Does the Net Present Value as a Financial Metric Fit Investment in Green Energy Security?

Abstract

:1. Introduction

2. Literature Review

3. Materials and Methods

4. Results and Discussion

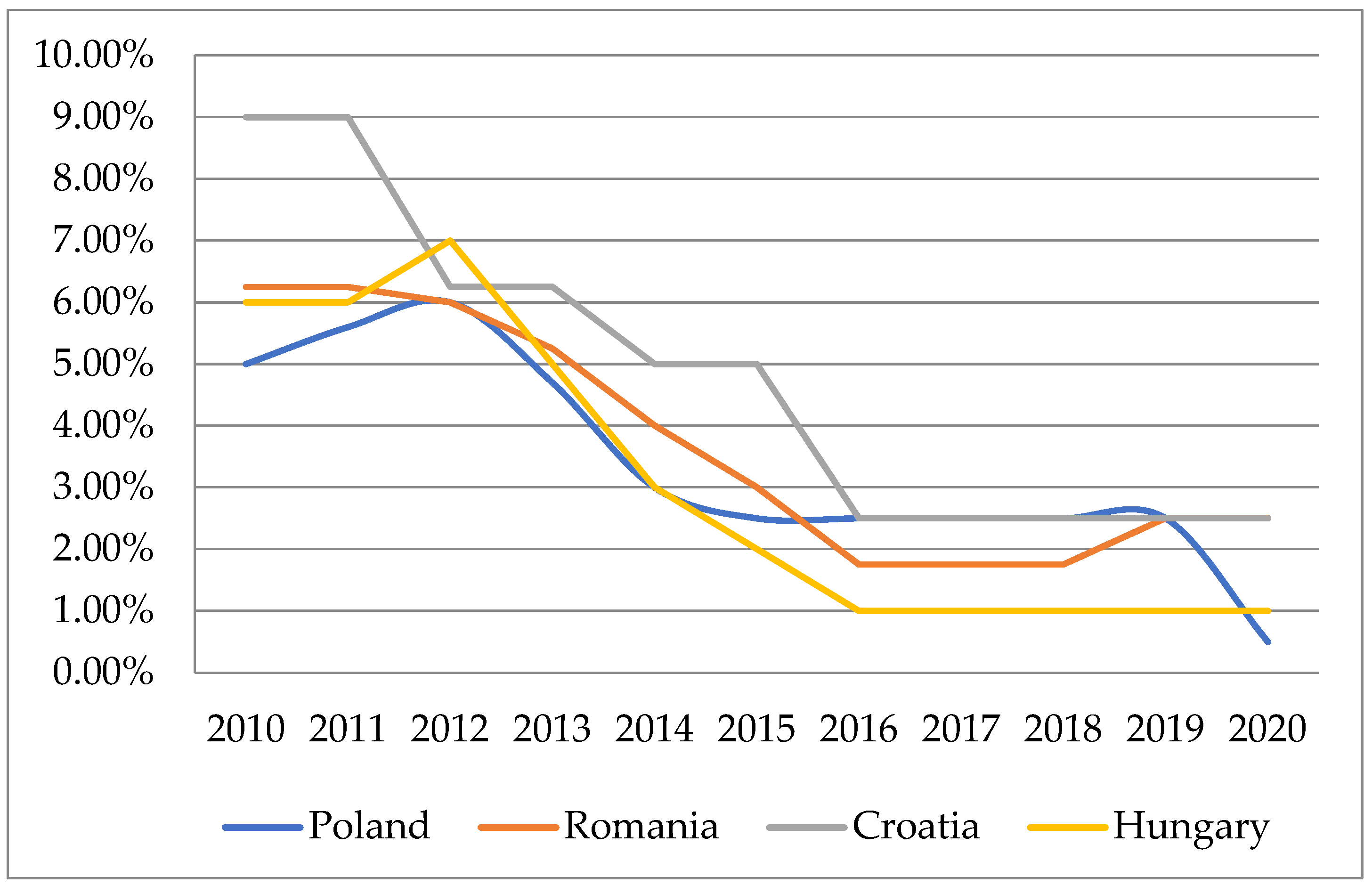

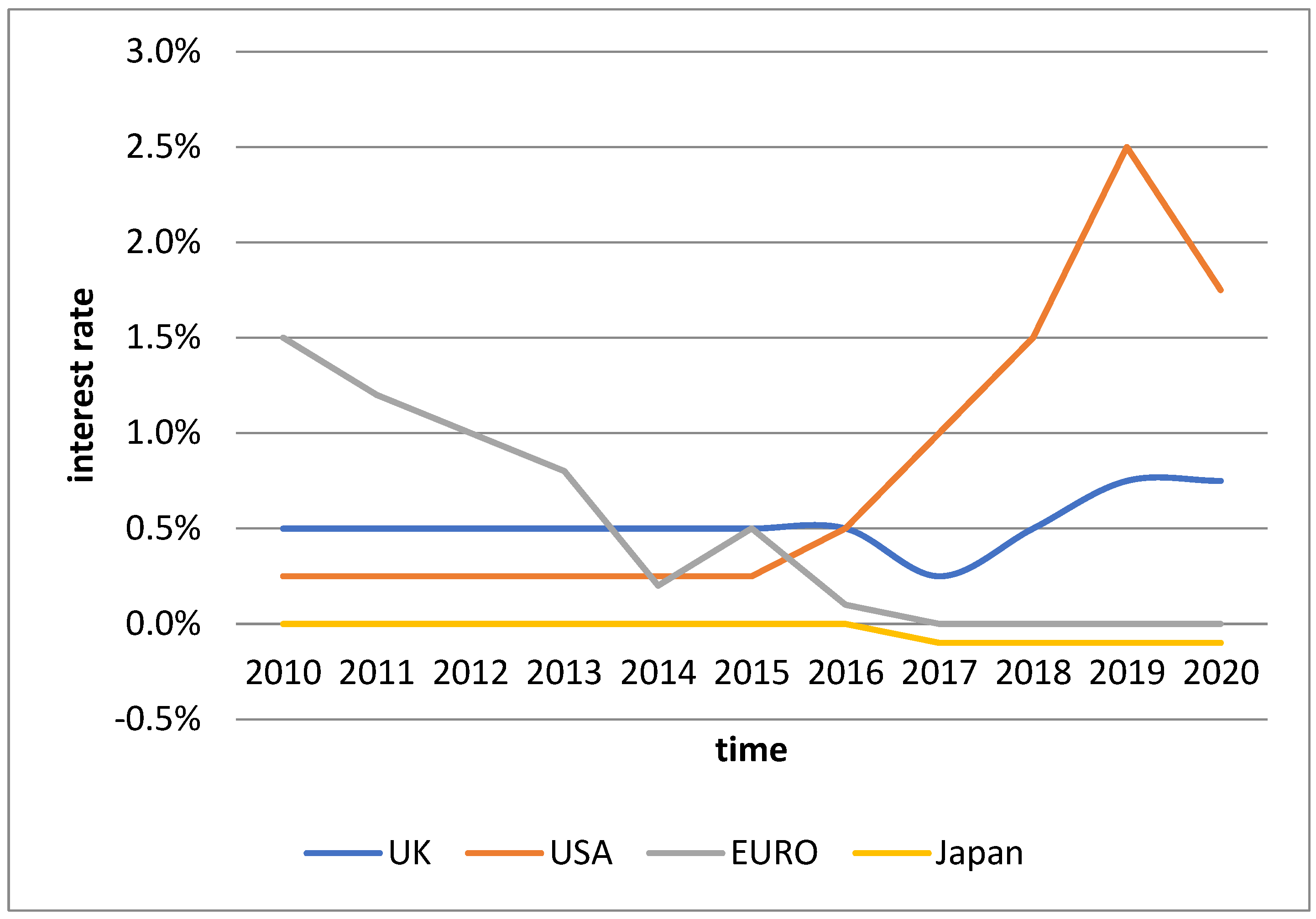

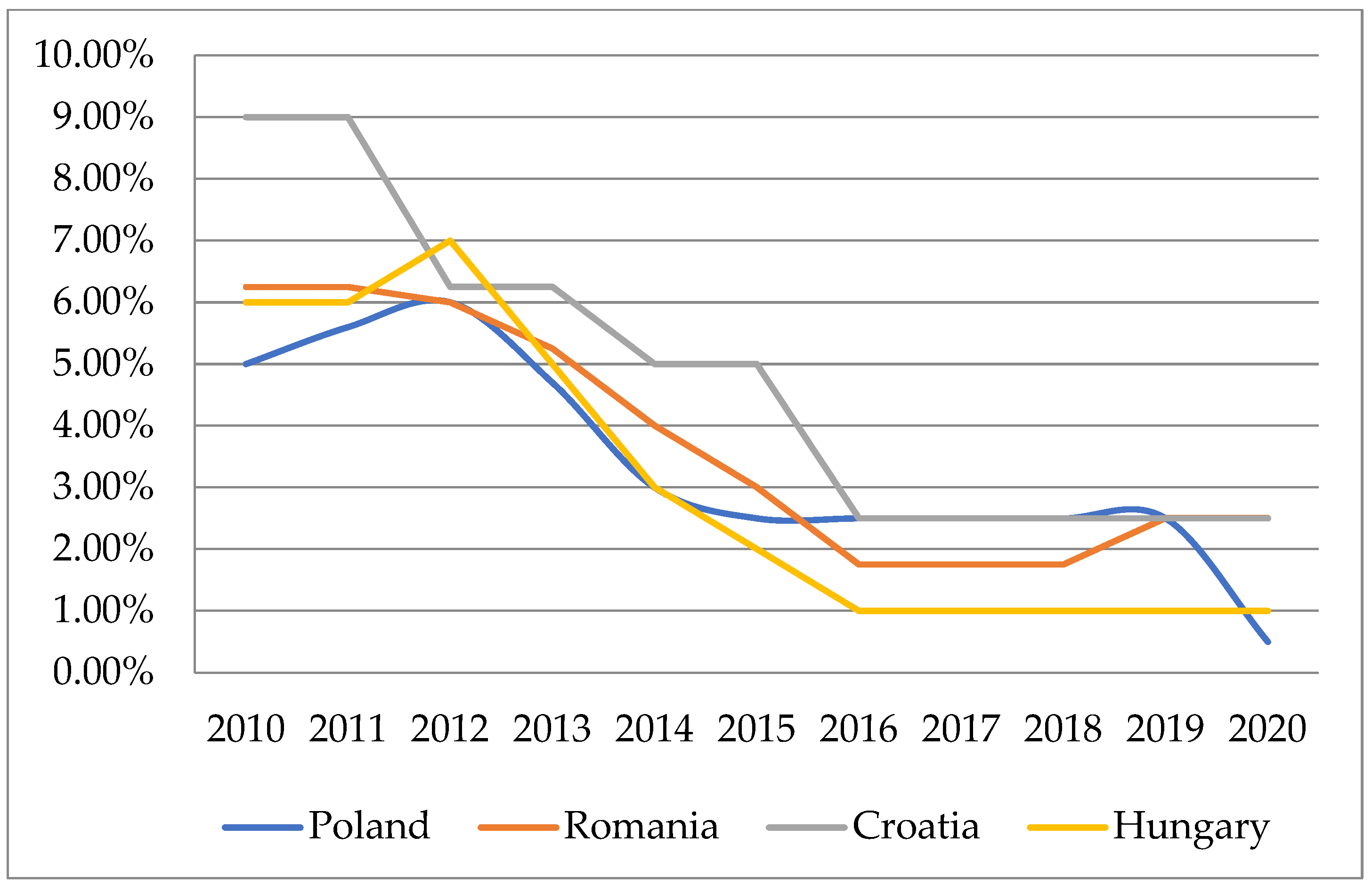

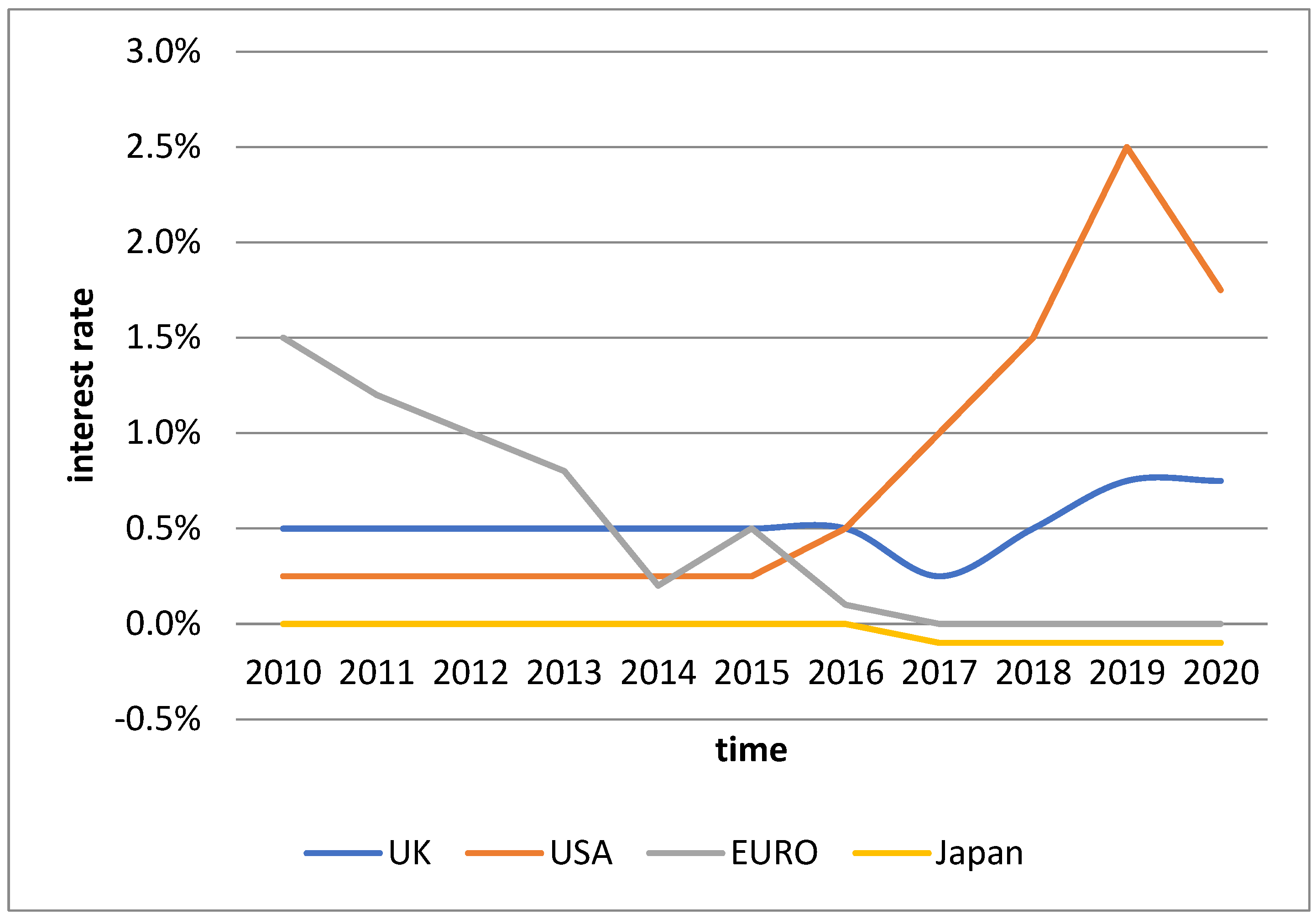

4.1. Current NPV as a Financial Metric and Interest Rates

4.2. Towards a Modified NPV as a Financial Metric

5. Conclusions

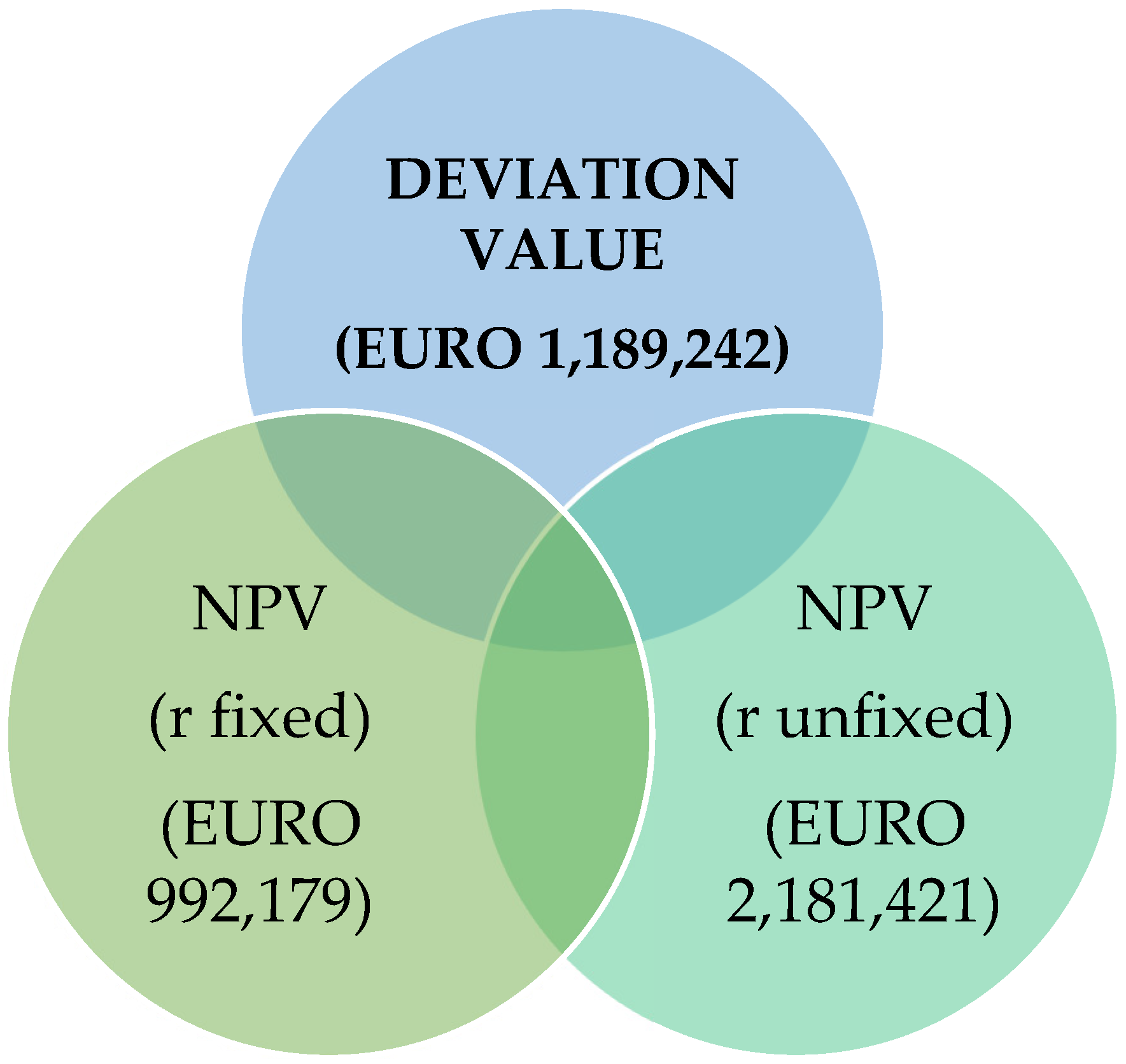

- When deciding to carry out a given investment based on the traditional NPV model, which assumes a fixed interest rate, the investor is exposed to the lack of credibility of the calculations obtained; usage of the traditional NPV model creates a possibility of rejecting investment projects that may become profitable in the case of favourable changes in the price of money in later periods. Such a situation may lead to loss of future profit or even to the reduction of future market position.

- There is a risk of choosing a wrong project, which may lead to the company’s bankruptcy.

- Frequent changes of interest rates shaped by monetary institutions make it difficult to estimate their level in the medium and long term, which significantly reduces the financial rationality of investments; investors’ financial problems may be exacerbated by the negative interaction between interest rates and the level of cash flows. Realising the method of expressing the difference between the current cash inflows and their current outflows will allow for a better assessment of the investment effectiveness in the event of the volatility of interest rates.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Al-Mulali, U. GDP growth—Energy consumption relationship: Revisited. Int. J. Energy Sect. Manag. 2014, 8, 356–379. [Google Scholar] [CrossRef]

- Simionescu, M.; Bilan, Y.; Krajňáková, E.; Streimikiene, D.; Gȩdek, S. Renewable energy in the electricity sector and GDP per capita in the European Union. Energies 2019, 12, 2520. [Google Scholar] [CrossRef] [Green Version]

- Hannesson, R. Energy and GDP growth. Int. J. Energy Sect. Manag. 2009, 3, 157–170. [Google Scholar] [CrossRef]

- Dobrowolski, Z. Internet of Things and Other E-Solutions in Supply Chain Management May Generate Threats in the Energy Sector—The Quest for Preventive Measures. Energies 2021, 14, 5381. [Google Scholar] [CrossRef]

- Dobrowolski, Z. Energy and Local Safety: How the Administration Limits Energy Security. Energies 2021, 14, 4841. [Google Scholar] [CrossRef]

- Najwyższa Izba Kontroli. Lokalne Bezpieczeństwo Energetyczne. Warszawa. 2020. Available online: https://www.nik.gov.pl/kontrole/P/19/014/ (accessed on 17 May 2021).

- Berkovitch, E.; Israel, R. Why the NPV Criterion does not Maximize NPV. Rev. Financ. Stud. 2004, 17, 239–255. [Google Scholar] [CrossRef]

- Antle, R.; Eppen, G.D. Capital Rationing and Organizational Slack in Capital Budgeting. Manag. Sci. 1985, 31, 163–174. [Google Scholar] [CrossRef]

- Harris, M.; Raviv, A. The Capital Budgeting Process, Incentives and Information. J. Financ. 1996, 51, 1139–1174. [Google Scholar] [CrossRef]

- Magni, C.A.; Marchioni, A. Average rates of return, working capital, and NPV-consistency in project appraisal: A sensitivity analysis approach. Int. J. Prod. Econ. 2020, 229, 107769. [Google Scholar] [CrossRef]

- Investopedia. Net Present Value (NPV). Available online: https://www.investopedia.com/terms/n/npv.asp (accessed on 23 March 2021).

- Goldenberg, J.; Libai, B.; Moldovan, S.; Muller, E. The NPV of bad news. Int. J. Res. Mark. 2007, 24, 186–200. [Google Scholar] [CrossRef]

- Shank, J.K. Analysing technology investments—From NPV to Strategic Cost Management (SCM). Manag. Account. Res. 1996, 7, 185–197. [Google Scholar] [CrossRef]

- Osborne, M.J. A resolution to the NPV–IRR debate? Q. Rev. Econ. Financ. 2010, 50, 234–239. [Google Scholar] [CrossRef]

- Stein, J.C. Internal Capital Markets and the Competition for Corporate Resources. J. Financ. 1997, 52, 111–133. [Google Scholar] [CrossRef]

- Gardiner, P.D.; Stewart, K. Revisiting the golden triangle of cost, time and quality: The role of NPV in project control, success and failure. Int. J. Proj. Manag. 2000, 18, 251–256. [Google Scholar] [CrossRef]

- Ramezanalizadeh, T.; Monjezi, M.; Sayadi, A.R.; Mousavi, A. Development of a MIP model to maximize NPV and minimize adverse environmental impact—A heuristic approach. Env. Monit. Assess. 2020, 192, 605. [Google Scholar] [CrossRef]

- Cigola, M.; Peccati, L. On the comparison between the APV and the NPV computer via the WACC. Eur. J. Oper. Res. 2005, 161, 377–385. [Google Scholar] [CrossRef]

- Chiang, Y.; Cheng, E.; Lam, P. Employing the Net Present Value-Consistent IRR Methods for PFI Contracts. J. Constr. Eng. Manag. 2010, 136, 811–814. [Google Scholar] [CrossRef]

- Hajdasinski, M.M. NPV-compatibility, project ranking, and related issues. Eng. Econ. 1997, 42, 325–339. [Google Scholar] [CrossRef]

- Hartman, J.C. On the equivalence of net present value and market value added as measures of a project’s economic worth. Eng. Econ. 2000, 45, 158–165. [Google Scholar] [CrossRef]

- Chrysafis, K.A.; Papadopoulos, B.K. Decision Making for Project Appraisal in Uncertain Environments: A Fuzzy-Possibilistic Approach of the Expanded NPV Method. Symmetry 2021, 13, 27. [Google Scholar] [CrossRef]

- Castagneto, G.; Zakeri, G.B.; Dodds, P.E.; Subkhankulova, D. Evaluating consumer investments in distributed energy technologies. Energy Policy 2021, 149, 112008. [Google Scholar] [CrossRef]

- Pfeiffer, T. Net Present Value-consistent investment criteria based on accruals: A generalisation of the residual income-identity. J. Bus. Financ. Account. 2004, 31, 905–926. [Google Scholar] [CrossRef]

- Quaranta, E.; Dorati, C.; Pistocchi, A. Water, energy and climate benefits of urban greening throughout Europe under different climatic scenarios. Sci. Rep. 2021, 11, 12163. [Google Scholar] [CrossRef]

- Wyrobek, J.; Popławski, Ł.; Dzikuć, M. Analysis of Financial Problems of Wind Farms in Poland. Energies 2021, 14, 1239. [Google Scholar] [CrossRef]

- Mukhtar, M.; Ameyaw, B.; Yimen, N.; Zhang, Q.; Bamisile, O.; Adun, H.; Dagbasi, M. Building Retrofit and Energy Conservation/Efficiency Review: A Techno-Environ-Economic Assessment of Heat Pump System Retrofit in Housing Stock. Sustainability 2021, 13, 983. [Google Scholar] [CrossRef]

- Pike, R.H.; Ooi, T.S. The impact of corporate investment objectives and constraints on capital budgeting practices. Br. Account. Rev. 1988, 20, 159–173. [Google Scholar] [CrossRef]

- Evans, D.A.; Forbes, S.M. Decision making and display methods: The case of prescription and practice in capital budgeting. Eng. Econ. 1993, 39, 87–92. [Google Scholar] [CrossRef]

- Graham, J.R.; Harvey, C.R. The theory and practice of corporate finance: Evidence from the field. J. Financ. Econ. 2001, 60, 187–243. [Google Scholar] [CrossRef]

- Lindblom, T.; Sjögren, S. Increasing goal congruence in project evaluation by introducing a strict market depreciation schedule. Int. J. Prod. Econ. 2009, 121, 519–532. [Google Scholar] [CrossRef]

- Sandahl, G.; Sjögren, S. Capital budgeting methods among Sweden’s largest groups of companies. The state of the art and a comparison with earlier studies. Int. J. Prod. Econ. 2003, 84, 51–69. [Google Scholar] [CrossRef]

- Pasqual, J.; Padilla, E.; Jadotte, E. Technical note: Equivalence of different profitability criteria with the net present value. Int. J. Prod. Econ. 2013, 142, 205–210. [Google Scholar] [CrossRef]

- Percoco, M.; Borgonovo, E. A note on the sensitivity analysis of the internal rate of return. Int. J. Prod. Econ. 2012, 135, 526–529. [Google Scholar] [CrossRef]

- Borgonovo, E.; Peccati, L. Sensitivity analysis in investment project evaluation. Int. J. Prod. Econ. 2004, 90, 17–25. [Google Scholar] [CrossRef]

- Borgonovo, E.; Peccati, L. Uncertainty and global sensitivity analysis in the evaluation of investment projects. Int. J. Prod. Econ. 2006, 104, 62–73. [Google Scholar] [CrossRef]

- Magni, C.A. Average Internal Rate of Return and investment decisions: A new perspective. Eng. Econ. 2010, 55, 150–180. [Google Scholar] [CrossRef]

- Marchioni, A.; Magni, C. AInvestment decisions and sensitivity analysis: NPV consistency of rates of return. Eur. J. Oper. Res. 2018, 268, 361–372. [Google Scholar] [CrossRef] [Green Version]

- Li, X. Diversification and localization of energy systems for sustainable development and energy security. Energy Policy 2005, 33, 2237–2243. [Google Scholar] [CrossRef]

- Sovacool, B.K.; Mukherjee, I. Conceptualizing and measuring energy security: A synthesized approach. Energy 2011, 36, 5343–5355. [Google Scholar] [CrossRef]

- Hossain, Y.; Loring, P.A.; Marsik, T. Defining energy security in the rural North—Historical and contemporary perspectives from Alaska. Energy Res. Soc. Sci. 2016, 16, 89–97. [Google Scholar] [CrossRef] [Green Version]

- Sovacool, B.K.; Brown, M.A. Competing dimensions of energy security: An international perspective. Annu. Rev. Environ. Resour. 2010, 35, 77–108. [Google Scholar] [CrossRef] [Green Version]

- Kruyt, B.; van Vuuren, D.P.; de Vries, H.J.M.; Groenenberg, H. Indicators for energy security. Energy Policy 2009, 37, 2166–2181. [Google Scholar] [CrossRef]

- Yergin, D. Ensuring Energy Security. Foreign Aff. 2006, 85, 69–82. [Google Scholar] [CrossRef]

- Unruh, G.C. Understanding carbon lock-in. Energy Policy 2000, 28, 817–830. [Google Scholar] [CrossRef]

- Bottomly, J.M. Energy assistance programs: Keeping older adults housed and warm. Top. Geriatr. Rehabil. 2001, 17, 71–81. [Google Scholar] [CrossRef]

- Kuik, O.J.; Lima, M.B.; Gupta, J. Energy security in a developing world. Wiley Interdiscip. Rev. 2011, 2, 627–634. [Google Scholar] [CrossRef] [Green Version]

- Simpson, A. The environment–Energy security nexus: Critical analysis of an energy ‘love triangle’ in Southeast Asia. Third World Q. 2007, 28, 539–554. [Google Scholar] [CrossRef]

- Muller-Kraenner, S. Energy Security, 1st ed.; Routledge: London, UK, 2007. [Google Scholar]

- Vukadinovic, R.D. Directive 2005/89/EC of the European Parliament and of the Council of 18 January 2006 concerning measures to safeguard security supply and infrastructure investment. Rev. Eur. L. 2007, 9, 109. [Google Scholar]

- Dobrowolski, Z.; Sułkowski, Ł. Business Model Canvas and Energy Enterprises. Energies 2021, 14, 7198. [Google Scholar] [CrossRef]

- Harris, J.M. Sustainability and Sustainable Development, Internet Encyclopaedia of Ecological Economics, International Society for Ecological Economics. 2003. Available online: https://www.researchgate.net/publication/237398200_Sustainability_and_Sustainable_Development (accessed on 16 October 2019).

- Boyer, R.H.; Peterson, N.D.; Arora, P.; Caldwell, K. Five approaches to social sustainability and an integrated way forward. Sustainability 2016, 8, 878. [Google Scholar] [CrossRef] [Green Version]

- Chohaney, M.L.; Yeager, C.D.; Gatrell, J.D.; Nemeth, D.J. Poverty, Sustainability, & Metal Recycling: Geovisualizing the Case of Scrapping as a Sustainable Urban Industry in Detroit. In Urban Sustainability: Policy and Praxis; Gatrell, J.D., Jensen, R.R., Patterson, M.W., Hoalst-Pullen, N., Eds.; Springer International Publishing: Cham, Switzerland, 2016; pp. 99–133. [Google Scholar]

- Herremans, I.M.; Nazari, J.A.; Mahmoudian, F. Stakeholder relationships, engagement, and sustainability reporting. J. Bus. Ethics 2016, 138, 417–435. [Google Scholar] [CrossRef]

- Basic NBP Interest Rates in 1998–2020. NBP. Available online: https://www.nbp.pl (accessed on 23 February 2021).

- Monetary Policy and Standing Facilities Interest Rates. BNR. Available online: https://www.bnro.ro (accessed on 6 February 2021).

- Monetary Policy Implementation. HNB. Available online: https://www.hnb.hr (accessed on 3 February 2021).

- Monetary Policy. MNB. Available online: http://www.mnb.hu (accessed on 9 March 2021).

- Interest Rates and Bank Rate. Bank of England. Available online: https://www.bankofengland.co.uk (accessed on 4 March 2021).

- Monetary Policy. Bank of Japan. Available online: www.boj.or.jp (accessed on 12 March 2021).

- Monetary Policy. FOMC. Available online: www.federalreserve.gov (accessed on 10 March 2021).

- Monetary Policy. Bank of Israel. Available online: www.boi.org.il (accessed on 6 February 2021).

- Euro Area Interest Rate. 2021. Available online: www.tradingeconomics.com/euro-area/interest-rate (accessed on 11 August 2021).

- Nordqvist, M.; Gartner, W.B. Literature, fiction, and the family business. Fam. Bus. Rev. 2020, 33, 122–129. [Google Scholar] [CrossRef]

- Short, J.C.; Payne, G.T. In Their Own Words: A Call for Increased Use of Organizational Narratives in Family Business Research. Fam. Bus. Rev. 2020, 33, 342–350. [Google Scholar] [CrossRef]

- Kuhn, T. The Structure of Scientific Revolutions; 50th Anniversary Edition; The University of Chicago Press: Chicago, IL, USA, 2012. [Google Scholar]

- Burrell, G.; Morgan, G. Sociological Paradigms and Organisational Analysis. Elements of the Sociology of Corporate Life; Routledge: London, UK, 2017. [Google Scholar]

- Babbie, E. The Practice of Social Research, 15th ed.; Cengage: Boston, MA, USA, 2021. [Google Scholar]

- Campbell, D.T.; Fiske, D.W. Convergent and Discriminant Validation by the Multitrait-Multimethod Matrix. Psychol. Bull. 1959, 56, 81–105. [Google Scholar] [CrossRef] [Green Version]

- Webb, E.J.; Campbell, D.T.; Schwartz, R.D.; Sechrest, L. Unobtrustive Maeasures. Revised Edition; Sage Publications: Thousand Oaks, CA, USA, 2000. [Google Scholar]

- Greene, J.C.; Caracelli, V.J.; Graham, W.F. Toward a Conceptual Framework for Mixed Evaluation Design. Educ. Eval. Policy Anal. 1989, 11, 255–274. [Google Scholar] [CrossRef]

- Brealey, R.; Myers, S. Principles of Corporate Finance, 13th ed.; McGraw-Hill Education: New York, NY, USA, 2020. [Google Scholar]

- Cogley, T. A Simple Adaptive Measure of Core Inflation. J. Money Credit Bank 2002, 34, 94–113. [Google Scholar] [CrossRef]

- Marques, C.R.; Neves, P.D.; Sarmento, L.M. Evaluating Core Inflation Indicators. Econ. Model. 2003, 20, 765–775. [Google Scholar] [CrossRef] [Green Version]

- O’Brien, R.M. A caution regarding rules of thumb for variance inflation factors. Qual. Quant. 2007, 41, 673–690. [Google Scholar] [CrossRef]

- Datta, T.K.; Pal, A.K. Effects of inflation and time-value of money on an inventory model with linear time-dependent demand rate and shortages. Eur. J. Oper. Res. 1991, 52, 326–333. [Google Scholar] [CrossRef]

- Leclerc, F.; Schmitt, B.H.; Dubé, L. Waiting Time and Decision Making: Is Time like Money? J. Consum. Res. 1995, 22, 110–119. [Google Scholar] [CrossRef]

- Selten, R. Bounded Rationality. J. Inst. Theor. Econ. 1990, 146, 649–658. [Google Scholar]

- Jones, B.D. Bounded Rationality. Annu. Rev. Political Sci. 1999, 2, 297–321. [Google Scholar] [CrossRef]

- Simon, H.A. Bounded rationality in social science: Today and tomorrow. Mind Soc. 2000, 1, 25–39. [Google Scholar] [CrossRef]

- Myers, S.C. Capital structure. J. Econ. Perspect. 2001, 15, 81–102. [Google Scholar] [CrossRef] [Green Version]

- Harris, M.; Raviv, A. The Theory of Capital Structure. J. Financ. 1991, 46, 297–355. [Google Scholar] [CrossRef]

- Baker, M.; Wurgler, M.J. Market Timing and Capital Structure. J. Financ. 2020, 57, 1–32. [Google Scholar] [CrossRef]

- Titman, S.; Wessels, R. The Determinants of Capital Structure Choice. J. Financ. 1988, 43, 1–19. [Google Scholar] [CrossRef]

- Faulkender, M.; Petersen, M.A. Does the Source of Capital Affect Capital Structure? Rev. Financ. Stud. 2006, 19, 45–79. [Google Scholar] [CrossRef] [Green Version]

- Scott, J.H., Jr. A Theory of Optimal Capital Structure. Bell J. Econ. 1976, 7, 33–54. [Google Scholar] [CrossRef]

- Rayan, K. Financial leverage and firm value. University of Pretoria, The South Africa. 2008. Available online: https://repository.up.ac.za/bitstream/handle/2263/23237/dissertation.pdf?sequence=1 (accessed on 6 February 2021).

- Campbell, T.C.; Galpin, N.; Johnson, S.A. Optimal inside debt compensation and the value of equity and debt. J. Financ. Econ. 2016, 119, 336–352. [Google Scholar] [CrossRef]

- Hill, C.W.L.; Jones, G.R. Strategic Management Theory: An Integrated Approach; Cengage: Boston, MA, USA, 2015. [Google Scholar]

- Fleisher, C.S.; Bensoussan, B. Strategic and Competitive Analysis: Methods and Techniques for Analyzing Business Competition; Prentice-Hall: New York, NY, USA, 2003. [Google Scholar]

- Lind, D.A.; Marchal, W.G.; Mason, R.D. Statistical Techniques in Business and Economics, 17th ed.; McGraw-Hill: New York, NY, USA, 2018. [Google Scholar]

- Carstensen, K.; Toubal, F. Foreign direct investment in Central and Eastern European countries: A dynamic panel analysis. J. Comp. Econ. 2004, 3, 3–22. [Google Scholar] [CrossRef] [Green Version]

- Bevan, A.A.; Estrin, S. The determinants of foreign direct investment into European transition economies. J. Comp. Econ. 2004, 32, 775–787. [Google Scholar] [CrossRef]

- Janicki, H.P.; Wunnava, P.V. Determinants of foreign direct investment: Empirical evidence from EU accession candidates. Appl. Econ. 2004, 36, 505–509. [Google Scholar] [CrossRef]

- Égert, B.; Crespo-Cuaresma, J.; Reininger, T. Interest rate pass-through in central and Eastern Europe: Reborn from ashes merely to pass away? J. Policy Model. 2007, 29, 209–225. [Google Scholar] [CrossRef] [Green Version]

- Agapova, A.; McNulty, J.E. Interest rate spreads and banking system efficiency: General considerations with an application to the transition economies of Central and Eastern Europe. Int. Rev. Financ. Anal. 2016, 47, 154–165. [Google Scholar] [CrossRef]

- Niţoi, M.; Spulbar, C. An Examination of Banks’ Cost Efficiency in Central and Eastern Europe. Procedia Econ. Financ. 2015, 22, 544–551. [Google Scholar] [CrossRef] [Green Version]

- Moagăr-Poladian, S.; Clichici, D.; Stanciu, C.-V. The Comovement of Exchange Rates and Stock Markets in Central and Eastern Europe. Sustainability 2019, 11, 3985. [Google Scholar] [CrossRef] [Green Version]

- Kiani, K.M. Federal budget deficits and long-term interest rates in USA. Q. Rev. Econ. Financ. 2009, 49, 74–84. [Google Scholar] [CrossRef]

- Peiró, A. Stock prices, production and interest rates: Comparison of three European countries with the USA. Empir. Econ. 1996, 21, 221–234. [Google Scholar] [CrossRef]

- Panagopoulos, Y.; Reziti, I.; Spiliotis, A. Monetary and banking policy transmission through interest rates: An empirical application to the USA, Canada, the UK and the Eurozone. Int. Rev. Appl. Econ. 2010, 24, 119–136. [Google Scholar] [CrossRef]

- Yazgan, M.E.; Yilmazkuday, H. Monetary policy rules in practice: Evidence from Turkey and Israel. Appl. Financ. Econ. 2007, 17, 1–8. [Google Scholar] [CrossRef]

- Ólan, T.H. Regime switching in the relationship between equity returns and short-term interest rates in the UK. J. Bank. Financ. 2009, 33, 405–414. [Google Scholar]

- Apergis, N.; Cooray, A. Asymmetric interest rate pass-through in the U.S., the U.K. and Australia: New evidence from selected individual banks. J. Macroecon. 2015, 45, 155–172. [Google Scholar] [CrossRef]

- Dunning, J.H. The investment development cycle revisited. Weltwirtschaftliches Arch. 1986, 122, 667–676. [Google Scholar] [CrossRef]

- Culp, C.L. The Risk Management Process. Business Strategy and Tactics; John Wiley & Sons: Hoboken, NJ, USA, 2001. [Google Scholar]

- Aven, T.; Renn, O. Risk Management and Risk Governance. Concepts, Guidelines and Applications; Springer: Berlin/Heidelberg, Germany, 2010. [Google Scholar]

- Hoyt, R.E.; Liebenberg, A.P. The Value of Enterprise Risk Management. J. Risk Insur. 2011, 78, 795–822. [Google Scholar] [CrossRef]

- Dickinson, G. Enterprise Risk Management: Its Origins and Conceptual Foundation. Geneva Pap. Risk Insur. Issues Pract. 2001, 26, 360–366. [Google Scholar] [CrossRef]

- Froot, K.A.; Scharfstein, D.S.; Stein, J.C. Risk Management: Coordinating Corporate Investment and Financing Policies. J. Financ. 1993, 48, 1629–1658. [Google Scholar] [CrossRef] [Green Version]

- Baker, H.K.; Filberg, G. Investment Risk Management; Oxford University Press: Oxford, UK; New York, NY, USA, 2015. [Google Scholar]

- Tupa, J.; Simota, J.; Steiner, F. Aspects of risk management implementation for Industry 4.0. Procedia Manuf. 2017, 11, 1223–1230. [Google Scholar] [CrossRef]

- Shirley, R.; Kammen, D. Renewable energy sector development in the Caribbean: Current trends and lessons from history. Energy Policy 2013, 57, 244–252. [Google Scholar] [CrossRef]

- Papież, M.; Śmiech, S.; Frodyma, K. Effects of renewable energy sector development on electricity consumption–Growth nexus in the European Union. Renew. Sustain. Energy Rev. 2019, 113, 109276. [Google Scholar] [CrossRef]

- Pakulska, T. Green Energy in Central and Eastern European (CEE) Countries: New Challenges on the Path to Sustainable Development. Energies 2021, 14, 884. [Google Scholar] [CrossRef]

- Kat, B.; Paltsev, S.; Yuan, M. Turkish energy sector development and the Paris Agreement goals: A CGE model assessment. Energy Policy 2018, 122, 84–96. [Google Scholar] [CrossRef] [Green Version]

- Su, W.; Zhang, D.; Zhang, C.; Streimikiene, D. Sustainability assessment of energy sector development in China and European Union. Sustain. Dev. 2020, 28, 1063–1076. [Google Scholar] [CrossRef]

- Amstalden, R.W.; Kost, M.; Nathani, C.; Imboden, D.M. Economic potential of energy-efficient retrofitting in the Swiss residential building sector: The effects of policy instruments and energy price expectations. Energy Policy 2007, 35, 1819–1829. [Google Scholar] [CrossRef]

- Dziekański, P.; Prus, P.; Maitah, M.; Wrońska, M. Assessment of Spatial Diversity of the Potential of the Natural Environment in the Context of Sustainable Development of Counties in Poland. Energies 2021, 14, 6027. [Google Scholar] [CrossRef]

- Drozdowski, G. Economic Calculus Qua an Instrument to Support Sustainable Development under Increasing Risk. J. Risk Financ. Manag. 2021, 14, 15. [Google Scholar] [CrossRef]

- Dobrowolski, Z.; Drozdowski, G.; Dobrowolska, M.; Sobon, J.; Sobon, D. Economic Calculus and Weak Signals: Prevention Against Foggy Bottom. Eur. Res. Stud. J. 2021, 14, 165–174. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Years | 1 | 2 | 3 | 4 | 5 | 6 | |

|---|---|---|---|---|---|---|---|

| Values | |||||||

| NCF | 2,565,500 | 4,378,300 | 6,254,630 | 6,547,300 | 6,525,720 | 5,973,420 | |

| Years | 1 | 2 | 3 | 4 | 5 | 6 | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Interests Rate | ||||||||||||

| interest rate (fixed) | 36% | 36% | 36% | 36% | 36% | 36% | ||||||

| unfixed interest rate | 36% | 34% | 31% | 27% | 27% | 28% | 30% | 26% | 23% | 23% | 21% | |

| number of days of interest rate validity | 150 | 210 | 197 | 163 | 256 | 104 | 167 | 193 | 360 | 62 | 298 | |

| Years | 1 | 2 | 3 | 4 | 5 | 6 | |

|---|---|---|---|---|---|---|---|

| PVIF | |||||||

| PVIF r—fixed | 0.74 | 0.54 | 0.39 | 0.29 | 0.22 | 0.16 | |

| PVIF r—variables | 0.72 | 0.55 | 0.43 | 0.33 | 0.27 | 0.22 | |

| Years | 1 | 2 | 3 | 4 | 5 | 6 | |

|---|---|---|---|---|---|---|---|

| PV | |||||||

| NCF | 2,565,500 | 4,378,300 | 6,254,630 | 6,547,300 | 6,525,720 | 5,973,420 | |

| PV(NCF) R—fixed | 1,898,470 | 2,364,282 | 2,439,305 | 1,898,717 | 1,435,658 | 955,747 | |

| PV(NCF) R—unfixed | 1,847,160 | 2,408,065 | 2,689,491 | 2,160,609 | 1,761,944 | 1,314,152 | |

| Deviation value | 51,310 | 43,783 | 250,186 | 261,892 | 326,286 | 358,405 | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Dobrowolski, Z.; Drozdowski, G. Does the Net Present Value as a Financial Metric Fit Investment in Green Energy Security? Energies 2022, 15, 353. https://doi.org/10.3390/en15010353

Dobrowolski Z, Drozdowski G. Does the Net Present Value as a Financial Metric Fit Investment in Green Energy Security? Energies. 2022; 15(1):353. https://doi.org/10.3390/en15010353

Chicago/Turabian StyleDobrowolski, Zbysław, and Grzegorz Drozdowski. 2022. "Does the Net Present Value as a Financial Metric Fit Investment in Green Energy Security?" Energies 15, no. 1: 353. https://doi.org/10.3390/en15010353

APA StyleDobrowolski, Z., & Drozdowski, G. (2022). Does the Net Present Value as a Financial Metric Fit Investment in Green Energy Security? Energies, 15(1), 353. https://doi.org/10.3390/en15010353