billion in 2050 (a 97% decline) is based entirely on wages, and, therefore, follows a similar trajectory to total job losses (

Figure 4) rather than tracking plant closures, with some variation due to differences in average wage over time.

When compared to the estimated current annual subsidy level of CNY 480 billion or more, the total of around CNY 330 billion in total tax revenue suggests that the net fiscal contribution of the coal industry to public revenues is likely to be negative, without accounting for the cost of negative externalities. As the revenues associated with capital assets fall more sharply after 2035, it becomes increasing likely that coal will become a net fiscal drain on China, even without accounting for the public health, productivity, and other environmental and climate externalities that coal mining and combustion generate. While subsidies to capital assets and power price subsidies for coal may fall as generation and coal consumption declines, other costs may rise to negate this, including contingent liabilities arising from state-owned power or mining company losses, defaults, or bankruptcies, restructuring efforts, and relocation/retraining costs for laid-off workers.

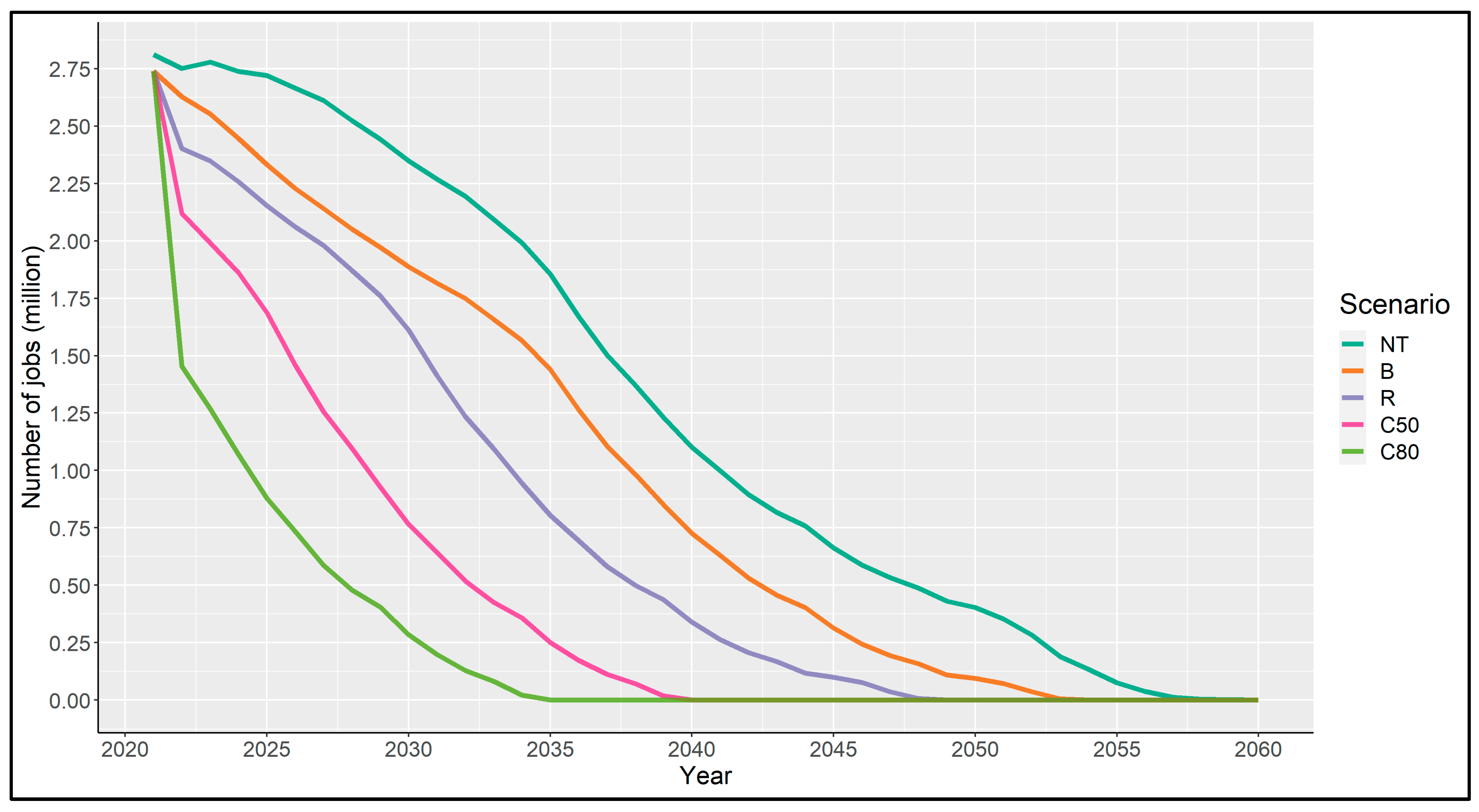

Comparing the baseline against the R scenario, with lower expected technology costs, and the more aggressive C50 and C80 scenarios, which artificially constrain total sector emissions, helps to understand the marginal impact of climate policy on thermal coal employment and the sector’s fiscal contribution. Under progressively stricter scenarios, the short-term drop in coal capacity (reflecting the retirement of older plants) needed to meet the target requirements becomes increasingly large.

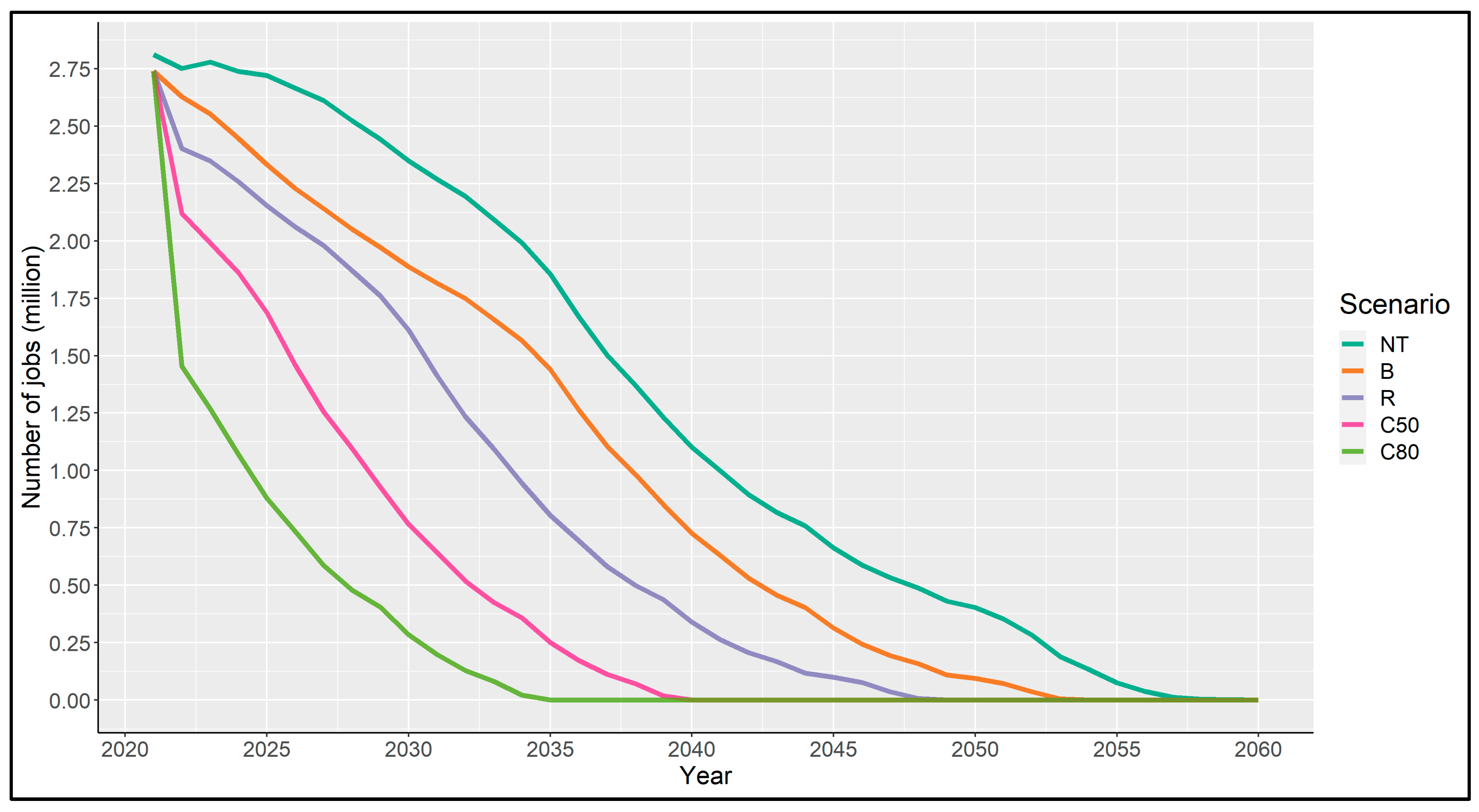

The R scenario has relatively little impact on total employment until the late 2020s, leading to about 270,000 fewer jobs in 2030 relative to the baseline (

Figure 6). The differential between the two pathways widens to over 630,000 in 2035, before converging back to 214,000 by 2045. Under the C50 scenario, implying coal phase-out by 2040, over 1.1 million additional job losses compared to the baseline would be expected by 2030, while, under the C80 scenario (phase-out by 2035), almost 1.6 million additional jobs disappear by 2030—almost 40% of total thermal coal industry jobs today. Notably, even the No Transition scenario, where all planned plants are built, only protects about 500,000 employees from redundancy by 2030 compared to the baseline. Total jobs still fall 40% by 2040 and 85% by 2050, declining to zero in 2060.

The more ambitious phase-out pathways do have serious employment consequences in the short term; however, the absolute magnitude of these changes is not unprecedented in China’s coal industry. Absolute job losses by 2030, even under the C80 scenario, are still fewer than the estimated 2.7 million coal industry jobs already lost between 2014 and 2020 [

62]. If 181 GW of CCS-enabled capacity were kept open in 2050 (as in the 2 °C scenario described above), even at the current rate of around 150 employees for a large (circa 1 GW) plant, this would be unlikely to support more than about 25,000–30,000 coal plant jobs at the most in the second half of the century, and fewer in mining and transport.

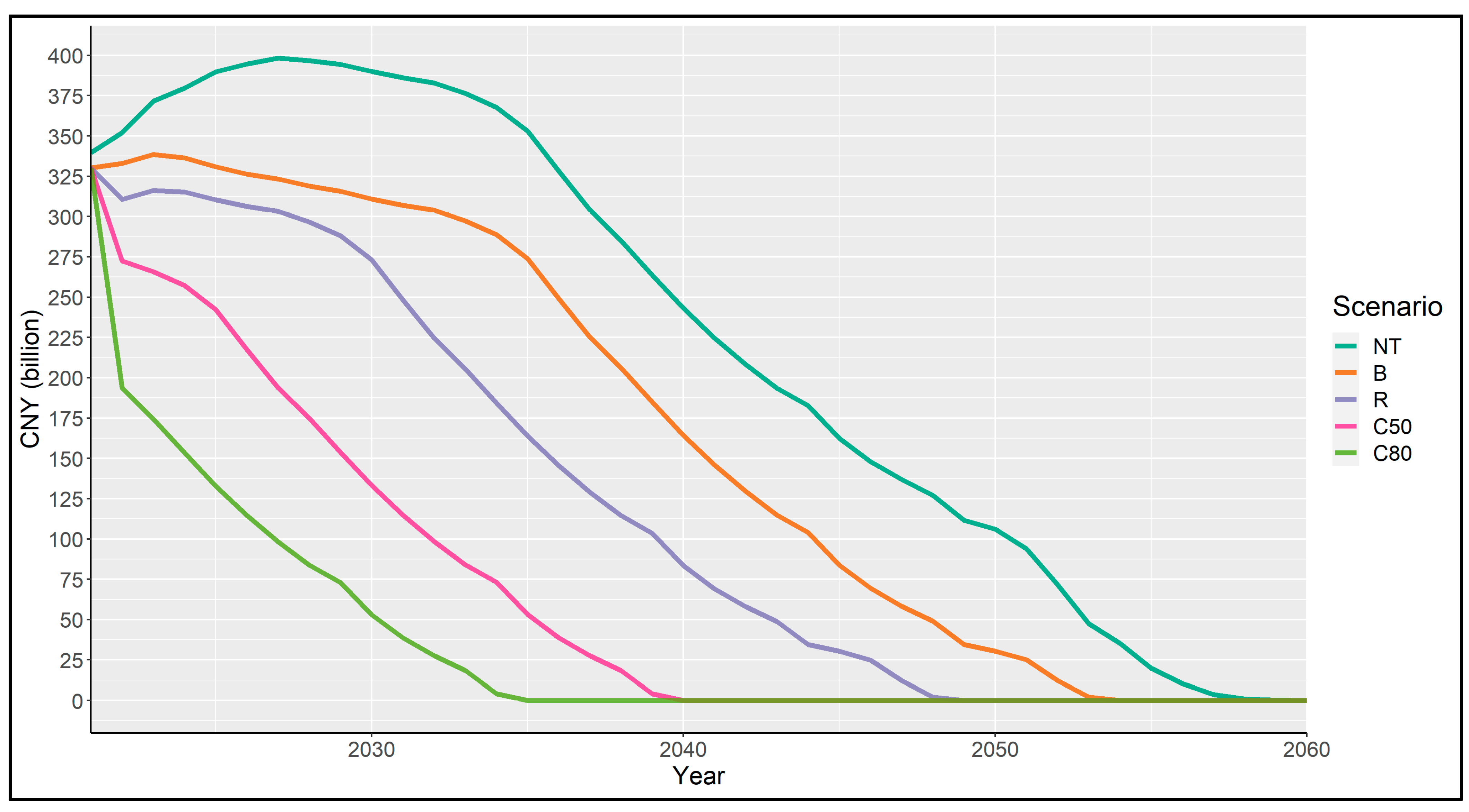

The fiscal picture (

Figure 7) is somewhat different for the first three scenarios. In the Baseline and No Transition scenarios, revenues keep increasing as long as coal generation capacity, hence also coal consumption (under the model assumptions), keeps increasing. Revenues peak in 2023 (CNY 339 billion) and 2027 (CNY 399 billion) under the B and NT scenarios, respectively. Total tax revenues remain relatively stable up to 2030 under the R scenario, falling by just 17% through the 2020s. They decline rapidly thereafter, following a similar trajectory as the baseline but, five years earlier, declining to zero in the late 2040s. In the C50 and C80 scenarios, the trajectory is also similar after a sharp initial drop in revenues, with subsequent rates of decline tracking the baseline, but starting 10–11 years and 15–16 years sooner, respectively. These patterns again reflect that the tax base for coal is much more capital-intensive than labour-intensive, since initial job losses do not offset increasing tax revenues from new plants, and, in each scenario, sharp declines in tax revenues coincide with increasing rates of capacity retirement.

Overall, scenario analysis suggests that the additional job losses associated with a pre-2050 coal phase-out target are relatively minor, even without counting job creation in the renewables sector. Job losses are much faster in the C50 and C80 scenarios but still slower in absolute terms than China has seen over the past decade. The timing, rather than the rate, of tax revenue decline is most affected by more ambitious phase-out scenarios.

4.2. Province-Level Results

The impact of coal phase-out is very different across provinces, due to differential exposure to the coal industry. When ‘internal’ coal jobs in each province (jobs at coal plants, and jobs at coal mines in the same province that supply these plants), and ‘external’ ones (jobs at coal mines in other provinces supported by demand from coal plants) are overlaid on the production-consumption network in

Figure 2, the results follow a markedly different pattern, due to the differences in labour intensity between coal mines in different provinces (

Table 3; see

Appendix C for full results for other scenarios) and how these interact with changing coal demand over space and time. Under the baseline scenario, 31% of coal industry jobs (853,000) are lost by 2030, at a similar rate to the IEA’s global predictions and consistent with its finding of a slightly higher rate of job loss in China than elsewhere. Perhaps most notably, the provinces at the root of the largest absolute jobs losses in the medium term (2021–2030) are not the large mining provinces, but those with large coal fleets that are declining in size, and moderate-to-large coal mining industries with high, but declining, labour intensity. In combination, plant closures and inefficient local mining means the number of total jobs lost for each GW of capacity closed is more than twice as high in Jiangsu (where 13.5 GW are retired from 2021–2030) as Hebei (11.5 GW).

Similarly, coal plants in Inner Mongolia, despite accounting for over 10% of China’s thermal coal demand in 2021, initially support only 3.7% of total coal jobs because the coal mines supplying most of these plants are also in (highly labour-efficient) Inner Mongolia. Similarly, plants in Shandong account for 8% of coal demand, but support 18% of coal jobs nationally because of the higher average labour intensity of the mines supplying them—some of which are in Shandong, with most of the rest sourced from Inner Mongolia, Shaanxi, and Shanxi. By 2050, differences in labour intensity have converged significantly and interprovincial trade in coal has largely disappeared, such that most remaining coal mining jobs are supported by demand from plants in the same province, with Shandong remaining the only notable exception.

For provinces that are already very labour-efficient, productivity improvements have less absolute impact over time relative to total provincial mining jobs, while, for provinces with high labour intensity, annual job losses are much greater, reflecting the active consolidation, closure of small mines and rollout of automated mining infrastructure that are a feature of current government policy. In Shanxi province, for instance, the Yangquan Coal Industry Group is using 5G technology to monitor and run mining operations remotely at its Xinyuan mine. Having employed 3000 workers in 2012, the mine expects to provide under 1000 jobs by 2025 [

55]. This means that more jobs are lost to efficiency than to planned or policy-accelerated plant closures and the ensuing effects on coal demand, at least in the short term, under current policies.

The following section explores in more detail the employment and fiscal implications of coal phase-out for a major net coal-producing province (Inner Mongolia) and a net coal-consumer (Jing-Jin-Ji region), comparing the two and reflecting on the dynamics these and provinces with similar net-producer and net-consumer characteristics are likely to see if China’s coal demand falls as projected.

4.2.1. Inner Mongolia

Inner Mongolia is the largest coal-producing province in China, at over 900 million tonnes annually, 37% of national production and nearly twice that of the next-largest producers, Shanxi (20%) and Shaanxi (19%). As one of China’s most suitable locations for wind farm development [

78], the province also hosts substantially more wind generation capacity than any other, at 11.4 GW, with a further 3.3 GW currently planned, although these are still dwarfed by its 103 GW of thermal coal generation capacity (as of 2021). Inner Mongolia has historically seen high curtailment rates for wind energy. These have since declined, from an average of 15% in 2016 to 10% in 2018 [

79], supported by greater long-distance transmission capacity to serve markets in Eastern provinces. Investment in additional transmission capacity appears to have grown since the onset of COVID-19, and is believed to have been supporting the transmission of locally generated coal-fired electricity to demand centres in the East for at least 7.9 GW of capacity commissioned in the first half of the year [

80].

Inner Mongolia is also fast becoming China’s largest consumer of coal. As of 2021, the province hosts 103 GW of capacity, nearly 9% of China’s total and just shy of Shandong’s 110 GW. Based on plants currently under construction, Inner Mongolia will overtake Shandong in 2023 to become host to China’s largest provincial fleet, reaching peak capacity at 120 GW in 2024. This is more than the total combined fleets of Germany and Japan, and roughly half the size of the entire fleets of the U.S. and India. Its dependence on coal mining and other minerals, the use of coal for domestic heating, and the provincial government’s support for coal (extending to enterprises under government control), support the continued expansion of the coal industry despite national policy.

In terms of employment, Inner Mongolia is, however, relatively well positioned to transition away from a coal-based economy, with appropriate planning. Its mining workforce is the most efficient in China, at 1.7 jobs per additional 10,000 tonnes produced (the second-least labour intensive are Shaanxi, at 3.3, and Xinjiang, at 3.5). Thus, despite massive coal mining and combustion operations, coal plants located in Inner Mongolia are estimated to support just 102,000 jobs, of which only 27,000 are in the mining industry.

However, since Inner Mongolia exports over two-thirds of its coal and meets almost 40% of total interprovincial demand, the jobs associated with meeting demand from other provinces are several times those associated with supplying just its own plants. Over 440,000 additional coal mining jobs and 39,000 coal transport jobs are associated with coal supplied by Inner Mongolia to other provinces. Once accounting for exported coal, therefore, over 500,000 jobs in Inner Mongolia depend on demand for thermal coal.

On the fiscal front, Inner Mongolia’s coal industry contributes CNY 33.7 billion to central government revenues (about 15% of national revenues from coal), peaking at CNY 35.9 billion in 2024 before falling sharply after 2030 to under CNY 15 billion by 2041. Contribution to subnational tax revenues (in Inner Mongolia and the provinces it exports to) start at a higher level, peaking at CNY 44 billion in 2023 and falling below CNY 15 billion by 2043. Of these subnational tax revenues, over 40% are resource taxes and nearly 20% are VAT payments. This is as expected: the relatively low labour intensity of coal production, low environmental pollution taxes, and the fact that most of Inner Mongolia’s coal is exported, means that tax revenues associated with the local coal industry are closely tied to the production and sale of coal.

Estimates of subsidies directed by the provincial government to Inner Mongolia’s coal industry in the past add some context to these estimates, suggesting that the apparent net fiscal boon from coal industry operations is not as great as it first appears. While subsidies vary from year to year depending on funding priorities and are difficult to measure with any accuracy or certainty, historically, Inner Mongolia is estimated to have granted at least CNY 720 million in temporary tax relief for coal price adjustments and coal rail transport. In 2013, the cost to Inner Mongolia’s provincial government of providing coal users with rail transportation below market rate was estimated at CNY 7.2 billion [

73].

4.2.2. Jing-Jin-Ji

‘Jing-Jin-Ji’ is shorthand for the combined Beijing, Hebei and Tianjin area, a heavily urbanised region with a population of over 112 million. In Beijing’s case, the municipality contains no coal mines, and recently closed its last coal-fired power plant. It imports large volumes of electricity, a majority of which is necessarily from coal plants given China’s electricity mix but does not directly contribute to employment or tax revenue in the coal sector. Tianjin does not produce any coal but hosts 15 GW of coal-fired power plant capacity, while Hebei hosts 58 GW of generating capacity. The combined total of about 72 GW represents 6% of China’s total operating capacity in 2021. Hebei produces about 0.1% of China’s thermal coal (3 million tonnes annually). No new coal capacity is planned, and current capacity will decline as existing plants are progressively closed.

The wealth and population density of Jing-Jin-Ji relative to other provinces, and its status as political capital, have direct implications for the political economy of coal phase-out. With the effects of local air pollution affecting a very large populace, pressure to address air quality issues that have plagued the area for decades has led to the relocation of coal power serving Jing-Jin-Ji away from city areas, and the imposition of the highest environmental pollution tax rates in China. At the same time, government policy promotes the maintenance of stable, affordable electricity prices to help sustain continued high growth rates. Achieving these goals simultaneously requires importing electricity from sources cheap and flexible enough to offset transmission infrastructure costs and ensure uninterrupted power supplies, a role still played predominantly by coal.

Neither electricity prices (both benchmark and spot prices) nor coal prices in Jing-Jin-Ji are particularly high or low, hovering near the national median. This implies greater tax revenue per unit of coal mined or consumed in Jing-Jin-Ji than Inner Mongolia (through greater unit VAT and resource tax revenues, both generated ad valorem). Beijing, Hebei, and Tianjin all impose maximum plant-level environmental pollution taxes (CNY 12/kg for air pollutants, and CNY 14/m

3 for wastewater), the only provinces currently doing so (see

Appendix D,

Figure A1). In Tianjin, these charges are relatively immaterial given the lack of a coal mining industry and relatively small amount of coal-fired generation. In Beijing, they are non-existent. (It should be noted that 65% of Beijing’s electricity demand and 40% of Tianjin’s is met through imported electricity, the bulk of which is generated in coal-fired units in Inner Mongolia, Shanxi, Shaanxi, and Hebei and exported via long-distance transmission lines [

81]).

Hebei’s significant coal plant and mining industry, however, faces higher charges per tonne of coal extracted or burned than other provinces. In combination, the Jing-Jin-Ji provinces collect CNY 1 billion in environmental taxes on coal plants annually (compared to CNY 0.43 billion in Inner Mongolia, which has nearly twice the generation capacity, albeit with fewer operating hours). Further, the estimated average labour intensity of coal mining in Hebei is 16.7 jobs per additional 10,000 tonnes extracted, more than five times that of Inner Mongolia (2.8). Consequently, despite having half as much coal power plant capacity, Hebei’s coal plants support nearly 70% more local coal mining jobs (45,000) as Inner Mongolian plants do (27,000).

4.2.3. Province-Level Comparison

In terms of employment, the national coal industry supports ten times as many mining jobs in Inner Mongolia as Jing-Jin-Ji, and the gap will remain significant for the next two decades. Because of Inner Mongolia’s superior labour efficiency and much larger scale, the absolute numbers converge sharply by 2040, not least because some coal mine employment in Inner Mongolia depends on demand from Jing-Jin-Ji, and Jing-Jin-Ji’s coal demand supports Inner Mongolia jobs. The gap narrows to under 10,000 jobs by 2050. Plant jobs decline steadily in Jing-Jin-Ji as its remaining plants retire on a smooth trajectory to 2050. In Inner Mongolia, employment in plants is stable until the mid-2030s, before declining sharply to 2040 as plants built in the 2010s start to retire and reaching zero in the mid-2050s.

Where the focus for Inner Mongolia is on coal production, continued industrial development, growth in electricity generation and upgrading its position on the electricity value chain, Jing-Jin-Ji is more likely to be concerned with securing reliable, affordable power to facilitate further economic development. These contrasting potential motivations, which mirror the relationship between net coal producers and consumers across China, are not incompatible—in fact, the provinces’ respective interests are well-aligned, such that an expansion of coal power in Inner Mongolia benefits both, particularly in the context of power shortages induced by a shortage of coal supplies in late 2020 [

82] and autumn 2021 [

83].

4.3. Firm-Level Results

Company identifiers in the source datasets allow the composition and trajectory of jobs and tax revenues supported by plants operated by individual companies to be traced. This analysis does so at the parent level, since China’s power generation firms typically control many subsidiaries that ultimately share a beneficial owner—often the government. Since plants can also be owned in different shares by multiple companies, the number of jobs associated with each company is scaled by the proportion of equity ownership it has in a given plant.

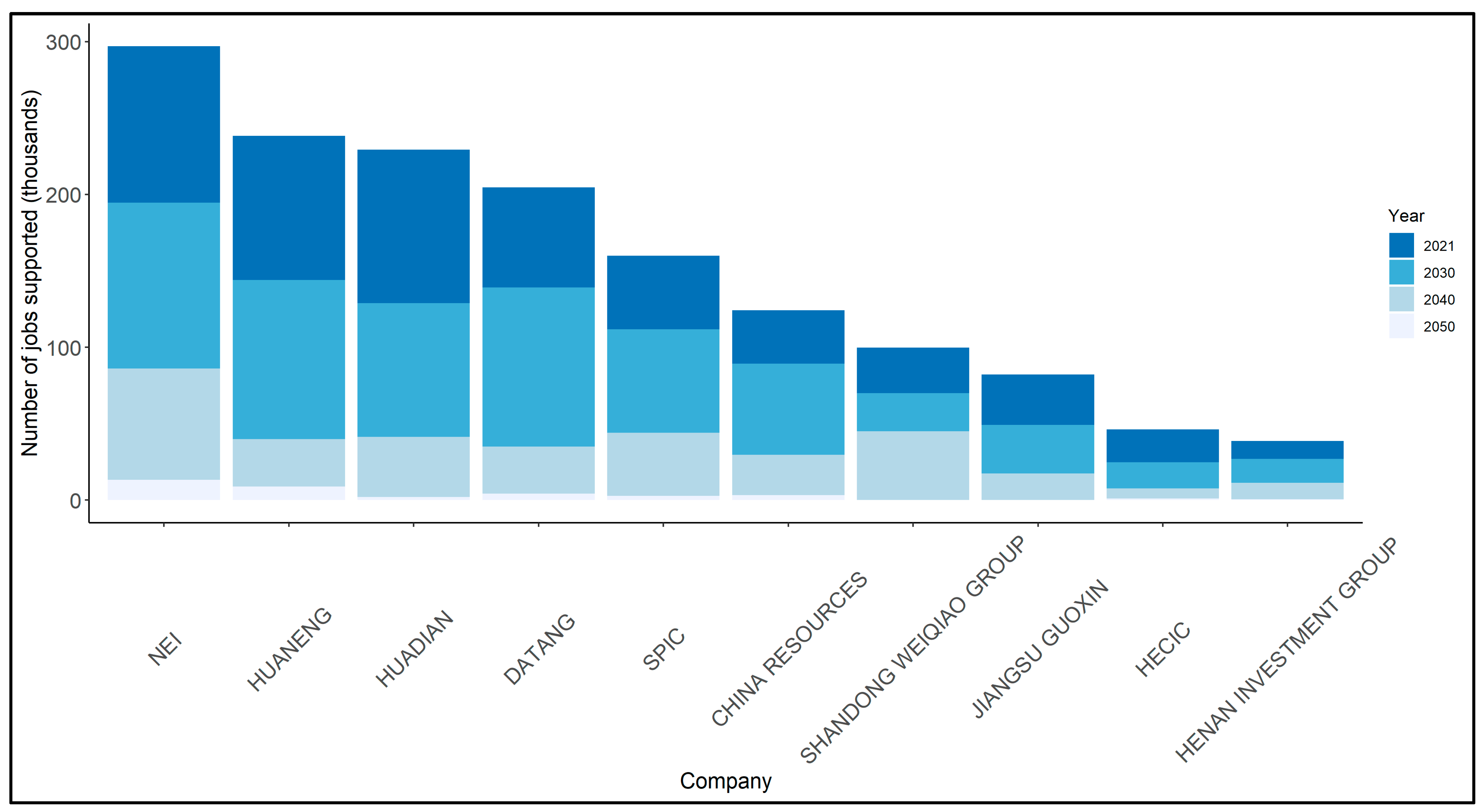

Under the B scenario, the five largest sources of employment in coal power generation and the mines supplying them in 2021 are the ‘Big Five’ power generation companies. In descending order of coal-fired generation capacity, these are National Energy Investment Group (NEI; formerly Shenhua and also known as CHN Energy), Huaneng, Datang, Huadian, and State Power Investment Corporation (SPIC). Each of these firms also controls a considerable amount of coal production (see

Table 4). NEI, created from a merger between two large generating and mining firms, is by far the largest annual producer, at 183 million tonnes.

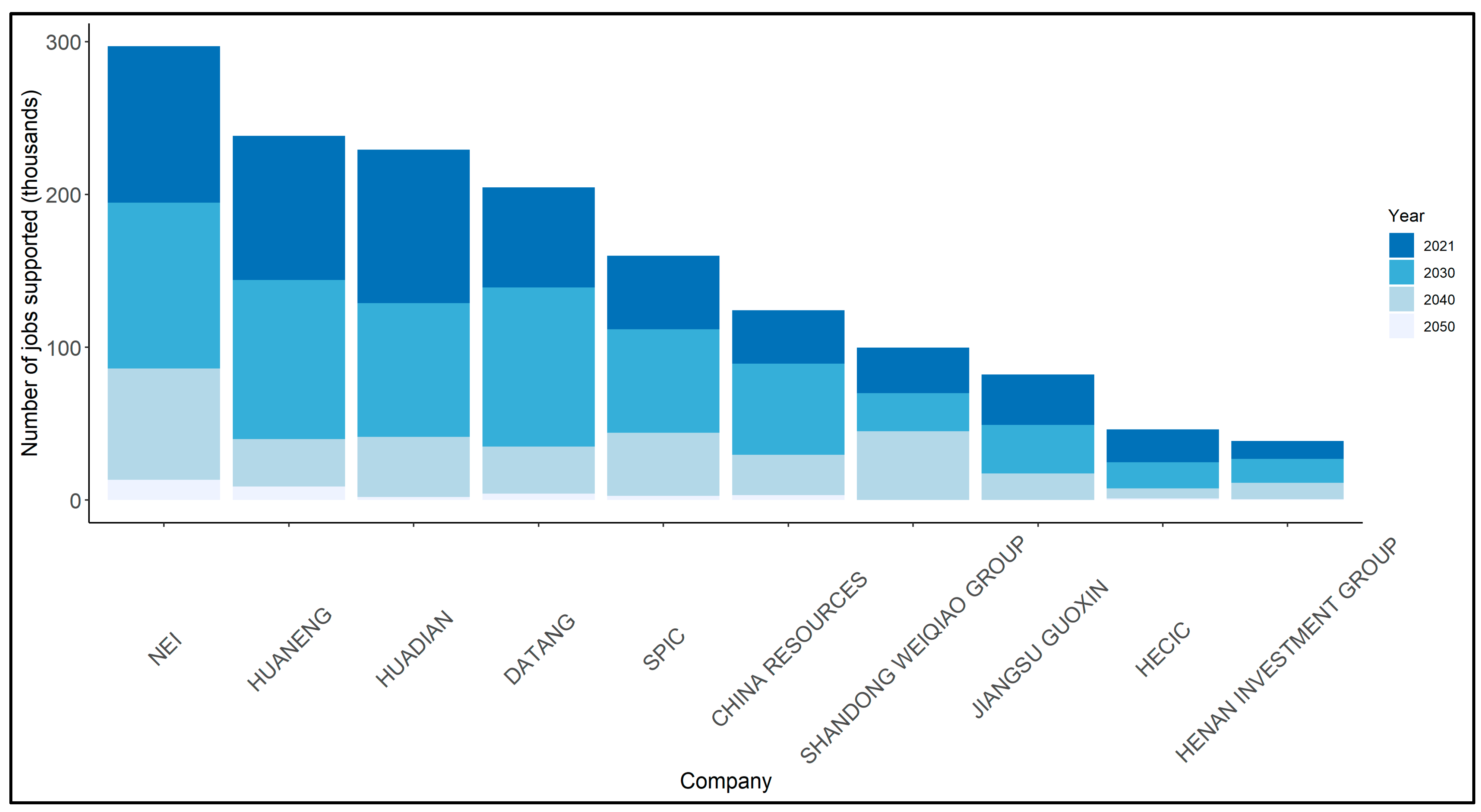

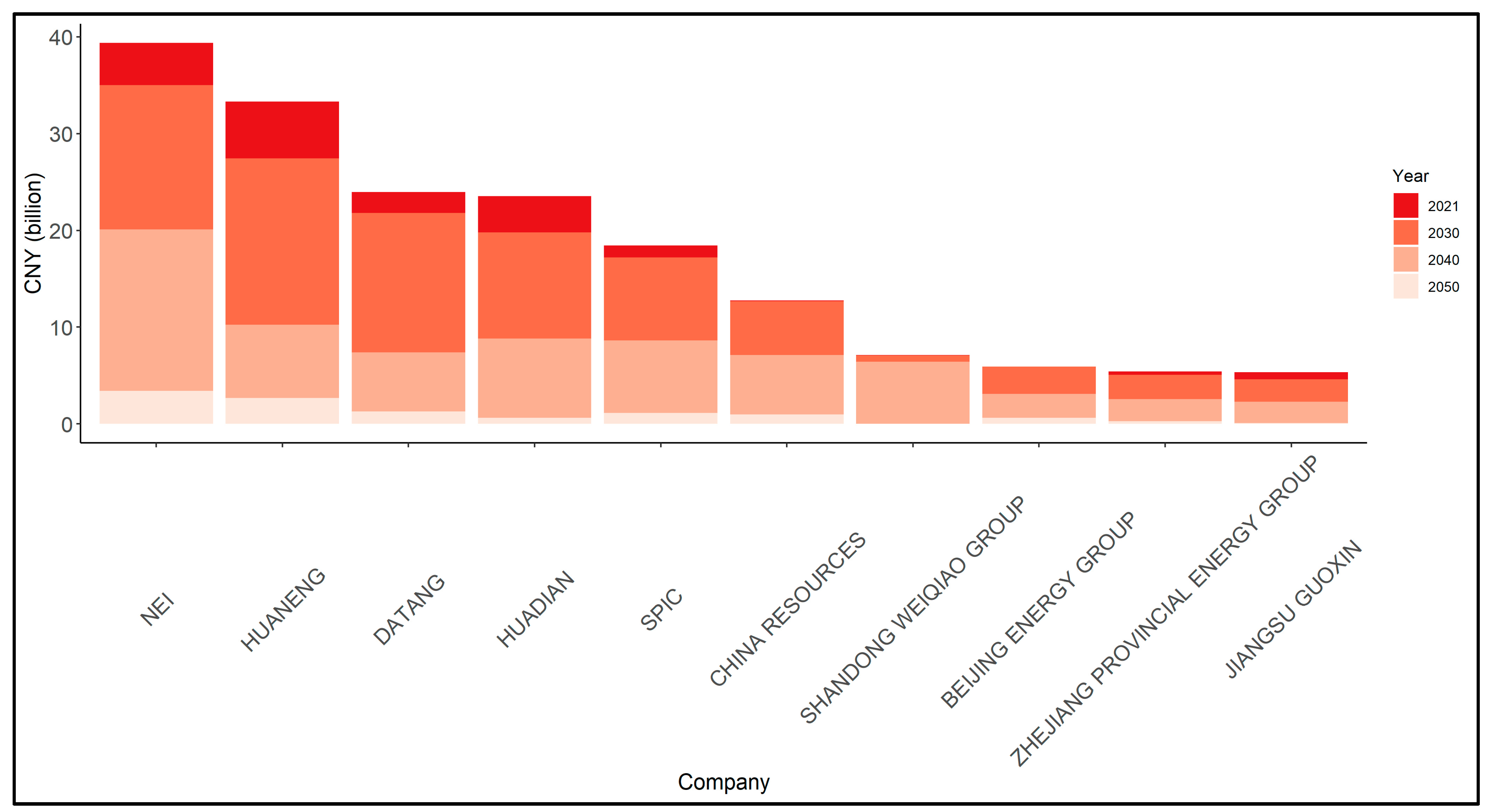

Between them, the ‘Big Five’ support 43% of the jobs in China’s thermal coal industry; the top 10 support 56%. The largest single source of employment, at 297,000, is NEI (see

Figure 8). The coal activities of Huaneng and Huadian support 238,400 and 229,400 jobs each, respectively, while Datang supports 204,700. SPIC supports 160,000. Beyond the ‘Big Five’, plants owned by China Resources (a state-owned integrated mining company) are the next largest source of employment, supporting 135,000 jobs. Among the remaining top ten firms, Shandong Weiqiao (a private sector aluminium producer), and Jiangsu Guoxin (a diversified state-owned investment company) support over 80,000 workers apiece. Looking only at these ten largest firms, it is possible to deduce that close to half of all coal jobs in China, and likely much more across all firms, are directly supported by coal plants in which state-owned enterprises have controlling or minority interests.

Mirroring the trajectory of job losses nationally, in the B scenario, 28% of the jobs currently supported by each of the Big 5 are lost by 2030, and another 50% are lost by 2040. By the 2040s, employment supported by the ten largest firms has declined by 77% in aggregate, ranging from 71–84% for individual companies. The exception is Shandong Weiqiao, where job losses are slower because of Shandong’s high mining labour intensity and significant local coal resources, meaning it imports relatively less from more efficient provinces than other firms.

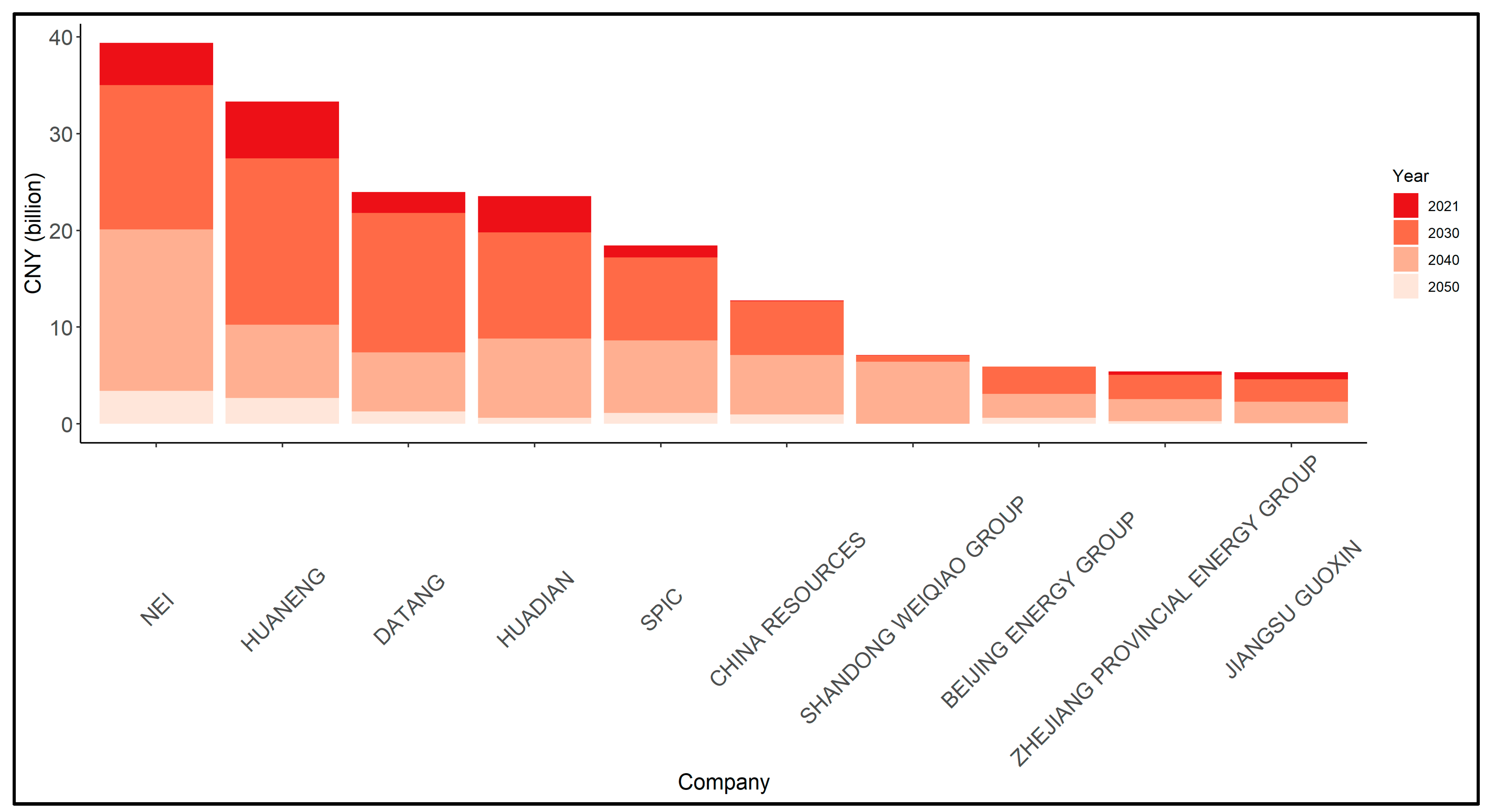

Unsurprisingly, the Big Five are also the largest contributors (directly and indirectly) to tax revenues nationally (see

Figure 9), with the activities of the two largest, NEI and Huaneng, generating CNY 39.4 billion and CNY 33.3 billion in revenue respectively, and the ‘Big Five’ together, almost CNY 140 billion. The largest ten firms contribute almost CNY 175 billion between them, representing more than half of total tax revenues from thermal coal. Mirroring the national trajectory, total tax contributions from the ‘Big Five’ decline relatively slowly at first, falling just 13% to CNY 121.2 billion in 2030, then start to fall much more rapidly after 2034, falling by 60% from their 2021 levels to just CNY 55.2 billion by 2040. The tax contribution of each top ten firm falls by 43–69% by 2040, with the exception of China Resources. By 2050, revenues from the ‘Big Five’ are CNY 9.2 billion (6.6% of their starting value), and those from the top ten firms, CNY 11.1 billion (6.3%).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}