The Impact of Renewable Energy Supply on Economic Growth and Productivity

Abstract

:1. Introduction

2. Literature Review

3. Materials and Methods

3.1. Preliminary Assumptions

3.2. The Parametric Part of the Model

3.3. The Stochastic Part of the Model

3.4. Data

4. Results

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| 1 | Angola | 46 | Ghana | 91 | Norway (hd) |

| 2 | Albania | 47 | Greece (hd) | 92 | Nepal |

| 3 | United Arab Emir. (hd) | 48 | Guatemala | 93 | New Zealand |

| 4 | Argentina | 49 | China (hd) | 94 | Oman |

| 5 | Armenia | 50 | Honduras | 95 | Pakistan |

| 6 | Australia (hd) | 51 | Croatia | 96 | Panama |

| 7 | Austria (hd) | 52 | Haiti | 97 | Peru |

| 8 | Azerbaijan | 53 | Hungary | 98 | Philippines |

| 9 | Belgium (hd) | 54 | Indonesia | 99 | Poland |

| 10 | Benin | 55 | India | 100 | Portugal |

| 11 | Bangladesh | 56 | Ireland (hd) | 101 | Paraguay |

| 12 | Bulgaria | 57 | Iran | 102 | Qatar |

| 13 | Bahrain | 58 | Iraq | 103 | Romania |

| 14 | Bosnia and Herzegovina | 59 | Iceland (hd) | 104 | Russian Federation |

| 15 | Belarus | 60 | Israel | 105 | Saudi Arabia |

| 16 | Bolivia | 61 | Italy (hd) | 106 | Sudan (Former) |

| 17 | Brazil | 62 | Jamaica | 107 | Senegal |

| 18 | Brunei Darussalam | 63 | Jordan | 108 | Singapore (hd) |

| 19 | Botswana | 64 | Japan (hd) | 109 | El Salvador |

| 20 | Canada (hd) | 65 | Kazakhstan | 110 | Serbia |

| 21 | Switzerland (hd) | 66 | Kenya | 111 | Slovakia |

| 22 | Chile | 67 | Kyrgyzstan | 112 | Slovenia |

| 23 | China | 68 | Cambodia | 113 | Sweden (hd) |

| 24 | Côte dIvoire | 69 | Republic of Korea (hd) | 114 | Syrian Arab Republic |

| 25 | Cameroon | 70 | Kuwait | 115 | Togo |

| 26 | D.R. of the Congo | 71 | Lebanon | 116 | Thailand |

| 27 | Congo | 72 | Sri Lanka | 117 | Tajikistan |

| 28 | Colombia | 73 | Lithuania | 118 | Turkmenistan |

| 29 | Costa Rica | 74 | Luxembourg (hd) | 119 | Trinidad and Tobago |

| 30 | Cyprus (hd) | 75 | Latvia | 120 | Tunisia |

| 31 | Czech Republic | 76 | Morocco | 121 | Turkey |

| 32 | Germany (hd) | 77 | Republic of Moldova | 122 | Taiwan (hd) |

| 33 | Denmark (hd) | 78 | Mexico | 123 | U.R. of Tanzania |

| 34 | Dominican Republic | 79 | TFYR of Macedonia | 124 | Ukraine |

| 35 | Algeria | 80 | Malta | 125 | Uruguay |

| 36 | Ecuador | 81 | Myanmar | 126 | United States (hd) |

| 37 | Egypt | 82 | Montenegro | 127 | Uzbekistan |

| 38 | Spain (hd) | 83 | Mongolia | 128 | Venezuela |

| 39 | Estonia | 84 | Mozambique | 129 | Viet Nam |

| 40 | Ethiopia | 85 | Malaysia | 130 | Yemen |

| 41 | Finland (hd) | 86 | Namibia | 131 | South Africa |

| 42 | France (hd) | 87 | Niger | 132 | Zambia |

| 43 | Gabon | 88 | Nigeria | 133 | Zimbabwe |

| 44 | United Kingdom (hd) | 89 | Nicaragua | ||

| 45 | Georgia | 90 | Netherlands (hd) |

References

- Chen, C.; Pinar, M.; Stengos, T. Renewable energy consumption and economic growth nexus: Evidence from a threshold model. Energy Policy 2020, 139, 111295. [Google Scholar] [CrossRef]

- Dees, P.; Vidican Auktor, G. Renewable energy and economic growth in the MENA region: Empirical evidence and policy implications. Middle East Dev. J. 2018, 10, 225–247. [Google Scholar] [CrossRef]

- Bhattacharya, M.; Paramati, S.R.; Ozturk, I.; Bhattacharya, S. The effect of renewable energy consumption on economic growth: Evidence from top 38 countries. Appl. Energy 2016, 162, 733–741. [Google Scholar] [CrossRef]

- Ozturk, I.; Bilgili, F. Economic growth and biomass consumption nexus: Dynamic panel analysis for Sub-Sahara African countries. Appl. Energy 2015, 137, 110–116. [Google Scholar] [CrossRef]

- Marques, A.C.; Fuinhas, J.A. Is renewable energy effective in promoting growth? Energy Policy 2012, 46, 434–442. [Google Scholar] [CrossRef]

- Bowden, N.; Payne, J.E. Sectoral Analysis of the Causal Relationship between Renewable and Non-Renewable Energy Consumption and Real Output in the US. Energy Sources Part B Econ. Plan. Policy 2010, 5, 400–408. [Google Scholar] [CrossRef]

- Brodny, J.; Tutak, M.; Bindzár, P. Assessing the Level of Renewable Energy Development in the European Union Member States. A 10-Year Perspective. Energies 2021, 14, 3765. [Google Scholar] [CrossRef]

- Papież, M.; Śmiech, S.; Frodyma, K. Determinants of renewable energy development in the EU countries. A 20-year perspective. Renew. Sustain. Energy Rev. 2018, 91, 918–934. [Google Scholar] [CrossRef]

- Bórawski, P.; Bełdycka-Bórawska, A.; Szymańska, E.J.; Jankowski, K.J.; Dubis, B.; Dunn, J.W. Development of renewable energy sources market and biofuels in The European Union. J. Clean. Prod. 2019, 228, 467–484. [Google Scholar] [CrossRef]

- Bhuiyan, M.A.; Zhang, Q.; Khare, V.; Mikhaylov, A.; Pinter, G.; Huang, X. Renewable Energy Consumption and Economic Growth Nexus—A Systematic Literature Review. Front. Environ. Sci. 2022, 10, 412. [Google Scholar] [CrossRef]

- Bulut, U.; Muratoglu, G. Renewable energy in Turkey: Great potential, low but increasing utilization, and an empirical analysis on renewable energy-growth nexus. Energy Policy 2018, 123, 240–250. [Google Scholar] [CrossRef]

- Menegaki, A.N. Growth and renewable energy in Europe: A random effect model with evidence for neutrality hypothesis. Energy Econ. 2011, 33, 257–263. [Google Scholar] [CrossRef]

- Cevik, E.I.; Yıldırım, D.Ç.; Dibooglu, S. Renewable and non-renewable energy consumption and economic growth in the US: A Markov-Switching VAR analysis. Energy Environ. 2021, 32, 519–541. [Google Scholar] [CrossRef]

- Doytch, N.; Narayan, S. Does transitioning towards renewable energy accelerate economic growth? An analysis of sectoral growth for a dynamic panel of countries. Energy 2021, 235, 121290. [Google Scholar] [CrossRef]

- Tutak, M.; Brodny, J. Renewable energy consumption in economic sectors in the EU-27. The impact on economics, environment and conventional energy sources. A 20-year perspective. J. Clean. Prod. 2022, 345, 131076. [Google Scholar] [CrossRef]

- Wang, Q.; Wang, L.; Li, R. Renewable energy and economic growth revisited: The dual roles of resource dependence and anticorruption regulation. J. Clean. Prod. 2022, 337, 130514. [Google Scholar] [CrossRef]

- Hao, L.-N.; Umar, M.; Khan, Z.; Ali, W. Green growth and low carbon emission in G7 countries: How critical the network of environmental taxes, renewable energy and human capital is? Sci. Total Environ. 2021, 752, 141853. [Google Scholar] [CrossRef]

- Fried, H.O.; Lovell, C.A.K.; Schmidt, S.S. (Eds.) The Measurement of Productive Efficiency and Productivity Growth; Oxford University Press: Oxford, UK, 2008; ISBN 0195183525. [Google Scholar]

- Keen, S.; Ayres, R.U.; Standish, R. A Note on the Role of Energy in Production. Ecol. Econ. 2019, 157, 40–46. [Google Scholar] [CrossRef] [Green Version]

- Keen, S. The appallingly bad neoclassical economics of climate change. Globalizations 2022, 18, 1149–1177. [Google Scholar] [CrossRef]

- Ozturk, I. A literature survey on energy–growth nexus. Energy Policy 2010, 38, 340–349. [Google Scholar] [CrossRef]

- Gabr, E.M.; Mohamed, S.M. Energy management model to minimize fuel consumption and control harmful gas emissions. Int. J. Energy Water Res. 2020, 4, 453–463. [Google Scholar] [CrossRef]

- Huang, B.-N.; Hwang, M.J.; Yang, C.W. Causal relationship between energy consumption and GDP growth revisited: A dynamic panel data approach. Ecol. Econ. 2008, 67, 41–54. [Google Scholar] [CrossRef]

- Saldivia, M.; Kristjanpoller, W.; Olson, J.E. Energy consumption and GDP revisited: A new panel data approach with wavelet decomposition. Appl. Energy 2020, 272, 115207. [Google Scholar] [CrossRef]

- Bilan, Y.; Streimikiene, D.; Vasylieva, T.; Lyulyov, O.; Pimonenko, T.; Pavlyk, A. Linking between Renewable Energy, CO2 Emissions, and Economic Growth: Challenges for Candidates and Potential Candidates for the EU Membership. Sustainability 2019, 11, 1528. [Google Scholar] [CrossRef] [Green Version]

- Osiewalski, J.; Wróblewska, J.; Makieła, K. Bayesian comparison of production function-based and time-series GDP models. Empir. Econ. 2020, 58, 1355–1380. [Google Scholar] [CrossRef] [Green Version]

- Makieła, K. Bayesian inference and Gibbs sampling in generalized true random-effects models. Cent. Eur. J. Econ. Model. Econom. 2017, 9, 69–95. [Google Scholar]

- Aigner, D.; Lovell, C.K.; Schmidt, P. Formulation and estimation of stochastic frontier production function models. J. Econom. 1977, 6, 21–37. [Google Scholar] [CrossRef]

- Meeusen, W.; van den Broeck, J. Efficiency estimation from Cobb-Douglas production functions with composed error. Int. Econ. Rev. 1977, 18, 435–444. [Google Scholar] [CrossRef]

- Barro, R.; Sala-i-Martin, X. Economic Growth, 2nd ed.; MIT Press: Cambridge, MA, USA, 2003. [Google Scholar]

- Colombi, R.; Kumbhakar, S.C.; Martini, G.; Vittadini, G. Closed-skew normality in stochastic frontiers with individual effects and long/short-run efficiency. J. Product. Anal. 2014, 42, 123–136. [Google Scholar] [CrossRef]

- Tsionas, E.G.; Kumbhakar, S.C. Firm-heterogeneity, persistent and transient technical inefficiency: A generalized true random effects model. J. Appl. Econ. 2014, 29, 110–132. [Google Scholar] [CrossRef]

- Badunenko, O.; Kumbhakar, S.C. When, where and how to estimate persistent and transient efficiency in stochastic frontier panel data models. Eur. J. Oper. Res. 2016, 255, 272–287. [Google Scholar] [CrossRef] [Green Version]

- Filippini, M.; Greene, W. Persistent and transient productive inefficiency: A maximum simulated likelihood approach. J. Product. Anal. 2016, 45, 187–196. [Google Scholar] [CrossRef]

- Carvalho, A. Energy efficiency in transition economies: A stochastic frontier approach. Econ. Transit. 2018, 26, 553–578. [Google Scholar] [CrossRef]

- Koop, G.; Osiewalski, J.; Steel, M.F.J. Bayesian efficiency analysis through individual effects: Hospital cost frontiers. J. Econom. 1997, 76, 77–105. [Google Scholar] [CrossRef]

- Makieła, K.; Wojciechowski, L.; Wach, K. Effectiveness of FDI, technological gap and sectoral level productivity in the Visegrad Group. Technol. Econ. Dev. Econ. 2021, 27, 149–174. [Google Scholar] [CrossRef]

- Koop, G.; Osiewalski, J.; Steel, M.F. Hospital Efficiency Analysis through Individual Effects: A Bayesian Approach; CentER Discussion Paper 9447; Tilburg University: Tilburg, The Netherlands, 1994. [Google Scholar]

- OECD. Renewable Energy (Indicator). Available online: https://data.oecd.org/energy/renewable-energy.htm (accessed on 1 February 2022).

- Feenstra, R.C.; Inklaar, R.; Timmer, M.P. The Next Generation of the Penn World Table. Am. Econ. Rev. 2015, 105, 3150–3182. [Google Scholar] [CrossRef] [Green Version]

- Adedoyin, F.F.; Bekun, F.V.; Alola, A.A. Growth impact of transition from non-renewable to renewable energy in the EU: The role of research and development expenditure. Renew. Energy 2020, 159, 1139–1145. [Google Scholar] [CrossRef]

- Doytch, N.; Narayan, S. Does FDI influence renewable energy consumption? An analysis of sectoral FDI impact on renewable and non-renewable industrial energy consumption. Energy Econ. 2016, 54, 291–301. [Google Scholar] [CrossRef]

- Makiela, K.; Ouattara, B. Foreign direct investment and economic growth: Exploring the transmission channels. Econ. Model. 2018, 72, 296–305. [Google Scholar] [CrossRef]

- Felipe, J.; McCombie, J.S. The Aggregate Production Function and the Measurement of Technical Change; Edward Elgar: Cheltenham, UK, 2013. [Google Scholar]

- Growiec, J. Aggregate Production Function in Studies of Economic Growth and Convergence; Warsaw School of Economics Press: Warsaw, Poland, 2012. (In Polish) [Google Scholar]

- Koop, G.; Osiewalski, J.; Steel, M.F.J. Modeling the Sources of Output Growth in a Panel of Countries. J. Bus. Econ. Stat. 2000, 18, 284–299. [Google Scholar] [CrossRef]

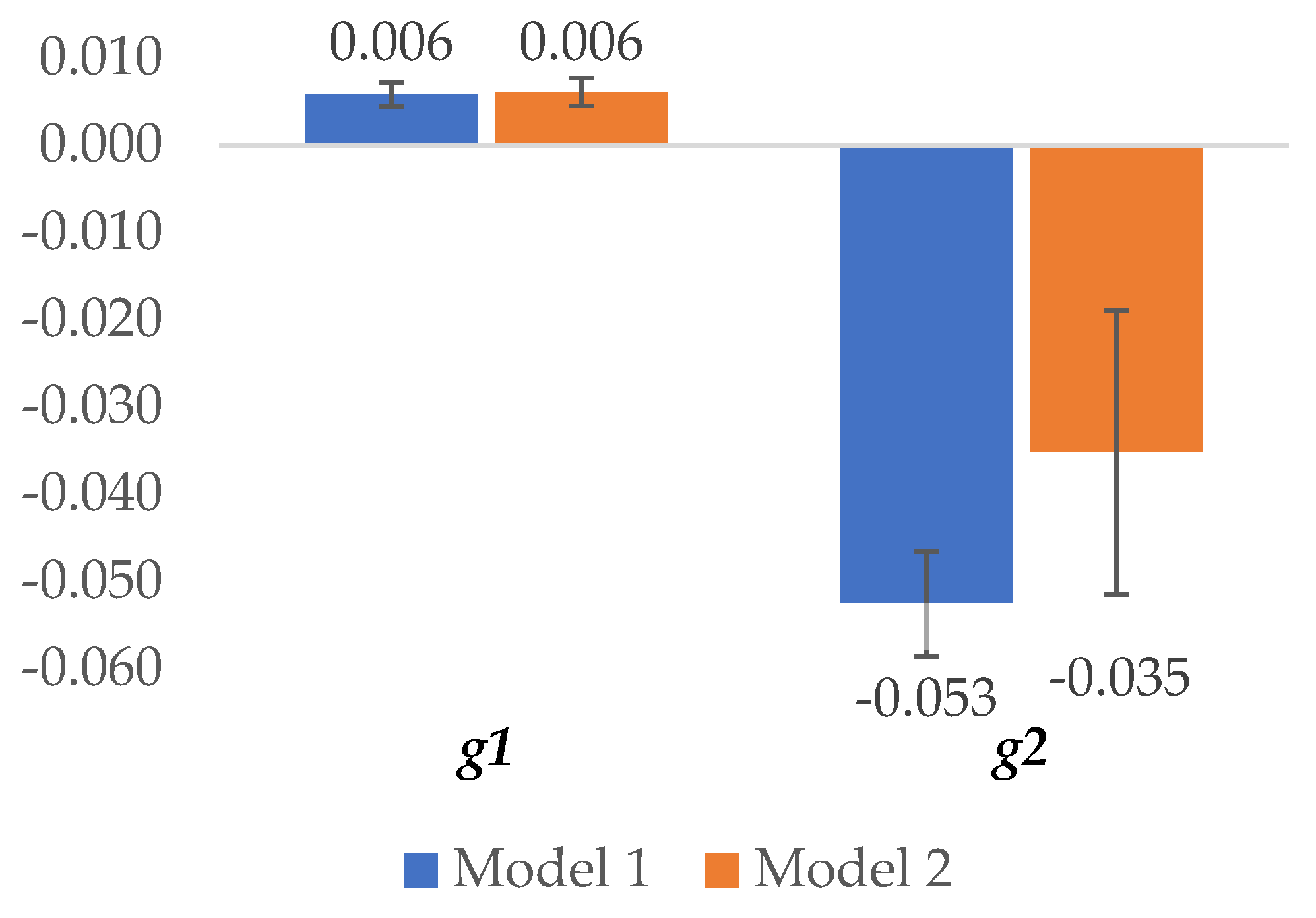

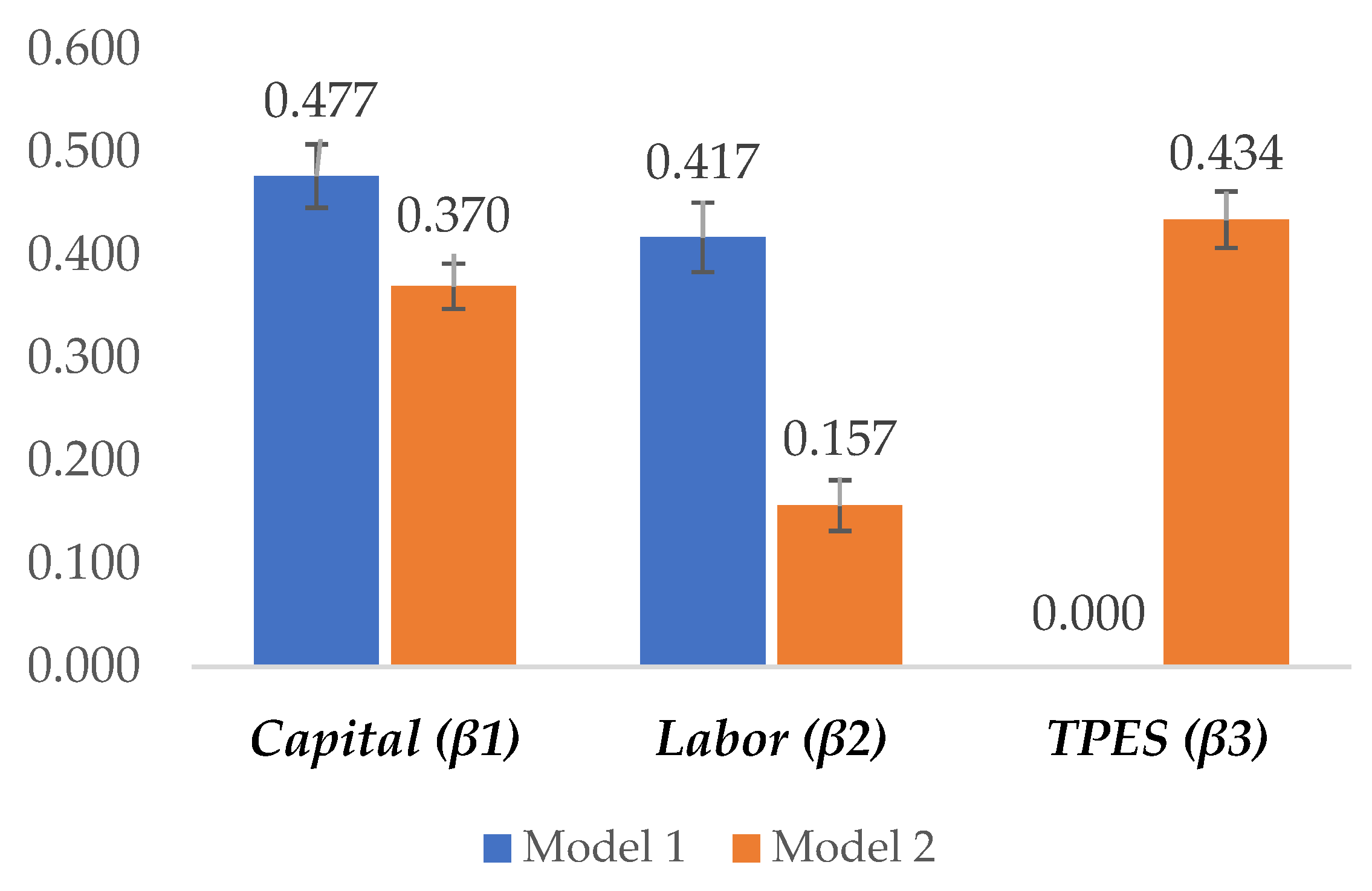

| Parameter | P.Mean | P.Std | t |

|---|---|---|---|

| 12.4269 | 0.0416 | 299.00 | |

| 0.4769 | 0.0309 | 15.43 | |

| 0.4174 | 0.0338 | 12.37 | |

| −0.0356 | 0.0073 | 4.87 | |

| −0.0140 | 0.0143 | 0.98 | |

| 0.0841 | 0.0142 | 5.92 | |

| 0.0002 | 0.0019 | 0.11 | |

| 0.3613 | 0.0468 | 7.71 | |

| 0.0300 | 0.0029 | 10.17 | |

| 0.4692 | 0.0579 | 8.10 | |

| (av.) | 0.0765 | 0.0052 | 14.86 |

| −2.5722 | 0.0670 | 38.38 | |

| 0.0058 | 0.0014 | 4.24 | |

| −0.0525 | 0.0060 | 8.73 |

| Parameter | P.Mean | P.Std | t |

|---|---|---|---|

| 12.3775 | 0.0429 | 288.74 | |

| 0.3699 | 0.0220 | 16.83 | |

| 0.1568 | 0.0247 | 6.35 | |

| 0.4344 | 0.0274 | 15.85 | |

| 0.0514 | 0.0111 | 4.65 | |

| −0.0052 | 0.0183 | 0.28 | |

| 0.1200 | 0.0238 | 5.03 | |

| 0.0848 | 0.0172 | 4.93 | |

| −0.1835 | 0.0291 | 6.30 | |

| −0.0607 | 0.0311 | 1.95 | |

| 0.0049 | 0.0017 | 2.82 | |

| 0.1530 | 0.0329 | 4.65 | |

| 0.0373 | 0.0032 | 11.64 | |

| 0.4498 | 0.0494 | 9.11 | |

| (av.) | 0.0600 | 0.0044 | 13.66 |

| −2.8003 | 0.0858 | 32.65 | |

| 0.0061 | 0.0016 | 3.93 | |

| −0.0352 | 0.0163 | 2.16 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Makieła, K.; Mazur, B.; Głowacki, J. The Impact of Renewable Energy Supply on Economic Growth and Productivity. Energies 2022, 15, 4808. https://doi.org/10.3390/en15134808

Makieła K, Mazur B, Głowacki J. The Impact of Renewable Energy Supply on Economic Growth and Productivity. Energies. 2022; 15(13):4808. https://doi.org/10.3390/en15134808

Chicago/Turabian StyleMakieła, Kamil, Błażej Mazur, and Jakub Głowacki. 2022. "The Impact of Renewable Energy Supply on Economic Growth and Productivity" Energies 15, no. 13: 4808. https://doi.org/10.3390/en15134808

APA StyleMakieła, K., Mazur, B., & Głowacki, J. (2022). The Impact of Renewable Energy Supply on Economic Growth and Productivity. Energies, 15(13), 4808. https://doi.org/10.3390/en15134808