Bank as a Stakeholder in the Financing of Renewable Energy Sources. Recommendations and Policy Implications for Poland

Abstract

:1. Introduction

2. Literature Review and Theoretical Background

2.1. Analysis of Renewable Energy Market in Poland in Comparison with EU Countries

- RES share in electricity production (in the energy mix) for the year,

- RES share in final electricity consumption for the year,

- year-on-year growth rate for the two above-mentioned variables,

- share of RES expenditure in GDP for the year.

- a subsidy system for investments in renewable energy sources (funds granted at the central and local level, EU funds, funds from the National Fund for Environmental Protection and Water Management (NFOŚiGW) and its provincial branches),

- large investment loans (bank consortia) for the construction of power plants producing electricity from RES,

- preferential credits and loans granted by the banking sector,

- project finance,

- public-private partnership (PPP),

- leasing,

- green bonds,

- issue of shares,

- feed-in-tariff (TiF) and feed-in-premium (FiP),

- auction system,

- tradable green certificates system,

- tax benefits:

- -

- for individual clients—beneficiaries of subsidies: exemption from individual income tax for subsidies and thermo modernization relief,

- -

- for RES energy producers—exemption from VAT and excise duty.

- (1)

- sources of NFOŚiGW, including [13]:

- domestic sources, programs like: Mój Prąd, Kawka, Kawka Plus, Czyste Powietrze, Agroenergia,

- sources from EU, e.g., Operational Program Infrastructure and Environment 2014–2020, LIFE Program,

- Norway grants and grants from the European Economic Area (EEA),

- green investment scheme,

- (2)

- type of financing source:

- private sources: funds granted in the form of preferential credits and loans for pro-ecological investments, mainly by the banking sector,

- public sources,

- funds from foreign sources e.g., Program PolSEFF2–Polish Sustainable Energy Financing Facility,

- (3)

- type of the beneficiary:

- individual clients,

- enterprises, mainly SMEs,

- local governments,

- others, e.g., farmers, housing communities.

2.2. Regulations and EU Goals Concerning RES

- The appreciation of the technology used in the production and storage of renewable sources of energy as the strategic elements of the supply chain;

- Investing over the next 30 years more than 2 billion euros in the wind and solar energy;

- Placement of renewable energy production in Europe.

2.3. Financing of Renewable Energy in the World

2.4. Financing RES by Banks

- Clean Energy Finance Corporation (CEFC) in Australia: debt (market rate, long-term), debt (concessional, limited to AUD 300 million (USD 237 million) in NPV terms per year, equity (introduced after interviews), securitization/aggregation products, guarantees (restricted to 5% uncommitted balance),

- Green Investment Bank (GIB) in the UK: debt (market rate, long-term), debt (subordinated, mezzanine), equity (incl. bridging equity loans), securitization/aggregation products,

- Kreditanstalt fuer Wiederaufbau (KfW) in Germany: debt (concessional, long-term), debt (market rate, long-term, for offshore wind, energy transition-related R&D, SME and large corporate projects), equity (limited amount), and grants.

3. Materials and Methods

- scientific papers–for literature review and discussion about the role of the banks in the financing of renewable energy projects in different parts of the world, to discuss the selection of financial instruments used by banks and to find out the risk factors related to RES investments;

- energy sector reports and reports of future studies agencies and think tanks such as Wise Europa and research foundation of The Polish Bank Association–as a background for our recommendations for the banking sector in Poland and deriving simulations and scenarios of the future of the energy sector in Poland and its sources of funding;

- statistical data from IMF and Eurostat–to retrieve data about GDP and investments in RES and

- Enerdata materials for detailed analysis of renewable energy shares in energy production.

- literature review findings;

- policy recommendations of European Union;

- results of scenarios of the future and simulation for investments in the renewable energy and sources of financing;

- analysis of strategies and instruments used in other countries; and

- risk analysis.

4. Results

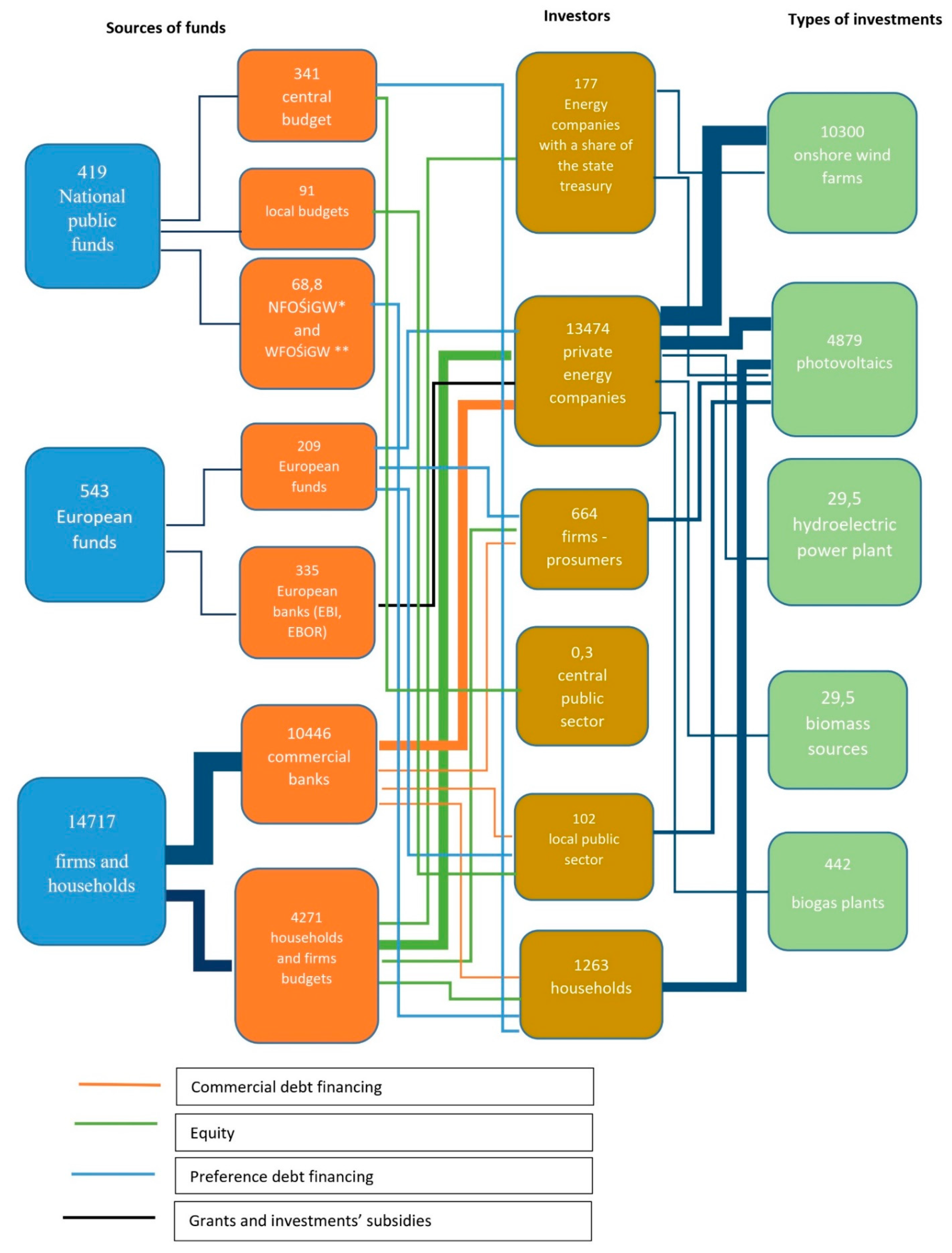

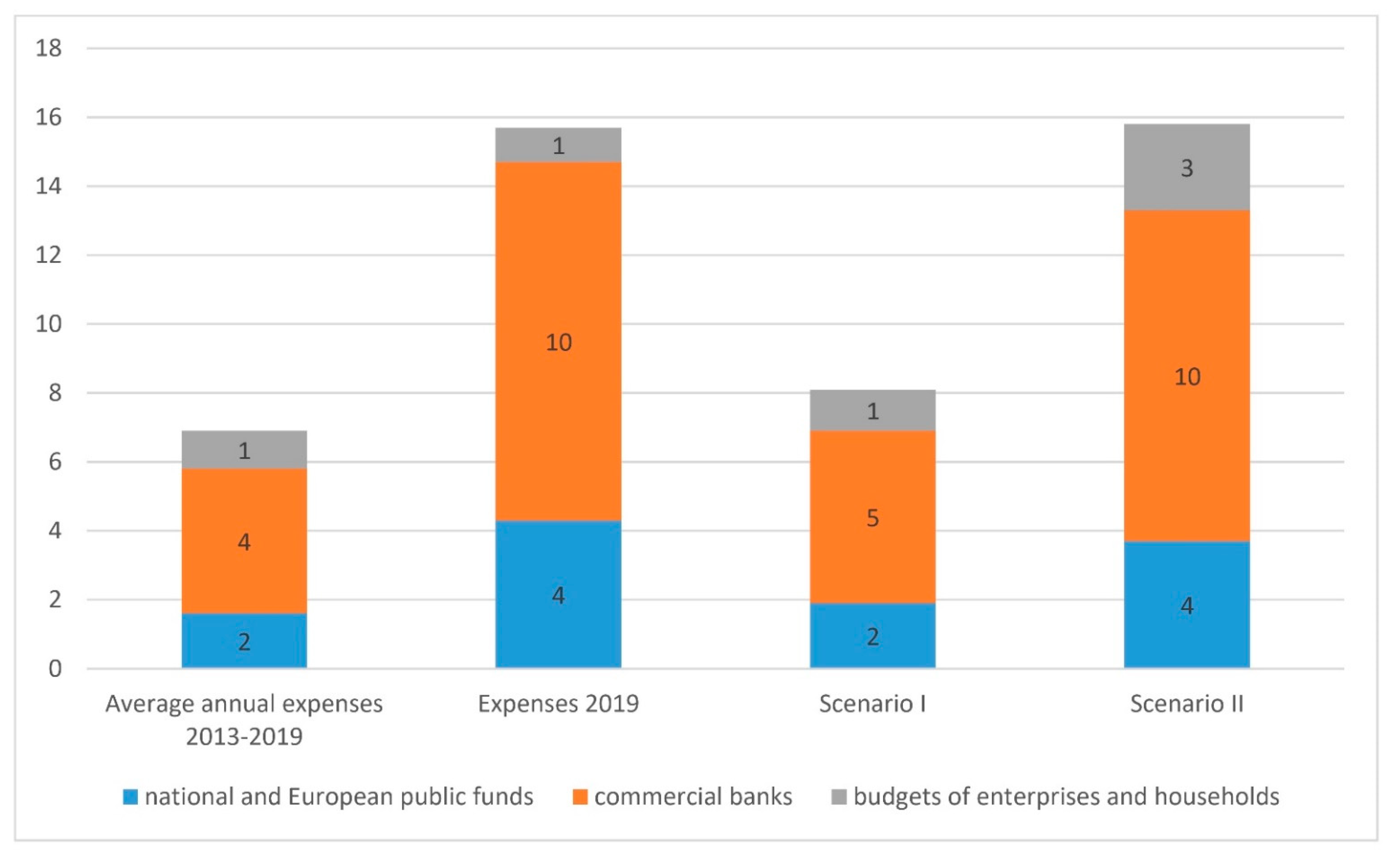

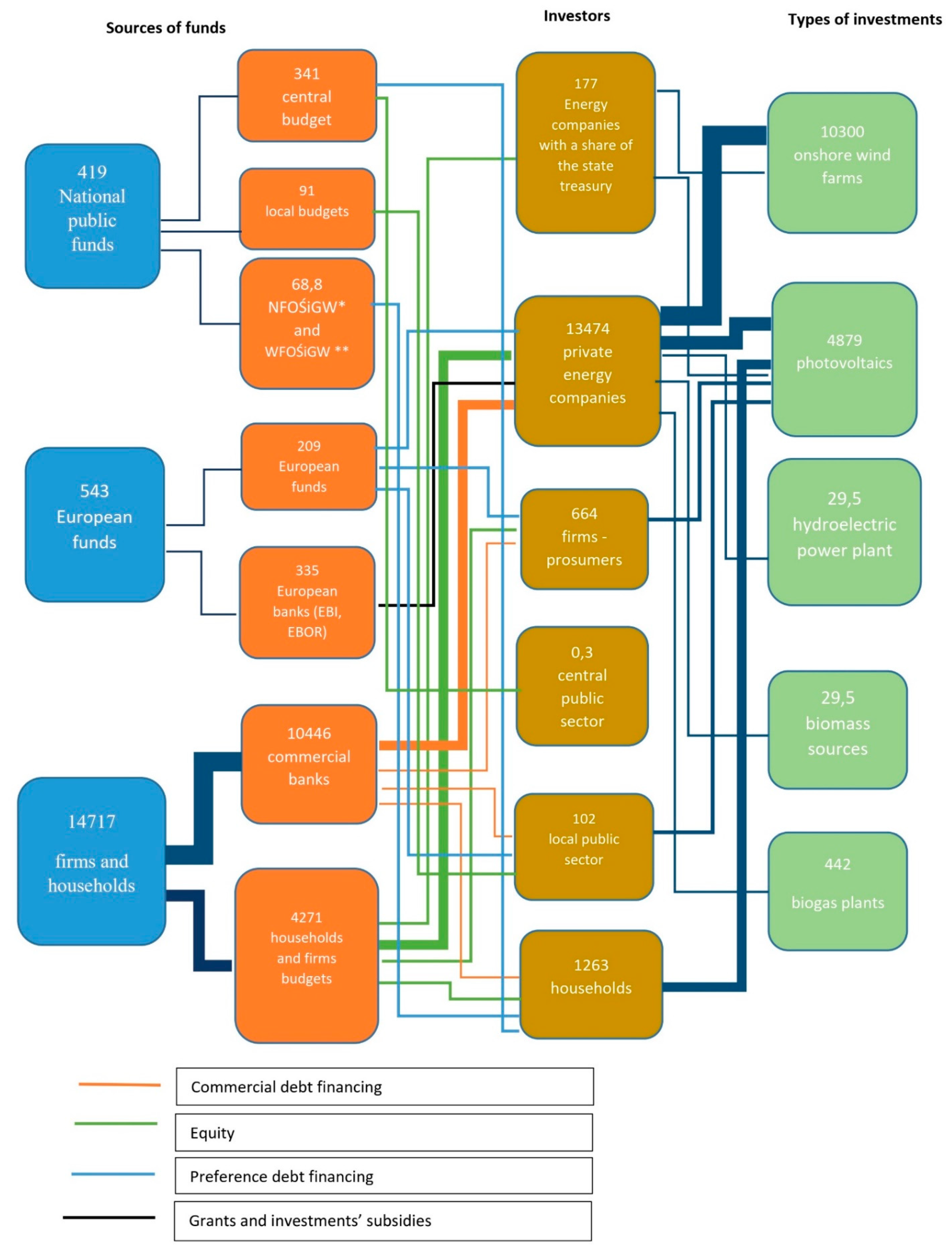

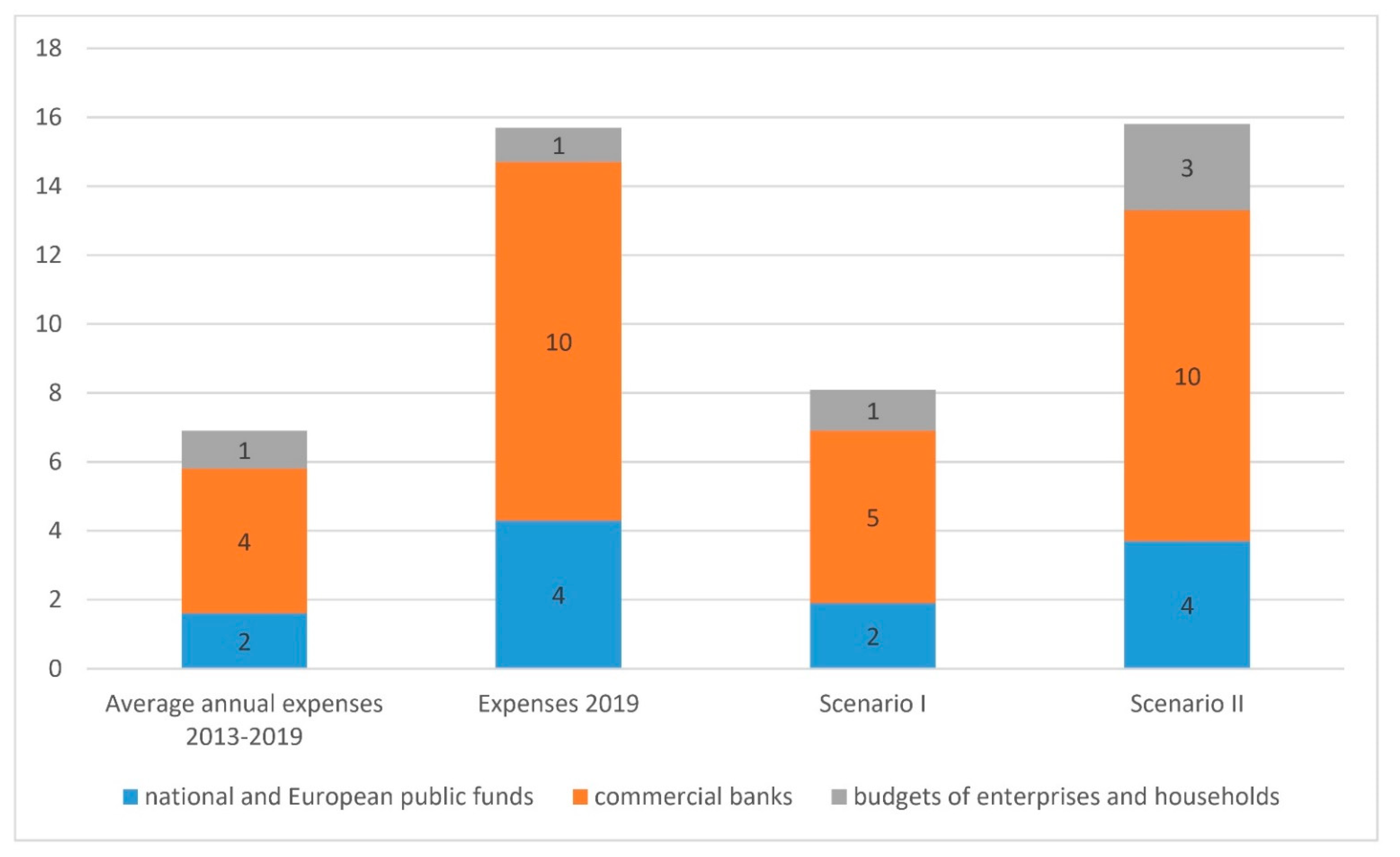

4.1. Bank as a Main Source of Capital in Financing Renewable Energy

- Scenario I: based on National Plan for Energy and Climate approved at the end of 2019;

- Scenario II: based on the version of the National Plan for Energy and Climate that includes the shutdown of coal-fired power plants until 2035 and that assumes accelerated investment in RE (additional onshore wind farms with a capacity of 13 GW and photovoltaic farms with a capacity of 11 GW) supplemented with gas power plants and gas heat and power plants (total power of 16 GW until 2035).

4.2. The Assessment of Investment Risk in Renewable Energy by Banks in Poland

- Bank as an issuer of debt instrument, as straight bonds or green bonds, the capital acquired through this issue is used to provide loans to finance renewable energy investments;

- Bank as an investor on the debt market, in such instruments like bonds (including green bonds), loans, also in project-finance and public-private partnerships;

- Bank as an intermediary (underwriter) of the issue.

4.2.1. Bank as an Issuer of Debt Instrument

- risk of nonplacement of the issue;

- interest rate risk.

- fixed interest bond;

- floating interest bond.

4.2.2. Bank as an Investor on the Debt Market

- credit risk;

- interest rate risk;

- prepayment risk.

- probability of default;

- loss given default.

- fixed interest bond;

- floating interest bond.

4.2.3. Bank as an Investor on the Equity Market

4.2.4. Bank as an Intermediary (Underwriter) and Organizer of the Issue

- The rejection, by the energy operator, of including the installation in the network (in Poland this refers to the installations above 50 kW);

- The low reliability of the installation (e.g., for heat pump).

4.3. Assessment of the Instruments Provided by Banks in Poland to Finance Renewable Energy Projects

- loans and borrowings,

- investment loans,

- project finance,

- public-private partnership (PPP),

- leasing,

- green bonds,

- VC/PE funds,

- hybrid instruments.

- risk—creditworthiness of the customer, credibility of the technology supplier;

- value of the capital engaged—the value of investment and value of financial instrument;

- profitability—the rate of return on the instrument;

- availability for the bank–easiness of organization of the process (repeatability vs. tailor-made);

- reputation—the image of the bank;

- support for energy transformation.

5. Conclusions and Discussion

- The general strategy of the European Commission on ecological financing concerns “investments and financing to complete the transition to the economy which is climate-neutral”. Therefore, the European Commission or European Parliament would seek ways to reflect climate risk in the bank capital in Poland or through supervisory actions in Pillar 2 or through supporting green investments in Pillar as the supplement to CRR3.

- The growth of the interest of banks in Polish market in different programs can be observed. At present, the financing of renewable energy projects is either through programs of NFOŚiGW and foreign financing or through preferential loans offered by banks.

- It seems that different forms of financing renewable energy in Poland need to be combined, e.g., equity, credit, and liabilities. This recommendation refers to a one-off one-time return, e.g., by energy companies.

- Wind energy, as a source with a dominant share of power in all types of RES in Poland, requires special attention in the context of the functioning of all stakeholder groups: decision-makers, producers (of individual elements of wind turbines), investors, banks, and households.

- It is crucial to analyze the impact of wind energy on the natural environment and an information campaign on this subject among local communities, in the case of financing wind energy, the Polish banking sector should also have this type of analysis.

- The incumbent, insignificant number of offers of banks on the Polish market dedicated to financing RE investments are dominated by loans for financing photovoltaic installations (an increase in the share of the solar energy in the energy mix of Poland and internationally over the last few years can be noticed). The increase also results from the current system of subsidies for this type of investment in RES. It seems that this trend will be observed in the longer term. Therefore, it is recommended for the Polish banking industry to develop new products dedicated to this type of RES. A solution may also be to emphasize that a given bank product (e.g., a standard cash loan) can be used to finance photovoltaic or solar installations, and then the applicant will receive more preferential conditions than for a standard product (e.g., related to APRC).

- In the above context, the fact of receiving a subsidy for a part of the investment in the field of renewable energy investments (e.g., for the Mój Prąd program the subsidy amount of PLN 5000 only for a part of the investment) should be considered in the assessment of creditworthiness. If the applicant has received a grant, it means that he is environmentally conscious, has adequate income to pay off future loan obligations.

- It is recommended to banking sector in Poland enable the receipt of a loan from a RES device supplier (e.g., Paribas Bank). Such a simplification of the procedure could result in the greater interest of potential applicants who are usually discouraged by extended loan/credit procedures.

- In the case of bank loans we recommend transferring funds to an account indicated by the applicant (which does not have to be an account kept with the lender).

- We postulate an increase in the possibility of using leasing to finance investments in renewable energy in Poland. Currently, 5 leasing companies deal with the financing of photovoltaic installations, and two years ago, none of the companies wanted to finance this type of investment. Therefore, it seems justified to promote leasing for potential clients of financial institutions. An important issue in a photovoltaic (PV) installation is the interpretation of whether a given device should be treated as one that is permanently connected to the ground or not. If following the interpretation adopted by the bank, a given device can be treated as non-permanently connected to the ground, then it may be the subject of security in leasing financing.

- In the case of granting long-term loans related to RES financing, the credit risk should be carefully analyzed; the following proposed indicators may prove helpful:

- (a)

- relation: the value of commission and interest income from loans for investments in renewable energy sources/total commission and interest income;

- (b)

- relation: the percentage share of all outstanding and untimely repaid loans for RES investments in total loans/percentage share of all outstanding and untimely repaid loans in total loans.

- According to experts (Eriks Atvars, Managing Director-UniCredit Bank AG), the lender (primarily the bank) must have clarity, transparency, and regulatory certainty for investing in RES. Therefore, a general conclusion could be drawn to improve these aspects in the Polish banking sector.

- When analyzing various forms of renewable energy financing in Poland, a lack of financing with hybrid instruments can be noticed; more attention should be paid to this type of product, e.g., mezzanine.

- Investments through VC/PE funds have played a minor role in recent years (almost 1% of the total invested funds on a global scale), therefore this form should also be more broadly considered and analyzed in the possibilities of financing investments in renewable energy.

- The instruments that support the energy transformation to the greatest extent are large investment loans, as well as project finance and PPP projects globally. Therefore, we recommend extending the introduction of those instruments on Polish grounds.

- The lowest risk is related to credits and loans (granted to individuals and small business entities) and loans granted to large entities as part of public-private partnership (PPP) projects. This leads to the conclusion that these types of instruments should be preferred by Polish banks.

- The analysis of banking risk related to investing in financial instruments which could be the source of financing of RES indicates that this type of risk is relatively low, therefore this type of bank involvement should be included in the policy recommendations.

- The development of an up-to-date database of support programs, with information about banks and their location where the missing part of funding can be received in the form of a loan or credit. The following can be used as benchmarks:https://www.deutschland-machts-effizient.de/KAENEF/Navigation/DE/Home/home.html (accessed on 13 August 2021).https://www.foerderdatenbank.de/FDB/DE/Home/home.html (accessed on 13 August 2021).

- Closer cooperation of financing institutions (including the National Fund for Environmental Protection and Water Management-NFOŚiGW) and the banking sector.https://www.deutschland-machts-effizient.de/KAENEF/Navigation/DE/Home/home.html (accessed on 13 August 2021).https://www.foerderdatenbank.de/FDB/DE/Home/home.html (accessed on 13 August 2021).

- Banks’ offers for financing renewable energy should contain information with which support programs given financing may be combined.

- Applications for financing investments in RES should be submitted together with applications for granting a preferential loan.

- Based on the analysis of the system operating in Romania, we can recommend for the banks operating at the Polish market:

- Implementation of a settlement system for owners of roof-mounted photovoltaic power plants with a unit capacity of more than 3 kW and up to a maximum of 100 kW, consisting in the sale of unused energy to energy companies at a rate set by the national regulator of the energy market.

- Increasing the use of green bonds.

- The creation of banks, which activities would be fully dedicated to financing green investments, such as the Nordic Investment Bank (NIB), which issues green bonds, and the Nordic Environment Finance Corporation (NEFCO).

6. Limitations, Futures Studies and Directions

Author Contributions

Funding

Conflicts of Interest

References

- Owusu, P.A.; Sarkodie, S.A. A review of renewable energy sources, sustainability issues and climate change mitigation. Cogent Eng. 2016, 3, 2–14. [Google Scholar] [CrossRef]

- Matthäus, M.; Mehling, M. De-risking Renewable Energy Investments in Developing Countries: A Multilateral Guarantee Mechanism. Joule 2020, 4, 2627–2645. [Google Scholar] [CrossRef]

- Szakály, Z.; Balogh, P.; Kontor, E.; Gabnai, Z.; Bai, A. Attitude toward and Awareness of Renewable Energy Sources: Hungarian Experience and Special Features. Energies 2021, 14, 22. [Google Scholar] [CrossRef]

- Share of Renewables in Electricity Production. Available online: https://yearbook.enerdata.net/renewables/renewable-in-electricity-production-share.html (accessed on 13 August 2021).

- Luthra, S.; Kumar, S.; Garg, D.; Haleem, A. Barriers to renewable/sustainable energy technologies adoption: Indian perspective. Renew. Sustain. Energy Rev. 2015, 41, 762–776. [Google Scholar] [CrossRef]

- Martin, N.; Rice, J. Developing renewable energy supply in Queensland, Australia: A study of the barriers, targets, policies and actions. Renew. Energy 2012, 44, 119–127. [Google Scholar] [CrossRef]

- Dincer, I. Renewable energy and sustainable development: A crucial review. Renew. Sustain. Energy Rev. 2000, 4, 157–175. [Google Scholar] [CrossRef]

- Foxon, T.J.; Gross, R.; Chase, A.; Howes, J.; Arnall, A.; Anderson, D. UK innovation systems for new and renewable energy technologies: Drivers, barriers and systems failures. Energy Policy 2005, 33, 2123–2137. [Google Scholar] [CrossRef]

- Fouquet, D.; Johansson, T. European renewable energy policy at crossroads—Focus on electricity support mechanisms. Energy Policy 2008, 36, 4079–4092. [Google Scholar] [CrossRef]

- Steffen, B. The importance of project finance for renewable energy projects. Energy Econ. 2018, 69, 280–294. [Google Scholar] [CrossRef] [Green Version]

- Polzin, F.; Sanders, M. How to finance the transition to low-carbon energy in Europe? Energy Policy 2020, 147, 111863. [Google Scholar] [CrossRef]

- Lazaroiu, G.; Mihaescul, L.; Jarcu, E.A.; Stanescu, L.A.; Ciupageanu, D.A. Renewable energy employment in Romania: An environmental impact discussion. In Proceedings of the 20th International Multidisciplinary Scientific GeoConference SGEM 2020, Sofia, Bulgaria, 18–24 August 2020; Volume 20, pp. 177–184. [Google Scholar] [CrossRef]

- National Fund for Environmental Protection and Water Management. Available online: http://www.nfosigw.gov.pl/oferta-finansowania/ (accessed on 15 January 2020).

- Ma, J.; Oppong, A.; Acheampong, K.N.; Abruquah, L.A. Forecasting Renewable Energy Consumption under Zero Assumptions. Sustainability 2018, 10, 576. [Google Scholar] [CrossRef] [Green Version]

- Siemiątkowski, P.; Tomaszewski, P.; Marszałek-Kawa, J.; Gierszewski, J. The Financing of Renewable Energy Sources and the Level of Sustainable Development of Poland’s Provinces in the Area of Environmental Order. Energies 2020, 13, 5591. [Google Scholar] [CrossRef]

- European Parliament. European Commission Directive (EU) 2018/2001 of the European Parliament and of the Council of 11 December 2018 on the Promotion of the Use of Energy from Renewable Sources; European Parliament: Brussels, Belgium, 2018. [Google Scholar]

- Ciupăgeanu, D.; Lăzăroiu, G.; Tîrşu, M. Carbon dioxide emissions reduction by renewable energy employment in Romania. In Proceedings of the 2017 International Conference on Electromechanical and Power Systems (SIELMEN), Iasi, Romania, 11–13 October 2017; pp. 281–285. [Google Scholar] [CrossRef]

- Europe 2020–A Strategy for Smart, Sustainable and Inclusive Growth. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:52010DC2020&from=EN (accessed on 13 August 2021).

- European Commission. A European Green Deal. Available online: https://ec.europa.eu/info/strategy/priorities-2019-2024/european-green-deal_pl (accessed on 20 June 2020).

- European Commission. Clean energy. Available online: https://ec.europa.eu/commission/presscorner/detail/pl/fs_19_6723 (accessed on 22 June 2020).

- Ministry of Climate and Environment. Energy policy of Poland until 2040. Available online: https://www.gov.pl/web/klimat/polityka-energetyczna-polski (accessed on 13 August 2021).

- Jajuga, K.; Zabawa, J.; Daszyńska-Żygadło, K. Report “Financing Investments in Renewable Energy by Polish Banks”; Programu Analityczno-Badawczego Fundacji Warszawski Instytut Bankowości; The Polish Bank Association: Warszawa, Poland, 2020. [Google Scholar]

- Standar, A.; Kozera, A.; Satoła, Ł. The Importance of Local Investments Co-Financed by the European Union in the Field of Renewable Energy Sources in Rural Areas of Poland. Energies 2021, 14, 450. [Google Scholar] [CrossRef]

- Zhang, F. Leaders and followers in finance mobilization for renewable energy in Germany and China. Environ. Innov. Soc. Transit. 2020, 37, 203–224. [Google Scholar] [CrossRef]

- Geddes, A.; Schmidt, T.S.; Steffen, B. The multiple roles of state investment banks in low-carbon energy finance: An analysis of Australia, the UK and Germany. Energy Policy 2018, 115, 158–170. [Google Scholar] [CrossRef]

- D’Orazio, P.; Löwenstein, P. Mobilising investments in renewable energy in Germany: Which role for public investment banks? J. Sustain. Financ. Invest. 2020, AHEAD-OF-PRINT. 1–24. [Google Scholar] [CrossRef]

- Chen, X.; Gallagher, K.P.; Mauzerall, D.L. Chinese Overseas Development Financing of Electric Power Generation: A Comparative Analysis. One Earth 2020, 3, 491–503. [Google Scholar] [CrossRef]

- Zhang, S. Innovative business models and financing mechanisms for distributed solar PV (DSPV) deployment in China. Energy Policy 2016, 95, 458–467. [Google Scholar] [CrossRef]

- Niczyporuk, H.; Urpelainen, J. Taking a gamble: Chinese overseas energy finance and country risk. J. Clean. Prod. 2021, 281, 124993. [Google Scholar] [CrossRef]

- He, L.; Liu, R.; Zhong, Z.; Wang, D.; Xia, Y. Can green financial development promote renewable energy investment efficiency? A consideration of bank credit. Renew. Energy 2019, 143, 974–984. [Google Scholar] [CrossRef]

- Ponorîcă, A.G.; Zaqeer, L.J.; Al Saedi, A.H.J. Public funding for emerging countries. Qual. Access Success. 2015, 16, 7–11. [Google Scholar]

- Steffen, B.; Schmidt, T.S. A quantitative analysis of 10 multilateral development banks’ investment in conventional and renewable power-generation technologies from 2006 to 2015, 4. Nat. Energy 2019, 4, 75–82. [Google Scholar] [CrossRef]

- Cabré, M.M.; Gallagher, K.P.; Li, Z. Renewable Energy: The Trillion Dollar Opportunity for Chinese Overseas Investment. China World Econ. 2018, 26, 27–49. [Google Scholar] [CrossRef]

- Hochstetler, K.; Kostka, G. Wind and Solar Power in Brazil and China: Interests, State–Business Relations, and Policy Outcomes. Glob. Environ. Politics 2015, 15, 74–94. [Google Scholar] [CrossRef]

- Oliveira, L.G.; Aquila, G.; Balestrassi, P.P.; Paiva, A.P.; de Queiroz, A.R.; de Oliveira Pamplona, E.; Camattaca, U.P. Evaluating economic feasibility and maximization of social welfare of photovoltaic projects developed for the Brazilian northeastern coast: An attribute agreement analysis. Renew. Sustain. Energy Rev. 2020, 123, 109786. [Google Scholar] [CrossRef]

- Lara, M.O.D.; Unsihuay-Vila, C.; Silva, V.R.G.R.D. Technical and economic viability of the installation of a hybrid solar-wind generation system in a Brazilian industry. Braz. Arch. Biol. Technol. 2019, 62, e19190005. [Google Scholar] [CrossRef]

- Proctor, D. Kazakhstan Adds New Solar Plant to Growing Renewables Capacity. 2019. Available online: https://www.powermag.com/kazakhstan-adds-new-solar-plant-to-growing-renewables-capacity/ (accessed on 13 May 2021).

- Amesho, K.T.T.; Edoun, E.I. Financing Renewable Energy in Namibia—A Fundamental Key Challenge to the Sustainable Development Goal 7: Ensuring Access to Affordable, Reliable, Sustainable and Modern Energy for All. Int. J. Energy Econ. Policy 2019, 9, 442–450. [Google Scholar] [CrossRef] [Green Version]

- Kalirajan, K.; Chen, H. Private Financing in Low-Carbon Energy Transition: Imbalances and Determinants. In Financing for Low-carbon Energy Transition; Anbumozhi, V., Kalirajan, K., Kimura, F., Eds.; Springer: Singapore, 2018. [Google Scholar] [CrossRef]

- Albertario, P. System of self-financing strategy for the policies aimed at the eco-innovation in the productive sectors, Procedia Environmental Science. Eng. Manag. 2016, 3, 1–6. [Google Scholar]

- Panteli, C.; Klumbytė, E.; Apanavičienė, R.; Fokaides, P.A. An Overview of the Existing Schemes and Research Trends in Financing the Energy Upgrade of Buildings in Europe. J. Sustain. Archit. Civil. Eng. 2020, 27, 53–62. [Google Scholar] [CrossRef]

- Zabawa, J. Bankowość Ekologiczna w Społecznej Odpowiedzialności Biznesu. Rola, Uwarunkowania i Mierniki; Wydawnictwo UE we Wrocławiu: Wrocław, Poland, 2019. [Google Scholar]

- Zabawa, J.; Kozyra, C. Eco-Banking in Relation to Financial Performance of the Sector—The Evidence from Poland. Sustainability 2020, 12, 2162. [Google Scholar] [CrossRef] [Green Version]

- Masud, M.A.K.; Bae, S.M.; Kim, J.D. Analysis of Environmental Accounting and Reporting Practices of Listed Banking Companies in Bangladesh. Sustainability 2017, 9, 1717. [Google Scholar] [CrossRef] [Green Version]

- Garcia-Bernabeu, A.; Mayor-Vitoria, F.; Bravo, M.; Pla-Santamaria, D. Financial risk management in renewable energy projects: A multicriteria approach. J. Manag. Inf. Decis. Sci. 2019, 22, 360–371. [Google Scholar]

- Lowitzsch, J. Consumer Stock Ownership Plans (CSOPs)—The Prototype Business Model for Renewable Energy Communities. Energies 2020, 13, 118. [Google Scholar] [CrossRef] [Green Version]

- McInerney, C.; Bunn, D.W. Expansion of the investor base for the energy transition. Energy Policy 2019, 129, 1240–1244. [Google Scholar] [CrossRef]

- Frisari, G.; Stadelmann, M. De-risking concentrated solar power in emerging markets: The role of policies and international finance institutions. Energy Policy 2015, 82, 12–22. [Google Scholar] [CrossRef]

- Sukirman, Y.A. Developing a green lending model for renewable energy project (case study electricity from biogas fuel at Palm Oil Industry). IOP Conf. Ser. Earth Environ. Sci. 2018, 131, 012037. [Google Scholar] [CrossRef] [Green Version]

- Mazzucato, M.; Semieniuk, G. Financing renewable energy: Who is financing what and why it matters. Technol. Forecast. Soc. Chang. 2018, 127, 8–22. [Google Scholar] [CrossRef]

- Safarzyńska, K.; van den Bergh, J.C.J.M. Financial stability at risk due to investing rapidly in renewable energy. Energy Policy 2017, 108, 12–20. [Google Scholar] [CrossRef]

- Bukowski, M.; Marszał, K.; Micuła, P.; Śniegocki, A.; Wetmańska, Z.; Zmienny, P. Panorama Niskoemisyjnych Inwestycji w Energetyce; WiseEuropa: Warszawa, Poland, 2020. [Google Scholar]

- Scenariusz Polityki Energetyczno-Klimatycznej (PEK). Available online: https://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=&ved=2ahUKEwic-ZOLtrDzAhVggv0HHWHeCI0QFnoECAYQAQ&url=https%3A%2F%2Fwww.gov.pl%2Fattachment%2Fa8db078d-535b-4b1b-bfe5-bda64df73778&usg=AOvVaw1Nhw_rdv51Zj_KoGuSX_pO (accessed on 25 May 2021).

{kind=link}

{kind=link}

| Country | RES Share in Electricity Production (%) | RES Share in Final Electricity Consumption for the Year (%) | Investment Expenditure/GDP% | GDP per Capita (USD) | |

|---|---|---|---|---|---|

| 1 | Norway | 97.88 | 72.75 | 0.368905 | 81,695 |

| 2 | Denmark | 68.30 | 35.71 | 0.482870 | 60,692 |

| 3 | Sweden | 55.27 | 54.65 | 0.809246 | 53,873 |

| 4 | Portugal | 52.18 | 30.32 | n/a | 23,186 |

| 5 | Finland | 45.10 | 41.16 | 0.364680 | 49,845 |

| 6 | Romania | 41.27 | 23.88 | n/a | 12,285 |

| 7 | Italy | 39.87 | 17.78 | 0.096346 | 34,260 |

| 8 | Spain | 38.62 | 17.45 | 0.525382 | 30,697 |

| 9 | Germany | 36.00 | 16.48 | 0.159440 | 48,264 |

| 10 | Great Britain | 33.98 | 11.02 | 0.311082 | 42,558 |

| 11 | Poland | 12.70 | 11.84 | 0.90000 (Estimates) | 15,431 |

| Until 2025 (TWh) | Until 2030 (TWh) | Until 2035 (TWh) | Within 15 Years (TWh) | Annual (GWh) | Share in % | Scenario I (PLN) | Scenario II (PLN) | |

|---|---|---|---|---|---|---|---|---|

| Hydro energy | 2.9 | 3 | 3 | 8.9 | 593.33 | 4.79 | 239,376,009 | 459,601,937 |

| Biomass | 9.7 | 11.6 | 11.4 | 32.7 | 2180.00 | 17.59 | 879,505,110 | 1,688,649,812 |

| Biogas | 2.7 | 3.9 | 5 | 11.6 | 773.33 | 6.24 | 311,995,697 | 599,031,737 |

| Wind onshore | 23.7 | 23.8 | 24.2 | 71.7 | 4780.00 | 38.57 | 1,928,456,159 | 3,702,635,826 |

| Wind offshore | 2.7 | 14.5 | 21.7 | 38.9 | 2593.33 | 20.93 | 1,046,261,431 | 2,008,821,947 |

| Solar energy | 4.5 | 6.8 | 10.8 | 22.1 | 1473.33 | 11.89 | 594,405,594 | 1,141,258,741 |

| Total | 46.2 | 63.6 | 76.1 | 185.90 | 12,393.33 | 100.00 | 5,000,000,000 | 9,600,000,000 |

| Until 2025 (Million EUR) | Until 2030 (Million EUR) | Until 2035 (Million EUR) | Within 15 Years (Million EUR) | Annual (Million EUR) | Shares in % | Scenario I (PLN) | Scenario II (PLN) | |

|---|---|---|---|---|---|---|---|---|

| Hydro energy | 317 | 120 | 120 | 557 | 37 | 2.06 | 103,102,325 | 197,956,464 |

| Wind energy | 1842 | 7467 | 5504 | 14,813 | 988 | 54.84 | 2,741,929,513 | 5,264,504,665 |

| Solar energy | 2156 | 1659 | 2819 | 6634 | 442 | 24.56 | 1,227,972,753 | 2,357,707,685 |

| Biomass | 1318 | 1109 | 93 | 2520 | 168 | 9.33 | 466,459,351 | 895,601,955 |

| Biogas | 786 | 837 | 865 | 2488 | 166 | 9.21 | 460,536,058 | 884,229,231 |

| Total | 6419 | 11,192 | 9401 | 27,012 | 1801 | 100 | 5,000,000,000 | 9,600,000,000 |

| Type of the Instrument | Criteria | ||||||

|---|---|---|---|---|---|---|---|

| Risk | Value of the Capital | Profitability | Availability | Reputation | Energy Transformation Support | Total | |

| loans and borrowings | 3 | 1 | 1 | 3 | 3 | 2 | 13 |

| investment loans | 2 | 2 | 2 | 2 | 3 | 3 | 14 |

| Bonds | 1 | 2 | 3 | 2 | 1 | 1 | 10 |

| Green bonds | 2 | 2 | 2 | 2 | 3 | 2 | 13 |

| Leasing | 2 | 1 | 1 | 3 | 1 | 1 | 9 |

| Project finance | 2 | 3 | 2 | 1 | 3 | 3 | 14 |

| PPP | 3 | 3 | 2 | 1 | 3 | 3 | 15 |

| Ranking | Type of the Instrument | Total |

|---|---|---|

| 1. | PPP | 15 |

| 2. | Investment loans | 14 |

| 2. | Project-finance | 14 |

| 3. | Loans and borrowings | 13 |

| 4. | Green bonds | 13 |

| 5. | Bonds | 10 |

| 6. | Leasing | 9 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Daszyńska-Żygadło, K.; Jajuga, K.; Zabawa, J. Bank as a Stakeholder in the Financing of Renewable Energy Sources. Recommendations and Policy Implications for Poland. Energies 2021, 14, 6422. https://doi.org/10.3390/en14196422

Daszyńska-Żygadło K, Jajuga K, Zabawa J. Bank as a Stakeholder in the Financing of Renewable Energy Sources. Recommendations and Policy Implications for Poland. Energies. 2021; 14(19):6422. https://doi.org/10.3390/en14196422

Chicago/Turabian StyleDaszyńska-Żygadło, Karolina, Krzysztof Jajuga, and Justyna Zabawa. 2021. "Bank as a Stakeholder in the Financing of Renewable Energy Sources. Recommendations and Policy Implications for Poland" Energies 14, no. 19: 6422. https://doi.org/10.3390/en14196422

APA StyleDaszyńska-Żygadło, K., Jajuga, K., & Zabawa, J. (2021). Bank as a Stakeholder in the Financing of Renewable Energy Sources. Recommendations and Policy Implications for Poland. Energies, 14(19), 6422. https://doi.org/10.3390/en14196422