eCooking Delivery Models: Approach to Designing Delivery Models for Electric Pressure Cookers with Case Study for Tanzania

Abstract

:1. Introduction

1.1. Research Context

1.2. Literature Review

1.2.1. Energy Delivery Models

- The enabling environment: the legal frameworks and policies that influence the delivery of energy services.

- The socio-cultural context: the cultural and social values of the end-users and other actors in the energy service supply chain.

- Support services: additional inputs required to overcome barriers or weaknesses in the enabling environment or socio-cultural context, these are extensions of the EDM itself.

1.2.2. Energy Market System Framework

- The market chain: the actors and actions that comprise the delivery of the product or service to the end-users.

- Inputs, services, finance: secondary inputs that support the actors and their activities in the main market chain, some of which will have their own value chains (e.g., physical materials, transport services, loans).

- The enabling environment: the conditions in which the other two levels operate (political, regulatory, financial, and, in contrast to the EDM concept, inclusive of socio-cultural factors which affect energy service uptake and use).

1.2.3. Clean Cooking Scale-Up Models

- The enabling environment: policy and regulations, fiscal context, the political context.

- ‘Industry’ structure and services: physical infrastructure related to the fuel; practices, rules and regulations related to the industry actors; sustainability of supply.

- Energy pricing and costing: capital and running costs of clean fuels and the alternatives, possible cobenefits.

- User and community needs and perceptions: perceptions of affordability, safety, convenience, and aspirational nature of the fuel; awareness of the options.

- Factors influencing consumer demand: other factors not yet covered including consumer knowledge of fuel performance; consumer setting; reliability and quantity of supply; affordability; accessibility; presence of training and finance; and other socio-economic factors.

1.2.4. Reflection on Literature

1.2.5. Paper Scope and Layout

2. Materials and Methods

2.1. eCooking Delivery Models and the eCooking Market System

- eCooking Delivery Model. The specific route to end-users, comprising the activities, resources, and actors in the market chain needed to deliver eCooking appliances to them. These include:

- ○

- The appliance itself.

- ○

- The market chain to be used or optimized for appliance distribution to end-users: Manufacturers, importers, retailers, distributors.

- ○

- The electricity infrastructure to supply the electricity.

- ○

- Securing finance to enable market actors in their activities.

- ○

- Maintenance and repair of the appliances.

- Support services. These are an extension of the delivery model itself, being additional support services needed to deliver eCooking appliances to end-users and support their sustained use. The support services are required to strengthen the market system, addressing weaknesses or gaps in the enabling environment, socio-economic and cultural context, or market chains.

- Socio-economic and cultural context. While this encompasses socio-economic and cultural context of end-users (their values, customs, and practices that might influence their behaviors towards adopting or not adopting an eCooking appliance), it is also applied to other actors in the market chain, given these factors could be drivers or barriers for their participation in an eCDM or support service.

- Enabling environment. The policies and legal frameworks that influence the delivery of eCooking appliances and the electricity infrastructure. Although many of the enabling environment factors are beyond the direct control of the market actors and end-users, assessment of these attributes is important for designing measures for developing sustainable eCDMs.

- Market chains. Market chain actors and established and potential market chains, and data on how the market chains are functioning, i.e., the size of the market and its existing operation.

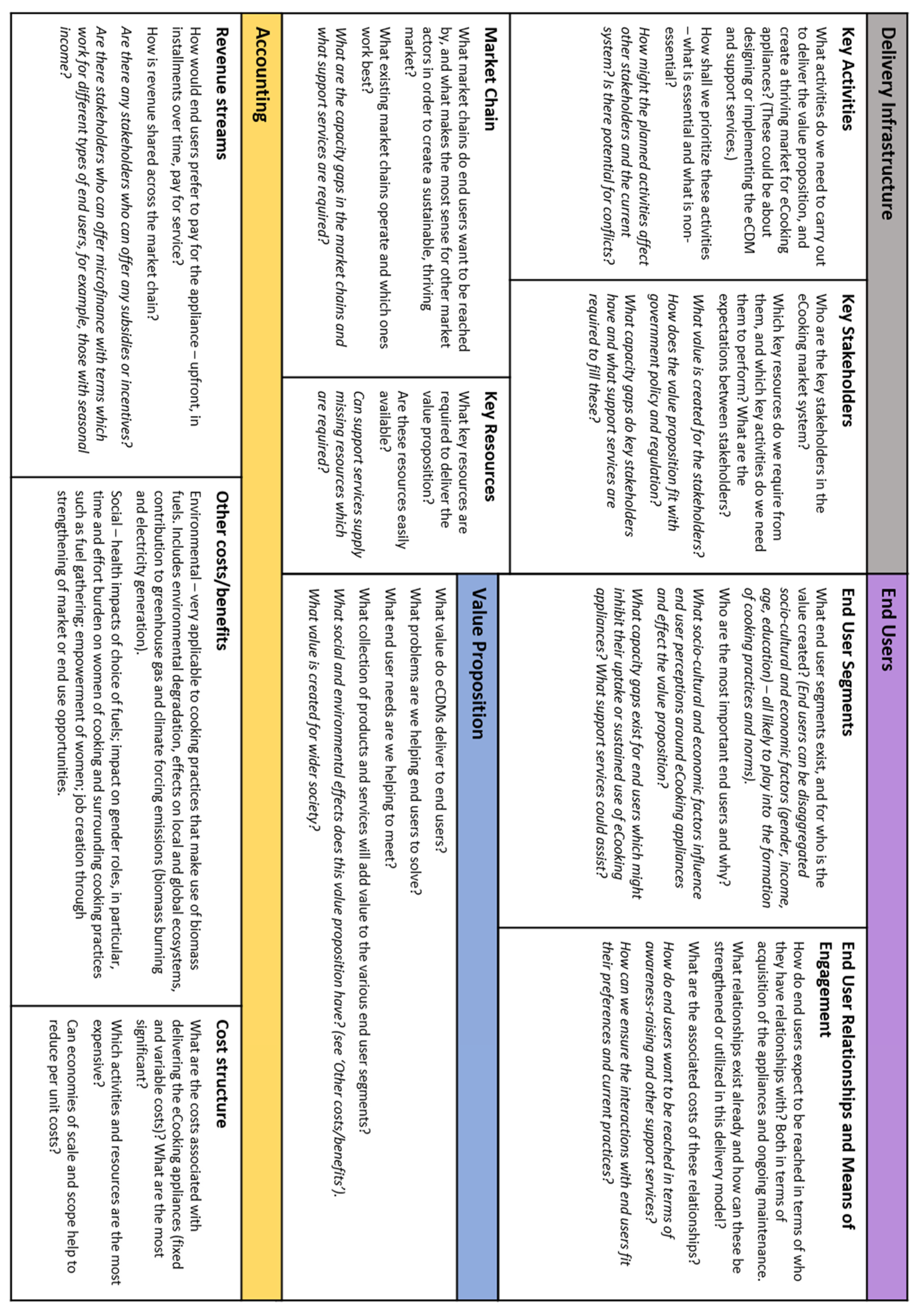

2.2. eCooking Delivery Model Design Approach

2.3. Conducting the eCooking Delivery Model Design Approach in Tanzania

- Rural end-users: End-users in rural areas who have access to electricity through mini-grids run by PowerGen Renewable Energy. They were mostly low-income smallholder farmers who depend on income from agricultural products at Kitaita and Songambele, Gairo District, Morogoro Region.

- Peri-urban/urban end-users: End-users in peri-urban and urban areas who have access to electricity through the national grid. They were from high, medium and low-income households of Kinondoni and Ubungo Districts in Dar es Salaam Region.

3. Results

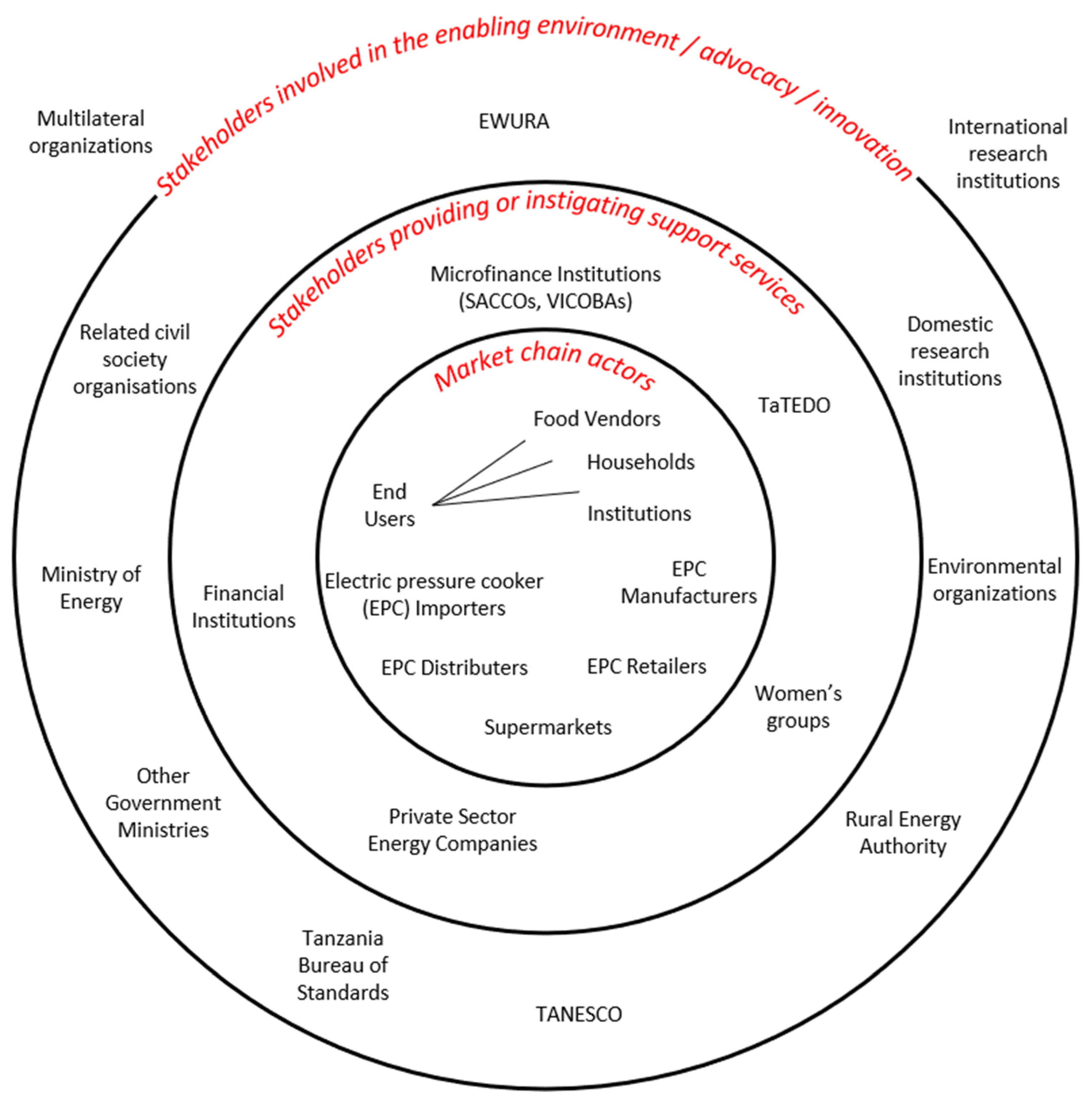

3.1. Step 2: Stakeholder Mapping

3.2. Step 3: Understanding the End-User

3.2.1. End-User Segments

3.2.2. Demand for EPCs

3.2.3. Barriers for End-User Adoption of EPCs

3.2.4. End-User Drivers for Adoption and Value Proposition

3.3. Step 4: Understanding the Market Chains

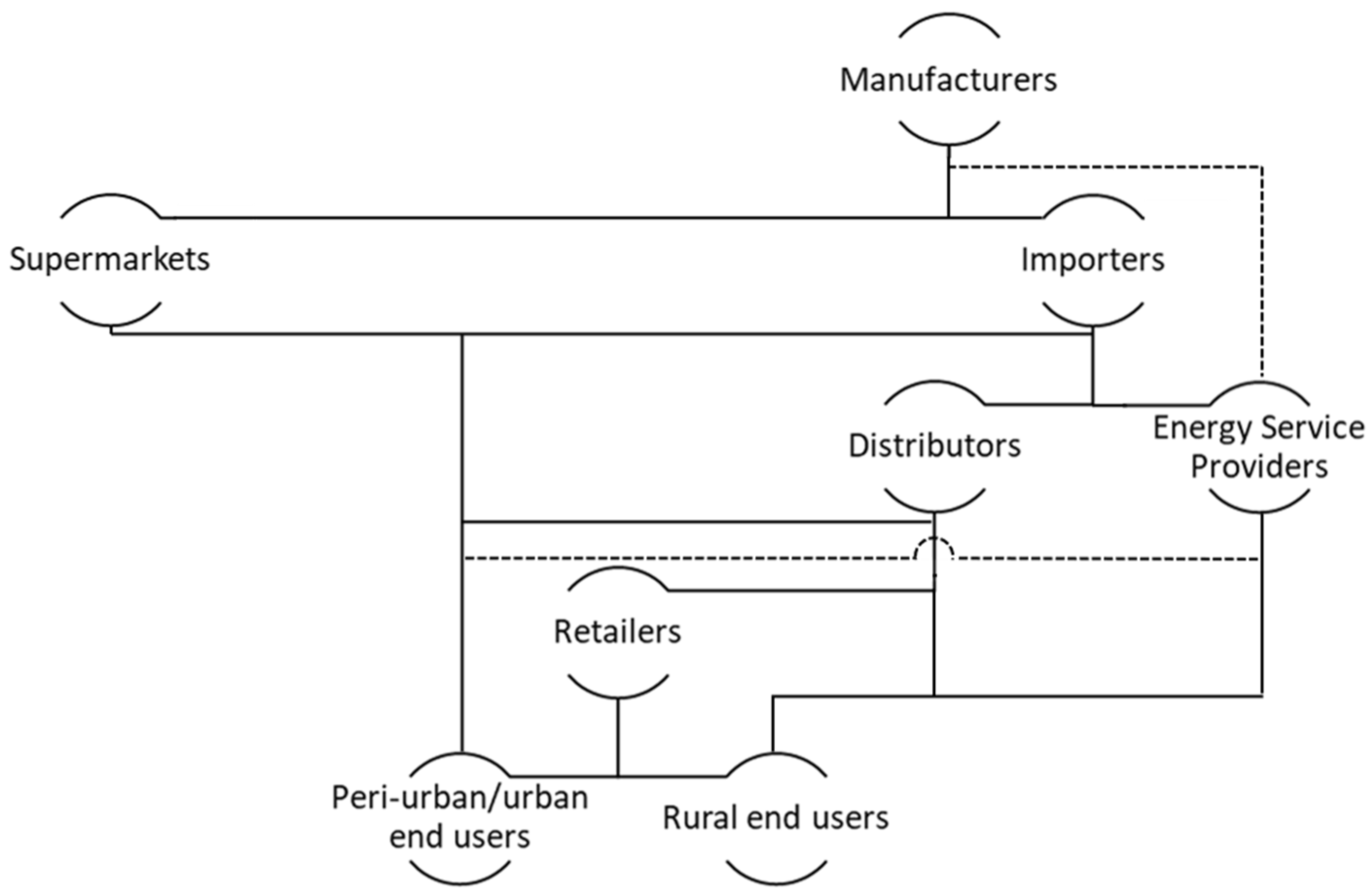

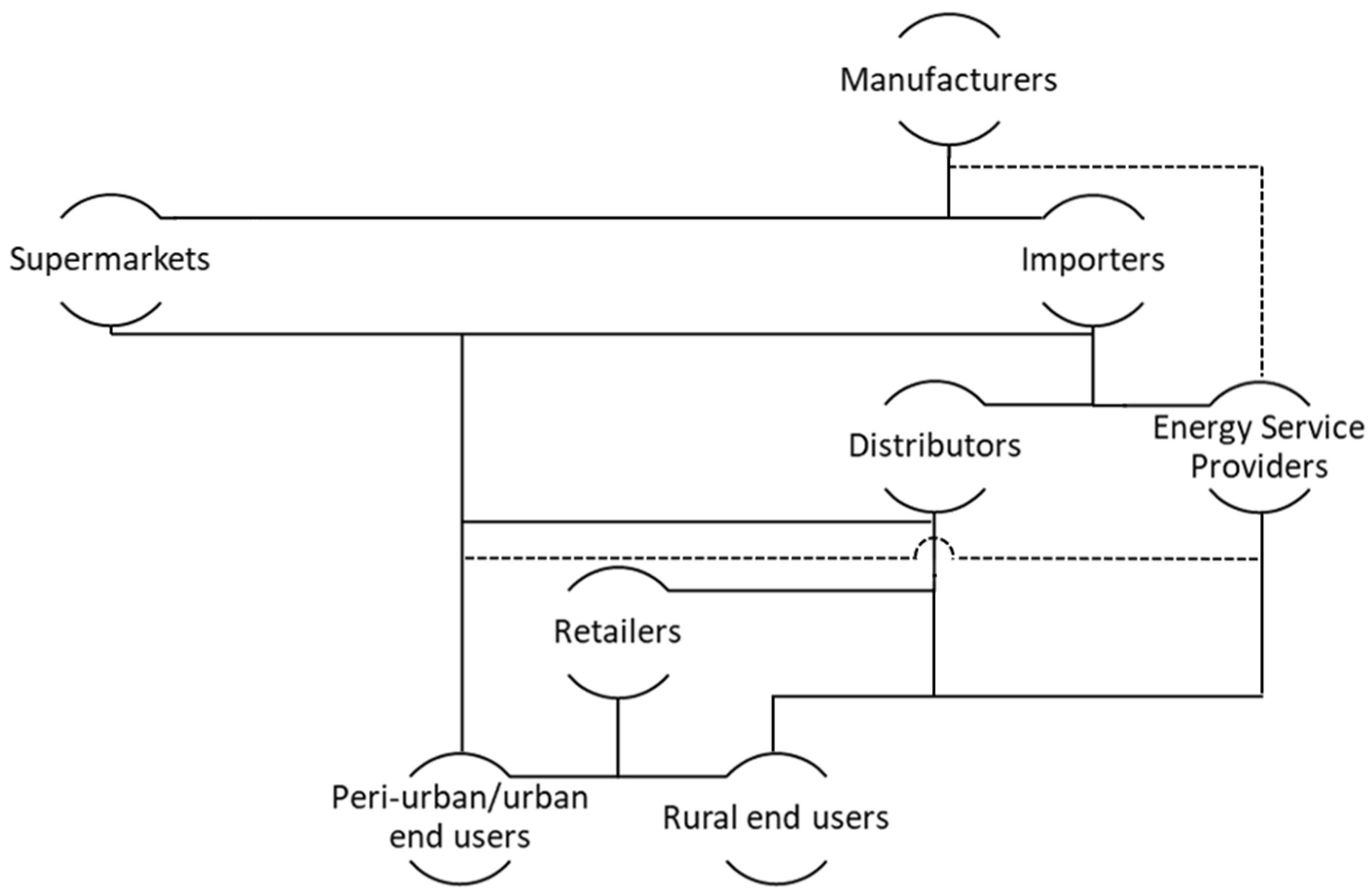

3.3.1. Identification of Market Chains

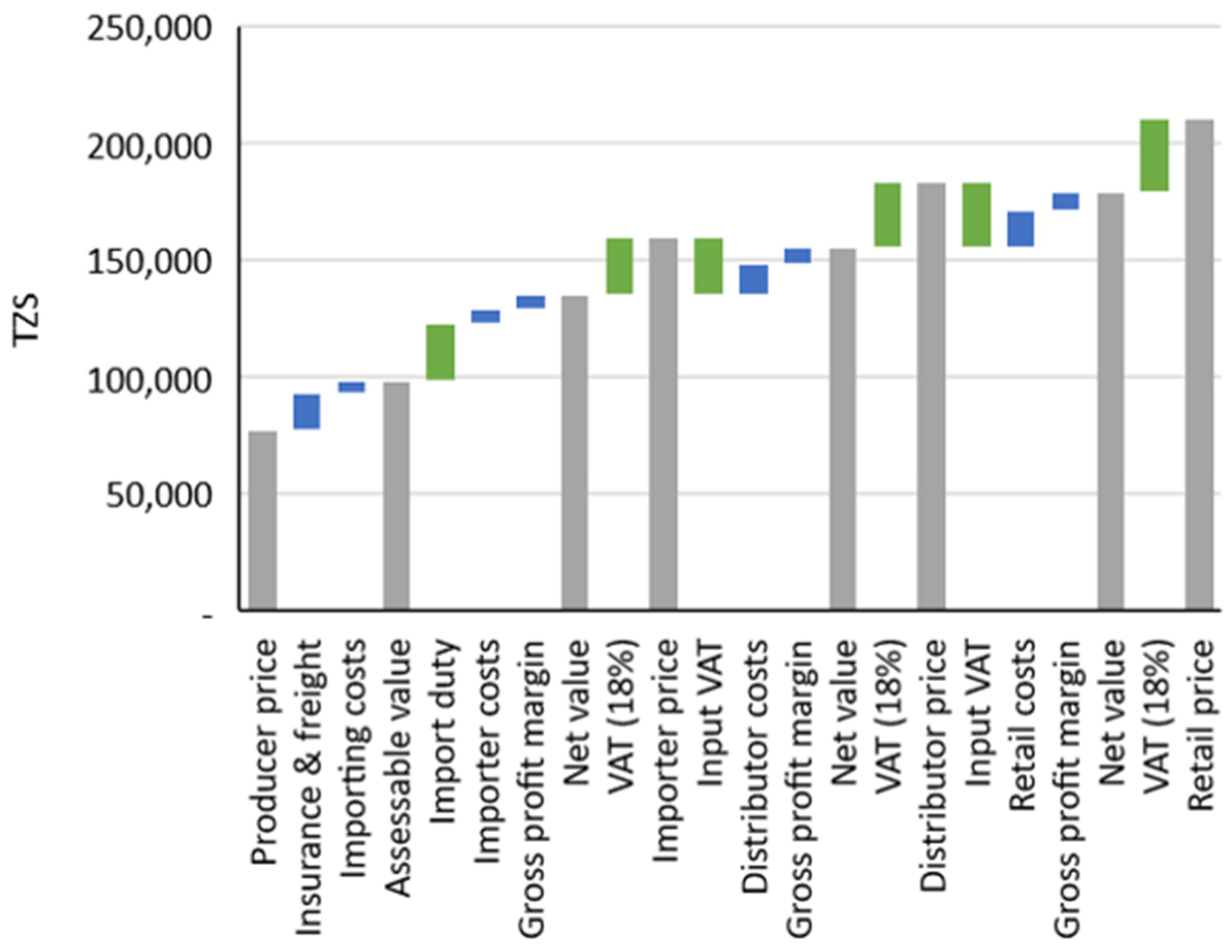

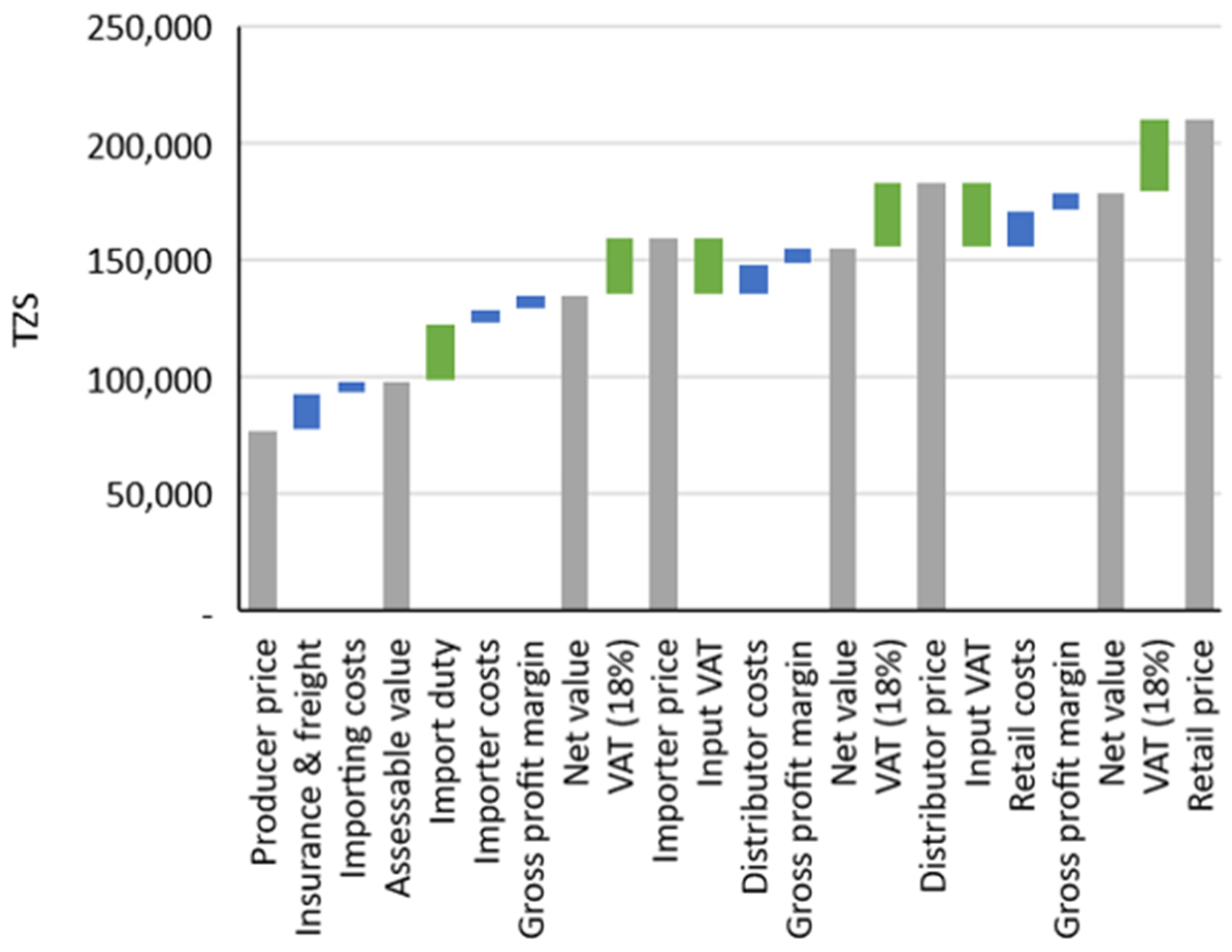

3.3.2. EPC Gross Margin and Tax Analysis

3.3.3. Capacity Gaps for Market Chain Actors

3.4. Step 5: Understanding the Enabling Environment

3.4.1. Electricity Access

3.4.2. Policies and the Policy Environment

3.5. Step 6: Identify and Design eCDM and Support Services

- Awareness-raising campaigns and promotion of EPCs to end-users and other market actors.

- Capacity building training on how to use the EPC for end-users.

- Financial support for market chain actors and end-users.

- After sale services for EPCs.

- Advocacy for import tax exemptions and quality standards.

3.5.1. eCDM for Rural End-users

3.5.2. eCDM for Peri-Urban/Urban End-Users

3.5.3. Other Support Services

3.6. Step 7: Plan and Implement

- Dissemination of the Tanzania eCookbook [56], and training and workshop events, to raise awareness and provide training in how to use an EPC.

- Investigation of EPC repair and maintenance and compilation of a technical manual to be used by technicians providing after sales services.

- Training of technicians in Dar es Salaam, Dodoma, and Kilimanjaro to provide these after sales services.

- Recruitment and training of distribution agents—individuals with strong links into target communities, to disseminate EPCs from an importer of quality EPCs (to reduce the length of the market chain).

- Advocacy targeted at relevant ministries to remove import tax on EPCs to reduce the cost to the end-user.

- Advocacy for financial support for market chain actors to bulk trade in EPCs to address the upcoming availability barrier.

- Advocacy directed at TBS to set eCooking appliance standards and a process to enforce them.

- Conception of an alliance of market chain actors in the eCooking Market System in Tanzania to work together to address enabling environment gaps or market system deficits.

- Trialing credit services for low-income end-users and investigating which microfinance institutions can offer these successfully.

Implementation Thus Far

4. Discussion

4.1. Finance and Credit Mechanisms

4.2. Reflection on the eCDM Concept and Approach

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

Appendix B

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Financial Institutions | Development Partners | Sectoral Ministries and Government Institutions |

|---|---|---|

| Access Bank Akiba Commercial Bank National Microfinance Bank FINCA Microfinance Bank Ngome SACCOS | Embassy of People’s Republic of China Embassy of Japan DFID Tanzania Delegation of the European Union to Tanzania Swedish Embassy in Tanzania United Nations Development Programme (UNDP) United Nations Capital Development Fund (UNCDF) | Ministry of Energy Ministry of Trade and Industries President Office-Ministry of Regional Administration and Local Governments Energy and Water Utilities Regulatory Authority (EWURA) Rural Energy Agency (REA) Tanzania Electric Supply Company (TANESCO) |

References

- IEA; IRENA; UNSD; World Bank; WHO. Tracking SDG 7: The Energy Progress Report; World Bank: Washington, DC, USA, 2021. [Google Scholar]

- WHO. WHO: Household Air Pollution and Health. 2018. Available online: https://www.who.int/en/news-room/fact-sheets/detail/household-air-pollution-and-health (accessed on 13 May 2021).

- Batchelor, S.; Brown, E.; Scott, N.; Leary, J. Two Birds, One Stone—Reframing Cooking Energy Policies in Africa and Asia. Energies 2019, 12, 1591. [Google Scholar] [CrossRef] [Green Version]

- IEA. World Energy Outlook 2020; IEA: Paris, France, 2020; Available online: https://www.iea.org/reports/world-energy-outlook-2020 (accessed on 15 May 2021).

- Leary, J.; Scott, N.; Serenje, N.; Mwila, F.; Batchelor, S. Opportunities & Challenges for eCook Zambia–October 2019 Working Paper. 2019. Available online: https://mecs.org.uk/wp-content/uploads/2020/12/eCook-Zambia-Country-Working-Paper-2-11-19-COMPRESSED.pdf (accessed on 15 May 2021).

- Batchelor, S.; Leary, J.; Sago, S.; Minja, A.; Chepkurui, K.; Sawe, E.; Shuma, J.; Scott, N. Opportunities & Challenges for eCook Tanzania—October 2019 Working Paper. 2019. TaTEDO, Loughborough University, University of Surrey & Gamos Ltd. supported by Innovate UK, UK Aid (DfID) & Gamos Ltd. Available online: https://mecs.org.uk/wp-content/uploads/2020/12/eCook-TZ-Country-Working-Paper-24-10-18-COMPRESSED.pdf (accessed on 15 May 2021).

- Leary, J.; Scott, N.; Numi, A.; Chepkurui, K.; Hanlin, R.; Chepkemoi, M.; Batchelor, S. eCook Kenya Cooking Diaries—September 2019 Working Paper. 2019. Available online: https://mecs.org.uk/wp-content/uploads/2020/12/eCook-Kenya-Cooking-Diaries-September-2019-Working-Paper.pdf (accessed on 15 May 2021).

- Leary, J.; Hlaing, W.W.; Myint, A.; Sane, S.; Win, P.P.; Phyu, T.M.; Moe, E.T.; Htay, T.; Scott, N.; Batchelor, S.; et al. Opportunities & Challenges for eCook Myanmar–October 2019 Working Paper. 2019. Available online: https://mecs.org.uk/wp-content/uploads/2020/12/eCook-Myanmar-Country-Working-Paper-29-10-19-COMPRESSED.pdf (accessed on 15 May 2021).

- Energy Sector Management Assistance Program (ESMAP). Cooking with Electricity: A Cost Perspective; World Bank: Washington, DC, USA, 2020. [Google Scholar]

- Batchelor, S.; Brown, E.; Scott, N.; Leary, J. Experiences of electric pressure cookers in East Africa. In Proceedings of the 10th International Conference on Energy Efficiency in Domestic Appliances and Lighting (EEDAL 19), Jinan, China, 6–8 November 2019; pp. 1–29. [Google Scholar]

- Global LEAP Awards: 2020 Buyer’s Guide for Electric Pressure Cookers. 2021. Available online: https://storage.googleapis.com/e4a-website-assets/2020-Global-LEAP-EPC-Buyers-Guide.pdf (accessed on 25 November 2021).

- International Market Analysis Research and Consulting Group. Multi Cooker Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2019–2024; International Market Analysis Research and Consulting Group: Uttar Pradesh, India, 2019. [Google Scholar]

- Scott, N.; Barnard-Tallier, M.; Clements, A.; Inston, R.; Lapworth, S.; Price, M. Landscaping Study—Modern Foods (Working Paper). 2020. Available online: https://mecs.org.uk/wp-content/uploads/2020/12/Landscape-Study-Modern-Foods-and-Eating-Habits.pdf (accessed on 25 November 2021).

- World Bank. World Bank: Population, Total—Tanzania. Database. Available online: https://data.worldbank.org/indicator/SP.POP.TOTL?locations=TZ (accessed on 25 November 2021).

- Ministry of Finance and Planning—Poverty Eradication Division (MoFP-PED) [Tanzania Mainland] and National Bureau of Statistics (NBS). Tanzania Mainland Household Budget Survey 2017–18, Key Indicators Report; Ministry of Finance and Planning—Poverty Eradication Division (MoFP-PED) [Tanzania Mainland] and National Bureau of Statistics (NBS): Dodoma, Tanzania, 2019.

- Wilson, E.; Wood, R.G.; Garside, B. Sustainable Energy for All? Linking Poor Communities to Modern Energy Services. Working Paper No. 1. 2012. IIED. Available online: https://pubs.iied.org/16038iied (accessed on 11 January 2022).

- Garside, B.; Wykes, S. Planning Pro-Poor Energy Services for Maximum Impact: The Energy Delivery Model Toolkit. 2017. CAFOD and IIED. Available online: https://pubs.iied.org/sites/default/files/pdfs/migrate/16638IIED.pdf (accessed on 11 January 2022).

- Bellanca, R.; Wilson, E. Using the energy delivery model canvas to analyse social enterprises: A biomass briquettes producer in Haiti. Boil. Point 2014, 63, 31–34. [Google Scholar]

- Stakeholder Democracy Network. Solar Lanterns in Niger Delta Communities: Experiences in Building a Sustainable Distribution Model; IIED: London, UK, 2016. [Google Scholar]

- Bellanca, R.; Garside, B. An Approach to Designing Energy Delivery Models That Work for People Living in Poverty. 2013. CAFOD and IIED. Available online: https://pubs.iied.org/16551iied (accessed on 11 January 2022).

- Wilson, E.; Garside, B. Sustainable energy for the poor: Using delivery model analysis to understand and design successful interventions. Boil. Point 2014, 63, 26–30. [Google Scholar]

- Garside, B.; Perera, N. Energy Services for Local Development: Integrated and Inclusive Planning for Country Governments in Kenya; IIED: London, UK, 2021. [Google Scholar]

- Rajagopal, S.; Garside, B.; Walker, L.; Wykes, S. Using the EDM Toolkit to Analyse Impact: A Small-Scale Horticulture Project in Kenya Using the EDM Toolkit to Analyse Impact: A Small-Scale Horticulture Project in Kenya. 2017. CAFOD and IIED. Available online: https://cafod.org.uk/content/download/44015/514078/version/1/file/EDM%20Kenya%20Case%20Study%20Nov%2017.pdf (accessed on 11 January 2022).

- Osterwalder, A.; Pigneur, Y. Business Model Generation: A Handbook for Visionaries, Game Changers and Challengers; John Wiley and Sons, Inc.: Hoboken, NJ, USA, 2010. [Google Scholar]

- Nerini, F.F.; Tomei, J.; To, L.S.; Bisaga, I.; Parikh, P.; Black, M.; Borrion, A.; Spataru, C.; Broto, V.C.; Anandarajah, G.; et al. Mapping synergies and trade-offs between energy and the Sustainable Development Goals. Nat. Energy 2018, 3, 10–15. [Google Scholar] [CrossRef] [Green Version]

- Scott, N.; Batchelor, S.; Jones, T. External Evaluation of Mobile Phone Technology-Based Nutrition and Agriculture Advisory Services in Africa: Mobile Phones, Nutrition, and Health in Tanzania: Business Modelling Endline Report; Institute of Development Studies: Brighton, UK, 2020. [Google Scholar]

- Ching, H.Y.; Fauvel, C. Criticisms, variations and experiences with business model canvas. Eur. J. Agric. For. Res. 2013, 1, 26–37. [Google Scholar]

- Joyce, A.; Paquin, R.L. The triple layered business model canvas: A tool to design more sustainable business models. J. Clean. Prod. 2016, 135, 1474–1486. [Google Scholar] [CrossRef]

- Kwak, H.Y.; Kim, J.C.S.; Lee, S.T.; Gim, G.Y. A Study on The Sustainable Value Generation of Mobile Messenger Service Using ‘Triple Layered Business Model Canvas’. In Proceedings of the 2019 20th IEEE/ACIS International Conference on Software Engineering, Artificial Intelligence, Networking and Parallel/Distributed Computing (SNPD), Toyama, Japan, 8–11 July 2019; pp. 340–350. [Google Scholar]

- Mallard, K.; Garbuio, L.; Debusschere, V. Towards sustainable business model and sustainable design of a hydro generator system dedicated to isolated communities. Procedia CIRP 2020, 90, 251–255. [Google Scholar] [CrossRef]

- Qastharin, A.R. Business model canvas for social enterprise. In Proceedings of the 7th Indonesia International Conference on Innovation, Entrepreneurship, and Small Business, Bandung, Indonesia, 4–6 August 2015. [Google Scholar]

- Sparviero, S. The Case for a Socially Oriented Business Model Canvas: The Social Enterprise Model Canvas. J. Soc. Entrep. 2019, 10, 232–251. [Google Scholar] [CrossRef] [Green Version]

- Leopold, A.; Bloomfield, E.; Meikle, A.; Stevens, L. Toward Universal Energy Access: The Energy Market System Framework; Springer: Cham, Switzerland, 2015. [Google Scholar]

- European Union Energy Initiative Partnership Dialogue Facility (EUEI PDF) and Practical Action. Building Energy Access Markets: A Value Chain Analysis of Key Energy Market Systems; EUEI PDF: Eschborn, Germany, 2015. [Google Scholar]

- Stevens, L.; Santangelo, E.; Muzee, K.; Clifford, M.; Jewitt, S. Market mapping for improved cookstoves: Barriers and opportunities in East Africa. Dev. Pract. 2020, 30, 37–51. [Google Scholar] [CrossRef]

- Puzzolo, E.; Pope, D.; Stanistreet, D.; Rehfuess, E.A.; Bruce, N.G. Clean fuels for resource-poor settings: A systematic review of barriers and enablers to adoption and sustained use. Environ. Res. 2016, 146, 218–234. [Google Scholar] [CrossRef] [PubMed]

- Rosenthal, J.; Balakrishnan, K.; Bruce, N.; Chambers, D.; Graham, J.; Jack, D.; Kline, L.; Masera, O.; Mehta, S.; Mercado, I.R.; et al. Perspectives|Brief Communication Implementation Science to Accelerate Clean Cooking for Public Health. Environ. Health Perspect. 2017, 125, A3–A7. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Quinn, A.K.; Bruce, N.; Puzzolo, E.; Dickinson, K.; Sturke, R.; Jack, D.W.; Mehta, S.; Shankar, A.; Sherr, K.; Rosenthal, J.P. An analysis of efforts to scale up clean household energy for cooking around the world. Energy Sustain. Dev. 2018, 46, 1–10. [Google Scholar] [CrossRef] [PubMed]

- Puzzolo, E.; Zerriffi, H.; Carter, E.; Clemens, H.; Stokes, H.; Jagger, P.; Rosenthal, J.; Petach, H. Supply Considerations for Scaling Up Clean Cooking Fuels for Household Energy in Low- and Middle-Income Countries. GeoHealth 2019, 3, 370–390. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Scott, N.; Sago, S.; Minja, A.; Batchelor, B.; Chepkurui, K.; Sawe, E. eCook Tanzania Cooking Diaries (Working Paper). 2019. TaTEDO, Loughborough University, University of Surrey & Gamos Ltd. supported by Innovate UK, UK Aid (DfID) & Gamos Ltd. Available online: https://mecs.org.uk/wp-content/uploads/2020/12/eCook-Tanzania-Cooking-Diaries-Working-Paper-13-10-19-JL-COMPRESSED.pdf (accessed on 20 July 2021).

- Leary, J.; Sago, S.; Minja, A.; Chepkurui, K.; Sawe, E.; Shuma, J.; Batchelor, S. eCook Tanzania Focus Group Discussions Summary Report–October 2019 Working Paper. 2019. TaTEDO, Loughborough University, University of Surrey & Gamos Ltd. supported by Innovate UK, UK Aid (DfID) & Gamos Ltd. Available online: www.MECS.org.uk (accessed on 20 July 2021).

- Scott, N.; Leary, J.; Sago, S.; Minja, A.; Batchelor, S.; Chepkurui, K.; Sawe, E.; Leach, M.; Brown, E. eCook Tanzania Discrete Choice Modelling–October 2019 Working Paper. 2019. TaTEDO, Loughborough University, University of Surrey & Gamos Ltd. supported by Innovate UK, UK Aid (DfID) & Gamos Ltd. Available online: https://mecs.org.uk/wp-content/uploads/2020/12/eCook-Tanzania-DCE-Working-Paper-23-10-19-JL-2-COMPRESSED.pdf (accessed on 20 July 2021).

- Mayers, J.; Vermeulen, S. Stakeholder Influence Mapping; IIED: London, UK, 2005; Available online: https://policy-powertools.org/Tools/Understanding/docs/stakeholder_influence_mapping_tool_english.pdf (accessed on 12 January 2022).

- Byrne, R.; Onjala, B.; Todd, J.F.; Onsongo, E.; Kabera, T.; Chengo, V.; Ockwell, D.; Atela, J. Electric Cooking in Tanzania: An Actor-Network Map and Analysis of a Nascent Socio-Technical Innovation System. 2020. Modern Energy Cooking Services Programme. Available online: https://mecs.org.uk/wp-content/uploads/2020/12/Byrne-et-al-2020-Tanzania-ISM-MECS-format-200809-1.pdf (accessed on 12 January 2022).

- World Bank. World Bank: Access to Electricity (% of Population)—Tanzania. Database. Available online: https://data.worldbank.org/indicator/EG.ELC.ACCS.ZS?locations=TZ (accessed on 21 May 2021).

- World Bank. World Bank: Access to Electricity, Urban (% of Urban Population)—Tanzania. Database. Available online: https://data.worldbank.org/indicator/EG.ELC.ACCS.UR.ZS?locations=TZ (accessed on 16 December 2021).

- Tanesco. Tanesco Tariffs (BEI ZA Umeme Zilizoidhinishwa). TANESCO Webpage. 2017. Available online: http://www.tanesco.co.tz/index.php/customer-service/tariffs/7-bei-za-umeme-zilizoidhinishwa/file (accessed on 26 November 2021).

- Ministry of Finance and Planning. National Five Year Development Plan 2021/22-2025/26: Realising Competitiveness and Industrialisation for Human Development. 2021. The United Republic of Tanzania. Available online: https://mof.go.tz/docs/news/FYDP%20III%20English.pdf (accessed on 12 January 2022).

- Odarno, L.; Sawe, E.; Swai, M.; Katyega, M.J.J.; Lee, A. Accelerating Mini-Grid Deployment in Sub-Saharan Africa-Lessons from Tanzania; World Resources Institute: Washington, DC, USA, 2017. [Google Scholar]

- Kweka, A.; Clements, A.; Bomba, M.; Schürhoff, N.; Bundala, J.; Mgonda, E.; Nilsson, M.; Avila, E.; Scot, N. Tracking the adoption of electric pressure cookers among mini-grid customers in Tanzania. Energies 2021, 14, 4574. [Google Scholar] [CrossRef]

- Leary, J.; Batchelor, S.; Sago, S.; Minja, A.; Chepkurui, K.; Sawe, E.; Shuma, J. Policy & National Markets Review for eCook in Tanzania–October 2019 Working Paper. 2019. TaTEDO, Loughborough University, University of Surrey & Gamos Ltd. supported by Innovate UK, UK Aid (DfID) & Gamos Ltd. Available online: https://mecs.org.uk/wp-content/uploads/2020/12/TANZANIA-Policy-Review-JL-4-10-19-2-COMPRESSED.pdf (accessed on 12 January 2022).

- Ministry of Energy and Minerals. National Energy Policy (2015); United Republic of Tanzania: Dodoma, Tanzania, 2015. [Google Scholar]

- Camco Clean Energy (Tanzania) Ltd. Biomass Energy Strategy (BEST) Tanzania; EUEI PDF: Eschborn, Germany, 2014. [Google Scholar]

- Uganda National Renewable Energy and Energy Efficiency Alliance (UNREEEA); Uganda Solar Energy Association (USEA); Kenya Renewable Energy Association (KEREA). The East African Regional Hadbook on Solar Taxation. 2020. Supported by UKAID, GOGLA, TEA. Available online: https://www.bdo-ea.com/en-gb/insights/east-africa-regional-solar-taxation-handbook (accessed on 12 January 2022).

- Nygaard, I.; Hansen, U.E.; Mackenzie, G.; Pedersen, M.B. Measures for diffusion of solar PV in selected African countries. Int. J. Sustain. Energy 2017, 36, 707–721. [Google Scholar] [CrossRef] [Green Version]

- Sawe, E.; Aloyce, K. The Tanzania eCookbook, 1st ed.; TaTEDO: Dar es Salaam, Tanzania, 2020. [Google Scholar]

- Energy 4 Impact and Modern Energy Cooking Services. Clean Cooking: Financing Appliances for End Users. 2021. Available online: https://energy4impact.org/sites/default/files/financing_appliances_report.pdf (accessed on 12 January 2022).

- Perros, T.; Büttner, P.; Leary, J.; Parikh, P. Pay-as-you-go LPG: A mixed-methods pilot study in urban Rwanda. Energy Sustain. Dev. 2021, 65, 117–129. [Google Scholar] [CrossRef]

- Shupler, M.; Bonadio, R.C.; Cagnacci, A.Q.C.; Senna, L.A.L.; Campos, R.d.N.G.; Cotti, G.C.; Hoff, P.M.; Fragoso, M.C.B.V.; Estevez-Diz, M.P. Pay-as-you-go liquefied petroleum gas supports sustainable clean cooking in Kenyan informal urban settlement during COVID-19 lockdown. Appl. Energy 2021, 292, 116769. [Google Scholar] [CrossRef] [PubMed]

- Yumkella, K.; Brown, E.; Haselip, J.; Batchelor, S. Solving the clean cooking conundrum in Africa: Technology options in support of SDG7 and the Paris Agreement on Climate Change. In Scaling Up Investment in Climate Technologies: Pathways to Realising Technology Development and Transfer in Support of the Paris Agreement; UNEP DTU: København, Denmark, 2021; pp. 13–26. [Google Scholar]

- Harris, L. A Cutting Edge Solution to a Global Problem: Why PAYGO Electromagnetic Induction Stoves Will Become the Leading Clean Cooking Technology by 2030. NextBillion. 2021. Available online: https://nextbillion.net/paygo-electromagnetic-induction-stoves-clean-cooking-technology/ (accessed on 7 December 2021).

| Rural | Urban/Peri-Urban |

|---|---|

| 11 household surveys | 40 household surveys |

| Two focus groups (1 incl. eCooking demo) (Participants: village leaders, leaders of women’s groups, leaders and members of VICOBAs, minigrid staff) | Nine focus groups (incl. eCooking demos) (Participants: One with VICOBA representatives; Three with local government staff; Five with mixed stakeholders: women’s group representatives, local government staff, local appliance vendors, VICOBA/SACCO representatives) |

| One participatory rural appraisal workshop (incl. eCooking demo) (Participants: village leaders and a demographic range of village members) | |

| Total participants: 47 smallholder and medium scale farmers, 86 households, and 24 businesses | Total participants: 117 households, 92 households engaging in the informal business sector, and 29 enterprises |

| Low Income Segment | Medium Income Segment | High Income Segment | |

|---|---|---|---|

| Daily income (GBP) | <7.50 | 7.50 ≤ x < 15.00 | ≥15.00 |

| Livelihood activities and location | Smallholder farmers (rural) Informal business sector (rural and urban) Other rural and urban households | Medium-scale farmers (rural) Rural enterprises Faith-based organization employees (rural and urban) | Large farmers (rural) Salaried employees (urban) Business owners (urban) |

| % National population | 53 (31.6 million) | 32 (19.1 million) | 15 (9 million) |

| End-User Group | EPCs Purchased in Study | EPCs Purchased at End of Study |

|---|---|---|

| Rural (all deposit and installments) | 6 | 10 |

| Peri-urban/urban | 16 | 72 |

| (Cash) | (9) | |

| (VICOBAs) | (5) | |

| (SACCOs) | (2) |

| Rural | Peri-Urban/Urban |

|---|---|

| Reduce time and labor for collecting cooking fuels Reduce time spent cooking | Reduce household expenditure on cooking fuels Reduce time and effort spent cooking Reduce indoor air pollution Increased safety when cooking Potential to use in a food vending business Cleaner kitchen environment |

| Item | TZS | GBP |

|---|---|---|

| Retail price | 211,192 | 69.69 |

| VAT (18%) | 32,216 | 10.63 |

| Net value | 178,976 | 59.06 |

| Gross profit margin | 7782 | 2.57 |

| Retail costs | 15,563 | 5.14 |

| Input VAT | −28,014 | −9.24 |

| Distributor price | 183,645 | 60.60 |

| VAT (18%) | 28,014 | 9.24 |

| Net value | 155,632 | 51.36 |

| Gross profit margin | 6767 | 2.23 |

| Distributor costs | 13,533 | 4.47 |

| Input VAT | −24,360 | −8.04 |

| Importer price | 159,692 | 52.70 |

| VAT (18%) | 24,360 | 8.04 |

| Net value | 135,332 | 44.66 |

| Gross profit margin | 6444 | 2.13 |

| Importer costs | 6138 | 2.03 |

| Import duty | 24,550 | 8.10 |

| Assessable value | 98,200 | 32.41 |

| Importing costs | 5200 | 1.72 |

| Insurance & freight | 15,500 | 5.12 |

| Producer price | 77,500 | 25.58 |

| Importers | Distributors | Retailers |

|---|---|---|

| Lack of capital for import duties Lack of knowledge on quality, and no standards to regulate quality Requires business training (enterprise development training) | Lack of established market networks Undeveloped marketing techniques/experience for EPCs | Weak transport links Lack of established customer network |

| Lack of awareness of the EPC Does not have EPC repair skills or links to after sales services | ||

| ----------------Lack of capital for bulk appliance purchase---------------- | ||

| Policies | Strategies/Programs | Legal Documents |

|---|---|---|

| Tanzania Monetary Policy (2018) Tanzania Fiscal Policy (2017) Tanzania Trade Policy (2017) National Micro-Finance Policy (2017) National Energy Policy (2015) Energy Subsidy Policy (2013) National Public Private Partnership Policy (2009) Feed-in Tariff Policy (2004) National SMEs Policy (2003) | Power System Master Plan (2016) SE4ALL Action Agenda (2015) Tanzania Investment Prospectus (SE4ALL) (2015) Electricity Supply Industry Reform Strategy and Roadmap 2014–2025 (2014) Biomass Energy Strategy for Tanzania (BEST) (2014) Standardized Power Purchase Agreement & Tariffs (2008) National Five-Year Development Plan 2021/22–2025/26 | Tanzania Trade Development Authority Act (2009) Electricity Act of 2008 Business Activities Registration Act 2007 Energy and Water Utility Regulatory Authority Act (2006) Rural Energy Agency Act of 2005 Environmental Management Act 2004 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Shuma, J.C.; Sawe, E.; Clements, A.; Meena, S.B.; Aloyce, K.; Ngaya, A.E. eCooking Delivery Models: Approach to Designing Delivery Models for Electric Pressure Cookers with Case Study for Tanzania. Energies 2022, 15, 771. https://doi.org/10.3390/en15030771

Shuma JC, Sawe E, Clements A, Meena SB, Aloyce K, Ngaya AE. eCooking Delivery Models: Approach to Designing Delivery Models for Electric Pressure Cookers with Case Study for Tanzania. Energies. 2022; 15(3):771. https://doi.org/10.3390/en15030771

Chicago/Turabian StyleShuma, Jensen C., Estomih Sawe, Anna Clements, Shukuru B. Meena, Katarina Aloyce, and Anande E. Ngaya. 2022. "eCooking Delivery Models: Approach to Designing Delivery Models for Electric Pressure Cookers with Case Study for Tanzania" Energies 15, no. 3: 771. https://doi.org/10.3390/en15030771

APA StyleShuma, J. C., Sawe, E., Clements, A., Meena, S. B., Aloyce, K., & Ngaya, A. E. (2022). eCooking Delivery Models: Approach to Designing Delivery Models for Electric Pressure Cookers with Case Study for Tanzania. Energies, 15(3), 771. https://doi.org/10.3390/en15030771