Assessing the Role of Carbon Capture and Storage in Mitigation Pathways of Developing Economies

Abstract

1. Introduction

2. Policy and Technology Landscape Related to Carbon Capture

2.1. The Current State of CCS Technologies Globally

2.2. Policies Related to CCS and Energy System Decarbonisation

2.3. The Role of CCS in Mitigation Pathways

3. Methodology

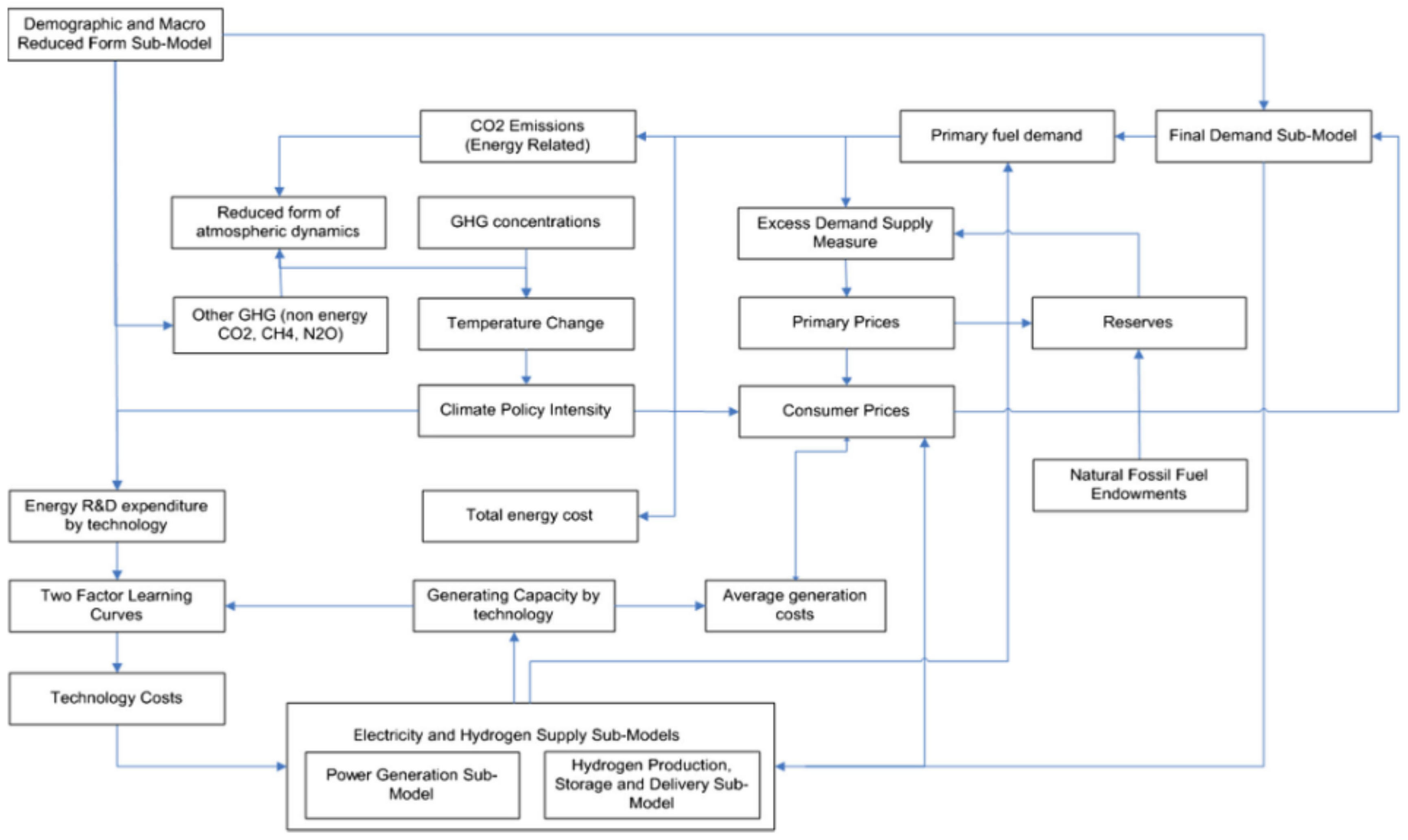

3.1. The PROMETHEUS Energy System Model

3.2. Study and Scenario Design

4. Scenario Results

4.1. Impacts on CO2 Emissions

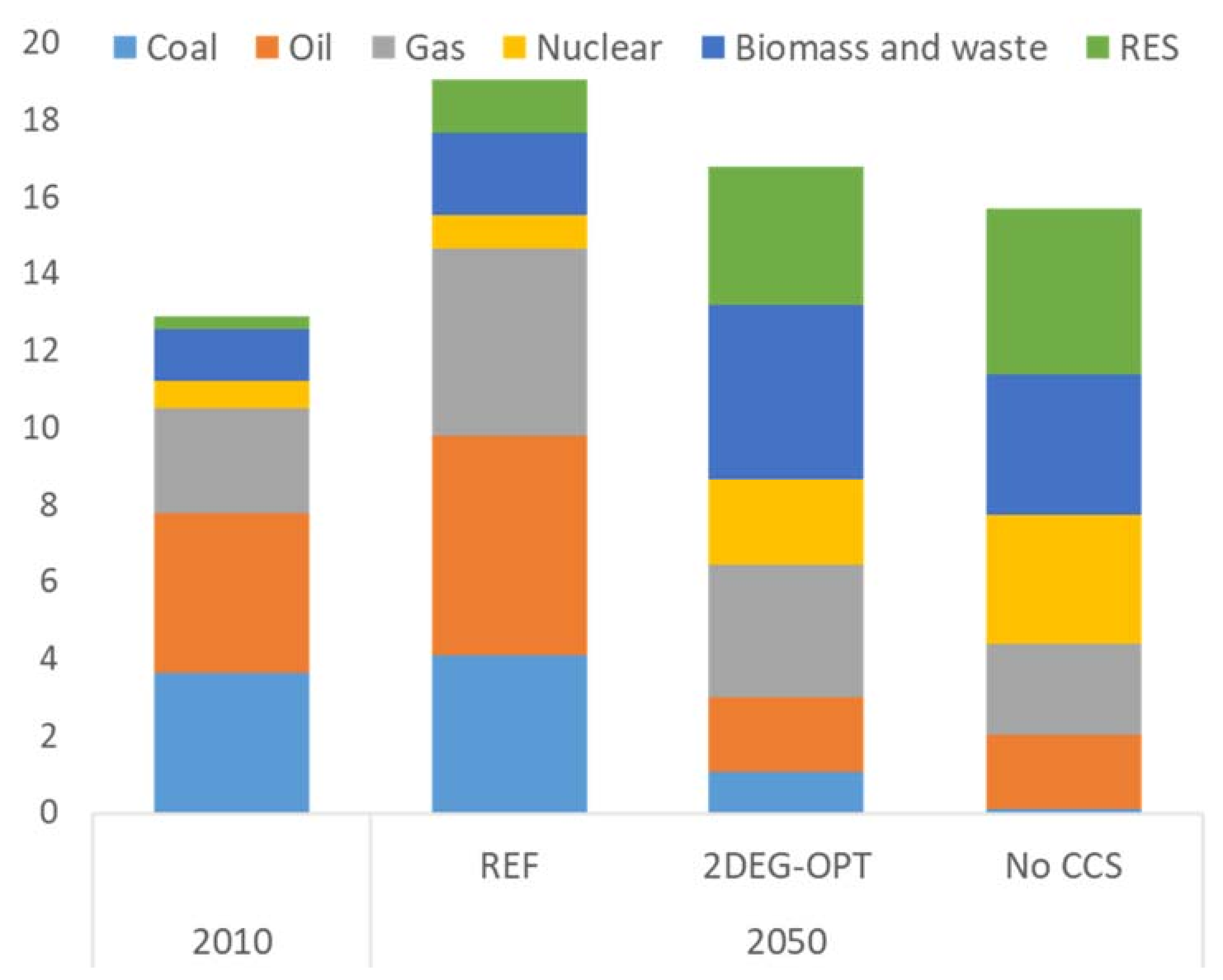

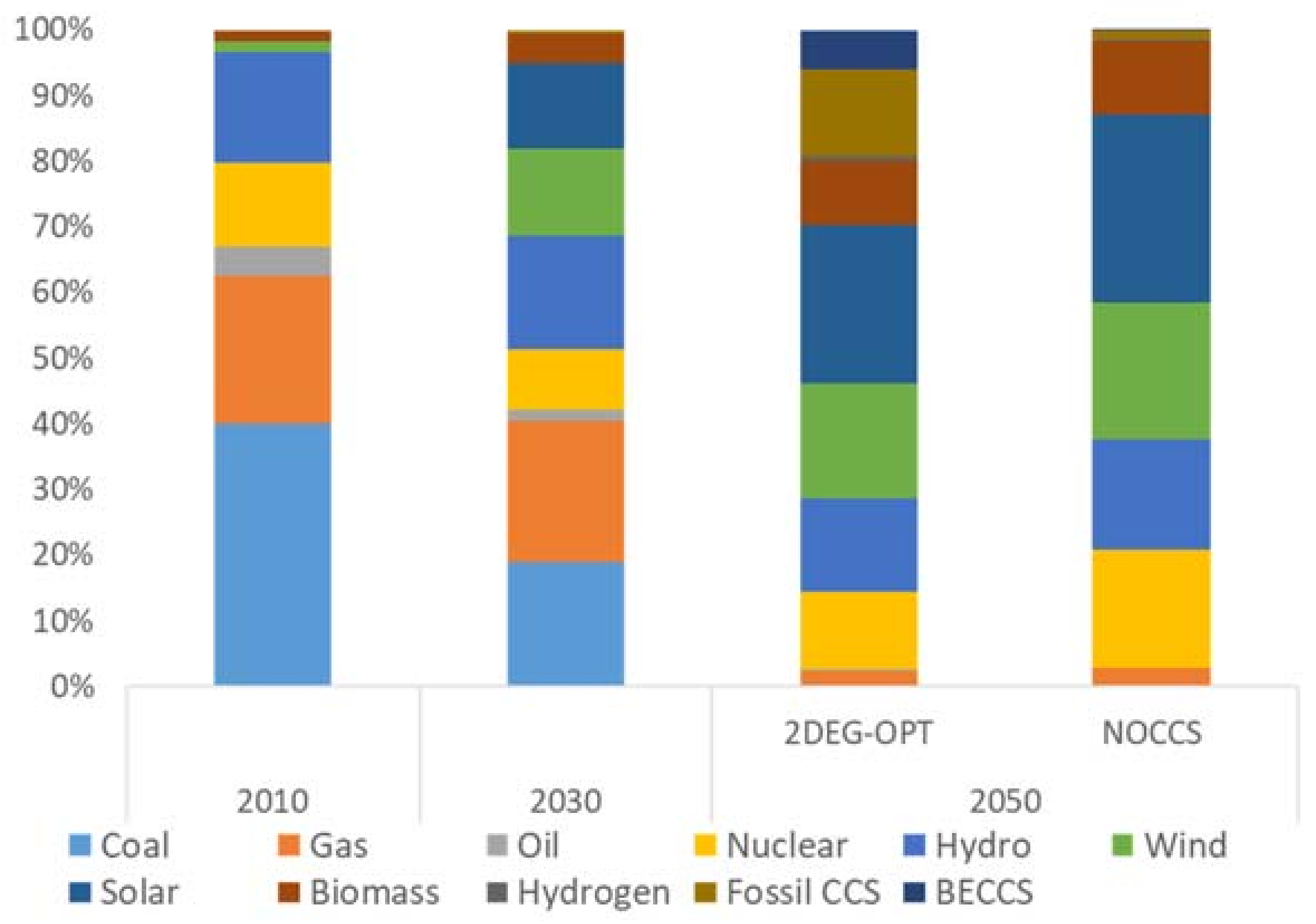

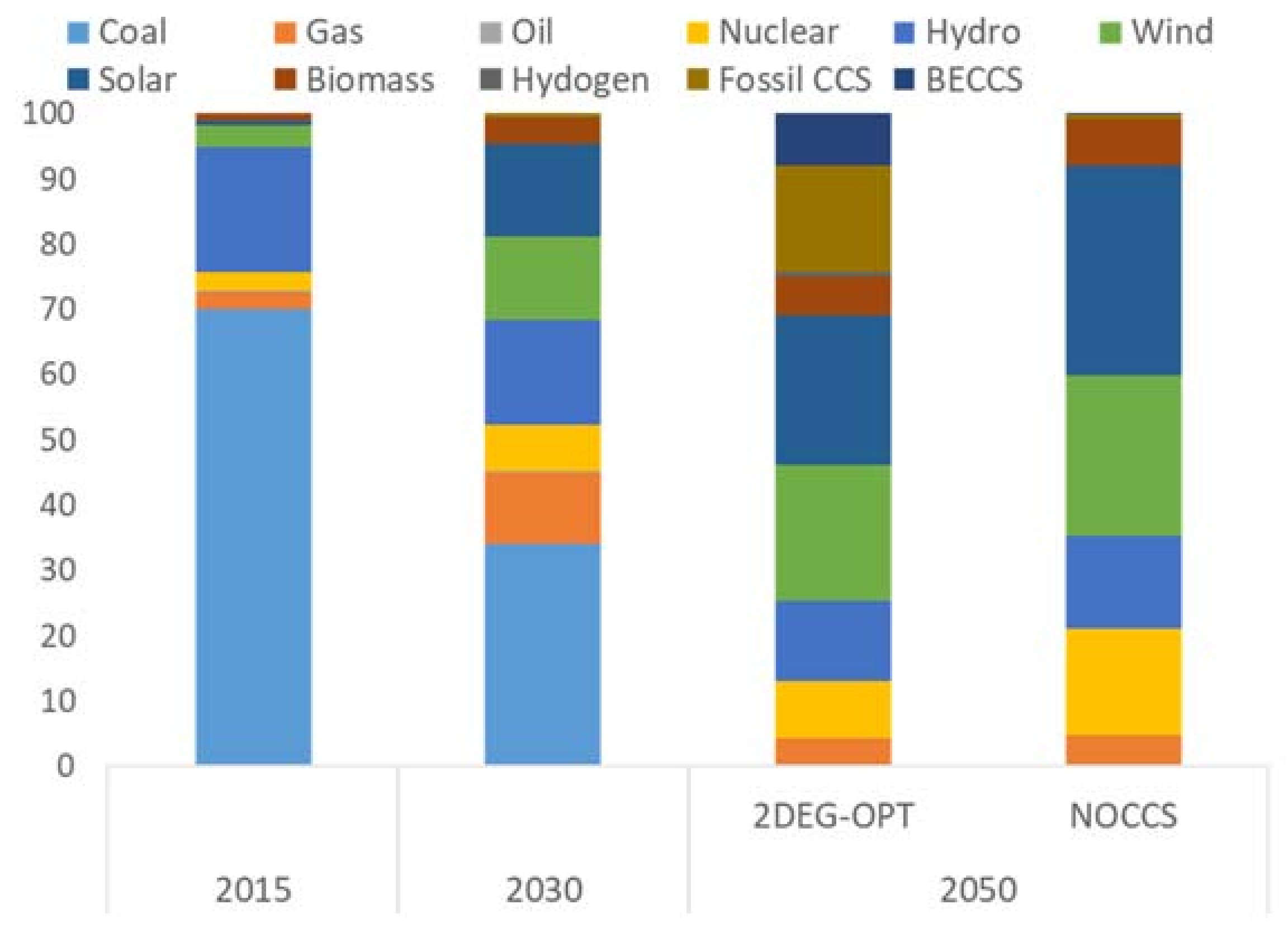

4.2. Impacts on Global Energy System Transformation

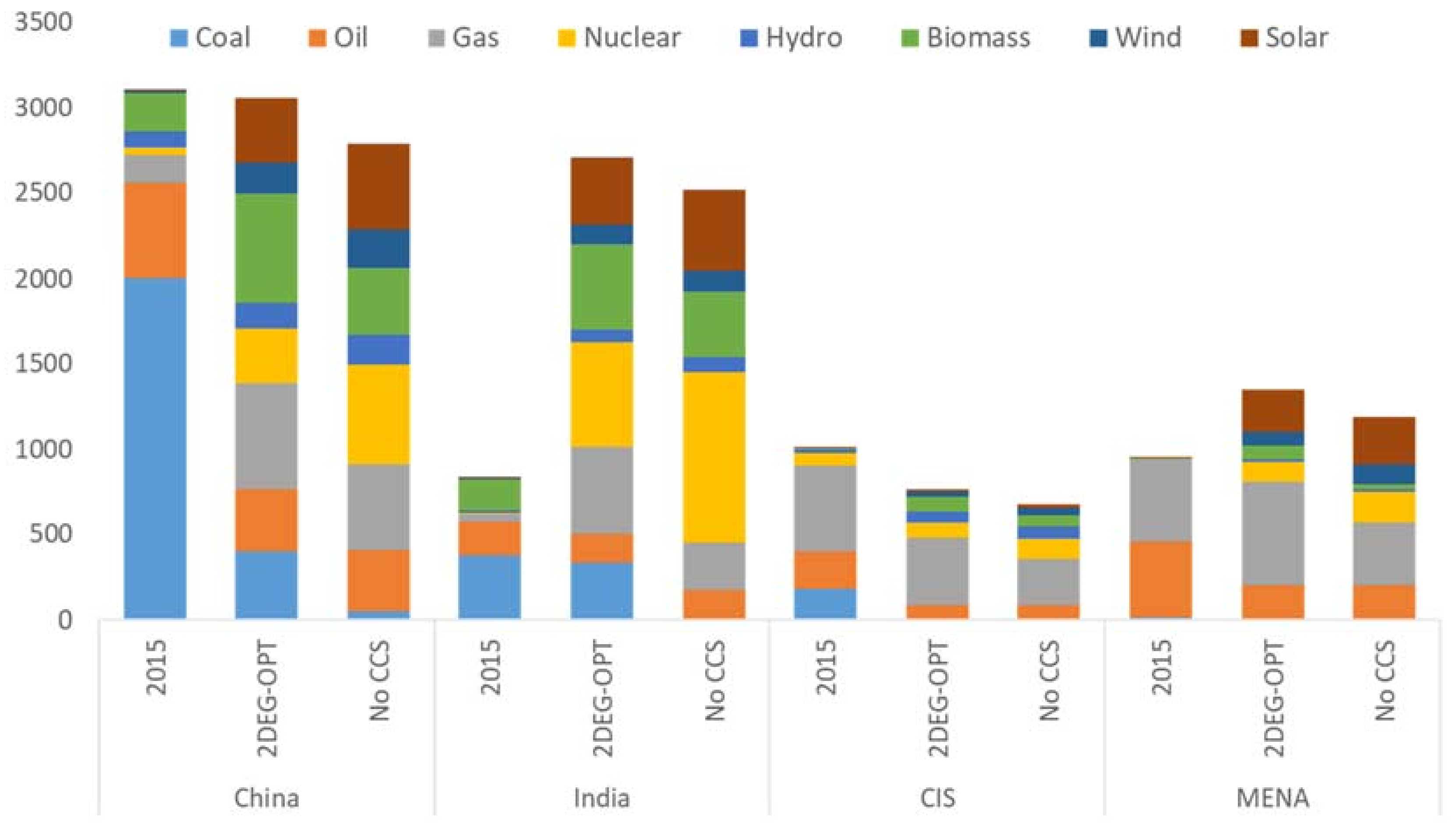

4.3. Impacts on Energy Systems of Developing Countries

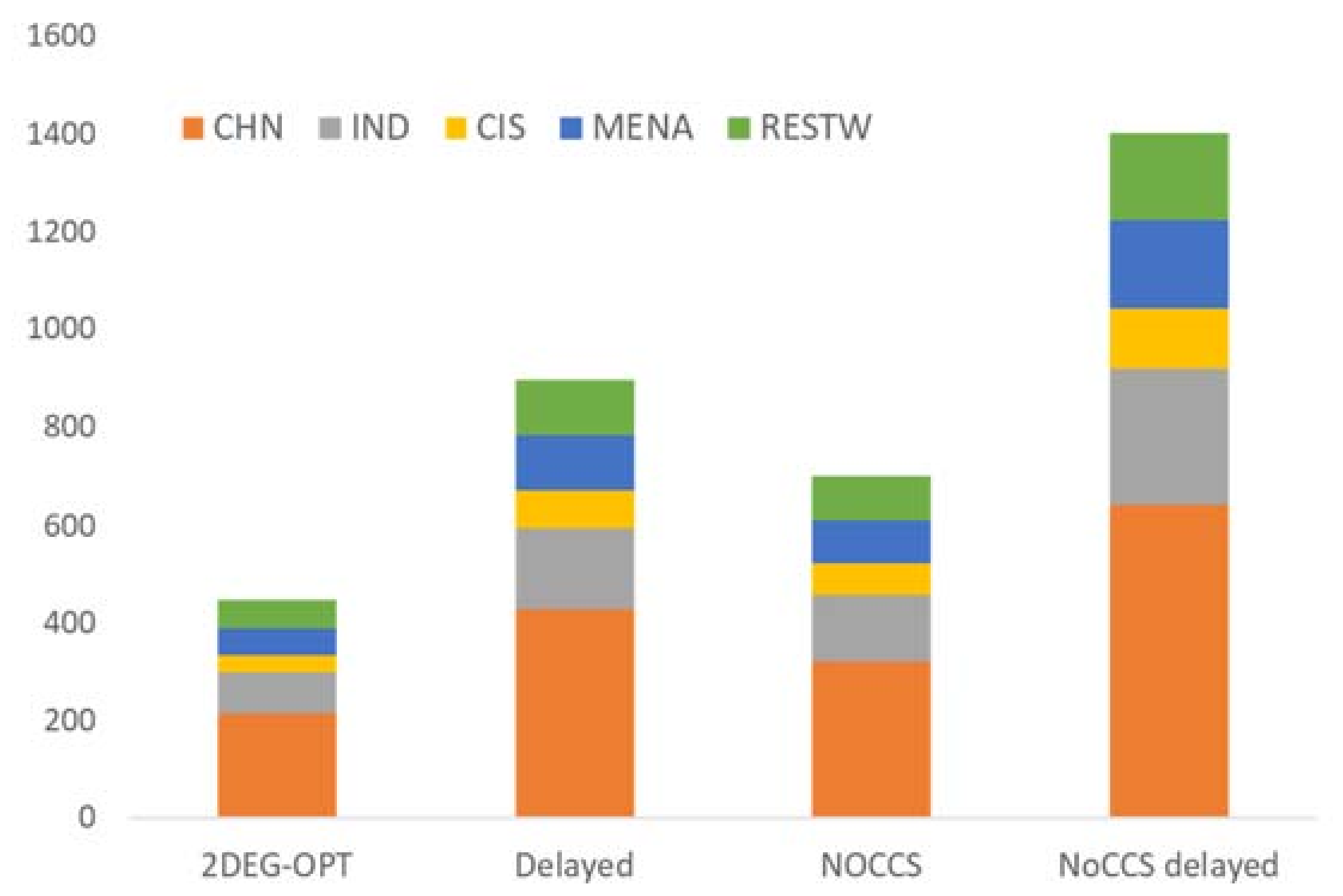

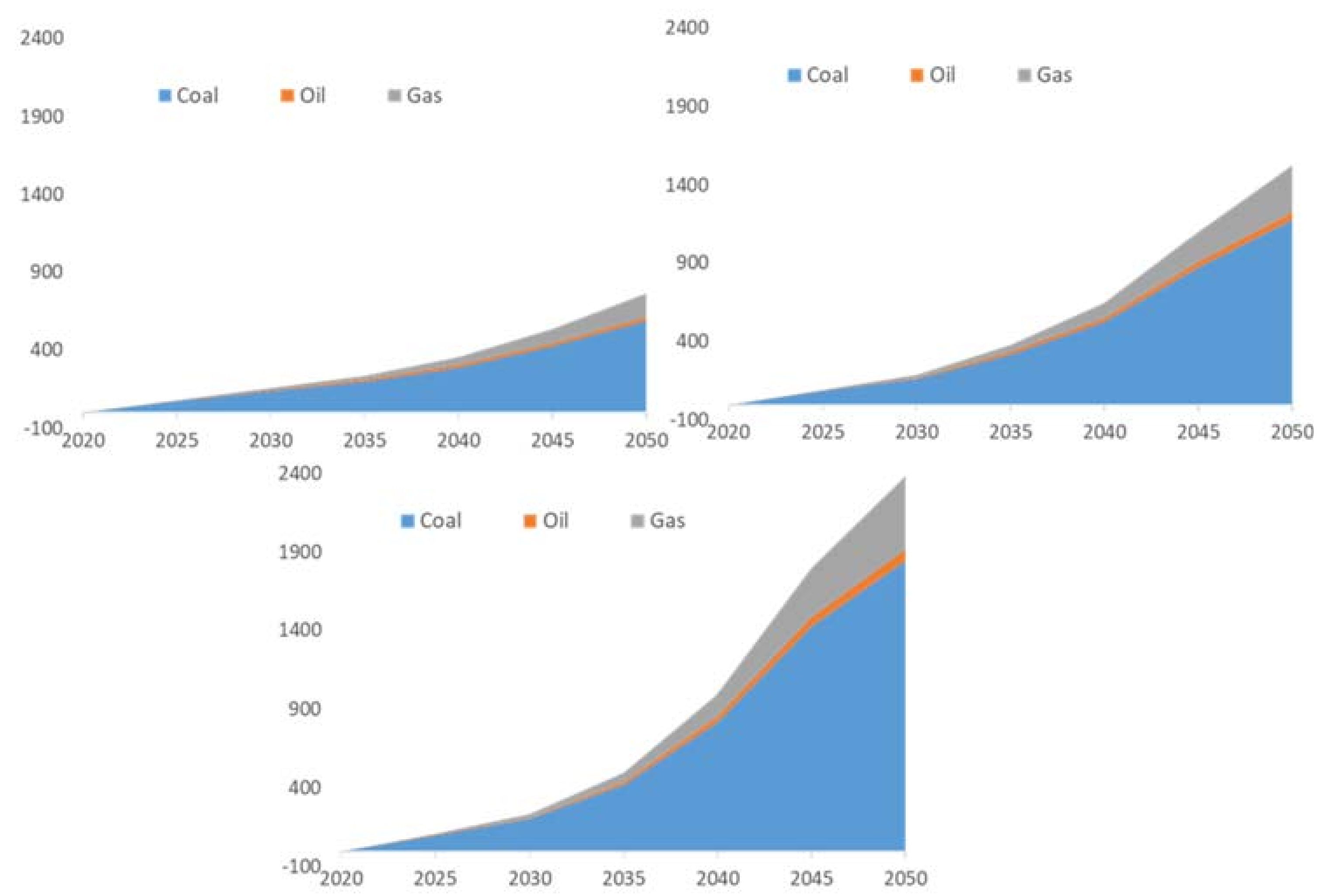

4.4. Impacts for Stranded Fossil Fuel Assets

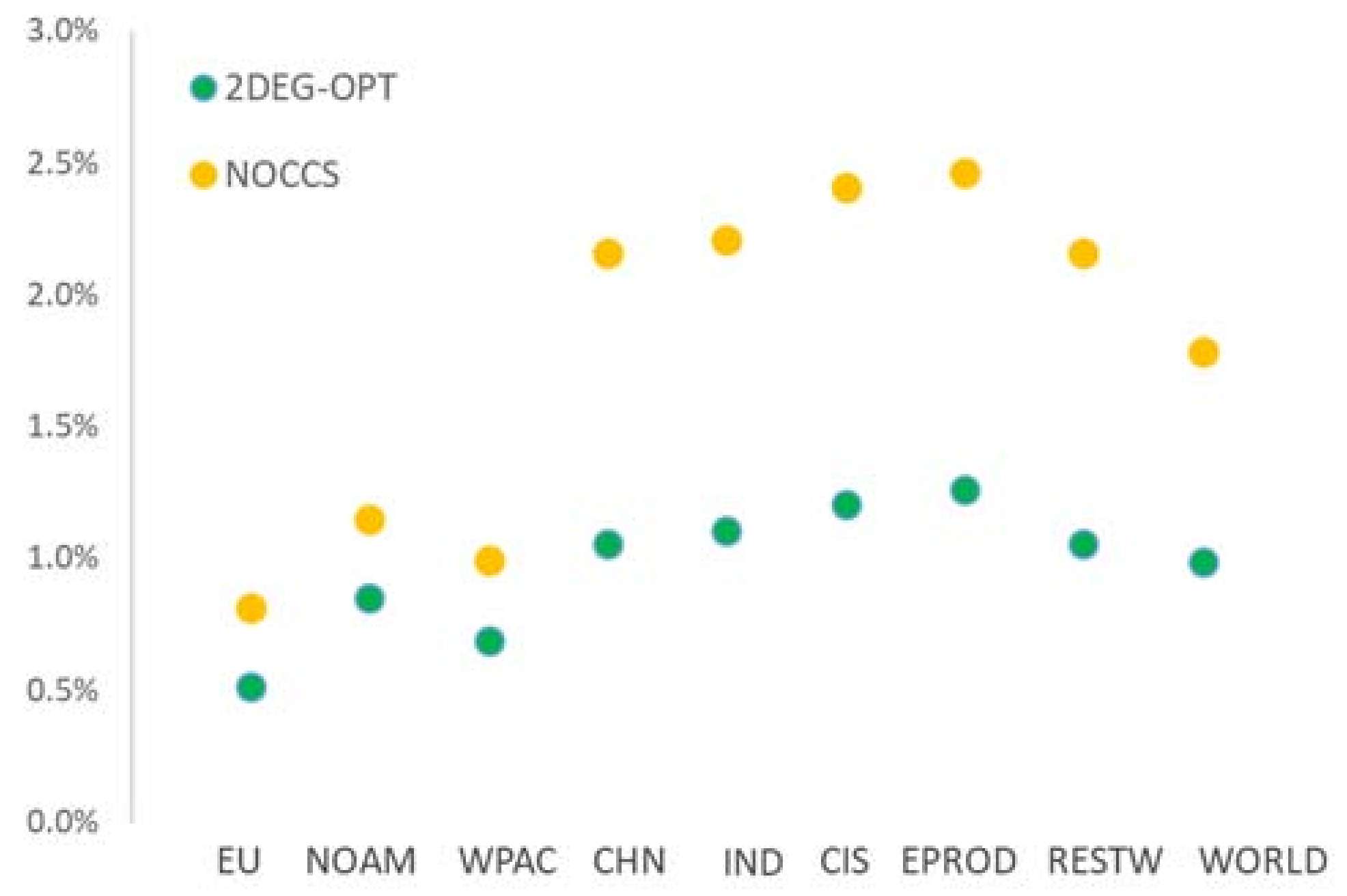

4.5. Impacts on Mitigation Costs

5. Policy Recommendations and Conclusions

- CCS can be an important technology towards achieving energy system decarbonisation, as it can minimise remaining emissions from power generation and industrial processes.

- Despite the challenges currently faced by CCS technologies, their market uptake can induce deep emission reduction and alleviate cost increases, especially in developing economies such as China, which can lead the deployment of CCS globally.

- The market uptake of CCS would reduce the risks for carbon lock-in and stranded assets, especially related to coal power plants.

- Climate policy delays and technology limitations for CCS would reduce the capability to achieve carbon neutrality by mid-century and increase energy system costs.

- New coal infrastructure without CCS would likely be inconsistent with the Paris goals.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Fragkos, P. Global Energy System Transformations to 1.5 °C: The Impact of Revised Intergovernmental Panel on Climate Change Carbon Budgets. Energy Technol. 2020, 8, 2000395. [Google Scholar] [CrossRef]

- European Commission. Communication from the Commission to the European Parliament, the European Council, the Council, the European Economic and Social Committee and the Committee of the Regions; COM(2019) 640 Final, The European Green Deal; European Commission: Brussels, Belgium, 2019. [Google Scholar]

- Fragkos, P.; Fragkiadakis, K.; Paroussos, L. Reducing the decarbonization cost burden for EU energy-intensive industries. Energies 2021, 14, 236. [Google Scholar] [CrossRef]

- Paroussos, L.; Mandel, A.; Fragkidakis, K.; Fragkos, P.; Hinkel, J.; Vrontisi, Z. Climate clubs and the macro-economic benefits of international cooperation on climate policy. Nat. Clim. Chang. 2019, 9, 542–546. [Google Scholar] [CrossRef]

- McCollum, D.L.; Zhou, W.; Bertram, C.; de Boer, H.; Bosetti, V.; Busch, S.; Després, J.; Drouet, L.; Emmerling, J.; Fay, M.; et al. Energy investment needs for fulfilling the Paris agreement and achieving the sustainable development goals. Nat. Energy 2018. [Google Scholar] [CrossRef]

- Fragkos, P. Energy System Transitions and Low-Emission Pathways in Australia, Brazil, Canada, China, EU-28, India, Indonesia, Japan, Republic of Korea, Russia, and United States. Energy 2021, 216, 119385. [Google Scholar] [CrossRef]

- Capros, P.; Paroussos, L.; Fragkos, P.; Tsani, S.; Boitier, B.; Wagner, F.; Busch, S.; Resch, G.; Blesl, M.; Bollen, J. European decarbonisation pathways under alternative technological and policy choices: A multi-model analysis. Energy Strategy Rev. 2014, 2, 231–245. [Google Scholar] [CrossRef]

- Marcucci, A.; Panos, E.; Kypreos, S.; Fragkos, P. Probabilistic assessment of realizing the 1.5 °C climate target. Appl. Energy Appl. Energy 2019, 239, 239–251. [Google Scholar] [CrossRef]

- Lund, H.; Mathiesen, B.V. Energy system analysis of 100% renewable energy systems-The 17 case of Denmark in years 2030 and 2050. Energy 2009, 34, 524–531. [Google Scholar] [CrossRef]

- Bogdanov, D.; Farfan, J.; Sadovskaia, K.; Aghahosseini, A.; Child, M.; Gulagi, A.; Solomon, A.; de Souza, L.; Barbosa, N.; Breyer, C. Radical transformation pathway towards sustainable electricity via evolutionary steps. Nat. Commun. 2019, 10, 1077. [Google Scholar] [CrossRef]

- De Coninck, H.; Benson, S.M. Carbon dioxide capture and storage: Issues and prospects. Annu. Rev. Environ. Resour. 2014, 39, 243–270. [Google Scholar] [CrossRef]

- Lovins, A.B.; Palazzi, T.; Laemel, R.; Goldfiled, E. Relative deployment rates of renewable and nuclear power: A cautionary tale of two metrics. Energy Res. Soc. Sci. 2018, 38, 188–192. [Google Scholar] [CrossRef]

- Rogelj, J.D.; Shindel, D.; Jang, K.; Fifita, S.; Forster, P.; Ginzburg, V.; Handa, K.; Khesghi, D.; Kobayashi, S.; Kriegler, E. Mitigation Pathways Compatible with 1.5 °C in the Context of Sustainable Development in Global Warming of 1.5 °C: An IPCC Special Report on the Impacts of Global Warming of 1.5 °C above Pre-Industrial Levels; IPCC: Geneva, Switzerland, 2018. [Google Scholar]

- IEA. World Energy Outlook 2019; International Energy Agency: Paris, France, 2019. [Google Scholar]

- European Commission. In-Depth Analysis in Support of the Commission Communication COM (2018) 773, A Clean Planet for All: A European Long-Term Strategic Vision for a Prosperous, Modern, Competitive and Climate Neutral Economy; European Commission: Brussels, Belgium, 2018. [Google Scholar]

- Global CCS Institute. Global Status of CCS 2019. Available online: https://www.globalccsinstitute.com/wp-content/uploads/2019/12/GCC_GLOBAL_STATUS_REPORT_2019.pdf (accessed on 10 January 2021).

- Hoppe, W.; Thonemann, N.; Bringezu, S. Life Cycle Assessment of Carbon Dioxide–Based Production of Methane and Methanol and Derived Polymers. J. Ind. Ecol. 2018, 22, 327–340. [Google Scholar] [CrossRef]

- Hepburn, C.; Adlen, E.; Beddington, J.; Carter, E.A.; Fuss, S.; Mac Dowel, N.; Minx, J.C.; Smith, P.; Williams, C.K. The technological and economic prospects for CO2 utilization and removal. Nature 2019, 575, 87–97. [Google Scholar] [CrossRef]

- Rosa, L.J.; Reimer, J.A.; Went, M.S.; D’Odorico, P. Hydrological limits to carbon capture and storage. Nat. Sustain. 2020, 3, 658–666. [Google Scholar] [CrossRef]

- Muratori, M.; Kheshgi, H.; Mignone, B.; Clarke, L.; McJeon, H.; Edmonds, J. Carbon capture and storage across fuels and sectors in energy system transformation pathways. Int. J. Greenh. Gas Control 2017, 57, 34–41. [Google Scholar] [CrossRef]

- Bui, M.; Adjiman, C.; Bardow, A.; Anthony, E.; Boston, A.; Brown, S.; Fennell, P.S.; Fuss, S.; Galindo, A.; Hackett, L. Carbon Capture and Storage (CCS): The way forward. Energy Environ. Sci. 2018, 11, 1062–1176. [Google Scholar] [CrossRef]

- Demski, C.; Spence, A.; Pidgeon, N. Effects of exemplar scenarios on public preferences for energy futures using the my2050 scenario-building tool. Nat. Energy 2017, 2, 1–7. [Google Scholar] [CrossRef]

- Fowlie, M. “Biden’s New Climate Plan” Energy Institute Blog, UC Berkeley. 3 August 2020. Available online: https://energyathaas.wordpress.com/2020/07/27/how-utility-customers-will-pay-for-the-pandemic/ (accessed on 10 January 2021).

- McKenzie, B. The European Union’s Upcoming Policy and Regulatory Initiatives in the Energy Sector. October 2020. Available online: https://www.bakermckenzie.com/en/insight/publications/2020/10/eu-upcoming-policy-regulatory-initiatives (accessed on 5 February 2021).

- European Commission. Regulation (EU) 2020/852 of the European Parliament and of the Council of 18 June 2020 on the Establishment of a Framework to Facilitate Sustainable Investment, and Amending Regulation; European Commission: Brussels, Belgium, 2020. [Google Scholar]

- Fragkos, P.; Kouvaritakis, N. Model-based analysis of Intended Nationally Determined Contributions and 2 °C pathways for major economies. Energy 2018, 160, 965–978. [Google Scholar] [CrossRef]

- Capros, P.; DeVita, A.; Tasios, N.; Siskos, P.; Kannavou, M.; Petropoulos, A.; Evangelopoulou, S.; Zampara, M.; Papadopoulos, D.; Paroussos, L.; et al. EU Reference Scenario 2016—Energy, Transport and GHG Emissions Trends to 2050; European Commission Directorate General for Energy, Directorate General for Climate Action and Directorate General for Mobility and Transport: Brussels, Belgium, 2016. [Google Scholar]

- Fragkos, P.; Tasios, N.; Paroussos, L.; Carpos, P.; Tsani, S. Energy system impacts and policy implications of the European Intended Nationally Determined Contribution and low-carbon pathway to 2050. Energy Policy 2017, 100, 216–226. [Google Scholar] [CrossRef]

- IRENA. Stranded Assets and Renewables: How the Energy Transition Affects the Value of Energy Reserves, Buildings and Capital Stock; International Renewable Energy Agency (IRENA): Abu Dhabi, United Arab Emirates, 2017. [Google Scholar]

- Pietzcker, R.C.; Ueckerdt, F.; Carrara, S.; Boer, H.; Després, J.; Fujimori, S.; Johnson, N.; Kitousi, A.; Scholz, Y.; Sullivan, P.; et al. System integration of wind and solar power in Integrated Assessment Models: A cross-model evaluation of new approaches. Energy Econ. 2016, 64, 583–599. [Google Scholar] [CrossRef]

- Creutzig, F.; Agoston, P.; Goldschmidt, J.; Luderer, G.; Nemet, G.; Pietzcker, R. The underestimated potential of solar energy to mitigate climate change. Nat. Energy 2017, 2, 17140. [Google Scholar] [CrossRef]

- Hansen, K.; Breyer, C.; Lund, H. Status and perspectives on 100% renewable energy systems. Energy 2019, 175, 471–480. [Google Scholar] [CrossRef]

- Iyer, G.; Ledna, C.; Clarke, L.; Edmonds, J.; McJeon, H.; Kyle, P.; Williams, J. Measuring progress from nationally determined contributions to mid-century strategies. Nat. Clim. Chang. 2017, 7. [Google Scholar] [CrossRef]

- Muratori, M.; Calvin, K.; Wise, M.; Kyle, P.; Edmonds, J. Global economic consequences of deploying bioenergy with carbon capture and storage (BECCS). Environ. Res. Lett. 2016, 11, 095004. [Google Scholar] [CrossRef]

- Vishwanathan, S.S.; Garg, A. Energy system transformation to meet NDC, 2 °C, and well below 2 °C targets for India. Clim. Chang. 2020, 162, 1877–1891. [Google Scholar] [CrossRef]

- Xie, Y.; Liu, X.; Chen, Q.; Zhang, S. An integrated assessment for achieving the 2 °C target pathway in China by 2030. J. Clean. Prod. 2020, 268, 122238. [Google Scholar] [CrossRef]

- Jewell, J.; Vinichenko, V.; McCollum, D.; Bauer, N.; Riahi, K.; Aboumahboub, T.; Fricko, O.; Harmsen, M.; Kober, T.; Krey, V.; et al. Comparison and interactions between the long-term pursuit of energy independence and climate policies. Nat. Energy 2016, 1, 16073. [Google Scholar] [CrossRef]

- Fofrich, R.; Tong, D.; Calvin, K.; De Boer, H.; Emmerling, J.; Fricko, O.; Fujimori, S.; Luderer, G.; Rogelj, J.; Davis, S.; et al. Early retirement of power plants in climate mitigation scenarios. Environ. Res. Lett. 2020, 15, 094064. [Google Scholar] [CrossRef]

- Malik, A.; Bertram, C.; Despres, J.; Emmerling, J.; Fujimori, S.; Garg, A.; Kriegler, E.; Luderer, G.; Marthur, R.; Roefsema, M.; et al. Reducing stranded assets through early action in the Indian power sector. Environ. Res. Lett. 2020, 15, 9. [Google Scholar] [CrossRef]

- Fragkos, P.; Kouvaritakis, N.; Capros, P. Incorporating uncertainty into world energy modelling: The Prometheus model. Environ. Model. Assess. 2015, 20, 549–569. [Google Scholar] [CrossRef]

- Rubin, E.S. A review of learning rates for electricity supply technologies. Energy Policy 2015, 86, 198–218. [Google Scholar] [CrossRef]

- PRIMES Model Documentation. 2018. Available online: https://e3modelling.com/modelling-tools/primes/ (accessed on 4 January 2021).

- Fricko, O.; Havlik, P.; Rogelj, R.; Klimont, Z.; Gusti, M.; Johnson, N.; Kolp, P.; Strubberger, B.; Valin, H.; Ammann, M.; et al. The marker quantification of the shared socioeconomic pathway 2: A middle-of-the-road scenario for the 21st century. Glob. Environ. Chang. 2017, 42, 251–267. [Google Scholar] [CrossRef]

- IRENA. Renewable Power Generation Costs in 2019; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2020. [Google Scholar]

- Liu, Z.; Ciais, P.; Deng, Z.; Lei, R.; Davis, S.; Feng, S.; Zheng, B.; Cui, D.; Dou, X.; Zhu, B.; et al. Near-real-time monitoring of global CO2 emissions reveals the effects of the COVID-19 pandemic. Nat. Commun. 2020, 11, 5172. [Google Scholar] [CrossRef]

- IEA. Sustainable Recovery; International Energy Agency: Abu Dhabi, United Arab Emirates, 2020. [Google Scholar]

- Karkatsoulis, P.; Capros, P.; Fragkos, P.; Paroussos, L.; Tsani, S. First-mover advantages of the European Union’s climate change mitigation strategy. Int. J. Energy Res. 2016, 40, 814–830. [Google Scholar] [CrossRef]

- He, G.; Lin, J.; Zhang, Y.; Zhang, W.; Larangeira, G.; Zhang, C.; Peng, W.; Liu, M.; Yang, F. Enabling a Rapid and Just Transition away from Coal in China. One Earth 2020, 3, 187–194. [Google Scholar] [CrossRef]

- Mc Laren, D. Quantifying the potential scale of mitigation deterrence from greenhouse gas removal techniques. Clim. Chang. 2020, 162, 2411–2428. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Abbreviation | Country/Region |

|---|---|

| EU + NO | The European Union Member States plus the UK and Norway |

| North America | The United States of America and Canada |

| ROECD | Japan, South Korea, Australia, and New Zealand |

| China | China and Hong Kong |

| India | India |

| CIS | The former Soviet Union excluding the Baltic Republics |

| MENA | The Middle East and North Africa region |

| RESTW | All other countries, mostly economies in Africa, Latin America, and Asia |

| Scenario Description | Global Climate Targets | |

|---|---|---|

| REF | Reference scenario | Countries meet national policies, but policy ambition does not increase after 2020 |

| 2DEG-OPT | Decarbonisation to 2 °C with all options available | All countries adopt universal carbon pricing from 2020 onwards to meet the global carbon budget of 900 Gt over 2010–2050 |

| NOCCS | Decarbonisation to 2 °C but without CCS uptake | Same as above |

| Delayed | Decarbonisation to 2 °C with all options available | Delayed climate action starting from 2030 onwards globally |

| NOCCS_Delayed | Decarbonisation to 2 °C but without CCS uptake | Same as above |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Fragkos, P. Assessing the Role of Carbon Capture and Storage in Mitigation Pathways of Developing Economies. Energies 2021, 14, 1879. https://doi.org/10.3390/en14071879

Fragkos P. Assessing the Role of Carbon Capture and Storage in Mitigation Pathways of Developing Economies. Energies. 2021; 14(7):1879. https://doi.org/10.3390/en14071879

Chicago/Turabian StyleFragkos, Panagiotis. 2021. "Assessing the Role of Carbon Capture and Storage in Mitigation Pathways of Developing Economies" Energies 14, no. 7: 1879. https://doi.org/10.3390/en14071879

APA StyleFragkos, P. (2021). Assessing the Role of Carbon Capture and Storage in Mitigation Pathways of Developing Economies. Energies, 14(7), 1879. https://doi.org/10.3390/en14071879