Corporate Social Responsibility and Financial Performance among Energy Sector Companies

Abstract

:1. Introduction

2. Materials and Methods

2.1. Data and Sample

2.2. Key Variables

2.3. Research Model

+ β4(EBITDA per share) + β5(EV EBITDA) + β6(BETA) + e

3. Results

3.1. Descriptive Statistics and Correlation Matrix

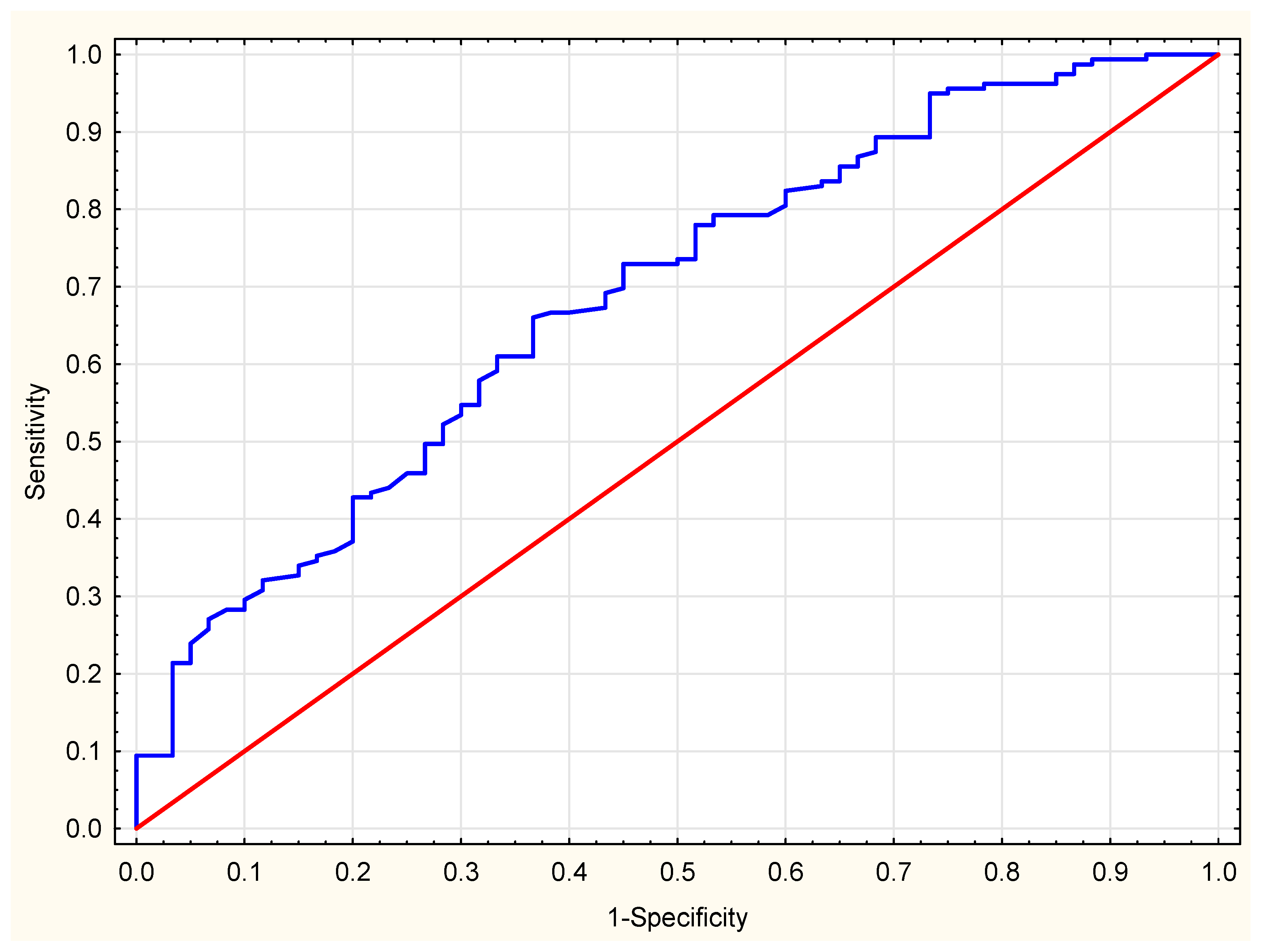

3.2. Binary Logit Model

4. Discussion

5. Conclusions and Implications

6. Limitation and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Commission of the European Communities. Promoting a European Framework for Corporate Social Responsibility: Green Paper; Office for Official Publications of the European Communities: Luxembourg, 2001. [Google Scholar]

- Chamberlain, N.W. The limits of Corporate Responsibility; Institute of National Affairs: Port Moresby, Papua New Guinea, 1979. [Google Scholar]

- Carroll, A.B. Corporate Social Responsibility. Bus. Soc. 1999, 38, 268–295. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D. Corporate Social Responsibility: A Theory of the Firm Perspective. Acad. Manag. Rev. 2001, 26, 117. [Google Scholar] [CrossRef]

- Nelling, E.; Webb, E. Corporate social responsibility and financial performance: The “virtuous circle” revisited. Rev. Quant. Financ. Acc. 2008, 32, 197–209. [Google Scholar] [CrossRef]

- Barnett, M.L. Stakeholder influence capacity and the variability of financial returns to corporate social responsibility. Acad. Manag. Rev. 2007, 32, 794–816. [Google Scholar] [CrossRef]

- Glavopoulos, E.; Bersimis, S.; Georgakellos, D.; Sfakianakis, M. Investigating the factors affecting companies’ attitudes towards CSR and CER during the fiscal crisis in Greece. J. Environ. Plan. Manag. 2013, 57, 1612–1641. [Google Scholar] [CrossRef]

- Roszko-Wójtowicz, E.; Grzelak, M.M.; Laskowska, I. The impact of research and development activity on the TFP level in manufacturing in Poland. Equilibrium 2019, 14, 711–737. [Google Scholar] [CrossRef] [Green Version]

- Piersiala, L. The usage pattern of development method to assess the functioning of special economic zones: The case of Poland. Equilibrium 2019, 14, 167–181. [Google Scholar] [CrossRef] [Green Version]

- Rollnik-Sadowska, E.; Dąbrowska, E. Cluster analysis of effectiveness of labour market policy in the European Union. Oeconomia Copernic. 2018, 9, 143–158. [Google Scholar] [CrossRef]

- Kijek, A.; Matras-Bolibok, A. Technological convergence across European regions. Equilibrium 2020, 15, 295–313. [Google Scholar] [CrossRef]

- Kijek, T.; Matras-Bolibok, A. The relationship between TFP and innovation performance: Evidence from EU regions. Equilibrium 2019, 14, 695–709. [Google Scholar] [CrossRef]

- Wood, D.J. Corporate Social Performance Revisited. Acad. Manag. Rev. 1991, 16, 691–718. [Google Scholar] [CrossRef] [Green Version]

- Scholtens, B. A note on the interaction between corporate social responsibility and financial performance. Ecol. Econ. 2008, 68, 46–55. [Google Scholar] [CrossRef]

- Margolis, J.D.; Walsh, J.P. People and Profits?: The Search for a Link between a Company’s Social and Financial Performance; Psychology Press: Hove East Sussex, UK, 2001; ISBN 1135642265. [Google Scholar]

- Donaldson, T.; Preston, L.E. The Stakeholder Theory of the Corporation: Concepts, Evidence, and Implications. Acad. Manag. Rev. 1995, 20, 65. [Google Scholar] [CrossRef] [Green Version]

- Hillman, A.J.; Keim, G.D. Shareholder value, stakeholder management, and social issues: What’s the bottom line? Strateg. Manag. J. Strat. Mgmt. J. 2001, 22, 125–139. [Google Scholar] [CrossRef]

- Allouche, J.; Laroche, P.; Allouche, J.; Laroche, P. A Meta-analytical investigation of the relationship between corporate social and financial performance. Rev. Gest. Ressour. Hum. 2005, 57, 18. [Google Scholar]

- Wang, Q.; Dou, J.; Jia, S. A Meta-Analytic Review of Corporate Social Responsibility and Corporate Financial Performance. Bus. Soc. 2016, 55, 1083–1121. [Google Scholar] [CrossRef]

- Waddock, S.A.; Graves, S.B.; Carroll, W.E. The corporate social performance-financial performance link. Strateg. Manag. J. 1997, 18, 303–319. [Google Scholar] [CrossRef]

- Ferreira, E.J.; Sinha, A.; Varble, D. Long-run performance following quality management certification. Rev. Quant. Financ. Acc. 2007, 30, 93–109. [Google Scholar] [CrossRef]

- Cheng, C.A.; Collins, D.; Huang, H.H. Shareholder rights, financial disclosure and the cost of equity capital. Rev. Quant. Financ. Acc. 2006, 27, 175–204. [Google Scholar] [CrossRef]

- Parmar, B.L.; Freeman, R.E.; Harrison, J.S.; Wicks, A.C.; Purnell, L.; De Colle, S. Stakeholder Theory: The State of the Art. Acad. Manag. Ann. 2010, 4, 403–445. [Google Scholar] [CrossRef]

- Albinger, H.S.; Freeman, S.J. Corporate Social Performance and Attractiveness as an Employer to Different Job Seeking Populations. J. Bus. Ethics 2000, 28, 243–253. [Google Scholar] [CrossRef]

- Pätäri, S.; Arminen, H.; Tuppura, A.; Jantunen, A. Competitive and responsible? The relationship between corporate social and financial performance in the energy sector. Renew. Sustain. Energy Rev. 2014, 37, 142–154. [Google Scholar] [CrossRef]

- Kurucz, E.C.; Colbert, B.A.; Wheeler, D. The Business Case for Corporate Social Responsibility. Oxford Handb. Corp. Soc. Responsib. 2009, 83–112. [Google Scholar] [CrossRef]

- Berens, G.; Van Riel, C.B.M.; Van Rekom, J. The CSR-Quality Trade-Off: When can Corporate Social Responsibility and Corporate Ability Compensate Each Other? J. Bus. Ethic 2007, 74, 233–252. [Google Scholar] [CrossRef] [Green Version]

- Margolis, J.D.; Walsh, J.P. Misery Loves Companies: Rethinking Social Initiatives by Business. Adm. Sci. Q. 2003, 48, 268. [Google Scholar] [CrossRef] [Green Version]

- López, M.V.; Garcia, A.; Rodriguez, L. Sustainable Development and Corporate Performance: A Study Based on the Dow Jones Sustainability Index. J. Bus. Ethics 2007, 75, 285–300. [Google Scholar] [CrossRef]

- Shen, C.-H.; Chang, Y. Ambition Versus Conscience, Does Corporate Social Responsibility Pay off? The Application of Matching Methods. J. Bus. Ethics 2008, 88, 133–153. [Google Scholar] [CrossRef] [Green Version]

- Cai, Y.; Jo, H.; Pan, C. Doing Well While Doing Bad? CSR in Controversial Industry Sectors. J. Bus. Ethics 2011, 108, 467–480. [Google Scholar] [CrossRef]

- Groza, M.D.; Pronschinske, M.R.; Walker, M. Perceived Organizational Motives and Consumer Responses to Proactive and Reactive CSR. J. Bus. Ethics 2011, 102, 639–652. [Google Scholar] [CrossRef]

- Preston, L.E.; O’Bannon, D.P. The Corporate Social-Financial Performance Relationship. Bus. Soc. 1997, 36, 419–429. [Google Scholar] [CrossRef]

- Bowen, F.E. Environmental visibility: A trigger of green organizational response? Bus. Strat. Environ. 2000, 9, 92–107. [Google Scholar] [CrossRef]

- Agudelo, M.A.L.; Johannsdottir, L.; Davidsdottir, B. Drivers that motivate energy companies to be responsible. A systematic literature review of Corporate Social Responsibility in the energy sector. J. Clean. Prod. 2019, 247, 119094. [Google Scholar] [CrossRef]

- Georgopoulou, E.; Sarafidis, Y.; Mirasgedis, S.; Zaimi, S.; Lalas, D. A multiple criteria decision-aid approach in defining national priorities for greenhouse gases emissions reduction in the energy sector. Eur. J. Oper. Res. 2003, 146, 199–215. [Google Scholar] [CrossRef]

- Omer, A.M. Green energies and the environment. Renew. Sustain. Energy Rev. 2008, 12, 1789–1821. [Google Scholar] [CrossRef]

- Frynas, J.G. The false developmental promise of Corporate Social Responsibility: Evidence from multinational oil companies. Int. Aff. 2005, 81, 581–598. [Google Scholar] [CrossRef]

- Streimikiene, D.; Simanaviciene, Z.; Kovaliov, R. Corporate social responsibility for implementation of sustainable energy development in Baltic States. Renew. Sustain. Energy Rev. 2009, 13, 813–824. [Google Scholar] [CrossRef]

- Shahbaz, M.; Karaman, A.S.; Kilic, M.; Uyar, A. Board attributes, CSR engagement, and corporate performance: What is the nexus in the energy sector? Energy Policy 2020, 143, 111582. [Google Scholar] [CrossRef]

- Lee, S.P. Environmental responsibility, CEO power and financial performance in the energy sector. Rev. Manag. Sci. 2021, 1–20. [Google Scholar] [CrossRef]

- Pätäri, S.; Jantunen, A.; Kyläheiko, K.; Sandström, J. Does Sustainable Development Foster Value Creation? Empirical Evidence from the Global Energy Industry. Corp. Soc. Responsib. Environ. Manag. 2011, 19, 317–326. [Google Scholar] [CrossRef]

- Ekatah, I.; Samy, M.; Bampton, R.; Halabi, A. The Relationship Between Corporate Social Responsibility and Profitability: The Case of Royal Dutch Shell Plc. Corp. Reput. Rev. 2011, 14, 249–261. [Google Scholar] [CrossRef]

- Cho, S.J.; Chung, C.Y.; Young, J. Study on the Relationship between CSR and Financial Performance. Sustainability 2019, 11, 343. [Google Scholar] [CrossRef] [Green Version]

- Cardebat, J.-M.; Sirven, N. Responsabilité sociale et rendements boursiers: Une relation négative? Manag. Avenir 2009, 29, 363–378. [Google Scholar] [CrossRef]

- Chetty, S.; Naidoo, R.; Seetharam, Y. The Impact of Corporate Social Responsibility on Firms’ Financial Performance in South Africa. Contemp. Econ. 2015, 9, 193–214. [Google Scholar] [CrossRef] [Green Version]

- El Yaagoubi, J. Impact of CSR on financial performance of Casablanca Stock Exchange companies: A longitudinal study-ProQuest. Int. J. Innov. Appl. Stud. 2020, 29, 1142–1152. [Google Scholar]

- Sun, W.; Zhao, C.; Cho, C.H. Institutional transitions and the role of financial performance in CSR reporting. Corp. Soc. Responsib. Environ. Manag. 2018, 26, 367–376. [Google Scholar] [CrossRef]

- Dhaliwal, D.S.; Li, O.Z.; Tsang, A.; Yang, Y.G. Voluntary Nonfinancial Disclosure and the Cost of Equity Capital: The Initiation of Corporate Social Responsibility Reporting. Acc. Rev. 2011, 86, 59–100. [Google Scholar] [CrossRef]

- Lin, C.-S.; Chang, R.-Y.; Dang, V.T. An Integrated Model to Explain How Corporate Social Responsibility Affects Corporate Financial Performance. Sustainability 2015, 7, 8292–8311. [Google Scholar] [CrossRef] [Green Version]

- Moore, G. Corporate Social and Financial Performance: An Investigation in the U.K. Supermarket Industry. J. Bus. Ethics 2001, 34, 299–315. [Google Scholar] [CrossRef]

- Obradovich, J.; Gill, A. The Impact of Corporate Governance and Financial Leverage on The Impact of Corporate Governance and Financial Leverage on the Value of American Firms. Int. Res. J. Financ. Econ. 2013, 91, 1–14. [Google Scholar]

- Biger, N.; Mathur, N.A. The effects of capital structure on profitability: Evidence from United States. Int. J. Manag. 2011, 28, 3. [Google Scholar]

- Angelia, D.; Suryaningsih, R. The Effect of Environmental Performance and Corporate Social Responsibility Disclosure Towards Financial Performance (Case Study to Manufacture, Infrastructure, And Service Companies that Listed at Indonesia Stock Exchange). Procedia-Soc. Behav. Sci. 2015, 211, 348–355. [Google Scholar] [CrossRef] [Green Version]

- Qamar, R.; Pet, M. Relationship between Corporate Social Responsibility (CSR) and Corporate Financial Performance (CFP): Literature review approach. Elixir Fin. Mgmt. 2012, 46, 8404–8409. [Google Scholar]

- Uadiale, O.; Fagbemi, T. Corporate Social Responsibility and Financial Performance in Developing Economies: The Nigerian Experience. J. Econ. Sustain. Dev. 2012, 3, 44–55. [Google Scholar]

- Wu, M.-W.; Shen, C.-H. Corporate social responsibility in the banking industry: Motives and financial performance. J. Bank. Financ. 2013, 37, 3529–3547. [Google Scholar] [CrossRef]

- Rappaport, A. Creating Shareholder Value: A Guide for Managers and Investors; The Free Press: New York, NY, USA, 1998; ISBN 0-684-84456-7. [Google Scholar]

- Monteiro, A. A quick guide to financial ratios: Education. Pers. Financ. 2006, 307, 8–10. [Google Scholar]

- Ahsan, A.M.; Mainul Ahsan, A.F.M. Can Return on equity be used to predict portfolio performance? Can Roe be used to predict portfolio performance? Manag. Financ. Mark. 2012, 7, 132–148. [Google Scholar]

- Choi, J.-S.; Kwak, Y.-M.; Choe, C. Munich Personal RePEc Archive Corporate Social Responsibility and Corporate Financial Performance: Evidence from Korea Corporate Social Responsibility and Corporate Financial Performance: Evidence from Korea; MPRA: Munich, Germany, 2010. [Google Scholar]

- Mwanja, S.K.; Evusa, Z.; Ndirangu, A.W. Influence of Corporate Social Responsibility on Firm Performance among Companies Listed on the Nairobi Securities Exchange. Int. J. Appl. Econ. Financ. Acc. 2018, 3, 56–63. [Google Scholar] [CrossRef]

- Michelon, G.; Boesso, G.; Kumar, K. Examining the Link between Strategic Corporate Social Responsibility and Company Performance: An Analysis of the Best Corporate Citizens. Corp. Soc. Responsib. Environ. Manag. 2012, 20, 81–94. [Google Scholar] [CrossRef] [Green Version]

- Oeyono, J.; Samy, M.; Bampton, R. An examination of corporate social responsibility and financial performance. J. Glob. Responsib. 2011, 2, 100–112. [Google Scholar] [CrossRef]

- Koller, T.; Goedhart, M.; Wessels, D. The Right Role for Multiples in Valuation. McKinsey Financ. 2005, 15, 7–11. [Google Scholar]

- Uduji, J.I.; Okolo-Obasi, E.N. Multinational Oil Firms’ CSR Initiatives in Nigeria: The Need of Rural Farmers in Host Communities. J. Int. Dev. 2016, 29, 308–329. [Google Scholar] [CrossRef] [Green Version]

- Ting, H.W.; Ramasamy, B.; Ging, L.C. Management systems and the CSR engagement. Soc. Responsib. J. 2010, 6, 362–373. [Google Scholar] [CrossRef]

- Obi, P.; Ode-Ichakpa, I. Financial indicators of corporate social responsibility in Nigeria: A binary choice analysis. Int. J. Bus. Gov. Ethics 2020, 14, 34. [Google Scholar] [CrossRef]

- McGuire, J.B.; Sundgren, A.; Schneeweis, T. Corporate Social Responsibility and Firm Financial Performance. Acad. Manag. J. 1988, 31, 854–872. [Google Scholar] [CrossRef]

- Gautam, R.; Singh, A.; Bhowmick, D. Demystifying relationship between Corporate Social Responsibility (CSR) and financial performance: An Indian business perspective. Indep. J. Manag. Prod. 2016, 7, 1034–1062. [Google Scholar] [CrossRef] [Green Version]

- Agrawal, O.; Bansal, P.; Kathpal, S. Effect of Financial Performance on Corporate Social Responsibility and Stock Price: A Study of BSE Listed Companies. Int. J. Emerg. Technol. 2020, 11, 286–291. [Google Scholar]

- Maqbool, S.; Hurrah, S.A. Exploring the Bi-directional relationship between corporate social responsibility and financial performance in Indian context. Soc. Responsib. J. 2020. [Google Scholar] [CrossRef]

- Prado, G.F.D.; Piekarski, C.M.; da Luz, L.M.; de Souza, J.T.; Salvador, R.; de Francisco, A.C. Sustainable development and economic performance: Gaps and trends for future research. Sustain. Dev. 2019, 28, 368–384. [Google Scholar] [CrossRef]

- Surroca, J.; Tribó, J.A.; Waddock, S. Corporate responsibility and financial performance: The role of intangible resources. Strat. Manag. J. 2009, 31, 463–490. [Google Scholar] [CrossRef]

- Laguir, I.; Marais, M.; El Baz, J.; Stekelorum, R. Reversing the business rationale for environmental commitment in banking. Manag. Decis. 2018, 56, 358–375. [Google Scholar] [CrossRef]

- Lee, S.; Heo, C.Y. Corporate social responsibility and customer satisfaction among US publicly traded hotels and restaurants. Int. J. Hosp. Manag. 2009, 28, 635–637. [Google Scholar] [CrossRef]

- Dewi, D.M. CSR effect on market and financial performance. Dinar 2014, 1, 198–216. [Google Scholar] [CrossRef] [Green Version]

- Okegbe, T.O.; Egbunike, F.C. Corporate Social Responsibility and Financial Performance of Selected Quoted Companies in Nigeria. NG-J. Soc. Dev. 2016, 5, 168–189. [Google Scholar] [CrossRef]

- Uwuigbe, U.; Egbide, B.-C. Corporate Social Responsibility Disclosures in Nigeria: A Study of Listed Financial and Non-Financial Firms. J. Manag. Sustain. 2012, 2, 160. [Google Scholar] [CrossRef] [Green Version]

- Aras, G.; Aybars, A.; Kutlu, O. Managing corporate performance. Int. J. Prod. Perform. Manag. 2010, 59, 229–254. [Google Scholar] [CrossRef]

- Chang, D.-S.; Kuo, L.-C.R. The effects of sustainable development on firms’ financial performance—An empirical approach. Sustain. Dev. 2008, 16, 365–380. [Google Scholar] [CrossRef]

- Reverte, C. Determinants of Corporate Social Responsibility Disclosure Ratings by Spanish Listed Firms. J. Bus. Ethics 2008, 88, 351–366. [Google Scholar] [CrossRef]

- Li, Z.F.; Morris, T.; Young, B. Corporate Visibility in Print Media and Corporate Social Responsibility. Sustainability 2018, 10, 18. [Google Scholar]

- Pekovic, S.; Vogt, S. The fit between corporate social responsibility and corporate governance: The impact on a firm’s financial performance. Rev. Manag. Sci. 2020, 15, 1095–1125. [Google Scholar] [CrossRef]

- Li, Y.; Gong, M.; Zhang, X.-Y.; Koh, L. The impact of environmental, social, and governance disclosure on firm value: The role of CEO power. Br. Account. Rev. 2018, 50, 60–75. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

| Country | n | % |

|---|---|---|

| United States of America | 90 | 41.10 |

| Canada | 38 | 17.35 |

| China | 16 | 7.31 |

| Bermuda | 10 | 4.57 |

| United Kingdom | 8 | 3.65 |

| Norway | 7 | 3.20 |

| Australia | 6 | 2.74 |

| Thailand | 6 | 2.74 |

| Indonesia | 5 | 2.28 |

| Brazil | 4 | 1.83 |

| France | 3 | 1.37 |

| Netherlands | 3 | 1.37 |

| Greece | 3 | 1.37 |

| Italy | 2 | 0.91 |

| Papua New Guinea | 1 | 0.46 |

| Russia | 1 | 0.46 |

| Hungary | 1 | 0.46 |

| Turkey | 1 | 0.46 |

| Austria | 1 | 0.46 |

| Spain | 1 | 0.46 |

| Switzerland | 1 | 0.46 |

| Israel | 1 | 0.46 |

| Poland | 1 | 0.46 |

| Sweden | 1 | 0.46 |

| South Africa | 1 | 0.46 |

| Luxembourg | 1 | 0.46 |

| Belgium | 1 | 0.46 |

| Finland | 1 | 0.46 |

| Jersey | 1 | 0.46 |

| Japan | 1 | 0.46 |

| Portugal | 1 | 0.46 |

| Monaco | 1 | 0.46 |

| Total | 219 | 100 |

| Variables | Mean (SD) | Median (Q1; Q3) |

|---|---|---|

| ROA | −8.317 (16.223) | −3.266 (13.571; 1.408) |

| ROE | −27.39 (363.88) | 2.940 (−5.714; 8.724) |

| Beta | 1.447 (0.586) | 1.342 (1.057; 1.814) |

| EBIT | 467,626,496.818 (1,934,173,648.88) | 46,310,761.980 (−40,537,996.858; 371,448,973.763) |

| EBITDA Per Share | 2.956 (6.628) | 1.270 (0.388; 3.105) |

| EV EBITDA | 14.601 (25.344) | 9.585 (6.572; 14.14) |

| Variables | CSR Adoption (n = 159) | CSR Non-Adoption (n = 60) | p-Value |

|---|---|---|---|

| Mean (SD) Median (Q1; Q3) | |||

| ROA | −6.500 (13.503) | −13.131 (21.254) | 0.075 |

| −2.720 [−11.16; 2.089] | −5.124 (−20.661; 0.866) | ||

| ROE | −35.942 (426.212) | −4.748 (39.204) | NS |

| 3.770 [−4.661; 8.706] | 0.303 (−7.068; 8.855) | ||

| Beta | 1.436 (0.567) | 1.475 (0.640) | NS |

| 1.336 [1.097; 1.791] | 1.383 (0.990; 1.905) | ||

| EBIT | 636,045,952.00 (2,243,399,749.418) | 21,314,940.955 (256,879,626.43) | 0.06 |

| 125,499,113.600 [−58,544,200; 536,477,760] | 3.754.670,965 (−14,541,069.2; 52,592,469.19) | ||

| EBITDA per Share | 2.764 (5.106) | 3.464 (9.597) | NS |

| 1.466 [0.409; 3.159] | 0.898 (0.260; 2.815) | ||

| EV EBITDA | 11.163 (7.554) | 23.713 (45.871) | NS |

| 9.179 [6.291; 13.604] | 9.974 (7.473; 19.348) | ||

| Variables | ROA | ROE | BETA | EBIT | EBITDA per Share | EV to EBITDA |

|---|---|---|---|---|---|---|

| ROA | 1 | 0.0653 * | 0.1387 * | 0.0293 * | 0.0058 | 0.0004 |

| ROE | 0.0653 * | 1 | 0.0045 | 0.0001 | 0.0004 | 0.0001 |

| BETA | 0.1387 * | 0.0045 | 1 | 0.0231 * | 0.0024 | 0.0021 |

| EBIT | 0.0293 * | 0.0001 | 0.0231 * | 1 | 0.0001 | 0.0031 |

| EBITDA Per Share | 0.0058 | 0.0004 | 0.0024 | 0.0001 | 1 | 0.0106 |

| EV EBITDA | 0.0004 | 0.0001 | 0.0031 | 0.0031 | 0.0106 | 1 |

| Variables | β-Coefficient | OR | IC | p-Value |

|---|---|---|---|---|

| ROA | 0.023 | 1.023 | (1.002–1.044) | <0.001 |

| ROE | −0.002 | 0.998 | (0.990–1.005) | 0.556 |

| BETA | 0.099 | 1.104 | (0.617–1.976) | 0.738 |

| EBIT | 0.000 | 1.000 | (1.000–1.000) | 0.121 |

| EBITDA Per Share | −0.027 | 0.974 | (0.931–1.018) | 0.238 |

| EV EBITDA | −0.034 | 0.967 | (0.937–0.997) | <0.001 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kludacz-Alessandri, M.; Cygańska, M. Corporate Social Responsibility and Financial Performance among Energy Sector Companies. Energies 2021, 14, 6068. https://doi.org/10.3390/en14196068

Kludacz-Alessandri M, Cygańska M. Corporate Social Responsibility and Financial Performance among Energy Sector Companies. Energies. 2021; 14(19):6068. https://doi.org/10.3390/en14196068

Chicago/Turabian StyleKludacz-Alessandri, Magdalena, and Małgorzata Cygańska. 2021. "Corporate Social Responsibility and Financial Performance among Energy Sector Companies" Energies 14, no. 19: 6068. https://doi.org/10.3390/en14196068

APA StyleKludacz-Alessandri, M., & Cygańska, M. (2021). Corporate Social Responsibility and Financial Performance among Energy Sector Companies. Energies, 14(19), 6068. https://doi.org/10.3390/en14196068