1. Introduction: The ‘Green Curtain’ Akin to the Iron Curtain

The bioeconomy, i.e., an economy based on producing or using biological goods and services, occupies the centre of the European Union’s Green Deal, a plan to boost economic growth in the post-COVID-19 period while transforming the economy by decarbonising it [

1,

2,

3,

4,

5,

6,

7]. Within the EU, the countries of Central and East Europe (CEE) (Bulgaria, Croatia, Czech Republic, Estonia, Hungary, Latvia, Lithuania, Poland, Romania, Slovakia, and Slovenia) are often seen as lagging behind in developing their bioeconomy, thereby not harnessing the huge potential held by the bioeconomy (e.g., almost one-third of agricultural and one-quarter of forest biomass in the EU) [

8,

9,

10,

11].

The EU recognises this untapped potential in CEE as a specific problem. The EU’s updated bioeconomy strategy states that the “…low bioeconomy added value in the CEE is at odds with their high, and, compared to other European regions, yet underutilised biomass potential” [

12]. An EU Council session devoted to the bioeconomy organised in 2019 during Finland’s presidency reiterated the importance of this gap. Despite this, actions to bridge the gap have remained limited in terms of supporting the BIOEAST macroregional initiative which, since being established in 2016, coordinates activities aimed at boosting cooperation in strategic innovation and research as well as developing dedicated bioeconomy strategies in CEECs. Thus, the Council has fallen short of CEE countries’ expectations of stronger action being taken. With the European Green Deal, the new multiannual budget for the period 2021–2027, and the Recovery and Resilience Fund in the post-COVID-19 period stepping up activities for transformative growth [

4,

5,

13,

14], the position of the CEE laggards has attracted greater attention. Moreover, the increasing East–West divisions within the EU [

15], exacerbated by the COVID-19 pandemic, have made them more politically significant. The pandemic has seen much higher death tolls in the Eastern EU countries as opposed to the Western ones [

16,

17], reflecting the varying capacity of public institutions, policy, and the slow catch-up in (economic) convergence.

CEE countries’ position in being slow to utilise the bioeconomy’s potential is recognised in the literature. Dietz et al. [

18] argue that the EU is one of the leading bioeconomy regions where considerable differences exist among member states. Studies focusing on value added and employment in the bioeconomy sectors reveal the relative importance of the primary sector and low productivity in CEE (i.e., agriculture accounting for 65% of jobs and 38% of value added) [

8,

9]. These studies noted certain variations among the countries, i.e., a subgroup firmly specialised in bioeconomy sectors and with a low level of productivity (Bulgaria, Croatia, Latvia, Lithuania, Poland, and Romania) and another group of countries with mid-level specialisation and low- to mid-level productivity (Czech Republic, Estonia, Hungary, Slovakia, and Slovenia) [

11]. Over time, the gap between CEE countries and the rest of the EU has expanded since not one CEE country has been able to significantly increase the share of sectors with higher value added and, relatedly, higher labour productivity [

9]. Other constraints pointed to are the stronger fossil dependence and socioeconomic role of the primary sector, e.g., in rural regions [

11].

The purpose of this article is to shed light on the position of CEE countries in deploying the (sustainable) bioeconomy in order to evaluate current policy actions. The chief focus of the EU’s bioeconomy policy has been on research and innovation as well as policy coordination to enhance markets [

7,

12,

13,

19,

20]. In contrast, this article argues that, while relevant, these support mechanisms are more relevant to countries possessing advanced knowledge- and capital-intensive bioeconomy sectors, but are not overly relevant for CEE countries. This view finds support in the argument that the EU’s approach is based on the science–technology–innovation (STI) transformation model that typically works best with sectors featuring high value added. In CEE, where primary and traditional bioeconomy sectors play a more important role, what might prove to be of greater relevance is a model based on the transfer of more tacit knowledge and practices, vertical and horizontal interaction within the value chains, and commercialisation (i.e., DUI: do–use–interact) [

21].

We begin by defining the bioeconomy, the specific transition pathways, and various context-dependent enablers in the process. We confront the two paradigms (STI and DUI) that shape the transition to the (sustainable) bioeconomy and map out the role played by the EU’s policies in this respect. In the methodology section, we discuss the data used in existing studies and present the rationale underlying the survey on the transition pathways and assets conducted among experts in the region. This is followed by a presentation of the main findings in the context of existing studies and data, as well as a discussion of them in regard to the relevance of the main argument of this article. The article concludes by focusing on the findings’ policy relevance and making a call for further research.

2. Framework for Explaining the Transition to a Sustainable Bioeconomy

2.1. Sustainable Bioeconomy

The term bioeconomy is constantly evolving and gaining new emphases. According to the European Commission’s comprehensive definition [

12,

20,

22], the bioeconomy refers to: (a) primary sectors that supply biomass (agriculture, forestry, fisheries, and aquaculture); (b) secondary or industrial sectors that demand and transform biomass into intermediary or final products (conventional ones based on bulky biomass, such as food, wood, paper, and energy, as well as new ones based on low-bulk and high-value applications, such as chemicals, plastics and rubber, and the pharmaceutical industry); and (c) other sectors, such as waste and ecosystem services.

The bioeconomy was first mentioned in the 1970s amid the growing scarcity of carbon-based energy sources and the oil crisis that triggered the search for price-efficient alternatives to fossil fuels, preferably ones with a lower environmental impact [

23]. The bioeconomy first focused on making advances in technologies used in industrial production, namely the aspect of the bioeconomy also known as bioindustry [

24,

25]. In the 2000s and in the context of rising demand for biomass, accelerated by the competitive pressure to use biomass for either food or biofuel production and accompanied by growing environmental pressures, the bioeconomy moved into the centre of attention, also focusing on primary sectors, side streams, and waste, as well as ecological functions of the environment, such as ecosystem services [

12].

Another emerging concept is circularity, which refers to closing the material and energy loops that occur in the use of resources and production of commodities [

2,

26,

27]. The concept shares with the bioeconomy the need for resource efficiency. In terms of the bioeconomy, this has been related to the cascade [

28], i.e., using resources first for strategic (food) and higher-value-added products, reusing the side streams in subsequent production cycles from more valuable products and components, such as bio-based materials, and proceeding towards bulky and low-value outputs, such as energy [

29,

30]. Within bioindustry, concepts such as industrial symbiosis were introduced to highlight the challenges of integrating sources (including side streams and waste) and processes, e.g., through biorefining.

In the 2010s, an ever-increasing number of studies argued that the bioeconomy could be unsustainable with regard to the environment as well as the ecological functions of nature and could lead to the inefficient use of natural resources in addition to degradation [

31,

32,

33]. Researchers emphasised that public policy should support a sustainable bioeconomy [

33,

34,

35]. Primary sectors such as agriculture and forestry, which are the biggest producers and, in the case of agriculture, consumers of biomass [

9], as well as cover a vast share of the area (40% and 43% in the EU, see [

10,

11]), dominate environmental impacts such as loss of biodiversity and contribute a substantial share of GHG emissions [

2,

36,

37]. Their environmental impact partly relates to technology and partly to policies. Public policy should focus on support for a bioeconomy that clearly delivers on public goods such as food and the environment. Interestingly, the key way of supporting the bioeconomy is seen not in (more) subsidies for production but in the removal of the current support (subsidies, tax relief) for the use of non-renewables, in addition to a proper valorisation of the environment and its functions via the effective implementation of the polluter/consumer pays principle so as to facilitate sustainable management practices and innovations [

38].

To summarise, renewables, resource efficiency, and ecological functions of nature have become the three pillars of the sustainable bioeconomy, also keeping in mind the social aspects of sustainability such as jobs and social inclusion [

39].

2.2. The Transition Pathways

Studies describe the transition to the bioeconomy, e.g., of leading countries such as the Netherlands and Finland [

40], as a complex process of the co-evolution of the economy, technology, institutions, culture, and the environment. This process is multi-phase, non-linear, and multi-level. It starts with developments on a micro-level in response to the shifting context, accelerates through the meso-level regime’s development, affecting the structure of demand and supply, and is consolidated through a long-term systemic change. In the centre of the process lies the interaction of the industry, government, and knowledge institutions, also known as the triple helix [

41]. Due to the importance of other actors such as civil society and consumers, some refer to the quadruple helix [

42] and given the specific importance of the natural environment also to the quintuple helix [

43]. While the role of other actors is important in the sense of trade-offs, contestation, and legitimacy [

44,

45], environmental awareness highlights the limits of the exploitation of natural resources and the need to go beyond the trade-offs that may create certain long-term dependencies [

46].

Bioeconomy policy has pursued a knowledge-based approach, ranging from the assessment of (sustainable) biomass’ potential to research and innovation in individual sectors as well as policy coordination [

2,

12,

13,

19,

20]. Dietz et al. [

18] divide measures into: (a) enabling; (b) regulatory; and (c) international cooperation. Enabling measures include supply-side measures such as support for research and innovation, technologies, inventories, infrastructure and logistics, and clusters, as well as demand-side measures such as the funding of environmental goods, either directly (payment for the provision of public goods and income foregone, public procurement) or indirectly (support for awareness-raising measures to engage consumers). Regulatory measures include requirements for different products, standards, and certificates that enable the implementation of principles such as the polluter and the consumer pays. International cooperation enables cross-border externalities, network, and transfer knowledge to be addressed.

More developed bioeconomies are associated with the greater complexity of overlapping (and conflicting) objectives, policy designs, and measures [

18,

46,

47]. For example, rising productivity and new technologies may come with negative environmental effects that impact the growing ecosystem service-related economy. More advanced stages of the bioeconomy require the coordination of different sectors, stakeholders, and value chains by supporting cross-sector strategies, sustainable production and the use of biomass, the deployment of enabling technologies and practices, and the development of markets (new products and services).

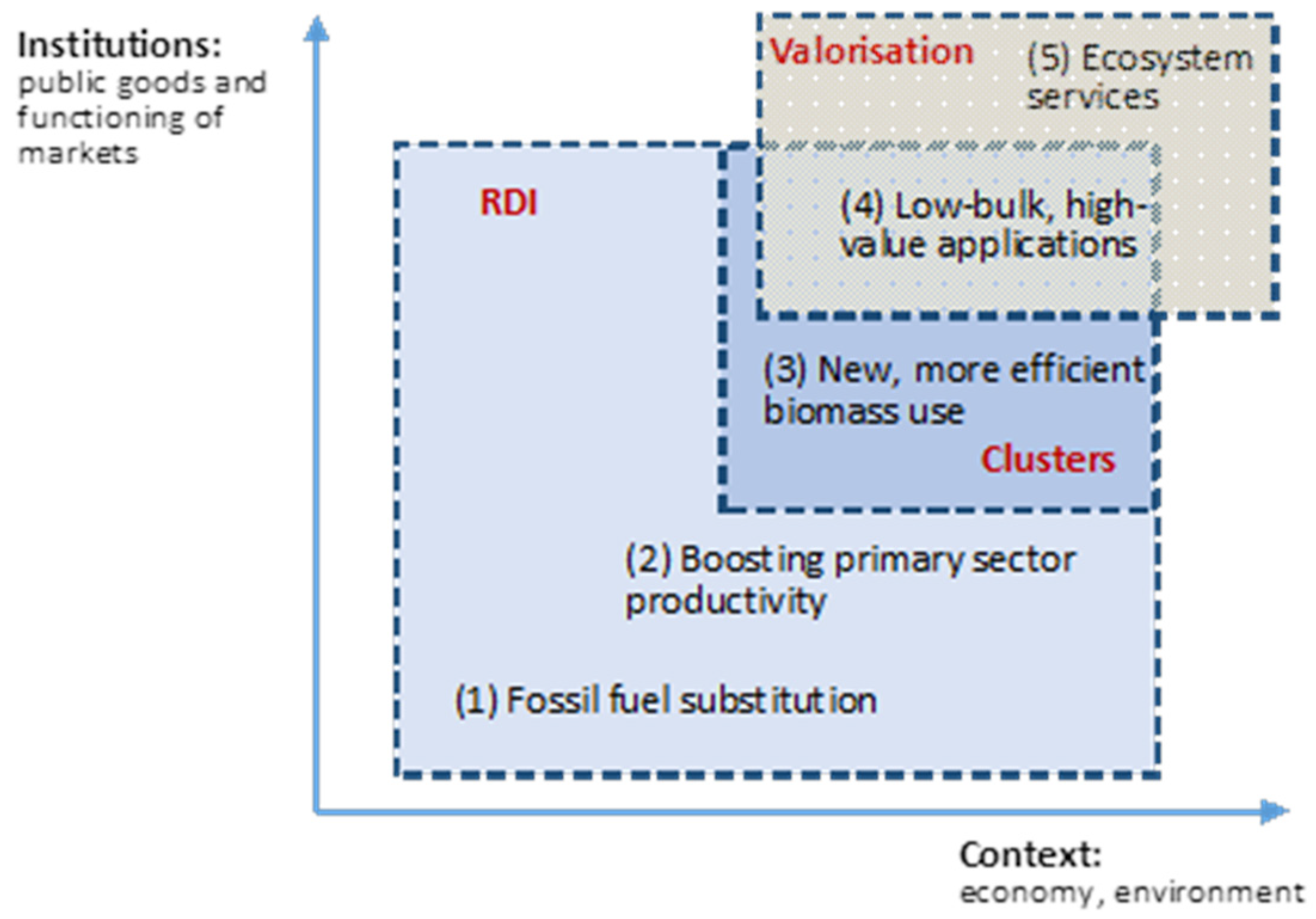

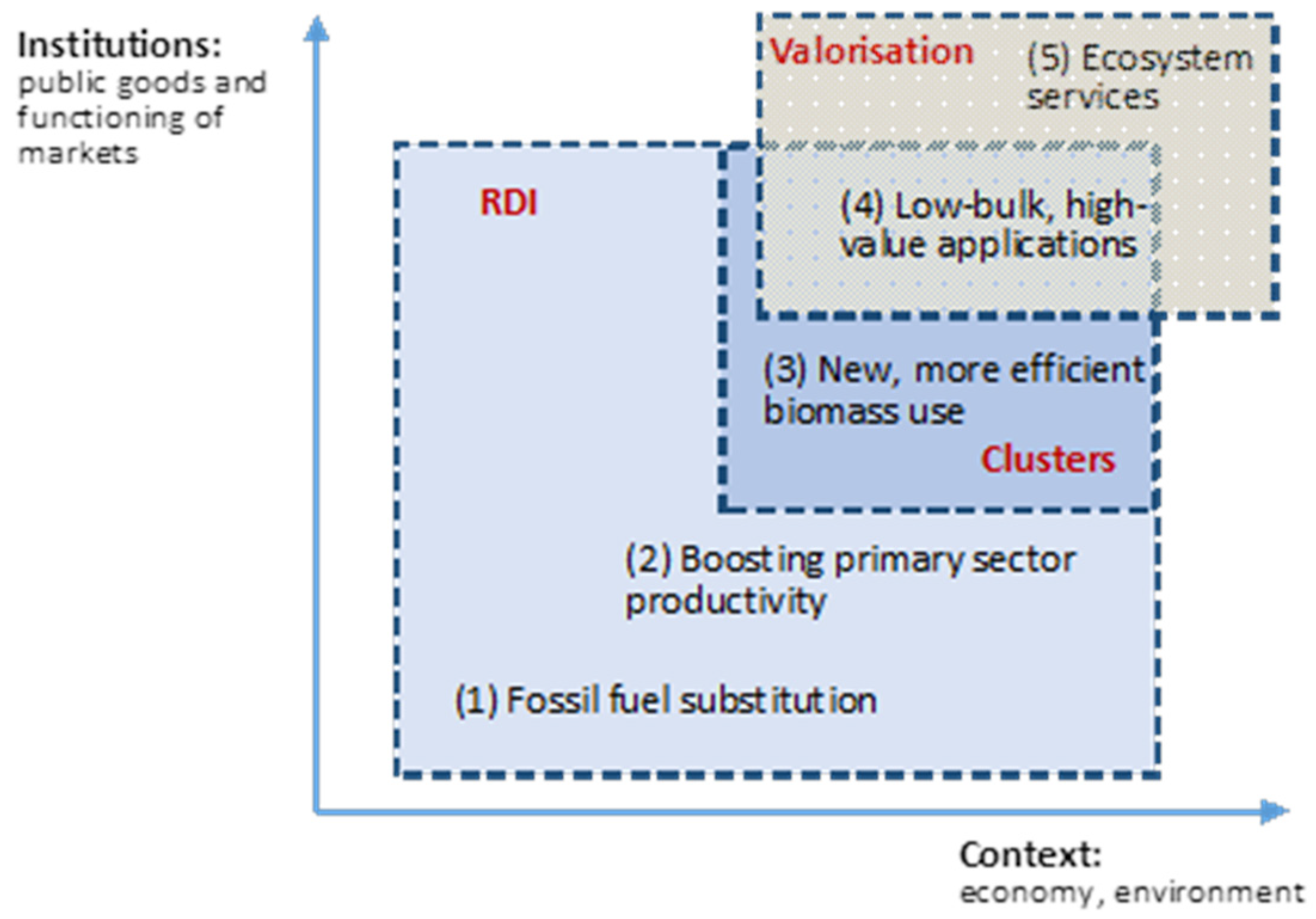

Building on and slightly upgrading Dietz et al. [

18], we distinguish five interrelated yet distinct transition pathways towards the bioeconomy (

Figure 1). The first way (1) entails the substitution of non-renewables as a source of energy, which is linked to increasing energy costs, access to alternative energy sources, and geopolitics. The second (2) is the development of productivity in the primary sector (especially agriculture), which in some cases, such as in developing countries and transition economies, is associated with modernisation and restructuring, and in some instances, such as heavy monocultures, specialisations and natural resource extraction can produce a negative environmental impact. The third pathway (3) involves more efficient and new uses of biomass that encompass side streams and waste, including both conventional and new bioindustries, supply side mobilisation and innovation downstream, biorefining, new cost-efficient technologies, and increases in value added through bioindustry, including through market demand. The fourth way (4) is the development of low-bulk, high-value applications and processes based on biological principles independent of biomass streams, such as cheaper and environmentally friendlier methods and processes, new products, products with improved functionality, advanced solutions, the broad application of biological principles, and the complex interaction of value chains (e.g., between food and health). To this, we add the fifth (5) pathway based on the valorisation of non-commodity aspects such as ecosystem services through public and private action [

48].

The pathways located on the edges of the system (1 and 5) are specifically associated with the role of ‘objective’ contexts (economic development impacting micro-level decisions and the environment impacting the systemic level). Pathways 1–4 are particularly related with institutions and policies that promote research, development, and innovation adoption (RDI). In addition, pathways 3 and 4 are characterised by the interaction of supply and demand through enabling institutions, such as economic clusters. Pathways 4 and 5 are again context-dependent, building on the demand-side trends that allow for the market valorisation of technological advances (4) or ecosystem services (5).

2.3. Enablers on Different Levels of Integration and Complexity of the Transition to the Bioeconomy

As described in the introduction, the STI approach found in the centre of the EU’s public policy is more appropriate for knowledge-intensive and integrated transformation pathways (3 and 4 in

Figure 1), while for less complex ones (pathways 1, 2, and 5) the DUI model performs better [

21]. STI vs. DUI forms part of the debate on the innovation systems that constitute the core of the government–industry–science nexus [

49,

50]. They refer to different inputs and outputs that are not equally relevant at various stages of development [

51]. STI is based on the adoption of research, development, and innovation, highly skilled human resources, advanced technologies, and infrastructure. It supports formalised interactions with knowledge and research institutions (ibid.). Its outputs are new technologies, patents, and publications. In contrast, DUI stresses the importance of practice as well as interaction both within the firm and chain in addition to with the competitors. It is based on routines as opposed to formal knowledge (ibid.). The outputs are more commercial in nature [

51,

52]. STI can better fit high-technology bioindustry, such as the chemical industry, pharmaceutics, and new materials. DUI may be more appropriate for sectors with mature and standardised technology as well as practices, such as agriculture, forestry, food, wood, paper, and energy.

Empirical research has also shown that innovation systems in advanced economies focus more on STI, whereas in economies that are catching up DUI is more common and may contribute to improved competitiveness and economic performance through new sources of supply as well as types of industrial organisation [

50,

53]. Since DUI can also relate to transaction costs and tacit knowledge in local structures resulting in lock-ins [

52], in small or less integrated economies ongoing structural change, such as that in CEE countries, it can specifically work in the context of internationalisation (including export and FDI), which enables it to draw from broader networks and markets [

51]. Still, FDI- and export-based development alone is insufficient for ensuring sustainable development, since in the small–transition economy context it has been associated with an unfavourable position in international value chains and a limited positive impact on the local economy, such as heavy specialisations and mass high-bulk, low-value exports [

54,

55,

56,

57]. Instead, internationalisation and targeted domestic support structures should go hand in hand.

The performance of individual innovation models is specifically related to clusters. Clusters are considered essential for improving the performance of the region’s economies as opposed to that of individual firms [

35,

58]. For a biocluster, along with standard features such as competitiveness, employment, and innovation, sustainability and environmental innovations matter [

59]. Focusing on productivity, innovation, and employment, studies have demonstrated the importance of clusters relative to DUI [

60]. Clusters impact productivity by lowering transaction costs with untraded dependencies. Innovation may occur through knowledge exchange resulting from the proximity of actors necessary for tacit knowledge. Income and employment growth may occur based on business formations, mentoring, role models, learning, communication, and commercialisation that arise from the biocluster setting [

60]. A study of bioclusters [

61] also revealed factors that can be progressively linked to different transition pathways, such as biomass, ecological conditions, infrastructure and logistics including biorefineries, final transformation, competitive products, cascade, biopharmaceutical, fine chemicals, functional foods, and ingredients. While knowledge institutions are key in some cluster settings [

62], a broad industrial base is also important, including conventional manufacturing sectors (e.g., food, wood processing, and pulp and paper), especially for bulky outputs such as biofuel and electricity, but also for industrial demand for chemicals, polymers, and materials for construction. Other types of enabling institutions such as business incubators and accelerators as well as technology parks are also valuable in terms of the development of regulatory and policy frameworks (standards, certification, and public procurement), entrepreneurial culture, and international networking.

2.4. The EU’s Bioeconomy Policy

The EU is a rare case of a regional organisation with a common broad bioeconomy strategy [

25]. The term bioeconomy initially appeared in the fifth framework programme (FP) on financing research. The seventh FP introduced the term knowledge-based bioeconomy, which highlighted the value of evidence and data for fact-based decision making. In 2012 the EU published A bioeconomy strategy for Europe, which aimed at accelerating the “transition from a fossil-based to a bio-based society, with research and innovation as the motor” [

19]. The strategy focused on targeted research funding and policy coordination, leading to better stakeholder interactions and market integration. A bigger emphasis on research was given in order to make better use of the fragmented potential [

10,

39], with a view to establishing synergies between hitherto unrelated RDI efforts and policies in EU competencies—agricultural policy and fisheries (supply side), energy (demand side), and climate and environment (horizontal). In 2018, the EU’s bioeconomy strategy was updated to put greater emphasis on environmental sustainability and ecosystem services [

12,

33]. The strategy was thereby intended to better respond to the changes in the global policy context, such as the SDGs and the Paris Agreement, as well as to put stress on the strategic objectives of Juncker’s Commission, such as reindustrialisation, source efficiency, and circularity. More attention was placed on coherence, both horizontally (between policy areas) and vertically (national strategies and plans relying on EU funding) [

12]. Following the European Parliament elections in 2019, the new von der Leyen Commission has located the bioeconomy in the centre of the Green Deal, its transformative growth plan [

1]. It introduced new (cross)sectoral strategies and plans such as Farm2Fork (agriculture, food, and health) [

63], a forestry strategy, biodiversity strategy [

2], and circular economy action plan [

7], with specific objectives concerning housing and the textiles sector, and increased the ambition of existing plans such as the CAP strategic plans as well as the national energy and climate plans. Bigger shares of overall funding were earmarked for climate action, planning to mobilise further investments, while taxes on carbon and non-renewables, the greening of VAT, and fiscal recommendations were foreseen (European semester) [

2,

3,

4,

5,

6,

14]. The COVID-19 pandemic that followed has created additional opportunities for financing the bio-based transition by using the EU’s public spending on the recovery to boost the transformation [

63,

64].

As mentioned in the introduction, even though the EU’s updated bioeconomy strategy recognises that the CEE member states are systematically lagging behind in bioeconomy development [

12], only a few instruments have been introduced to address this issue. In 2019, the Policy Support Facility (PSF) was introduced for the CEE macro-region in order to support the development of national bioeconomy strategies and to learn from good examples of bioeconomy deployment through EU programmes and financial mechanisms. Strategic macro-regional cooperation on bioeconomy-related research and innovation is a goal of the intergovernmental initiative BIOEAST, established in 2016. In terms of more tangible financial support for physical investments in technology transfer and industrial installations, virtually the whole territory of CEE (except for its most developed metropolitan areas) is eligible for bigger total envelopes and higher co-funding rates within the EU cohesion and structural policy.

3. Materials and Methods

This research attempts to evaluate three factors that influence the process of the transition to the bioeconomy in CEE countries: (a) indicators representing the macroeconomic and R&D potential for the bioeconomy’s deployment in the region; (b) assets and (sector-specific) transition pathways related to the development of the bioeconomy; and (c) the role of the STI vs. DUI support structures in this process.

The absence of a clear definition and concrete measurable objectives means that macro-regional research on the bioeconomy is still in an early stage, as seen in the indicator frameworks [

9,

12,

24,

25,

33,

65]. Since the monitoring system has not yet been adapted to the specifics of the bioeconomy, the evidence base typically refers to (a) physical indicators of biomass resources and flows as well as (b) macro-economic aggregates such as turnover, value added, and employment in bioeconomy sectors. Regarding the latter, researchers in the EU were able to consolidate the methodology on the ‘hybrid’ sectors [

20], whose raw material base may be renewable (bio-based) or non-renewable (usually fossil-based) resources. More complex multicriteria studies and assessments taking account of the environmental footprint throughout the product life cycle and comparing this to fossil-based alternatives are only available for individual streams and products (e.g., biofuels). Moreover, they show a varying impact that depends on the different contexts in which products are made. The data are not much better on the national level as the most frequently employed indicators refer to economic contexts, feedstock and biomass flows, and occasionally to output and result indicators such as R&D expenditure and the recycling rate. Environmental indicators are rare [

66].

To present the economic/environmental context, we use the most recent data on natural assets and economic aggregates provided by the EU’s bioeconomy knowledge centre [

20]. We complement this with various data taken from Eurostat, Forest Europe, and others.

The insight into (sector-specific) bioeconomy-related assets and transformation pathways in CEE countries draws from the results of a survey conducted as part of the BIOEASTsUP research project [

67]. A (web-based) survey, whose principal aim was to provide insight into the qualitative aspects of the bioeconomy’s potential in the region, was carried out between December 2020 and February 2021. The survey was participated in by 352 experts, who gave 732 sector-based responses since the respondents were asked to comment on those bioeconomy sectors that they considered themselves to be familiar with enough to hold informed judgements. In regard to the sample, the main goal was to cover sector-specific expertise in different aspects of RDI, business organisation, and policies related to the bioeconomy, while the actual number of respondents was considered less important. The respondents cover a wide range of sectors relevant to the bioeconomy: agriculture (21%); renewable energy (13%); food products, beverages, and tobacco (9%); forestry and hunting (9%); green care, nature tourism, and recreation (7%); wood and wood products (6%); fisheries, aquaculture, and algae (6%); and other bioeconomy-related sectors (5%).

The respondents were asked to assess the relevance of various bioeconomy-related assets (see below) and transformation pathways (see

Section 2.2). In addressing the key assets shaping the velocity and scope of the transition to the bioeconomy, the survey was consistent with the approach originally developed for analysing bioclusters in the EU [

54]. The following assets were evaluated: (a) stable supply of biomass and efficient logistics; (b) presence of strong ‘conventional’ bioeconomy sectors; (c) level of business consolidation; (d) emerging industrial initiatives for bio-based transformations; (e) policy commitment, availability of public funding; (f) presence and engagement of national research and higher education institutions; (g) actors engaged in innovation transfer and business growth; and (h) availability of private funding. Individual transition pathways (early vs. late stage) and assets (d), (f), and (g) are specifically relevant to the STI vs. DUI debate, while assets (a), (b), and (c) are indirectly relevant, and assets (e) and (h) account for the availability of funding as an additional variable. Despite the obvious difference in the scale of the two analyses (micro- or meso-level of bioclusters in the original approach [

61] vs. the national- or regional-economy level in our analysis), the same groups of actors interact in the development of technologically advanced bio-based value chains.

The experts’ assessment of the relevance of the above-listed bioeconomy-related assets and transition was based on a five-level Likert scale. To synthesise the survey results, we used a particular method. Due to the varying number of responses by the countries, we calculated the median values for each asset/transformation pathway for every sector and individual country. By doing so, we attributed an equal weight to each country. Based on the obtained medians, results were visualised for the CEE region as a whole in boxplots using R 4.0.4 software. By maintaining the medians in this way, we obtained values that deviate from the original Likert scale, i.e., intermediate values. Given that Likert’s scale is ordinal, this is methodologically controversial. However, because such an approach to presenting results enables the most expedient and intuitive interpretation, we decided to make this compromise.

To ensure a better understanding of the RIS/RDI, which is found in the centre of the STI vs. DUI debate, we used data on research intensity from Eurostat (gross expenditure on R&D–GERD and business expenditures on R&D–BERD) on the participation of CEE countries in the Bio-based industries Joint Undertaking, the bioeconomy’s integration in smart specialisation strategies (S3) for the 2014–2020 programming period, which are essential for targeting investments based on the EU’s enabling policies, and on the support institutions in the bioeconomy, such as knowledge hubs, business accelerators, start-ups, technological parks, and venture capital [

67].

In order to validate the importance of demand–pull factors and the integration with international value chains in the specific CEE context (relevant to the DUI hypothesis as outlined in

Section 2.2), we assessed the scope of bio-based sectors in the current industrial structure in CEE countries. The assessment builds on a synthesis of PRODCOM data presented in an analysis of bioeconomy-related sectors in CEE countries [

68]. The analysis of the PRODCOM data more closely considers the industrial products that generate 50% of the total value of production in the analysed countries.

4. Results: Contexts, Performance, and Enabling Environment of the Bioeconomy in CEE

4.1. Resource Base for the Bioeconomy, Performance of Bioeconomy Sectors

The magnitude of the bioeconomy resource base of CEE countries accounts for 35% of the EU’s cropland (30% of which is attributed to Poland) and 27% of the EU’s woodland (25%, again attributed to Poland). Endowments differ considerably among countries. In Slovenia, Estonia, Latvia, and Croatia woodland covers over half the land available for biomass production. On the other hand, agricultural land cover prevails in Hungary, Poland, and Romania, with the largest share of cropland for cereal production being attributed to Hungary (33%). The richness of the region’s resource base is also reflected in production data. With respect to the total volume of production in the EU, the production of agricultural biomass in CEE countries accounts for 31%, while the share of forestry biomass is 27% [

69].

With respect to the available resource base and the exploitation of its potential, benchmarking with the EU average reveals a clear productivity gap in agriculture, although productivity varies from sector to sector and country to country, with some countries achieving comparable yields in certain sectors and others lagging behind significantly. Similarly, there is considerable potential in terms of increasing tree felling, which often lags significantly behind annual increments (and sometimes reaches as low as 44% of the recommended threshold), albeit care must be taken to avoid doing this in an unsustainable manner [

70].

The productivity gap in agriculture is further shown by the fact that, although agriculture largely prevails (65%) in bioeconomy-related employment, it only contributes 38% to the region’s bioeconomy value added (VA). While some productivity growth was seen in the countries’ primary sectors (agriculture, forestry, and fisheries) in the period 2008–2018, this is mainly attributable to the significant drop in employment.

This is in line with the findings of studies concerned with the status of CEE in the transition to the bioeconomy, which place CEE countries in the initial stage of the bioeconomy [

11]. It supports the argument that the key gap between CEE and the leading bioeconomy performers in the EU occurs in the apparent labour productivity, a gap which even expanded between 2008 and 2018 and whose closing holds great potential for developing the bioeconomy.

Another finding consistent with the above-mentioned study is that it is almost a general characteristic of CEE countries that they tend to export primary products and import processed ones, thereby achieving very low value added of both agricultural products and woody biomass.

The total VA of the region’s bioeconomy sectors accounts for 14% of the EU-27′s VA. Apart from the primary sector (agriculture, forestry, and fisheries), conventional bioeconomy processing sectors (food and beverages, pulp and paper, and wood) mainly dominate, although sectoral composition (endowments, biomass resources, and industrial structure) varies. The region is characterised by the relatively dense distribution of industrial plants in ‘conventional’ bioeconomy sectors, yet there is the largely untapped potential of biomass side streams. There is a notable lack of integrated biorefineries, with the region’s capacities accounting for just 10% of those of the EU-27 [

71]. The structure of bioeconomy sectors is adapting slowly. However, high employment and VA growth are recorded in some sectors that are currently still marginal in CEE national economies (e.g., biopharmaceuticals, bio-enzymes and active components, and bio-based chemicals).

4.2. Assets Related to Developing the Bioeconomy

4.2.1. Stable Supply of Biomass and Efficient Logistics

The survey results attribute great relevance to the stable supply of biomass, especially to agriculture, forestry, and their immediately related downstream sectors (food and feed production, wood processing, pulp and paper, and also bioenergy). Efficient logistics is important as well, including for the industrial use of side streams (e.g., lignocellulose materials) where the cost-efficient and constant inflow of inputs of constant quality is required for the efficient organisation of business processes. Despite this, a specific feature of a large part of CEE countries is the small-scale and scattered ownership in addition to the production structure. This makes it challenging to establish efficient logistic flows and provide biomass at an industrial scale.

4.2.2. The Presence of Strong ‘Conventional’ Bioeconomy Sectors

The presence of entrepreneurs and entrepreneurial culture is often regarded as a key asset for developing bioeconomy clusters [

61]. The presence and active participation of large industrial actors from ‘conventional’ bioeconomy sectors (e.g., food and feed production, wood processing, and pulp and paper) appear particularly important while developing innovative products or components (chemicals and polymers, construction, etc.), applying the principle of the cascading use of biomass. As previous research reveals, bioeconomy clusters in CEE countries are principally focused on the agri-food sector and bioenergy [

8]. The survey results [

67] indicate that the potential for establishing clusters is also present in other bioeconomy sectors, especially in the sectors of forestry and wood, paper and pulp, and organic waste management. The low capturing of value in the bioeconomy-related primary and manufacturing sectors in the region (see

Section 4.1) might pose another obstacle in this process.

4.2.3. Level of Business Consolidation

The logic behind this asset is that sectors with strong, consolidated firms find it easier to provide leverage for the development of bioeconomy clusters. The assessment relates to the level of ownership and/or management consolidation in the sectors concerned. The overall level of business integration into CEE countries is quite low, which prevents the scale effects needed for a functioning ‘standard’ bioeconomy concept, integrating firms into the same or complementary sectors with a biorefinery at its core. Experts attributed great importance to this asset especially in bioeconomy sectors that are currently not consolidated and thus unable to reap the benefits of integrated operation. However, as revealed in industrial initiatives [

67], the integration of industries from CEE countries into international value chains, particularly in more technology-intensive sectors (e.g., the chemical industry, automotive) may provide an important engine of growth for bio-based industrial applications.

4.2.4. Emerging Industrial Initiatives for Bio-Based Transformations

The subject of assessment is industrial initiatives (e.g., smart specialisation, KET, and clusters) that actively develop circular bioeconomy technological solutions and business models. With regard to this asset, apart from the survey, a desk study was carried out, analysing bioeconomy-related priorities in the national S3 of BIOEAST countries [

67]. The analysis shows that the S3 priorities resonate quite well with their resource endowments for the bioeconomy as well as with the associated economic sectors. As a rule, the central role in bioeconomy-related priorities is attributed to the agri-food and forest–wood value chains (except for Czechia, which also emphasises organic waste management and sustainable transport, and Croatia, with additional emphasis on the blue bioeconomy) [

60]. Particularly in the case of S3 priorities that only partly relate to the bioeconomy, one can find a whole set of prospective technological solutions (such as, e.g., the extraction of bioactive compounds and other biorefining processes, the development of advanced bio-based materials, industrial biotechnology applications, biofuels, and bioenergy). Additionally, quite strongly represented is a set of supporting enabling technologies (e.g., digitalisation, advanced materials and technologies, and energy-efficient networks) and social innovations (e.g., smart villages, eco-tourism). What is also perceivable, however, is a relatively weak commitment to comprehensive technological and social solutions for closing the material, energy, and economic loops.

4.2.5. Policy Commitment, Availability of Public Funding

The assessment applies to publicly supported measures and instruments that are sector-specific, or available to the sector, and where bioeconomy-oriented projects are eligible for that support. This asset is perceived as very relevant in sectors currently in receipt of large subsidies, such as agriculture (e.g., the EU’s CAP), energy (e.g., feed-in tariffs), and organic waste management. Public support is also seen as particularly relevant for two other primary sectors (forestry and hunting; fisheries, aquaculture, and algae sector). Among the manufacturing sectors, the sector of wood and wood products stands out here.

4.2.6. Presence and Engagement of National Research and Higher Education Institutions

The assessment here applies not just to the presence but the actual engagement of national R&I and higher education institutions in applied research relating to the sector concerned. According to the survey results, the presence and engagement of national research and higher education institutions is an overall relevant asset in the CEE macro-region. With respect to this asset, CEE is still below the EU average in terms of GERD, although the gap has been reduced mostly by virtue of growth in BERD. The investments are concentrated in individual (export) oriented industrial sectors where biological components are only slowly replacing fossil-based ones. The in-depth desk research [

67] further revealed the reluctance of the industry to invest in new bio-based technologies for various reasons (e.g., cost efficiency, demand-side risks, and lacking financial leverage). The region is also facing RDI challenges, such as a high proportion of small businesses unable to invest in this field, an insufficient level of private sector investment, a small number of employees in RDI, a small number of scientists focused on applied research, and a lack of cooperation and coordination between academia, public administration, and industry (ibid.).

4.2.7. Actors Engaged in Innovation Transfer and Business Growth

This asset relates to the presence and importance of various actors engaged in innovation transfer (innovative products, processes, or business models), digitalisation, and commercialisation (business angels, business incubators and accelerators, or similar). The survey results reveal that this asset is relevant to the bioeconomy’s development in most of the sectors concerned. Alongside the survey, additional emphasis has been put on the environment that enables business growth, such as business clusters, technology parks, and start-up accelerators. Results of the dedicated survey on business clusters (general or sector-specific) that develop bioeconomy-related technologies in CEE countries reveal a diverse and dynamic situation [

67]. Industrial and other stakeholders are increasingly pooling their resources to exploit synergies in business clusters. The dynamism and scope entailed suggest that industrial initiatives may be taking on the leading role in exploiting the potential held by the bioeconomy in the region. Technology parks have evolved into a mainstream support tool for boosting technology transfer as well as innovative start-ups and SMEs across the region. Yet, in most cases, technology parks do not make distinctions concerning eligible sectors. What holds for technology parks similarly applies to business accelerators. A vibrant network of business accelerators has emerged across the whole CEE macro-region. As a rule, they are complemented with public funding.

4.2.8. Availability of Private Funding

This asset relates to the availability, quality, and affordability of financial services for specialised financial institutions (venture capital, banks, and insurance firms) that support bioeconomy-related projects in the sectors concerned. Based on the assessment of the survey respondents, the availability of private funding is generally a slightly less relevant asset for developing the bioeconomy in the CEE macro-region compared to the availability of public funding. The mentioned desk study showed that financial institutions dealing with risk financing are more concerned about returns on their investments and less about the sectors their client firms are engaging with [

67]. As part of de-risking strategies, public funding sometimes complements risk financing (Latvia, Poland, and Slovenia). The conditions of support, and especially the financial leverage of risk financing, vary largely. A more favourable environment for risk financing is found in countries with a larger scale and/or maturity of the venture capital market (Czechia, Estonia, Hungary, and Poland).

4.3. (Sector-Specific) Transition Pathways

The course and effects of bioeconomic transformation processes largely build on the existing mix and technological level of bioeconomy sectors, the efficient provision of biomass, and a favourable institutional environment. Among the transformation pathways relevant to CEE countries (

Table 1), regional bioeconomy experts highlight the importance of accelerated technological improvements in primary sectors (agriculture, forestry), and conventional bioeconomy sectors (food and feed, wood processing, and paper and pulp). Despite this, as boosts in productivity in land-based sectors (agriculture, forestry) have also been shown to increase the demand for land in ecologically sensitive areas, care must be taken to prevent losses in ecosystem services (especially through the over-intensification of land use in unprotected areas).

The fossil fuel substitution transition pathway has (as expected) been recognised as particularly relevant for the side streams of biomass in primary (agricultural and forestry) production and partly in relation to organic waste management. The production of biogas and biofuels is firmly rooted in the bioeconomy in CEE countries that possess favourable resource endowments (Czechia, Slovakia, and Poland), while the energetic use of biomass is considered a ‘success story’ in Lithuania. Still, this transformation pathway must be treated with some caution, especially in the case of relatively large installations, changing regulations (e.g., restricting the use of plant substrates, mainly maize silage), and high subsidies (e.g., feed-in tariffs). Slovenia is a good example here, with a number of (fairly recent) stranded investments in this sector resulting from unsustainable technology (plant-based substrate) and non-viable business models (not sustaining drastic reductions in feed-in tariffs). In regions with relatively scarce and scattered biomass resources, the ‘production of biofuels’ is a strategy only feasible for small-scale operators to improve the (energy, ecological, and economic) performance of their biomass side streams, whereas it cannot serve as a backup technology for renewables such as solar and wind energy [

72].

Another transformation pathway that should be noted with respect to the bioeconomy’s growth in CEE countries relates to the innovation in downstream sectors that increases the efficiency of biomass use and waste stream recycling. New and more efficient uses of biomass streams through cascaded use is gaining new meaning in the bioeconomy, especially in primary sectors (agriculture, forestry) and ‘conventional’ manufacturing sectors (notably wood and wood products). Among novel bioeconomy sectors, the sector of chemicals and chemical products stands out as the most relevant according to the survey results. However, several factors need to be efficiently tackled before the potential of this transformation pathway is unleashed. The first challenge is inter-sectoral cooperation (let alone integration) among bioeconomy sectors, which is relatively low, resulting in broken and incomplete value chains. The next challenge, which adds to the previous one, is associated with the establishment of biorefineries (already addressed previously). Their impact depends on supply dynamics, consumer behaviour, and the regulatory environment.

The possibilities of using the untapped potential for improving product functionalities and adding value with technologically advanced bio-based solutions in the CEE macro-region is overall a very relevant transformation pathway as the respondents’ assessments are not lower than relevant in most of the sectors concerned. The low-bulk, high-value transition pathway seems more feasible for high-technology sectors such as biotechnology, biopharmaceuticals, and biomaterials. The national survey reports further that the biggest challenge concerning this transformation pathway is the poor industrial uptake of low-bulk, high-value bio-based applications (usually developed within the R&D sector) [

67].

In general, the valorisation of ecosystem services, such as biodiversity, water regimes, rural vitality, and tradition, for adding to the market value of commodities in the CEE macro-region has been assessed as a relevant to a very relevant transformation pathway in all sectors under study. This transformation pathway is the most applicable, based on the respondents’ judgement, in the sector of green care, nature tourism and recreation. Among primary sectors, this transformation pathway appears to be the most promising for the development of organic farming and its market penetration.

4.4. Demand–Pull Factors: Integration with International Value-Chains

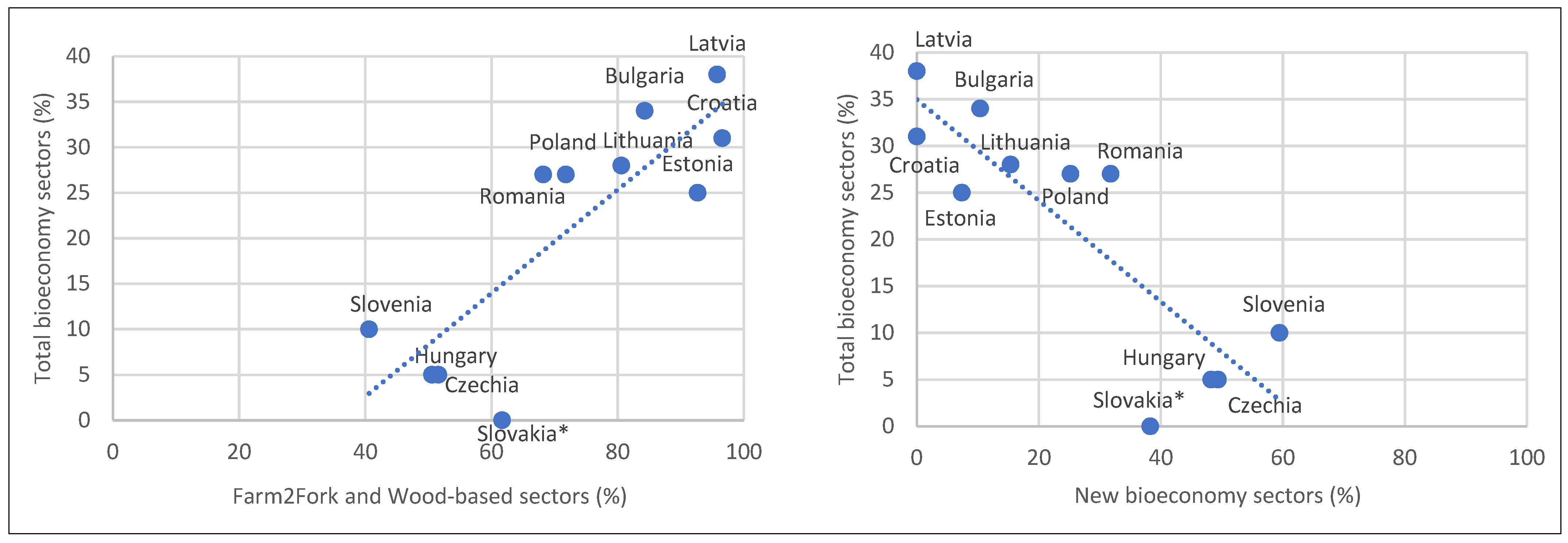

Table 2 presents the share of (potentially) bio-based products among PRODCOM products that generate 50% of the total value of production. Slovakia is the sole exception to this approach. As non-bioeconomy sectors (mainly related to the automotive industry) account for over 50% of PRODCOM value, the structure of bio-based industry is estimated from the largest 12 PRODCOM items. Products are presented in the form of four sector aggregates: (i) ‘Farm2Fork’ (i.e., agriculture and food) sectors; (ii) wood-based sectors; (iii) new (potential) bioeconomy sectors (e.g., chemical products, plastics and rubber, and textiles); and (iv) other bioeconomy sectors (e.g., biofuels and bioenergy, fishery and aquaculture products).

The overall significance of (potentially) bio-based sectors in the structure of manufacturing outputs differs considerably in the CEE macro-region. In Latvia, Bulgaria, and Croatia, (potentially) bio-based products contribute about one-third of the total value of production to their countries’ leading industrial outputs (i.e., the upper 50% of PRODCOM value). Lithuania, Romania, Poland, and Estonia follow closely, with shares ranging from 25% to 28%. The remaining four countries (Slovenia, Czechia, Hungary, and Slovakia) reveal a completely different picture. Bio-based and potentially bio-based products are only marginally found in the upper 50% of the total industrial production value.

Table 2 also shows marked differences in the sectoral structure of the leading (potential) bio-based products in the CEE macro-region. The ‘Farm2Fork’ (i.e., agri-food) sectors dominate in the overall PRODCOM structure in Bulgaria and Croatia. Poland and Romania also exhibit the dominant role of the agri-food sector in the sectoral structure of the bioeconomy’s output. The wood value chain dominates the structure of the bioeconomy’s output in the Baltic states. The sectors that have yet to start replacing conventional (mostly fossil-based) ingredients with bio-based ones are most strongly represented in Czechia, Hungary, and Slovenia.

The indicators described above do not provide straightforward information about the integration of industrial sectors into international value chains. Yet, they may be indicative in the sense that the sectors exhibiting the largest scale can only do so if integrated into international markets (and, most often, into international value chains). Based on this assumption, we may infer that the leading bioeconomy sectors in CEE countries’ sectoral structure are those that are most probably integrated into international value chains.

5. Discussion

This research provides insights from different angles concerning the central research question of this article, i.e., the relevance of the (currently supported by EU policy) STI- vs. (alternative) DUI-based support structures to bridge the gap seen in the bioeconomy’s development in the CEE region.

To begin with, data on the existing bioeconomy’s development levels and resources confirm that CEE has untapped potential for the development of productivity and sustainable production growth in the primary and conventional bioeconomy sectors, especially in the forestry, wood, and pulp and paper industries, while the improvement of productivity in agriculture should be accompanied by the development of sustainable management practices [

10]. For this approach, the relevance of STI is limited as opposed to DUI due to the mature level of technologies and the need to address specific context- and practice-related challenges to their efficient application.

Second, while the survey of the experts and the research into the assets relevant for the development of the bioeconomy [

67] do not give a straightforward answer on the comparative roles of the STI vs. the DUI model, they do indicate the specific relevance of the former. The survey showed the importance of efficient supply and logistics for both primary and downstream sectors, especially for tapping the side streams, which is where CEE has some potential. The fragmented ownership and production structures (and in some cases huge conglomerates that impact market prices) pose a specific challenge to CEE. While this does not refer directly to the STI vs. DUI debate, horizontal stakeholder interaction and organisation is generally associated with the efficient operation of DUI. The survey also highlighted the relevance of the traditional industries, particularly their consolidation, which is often seen as a problem in individual sectors in CEE. The level of business consolidation underlines the validity of DUI as a valid transition mode for the smaller, less integrated (in terms of infrastructure and networks), and less globalised CEE macro-region. Moreover, according to the mentioned survey and desk research, strategic industrial development initiatives that focus on key technologies typically associated with bioindustries can be found across the region. Investment, especially by private companies, is growing and catching up to that in the most advanced CEE countries, but is also heavily concentrated in individual sectors, especially those where the replacement with biological sources is slow. While private and business support structures are in the centre of the bioeconomy’s development, small and fragmented businesses often find it hard to mobilise sufficient RDI investments or engage more with the higher education and research sector. It then follows that the support structures typically associated with the STI model are largely present in the region but that the bioeconomy uptake they facilitate is quite narrowly distributed [

67]. A broader development would require stronger interaction both horizontally and with downstream sectors to allow operation of the DUI model. Meanwhile, the assets corresponding to alternative variables such as policy commitment and funding turned out only to be relevant for specific sectors (policy for agriculture and energy) or less relevant (funding).

Third, the experts’ views on specific transition pathways confirmed the prioritisation of the productivity development pathway: (1) in the primary and conventional industry pathway, previously associated with the relevance of the DUI-based approach. The fossil fuel substitution pathway (2) has been recognised as relevant in relation to side streams and waste, which relates to the discussion on the challenge of mobilising sources via efficient logistics. The data showed that biomass use for heating in CEE between 2011 and 2015 was below the EU average (3.5% vs. 11.5%) but above the average for biofuel production (2.1% vs. 1.5%) [

8], highlighting the role of policy in this area, i.e., subsidies for biofuel production which, however, did not support sustainable practices nor long-term market uptake. Enhanced supply dynamics and regulation of fossil sources would better support this sector’s development. Due to a different context, the use of biomass for heat production should not be seen as a general solution but as a solution suitable for certain individual localities. The improved source efficiency pathway (3) was considered relevant by the experts for the downstream sectors in particular, pointing to the role of DUI, but also for individual, more advanced sectors such as chemicals. Yet, to exploit the potential there is a need for enhanced horizontal and vertical interaction, which is specifically related to DUI. Among other things, CEE features a relatively small share of integrated biorefineries. As for the low-bulk, high-value transition pathway (4), the poor uptake of high-tech applications demonstrates the limits of an STI-based approach. The valorisation of the ecosystem services pathway (5) is considered relevant across different sectors. However, its effective deployment requires a combination of effective demand supported by public policy and the overcoming of fragmented structures as well as distrust in cooperation in sectors such as agriculture and services, a typical feature in the region that is hindering a DUI-associated transfer and the adaptation of marketing- and organisation-related practices to particular local contexts.

Fourth and finally, among PRODCOM products that generate the upper half of the total value, higher shares of the primary and conventional sectors (Farm2Fork and wood-based) are typically associated with a larger overall share of bioeconomy products, while bigger shares of novel bioeconomy sectors typical of countries with overall higher productivity levels are associated with bioeconomy products being less important in the PRODCOM structure (

Figure 2). In spite of its traditional FDI-based industrial export orientation, FDI on a larger scale is absent in the CEE Farm2Fork and wood chains, apart from food in Bulgaria, Czech Republic, Hungary, Poland and Romania, agriculture in Czech Republic, and forestry and wood in Latvia [

73]. This reveals untapped potential in terms of integration into international value chains to draw on the DUI transition mechanism. The current trade patterns in the bioeconomy in terms of exports of raw commodities and imports of processed goods indicate the need to enable environment-prioritising investments related to the stronger integration of the value chain and value capture.

6. Conclusions: The Need to Revive Industry in CEECs

The purpose of this article was to address the gap between the Western and Eastern parts of the EU in bioeconomy development from a new angle, pointing to the limited relevance of the current STI-based, EU-level public policy approach which is more suitable for the Western EU member states where the bioeconomy has reached a more advanced level. In contrast, we have argued that for the Central and Eastern part of the EU a DUI model focusing on horizontal and vertical interaction within value chains, the transfer of tacit knowledge, and practices oriented to commercialisation is more appropriate.

From a broader theory and policy perspective, this article adheres to the economic geography literature after the outbreak of the financial and economic crisis in 2008 that emphasises the importance of industrial development for the well-being of nations. This issue might be even more pronounced for CEE, whose economic landscape has changed considerably over the past three decades. Recent industrial policy developments in CEE note note the relatively strong, yet unevenly distributed reindustrialisation. In contrast to conventional industrial policy theory, which associates industrial growth with research and innovation funding as well as policy coordination, they argue that the impulse for reindustrialisation in the region is better explained by the improvements made in export sophistication. If that were the case, this would require a revision of the current EU policy tools in place, which are largely based on conventional industrial policy theory. Stronger emphasis should also be given to the changing global demand patterns, where growth levels in bio-based industrial sectors are anticipated for the next two decades.

This article indicates certain gaps in the research that still need to be addressed; the (hypothetical) relevance of the DUI-based innovation model should be further tested by building on cases of its successful application in practice in the region. In addition, as mentioned, DUI has been often associated with lagging economies and might also lead to local lock-ins. Namely, potential downsides should also be considered. This would help to devise more specific and better target policy, taking various trade-offs into account. Finally, this research does not reject the relevance of the STI-based innovation model and instead highlights the lack of attention paid to particular contexts and complementary approaches. The limited impact of the STI approach in the region and especially the concentrated distribution of advanced bioindustry investments in the region call for further attention to be properly understood.

This research confirms the need for policy support in CEE for better horizontal and vertical interaction, overcoming the fragmented or overly concentrated ownership structures and distrust, efficient logistics, the integration of side streams, biorefinery installations, the removal of measures supporting unsustainable practices, and improved (cross-sectorial) regulation. Export orientation and FDI should be seen as an important (but insufficient in themselves) factors that could contribute to achieving those ends.

A possible specific policy solution that would build on the existing mechanisms entails expanding the role played by the BIOEAST initiative by giving greater attention to the DUI approach in the sense of bringing stakeholders from the business sector on to the board and expressly supporting the build-up of business cooperation networks and hubs, B2B initiatives, demonstration, training and peer-to-peer projects, advisory services, and regional market integration.

Author Contributions

Conceptualisation, M.L. and L.J.; methodology, L.J.; resources, L.J.; data curation, L.J.; writing—original draft preparation, M.L.; writing—review and editing, M.L. and L.J.; visualisation, M.L. and L.J.; funding acquisition, L.J. All authors have read and agreed to the published version of the manuscript.

Funding

This paper has benefited from the research projects ‘Advancing Sustainable Circular Bioeconomy in Central and Eastern European countries’—BIOEASTsUP (Horizon 2020 research and innovation programme under Grant Agreement No. 862699) and ‘Bridging gaps in Bioeconomy: from Forestry and Agriculture Biomass to Innovative Technological solutions’—BRIDGE2BIO (V4-1824, financed by the Slovenian Research Agency and the Ministry of Agriculture, Forestry and Food of the Republic of Slovenia). The authors acknowledge the financial support received from the Slovenian Research Agency (research core funding P4-0022).

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Acknowledgments

We wish to thank the three double-blind peer reviewers for their helpful comments and suggestions regarding earlier versions of the article. It is understood that any remaining issues are solely the authors’ responsibility.

Conflicts of Interest

The authors declare no conflict of interest. The funders had no role in the design of the study; in the collection, analyses, or interpretation of the data; in the writing of the manuscript; or in the decision to publish the results.

References

- European Commission. Research and Innovation. Green Deal and Bioeconomy. Available online: https://ec.europa.eu/info/sites/info/files/research_and_innovation/research_by_area/documents/ec_rtd_greendeal-bioeconomy.pdf (accessed on 20 March 2021).

- EU Biodiversity Strategy for 2030. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52020DC0380 (accessed on 20 March 2021).

- Stepping Up Europe’s 2030 Climate Ambition—Investing in a Climate-Neutral Future for the Benefit of Our People. Available online: https://eur-lex.europa.eu/legal-content/en/ALL/?uri=CELEX:52020DC0562 (accessed on 20 March 2021).

- European Climate Law. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?qid=1588581905912&uri=CELEX:52020PC0080 (accessed on 20 March 2021).

- European Climate Pact. Available online: https://europa.eu/climate-pact/system/files/2020-12/20201209%20European%20Climate%20Pact%20Communication.pdf (accessed on 20 March 2021).

- The EU Budget Powering the Recovery Plan for Europe. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=COM:2020:442:FIN (accessed on 20 March 2021).

- A New Circular Economy Action Plan—For a Cleaner and More Competitive Europe. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=COM%3A2020%3A98%3AFIN (accessed on 20 March 2021).

- Piotrowski, S.; Dammer, L. State of Play of Central and Eastern Europe’s Bioeconomies. In SCAR Bioeconomy Strategic Working Group and CASA. 2018. Available online: https://scar-europe.org/images/SCAR-Documents/Reports_outcomes_studies/BSW2_18-11-22_State-of-play-of-central-and-eastern-Europes-bioeconomies.pdf (accessed on 20 March 2021).

- Ronzon, T.; M′Barek, R. Socioeconomic Indicators to Monitor the EU’s Bioeconomy in Transition. Sustainability 2018, 10, 1745. [Google Scholar] [CrossRef] [Green Version]

- Ronzon, T.; Piotrowski, S.; M′barek, R.; Carus, M.; Tamošiūnas, S. Jobs and Wealth in the EU Bioeconomy/JRC—Bioeconomics. European Commission, Joint Research Centre (JRC) [Dataset]. Available online: http://data.europa.eu/89h/7d7d5481-2d02-4b36-8e79-697b04fa4278 (accessed on 20 March 2021).

- Ronzon, T.; Piotrowski, S.; Tamosiunas, S.; Dammer, L.; Carus, M.; M′Barek, R. Developments of Economic Growth and Employment in Bioeconomy Sectors across the EU. Sustainability 2020, 12, 4507. [Google Scholar] [CrossRef]

- Updated Bioeconomy Strategy. Available online: https://knowledge4policy.ec.europa.eu/publication/updated-bioeconomy-strategy-2018_en (accessed on 20 March 2021).

- A New Industrial Strategy for Europe. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52020DC0102 (accessed on 20 March 2021).

- 2030 Climate Target Plan. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52020DC0562 (accessed on 20 March 2021).

- Andor, L. Fifteen Years of Convergence: East-West Imbalance and What the EU Should Do About it. Intereconomics 2019, 1, 19–23. [Google Scholar] [CrossRef] [Green Version]

- Niftiyev, I.; Huseynova, R. How has the Self-Perceived Health Shaped the COVID-19 Causalities in the Visegrad Countries? In Proceedings of the 3th International Scientific and Practical Conference “Theory and Practice of Science: Key Aspects”, Rome, Italy, 21–22 May 2021; Volume 58, pp. 60–71. [Google Scholar]

- Reuters. Excess Deaths—Europe’s COVID-19 Divide. Available online: https://graphics.reuters.com/HEALTH-CORONAVIRUS/DEATHS/jznvnmanrpl/ (accessed on 20 November 2021).

- Dietz, T.; Börner, J.; Förster, J.J.; von Braun, J. Governance of the Bioeconomy: A Global Comparative Study of National Bioeconomy Strategies. Sustainability 2018, 10, 3190. [Google Scholar] [CrossRef] [Green Version]

- Innovating for Sustainable Growth: A Bioeconomy for Europe (EU’s Bioeconomy Strategy). Available online: https://ec.europa.eu/research/bioeconomy/pdf/official-strategy_en.pdf (accessed on 20 March 2021).

- EU’s Bioeconomy Policy. Knowledge Centre for Bioeconomy. Available online: https://ec.europa.eu/knowledge4policy/bioeconomy/about_en (accessed on 6 March 2021).

- Stojčić, N.; Aralica, Z. (De) industrialisation and lessons for industrial policy in Central and Eastern Europe. Post-Communist Econ. 2018, 30, 713–734. [Google Scholar] [CrossRef]

- European Commission. Factsheet Food-Bio Resources. Available online: https://ec.europa.eu/info/sites/info/files/research_and_innovation/knowledge_publications_tools_and_data/documents/ec_rtd_factsheet-food-bio-resources-agri-envi_2019.pdf (accessed on 20 March 2021).

- Viaggi, D. Bioeconomy and the Common Agricultural Policy: Will a strategy in search of policies meet a policy in search of strategies? Bio-Based Appl. Econ. 2018, 7, 179–190. [Google Scholar]

- OECD. The Bioeconomy to 2030-Designing a Policy Agenda; OECD: Paris, France, 2009. [Google Scholar]

- FAO. Assessing the Contribution of Bioeconomy to Countries’ Economy; A Brief Review of National Frameworks; FAO: Rome, Italy, 2018. [Google Scholar]

- Towards a Circular Economy: A Zero Waste Programme for Europe. Available online: https://eur-lex.europa.eu/legal-content/EN/ALL/?uri=CELEX:52014DC0398 (accessed on 20 March 2021).

- Closing the Loop—An EU Action Plan for the Circular Economy. Available online: https://eur-lex.europa.eu/legal-content/EN/ALL/?uri=CELEX:52015DC0614 (accessed on 20 March 2021).

- Stegmann, P.; Londo, M.; Junginger, M. The Circular Bioeconomy: Its elements and role in European bioeconomy clusters. Resour. Conserv. Recycl. 2020, 6, 100029. [Google Scholar] [CrossRef]

- The Role of Waste-to-Energy in the Circular Economy. Available online: https://eur-lex.europa.eu/legal-content/EN/ALL/?uri=CELEX:52017DC0034 (accessed on 20 March 2021).

- A European Strategy for Plastics in a Circular Economy. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=COM:2018:28:FIN (accessed on 20 March 2021).

- Heimann, T. Bioeconomy and SDGs: Does the bioeconomy support the achievement of the SDGs? Earth’s Future 2019, 7, 43–57. [Google Scholar] [CrossRef] [Green Version]

- Philippidis, G.; Shutes, L.; M’Barek, R.; Ronzon, T.; Tabeau, A.; van Meijl, H. Snakes and ladders: World development pathways’ synergies and trade-offs through the lens of the Sustainable Development Goals. J. Clean. Prod. 2020, 267, 122147. [Google Scholar] [CrossRef]

- Ronzon, T.; Sanjuánc, A.I. Friends or foes? A compatibility assessment of bioeconomy-related Sustainable Development Goals for European policy coherence. J. Clean. Prod. 2020, 254, 119832. [Google Scholar] [CrossRef]

- Mukhtarov, F.; Gerlak, A.; Pierce, R. Away from fossil-fuels and toward a bioeconomy: Knowledge versatility for public policy? Environ. Plan. 2017, 35, 1010–1028. [Google Scholar] [CrossRef]

- Philp, J.; Winickoff, D.E. Clusters in Industrial Biotechnology and Bioeconomy: The Roles of the Public Sector. Trends Biotechnol. 2017, 35, 682–686. [Google Scholar] [CrossRef]

- Diaz, S.; Settele, J.; Brondízio, E.; Ngo, H.T.; Agard, J.; Arneth, A.; Balvanera, P.; Brauman, K.; Butchart, S.; Chan, K.; et al. Pervasive human-driven decline of life on Earth points to the need for transformative change. Science 2019, 366. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Shukla, P.R.; Skea, J.; Calvo Buendia, E.; Masson-Delmotte, V.; Pörtner, H.-O.; Roberts, D.C.; Zhai, P.; Slade, R.; Connors, S.; van Diemen, R.; et al. (Eds.) Climate Change and Land: An IPCC Special Report on Climate Change, Desertification, Land Degradation, Sustainable Land Management, Food Security, and Greenhouse Gas Fluxes in Terrestrial Ecosystems. Available online: https://www.ipcc.ch/srccl/ (accessed on 20 March 2021).

- OECD. Meeting Policy Challenges for a Sustainable Bioeconomy; OECD: Paris, France, 2018. [Google Scholar]

- Action Plan for Nature, People and the Economy. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52017DC0198 (accessed on 20 March 2021).

- Bosman, R.; Rotmans, J. Transition Governance towards a Bioeconomy: A Comparison of Finland and The Netherlands. Sustainability 2016, 8, 1017. [Google Scholar] [CrossRef] [Green Version]

- Etzkowitz, H.; Leydesdorff, L. The Triple Helix, University-Industry-Government Relations: A laboratory for Knowledge-Based Economic Development. EASST Rev. 1995, 14, 14–19. [Google Scholar]

- Carayannis, E.G.; Campbell, D.F. Triple helix, Quadruple helix and Quintuple helix and how do Knowledge, Innovation and the Environment relate To Each other? Int. J. Soc. Ecol. Sustain. Dev. 2012, 1, 41–69. [Google Scholar] [CrossRef]

- Carayannis, E.G.; Barth, T.D.; Campbell, D.F. The Quintuple Helix innovation model: Global warming as a challenge and driver for innovation. J. Innov. Entrep. 2012, 1, 2. [Google Scholar] [CrossRef] [Green Version]

- Lewandowski, I. Securing a sustainable biomass supply in a growing bioeconomy. Glob. Food Secur. 2015, 6, 34–42. [Google Scholar] [CrossRef]

- Grundel, I.; Dahlström, M. A Quadruple and Quintuple Helix Approach to Regional Innovation Systems in the Transformation to a Forestry-Based Bioeconomy. J. Knowl. Econ. 2016, 7, 963–983. [Google Scholar] [CrossRef] [Green Version]

- Fritsche, U.; Brunori, G.; Chiaramonti, D.; Galanakis, C.; Hellweg, S.; Matthews, R.; Panoutsou, C. Future Transitions for the Bioeconomy towards Sustainable Development and a Climate-Neutral Economy; Knowledge Synthesis Final Report; Publications Office of the European Union: Luxembourg, 2020. [Google Scholar]

- Robertson, G.P.; Swinton, S. Reconciling Agricultural Productivity and Environmental Integrity: A Grand Challenge for Agriculture. Front. Ecol. Environ. 2005, 3, 38–46. [Google Scholar] [CrossRef]

- Brouwer, F.; Mantino, F.; Polman, N.; Short, C.; Sterly, S.; Rac, I. Private Sector Actions to Valorise Public Benefits from Agriculture and Forestry. EuroChoices 2018, 17, 16–22. [Google Scholar] [CrossRef]

- Lundvall, B.A. National Systems of Innovation; Anthem Press: London, UK, 1992. [Google Scholar]

- Jensen, M.; Johnson, B.; Lorenz, E.; Lundvall, B.A. Forms of knowledge and modes of innovation. Res. Policy 2007, 36, 680–693. [Google Scholar] [CrossRef]

- Parrilli, D.M.; Alcalde Heras, H. STI and DUI innovation modes: Scientific-technological and context-specific nuances. Res. Policy 2016, 45, 747–756. [Google Scholar] [CrossRef] [Green Version]

- Fitjar, R.; Rodriguez-Pose, A. Firm collaboration and modes of innovation in Norway. Res. Policy 2013, 42, 128–138. [Google Scholar] [CrossRef]

- Imbert, E.; Ladu, L.; Tani, A.; Morone, P. The transition towards a bio-based economy: A comparative study based on social network analysis. J. Environ. Manag. 2019, 230, 255–265. [Google Scholar] [CrossRef] [PubMed]

- Niftiyev, I. Dutch Disease Effects in the Azerbaijan Economy: Results of Multivariate Linear Ordinary Least Squares (OLS) Estimations. HSE Econ. J. 2021, 25, 309–346. [Google Scholar] [CrossRef]

- Sadik-Zada, E.R. Addressing the growth and employment effects of the extractive industries: White and black box illustrations from Kazakhstan. Post-Communist Econ. 2019, 33, 402–434. [Google Scholar] [CrossRef]

- Sadik-Zada, E.R.; Loewenstein, W.; Hasanli, Y. Production linkages and dynamic fiscal employment effects of the extractive industries: Input-output and nonlinear ARDL analyses of Azerbaijani economy. Miner. Econ. 2021, 34, 3–18. [Google Scholar] [CrossRef]

- Sadik-Zada, E.R. Distributional Bargaining and the Speed of Structural Change in the Petroleum Exporting Labor Surplus Economies. Eur. J. Dev. Res. 2020, 32, 51–98. [Google Scholar] [CrossRef]

- Cortright, J. Making Sense of Clusters: Regional Competitiveness and Economic Development; The Brookings institution: Washington, DC, USA, 2006. [Google Scholar]

- Hermans, F. The potential contribution of transition theory to the analysis of bioclusters and their role in the transition to a bioeconomy. Biofuels Bioprod. Biorefining 2018, 12, 265–276. [Google Scholar] [CrossRef] [Green Version]

- PwC. Regional Biotechnology—Establishing a Methodology and Performance Indicators for Assessing Bioclusters and Bioregions Relevant to the KBBE Area; Final Report, Workshop “Regional Biotechnology”; PwC: Brussels, Belgium, 2010. [Google Scholar]

- BERST. A Representative Set of Case Studies; Public Deliverable—D 3.2. Project BERST (BioEconomy Regional Strategy Toolkit), Grant Agreement No: 613671; Wageningen University & Research: Wageningen, The Netherlands, 2015. [Google Scholar]

- IACGB. Global Bioeconomy Policy Report (IV): A Decade of Bioeconomy Policy Development around the World; A Report from the International Advisory Council on Global Bioeconomy; IACGB: Berlin, Germany, 2020; Available online: https://gbs2020.net/wp-content/uploads/2020/11/GBS-2020_Global-Bioeconomy-Policy-Report_IV_web.pdf (accessed on 16 April 2021).

- European Commission. Organic Action Plan. Available online: https://ec.europa.eu/info/sites/info/files/food-farming-fisheries/farming/documents/com2021_141-organic-action-plan_en.pdf (accessed on 20 March 2021).

- European Commission. Bioeconomy Financing Instruments. Available online: https://knowledge4policy.ec.europa.eu/bioeconomy/bioeconomy-eu-financing-instruments_en (accessed on 20 March 2021).

- Bracco, S.; Tani, A.; Çalicioglu, Ö.; Gomez San Juan, M.; Bogdanski, A. Indicators to Monitor and Evaluate the Sustainability of Bioeconomy. Overview and a Proposed Way Forward; FAO Working Paper 77; FAO: Rome, Italy, 2019. [Google Scholar]

- Lier, M.; Aarne, M.; Kärkkäinen, L.; Korhonen, K.T.; Yli-Viikari, A.; Packalen, T. Synthesis on Bioeconomy Monitoring Systems in the EU Member States—Indicators for Monitoring the Progress of Bioeconomy. Luke Natural Resources Institute, Finland. 2018. Available online: https://jukuri.luke.fi/handle/10024/542249 (accessed on 22 June 2020).

- Juvančič, L.; Novak, A.; Lovec, M.; Rac, I.; Kocjančič, T.; Arnič, D.; Nipers, A.; Upite, I.; Vitunskienė, V. Bioeconomy Institutional Profiles—Comparative Analysis, Benchmarking and Policy Recommendations; Deliverable D 1.4, Project BIOEASTsUP, Horizon 2020 Research and Innovation Programme under Grant Agreement No 862699; Institute of Soil Science and Plant Cultivation State Research Institute: Pulawy, Poland, 2021. [Google Scholar]

- Kulišić, B.; Perović, M.; Matijašević, N.; Mandarić, A.; Sauvula-Seppälä, T.; Lier, M. Report on Analysis of BIOEAST National Bioeconomy Related Sectors; Deliverable D 1.2, Project BIOEASTsUP, Horizon 2020 Research and Innovation Programme under Grant Agreement No 862699; Institute of Soil Science and Plant Cultivation State Research Institute: Pulawy, Poland, 2020. [Google Scholar]

- EUROSTAT. Land Cover Overview by NUTS 2 Regions [LAN_LCV_OVW__custom_680729]. Available online: https://ec.europa.eu/eurostat/databrowser/view/LAN_LCV_OVW__custom_680729/default/table (accessed on 14 February 2021).

- Forest Europe. Available online: https://www.eea.europa.eu/data-and-maps/indicators/forest-growing-stock-increment-and-fellings-3/assessment (accessed on 22 March 2021).

- Parisi, C.; Baldoni, E.; M′barek, R. Bio-Based Industry and Biorefineries. European Commission, Joint Research Centre (JRC) [Dataset]. 2020. Available online: http://data.europa.eu/89h/ee438b10-7723-4435-9f5e-806ab63faf37 (accessed on 22 March 2021).

- Sadik-Zada, E.R.; Gatto, A. Energy Security Pathways in South East Europe: Diversification of the Natural Gas Supplies, Energy Transition, and Energy Futures. In From Economic to Energy Transition. Energy, Climate and the Environment; Mišík, M., Oravcová, V., Eds.; Palgrave Macmillan: Cham, Switzerland, 2021. [Google Scholar] [CrossRef]

- OECD. Inward FDI Stocks by Industry (Indicator). Available online: https://www.oecd-ilibrary.org/finance-and-investment/inward-fdi-stocks-by-industry/indicator/english_2bf57022-en (accessed on 20 October 2021).

| Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).